GapDetectGap Severity Analysis Library

This library, GapDetect , simplifies the identification and evaluation of overnight gaps by leveraging statistical metrics such as standard deviation and percentage moves. It is ideal for detecting large abnormal gaps which may be used to modify how strategies may decide to enter or exit.

Key Features:

Overnight Gap Detection

Provides two core functions:

today : Computes the value of today's overnight gap.

todayPercent : Computes the percentage change for today's overnight gap.

Volatility Analysis

Includes functions for statistical gap analysis:

normal : Calculates the normal daily standard deviation of the overnight gap, filtering outliers using customizable thresholds.

normalPercent : Similar to normal , but for percentage-based gap moves.

Gap Severity Metric

severity : a positive or negative value that represents the ratio of the current overnight move compared to the standard deviation of previous ones.

Customizable Parameters

Supports custom session specifications, resolutions, and outlier thresholds.

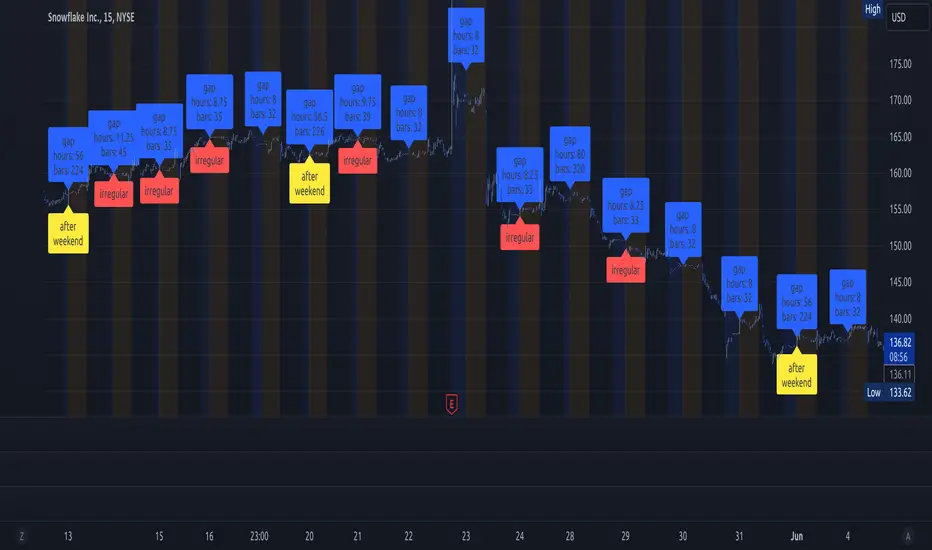

Gap

lib_session_gapsLibrary "lib_session_gaps"

simple lib to calculate the gaps between sessions

time_gap()

calculates the time gap between this and previous session (in case of irregular end of previous session, considering extended sessions)

Returns: the time gap between this and previous session in ms (time - time_close )

bar_gap()

calculates the bars missing between this and previous session (in case of irregular end of previous session, considering extended sessions)

Returns: the bars virtually missing between this and previous session (time gap / bar size in ms)

VolatilityLibrary "Volatility"

Functions for determining if volatility (true range) is within or exceeds normal.

The "True Range" (ta.tr) is used for measuring volatility.

Values are normalized by the volume adjusted weighted moving average (VAWMA) to be more like percent moves than price.

current(len) Returns the current price adjusted volatitlity ratio.

Parameters:

len : Number of bars to get a volume adjusted weighted average price.

normal(len, maxDeviation, level, gapDays, spec, res) Returns the normal upper range of volatility. Compensates for overnight gaps within a regular session.

Parameters:

len : Number of bars to measure volatility.

maxDeviation : The limit of volatility before considered an outlier.

level : The amount of standard deviation after cleaning outliers to be considered within normal.

gapDays : The number of days in the past to measure overnight gap volaility.

spec : session.regular (default), session.extended or other time spec.

res : The resolution (default = '1440').

isNormal(len, maxDeviation, level, gapDays, spec, res) Returns true if the volatility (true range) is within normal levels. Compensates for overnight gaps within a regular session.

Parameters:

len : Number of bars to measure volatility.

maxDeviation : The limit of volatility before considered an outlier.

level : The amount of standard deviation after cleaning outliers to be considered within normal.

gapDays : The number of days in the past to measure overnight gap volaility.

spec : session.regular (default), session.extended or other time spec.

res : The resolution (default = '1440').

severity(len, maxDeviation, level, gapDays, spec, res) Returns ratio of the current value to the normal value. Compensates for overnight gaps within a regular session.

Parameters:

len : Number of bars to measure volatility.

maxDeviation : The limit of volatility before considered an outlier.

level : The amount of standard deviation after cleaning outliers to be considered within normal.

gapDays : The number of days in the past to measure overnight gap volaility.

spec : session.regular (default), session.extended or other time spec.

res : The resolution (default = '1440').