Premarket Breakout (TP1 → BE → ATR Trail)this is the best ever you will really like i t and it does a lot its a really good scirpt please use it to make trades

Các mẫu biểu đồ

Premarket Breakout (TP1 → BE → ATR Trail)the best one you can find a very good indicator and strategy to help with al l trading needs in every way

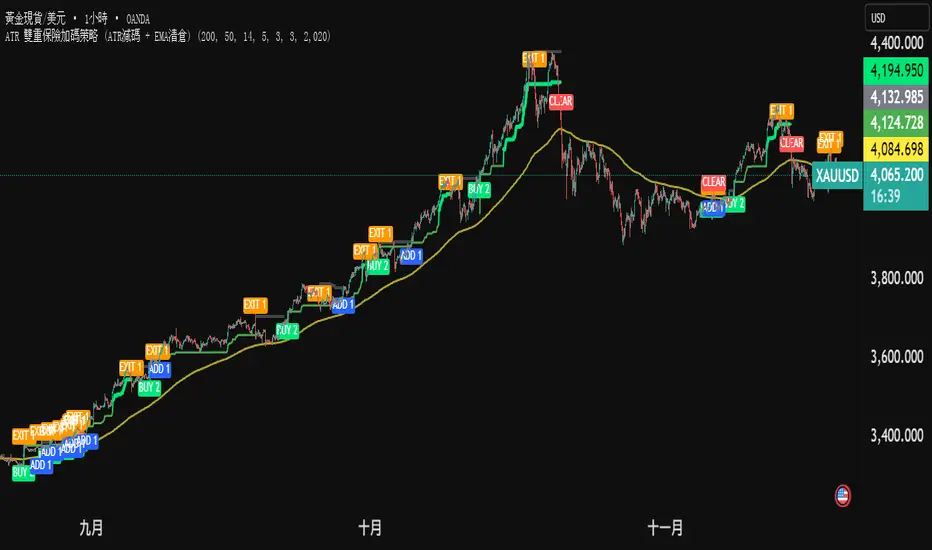

ATR 雙重保險加碼策略 (ATR減碼 + EMA清倉) (三寶爸黃金版)黃金雙保險戰法 (兩口單策略)

核心概念: 進場買兩口。一口賺了就跑(保本),一口死抱到底(拚大賺)。

1. 進場 (買 2 口):

只要價格站上黃線,而且突破前高。

別猶豫,直接買 2 口。

2. 減碼 (賣 1 口):

價格回檔碰到綠線。

代表短線轉弱,先賣掉 1 口。

好處: 錢先放口袋,心裡踏實。

3. 加碼 (買回 1 口):

如果你手上只剩 1 口,結果行情沒死,又創新高。

代表剛才賣錯了,趕快買回 1 口 (補回滿倉)。

好處: 繼續跟著趨勢賺錢。

4. 清倉 (全跑):

價格跌破黃線。

代表趨勢真的結束了,不管剩幾口,全部賣掉。

一句話總結: 「震盪時先賣一半保命,趨勢噴出時永遠滿倉在車上。」

Gold Dual-Insurance Tactic (2-Lot System)

Core Concept: Enter with 2 lots. Sell one early to lock in profits (Play Safe), and hold the other to catch the big wave (Go Big).

1. Entry (Buy 2 Lots):

When price is above the Yellow Line AND breaks the previous High.

Don't hesitate. Buy 2 lots immediately.

2. Scale Out (Sell 1 Lot):

When price pulls back and hits the Green Line.

This means short-term weakness. Sell 1 lot.

Benefit: Put money in your pocket. Peace of mind.

3. Add Position (Buy Back 1 Lot):

If you have only 1 lot left, but the market hits a New High.

It means the trend is alive. Quickly Buy back 1 lot (refill to full position).

Benefit: Continue maximizing profits with the trend.

4. Clear All (Exit Everything):

When price falls below the Yellow Line.

The trend is officially over. Sell everything, no matter what.

CyberG TestTesting the ability to test scripts. I have been working on multiple scripts I want to show my stats for, for possible interests in my scripts

MACD + KD Crossover Strategy (20% TP/10% SL )MACD + KD Crossover Strategy is my first try in tradingview, so it have a lot of space to improve, every can give me suggestion.

ILM & IFVG StrategyPlease feel free to adjust in any way possible. Let me know if you can create something better from this initial coding.

//═══════════════════════════════════════════════════════════════════════

// Inverted Liquidity Model (ILM) – Strategy

//═══════════════════════════════════════════════════════════════════════

//

// The **Inverted Liquidity Model (ILM)** is a liquidity-based algorithm

// built to capture high-probability reversals after:

//

// • A liquidity sweep (SSL/BSL taken)

// • Rejection back inside the range

// • A Fair Value Gap (FVG) forms

// • That FVG becomes invalidated → becomes an IFVG entry zone

//

// ILM combines:

// • LTF BOS / CHOCH structure confirmation

// • HTF structure (expansion) filtering

// • Premium / Discount filter (17:00 CST session midline)

// • Optional ATR volatility filter

// • Optional trading session restrictions

// • Optional partial profit-taking + runners

//

// When all conditions align, the strategy enters:

// ✔ Long after sweep of SSL + valid long IFVG + trend confirmation

// ✔ Short after sweep of BSL + valid short IFVG + trend confirmation

//

// Stops are placed at the sweep wick.

// Full target is set at the next structural high/low.

// Optional partial TP sends a runner to full target.

//

// Visual tools (labels, sweep lines, IFVG boxes, midline) assist

// with review and forward testing.

//

//───────────────────────────────────────────────────────────────────────

// USER CONFIGURABLE FEATURES

//───────────────────────────────────────────────────────────────────────

//

// • **Liquidity & Structure**

// - pivotLen → swing length for pivots / liquidity

// - htfOn → toggle higher-timeframe pivots

// - htfTF → timeframe for HTF structure/liquidity

// - useStructureFilter → enforce LTF BOS/CHOCH trend

// - useHtfExpansionFilter → enforce HTF trend

// - showStructureLabels → show BOS/CHOCH labels

// - showHtfStructureLabels → show HTF BOS/CHOCH labels

//

// • **Premium / Discount Midline**

// - usePremiumDiscountFilter → only long in discount / short in premium

// - pdSession → session used for midline (default 17:00 CST)

// - showPdMidLine → show 50% midline

//

// • **FVG / IFVG Detection**

// - useBodyGapFVG → FVG uses candle bodies instead of wicks

// - useDisplacementFVG → require displacement bar

// - dispAtrMult → minimum ATR threshold for displacement

// - showIFVG → draw IFVG boxes

//

// • **ATR / Volatility / Sessions**

// - useRangeFilter → require minimum ATR%

// - atrLen → ATR period

// - minAtrPerc → minimum ATR% of price

// - useSessionFilter → restrict trading hours

// - sessionTimes → allowed trading session

//

// • **Sweep Visualization**

// - showSweepLines → draw sweep lines at SSL/BSL sweeps

// - sweepLineWidth → thickness of sweep lines

//

// • **Exits: Partial Targets & Runners**

// - usePartialTargets → enable partial TP logic

// - tp1QtyPercent → percent closed at TP1

// - tp1FractionOfPath → TP1 relative to path to full target

//

// • **Formatting / Visibility**

// - labelFontSizeInput → tiny / small / normal / large / huge

// - showEntries → entry markers

// - showTargets → target lines

//

//═══════════════════════════════════════════════════════════════════════

// END OF STRATEGY DESCRIPTION

//═══════════════════════════════════════════════════════════════════════

Crude Oil Time + Fix Catalyst StrategyHybrid Workflow: Event-Driven Macro + Market DNA Micro

1. Macro Catalyst Layer (Your Overlays)

Event Mapping: Fed decisions, LBMA fixes, EIA releases, OPEC+ meetings.

Regime Filters: Risk-on/off, volatility regimes, macro bias (hawkish/dovish).

Volatility Scaling: ATR-based position sizing, adaptive overlays for London/NY sessions.

Governance: Max trades/day, cool-down logic, session boundaries.

👉 This layer answers when and why to engage.

2. Micro Execution Layer (Market DNA)

Order Flow Confirmation: Tape reading (Level II, time & sales, bid/ask).

Liquidity Zones: Identify support/resistance pools where buyers/sellers cluster.

Imbalance Detection: Aggressive buyers/sellers overwhelming the other side.

Precision Entry: Only trigger trades when order flow confirms macro catalyst bias.

Risk Discipline: Tight stops beyond liquidity zones, conviction-based scaling.

👉 This layer answers how and where to engage.

3. Unified Playbook

Step Macro Overlay (Your Edge) Market DNA (Jay’s Edge) Result

Event Trigger Fed/LBMA/OPEC+ catalyst flagged — Volatility window opens

Bias Filter Hawkish/dovish regime filter — Directional bias set

Sizing ATR volatility scaling — Position size calibrated

Execution — Tape confirms liquidity imbalance Precision entry

Risk Control Governance rules (cool-down, max trades) Tight stops beyond liquidity zones Disciplined exits

4. Gold & Silver Use Case

Gold (Fed Day):

Overlay flags volatility window → bias hawkish.

Market DNA shows sellers hitting bids at resistance.

Enter short with volatility-scaled size, stop just above liquidity zone.

Silver (LBMA Fix):

Overlay highlights fix window → bias neutral.

Market DNA shows buyers stepping in at support.

Enter long with adaptive size, HUD displays risk metrics.

5. HUD Integration

Macro Dashboard: Catalyst timeline, regime filter status, volatility bands.

Micro Dashboard: Live tape imbalance meter, liquidity zone map, conviction score.

Unified View: Macro tells you when to look, micro tells you when to pull the trigger.

⚡ This hybrid workflow gives you macro awareness + micro precision. Your overlays act as the radar, Jay’s Market DNA acts as the laser scope. Together, they create a disciplined, event-aware, volatility-scaled playbook for gold and silver.

Antonio — do you want me to draft this into a compile-safe Pine Script v6 template that embeds the macro overlay logic, while leaving hooks for Market DNA-style execution (order flow confirmation)? That way you’d have a production-ready skeleton to extend across TradingView, TradeStation, and NinjaTrader.

Antonio — do you want me to draft this into a compile-safe Pine Script v6 template that embeds the macro overlay logic, while leaving hooks for Market DNA-style execution (order flow confirmation)? That way you’d have a production-ready skeleton to extend across TradingView, TradeStation, and NinjaTrader.

Liquidity Sweep + BOS Retest System — Prop Firm Edition🟦 Liquidity Sweep + BOS Retest System — Prop Firm Edition

A High-Probability Smart Money Strategy Built for NQ, ES, and Funding Accounts

🚀 Overview

The Liquidity Sweep + BOS Retest System (Prop Firm Edition) is a precision-engineered SMC strategy built specifically for prop firm traders. It mirrors institutional liquidity behavior and combines it with strict account-safe entry rules to help traders pass and maintain funding accounts with consistency.

Unlike typical indicators, this system waits for three confirmations — liquidity sweep, displacement, and a clean retest — before executing any trade. Every component is optimized for low drawdown, high R:R, and prop-firm-approved risk management.

Whether you’re trading Apex, TakeProfitTrader, FFF, or OneUp Trader, this system gives you a powerful mechanical framework that keeps you within rules while identifying the market’s highest-probability reversal zones.

🔥 Key Features

1. Liquidity Sweep Detection (Stop Hunt Logic)

Automatically identifies when price clears a previous swing high/low with a sweep confirmation candle.

✔ Filters noise

✔ Eliminates early entries

✔ Locks onto true liquidity grabs

2. Automatic Break of Structure (BOS) Confirmation

Price must show true displacement by breaking structure opposite the sweep direction.

✔ Confirms momentum shift

✔ Removes fake reversals

✔ Ensures institutional intent

3. Precision Retest Entry Model

The strategy enters only when price retests the BOS level at premium/discount pricing.

✔ Zero chasing

✔ Extremely tight stop loss placement

✔ Prop-firm-friendly controlled risk

4. Built-In Risk & Trade Management

SL set at swept liquidity

TP set by user-defined R:R multiplier

Optional session filter (NY Open by default)

One trade at a time (no pyramiding)

Automatically resets logic after each trade

This prevents overtrading — the #1 cause of evaluation and account breaches.

5. Designed for Prop Firm Futures Trading

This script is optimized for:

Trailing/static drawdown accounts

Micro contract precision

Funding evaluations

Low-risk, high-probability setups

Structured, rule-based execution

It reduces randomness and emotional trading by automating the highest-quality SMC sequence.

🎯 The Trading Model Behind the System

Step 1 — Liquidity Sweep

Price must take out a recent high/low and close back inside structure.

This confirms stop-hunting behavior and marks the beginning of a potential reversal.

Step 2 — BOS (Break of Structure)

Price must break the opposite side swing with a displacement candle. This validates a directional shift.

Step 3 — Retest Entry

The system waits for price to retrace into the BOS level and signal continuation.

This creates optimal R:R entry with minimal drawdown.

📈 Best Markets

NQ (NASDAQ Futures) – Highly recommended

ES, YM, RTY

Gold (XAUUSD)

FX majors

Crypto (with high volatility)

Works best on 1m, 2m, 5m, or 15m depending on your trading style.

🧠 Why Traders Love This System

✔ No signals until all confirmations align

✔ Reduces overtrading and emotional decisions

✔ Follows market structure instead of random indicators

✔ Perfect for maintaining long-term funded accounts

✔ Built around institutional-grade concepts

✔ Makes your trading consistent, calm, and rules-based

⚙️ Recommended Settings

Session: 06:30–08:00 MST (NY Open)

R:R: 1.5R – 3R

Contracts: Start with 1–2 micros

Markets: NQ for best structure & volume

📦 What’s Included

Complete strategy logic

All plots, labels, sweep markers & BOS alerts

BOS retest entry automation

Session filtering

Stop loss & take profit system

Full SMC logic pipeline

🏁 Summary

The Liquidity Sweep + BOS Retest System is a complete, prop-firm-ready, structure-based strategy that automates one of the cleanest and most reliable SMC entry models. It is designed to keep you safe, consistent, and rule-compliant while capturing premium institutional setups.

If you want to trade with confidence, discipline, and prop-firm precision — this system is for you.

Good Luck -BG

Faraz Perfect Structure XL / XS (Trend-Filtered)Faraz’s Perfect Structure XL/XS identifies premium trend continuation and reversal setups using a three-filter system:

structural breakouts using dynamic swing-based support/resistance,

trend confirmation via 200-EMA slope,

momentum validation through RSI and MACD.

Signals only trigger when all factors align, eliminating noise, chop, and false signals.

Designed for traders who want clean, high-probability long (XL) and short (XS) entries.

Intellect TBTS V02 [Strategy]📌 Intellect V01 TBO – Trend Breakout Options Strategy

Intellect V01 TBO is an intraday trend-breakout strategy designed for index traders who follow Nifty, BankNifty, and FinNifty.

It identifies trend shifts using structural pivots, adaptive trendlines, and volatility-adjusted breakout zones.

The strategy provides automatic Long/Short signals, optional stop-loss and target projections, and allows users to generate alert messages that include index-option strike information.

🔍 How the Strategy Works

1. Pivot-Based Structure

The script identifies short-term high and low pivots using a user-defined period.

These pivots become anchor points for constructing directional trendlines.

2. Dynamic Trendline Projection

For each pivot, the script builds:

A projected trendline

Two offset lines above/below

A volatility band based on ATR

These help detect potential breakout zones.

3. Breakout Signal Logic

A trade signal is generated when price crosses the projected trendline:

Long Signal – detected when price breaks above a pivot-derived trendline.

Short Signal – detected when price breaks below a pivot-derived trendline.

Users may optionally restrict entries to a specific time window.

🎯 Stop-Loss & Target Zones

When a trade is active:

SL and TP levels are set using ATR-based volatility distance

Levels appear visually on the chart if enabled

Exits occur automatically when TP/SL is hit

The strategy also closes open trades near the end of the session (default 3:10 PM)

These levels are for visual and backtesting support only.

📝 Index Option Strike Calculation (For Alert Text Only)

The strategy can dynamically compute:

ATM strike (with optional bias)

Correct expiry day for Nifty (weekly) and BankNifty/FinNifty (monthly Tuesday)

CE strike for Long signals

PE strike for Short signals

This strike information is only included in alert text for users who configure external automation.

It does not affect backtesting results inside TradingView.

⏱️ Time Window Filter (Optional)

Users may define:

Start time

End time

Outside this window, no new trades are generated.

🎛️ User Adjustable Inputs

Pivot lookback period

Trendline style and extension

Display of target/stop-loss

Expiry selection mode

Strike-bias

Lot size (for alert formatting only)

Time filter settings

🔔 Alert Messages

Alerts include:

Direction (Long/Short)

Strike details

Option type (CE/PE)

Quantity

A formatted JSON message

TradingView does not execute these orders.

Users are responsible for managing external automation independently.

⚠️ Important Notes

This script does not integrate with any broker by default.

It does not place trades automatically; alerts only send text.

Backtests simulate index movement, not live option pricing.

We recommend using realistic slippage and commission settings.

✔️ This strategy is intended for educational and analytical use. Adjust settings as needed.

✅ 2. CLEAN CHART BEFORE PUBLISHING

To avoid moderator flags:

Do This Before Publishing:

✔ Remove all manual drawings

✔ Hide any other indicators on the chart

✔ Use light or clean background

✔ Keep only signals/SL/TP from your script

If you leave extra drawings, moderators may hide the script again.

✅ 3. FINAL PUBLISHING CHECKLIST

Before you click Publish, verify:

✔ Description matches the one above

✔ No broker names anywhere

✔ No "algo trading" or "automation" advertising

✔ Backtest settings are realistic

Commission enabled

Slippage > 1

Reasonable lot assumption

✔ Chart is clean

✔ Script is set to “Strategy” and compiles without warnings

Seawolf Pivot Hunter [Strategy]Overview

Seawolf Pivot Hunter is a practical trading strategy that enhances the classic pivot-box breakout system with a structured risk-management framework. Using ATR-based stop loss and take-profit calculations, position sizing, multi-layer filtering, and daily loss-limit protection, it provides a stable and sustainable trading environment. It preserves the strengths of the original version while adding systems designed to manage real-market risks more effectively.

Core Philosophy

The most important element in trading is not generating profits but controlling losses. Even the best entry signals cannot compensate for a single large loss that wipes out accumulated gains. This strategy precisely calculates the risk exposure for every trade and includes multiple layers of protection to safeguard the account under worst-case scenarios.

Indicator Setup Link

kr.tradingview.com

Example of Optimal Parameter Settings

Asset (Exchange): ETH/USDT (Binance)

Timeframe: 15-minute chart

Pivot Detection Length: 5

Upper Box Width: 2

Lower Box Width: 2

Enable Risk Management: False

Use Trailing Stop: False

Use Volume Filter

-Min Buy Volume % for Long: 50

-Min Sell Volume % for Short: 50

Use Trend Filter (EMA): False

Enable Max Loss Protection

-Max Daily Loss ($): 200

-Max Trades Per Day: 10

Calculated Bars: 50,000

Risk-Management System

Every trade automatically receives a stop-loss level at the moment of entry. The stop is calculated using ATR, adjusting dynamically to market volatility. When volatility increases, the stop widens; in stable conditions, it tightens to reduce unnecessary exits. The default distance is set to twice the ATR.

The standard take-profit level is set to four times the ATR, providing a 1:2 risk-reward structure. With this ratio, even a 50 percent win rate can produce profitability—while the typical trade structure aims for small losses and larger gains to support long-term performance.

A trailing-stop option is also available. Once the trade moves into profit, the stop level automatically trails behind price action, protecting gains while allowing the position to expand when momentum continues.

Position size is calculated automatically based on the selected risk percentage. For example, with a 2 percent risk setting, each stop-loss hit would result in exactly 2 percent of the account balance being lost. This ensures a consistent risk profile regardless of account size.

The daily loss-limit function prevents excessive drawdown by halting new trades once a predefined loss threshold is reached. This helps avoid emotional decision-making after consecutive losses.

A daily trade-limit feature is included as well. The default is 10 trades per day, protecting traders from overtrading and unnecessary fees.

Filtering System

The volume filter analyzes buying and selling pressure within the pivot box. Long trades are allowed only when buy volume exceeds a specified percentage; shorts require sell-volume dominance. The default threshold is 55 percent.

The trend filter uses an EMA to determine market direction. When price is above the 200-EMA, only long signals are permitted; when below, only shorts are allowed. This ensures alignment with the broader trend and reduces counter-trend risk.

Each filter can be toggled independently. More filters generally reduce trade frequency but improve signal quality.

Real-Time Monitoring

A real-time statistics panel displays daily profit/loss, the number of trades taken, the maximum allowed trades, and whether new trades are currently permitted. When daily limits are reached, the panel provides clear visual warnings.

Entry Logic

A trade is validated only after a pivot-box breakout occurs and all active filters—volume, trend, daily loss limit, and daily trade limit—are satisfied. Position size, stop loss, and take-profit levels are then calculated automatically. Entry arrows and labels on the chart help with later review and analysis.

Setup Guide

Risk percentage is the most critical setting. Beginners should start at 1 percent. Anything above 3 percent becomes aggressive.

ATR stop-loss multipliers should reflect asset volatility.

ATR take-profit multipliers determine reward ratio; 4.0 is the standard.

Volume thresholds are typically set between 50–60 percent depending on market conditions.

Daily loss limits are typically 2–5 percent of the account.

Trading Strategy

This strategy performs best in trending environments and works especially well on the 4-hour and daily charts. New users should begin with all filters enabled and trade conservatively. A minimum of one month of paper trading is recommended before committing real capital.

Suitable Users

The strategy is ideal for beginners who lack risk-management experience as well as advanced traders seeking a customizable structure. It is particularly helpful for traders who struggle with emotional decision-making, as pre-defined limits and rules enforce discipline.

Backtesting Guide

Use at least 2–3 years of historical data that includes bullish, bearish, and sideways conditions.

Target metrics:

Sharpe ratio: 1.5 or higher

Maximum drawdown: below 25 percent

Win rate: 40 percent or higher

Total trades: at least 100 for statistical relevance

Optimization Precautions

Avoid over-fitting parameters. Always test values around the “best” setting to verify stability.

Out-of-sample testing is essential for confirming robustness.

Test across multiple assets and timeframes to ensure consistency.

Live Deployment Roadmap

After successful backtesting, follow a gradual rollout:

Paper trading for at least one month

Small-account live testing

Slow scaling as performance stabilizes

Continuous Improvement

Keep a detailed trading journal and evaluate performance each quarter using recent data.

Adapt settings as market conditions evolve.

Conclusion

Seawolf Pivot Hunter aims to provide more than simple trade signals—it is designed to create a stable and sustainable trading system built on disciplined risk management. No strategy is perfect, and long-term success depends on consistency, patience, and strict adherence to rules. Start small, verify results, and scale progressively.

Disclaimer

This strategy is for educational and research purposes only. Past performance does not guarantee future results. All trading decisions are the responsibility of the user.

개요

Seawolf Pivot Hunter는 기본 피봇 박스 브레이크아웃 전략에 전문적인 리스크 관리 시스템을 더한 실전형 트레이딩 전략입니다. ATR 기반의 손절매와 목표가 설정, 포지션 사이징, 다층 필터링 시스템, 일일 손실 제한 기능을 통해 안정적이고 지속 가능한 트레이딩 환경을 제공합니다. 기본 버전의 장점은 유지하면서 실제 시장에서 발생할 수 있는 위험을 체계적으로 관리할 수 있도록 설계되었습니다.

핵심 철학

트레이딩에서 가장 중요한 것은 수익이 아니라 손실 관리입니다. 아무리 훌륭한 진입 조건이 있어도 한 번의 큰 손실로 모든 수익이 사라질 수 있습니다. 이 전략은 각 거래마다 감수할 리스크를 명확히 계산하고, 최악의 상황에서도 계좌를 보호하기 위한 다양한 안전장치를 제공합니다.

지표 적용 링크 공유

kr.tradingview.com

최적 조건값 설정(예시)

"종목(거래소): ETH/USDT(Binance)", "15 분봉 기준"

-Pivot Detection Length: 5

-Upper Box width: 2

-Lower Box width: 2

-Enable Risk Management: False

-Use Trailing Stop: False

-Use Volume Filter

-Min Buy Volume % for Long: 50

-Min Buy Volume % for Long: 50

-Use Trend Filter(EMA): False

-Enable Max Loss Protection

-Max Daily Loss($): 200

-Max Trades Per Day: 10

-Calucated bars: 50000

리스크 관리 시스템

모든 거래는 진입과 동시에 손절매 주문이 자동 설정됩니다. 손절가는 ATR을 기준으로 계산되며, 시장의 변동성에 따라 자동으로 조정됩니다. 변동성이 큰 시장에서는 넓은 손절폭을, 안정적인 시장에서는 좁은 손절폭을 사용해 불필요한 청산을 줄입니다. 기본값은 ATR의 2배입니다.

목표가는 ATR의 4배를 기본값으로 설정하여 손익비 1:2 구조를 유지합니다. 승률이 50퍼센트만 되어도 수익성이 가능하며, 실제로는 손절은 짧고 이익은 길게 가져가는 방식으로 장기 성과를 확보합니다.

트레일링 스톱 기능도 제공됩니다. 포지션이 수익 구간에 들어서면 손절가가 자동으로 함께 움직이며 수익을 보호합니다. 이 기능은 사용자가 켜거나 끌 수 있습니다.

포지션 크기는 리스크 퍼센트 기반으로 자동 계산됩니다. 예를 들어 리스크를 2퍼센트로 설정하면 손절 시 계좌 자산의 2퍼센트만 잃도록 수량이 조절됩니다. 계좌 크기와 무관하게 항상 일정한 비율의 리스크만 감수하게 되는 방식입니다.

일일 손실 제한 기능은 하루에 허용 가능한 최대 손실을 초과하지 않도록 합니다. 지정 금액에 도달하면 당일 거래는 더 이상 실행되지 않습니다. 감정적 거래를 막고 일정한 규율을 유지하도록 돕습니다.

일일 거래 횟수 제한 기능도 제공됩니다. 기본값은 하루 10회로, 과매매와 수수료 증가를 방지합니다.

필터링 시스템

볼륨 필터는 박스 구간 내 매수·매도 압력을 분석해 진입 신호를 검증합니다. 롱은 매수 볼륨이 일정 비율 이상일 때, 숏은 매도 볼륨이 우세할 때만 진입합니다. 기본값은 55퍼센트입니다.

추세 필터는 EMA를 사용하며, 가격이 200EMA 위에 있을 때는 롱 신호만, 아래에서는 숏 신호만 허용합니다. 큰 추세 방향에만 거래하여 역추세 리스크를 줄입니다.

필터는 독립적으로 켜고 끌 수 있으며, 필터가 많을수록 거래 횟수는 줄지만 신호 품질은 향상됩니다.

실시간 모니터링

화면에 실시간 통계 테이블이 표시되며, 일일 손익, 거래 횟수, 최대 허용 횟수, 현재 거래 가능 여부가 즉시 확인됩니다. 손실 제한 또는 거래 제한 도달 시 시각적으로 표시됩니다.

진입 로직

피봇 박스 브레이크아웃 발생 후 볼륨 필터, 추세 필터, 일일 손실·거래 제한을 모두 통과하면 포지션 크기를 계산하고 손절·목표가를 설정한 뒤 진입합니다. 진입 지점에는 화살표와 레이블이 표시되어 분석에 도움을 줍니다.

설정 가이드

리스크 퍼센트는 가장 중요한 설정입니다. 초보자는 1퍼센트를 추천하며 3퍼센트 이상은 위험합니다.

손절 ATR 배수는 자산 특성에 맞게 조절합니다.

목표가 ATR 배수는 손익비를 결정하며 기본값은 4.0입니다.

볼륨 비율은 시장 상황에 따라 50~60퍼센트 내외로 조정합니다.

일일 손실 제한은 계좌의 2~5퍼센트 수준이 적절합니다.

사용 전략

추세가 명확한 시장에서 가장 효과적이며, 4시간봉 또는 일봉을 추천합니다. 초반에는 모든 필터를 켜고 보수적으로 시작하며, 최소 한 달간 페이퍼 트레이딩을 권장합니다.

적합한 사용자

리스크 관리 경험이 부족한 초보자부터, 커스터마이징을 원하는 경험자까지 폭넓게 적합합니다. 감정적 트레이딩을 억제하는 기능이 있어 규율 유지가 어렵던 트레이더에게 특히 유용합니다.

백테스트 가이드

최소 2~3년 데이터로 테스트하며, 상승·하락·횡보 모두 포함해야 합니다.

샤프비율 1.5 이상, 최대 낙폭 25퍼센트 이하를 목표로 합니다.

승률은 40퍼센트 이상이면 충분합니다.

최소 100회 이상 거래가 있어야 통계적으로 의미가 있습니다.

최적화 주의사항

과최적화를 피하고 주변 값도 테스트해야 합니다.

샘플 외 기간 검증은 필수입니다.

여러 자산·여러 시간대에서 테스트하여 일관성을 확인해야 합니다.

실전 적용 로드맵

백테스트 후 바로 실전 투입하지 말고, 한 달 이상의 페이퍼 트레이딩 → 소액 실전 → 점진적 확대 순으로 진행합니다.

지속적 개선

일지를 기록하고 분기마다 최신 데이터로 점검합니다.

시장 변화에 따라 유연하게 조정해야 합니다.

마치며

Seawolf Pivot Hunter는 단순 신호 제공을 넘어, 안전하고 지속 가능한 트레이딩 환경 구축을 목표로 합니다. 어떤 전략도 완벽할 수 없으며, 장기적 성공을 위해서는 규칙 준수와 인내가 가장 중요합니다. 충분한 검증을 거쳐 작은 금액으로 시작하고 점진적으로 확장해나가는 접근을 추천합니다.

면책 조항

이 전략은 교육 및 연구 목적이며, 과거 성과는 미래를 보장하지 않습니다. 모든 투자 결정은 본인의 판단과 책임 하에 이루어져야 합니다.

CongTrader Strategy V1📈 CongTrader Strategy V1 — Official Overview

CongTrader Strategy V1 is a precision-built algorithm designed for intraday and swing traders who want a structured, rules-driven approach to capturing directional momentum while avoiding low-quality market conditions.

This strategy combines volatility-based logic, trend confirmation filters, and a market-conditioning engine to produce high-probability long and short signals with strictly candle-close confirmed entries (no intrabar repainting).

🔍 Core Philosophy

Modern markets move in bursts of volatility that are often preceded by subtle shifts in momentum and structure.

CongTrader V1 is engineered to:

identify emerging directional pressure early

filter out noise, consolidation, and choppy environments

only execute when multiple conditions align

maintain consistent, disciplined trade management

The result is a strategy that aims to trade quality over quantity, focusing on clear, structured setups rather than impulsive, intrabar signals.

🧠 Key Components (High-Level Explanation)

1️⃣ Directional Signal Engine (Trigger System)

The strategy uses a custom momentum-oscillation model to detect potential turning points and trend continuations.

This engine smooths price action, measures pressure extremes, and generates trigger crossovers that signal potential long or short opportunities.

(The exact formula and coefficients are proprietary and not displayed.)

2️⃣ ATR-Based Risk Management

Each trade is automatically paired with:

a volatility-adaptive stop loss, and

a volatility-adaptive profit target

This allows the strategy to adjust position management dynamically based on current market movement rather than fixed pip or dollar distances.

3️⃣ Trend Confirmation Filter (EMA)

A long-term EMA trend filter prevents counter-trend entries by ensuring:

Long positions trade only above trend

Short positions trade only below trend

This keeps signals aligned with higher-timeframe momentum.

4️⃣ VWAP Institutional Bias Filter

VWAP is used as a dynamic market fair-value reference.

The strategy only trades when price action shows favorable positioning relative to VWAP—helping avoid false moves and mean-reversion traps.

5️⃣ Range & Volatility Filter

A volatility/range filter avoids entering during tight consolidations.

If the market is not moving or lacks range expansion, the strategy waits patiently.

This significantly reduces chop and whipsaw trades.

6️⃣ RTH (Regular Trading Hours) Protection

Optionally limits trades to regular exchange hours for traders who avoid low-liquidity overnight sessions.

⏳ Candle-Close Entry Confirmation (No Repainting)

All entries are strictly confirmed after the bar closes, which means:

No intrabar fakeouts

No signal disappearance

No repainting

Cleaner, more realistic backtesting

This ensures the strategy behaves the same in backtests and in live charts.

🎯 Trade Logic Summary

A trade is only taken when:

✔ A directional trigger signal occurs

✔ Price meets VWAP bias conditions

✔ Price aligns with the long-term trend

✔ Sufficient volatility/range is present

✔ (Optional) Within regular trading hours

✔ The candle has fully confirmed

Every trade is managed automatically with ATR-based stop loss and take profit placement.

📊 Who This Strategy Is For

CongTrader V1 works well for:

Intraday traders (1–15m)

Swing traders (30m–4h)

Momentum and trend-followers

Algorithmic traders looking for disciplined, rules-based entries

Traders who want cleaner signals and less noise

Anyone who wants to avoid low-quality, choppy markets

🔔 Alerts Included

Built-in alerts notify you instantly when conditions for long or short entries are met, making it suitable for:

Manual execution

Automated trading systems

Signal services

🧩 Important Note

This strategy is designed for educational purposes and is not financial advice. Performance may vary depending on market conditions, broker feed, and instrument volatility. Always backtest thoroughly and use risk management.

Cognex Fibonacci Breakout StrategyTHE COMPLETE TRADE LOGIC (What We Want):

Step 1: Morning Session (9:30-10:30)

Track session high and low

Step 2: After 10:30 - Wait for Breakout

Bullish: Close above session high

Bearish: Close below session low

Step 3: Track Extreme After Breakout

Keep updating highest_after_breakout or lowest_after_breakout

This continuously updates as price makes new extremes

Step 4: Detect 28% Retracement (THE LOCK)

When price retraces to 28%, set last_extreme_for_retracement to the current extreme

This LOCKS the extreme for fibonacci calculations

fib_100 should use this locked value

Step 5: Place Limit Order EARLY (at 20% retracement)

When price retraces to 20%, place limit order at 28% entry

This is so the order is ready when price hits 28%

Step 6: Cancel & Recalculate if New Extreme

If price makes a NEW extreme AFTER the order is placed

Cancel the old order

Wait for new 20% retracement to place new order

Step 7: One Trade Per Day

Only ONE order placement attempt per day

Even if cancelled, don't try again

RubberBand Scalp NQ Strategy (V6 - High PF Focus)

================================================================================

RUBBERBAND SCALP NQ (V6 - HIGH PF FOCUS)

================================================================================

// STRATEGY OVERVIEW

// -----------------

// Instrument: NQ (Nasdaq 100 E-mini Futures)

// Style: Intraday mean-reversion scalping

// Core Idea: Price "stretches" away from VWAP, then "snaps back" → enter on strong reversal

// Session: 9:00 AM – 2:30 PM CST (America/Chicago)

// Timeframe: 1–5 min (ideal: 2–3 min)

// Position: 2 contracts, pyramiding = 0

// Commission: $2.00 per contract

// Goal: High Profit Factor via asymmetric exits (1R fixed + unlimited runner)

// KEY FILTERS

// -----------

// • Only trade when ATR(15) > 5.0 points (~$100 range) → avoids chop

// • Must be in session → forces flat at 2:30 PM

// • VWAP proximity: price must touch within 0.5 × ATR of VWAP

// ENTRY LOGIC (LONG)

// -----------------

// 1. In session & no position

// 2. Close > Open (bullish bar)

// 3. Close > highest high of last 4 bars → momentum confirmation

// 4. Close > VWAP

// 5. Low < VWAP + (0.5 × ATR) → pullback reached VWAP zone

// 6. ATR > 5.0

// 7. Bar confirmed

// → Plot green triangle below bar

// ENTRY LOGIC (SHORT) – Symmetric

// -----------------

// 1. Close < Open

// 2. Close < lowest low of last 4 bars

// 3. Close < VWAP

// 4. High > VWAP - (0.5 × ATR)

// 5. ATR > 5.0

// → Plot red triangle above bar

// STOP LOSS – DUAL SYSTEM (Widest Stop Wins)

// -----------------------------------------

// VWAP Stop (Long): VWAP - 0.20

// ATR Stop (Long): Close - min(ATR × 1.0, 15.0)

// Final Stop: MAX(VWAP Stop, ATR Stop) → then CAP at Close - 0.20

// Short: MIN of both → FLOOR at Close + 0.20

// → Max buffer: 0.20 pts = $20 (4 ticks)

// → Risk = |Entry – Final Stop|

// PROFIT TAKING – 2 CONTRACTS

// ---------------------------

// Contract #1: Fixed 1R → limit = entry + risk (long) / entry - risk (short)

// Contract #2: Trailing stop only → trail_points = risk, trail_offset = 0

// NO FIXED TAKE PROFIT ON RUNNER → lets 3R, 5R, 10R+ winners run

// BUG: Short runner uses trail_offset = 1.5 → CHANGE TO 0

// V6 IMPROVEMENTS

// ---------------

// 1. ATR_STOP_MULTIPLIER reduced from 1.5 → 1.0 → tighter average loss

// 2. Removed fixed 2R cap on runner → unlimited upside

// 3. Widest-stop logic → prevents premature stop-outs

// TRADE EXAMPLE (LONG)

// -------------------

// Entry: 18,125 (2 contracts)

// Stop: 18,110 → Risk = $300/contract

// 1R: 18,155 → Contract #1 exits (+$600)

// Runner trails by $300 → exits at 18,425 (+$6,000)

// Total P&L: +$6,600

// PERFORMANCE EXPECTATIONS

// ------------------------

// Win Rate: 40–50%

// Avg Winner: >3× avg loser

// Profit Factor: 2.0–3.5+

// Max Drawdown: <5% (with risk controls)

// DAILY CHECKLIST

// ---------------

// 2–3 min NQ chart

// Timezone: America/Chicago

// ATR > 5.0

// Price touched VWAP zone

// 4-bar breakout confirmed

// trail_offset = 0 (both sides)

// Alerts on

// Log R-multiple

// FINAL NOTES

// -----------

// This is a PROFIT FACTOR system — not a high win-rate system.

// Success = discipline + volatility + clean execution.

================================================================================

SP500 Session Gap Fade StrategySummary in one paragraph

SPX Session Gap Fade is an intraday gap fade strategy for index futures, designed around regular cash sessions on five minute charts. It helps you participate only when there is a full overnight or pre session gap and a valid intraday session window, instead of trading every open. The original part is the gap distance engine which anchors both stop and optional target to the previous session reference close at a configurable flat time, so every trade’s risk scales with the actual gap size rather than a fixed tick stop.

Scope and intent

• Markets. Primarily index futures such as ES, NQ, YM, and liquid index CFDs that exhibit overnight gaps and regular cash hours.

• Timeframes. Intraday timeframes from one minute to fifteen minutes. Default usage is five minute bars.

• Default demo used in the publication. Symbol CME:ES1! on a five minute chart.

• Purpose. Provide a simple, transparent way to trade opening gaps with a session anchored risk model and forced flat exit so you are not holding into the last part of the session.

• Limits. This is a strategy. Orders are simulated on standard candles only.

Originality and usefulness

• Unique concept or fusion. The core novelty is the combination of a strict “full gap” entry condition with a session anchored reference close and a gap distance based TP and SL engine. The stop and optional target are symmetric multiples of the actual gap distance from the previous session’s flat close, rather than fixed ticks.

• Failure mode it addresses. Fixed sized stops do not scale when gaps are unusually small or unusually large, which can either under risk or over risk the account. The session flat logic also reduces the chance of holding residual positions into late session liquidity and news.

• Testability. All key pieces are explicit in the Inputs: session window, minutes before session end, whether to use gap exits, whether TP or SL are active, and whether to allow candle based closes and forced flat. You can toggle each component and see how it changes entries and exits.

• Portable yardstick. The main unit is the absolute price gap between the entry bar open and the previous session reference close. tp_mult and sl_mult are multiples of that gap, which makes the risk model portable across contracts and volatility regimes.

Method overview in plain language

The strategy first defines a trading session using exchange time, for example 08:30 to 15:30 for ES day hours. It also defines a “flat” time a fixed number of minutes before session end. At the flat bar, any open position is closed and the bar’s close price is stored as the reference close for the next session. Inside the session, the strategy looks for a full gap bar relative to the prior bar: a gap down where today’s high is below yesterday’s low, or a gap up where today’s low is above yesterday’s high. A full gap down generates a long entry; a full gap up generates a short entry. If the gap risk engine is enabled and a valid reference close exists, the strategy measures the distance between the entry bar open and that reference close. It then sets a stop and optional target as configurable multiples of that gap distance and manages them with strategy.exit. Additional exits can be triggered by a candle color flip or by the forced flat time.

Base measures

• Range basis. The main unit is the absolute difference between the current entry bar open and the stored reference close from the previous session flat bar. That value is used as a “gap unit” and scaled by tp_mult and sl_mult to build the target and stop.

Components

• Component one: Gap Direction. Detects full gap up or full gap down by comparing the current high and low to the previous bar’s high and low. Gap down signals a long fade, gap up signals a short fade. There is no smoothing; it is a strict structural condition.

• Component two: Session Window. Only allows entries when the current time is within the configured session window. It also defines a flat time before the session end where positions are forced flat and the reference close is updated.

• Component three: Gap Distance Risk Engine. Computes the absolute distance between the entry open and the stored reference close. The stop and optional target are placed as entry ± gap_distance × multiplier so that risk scales with gap size.

• Optional component: Candle Exit. If enabled, a bullish bar closes short positions and a bearish bar closes long positions, which can shorten holding time when price reverses quickly inside the session.

• Session windows. Session logic uses the exchange time of the chart symbol. When changing symbols or venues, verify that the session time string still matches the new instrument’s cash hours.

Fusion rule

All gates are hard conditions rather than weighted scores. A trade can only open if the session window is active and the full gap condition is true. The gap distance engine only activates if a valid reference close exists and use_gap_risk is on. TP and SL are controlled by separate booleans so you can use SL only, TP only, or both. Long and short are symmetric by construction: long trades fade full gap downs, short trades fade full gap ups with mirrored TP and SL logic.

Signal rule

• Long entry. Inside the active session, when the current bar shows a full gap down relative to the previous bar (current high below prior low), the strategy opens a long position. If the gap risk engine is active, it places a gap based stop below the entry and an optional target above it.

• Short entry. Inside the active session, when the current bar shows a full gap up relative to the previous bar (current low above prior high), the strategy opens a short position. If the gap risk engine is active, it places a gap based stop above the entry and an optional target below it.

• Forced flat. At the configured flat time before session end, any open position is closed and the close price of that bar becomes the new reference close for the following session.

• Candle based exit. If enabled, a bearish bar closes longs, and a bullish bar closes shorts, regardless of where TP or SL sit, as long as a position is open.

What you will see on the chart

• Markers on entry bars. Standard strategy entry markers labeled “long” and “short” on the gap bars where trades open.

• Exit markers. Standard exit markers on bars where either the gap stop or target are hit, or where a candle exit or forced flat close occurs. Exit IDs “long_gap” and “short_gap” label gap based exits.

• Reference levels. Horizontal lines for the current long TP, long SL, short TP, and short SL while a position is open and the gap engine is enabled. They update when a new trade opens and disappear when flat.

• Session background. This version does not add background shading for the session; session logic runs internally based on time.

• No on chart table. All decisions are visible through orders and exit levels. Use the Strategy Tester for performance metrics.

Inputs with guidance

Session Settings

• Trading session (sess). Session window in exchange time. Typical value uses the regular cash session for each contract, for example “0830-1530” for ES. Adjust if your broker or symbol uses different hours.

• Minutes before session end to force exit (flat_before_min). Minutes before the session end where positions are forced flat and the reference close is stored. Typical range is 15 to 120. Raising it closes trades earlier in the day; lowering it allows trades later in the session.

Gap Risk

• Enable gap based TP/SL (use_gap_risk). Master switch for the gap distance exit engine. Turning it off keeps entries and forced flat logic but removes automatic TP and SL placement.

• Use TP limit from gap (use_gap_tp). Enables gap based profit targets. Typical values are true for structured exits or false if you want to manage exits manually and only keep a stop.

• Use SL stop from gap (use_gap_sl). Enables gap based stop losses. This should normally remain true so that each trade has a defined initial risk in ticks.

• TP multiplier of gap distance (tp_mult). Multiplier applied to the gap distance for the target. Typical range is 0.5 to 2.0. Raising it places the target further away and reduces hit frequency.

• SL multiplier of gap distance (sl_mult). Multiplier applied to the gap distance for the stop. Typical range is 0.5 to 2.0. Raising it widens the stop and increases risk per trade; lowering it tightens the stop and may increase the number of small losses.

Exit Controls

• Exit with candle logic (use_candle_exit). If true, closes shorts on bullish candles and longs on bearish candles. Useful when you want to react to intraday reversal bars even if TP or SL have not been reached.

• Force flat before session end (use_forced_flat). If true, guarantees you are flat by the configured flat time and updates the reference close. Turn this off only if you understand the impact on overnight risk.

Filters

There is no separate trend or volatility filter in this version. All trades depend on the presence of a full gap bar inside the session. If you need extra filtering such as ATR, volume, or higher timeframe bias, they should be added explicitly and documented in your own fork.

Usage recipes

Intraday conservative gap fade

• Timeframe. Five minute chart on ES regular session.

• Gap risk. use_gap_risk = true, use_gap_tp = true, use_gap_sl = true.

• Multipliers. tp_mult around 0.7 to 1.0 and sl_mult around 1.0.

• Exits. use_candle_exit = false, use_forced_flat = true. Focus on the structured TP and SL around the gap.

Intraday aggressive gap fade

• Timeframe. Five minute chart.

• Gap risk. use_gap_risk = true, use_gap_tp = false, use_gap_sl = true.

• Multipliers. sl_mult around 0.7 to 1.0.

• Exits. use_candle_exit = true, use_forced_flat = true. Entries fade full gaps, stops are tight, and candle color flips flatten trades early.

Higher timeframe gap tests

• Timeframe. Fifteen minute or sixty minute charts on instruments with regular gaps.

• Gap risk. Keep use_gap_risk = true. Consider slightly higher sl_mult if gaps are structurally wider on the higher timeframe.

• Note. Expect fewer trades and be careful with sample size; multi year data is recommended.

Properties visible in this publication

• On average our risk for each position over the last 200 trades is 0.4% with a max intraday loss of 1.5% of the total equity in this case of 100k $ with 1 contract ES. For other assets, recalculations and customizations has to be applied.

• Initial capital. 100 000.

• Base currency. USD.

• Default order size method. Fixed with size 1 contract.

• Pyramiding. 0.

• Commission. Flat 2 USD per order in the Strategy Tester Properties. (2$ buying + 2$selling)

• Slippage. One tick in the Strategy Tester Properties.

• Process orders on close. ON.

Realism and responsible publication

• No performance claims are made. Past results do not guarantee future outcomes.

• Costs use a realistic flat commission and one tick of slippage per trade for ES class futures.

• Default sizing with one contract on a 100 000 reference account targets modest per trade risk. In practice, extreme slippage or gap through events can exceed this, so treat the one and a half percent risk target as a design goal, not a guarantee.

• All orders are simulated on standard candles. Shapes can move while a bar is forming and settle on bar close.

Honest limitations and failure modes

• Economic releases, thin liquidity, and limit conditions can break the assumptions behind the simple gap model and lead to slippage or skipped fills.

• Symbols with very frequent or very large gaps may require adjusted multipliers or alternative risk handling, especially in high volatility regimes.

• Very quiet periods without clean gaps will produce few or no trades. This is expected behavior, not a bug.

• Session windows follow the exchange time of the chart. Always confirm that the configured session matches the symbol.

• When both the stop and target lie inside the same bar’s range, the TradingView engine decides which is hit first based on its internal intrabar assumptions. Without bar magnifier, tie handling is approximate.

Legal

Education and research only. This strategy is not investment advice. You remain responsible for all trading decisions. Always test on historical data and in simulation with realistic costs before considering any live use.

ETH SuperTrend Hull Strategy - 15min Futures(重制版)🟠 ETH SuperTrend Hull Strategy - 15min Futures

Strategy Overview

The "ETH SuperTrend Hull Strategy" is a sophisticated 15-minute trading system specifically designed for Bitcoin perpetual contracts. This advanced algorithm integrates SuperTrend indicators with Hull moving averages to deliver high-precision trend following through a triple-confirmation mechanism, featuring intelligent position management and multi-level take-profit systems.

Core Value Proposition

Triple Trend Confirmation: SuperTrend + Hull MA + ATR volatility filtering

Adaptive Take-Profit System: 6-level dynamic profit targets adjusted to market conditions

Smart Position Management: Three martingale modes with automatic sizing

Real-time Webhook Integration: Direct exchange connectivity for automated execution

🟠 Technical Framework

Multi-Layer Trend Detection

Layer 1 - SuperTrend Filter

pinescript

= ta.supertrend(supertrend_factor, supertrend_atr_period)

is_supertrend_long = direction < 0 // Bullish trend line

is_supertrend_short = direction >= 0 // Bearish trend line

Layer 2 - Hull MA Confirmation

pinescript

HMA = HMA(close, 73) // Hull Moving Average

hull_is_green = HULL > HULL // Uptrend confirmation

hull_is_red = HULL <= HULL // Downtrend confirmation

Layer 3 - ATR Breakout Signals

pinescript

xATR = ta.atr(5)

nLoss = key_value * xATR // Dynamic stop distance

Entry Conditions

Long Entry:

Price breaks above ATR trailing stop

Hull MA shows green uptrend

SuperTrend indicates bullish momentum

Price positioned above Hull MA

Short Entry:

Price breaks below ATR trailing stop

Hull MA shows red downtrend

SuperTrend indicates bearish momentum

Price positioned below Hull MA

🟠 Risk Management System

Position Sizing

text

Base Position = Initial Capital × Risk % / Entry Price × Leverage

Actual Position = Base Position × Martingale Multiplier (1.0-5.0x)

Martingale Modes

4x Mode: Conservative approach, maximum 4x position scaling

5x Mode: Balanced risk management, maximum 5x scaling

5x Big Mode: Aggressive growth with faster position increases

Dynamic Take-Profit System

6-Level Profit Targets:

TP1: 2.2×ATR (Close 30%)

TP2: 4.5×ATR (Close 25%)

TP3: 7.5×ATR (Close 20%)

TP4: 10.5×ATR (Close 10%)

TP5: 15.5×ATR (Close 7%)

TP6: 20.5×ATR (Close 3%)

ATR Adaptive Adjustment:

Short-term ATR > Long-term ATR: TP distance +0.5

Short-term ATR < Long-term ATR: TP distance -0.5

🟠 Configuration Parameters

Core Settings

pinescript

// Trend Sensitivity

key_value = 2.0 // ATR multiplier (lower = more sensitive)

supertrend_factor = 3.0 // SuperTrend factor

// Risk Management

risk_percent = 19.9 // Per trade risk %

leverage = 1.0 // Leverage multiplier

Hull MA Configuration

pinescript

length = 73 // Hull period (55-200)

modeSwitch = "Hma" // Hull variant (Hma/Thma/Ehma)

🟠 Quick Start Guide

Initial Setup

Apply to BTCUSDT perpetual 15-minute chart

Configure Webhook Signal ID and User ID

Adjust position parameters according to risk preference

Signal Monitoring

Long Signals: Green arrows with Hull MA turning green

Short Signals: Red arrows with Hull MA turning red

Trend Direction: SuperTrend line color changes

Execution Workflow

Wait for triple-signal confluence

Confirm all entry conditions met

System automatically calculates position size and TP levels

Webhook sends trade instructions to connected platform

Advanced Features

Heikin-Ashi Mode: Smooth price data using Heikin-Ashi candles

Fixed Position Mode: Disable martingale, use fixed sizing

Multi-Timeframe: Higher timeframe confirmation integration

🟠 ETH SuperTrend Hull Strategy - 15min Futures

策略概述

"ETH超级趋势Hull策略"是一款专为比特币永续合约设计的15分钟短线交易系统。该策略融合超级趋势指标与Hull均线,通过三重过滤机制实现高精度趋势跟踪,具备智能仓位管理和多级止盈体系。

核心价值

三重趋势确认:Supertrend + Hull均线 + ATR波动过滤

自适应止盈系统:6级动态止盈,根据市场波动调整目标

智能仓位管理:支持三种倍投模式,自动调整仓位规模

实时Webhook通知:直连交易平台,实现自动化执行

🟠 策略原理

趋势识别系统

第一层 - 超级趋势过滤

pinescript

= ta.supertrend(supertrend_factor, supertrend_atr_period)

is_supertrend_long = direction < 0 // 绿色趋势线

is_supertrend_short = direction >= 0 // 红色趋势线

第二层 - Hull均线确认

pinescript

HMA = HMA(close, 73) // Hull移动平均线

hull_is_green = HULL > HULL // 上升趋势

hull_is_red = HULL <= HULL // 下降趋势

第三层 - ATR突破信号

pinescript

xATR = ta.atr(5)

nLoss = key_value * xATR // 动态止损距离

入场条件

多头入场:

价格突破ATR追踪止损

Hull均线呈绿色上升趋势

超级趋势显示看涨信号

价格位于Hull均线上方

空头入场:

价格跌破ATR追踪止损

Hull均线呈红色下降趋势

超级趋势显示看跌信号

价格位于Hull均线下方

🟠 风险管理

仓位计算

text

基础仓位 = 初始资金 × 风险比例% / 入场价格 × 杠杆倍数

实际仓位 = 基础仓位 × 倍投系数 (1.0-5.0倍)

倍投模式

4倍模式:保守型,最大4倍加仓

5倍模式:均衡型,最大5倍加仓

5倍大模式:激进型,更快仓位增长

动态止盈系统

6级止盈目标:

TP1: 2.2×ATR (平仓30%)

TP2: 4.5×ATR (平仓25%)

TP3: 7.5×ATR (平仓20%)

TP4: 10.5×ATR (平仓10%)

TP5: 15.5×ATR (平仓7%)

TP6: 20.5×ATR (平仓3%)

ATR自适应调整:

短期ATR > 长期ATR:止盈距离+0.5

短期ATR < 长期ATR:止盈距离-0.5

🟠 参数配置

核心参数

pinescript

// 趋势敏感度

key_value = 2.0 // ATR乘数,值越小越敏感

supertrend_factor = 3.0 // 超级趋势因子

// 风险管理

risk_percent = 19.9 // 单次交易风险%

leverage = 1.0 // 杠杆倍数

Hull均线设置

pinescript

length = 73 // Hull周期 (55-200)

modeSwitch = "Hma" // Hull变体 (Hma/Thma/Ehma)

🟠 使用指南

初始设置

添加到BTCUSDT永续合约15分钟图表

配置Webhook信号ID和用户ID

根据风险偏好调整仓位参数

信号监控

多单信号:绿色箭头,Hull均线转绿

空单信号:红色箭头,Hull均线转红

趋势方向:超级趋势线颜色变化

执行流程

等待三重信号共振

确认入场条件满足

系统自动计算仓位和止盈

通过Webhook发送交易指令

高级功能

K线均线模式:使用Heikin-Ashi平滑价格

固定仓位模式:禁用倍投,固定仓位大小

多时间框架:集成更高时间框架确认

Sunflower Quant - ETH 15min Strategy🟠 Sunflower Quant - ETH 15min Strategy

Strategy Overview

The " Sunflower Quant - ETH 15min Strategy" is a sophisticated automated trading system specifically designed for ETH/USDT on 15-minute timeframes. This advanced algorithm integrates over 20 technical indicators and price action patterns to deliver intelligent entry decisions and comprehensive risk management.

Core Value Proposition

Multi-Timeframe Integration: Combines 1-hour and 4-hour higher timeframe data for signal validation

Dynamic Market Regime Detection: Real-time identification of Low Volatility, Ranging, and High Volatility market environments

Comprehensive Scoring System: Three-dimensional evaluation model based on Breakout Signals, Pattern Recognition, and Position Analysis

Adaptive Position Sizing: Dynamic allocation based on signal strength and market volatility

🟠 Core Architecture

Three-Layer Analytical Framework

1. Market Regime Detection System

Real-time market environment assessment through four dimensions:

ATR Relative Volatility

Bollinger Band Width

Average Amplitude

Momentum Strength

Market State Classification:

Low Volatility (≤30 points): Narrow ranges, awaiting breakout

Ranging Market (31-65 points): Moderate volatility, suitable for range trading

High Volatility (>65 points): Strong trends, ideal for trend following

2. Signal Generation Engine

Breakout Signal Layer:

Donchian Channel Breakouts (Upper/Middle/Lower)

Keltner Channel Breakouts (Upper/Middle/Lower)

Double ATR Momentum Confirmation

Pattern Recognition Layer:

Price Action: Outside Bars, Engulfing Patterns, False Breakouts

Candlestick Patterns: Hammer, Inverted Hammer, Doji, Dragonfly, Gravestone

Three Soldiers Method: Single-bar and Three-bar consecutive patterns

Position Analysis Layer:

Ichimoku Cloud Position (Above/Within/Below)

ADX Trend Strength Confirmation

DC/KC Middle Band Position Analysis

3. Volume & POC Analysis

Volume Confirmation:

High Volume Breakout Validation

Medium Volume Support Confirmation

Point of Control (POC) Value Areas:

Volume-based dense trading zone identification

POC Cluster Scoring System (Size Score + Volume Score + Time Score)

🟠 Trading Logic Specification

Entry Signal Classification

A-Class Signals (Strong Breakout)

Trigger: VP breaking key POC levels + strong pattern confirmation

Characteristics: High confidence, larger position sizing

Stop Loss: Wider stops based on historical ATR volatility

B-Class Signals (Pattern Confirmed)

Trigger: Clear price patterns + volume confirmation

Characteristics: Medium confidence, standard position sizing

Stop Loss: Based on pattern lows/highs

C-Class Signals (Weak Reversal)

Trigger: Single indicator signals + positional support

Characteristics: Lower confidence, small exploratory positions

Stop Loss: Tight stops for quick exits

Scoring Weight Distribution

text

Base Score = Breakout(30%) + Patterns(40%) + Position(30%)

Final Score = Base Score × Market Regime Coefficient × Cloud Position Coefficient

🟠 Risk Management System

Dynamic Stop Loss Strategy

Initial Stop Loss: ATR-based volatility + market regime adjustment

Trailing Stop: Phased tracking, progressively locking profits

Position Management

text

Base Position = Initial Capital × Base Coefficient / Stop Distance

Final Position = Base Position × Signal Strength Coefficient × Market Volatility Coefficient

Take Profit System

Scaled Profit Taking: 8 profit levels with proportional position distribution

Dynamic Adjustment: Trailing stop activation upon reaching specific profit tiers

🟠 Configuration Parameters

Market Regime Thresholds

pinescript

Low Volatility: ≤30 points

Ranging Market: 31-65 points

High Volatility: >65 points

Signal Strength Thresholds

pinescript

// Current Entry Thresholds (No Position)

Low Volatility: Long 82 / Short 82

Ranging: Long 75 / Short 80

High Volatility: Long 80 / Short 85

// Reversal Entry Thresholds

Low Volatility: Long 75 / Short 90

Ranging: Long 85 / Short 90

High Volatility: Long 90 / Short 100

🟠 Usage Guide

1. Initial Setup

Apply to ETH/USDT 15-minute chart

Configure webhook Signal ID and UID

Adjust initial capital parameters according to account size

2. Key Monitoring Elements

Market Regime Indicator: Watch background color changes

Signal Score Display: Monitor real-time long/short scores

POC Value Areas: Identify key support/resistance levels

3. Trading Decision Process

Trend Confirmation Phase:

text

1. Observe market regime background

2. Confirm Ichimoku cloud position

3. Check ADX trend strength

Entry Signal Screening:

text

1. Comprehensive score > corresponding threshold

2. Multiple indicator signal confluence

3. Volume confirmation alignment

Risk Management Execution:

text

1. Automatic position size calculation

2. Set scaled take profit and stop loss

3. Monitor trailing stop updates

4. Advanced Features

Lookback Mode: Historical signal validation

Special Close: Early exit based on ATR ratio

Signal Filtering: Optimize signal quality through component weight adjustment

This systematic multi-factor scoring strategy delivers stable automated trading decisions in complex market environments, particularly well-suited for the short-term volatility characteristics of cryptocurrencies like Ethereum.

Strategy Name: Sunflower Quantitative Strategy

Symbol: ETH/USDT

Timeframe: 15-minute

Market: Cryptocurrency

Strategy Type: Multi-timeframe Quantitative Analysis

Risk Level: Medium-High

Recommended Capital: $10,000+ for optimal position sizing

"向日葵量化"是一款专为ETH 15分钟图表设计的全自动量化交易策略。该策略通过多维度技术分析框架,集成超过20种技术指标与价格行为模式,实现智能化的入场决策与风险控制。

核心价值

多时间框架协同:整合1小时、4小时高周期数据,确保信号质量

动态市场状态识别:实时识别低波动、震荡、高波动三种市场环境

综合评分系统:基于突破信号、形态识别、位置分析的三维评分模型

智能仓位管理:根据信号强度与市场波动率动态调整仓位规模

🟠【核心架构】

策略基于三层分析框架构建:

1. 市场状态识别系统

通过ATR相对波动率、布林带宽、平均振幅、动量强度四个维度,实时判断当前市场环境:

低波动市场(≤30分):窄幅震荡,等待突破

震荡市场(31-65分):中等波动,适合区间交易

高波动市场(>65分):趋势明确,适合趋势跟踪

2. 信号生成引擎

突破信号层:

DC通道突破(上轨/中轨/下轨)

KC通道突破(上轨/中轨/下轨)

双ATR动量确认

形态识别层:

价格行为模式:外包线、吞没形态、假突破

K线形态:锤子线、倒锤子线、十字星、蜻蜓线、墓碑线

三兵三法:单根强度与三根连续形态

位置分析层:

云图位置关系(之上/之中/之下)

ADX趋势强度确认

DC/KC中轨位置判断

3. 成交量与POC分析

成交量确认:

高成交量突破确认

中等成交量支撑确认

POC价值区域:

基于成交量分布的密集成交区识别

POC集群评分系统(规模分+成交量分+时间分)

🟠【交易逻辑详解】

入场信号分类

A类信号(强势突破)

触发条件:VP突破POC关键位 + 强势形态确认

特征:高置信度,大仓位配置

止损设置:相对宽松,基于ATR历史波动率

B类信号(形态确认)

触发条件:明确价格形态 + 成交量确认

特征:中等置信度,标准仓位

止损设置:基于形态低点/高点

C类信号(弱势反弹)

触发条件:单一指标信号 + 位置支撑

特征:低置信度,小仓位试探

止损设置:紧凑止损,快速离场

评分权重分配

text

基础分 = 突破分(30%) + 形态分(40%) + 位置分(30%)

最终分 = 基础分 × 市场状态系数 × 云图位置系数

🟠【风险管理系统】

动态止损策略

初始止损:基于ATR波动率 + 市场状态调整系数

移动止损:分阶段跟踪,逐级锁定利润

仓位管理

text

基础仓位 = 初始资金 × 基础系数 / 止损距离

最终仓位 = 基础仓位 × 信号强度系数 × 市场波动系数

止盈系统

分级止盈:8个止盈级别,按仓位比例分配

动态调整:达到特定止盈级别后启动移动止损

🟠【配置参数】

市场状态阈值

pinescript

低波动区间:≤30分

震荡区间:31-65分

高波动区间:>65分

信号强度阈值

pinescript

// 当前开仓阈值(无持仓)

低波动:做多82分 / 做空82分

震荡:做多75分 / 做空80分

高波动:做多80分 / 做空85分

// 反转开仓阈值

低波动:做多75分 / 做空90分

震荡:做多85分 / 做空90分

高波动:做多90分 / 做空100分

🟠【使用指南】

1. 初始设置

添加到ETH/USDT 15分钟图表

配置webhook信号ID和UID

根据资金量调整初始资本参数

2. 监控要点

市场状态指示器:关注背景颜色变化

信号评分显示:实时查看多头/空头得分

POC价值区域:识别关键支撑阻力

3. 交易决策流程

趋势确认阶段:

text

1. 观察市场状态背景色

2. 确认云图位置关系

3. 检查ADX趋势强度

入场信号筛选:

text

1. 综合评分 > 对应阈值

2. 多指标信号共振

3. 成交量确认配合

风险管理执行:

text

1. 自动计算仓位大小

2. 设置分级止盈止损

3. 监控移动止损更新

4. 高级功能

回看模式:启用历史信号验证

特殊平仓:基于ATR比率的提前离场

信号过滤:通过调整各组件权重优化信号质量

该策略通过系统化的多因子评分机制,在复杂的市场环境中实现稳定的自动化交易决策,特别适合ETH等加密货币的短期波动特性。

AlosAlgoAlosAlgo Version: 1 BETA

A multi-timeframe, ATR-driven trend strategy with flexible entry engines (Open/Close vs Renko), optional HTF Heikin Ashi filtering, and a built-in 3-stage take-profit model designed to be backtested on TradingView and automated via webhooks.

Fractional Candlestick Long Only Experimental V4 Another example of use an idea of Fractional Candlestick , based on mathematical rules of Fractional Calculus , typical kernel Caputo-Fabrizio ( CF ) and Atangana-Baleanu is used, alfa factor ( esential for calculation ) is in range 0,1-0.9.

Let's fun with this script .

ATR + ATR 전략It is a strong trend strategy based on ATR and ADX. Optimized for 15 installments of Bitcoin futures.

Trilok saini EMA Pullback + MACD + ADX Strategy📌 HA Double EMA Pullback + MACD + ADX Strategy — Description

This strategy combines Heikin Ashi candles, Double EMA pullbacks, MACD momentum filtering, and ADX trend-strength confirmation to generate high-probability trend-continuation signals.

It is designed to avoid choppy markets and focus only on strong trending conditions.

🔥 Key Features

1️⃣ Heikin Ashi Trend Analysis

Heikin Ashi candles are calculated on the selected timeframe.

They smooth out market noise to highlight clear bullish or bearish trends.

Trend direction is displayed in a live info table.

2️⃣ Double EMA Pullback Logic

The main signal engine of this strategy:

Buy conditions

Price crosses above EMA 20

EMA 20 > EMA 50 (confirming uptrend)

A pullback is detected using the back-step (price was above EMA earlier)

MACD + ADX filters approve the trade

Sell conditions

Price crosses below EMA 20

EMA 20 < EMA 50 (confirming downtrend)

Pullback confirmation based on earlier price action

MACD + ADX filters approve the trade

This logic focuses on trend continuation instead of reversal setups.

3️⃣ MACD Momentum Filter

Buy signals appear only when MACD histogram is positive (green).

Sell signals appear only when MACD histogram is negative (red).

Prevents entries during weak or directionless momentum.

4️⃣ ADX Trend Strength Filter

Signals are blocked when ADX is below the selected threshold.

Ensures trades happen only in strong trending markets, reducing false signals.

5️⃣ Visual Enhancements

Clean Heikin Ashi candles with customizable colors

Optional regular candles for comparison

EMA overlays on HA candles

Buy/Sell labels with customizable text

Info table showing:

Trend direction

HA close

Regular close

EMA values

ADX reading

Active filters

🎯 Ideal Use Cases

Trend-following traders

Swing traders

Intraday traders who want filtered signals

Anyone wanting fewer false signals in sideways markets

⚠️ Disclaimer

This script is for educational and research purposes only.

Past performance does not guarantee future results. Always backtest and use proper risk management.