MA Divergences StrategyThis is the Strategy version of the Study I published. It is a Moving Average that can be applied to any plot to plot divergences on any oscillator, as well as perform backtesting. You'll need a REALLY good oscillator to perform live trades using this alone, but I think it is a valuable tool and had the Strategy hanging around and for some reason didn't upload it yet.

So here it is.

Turn Length to 1 to follow the oscillator without lag. Turn Length up if you are getting too many false signals or tweak the original oscillator settings.

M-oscillator

Denario momentum strategy Momentum strategy based on early trend detection indicator. It oscillates in the range . Negative values correspond to downtrend, positive to uptrend.

Values closer to 0 correspond to noise. You can set threshold values for long/short entry and exit.

But like any other momentum indicator use it along with extra filters to confirm entry and exit.

Super Momentum StrategyThis is a strategy utilizing multiple of Evergets RMI (thanks to him for permission to publish) and a Chance Momentum.

It buys when 4 of the RMIs are below their thresholds and sells when they are above. There is a 5th one I added last night that works in Reverse - buy when its above and sell when below, which should work better for pyramiding strats by using it at the right rate to set the overall trend.

Very basic sample below, I could have set it up better as my example but just want to publish.

Combo Backtest 123 Reversal & Market Facilitation Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Market Facilitation Index is an indicator that relates price range to

volume and measures the efficency of price movement. Use the indicator to

determine if the market is trending. If the Market Facilitation Index increased,

then the market is facilitating trade and is more efficient, implying that the

market is trending. If the Market Facilitation Index decreased, then the market

is becoming less efficient, which may indicate a trading range is developing that

may be a trend reversal.

WARNING:

- For purpose educate only

- This script to change bars colors.

RMI + Triple HMRSI + Double EVWRSI + TERSI + CMO StrategyThis is a strange experimental strategy WIP that I decided to upload an early version to share some of what I am working on. Just one script of a few.

It combines Chande Momentum with RMI and some weird ones I am experimenting with - Triple Hull MA RSI, Double Exponential + Volume Weighted RSI, Triple Exponential RSI. And to top it off, a final oscillator that combines the THMRSI with the RMI.

The main intention here, currently, is to test the usefulness of each on different timeframes and values. Currently it is considered to buy when all are below their threshold and sell when all are above, with the chande momentum crossing its line as the final confirmation.

For now there is no individual for each of the unique elements included. I am going to likely use this is a working house project to test other experimental indicators in the future.

It may be some of these are better suited for long term but I do think they have valid uses in checking short and long term momentum at the very least.

I copied the RMI from Everget.

[DS]Entry_Exit_TRADE.V01-StrategyThe proposal of this script is to show the possible trading points of BUY and SELL based on the 15-minute chart of the Nasdaq Future Index. The start point of the strategy was schedule for 2021/01/01 and until the time of this publication (2021/01/31), for 1 index contract the results presented area a Gross Profit of 2.97% with a Net Profit of 1.35%.

█ FEATURES

The indicator shows on the graph the position of the MACD and TSI indicators that are the places of strength among Buyers and Sellers.

It's possible to observe a sharp fall or rise in the price of these positions.

On the current candle, a label is displayed containing the value of the William %R Mod indicator, which will display the OverBought position (dark red) and OverSold position (dark green). The other colors like light red and green are the regions where the price makes the decision of which direction to go.

There are also other indicators:

a) The positions of the BUY (light green) and SELL areas (light red);

b) The label with the position of BUY (dark green) and SELL (dark red) with the line that connects these points;

c) DEMA 72 (orange);

d) EmaOchl4 in the color green for BULL and red for BEAR market;

e) Pivots high and low

f) Maximum (purple light) and minimum areas (blue light)

█ FUNCTIONS AND SETTINGS

The indicator uses the following functions:

(1) DEMA - Double Exponential Moving Average (08,17,34, 72)

(2) ema () - Exponential Moving Averge (72, ohlc4)

(3) plot()

(4) barcolor()

(5) cross()

(6) pivots ()

(7) William R% Md (OverBought = -7, OverSold=-93)

(8) Maximum and Minimum Value

(9) fill()

(10) macd () - Moving Average Convergence Divergence (Fast Lengt=12, Slow Length=26, Source=close, Signal Smoothing=9)

(11) tsi() - Trading Strenght Indicator==> Índice de Força Real ( IFR ) (Long Length=72, Short Length=17, Signal Length=17)

(12) Buy and Sell TRADE Points

█ PERFORMANCE AND ERRORS

The positions of BUY and SELL points are defined through the crossing of the Dema 34 candles with the Ema Ohcl4. As it is an indicator, it can present different positions from de market direction. Thus there is a need to observe the direction of the market in order to verify whether the indicate decision is really acceptable. The decision to BUY or SELL an asset must be well studied to avoid financial losses. The indicator will only help you in this decision, is your responsibility the decision of entering or leaving an asset.

█ THANKS TO

PineCoders for all they do, all the tools and help they provide, and their involvement in making a better community. All the PineCoders, Pine Pros, and Pine Wizards, people who share their work and knowledge for the sake of it and helping others, I'm very happy and grate full indeed.

█ NOTE

If you have any suggestions for improving the script or need help using it, please send a message in the comments

I SAHAM AK BUY LOW ____ Multi TimeFrame OversoldThis strategy is built to confirm the profitability of buying oversold using RSI indicator.

Buy & Sell point will appear on price chart.

Entry Point : RSI3, RSI10, AND RSI14 below 26.

Cut Loss : Entry Price - 5%.

Take Profit : Entry Price + 10%.

5 entries allowed in same direction eventhough open trade not yet closed. In layman words, you keep buying new low closing price for 5 times.

Commission fee fixed at 0.08%.

Decent fundamental counter is preferable.

Even at win rate of 50%, it is profitable due to Risk Reward Ratio of 1 to 2.

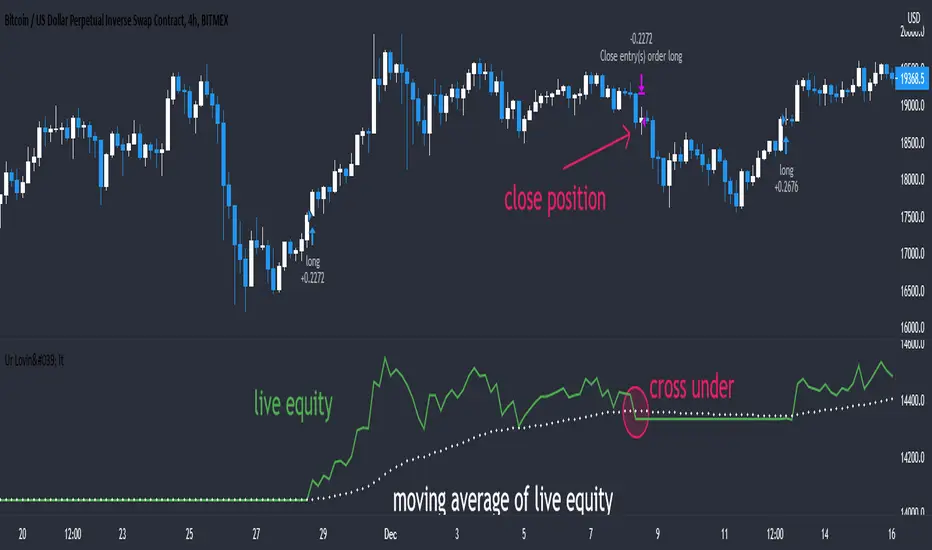

MACD controlled risk strategy exampleUsing a basic MACD as a signal this code is an example of how to base strategies around stops and calculated risk per trade rather than the more common approach of 'equity flipping' long and short for every trade and using an arbitrary %age stop which can leave you a bit exposed, lead to excessive drawdown and miss out on bigger sized positions for more profits.

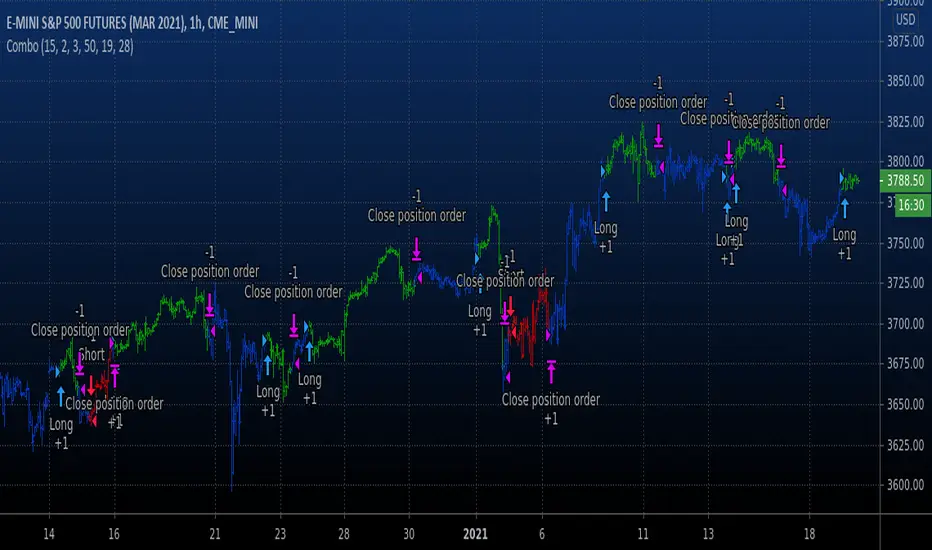

Self-Optimising MACD (Experimental)Hi guys, just thought I'd share a small part of an idea i've been working on.

One of the biggest problems with algo trading is optimisation and finding a way to constantly adapt to the market conditions as time unfolds.

First of all... You should NEVER EVER trade just using a MACD, including this study, and I only produced this script in a small amount of time, so make sure you backtest it properly before using it. When backtesting, it is my advice that your sample size should be at least 5000 trades, but I recommend 10000 in order to get sufficient statistical significance.

Also, I am not a financial advisor, and any trading based decisions are your sole responsibility.

Anyways...

This script is simple... it simply uses 4 different MACD's and tracks their profit/loss and automatically uses the one with the most historical profit at any given time to execute a trade. The type of MACD will obviously change as market states fluctuate.

Included are : Hull MACD, Ema MACD, Sma MACD and VWMA Macd.

You can adjust all four of their settings to your desire.

The trade execution is simple and definitely flawed... it simply tracks the MACD when it has a crossover for long, and then the opposite for short.

The green line represents the performance of the top MACD for Longs at any given time. This line refreshes once a year, and where it is in relation to price, reflects how profitable it has been I.e - the higher it is the better.

The Red line represents the performance on the Short side, and again, it reflects profit/loss, but this time the LOWER the line is in relation to price the better.

There is no exit strategy in place! This is why I do NOT recommend trading off this script alone, but to use it as a tool to help optimise your choice of MACD.

However, your exit strategy could change your optimal choice of MACD, so keep that in mind.

The lookback period represents how far the script will track the performance at any given time. This will change your results. The longer the period, the more it will show long term success and vice versa.

This optimisation process could be done with different indicators, moving averages, or even multiple strategies to find the most statistically viable option at any given time... if you wish to have this process coded into your strategies or indicators, message me.

Enjoy.

Combo Backtest 123 Reversal & Line Regression Intercept This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Linear Regression Intercept is one of the indicators calculated by using the

Linear Regression technique. Linear regression indicates the value of the Y

(generally the price) when the value of X (the time series) is 0. Linear

Regression Intercept is used along with the Linear Regression Slope to create

the Linear Regression Line. The Linear Regression Intercept along with the Slope

creates the Regression line.

WARNING:

- For purpose educate only

- This script to change bars colors.

cRSI + Waves Strategy with VWMA overlayStrategy based on my cRSI with motive/corrective wave indicator. Please note that it is far from perfect. I use it mostly to help me identify good entry and exit points when combined with my other technical analysis. It misses some obvious points, but on average it does pretty well. The challenge often is indicating when you have sufficient change in the cRSI to know that the trend has changed, that means sometimes it can be a little early or late. It definitely helps take a lot of the guess work out of things. It works better on some equities than others and better on some time frames than others. You just have to play with it. At the minimum, it is a good template to learn how to write your own.

POW EdgeHello fellow Trading View member,

Eventually our rebranded update with some extra features for our exclusive 'Edge' Strategy Script.

In this description I will run through;

The strategy itself, what is it?

What does it do?

How does it work?

How can it help you?

How good is it?

What is it.....

The Edge Strategy itself is based upon 5 indicators lining up in total confluence to enter a position in line with a trending move. Adding them together adds more confluence and probability to each individual trade outcome over the longer term. The individual strategies used are based on Trend strategies all used in combination.

The uniqueness to this is how they are combined. Indicators can work to a point individually of course, but combining them together and only trading when all are in a line was our concept, whilst reviewing how each individual indicator can be optimised to work with the others.

Also the motivation was to be the right side of the market in a trending move and capitalising on as much as that move as possible.

The first part is to ensure the candle close is above or below our moving average, we can then check the state and validity of each of the other 4 indicators. Once this confluence is in alignment a trade is valid for entry - this has to be valid at the same time - but not all valid on the same candle - they will come into alignment in different stages. But once they are, our trade is valid.

I will not reveal the other individual 3 indicators but the other is also an ADX function to add a threshold into the strategy to identify a trend - usually above 20/25. This has upsides and downsides as any user can visualise and see in the testing.

We also add to the script to look for a Buy then Sell, Sell then Buy - we found this had more profitable results overall and next phase was to review the money management; where and how we placed our SL and when and why we exited the trade.

Example - for a BUY trade to be valid, all 5 indictors must meet their own criteria before a BUY is printed on the chart. Absolutely no technical analysis is needed to trade this strategy and the data we have is based on using the strategy in isolation - how you wish to use this either independently or supporting your own trading is of course, up to you.

The SL and TP's are based on ATR Multipliers thus ensuring we are factoring in market volatility at that time. We also have a FT (Follow Trend) option, which is a worthy addition for capitalising on big trending moves.

This strategy will work on all markets and timeframes.

We understand and accept that all pairs and markets are different thus we have optimised certain pairs and timeframes with different parameters to provide increased returns, these are hard coded (H1 Timeframe) and also provided for your review.

Profitability is easily viewable in the ‘Strategy Tester’ - this is a great tool. This is where you can see historic / live data for the strategy.

Data like;

The Net Profit

Number of trades

Win Percentage

Every trade taken

Average Win

Average Loss

Maximal DD , etc.

We have individually optimised each pair to ensure this is the case and hard coded these parameters into the strategy. All you need to do is flick between the pairs - the strategy will then identify the pair you are on and change the parameters to suit in the background.

Whilst a trade is open, the strategy will convert all candles to the relevant colour - Green for an uptrend and Red for a downtrend (all customisable).

We find this is helpful for traders psychology - not getting 'spooked' by other candle colours, affecting your decision making.

When a new signal is valid, 'POW BUY' or 'POW SELL' will be displayed on the first candle open for entry. As well as this, you will also have the trade label print which will display the following;

- EP – Entry price

- SL – Stop loss

- TP – Take Profit

- Lot size

The trade information printed will also tell you the pip values of your stop loss and take profit based on how far away they are from the trade entry price.

The lot size printed is customisable and unique to your account- within the strategy settings you can simply input your account balance, currency and risk approach which includes a fixed risk amount, fixed lot size or a fixed percentage.

This removes the need for 3rd party apps or websites to quickly calculate your specific risk on your trade. Thus saving you time and making sure you aren't 'guessing' with your lot size.

No one likes losing more than they thought.

The progress and initial challenges....

To start, our first version simply showed the buy and sell arrows when a trade was valid. However, this caused subjectivity with where we would place our stop loss and how we would manage the exit of the trade once we were in it. So, we identified a solid strategy for this was incorporating the Average True Range (ATR) for SL and TP options.

I was especially keen to add the SL and exit management so I could obtain solid back testing data to support my thoughts that 'this works'. Every trader requires confidence and belief in their strategy, without it you simply won't succeed or be disciplined in your execution.

The other challenge we all face is calculating the lot sizes of our trades right? So, it was important that we incorporated a lot size calculator - its all about making it easy when a trade is valid to enter without trying to calculate this accurately.

Lastly, when pairs are stuck in a range - this can be a testing period of 'chop' for a trend strategy, so we also incorporated the ADX function to enable us to set a threshold level to identify when the instrument is more likely to be trending.

What does it do?

Ultimately, tells you when to buy and sell - where to place your SL and when to exit. Whilst also ensuring your risk management is on point, by displaying your trading lot size. Also providing you with live back tested data at your finger tips thank you to the strategy tester.

How does it work?

This will be visible on your trading view charts once you get access. And will work across all your devices, the trading view website or the app on your phone for example.

You can also use Trading View alerts, so you won't miss a trade and can go about your day as normal without watching the screen. This will work on the Free version of TV, however, in order to benefit from more alerts and templates it makes sense to upgrade to a higher package.

How can it help you?

This will help give you a mechanical approach to your trading. This means, less decision making on your part, with the instant benefit of seeing the data you have at your fingertips thanks to the 'Strategy Tester' TV Function.

It will save you time, you don't need to be in front of your screen or completing any subjective analysis.

Integrated lot size calculator can ensure you are always accurate with your risk - either in percentage or a fixed amount of risk - whichever you prefer.

Understand Probability - this is the key one for me. Losing runs happen in any trading strategy. The great benefit here, is you can see them. How long were the losing runs? How can I prepare and plan my risk management around them are all fundamental keys to managing your emotions and being detached from your trades. No one wants to feel stressed or anxious when trading.

Customisable exit strategies - A specific TP for a 1:1 RR or 1:10 RR for example can be adjusted and you can see instantly how this affects the profitability.

The exit strategy options are shown below;

TP 1/2/3

FT - Follow Trend (no stop loss and follow's from Buys to Sells, Sell to Buy, etc.

SL + FT - SL present, but trade is held until a reverse signal is presented.

How good is it?

We have some really positive back testing data across a range of pairs and markets - equities and indices too.

Drop me a DM to see these and I'll be happy to share.

Below let me show you a screen shot of how this can work for you.

How do you access this?

Please visit our website for signup / purchase information in the first instance (the link is on our trading view signature) or send us a private message on here - its impossible to keep track of comments on our posts so to ensure we don't miss you, a private DM will be great please.

The Back test shown on this example is based on the Trading View mid price and also a realistic starting Capital of £10,000. This test result is also based on a 0.1% risk per trade, with a 5 tick spread and a commission of

Regards

Darren

Disclaimer alert.

Please remember past performance is exactly that - how our strategy performed over those dates tested, it is not obviously a guarantee of future performance. Most of our H1 data is valid from Jan 2017 to now - so 4+ years and data on 650+ trades per pair.

Combo Backtest 123 Reversal & Laguerre-based RSI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is RSI indicator which is more sesitive to price changes.

It is based upon a modern math tool - Laguerre transform filter.

With help of Laguerre filter one becomes able to create superior

indicators using very short data lengths as well. The use of shorter

data lengths means you can make the indicators more responsive to

changes in the price.

WARNING:

- For purpose educate only

- This script to change bars colors.

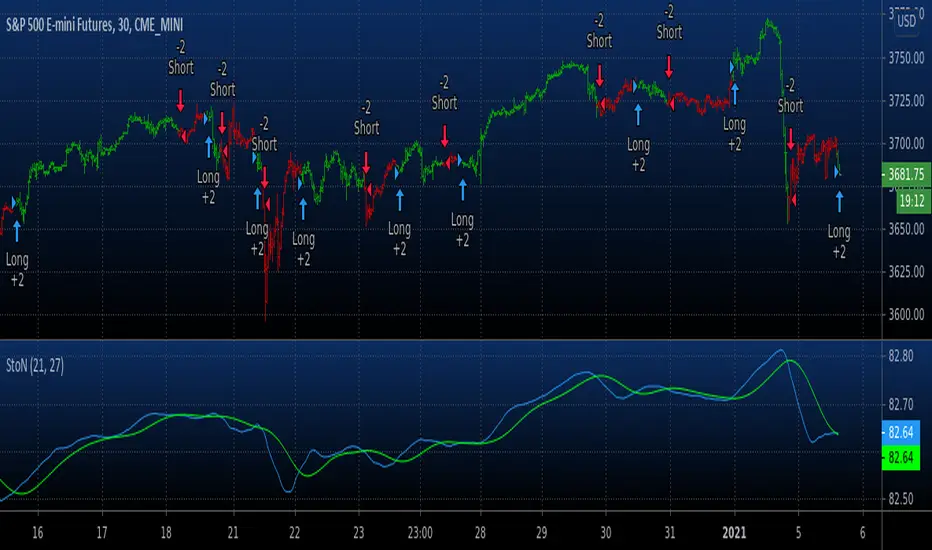

Combo Backtest 123 Reversal & Signal To Noise This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The signal-to-noise (S/N) ratio.

And Simple Moving Average.

WARNING:

- For purpose educate only

- This script to change bars colors.

Strategy- Double Decker RSIThis Strategy was LIVE coded during a webinar conducted by the author on 16-Jan-21 titled Backtesting in Tradingview. The system is named " Double Decker RSI ".

The rules of this strategy are:

LONG - RSI(5)>70 and RSI(14)>50 -- EXIT: RSI(5)<55

SHORT - RSI(5)<40 and RSI(14)<50 -- EXIT: RSI(5)>45

Instrument - BANKNIFTY - 1 HR Chart

The code is open source for you to edit and make changes as needed. For details on the strategy and webinar, you can refer to the website in signature of this strategy.

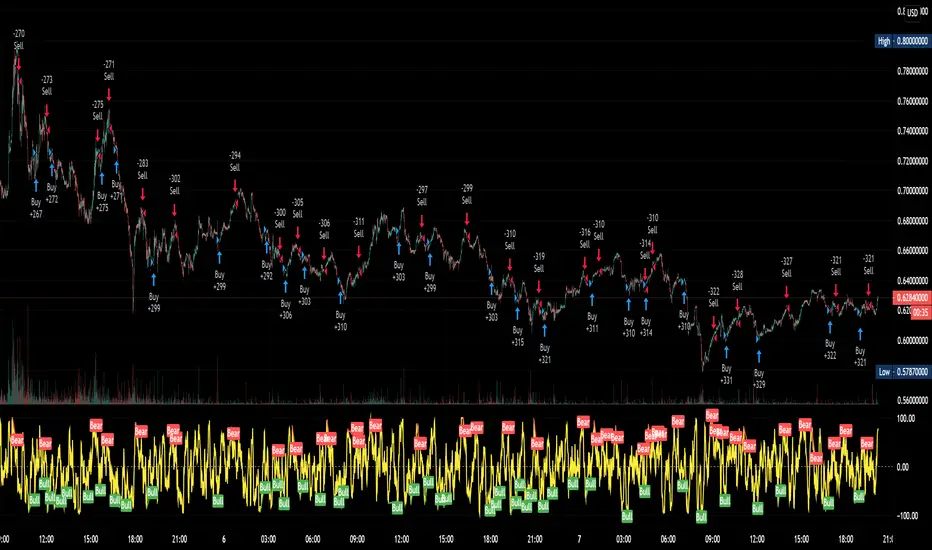

B1rd's Bitcoin Dominance OscillatorA Bitcoin Dominance Oscillator.

*OPTIMAL SETTINGS HAVE YET TO BE DISCOVERED"

Best used on BTC pairs.

The moving line is called the initiator line

Usage is simple: When line turns green you buy alts with bitcoin, When the line turns red you sell alts for bitcoin.

Functions:

Select a wide range of MA's for your Bitcoin dominance source and your initiator line.

Seperately set your MA length's.

A customizable noise filter (Value 0 = off)

Full description:

This indicator calculates the difference between the BTC.D and the selected moving average of BTC.D.

The units on the right represent the % of the BTC.D it moves above or below the MA.

For the purpose of trading alts I have swapped the positive and negative values. So when BTC.D starts moving up, the initiator line should point down in the negative. When BTC.D starts moving down, the initiator line will point up in the positive.

Ultimate Oscillator [Long] StrategyAfter I published Short Selling strategy with RSIofUO , I have been working for Long side strategy with same indicator.

but for Long strategy , I have used only the Ultimate Oscillator ... (Not the RSI of UO)

Logic behind this is , when UO goes below oversold level , high chance of possible reversal from there ...

Ultimate Oscialltor values , I have used are 5, 10 and 15

Signal Line 9

Above values are best/defaulted based on testing the strategy multiple symbols

BUY

when UO crossing up buyLine and close > open ( if the cross over is already done , it will wait for 3 candles to see a green bar i.e close>open )

Note when the bar color changes to orange , that means startegy is ready to take LONG position on next bar. But dont jump here , waith for the startegy take the Long Position :-)

Add

Signal appears when there is divergence (marked in yellow color ) ... strategy doesnt add the position , it is ony indicating you could add to existing OR if you missed the BUY signal you could enter here

Partial Exit

when UO crossing down partial exit level

Exit

When UO crossing down sell line

StopLoss

stop loss defaulted to 3%

Please note , I have slightly modified stop loss exit in this strategy.

Even though price hits 3% stoploss , strategy wont wind up the position ...

First , it will check if RSIofUO is above 30 , then it will hold on to the Long position.

Very reason behind this is , price is falling down and UO is going up ... That means there is bullish divergence here .. so it might turn this losing position to profitable one or will exit you with less than 3% loss.

Tested with SPY , QQQ , TSLA on 30mins to 4hrs. Though winning rate is average , net profit is exponential ...

Best working on 30 mins and 1 HR chart for QQQ

Warning

For the eductional purposes only ...

This is not a financial advise , before taking trading decission please do your own research

scalping low lag tema etalCredit for original idea goes to 1 min forex scalping by mikegoryunov

Changes include several lower lag filters (See line 3 for a list)

and values for profit, loss, and trail_points (See lines 48:53)

a, b, & c represent fast, medium, and slow filters. Basic idea is to monitor

crossovers of the three filters to determine buy/sells. Exits occur quickly within

the next time interval.

Note that this may be used for stocks and forex. The time interval can vary widely.

I have concerns about how to incorporate transaction costs with so many transactions.

Backtest Signal To Noise This source code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

© HPotter 05/01/2021

The signal-to-noise (S/N) ratio.

And Simple Moving Average.

Thank you for idea BlockchainYahoo

WARNING:

- For purpose educate only

- This script to change bars colors.

EURUSD DinhChienFX's signal V4.0Risk/reward: 1/1.3 | Entry by: Upper/Lower | Keltner crossing: 2 | Candle not entry: 80% | Stochastic: 70/15 | Adx: 31/9/9 | Notrade friday

Max risk: 3% - Risk / reward: 1 / 1.3.

1. Trend identification:

... Keltner: Price Through Upper / Lower 1 gives 1 point. 2 points are eligible for entry.

... Stochastic:

...... k> 70: Uptrend. k <15: Down trend.

... ADX: 31 provides strong trend following signal.

2. Entry point:

... Price corrects to Upper / Lower when 3 conditions Keltner , Stochastic & ADX indicator meet.

3. Not trade friday.

-------------

"Use the link below to obtain access to this indicator" or "PM us to obtain access"

Maximized Moving Average Crossing (by Coinrule)Using the crossings of two Moving Averages to trade in a trading strategy is a Trend-Following approach. As the name would suggest, to be successful, it requires the asset to be on-trend.

The general limit of a common strategy based on Moving Averages is that they underperform when the market is less volatile or trading sideways. When volatility compresses, the indicators get very close one to another, crossing each other very often. That's exactly the condition when trend-following strategies underperform.

To improve this strategy, it's useful to filter the buy signal using the RSI. When the RSI is close to overbought conditions, that means that the coin is likely trading in an uptrend. Strong uptrends usually come with RSI values that stay overbought for long periods, creating interesting opportunities.

Setup

Buy condition: the MA9 crosses above the MA50, and at the same time, the RSI has a value greater than 55.

Sell condition: the MA9 crosses below the MA50.

The strategy is optimized to provide better results on the 1-hr time frame, but it could work well also on higher time frames, such as the 4-hrs.

The strategy assumes each order to trade 30% of the available capital and opens a trade at a time. A trading fee of 0.1% is taken into account.

Oscilator candles - momentum strategyThis is momentum based strategy based on indicators published earlier:

Also trying to use delayed supertrend based on steps as mentioned in the published indicator:

Added option to filter trade entries based on higher timeframe pivots. But, it is not so effective and may need further optimization.