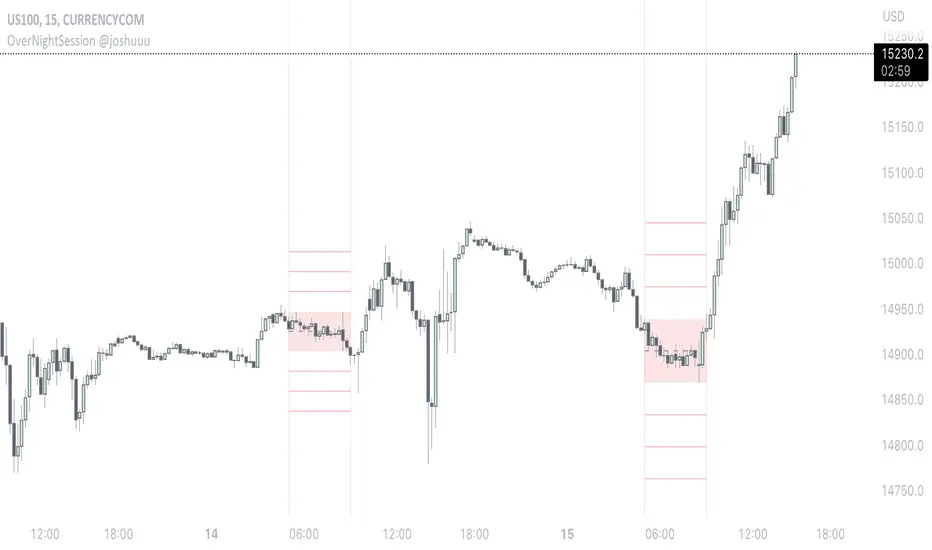

Overnight Z/VolRatio SignalThis indicator highlights overnight setups where both volatility expansion and prior-day range deviation suggest directional opportunity at the RTH open.

It calculates:

• Overnight Z-Score (Z_long): how far the overnight session’s range tilts from the 20-day overnight mean, standardized by its standard deviation.

• VolRatio: ratio of the current RTH session volume to the 20-day average, a proxy for participation and conviction.

Signal Logic (LONG bias)

A long-bias condition triggers when:

• Z_long ≥ 0.40 (overnight tilt strongly positive)

• VolRatio ≥ 1.30 (above-average RTH volume)

• Optional filters: R1/R4 region alignment, YDH/YDL proximity, and other context flags.

Visuals mark qualifying days with colored labels and session highlights.

It is intended as a context signal — not an auto-trading system — for SPY/SPX/ES or correlated large-cap indices.

Usage Notes

• Works best when applied to daily or intraday 5m chart with extended hours enabled.

• Typical exit: ~150 minutes after 09:30 ET.

• Fridays are optionally excluded to avoid expiration-related distortions.

Chỉ báo Pine Script®