Smart Impulse PRO v1.0Smart Impulse PRO (Invite‑Only) — Comprehensive Guide for TradingView

***

## English Version

Smart Impulse PRO (Invite‑Only) — Comprehensive Guide for TradingView

Strategy Concept & Uniqueness

Smart Impulse PRO is a trend‑following impulse continuation strategy built specifically for volatile crypto pairs . It uses a custom price×volume impulse signal normalized with Z‑score , then filters these impulses through multi‑timeframe trend conditions and a layered guard system that blocks structurally weak trades (flat, overextension, exhaustion).

Backtest Summary (Crypto Pairs)

Smart Impulse PRO was backtested on several volatile crypto perpetual pairs (including ETHUSDT, BTCUSDT and other majors/alts) on 1h charts in the period 01 Jan 2023 – 26 Dec 2025. On this sample, typical results were:

- Total trades per pair : ≈100–130

- Win rate range : ≈ 90–94%

- Profit factor range : ≈ 3.0–3.9

These values are historical backtest metrics on specific symbols and settings and do not guarantee similar performance in the future .

Why It’s Special

✅ Custom price×volume impulse model (Z‑score‑based) : Measures how unusual each bar’s move is in its recent context, not just simple MA/RSI crossovers

✅ 15+ Exhaustion & Structure Guards : Automatically block bad contexts (flat, low vol, overextended candles, climax volume)

✅ Dynamic TP Grid : Take‑profit levels adapt to current impulse strength |Z|

✅ Visual Transparency : Bubbles show exactly why signals were blocked

✅ Invite‑Only Logic : The concrete impulse model and guard interactions are proprietary and therefore published as invite‑only with protected source, as allowed by TradingView’s script rules.

***

### 1. What the Script Does (User View)

Smart Impulse PRO acts as an automated decision engine for volatile crypto pairs (e.g., ETHUSDT, BTCUSDT) on intraday and swing timeframes (15m–4h). It:

- Generates Long/Short entries only when both trend and impulse conditions align.

- Manages exits with a multi‑level TP grid, breakeven logic, optional trailing stop and time‑based exit.

- Visually shows both taken trades and blocked signals , including a short text reason for rejection.

This lets users trade crypto trends with a clear explanation of when and why the strategy chooses to act or stay out.

***

Entry Rules

Long (Buy):

Price is above EMA200 (long‑term trend is up)

Z‑score impulse > Z_threshold (e.g., 1.5)

Volume above recent average

ADX > Min ADX (e.g., 25)

ATR regime OK (ATR > ATR_floor and not in volatility squeeze)

All active guards pass (no overextended candle, no extreme wick against direction, no climax volume lock, no distance violation vs EMA200/VWAP, no Z‑streak lock)

Short (Sell):

Price is below EMA200 (long‑term trend is down)

Z‑score impulse > Z_threshold

Volume above recent average

ADX > Min ADX

ATR regime OK

All active guards pass (same checks, mirrored for shorts)

Logic:

The script first checks that the market is trending (EMA200 side + ADX + volatility filters), then validates that the current bar is a statistically strong price×volume impulse, and finally makes sure the bar is not an exhaustion spike or overextended move according to the guard system. Only if all three layers agree, a trade is opened.

Exit Rules

Stop‑Loss:

Initial stop‑loss is placed at a user‑defined distance (percent or ATR‑based), and position size is calculated so that a full stop equals Max Risk per Trade (%).

Take‑Profit grid:

Up to 10 TP levels.

Step type: Percent, ATR% or Hybrid.

Optional “Breathing grid”: TP distances are increased in proportion to |Z‑score| at entry (capped), so stronger impulses receive wider, more ambitious targets.

TP Profile (Equal / Aggressive / Balanced / Defensive) decides how much size is closed at each level.

Breakeven and Trailing:

Optional breakeven: after TP1 is hit, stop can be moved to entry price plus a small offset.

Optional ATR‑based trailing stop activates only after TP3 to avoid being shaken out too early by noise.

Time‑based Exit:

If enabled, any open trade that does not hit TP or SL within the chosen time limit (bars or minutes) is closed at market, to avoid very long, stagnant positions.

### 2. How the Script Works (Internals)

2.1 Impulse Engine (Custom Z‑Score Model)

At the core is a price×volume impulse series with Z‑score normalisation:

- Raw impulse:

`delta_impulse = (close - close ) * volume`

- Normalisation over N bars (default N = 20):

`zscore = (delta_impulse - avg(delta_impulse, N)) / stdev(delta_impulse, N)`

A bar becomes an impulse candidate only when:

- `abs(zscore) > Z_threshold` (default 1.5), and

- volume is above its recent average.

This is a custom implementation of a price×volume impulse model based on Z‑score; the exact combination of inputs, window, thresholds and how this signal feeds guards and exits is part of the proprietary logic.

2.2 Trend & Volatility Context — Why the Mashup Exists

The strategy combines several classic tools, but each covers a specific failure mode. The mashup is intentional:

| Component | What it checks | Why it is needed |

|----------|----------------|------------------|

| EMA200 | Long‑term bias (price above/below) | Prevents counter‑trend trading |

| EMA200 slope | Steepness of EMA over K bars | Filters flat/ranging phases even above/below EMA |

| VWAP | Distance of price from volume‑weighted fair value | Avoids entering when price is far from value (overextension) |

| ADX | Trend strength | Disables signals in low‑trend, choppy markets |

| ATR vs AvgATR50 | Current volatility vs recent average | Detects volatility squeezes and abnormally calm regimes |

| ATR% floor (Anti‑Flat Gate) | ATR as % of price | Hard “no‑trade” mode in ultra‑tight ranges |

An impulse alone is not sufficient in crypto; only impulses inside a suitable trend and volatility context are allowed to become trades.

2.3 Guard System (Exhaustion & Overextension)

Above trend filters, Smart Impulse PRO adds a guard layer designed from typical crypto problems (late entries, news spikes, “buying the top”):

- Max body / ATR : Rejects abnormally large real bodies (e.g., body > 3× ATR), often at the end of a move.

- Max range / ATR : Blocks extremely long high‑low bars.

- Upper/lower wick filters :

- Longs blocked when upper wick dominates (rejection from above).

- Shorts blocked when lower wick dominates (rejection from below).

- Z‑streak guard : After several consecutive impulse bars in the same direction, new entries in that direction are disabled to avoid chasing.

- Climax volume + cool‑off : When volume spikes above a multiple of its recent average, new trades are paused for N bars.

- Distance guards : Excessive distance (in ATR multiples) from EMA200 and VWAP can block trades.

These checks interact with the impulse model so that the final decision reflects a coherent risk framework rather than a loose collection of filters.

2.4 Dynamic TP Grid (Exit Logic)

- Up to 10 TP levels; step type: Percent, ATR% or Hybrid.

- With Breathing grid , TP spacing is increased by a factor of `k * abs(zscore)` (capped) at entry.

- Stronger impulses (higher |z|) → wider distances between TP levels; weaker impulses → tighter TP spacing.

- TP profiles (Equal / Aggressive / Balanced / Defensive) control how much position size is allocated to early vs late targets.

- Optional breakeven: move SL to entry (plus offset) after TP1.

- Optional trailing: ATR‑based trailing stop activates after TP3.

This links entry strength and exit geometry using the same impulse signal.

***

### 3. How to Use the Script (Practical Guide)

3.1 Quick Start

1. Add Smart Impulse PRO to a volatile crypto pair (e.g., ETHUSDT, BTCUSDT) on 15m–4h.

2. Keep the default preset and observe executed trades and blocked bubbles.

3. Use the dashboard to see which filters are active and which ones are blocking most trades (e.g., ADX, Flat, Exhaust).

4. If there are too few trades, gradually lower Z_threshold or Min ADX , or slightly relax guard limits — change one parameter at a time .

5. Set Max Risk per Trade (%) , stop distance, TP count/profile and optional trailing in line with your risk tolerance.

3.2 Example Profiles

- Aggressive intraday (15m)

- Z‑threshold 1.2

- Min ADX 20

- ATR% floor 0.2%

- Some exhaustion guards disabled (e.g., less strict wick limits).

- Conservative swing (1h–4h)

- Z‑threshold 1.5

- Min ADX 25–30

- ATR% floor 0.3–0.4%

- All guards enabled, higher‑timeframe filters ON.

3.3 Risk Management & Position Sizing

- Max Risk per Trade (%) — percentage of equity at risk if the full stop‑loss is hit.

- Position size is computed automatically from Max Risk %, stop distance and instrument price.

- Breakeven and trailing can be enabled to reduce open risk after partial profit is taken.

- Time‑based exit closes trades that stay open beyond a user‑defined duration without reaching TP or SL.

3.4 Alerts

Alerts use `strategy.order.alert_message` to send JSON containing side (long/short), entry, stop and TP levels. This allows users to connect the strategy with external bots or dashboards without exposing internal code.

***

### 4. Why This Script Is Invite‑Only (Originality Justification)

TradingView asks invite‑only scripts to explain why their logic is original and why source protection is justified. Smart Impulse PRO does that by:

- Implementing a custom price×volume impulse model based on Z‑score normalisation and integrating it with exits through the breathing TP grid.

- Using a coordinated guard framework that explicitly targets typical crypto issues (late chase entries, overextension vs VWAP/EMA200, volatility squeezes, volume spikes).

- Providing a structured indicator mashup where EMA200, VWAP, ADX, ATR and Anti‑Flat Gate each address different dimensions (trend, volatility, structure) and are designed to work together as a context gate for the impulse signal.

On ETHUSDT, BTCUSDT and a group of other volatile crypto pairs, Smart Impulse PRO showed approximately 90–94% win rate and profit factor above 3.0 in 2023–2025 backtests under default risk and filter settings. These numbers are illustrative only and do not promise or guarantee similar live results.

Risk Disclaimer

Trading cryptocurrencies involves substantial risk. Backtests are hypothetical and assume perfect execution without additional slippage, liquidity constraints or exchange issues. Always test the strategy on your own symbols and timeframes and keep risk per trade at a level you are comfortable with.

FAQ

Q: Does the strategy guarantee profit?

A: No. It is a rule‑based decision engine; all results depend on market conditions, parameters and execution, and backtests do not guarantee future performance.

Q: Can I use it on any crypto pair?

A: The logic is designed for volatile crypto pairs. It has been backtested on ETHUSDT, BTCUSDT and several other majors/alts, but each symbol should be tested and, if needed, re‑tuned by the user.

Q: Which timeframe is best?

A: The engine is intended for intraday and swing charts between 15m and 4h. Lower timeframes will generally produce more signals and more noise; higher ones will produce fewer, slower signals.

Q: Can I disable some filters or guards?

A: Yes. Trend filters, the Anti‑Flat Gate and most exhaustion guards can be turned on or off. It is recommended to change one setting at a time and monitor how it affects blocked signals and the equity curve.

Q: How are alerts meant to be used?

A: Alerts send a JSON payload with side, entry, stop and TP levels via strategy.order.alert_message, so users can connect the strategy to external bots or dashboards if they wish.

***

## Русская версия

Smart Impulse PRO (по приглашению) — Полное руководство для TradingView

Концепция и уникальность

Smart Impulse PRO — стратегия продолжения импульсов, разработанная под волатильные криптовалютные пары . В ней используется пользовательская модель импульса “цена×объём”, нормализованная через Z‑score , после чего такие импульсы проходят фильтрацию по тренду на разных таймфреймах и через каскад гардов, блокирующих слабые и рискованные сетапы (флэт, перетянутость, истощение).

Сводка тестов (крипто‑пары)

Стратегия тестировалась на нескольких волатильных крипто‑парах (перпетуальные контракты, включая ETHUSDT, BTCUSDT и ряд других мейджоров/альтов) на часовом таймфрейме за период 01.01.2023 – 26.12.2025. Типичные значения по этим тестам:

- Количество сделок на пару : ≈100–130

- Диапазон винрейта : ≈ 90–94%

- Диапазон фактора прибыли : ≈ 3.0–3.9

Это результаты тестов на истории по конкретным инструментам и настройкам и не гарантируют такой же доходности в будущем .

Почему она оригинальная

✅ Пользовательская модель импульса цена×объём (Z‑score) : измеряет “редкость” бара в его статистическом окружении, а не просто пересечение стандартных индикаторов

✅ 15+ гардов : системно защищают от догоняния, пампов, торговли в “пиле” и на перетянутых уровнях

✅ “Дышащая” TP‑сетка : цели автоматически подстраиваются под силу текущего импульса |Z|

✅ Прозрачность : пузырьки показывают причины каждого отказа от сделки

✅ Формат по приглашению : логика импульса и взаимодействие гардов публикуются как закрытый скрипт с Invite‑Only доступом, что соответствует правилам TradingView.

***

### 1. Что делает скрипт (для пользователя)

Smart Impulse PRO выступает как движок принятия решений для торговли волатильными крипто‑парами (ETHUSDT, BTCUSDT и др.) на таймфреймах от 15 минут до 4 часов:

- Открывает лонги/шорты только при одновременном совпадении трендовых и импульсных условий.

- Управляет выходом через многоуровневую сетку TP, безубыток, по желанию — трейлинг‑стоп и тайм‑стоп.

- Отображает как реальные сделки , так и отклонённые сигналы с короткой подписью причины блокировки.

Задача — структурировать трендовую торговлю криптой и сделать логику решений максимально понятной.

***

### 2. Как работает скрипт (внутренняя логика)

2.1 Импульсное ядро (кастомная модель на Z‑score)

В основе лежит ряд дельта×объём :

- Сырой импульс:

`delta_impulse = (close - close ) * volume`

- Нормализация по окну N баров (по умолчанию 20):

`zscore = (delta_impulse - среднее(delta_impulse, N)) / стд(delta_impulse, N)`

Бар считается кандидатом на импульс , только если:

- `abs(zscore) > Z_threshold` (по умолчанию 1.5);

- объём выше своей недавней средней.

Это собственная реализация импульсного сигнала цена×объём , нормализованного по Z‑score; выбор входных данных, окна, порогов и связка с гардами и выходами формируют проприетарную часть стратегии.

2.2 Зачем нужен “мэшап” индикаторов (тренд и волатильность)

Комбинация EMA200, VWAP, ADX, ATR и Anti‑Flat Gate собрана так, чтобы каждый компонент покрывал отдельный вид риска:

| Компонент | Что проверяет | Зачем нужен |

|----------|---------------|------------|

| EMA200 | Долгосрочный уклон (цена выше/ниже) | Защита от контртрендовых входов |

| Наклон EMA200 | Наклон за K баров | Отсекает участки со слабым трендом (флэт) |

| VWAP | Удалённость цены от “центра объёма” | Не даёт входить в явной перетянутости от справедливой цены |

| ADX | Силу тренда | Запрещает торговлю в пиле и боковике |

| ATR vs AvgATR50 | Текущую волатильность к средней | Находит режимы сжатия и аномально низкой волатильности |

| ATR% пол (Anti‑Flat Gate) | ATR в % от цены | Жёсткий запрет торговли в очень узком диапазоне |

Импульс может быть сильным, но без нормального тренда и адекватной волатильности сделка не допускается.

2.3 Система гардов (истощение, перетянутость)

- Макс тело/ATR : слишком большая свеча относительно ATR трактуется как возможное окончание движения.

- Макс диапазон/ATR : блокирует экстремальные по размеру бары.

- Фильтры по хвостам :

- Лонги блокируются при доминирующем верхнем хвосте (отторжение сверху).

- Шорты — при доминирующем нижнем хвосте.

- Z‑streak : после серии импульсных баров в одну сторону новые входы по этому направлению отключаются.

- Climax‑объём + пауза : при объёме выше кратности к средней входы на несколько баров ставятся на паузу.

- Дистанционные гарды : чрезмерное удаление цены от EMA200 и VWAP в ATR‑мультипликаторах может блокировать вход.

Эти условия работают совместно с импульсным ядром и трендовыми фильтрами, формируя связанную модель риска.

2.4 Динамическая TP‑сетка

- До 10 тейк‑профитов; шаг — в %, ATR% или гибридный.

- При включённой опции “Breathing grid” шаг между TP увеличивается пропорционально `|zscore|` (в пределах лимита).

- Сильные импульсы → более широкая сетка и шанс забрать длинное движение, слабые → более плотная сетка.

- Профили TP (равный / агрессивный / сбалансированный / защитный) задают распределение объёма между ближними и дальними целями.

- Можно включить перевод стопа в безубыток после TP1 и трейлинг‑стоп по ATR после TP3.

***

### 3. Как использовать стратегию (практика)

3.1 Быстрый старт

1. Откройте график волатильной крипто‑пары (ETHUSDT, BTCUSDT и т.п.) на ТФ 15m–4h и добавьте стратегию.

2. Оставьте настройки по умолчанию и наблюдайте маркеры сделок и пузырьки отклонённых сигналов.

3. Через дашборд смотрите, какие фильтры чаще всего блокируют сделки (ADX, Flat, Exhaust и др.).

4. Если сделок мало, по шагу снижайте порог Z‑score или ADX либо ослабляйте некоторые гарды — всегда меняйте только один параметр за раз.

5. Настройте Max Risk per Trade , размер стопа, количество и профиль TP, а также при необходимости безубыток и трейлинг‑стоп.

3.2 Типовые профили

- Агрессивный скальпинг (15m)

- Z‑порог 1.2

- ADX min 20

- ATR% пол 0.2%

- Несколько гардов истощения отключены.

- Консервативный свинг (1h–4h)

- Z‑порог 1.5

- ADX min 25–30

- ATR% пол 0.3–0.4%

- Все гарды включены, HTF‑фильтры активны.

3.3 Риск и размер позиции

- Max Risk per Trade (%) задаёт долю капитала, которую допускается потерять при полном срабатывании стоп‑лосса.

- Стратегия рассчитывает размер позиции из риска, стопа и цены инструмента.

- Можно включить перевод стопа в безубыток после TP1 и трейлинг‑стоп после TP3.

- Тайм‑стоп закрывает сделки, которые слишком долго остаются открытыми без достижения TP/SL.

3.4 Алерты

Алерты формируют JSON‑строку с направлением, ценой входа, стопом и всеми TP‑уровнями через `strategy.order.alert_message`. Это позволяет подключать внешние боты и панели без раскрытия кода.

***

### 4. Почему скрипт по приглашению (обоснование оригинальности)

Стратегия не сводится к “набору индикаторов на графике”. Формат Invite‑Only обоснован тем, что в коде реализованы:

- Пользовательская модель импульса цена×объём на базе Z‑score и использование этого же сигнала для адаптивной TP‑геометрии.

- Связанный набор гардов , построенный вокруг реальных проблем крипто‑торговли (поздние входы после пампов, перетянутость от VWAP/EMA200, режимы сжатия, всплески объёма).

- Логика мэшапа : EMA200, VWAP, ADX, ATR и Anti‑Flat Gate работают согласованно как фильтр контекста для импульса, а не как независимые визуальные индикаторы.

На ETHUSDT, BTCUSDT и ряде других крипто‑пар Smart Impulse PRO показывала ≈90–94% винрейт и фактор прибыли выше 3.0 в тестах 2023–2025 годов при стандартных настройках фильтров и риска. Эти значения служат иллюстрацией поведения стратегии в прошлом и не являются обещанием аналогичных результатов в реальной торговле.

Предупреждение о рисках

Торговля криптовалютами связана с повышенным риском. Результаты бэктестов гипотетичны и предполагают идеальное исполнение без дополнительного проскальзывания и проблем с ликвидностью. Перед использованием стратегии на реальном счёте протестируйте её на своих инструментах и выбирайте риск на сделку в соответствии с личной толерантностью к убыткам.

FAQ

В: Гарантирует ли стратегия прибыль?

О: Нет. Это набор правил для принятия решений; результат зависит от рынка, настроек и исполнения. Любые бэктесты не гарантируют такую же доходность в будущем.

В: Можно ли использовать её на любой крипто‑паре?

О: Логика рассчитана на волатильные криптовалютные пары. Стратегия тестировалась на ETHUSDT, BTCUSDT и нескольких других мейджорах/альтах, но для каждого инструмента параметры желательно проверить и при необходимости подстроить.

В: Какой таймфрейм предпочтителен?

О: Стратегия рассчитана на внутридневную и свинговую торговлю в диапазоне 15m–4h. На младших ТФ сигналов больше и шума выше; на старших — сигналов меньше, но они формируются медленнее.

В: Можно ли отключать отдельные фильтры и гарды?

О: Можно. Трендовые фильтры, Anti‑Flat Gate и большинство гардов истощения включаются и выключаются отдельно. Рекомендуется менять настройки по одной и смотреть, как это влияет на заблокированные сигналы и кривую капитала.

В: Для чего нужны алерты?

О: Алерты отправляют JSON‑сообщение с направлением, ценой входа, стопом и уровнями TP через strategy.order.alert_message, что позволяет при желании подключать внешних ботов и панели управления риском.

Tiền điện tử

ETH Dynamic Risk Strategy# ETH Dynamic Risk Strategy - Publication Description

## Overview

The ETH Dynamic Risk Strategy is a systematic approach to accumulating Ethereum during bear markets and distributing during bull markets. It combines multiple risk indicators into a single composite metric (0-1 scale) that identifies optimal buying and selling zones based on market conditions.

## Key Features

• **Multi-Component Risk Metric**: Combines 4 weighted indicators to assess market conditions

• **Tiered Buy/Sell System**: 3 levels of buy signals (L1, L2, L3) and 3 levels of sell signals based on risk thresholds

• **Configurable Filters**: Optional buy filters to reduce signal frequency by 30-50%

• **Visual Risk Zones**: Color-coded risk metric plot with clear threshold lines

• **Comprehensive Dashboard**: Real-time statistics including position size, P/L, and component scores

## How It Works

### Risk Components (Configurable Weights)

1. **Log Return from ATH** (Default: 35%)

- Tracks drawdown from all-time high over lookback period

- Deep drawdowns (-70% to -90%) = low risk / buying opportunity

- Near ATH (0% to -20%) = high risk / selling opportunity

2. **ETH/BTC Ratio** (Default: 25%)

- Measures ETH strength relative to Bitcoin

- Below historical average = ETH undervalued = low risk

- Above historical average = ETH overvalued = high risk

3. **Volatility Regime** (Default: 20%)

- Compares current volatility to long-term average

- Compressed volatility at lows = opportunity

- Expanded volatility at highs = danger

4. **Trend Strength** (Default: 20%)

- Uses multiple EMA alignment and slope analysis

- Strong downtrends = low risk scores

- Strong uptrends = high risk scores

### Trading Logic

**Buy Signals:**

- L1: Risk ≤ 0.30 → Buy $100 (default)

- L2: Risk ≤ 0.20 → Buy $250 total

- L3: Risk ≤ 0.10 → Buy $450 total

**Sell Signals (Sequential):**

- L1: Risk ≥ 0.75 → Sell 25% of position

- L2: Risk ≥ 0.85 → Sell 35% of remaining

- L3: Risk ≥ 0.95 → Sell 40% of remaining

**Buy Filters (Optional):**

- Minimum days between buys (prevents clustering)

- Minimum risk drop required (ensures falling risk)

- Toggle on/off to compare performance

## Settings Guide

### Risk Components

Toggle individual components on/off and adjust their weights. Total weight is automatically normalized. Experiment with different combinations to match your market view.

### Advanced Settings

- ATH Lookback: How far back to look for all-time highs (500-2000 recommended)

- Volatility Period: Window for volatility calculations (40-100 recommended)

- ETH/BTC MA Period: Moving average for ratio comparison (100-300 recommended)

- Trend Period: Base period for trend calculations (50-150 recommended)

### Trading Thresholds

Customize buy/sell trigger points and position sizes. Lower buy thresholds = more aggressive accumulation. Higher sell thresholds = holding longer into bull markets.

### Buy Filters

- Enable/disable filtering system

- Min Days Between Buys: Spacing between purchases (1-3 recommended)

- Min Risk Drop: How much risk must fall (-0.001 to -0.01 range)

## Best Practices

• **Timeframe**: Works best on daily (1D) and 3-day (3D) charts

• **Initial Capital**: Set based on your DCA budget (default $10,000)

• **Backtest First**: Test different parameter combinations on historical data

• **Position Sizing**: Adjust buy amounts to match your risk tolerance

• **Monitor Filters**: Check "Filtered Buys" stat to ensure filter isn't too strict

## Use Cases

- Long-term ETH accumulation strategy

- Systematic DCA with market-adaptive buying

- Risk-based portfolio rebalancing

- Educational tool for understanding crypto market cycles

## Disclaimer

This strategy is for educational purposes only. Past performance does not guarantee future results. Cryptocurrency trading involves substantial risk. The strategy uses historical price action and technical indicators which may not predict future movements. Always do your own research and never invest more than you can afford to lose.

## Credits

Strategy concept and development by nakphanan with assistance from Claude AI (Anthropic). Built using Pine Script v5....Mostly from Claude AI!!!

## Version History

v7.0 - Initial release with 4-component risk metric, tiered trading system, and optional buy filters

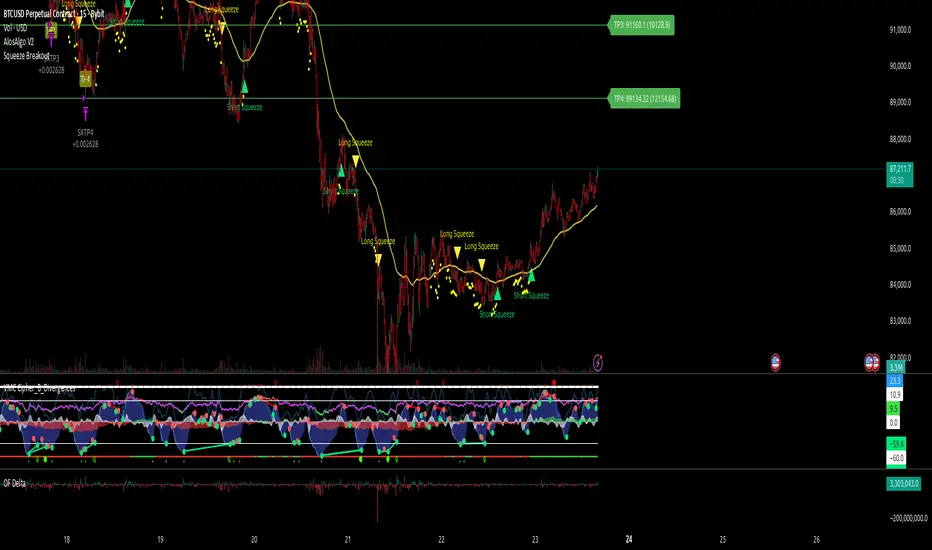

AlosAlgo V2 (BETA)— V2 BETA —

V2 – 2025-11-21 (Update)

• Rebuilt the core signal engine to remove repainting – higher-timeframe Heikin Ashi / Renko now use confirmed bars only for more stable signals & alerts.

• Added Trend Filter MA so longs are only taken above the MA and shorts only below (optional).

• Added MACD momentum filter and Price Action filter (Higher Low for longs, Lower High for shorts) to cut a lot of chop.

• Introduced a loss-streak “circuit breaker” – after X consecutive losing trades the strategy pauses for a set number of bars.

• New TP/SL engine with 2 modes: ATR-based or Fixed % moves, with 4 staged TPs plus an optional runner and break-even SL after TP2.

• Cleaned up TP/SL lines & labels so levels are fixed per trade and easier to read.

• General refactor for more realistic backtests, better live behaviour and easier parameter tuning compared to V1.

ABOUT

AlosAlgo V2 is a multi-timeframe trend + momentum strategy designed for BTC and other high-liquidity markets. It takes directional bias from a higher timeframe, then filters that bias with volatility, momentum and simple price-action structure before it ever opens a trade.

Purely rule-based, no AI / Bayesian / ML.

Core idea

– Use higher-timeframe structure for direction.

– Only trade when trend, momentum and basic price action agree.

– Manage exits with multiple TPs, an optional runner and a hard SL so risk is defined from the start.

Setups

Two main engines:

• Open/Close – Higher-timeframe Heikin Ashi body direction (close vs open) as the core trend signal.

• Renko – ATR-based Renko feed with EMA cross (fast vs slow) as the core trend signal.

Classic sideways filters (ATR + RSI) can be layered on top if you want to only trade in trending or ranging conditions.

Filters added in V2

• Trend Filter MA – Longs only above the MA, shorts only below (length configurable).

• Momentum Filter – Optional MACD filter; only takes longs when MACD is bullish and shorts when MACD is bearish.

• Price Action Filter – Optional HL/LH logic using pivots: longs after a Higher Low, shorts after a Lower High.

• Loss-Streak Circuit Breaker – After N losing trades in a row, the strategy pauses entries for a set number of bars to avoid bad regimes / tilt.

Risk & exits

Two TP/SL modes:

• ATR mode – SL and TP1–TP4 based on ATR at entry (stopFactor / profitFactor).

• Fixed % mode – SL and TP1–TP4 defined as % moves from entry.

On entry the strategy:

• Opens a single position.

• Places 4 staged TPs (TP1–TP4) with user-defined % sizing.

• Optionally leaves a “runner” managed only by SL and trend changes.

• Can move SL to break-even automatically after TP2 (toggle).

All TP/SL levels are locked at entry and drawn on the chart with labels so you can see exactly what the trade is trying to do.

Non-repainting behaviour

V2 is refactored to avoid the repainting behaviour that V1 used. Higher-timeframe and Renko data are taken from confirmed bars only, and entries are based on state (e.g. > / <) instead of repaint-prone crosses. Backtests are much closer to what you’ll see live, and alerts line up with executed trades more reliably.

How to use (suggested defaults)

• Setup: Open/Close

• TPSType: Fixed %

• Trend Filter: ON

• Momentum Filter: ON

• Price Action Filter: ON

• Sideways Filter: No Filtering

Then tweak TP/SL distances and filters per asset + timeframe, and forward-test before sizing up.

Disclaimer

This is not financial advice, not a guarantee of profit and not a “set and forget” money printer. Always forward-test, paper trade and tune risk before using real capital or automation. Markets change – this is a tool, not a promise.

BTC Risk Metric DCA Adapter (3Commas Webhook Strategy)Risk Metric DCA Adapter (3Commas Webhook Strategy) - WORK IN PROGRESS

This Pine Script strategy, originally inspired by the Risk Metric Indicator, is fundamentally engineered as an Adapter to interface with external trading bots like 3Commas via Webhooks. It calculates a dynamic market risk score and translates that score into specific dollar-cost averaging (DCA) entry levels and tiered profit-taking exits.

Key Features & Logic

Risk Metric Calculation (Credit to The Trading Parrot):

The strategy incorporates a complex, multi-timeframe Risk Metric calculation based on daily and weekly moving averages (SMA) and standard deviation (StDev). This metric aims to quantify the current market overextension or compression relative to long-term historical data. The resulting score dictates the level of conviction for a new trade.

Tiered DCA Entry Sizing:

The strategy defines three distinct Buy Levels (L1, L2, L3) corresponding to increasingly favorable (lower) Risk Metric scores.

L1 (Base): Risk is moderate, initiating the minimum defined trade amount.

L2 (Scaled): Risk is low, initiating L1 amount + L2 amount.

L3 (Aggressive): Risk is very low, initiating L1 + L2 + L3 amounts.

Tiered Profit-Taking Exits:

The strategy implements a staggered, partial profit-taking approach based on the Risk Metric rising:

Sell L1 & L2: Closes a percentage of the current position when the Risk Metric reaches defined high thresholds, locking in partial profits.

Sell L3 (Full Exit): Closes the remaining position when the Risk Metric reaches the highest defined threshold.

The Adapter Function (Webhook Integration)

This script is unique because it uses the Pine Script strategy() function to trigger Order Fills, which are necessary to access powerful placeholders in the TradingView alert system.

Trigger Type: The alert must be set to trigger on Any order fill.

Dynamic Webhook Data: Instead of using fixed alert() commands, the strategy generates dynamic labels (e.g., BUY_ENTRY_L3_USD_1000 or SELL_L1_PCT_25) using the strategy.entry and strategy.close commands.

Data Transfer: The alert message then uses the placeholder {{strategy.order.comment}} to pass these dynamic labels to the 3Commas bot, allowing the bot to execute the precise action (e.g., start_deal_with_volume_in_quote_currency or close_deal_at_market_percentage).

Full Strategy Webhook payload

{

"secret": "YOUR_3COMMAS_SECRET_KEY",

"max_lag": "300",

"timestamp": "{{timenow}}",

"trigger_price": "{{close}}",

"tv_exchange": "{{exchange}}",

"tv_instrument": "{{ticker}}",

"action": "{{strategy.order.action}}",

"bot_uuid": "YOUR_BOT_UUID",

"strategy_info": {

"market_position": "{{strategy.market_position}}",

"market_position_size": "{{strategy.market_position_size}}",

"prev_market_position": "{{strategy.prev_market_position}}",

"prev_market_position_size": "{{strategy.prev_market_position_size}}"

},

"order": {

"amount": "{{strategy.order.contracts}}",

"currency_type": "base",

"comment": "{{strategy.order.comment}}"

}

}

Disclaimer: This script is an adapter tool and does not guarantee profit. Trading requires manual configuration of risk settings, bot parameters, and adherence to platform-specific setup instructions.

AlosAlgoAlosAlgo Version: 1 BETA

A multi-timeframe, ATR-driven trend strategy with flexible entry engines (Open/Close vs Renko), optional HTF Heikin Ashi filtering, and a built-in 3-stage take-profit model designed to be backtested on TradingView and automated via webhooks.

EMA Cross + RSI + ADX - Autotrade Strategy V2Overview

A versatile trend-following strategy combining EMA 9/21 crossovers with RSI momentum filtering and optional ADX trend strength confirmation. Designed for both cryptocurrency and traditional futures/options markets with built-in stop loss management and automated position reversals.

Key Features

Multi-Market Compatibility: Works on both crypto futures (Bitcoin, Ethereum) and traditional markets (NIFTY, Bank NIFTY, S&P 500 futures, equity options)

Triple Confirmation System: EMA crossover + RSI filter + ADX strength (optional)

Automated Risk Management: 2% stop loss with wick-touch detection

Position Auto-Reversal: Opposite signals automatically close and reverse positions

Webhook Ready: Six distinct alert messages for automation (Entry Buy/Sell, Close Long/Short, SL Hit Long/Short)

Performance Metrics

NIFTY Futures (15min): 50%+ win rate with ADX filter OFF

Crypto Markets: Requires extensive backtesting before live deployment

Optimal Timeframes: 15-minute to 1-hour charts (patience required for higher timeframes)

Strategy Logic

Entry Signals:

LONG: EMA 9 crosses above EMA 21 + RSI > 55 + ADX > 20 (if enabled)

SHORT: EMA 9 crosses below EMA 21 + RSI < 45 + ADX > 20 (if enabled)

Exit Signals:

Opposite EMA crossover (auto-closes current position)

Stop loss hit at 2% from entry price (tracks candle wicks)

Technical Indicators:

Fast EMA: 9-period (short-term trend)

Slow EMA: 21-period (primary trend)

RSI: 14-period with 55/45 thresholds (momentum confirmation)

ADX: 14-period with 20 threshold (trend strength filter - optional)

Market-Specific Settings

Traditional Markets (NIFTY, Bank NIFTY, S&P Futures, Options)

Recommended Settings:

ADX Filter: Turn OFF (less choppy, cleaner trends)

Timeframe: 15-minute chart

Win Rate: 50%+ on NIFTY Futures

Why No ADX: Traditional markets have more institutional participation and smoother price action, making ADX unnecessary

Cryptocurrency Markets (BTC, ETH, Altcoins)

Recommended Settings:

ADX Filter: Turn ON (ADX > 20)

Timeframe: 15-minute to 1-hour

Extensive backtesting required before live trading

Why ADX: Crypto markets are highly volatile and prone to false breakouts; ADX filters low-quality chop

Best Practices

✅ Backtest thoroughly on your specific instrument and timeframe

✅ Use larger timeframes (1H, 4H) for higher quality signals and better risk/reward

✅ Adjust RSI thresholds based on market volatility (try 52/48 for more signals, 60/40 for fewer but stronger)

✅ Monitor ADX effectiveness - disable for traditional markets, enable for crypto

✅ Proper position sizing - adjust default_qty_value based on your capital and instrument price

✅ Paper trade first - test for 2-4 weeks before risking real capital

Risk Management

Fixed 2% stop loss per trade (adjustable)

Stop loss tracks candle wicks for accurate execution

Positions auto-reverse on opposite signals (no manual intervention needed)

0.075% commission built into backtest (adjust for your broker)

Customization Options

All parameters are adjustable via inputs:

EMA periods (default: 9/21)

RSI length and thresholds (default: 14-period, 55/45 levels)

ADX length and threshold (default: 14-period, 20 threshold)

Stop loss percentage (default: 2%)

Webhook Automation

This strategy includes six distinct alert messages for automated trading:

"Entry Buy" - Long position opened

"Entry Sell" - Short position opened

"Close Long" - Long position closed on opposite crossover

"Close Short" - Short position closed on opposite crossover

"SL Hit Long" - Long stop loss triggered

"SL Hit Short" - Short stop loss triggered

Compatible with Delta Exchange, Binance Futures, 3Commas, Alertatron, and other webhook platforms.

Important Notes

⚠️ Crypto markets require extensive backtesting - volatility patterns differ significantly from traditional markets

⚠️ Higher timeframes = better results - 15min works but 1H/4H provide cleaner signals

⚠️ ADX toggle is critical - OFF for traditional markets, ON for crypto

⚠️ Not financial advice - always conduct your own research and use proper risk management

⚠️ Past performance ≠ future results - backtest results may not reflect live trading conditions

Disclaimer

This strategy is for educational and informational purposes only. Trading futures and options involves substantial risk of loss. Always backtest thoroughly, start with paper trading, and never risk more than you can afford to lose. The author assumes no responsibility for any trading losses incurred using this strategy.

FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion

Components

• Directional Liquidity Pulse DLP. Measures signed participation from body and wick imbalance scaled by normalized volume and variance stabilized

• Volatility Curvature. Second difference of realized volatility from returns highlights expansion or compression

• Impact Efficiency. Price change per unit range and volume boosts gain during efficient moves

• Energy score. Z scores of the above form a single energy that controls the state gain

• One bar projection. Current slope extended by one bar for anticipatory checks

Fusion rule

Weighted sum inside the energy score then logistic mapping to a gain between k min and k max. The state updates toward price plus a small flow push.

Signal rule

• Long suggestion and order when close is below trend and the one bar projection is above the trend

• Short suggestion and flip when close is above trend and the one bar projection is below the trend

• WAIT is implicit when neither condition holds

• In position states end on the opposite condition

What you will see on the chart

• Colored trendline teal for rising red for falling gray for flat

• Optional projection line one bar ahead

• Optional background can be enabled in code

• Alerts on price cross and on slope flips

Inputs with guidance

Setup

• Price source. Close by default

Logic

• Flow window. Typical range 20 to 80. Higher smooths the pulse and reduces flips

• Vol window. Typical range 30 to 120. Higher calms curvature

• Energy window. Typical range 20 to 80. Higher slows regime changes

• Min gain and Max gain. Raise max to react faster. Raise min to keep momentum in chop

UI

• Show 1 bar projection. Colors for up down flat

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• Commission percent 0.03

• Slippage 5

• Default order size method percent of equity value 3%

• Pyramiding 0

• Process orders on close off

• Calc on every tick off

• Recalculate after order is filled off

Realism and responsible publication

• No performance claims

• Intrabar reminder. Shapes can move while a bar forms and settle on close

• Strategy uses standard candles only

Honest limitations and failure modes

• Sudden gaps and thin liquidity can still produce fast flips

• Very quiet regimes reduce contrast. Use larger windows and lower max gain

• Session time uses the exchange time of the chart if you enable any windows later

• Past results never guarantee future outcomes

Open source reuse and credits

• None

Hyper SAR Reactor Trend StrategyHyperSAR Reactor Adaptive PSAR Strategy

Summary

Adaptive Parabolic SAR strategy for liquid stocks, ETFs, futures, and crypto across intraday to daily timeframes. It acts only when an adaptive trail flips and confirmation gates agree. Originality comes from a logistic boost of the SAR acceleration using drift versus ATR, plus ATR hysteresis, inertia on the trail, and a bear-only gate for shorts. Add to a clean chart and run on bar close for conservative alerts.

Scope and intent

• Markets: large cap equities and ETFs, index futures, major FX, liquid crypto

• Timeframes: one minute to daily

• Default demo: BTC on 60 minute

• Purpose: faster yet calmer PSAR that resists chop and improves short discipline

• Limits: this is a strategy that places simulated orders on standard candles

Originality and usefulness

• Novel fusion: PSAR AF is boosted by a logistic function of normalized drift, trail is monotone with inertia, entries use ATR buffers and optional cooldown, shorts are allowed only in a bear bias

• Addresses false flips in low volatility and weak downtrends

• All controls are exposed in Inputs for testability

• Yardstick: ATR normalizes drift so settings port across symbols

• Open source. No links. No solicitation

Method overview

Components

• Adaptive AF: base step plus boost factor times logistic strength

• Trail inertia: one sided blend that keeps the SAR monotone

• Flip hysteresis: price must clear SAR by a buffer times ATR

• Volatility gate: ATR over its mean must exceed a ratio

• Bear bias for shorts: price below EMA of length 91 with negative slope window 54

• Cooldown bars optional after any entry

• Visual SAR smoothing is cosmetic and does not drive orders

Fusion rule

Entry requires the internal flip plus all enabled gates. No weighted scores.

Signal rule

• Long when trend flips up and close is above SAR plus buffer times ATR and gates pass

• Short when trend flips down and close is below SAR minus buffer times ATR and gates pass

• Exit uses SAR as stop and optional ATR take profit per side

Inputs with guidance

Reactor Engine

• Start AF 0.02. Lower slows new trends. Higher reacts quicker

• Max AF 1. Typical 0.2 to 1. Caps acceleration

• Base step 0.04. Typical 0.01 to 0.08. Raises speed in trends

• Strength window 18. Typical 10 to 40. Drift estimation window

• ATR length 16. Typical 10 to 30. Volatility unit

• Strength gain 4.5. Typical 2 to 6. Steepness of logistic

• Strength center 0.45. Typical 0.3 to 0.8. Midpoint of logistic

• Boost factor 0.03. Typical 0.01 to 0.08. Adds to step when strength rises

• AF smoothing 0.50. Typical 0.2 to 0.7. Adds inertia to AF growth

• Trail smoothing 0.35. Typical 0.15 to 0.45. Adds inertia to the trail

• Allow Long, Allow Short toggles

Trade Filters

• Flip confirm buffer ATR 0.50. Typical 0.2 to 0.8. Raise to cut flips

• Cooldown bars after entry 0. Typical 0 to 8. Blocks re entry for N bars

• Vol gate length 30 and Vol gate ratio 1. Raise ratio to trade only in active regimes

• Gate shorts by bear regime ON. Bear bias window 54 and Bias MA length 91 tune strictness

Risk

• TP long ATR 1.0. Set to zero to disable

• TP short ATR 0.0. Set to 0.8 to 1.2 for quicker shorts

Usage recipes

Intraday trend focus

Confirm buffer 0.35 to 0.5. Cooldown 2 to 4. Vol gate ratio 1.1. Shorts gated by bear regime.

Intraday mean reversion focus

Confirm buffer 0.6 to 0.8. Cooldown 4 to 6. Lower boost factor. Leave shorts gated.

Swing continuation

Strength window 24 to 34. ATR length 20 to 30. Confirm buffer 0.4 to 0.6. Use daily or four hour charts.

Properties visible in this publication

Initial capital 10000. Base currency USD. Order size Percent of equity 3. Pyramiding 0. Commission 0.05 percent. Slippage 5 ticks. Process orders on close OFF. Bar magnifier OFF. Recalculate after order filled OFF. Calc on every tick OFF. No security calls.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Shapes can move while a bar forms and settle on close. Strategies execute only on standard candles.

Honest limitations and failure modes

High impact events and thin books can void assumptions. Gap heavy symbols may prefer longer ATR. Very quiet regimes can reduce contrast and invite false flips.

Open source reuse and credits

Public domain building blocks used: PSAR concept and ATR. Implementation and fusion are original. No borrowed code from other authors.

Strategy notice

Orders are simulated on standard candles. No lookahead.

Entries and exits

Long: flip up plus ATR buffer and all gates true

Short: flip down plus ATR buffer and gates true with bear bias when enabled

Exit: SAR stop per side, optional ATR take profit, optional cooldown after entry

Tie handling: stop first if both stop and target could fill in one bar

Crypto Pro Strategy (Entry Model + Risk)Imma try to use this on a prop firm but if you want to use it itss free or im going to try to make it free

Quantum Flux Universal Strategy Summary in one paragraph

Quantum Flux Universal is a regime switching strategy for stocks, ETFs, index futures, major FX pairs, and liquid crypto on intraday and swing timeframes. It helps you act only when the normalized core signal and its guide agree on direction. It is original because the engine fuses three adaptive drivers into the smoothing gains itself. Directional intensity is measured with binary entropy, path efficiency shapes trend quality, and a volatility squash preserves contrast. Add it to a clean chart, watch the polarity lane and background, and trade from positive or negative alignment. For conservative workflows use on bar close in the alert settings when you add alerts in a later version.

Scope and intent

• Markets. Large cap equities and ETFs. Index futures. Major FX pairs. Liquid crypto

• Timeframes. One minute to daily

• Default demo used in the publication. QQQ on one hour

• Purpose. Provide a robust and portable way to detect when momentum and confirmation align, while dampening chop and preserving turns

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique concept or fusion. The novelty sits in the gain map. Instead of gating separate indicators, the model mixes three drivers into the adaptive gains that power two one pole filters. Directional entropy measures how one sided recent movement has been. Kaufman style path efficiency scores how direct the path has been. A volatility squash stabilizes step size. The drivers are blended into the gains with visible inputs for strength, windows, and clamps.

• What failure mode it addresses. False starts in chop and whipsaw after fast spikes. Efficiency and the squash reduce over reaction in noise.

• Testability. Every component has an input. You can lengthen or shorten each window and change the normalization mode. The polarity plot and background provide a direct readout of state.

• Portable yardstick. The core is normalized with three options. Z score, percent rank mapped to a symmetric range, and MAD based Z score. Clamp bounds define the effective unit so context transfers across symbols.

Method overview in plain language

The strategy computes two smoothed tracks from the chart price source. The fast track and the slow track use gains that are not fixed. Each gain is modulated by three drivers. A driver for directional intensity, a driver for path efficiency, and a driver for volatility. The difference between the fast and the slow tracks forms the raw flux. A small phase assist reduces lag by subtracting a portion of the delayed value. The flux is then normalized. A guide line is an EMA of a small lead on the flux. When the flux and its guide are both above zero, the polarity is positive. When both are below zero, the polarity is negative. Polarity changes create the trade direction.

Base measures

• Return basis. The step is the change in the chosen price source. Its absolute value feeds the volatility estimate. Mean absolute step over the window gives a stable scale.

• Efficiency basis. The ratio of net move to the sum of absolute step over the window gives a value between zero and one. High values mean trend quality. Low values mean chop.

• Intensity basis. The fraction of up moves over the window plugs into binary entropy. Intensity is one minus entropy, which maps to zero in uncertainty and one in very one sided moves.

Components

• Directional Intensity. Measures how one sided recent bars have been. Smoothed with RMA. More intensity increases the gain and makes the fast and slow tracks react sooner.

• Path Efficiency. Measures the straightness of the price path. A gamma input shapes the curve so you can make trend quality count more or less. Higher efficiency lifts the gain in clean trends.

• Volatility Squash. Normalizes the absolute step with Z score then pushes it through an arctangent squash. This caps the effect of spikes so they do not dominate the response.

• Normalizer. Three modes. Z score for familiar units, percent rank for a robust monotone map to a symmetric range, and MAD based Z for outlier resistance.

• Guide Line. EMA of the flux with a small lead term that counteracts lag without heavy overshoot.

Fusion rule

• Weighted sum of the three drivers with fixed weights visible in the code comments. Intensity has fifty percent weight. Efficiency thirty percent. Volatility twenty percent.

• The blend power input scales the driver mix. Zero means fixed spans. One means full driver control.

• Minimum and maximum gain clamps bound the adaptive gain. This protects stability in quiet or violent regimes.

Signal rule

• Long suggestion appears when flux and guide are both above zero. That sets polarity to plus one.

• Short suggestion appears when flux and guide are both below zero. That sets polarity to minus one.

• When polarity flips from plus to minus, the strategy closes any long and enters a short.

• When flux crosses above the guide, the strategy closes any short.

What you will see on the chart

• White polarity plot around the zero line

• A dotted reference line at zero named Zen

• Green background tint for positive polarity and red background tint for negative polarity

• Strategy long and short markers placed by the TradingView engine at entry and at close conditions

• No table in this version to keep the visual clean and portable

Inputs with guidance

Setup

• Price source. Default ohlc4. Stable for noisy symbols.

• Fast span. Typical range 6 to 24. Raising it slows the fast track and can reduce churn. Lowering it makes entries more reactive.

• Slow span. Typical range 20 to 60. Raising it lengthens the baseline horizon. Lowering it brings the slow track closer to price.

Logic

• Guide span. Typical range 4 to 12. A small guide smooths without eating turns.

• Blend power. Typical range 0.25 to 0.85. Raising it lets the drivers modulate gains more. Lowering it pushes behavior toward fixed EMA style smoothing.

• Vol window. Typical range 20 to 80. Larger values calm the volatility driver. Smaller values adapt faster in intraday work.

• Efficiency window. Typical range 10 to 60. Larger values focus on smoother trends. Smaller values react faster but accept more noise.

• Efficiency gamma. Typical range 0.8 to 2.0. Above one increases contrast between clean trends and chop. Below one flattens the curve.

• Min alpha multiplier. Typical range 0.30 to 0.80. Lower values increase smoothing when the mix is weak.

• Max alpha multiplier. Typical range 1.2 to 3.0. Higher values shorten smoothing when the mix is strong.

• Normalization window. Typical range 100 to 300. Larger values reduce drift in the baseline.

• Normalization mode. Z score, percent rank, or MAD Z. Use MAD Z for outlier heavy symbols.

• Clamp level. Typical range 2.0 to 4.0. Lower clamps reduce the influence of extreme runs.

Filters

• Efficiency filter is implicit in the gain map. Raising efficiency gamma and the efficiency window increases the preference for clean trends.

• Micro versus macro relation is handled by the fast and slow spans. Increase separation for swing, reduce for scalping.

• Location filter is not included in v1.0. If you need distance gates from a reference such as VWAP or a moving mean, add them before publication of a new version.

Alerts

• This version does not include alertcondition lines to keep the core minimal. If you prefer alerts, add names Long Polarity Up, Short Polarity Down, Exit Short on Flux Cross Up in a later version and select on bar close for conservative workflows.

Strategy has been currently adapted for the QQQ asset with 30/60min timeframe.

For other assets may require new optimization

Properties visible in this publication

• Initial capital 25000

• Base currency Default

• Default order size method percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Honest limitations and failure modes

• Past results do not guarantee future outcomes

• Economic releases, circuit breakers, and thin books can break the assumptions behind intensity and efficiency

• Gap heavy symbols may benefit from the MAD Z normalization

• Very quiet regimes can reduce signal contrast. Use longer windows or higher guide span to stabilize context

• Session time is the exchange time of the chart

• If both stop and target can be hit in one bar, tie handling would matter. This strategy has no fixed stops or targets. It uses polarity flips for exits. If you add stops later, declare the preference

Open source reuse and credits

• None beyond public domain building blocks and Pine built ins such as EMA, SMA, standard deviation, RMA, and percent rank

• Method and fusion are original in construction and disclosure

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Strategy add on block

Strategy notice

Orders are simulated by the TradingView engine on standard candles. No request.security() calls are used.

Entries and exits

• Entry logic. Enter long when both the normalized flux and its guide line are above zero. Enter short when both are below zero

• Exit logic. When polarity flips from plus to minus, close any long and open a short. When the flux crosses above the guide line, close any short

• Risk model. No initial stop or target in v1.0. The model is a regime flipper. You can add a stop or trail in later versions if needed

• Tie handling. Not applicable in this version because there are no fixed stops or targets

Position sizing

• Percent of equity in the Properties panel. Five percent is the default for examples. Risk per trade should not exceed five to ten percent of equity. One to two percent is a common choice

Properties used on the published chart

• Initial capital 25000

• Base currency Default

• Default order size percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Dataset and sample size

• Test window Jan 2, 2014 to Oct 16, 2025 on QQQ one hour

• Trade count in sample 324 on the example chart

Release notes template for future updates

Version 1.1.

• Add alertcondition lines for long, short, and exit short

• Add optional table with component readouts

• Add optional stop model with a distance unit expressed as ATR or a percent of price

Notes. Backward compatibility Yes. Inputs migrated Yes.

Universal Regime Alpha Thermocline StrategyCurrents settings adapted for BTCUSD Daily timeframe

This description is written to comply with TradingView House Rules and Script Publishing Rules. It is self contained, in English first, free of advertising, and explains originality, method, use, defaults, and limitations. No external links are included. Nothing here is investment advice.

0. Publication mode and rationale

This script is published as Protected . Anyone can add and test it from the Public Library, yet the source code is not visible.

Why Protected

The engine combines three independent lenses into one regime score and then uses an adaptive centering layer and a thermo risk unit that share a common AAR measure. The exact mapping and interactions are the result of original research and extensive validation. Keeping the implementation protected preserves that work and avoids low effort clones that would fragment feedback and confuse users.

Protection supports a single maintained build for users. It reduces accidental misuse of internal functions outside their intended context which might lead to misleading results.

1. What the strategy does in one paragraph

Universal Regime Alpha Thermocline builds a single number between zero and one that answers a practical question for any market and timeframe. How aligned is current price action with a persistent directional regime right now. To answer this the script fuses three views of the tape. Directional entropy of up versus down closes to measure unanimity.

Convexity drift that rewards true geometric compounding and penalizes drag that comes from chop where arithmetic pace is high but growth is poor.

Tail imbalance that counts decisive bursts in one direction relative to typical bar amplitude. The three channels are blended, optionally confirmed by a higher timeframe, and then adaptively centered to remove local bias. Entries fire when the score clears an entry gate. Exits occur when the score mean reverts below an exit gate or when thermo stops remove risk. Position size can scale with the certainty of the signal.

2. Why it is original and useful

It mixes orthogonal evidence instead of leaning on a single family of tools. Many regime filters depend on moving averages or volatility compression. Here we add an information view from entropy, a growth view from geometric drift, and a structural view from tail imbalance.

The drift channel separates growth from speed. Arithmetic pace can look strong in whipsaw, yet geometric growth stays weak. The engine measures both and subtracts drag so that only sequences with compounding quality rise.

Tail counting is anchored to AAR which is the average absolute return of bars in the window. This makes the threshold self scaling and portable across symbols and timeframes without hand tuned constants.

Adaptive centering prevents the score from living above or below neutral for long stretches on assets with strong skew. It recovers neutrality while still allowing persistent regimes to dominate once evidence accumulates.

The same AAR unit used in the signal also sets stop distance and trail distance. Signal and risk speak the same language which makes the method portable and easier to reason about.

3. Plain language overview of the math

Log returns . The base series is r equal to the natural log of close divided by the previous close. Log return allows clean aggregation and makes growth comparisons natural.

Directional entropy . Inside the lookback we compute the proportion p of bars where r is positive. Binary entropy of p is high when the mix of up and down closes is balanced and low when one direction dominates. Intensity is one minus entropy. Directional sign is two times p minus one. The trend channel is zero point five plus one half times sign times intensity. It lives between zero and one and grows stronger as unanimity increases.

Convexity drift with drag . Arithmetic mean of r measures pace. Geometric mean of the price ratio over the window measures compounding. Drag is the positive part of arithmetic minus geometric. Drift raw equals geometric minus drag multiplier times drag. We then map drift through an arctangent normalizer scaled by AAR and a nonlinearity parameter so the result is stable and remains between zero and one.

Tail imbalance . AAR equals the average of the absolute value of r in the window. We count up tails where r is greater than aar_mult times AAR and down tails where r is less than minus aar_mult times AAR. The imbalance is their difference over their total, mapped to zero to one. This detects directional impulse flow.

Fusion and centering . A weighted average of the three channels yields the raw score. If a higher timeframe is requested, the same function is executed on that timeframe with lookahead off and blended with a weight. Finally we subtract a fraction of the rolling mean of the score to recover neutrality. The result is clipped to the zero to one band.

4. Entries, exits, and position sizing

Enter long when score is strictly greater than the entry gate. Enter short when score is strictly less than one minus the entry gate unless direction is restricted in inputs.

Exit a long when score falls below the exit gate. Exit a short when score rises above one minus the exit gate.

Thermo stops are expressed in AAR units. A long uses the maximum of an initial stop sized by the entry price and AAR and a trail stop that references the running high since entry with a separate multiple. Shorts mirror this with the running low. If the trail is disabled the initial stop is active.

Cooldown is a simple bar counter that begins when the position returns to flat. It prevents immediate re entry in churn.

Dynamic position size is optional. When enabled the order percent of equity scales between a floor and a cap as the score rises above the gate for longs or below the symmetric gate for shorts.

5. Inputs quick guide with recommended ranges

Every input has a tooltip in the script. The same guidance appears here for fast reading.

Core window . Shared lookback for entropy, drift, and tails. Start near 80 on daily charts. Try 60 to 120 on intraday and 80 to 200 for swing.

Entry threshold . Typical range 0.55 to 0.65 for trend following. Faster entries 0.50 to 0.55.

Exit threshold . Typical range 0.35 to 0.50. Lower holds longer yet gives back more.

Weight directional entropy . Starting value 0.40. Raise on markets with clean persistence.

Weight convexity drift . Starting value 0.40. Raise when compounding quality is critical.

Weight tail imbalance . Starting value 0.20. Raise on breakout prone markets.

Tail threshold vs AAR . Typical range 1.0 to 1.5 to count decisive bursts.

Drag penalty . Typical range 0.25 to 0.75. Higher punishes chop more.

Nonlinearity scale . Typical range 0.8 to 2.0. Larger compresses extremes.

AAR floor in percent . Typical range 0.0005 to 0.002 for liquid instruments. This stabilizes the math during quiet regimes.

Adaptive centering . Keep on for most symbols. Center strength 0.40 to 0.70.

Confirm timeframe optional . Leave empty to disable. If used, try a multiple between three and five of the chart timeframe with a blend weight near 0.20.

Dynamic position size . Enable if you want size to reflect certainty. Floor and cap define the percent of equity band. A practical band for many accounts is 0.5 to 2.

Cooldown bars after exit . Start at 3 on daily or slightly higher on shorter charts.

Thermo stop multiple . Start between 1.5 and 3.0 on daily. Adjust to your tolerance and symbol behavior.

Thermo trailing stop and Trail multiple . Trail on locks gains earlier. A trail multiple near 1.0 to 2.0 is common. You can keep trail off and let the exit gate handle exits.

Background heat opacity . Cosmetic. Set to taste. Zero disables it.

6. Properties used on the published chart

The example publication uses BTCUSD on the daily timeframe. The following Properties and inputs are used so everyone can reproduce the same results.

Initial capital 100000

Base currency USD

Order size 2 percent of equity coming from our risk management inputs.

Pyramiding 0

Commission 0.05 percent

Slippage 10 ticks in the publication for clarity. Users should introduce slippage in their own research.

Recalculate after order is filled off. On every tick off.

Using bar magnifier on. On bar close on.

Risk inputs on the published chart. Dynamic position size on. Size floor percent 2. Size cap percent 2. Cooldown bars after exit 3. Thermo stop multiple 2.5. Thermo trailing stop off. Trail multiple 1.

7. Visual elements and alerts

The score is painted as a subtle dot rail near the bottom. A background heat map runs from red to green to convey regime strength at a glance. A compact HUD at the top right shows current score, the three component channels, the active AAR, and the remaining cooldown. Four alerts are included. Long Setup and Short Setup on entry gates. Exit Long by Score and Exit Short by Score on exit gates. You can disable trading and use alerts only if you want the score as a risk switch inside a discretionary plan.

8. How to reproduce the example

Open a BTCUSD daily chart with regular candles.

Add the strategy and load the defaults that match the values above.

Set Properties as listed in section 6.(they are set by default) Confirm that bar magnifier is on and process on bar close is on.

Run the Strategy Tester. Confirm that the trade count is reasonable for the sample. If the count is too low, slightly lower the entry threshold or extend history. If the count is excessively high, raise the threshold or add a small cooldown.

9. Practical tuning recipes

Trend following focus . Raise the entry threshold toward 0.60. Raise the trend weight to 0.50 and reduce tail weight to 0.15. Keep drift near 0.35 to retain the growth filter. Consider leaving the trail off and let the exit threshold manage positions.

Breakout focus . Keep entry near 0.55. Raise tail weight to 0.35. Keep aar_mult near 1.3 so only decisive bursts count. A modest cooldown near 5 can reduce immediate false flips after the first burst bar.

Chop defense . Raise drag multiplier to 0.70. Raise exit threshold toward 0.48 to recycle capital earlier. Consider a higher cooldown, for example 8 to 12 on intraday.

Higher timeframe blend . On a daily chart try a weekly confirm with a blend near 0.20. On a five minute chart try a fifteen minute confirm. This moderates transitions.

Sizing discipline . If you want constant position size, set floor equal to cap. If you want certainty scaling, set a band like 0.5 to 2 and monitor drawdown behavior before widening it.

10. Strengths and limitations

Strengths

Self scaling unit through AAR makes the tool portable across markets and timeframes.

Blends evidence that target different failure modes. Unanimity, growth quality, and impulse flow rarely agree by chance which raises confidence when they align.

Adaptive centering reduces structural bias at the score level which helps during regime flips.

Limitations

In very quiet regimes AAR becomes small even with a floor. If your symbol is thin or gap prone, raise the floor a little to keep stops and drift mapping stable.

Adaptive centering can delay early breakout acceptance. If you miss starts, lower center strength or temporarily disable centering while you evaluate.

Tail counting uses a fixed multiple of AAR. If a market alternates between very calm and very violent weeks, a single aar_mult may not capture both extremes. Sweep this parameter in research.

The engine reacts to realized structure. It does not anticipate scheduled news or liquidity shocks. Use event awareness if you trade around releases.

11. Realism and responsible publication

No promises or projections of performance are made. Past results never guarantee future outcomes.

Commission is set to 0.05 percent per round which is realistic for many crypto venues. Adjust to your own broker or exchange.

Slippage is set at 10 in the publication . Introduce slippage in your own tests or use a percent model.

Position size should respect sustainable risk envelopes. Risking more than five to ten percent per trade is rarely viable. The example uses a fixed two percent position size.

Security calls use lookahead off. Standard candles only. Non standard chart types like Heikin Ashi or Renko are not supported for strategies that submit orders.

12. Suggested research workflow

Begin with the balanced defaults. Confirm that the trade count is sensible for your timeframe and symbol. As a rough guide, aim for at least one hundred trades across a wide sample for statistical comfort. If your timeframe cannot produce that count, complement with multiple symbols or run longer history.

Sweep entry and exit thresholds on a small grid and observe stability. Stability across windows matters more than the single best value.

Try one higher timeframe blend with a modest weight. Large weights can drown the signal.

Vary aar_mult and drag_mult together. This tunes the aggression of breakouts versus defense in chop.

Evaluate whether dynamic size improves risk adjusted results for your style. If not, set floor equal to cap for constancy.

Walk forward through disjoint segments and inspect results by regime. Bootstrapping or segmented evaluation can reveal sensitivity to specific periods.

13. How to read the HUD and heat map

The HUD presents a compact view. Score is the current fused value. Trend is the directional entropy channel. Drift is the compounding quality channel. Tail is the burst flow channel. AAR is the current unit that scales stops and the drift map. CD is the cooldown counter. The background heat is a visual aid only. It can be disabled in inputs. Green zones near the upper band show alignment among the channels. Muted colors near the mid band show uncertainty.

14. Frequently asked questions

Can I use this as a pure indicator . Yes. Disable entries by restricting direction to one side you will not trade and use the alerts as a regime switch.

Will it work on intraday charts . Yes. The AAR unit scales with bar size. You will likely reduce the core window and increase cooldown slightly.

Should I enable the adaptive trail . If you wish to lock gains sooner and accept more exits, enable it. If you prefer to let the exit gate do the heavy lifting, keep it off.

Why do I sometimes see a green background without a position . Heat expresses the score. A position also depends on threshold comparisons, direction mode, and cooldown.

Why is Order size set to one hundred percent if dynamic size is on . The script passes an explicit quantity percent on each entry. That explicit quantity overrides the property. The property is kept at one hundred percent to avoid confusion when users later disable dynamic sizing.

Can I combine this with other tools on my chart . You can, yet for publication the chart is kept clean so users and moderators can see the output clearly. In your private workspace feel free to add other context.

15. Concepts glossary

AAR . Average absolute return across the lookback. Serves as a unit for tails, drift scaling, and stops.

Directional entropy . A measure of uncertainty of up versus down closes. Low entropy paired with a directional sign signals unanimity.

Geometric mean growth . Rate that preserves the effect of compounding over many bars.

Drag . The positive difference between arithmetic pace and geometric growth. Larger drag often signals churn that looks active but fails to compound.

Thermo stops . Stops expressed in the same AAR unit as the signal. They adapt with volatility and keep risk and signal on a common scale.

Adaptive centering . A bias correction that recenters the fused score around neutral so the meter does not drift due to persistent skew.

16. Educational notice and risk statement

Markets involve risk. This publication is for education and research. It does not provide financial advice and it is not a recommendation to buy or sell any instrument. Use realistic costs. Validate ideas with out of sample testing and with conservative position sizing. Past performance never guarantees future results.

17. Final notes for readers and moderators

The goal of this strategy is clarity and portability. Clarity comes from a single score that reflects three independent features of the tape. Portability comes from self scaling units that respect structure across assets and timeframes. The publication keeps the chart clean, explains the math plainly, lists defaults and Properties used, and includes warnings where care is required. The code is protected so the implementation remains consistent for the community while the description remains complete enough for users to understand its purpose and for moderators to evaluate originality and usefulness. If you explore variants, keep them self contained, explain exactly what they contribute, publish in English first, and treat others with respect in the comments.

Load the strategy on BTCUSD daily with the defaults listed above and study how the score transitions across regimes. Then adjust one lever at a time. Observe how the trend channel, the drift channel, and the tail channel interact during starts, pauses, and reversals. Use the alerts as a risk switch inside your own process or let the built in entries and exits run if you prefer an automated study. The intent is not to promise outcomes. The intent is to give you a robust meter for regime strength that travels well across markets and helps you structure decisions with more confidence.

Thank you for your time to read all of this

AlgoAIDESIGNED FOR HEIKEN ASHI BARS

Gain Access here: algoai.store

AlgoAI

The Dark Edge of Trading

An AI-powered TradingView strategy that thrives across all markets. Short altcoin pumps. Ride NAS100 waves. Dominate gold, FX, stocks, and futures — all with one AI brain.

#1

Semi-Automatic Trading (Recommended)

Set up alerts on AlgoAI signals. As they come in, grade the setups and choose to enter manually. This gives you full control while leveraging AI precision.

#2

Fully Automated Trading

Pass signals via webhooks to TradersPost for futures or PineConnector for FX. Note: When running fully automated, it's suggested to use long-only or short-only mode to avoid side swiping and potential unintended drawdown.

BITSTAMP:BTCUSD