Exponential Grid [Phi, Pi, Euler]If you disagree with one of the EMH principles that price is too random, then by definition you must agree that historic price has deterministic function to a scenario ahead.

I personally believe that constants like phi, pi and e can mimic exponential growth of the price.

In this script, first grid is based on the Lowest price multiplied with self fraction of the constant.

For example:

If you are familiar with fib ratio 1.272, then you must know that it is 1.618 to the power of 0.5.

With default settings of exponent step 0.25

First grid = Lowest price x phi^0.25

Second grid = Lowest price x phi^0.25x2

Third grid = Lowest price x phi^0.25x3 and so on

The script will automatically find the lowest price and update the grid values.

Or you can set up your custom Lowest price manually if you feel like the All Time Low level loses its relevance value after long period.

There are 64 grids including Lowest price level. And it wasn't by a chance. Pine Script has a limitation of max 64 plots. Number of grids shown in the chart depends on the highest price. Once price breaks above ATH a couple of next grids will be plotted automatically. In most cases if everything is plotted, the chart appears squeezed and you'll need to zoom in to see it. Therefore, I adjusted it relatively to the scale of the chart for the comfort.

In some cases 64 plots aren't enough to cover the whole chart. For example, let's take a look at NVIDIA chart:

Since the price has started with 0.0333, it is way too small to cover all with default settings.

We are left with 2 choices:

Either Enable "Round"

OR increase Exponent Step (from 0.25 to 0.5 in the particular example below)

If you set constant to pi or e which is a bigger number than phi, expect the gaps to be bigger. To reduce it to a more gradual way of expansion you can decrease Exponent Step.

Euler

mathLibrary "math"

It's a library of discrete aproximations of a price or Series float it uses Fourier Discrete transform, Laplace Discrete Original and Modified transform and Euler's Theoreum for Homogenus White noice operations. Calling functions without source value it automatically take close as the default source value.

Here is a picture of Laplace and Fourier approximated close prices from this library:

Copy this indicator and try it yourself:

import AutomatedTradingAlgorithms/math/1 as math

//@version=5

indicator("Close Price with Aproximations", shorttitle="Close and Aproximations", overlay=false)

// Sample input data (replace this with your own data)

inputData = close

// Plot Close Price

plot(inputData, color=color.blue, title="Close Price")

ltf32_result = math.LTF32(a=0.01)

plot(ltf32_result, color=color.green, title="LTF32 Aproximation")

fft_result = math.FFT()

plot(fft_result, color=color.red, title="Fourier Aproximation")

wavelet_result = math.Wavelet()

plot(wavelet_result, color=color.orange, title="Wavelet Aproximation")

wavelet_std_result = math.Wavelet_std()

plot(wavelet_std_result, color=color.yellow, title="Wavelet_std Aproximation")

DFT3(xval, _dir)

Discrete Fourier Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

DFT2(xval, _dir)

Discrete Fourier Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

FFT(xval)

Fast Fourier Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DFT32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DTF32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

LFT3(xval, _dir, a)

Discrete Laplace Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT2(xval, _dir, a)

Discrete Laplace Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT(xval, a)

Fast Laplace Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LTF32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

whitenoise(indic_, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise, without extra aproximated src.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

whitenoise(indic_, dft1, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise and DFT1.

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

dft1 (float) : Aproximated src value for white noice calculation

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

smooth(dft1, indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series and aproximated source value

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

dft1 (float) : Value to be smoothed.

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed source (src) series

smooth(indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed src series

vzo_ema(src, len)

Volume Zone Oscillator with EMA smoothing

Parameters:

src (float) : Source series

len (simple int) : Length parameter for EMA

Returns: VZO value

vzo_sma(src, len)

Volume Zone Oscillator with SMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for SMA

Returns: VZO value

vzo_wma(src, len)

Volume Zone Oscillator with WMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for WMA

Returns: VZO value

alma2(series, windowsize, offset, sigma)

Arnaud Legoux Moving Average 2 accepts sigma as series float

Parameters:

series (float) : Input series

windowsize (int) : Size of the moving average window

offset (float) : Offset parameter

sigma (float) : Sigma parameter

Returns: ALMA value

Wavelet(src, len, offset, sigma)

Aproxiates srt using Discrete wavelet transform.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (simple float)

sigma (simple float)

Returns: Wavelet-transformed series

Wavelet_std(src, len, offset, mag)

Aproxiates srt using Discrete wavelet transform with standard deviation as a magnitude.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (float) : Offset parameter for ALMA

mag (int) : Magnitude parameter for standard deviation

Returns: Wavelet-transformed series

LaplaceTransform(xval, N, a)

Original Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

Returns: Aproxiated source value

NLaplaceTransform(xval, N, a, repeat)

Y repetirions on Original Laplace Transform over N set of close prices, each time N-k set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformsum(xval, N, a, b)

Sum of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiff(xval, N, a, b, repeat)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiff(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, with dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiff(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor, dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiffFrom2(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

Fine-tune Inputs: Fourier Smoothed Volume zone oscillator WFSVZ0Use this Strategy to Fine-tune inputs for the (W&)FSVZ0 Indicator.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame.

MEANINGFUL DESCRIPTION:

The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Wavelet & Fourier Smoothed Volume Zone Oscillator (W&)FSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the Discrete Fourier Transform . Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Wavalet and Fourier aproximation with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

When I ndicator/Strategy returns 0 or natural trend , Strategy Closes All it's positions.

ORIGINALITY & USFULLNESS:

Personal combination of Fourier and Wavalet aproximation of a price which results in less noise Volume Zone Oscillator.

The Wavelet Transform is a powerful mathematical tool for signal analysis, particularly effective in analyzing signals with varying frequency or non-stationary characteristics. It dissects a signal into wavelets, small waves with varying frequency and limited duration, providing a multi-resolution analysis. This approach captures both frequency and location information, making it especially useful for detecting changes or anomalies in complex signals.

The Discrete Fourier Transform (DFT) is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

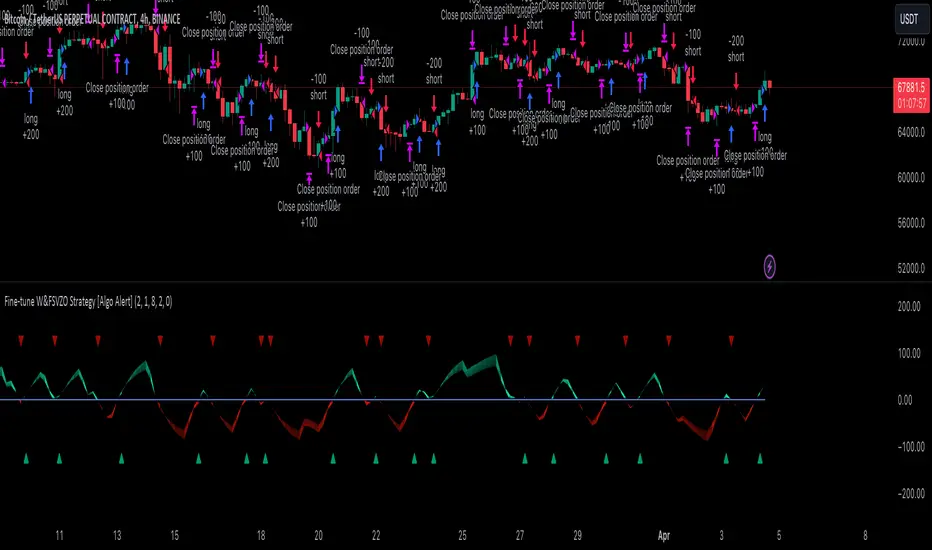

Thus the indicator returns 0 and Strategy closes all it's positions when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

In the next Image you can see that trend is negative on 4h, negative on 12h and positive on 1D. That means trend is negative.

I am sorry, the chart is a bit messy. The idea is to use the indicator over more than 1 Timeframe.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Fourier and Wavelet approximation of a close price are taken from aprox library.

Key Features:

You can tailor the Indicator/Strategy to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Fourier Transform (FFT) , the innovative Double Discrete Fourier Transform (DTF32) and Wavelet soothed Fourier soothed price series to suit your analytical needs.

Image of Wavelet transform with FAST settings, Double Fourier transform with FAST settings. Improved noice reduction with SLOW settings, and standard FSVZO with SLOW settings:

Fast setting are setting by default:

VZO length = 2

NoiceR max Length = 2

Slow settings are:

VZO length = 5 or 7

NoiceR max Length = 8

As you can see fast setting are more volatile. I suggest averaging fast setting on 4h 12h 1d 2d 3d 4d W and M Timeframe to get a clear view on market trend.

What if I want long only when VZO is rising and above 15 not 0?

You have set Setting VzoDifference to 15. That reduces the number of trend changes.

Example of W&FSVZO with VzoDifference 15 than 0:

VZO crossed 0 line but not 15 line and that's why Indicator returns 0 in one case an 1 in another.

What is Smooth length setting?

A way of calculating Bullish or Bearish (W&)FSVZO .

If smooth length is 2 the trend is rising if:

rising = VZO > ta.ema(VZO, 2)

Meaning that we check if VZO is higher that exponential average of the last 2 elements.

If smooth length is 1 the trend is rising if:

rising = VZO_ > VZO_

Use this Strategy to fine-tune inputs for the (W&)FSVZO Indicator.

(Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data)

I suggest using " Close all " input False when fine-tuning Inputs for 1 TimeFrame . When you export data to Excel/Numbers/GSheets I suggest using " Close all " input as True , except for the lowest TimeFrame . I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Fine-Tune Inputs: Fourier Smoothed Hybrid Volume Spread AnalysisUse this Strategy to Fine-tune inputs for the HSHVSA Indicator.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

I suggest using " Close all " input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using " Close all " input as True , except for the lowest TimeFrame.

MEANINGFUL DESCRIPTION:

The Fourier Smoothed Hybrid Volume Spread Analysis (FSHVSA) Strategy/Indicator is an innovative trading tool designed to fuse volume analysis with trend detection capabilities, offering traders a comprehensive view of market dynamics.

This Strategy/Indicator stands apart by integrating the principles of the Discrete Fourier Transform (DFT) and volume spread analysis, enhanced with a layer of Fourier smoothing to distill market noise and highlight trend directions with unprecedented clarity.

This smoothing process allows traders to discern the true underlying patterns in volume and price action, stripped of the distractions of short-term fluctuations and noise.

The core functionality of the FSHVSA revolves around the innovative combination of volume change analysis, spread determination (calculated from the open and close price difference), and the strategic use of the EMA (default 10) to fine-tune the analysis of spread by incorporating volume changes.

Trend direction is validated through a moving average (MA) of the histogram, which acts analogously to the Volume MA found in traditional volume indicators. This MA serves as a pivotal reference point, enabling traders to confidently engage with the market when the histogram's movement concurs with the trend direction, particularly when it crosses the Trend MA line, signalling optimal entry points.

It returns 0 when MA of the histogram and EMA of the Price Spread are not align.

WHAT IS FSHVSA INDICATOR:

The FSHVSA plots a positive trend when a positive Volume smoothed Spread and EMA of Volume smoothed price is above 0, and a negative when negative Volume smoothed Spread and EMA of Volume smoothed price is below 0. When this conditions are not met it plots 0.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

ORIGINALITY & USEFULNESS:

The FSHVSA Strategy is unique because it applies DFT for data smoothing, effectively filtering out the minor fluctuations and leaving traders with a clear picture of the market's true movements. The DFT's ability to break down market signals into constituent frequencies offers a granular view of market dynamics, highlighting the amplitude and phase of each frequency component. This, combined with the strategic application of Ehler's Universal Oscillator principles via a histogram, furnishes traders with a nuanced understanding of market volatility and noise levels, thereby facilitating more informed trading decisions.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is the meaning of price spread?

In finance, a spread refers to the difference between two prices, rates, or yields. One of the most common types is the bid-ask spread, which refers to the gap between the bid (from buyers) and the ask (from sellers) prices of a security or asset.

We are going to use Open-Close spread.

What is Volume spread analysis?

Volume spread analysis (VSA) is a method of technical analysis that compares the volume per candle, range spread, and closing price to determine price direction.

What does this mean?

We need to have a positive Volume Price Spread and a positive Moving average of Volume price spread for a positive trend. OR via versa a negative Volume Price Spread and a negative Moving average of Volume price spread for a negative trend.

What if we have a positive Volume Price Spread and a negative Moving average of Volume Price Spread?

It results in a neutral, not trending price action.

Thus the Indicator/Strategy returns 0 and Closes all long and short positions.

In the next Image you can see that trend is negative on 4h, we just move Negative on 12h and Positive on 1D. That means trend/Strategy flipped negative .

I am sorry, the chart is a bit messy. The idea is to use the indicator/strategy over more than 1 Timeframe.

Use this Strategy to fine-tune inputs for the HSHVSA Indicator.

(Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data)

I suggest using " Close all " input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using " Close all " input as True , except for the lowest TimeFrame. I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Fourier Smoothed Hybrid Volume Spread AnalysisIndicator id:

USER;91bdff47320b4284a375f428f683b21e

(only relevant to those that use API requests)

MEANINGFUL DESCRIPTION:

The Fourier Smoothed Hybrid Volume Spread Analysis (FSHVSA) indicator is an innovative trading tool designed to fuse volume analysis with trend detection capabilities, offering traders a comprehensive view of market dynamics.

This indicator stands apart by integrating the principles of the Discrete Fourier Transform (DFT) and volume spread analysis, enhanced with a layer of Fourier smoothing to distill market noise and highlight trend directions with unprecedented clarity.

This smoothing process allows traders to discern the true underlying patterns in volume and price action, stripped of the distractions of short-term fluctuations and noise.

The core functionality of the FSHVSA revolves around the innovative combination of volume change analysis, spread determination (calculated from the open and close price difference), and the strategic use of the EMA (default 10) to fine-tune the analysis of spread by incorporating volume changes.

Trend direction is validated through a moving average (MA) of the histogram, which acts analogously to the Volume MA found in traditional volume indicators. This MA serves as a pivotal reference point, enabling traders to confidently engage with the market when the histogram's movement concurs with the trend direction, particularly when it crosses the Trend MA line, signalling optimal entry points.

It returns 0 when MA of the histogram and EMA of the Price Spread are not align.

HOW TO USE THE INDICATOR:

The FSHVSA plots a positive trend when a positive Volume smoothed Spread and EMA of Volume smoothed price is above 0, and a negative when negative Volume smoothed Spread and EMA of Volume smoothed price is below 0. When this conditions are not met it plots 0.

ORIGINALITY & USEFULNESS:

The FSHVSA is unique because it applies DFT for data smoothing, effectively filtering out the minor fluctuations and leaving traders with a clear picture of the market's true movements. The DFT's ability to break down market signals into constituent frequencies offers a granular view of market dynamics, highlighting the amplitude and phase of each frequency component. This, combined with the strategic application of Ehler's Universal Oscillator principles via a histogram, furnishes traders with a nuanced understanding of market volatility and noise levels, thereby facilitating more informed trading decisions.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is the meaning of price spread?

In finance, a spread refers to the difference between two prices, rates, or yields. One of the most common types is the bid-ask spread, which refers to the gap between the bid (from buyers) and the ask (from sellers) prices of a security or asset.

We are going to use Open-Close spread.

What is Volume spread analysis?

Volume spread analysis (VSA) is a method of technical analysis that compares the volume per candle, range spread, and closing price to determine price direction.

What does this mean?

We need to have a positive Volume Price Spread and a positive Moving average of Volume price spread for a positive trend. OR via versa a negative Volume Price Spread and a negative Moving average of Volume price spread for a negative trend.

What if we have a positive Volume Price Spread and a negative Moving average of Volume Price Spread ?

It results in a neutral, not trending price action.

Thus the indicator returns 0.

In the next Image you can see that trend is negative on 4h, neutral on 12h and neutral on 1D. That means trend is negative .

I am sorry, the chart is a bit messy. The idea is to use the indicator over more than 1 Timeframe.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Fourier and Euler approximation of a spread are taken from aprox library.

Key Features:

Noise Reduction leverages Euler's White noise capabilities for effective Volume smoothing, providing a cleaner and more accurate representation of market dynamics.

Choose between the innovative Double Discrete Fourier Transform (DTF32) and Regular Open & Close price series.

Mathematical equations presented in Pinescript:

Fourier of the real (x axis) discrete:

x_0 = array.get(x, 0) + array.get(x, 1) + array.get(x, 2)

x_1 = array.get(x, 0) + array.get(x, 1) * math.cos( -2 * math.pi * _dir / 3 ) - array.get(y, 1) * math.sin( -2 * math.pi * _dir / 3 ) + array.get(x, 2) * math.cos( -4 * math.pi * _dir / 3 ) - array.get(y, 2) * math.sin( -4 * math.pi * _dir / 3 )

x_2 = array.get(x, 0) + array.get(x, 1) * math.cos( -4 * math.pi * _dir / 3 ) - array.get(y, 1) * math.sin( -4 * math.pi * _dir / 3 ) + array.get(x, 2) * math.cos( -8 * math.pi * _dir / 3 ) - array.get(y, 2) * math.sin( -8 * math.pi * _dir / 3 )

Fourier of the imaginary (y axis) discrete:

y_0 = array.get(x, 0) + array.get(x, 1) + array.get(x, 2)

y_1 = array.get(x, 0) + array.get(x, 1) * math.sin( -2 * math.pi * _dir / 3 ) + array.get(y, 1) * math.cos( -2 * math.pi * _dir / 3 ) + array.get(x, 2) * math.sin( -4 * math.pi * _dir / 3 ) + array.get(y, 2) * math.cos( -4 * math.pi * _dir / 3 )

y_2 = array.get(x, 0) + array.get(x, 1) * math.sin( -4 * math.pi * _dir / 3 ) + array.get(y, 1) * math.cos( -4 * math.pi * _dir / 3 ) + array.get(x, 2) * math.sin( -8 * math.pi * _dir / 3 ) + array.get(y, 2) * math.cos( -8 * math.pi * _dir / 3 )

Euler's Smooth with Discrete Furrier approximated Volume.

a = math.sqrt(2) * math.pi / _devided

b = math.cos(math.sqrt(2) * 180 / _devided)

c2 = 2 * math.pow(a, 2) * b

c3 = math.pow(a, 4)

c1 = 1 - 2 * math.pow(a, 2) * math.cos(b) + math.pow(a, 4)

filt := na(filt ) ? 0 : c1 * (w + nz(w )) / 2.0 + c2 * nz(filt ) + c3 * nz(filt )

Usecase:

First option:

Leverage the script to identify Bullish and Bearish trends, shown with green and red triangle.

Combine Different Timeframes to accurately determine market trend.

Second option:

Pull the data with API sockets to automate your trading journey.

plot(close, title="ClosePrice", display=display.status_line)

plot(open, title="OpenPrice", display=display.status_line)

plot(greencon ? 1 : redcon ? -1 : 0, title="position", display=display.status_line)

Use ClosePrice, OpenPrice and "position" titles to easily read and backtest your strategy utilising more than 1 Time Frame.

Indicator id:

USER;91bdff47320b4284a375f428f683b21e

(only relevant to those that use API requests)

Prime, E & PI Superiority CyclesIf you have been studying the markets long enough you will probably have noticed a certain pattern. Whichever trade entry/exit logic you try to use, it will go through phases of working really well and phases where it doesn't work at all. This is the markets way of ensuring anyone who sticks to an oversimplified, one-dimensional strategy will not profit. Superiority cycles are a method I devised by which code interrogates the nature of where price has been pivoting in relation to three key structures, the Prime Frame, E Frame and Pi Frame which are plotted as horizontal lines at these values:

* Use script on 1 minute chart ONLY

prime numbers up to 100: 2.0,3.0,5.0,7.0,11.0,13.0,17.0,19.0,23.0,27.0,29.0,31.0,37.0,41.0,43.0,47.0,53.0,59.0,61.0,67.0,71.0,73.0,79.0,83.0,89.0,97.0

multiples of e up to 100: 2.71828, 5.43656, 8.15484, 10.87312, 13.5914, 16.30968, 19.02796, 21.74624, 24.46452, 27.1828, 29.90108, 32.61936, 35.33764,

38.05592, 40.7742, 43.49248, 46.21076, 48.92904, 51.64732, 54.3656, 57.08388, 59.80216, 62.52044, 65.23872, 67.957, 70.67528, 73.39356000000001, 76.11184,

78.83012, 81.5484, 84.26668000000001, 86.98496, 89.70324, 92.42152, 95.13980000000001, 97.85808

multiples of pi up to 100: 3.14159, 6.28318, 9.424769999999999, 12.56636, 15.70795, 18.849539999999998, 21.99113, 25.13272, 28.27431, 31.4159, 34.55749,

37.699079999999995, 40.840669999999996, 43.98226, 47.12385, 50.26544, 53.40703, 56.54862, 59.69021, 62.8318, 65.97339, 69.11498, 72.25657, 75.39815999999999,

78.53975, 81.68133999999999, 84.82293, 87.96452, 91.10611, 94.2477, 97.38929

These values are iterated up the chart as seen below:

The script sums the distance of pivots to each of the respective frames (olive lines for Prime Frame, green lines for E Frame and maroon lines for Pi Frame) and determines which frame price has been reacting to in the least significant way. The worst performing frame is the next frame we target reversals at. The table in the bottom right will light up a color that corresponds to the frame color we should target.

Here is an example of Prime Superiority, where we prioritize trading from prime levels:

The table and the background color are both olive which means target prime levels. In an ideal world strong moves should start and finish where the white flags are placed i.e. in this case $17k and $19k. The reason these levels are 17,000 and 19,000 and not just 17 and 19 like in the original prime number sequence is due to the scaling code in the get_scale_func() which allows the code to operate on all assets.

This is E Superiority where we would hope to see major reversals at green lines:

This is Pi Superiority where we would hope to see major reversals at maroon lines:

And finally I would like to show you a market moving from one superiority to another. This can be observed by the bgcolor which tells us what the superiority was at every historical minute

Pi Frame Superiority into E Frame Superiority example:

Prime Frame Superiority into E Frame Superiority example:

Prime Frame Superiority into Pi Frame Superiority example:

By rotating the analysis we use to enter trades in this way we hope to hide our strategy better from market makers and artificial intelligence, and overall make greater profits.

Euler Frame (Dynamic)Euler frame posted as lines instead of plots, allowing for complete colour change and extension.

Be warned, the entire frame moves in real time with price so do not look at the corresponding lines for scale factors below (i.e. it will show the current levels in this graph for also under 10k).

To see the correct levels for the <10k range you can use the TV replay function or refer to my "Euler Price Levels" script, which plots accordingly with scale factor.

Confluence Zones & MidpointsConfluence zones between tight Prime / Euler / Pi levels, and their midpoints.

Colour and extend options included.

Pythagorean Means of Moving AveragesDESCRIPTION

Pythagorean Means of Moving Averages

1. Calculates a set of moving averages for high, low, close, open and typical prices, each at multiple periods.

Period values follow the Fibonacci sequence.

The "short" set includes moving average having the following periods: 5, 8, 13, 21, 34, 55, 89, 144, 233, 377.

The "mid" set includes moving average having the following periods: 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597.

The "long" set includes moving average having the following periods: 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584, 4181.

2. User selects the type of moving average: SMA, EMA, HMA, RMA, WMA, VWMA.

3. Calculates the mean of each set of moving averages.

4. User selects the type of mean to be calculated: 1) arithmetic, 2) geometric, 3) harmonic, 4) quadratic, 5) cubic. Multiple mean calculations may be displayed simultaneously, allowing for comparison.

5. Plots the mean for high, low, close, open, and typical prices.

6. User selects which plots to display: 1) high and low prices, 2) close prices, 3) open prices, and/or 4) typical prices.

7. Calculates and plots a vertical deviation from an origin mean--the mean from which the deviation is measured.

8. Deviation = origin mean x a x b^(x/y)/c.

9. User selects the deviation origin mean: 1) high and low prices plot, 2) close prices plot, or 3) typical prices plot.

10. User defines deviation variables a, b, c, x and y.

Examples of deviation:

a) Percent of the mean = 1.414213562 = 2^(1/2) = Pythagoras's constant (default).

b) Percent of the mean = 0.7071067812 = = = sin 45˚ = cos 45˚.

11. Displaces the plots horizontally +/- by a user defined number of periods.

PURPOSE

1. Identify price trends and potential levels of support and resistance.

CREDITS

1. "Fibonacci Moving Average" by Sofien Kaabar: two plots, each an arithmetic mean of EMAs of 1) high prices and 2) low prices, with periods 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584, 4181.

2. "Solarized" color scheme by Ethan Schoonover.

Eliza S&R FrameSource code for the e (euler based) S&R frame as requested by a few people. Yellow line are major levels, blue lines are minor levels but all are important. Use in conjunction with 27 minute chart or 271 minute chart if you want to go full Eulerian in your trading approach. For an asset over $10,000 the lines are $2718 apart starting from 0. For an asset over $1,000 the lines are $271.8 apart starting from 0. This pattern continues through the decimal point scale. Remember the first real attempt on one of these lines by the price is the most important. If you see a wick through price will often need to move to the next line in the frame as strong support or resistance will turn price away without ever being broken.

Euler Cubes - CubᵋI give you the "Euler Cubes", inspired by the mathematical number 'e' (Euler's number).

It is suggested (fibonacci ratios analogy) that price/e ratio can give Support/Resistance area's.

The first cube is made by a low/high of choice, for example:

You set the 'source low'/'source high' in position:

Then you choose the 'e ratio' (x times 'e')

This multiplies the distance 'high-low' times '0.271828' times 'the set number' .

For example, choosing 5 gives 5 x 0.271828 = 1.35914, the distance 'high-low' hereby multiplied by 1.35914, the following cubes multiply the previous distance by 1.35914.

(Settings below 5 will give cubes smaller than the 'high-low' distance)

In the case of x times 'e' = 5:

You can extend the lines:

Now you can give it an angle:

Do mind, using it over very little bars and using an angle can cause some lines to not align as intended, because for now, it is not possible to plot in between bars.

There are also 'Euler' SMA and EMA available with following length's:

27, 54, 82,109, 136, 163, 190 and 217

Cheers!

[RS][V4]ZigZag Percent Reversal - Helper - Retrace LevelsA helper script with multiple retrace level options.