Extremum Range MA Crossover Strategy1. Principle of Work & Strategy Logic ⚙️📈

Main idea: The strategy tries to catch the moment of a breakout from a price consolidation range (flat) and the start of a new trend. It combines two key elements:

Moving Average (MA) 📉: Acts as a dynamic support/resistance level and trend filter.

Range Extremes (Range High/Low) 🔺🔻: Define the borders of the recent price channel or consolidation.

The strategy does not attempt to catch absolute tops and bottoms. Instead, it enters an already formed move after the breakout, expecting continuation.

Type: Trend-following, momentum-based.

Timeframes: Works on different TFs (H1, H4, D), but best suited for H4 and higher, where breakouts are more meaningful.

2. Justification of Indicators & Settings ⚙️

A. Moving Average (MA) 📊

Why used: Core of the strategy. It smooths price fluctuations and helps define the trend. The price (via extremes) must cross the MA → signals a potential trend shift or strengthening.

Parameters:

maLength = 20: Default length (≈ one trading month, 20-21 days). Good balance between sensitivity & smoothing.

Lower TF → reduce (10–14).

Higher TF → increase (50).

maSource: Defines price source (default = Close). Alternatives (HL2, HLC3) → smoother, less noisy MA.

maType: Default = EMA (Exponential MA).

Why EMA? Faster reaction to recent price changes vs SMA → useful for breakout strategies.

Other options:

SMA 🟦 – classic, slowest.

WMA 🟨 – weights recent data stronger.

HMA 🟩 – near-zero lag, but “nervous,” more false signals.

DEMA/TEMA 🟧 – even faster & more sensitive than EMA.

VWMA 🔊 – volume-weighted.

ZLEMA ⏱ – reduced lag.

👉 Choice = tradeoff between speed of reaction & false signals.

B. Range Extremes (Previous High/Low) 📏

Why used: Define borders of recent trading range.

prevHigh = local resistance.

prevLow = local support.

Break of these levels on close = trigger.

Parameters:

lookbackPeriod = 5: Searches for highest high / lowest low of last 5 candles. Very recent range.

Higher value (10–20) → wider, stronger ranges but rarer signals.

3. Entry & Exit Rules 🎯

Long signals (BUY) 🟢📈

Condition (longCondition): Previous Low crosses MA from below upwards.

→ Price bounced from the bottom & strong enough to push range border above MA.

Execution: Auto-close short (if any) → open long.

Short signals (SELL) 🔴📉

Condition (shortCondition): Previous High crosses MA from above downwards.

→ Price rejected from the top, upper border failed above MA.

Execution: Auto-close long (if any) → open short.

Exit conditions 🚪

Exit Long (exitLongCondition): Close below prevLow.

→ Uptrend likely ended, range shifts down.

Exit Short (exitShortCondition): Close above prevHigh.

→ Downtrend likely ended, range shifts up.

⚠️ Important: Exit = only on candle close beyond extremes (not just wick).

4. Trading Settings ⚒️

overlay = true → indicators shown on chart.

initial_capital = 10000 💵.

default_qty_type = strategy.cash, default_qty_value = 100 → trades fixed $100 per order (not lots). Can switch to % of equity.

commission_type = strategy.commission.percent, commission_value = 0.1 → default broker fee = 0.1%. Adjust for your broker!

slippage = 3 → slippage = 3 ticks. Adjust to asset liquidity.

currency = USD.

margin_long = 100, margin_short = 100 → no leverage (100% margin).

5. Visualization on Chart 📊

The strategy draws 3 lines:

🔵 MA line (thickness 2).

🔴 Previous High (last N candles).

🟢 Previous Low (last N candles).

Also: entry/exit arrows & equity curve shown in backtest.

Disclaimer ⚠️📌

Risk Warning: This description & code are for educational purposes only. Not financial advice. Trading (Forex, Stocks, Crypto) carries high risk and may lead to full capital loss. You trade at your own risk.

Testing: Always backtest & demo test first. Past results ≠ future profits.

Responsibility: Author of this strategy & description is not responsible for your trading decisions or losses.

Highlow

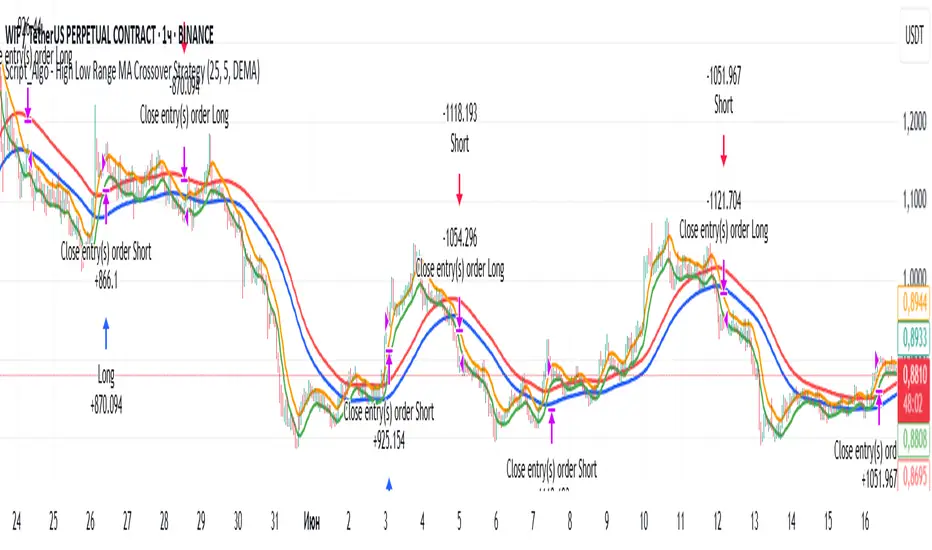

Script_Algo - High Low Range MA Crossover Strategy🎯 Core Concept

This strategy uses modified moving averages crossover, built on maximum and minimum prices, to determine entry and exit points in the market. A key advantage of this strategy is that it avoids most false signals in trendless conditions, which is characteristic of traditional moving average crossover strategies. This makes it possible to improve the risk/reward ratio and, consequently, the strategy's profitability.

📊 How the Strategy Works

Main Mechanism

The strategy builds 4 moving averages:

Two senior MAs (on high and low) with a longer period

Two junior MAs (on high and low) with a shorter period

Buy signal 🟢: when the junior MA of lows crosses above the senior MA of highs

Sell signal 🔴: when the junior MA of highs crosses below the senior MA of lows

As seen on the chart, it was potentially possible to make 9X on the WIFUSDT cryptocurrency pair in just a year and a half. However, be careful—such results may not necessarily be repeated in the future.

Special Feature

Position closing priority ❗: if an opposite signal arrives while a position is open, the strategy first closes the current position and only then opens a new one

⚙️ Indicator Settings

Available Moving Average Types

EMA - Exponential MA

SMA - Simple MA

SSMA - Smoothed MA

WMA - Weighted MA

VWMA - Volume Weighted MA

RMA - Adaptive MA

DEMA - Double EMA

TEMA - Triple EMA

Adjustable Parameters

Senior MA Length - period for long-term moving averages

Junior MA Length - period for short-term moving averages

✅ Advantages of the Strategy

🛡️ False Signal Protection - using two pairs of modified MAs reduces the number of false entries

🔄 Configuration Flexibility - ability to choose MA type and calculation periods

⚡ Automatic Switching - the strategy automatically closes the current position when receiving an opposite signal

📈 Visual Clarity - all MAs are displayed on the chart in different colors

⚠️ Disadvantages and Risks

📉 Signal Lag - like all MA-based strategies, it may provide delayed signals during sharp movements

🔁 Frequent Switching - in sideways markets, it may lead to multiple consecutive position openings/closings

📊 Requires Optimization - optimal parameters need to be selected for different instruments and timeframes

💡 Usage Recommendations

Backtest - test the strategy's performance on historical data

Optimize Parameters - select MA periods suitable for the specific trading instrument

Use Filters - add additional filters to confirm signals

Manage Risks - always use stop-loss and take-profit orders.

You can safely connect to the exchange via webhook and enjoy trading.

Good luck and profits to everyone!!

Octopus Nest Strategy Hello Fellas,

Hereby, I come up with a popular strategy from YouTube called Octopus Nest Strategy. It is a no repaint, lower timeframe scalping strategy utilizing PSAR, EMA and TTM Squeeze.

The strategy considers these market factors:

PSAR -> Trend

EMA -> Trend

TTM Squeeze -> Momentum and Volatility by incorporating Bollinger Bands and Keltner Channels

Note: As you can see there is a potential improvement by incorporating volume.

What's Different Compared To The Original Strategy?

I added an option which allows users to use the Adaptive PSAR of @loxx, which will hopefully improve results sometimes.

Signals

Enter Long -> source above EMA 100, source crosses above PSAR and TTM Squeeze crosses above 0

Enter Short -> source below EMA 100, source crosses below PSAR and TTM Squeeze crosses below 0

Exit Long and Exit Short are triggered from the risk management. Thus, it will just exit on SL or TP.

Risk Management

"High Low Stop Loss" and "Automatic High Low Take Profit" are used here.

High Low Stop Loss: Utilizes the last high for short and the last low for long to calculate the stop loss level. The last high or low gets multiplied by the user-defined multiplicator and if no recent high or low was found it uses the backup multiplier.

Automatic High Low Take Profit: Utilizes the current stop loss level of "High Low Stop Loss" and gets calculated by the user-defined risk ratio.

Now, follows the bunch of knowledge for the more inexperienced readers.

PSAR: Parabolic Stop And Reverse; Developed by J. Welles Wilders and a classic trend reversal indicator.

The indicator works most effectively in trending markets where large price moves allow traders to capture significant gains. When a security’s price is range-bound, the indicator will constantly be reversing, resulting in multiple low-profit or losing trades.

TTM Squeeze: TTM Squeeze is a volatility and momentum indicator introduced by John Carter of Trade the Markets (now Simpler Trading), which capitalizes on the tendency for price to break out strongly after consolidating in a tight trading range.

The volatility component of the TTM Squeeze indicator measures price compression using Bollinger Bands and Keltner Channels. If the Bollinger Bands are completely enclosed within the Keltner Channels, that indicates a period of very low volatility. This state is known as the squeeze. When the Bollinger Bands expand and move back outside of the Keltner Channel, the squeeze is said to have “fired”: volatility increases and prices are likely to break out of that tight trading range in one direction or the other. The on/off state of the squeeze is shown with small dots on the zero line of the indicator: red dots indicate the squeeze is on, and green dots indicate the squeeze is off.

EMA: Exponential Moving Average; Like a simple moving average, but with exponential weighting of the input data.

Don't forget to check out the settings and keep it up.

Best regards,

simwai

---

Credits to:

@loxx

@Bjorgum

@Greeny

Strategy Gaussian Anomaly DerivativeConcept behind this Strategy :

Considering a normal "buy/sell" situation, an asset would be bought in average at the median price following a Gaussian like concept. A higher or lower average trend would significate that the current perceived value is respectively higher or lower than the current median price, which mean that the buyers are evaluating the price underpriced or overpriced.

This behaviour would be even more relevent depending on its derivative evolution.

Therefore, this Strategy setup is based on this Gaussian like concept anomaly of average close positionning compare to high-low average derivative, such as the derivative of the following ploted basic signal : 1-(high+low)/(2*close).

This Strategy can actually be used like a trend change and continuation strength indicator aswell.

In the Setup Signal part :

You can define the filtering of the basis signal "1-(high+low)/(2*close)" on EMA or SMA as you wish.

You can define the corresponding period and the threathold as a mutiply of the average 1/3 of all time value of the basis signal.

You can define the SMA filtering period of the Derivative signal and the corresponding threathold on the same mutiply of the average 1/3 of all time value of the derivative.

In the Setup Strategy part :

You can set up your strategy assesment based on Long and/or Short. You can also define the considered period.

The most successful tuned strategies I did were based on the derivative indicator with periods on the basis signal and the derivative under 30, can be 1 to 3 of te derivative and 7 to 21 for the basis signal. The threathold depends on the asset volatility aswell, 1 is usually the most efficient but 0 to 10 can be relevent depending on the situation I met. You can find an example of tuning for this strategy based on Kering's case hereafter.

I hoping that you will enjoy using this Strategy, don't hesitate to comment, to question, to correct or complete it ! I would be very curious about similar famous approaches that would have already been made.

Thank to you !

Combo Backtest 123 Reversal & High and Low Levels This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This script shows a high and low period value.

Width - width of lines

SelectPeriod - Day or Week or Month and etc.

LookBack - Shift levels 0 - current period, 1 - previous and etc.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & High Low Bands This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

As the name suggests, High low bands are two bands surrounding the underlying’s

price. These bands are generated from the triangular moving averages calculated

from the underlying’s price. The triangular moving average is, in turn, shifted

up and down by a fixed percentage. The bands, thus formed, are termed as High

low bands. The main theme and concept of High low bands is based upon the triangular

moving average.

WARNING:

- For purpose educate only

- This script to change bars colors.

Last High and Low Level Backtest This script shows a high and low period value.

SelectPeriod - Day or Week or Month and etc.

LookBackPeriods - Shift levels 0 - current period, 1 - previous and etc.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

High and Low Levels Backtest This script shows a high and low period value.

Width - width of lines

SelectPeriod - Day or Week or Month and etc.

LookBack - Shift levels 0 - current period, 1 - previous and etc.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.