Kalman Gain Parameter MechanicsFrequently asked question is to explain how Gain parameter works in kalman funtion. This script serves as a visual representation of Gain parameter of Kalman function used in HMA-Kalman & Trendlines script. (The function creator's name was misspeled in that script as Kahlman)

To see better results set your Chart's timeframe to Daily.

Smoothing

Kendall Rank Correlation NET on SMA [Loxx]Kendall Rank Correlation NET on SMA is an SMA that uses Kendall Rank Correlation to form a sort of noise elimination technology to smooth out trend shifts. You'll notice that the slope of the SMA line doesn't always match the color of the SMA line. This is behavior is expected and is the NET that removes noise from the SMA.

What is Kendall Rank Correlation?

Also commonly known as “Kendall’s tau coefficient”. Kendall’s Tau coefficient and Spearman’s rank correlation coefficient assess statistical associations based on the ranks of the data. Kendall rank correlation (non-parametric) is an alternative to Pearson’s correlation (parametric) when the data you’re working with has failed one or more assumptions of the test. This is also the best alternative to Spearman correlation (non-parametric) when your sample size is small and has many tied ranks.

Kendall rank correlation is used to test the similarities in the ordering of data when it is ranked by quantities. Other types of correlation coefficients use the observations as the basis of the correlation, Kendall’s correlation coefficient uses pairs of observations and determines the strength of association based on the patter on concordance and discordance between the pairs.

Concordant: Ordered in the same way (consistency). A pair of observations is considered concordant if (x2 — x1) and (y2 — y1) have the same sign.

Discordant: Ordered differently (inconsistency). A pair of observations is considered concordant if (x2 — x1) and (y2 — y1) have opposite signs.

Kendall’s Tau coefficient of correlation is usually smaller values than Spearman’s rho correlation. The calculations are based on concordant and discordant pairs. Insensitive to error. P values are more accurate with smaller sample sizes.

Included:

-Toggle on/off bar coloring

Adaptive, Double Jurik Filter Moving Average (AJFMA) [Loxx]Adaptive, Double Jurik Filter Moving Average (AJFMA) is moving average like Jurik Moving Average but with the addition of double smoothing and adaptive length (Autocorrelation Periodogram Algorithm) and power/volatility {Juirk Volty) inputs to further reduce noise and identify trends.

What is Jurik Volty?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

That's why investors, banks and institutions worldwide ask for the Jurik Research Moving Average ( JMA ). You may apply it just as you would any other popular moving average. However, JMA's improved timing and smoothness will astound you.

What is adaptive Jurik volatility?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman’s adaptive moving average ( KAMA ) and Tushar Chande’s variable index dynamic average ( VIDYA ) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index ( RSI ), commodity channel index ( CCI ), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

Included

- Double calculation of AJFMA for even smoother results

Nadaraya-Watson Envelope [LuxAlgo]This indicator builds upon the previously posted Nadaraya-Watson smoothers. Here we have created an envelope indicator based on Kernel Smoothing with integrated alerts from crosses between the price and envelope extremities. Unlike the Nadaraya-Watson estimator, this indicator follows a contrarian methodology.

Please note that by default this indicator can be subject to repainting. Users can use a non-repainting smoothing method available from the settings. The triangle labels are designed so that the indicator remains useful in real-time applications.

🔶 USAGE

🔹 Non Repainting

This tool can outline extremes made by the prices. This is achieved by estimating the underlying trend in the price, then calculating the mean absolute deviations from it, the obtained result is added/subtracted to the estimated underlying trend.

The non-repainting method estimates the underlying trend in price using an "endpoint Nadaraya-Watson estimator", and would return similar results to more classical band indicators.

🔹 Repainting

The repainting method makes use of the Nadaraya-Watson estimator to estimate the underlying trend in the price. The construction of the band extremities is the same as in the non-repainting method.

We can expect the price to reverse when crossing one of the envelope extremities. Crosses between the price and the envelopes extremities are indicated with triangles on the chart.

For real-time applications, triangles are always displayed when a cross occurs and remain displayed at the location it first appeared even if the cross is no longer visible after a recalculation of the envelope.

By popular demand, we have integrated alerts for this indicator from the crosses between the price and the envelope extremities. However, we do not recommend this precise method to be used alone or for solely real-time applications. We do not have data supporting the performance of this tool over more classical bands/envelope/channels indicators.

🔶 SETTINGS

Bandwidth: Controls the degree of smoothness of the envelopes, with higher values returning smoother results.

Mult: Controls the envelope width.

Source: Input source of the indicator.

Repainting Smoothing: Determine if a repainting or non-repainting method should be used for the calculation of the indicator.

🔶 RELATED SCRIPTS

For more information on the Nadaraya-Watson estimator see:

Nadaraya-Watson Smoothers [LuxAlgo]The following tool smoothes the price data using various methods derived from the Nadaraya-Watson estimator, a simple Kernel regression method. This method makes use of the Gaussian kernel as a weighting function.

Users have the option to use a non-repainting as well as a repainting method, see the USAGE section for more information.

🔶 USAGE

🔹 Non Repainting

When Repainting Smoothing is disabled the returned indicator acts similarly to a regular causal moving average. This result could be described as an "endpoint Nadaraya-Watson estimator".

Unlike a regular moving average whose degree of smoothness is commonly determined by the length of its calculation window, the degree of smoothness of the proposed indicator is determined by the bandwidth setting, with a higher value returning smoother results.

In the above chart, a bandwidth value of 50 is used. An increasing value of the smoother is indicative of an uptrend, while a decreasing value is indicative of a downtrend.

🔹 Repainting

Non-causal smoothing methods have found low support from technical analysts because they tend to repaint. Yet, they can provide powerful insights such as estimating underlying trends in the price as well as seeing how far prices deviate from them. They can also make drawing certain patterns easier and can help see underlying structures in the price more clearly.

Using higher bandwidth values allows for estimating longer-term trends in the price.

Triangular labels highlight points where the direction of the estimator change. This allows for the identification of tops and bottoms in the underlying trend which can be compared to the actual price tops and bottoms.

Note that multiple labels can appear in real time, highlighting real-time changes in the estimator's direction. The most recent label on a series of labels is the first to appear. This can eventually be useful for the real-time predictive application of the estimator. However, it is not a usage we particularly recommend.

🔶 DETAILS

The Nadaraya-Watson estimator can be described as a series of weighted averages using a specific normalized kernel as a weighting function. For each point of the estimator at time t , the peak of the kernel is located at time t , as such the highest weights are attributed to values neighboring the price located at time t .

A lower bandwidth value would contribute toward a more important weighting of the price at a precise point and would as such less smooth results. In the case where our bandwidth is so small that the resulting kernel is just an impulse, we would get the raw price back.

However, when the bandwidth is sufficiently large, prices would be weighted similarly, thus resulting in a result closer to the price mean.

It can be interesting to note that due to the nature of the estimator and its weighting procedure, real-time results would not deviate drastically for points in the estimator near the center of the calculation window.

🔶 SETTINGS

Bandwidth : controls the bandwidth of the Gaussian kernel, with higher values returning smoother results.

Src : Input source of the kernel regression.

Repainting Smoothing : Determine if the smoothing method should repaint or not. If disabled the "endpoint Nadaraya-Watson estimator" is returned.

Ehlers Adaptive Relative Strength Index V1 [CC]The Adaptive Relative Strength Index was created by John Ehlers and this is his first version. I will of course publish his updated version at a later date along with publishing the final script from Jim Sloman's Ocean Theory book. I have changed his script to include extra smoothing to provide clear buy and sell signals. This is a version of a RSI that is very adaptive to changes by finding the length of the current cycle and using that to calculate the rsi and I use this same basic process to provide extra smoothing. A great strategy of course is to buy right after the indicator goes from below the oversold level to right above it and stay in until the indicator turns red or when it reaches the overbought level. I have included strong buy and sell signals in addition to normal ones and the darker colors mean strong signals and lighter colors are normal signals.

Let me know what other indicators you would like to see me publish!

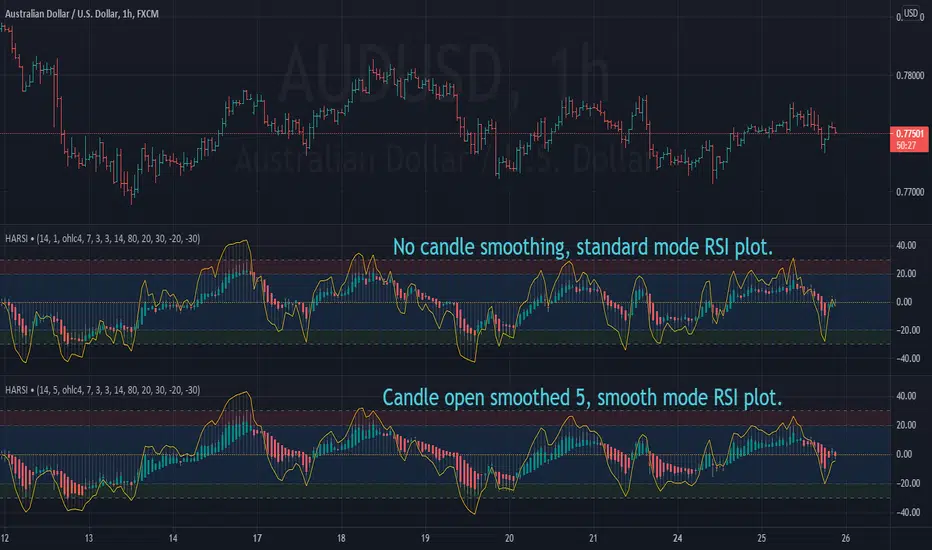

Heikin Ashi RSI OscillatorIntroducing HARSI - the RSI based Heikin Ashi candle oscillator.

...that's right, you read it correctly. This is Heikin Ashi candles in an oscillator

format derived from RSI calculations, aimed at smoothing out some of the

inherent noise seen with standard RSI indicators.

Science!

We likes it we does.

Included plot options for standard RSI plot overlay, and a smoothed variant with

it's own seperate length from the candles, oh and histogram option, for reasons.

Articles and further reading:

investopedia.com - RSI

investopedia.com - Heikin Ashi

This is a REALTIME indicator, so any values used for conditions should use

history 1, or alternatively, alerts should be called using once-per-bar-close.

Modified Smoothed Heiken AshiThis code is based on Smoothed HA candle which will work on all chart types

condition for BUY:

1. When close crosses Smoothed HA

2.Close should be in side upper band

3.BBW must be greater than the average

vice versa for sell

this code takes data from HA chart so that it can be applied on all chart type.

Bollinger band and Bollinger band width conditions added for removal of unwanted signals

Alert added so that you can apply alert and check it in real time performance

thanks to The Secret Mindset You tube channel from where I got the idea to convert this into a pine script indicator

smooth HA taken from "Smoothed Heiken Ashi Candles v1" at //@jackvmk

SAK-MPI: Smooth DXDescription : This SwissArmyKnife - MultiPurposeIndicator allows user to modify the Directional index based on one of filtering tools proposed by John F.Ehlers .

Details of each filtering type can be read in Ehlers Technical Papers: "Swiss Army Knife Indicator" and/or his book "Cybernetics Analysis for Stock and Futures"

Disclaimer:

These study scripts was built only to test/visualize an idea to see its viability and if it can be used to optimize existing strategy.

This is experimental indicator. Any ideas to further improve this indicator are welcome :)

Blackman Filter - The Smoother The BetterIntroduction

Who doesn't like smooth things? I'd like a smooth market price for christmas! But i can't get it, instead its so noisy...so you apply a filter to smooth it, such filters are called low-pass filters, they smooth and its great but they have lag, so nobody really use them, but they are pretty to look at.

Its on a childish note that i will introduce this indicator, so what it is all about? I propose a new FIR filter using a blackman function as filter kernel for financial time-series smoothing, do you prefer the childish tone ? Fear not its surprisingly easy!

The Blackman Function

The blackman function look like a bell shaped curve, look:

The blackman function will produce such curve. This function is called a cosine sum function because she is based on the sum of cosine functions, here only 2.

0.42 - 0.5 * cos(2 * pi * k) + 0.08 * cos(4 * pi * k)

Originally you use this function for windowing , what does it means? In signal processing you have a function called sync function , if you use this function as filter kernel you would get the ideal frequency domain response filter, sometime called brickwall filter, it would be extremely smooth.

Above the optimal low pass filter frequency response.

However the sync function has no ending values and goes on forever, therefore we can't use it for convolution, expect if we apply windowing. Filters using windowing are called windowed-sinc filters, i will describe the procedure below :

1 - Create a sync function = sin(pi*n)/(pi*n)

2 - Truncate it = I only keep the first length points of the sync function.

This create a abrupt end, the frequency of a filter using step 1 as kernel would contain ripples in the pass band and stop band, this is bad! The frequency response would look like this :

3 - I multiply my values of step 2 by a window function, it can the blackman window, i no longer have an abrupt end, its smooth!

The frequency response of the filter using this kernel would no longer have ripples! This is the power of windowing functions.

Here we are not using such thing, but we could in the future. Here instead we use the blackman function as filter kernel, because this function is bell shaped this mean that the filter will certainly be smooth (symmetrical weighting is a rule of thumb for kernels when we want really smooth filters).

The Filter

This filter is quite smooth, unlike the gaussian filter this filter give less weights to recent and past values, this is because the blackman function has fatter tails than the gaussian one. I could make a comparison of both, however they are quite alike, if you often use a gaussian filter its up to you to decide which one you prefer.

The filter can do a better job than the moving average when it comes to preserve the frequency components that constitute the cycles/trend.

We can see that the filter has a greater performance when it comes to keep the shape of the market price, thus it has a slightly better fit.

Conclusion

Ok so in this post you learned a bit about the sync function and windowing, those are basic subjects in signal processing, they allow us to approximate the filter with the ideal frequency response, i also showed you that those windowing function could be used as kernel and that they where pretty smooth on their own, there are many others, but the one i prefer is the blackman windowing function.

I know what you are thinking, "we want trailing stops, alerts, colors, arrows!", and i understand you pal, but sometimes its cool to take a break from all this stuff. However i can tell that i'am working on a side project that aim to estimate rolling maximum/minimum as fast as possible, any experiments will be published here, and i can ensure you that those indicators will make your day quite brighter, we will see that soon.

I hope you learned something from this post! I'am a bit tired (look i'am disappearing !)

Thanks for reading !

Setting-Less Trend-Step FilteringIntroduction

Indicators settings have been a major concern in trading strategies, in order to provide the best results each indicators involved in the strategy must have its settings optimized, when using only 1 indicator this task can easily be achieved, but an increasing number of indicators involve more slower computations, lot of softwares will use brute force for indicators settings optimization, this involve testing each indicator settings and see which setting/combination maximize the equity, in order to fasten this process softwares can use a user defined range for the indicator settings. Nonetheless the combination that maximize the equity at time t might be different at time t+1...n .

Therefore i propose an indicator without any numerical setting that aim to filter small price variations using the architecture of the T-step lsma, such indicator can provide robust filtering and can therefore be used as input for other indicators.

Robustness Vs Non Robustness

Robustness is often defined as the ability of certain statistical tools to be less affected by outliers, outliers are defined as huge variations in a data-set, high volatility movements and large gaps might be considered as outliers. However here we define robustness as the ability of an indicator to be non affected by price variations that are not correlated with the main trend, which can be defined in technical analysis as pullbacks.

Some small pullbacks in INTEL, the indicator is not affected by them, which allow the indicator to filter the price in a "smart" way.

This effect is made possible by using exponential averaging in the indicator, exponential averaging is defined as y = sc*x + (1-sc)*y , with 1 > sc > 0 . Here sc is calculated in a similar way as the kalman gain, which is in the form of a/(a + b) , in our case this is done with :

sc = abs(input - nz(b ))/(abs(input - nz(b )) + nz(a ))

Non Robust Version Of The Indicator

The user is allowed to use the non robust version of the indicator by unchecking "robust" in the setting panel, this allow a better fit with the price at the cost of less filtering.

robust checked

robust unchecked

Conclusion

I proposed a technical indicator that aim to filter short frequencies without the use of parameters, the indicator proven to be robust to various pullbacks and therefore was able to follow the main trend, although using the term trend for such small price variations might be wrong. Removing high frequencies is always beneficial in trading, noisy series are harder to manipulate, this is why you'll see a lot of indicators using median price often defined as hl2 instead of the closing price.

Like previous settings-less indicators i published this one can behave differently depending on the time frame selected by the user, lower time frames will make the indicator filter more. I'll try to make more setting-less indicators that will correct this effect.

Acknowledgements

The support and interest of the community is only thing that allowed me to be where i'am today, i'am thankful. Special thanks to the tv staff, LucF, and my family who may not have believed in this project but are still proud of their son.

Hybrid Convolution FilterIntroduction

Today i propose an hybrid filter that use a classical FIR architecture while using recursion. The proposed method aim to reduce the lag generated by fir filters. This particular filter is a sine weighted moving average, but you can change it since the indicator is built with the custom filter template (1). Even if it use recursion it still is a FIR filter since the impulse response is finite.

The Indicator

In red the hybrid swma and in blue the classic swma of both the same period. The difference can be seen.

The switch between the input price and the past values of the previous convolution values is made by using exponential averaging, the window function is the same as f(x) in the code.

Any filter can use this architecture, the indicator is built around the custom fir template, see (1)

Conclusion

I presented a FIR filter using recursion in its calculation, the integration is made with respect to the proposed template, therefore any user can simply modify f(x) to have different filter without the need to make any change. However curious users might want to change the window function of the exponential averager, in order to do so change sgn = f(i/length) in line 11 for sgn = fun(i/length) where fun is your custom function, make sure to add it at the start of the script where all the other functions declarations are.

Thanks for reading !

(1)

Template For Custom FIR Filters - Make Your Moving AverageIntroduction

FIR filters (finite impulse response) are widely used in technical analysis, there is the simple or arithmetic moving average, the triangular, the weighted, the least squares...etc. A FIR filter is characterized by the fact that its impulse response (the output of a filter using an impulse as input) is finite, this mean that the impulse response won't have infinite outputs unlike IIR filters.

They are extremely simple to design to, even without the Fourier transform, this is why i post this template that will let you create custom filters from step responses. Don't hesitate to post your results.

How It Works

Originally you create your filters from the frequency response you want your filter to have, this is because the inverse Fourier transform of the frequency response is the filter impulse response.

After that step you use convolution (convolution is the sum of the product between the signal and the impulse response) and you will have your filter. But we don't have Fourier transforms in pine so how can we possibly make FIR filters from convolution ? Well here the thing, the impulse response is the derivative of the step response and the step response is the sum of the impulse response, this mean we can create filters from step responses.

Step response of a moving average.

Step responses are easy to design, you just need a function that start at 0 and end up at 1.

How To Use The Template

All the work is done for you, the only thing you need to do is to enter your function at line 5 :

f(x)=> your function

For example if you want your filter to have a step response equal to sqrt(x) just enter :

f(x)=> sqrt(x)

This will give the following filter output :

You can create custom step responses from online graphing tools like fooplot or wolfram alpha, i recommend fooplot.

You can also design your filter step response from the line 14/15/16, b will be your filter step response, just use a , for example b = pow(a,2) , then replace output in plot by b and use overlay false, you can also plot step , if you like your step response copy the content of b and paste after f(x) => .

Filter Characteristics

The impulse response determine how many of a certain signal you want in your filter, this is also called weighting, you can think of filter design as cooking where your ingredients are the the signal at different periods and the impulse response determine how many of an ingredient you must include in the recipe. The step response can also tell you about your filter characteristics, for example :

This one converge faster to the step function, this mean that the filter will have less lag.

However this one converge slower to the step function, this mean the filter might have more lag but could be smoother.

Be aware that you must find a good weighting balance, else you can have output equals to the signal or just a delayed version of the signal without smoothing.

Real Case

Lets design a sine weighted moving average (swma), this FIR filter use the first 180 degrees of a sine wave function as impulse response.

Impulse response of the swma.

We can design it from the step response without much problems, remember that the impulse response is the derivative of the step response, therefore the derivative of the step response is equal to the first 180 degrees of a sine wave, the derivative of the cosine function is a sine function, therefore :

f(x)=> .5*(1 - cos(x*pi))

And voila.

Designing A BandPass Filter

The bandpass filter like a low-pass and high pass filter, you can think of it as a smooth oscillator.

To design a bandpass filter your step response must be bell shaped, or starting at 0 and ending at 0, for example :

f(x)=>sin(x*pi) give :

Conclusion

Just use fooplot and experiment, you could get nice filters, i will try to post some using this template but it would be really nice to have other people use it. If you need further help pm me.

Thanks for reading !

3HMAIntroduction

The Hull smoothing method aim to reduce the lag of a moving average by using a simple calculation involving smoothing with a moving average of period √p the subtraction of a moving average of period p/2 multiplied by 2 with another moving average of period p , however it is possible to extend this calculation by introducing more terms thus reducing both the lag and overshoot of the classical HMA.

Comparison

The proposed filter add 1 more term to the classical hull moving average thus ending with : sma(sma(p/3) * 3 - sma(p/2) - sma(p),p) , this can be developed as long as every terms add to total unity, more terms will often require more smoothing, this is why i replace √p by p .

In blue a HMA and in red the proposed filter of both period 50. The third term added allow for more reactivity which sometimes allow for overshoots with lower amplitudes.

Conclusions

Adding more terms to certain filtering methods can correct certain behaviours as well as reducing lag or increasing smoothing.

R2-Adaptive RegressionIntroduction

I already mentioned various problems associated with the lsma, one of them being overshoots, so here i propose to use an lsma using a developed and adaptive form of 1st order polynomial to provide several improvements to the lsma. This indicator will adapt to various coefficient of determinations while also using various recursions.

More In Depth

A 1st order polynomial is in the form : y = ax + b , our indicator however will use : y = a*x + a1*x1 + (1 - (a + a1))*y , where a is the coefficient of determination of a simple lsma and a1 the coefficient of determination of an lsma who try to best fit y to the price.

In some cases the coefficient of determination or r-squared is simply the squared correlation between the input and the lsma. The r-squared can tell you if something is trending or not because its the correlation between the rough price containing noise and an estimate of the trend (lsma) . Therefore the filter give more weight to x or x1 based on their respective r-squared, when both r-squared is low the filter give more weight to its precedent output value.

Comparison

lsma and R2 with both length = 100

The result of the R2 is rougher, faster, have less overshoot than the lsma and also adapt to market conditions.

Longer/Shorter terms period can increase the error compared to the lsma because of the R2 trying to adapt to the r-squared. The R2 can also provide good fits when there is an edge, this is due to the part where the lsma fit the filter output to the input (y2)

Conclusion

I presented a new kind of lsma that adapt itself to various coefficient of determination. The indicator can reduce the sum of squares because of its ability to reduce overshoot as well as remaining stationary when price is not trending. It can be interesting to apply exponential averaging with various smoothing constant as long as you use : (1- (alpha+alpha1)) at the end.

Thanks for reading

Well Rounded Moving AverageIntroduction

There are tons of filters, way to many, and some of them are redundant in the sense they produce the same results as others. The task to find an optimal filter is still a big challenge among technical analysis and engineering, a good filter is the Kalman filter who is one of the more precise filters out there. The optimal filter theorem state that : The optimal estimator has the form of a linear observer , this in short mean that an optimal filter must use measurements of the inputs and outputs, and this is what does the Kalman filter. I have tried myself to Kalman filters with more or less success as well as understanding optimality by studying Linear–quadratic–Gaussian control, i failed to get a complete understanding of those subjects but today i present a moving average filter (WRMA) constructed with all the knowledge i have in control theory and who aim to provide a very well response to market price, this mean low lag for fast decision timing and low overshoots for better precision.

Construction

An good filter must use information about its output, this is what exponential smoothing is about, simple exponential smoothing (EMA) is close to a simple moving average and can be defined as :

output = output(1) + α(input - output(1))

where α (alpha) is a smoothing constant, typically equal to 2/(Period+1) for the EMA.

This approach can be further developed by introducing more smoothing constants and output control (See double/triple exponential smoothing - alpha-beta filter) .

The moving average i propose will use only one smoothing constant, and is described as follow :

a = nz(a ) + alpha*nz(A )

b = nz(b ) + alpha*nz(B )

y = ema(a + b,p1)

A = src - y

B = src - ema(y,p2)

The filter is divided into two components a and b (more terms can add more control/effects if chosen well) , a adjust itself to the output error and is responsive while b is independent of the output and is mainly smoother, adding those components together create an output y , A is the output error and B is the error of an exponential moving average.

Comparison

There are a lot of low-lag filters out there, but the overshoots they induce in order to reduce lag is not a great effect. The first comparison is with a least square moving average, a moving average who fit a line in a price window of period length .

Lsma in blue and WRMA in red with both length = 100 . The lsma is a bit smoother but induce terrible overshoots

ZLMA in blue and WRMA in red with both length = 100 . The lag difference between each moving average is really low while VWRMA is way more precise.

Hull MA in blue and WRMA in red with both length = 100 . The Hull MA have similar overshoots than the LSMA.

Reduced overshoots moving average (ROMA) in blue and WRMA in red with both length = 100 . ROMA is an indicator i have made to reduce the overshoots of a LSMA, but at the end WRMA still reduce way more the overshoots while being smoother and having similar lag.

I have added a smoother version, just activate the extra smooth option in the indicator settings window. Here the result with length = 200 :

This result is a little bit similar to a 2 order Butterworth filter. Our filter have more overshoots which in this case could be useful to reduce the error with edges since other low pass filters tend to smooth their amplitude thus reducing edge estimation precision.

Conclusions

I have presented a well rounded filter in term of smoothness/stability and reactivity. Try to add more terms to have different results, you could maybe end up with interesting results, if its the case share them with the community :)

As for control theory i have seen neural networks integrated to Kalman flters which leaded to great accuracy, AI is everywhere and promise to be a game a changer in real time data smoothing. So i asked myself if it was possible for a neural networks to develop pinescript indicators, if yes then i could be replaced by AI ? Brrr how frightening.

Thanks for reading :)

Edge-Preserving FilterIntroduction

Edge-preserving smoothing is often used in image processing in order to preserve edge information while filtering the remaining signal. I introduce two concepts in this indicator, edge preservation and an adaptive cumulative average allowing for fast edge-signal transition with period increase over time. This filter have nothing to do with classic filters for image processing, those filters use kernels convolution and are most of the time in a spatial domain.

Edge Detection Method

We want to minimize smoothing when an edge is detected, so our first goal is to detect an edge. An edge will be considered as being a peak or a valley, if you recall there is one of my indicator who aim to detect peaks and valley (reference at the bottom of the post) , since this estimation return binary outputs we will use it to tell our filter when to stop filtering.

Filtering Increase By Using Multi Steps Cumulative Average

The edge detection is a binary output, using a exponential smoothing could be possible and certainly more efficient but i wanted instead to try using a cumulative average approach because it smooth more and is a bit more original to use an adaptive architecture using something else than exponential averaging. A cumulative average is defined as the sum of the price and the previous value of the cumulative average and then this result is divided by n with n = number of data points. You could say that a cumulative average is a moving average with a linear increasing period.

So lets call CMA our cumulative average and n our divisor. When an edge is detected CMA = close price and n = 1 , else n is equal to previous n+1 and the CMA act as a normal cumulative average by summing its previous values with the price and dividing the sum by n until a new edge is detected, so there is a "no filtering state" and a "filtering state" with linear period increase transition, this is why its multi-steps.

The Filter

The filter have two parameters, a length parameter and a smooth parameter, length refer to the edge detection sensitivity, small values will detect short terms edges while higher values will detect more long terms edges. Smooth is directly related to the edge detection method, high values of smooth can avoid the detection of some edges.

smooth = 200

smooth = 50

smooth = 3

Conclusion

Preserving the price edges can be useful when it come to allow for reactivity during important price points, such filter can help with moving average crossover methods or can be used as a source for other indicators making those directly dependent of the edge detection.

Rsi with a period of 200 and our filter as source, will cross triggers line when an edge is detected

Feel free to share suggestions ! Thanks for reading !

References

Peak/Valley estimator used for the detection of edges in price.

Zero Phase Filtering [Repaint] - ExperimentalImportant !

The indicator is for experimental purpose only, it must not be used as a decisional tool but only as a visual one (like Zig-Zag, Fractal etc). The information this indicator display is uncertain and subject to drastic changes over time. If you have further question feel free to pm me.

Introduction

Most of the filters you will find are causal, this mean that they depend on present and past input values, this explain the lag they produce. Non causal filters however will use future input values. A well know way to get a zero-phase filter is by using the forward backward method, but this is not possible in pinescript as i recall. So we have to use some kind of function that will display future values, this is possible using the security function in version 2 or the one in version 3 using barmerge.lookahead_on .

The Use Of A Repainting Indicator

Its always better to filter data in order to have a clearer view of what is happening, this can be useful when doing some forecasting or doing less formal kind of analysis. However since it repaint you cant use it as a signal provider or use signals of other indicators using this filter as source.

For example if you want to forecast a smooth indicator, the forecast of this indicator under normal circumstances could still have lag associated with it, so you would have to react before your forecast, this wont happen if you apply this filter as your indicator source.

The Filter

We smooth with a simple moving average the price provided by the security function twice, length control the smoothing level. Since security depend on the time frame you are in you must select your time frame in the indicator parameter selection window.

Filtering using 45 minutes time frame close price in a 5 minutes chart, we fix this by selecting our time frame.

Consider the fact that the input of the indicator is just periodic price, so sometimes the lag can sometimes be less or more than 0 and the estimation not centered.

The indicator can work on time frames up to 1h, after that the filter have some lag, i tried fixing this and i ended up having data errors.

Applying our filter as source for the rsi oscillator.

Conclusion

It is possible to have a kind of zero-phase filters, but it would be better if pinescript could support backward indexing thus making us able to do forward backward filtering.

Since noise can affect our analysis, applying smoothing without having to use offset in plot can be considered useful.

Pentuple Exponential Moving Average (PEMA)This type of moving average was originally developed by Bruno Pio in 2010. I just ported the original code from MetaTrader 5. The method uses a linear combination of EMA cascades to achieve better smoothness. Well, actually you can create your own X-uple EMA, but be sure that the combination' coefficients are valid.

Quadruple Exponential Moving Average (QEMA)This type of moving average was originally developed by Bruno Pio in 2010. I just ported the original code from MetaTrader 5.

Parabolic Weighted Moving AverageThe weights of this moving average are powers of the weights of the standard weighted moving average WMA .

Remember:

When parameter Power = 0, you will get SMA .

When parameter Power = 1, you will get WMA .

Good luck!

Kalman SmootherA derivation of the Kalman Filter.

Lower Gain values create smoother results.The ratio Smoothing/Lag is similar to any Low Lagging Filters.

The Gain parameter can be decimal numbers.

Kalman Smoothing With Gain = 20

For any questions/suggestions feel free to contact me

One Dimensional Parametric Kalman FilterA One Dimensional Kalman Filter, the particularity of Kalman Filtering is the constant recalculation of the Error between the measurements and the estimate.This version is modified to allow more/less filtering using an alternative calculation of the error measurement.

Camparison of the Kalman filter Red with a moving average Black of both period 50

Can be used as source for others indicators such as stochastic/rsi/moving averages...etc

For any questions/suggestions feel free to contact me