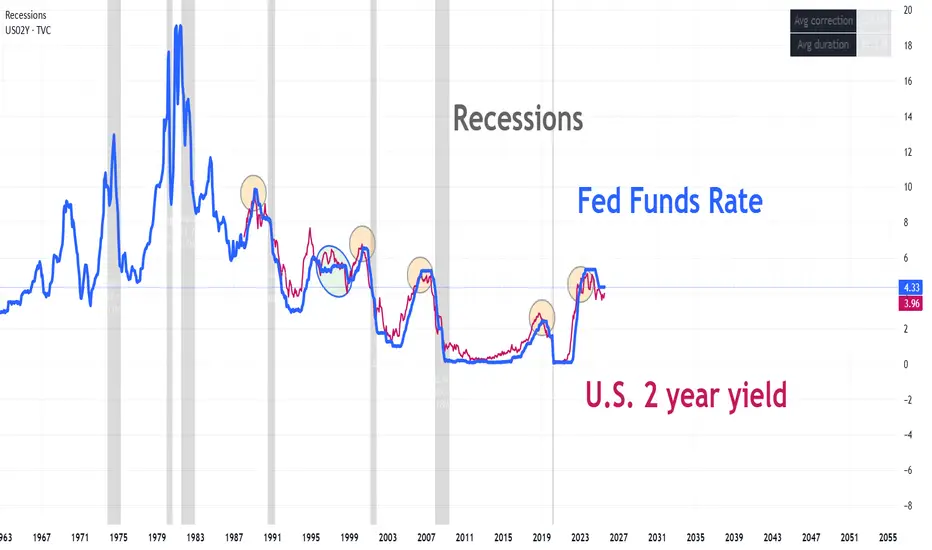

On August 4, we published a report analyzing the relationship between the 2-year yield and the Fed rate. At first glance, it looks like a technical oscillator, except in this case it represents market expectations for the 2-year rate. It embeds the expected real rate, expected inflation, and the term premium. Every time it gave a short signal, a recession followed shortly after. It generated one false signal and correctly anticipated the last four recessions. Two weeks after the report, Jackson Hole brought the pseudo-confirmation of the rate cut.

@intermarketflow

Thông báo miễn trừ trách nhiệm

Thông tin và ấn phẩm không có nghĩa là và không cấu thành, tài chính, đầu tư, kinh doanh, hoặc các loại lời khuyên hoặc khuyến nghị khác được cung cấp hoặc xác nhận bởi TradingView. Đọc thêm trong Điều khoản sử dụng.

@intermarketflow

Thông báo miễn trừ trách nhiệm

Thông tin và ấn phẩm không có nghĩa là và không cấu thành, tài chính, đầu tư, kinh doanh, hoặc các loại lời khuyên hoặc khuyến nghị khác được cung cấp hoặc xác nhận bởi TradingView. Đọc thêm trong Điều khoản sử dụng.