US Presidents (Alternating Fills by Order)📜 Indicator Description: US Presidents Background Fill

This indicator highlights the terms of U.S. Presidents on your chart with alternating red and blue background fills based on their political party:

• 🟥 Republicans = Red

• 🟦 Democrats = Blue

• 🎨 Dark/Light shading alternates with each new president to clearly distinguish consecutive terms, even within the same party.

The fill starts from President Ulysses S. Grant (18th President, 1873) through to the 47th president in 2025. It is designed to work with any asset and automatically adapts to the visible date range on your chart.

Ideal for visualizing macro trends, historical context, and how markets may have reacted under different political administrations.

Tìm kiếm tập lệnh với "微软股息支付率2025最新数据"

TASC 2025.04 The Ultimate Oscillator█ OVERVIEW

This script implements an alternative, refined version of the Ultimate Oscillator (UO) designed to reduce lag and enhance responsiveness in momentum indicators, as introduced by John F. Ehlers in his article "Less Lag In Momentum Indicators, The Ultimate Oscillator" from the April 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers states that indicators are essentially filters that remove unwanted noise (i.e., unnecessary information) from market data. Simply put, they process a series of data to place focus on specific information, providing a different perspective on price dynamics. Various filter types attenuate different periodic signals within the data. For instance, a lowpass filter allows only low-frequency signals, a highpass filter allows only high-frequency signals, and a bandpass filter allows signals within a specific frequency range .

Ehlers explains that the key to removing indicator lag is to combine filters of different types in such a way that the result preserves necessary, useful signals while minimizing delay (lag). His proposed UltimateOscillator aims to maintain responsiveness to a specific frequency range by measuring the difference between two highpass filters' outputs. The oscillator uses the following formula:

UO = (HP1 - HP2) / RMS

Where:

HP1 is the first highpass filter.

HP2 is another highpass filter that allows only shorter wavelengths than the critical period of HP1.

RMS is the root mean square of the highpass filter difference, used as a scaling factor to standardize the output.

The resulting oscillator is similar to a bandpass filter , because it emphasizes wavelengths between the critical periods of the two highpass filters. Ehlers' UO responds quickly to value changes in a series, providing a responsive view of momentum with little to no lag.

█ USAGE

Ehlers' UltimateOscillator sets the critical periods of its highpass filters using two parameters: BandEdge and Bandwidth :

The BandEdge sets the critical period of the second highpass filter, which determines the shortest wavelengths in the response.

The Bandwidth is a multiple of the BandEdge used for the critical period of the first highpass filter, which determines the longest wavelengths in the response. Ehlers suggests that a Bandwidth value of 2 works well for most applications. However, traders can use any value above or equal to 1.4.

Users can customize these parameters with the "Bandwidth" and "BandEdge" inputs in the "Settings/Inputs" tab.

The script plots the UO calculated for the specified "Source" series in a separate pane, with a color based on the chart's foreground color. Positive UO values indicate upward momentum or trends, and negative UO values indicate the opposite.

Additionally, this indicator provides the option to display a "cloud" from 10 additional UO series with different settings for an aggregate view of momentum. The "Cloud" input offers four display choices: "Bandwidth", "BandEdge", "Bandwidth + BandEdge", or "None".

The "Bandwidth" option calculates oscillators with different Bandwidth values based on the main oscillator's setting. Likewise, the "BandEdge" option calculates oscillators with varying BandEdge values. The "Bandwidth + BandEdge" option calculates the extra oscillators with different values for both parameters.

When a user selects any of these options, the script plots the maximum and minimum oscillator values and fills their space with a color gradient. The fill color corresponds to the net sum of each UO's sign , indicating whether most of the UOs reflect positive or negative momentum. Green hues mean most oscillators are above zero, signifying stronger upward momentum. Red hues mean most are below zero, indicating stronger downward momentum.

Mogwai Method with RSI and EMA - BTCUSD 15mThis is a custom TradingView indicator designed for trading Bitcoin (BTCUSD) on a 15-minute timeframe. It’s based on the Mogwai Method—a mean-reversion strategy—enhanced with the Relative Strength Index (RSI) for momentum confirmation. The indicator generates buy and sell signals, visualized as green and red triangle arrows on the chart, to help identify potential entry and exit points in the volatile cryptocurrency market.

Components

Bollinger Bands (BB):

Purpose: Identifies overextended price movements, signaling potential reversions to the mean.

Parameters:

Length: 20 periods (standard for mean-reversion).

Multiplier: 2.2 (slightly wider than the default 2.0 to suit BTCUSD’s volatility).

Role:

Buy signal when price drops below the lower band (oversold).

Sell signal when price rises above the upper band (overbought).

Relative Strength Index (RSI):

Purpose: Confirms momentum to filter out false signals from Bollinger Bands.

Parameters:

Length: 14 periods (classic setting, effective for crypto).

Overbought Level: 70 (price may be overextended upward).

Oversold Level: 30 (price may be overextended downward).

Role:

Buy signal requires RSI < 30 (oversold).

Sell signal requires RSI > 70 (overbought).

Exponential Moving Averages (EMAs) (Plotted but not currently in signal logic):

Purpose: Provides trend context (included in the script for visualization, optional for signal filtering).

Parameters:

Fast EMA: 9 periods (short-term trend).

Slow EMA: 50 periods (longer-term trend).

Role: Can be re-added to filter signals (e.g., buy only when Fast EMA > Slow EMA).

Signals (Triangles):

Buy Signal: Green upward triangle below the bar when price is below the lower Bollinger Band and RSI is below 30.

Sell Signal: Red downward triangle above the bar when price is above the upper Bollinger Band and RSI is above 70.

How It Works

The indicator combines Bollinger Bands and RSI to spot mean-reversion opportunities:

Buy Condition: Price breaks below the lower Bollinger Band (indicating oversold conditions), and RSI confirms this with a reading below 30.

Sell Condition: Price breaks above the upper Bollinger Band (indicating overbought conditions), and RSI confirms this with a reading above 70.

The strategy assumes that extreme price movements in BTCUSD will often revert to the mean, especially in choppy or ranging markets.

Visual Elements

Green Upward Triangles: Appear below the candlestick to indicate a buy signal.

Red Downward Triangles: Appear above the candlestick to indicate a sell signal.

Bollinger Bands: Gray lines (upper, middle, lower) plotted for reference.

EMAs: Blue (Fast) and Orange (Slow) lines for trend visualization.

How to Use the Indicator

Setup

Open TradingView:

Log into TradingView and select a BTCUSD chart from a supported exchange (e.g., Binance, Coinbase, Bitfinex).

Set Timeframe:

Switch the chart to a 15-minute timeframe (15m).

Add the Indicator:

Open the Pine Editor (bottom panel in TradingView).

Copy and paste the script provided.

Click “Add to Chart” to apply it.

Verify Display:

You should see Bollinger Bands (gray), Fast EMA (blue), Slow EMA (orange), and buy/sell triangles when conditions are met.

Trading Guidelines

Buy Signal (Green Triangle Below Bar):

What It Means: Price is oversold, potentially ready to bounce back toward the Bollinger Band middle line.

Action:

Enter a long position (buy BTCUSD).

Set a take-profit near the middle Bollinger Band (bb_middle) or a resistance level.

Place a stop-loss 1-2% below the entry (or based on ATR, e.g., ta.atr(14) * 2).

Best Context: Works well in ranging markets; avoid during strong downtrends.

Sell Signal (Red Triangle Above Bar):

What It Means: Price is overbought, potentially ready to drop back toward the middle line.

Action:

Enter a short position (sell BTCUSD) or exit a long position.

Set a take-profit near the middle Bollinger Band or a support level.

Place a stop-loss 1-2% above the entry.

Best Context: Effective in ranging markets; avoid during strong uptrends.

Trend Filter (Optional):

To reduce false signals in trending markets, you can modify the script:

Add and ema_fast > ema_slow to the buy condition (only buy in uptrends).

Add and ema_fast < ema_slow to the sell condition (only sell in downtrends).

Check the Fast EMA (blue) vs. Slow EMA (orange) alignment visually.

Tips for BTCUSD on 15-Minute Charts

Volatility: BTCUSD can be erratic. If signals are too frequent, increase bb_mult (e.g., to 2.5) or adjust RSI levels (e.g., 75/25).

Confirmation: Use volume spikes or candlestick patterns (e.g., doji, engulfing) to confirm signals.

Time of Day: Mean-reversion works best during low-volume periods (e.g., Asian session in crypto).

Backtesting: Use TradingView’s Strategy Tester (convert to a strategy by adding entry/exit logic) to evaluate performance with historical BTCUSD data up to March 13, 2025.

Risk Management

Position Size: Risk no more than 1-2% of your account per trade.

Stop Losses: Always use stops to protect against BTCUSD’s sudden moves.

Avoid Overtrading: Wait for clear signals; don’t force trades in choppy or unclear conditions.

Example Scenario

Chart: BTCUSD, 15-minute timeframe.

Buy Signal: Price drops to $58,000, below the lower Bollinger Band, RSI at 28. A green triangle appears.

Action: Buy at $58,000, target $59,000 (middle BB), stop at $57,500.

Sell Signal: Price rises to $60,500, above the upper Bollinger Band, RSI at 72. A red triangle appears.

Action: Sell at $60,500, target $59,500 (middle BB), stop at $61,000.

This indicator is tailored for mean-reversion trading on BTCUSD. Let me know if you’d like to tweak it further (e.g., add filters, alerts, or alternative indicators)!

Full Moon and New Moon IndicatorThe Full Moon & New Moon Indicator is a custom Pine Script indicator which marks Full Moon (Pournami) and New Moon (Amavasya) events on the price chart. This indicator helps traders who incorporate lunar cycles into their market analysis, as certain traders believe these cycles influence market sentiment and price action. The current script is added for the year 2024 and 2025 and the dates are considered as per the Telugu calendar.

Features

✅ Identifies and labels Full Moon & New Moon days on the chart for the year 2024 and 2025

How it Works!

On a Full Moon day, it places a yellow label ("Pournami") above the corresponding candle.

On a New Moon day, it places a blue label ("Amavasya") above the corresponding candle.

Example Usage

When a Full Moon label appears, check for potential trend reversals or high volatility.

When a New Moon label appears, watch for market consolidation or a shift in sentiment.

Combine with candlestick patterns, support/resistance, or momentum indicators for a stronger trading setup.

🚀 Add this indicator to your TradingView chart and explore the market’s reaction to lunar cycles! 🌕

TASC 2025.03 A New Solution, Removing Moving Average Lag█ OVERVIEW

This script implements a novel technique for removing lag from a moving average, as introduced by John Ehlers in the "A New Solution, Removing Moving Average Lag" article featured in the March 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers explains that the average price in a time series represents a statistical estimate for a block of price values, where the estimate is positioned at the block's center on the time axis. In the case of a simple moving average (SMA), the calculation moves the analyzed block along the time axis and computes an average after each new sample. Because the average's position is at the center of each block, the SMA inherently lags behind price changes by half the data length.

As a solution to removing moving average lag, Ehlers proposes a new projected moving average (PMA) . The PMA smooths price data while maintaining responsiveness by calculating a projection of the average using the data's linear regression slope.

The slope of linear regression on a block of financial time series data can be expressed as the covariance between prices and sample points divided by the variance of the sample points. Ehlers derives the PMA by adding this slope across half the data length to the SMA, creating a first-order prediction that substantially reduces lag:

PMA = SMA + Slope * Length / 2

In addition, the article includes methods for calculating predictions of the PMA and the slope based on second-order and fourth-order differences. The formulas for these predictions are as follows:

PredictPMA = PMA + 0.5 * (Slope - Slope ) * Length

PredictSlope = 1.5 * Slope - 0.5 * Slope

Ehlers suggests that crossings between the predictions and the original values can help traders identify timely buy and sell signals.

█ USAGE

This indicator displays the SMA, PMA, and PMA prediction for a specified series in the main chart pane, and it shows the linear regression slope and prediction in a separate pane. Analyzing the difference between the PMA and SMA can help to identify trends. The differences between PMA or slope and its corresponding prediction can indicate turning points and potential trade opportunities.

The SMA plot uses the chart's foreground color, and the PMA and slope plots are blue by default. The plots of the predictions have a green or red hue to signify direction. Additionally, the indicator fills the space between the SMA and PMA with a green or red color gradient based on their differences:

Users can customize the source series, data length, and plot colors via the inputs in the "Settings/Inputs" tab.

█ NOTES FOR Pine Script® CODERS

The article's code implementation uses a loop to calculate all necessary sums for the slope and SMA calculations. Ported into Pine, the implementation is as follows:

pma(float src, int length) =>

float PMA = 0., float SMA = 0., float Slope = 0.

float Sx = 0.0 , float Sy = 0.0

float Sxx = 0.0 , float Syy = 0.0 , float Sxy = 0.0

for count = 1 to length

float src1 = src

Sx += count

Sy += src

Sxx += count * count

Syy += src1 * src1

Sxy += count * src1

Slope := -(length * Sxy - Sx * Sy) / (length * Sxx - Sx * Sx)

SMA := Sy / length

PMA := SMA + Slope * length / 2

However, loops in Pine can be computationally expensive, and the above loop's runtime scales directly with the specified length. Fortunately, Pine's built-in functions often eliminate the need for loops. This indicator implements the following function, which simplifies the process by using the ta.linreg() and ta.sma() functions to calculate equivalent slope and SMA values efficiently:

pma(float src, int length) =>

float Slope = ta.linreg(src, length, 0) - ta.linreg(src, length, 1)

float SMA = ta.sma(src, length)

float PMA = SMA + Slope * length * 0.5

To learn more about loop elimination in Pine, refer to this section of the User Manual's Profiling and optimization page.

TASC 2025.02 Autocorrelation Indicator█ OVERVIEW

This script implements the Autocorrelation Indicator introduced by John Ehlers in the "Drunkard's Walk: Theory And Measurement By Autocorrelation" article from the February 2025 edition of TASC's Traders' Tips . The indicator calculates the autocorrelation of a price series across several lags to construct a periodogram , which traders can use to identify market cycles, trends, and potential reversal patterns.

█ CONCEPTS

Drunkard's walk

A drunkard's walk , formally known as a random walk , is a type of stochastic process that models the evolution of a system or variable through successive random steps.

In his article, John Ehlers relates this model to market data. He discusses two first- and second-order partial differential equations, modified for discrete (non-continuous) data, that can represent solutions to the discrete random walk problem: the diffusion equation and the wave equation. According to Ehlers, market data takes on a mixture of two "modes" described by these equations. He theorizes that when "diffusion mode" is dominant, trading success is almost a matter of luck, and when "wave mode" is dominant, indicators may have improved performance.

Pink spectrum

John Ehlers explains that many recent academic studies affirm that market data has a pink spectrum , meaning the power spectral density of the data is proportional to the wavelengths it contains, like pink noise . A random walk with a pink spectrum suggests that the states of the random variable are correlated and not independent. In other words, the random variable exhibits long-range dependence with respect to previous states.

Autocorrelation function (ACF)

Autocorrelation measures the correlation of a time series with a delayed copy, or lag , of itself. The autocorrelation function (ACF) is a method that evaluates autocorrelation across a range of lags , which can help to identify patterns, trends, and cycles in stochastic market data. Analysts often use ACF to detect and characterize long-range dependence in a time series.

The Autocorrelation Indicator evaluates the ACF of market prices over a fixed range of lags, expressing the results as a color-coded heatmap representing a dynamic periodogram. Ehlers suggests the information from the periodogram can help traders identify different market behaviors, including:

Cycles : Distinguishable as repeated patterns in the periodogram.

Reversals : Indicated by sharp vertical changes in the periodogram when the indicator uses a short data length .

Trends : Indicated by increasing correlation across lags, starting with the shortest, over time.

█ USAGE

This script calculates the Autocorrelation Indicator on an input "Source" series, smoothed by Ehlers' UltimateSmoother filter, and plots several color-coded lines to represent the periodogram's information. Each line corresponds to an analyzed lag, with the shortest lag's line at the bottom of the pane. Green hues in the line indicate a positive correlation for the lag, red hues indicate a negative correlation (anticorrelation), and orange or yellow hues mean the correlation is near zero.

Because Pine has a limit on the number of plots for a single indicator, this script divides the periodogram display into three distinct ranges that cover different lags. To see the full periodogram, add three instances of this script to the chart and set the "Lag range" input for each to a different value, as demonstrated in the chart above.

With a modest autocorrelation length, such as 20 on a "1D" chart, traders can identify seasonal patterns in the price series, which can help to pinpoint cycles and moderate trends. For instance, on the daily ES1! chart above, the indicator shows repetitive, similar patterns through fall 2023 and winter 2023-2024. The green "triangular" shape rising from the zero lag baseline over different time ranges corresponds to seasonal trends in the data.

To identify turning points in the price series, Ehlers recommends using a short autocorrelation length, such as 2. With this length, users can observe sharp, sudden shifts along the vertical axis, which suggest potential turning points from upward to downward or vice versa.

Highs & Lows RTH/OVN/IBs/D/W/M/YOverview

Plots the highs and lows of RTH, OVN/ETH, IBs of those sessions, previous Day, Week, Month, and Year.

Features

Allows the user to enable/disable plotting the high/low of each period.

Lines' length, offset, and colors can be customized

Labels' position, size, color, and style can be customized

Support

Questions, feedbacks, and requests are welcomed. Please feel free to use Comments or direct private message via TradingView.

Disclaimer

This stock chart indicator provided is for informational purposes only and should not be considered as financial or investment advice. The data and information presented in this indicator are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy.

Users should be aware that:

Any investment decisions made based on this indicator are at your own risk.

The creators and providers of this indicator disclaim all liability for any losses, damages, or other consequences resulting from its use. By using this stock chart indicator, you acknowledge and accept the inherent risks associated with trading and investing in financial markets.

Release Date: 2025-01-17

Release Version: v1 r1

Release Notes Date: 2025-01-17

SW monthly Gann Days**Script Description:**

The script you are looking at is based on the work of W.D. Gann, a famous trader and market analyst in the early 20th century, known for his use of geometry, astrology, and numerology in market analysis. Gann believed that certain days in the market had significant importance, and he observed that markets often exhibited significant price moves around specific dates. These dates were typically associated with cyclical patterns in price movements, and Gann referred to these as "Gann Days."

In this script, we have focused on highlighting certain days of the month that Gann believed to have an influence on market behavior. The specific days in question are the **6th to 7th**, **9th to 10th**, **14th to 15th**, **19th to 20th**, **23rd to 24th**, and **29th to 31st** of each month. These ranges are based on Gann’s theory that there are recurring time cycles in the market that cause turning points or critical price movements to occur around certain days of the month.

### **Why Gann Used These Days:**

1. **Mathematical and Astrological Cycles:**

Gann believed that markets were influenced by natural cycles, and that certain dates (or combinations of dates) played a critical role in the price movements. These specific days are part of his broader theory of "time cycles" where the market would often change direction, reverse, or exhibit significant volatility on particular days. Gann's research was based on both mathematical principles and astrological observations, leading him to assign importance to these days.

2. **Gann's Universal Timing Theory:**

According to Gann, financial markets operate in a universe governed by geometric and astrological principles. These cycles repeat themselves over time, and specific days in a given month correspond to key turning points within these repeating cycles. Gann found that the 6th to 7th, 9th to 10th, 14th to 15th, 19th to 20th, 23rd to 24th, and 29th to 31st often marked significant changes in the market, making them particularly important for traders to watch.

3. **Market Psychology and Sentiment:**

These specific days likely correspond to key moments where market participants tend to react in predictable ways, influenced by past market behavior on similar dates. For example, news events or scheduled economic reports might fall within these time windows, causing the market to respond in a particular way. Gann's method involves using these cyclical patterns to predict turning points in market prices, enabling traders to anticipate when the market might make a reversal or face a significant shift in direction.

4. **Turning Points:**

Gann believed that markets often reversed or encountered critical points around specific dates. This is why he considered certain days more important than others. By identifying and focusing on these days, traders can better anticipate the market’s movement and make more informed trading decisions.

5. **Numerology:**

Gann also utilized numerology in his trading system, believing that numbers, and particularly certain key numbers, had significance in predicting market movements. The days selected in this script may correspond to numerological patterns that Gann identified in his analysis of the markets, such as recurring numbers in his astrological and geometric systems.

### **Purpose of the Script:**

This script highlights these "Gann Days" within a trading chart for 2024 and 2025. The color-coding or background highlighting is intended to draw attention to these dates, so traders can observe the potential for significant market movements during these times. By identifying these specific dates, traders following Gann's theories may gain insights into possible turning points, corrections, or key price movements based on the market's historical behavior around these days.

Overall, Gann’s use of specific days was based on his deep belief in the cyclical nature of the market and his attempt to tie those cycles to the natural laws of time, geometry, and astrology. By focusing on these dates, Gann aimed to give traders an edge in predicting significant market events and price shifts.

TASC 2025.01 Linear Predictive Filters█ OVERVIEW

This script implements a suite of tools for identifying and utilizing dominant cycles in time series data, as introduced by John Ehlers in the "Linear Predictive Filters And Instantaneous Frequency" article featured in the January 2025 edition of TASC's Traders' Tips . Dominant cycle information can help traders adapt their indicators and strategies to changing market conditions.

█ CONCEPTS

Conventional technical indicators and strategies often rely on static, unchanging parameters, which may fail to account for the dynamic nature of market data. In his article, John Ehlers applies digital signal processing principles to address this issue, introducing linear predictive filters to identify cyclic information for adapting indicators and strategies to evolving market conditions.

This approach treats market data as a complex series in the time domain. Analyzing the series in the frequency domain reveals information about its cyclic components. To reduce the impact of frequencies outside a range of interest and focus on a specific range of cycles, Ehlers applies second-order highpass and lowpass filters to the price data, which attenuate or remove wavelengths outside the desired range. This band-limited analysis isolates specific parts of the frequency spectrum for various trading styles, e.g., longer wavelengths for position trading or shorter wavelengths for swing trading.

After filtering the series to produce band-limited data, Ehlers applies a linear predictive filter to predict future values a few bars ahead. The filter, calculated based on the techniques proposed by Lloyd Griffiths, adaptively minimizes the error between the latest data point and prediction, successively adjusting its coefficients to align with the band-limited series. The filter's coefficients can then be applied to generate an adaptive estimate of the band-limited data's structure in the frequency domain and identify the dominant cycle.

█ USAGE

This script implements the following tools presented in the article:

Griffiths Predictor

This tool calculates a linear predictive filter to forecast future data points in band-limited price data. The crosses between the prediction and signal lines can provide potential trade signals.

Griffiths Spectrum

This tool calculates a partial frequency spectrum of the band-limited price data derived from the linear predictive filter's coefficients, displaying a color-coded representation of the frequency information in the pane. This mode's display represents the data as a periodogram . The bottom of each plotted bar corresponds to a specific analyzed period (inverse of frequency), and the bar's color represents the presence of that periodic cycle in the time series relative to the one with the highest presence (i.e., the dominant cycle). Warmer, brighter colors indicate a higher presence of the cycle in the series, whereas darker colors indicate a lower presence.

Griffiths Dominant Cycle

This tool compares the cyclic components within the partial spectrum and identifies the frequency with the highest power, i.e., the dominant cycle . Traders can use this dominant cycle information to tune other indicators and strategies, which may help promote better alignment with dynamic market conditions.

Notes on parameters

Bandpass boundaries:

In the article, Ehlers recommends an upper bound of 125 bars or higher to capture longer-term cycles for position trading. He recommends an upper bound of 40 bars and a lower bound of 18 bars for swing trading. If traders use smaller lower bounds, Ehlers advises a minimum of eight bars to minimize the potential effects of aliasing.

Data length:

The Griffiths predictor can use a relatively small data length, as autocorrelation diminishes rapidly with lag. However, for optimal spectrum and dominant cycle calculations, the length must match or exceed the upper bound of the bandpass filter. Ehlers recommends avoiding excessively long lengths to maintain responsiveness to shorter-term cycles.

Ichimoku MTF Heatmap WITH ALERT meeting D and W conditionsThis is a version of the Ichimoku Cloud Heatmap but adds a can't miss alert when it meets Daily and Weekly conditions. The cloud metric is still being refined and the qualifier is ignoring just the cloud for now. As of 12/21/2025 GLD is meeting the conditions to set this flag.

BTC - Institutional Cost Corridor (Overlay)BTC - Institutional Cost Corridor | RM

Strategic Context

The approval of Spot Bitcoin ETFs on January 11, 2024, signaled the beginning of the "Institutional Era." Since then, price discovery has shifted from being purely retail-driven to being heavily influenced by massive, off-chain equity flows.

The Institutional Cost Corridor is an approach for a quantitative tool designed to solve the problem of "Institutional Blindness" by mapping the aggregate cost basis of Wall Street's entry. It allows for the identification of structural "gravity zones" where institutional capital is most likely to move from a state of profit into a state of defense.

The Methodology: Data Selection & Weighting

To ensure the output is statistically significant, the data engine focuses exclusively on the "Big 3" liquidity providers: BlackRock (IBIT), Fidelity (FBTC), and Bitwise (BITB). These three funds represent over 80% of total Spot ETF liquidity. A weighted ratio is applied (prioritizing BlackRock) to reflect the reality that a dollar flowing into IBIT has a significantly higher impact on market structure than a dollar in smaller, fragmented funds. This ensures the indicator follows the actual mass of institutional capital.

Recalculating the Shadow: Nominal Price & AUM

A common point of confusion is that Bitcoin ETFs have a completely different nominal price than Bitcoin itself (e.g., an IBIT share may trade at $50 while BTC is at $100,000). To solve this, the script does not look at the dollar price of the shares. Instead, it uses Assets Under Management (AUM) and Relative Performance Mapping . By calculating the percentage growth of the funds' underlying value since inception and projecting that growth onto the Bitcoin price axis, the script "re-scales" the institutional entry levels. This allows us to see exactly where Wall Street is "underwater" on a standard Bitcoin chart.

The Mathematical Foundations: Genesis vs. Anchored

The indicator utilizes two distinct mathematical approaches to triangulate the "Truth" of institutional positioning. These are not arbitrary assumptions, but forward-mapped models verified against professional financial benchmarks.

1. Conservative Floor (Genesis Mode)

• The Logic: This model uses a Cumulative Inflow VWAP . It treats every dollar that has entered the ETFs since Day 1 as part of a single, massive ledger.

• Scientific Justification: This approach maps to the "Fortress Zone" of early, high-conviction capital. Historical AUM performance data suggests that the largest influx of structural capital occurred during the launch phase of 2024. This logic identifies the Ultimate Floor —the level where the entire ETF cohort would flip to a net loss. In late 2025 research (e.g., Glassnode "True Market Mean"), this model consistently aligns with the deepest structural support of the bull cycle.

2. Wall Street Entry (Anchored Mode)

• The Logic: This model utilize a Relative Performance Anchor . It synchronizes the Bitcoin price on Launch Day with the growth performance of the ETF fund shares.

• Scientific Justification: This approach identifies the "Active Participant Basis." It reflects the entry price for the capital that fueled the most recent expansion cycles. It maps directly to the "Active Investors' Realized Price" cited by institutional research firms, identifying the immediate psychological "pain threshold" for the current market majority.

3. Institutional Mean (Hybrid Mode)

• The Logic: A 50/50 mathematical blend of the Conservative Floor and the Wall Street Entry .

• Justification: This is the "Equilibrium Zone." It serves as a neutral baseline by balancing early-stage "Genesis" conviction with late-cycle volatility. It represents the median cost basis of all current institutional holders.

4. The Shadow Corridor (Full Range)

• The Logic: Visualizes the entire spread between the Conservative Floor and the Wall Street Entry.

• Justification: The "Structural Support Cloud." Instead of a single price, it defines a regime . As long as Bitcoin remains above this cloud, the institutional trend remains in an "Expansion Phase." A re-entry into this corridor suggests a transition from a trending market into a value-accumulation phase.

Tactical Playbook: Scenario Logic

The Shadow Corridor (Full Range) visualizes the area between these two models, creating an "Institutional War Zone."

• Active Support Test: When price tests the Wall Street Entry (upper boundary), it indicates the active institutional majority is at breakeven. Expect significant defensive buying (bids) as funds protect their yearly performance reports.

• Deep Value Regime: Trading inside the Corridor is defined as a "Value Regime." This is where institutional accumulation historically absorbs retail capitulation.

• The Premium Trap: When the distance between price and the Corridor exceeds 35-40%, the market is "speculatively overextended," signaling a high probability of mean-reversion.

• Macro Breakdown: A Weekly (1W) candle closing below the Conservative Floor (lower boundary) signals a structural trend shift, indicating the majority of ETF-era capital is officially in a drawdown.

Operational Recommendation Best viewed on the Daily (1D) timeframe for macro structural analysis, providing the most reliable signal for institutional defense zones.

Tags: bitcoin, btc, etf, blackrock, ibit, institutional, cost-basis, vwap, macro, cycle, realized-price, Rob Maths

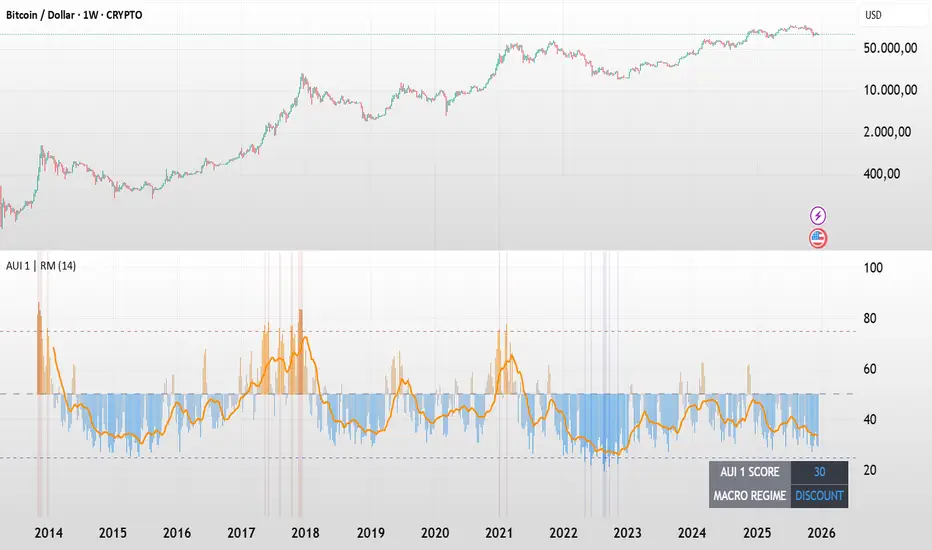

BTC - AUI 1: Macro Sentiment & On-Chain CompositeBTC - AUI 1: Macro Sentiment & On-Chain Composite | RM

Overview & Philosophy The AUI 1 ( Another Ultimate Indicator, Volume 1 ) is a 10-pillar quantitative composite designed to solve the "noise problem" in Bitcoin analysis. Most traders fail because they rely on a single metric in isolation. The AUI 1 aggregates ten distinct dimensions of the network — from speculative flow to institutional extension — into a singular 0–100 score.

The 10-Pillar Quant Framework

Each pillar is mathematically normalized to a standardized 0 to 10 scale . The sum of these pillars creates the final 0–100 index:

1. BEAM (Adaptive Logarithmic Multiple)

• Method: Log-deviation from the 4-year cycle mean.

• Logic: Measures price distance from its fundamental growth curve.

(Credit: BitcoinEcon)

2. MVRV Z-Score (Statistical Distance)

• Method: Standard deviations between Market Cap and Realized Cap.

• Logic: Identifies historical "Fair Value" vs. "Bubble" extremes.

(Credit: M. Mahmudov & D. Puell)

3. Metcalfe’s Law (Network Utility)

• Method: Logarithmic scaling of Active Addresses.

• Logic: Ensures price growth is supported by actual user adoption.

(Credit: T. Peterson)

4. RHODL Proxy (Speculative Flow)

• Method: Supply rotation intensity between HODLers and New Money.

• Logic: Cycle peaks are defined by "Old Money" distributing to "New Money."

(Credit: Philip Swift)

5. AXIS Momentum (Structural Trend Intensity)

• Method: Dual-speed Rate of Change (RoC) fusion engine.

• Logic: Identifies the acceleration and "torque" of the macro trend.

(Credit: Rob_Maths)

6. Mayer Multiple (Institutional Extension)

• Method: Raw distance from the 200-day SMA.

• Logic: Tracks the primary anchor used by institutional mean-reversion desks.

(Credit: Trace Mayer)

7. Unrealized Profit (Financial Pressure)

• Method: Absolute MVRV Ratio mapping.

• Logic: Measures the financial "stress" or "greed" held by the average holder.

8. Retail Participation (Psychology Proxy)

• Method: Inverted Log-Average Transaction Size (USD).

• Logic: Declining transaction sizes historically signal retail FOMO (Euphoria).

9. Volatility Overextension (Structural Risk)

• Method: 30-day Standard Deviation relative to the mean.

• Logic: High-intensity volatility clusters often precede cycle trend-shifts.

10. Macro RSI (Cycle Maturity)

• Method: High-timeframe momentum saturation levels.

• Logic: Identifies the statistical "Buying Exhaustion" of a macro move.

(Credit: J. Welles Wilder Jr.)

How to Read the AXIS Quadrants

The AUI 1 uses a Seamless Heatmap to categorize the market into four specific macro regimes:

❄️ 0–25: FROZEN (Deep Blue) Maximum Opportunity. Structural capitulation where only long-term conviction remains. Historically the "Generational Wealth" window.

🔵 25–50: DISCOUNT (Light Blue to Gray) Value Accumulation. The market is cooling down; risk is mathematically low, and the network is building a structural floor.

🟠 50–75: EXPANSION (Gray to Orange) Trend Acceleration. Healthy bullish growth supported by network utility and positive momentum.

🔥 75–100: SCORCHED (Orange to Deep Red) Terminal Euphoria. Maximum Risk zone. Speculative FOMO is at its peak; the market is fundamentally overextended.

The Orange Signal Line

To filter short-term noise, the AUI 1 includes a Signal Smoothing Line (Parametrizable).

• Cycle Confirmation: Index Bars crossing above the Signal Line indicates trend acceleration.

• Peak Confirmation: If the Index Score rolls over and breaks below the Signal Line while in the SCORCHED zone, the cycle peak is likely confirmed.

Credits & Data Built by Rob_Maths (2025) using on-chain frameworks from Glassnode and IntoTheBlock. Special recognition to the pioneers: Murad Mahmudov, David Puell, Philip Swift, Trace Mayer, and Timothy Peterson.

Strategic Recommendation: For the most accurate macro cycle signals and to filter daily market noise, it is strongly recommended to use this indicator on the Weekly (1W) timeframe.

⚠️ Data Requirement Note: This quantitative composite utilizes professional on-chain data feeds, specifically GLASSNODE:BTC_ACTIVEADDRESSES , GLASSNODE:BTC_ACTIVE1Y , and INTOTHEBLOCK:BTC_MVRV . A TradingView paid plan (Essential or higher) may be required to access these institutional data streams.

Disclaimer This script is for macro-economic research purposes. It is a probabilistic model, not a crystal ball. Past performance is not a guarantee of future results.

Tags:

bitcoin, btc, on-chain, macro, composite, mvrv, rhodl, momentum, index, valuation, active-addresses, cycles, sentiment, risk, AUI, Rob Maths

Optimized Options Day Trading Script -Anurag Dec20-2025This indicator is a specialized Multi-Timeframe Trend & Regime System designed specifically for intraday trading on SPY, QQQ, and SPX. It is optimized for high-volatility execution (like 0DTE) by filtering out "choppy" low-probability conditions before they happen.

Unlike standard indicators that only look at the current chart, this script runs a background check on the 15-Minute Timeframe

deKoder | Business Cycle vs BitcoinThis indicator overlays Bitcoin's detrended momentum with the US ISM Manufacturing PMI (a key business cycle proxy) to visually dissect the relationship between crypto cycles and broader economic health.

Inspired by ongoing debates in crypto macro analysis (e.g., "Is there a 4-year halving cycle, or is it just the business cycle?" ), it highlights potential lead-lag dynamics - challenging the popular view that PMI strictly leads Bitcoin rallies and tops.

Key Features

• BTC Momentum Wave (Yellow/Orange Line):

Detrended deviation from Bitcoin's long-term "fair value" (24-month SMA).

Formula: ((close / sma(close, 24)) * 100 - 100) * 0.15

- Positive (yellow): BTC overvalued relative to trend | bullish momentum

- Negative (orange): Undervalued relative to trend | bearish momentum

• PMI Wave (Teal/Red Line):

ISM Manufacturing PMI centered at zero (raw PMI - 50, scaled ×3 for alignment).

- Positive (teal): Expansion (>50 raw) — economic tailwinds.

- Negative (red): Contraction (<50 raw) — headwinds, often linked to risk-off in assets.

• S&P 500 Momentum (White Line, Optional):

Similar deviation for SPX, showing how equities bridge BTC's volatility and PMI's smoothness.

• Divergence Highlights (Bar & Background Colors):

- Teal/Green Zones : BTC momentum positive while PMI negative → BTC signaling early recovery (potential lead by 1-3+ months at bottoms).

- Maroon/Red Zones : BTC momentum negative while PMI positive → BTC warning of rollovers (early bear signals).

- Neutral: No color — aligned cycles.

• Overlaid SMA on Price Chart :

24-month SMA for BTC (teal when price above, red when below) — quick fair value reference.

How to Interpret: Does BTC Lead the Business Cycle?

The chart flips the common meme ( "No 4-year cycle, it's just the business cycle" ) by visually emphasising BTC's potential as a forward-looking signal .

Historical cycles (2013–2025) show:

• BTC Leads at Bottoms : E.g., 2018–2019 and 2022 troughs — BTC momentum crosses positive 2–4 months before PMI, as speculative traders price in liquidity easing/recoveries ahead of manufacturing data.

• Coincident or BTC-Led at Tops : Peaks align closely (e.g., 2017, 2021), with PMI rollovers often coinciding or slightly leading the initial BTC euphoria fade. BTC then rolls over before PMI confirms later.

• Why? Markets are anticipatory (6–12 months forward), while PMI is a lagged survey snapshot. BTC, as a high-beta risk asset, amplifies early sentiment shifts before they hit factory orders/employment.

Inputs & Customization

• BTC Source (Default: BITSTAMP:BTCUSD)

• Fair Value MA Length (Default: 24 months)

• Show S&P (Default: False)

• PMI Multiplier (Default: 3.0)

• BTC Momentum Multiplier (Default: 0.15)

• Cap BTC Momentum at ±100 (Default: True)

• Toggle Early Cross Arrows, Bar/Background Deviation Colors, Difference Histogram

V3 Valentini Pro Scalper [Dashboard]Gemini 3.0 pro's take on Fabio Valentini's world #1 strategy scalp 12/19/2025

Simple Trend Pullback Tool (EMA) v1.1Simple Trend Pullback Filter (EMA)

Overview This script is a lightweight, objective tool designed to filter out market noise and identify high-probability entry zones in trending markets. Built on the core principle of "The Rising Tide," it utilizes a dual-EMA cloud to visualize the trend’s health and highlight where the price is likely to find support after an overextended breakout.

How It Works

Trend Identification: The script tracks the alignment between the EMA 50 and EMA 200. When the price is consistently above this "Cloud," the market is in a confirmed uptrend.

The Pullback Logic: Instead of chasing breakouts (which often lead to FOMO-driven losses), this tool highlights the 'Mean Reversion' zone. It signals an entry when price action "pulls back" into the EMA cloud while the primary trend remains bullish.

Simplicity First: There are no laggy oscillators or repainting signals. It uses price action relative to time-weighted moving averages to keep your chart clean and your decisions logical.

Example Use Case: $CUU.V and NASDAQ:RKLB In the current market (December 2025), we see high-velocity breakouts in sectors like Space and Copper. While a stock like Copper Fox ($CUU.V) may jump 28% on merger news, this script helps traders wait for the necessary consolidation back toward the EMA 20/50 support before committing capital.

Settings

EMA 1 (Fast): Default 50 — Tracks intermediate momentum.

EMA 2 (Slow): Default 200 — The "Line in the Sand" for long-term trend direction.

TASC 2026.01 The Reversion Index█ OVERVIEW

This script implements the Reversion Index as presented by John F. Ehlers in the January 2026 edition of the TASC Traders' Tips , "Identifying Peaks And Valleys In Ranging Markets”. This indicator was created to provide timely buy and sell signals for mean reversion strategies.

█ CONCEPTS

Ehlers came up with the idea for the Reversion Index following the development of the "Continuation Index" (featured in the September 2025 edition). While the Continuation Index provides indications for trend onset, continuation, and exhaustion; the Reversion Index serves as its counterpart for mean-reversion trading.

The raw Reversion Index value is calculated as the net change in price normalized to the sum of the absolute value of change in price over the same period; for clarity, it is then smoothed using Ehlers' SuperSmoother.

The Smooth Reversion Index value is led by a "Trigger" line, which is created by smoothing the raw data to half the smoothing period of the smoothed index.

Note: Ehlers suggests the smoothing lengths be left at 8 and 4 (Reversion Index & Trigger). For this reason these lengths are hard-coded in the script but can be easily modified in the code.

█ USAGE

In order to identify peaks and valleys effectively, the "Length" should ideally be set to half of that of the expected cycle of the data. If the expected cycle of your trading data is 20 bars, a 10 bar length should be set.

Note: The Reversion Index is intended to identify peaks and valleys within a cycle, not over a large sample period. Ehlers suggests that this would create an estimation of trend, which is not the goal here.

Once the length is set, peaks and valleys are interpreted as the cross of the "Trigger" and "Smooth" lines.

X-Trend Macro Command CenterX-Trend Macro Command Center (MCC) | Institutional Grade Dashboard

📝 Description Body

The Invisible Engine of the Market Revealed.

Traders often focus solely on Price Action, ignoring the massive underwater currents that actually drive trends: Global Liquidity, Inflation, and Central Bank Policy. We created X-Trend Macro Command Center (MCC) to solve this problem.

This is not just an indicator. It is a fundamental heads-up display that bridges the gap between technical charts and macroeconomic reality.

💡 The Idea & Philosophy

Markets don't move in a vacuum. Bull runs are fueled by M2 Money Supply expansion and negative real yields. Crashes are triggered by liquidity crunches and aggressive rate hikes. X-Trend MCC was built to give retail traders the same "Macro Awareness" that institutional desks possess. It aggregates fragmented economic data from Federal Reserve databases (FRED) directly onto your chart in real-time.

🚀 Application & Logic

This tool is designed for Trend Traders, Crypto Investors, and Macro Analysts.

Identify the Regime: Instantly see if the environment is "RISK ON" (High Liquidity, Low Real Rates) or "RISK OFF" (Monetary Tightening).

Validate the Trend: Don't buy the dip if Liquidity (M2) is crashing. Don't short the rally if Real Yields are negative.

Multi-Region Analysis: Switch instantly between economic powerhouses (US, China, Japan) to see where the capital is flowing.

📊 Dashboard Metrics Explained

Every row in the Command Center tells a specific story about the economy:

Interest Rate: The "Gravity" of finance. Higher rates weigh down risk assets (Stocks/Crypto).

Inflation (YoY): The erosion of purchasing power. We calculate this dynamically based on CPI data.

Real Yield (The "Golden" Metric): Calculated as Interest Rate - Inflation.

Green: Real Yield is low/negative. Cash is trash, assets fly.

Red: Real Yield is high. Cash is King, assets struggle.

US Debt & GDP: Fiscal health indicators formatted in Trillions ($T). Watch the Debt-to-GDP ratio—if it spikes >120%, expect currency debasement.

M2 Money Supply: The fuel tank of the market. Tracks the total amount of money in circulation.

↗ Trend: Liquidity is entering the system (Bullish).

↘ Trend: Liquidity is drying up (Bearish).

🧩 The X-Trend Ecosystem

X-Trend MCC is just the tip of the iceberg. This module is part of the larger X-Trend Project — a comprehensive suite of algorithmic tools being developed to quantify market chaos. While our Price Action algorithms (Lite/Pro/Ultra) handle the Micro, the MCC handles the Macro.

Technical Note:

Data Sources: Direct connection to FRED (Federal Reserve Economic Data).

Zero Repainting: Historical data is requested strictly using closed bars to ensure accuracy.

Open Source: We believe in transparency. The code is open for study under MPL 2.0.

Build by Dev0880 | X-Trend © 2025

Simple Candle Strategy# Candle Pattern Strategy - Pine Script V6

## Overview

A TradingView trading strategy script (Pine Script V6) that identifies candlestick patterns over a configurable lookback period and generates trading signals based on pattern recognition rules.

## Strategy Logic

The strategy analyzes the most recent N candlesticks (default: 5) and classifies their patterns into three categories, then generates buy/sell signals based on specific pattern combinations.

### Candlestick Pattern Classification

Each candlestick is classified as one of three types:

| Pattern | Definition | Formula |

|---------|-----------|---------|

| **Close at High** | Close price near the highest price of the candle | `(high - close) / (high - low) ≤ (1 - threshold)` |

| **Close at Low** | Close price near the lowest price of the candle | `(close - low) / (high - low) ≤ (1 - threshold)` |

| **Doji** | Opening and closing prices very close; long upper/lower wicks | `abs(close - open) / (high - low) ≤ threshold` |

### Trading Rules

| Condition | Action | Signal |

|-----------|--------|--------|

| Number of Doji candles ≥ 3 | **SKIP** - Market is too chaotic | No trade |

| "Close at High" count ≥ 2 + Last candle closes at high | **LONG** - Bullish confirmation | Buy Signal |

| "Close at Low" count ≥ 2 + Last candle closes at low | **SHORT** - Bearish confirmation | Sell Signal |

## Configuration Parameters

All parameters are adjustable in TradingView's "Settings/Inputs" tab:

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| **K-line Lookback Period** | 5 | 3-20 | Number of candlesticks to analyze |

| **Doji Threshold** | 0.1 | 0.0-1.0 | Body size / Total range ratio for doji identification |

| **Doji Count Limit** | 3 | 1-10 | Number of dojis that triggers skip signal |

| **Close at High Proximity** | 0.9 | 0.5-1.0 | Required proximity to highest price (0.9 = 90%) |

| **Close at Low Proximity** | 0.9 | 0.5-1.0 | Required proximity to lowest price (0.9 = 90%) |

### Parameter Tuning Guide

#### Proximity Thresholds (Close at High/Low)

- **0.95 or higher**: Stricter - only very strong candles qualify

- **0.90 (default)**: Balanced - good for most market conditions

- **0.80 or lower**: Looser - catches more patterns, higher false signals

#### Doji Threshold

- **0.05-0.10**: Strict doji identification

- **0.10-0.15**: Standard doji detection

- **0.15+**: Includes near-doji patterns

#### Lookback Period

- **3-5 bars**: Fast, sensitive to recent patterns

- **5-10 bars**: Balanced approach

- **10-20 bars**: Slower, filters out noise

## Visual Indicators

### Chart Markers

- **Green Up Arrow** ▲: Long entry signal triggered

- **Red Down Arrow** ▼: Short entry signal triggered

- **Gray X**: Skip signal (too many dojis detected)

### Statistics Table

Located at top-right corner, displays real-time pattern counts:

- **Close at High**: Count of candles closing near the high

- **Close at Low**: Count of candles closing near the low

- **Doji**: Count of doji/near-doji patterns

### Signal Labels

- Green label: "✓ Long condition met" - below entry bar

- Red label: "✓ Short condition met" - above entry bar

- Gray label: "⊠ Too many dojis, skip" - trade skipped

## Risk Management

### Exit Strategy

The strategy includes built-in exit rules based on ATR (Average True Range):

- **Stop Loss**: ATR × 2

- **Take Profit**: ATR × 3

Example: If ATR is $10, stop loss is at -$20 and take profit is at +$30

### Position Sizing

Default: 100% of equity per trade (adjustable in strategy properties)

**Recommendation**: Reduce to 10-25% of equity for safer capital allocation

## How to Use

### 1. Copy the Script

1. Open TradingView

2. Go to Pine Script Editor

3. Create a new indicator

4. Copy the entire `candle_pattern_strategy.pine` content

5. Click "Add to Chart"

### 2. Apply to Chart

- Select your preferred timeframe (1m, 5m, 15m, 1h, 4h, 1d)

- Choose a trading symbol (stocks, forex, crypto, etc.)

- The strategy will generate signals on all historical bars and in real-time

### 3. Configure Parameters

1. Right-click the strategy on chart → "Settings"

2. Adjust parameters in the "Inputs" tab

3. Strategy will recalculate automatically

4. Backtest results appear in the Strategy Tester panel

### 4. Backtesting

1. Click "Strategy Tester" (bottom panel)

2. Set date range for historical testing

3. Review performance metrics:

- Win rate

- Profit factor

- Drawdown

- Total returns

## Key Features

✅ **Execution Model Compliant** - Follows official Pine Script V6 standards

✅ **Global Scope** - All historical references in global scope for consistency

✅ **Adjustable Sensitivity** - Fine-tune all pattern detection thresholds

✅ **Real-time Updates** - Works on both historical and real-time bars

✅ **Visual Feedback** - Clear signals with labels and statistics table

✅ **Risk Management** - Built-in ATR-based stop loss and take profit

✅ **No Repainting** - Signals remain consistent after bar closes

## Important Notes

### Before Trading Live

1. **Backtest thoroughly**: Test on at least 6-12 months of historical data

2. **Paper trading first**: Practice with simulated trades

3. **Optimize parameters**: Find the best settings for your trading instrument

4. **Manage risk**: Never risk more than 1-2% per trade

5. **Monitor performance**: Review trades regularly and adjust as needed

### Market Conditions

The strategy works best in:

- Trending markets with clear directional bias

- Range-bound markets with defined support/resistance

- Markets with moderate volatility

The strategy may underperform in:

- Highly choppy/noisy markets (many false signals)

- Markets with gaps or overnight gaps

- Low liquidity periods

### Limitations

- Works on chart timeframes only (not intrabar analysis)

- Requires at least 5 bars of history (configurable)

- Fixed exit rules may not suit all trading styles

- No trend filtering (will trade both directions)

## Technical Details

### Historical Buffer Management

The strategy declares maximum bars back to ensure enough historical data:

```pine

max_bars_back(close, 20)

max_bars_back(open, 20)

max_bars_back(high, 20)

max_bars_back(low, 20)

```

This prevents runtime errors when accessing historical candlestick data.

### Pattern Detection Algorithm

```

For each bar in lookback period:

1. Calculate (high - close) / (high - low) → close_to_high_ratio

2. If close_to_high_ratio ≤ (1 - threshold) → count as "Close at High"

3. Calculate (close - low) / (high - low) → close_to_low_ratio

4. If close_to_low_ratio ≤ (1 - threshold) → count as "Close at Low"

5. Calculate abs(close - open) / (high - low) → body_ratio

6. If body_ratio ≤ doji_threshold → count as "Doji"

Signal Generation:

7. If doji_count ≥ cross_count_limit → SKIP_SIGNAL

8. If close_at_high_count ≥ 2 AND last_close_at_high → LONG_SIGNAL

9. If close_at_low_count ≥ 2 AND last_close_at_low → SHORT_SIGNAL

```

## Example Scenarios

### Scenario 1: Bullish Signal

```

Last 5 bars pattern:

Bar 1: Closes at high (95%) ✓

Bar 2: Closes at high (92%) ✓

Bar 3: Closes at mid (50%)

Bar 4: Closes at low (10%)

Bar 5: Closes at high (96%) ✓ (last bar)

Result:

- Close at high count: 3 (≥ 2) ✓

- Last closes at high: ✓

- Doji count: 0 (< 3) ✓

→ LONG SIGNAL ✓

```

### Scenario 2: Skip Signal

```

Last 5 bars pattern:

Bar 1: Doji pattern ✓

Bar 2: Doji pattern ✓

Bar 3: Closes at mid

Bar 4: Doji pattern ✓

Bar 5: Closes at high

Result:

- Doji count: 3 (≥ 3)

→ SKIP SIGNAL - Market too chaotic

```

## Performance Optimization

### Tips for Better Results

1. **Use Higher Timeframes**: 15m or higher reduces false signals

2. **Combine with Indicators**: Add volume or trend filters

3. **Seasonal Adjustment**: Different parameters for different seasons

4. **Instrument Selection**: Test on liquid, high-volume instruments

5. **Regular Rebalancing**: Adjust parameters quarterly based on performance

## Troubleshooting

### No Signals Generated

- Check if lookback period is too large

- Verify proximity thresholds aren't too strict (try 0.85 instead of 0.95)

- Ensure doji limit allows for trading (try 4-5 instead of 3)

### Too Many False Signals

- Increase proximity thresholds to 0.95+

- Reduce lookback period to 3-4 bars

- Increase doji limit to 3-4

- Test on higher timeframes

### Strategy Tester Shows Losses

- Review individual trades to identify patterns

- Adjust stop loss and take profit ratios

- Change lookback period and thresholds

- Test on different market conditions

## References

- (www.tradingview.com)

- (www.tradingview.com)

- (www.investopedia.com)

- (www.investopedia.com)

## Disclaimer

**This strategy is provided for educational and research purposes only.**

- Not financial advice

- Past performance does not guarantee future results

- Always conduct thorough backtesting before live trading

- Trading involves significant risk of loss

- Use proper risk management and position sizing

## License

Created: December 15, 2025

Version: 1.0

---

**For updates and modifications, refer to the accompanying documentation files.**

Trading Dashboard + Daily SMAsThis indicator is an all-in-one workspace overlay designed for futures and intraday traders. It consolidates critical market internals, session statistics, and daily technical levels into a single, highly customizable dashboard.

The goal of this script is to reduce chart clutter by placing essential data into a clean table while overlaying key Daily Moving Averages onto your intraday timeframe.

Key Features:

1. Comprehensive Market Internals Dashboard Monitor the health of the broad market directly from your chart. The dashboard includes real-time data for:

VIX: Volatility Index.

TICK & TRIN: Sentiment and volume flow indicators.

Breadth Data: ADD, ADV, and DECL (Advance/Decline lines and volume).

Multi-Ticker Watch: Monitor 3 additional assets (Defaults: NQ, RTY, YM) with real-time price and % change.

2. Session Statistics & Probabilities Automated calculation of intraday statistics based on a user-defined lookback period (default 100 days):

RTH Data: Tracks Regular Trading Hours Open, Close, and Range.

Contextual ATR: Compares current RTH range to the 14-day ATR.

Probabilities: Displays historical probabilities for "Gap Fill," "Break of Yesterday's High," and "Break of Yesterday's Low."

3. Daily SMAs on Intraday Charts Plot key Daily Simple Moving Averages (21, 50, 200) directly on your lower timeframe charts (1m, 5m, etc.) without switching views.

Fully Customizable: Toggle each SMA on/off individually.

Color Control: Users can change the color of every SMA line to fit their theme.

4. "Dark Mode" Optimized The dashboard features a specific "Very Dark Grey" (#121212) background by default, designed to reduce eye strain and blend seamlessly with dark-themed trading setups.

Settings & Customization:

Session Times: Define your specific RTH start and end times.

Symbols: All ticker symbols (VIX, ADD, NQ, etc.) can be customized in the settings menu to match your data provider.

Visibility: Every element in the table and every SMA line has a toggle switch. You only see what you need.

Visuals: Change table position, text size, and line colors.

Author's Instructions: Configuration Guide

This script relies on specific ticker symbols to pull data for Market Internals (TICK, TRIN, ADD) and the Watchlist. Depending on your data subscription plan (CME, CBOE, etc.), you may need to adjust the default symbols to match what you have access to.

1. How to Change Symbols

Add the indicator to your chart.

Hover over the indicator name in the top-left corner and click the Settings (Gear Icon).

Scroll to the "Symbols" section.

Click inside the text box for the symbol you want to change.

2. Common Symbol Formats If the default symbols show "N/A" or "Error," try these alternatives based on your data feed:

TICK (NYSE Tick)

Default: USI:TICK (Requires specific data)

Alternative: TVC:TICK (General TradingView feed)

Alternative: TICK (Generic)

TRIN (Arms Index)

Default: USI:TRIN

Alternative: TVC:TRIN

Alternative: TRIN

Breadth (ADD/ADV/DECL)

ADD (Advance-Decline Line): Try USI:ADD, TVC:ADD, or ADD

ADV (Advancing Volume): Try USI:ADV, TVC:ADV, or UVOL (Up Volume)

DECL (Declining Volume): Try USI:DECL, TVC:DECL, or DVOL (Down Volume)

VIX

Standard: CBOE:VIX or TVC:VIX

3. Setting Up the Ticker Watchlist (Ticker 1, 2, 3) The script defaults to "Continuous Contracts" (indicated by the 1!), which automatically rolls to the front month.

Nasdaq: CME_MINI:NQ1!

S&P 500: CME_MINI:ES1!

Russell 2000: CME_MINI:RTY1!

Dow Jones: CBOT_MINI:YM1!

Note: If you want to watch a specific contract month (e.g., December 2025), enter the specific code like NQZ2025.

4. Troubleshooting "N/A" Data If a cell in the table is empty or says "N/A":

Verify you are not viewing the chart on a timeframe that excludes the data (though dynamic_requests=true usually handles this).

Ensure you have the correct data permission for that specific symbol.

Market Closed: Some internal data points only populate during the active NYSE session (09:30 - 16:00 ET).

Disclaimer: This tool is for informational purposes only and does not constitute financial advice. Past probabilities do not guarantee future results.

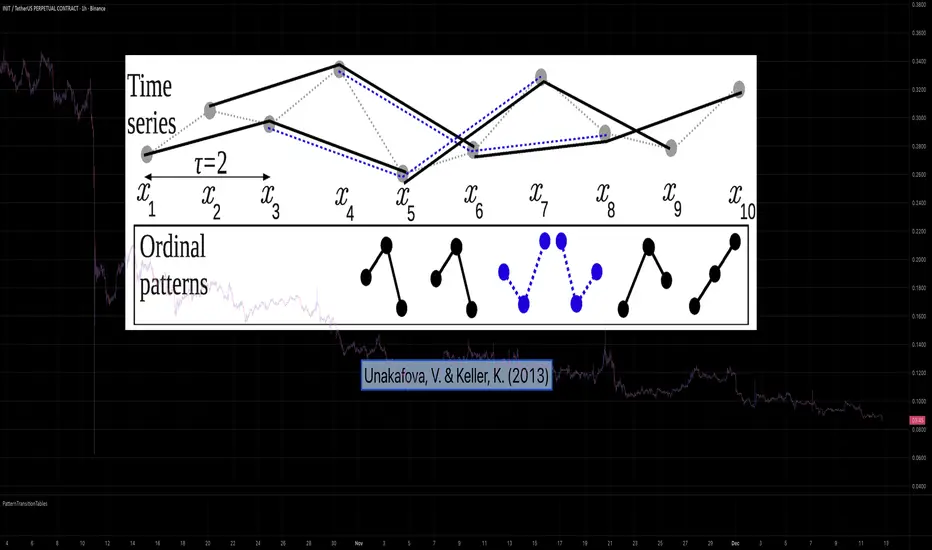

PatternTransitionTablesPatternTransitionTables Library

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- 1. INTRODUCTION --------- 🌸

💮 Overview

This library provides precomputed state transition tables to enable ultra-efficient, O(1) computation of Ordinal Patterns. It is designed specifically to support high-performance indicators calculating Permutation Entropy and related complexity measures.

💮 The Problem & Solution

Calculating Permutation Entropy, as introduced by Bandt and Pompe (2002), typically requires computing ordinal patterns within a sliding window at every time step. The standard successive-pattern method (Equations 2+3 in the paper) requires ≤ 4d-1 operations per update.

Unakafova and Keller (2013) demonstrated that successive ordinal patterns "overlap" significantly. By knowing the current pattern index and the relative rank (position l) of just the single new data point, the next pattern index can be determined via a precomputed look-up table. Computing l still requires d comparisons, but the table lookup itself is O(1), eliminating the need for d multiplications and d additions. This reduces total operations from ≤ 4d-1 to ≤ 2d per update (Table 4). This library contains these precomputed tables for orders d = 2 through d = 5.

🌸 --------- 2. THEORETICAL BACKGROUND --------- 🌸

💮 Permutation Entropy

Bandt, C., & Pompe, B. (2002). Permutation entropy: A natural complexity measure for time series.

doi.org

This concept quantifies the complexity of a system by comparing the order of neighbouring values rather than their magnitudes. It is robust against noise and non-linear distortions, making it ideal for financial time series analysis.

💮 Efficient Computation

Unakafova, V. A., & Keller, K. (2013). Efficiently Measuring Complexity on the Basis of Real-World Data.

doi.org

This library implements the transition function φ_d(n, l) described in Equation 5 of the paper. It maps a current pattern index (n) and the position of the new value (l) to the successor pattern, reducing the complexity of updates to constant time O(1).

🌸 --------- 3. LIBRARY FUNCTIONALITY --------- 🌸

💮 Data Structure

The library stores transition matrices as flattened 1D integer arrays. These tables are mathematically rigorous representations of the factorial number system used to enumerate permutations.

💮 Core Function: get_successor()

This is the primary interface for the library for direct pattern updates.

• Input: The current pattern index and the rank position of the incoming price data.

• Process: Routes the request to the specific transition table for the chosen order (d=2 to d=5).

• Output: The integer index of the next ordinal pattern.

💮 Table Access: get_table()

This function returns the entire flattened transition table for a specified dimension. This enables local caching of the table (e.g. in an indicator's init() method), avoiding the overhead of repeated library calls during the calculation loop.

💮 Supported Orders & Terminology

The parameter d is the order of ordinal patterns (following Bandt & Pompe 2002). Each pattern of order d contains (d+1) data points, yielding (d+1)! unique patterns:

• d=2: 3 points → 6 unique patterns, 3 successor positions

• d=3: 4 points → 24 unique patterns, 4 successor positions

• d=4: 5 points → 120 unique patterns, 5 successor positions

• d=5: 6 points → 720 unique patterns, 6 successor positions

Note: d=6 is not implemented. The resulting code size (approx. 191k tokens) exceeds the Pine Script limit of 100k tokens (as of 2025-12).

Trend Following $BTC - Multi-Timeframe Structure + ReversTREND FOLLOWING STRATEGY - MULTI-TIMEFRAME STRUCTURE BREAKOUT SYSTEM

Strategy Overview

This is an enhanced Turtle Trading system designed for cryptocurrency spot trading. It combines Donchian Channel breakouts with multi-timeframe structure filtering and ATR-based dynamic risk management. The strategy trades both long and short positions using reverse signal exits to maximize trend capture.

Core Features

Multi-Timeframe Structure Filtering

The strategy uses Swing High/Low analysis to identify market structure trends. You can customize the structure timeframe (default: 3 minutes) to match your trading style. Only enters trades aligned with the identified trend direction, avoiding counter-trend positions that often lead to losses.

Reverse Signal Exit System

Instead of using fixed stop-losses or time-based exits, this strategy exits positions only when a reverse entry signal triggers. This approach maximizes trend profits and reduces premature exits during normal market retracements.

ATR Dynamic Pyramiding

Automatically adds positions when price moves 0.5 ATR in your favor. Supports up to 2 units maximum (adjustable). This pyramid scaling enhances profitability during strong trends while maintaining disciplined risk management.

Complete Risk Management

Fixed position sizing at 5000 USD per unit. Includes realistic commission fees of 0.06% (Binance spot rate). Initial capital set at 10,000 USD. All backtest parameters reflect real-world trading conditions.

Trading Logic

Entry Conditions

Long Entry: Close price breaks above the 20-period high AND structure trend is bullish (price breaks above Swing High)

Short Entry: Close price breaks below the 20-period low AND structure trend is bearish (price breaks below Swing Low)

Position Scaling

Long positions: Add when price rises 0.5 ATR or more

Short positions: Add when price falls 0.5 ATR or more

Maximum 2 units including initial entry

Exit Conditions

Long Exit: Triggers when short entry signal appears (price breaks 20-period low + structure turns bearish)

Short Exit: Triggers when long entry signal appears (price breaks 20-period high + structure turns bullish)

Default Parameters

Channel Settings

Entry Channel Period: 20 (Donchian Channel breakout period)

Exit Channel Period: 10 (reserved parameter)

ATR Settings

ATR Period: 20

Stop Loss ATR Multiplier: 2.0

Add Position ATR Multiplier: 0.5

Structure Filter

Swing Length: 300 (Swing High/Low calculation period)

Structure Timeframe: 3 minutes

Adjust these based on your trading timeframe and asset volatility

Position Management

Maximum Units: 2 (including initial entry)

Capital Per Unit: 5000 USD

Visualization Features

Background Colors

Light Green: Bullish market structure

Light Red: Bearish market structure

Dark Green: Long position entry

Dark Red: Short position entry

Optional Display Elements (Default: OFF)

Entry and exit channel lines

Structure high/low reference lines

ATR stop-loss indicator

Next position add level

Entry/exit labels

Alert Message Format

The strategy sends notifications with the following format:

Entry: "5m Long EP:90450.50"

Add Position: "15m Add Long 2/2 EP:91000.25"

Exit: "5m Close Long Reverse Signal"

Where the first part shows your current chart timeframe and EP indicates Entry Price

Backtest Settings

Capital Allocation

Initial Capital: 10,000 USD

Per Entry: 5,000 USD (split into 2 potential entries)

Leverage: 0x (spot trading only)

Trading Costs

Commission: 0.06% (Binance spot VIP0 rate)

Slippage: 0 (adjust based on your experience)

Best Use Cases

Ideal Scenarios

Trending markets with clear directional movement

Moderate to high volatility assets

Timeframes from 1-minute to 4-hour charts

Best suited for major cryptocurrencies with good liquidity

Not Recommended For

Highly volatile choppy/ranging markets

Low liquidity small-cap coins

Extreme market conditions or black swan events

Usage Recommendations

Timeframe Guidelines

1-5 minute charts: Use for scalping, consider Swing Length 100-160

15-30 minute charts: Good for short-term trading, Swing Length 50-100

1-4 hour charts: Suitable for swing trading, Swing Length 20-50

Optimization Tips

Always backtest on historical data before live trading

Adjust swing length based on asset volatility and your timeframe

Different cryptocurrencies may require different parameter settings

Enable visualization options initially to understand entry/exit points

Monitor win rate and drawdown during backtesting

Technical Details

Built on Pine Script v6

No repainting - uses proper bar referencing with offset

Prevents lookahead bias with lookahead=off parameter

Strategy mode with accurate commission and slippage modeling

Multi-timeframe security function for structure analysis

Proper position state tracking to avoid duplicate signals

Risk Disclaimer

This strategy is provided for educational and research purposes only. Past performance does not guarantee future results. Backtesting results may differ from live trading due to slippage, execution delays, and changing market conditions. The strategy performs best in trending markets and may experience drawdowns during ranging conditions. Always practice proper risk management and never risk more than you can afford to lose. It is recommended to paper trade first and start with small position sizes when going live.

How to Use

Add the strategy to your TradingView chart

Select your desired timeframe (1m to 4h recommended)

Adjust parameters based on your risk tolerance and trading style

Review backtest results in the Strategy Tester tab

Set up alerts for automated notifications

Consider paper trading before risking real capital

Tags

Trend Following, Turtle Trading, Donchian Channel, Structure Breakout, ATR, Cryptocurrency, Spot Trading, Risk Management, Pyramiding, Multi-Timeframe Analysis

---

Strategy Name: Trend Following BTC

Version: v1.0

Pine Script Version: v6

Last Updated: December 2025

Trend Following $ZEC - Multi-Timeframe Structure Filter + Revers# Trend Following CRYPTOCAP:ZEC - Strategy Guide

## 📊 Strategy Overview

Trend Following CRYPTOCAP:ZEC is an enhanced Turtle Trading system designed for cryptocurrency spot trading, combining Donchian Channel breakouts, multi-timeframe structure filtering, and ATR-based dynamic risk management for both long and short positions.

---

## 🎯 Core Features

1. Multi-Timeframe Structure Filtering

- Uses Swing High/Low to identify market structure

- Customizable structure timeframe (default: 1 minute)

- Only enters trades in the direction of the trend, avoiding counter-trend positions

2. Reverse Signal Exit

- No fixed stop-loss or fixed-period exits

- Exits only when a reverse entry signal triggers

- Maximizes trend profits, reduces premature exits

3. ATR Dynamic Pyramiding

- Adds positions when price moves 0.5 ATR in favorable direction

- Supports up to 2 units maximum (adjustable)

- Pyramid scaling to enhance profitability

4. Complete Risk Management

- Fixed position size (5000 USD per unit)

- Commission fee 0.06% (Binance spot rate)

- Initial capital 10,000 USD

---

## 📈 Trading Logic

Entry Conditions

✅ Long Entry:

- Close price breaks above 20-period high

- Structure trend is bullish (price breaks above Swing High)

✅ Short Entry:

- Close price breaks below 20-period low

- Structure trend is bearish (price breaks below Swing Low)

Add Position Conditions

- Long: Price rises ≥ 0.5 ATR

- Short: Price falls ≥ 0.5 ATR

- Maximum 2 units including initial entry

Exit Conditions

- Long Exit: When short entry signal triggers (price breaks 20-period low + structure turns bearish)

- Short Exit: When long entry signal triggers (price breaks 20-period high + structure turns bullish)

---

## ⚙️ Parameter Settings

Channel Settings

- Entry Channel Period: 20 (Donchian Channel breakout period)

- Exit Channel Period: 10 (reserved parameter, actually uses reverse signal exit)

ATR Settings

- ATR Period: 20

- Stop Loss ATR Multiplier: 2.0 (reserved parameter)

- Add Position ATR Multiplier: 0.5

Structure Filter

- Swing Length: 160 (Swing High/Low calculation period)

- Structure Timeframe: 1 minute (can change to 5/15/60, etc.)

Position Management

- Maximum Units: 2 (including initial entry)

- Capital Per Unit: 5000 USD

---

## 🎨 Visualization Features

Background Colors

- Light Green: Bullish structure

- Light Red: Bearish structure

- Dark Green: Long entry

- Dark Red: Short entry

Optional Display (Default: OFF)

- Entry/exit channel lines

- Structure high/low lines

- ATR stop-loss line

- Next add position indicator

- Entry/exit labels

---

## 📱 Alert Message Format

Strategy sends notifications on entry/exit with the following format:

- Entry: `1m Long EP:428.26`

- Add Position: `15m Add Long 2/2 EP:429.50`

- Exit: `1m Close Long Reverse Signal`

Where:

- `1m`/`15m` = Current chart timeframe

- `EP` = Entry Price

---

## 💰 Backtest Settings

Capital Allocation

- Initial Capital: 10,000 USD

- Per Entry: 5,000 USD (split into 2 entries)

- Leverage: 0x (spot trading)

Trading Costs

- Commission: 0.06% (Binance spot VIP0)