OPEN-SOURCE SCRIPT

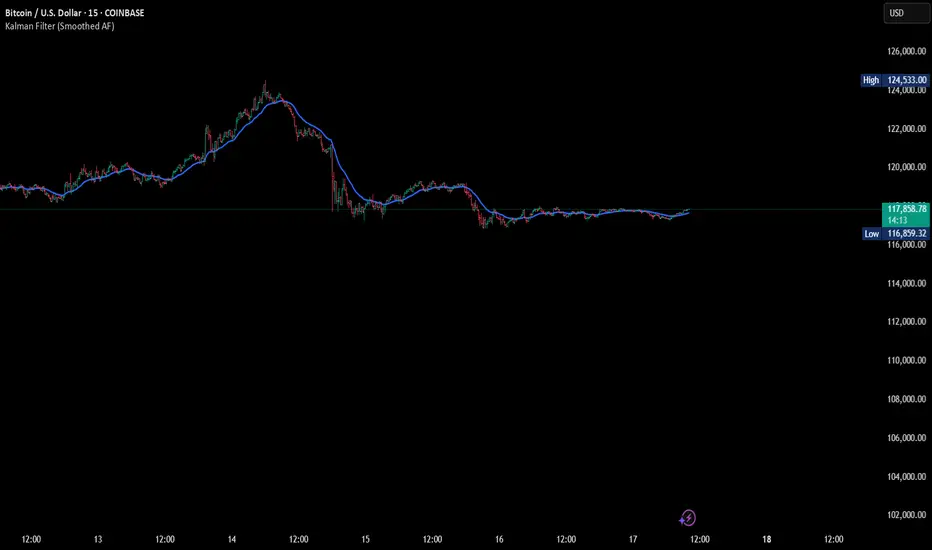

Kalman Filter (Smoothed)

The Kalman Filter is a recursive statistical algorithm that smooths noisy price data while adapting dynamically to new information. Unlike simple moving averages or EMAs, it minimizes lag by balancing measurement noise (R) and process noise (Q), giving traders a clean, adaptive estimate of true price action.

🔹 Core Features

Real-time recursive estimation

Adjustable noise parameters (R = sensitivity to price, Q = smoothness vs. responsiveness)

Reduces market noise without heavy lag

Overlay on chart for direct comparison with raw price

🔹 Trading Applications

Smoother trend visualization compared to traditional MAs

Spotting true direction during volatile/sideways markets

Filtering out market “whipsaws” for cleaner signals

Building blocks for advanced quant/trading models

⚠️ Note: The Kalman Filter is a state-space model; it doesn’t predict future price, but smooths past and present data into a more reliable signal.

🔹 Core Features

Real-time recursive estimation

Adjustable noise parameters (R = sensitivity to price, Q = smoothness vs. responsiveness)

Reduces market noise without heavy lag

Overlay on chart for direct comparison with raw price

🔹 Trading Applications

Smoother trend visualization compared to traditional MAs

Spotting true direction during volatile/sideways markets

Filtering out market “whipsaws” for cleaner signals

Building blocks for advanced quant/trading models

⚠️ Note: The Kalman Filter is a state-space model; it doesn’t predict future price, but smooths past and present data into a more reliable signal.

Mã nguồn mở

Theo đúng tinh thần TradingView, tác giả của tập lệnh này đã công bố nó dưới dạng mã nguồn mở, để các nhà giao dịch có thể xem xét và xác minh chức năng. Chúc mừng tác giả! Mặc dù bạn có thể sử dụng miễn phí, hãy nhớ rằng việc công bố lại mã phải tuân theo Nội quy.

Thông báo miễn trừ trách nhiệm

Thông tin và các ấn phẩm này không nhằm mục đích, và không cấu thành, lời khuyên hoặc khuyến nghị về tài chính, đầu tư, giao dịch hay các loại khác do TradingView cung cấp hoặc xác nhận. Đọc thêm tại Điều khoản Sử dụng.

Mã nguồn mở

Theo đúng tinh thần TradingView, tác giả của tập lệnh này đã công bố nó dưới dạng mã nguồn mở, để các nhà giao dịch có thể xem xét và xác minh chức năng. Chúc mừng tác giả! Mặc dù bạn có thể sử dụng miễn phí, hãy nhớ rằng việc công bố lại mã phải tuân theo Nội quy.

Thông báo miễn trừ trách nhiệm

Thông tin và các ấn phẩm này không nhằm mục đích, và không cấu thành, lời khuyên hoặc khuyến nghị về tài chính, đầu tư, giao dịch hay các loại khác do TradingView cung cấp hoặc xác nhận. Đọc thêm tại Điều khoản Sử dụng.