Overnight Gap Dominance Indicator (OGDI)The Overnight Gap Dominance Indicator (OGDI) measures the relative volatility of overnight price gaps versus intraday price movements for a given security, such as SPY or SPX. It uses a rolling standard deviation of absolute overnight percentage changes divided by the standard deviation of absolute intraday percentage changes over a customizable window. This helps traders identify periods where overnight gaps predominate, suggesting potential opportunities for strategies leveraging extended market moves.

Instructions

A

pply the indicator to your TradingView chart for the desired security (e.g., SPY or SPX).

Adjust the "Rolling Window" input to set the lookback period (default: 60 bars).

Modify the "1DTE Threshold" and "2DTE+ Threshold" inputs to tailor the levels at which you switch from 0DTE to 1DTE or multi-DTE strategies (default: 0.5 and 0.6).

Observe the OGDI line: values above the 1DTE threshold suggest favoring 1DTE strategies, while values above the 2DTE+ threshold indicate multi-DTE strategies may be more effective.

Use in conjunction with low VIX environments and uptrend legs for optimal results.

Options

SPX → NQ Levels ConverterSPX → NQ Levels Converter is a Pine Script indicator that projects key S&P 500 (SPX) levels onto the NASDAQ 100 (NQ) chart using a configurable conversion ratio.

• Dynamic ratio: calculates the live SPX/NQ ratio in real time.

• Static ratio: allows manual input of a fixed ratio.

• Supports up to 10 custom SPX levels, automatically converted into their equivalent NQ values.

• Each level is displayed with a line and label (SPX → NQ) with independent color settings.

• Advanced visualization controls:

• line extension (right, left, both, or fixed)

• line length & placement

• label side & offset.

• Lines and labels auto-update on every bar to stay accurate over time.

Use case: particularly useful for traders who track SPX option levels or support/resistance zones but execute trades on the NQ.

Monthly Expected Move (IV + Realized)What it does

Overlays 1-month expected move bands on price using both forward-looking options data and backward-looking realized movement:

IV30 band — from your pasted 30-day implied vol (%)

Straddle band — from your pasted ATM ~30-DTE call+put total

HV band — from Historical Volatility computed on-chart

ATR band — from ATR% extrapolated to ~1 trading month

Use it to quickly answer: “How much could this stock move in ~1 month?” and “Is the market now pricing more/less movement than we’ve actually been getting?”

Inputs (quick)

Implied (forward-looking)

Use IV30 (%) — paste annualized IV30 from your options platform.

Use ATM 30-DTE Straddle — paste Call+Put total (per share) at the ATM strike, ~30 DTE.

Realized (backward-looking)

HV lookback (days) — default 21 (≈1 trading month).

ATR length — default 14.

Note: TradingView can’t fetch option data automatically. Paste the IV30 % or the straddle total you read from your broker (use Mark/mid prices).

How it’s calculated

IV band (±%) = IV30 × √(21/252) (annualized → ~1-month).

Straddle band (±%) = (ATM Call + Put) / Spot to that expiry (≈30 DTE).

HV band (±%) = stdev(log returns, N) × √252 × √(21/252).

ATR band (±%) = (ATR(len)/Close) × √21.

All bands are plotted as upper/lower envelopes around price, plus an on-chart readout of each ±% for quick scanning.

How to use it (at a glance)

IV/Straddle bands wider than HV/ATR → market expects bigger movement than recent actuals (possible catalyst/expansion).

All bands narrow → likely a low-mover; look elsewhere if you want action.

HV > IV → realized swings exceed current pricing (mean-reversion or vol bleed often follows).

Pro tips

For ATM straddle: pick the expiry closest to ~30 DTE, use the ATM strike (closest to spot), and add Call Mark + Put Mark (per share). If the exact ATM strike isn’t quoted, average the two neighboring strikes.

The simple straddle/spot heuristic can read slightly below the IV-derived 1σ; that’s normal.

Keep the chart on daily timeframe—the math assumes trading-day conventions (~252/yr, ~21/mo).

Volume Imbalance Heatmap + Delta Cluster [@darshakssc]🔥 Volume Imbalance Heatmap + Delta Cluster

Created by: @darshakssc

This indicator is designed to visually reveal institutional pressure zones using a combination of:

🔺 Delta Cluster Detection: Highlights candles with strong body ratios and volume spikes, helping identify aggressive buying or selling activity.

🌡️ Real-Time Heatmap Overlay: Background color dynamically adjusts based on volume imbalance relative to its moving average.

🧠 Adaptive Dashboard: Displays live insights into current market imbalance and directional flow (Buy/Sell clusters).

📈 How It Works:

A candle is marked as a Buy Cluster if it closes bullish, has a strong body, and exhibits a volume spike above average.

A Sell Cluster triggers under the inverse conditions.

The heatmap shades the chart background to reflect areas of high or low imbalance using a color gradient.

⚙️ Inputs You Can Adjust:

Volume MA Length

Minimum Body Ratio

Imbalance Multiplier Sensitivity

Dashboard Location

🚫 Note: This is not a buy/sell signal tool, but a visual aid to support institutional flow tracking and confluence with your existing system.

For educational use only. Not financial advice.

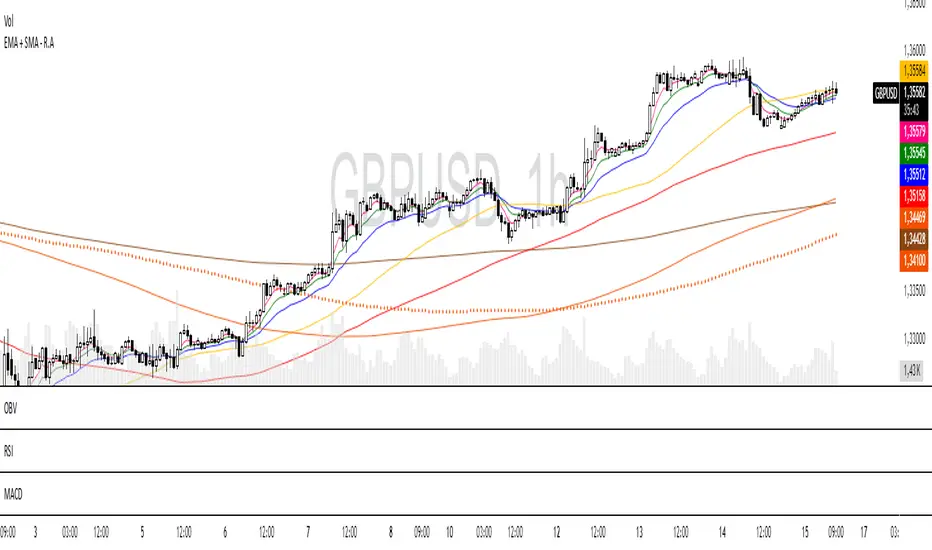

EMA + SMA - R.AR.A. Trader - Multi-MA Suite (EMA & SMA)

1. Overview

Welcome, students of R.A. Trader!

This indicator is a powerful and versatile tool designed specifically to support the trading methodologies taught by Rudá Alves. The R.A. Trader Multi-MA Suite combines two fully customizable groups of moving averages into a single, clean indicator.

Its purpose is to eliminate chart clutter and provide a clear, at-a-glance view of market trends, momentum, and dynamic levels of support and resistance across multiple timeframes. By integrating key short-term and long-term moving averages, this tool will help you apply the R.A. Trader analytical framework with greater efficiency and precision.

2. Core Features

Dual Moving Average Groups: Configure two independent sets of moving averages, perfect for separating short-term (EMA) and long-term (SMA) analysis.

Four MAs Per Group: Each group contains four fully customizable moving averages.

Multiple MA Types: Choose between several types of moving averages for each group (SMA, EMA, WMA, HMA, RMA).

Toggle Visibility: Easily show or hide each group with a single click in the settings panel.

Custom Styling: Key moving averages are styled for instant recognition, including thicker lines for longer periods and a special dotted line for the 250-period SMA.

Clean and Efficient: The code is lightweight and optimized to run smoothly on the TradingView platform.

Group 1 (Default: EMAs)

This group is pre-configured for shorter-term Exponential Moving Averages but is fully customizable.

Setting Label Description

MA Type - EMA Select the type of moving average for this entire group (e.g., EMA, SMA).

EMA 5 Sets the period for the first moving average.

EMA 10 Sets the period for the second moving average.

EMA 20 Sets the period for the third moving average.

EMA 400 Sets the period for the fourth moving average.

Show EMA Group A checkbox to show or hide all MAs in this group.

Exportar para as Planilhas

Group 2 (Default: SMAs)

This group is pre-configured for longer-term Simple Moving Averages, often used to identify major trends.

Setting Label Description

MA Type - SMA Select the type of moving average for this entire group.

SMA 50 Sets the period for the first moving average.

SMA 100 Sets the period for the second moving average.

SMA 200 Sets the period for the third moving average.

SMA 250 Sets the period for the fourth moving average (styled as a dotted line).

Show SMA Group A checkbox to show or hide all MAs in this group.

Exportar para as Planilhas

Index Options Expirations and Calendar EffectsFeatures

- Highlights monthly equity options expiration (opex) dates.

- Marks VIX options expiration dates based on standard 30-day offset.

- Shows configurable vanna/charm pre-expiration window (green shading).

- Shows configurable post-opex weakness window (red shading).

- Adjustable colors, start/end offsets, and on/off toggles for each element.

What this does

This overlay highlights option-driven calendar windows around monthly equity options expiration (opex) and VIX options expiration. It draws:

- Solid blue lines on the third Friday of each month (typical monthly opex).

- Dashed orange lines on the Wednesday ~30 days before next month’s opex (typical VIX expiration schedule).

- Green shading during a pre-expiration window when vanna/charm effects are often strongest.

- Red shading during the post-expiration "window of non-strength" often observed into the Tuesday after opex.

How it works

1. Monthly opex is detected when Friday falls between the 15th–21st of the month.

2. VIX expiration is calculated by finding next month’s opex date, then subtracting 30 calendar days and marking that Wednesday.

3. Vanna/charm window (green) : starts on the Monday of the week before opex and ends on Tuesday of opex week.

4. Post-opex weakness window (red) : starts Wednesday of opex week and ends Tuesday after opex.

How to use

- Add to any chart/timeframe.

- Adjust inputs to toggle VIX/opex lines, choose colors, and fine-tune the start/end offsets for shaded windows.

- This is an educational visualization of typical timing and not a trading signal.

Limitations

- Exchange holidays and contract-specific exceptions can shift expirations; this script uses standard calendar rules.

- No forward-looking data is used; all dates are derived from historical and current bar time.

- Past patterns do not guarantee future behavior.

Originality

Provides a single, adjustable visualization combining opex, VIX expiration, and configurable vanna/charm/weakness windows into one tool. Fully explained so non-coders can use it without reading the source code.

Straddle Charts - Live (Enhanced)Track options straddles with ease using the Straddle Charts - Live (Enhanced) indicator! Originally inspired by @mudraminer, this Pine Script v5 tool visualizes live call, put, and straddle prices for instruments like BANKNIFTY. Plotting call (green), put (red), and straddle (black) prices in a separate pane, it offers real-time insights for straddle strategy traders.

Key Features:

Live Data: Fetches 1-minute (customizable) option prices with error handling for invalid symbols.

Price Table: Displays call, put, straddle prices, and percentage change in a top-left table.

Volatility Alerts: Highlights bars with straddle price changes above a user-defined threshold (default 5%) with a yellow background and concise % labels.

Robust Design: Prevents plot errors with na checks and provides clear error messages.

How to Use: Input your call/put option symbols (e.g., NSE:NIFTY250814C24700), set the timeframe, and adjust the volatility threshold. Monitor straddle costs and volatility for informed trading decisions.

Perfect for options traders seeking a simple, reliable tool to track straddle performance. Check it out and share your feedback!

13/48 EMA Trading Scalper (ATR TP/SL)13/48 EMA Trading Scalper (ATR TP/SL)

What it does:

This tool looks for price “touches” of the 13-EMA, only takes CALL entries when the 13 is above the 48 (uptrend) and PUT entries when the 13 is below the 48 (downtrend), and confirms with a simple candle pattern (green > red with expansion for calls, inverse for puts). Touch sensitivity is ATR-scaled, so signals adapt to volatility. Each trade gets auto-drawn entry, TP, and SL lines, colored labels with $ / % distance from entry, plus optional TP/SL hit alerts. A rotating color palette and per-bar label staggering help keep the chart readable. Old objects are auto-pruned via maxTracked.

How it works

Trend filter: 13-EMA vs 48-EMA.

Entry: ATR-scaled touch of the 13-EMA + candle confirmation.

Risk: TP/SL = ATR multiples you control.

Visuals: Entry/TP/SL lines (extend right), vertical entry marker (optional), multi-line labels.

Hygiene: maxTracked keeps only the last N trades’ objects; labels are staggered to reduce overlap.

Alerts: Buy Call, Buy Put, Take Profit Reached, Stop Loss Hit.

Key Inputs

Fast EMA (13), Trend EMA (48), ATR Length (14)

Touch Threshold (x ATR) – how close price must come to the EMA

Take Profit (x ATR), Stop Loss (x ATR)

maxTracked – number of recent trades to keep on chart

Tips

Start with Touch = 0.10–0.20 × ATR; TP=2×ATR, SL=1×ATR, then tune per symbol/timeframe.

Works on intraday and higher TFs; fewer, cleaner signals on higher TFs.

This is an indicator, not a broker—always backtest and manage risk.

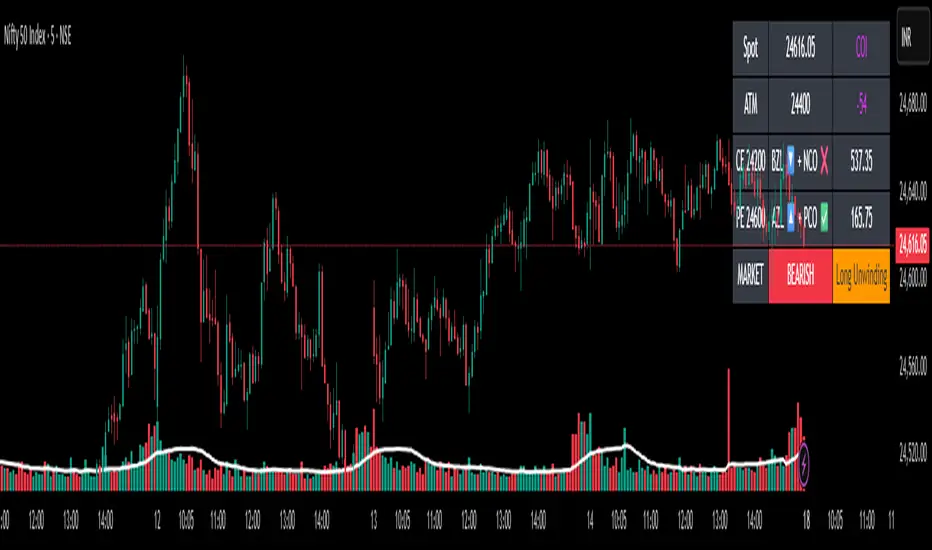

✨Smart Option MACD: Bullish, Bearish, Neutral Logic by AKM ✨The **Smart Option MACD: Bullish, Bearish, Neutral Logic by AKM** is an advanced indicator designed for TradingView, tailored for option traders on indices like NIFTY. It automates options trend scanning by applying MACD analysis to both Call (CE) and Put (PE) options near the ATM (At-The-Money) strike, providing actionable market states—Bullish, Bearish, or Neutral—using distinct logic for both strikes and overall market context.

***

### Core Features

- **Option Selection Logic:** The script dynamically calculates ATM, CE, and PE strike prices based on the underlying index spot price and customizable user inputs for expiry, strike distance, and OTM/ITM shift.

- **MACD on Option Prices:** For both CE and PE symbols, the indicator computes the MACD (Moving Average Convergence Divergence) and Signal lines. It uses standard MACD settings: 12-period EMA (fast), 26-period EMA (slow), and 9-period Signal.

- **Strike Status Classification:**

- AZL 🔼: Indicates MACD > 0 for that option, signifying positive momentum.

- BZL 🔽: Indicates MACD 0 & crossover up), PE is bearish (MACD<0 & crossover down).

- **Bearish:** PE is bullish & crossover up, CE is bearish & crossover down.

- **Neutral:** All other scenarios—including mixed or undefined signals.

***

### Table Output

A real-time table is displayed on the chart (top-right) with key option and market details:

- Spot price

- ATM Strike

- CE/PE strike status (momentum + crossover logic)

- Option prices

- Overall market state, color-coded for clarity

***

### How to Use This Indicator

- **Entry Signal:** Use the Bullish/Bearish status for directional trades or option strategies. Bullish calls for buying or selling upward momentum options; Bearish favors downside trades. Neutral advises caution or range-bound trades.

- **Customizability:** Expiry, strike width, OTM/ITM offset, and chart resolution are user-controlled, allowing adaptation to different market contexts.

- **Best Practice:** Use alongside price action, support/resistance zones and other indicators to confirm options momentum, as MACD is powerful yet not infallible.

***

### Who Is It For?

- **Option traders** who want to automate trend/momentum detection for CE/PE strikes instead of manual chart switching.

- **Index traders** (NIFTY, BANKNIFTY...) seeking systematic edge in intraday/positional strategies tied to option momentum.

- **Technical analysts** interested in visual, rule-based signals combining options data and classic MACD logic.

***

The Smart Option MACD indicator streamlines multi-strike, multi-option momentum analysis and presents clear actionable logic directly on your chart for enhanced decision-making. Use it as a core part of your TradingView toolkit for options-focused market views.

RSI 20/80 Arrows + AlertsRSI 20/80 Arrows + Alerts

This indicator is a modified Relative Strength Index (RSI) tool designed to help traders spot potential overbought and oversold conditions using customizable threshold levels (default 80 for overbought, 20 for oversold).

Features:

Custom RSI Levels – Default to 80/20 instead of the standard 70/30, but fully adjustable by the user.

Visual Signals –

Blue Arrow Up appears below the bar when RSI crosses up from below the oversold level (potential buy zone).

Red Arrow Down appears above the bar when RSI crosses down from above the overbought level (potential sell zone).

Alerts Built In – Receive notifications when either signal occurs, with the option to confirm signals only on bar close for reduced noise.

Guide Levels – Optionally display overbought/oversold reference lines on the chart for quick visual reference.

Overlay Mode – Signals are plotted directly on the price chart, so you don’t need to switch between chart windows.

Use Case:

Ideal for traders who want quick, visual confirmation of potential turning points based on RSI, especially in strategies where more extreme levels (like 20/80) help filter out weaker signals. Works well across all markets and timeframes.

Price Level Alert System

Price Level Alert System - Manage Multiple Price Alerts in One

This indicator is designed to simplify price level monitoring by allowing you to manage up to 5 different price alerts through a single, unified alert system. Instead of creating multiple separate alerts for different price levels, you can now monitor all your key levels with just one alert subscription.

Key Benefits:

Unified Alert Management - Monitor 5 price levels with a single alert, saving your valuable alert slots

Clean Chart Interface - Toggle price levels on/off without cluttering your chart

Smart Alert Types - Get notified for price crosses (above/below) and approaching alerts

Customizable Appearance - Adjust colors, transparency, and line width for each level individually

Efficient Workflow - Inline controls make setup quick and intuitive

Perfect For:

Traders monitoring multiple support/resistance levels

Swing traders tracking key price targets

Day traders needing quick alert setup

Anyone wanting to maximize their TradingView alert efficiency

How It Works:

Simply enter your desired price levels, check the boxes to enable them, and click the bell icon to activate alerts. The indicator will monitor all enabled levels and send notifications through a single alert when price action occurs at any of your specified levels.

Features:

5 independent price levels

Individual on/off toggles

Approaching distance alerts (customizable percentage)

Cross above/below notifications

Professional line styling options

Status line price display

Save your alert slots and streamline your trading workflow with this efficient price level monitoring solution. Whether you're tracking support/resistance, psychological levels, or price targets, this indicator helps you stay informed without the complexity of managing multiple individual alerts.

ICT/SMC Liquidity Map V3 KyroowThe indicator is designed to map liquidity on the chart following the ICT/SMC logic, with the added feature of precise tracking of the Asian session.

It shows you:

PDH / PDL → Previous Day High & Low, automatically removed once taken out.

EQH / EQL → Equal Highs & Equal Lows (double tops/bottoms), with pip tolerance and a check to ensure no candle has already "cleared" the range.

ASH / ASL → Asian Session High & Low (the highs/lows of each closed Asian session).

Asian Session → Displayed as a box or shaded area, with visual history.

Dynamic tolerance management → EQH/EQL can have different tolerances depending on the timeframe.

Automatic removal → Levels are removed once the market takes them (via wick or body, configurable).

💡 In practice:

It helps you quickly identify likely liquidity grab zones, whether they come from the previous day, the Asian session, or equal highs/lows. This allows you to anticipate market reactions around these levels.

GLD GC Price Converter Its primary function is to fetch the prices of the Gold ETF (ticker: GLD) and Gold Futures (ticker: GC1!) and then project significant price levels from one or both of these assets onto the chart of whatever instrument you are currently viewing.

Core Functionality & Features

Dual Asset Tracking: The script simultaneously tracks the prices of GLD and Gold Futures (GC).

Dynamic Price Level Projection: The script's main feature is its ability to calculate and draw horizontal price levels. It determines a "base price" (e.g., the nearest $100 level for GC) and then draws lines at specified increments above and below it. The key is that these levels are projected onto the current chart's price scale.

On-Chart Information Display:

Price Table: A customizable table can be displayed in any corner of the chart, showing the current prices of GLD and GC. It can also show the daily percentage change for GC, colored green for positive changes and red for negative ones.

Last Price Label: It can show a label next to the most recent price bar that displays the current prices of both GLD and GC.

Extensive Customization: The user has significant control over the indicator's appearance and behavior through the settings panel.

This includes:

Toggling the display for GLD and GC levels independently.

Adjusting the multiplier for the price levels (e.g., show levels every $100 or $50 for GC).

Changing the colors, line styles (solid, dashed, dotted), and horizontal offset for the labels.

Defining the number of price levels to display.

Controlling the text size for labels and the table.

Choosing whether the script updates on every tick or only once per candle close for better performance.

💎 ENJOYBLUE ⏰ Open Price AlertThis Pine Script (version 6) is designed for TradingView to monitor the closing of a user-selected Timeframe (TF) — for example, M30, H1, H4, or D1 — and trigger an alert immediately when that TF’s candle closes. Along with the alert, it displays the current open prices from four higher-level timeframes:

Open MN: Open price of the current monthly candle

Open W1: Open price of the current weekly candle

Open D1: Open price of the current daily candle

Open H4: Open price of the current 4-hour candle

The alert message is formatted into a single compact line to ensure it is fully visible on mobile devices!

~ENJOYBLUE 💎

TCP | Market Session | Session Analyzer📌 TCP | Market Session Indicator | Crypto Version

A powerful, real-time market session visualization tool tailored for crypto traders. Track the heartbeat of Asia, Europe, and US trading hours directly on your chart with live session boxes, behavioral analysis, liquidity grab detection, and countdown timers. Know when the action starts, how the market behaves, and where the traps lie.

🔰 Introduction:

Trade the Right Hours with the Right Tools

Time matters in trading. Most significant moves happen during key sessions—and knowing when and how each session unfolds can give you a sharp edge. The TCP Market Session Indicator, developed by Trade City Pro (TCP), puts professional session tracking and behavioral insights at your fingertips.

Whether you're a scalper or swing trader, this indicator gives you the timing context to enter and exit trades with greater confidence and clarity.

🕒 Core Features

• Live Session Boxes :

Highlight active ranges during Asia, Europe, and US sessions with dynamic high/low updates.

• Session Start/End Labels :

Know exactly when each session begins and ends plotted clearly on your chart with context.

• Session Behavior Analysis :

At the end of each session, the indicator classifies the price action as:

- Trend Up

- Trend Down

- Consolidation

- Manipulation

• Liquidity Grab Detection: Automatically detects possible stop hunts (fake breakouts) and marks them on the chart with precision filters (volume, ATR, reversal).

• Session Countdown Table: A live dashboard showing:

- Current active session

- Time left in session

- Upcoming session and how many minutes until it starts

- Utility time converter (e.g. 90 min = 01:30)

• Vertical Session Lines: Visualize past and upcoming session boundaries with customizable history and future range.

• Multi-Day Support: Draw session ranges for previous, current, and future days for better backtesting and forecasting.

⚙️ Settings Panel

Customize everything to fit your trading style and schedule:

• Session Time Settings:

Set the opening and closing time for each session manually using UTC-based minute inputs.

→ For example, enter Asia Start: 0, Asia End: 480 for 00:00–08:00 UTC.

This gives full flexibility to adjust session hours to match your preferred market behavior.

• Enable or Disable Elements:

Toggle the visibility of each session (Asia, Europe, US), as well as:

- Session Boxes

- Countdown Table

- Session Lines

- Liquidity Grab Labels

• Timezone Selection:

Choose between using UTC or your chart’s local timezone for session calculations.

• Customization Options:

Select number of past and future days to draw session data

Adjust vertical line transparency

Fine-tune label offset and spacing for clean layout

📊 Smart Session Boxes

Each session box tracks high, low, open, and close in real time, providing visual clarity on market structure. Once a session ends, the box closes, and the behavior type is saved and labeled ideal for spotting patterns across sessions.

• Asia: Green Box

• Europe: Orange Box

• US: Blue Box

💡 Why Use This Tool?

• Perfect Timing: Don’t get chopped in low-liquidity hours. Focus on sessions where volume and volatility align.

• Pattern Recognition: Study how price behaves session-to-session to build better strategies.

• Trap Detection: Spot manipulation moves (liquidity grabs) early and avoid common retail pitfalls.

• Macro Session Mapping: Use as a foundational layer to align trades with market structure and news cycles.

🔍 Example Use Case

You're watching BTC at 12:45 UTC. The indicator tells you:

The Asia session just ended (label shows “Asia Session End: Trend Up”)

Europe session starts in 15 minutes

A liquidity grab just triggered at the previous high—label confirmed

Now you know who’s active, what the market just did, and what’s about to start—all in one glance.

✅ Why Traders Trust It

• Visual & Intuitive: Fully chart-based, no clutter, no guessing

• Crypto-Focused: Designed specifically for 24/7 crypto markets (not outdated forex models)

• Non-Repainting: All labels and boxes stay as printed—no tricks

• Reliable: Tested across multiple exchanges, pairs, and timeframes

🧩 Built by Trade City Pro (TCP)

The TCP Market Session Indicator is part of a suite of professional tools used by over 150,000 traders. It’s coded in Pine Script v6 for full compatibility with TradingView’s latest capabilities.

🔗 Resources

• Tutorial: Learn how to analyze sessions like a pro in our TradingView guide:

"TradeCityPro Academy: Session Mapping & Liquidity Traps"

• More Tools: Explore our full library of indicators on

SquirrelofwallstreetAlien technologia

possible strategic entrie

English:

This content is provided for informational purposes only. We disclaim any responsibility for how it may be used. Please consult a qualified professional for any specific advice.

Ayman – Full Smart Suite Auto/Manual Presets + PanelIndicator Name

Ayman – Full Smart Suite (OB/BoS/Liq/FVG/Pin/ADX/HTF) + Auto/Manual Presets + Panel

This is a multi-condition trading tool for TradingView that combines advanced Smart Money Concepts (SMC) with classic technical filters.

It generates BUY/SELL signals, draws Stop Loss (SL) and Take Profit (TP1, TP2) levels, and displays a control panel with all active settings and conditions.

1. Main Features

Smart Money Concepts Filters:

Order Block (OB) Zones

Break of Structure (BoS)

Liquidity Sweeps

Fair Value Gaps (FVG)

Pin Bar patterns

ADX filter

Higher Timeframe EMA filter (HTF EMA)

Two Operating Modes:

Auto Presets: Automatically adjusts all settings (buffers, ATR multipliers, RR, etc.) based on your chart timeframe (M1/M5/M15).

Manual Mode: Fully customize all parameters yourself.

Trade Management Levels:

Stop Loss (SL)

TP1 – partial profit

TP2 – full profit

Visual Panel showing:

Current settings

Filter status

Trend direction

Last swing levels

SL/TP status

Alerts for BUY/SELL conditions

2. Entry Conditions

A BUY signal is generated when all these are true:

Trend: Price above EMA (bullish)

HTF EMA: Higher timeframe trend also bullish

ADX: Trend strength above threshold

OB: Price in a valid bullish Order Block zone

BoS: Structure break to the upside

Liquidity Sweep: Sweep of recent lows in bullish context

FVG: A bullish Fair Value Gap is present

Pin Bar: Bullish Pin Bar pattern detected (if enabled)

A SELL signal is generated when the opposite conditions are met.

3. Stop Loss & Take Profits

SL: Placed just beyond the last swing low (BUY) or swing high (SELL), with a small ATR buffer.

TP1: Partial profit target, defined as a ratio of the SL distance.

TP2: Full profit target, based on Reward:Risk ratio.

4. How to Use

Step 1 – Apply Indicator

Open TradingView

Go to your chart (recommended: XAUUSD, M1/M5 for scalping)

Add the indicator script

Step 2 – Choose Mode

AUTO Mode: Leave “Use Auto Presets” ON – parameters adapt to your timeframe.

MANUAL Mode: Turn Auto OFF and adjust all lengths, buffers, RR, and filters.

Step 3 – Filters

In the Filters On/Off section, enable/disable specific conditions (OB, BoS, Liq, FVG, Pin Bar, ADX, HTF EMA).

Step 4 – Trading the Signals

Wait for a BUY or SELL arrow to appear.

SL and TP levels will be plotted automatically.

TP1 can be used for partial close and TP2 for full exit.

Step 5 – Alerts

Set alerts via BUY Signal or SELL Signal to receive notifications.

5. Best Practices

Scalping: Use M1 or M5 with AUTO mode for gold or forex pairs.

Swing Trading: Use M15+ and adjust buffers/ATR manually.

Combine with price action confirmation before entering trades.

For higher accuracy, wait for multiple filter confirmations rather than acting on the first arrow.

6. Summary Table

Feature Purpose Can Disable?

Order Block Finds key supply/demand zones ✅

Break of Structure Detects trend continuation ✅

Liquidity Sweep Finds stop-hunt moves ✅

Fair Value Gap Confirms imbalance entries ✅

Pin Bar Price action reversal filter ✅

ADX Trend strength filter ✅

HTF EMA Higher timeframe confirmation ✅

Crypto Options Greeks & Volatility Analyzer [BackQuant]Crypto Options Greeks & Volatility Analyzer

Overview

The Crypto Options Greeks & Volatility Analyzer is a comprehensive analytical tool that calculates Black-Scholes option Greeks up to the third order for Bitcoin and Ethereum options. It integrates implied volatility data from VOLMEX indices and provides multiple visualization layers for options risk analysis.

Quick Introduction to Options Trading

Options are financial derivatives that give the holder the right, but not the obligation, to buy or sell an underlying asset at a predetermined price (strike price) within a specific time period (expiration date). Understanding options requires grasping two fundamental concepts:

Call Options : Give the right to buy the underlying asset at the strike price. Calls increase in value when the underlying price rises above the strike price.

Put Options : Give the right to sell the underlying asset at the strike price. Puts increase in value when the underlying price falls below the strike price.

The Language of Options: Greeks

Options traders use "Greeks" - mathematical measures that describe how an option's price changes in response to various factors:

Delta : How much the option price moves for each $1 change in the underlying

Gamma : How fast delta changes as the underlying moves

Theta : Daily time decay - how much value erodes each day

Vega : Sensitivity to implied volatility changes

Rho : Sensitivity to interest rate changes

These Greeks are essential for understanding risk. Just as a pilot needs instruments to fly safely, options traders need Greeks to navigate market conditions and manage positions effectively.

Why Volatility Matters

Implied volatility (IV) represents the market's expectation of future price movement. High IV means:

Options are more expensive (higher premiums)

Market expects larger price swings

Better for option sellers

Low IV means:

Options are cheaper

Market expects smaller moves

Better for option buyers

This indicator helps you visualize and quantify these critical concepts in real-time.

Back to the Indicator

Key Features & Components

1. Complete Greeks Calculations

The indicator computes all standard Greeks using the Black-Scholes-Merton model adapted for cryptocurrency markets:

First Order Greeks:

Delta (Δ) : Measures the rate of change of option price with respect to underlying price movement. Ranges from 0 to 1 for calls and -1 to 0 for puts.

Vega (ν) : Sensitivity to implied volatility changes, expressed as price change per 1% change in IV.

Theta (Θ) : Time decay measured in dollars per day, showing how much value erodes with each passing day.

Rho (ρ) : Interest rate sensitivity, measuring price change per 1% change in risk-free rate.

Second Order Greeks:

Gamma (Γ) : Rate of change of delta with respect to underlying price, indicating how quickly delta will change.

Vanna : Cross-derivative measuring delta's sensitivity to volatility changes and vega's sensitivity to price changes.

Charm : Delta decay over time, showing how delta changes as expiration approaches.

Vomma (Volga) : Vega's sensitivity to volatility changes, important for volatility trading strategies.

Third Order Greeks:

Speed : Rate of change of gamma with respect to underlying price (∂Γ/∂S).

Zomma : Gamma's sensitivity to volatility changes (∂Γ/∂σ).

Color : Gamma decay over time (∂Γ/∂T).

Ultima : Third-order volatility sensitivity (∂²ν/∂σ²).

2. Implied Volatility Analysis

The indicator includes a sophisticated IV ranking system that analyzes current implied volatility relative to its recent history:

IV Rank : Percentile ranking of current IV within its 30-day range (0-100%)

IV Percentile : Percentage of days in the lookback period where IV was lower than current

IV Regime Classification : Very Low, Low, High, or Very High

Color-Coded Headers : Visual indication of volatility regime in the Greeks table

Trading regime suggestions based on IV rank:

IV Rank > 75%: "Favor selling options" (high premium environment)

IV Rank 50-75%: "Neutral / Sell spreads"

IV Rank 25-50%: "Neutral / Buy spreads"

IV Rank < 25%: "Favor buying options" (low premium environment)

3. Gamma Zones Visualization

Gamma zones display horizontal price levels where gamma exposure is highest:

Purple horizontal lines indicate gamma concentration areas

Opacity scaling : Darker shading represents higher gamma values

Percentage labels : Shows gamma intensity relative to ATM gamma

Customizable zones : 3-10 price levels can be analyzed

These zones are critical for understanding:

Pin risk around expiration

Potential for explosive price movements

Optimal strike selection for gamma trading

Market maker hedging flows

4. Probability Cones (Expected Move)

The probability cones project expected price ranges based on current implied volatility:

1 Standard Deviation (68% probability) : Shown with dashed green/red lines

2 Standard Deviations (95% probability) : Shown with dotted green/red lines

Time-scaled projection : Cones widen as expiration approaches

Lognormal distribution : Accounts for positive skew in asset prices

Applications:

Strike selection for credit spreads

Identifying high-probability profit zones

Setting realistic price targets

Risk management for undefined risk strategies

5. Breakeven Analysis

The indicator plots key price levels for options positions:

White line : Strike price

Green line : Call breakeven (Strike + Premium)

Red line : Put breakeven (Strike - Premium)

These levels update dynamically as option premiums change with market conditions.

6. Payoff Structure Visualization

Optional P&L labels display profit/loss at expiration for various price levels:

Shows P&L at -2 sigma, -1 sigma, ATM, +1 sigma, and +2 sigma price levels

Separate calculations for calls and puts

Helps visualize option payoff diagrams directly on the chart

Updates based on current option premiums

Configuration Options

Calculation Parameters

Asset Selection : BTC or ETH (limited by VOLMEX IV data availability)

Expiry Options : 1D, 7D, 14D, 30D, 60D, 90D, 180D

Strike Mode : ATM (uses current spot) or Custom (manual strike input)

Risk-Free Rate : Adjustable annual rate for discounting calculations

Display Settings

Greeks Display : Toggle first, second, and third-order Greeks independently

Visual Elements : Enable/disable probability cones, gamma zones, P&L labels

Table Customization : Position (6 options) and text size (4 sizes)

Price Levels : Show/hide strike and breakeven lines

Technical Implementation

Data Sources

Spot Prices : INDEX:BTCUSD and INDEX:ETHUSD for underlying prices

Implied Volatility : VOLMEX:BVIV (Bitcoin) and VOLMEX:EVIV (Ethereum) indices

Real-Time Updates : All calculations update with each price tick

Mathematical Framework

The indicator implements the full Black-Scholes-Merton model:

Standard normal distribution approximations using Abramowitz and Stegun method

Proper annualization factors (365-day year)

Continuous compounding for interest rate calculations

Lognormal price distribution assumptions

Alert Conditions

Four categories of automated alerts:

Price-Based : Underlying crossing strike price

Gamma-Based : 50% surge detection for explosive moves

Moneyness : Deep ITM alerts when |delta| > 0.9

Time/Volatility : Near expiration and vega spike warnings

Practical Applications

For Options Traders

Monitor all Greeks in real-time for active positions

Identify optimal entry/exit points using IV rank

Visualize risk through probability cones and gamma zones

Track time decay and plan rolls

For Volatility Traders

Compare IV across different expiries

Identify mean reversion opportunities

Monitor vega exposure across strikes

Track higher-order volatility sensitivities

Conclusion

The Crypto Options Greeks & Volatility Analyzer transforms complex mathematical models into actionable visual insights. By combining institutional-grade Greeks calculations with intuitive overlays like probability cones and gamma zones, it bridges the gap between theoretical options knowledge and practical trading application.

Whether you're:

A directional trader using options for leverage

A volatility trader capturing IV mean reversion

A hedger managing portfolio risk

Or simply learning about options mechanics

This tool provides the quantitative foundation needed for informed decision-making in cryptocurrency options markets.

Remember that options trading involves substantial risk and complexity. The Greeks and visualizations provided by this indicator are tools for analysis - they should be combined with proper risk management, position sizing, and a thorough understanding of options strategies.

As crypto options markets continue to mature and grow, having professional-grade analytics becomes increasingly important. This indicator ensures you're equipped with the same analytical capabilities used by institutional traders, adapted specifically for the unique characteristics of 24/7 cryptocurrency markets.

Options Strategy V2.0📈 Options Strategy V2.0 – Intraday Reversal-Resilient Momentum System

Overview:

This strategy is designed specifically for intraday SPY, TSLA, MSFT, etc. options trading (0DTE or 1DTE), using high-probability signals derived from a confluence of technical indicators: EMA crossovers, RSI thresholds, ATR-based risk control, and volume spikes. The strategy aims to capture strong directional moves while avoiding overtrading, thanks to a built-in cooldown logic and optional time/session filters.

⚙️ Core Concept

The strategy executes trades only in the direction of the prevailing trend, determined by short- and long-term Exponential Moving Averages (EMA). Entry signals are generated when the Relative Strength Index (RSI) confirms momentum in the direction of the trend, and volume spikes suggest institutional activity.

To increase adaptability and user control, it includes a highly customizable parameter set for both long and short entries independently.

📌 Key Features

✅ Trend-Following Logic

Long entries are only allowed when EMA(short) > EMA(long)

Short entries are only allowed when EMA(short) < EMA(long)

✅ RSI Confirmation

Long: Requires RSI crossover above a configurable threshold

Short: Requires RSI crossunder below a configurable threshold

Optional rejection filters: Entry blocked above/below specific RSI extremes

✅ Volume Spike Filter

Confirms institutional participation by comparing current volume to an average multiplied by a user-defined factor.

✅ ATR-Based Risk Management

Both Stop Loss (SL) and Take Profit (TP) are dynamically calculated using ATR × a multiplier.

TP/SL ratio is fully configurable.

✅ Cooldown Control

After every trade, the system waits for a set number of bars before allowing new entries.

This prevents overtrading and increases signal quality.

Optionally, cooldown is ignored for reversal trades, ensuring the system can react immediately to a confirmed trend change.

✅ Candle Body Filter (Noise Control)

Avoids trades on candles with too small bodies relative to wicks (often noise or indecision candles).

✅ VWAP Confirmation (Optional)

Ensures price is trading above VWAP for long entries, or below for short entries.

✅ Time & Session Filters

Trades only during regular market hours (09:30–16:00 EST).

No-trade zone (e.g., 14:15–15:45 EST) to avoid low-liquidity traps or late-day whipsaws.

✅ End-of-Day Auto Close

All open positions are force-closed at 15:55 EST, protecting against overnight risk (especially relevant for 0DTE options).

📊 Visual Aids

EMA plots show trend direction

VWAP line provides real-time mean-reversion context

Stop Loss and Take Profit lines appear dynamically with each trade

Alerts notify of entry signals and exit triggers

🔧 Customization Panel

Nearly every element of the strategy can be tailored:

EMA lengths (short and long, for both sides)

RSI thresholds and length

ATR length, SL multiplier, and TP/SL ratio

Volume spike sensitivity

Minimum EMA distance filter

Candle body ratio filter

Session restrictions

Cooldown logic (duration + reversal exception)

This makes the strategy extremely versatile, allowing both conservative and aggressive configurations depending on the trader’s profile and the market context.

📌 Example Use Case: SPY Options (0DTE or 1DTE)

This system was designed and tested specifically for SPY and other intraday options trading, where:

Delta is around 0.50 or higher

Trades are short-lived (often 1–5 candles)

You aim to trade 1–3 signals per day, filtering out weak entries

🚫 Important Notes

It is not a scalping strategy; it relies on confirmed breakouts with trend support

No pyramiding or re-entries without cooldown to preserve risk integrity

Should be used with real-time alerts and manual broker execution

📈 Alerts Included

📈 Long Entry Signal

📉 Short Entry Signal

⚠️ Auto-closed all positions at 15:55 EST

✅ Proven Settings – Real Trades + Backtest Results

The current version of the strategy includes the optimal settings I’ve arrived at through extensive backtesting, as well as 3 months of real trading with consistent profitability. These results reflect real-world execution under live market conditions using 0DTE SPY options, with disciplined trade management and risk control.

🧠 Final Thoughts

Options Strategy V2.0 is a robust, highly tunable intraday strategy that blends momentum, trend-following, and volume confirmation. It is ideal for disciplined traders focused on SPY or other 0DTE/1DTE options, and it includes guardrails to reduce false signals and improve execution timing.

Perfect for those who seek precision, flexibility, and risk-defined setups—not blind automation.

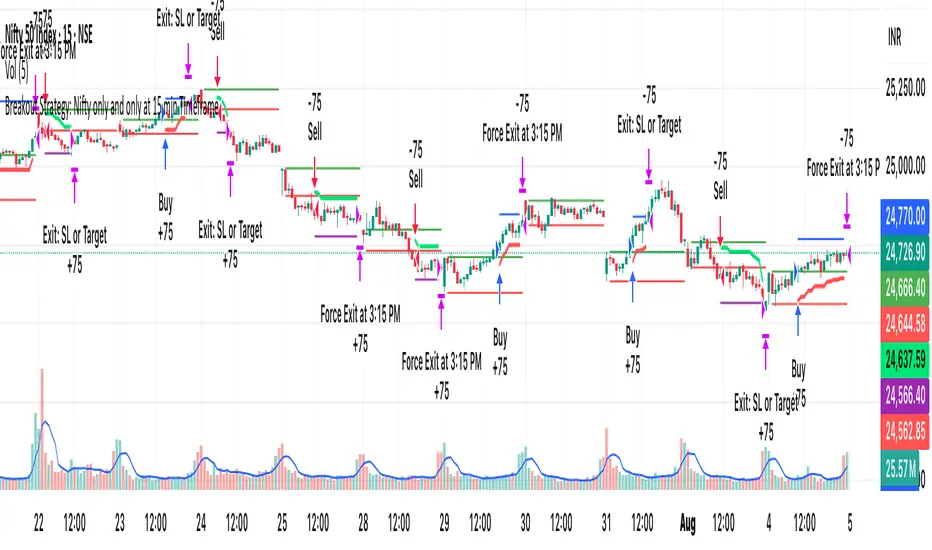

[PS]Breakout Strategy: Nifty/BN only at 15 min TimeframeIt only works on 15 min timeframe for nifty and Bank nifty.

VIX Sentiment Table – ResolutionThis indicator provides verbal representation of the current VIX value and likely market trend for easy to view and interpret