rj_temu_pair_tradea simple "temu" implementation of a pair trade

see robotjames.substack.com for details.

Dải Bollinger (BB)

Long Bollinger Bands StrategyLong Bollinger Bands Strategy (XAUUSD) — Lower Band Reversal + 4-Step Scaling + Daily DD Guard

Long Bollinger Bands Strategy is a long-only Bollinger Bands reversal/mean-reversion strategy designed mainly for XAUUSD. It looks for a bearish push below the Lower Band followed by a bullish reclaim on candle close, then optionally scales in up to 4 entries (E1–E4) as price pulls back.

1) Risk Management & Position Sizing

The strategy includes a USD-based risk input: Risk per setup (USD).

It automatically calculates position size using the average SL distance across the 4-entry structure, then distributes size across entries with built-in weighting.

BackTest Lot checkbox:

OFF (default): uses normalized sizing (qty divided by 100)

ON: uses raw qty for backtesting workflows

2) SL/TP Management (Locked SL + Optional Range TP)

Stop Loss (SL): based on SL distance (pips from entry) from E1.

Take Profit (TP):

If TP (pips) > 0: fixed pip TP from E1

If TP (pips) = 0: TP is based on the signal candle range (high–low)

SL Lock: once the stop is tightened, it never loosens again (only moves in a protective direction) until the trade closes.

3) Daily Drawdown Protection

Tracks equity by day and stops opening new positions once Max daily drawdown (USD) is reached for that day.

4) Notes / Disclaimer

This strategy does not use volume, RSI, fundamentals, news filters, or session filters. Users should apply discretion and consider confirmations from other tools and market context. Results depend on symbol settings, spread, commission, and volatility regime. Always forward-test before using in live trading.

Designed for XAUUSD. The script uses an internal pip conversion (pipSize = 0.1) consistent with common gold quoting; verify your broker’s pip definition for best alignment.

5) Suggested Usage

Best used during volatile conditions or after a clear lower-band sweep and reclaim.

Consider pairing with trend filters or higher-timeframe bias.

6) Release Notes

Initial release: Long-only BB reclaim logic with 4-step scaling

Added: SL/TP lock logic and visual SL/TP lines

Added: Daily drawdown guard and backtest lot toggle OANDA:XAUUSD

Bollinger Bands Mean Reversion using RSI [Krishna Peri]How it Works

Long entries trigger when:

- RSI reaches oversold levels, and

- At least one bullish candle closes inside the lower Bollinger Band

Short entries trigger when:

- RSI reaches overbought levels, and

- At least one bearish candle closes inside the upper Bollinger Band

This approach aims to capture exhaustion moves where price pushes into extreme deviation from its mean and then snaps back toward the middle band.

Important Disclaimer

This is a mean-reversion strategy, which means it performs best in sideways, ranging, or slowly oscillating market conditions. When markets shift into strong trends, Bollinger Bands expand and volatility increases, which may cause some signals to become inaccurate or fail altogether.

For best results, combine this script with:

- Price action

- Market structure

- Higher-timeframe trend context

- Previous day/week/month highs & lows

- Untested liquidity levels or imbalance zones

- Session timing (Asia, London, NY)

Using these confluences helps filter out low-probability trades and significantly improves consistency and precision.

Center and Volume AnalyzerCenter and Volume Analyzer that utilizes the chart's Center of Gravity alongside the Rate of Change with Bollinger Bands with a basis for the midpoint. As always, none of this is investment or financial advice. Please do your own due diligence and research.

MPI Strategy (Hardcoded 2025)MPI Strategy (Hardcoded 2025)MPI Strategy (Hardcoded 2025)MPI Strategy (Hardcoded 2025)MPI Strategy (Hardcoded 2025)

Pro Bollinger Bands Strategy [Breno]This strategy excels in highly volatile financial instruments, including cryptocurrencies, high-beta stocks, commodity futures, and certain exchange-traded funds (ETFs) that exhibit clear mean-reversion characteristics around their Bollinger Bands. The system's ability to utilize scaling (position averaging) and an ATR-based stop loss makes it particularly effective in markets with significant price swings, allowing the trader to capture profits from price extremes while managing increased volatility-related risk.

Core Strategy Logic

This Strategy implements a comprehensive trend-following and mean-reversion strategy primarily leveraging the Bollinger Bands (BB) indicator for entry and exit signals, complemented by an Average True Range (ATR)-based Stop Loss mechanism and an optional EMA filter. It is designed with robust features for capital management, including configurable leverage and a sophisticated position averaging (scaling) system.

Long Entry: A long position is initiated when the closing price crosses over the Lower Bollinger Band (ta.crossover(close,lowerBB)). This signals a potential mean-reversion opportunity following a price dip.

Short Entry: A short position is initiated when the closing price crosses under the Upper Bollinger Band (ta.crossunder(close,upperBB)). (Note: Short entries are disabled by default in the script inputs).

Exit Conditions (Profit Target): Long positions aim to exit upon interaction with the Upper Bollinger Band. Users can select from three exit methods:

"Close When Touch": Exits when close≥upperBB.

"Close Above then Below": Exits when the previous close was above the upper band, and the current close is below it (a reversal signal).

"High Above": Exits when high>upperBB. The strategy features an optional profitOnly setting, which restricts all exits to only occur if the trade is currently in profit (i.e., close is above the strategy.position_avg_price for longs).

Key Features and Customization

Bollinger Bands & Filters -

Customizable BB Parameters: The Length and Deviation of the Bollinger Bands are fully adjustable, allowing users to fine-tune the sensitivity of the entry and exit signals.

Optional EMA Filter: An optional EMA Filter can be enabled to align entries with the prevailing trend, where a Long entry is only permitted if close≥EMA(EmaFilterRange).

Risk and Capital Management -

Equity Allocation: Position size is dynamically calculated based on a Percentage of Equity (capitalPerc) combined with the set Leverage multiplier.

Dynamic Stop Loss (ATR-Based):

An optional Stop Loss (SL) is calculated using a multiple (slAtrInput) of the Average True Range (ATR).

The SL is set relative to the entry price upon trade activation, providing a volatility-adjusted risk management layer.

Position Averaging (Scaling): The script supports the addition of multiple units (pyramiding) to an existing position based on three user-selected criteria:

"No": No averaging.

"Percent": Adds to the position if the price has dropped by a set percentage (addPct) from the average price.

"ATR": Adds to the position if the current price is significantly below a calculated ATR-based support level from the average price.

Oleg_Aryukov_StrategyTrader Oleg Aryukov's strategy, based on a variety of oscillators, allows him to try to catch reversals in cryptocurrencies.

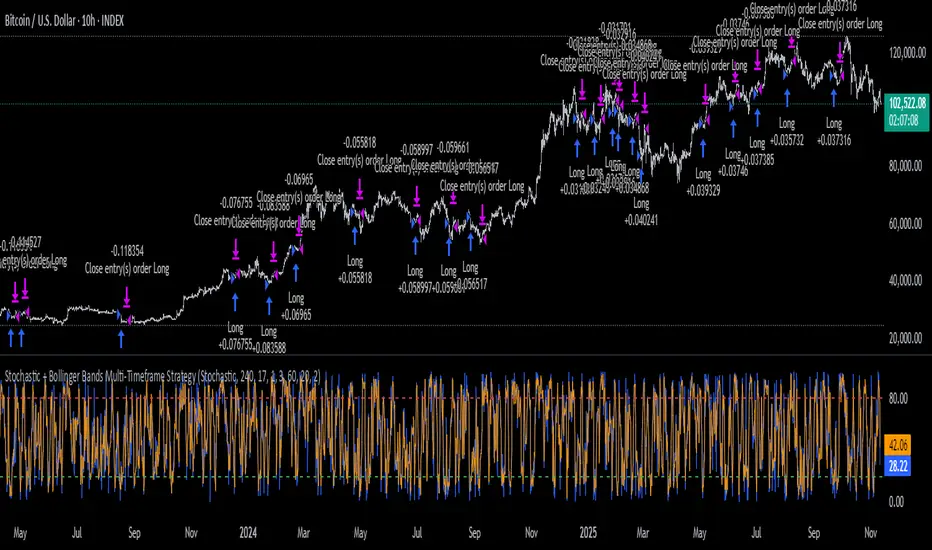

Stochastic + Bollinger Bands Multi-Timeframe StrategyThis strategy fuses the Stochastic Oscillator from the 4-hour timeframe with Bollinger Bands from the 1-hour timeframe, operating on a 10-hour chart to capture a unique volatility rhythm and temporal alignment discovered through observational alpha.

By blending momentum confirmation from the higher timeframe with short-term volatility extremes, the strategy leverages what some traders refer to as “rotating volatility” — a phenomenon where multi-timeframe oscillations sync to reveal hidden trade opportunities.

🧠 Strategy Logic

✅ Long Entry Condition:

Stochastic on the 4H timeframe:

%K crosses above %D

Both %K and %D are below 20 (oversold zone)

Bollinger Bands on the 1H timeframe:

Price crosses above the lower Bollinger Band, indicating a potential reversal

→ A long trade is opened when both momentum recovery and volatility reversion align.

✅ Long Exit Condition:

Stochastic on the 4H:

%K crosses below %D

Both %K and %D are above 80 (overbought zone)

Bollinger Bands on the 1H:

Price reaches or exceeds the upper Bollinger Band, suggesting exhaustion

→ The long trade is closed when either signal suggests a potential reversal or overextension.

🧬 Temporal Structure & Alpha

This strategy is deployed on a 10-hour chart — a non-standard timeframe that may align more effectively with multi-timeframe mean reversion dynamics.

This subtle adjustment exploits what some traders identify as “temporal drift” — the desynchronization of volatility across timeframes that creates hidden rhythm in price action.

→ For example, Stochastic on 4H (lookback 17) and Bollinger Bands on 1H (lookback 20) may periodically sync around 10H intervals, offering unique alpha windows.

📊 Indicator Components

🔹 Stochastic Oscillator (4H, Length 17)

Detects momentum reversals using %K and %D crossovers

Helps define overbought/oversold zones from a mid-term view

🔹 Bollinger Bands (1H, Length 20, ±2 StdDev)

Measures price volatility using standard deviation around a moving average

Entry occurs near lower band (support), exits near upper band (resistance)

🔹 Multi-Timeframe Logic

Uses request.security() to safely reference 4H and 1H indicators from a 10H chart

Avoids repainting by using closed higher-timeframe candles only

📈 Visualization

A plot selector input allows toggling between:

Stochastic Plot (%K & %D, with overbought/oversold levels)

Bollinger Bands Plot (Upper, Basis, Lower from 1H data)

This helps users visually confirm entry/exit triggers in real time.

🛠 Customization

Fully configurable Stochastic and BB settings

Timeframes are independently adjustable

Strategy settings like position sizing, slippage, and commission are editable

⚠️ Disclaimer

This strategy is intended for educational and informational purposes only.

It does not constitute financial advice or a recommendation to buy or sell any asset.

Market conditions vary, and past performance does not guarantee future results.

Always test any trading strategy in a simulated environment and consult a licensed financial advisor before making real-world investment decisions.

BB SPY Mean Reversion Investment StrategySummary

Mean reversion first, continuation second. This strategy targets equities and ETFs on daily timeframes. It waits for price to revert from a Bollinger location with candle and EMA agreement, then manages risk with ATR based exits. Uniqueness comes from two elements working together. One, an adaptive band multiplier driven by volatility of volatility that expands or contracts the envelope as conditions change. Two, a bias memory that re arms the same direction after any stop, target, or time exit until a true opposite signal appears. Add it to a clean chart, use the markers and levels, and select on bar close for conservative alerts. Shapes can move while the bar is open and settle on close.

Scope and intent

• Markets. Currently adapted for SPY, needs to be optimized for other assets

• Timeframes. Daily primary. Other frames are possible but not the default

• Default demo. SPY on daily

• Purpose. Trade mean reversion entries that can chain into a longer swing by splitting holds into ATR or time segments

Originality and usefulness

• Novelty. Adaptive band width from volatility of volatility plus a persistent bias array that keeps the original direction alive across sequential entries until an opposite setup is confirmed

• Failure modes mitigated. False starts in chop are reduced by candle color and EMA location. Missed continuation after a take profit or stop is addressed by the re arm engine. Oversized envelopes during quiet regimes are avoided by the adaptive multiplier

• Testability. Every module has Inputs and visible levels so users can see why a suggestion appears

• Portable yardstick. All risk and targets are expressed in ATR units

Method overview in plain language

The engine measures where price sits relative to Bollinger bands, confirms with candle color and EMA location, requires ADX for shorts(in our case long close since we use it currently as long only), and optionally requires a trend or mean reversion regime using band width percent rank and basis slope. Risk uses ATR for stop, target, and optional breakeven. A small array stores the last confirmed direction. While flat, the engine keeps a pending order in that direction. The array flips only when a true opposite setup appears.

Base measures

• Range basis. True Range smoothed over a user defined ATR Length

• Return basis. Not required

Components

• Bollinger envelope. SMA length and standard deviation multiplier. Entry is based on cross of close through the band with location bias

• Candle and EMA filter. Close relative to open and close relative to EMA align direction

• ADX gate for shorts. Requires minimum trend strength for short trades

• Adaptive multiplier. Band width scales using volatility of volatility so envelopes breathe with conditions

• Regime gate optional. Band width percent rank and basis slope identify trend or mean reversion regimes

• Risk manager. ATR stop, ATR target, optional breakeven, optional time exit

• Bias memory. Array stores last confirmed direction and re arms entries while flat

Fusion rule

Minimum satisfied gates count style. All required gates must be true. Optional gates are controlled in Inputs. Bias memory never overrides an opposite confirmed setup.

Signal rule

• Long setup when close crosses up through the lower band, the bar closes green, and close is above the long EMA

• Short setup when close crosses down through the upper band, the bar closes red, close is below the short EMA, and ADX is above the minimum

• While flat the model keeps a pending order in the stored direction until a true opposite setup appears

• IN LONG or IN SHORT describes states between entry and exit

What you will see on the chart

• Markers for Long and Short setups

• Exit markers from ATR or time rules

• Reference levels for entry, stop, and target

• Bollinger bands and optional adaptive bands

Inputs with guidance

Setup

• Signal timeframe. Uses the chart timeframe

• Invert direction optional. Flips long and short

Logic

• BB Length. Typical 10 to 50. Higher smooths more

• BB Mult. Typical 1.0 to 2.5. Higher widens entries

• EMA Length long. Typical 10 to 50

• EMA Length short. Typical 5 to 30

• ADX Minimum for short. Typical 15 to 35

Filters

• Regime Type. none or trend or mean reversion

• Rank Lookback. Typical 100 to 300

• Basis Slope Length and Threshold. Larger values reduce false trends

Risk

• ATR Length. Typical 10 to 21

• ATR Stop Mult. Typical 1.0 to 3.0

• ATR Take Profit Mult. Typical 2.0 to 5.0

• Breakeven Trigger R. Move stop to entry after the chosen multiple

• Time Exit. Minimum bars and extension when profit exceeds a fraction of ATR

Bias and rearm

• Bias flips kept. Array depth

• Keep rearm when flat. Maintain a pending order while flat

UI

• Show markers and levels. Clean defaults

Usage recipes

Alerts update in real time and can change while the bar forms. Select on bar close for conservative workflows.

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• If any higher timeframe calls are enabled, request.security uses lookahead off

• Commission 0.03 percent

• Slippage 3 ticks

• Default order size method Percent of equity with value 5

• Pyramiding 0

• Process orders on close On

• Bar magnifier Off

• Recalculate after order is filled Off

• Calc on every tick Off

Realism and responsible publication

No performance claims. Costs and fills vary by venue. Shapes can move intrabar and settle on close. Strategies use standard candles only.

Honest limitations and failure modes

High impact releases and thin liquidity can break assumptions. Gap heavy symbols may require larger ATR. Very quiet regimes can reduce contrast in the mean reversion signal. If stop and target can both be touched inside one bar, outcome follows the TradingView order model for that bar path.

Regimes with extreme one sided trend and very low volatility can reduce mean reversion edges. Results vary by symbol and venue. Past results never guarantee future outcomes.

Open source reuse and credits

None.

Backtest realism

Costs are realistic for liquid equities. Sizing does not exceed five percent per trade by default. Any departure should be justified by the user.

If you got any questions please le me know

Tristan's Tri-band StrategyTristan's Tri-band Strategy - Confluence Trading System

Strategy Overview:

This strategy combines three powerful technical indicators - RSI, Williams %R, and Bollinger Bands - into a single visual trading system. Instead of cluttering your chart with separate indicator panels, all signals are displayed directly on the price chart using color-coded gradient overlays, making it easy to spot high-probability trade setups at a glance.

How It Works:

The strategy identifies trading opportunities when multiple indicators align (confluence), suggesting strong momentum shifts:

📈 Long Entry Signals:

RSI drops to 30 or below (oversold)

Williams %R reaches -80 to -100 range (oversold)

Price touches or breaks below the lower Bollinger Band

All three conditions must align during your selected trading session

📉 Short Entry Signals:

RSI rises to 70 or above (overbought)

Williams %R reaches 0 to -20 range (overbought)

Price touches or breaks above the upper Bollinger Band

All three conditions must align during your selected trading session

Visual Indicators:

(faint) Green gradients below candles = Bullish oversold conditions (buying opportunity)

(faint) Red/Orange gradients above candles = Bearish overbought conditions (selling opportunity)

Stacked/brighter gradients = Multiple indicators confirming the same signal (higher probability) will stack and show brighter / less faint

Blue Bollinger Bands = Volatility boundaries and mean reversion zones

Exit Strategy:

Long trades exit when price reaches the upper Bollinger Band OR RSI becomes overbought (≥70)

Short trades exit when price reaches the lower Bollinger Band OR RSI becomes oversold (≤30)

Key Features:

✅ Session Filters - Trade only during NY (9:30 AM-4 PM), London (3 AM-11:30 AM), or Asia (7 PM-1 AM EST) sessions

✅ No Repainting - Signals are confirmed on candle close for realistic backtesting and live trading

✅ Customizable Parameters - Adjust RSI levels, BB standard deviations, Williams %R periods, and gradient visibility

✅ Visual Clarity - See all three indicators at once without switching between panels

✅ Built-in Alerts - Get notified when entry and exit conditions are met

How to Use Effectively:

Choose Your Trading Session - For day trading US stocks, enable only the NY session. For forex or 24-hour markets, select the sessions that match your schedule.

Look for Gradient Stacking - The brightest, most visible gradients occur when both RSI and Williams %R signal together. These are your highest-probability setups.

Confirm with Price Action - Wait for the candle to close before entering. The strategy enters on the next bar's open to prevent repainting.

Respect the Bollinger Bands - Entries occur at the outer bands (price extremes), and exits occur at the opposite band or when momentum reverses.

Backtest First - Test the strategy on your preferred instruments and timeframes. Works best on liquid assets with clear trends and mean reversion patterns (stocks, major forex pairs, indices).

Adjust Gradient Visibility - Use the "Gradient Strength" slider (lower = more visible) to make signals stand out on your chart style.

Best Timeframes: 5-minute to 1-hour charts for intraday trading; 4-hour to daily for swing trading (I have also found the 3 hour timeframe to work really well for some stocks / ETFs.)

Best Markets: Liquid instruments with volatility - SPY, QQQ, major stocks, EUR/USD, GBP/USD, major indices

Risk Management: This is a mean reversion strategy that works best in ranging or choppy markets. In strong trends, signals may appear less frequently. Always use proper position sizing and stop losses based on your risk tolerance.

----------------------------------------------

Note: Past performance does not guarantee future results. This strategy is provided for educational purposes. Always backtest thoroughly and practice proper risk management before live trading.RetryClaude can make mistakes. Please double-check responses. Sonnet 4.5

Bollinger Bands Breakout StrategyHey guys check out this strategy script.

Chart plotting:

I use a classic plot of Bollinger Bands to define a consolidation zone, I also use a separate Trend Filter (SMA).

Logic:

When the price is above the SMA and above the Bollinger Upper Band the strategy goes Long. When the price is below the SMA and below the Bollinger Lower Band the strategy goes Short. Simple.

Exits:

TP and SL are a percentage of the price.

Notes: This simple strategy can be used at any timeframe (I prefer the 15min for day trading). It avoids consolidation, when the price is inside the Bollinger Bands, and has a good success rate. Adjust the Length of the BB to suit your style of trading (Lower numbers=more volatile, Higher numbers=more restrictive). Also you can adjust the Trend Filter SMA, I presonally chose the 50 SMA. Finally the SL/TP can be also adjusted from the input menu.

Test it for yourself!

Have great trades!

Fury by Tetrad Fury by Tetrad

What it is:

A rules-based Bollinger+RSI strategy that fades extremes: it looks for price stretching beyond Bollinger Bands while RSI confirms exhaustion, enters countertrend, then exits at predefined profit multipliers or optional stoploss. “Ultra Glow” visuals are purely cosmetic.

How it works — logic at a glance

Framework: Classic Bollinger Bands (SMA basis; configurable length & multiplier) + RSI (configurable length).

Long entries:

Price closes below the lower band and RSI < Long RSI threshold (default 28.3) → open LONG (subject to your “Market Direction” setting).

Short entries:

Price closes above the upper band and RSI > Short RSI threshold (default 88.4) → open SHORT.

Profit exits (price targets):

Uses simple multipliers of the strategy’s average entry price:

Long exit = `entry × Long Exit Multiplier` (default 1.14).

Short exit = `entry × Short Exit Multiplier` (default 0.915).

Risk controls:

Optional pricebased stoploss (disabled by default) via:

Long stop = `entry × Long Stop Factor` (default 0.73).

Short stop = `entry × Short Stop Factor` (default 1.05).

Directional filter:

“Market Direction” input lets you constrain entries to Market Neutral, Long Only, or Short Only.

Visuals:

“Ultra Glow” draws thin layered bands around upper/basis/lower; these do not affect signals.

> Note: Inputs exist for a timebased stop tracker in code, but this version exits via targets and (optional) price stop only.

Why it’s different / original

Explicit extreme + momentum pairing: Entries require simultaneous band breach and RSI exhaustion, aiming to avoid entries on gardenvariety volatility pokes.

Deterministic exits: Multiplier-based targets keep results auditable and reproducible across datasets and assets.

Minimal, unobtrusive visuals: Thin, layered glow preserves chart readability while communicating regime around the Bollinger structure.

Inputs you can tune

Bollinger: Length (default 205), Multiplier (default 2.2).

RSI: Length (default 23), Long/Short thresholds (28.3 / 88.4).

Targets: Long Exit Mult (1.14), Short Exit Mult (0.915).

Stops (optional): Enable/disable; Long/Short Stop Factors (0.73 / 1.05).

Market Direction: Market Neutral / Long Only / Short Only.

Visuals: Ultra Glow on/off, light bar tint, trade labels on/off.

How to use it

1. Timeframe & assets: Works on any symbol/timeframe; start with liquid majors and 60m–1D to establish baseline behavior, then adapt.

2. Calibrate thresholds:

Narrow/meanreverting markets often tolerate tighter RSI thresholds.

Fast/volatile markets may need wider RSI thresholds and stronger stop factors.

3. Pick realistic targets: The default multipliers are illustrative; tune them to reflect typical mean reversion distance for your instrument/timeframe (e.g., ATRinformed profiling).

4. Risk: If enabling stops, size positions so risk per trade ≤ 1–2% of equity (max 5–10% is a commonly cited upper bound).

5. Mode: Use Long Only or Short Only when your discretionary bias or higher timeframe model favors one side; otherwise Market Neutral.

Recommended publication properties (for backtests that don’t mislead)

When you publish, set your strategy’s Properties to realistic values and keep them consistent with this description:

Initial capital: 10,000 (typical retail baseline).

Commission: ≥ 0.05% (adjust for your venue).

Slippage: ≥ 2–3 ticks (or a conservative pertrade value).

Position sizing: Avoid risking > 5–10% equity per trade; fixedfractional sizing ≤ 10% or fixedcash sizing is recommended.

Dataset / sample size: Prefer symbols/timeframes yielding 100+ trades over the tested period for statistical relevance. If you deviate, say why.

> If you choose different defaults (e.g., capital, commission, slippage, sizing), explain and justify them here, and use the same settings in your publication.

Interpreting results & limitations

This is a countertrend approach; it can struggle in strong trends where band breaches compound.

Parameter sensitivity is real: thresholds and multipliers materially change trade frequency and expectancy.

No predictive claims: Past performance is not indicative of future results. The future is unknowable; treat outputs as decision support, not guarantees.

Suggested validation workflow

Try different assets. (TSLA, AAPL, BTC, SOL, XRP)

Run a walkforward across multiple years and market regimes.

Test several timeframes and multiple instruments. (30m Suggested)

Compare different commission/slippage assumptions.

Inspect distribution of returns, max drawdown, win/loss expectancy, and exposure.

Confirm behavior during trend vs. range segments.

Alerts & automation

This release focuses on chart execution and visualization. If you plan to automate, create alerts at your entry/exit conditions and ensure your broker/venue fills reflect your slippage/fees assumptions.

Disclaimer

This script is provided for educational and research purposes. It is not investment advice. Trading involves risk, including the possible loss of principal. © Tetrad Protocol.

Universal Breakout Strategy [KedArc Quant]Description:

A flexible breakout framework where you can test different logics (Prev Day, Bollinger, Volume, ATR, EMA Trend, RSI Confirm, Candle Confirm, Time Filter) under one system.

Choose your breakout mode, and the strategy will handle entries, exits, and optional risk management (ATR stops, take-profits, daily loss guard, cooldowns).

An on-chart info table shows live mode values (like Prev High/Low, Bollinger levels, RSI, etc.) plus P&L stats for quick analysis.

Use it to compare which breakout style works best on your instrument and timeframe, whether intraday, swing, or positional trading

🔑 Why it’s useful

* Flexibility: Switch between breakout strategies without loading different indicators.

* Clarity: On-chart info table displays current mode, relevant indicator levels, and live strategy P&L stats.

* Testing efficiency: Quickly A/B test different breakout styles under the same backtest environment.

* Transparency: Every trade is rule-based and displayed with entry/exit markers.

🚀 How it helps traders

* Lets you experiment with breakout strategies quickly without loading multiple scripts.

* Helps identify which breakout method fits your instrument & timeframe.

* Gives clear on-chart visual + statistical feedback for confident decision-making.

⚙️ Input Configuration

* Breakout Mode → choose which strategy to test:

* *Prev Day* → breakouts of yesterday’s High/Low.

* *Bollinger* → Upper/Lower BB pierce.

* *Volume* → Breakout confirmed with volume above average.

* *ATR Stop* → Wide range breakout using ATR filter.

* *Time Filter* → Breakouts inside defined session hours.

* *EMA Trend* → Breakouts only in EMA fast > slow alignment.

* *RSI Confirm* → Breakouts with RSI confirmation (e.g. >55 for longs).

* *Candle Confirm* → Breakouts validated by bullish/bearish candle.

* Lookback / ATR / Bollinger inputs → adjust sensitivity.

* Intrabar mode → option to evaluate breakouts using bar highs/lows instead of closes.

* Table options → show/hide info table, show/hide P&L stats, choose corner placement.

📈 Entry & Exit Logic

* Entry → occurs when breakout condition of chosen mode is met.

* Exit → default exits via opposite signals or optional stop/target if enabled.

* Session filter → optional auto-flat at session end.

* P&L management → optional daily loss guard, cooldown between trades, and ATR-based stop/take profit.

❓ FAQ — Choosing the best setup

Q: Which strategy should I use for which chart?

* *Prev Day Breakouts*: Best on indices, FX, and liquid futures with strong daily levels.

* *Bollinger*: Works well in range-bound environments, or crypto pairs with volatility compression.

* *Volume*: Good on equities where breakout strength is tied to volume spikes.

* *ATR Stop*: Suits volatile instruments (commodities, crypto).

* *EMA Trend*: Useful in trending markets (stocks, indices).

* *RSI Confirm*: Adds momentum filter, better for swing trades.

* *Candle Confirm*: Ideal for scalpers needing visual confirmation.

* *Time Filter*: For intraday traders who want signals only in high-liquidity sessions.

Q: What timeframe should I use?

* Intraday traders → 5m to 15m (Time Filter, Candle Confirm).

* Swing traders → 1H to 4H (EMA Trend, RSI Confirm, ATR Stop).

* Position traders → Daily (Prev Day, Bollinger).

* Breakout

A trade entry condition triggered when price crosses above a resistance level (for longs) or below a support level (for shorts).

* Prev Day High/Low

Formula:

Prev High = High of (Day )

Prev Low = Low of (Day )

* Bollinger Bands

Formula:

Basis = SMA(Close, Length)

Upper Band = Basis + (Multiplier × StdDev(Close, Length))

Lower Band = Basis – (Multiplier × StdDev(Close, Length))

* Volume Confirmation

A breakout is only valid if:

Volume > SMA(Volume, Length)

* ATR (Average True Range)

Measures volatility.

Formula:

ATR = SMA(True Range, Length)

where True Range = max(High–Low, |High–Close |, |Low–Close |)

* EMA (Exponential Moving Average)

Weighted moving average giving more weight to recent prices.

Formula:

EMA = (Price × α) + (EMA × (1–α))

with α = 2 / (Length + 1)

* RSI (Relative Strength Index)

Momentum oscillator scaled 0–100.

Formula:

RSI = 100 – (100 / (1 + RS))

where RS = Avg(Gain, Length) ÷ Avg(Loss, Length)

* Candle Confirmation

Bullish candle: Close > Open AND Close > Close

Bearish candle: Close < Open AND Close < Close

Win Rate (%)

Formula:

Win Rate = (Winning Trades ÷ Total Trades) × 100

* Average Trade P&L

Formula:

Avg Trade = Net Profit ÷ Total Trades

📊 Performance Notes

The Universal Breakout Strategy is designed as a framework rather than a single-asset optimized system. Results will vary depending on the chart, timeframe, and asset chosen.

On the current defaults (15-minute, INR-denominated example), the backtest produced 132 trades over the selected period. This provides a statistically sufficient sample size.

Win rate (~35%) is relatively low, but this is balanced by a positive reward-to-risk ratio (~1.8). In practice, a lower win rate with larger wins versus smaller losses is sustainable.

The average P&L per trade is close to breakeven under default settings. This is expected, as the strategy is not tuned for a single symbol but offered as a universal breakout framework.

Commissions (0.1%) and slippage (1 tick) are included in the simulation, ensuring realistic conditions.

Risk management is conservative, with order sizing set at 1 unit per trade. This avoids over-leveraging and keeps exposure well under the 5-10% equity risk guideline.

👉 Traders are encouraged to:

Experiment with inputs such as ATR period, breakout length, or Bollinger parameters.

Test across different timeframes and instruments (equities, futures, forex, crypto) to find optimal setups.

Combine with filters (trend direction, volatility regimes, or volume conditions) for further refinement.

⚠️ Disclaimer This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Penguin Volatility State StrategyThe Penguin Volatility State Strategy is a comprehensive technical analysis framework designed to identify the underlying "state" or "regime" of the market. Instead of just providing simple buy or sell signals, its primary goal is to classify the market into one of four distinct states by combining trend, momentum, and volatility analysis.

The core idea is to trade only when these three elements align, focusing on periods of volatility expansion (a "squeeze breakout") that occur in the direction of a confirmed trend and are supported by strong momentum.

Key Components

The strategy is built upon two main engines

The Volatility Engine (Bollinger Bands vs. Keltner Channels)

This engine detects periods of rapidly increasing volatility. It measures the percentage difference (diff) between the upper bands of Bollinger Bands (which are based on standard deviation) and Keltner Channels (based on Average True Range). During a volatility "squeeze," both bands are close. When price breaks out, the Bollinger Band expands much faster than the Keltner Channel, causing the diff value to become positive. A positive diff signals a volatility breakout, which is the moment the strategy becomes active.

The Trend & Momentum Engine (Multi-EMA System)

This engine determines the market's direction and strength. It uses:

A Fast EMA (e.g., 12-period) and a Slow EMA (e.g., 26-period): The crossover of these two moving averages defines the primary, underlying trend (similar to a MACD).

An Ultra-Fast EMA (e.g., 2-period of ohlc4): This is used to measure the immediate, short-term momentum of the price.

The Four Market States

By combining the Trend and Momentum engines, the strategy categorizes the market into four visually distinct states, represented by the chart's background color. This is the most crucial aspect of the system.

💚 Green State: Strong Bullish

The primary trend is UP (Fast EMA > Slow EMA) AND the immediate momentum is STRONG (Price > Fast EMA).

Interpretation: This represents a healthy, robust uptrend where both the underlying trend and short-term price action are aligned. It is considered the safest condition for taking long positions.

❤️ Red State: Strong Bearish

Condition: The primary trend is DOWN (Fast EMA < Slow EMA) AND the immediate momentum is WEAK (Price < Fast EMA).

Interpretation: This represents a strong, confirmed downtrend. It is considered the safest condition for taking short positions.

💛 Yellow State: Weakening Bullish / Pullback

Condition: The primary trend is UP (Fast EMA > Slow EMA) BUT the immediate momentum is WEAK (Price < Fast EMA).

Interpretation: This is a critical warning signal for bulls. While the larger trend is still up, the short-term price action is showing weakness. This could be a minor pullback, a period of consolidation, or the very beginning of a trend reversal. Caution is advised.

💙 Blue State: Weakening Bearish / Relief Rally

Condition: The primary trend is DOWN (Fast EMA < Slow EMA) BUT the immediate momentum is STRONG (Price > Fast EMA).

Interpretation: This signals that a downtrend is losing steam. It often represents a short-covering rally (a "bear market rally") or the first potential sign of a market bottom. Bears should be cautious and consider taking profits.

How the Strategy Functions

The strategy uses these four states as its foundation for making trading decisions. The entry and exit arrows (Long, Short, Close) are generated based on a set of rules that can be customized by the user. For instance, a trader can configure the strategy to

Only take long trades during the Green State.

Require a confirmed volatility breakout (diff > 0) before entering a trade.

Use the "RSI on Diff" indicator to ensure that the breakout is supported by accelerating momentum.

Summary

In essence, the Penguin Volatility State Strategy provides a powerful "dashboard" for viewing the market. It moves beyond simple indicators to offer a contextual understanding of price action. By waiting for the alignment of Trend (the State), Volatility (the Breakout), and Momentum (the Acceleration), it helps traders to identify higher-probability setups and, just as importantly, to know when it is better to stay out of the market.

License / disclaimer

© waranyu.trkm — MIT License. Educational use only; not financial advice.

rsi indicator strategyRSIBB Strategy Based on Oversold, Overrbuy Bolinger Band Band. In usoil . Time Indicators is set and the timing is in 5 minutes

An example of Long. When the green marker appears, our entry point is High High If the price fails to reject our High High, our entry will change to the next candlestick. This process will continue until we enter the position.

A marker appears in purple when the green marker appears to us, in which information appears:

The first digit related to the strategist code

The second digit is that we have a few pips to be sure of the candlestick of our entry point

The third digit is our SL that is a coefficient of overall size of yogurt (HIGH - LOW)

Charmin is the digit of our tp that is a coefficient of overall size of yogurt (HIGH - LOW)

In 6 sets

استراتژی RSIBB بر اساس اشباع فروش، اشباع خرید، باند بولینگر. در این روش، اندیکاتورهای زمانی تنظیم شده و زمانبندی ۵ دقیقه است.

مثالی از موقعیت خرید. وقتی نشانگر سبز ظاهر میشود، نقطه ورود ما High است. اگر قیمت نتواند High ما را رد کند، ورود ما به کندل بعدی تغییر میکند. این فرآیند تا زمانی که وارد موقعیت شویم ادامه خواهد داشت.

وقتی نشانگر سبز برای ما ظاهر میشود، یک نشانگر به رنگ بنفش ظاهر میشود که در آن اطلاعات زیر ظاهر میشود:

رقم اول مربوط به کد استراتژیست است.

رقم دوم این است که ما چند پیپ برای اطمینان از کندل نقطه ورود خود داریم.

رقم سوم SL ما است که ضریبی از اندازه کلی ماست (HIGH - LOW) است.

چارمین رقم tp ما است که ضریبی از اندازه کلی ماست (HIGH - LOW) است.

逆勢布林+RSI策略 for SOL可以直接套用到 SOLUSDT, SOLPERP, 或其他 SOL 合約。

在策略回測介面中選擇 5min 或 15min 看策略表現。

若要調整停利%或 RSI 數值,改變 rsi < 25 與 (shortEntryPrice - close) / shortEntryPrice >= 0.035 即可。

This can be directly applied to SOLUSDT, SOLPERP, or other SOL futures.

In the strategy backtesting interface, select 5-minute or 15-minute periods to view strategy performance.

To adjust the take-profit percentage or RSI value, set RSI < 25 and (shortEntryPrice - close) / shortEntryPrice >= 0.035.

Bollinger Band Breakout With Volatility StoplossDetailed Explanation of the Bollinger Band Breakout With Volatility Stoploss System

Introduction

The "Bollinger Band Breakout With Volatility Stoploss" system is a trading strategy designed to exploit price volatility in financial markets using the Bollinger Bands indicator, a widely recognized tool developed by John Bollinger. This system adapts the traditional Bollinger Bands framework into a Volatility Breakout strategy, focusing on capturing significant price movements by leveraging customized parameters and precise trading rules. The system operates exclusively on long positions, employs a daily timeframe, and incorporates dynamic risk management techniques to optimize trade outcomes while preserving capital.

System Parameters

The system modifies the standard Bollinger Bands configuration to suit its breakout methodology:

Standard Deviation (SD): Set to 1x, determining the width of the bands relative to the central moving average. This tighter setting enhances sensitivity to price movements, making the system responsive to smaller volatility shifts compared to the conventional 2x SD.

Period: A 30-day (1-month) lookback period is used to calculate the bands, providing a balance between capturing medium-term price trends and avoiding excessive noise from shorter timeframes.

Moving Average Type: The system uses an Exponential Moving Average (EMA) instead of the Simple Moving Average (SMA). The EMA places greater weight on recent price data, making it more responsive to current market conditions and better suited for detecting breakout opportunities in dynamic markets.

Core Concept

The Bollinger Band Breakout system is built on the principle of Volatility Breakout, which seeks to capitalize on significant price movements when the price breaks out of a defined volatility range. The Bollinger Bands, consisting of an EMA as the central line and two bands (Upper and Lower) calculated as the EMA plus or minus 1x SD, define this range. The system operates on a Daily Chart (D) timeframe, making it suitable for traders who prefer analyzing and executing trades based on daily price action. By focusing solely on Long Positions (buying low and selling high), the system avoids short-selling, aligning with strategies that capitalize on upward price momentum.

The core idea is to use the 1x SD multiplier over a 30-day period to establish a dynamic price range that reflects recent market volatility. Breakouts above the Upper Band signal potential buying opportunities, while penetrations below the Lower Band indicate exits, ensuring trades are aligned with significant price movements.

Trading Signals

The system generates clear entry and exit signals based on price interactions with the Bollinger Bands:

Buy Signal: A buy signal is triggered when the closing price of a daily candle exceeds the Upper Bollinger Band (EMA + 1x SD over 30 days). The trade is entered at the opening price of the subsequent candle, ensuring the breakout is confirmed by the close of the prior day. This approach minimizes false signals by waiting for a definitive breach of the volatility threshold.

Sell Signal: A sell signal occurs when the closing price falls below the Lower Bollinger Band (EMA - 1x SD over 30 days). The position is exited at the opening price of the next candle, allowing the trader to lock in profits or limit losses when the price reverses or loses momentum.

Risk Management

Risk management is a cornerstone of the system, ensuring capital preservation and disciplined trade execution:

Initial Stoploss: The stoploss is set at the Lower Bollinger Band of the candle that triggered the buy signal. This level acts as a volatility-based threshold, below which the trade is deemed invalid, prompting an immediate exit to protect capital. Traders have two options for implementing the stoploss:

Pending Stoploss: A predefined stoploss order placed at the Lower Band level.

Conditional Exit: Using the sell signal condition (price closing below the Lower Band) as the exit trigger, effectively aligning the stoploss with the system’s exit rules.

Position Sizing: The system employs Fixed Fractional Position Sizing with a risk per trade capped at 3% of the account balance. The position size is calculated based on the distance between the entry price and the Initial Stoploss, incorporating Volatility Position Sizing. This method adjusts the trade size according to the market’s volatility, ensuring that risk remains consistent across varying market conditions. Two options are available for managing capital:

Gear Up Option: Profits from previous trades are reinvested into the account’s capital, increasing the base for calculating the next position size. This compounding approach can amplify returns but also increases risk exposure.

Fixed Equity Option: Profits from previous trades are withdrawn, and only the remaining capital is used for calculating the next position size. This conservative approach prioritizes capital preservation by not compounding gains.

Trailing Stop: The system uses the Lower Bollinger Band as a dynamic trailing stop, which adjusts with price movements and volatility. This ensures that profits are protected during favorable trends while allowing the trade to remain open as long as the price stays above the Lower Band. The trailing stop aligns with the sell signal condition, maintaining consistency in the system’s exit strategy.

Supporting Indicators

The system incorporates two additional indicators to enhance market analysis and decision-making:

Bollinger Band Width (BBW): BBW measures the distance between the Upper and Lower Bollinger Bands relative to the EMA, serving as a proxy for market volatility.

A high BBW indicates significant price volatility, often associated with strong trends or large price movements, which may confirm the strength of a breakout.

A low BBW suggests low volatility, potentially signaling a period of consolidation or "squeeze" that could precede a breakout. This can help traders anticipate potential trade setups.

The BBW calculation uses the EMA to maintain consistency with the system’s core parameters.

Bollinger Band Ratio (BBR) or %B: BBR measures the price’s position relative to the Bollinger Bands, providing insight into market conditions.

BBR > 1: The price is above the Upper Band, indicating potential overbought conditions or strong upward momentum, which aligns with the system’s buy signal.

BBR < 0: The price is below the Lower Band, suggesting oversold conditions or downward momentum, corresponding to the sell signal or stoploss trigger.

BBR between 0 and 1: The price is within the bands, indicating a neutral state where no immediate action is required.

Like BBW, BBR is calculated using the EMA for consistency.

Backtesting and Implementation

To evaluate the system’s performance, traders can utilize the Backtest Parameter function, which allows for testing the strategy across user-defined time periods. This feature enables traders to assess the system’s effectiveness under various market conditions, optimize parameters, and refine their approach based on historical data.

Conclusion

The Bollinger Band Breakout With Volatility Stoploss system is a robust, volatility-driven trading strategy that combines the predictive power of Bollinger Bands with disciplined risk management. By focusing on long positions, using a 1x SD multiplier, and incorporating EMA-based calculations, the system is designed to capture significant price breakouts while minimizing risk through dynamic stoplosses and volatility-adjusted position sizing. The inclusion of BBW and BBR indicators provides additional context for assessing market conditions, enhancing the trader’s ability to make informed decisions. With its structured approach and backtesting capabilities, this system is well-suited for traders seeking a systematic, data-driven method to trade in volatile markets.

MACD + RSI + EMA + BB + ATR Day Trading StrategyEntry Conditions and Signals

The strategy implements a multi-layered filtering approach to entry conditions, requiring alignment across technical indicators, timeframes, and market conditions .

Long Entry Requirements

Trend Filter: Fast EMA (9) must be above Slow EMA (21), price must be above Fast EMA, and higher timeframe must confirm uptrend

MACD Signal: MACD line crosses above signal line, indicating increasing bullish momentum

RSI Condition: RSI below 70 (not overbought) but above 40 (showing momentum)

Volume & Volatility: Current volume exceeds 1.2x 20-period average and ATR shows sufficient market movement

Time Filter: Trading occurs during optimal hours (9:30-11:30 AM ET) when market volatility is typically highest

Exit Strategies

The strategy employs multiple exit mechanisms to adapt to changing market conditions and protect profits :

Stop Loss Management

Initial Stop: Placed at 2.0x ATR from entry price, adapting to current market volatility

Trailing Stop: 1.5x ATR trailing stop that moves up (for longs) or down (for shorts) as price moves favorably

Time-Based Exits: All positions closed by end of trading day (4:00 PM ET) to avoid overnight risk

Best Practices for Implementation

Settings

Chart Setup: 5-minute timeframe for execution with 15-minute chart for trend confirmation

Session Times: Focus on 9:30-11:30 AM ET trading for highest volatility and opportunity

Breakout Core | by Solid#SignalsBreakout Core | by SolidSignals

General Overview

Breakout Core is an advanced breakout trading strategy designed for Bitcoin (BTC). Optimized for the unique market dynamics following the launch of BlackRock’s Spot ETFs in January 2024, it adapts to Bitcoin’s post-ETF volatility patterns. The strategy’s core strength lies in its low drawdown, achieved through a proprietary time-based signal-filtering algorithm that sets it apart from traditional breakout strategies. Breakout Core offers traders a reliable tool for navigating Bitcoin’s evolving market with reduced risk and enhanced precision.

Mechanisms

Breakout Core combines well-known indicators BB, EMAs, MAs with custom-tuned parameters to improve signal accuracy. Its unique feature is a proprietary time-filter algorithm that prioritizes high-probability breakout signals during specific high-volatility trading hours, derived from market analysis post-ETF launch. This algorithm minimizes false positives, particularly in volatile conditions, by integrating time-based volatility patterns with price action. The result is a robust strategy that optimizes entry and exit points for Bitcoin trading.

Objectives

Breakout Core aims to provide steady returns with controlled risk by targeting Bitcoin’s breakout patterns in the post-ETF market. Its low drawdown, achieved through extensive optimization and proprietary logic, makes it suitable for leverage trading (e.g., 3–5x leverage), balancing growth with capital protection. Tailored for BTC, the strategy equips traders with a precise tool to navigate Bitcoin’s transformed market dynamics.

Backtesting and Parameter Notes

Backtesting was performed using a $10,000 USDT account, risking up to 10% of equity per trade, including 0.06% commission fees and 2-tick slippage, aligned with standard exchange conditions. The strategy report details backtesting results from the launch of BlackRock’s Spot ETFs. These settings are the script’s defaults, ensuring transparency. Traders are encouraged to verify results using TradingView’s Deep Backtest feature to adapt to current market conditions.

Please note: Past performance does not guarantee future results.

Chart and Usage

The chart is clean and intuitive, displaying only Breakout Core’s buy and sell signals for easy interpretation. Parameters are pre-optimized for immediate use, with adjustable Take Profit (TP) and Stop Loss (SL) levels. Traders should validate custom settings via TradingView’s backtesting tools to ensure market compatibility. An integrated Alarm Panel supports API connectivity, providing clear Entry/Exit commands for Long and Short positions, enabling seamless automated trading workflows.

Originality Statement

Breakout Core is an original strategy developed by SolidSignals, leveraging standard indicators (Bollinger Bands, EMAs, MAs) combined with a proprietary time-filter algorithm. No third-party or open-source code is used, ensuring full compliance with TradingView’s originality requirements. The time-filter mechanism, based on post-ETF volatility analysis, distinguishes this strategy from conventional breakout approaches.

Important Disclaimer

Market conditions evolve continuously, and past performance is not indicative of future results. Traders are responsible for validating the strategy’s settings and performance under current market conditions before use.

External Signals Strategy Tester v5External Signals Strategy Tester v5 – User Guide (English)

1. Purpose

This Pine Script strategy is a universal back‑tester that lets you plug in any external buy/sell series (for example, another indicator, webhook feed, or higher‑time‑frame condition) and evaluate a rich set of money‑management rules around it – with a single click on/off workflow for every module.

2. Core Workflow

Feed signals

Buy Signal / Sell Signal inputs accept any series (price, boolean, output of request.security(), etc.).

A crossover above 0 is treated as “signal fired”.

Date filter

Start Date / End Date restricts the test window so you can exclude unwanted history.

Trade engine

Optional Long / Short enable toggles.

Choose whether opposite signals simply close the trade or reverse it (flip direction in one transaction).

Risk modules – all opt‑in via check‑boxes

Classic % block – fixed % Take‑Profit / Stop‑Loss / Break‑Even.

Fibonacci Bollinger Bands (FBB) module

Draws dynamic VWMA/HMA/SMA/EMA/DEMA/TEMA mid‑line with ATR‑scaled Fibonacci envelopes.

Every line can be used for stops, trailing, or multi‑target exits.

Separate LONG and SHORT sub‑modules

Each has its own SL plus three Take‑Profits (TP1‑TP3).

Per TP you set line, position‑percentage to close, and an optional trailing flag.

Executed TP/SLs deactivate themselves so they cannot refire.

Trailing behaviour

If Trail is checked, the selected line is re‑evaluated once per bar; the order is amended via strategy.exit().

3. Inputs Overview

Group Parameter Notes

Trade Settings Enable Long / Enable Short Master switches

Close on Opposite / Reverse Position How to react to a counter‑signal

Risk % Use TP / SL / BE + their % Traditional fixed‑distance management

Fibo Bands FIBO LEVELS ENABLE + visual style/length Turn indicator overlay on/off

FBB LONG SL / TP1‑TP3 Enable, Line, %, Trail Rules applied only while a long is open

FBB SHORT SL / TP1‑TP3 Enable, Line, %, Trail Rules applied only while a short is open

Line choices: Basis, 0.236, 0.382, 0.5, 0.618, 0.764, 1.0 – long rules use lower bands, short rules use upper bands automatically.

4. Algorithm Details

Position open

On the very first bar after entry, the script checks the direction and activates the corresponding LONG or SHORT module, deactivating the other.

Order management loop (every bar)

FBB Stop‑Loss: placed/updated at chosen band; if trailing, follows the new value.

TP1‑TP3: each active target updates its limit price to the selected band (or holds static if trailing is off).

The classic % block runs in parallel; its exits have priority because they call strategy.close_all().

Exit handling

When any strategy.exit() fires, the script reads exit_id and flips the *_Active flag so that order will not be recreated.

A Stop‑Loss (SL) also disables all remaining TPs for that leg.

5. Typical Use Cases

Scenario Suggested Setup

Scalping longs into VWAP‐reversion Enable LONG TP1 @ 0.382 (30 %), TP2 @ 0.618 (40 %), SL @ 0.236 + trailing

Fade shorts during news spikes Enable SHORT SL @ 1.0 (no trail) and SHORT TP1,2,3 on consecutive lowers with small size‑outs

Classic trend‑follow Use only classic % TP/SL block and disable FBB modules

6. Hints & Tips

Signal quality matters – this script manages exits, it does not generate entries.

Keep TV time zone in mind when picking start/end dates.

For portfolio‑style testing allocate smaller default_qty_value than 100 % or use strategy.percent_of_equity sizing.

You can combine FBB exits with fixed‑% ones for layered management.

7. Limitations / Safety

No pyramiding; the script holds max one position at a time.

All calculations are bar‑close; intra‑bar touches may differ from real‑time execution.

The indicator overlay is optional, so you can run visual‑clean tests by unchecking FIBO LEVELS ENABLE.

Dskyz (DAFE) Adaptive Regime - Quant Machine ProDskyz (DAFE) Adaptive Regime - Quant Machine Pro:

Buckle up for the Dskyz (DAFE) Adaptive Regime - Quant Machine Pro, is a strategy that’s your ultimate edge for conquering futures markets like ES, MES, NQ, and MNQ. This isn’t just another script—it’s a quant-grade powerhouse, crafted with precision to adapt to market regimes, deliver multi-factor signals, and protect your capital with futures-tuned risk management. With its shimmering DAFE visuals, dual dashboards, and glowing watermark, it turns your charts into a cyberpunk command center, making trading as thrilling as it is profitable.

Unlike generic scripts clogging up the space, the Adaptive Regime is a DAFE original, built from the ground up to tackle the chaos of futures trading. It identifies market regimes (Trending, Range, Volatile, Quiet) using ADX, Bollinger Bands, and HTF indicators, then fires trades based on a weighted scoring system that blends candlestick patterns, RSI, MACD, and more. Add in dynamic stops, trailing exits, and a 5% drawdown circuit breaker, and you’ve got a system that’s as safe as it is aggressive. Whether you’re a newbie or a prop desk pro, this strat’s your ticket to outsmarting the markets. Let’s break down every detail and see why it’s a must-have.

Why Traders Need This Strategy

Futures markets are a gauntlet—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional traps that punish the unprepared. Meanwhile, platforms are flooded with low-effort scripts that recycle old ideas with zero innovation. The Adaptive Regime stands tall, offering:

Adaptive Intelligence: Detects market regimes (Trending, Range, Volatile, Quiet) to optimize signals, unlike one-size-fits-all scripts.

Multi-Factor Precision: Combines candlestick patterns, MA trends, RSI, MACD, volume, and HTF confirmation for high-probability trades.

Futures-Optimized Risk: Calculates position sizes based on $ risk (default: $300), with ATR or fixed stops/TPs tailored for ES/MES.

Bulletproof Safety: 5% daily drawdown circuit breaker and trailing stops keep your account intact, even in chaos.

DAFE Visual Mastery: Pulsing Bollinger Band fills, dynamic SL/TP lines, and dual dashboards (metrics + position) make signals crystal-clear and charts a work of art.

Original Craftsmanship: A DAFE creation, built with community passion, not a rehashed clone of generic code.

Traders need this because it’s a complete, adaptive system that blends quant smarts, user-friendly design, and DAFE flair. It’s your edge to trade with confidence, cut through market noise, and leave the copycats in the dust.

Strategy Components

1. Market Regime Detection

The strategy’s brain is its ability to classify market conditions into five regimes, ensuring signals match the environment.

How It Works:

Trending (Regime 1): ADX > 20, fast/slow EMA spread > 0.3x ATR, HTF RSI > 50 or MACD bullish (htf_trend_bull/bear).

Range (Regime 2): ADX < 25, price range < 3% of close, no HTF trend.

Volatile (Regime 3): BB width > 1.5x avg, ATR > 1.2x avg, HTF RSI overbought/oversold.

Quiet (Regime 4): BB width < 0.8x avg, ATR < 0.9x avg.

Other (Regime 5): Default for unclear conditions.

Indicators: ADX (14), BB width (20), ATR (14, 50-bar SMA), HTF RSI (14, daily default), HTF MACD (12,26,9).

Why It’s Brilliant:

Regime detection adapts signals to market context, boosting win rates in trending or volatile conditions.

HTF RSI/MACD add a big-picture filter, rare in basic scripts.

Visualized via gradient background (green for Trending, orange for Range, red for Volatile, gray for Quiet, navy for Other).

2. Multi-Factor Signal Scoring

Entries are driven by a weighted scoring system that combines candlestick patterns, trend, momentum, and volume for robust signals.

Candlestick Patterns:

Bullish: Engulfing (0.5), hammer (0.4 in Range, 0.2 else), morning star (0.2), piercing (0.2), double bottom (0.3 in Volatile, 0.15 else). Must be near support (low ≤ 1.01x 20-bar low) with volume spike (>1.5x 20-bar avg).

Bearish: Engulfing (0.5), shooting star (0.4 in Range, 0.2 else), evening star (0.2), dark cloud (0.2), double top (0.3 in Volatile, 0.15 else). Must be near resistance (high ≥ 0.99x 20-bar high) with volume spike.

Logic: Patterns are weighted higher in specific regimes (e.g., hammer in Range, double bottom in Volatile).

Additional Factors:

Trend: Fast EMA (20) > slow EMA (50) + 0.5x ATR (trend_bull, +0.2); opposite for trend_bear.

RSI: RSI (14) < 30 (rsi_bull, +0.15); > 70 (rsi_bear, +0.15).

MACD: MACD line > signal (12,26,9, macd_bull, +0.15); opposite for macd_bear.

Volume: ATR > 1.2x 50-bar avg (vol_expansion, +0.1).

HTF Confirmation: HTF RSI < 70 and MACD bullish (htf_bull_confirm, +0.2); RSI > 30 and MACD bearish (htf_bear_confirm, +0.2).

Scoring:

bull_score = sum of bullish factors; bear_score = sum of bearish. Entry requires score ≥ 1.0.

Example: Bullish engulfing (0.5) + trend_bull (0.2) + rsi_bull (0.15) + htf_bull_confirm (0.2) = 1.05, triggers long.

Why It’s Brilliant:

Multi-factor scoring ensures signals are confirmed by multiple market dynamics, reducing false positives.

Regime-specific weights make patterns more relevant (e.g., hammers shine in Range markets).

HTF confirmation aligns with the big picture, a quant edge over simplistic scripts.

3. Futures-Tuned Risk Management

The risk system is built for futures, calculating position sizes based on $ risk and offering flexible stops/TPs.

Position Sizing:

Logic: Risk per trade (default: $300) ÷ (stop distance in points * point value) = contracts, capped at max_contracts (default: 5). Point value = tick value (e.g., $12.5 for ES) * ticks per point (4) * contract multiplier (1 for ES, 0.1 for MES).

Example: $300 risk, 8-point stop, ES ($50/point) → 0.75 contracts, rounded to 1.

Impact: Precise sizing prevents over-leverage, critical for micro contracts like MES.

Stops and Take-Profits:

Fixed: Default stop = 8 points, TP = 16 points (2:1 reward/risk).

ATR-Based: Stop = 1.5x ATR (default), TP = 3x ATR, enabled via use_atr_for_stops.

Logic: Stops set at swing low/high ± stop distance; TPs at 2x stop distance from entry.

Impact: ATR stops adapt to volatility, while fixed stops suit stable markets.

Trailing Stops:

Logic: Activates at 50% of TP distance. Trails at close ± 1.5x ATR (atr_multiplier). Longs: max(trail_stop_long, close - ATR * 1.5); shorts: min(trail_stop_short, close + ATR * 1.5).

Impact: Locks in profits during trends, a game-changer in volatile sessions.

Circuit Breaker:

Logic: Pauses trading if daily drawdown > 5% (daily_drawdown = (max_equity - equity) / max_equity).

Impact: Protects capital during black swan events (e.g., April 27, 2025 ES slippage).

Why It’s Brilliant:

Futures-specific inputs (tick value, multiplier) make it plug-and-play for ES/MES.

Trailing stops and circuit breaker add pro-level safety, rare in off-the-shelf scripts.

Flexible stops (ATR or fixed) suit different trading styles.

4. Trade Entry and Exit Logic

Entries and exits are precise, driven by bull_score/bear_score and protected by drawdown checks.

Entry Conditions:

Long: bull_score ≥ 1.0, no position (position_size <= 0), drawdown < 5% (not pause_trading). Calculates contracts, sets stop at swing low - stop points, TP at 2x stop distance.

Short: bear_score ≥ 1.0, position_size >= 0, drawdown < 5%. Stop at swing high + stop points, TP at 2x stop distance.

Logic: Tracks entry_regime for PNL arrays. Closes opposite positions before entering.

Exit Conditions:

Stop-Loss/Take-Profit: Hits stop or TP (strategy.exit).

Trailing Stop: Activates at 50% TP, trails by ATR * 1.5.

Emergency Exit: Closes if price breaches stop (close < long_stop_price or close > short_stop_price).

Reset: Clears stop/TP prices when flat (position_size = 0).

Why It’s Brilliant:

Score-based entries ensure multi-factor confirmation, filtering out weak signals.

Trailing stops maximize profits in trends, unlike static exits in basic scripts.

Emergency exits add an extra safety layer, critical for futures volatility.

5. DAFE Visuals

The visuals are pure DAFE magic, blending function with cyberpunk flair to make signals intuitive and charts stunning.

Shimmering Bollinger Band Fill:

Display: BB basis (20, white), upper/lower (green/red, 45% transparent). Fill pulses (30–50 alpha) by regime, with glow (60–95 alpha) near bands (close ≥ 0.995x upper or ≤ 1.005x lower).

Purpose: Highlights volatility and key levels with a futuristic glow.

Visuals make complex regimes and signals instantly clear, even for newbies.

Pulsing effects and regime-specific colors add a DAFE signature, setting it apart from generic scripts.

BB glow emphasizes tradeable levels, enhancing decision-making.

Chart Background (Regime Heatmap):

Green — Trending Market: Strong, sustained price movement in one direction. The market is in a trend phase—momentum follows through.

Orange — Range-Bound: Market is consolidating or moving sideways, with no clear up/down trend. Great for mean reversion setups.

Red — Volatile Regime: High volatility, heightened risk, and larger/faster price swings—trade with caution.

Gray — Quiet/Low Volatility: Market is calm and inactive, with small moves—often poor conditions for most strategies.

Navy — Other/Neutral: Regime is uncertain or mixed; signals may be less reliable.

Bollinger Bands Glow (Dynamic Fill):

Neon Red Glow — Warning!: Price is near or breaking above the upper band; momentum is overstretched, watch for overbought conditions or reversals.

Bright Green Glow — Opportunity!: Price is near or breaking below the lower band; market could be oversold, prime for bounce or reversal.

Trend Green Fill — Trending Regime: Fills between bands with green when the market is trending, showing clear momentum.

Gold/Yellow Fill — Range Regime: Fills with gold/aqua in range conditions, showing the market is sideways/oscillating.

Magenta/Red Fill — Volatility Spike: Fills with vivid magenta/red during highly volatile regimes.

Blue Fill — Neutral/Quiet: A soft blue glow for other or uncertain market states.

Moving Averages:

Display: Blue fast EMA (20), red slow EMA (50), 2px.

Purpose: Shows trend direction, with trend_dir requiring ATR-scaled spread.

Dynamic SL/TP Lines:

Display: Pulsing colors (red SL, green TP for Trending; yellow/orange for Range, etc.), 3px, with pulse_alpha for shimmer.

Purpose: Tracks stops/TPs in real-time, color-coded by regime.

6. Dual Dashboards

Two dashboards deliver real-time insights, making the strat a quant command center.

Bottom-Left Metrics Dashboard (2x13):

Metrics: Mode (Active/Paused), trend (Bullish/Bearish/Neutral), ATR, ATR avg, volume spike (YES/NO), RSI (value + Oversold/Overbought/Neutral), HTF RSI, HTF trend, last signal (Buy/Sell/None), regime, bull score.

Display: Black (29% transparent), purple title, color-coded (green for bullish, red for bearish).

Purpose: Consolidates market context and signal strength.

Top-Right Position Dashboard (2x7):

Metrics: Regime, position side (Long/Short/None), position PNL ($), SL, TP, daily PNL ($).

Display: Black (29% transparent), purple title, color-coded (lime for Long, red for Short).

Purpose: Tracks live trades and profitability.

Why It’s Brilliant:

Dual dashboards cover market context and trade status, a rare feature.

Color-coding and concise metrics guide beginners (e.g., green “Buy” = go).

Real-time PNL and SL/TP visibility empower disciplined trading.

7. Performance Tracking

Logic: Arrays (regime_pnl_long/short, regime_win/loss_long/short) track PNL and win/loss by regime (1–5). Updated on trade close (barstate.isconfirmed).

Purpose: Prepares for future adaptive thresholds (e.g., adjust bull_score min based on regime performance).

Why It’s Brilliant: Lays the groundwork for self-optimizing logic, a quant edge over static scripts.

Key Features

Regime-Adaptive: Optimizes signals for Trending, Range, Volatile, Quiet markets.

Futures-Optimized: Precise sizing for ES/MES with tick-based risk inputs.

Multi-Factor Signals: Candlestick patterns, RSI, MACD, and HTF confirmation for robust entries.

Dynamic Exits: ATR/fixed stops, 2:1 TPs, and trailing stops maximize profits.

Safe and Smart: 5% drawdown breaker and emergency exits protect capital.

DAFE Visuals: Shimmering BB fill, pulsing SL/TP, and dual dashboards.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

How to Use

Add to Chart: Load on a 5min ES/MES chart in TradingView.

Configure Inputs: Set instrument (ES/MES), tick value ($12.5/$1.25), multiplier (1/0.1), risk ($300 default). Enable ATR stops for volatility.

Monitor Dashboards: Bottom-left for regime/signals, top-right for position/PNL.

Backtest: Run in strategy tester to compare regimes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see regime shifts and stops.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance does not guarantee future results. Backtest results may differ from live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Slippage: 3

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Adaptive Regime - Quant Machine Pro is more than a strategy—it’s a revolution. Crafted with DAFE’s signature precision, it rises above generic scripts with adaptive regimes, quant-grade signals, and visuals that make trading a thrill. Whether you’re scalping MES or swinging ES, this system empowers you to navigate markets with confidence and style. Join the DAFE crew, light up your charts, and let’s dominate the futures game!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Daily Bollinger Band StrategyOverview of the Daily Bollinger Band Strategy

1. Strategy Overview and Features

This strategy is a tool for backtesting a trading method that uses Bollinger Bands. It is *not* a tool for automated trading.

1-1. Main Display Items

The main chart displays the Bollinger Bands and the 200-day moving average.

It also shows the entry and exit points along with the position size (in units of 100 shares).

1-2. Summary of Trading Rules

For long (buy) strategies, the trade enters when the price crosses above the +1σ line of the Bollinger Bands, aiming to ride an upward trend. The position is exited when the price crosses below the middle band.

For short (sell) strategies, the trade enters when the price crosses below the -1σ line of the Bollinger Bands, aiming to ride a downward trend. The position is exited when the price crosses above the middle band.

1-3. Strategic Enhancements

The strategy uses the slope of the 200-day moving average to determine the trend direction and enter trades accordingly. This improves the win rate and payoff ratio.

Additionally, to reduce the probability of ruin, the risk per trade is limited to 1.0% of capital, and position sizing is adjusted using ATR (a volatility indicator).

2. Trading Rules

2-1. Chart Type

Only daily charts are used.

2-2. Indicators Used

(1) Bollinger Bands** (used for entry and exit signals)

- Period: Fixed at 80 days

- Upper and lower bands: Fixed at ±1σ

(2) Moving Average** (used to determine trend direction)

- Period: Fixed at 200 days

- Trend direction is judged based on whether the difference from the previous day is positive (upward) or negative (downward)

2-3. Buy Rules

Setup:

- Price crosses above the +1σ line from below

- Both the middle band and 200-day moving average are upward sloping

Entry:

- Buy at the next day’s market open using a market order

Exit:

- If the price crosses below the middle band, sell at the next day’s open using a market order

2-4. Sell Rules

Setup:

- Price crosses below the -1σ line from above

- Both the middle band and 200-day moving average are downward sloping

Entry:

- Sell at the next day’s market open using a market order

Exit:

- If the price crosses above the middle band, buy back at the next day’s open using a market order

2-5. Risk Management Rules

- Risk per trade: 1.0% of total capital (acceptable loss = capital × 1.0%)

- Position size: Acceptable loss ÷ 2ATR (rounded down to the nearest unit of 100 shares)

2-6. Other Notes

- No brokerage fees

- No pyramiding

- No partial exits

- No reverse positions (no “stop-and-reverse” trades)

3. Strategy Parameters

The following settings can be specified:

3-1. Period Settings

- Start date: Set the start date for the backtest period

- Stop date: Set the end date for the backtest period

3-2. Display of Trend and Signals

- Show trend: When checked, the background color of the bars is light red for an uptrend and light blue for a downtrend

- Show signal: When checked, entry and exit signals are displayed (note: signals are executed at the next day’s open, so there is a one-day lag in the display)

3-3. Capital Management Settings

- Funds: Capital available for trading (in JPY)

- Risk rate: Specify what percentage of the capital to risk per trade

Settings in the “Properties” tab are not used in this strategy.

4. Backtest Results (Example)

Here are the backtest results conducted by the author:

- Target Stocks: All components of the Nikkei 225

- Test Period: January 4, 2000 – December 30, 2024

- Data Points: 12,886

- Win Rate: 33.45%

- Net Profit: ¥82,132,380

- Payoff Ratio: 2.450

- Expected Value: ¥6,373.8

- Risk Rate: 1.0%

- Probability of Ruin: 0.00%

---

デイリー・ボリンジャーバンド・ストラテジーの概要

1. ストラテジーの概要と特徴

このストラテジーは、ボリンジャーバンドを使ったトレード手法のバックテストを行うツールです。自動売買を行うツールではありません。

1-1. 主な表示項目

メインチャートにボリンジャーバンドと 200日移動平均線を表示します。

また、エントリーと手仕舞いのタイミングと数量(100株単位)も表示されます。

1-2. トレードルールの概要

買い戦略の場合、ボリンジャーバンドの +1σ 超えでエントリーして上昇トレンドに乗り、ミドルバンドを割ったら決済します。

売り戦略の場合、ボリンジャーバンドの -1σ 割りでエントリーして下降トレンドに乗り、ミドルバンドを上抜けたら決済します。

1-3. ストラテジーの工夫点

200日移動平均線の傾きを見てトレンド方向にエントリーをしています。こうして勝率とペイオフレシオの成績を向上しています。

また、破産確率を抑えるために、リスク資金比率を 1.0% にして、ATR(ボラティリティ指標) を使って注文数を調整しています。

2. 売買ルール

2-1. 使用するチャート

日足チャートに限定します

2-2. 使用する指標

(1) ボリンジャーバンド(仕掛けと手仕舞いのシグナルに使用)

期間は80日に固定

上下バンドは ±1σ に固定

(2) 移動平均線(トレンドの方向を見るために使用)

期間は200日に固定

移動平均の値の前日との差がプラスのとき上向き、マイナスのとき下向きと判断

2-3. 買いのルール

セットアップ:ボリンジャーバンドの +1σ を価格が下から上に交差 かつ ミドルバンドと 200日移動平均線が上向き

仕掛け:翌日の寄り付きに成行で買う

手仕舞い:ボリンジャーバンドのミドルバンドを価格が上から下に交差したら、翌日の寄り付きに成行で売る

2-4. 売りのルール

セットアップ:ボリンジャーバンドの -1σ を価格が上から下に交差 かつ ミドルバンドと 200日移動平均線が下向き

仕掛け:翌日の寄り付きに成行で売る

手仕舞い:ボリンジャーバンドのミドルバンドを価格が下から上に交差したら、翌日の寄り付きに成行で買い戻す

2-5. 資金管理のルール

リスク資金比率:資産の 1.0%(許容損失 = 資産 × 1.0%)

注文数:許容損失 ÷ 2ATR(単元株数未満は切り捨て)

2-6. その他

仲介手数料:なし

ピラミッディング:なし

分割決済:なし

ドテン:しない

3. ストラテジーのパラメーター

次の項目が指定できます。

3-1. 期間の設定

Staer date : バックテストの検証期間の開始日を指定します

Stop date : バックテストの検証期間の終了日を指定します

3-2. トレンドとシグナルの表示