NSE Bullish Swing Strategy - 7-8% TargetHelps capture bullish swing trading set ups ( PULL BACK , BREAKOUT & MOMENTUM ) and achieve 7-8 % profit in minimum possible time. Also scans the trend continuously & gives the strength of the trend. Use in daily time frame.

Only for educational use.

Educational

VWolf – Slope GuardOVERVIEW

Slope Guard combines a momentum core (WaveTrend + RSI/MFI + QQE family) with a directional bias (EMA/DEMA and a DEMA-slope filter). Trade direction can be constrained by the Supertrend regime (Normal or Pivot). Risk is managed with ATR-based stops and targets, optional Supertrend-anchored dynamic levels, and a two-stage take-profit that can shift the stop to break-even after the first partial. The strategy supports explicit Backtest and Forward-test windows and adapts certain thresholds by market type (Forex vs. Stocks).

RECOMMENDED USE

Markets: Forex and equities; use Market Type to properly scale the DEMA-slope gate.

Timeframes: M15–H4 for intraday-swing and H1–D1 for slower swing; avoid ultra-low TFs without tightening ADX/QQE.

Assets: Instruments with persistent trends and orderly pullbacks; avoid flat ranges without sufficient ADX.

Strengths

Multi-layer confluence: trend bias + momentum + regime + strength.

Flexible risk engine: ATR vs. Supertrend anchoring, staged exits, and automatic break-even.

Clean research workflow: separated Backtest and Forward-test windows.

Precautions

Structural latency: Pivot-based constructs confirm with delay; validate with Forward-test.

Filter interaction: QQE Strict + ADX + WT zero-line can become overly selective; calibrate by asset/TF.

Overfitting risk: Prefer simple, portable parameter sets and validate across symbols/TFs.

CONCLUSION

Slope Guard is a “trend + momentum” framework with risk control at its core. By enforcing a baseline bias, validating momentum with the Vuman composite, and offering ATR or Supertrend-anchored exits—plus staged profits and break-even shifts—it seeks to capture the core of directional swings while compressing drawdowns. Keep testing windows isolated, start with moderate filters (QQE Normal, ADX ~20–25), and only add stricter gates (WT zero-line, DEMA slope) once they demonstrably improve stability without starving signals.

FOR MORE INFORMATION VISIT vwolftrading.com

VWolf - Shadow PulseOVERVIEW

The Trend Momentum Breakout Strategy is a rule-based trading system designed to identify high-probability entries in trending markets using a combination of trend confirmation, momentum filtering, and precise trigger conditions. The strategy is suitable for intermediate to advanced traders who prefer mechanical systems with clear entry/exit logic and configurable risk management options.

At its core, this strategy seeks to enter pullbacks within strong trends, capitalizing on momentum continuation after brief pauses in price movement. By integrating multiple moving averages (MAs) for trend validation, ADX (Average Directional Index) as a strength filter, and Stochastic RSI as an entry trigger, the strategy filters out weak trends and avoids overextended market conditions. Exit logic is based on a customizable fixed stop-loss (SL) and take-profit (TP) framework, with optional dynamic risk-reduction mechanisms powered by the Supertrend indicator.

This strategy is designed to perform best in clearly trending markets and is especially effective in avoiding false breakouts or choppy sideways action thanks to its ADX-based filtering. It can be deployed across a variety of asset classes, including forex, stocks, cryptocurrencies, and indices, and is optimized for intra-day to swing trading timeframes.

RECOMMENDED USE

This strategy is designed to be flexible across multiple markets, but it performs best under certain conditions:

Best Suited For:

Trending markets with clear directional momentum.

High-volume instruments that avoid erratic price action.

Assets with intraday volatility and swing patterns.

Recommended Asset Classes:

Forex pairs (e.g., EUR/USD, GBP/JPY)

Cryptocurrencies (e.g., BTC/USD, ETH/USDT)

Major indices (e.g., S&P 500, NASDAQ, DAX)

Large-cap stocks (especially those with consistent liquidity)

Suggested Timeframes:

15-minute to 1-hour charts for intraday setups.

4-hour and daily charts for swing trading.

Lower timeframes (1–5 min) may generate too much noise unless fine-tuned.

Market Conditions to Avoid:

Ranging or sideways markets with low ADX values.

Assets with irregular price structures or low liquidity.

News-heavy periods with unpredictable price spikes.

CONCLUSION

This strategy stands out for its robust and modular approach to trend-following trading, offering a high level of customization while maintaining clear logic and structural discipline in entries and exits. By combining three distinct layers of confirmation—trend identification (via configurable moving averages), trend strength validation (via the DMI filter), and timing (via the Stochastic RSI trigger)—it aims to reduce noise and increase the probability of entering trades with directional bias and momentum on its side.

Its flexibility is one of its strongest points: users can tailor the strategy to fit various trading styles and market conditions. Whether the trader prefers conservative setups using only the slowest moving average, or more aggressive entries requiring full alignment of fast, medium, and slow MAs, the system adjusts accordingly. Likewise, exit management offers both static and dynamic methods—such as ATR-based stop losses, Supertrend-based adaptive exits, and partial profit-taking mechanisms—allowing risk to be managed with precision.

This makes the strategy particularly suitable for trend-driven markets, such as major currency pairs, indices, or volatile stocks that demonstrate clear directional moves. It is not ideal for sideways or choppy markets, where multiple filters may reduce the number of trades or result in whipsaws.

From a practical standpoint, the strategy also incorporates real-world trading mechanics, like time-based filters and account risk control, which elevate it from a purely theoretical model to a more execution-ready system.

In summary, this is a well-structured, modular trend strategy ideal for intermediate to advanced traders who want to maintain control over their system parameters while still benefiting from layered signal confirmation. With proper calibration, it has the potential to become a reliable tool in any trader’s arsenal—particularly in markets where trends emerge clearly and sustainably.

FOR MORE INFORMATION VISIT vwolftrading.com

VWolf - Raptor ClawOVERVIEW

The 'VWolf - Raptor Claw' is a straightforward scalping strategy designed for high-frequency trades based on the Stochastic RSI indicator. It focuses exclusively on identifying potential trend reversals through stochastic cross signals in extreme zones, without the need for additional confirmations. This makes it highly responsive to market movements, capturing rapid price shifts while maintaining simplicity.

This strategy is best suited for highly liquid and volatile markets like forex, indices, and major cryptocurrencies, where quick momentum shifts are common. It is ideal for experienced scalpers who prioritize fast entries and exits, but it can also be adapted for swing trading in lower timeframes.

Entry Conditions:

Long Entry:Stochastic RSI crosses above the oversold threshold (typically 20), indicating a potential bullish reversal.

Short Entry:Stochastic RSI crosses below the overbought threshold (typically 80), indicating a potential bearish reversal.

Exit Conditions:

Stop Loss: Set at the minimum (for longs) or maximum (for shorts) within a configurable lookback window to reduce risk.

Take Profit: Defined by a risk-reward ratio (RRR) input to optimize potential gains relative to risk.

CONCLUSION

The 'VWolf - Raptor Claw' strategy is perfect for traders seeking a simple yet aggressive approach to the markets. It capitalizes on sharp momentum shifts in extreme zones, relying on precise stop loss and take profit settings to capture rapid profits while minimizing risk. This approach is highly effective in high-volatility environments where quick decision-making is essential.

FOR MORE INFORMATION VISIT vwolftrading.com

VWolf - Quantum DriftOVERVIEW

The Quantum Drift strategy is a sophisticated, highly customizable trading approach designed to identify market entries and exits by leveraging multiple technical indicators. The strategy uniquely combines the Dynamic Exponential Moving Average (DEMA), QQE indicators, Volume Oscillator, and Hull Moving Average (HULL), enabling precise detection of trend direction, momentum shifts, and volatility adjustments. It stands out due to its adaptability across different market conditions by allowing significant user customization through various input parameters.

RECOMMENDED USE

Markets: Ideal for Forex and Stocks due to the strategy's volatility-sensitive and trend-following nature.

Timeframes: Best suited for medium to higher timeframes (15m, 1H, 4H), where clearer trend signals and less noise occur, enhancing strategy reliability.

CONCLUSION

The Quantum Drift strategy is tailored for intermediate to advanced traders seeking a versatile and adaptive system. Its strength lies in combining momentum, volatility, and trend-following components, providing robust entry and exit signals. However, its effectiveness relies significantly on accurate parameter tuning by traders familiar with the underlying indicators and market behavior.

FOR MORE INFORMATION VISIT vwolftrading.com

VWolf – Pivot VumanSkewOVERVIEW

This strategy blends a lightweight trend scaffold (EMA/DEMA) with a skew-of-volatility filter and VuManchu/WaveTrend momentum signals. It’s designed to participate only when trending structure, momentum alignment, and volatility asymmetry converge, while delegating execution management to either a standard SuperTrend or a Pivot-based SuperTrend. Position sizing is risk‑based, with optional two‑step profit taking and automatic stop movement once price confirms in favor.

RECOMMENDED USE

Markets: Designed for Forex and equities, and readily adaptable to indices or liquid futures.

Timeframes: Performs best from 15m to 4h where momentum and trend layers both matter; daily can be used for confirmation/context.

Conditions: Trending or range‑expansion phases with clear volatility asymmetry. Avoid extremely compressed sessions unless thresholds are relaxed.

Strengths

Multi‑layer confluence (trend + skew + momentum) reduces random signals.

Dual SuperTrend modes provide flexible trailing and regime control.

Built‑in hygiene (ADX/DMI, lockout after loss, ATR gap) curbs over‑trading.

Risk‑% sizing and two‑step exits support consistent, plan‑driven execution.

Precautions

Over‑tight thresholds can lead to missed opportunities; start from defaults and tune gradually.

High sensitivity in momentum settings may overfit to a single instrument/timeframe.

In very low volatility, ATR‑gap or skew filters may block entries—consider adaptive thresholds.

CONCLUSION

VWolf – Pivot VumanSkew is a disciplined trend‑participation strategy that waits for directional structure, volatility asymmetry, and synchronized momentum before acting. Its execution layer—selectable between Normal and Pivot SuperTrend—keeps management pragmatic: scale out early when appropriate, trail intelligently, and defend capital with volatility‑aware stops. For users building a diversified playbook, Pivot VumanSkew serves as a trend‑continuation workhorse that can be tightened for precision or relaxed for higher participation depending on the market’s rhythm.

VWolf – Momentum TwinOVERVIEW

VWolf – Momentum Twin is designed to identify high-probability momentum reversals emerging from overbought or oversold market conditions. It employs a double confirmation from the Stochastic RSI oscillator, optionally filtered by trend and directional movement conditions, before executing trades.

The strategy emphasizes consistent risk management by scaling stop-loss and take-profit targets according to market volatility (ATR), and it provides advanced position management features such as partial profit-taking and automated stop-loss adjustments.

RECOMMENDED USE

Markets: Major FX pairs, index futures, large-cap stocks, and top-volume cryptocurrencies.

Timeframes: Best suited for M15–H4; adaptable for swing trading on daily charts.

Trader Profile: Traders who value structured, volatility-adjusted momentum reversal setups.

Strengths:

Double confirmation filters out many false signals.

Multiple filter options allow strategic flexibility.

ATR scaling maintains consistent risk across assets.

Trade management tools improve adaptability in dynamic markets.

Precautions:

May produce fewer trades in strong one-direction trends.

Over-filtering can reduce trade frequency.

Requires validation across instruments and timeframes before deployment.

CONCLUSION

The VWolf – Momentum Twin offers a disciplined framework for capturing momentum reversals while preserving flexibility through its customizable filters and risk controls. Its double confirmation logic filters out a significant portion of false reversals, while ATR-based scaling ensures consistency across varying market conditions. The optional trade management features, including partial profit-taking and automatic stop adjustments, allow the strategy to adapt to both trending and ranging environments. This makes it a versatile tool for traders who value structured entries, robust risk control, and adaptable management in a variety of markets and timeframes.

VWolf – EquinoxOVERVIEW

The VWolf – Equinox strategy integrates multiple technical filters, skew deviation logic, and advanced momentum indicators to identify high-probability trend continuation and reversal setups. Built upon the Vumanchu framework, this strategy applies filters such as EMA, DEMA, Supertrend, QQE, ADX/DMI, and customized skew thresholds. It combines these with divergence detection, volatility conditions, and risk-managed trade execution for dynamic adaptability across market conditions.

Its architecture is designed to provide flexibility for both backtesting and forward testing periods, while allowing traders to fine-tune entry confirmations and risk management tools based on their preferred market or timeframe.

RECOMMENDED USE

Markets: Forex, equities, and potentially crypto markets due to skew/volatility adaptability.

Timeframes: Works best on intraday (15m–1H) and swing-trading (4H–1D) horizons.

Trader Profile: Suited for intermediate to advanced traders who value multiple confirmation layers and dynamic risk management.

Strengths:

Robust filter system reduces false signals.

Flexible exit strategies with dynamic profit-taking.

Adaptability across different assets and timeframes.

Precautions:

Complexity may overwhelm beginners; careful parameter tuning is recommended.

Too many active filters can reduce signal frequency, potentially missing opportunities.

Divergence and skew thresholds require calibration to each market’s volatility regime.

CONCLUSION

The VWolf – Equinox stands out as one of the most comprehensive strategies in the VWolf library, combining skew deviation with a wide array of technical filters. Its layered confirmation system reduces noise and improves reliability across volatile markets. While powerful, its effectiveness depends on thoughtful parameter selection and disciplined risk management. This makes it a strong candidate for experienced traders seeking depth, adaptability, and dynamic trade control.

FOR MORE INFORMATION VISIT vwolftrading.com

VWolf - Basic EdgeOVERVIEW

VWolf - Basic Edge is a clean and accessible crossover strategy built on the core principle of moving average convergence. Designed for simplicity and ease of use, it allows traders to select from multiple types of moving averages—including EMA, SMA, HULL, and DEMA—and defines entry points strictly based on the crossover of two user-defined MAs.

This strategy is ideal for traders seeking a minimal, no-frills trend-following system with flexible exit conditions. Upon crossover in the selected direction (e.g., fast MA crossing above slow MA for a long entry), the strategy opens a trade and then manages the exit based on the user’s chosen method:

Signal-Based Exit:Trades are closed on the opposite crossover signal (e.g., long is exited when the fast MA crosses below the slow MA).

Fixed SL/TP Exit:The trade is closed based on fixed Stop Loss and Take Profit levels.Both SL and TP values are customizable via the strategy’s input settings.Once either the TP or SL is reached, the position is exited.

Additional filters such as date ranges and session times are available for backtesting control, but no extra indicators are used—staying true to the “basic edge” philosophy. This strategy works well as a starting framework for beginners or as a reliable, lightweight system for experienced traders wanting clean, rule-based entries and exits.

RECOMMENDED FOR

- Beginner to intermediate traders who want a transparent and easy-to-follow system.

- Traders looking to understand or build upon classic moving average crossover logic.

- Users who want a customizable but uncluttered strategy framework.

🌍 Markets & Instruments:

Well-suited for liquid and trending markets, including:Major forex pairs

Stock indices

Commodities (e.g., gold, oil)

Cryptocurrencies with stable trends (e.g., BTC, ETH)

⏱ Recommended Timeframes:

Performs best on higher intraday or swing trading timeframes, such as:15m, 1h, 4h, and 1D

Avoid low-timeframe noise (e.g., 1m, 3m) unless paired with strict filters or volatility controls.

FOR MORE INFORMATION VISIT vwolftrading.com

5-Min Range Breakout (09:30 NY on MNQ)This is a 5 - min orb strat that a youtuber mentioned and i had a manual look for a while and thought it was actually pretty good but my results are bad. Feel free to look yourself with this code.

Basically this strat is using the 5min orb then go down to 1min timeframe and wait for a breakout with FVG confirmation. So candle after breaking candle is our entry only if FVG is formed.

However i do notice if you dump this code onto 5min timefraem and above you start consistently making money but it is a very small amount for me so you all can have it. Good starter strat on 5min or 10min timeframe

Momentum FlowThis is a rule-based, fully automated trading strategy** developed **exclusively for BANKNIFTY** and optimized strictly for the **2-Hour (2H) timeframe**. The system is designed to identify **high-quality directional opportunities** while filtering out low-probability market noise.

The strategy is built for traders who prefer:

* Clean positional trading

* Limited, high-quality signals

* Fully mechanical execution

* No discretionary decision-making

This system is **locked by design** and will **only operate on BANKNIFTY – 2H timeframe** to preserve performance integrity. Usage on any other symbol or timeframe is intentionally restricted.

---

### ✅ SUITABLE FOR:

* Positional traders

* Swing traders

* Working professionals

* Traders seeking structured, disciplined systems

---

### ❌ NOT SUITABLE FOR:

* Scalping

* Low-timeframe trading

* High-frequency setups

* Traders seeking daily signals

---

### ⚠️ IMPORTANT DISCLAIMER:

This strategy is provided strictly for **educational and research purposes only**. Trading in financial markets involves significant risk, and losses are possible. Past performance does not guarantee future results. The creator is not responsible for any financial losses incurred by the use of this strategy. Always trade with proper risk management.

---

12M Return Strategy This strategy is based on the original Dual Momentum concept presented by Gary Antonacci in his book “Dual Momentum Investing.”

It implements the absolute momentum portion of the framework using a 12-month rate of change, combined with a moving-average filter for trend confirmation.

The script automatically adapts the lookback period depending on chart timeframe, ensuring the return calculation always represents approximately one year, whether you are on daily, weekly, or monthly charts.

How the Strategy Works

1. 12-Month Return Calculation

The core signal is the 12-month price return, computed as:

(Current Price ÷ Price from ~1 year ago) − 1

This return:

Plots as a histogram

Turns green when positive

Turns red when negative

The lookback adjusts automatically:

1D chart → 252 bars

1W chart → 52 bars

1M chart → 12 bars

Other timeframes → estimated to approximate 1 calendar year

2. Trend Filter (Moving Average of Return)

To smooth volatility and avoid noise, the strategy applies a moving average to the 12M return:

Default length: 12 periods

Plotted as a white line on the indicator panel

This becomes the benchmark used for crossovers.

3. Trade Signals (Long / Short / Cash)

Trades are generated using a simple crossover mechanism:

Bullish Signal (Go Long)

When:

12M Return crosses ABOVE its MA

Action:

Close short (if any)

Enter long

Bearish Signal (Go Short or Go Flat)

When:

12M Return crosses BELOW its MA

Action:

If shorting is enabled → Enter short

If shorting is disabled → Exit position and go to cash

Shorting can be enabled or disabled with a single input switch.

4. Position Sizing

The strategy uses:

Percent of Equity position sizing

You can specify the percentage of your portfolio to allocate (default 100%).

No leverage is required, but the strategy supports it if your account settings allow.

5. Visual Signals

To improve clarity, the strategy marks signals directly on the indicator panel:

Green Up Arrows: return > MA

Red Down Arrows: return < MA

A status label shows the current mode:

LONG

SHORT

CASH

6. Backtest-Ready

This script is built as a full TradingView strategy, not just an indicator.

This means you can:

Run complete backtests

View performance metrics

Compare long-only vs long/short behavior

Adjust inputs to tune the system

It provides a clean, rule-driven interpretation of the classic absolute momentum approach.

Inspired By: Gary Antonacci – Dual Momentum Investing

This script reflects the absolute momentum side of Antonacci’s original research:

Uses 12-month momentum (the most statistically validated lookback)

Applies a trend-following overlay to control downside risk

Recreates the classic signal structure used in academic studies

It is a simplified, transparent version intended for practical use and educational clarity.

Disclaimer

This script is for educational and research purposes only.

Historical performance does not guarantee future results.

Always use proper risk management.

Robrechtian Long-Medium Breakout Trend SystemRobrechtian Long–Medium-Term Breakout Trend System

A professional, rule-based trend-following strategy designed to capture large, sustained price movements using pure price action and breakouts.

This system follows long-established trend-following philosophy: no prediction, no volatility targeting, and no profit targets. Only disciplined entries, position additions, and exits driven entirely by trend structure.

Core Principles

Breakout-driven entries: Initial positions are taken only when price breaks above/below the 80-day Donchian channel, confirming a long–medium-term trend shift.

Short-term confirmation: Breakouts must also exceed the 20-day channel, reducing false positives.

Trend-direction filter: A 50-day moving average slope filter ensures alignment with the broader trend.

Explosive bar filter: Entries avoid excessively large, single-candle expansions (>2.5× ATR(20)) to prevent chasing exhaustion spikes.

Pyramiding into strength: Additional units are added only when price makes fresh 20-day breakouts in the direction of the trend. No scaling out. No adding on dips.

Exit only on trend violation: Positions are closed exclusively when price breaks the opposite 80-day channel. This preserves unlimited upside while enforcing disciplined exits.

Pure trend philosophy: No volatility targeting, no smoothing, no discretionary overrides, no optimization for short-term performance.

Intended Use

This system is designed primarily for diversified futures portfolios, where diversification across dozens of globally liquid markets creates robustness and stability. However, it may also be used on individual assets for educational and analytical purposes.

The system embraces the core trend-following logic:

Small losses, big winners, and unlimited upside when trends persist.

⚠️ WARNINGS / DISCLAIMERS

⚠️ Warning 1 — This strategy is not optimized for single stocks

The Robrechtian Trend System is designed for multi-asset futures portfolios, not single equities.

Performance on individual tickers may vary greatly due to lack of diversification.

⚠️ Warning 2 — Trend following includes substantial drawdowns

Deep drawdowns are a normal and expected feature of all long-term trend-following systems.

The strategy does not attempt to smooth returns or manage volatility.

If you seek steady, low-volatility equity curves, this system is not suitable.

⚠️ Warning 3 — No volatility targeting or risk smoothing

This system intentionally avoids volatility-based position sizing.

Trades may experience larger fluctuations than systems using risk parity or vol targeting.

⚠️ Warning 4 — Not financial advice

This script is for educational and research purposes only.

Past performance does not guarantee future results.

Use at your own risk.

⚠️ Warning 5 — TradingView backtests have known limitations

TradingView does not simulate:

futures contract roll logic

slippage

real bid/ask spreads

liquidity conditions

limit-up/limit-down behavior

Results may vary from live market execution.

Relative Outperformance Strategy (Long Only)Relative Strength used to spot entries. Gives good returns overall.

MACD with EMA FilterThis indicator combines the MACD (Moving Average Convergence Divergence) with an EMA-based trend filter to improve the quality of entry signals.

MACD identifies changes in momentum and potential trend reversals, while the EMA ensures that signals are taken only in the direction of the broader trend.

NIFTY 5m/15m Smart Money CE/PE – High WinRatenice strategy for intraday NIFTY option trading. It works best on 5 minute time frame on NIFTY Index Chart

SSL ST Strategy – Accuracy Enhanced v2.0 (Parser Safe)This strategy is built to identify high-probability trend breakouts using a combination of SSL Channel, Baseline, Hull / EMA signals, and Candle-based confirmations.

The goal is to filter noise, avoid false breakouts, and enter only when the trend is truly shifting.

This strategy identifies high-probability trend breakouts using SSL Channel, Baseline, Hull/EMA, and candle

confirmations.

1. SSL shows trend shift when price breaks high/low levels.

2. Baseline filters direction (price above = buy bias, below = sell bias).

3. Hull/EMA gives early momentum confirmation.

4. Candle breakout ensures real momentum (breaks previous high/low).

5. Optional filters: ATR, reversal logic, continuation entries.

6. Exits occur on SSL flip, baseline cross, or weakness

Disclaimer

This strategy is provided strictly for educational and informational purposes only. It does not guarantee any profit, nor does it protect against losses of any kind. Financial markets are inherently unpredictable, and any market movement can only be assumed or estimated with a probability that is never guaranteed and can often be no better than a 50/50 chance.

By using this strategy, you acknowledge that all trading decisions are made solely at your own risk. I am not liable for any profits, losses, or financial consequences incurred by anyone using or relying on this strategy. Always perform your own research, manage your risk responsibly, and consult with a qualified financial advisor before trading.

SenxseAiSenxseiAI is a fully modular, multi-framework trading system designed for precision, clarity, and ease of use.

This tool blends market structure, dynamic S/R mapping, trend-logic, and session-based liquidity levels into a unified visual workflow. It highlights real-time entry signals with clean rays and labeled flags, while optional session, daily, and weekly highs/lows anchor traders to key liquidity points. A comprehensive theme engine—with multiple color packs and custom overrides—allows the interface to adapt to any chart style or user preference.

The UI is intentionally minimal, using toggle-based controls instead of overwhelming parameter lists, making the script beginner-friendly while maintaining professional depth.

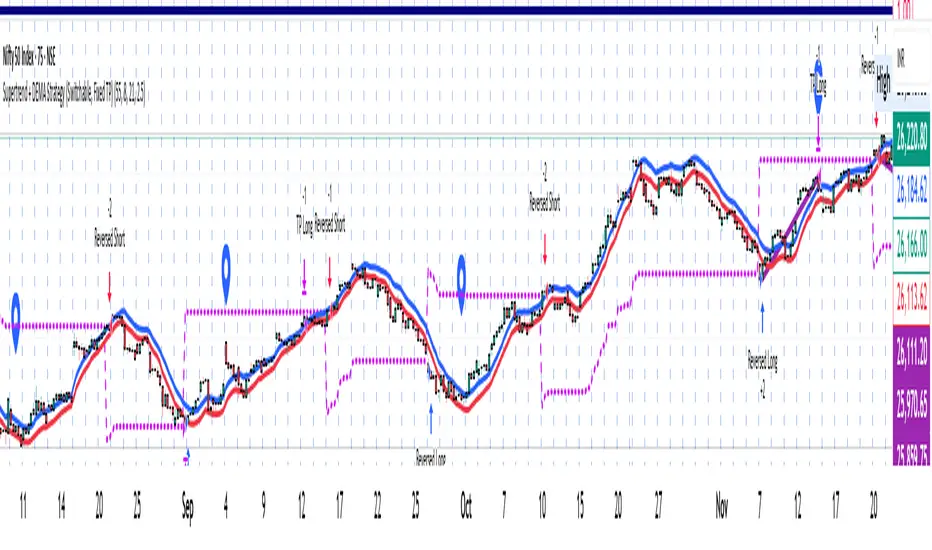

Supertrend + DEMA Strategy ( customised & Switchable, Fixed TP)Supertrend line – a moving line that follows the price and shows whether the market is trending up or down.

If the price goes above this line, it usually means the market is going up.

If the price goes below, it usually means the market is going down.

DEMA (Double Exponential Moving Average) – another line that smooths out price movements to spot trends more clearly.

It calculates an average of prices but reacts faster than a normal moving average.

VWolf – Apex GateOverview

VWolf – Apex Gate is a trend-continuation system that blends a Pivot-weighted Supertrend (PVT ST) with an optional **Normal Supertrend** trigger, all **gated by a 200-EMA directional filter. The strategy’s risk controls are volatility-aware—**stops and targets scale by ATR**, and quantity is computed from a fixed **% risk per trade**. Clear **Backtest / Forwardtest** modes with date windows let you validate on segmented datasets before committing to live use.

Recommended Use

- **Markets:** High-liquidity instruments (indices, large-cap equities, liquid FX and major crypto pairs) where trends and pullbacks are clean.

- **Timeframes:** 15m–1h for active intraday; 4h–1D for swing. Lower timeframes may benefit from stricter EMA gating and slightly wider ATR stops.

- **Workflow:**

1. Start with **Backtest** to set baseline ATR/EMA parameters.

2. Move to **Forwardtest** to confirm generalization.

3. Consider walk-forward or multi-symbol rotation to assess robustness.

Strengths & Precautions

Strengths

- **Dual engine** (PVT ST + Normal ST) improves signal quality; the **EMA gate** screens counter-trend noise.

- **ATR-native** stops/targets standardize risk across regimes/instruments.

- **Capital-proportional sizing** preserves account geometry and smooths drawdowns.

- **Clear test segmentation** supports objective evaluation.

Precautions

- **Whipsaw risk** in tight ranges: widen ATR multipliers, enable the EMA gate, or require co-confirmation.

- **Supertrend-anchored stops** can expand in volatility spikes; ensure **% risk** remains within tolerance.

- **One-position policy** avoids stacking risk but forgoes scaling into strong trends; advanced users may prefer add-on frameworks outside this baseline.

Conclusion

VWolf – Apex Gate seeks to enter shortly after **regime flips**, demanding alignment between a **pivot-aware Supertrend** and (optionally) a **classic Supertrend**, while an **EMA gate** enforces directional discipline. With **ATR-driven** stops/targets and **fixed-fraction** sizing, the system adapts naturally to changing volatility. Use the **Backtest** window to dial ranges and the **Forwardtest** window to prove durability on unseen data. For best results, tailor ATR multipliers and the EMA gate to your instrument’s structure and your personal drawdown tolerance.

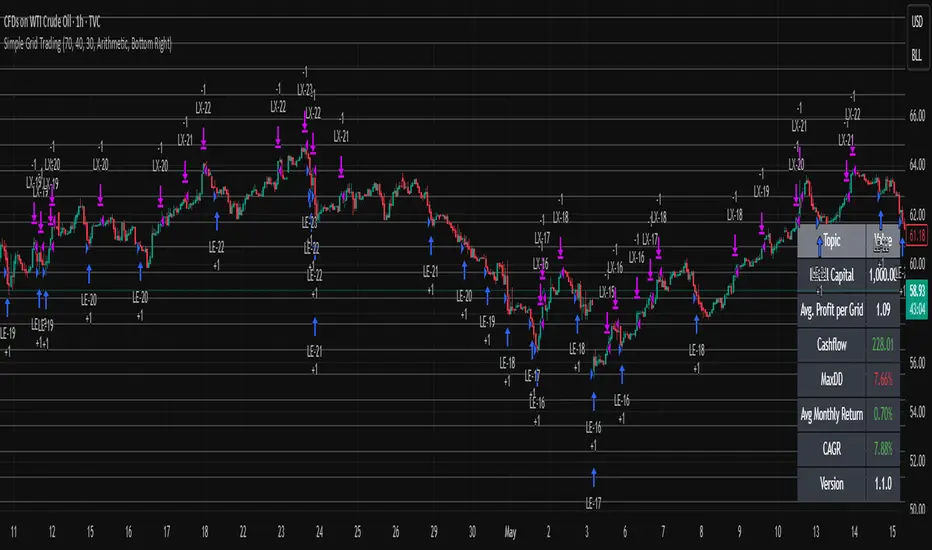

Simple Grid Trading v1.0 [PUCHON]Simple Grid Trading v1.0

Overview

This is a Long-Only Grid Trading Strategy developed in Pine Script v6 for TradingView. It is designed to profit from market volatility by placing a series of Buy Limit orders at predefined price levels. As the price drops, the strategy accumulates positions. As the price rises, it sells these positions at a profit.

Features

Grid Types : Supports both Arithmetic (equal price spacing) and Geometric (equal percentage spacing) grids.

Flexible Order Management : Uses strategy.order for precise control and prevents duplicate orders at the same level.

Performance Dashboard : A real-time table displaying key metrics like Capital, Cashflow, and Drawdown.

Advanced Metrics : Includes Max Drawdown (MaxDD) , Avg Monthly Return , and CAGR calculations.

Customizable : Fully adjustable price range, grid lines, and lot size.

Dashboard Metrics

The dashboard (default: Bottom Right) provides a quick snapshot of the strategy's performance:

Initial Capital : The starting capital defined in the strategy settings.

Lot Size : The fixed quantity of assets purchased per grid level.

Avg. Profit per Grid : The average realized profit for each closed trade.

Cashflow : The total realized net profit (closed trades only).

MaxDD : Maximum Drawdown . The largest percentage drop in equity (realized + unrealized) from a peak.

Avg Monthly Return : The average percentage return generated per month.

CAGR : Compound Annual Growth Rate . The mean annual growth rate of the investment over the specified time period.

Strategy Settings (Inputs)

Grid Settings

Upper Price : The highest price level for the grid.

Lower Price : The lowest price level for the grid.

Number of Grid Lines : The total number of levels (lines) in the grid.

Grid Type :

Arithmetic: Distance between lines is fixed in price terms (e.g., $10, $20, $30).

Geometric: Distance between lines is fixed in percentage terms (e.g., 1%, 2%, 3%).

Lot Size : The fixed amount of the asset to buy at each level.

Dashboard Settings

Show Dashboard : Toggle to hide/show the performance table.

Position : Choose where the dashboard appears on the chart (e.g., Bottom Right, Top Left).

How It Works

Initialization : On the first bar, the script calculates the price levels based on your Upper/Lower price and Grid Type.

Entry Logic :

The strategy places Buy Limit orders at every grid level below the current price.

It checks if a position already exists at a specific level to avoid "stacking" multiple orders on the same line.

Exit Logic :

For every Buy order, a corresponding Sell Limit (Take Profit) order is placed at the next higher grid level.

MaxDD Calculation :

The script continuously tracks the highest equity peak.

It calculates the drawdown on every bar (including intra-bar movements) to ensure accuracy.

Displayed as a percentage (e.g., 5.25%).

Disclaimer

This script is for educational and backtesting purposes only. Grid trading involves significant risk, especially in strong trending markets where the price may move outside your grid range. Always use proper risk management.