Custom NYSE Hourly Intervals (Gris Extra Claro/T)NYSE Custom Hourly Intervals (Background Shading)

Indicator Overview:

This TradingView indicator visually highlights specific hourly intervals during the NYSE trading session (9:30 AM - 4:00 PM ET) using background shading. Its purpose is to help traders easily identify these key periods while analyzing price action.

Features:

Hourly Segmentation: Clearly marks the following hourly blocks within the NYSE session:

9:30 - 10:00 ET

10:00 - 11:00 ET

11:00 - 12:00 ET

12:00 - 13:00 ET

13:00 - 14:00 ET

14:00 - 15:00 ET

15:00 - 16:00 ET

Alternating Background: Uses a subtle, alternating background pattern for visual distinction:

Transparent: Applied during the 9:30-10:00, 11:00-12:00, 13:00-14:00, and 15:00-16:00 intervals (shows your default chart background).

Very Light Gray: Applied during the 10:00-11:00, 12:00-13:00, and 14:00-15:00 intervals.

Timeframe Restriction: The background shading is active only on chart timeframes of 30 minutes or less (e.g., 30m, 15m, 5m, 1m). It will not appear on higher timeframes.

Session Restriction: Shading only occurs during the defined NYSE session hours (9:30 AM - 4:00 PM ET).

Customization: The color and transparency level of the "Very Light Gray" shading can be adjusted in the indicator's settings.

Purpose & Use Case:

This indicator is ideal for intraday traders who want a clean visual guide to track price movement within specific hourly segments of the NYSE trading day, without needing complex overlays.

Tìm kiếm tập lệnh với "30年国债收益率"

Multi-Timeframe Open LinesThe Multi-Timeframe Open Lines indicator is designed to help traders visualize key price levels at the open of specific time intervals. It draws horizontal lines at the open of 5-minute, 15-minute, 30-minute, and hourly candles, extending these lines to the start of the next respective interval. Traders can now control which timeframes are displayed and how many past opening lines are shown, ensuring a clean and organized chart.

Key Features:

Customizable Lines:

5-Minute Lines: Highlight the open of every 5-minute candle, ending at the start of the next 5-minute candle.

15-Minute Lines: Highlight the open of every 15-minute candle, ending at the start of the next 15-minute candle.

30-Minute Lines: Highlight the open of every 30-minute candle, ending at the start of the next 30-minute candle.

Hourly Lines: Highlight the open of every hourly candle, ending at the start of the next hourly candle.

Each timeframe's lines can be customized in terms of color, line style, and thickness.

Toggle Options:

Easily turn on or off the display of lines for each timeframe (5m, 15m, 30m, 1h) using checkboxes in the settings.

User-Defined Limits:

Control the number of past opening lines displayed for each timeframe (5m, 15m, 30m, 1h).

Prevents chart clutter by limiting the number of visible lines.

Multi-Timeframe Analysis:

Enables traders to analyze price action across multiple timeframes simultaneously, providing a clearer picture of market structure and key levels.

User-Friendly Inputs:

Easy-to-use settings for customizing line appearance and behavior, ensuring the indicator fits seamlessly into any trading strategy.

How to Use:

Apply the indicator to your chart to visualize the open price levels for 5-minute, 15-minute, 30-minute, and hourly candles.

Use the lines as dynamic support/resistance levels or to identify potential breakout/breakdown points.

Customize the colors, styles, and the number of visible lines to match your chart theme or trading preferences.

Toggle specific timeframes on or off to focus on the most relevant price levels.

Ideal For:

Traders who use multi-timeframe analysis.

Those who rely on key price levels for decision-making.

Anyone looking to enhance their chart with clear, customizable reference lines while avoiding clutter.

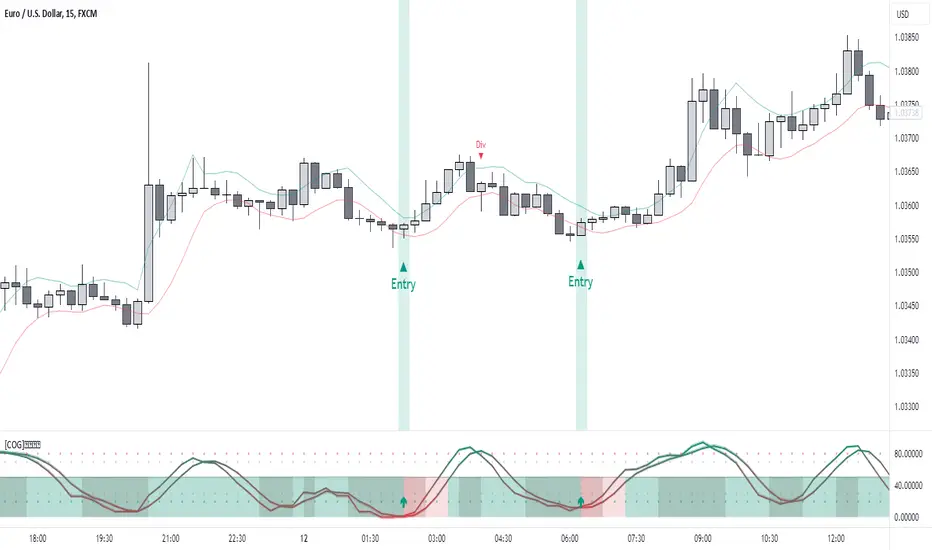

[COG]StochRSI Zenith📊 StochRSI Zenith

This indicator combines the traditional Stochastic RSI with enhanced visualization features and multi-timeframe analysis capabilities. It's designed to provide traders with a comprehensive view of market conditions through various technical components.

🔑 Key Features:

• Advanced StochRSI Implementation

- Customizable RSI and Stochastic calculation periods

- Multiple moving average type options (SMA, EMA, SMMA, LWMA)

- Adjustable signal line parameters

• Visual Enhancement System

- Dynamic wave effect visualization

- Energy field display for momentum visualization

- Customizable color schemes for bullish and bearish signals

- Adaptive transparency settings

• Multi-Timeframe Analysis

- Higher timeframe confirmation

- Synchronized market structure analysis

- Cross-timeframe signal validation

• Divergence Detection

- Automated bullish and bearish divergence identification

- Customizable lookback period

- Clear visual signals for confirmed divergences

• Signal Generation Framework

- Price action confirmation

- SMA-based trend filtering

- Multiple confirmation levels for reduced noise

- Clear entry signals with customizable display options

📈 Technical Components:

1. Core Oscillator

- Base calculation: 13-period RSI (adjustable)

- Stochastic calculation: 8-period (adjustable)

- Signal lines: 5,3 smoothing (adjustable)

2. Visual Systems

- Wave effect with three layers of visualization

- Energy field display with dynamic intensity

- Reference bands at 20/30/50/70/80 levels

3. Confirmation Mechanisms

- SMA trend filter

- Higher timeframe alignment

- Price action validation

- Divergence confirmation

⚙️ Customization Options:

• Visual Parameters

- Wave effect intensity and speed

- Energy field sensitivity

- Color schemes for bullish/bearish signals

- Signal display preferences

• Technical Parameters

- All core calculation periods

- Moving average types

- Divergence detection settings

- Signal confirmation criteria

• Display Settings

- Chart and indicator signal placement

- SMA line visualization

- Background highlighting options

- Label positioning and size

🔍 Technical Implementation:

The indicator combines several advanced techniques to generate signals. Here are key components with code examples:

1. Core StochRSI Calculation:

// Base RSI calculation

rsi = ta.rsi(close, rsi_length)

// StochRSI transformation

stochRSI = ((ta.highest(rsi, stoch_length) - ta.lowest(rsi, stoch_length)) != 0) ?

(100 * (rsi - ta.lowest(rsi, stoch_length))) /

(ta.highest(rsi, stoch_length) - ta.lowest(rsi, stoch_length)) : 0

2. Signal Generation System:

// Core signal conditions

crossover_buy = crossOver(sk, sd, cross_threshold)

valid_buy_zone = sk < 30 and sd < 30

price_within_sma_bands = close <= sma_high and close >= sma_low

// Enhanced signal generation

if crossover_buy and valid_buy_zone and price_within_sma_bands and htf_allows_long

if is_bullish_candle

long_signal := true

else

awaiting_bull_confirmation := true

3. Multi-Timeframe Analysis:

= request.security(syminfo.tickerid, mtf_period,

)

The HTF filter looks at a higher timeframe (default: 4H) to confirm the trend

It only allows:

Long trades when the higher timeframe is bullish

Short trades when the higher timeframe is bearish

📈 Trading Application Guide:

1. Signal Identification

• Oversold Opportunities (< 30 level)

- Look for bullish crosses of K-line above D-line

- Confirm with higher timeframe alignment

- Wait for price action confirmation (bullish candle)

• Overbought Conditions (> 70 level)

- Watch for bearish crosses of K-line below D-line

- Verify higher timeframe condition

- Confirm with bearish price action

2. Divergence Trading

• Bullish Divergence

- Price makes lower lows while indicator makes higher lows

- Most effective when occurring in oversold territory

- Use with support levels for entry timing

• Bearish Divergence

- Price makes higher highs while indicator shows lower highs

- Most reliable in overbought conditions

- Combine with resistance levels

3. Wave Effect Analysis

• Strong Waves

- Multiple wave lines moving in same direction indicate momentum

- Wider wave spread suggests increased volatility

- Use for trend strength confirmation

• Energy Field

- Higher intensity in trading zones suggests stronger moves

- Use for momentum confirmation

- Watch for energy field convergence with price action

The energy field is like a heat map that shows momentum strength

It gets stronger (more visible) when:

Price is in oversold (<30) or overbought (>70) zones

The indicator lines are moving apart quickly

A strong signal is forming

Think of it as a "strength meter" - the more visible the energy field, the stronger the potential move

4. Risk Management Integration

• Entry Confirmation

- Wait for all signal components to align

- Use higher timeframe for trend direction

- Confirm with price action and SMA positions

• Stop Loss Placement

- Consider placing stops beyond recent swing points

- Use ATR for dynamic stop calculation

- Account for market volatility

5. Position Management

• Partial Profit Taking

- Consider scaling out at overbought/oversold levels

- Use wave effect intensity for exit timing

- Monitor energy field for momentum shifts

• Trade Duration

- Short-term: Use primary signals in trading zones

- Swing trades: Focus on divergence signals

- Position trades: Utilize higher timeframe signals

⚠️ Important Usage Notes:

• Avoid:

- Trading against strong trends

- Relying solely on single signals

- Ignoring higher timeframe context

- Over-leveraging based on signals

Remember: This tool is designed to assist in analysis but should never be used as the sole decision-maker for trades. Always maintain proper risk management and combine with other forms of analysis.

Opening Range, Initial Balance, Opening Price, Pre-market Levels### Description of the Indicator: **Opening Range, Initial Balance, Opening Price, Pre-market Levels**

This custom TradingView indicator provides a comprehensive view of key price levels for intraday trading, specifically designed to track important levels from the Opening Range (OR), Initial Balance (IB), Opening Price (OP), and Pre-market session (PM). These levels are essential for traders to gauge potential market movements and identify critical areas of support and resistance.

#### **Features:**

1. **Opening Range (OR):**

- This is the high and low of the first 30 minutes of the regular market session (09:30 - 10:00 EST).

- The OR high and low act as significant levels that may influence price movement for the rest of the day.

- The mid-level of the Opening Range (OR Mid) is also plotted to give a more detailed view of potential price action.

2. **Initial Balance (IB):**

- The Initial Balance is the range created during the first hour of market activity (09:30 - 10:30 EST).

- This range often sets the tone for the market's direction. The IB high and low, along with the IB midline, are plotted for quick reference.

3. **Opening Price (OP):**

- The opening price of the market is marked as a circle and labeled "OP."

- This level provides context for market sentiment when compared to the high and low levels.

4. **Pre-market Levels (PM):**

- The pre-market session (04:00 - 09:30 EST) has its own important levels that are calculated for the high, low, and mid range (PM High, PM Low, and PM Mid).

- These levels are plotted and are useful for traders to understand where the market stood before the regular session opened.

#### **Customization Options:**

- **Exchange Timezone:** You can choose whether to display the times in the exchange's local timezone or in your own preferred timezone.

- **Mid Levels Display:** You can toggle whether the mid levels for each range (OR, IB, PM) should be shown on the chart.

- **Level Color Change:** The colors of the plotted levels (high, low, mid) change based on whether the price is above or below the respective level, making it easy to visualize potential support and resistance.

- **Label Positions:** The position of the labels (OR, IB, OP, PM) on the chart can be customized to avoid overlap with other data points.

#### **Key Use Cases:**

- **Intraday Trend Analysis:** Use the OR and IB to identify key levels for the day, providing insights into the possible trend or range for the day.

- **Pre-market Insights:** The PM levels are crucial for understanding where the market stood during the pre-market hours and can be used as reference points during the regular session.

- **Potential Support and Resistance:** The high and low levels of the OR, IB, and PM sessions can act as potential support or resistance, which are useful for setting stop-loss and take-profit levels.

#### **How to Use:**

- Pay attention to the levels provided for OR, IB, and PM as potential entry and exit points.

- Watch for breakouts or reversals around these levels, especially when combined with other technical indicators or price action patterns.

- The mid levels offer an additional reference to assess price direction or identify possible areas of consolidation.

This indicator is perfect for day traders who rely on key intraday levels and pre-market activity to make informed trading decisions. It helps to streamline the process of identifying potential breakouts, reversals, and ranges in the market.

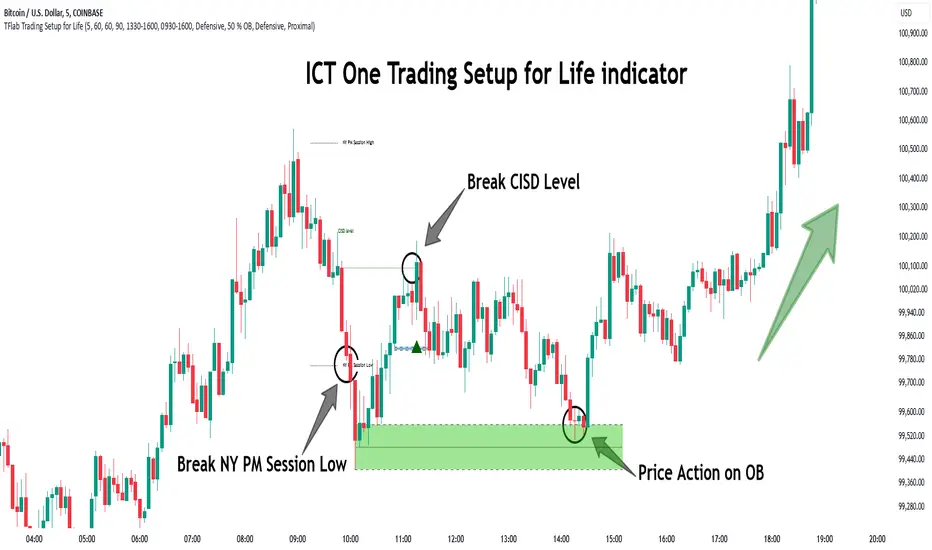

One Trading Setup for Life ICT [TradingFinder] Sweep Session FVG🔵 Introduction

ICT One Trading Setup for Life is a trading strategy based on liquidity and market structure shifts, utilizing the PM Session Sweep to determine price direction. In this strategy, the market first forms a price range during the PM Session (from 13:30 to 16:00 EST), which includes the highest high (PM Session High) and lowest low (PM Session Low).

In the next session, the price first touches one of these levels to trigger a Liquidity Hunt before confirming its trend by breaking the Change in State of Delivery (CISD) Level. After this confirmation, the price retraces toward a Fair Value Gap (FVG) or Order Block (OB), which serve as the best entry points in alignment with liquidity.

In financial markets, liquidity is the primary driver of price movement, and major market participants such as institutional investors and banks are constantly seeking liquidity at key levels. This process, known as Liquidity Hunt or Liquidity Sweep, occurs when the price reaches an area with a high concentration of orders, absorbs liquidity, and then reverses direction.

In this setup, the PM Session range acts as a trading framework, where its highs and lows function as key liquidity zones that influence the next session’s price movement. After the New York market opens at 9:30 EST, the price initially breaks one of these levels to capture liquidity.

However, for a trend shift to be confirmed, the CISD Level must be broken.

Once the CISD Level is breached, the price retraces toward an FVG or OB, which serve as optimal trade entry points.

Bullish Setup :

Bearish Setup :

🔵 How to Use

In this strategy, the PM Session range is first identified, which includes the highest high (PM Session High) and lowest low (PM Session Low) between 13:30 and 16:00 EST. In the following session, the price touches one of these levels for a Liquidity Hunt, followed by a break of the Change in State of Delivery (CISD) Level. The price then retraces toward a Fair Value Gap (FVG) or Order Block (OB), creating a trading opportunity.

This process can occur in two scenarios : bearish and bullish setups.

🟣 Bullish Setup

In a bullish scenario, the PM Session High and PM Session Low are identified. In the following session, the price first breaks the PM Session Low, absorbing liquidity. This process results in a Fake Breakout to the downside, misleading retail traders into taking short positions.

After the Liquidity Hunt, the CISD Level is broken, confirming a trend reversal. The price then retraces toward an FVG or OB, offering an optimal long entry opportunity.

The initial take-profit target is the PM Session High, but if higher timeframe liquidity levels exist, extended targets can be set.

The stop-loss should be placed below the Fake Breakout low or the first candle of the FVG.

🟣 Bearish Setup

In a bearish scenario, the market first defines its PM Session High and PM Session Low. In the next session, the price initially breaks the PM Session High, triggering a Liquidity Hunt. This movement often causes a Fake Breakout, misleading retail traders into taking incorrect positions.

After absorbing liquidity, the CISD Level breaks, indicating a shift in market structure. The price then retraces toward an FVG or OB, offering the best short entry opportunity.

The initial take-profit target is the PM Session Low, but if additional liquidity exists on higher timeframes, lower targets can be considered.

The stop-loss should be placed above the Fake Breakout high or the first candle of the FVG.

🔵 Setting

CISD Bar Back Check : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

Order Block Validity : The number of candles that determine the validity of an Order Block.

FVG Validity : The duration for which a Fair Value Gap remains valid.

CISD Level Validity : The duration for which a CISD Level remains valid after being broken.

New York PM Session : Defines the PM Session range from 13:30 to 16:00 EST.

New York AM Session : Defines the AM Session range from 9:30 to 16:00 EST.

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

Demand Order Block : Enables or disables bullish Order Block.

Supply Order Block : Enables or disables bearish Order Blocks.

Demand FVG : Enables or disables bullish FVG.

Supply FVG : Enables or disables bearish FVGs.

Show All CISD : Enables or disables the display of all CISD Levels.

Show High CISD : Enables or disables high CISD levels.

Show Low CISD : Enables or disables low CISD levels.

🔵 Conclusion

The ICT One Trading Setup for Life is a liquidity-based strategy that leverages market structure shifts and precise entry points to identify high-probability trade opportunities. By focusing on PM Session High and PM Session Low, this setup first captures liquidity at these levels and then confirms trend shifts with a break of the Change in State of Delivery (CISD) Level.

Entering a trade after a retracement to an FVG or OB allows traders to position themselves at optimal liquidity levels, ensuring high reward-to-risk trades. When used in conjunction with higher timeframe bias, order flow, and liquidity analysis, this strategy can become one of the most effective trading methods within the ICT Concept framework.

Successful execution of this setup requires risk management, patience, and a deep understanding of liquidity dynamics. Traders can enhance their confidence in this strategy by conducting extensive backtesting and analyzing past market data to optimize their approach for different assets.

ICT Open Range Gap & 1st FVG (fadi)In his 2024 mentorship program, ICT detailed how price action interacts with Open Range Gaps and the initial 1-minute Fair Value Gap following the market open at 9:30 AM.

What is an Open Range Gap?

An Open Range Gap occurs when the market opens at 9:30 AM at a higher or lower level compared to the previous day's close at 4:14 PM, primarily relevant in futures trading. According to ICT, there is a statistical probability of 70% that the price action will close 50% or more of the Open Range Gap within the first 30 minutes of trading (9:30 AM to 10:00 AM).

What is the First 1-Minute Fair Value Gap?

ICT places significant emphasis on the first 1-minute Fair Value Gap (FVG) that forms after the market opens at 9:30 AM. The FVG must occur at 9:31 AM or later to be considered valid. This gap often presents key opportunities for traders, as it represents a temporary imbalance between supply and demand that the market seeks to correct.

Understanding and leveraging these patterns can enhance trading strategies by offering insights into potential price movements shortly after market open.

ICT Open Range Gap & 1st FVG

This indicator is engineered to identify and highlight the Open Range Gaps and the first 1-minute Fair Value Gap. Furthermore, it functions across multiple timeframes, from seconds to hours, catering to various trading preferences. This flexibility is particularly beneficial for traders who favor higher timeframes or wish to observe these patterns' application at broader intervals.

Settings

The Open Range Gap indicator offers flexible display settings. It identifies the quadrants and provides optional color coding to distinguish them. Additionally, it tracks the "fill" level to visualize how far the price action has progressed into the gap, enhancing traders' ability to monitor and analyze price movements effectively. By default, the Open Range Gap will stop extending at 10:00 AM; however, there is an option to continue extending until the end of the trading day.

The 1st Fair Value Gap (FVG) can be viewed on any timeframe the indicator is active on, offering various styling options to match each trader's preferences. While the 1st FVG is particularly relevant to the day it is created, previous 1st FVGs within the same week may provide additional value. This indicator allows traders to extend Monday's 1st FVG, marking the first FVG of the week, or to extend all 1st FVGs throughout the week.

Opening Range Breakout [UkutaLabs]█ OVERVIEW

The Opening Range Breakout is a powerful trading tool that indicates a strong range based on the high and low of the first fifteen or thirty minutes after market open. This range serves as a potential area of Support or Resistance that traders should be aware of during their trading. Because of this, the Opening Range Breakout is a versatile trading tool that can be included in a wide variety of trading strategies.

The aim of this script is to simplify the trading experience of users by automatically identifying and displaying price levels that they should be aware of.

█ USAGE

When the New York Market opens each day, the script will automatically identify and label the opening range in real time. The user can control whether the script measures the first 15 or 30 minutes of each trading day to fit each trader’s trading style.

Because there tends to be a spike in volume during this period, the range that is identified can serve as a powerful indication of overall market strength. Once the price breaks out of this range, it then can be used as an area of support or resistance depending on the direction of the breakout.

█ SETTINGS

Configuration

• Show Labels: Determines whether labels are drawn within the range.

• Display Mode: Determines the number of days the script should load.

Range Settings

• 15 Minute: Determines whether or not the 15 minute range is drawn.

• 15 Minute Color: Determines the color of the 15 minute range and labels.

• 30 Minute: Determines whether or not the 30 minute range is drawn.

• 30 Minute Color: Determines the color of the 30 minute range and labels.

@tk · fractal rsi levels█ OVERVIEW

This script is an indicator that helps traders to identify the RSI Levels for multiple fractals wherever the current timeframe is. This script was based on RSI Levels, 20-30 & 70-80 by abdomi indicator, that calculates the Relative Strenght Index levels based on the asset's price and plots it into the chart, creating a "wave" style indicator. The core feature of this indicator is the fractal rays, so trader can visualize each of the oversold and overbought levels of multiple timeframe on the current timeframe that he is on. The indicator will plots multiple rays after the chart bars. indicating where is the oversold and overbought levels for others fractals.

█ MOTIVATION

Since the RSI Levels, 20-30 & 70-80 by abdomi indicator helps a lot to identify the possible price levels when the asset is oversold or overbought, I saw myself drawing multiple horizontal lines on these levels in lower timeframes so, in an uptrend or downtrend, I can try to get a pullback of these trends when the asset reaches oversold or overboght levels. So, I get the idea to make those lines visible in multiple timeframes so I don't need to draw it myself manually anymore.

█ CONCEPT

The trading concept to use this indicator is the concept to make entries on uptrend or downtrend pullbacks when the asset price reaches oversold or overbought levels. But this strategy don't works alone. It needs to be aligned together with others indicators like Exponential Moving Averages, Chart Patterns, Support and Resistance, and so on... Even more confluences that you have, bigger are your chances to increase the probability for a successful trade. So, don't use this indicator alone. Compose a trading strategy and use it to improve your analysis.

█ CUSTOMIZATION

This indicator allows the trader to customize the following settings:

GENERAL

Text size

Changes the font size of the labels to improve accessibility.

Type: string

Options: `tiny`, `small`, `normal`, `large`.

Default: `small`

RSI LEVELS · SETTINGS

Pre-oversold Level

Changes the RSI Level to calculate the "pre-oversold" price level on the chart.

Type: int

Min: 1

Max: 49

Default: 33

Pre-overbought Level

Changes the RSI Level to calculate the "pre-overbought" price level on the chart.

Type: int

Min: 51

Max: 100

Default: 67

Show "Pre-over" Levels

Enables / Disables the pre-oversold and pre-overbought levels on the chart.

Type: bool

Default: true

FRACTAL RAYS · SETTINGS

Length

Changes the base length for the RSI calculation.

Type: int

Min: 1

Default: 14

Source

Changes the base source for the RSI calculation.

Type: float

Default: close

FRACTAL RAYS · STYLE

Ray Color

Changes the color of all fractal rays and its label.

Type: color

Default: color.rgb(187, 74, 207)

Ray Style

Changes the style of all fractal rays.

Type: string

Options: `line.style_solid`, `line.style_dashed`, `line.style_dotted`

Default: line.style_dotted

Ray Length

Changes the length of all fractal rays.

Type: int

Default: 15

FRACTAL RAYS · OVERSOLD

Oversold Level

Changes the base RSI Level for fractal rays calculation.

Type: int

Min: 1

Default: 30

Oversold Prefix

Customizes the fractal ray label with a prefix text.

Type: string

Default: 🚀

Oversold Suffix

Customizes the fractal ray label with a suffix text.

Type: string

Default: (empty)

FRACTAL RAYS · OVERBOUGHT

Overbought Level

Changes the base RSI Level for fractal rays calculation.

Type: int

Min: 1

Default: 70

Overbought Prefix

Customizes the fractal ray label with a prefix text.

Type: string

Default: 🐻

Overbought Suffix

Customizes the fractal ray label with a suffix text.

Type: string

Default: (empty)

FRACTAL RAYS · VISIBILITY RULES

These rules are applied for each of fractal rays so, the traders can choose what timeframes they wants to show the fractal rays for each of it. The rule will be applied as the following condition: `if timeframe != CURRENT_TIMEFRAME and timeframe <= CHOSEN_OPTION`. Actually, the fractal rays are on the chart but, isn't visible because it was applied a transparent color, so it is visually not on the chart to prevent chart's over polution.

LABELS

Show Labels on Price Scale

Shows labels on price scale.

Type: bool

Default: false

Show Price on Fractal Rays

Shows the RSI Level price on each of fractal rays respectively.

Type: bool

Default: false

█ EXTERNAL LIBRARIES

This script uses the `tk` library to calculate RSI Levels. It is a library that contains various functions that helps pine script developers to calculate RSI Levels.

█ FUNCTIONS

The library contains the following functions:

fn_fractalVisibilityRule(string visibilityRule)

Converts the fractal rays timeframe visibility rule label to timestamp int.

Parameters:

visibilityRule: (string) Fractal ray visibility rule label.

Returns: (int) Fractal ray visibility rule timestamp.

fn_requestFractal(string period, expression)

Converts the fractal rays timeframe visibility rule label to timestamp int.

Parameters:

period: (string) Timeframe period for the desired fractal.

expression: (mixed) Security expression that will be applied for calculation.

Returns: (mixed) A result determined by expression.

fn_plotRay(float y, string label, color color, int length)

Plots ray after chart bars for the current time.

Parameters:

period: (string) Timeframe period for the desired fractal.

expression: (mixed) Security expression that will be applied for calculation.

Returns: (void) This function only plots the elements into the chart

fn_plotRsiLevelRay(simple string period, simple int level, color color)

Plots RSI Levels ray after chart bars for the current time.

Parameters:

period: (simple string) Timeframe period.

level: (simple int) Relative Strength Index level.

color: (color) The color of both, ray and label text.

Returns: (void) This function only plots the elements into the chart

Any Oscillator Underlay [TTF]We are proud to release a new indicator that has been a while in the making - the Any Oscillator Underlay (AOU) !

Note: There is a lot to discuss regarding this indicator, including its intent and some of how it operates, so please be sure to read this entire description before using this indicator to help ensure you understand both the intent and some limitations with this tool.

Our intent for building this indicator was to accomplish the following:

Combine all of the oscillators that we like to use into a single indicator

Take up a bit less screen space for the underlay indicators for strategies that utilize multiple oscillators

Provide a tool for newer traders to be able to leverage multiple oscillators in a single indicator

Features:

Includes 8 separate, fully-functional indicators combined into one

Ability to easily enable/disable and configure each included indicator independently

Clearly named plots to support user customization of color and styling, as well as manual creation of alerts

Ability to customize sub-indicator title position and color

Ability to customize sub-indicator divider lines style and color

Indicators that are included in this initial release:

TSI

2x RSIs (dubbed the Twin RSI )

Stochastic RSI

Stochastic

Ultimate Oscillator

Awesome Oscillator

MACD

Outback RSI (Color-coding only)

Quick note on OB/OS:

Before we get into covering each included indicator, we first need to cover a core concept for how we're defining OB and OS levels. To help illustrate this, we will use the TSI as an example.

The TSI by default has a mid-point of 0 and a range of -100 to 100. As a result, a common practice is to place lines on the -30 and +30 levels to represent OS and OB zones, respectively. Most people tend to view these levels as distance from the edges/outer bounds or as absolute levels, but we feel a more way to frame the OB/OS concept is to instead define it as distance ("offset") from the mid-line. In keeping with the -30 and +30 levels in our example, the offset in this case would be "30".

Taking this a step further, let's say we decided we wanted an offset of 25. Since the mid-point is 0, we'd then calculate the OB level as 0 + 25 (+25), and the OS level as 0 - 25 (-25).

Now that we've covered the concept of how we approach defining OB and OS levels (based on offset/distance from the mid-line), and since we did apply some transformations, rescaling, and/or repositioning to all of the indicators noted above, we are going to discuss each component indicator to detail both how it was modified from the original to fit the stacked-indicator model, as well as the various major components that the indicator contains.

TSI:

This indicator contains the following major elements:

TSI and TSI Signal Line

Color-coded fill for the TSI/TSI Signal lines

Moving Average for the TSI

TSI Histogram

Mid-line and OB/OS lines

Default TSI fill color coding:

Green : TSI is above the signal line

Red : TSI is below the signal line

Note: The TSI traditionally has a range of -100 to +100 with a mid-point of 0 (range of 200). To fit into our stacking model, we first shrunk the range to 100 (-50 to +50 - cut it in half), then repositioned it to have a mid-point of 50. Since this is the "bottom" of our indicator-stack, no additional repositioning is necessary.

Twin RSI:

This indicator contains the following major elements:

Fast RSI (useful if you want to leverage 2x RSIs as it makes it easier to see the overlaps and crosses - can be disabled if desired)

Slow RSI (primary RSI)

Color-coded fill for the Fast/Slow RSI lines (if Fast RSI is enabled and configured)

Moving Average for the Slow RSI

Mid-line and OB/OS lines

Default Twin RSI fill color coding:

Dark Red : Fast RSI below Slow RSI and Slow RSI below Slow RSI MA

Light Red : Fast RSI below Slow RSI and Slow RSI above Slow RSI MA

Dark Green : Fast RSI above Slow RSI and Slow RSI below Slow RSI MA

Light Green : Fast RSI above Slow RSI and Slow RSI above Slow RSI MA

Note: The RSI naturally has a range of 0 to 100 with a mid-point of 50, so no rescaling or transformation is done on this indicator. The only manipulation done is to properly position it in the indicator-stack based on which other indicators are also enabled.

Stochastic and Stochastic RSI:

These indicators contain the following major elements:

Configurable lengths for the RSI (for the Stochastic RSI only), K, and D values

Configurable base price source

Mid-line and OB/OS lines

Note: The Stochastic and Stochastic RSI both have a normal range of 0 to 100 with a mid-point of 50, so no rescaling or transformations are done on either of these indicators. The only manipulation done is to properly position it in the indicator-stack based on which other indicators are also enabled.

Ultimate Oscillator (UO):

This indicator contains the following major elements:

Configurable lengths for the Fast, Middle, and Slow BP/TR components

Mid-line and OB/OS lines

Moving Average for the UO

Color-coded fill for the UO/UO MA lines (if UO MA is enabled and configured)

Default UO fill color coding:

Green : UO is above the moving average line

Red : UO is below the moving average line

Note: The UO naturally has a range of 0 to 100 with a mid-point of 50, so no rescaling or transformation is done on this indicator. The only manipulation done is to properly position it in the indicator-stack based on which other indicators are also enabled.

Awesome Oscillator (AO):

This indicator contains the following major elements:

Configurable lengths for the Fast and Slow moving averages used in the AO calculation

Configurable price source for the moving averages used in the AO calculation

Mid-line

Option to display the AO as a line or pseudo-histogram

Moving Average for the AO

Color-coded fill for the AO/AO MA lines (if AO MA is enabled and configured)

Default AO fill color coding (Note: Fill was disabled in the image above to improve clarity):

Green : AO is above the moving average line

Red : AO is below the moving average line

Note: The AO is technically has an infinite (unbound) range - -∞ to ∞ - and the effective range is bound to the underlying security price (e.g. BTC will have a wider range than SP500, and SP500 will have a wider range than EUR/USD). We employed some special techniques to rescale this indicator into our desired range of 100 (-50 to 50), and then repositioned it to have a midpoint of 50 (range of 0 to 100) to meet the constraints of our stacking model. We then do one final repositioning to place it in the correct position the indicator-stack based on which other indicators are also enabled. For more details on how we accomplished this, read our section "Binding Infinity" below.

MACD:

This indicator contains the following major elements:

Configurable lengths for the Fast and Slow moving averages used in the MACD calculation

Configurable price source for the moving averages used in the MACD calculation

Configurable length and calculation method for the MACD Signal Line calculation

Mid-line

Note: Like the AO, the MACD also technically has an infinite (unbound) range. We employed the same principles here as we did with the AO to rescale and reposition this indicator as well. For more details on how we accomplished this, read our section "Binding Infinity" below.

Outback RSI (ORSI):

This is a stripped-down version of the Outback RSI indicator (linked above) that only includes the color-coding background (suffice it to say that it was not technically feasible to attempt to rescale the other components in a way that could consistently be clearly seen on-chart). As this component is a bit of a niche/special-purpose sub-indicator, it is disabled by default, and we suggest it remain disabled unless you have some pre-defined strategy that leverages the color-coding element of the Outback RSI that you wish to use.

Binding Infinity - How We Incorporated the AO and MACD (Warning - Math Talk Ahead!)

Note: This applies only to the AO and MACD at time of original publication. If any other indicators are added in the future that also fall into the category of "binding an infinite-range oscillator", we will make that clear in the release notes when that new addition is published.

To help set the stage for this discussion, it's important to note that the broader challenge of "equalizing inputs" is nothing new. In fact, it's a key element in many of the most popular fields of data science, such as AI and Machine Learning. They need to take a diverse set of inputs with a wide variety of ranges and seemingly-random inputs (referred to as "features"), and build a mathematical or computational model in order to work. But, when the raw inputs can vary significantly from one another, there is an inherent need to do some pre-processing to those inputs so that one doesn't overwhelm another simply due to the difference in raw values between them. This is where feature scaling comes into play.

With this in mind, we implemented 2 of the most common methods of Feature Scaling - Min-Max Normalization (which we call "Normalization" in our settings), and Z-Score Normalization (which we call "Standardization" in our settings). Let's take a look at each of those methods as they have been implemented in this script.

Min-Max Normalization (Normalization)

This is one of the most common - and most basic - methods of feature scaling. The basic formula is: y = (x - min)/(max - min) - where x is the current data sample, min is the lowest value in the dataset, and max is the highest value in the dataset. In this transformation, the max would evaluate to 1, and the min would evaluate to 0, and any value in between the min and the max would evaluate somewhere between 0 and 1.

The key benefits of this method are:

It can be used to transform datasets of any range into a new dataset with a consistent and known range (0 to 1).

It has no dependency on the "shape" of the raw input dataset (i.e. does not assume the input dataset can be approximated to a normal distribution).

But there are a couple of "gotchas" with this technique...

First, it assumes the input dataset is complete, or an accurate representation of the population via random sampling. While in most situations this is a valid assumption, in trading indicators we don't really have that luxury as we're often limited in what sample data we can access (i.e. number of historical bars available).

Second, this method is highly sensitive to outliers. Since the crux of this transformation is based on the max-min to define the initial range, a single significant outlier can result in skewing the post-transformation dataset (i.e. major price movement as a reaction to a significant news event).

You can potentially mitigate those 2 "gotchas" by using a mechanism or technique to find and discard outliers (e.g. calculate the mean and standard deviation of the input dataset and discard any raw values more than 5 standard deviations from the mean), but if your most recent datapoint is an "outlier" as defined by that algorithm, processing it using the "scrubbed" dataset would result in that new datapoint being outside the intended range of 0 to 1 (e.g. if the new datapoint is greater than the "scrubbed" max, it's post-transformation value would be greater than 1). Even though this is a bit of an edge-case scenario, it is still sure to happen in live markets processing live data, so it's not an ideal solution in our opinion (which is why we chose not to attempt to discard outliers in this manner).

Z-Score Normalization (Standardization)

This method of rescaling is a bit more complex than the Min-Max Normalization method noted above, but it is also a widely used process. The basic formula is: y = (x – μ) / σ - where x is the current data sample, μ is the mean (average) of the input dataset, and σ is the standard deviation of the input dataset. While this transformation still results in a technically-infinite possible range, the output of this transformation has a 2 very significant properties - the mean (average) of the output dataset has a mean (μ) of 0 and a standard deviation (σ) of 1.

The key benefits of this method are:

As it's based on normalizing the mean and standard deviation of the input dataset instead of a linear range conversion, it is far less susceptible to outliers significantly affecting the result (and in fact has the effect of "squishing" outliers).

It can be used to accurately transform disparate sets of data into a similar range regardless of the original dataset's raw/actual range.

But there are a couple of "gotchas" with this technique as well...

First, it still technically does not do any form of range-binding, so it is still technically unbounded (range -∞ to ∞ with a mid-point of 0).

Second, it implicitly assumes that the raw input dataset to be transformed is normally distributed, which won't always be the case in financial markets.

The first "gotcha" is a bit of an annoyance, but isn't a huge issue as we can apply principles of normal distribution to conceptually limit the range by defining a fixed number of standard deviations from the mean. While this doesn't totally solve the "infinite range" problem (a strong enough sudden move can still break out of our "conceptual range" boundaries), the amount of movement needed to achieve that kind of impact will generally be pretty rare.

The bigger challenge is how to deal with the assumption of the input dataset being normally distributed. While most financial markets (and indicators) do tend towards a normal distribution, they are almost never going to match that distribution exactly. So let's dig a bit deeper into distributions are defined and how things like trending markets can affect them.

Skew (skewness): This is a measure of asymmetry of the bell curve, or put another way, how and in what way the bell curve is disfigured when comparing the 2 halves. The easiest way to visualize this is to draw an imaginary vertical line through the apex of the bell curve, then fold the curve in half along that line. If both halves are exactly the same, the skew is 0 (no skew/perfectly symmetrical) - which is what a normal distribution has (skew = 0). Most financial markets tend to have short, medium, and long-term trends, and these trends will cause the distribution curve to skew in one direction or another. Bullish markets tend to skew to the right (positive), and bearish markets to the left (negative).

Kurtosis: This is a measure of the "tail size" of the bell curve. Another way to state this could be how "flat" or "steep" the bell-shape is. If the bell is steep with a strong drop from the apex (like a steep cliff), it has low kurtosis. If the bell has a shallow, more sweeping drop from the apex (like a tall hill), is has high kurtosis. Translating this to financial markets, kurtosis is generally a metric of volatility as the bell shape is largely defined by the strength and frequency of outliers. This is effectively a measure of volatility - volatile markets tend to have a high level of kurtosis (>3), and stable/consolidating markets tend to have a low level of kurtosis (<3). A normal distribution (our reference), has a kurtosis value of 3.

So to try and bring all that back together, here's a quick recap of the Standardization rescaling method:

The Standardization method has an assumption of a normal distribution of input data by using the mean (average) and standard deviation to handle the transformation

Most financial markets do NOT have a normal distribution (as discussed above), and will have varying degrees of skew and kurtosis

Q: Why are we still favoring the Standardization method over the Normalization method, and how are we accounting for the innate skew and/or kurtosis inherent in most financial markets?

A: Well, since we're only trying to rescale oscillators that by-definition have a midpoint of 0, kurtosis isn't a major concern beyond the affect it has on the post-transformation scaling (specifically, the number of standard deviations from the mean we need to include in our "artificially-bound" range definition).

Q: So that answers the question about kurtosis, but what about skew?

A: So - for skew, the answer is in the formula - specifically the mean (average) element. The standard mean calculation assumes a complete dataset and therefore uses a standard (i.e. simple) average, but we're limited by the data history available to us. So we adapted the transformation formula to leverage a moving average that included a weighting element to it so that it favored recent datapoints more heavily than older ones. By making the average component more adaptive, we gained the effect of reducing the skew element by having the average itself be more responsive to recent movements, which significantly reduces the effect historical outliers have on the dataset as a whole. While this is certainly not a perfect solution, we've found that it serves the purpose of rescaling the MACD and AO to a far more well-defined range while still preserving the oscillator behavior and mid-line exceptionally well.

The most difficult parts to compensate for are periods where markets have low volatility for an extended period of time - to the point where the oscillators are hovering around the 0/midline (in the case of the AO), or when the oscillator and signal lines converge and remain close to each other (in the case of the MACD). It's during these periods where even our best attempt at ensuring accurate mirrored-behavior when compared to the original can still occasionally lead or lag by a candle.

Note: If this is a make-or-break situation for you or your strategy, then we recommend you do not use any of the included indicators that leverage this kind of bounding technique (the AO and MACD at time of publication) and instead use the Trandingview built-in versions!

We know this is a lot to read and digest, so please take your time and feel free to ask questions - we will do our best to answer! And as always, constructive feedback is always welcome!

DR/IDR Candles [LuxAlgo]This indicator displays defining ranges (DR) and implied defining ranges (IDR) constructed from two user set sessions (RDR/ODR) as graphical candles on the chart. The script introduces additional graphical elements to the original DR/IDR concept and as such can be thought as a graphical method in addition to a technical indicator.

Additionally, this script can display various Fibonacci retracements from the constructed DR/IDR if enabled within the settings.

Settings

Regular Session: Enable/disable regular session's DR/IDR alongside setting the session time. By default, 09:30 - 10:30 am.

Overnight Session: Enable/disable overnight session's DR/IDR alongside setting the session time. By default, 03:00 - 04:00 am.

UTC Offset: UTC offset for the time zone, by default -5 (EST)

Retracements

Reverse: Inverts source range upper/lower value for constructing the retracements.

From: Source range used to construct the retracements, by default DR is used.

By default, the 0.5 retracement (average line) is displayed.

Usage

The used sessions are highlighted by a gray background. DRs are highlighted by dashed lines while IDRs are highlighted by solid ones. The maximum/minimum price between each user set session is highlighted by solid wicks.

The color of the DRs/IDRs/wicks are determined by the price position relative to the DR; if price is above the DR maximum, then a blue color is used. If price is below, then an orange color is used, and if price is within the DR range, then a gray color is used.

Additionally, the area of the DR range is used to highlight the number of time price is located within the DR, with a longer background highlighting a higher number of occurrences. This can help highlight if the DR levels were potentially useful as support/resistance.

When price is outside the IDR range, the area between the price and IDR is highlighted, in blue if price is above the IDR, and orange if it is under.

The original author of the DR/IDR concept describes 3 rules using the price position relative to the DR/IDR levels:

1.) If price on the 5-minute timeframe closes above the DR high after 10:30 AM or 04:00 AM then the DR low will likely be the low of the trading session.

2.) If price on the 5-minute timeframe closes below the DR low after 10:30 AM or 04:00 AM then the DR high will likely be the high of the trading session.

3.) If price closes above the IDR high after 10:30 AM or 04:00 AM it is an early indication that the low of the DR will be the low of the day and vice versa.

We can see that the above rules are cases of conditional probabilities.

There is no significant data supporting or regarding any statistical probability of the above rules to be true, which are more than uncertain given the stochastic nature of prices. The lack of precision of these rules is also a concern (time zone dependance, applicable markets, etc...).

Credits

Credits to trader TheMas7er who originally created the DR/IDR concept in November of 2022. This script was derived from his proposed session times & rules for trading.

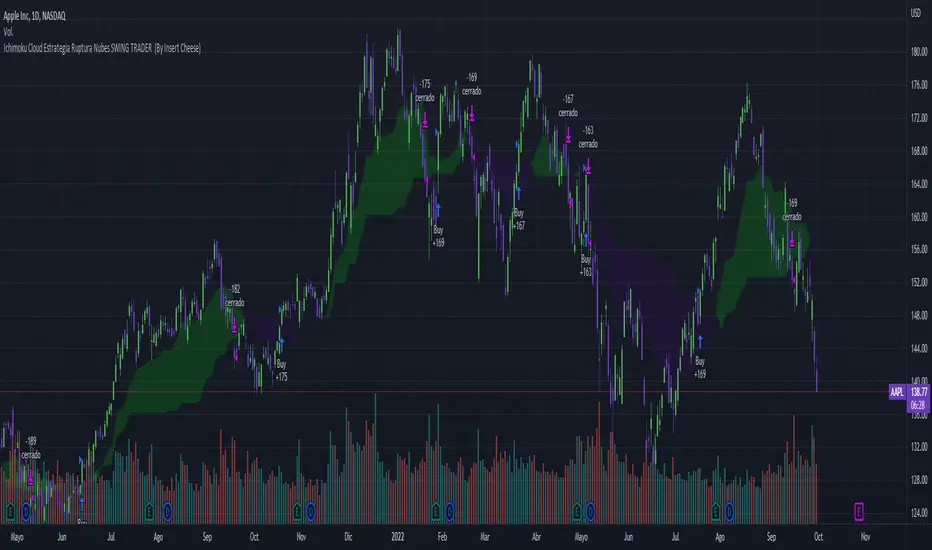

Ichimoku Breakout Kumo SWING TRADER (By Insert Cheese)A simple strategy for long spot or long futures (swing traders) based on a basic method of Ichimoku Kinko Hyo strategies.

The strategy is simple:

- Buy when the price breaks the cloud

- Close the trade when the price closes again inside the cloud.

The parameters that work best on this strategy are 10,30,60,30 and 1 for Senkou-Span A

but you can try classic Ichimoku parameters (9,26,52,26,26) or whatever you want like (7,22,44,22,22), (10,30,60,30,30) and others.

-1D chart

I have removed everything from the interface except the cloud to make it visually more aesthetic :D (but if you want to see all the ichimoku indicator you can put in again into the chart)

I have also added several functions for you to do your own backtesting:

- Date range

- TP AND SL method

- Includes long or short trades

The strategy starts with 500 $ and use 100% for trade to make the power of the compounding :P

Remember that this is for only educational porpouse and you must to do your own research and backtested on your usually market..

I hope you like it enjoy and support this indicator :)

Donate (BEP20) 0xC118f1ffB3ac40875C13B3823C182eA2Af344c6d

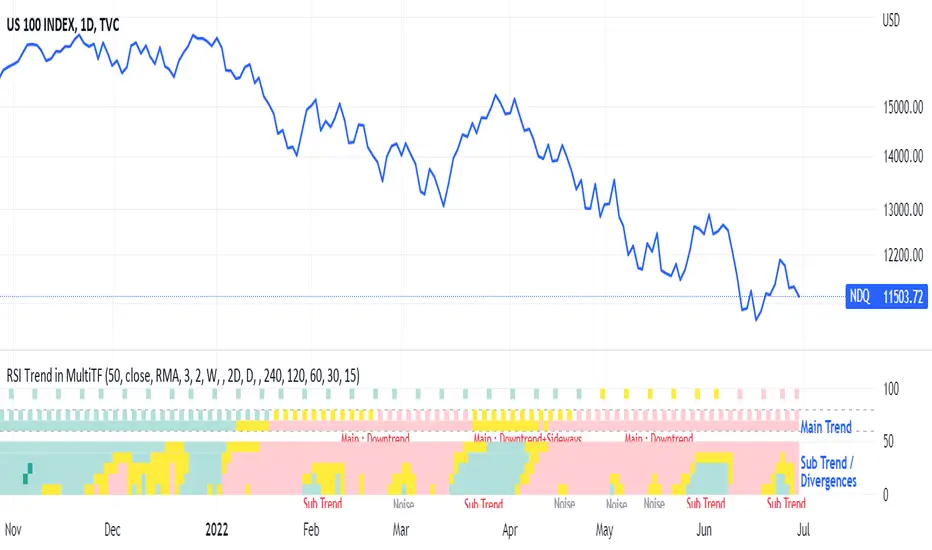

RSI Trend Heatmap in Multi TimeframesRSI Trend Heatmap in Multi Timeframes

Description

Sometimes you want to look at the RSI Trend across multiple time frames.

You have to waste time browsing through them.

So we've put together every time frame you want to see in one indicator.

We have 10 layers of RSI Trend heatmap available for you.

You can set the timeframe as you want on the Settings page.

Description of Parameter RSI Setting ** You can change it by setting.

RSI Trend Length : (Default 50)

Source : (Default close)

RSI Sideways Length : (Default 2 = RSI between 48 .. 52)

Description of Parameter RSI Timeframe ** You can change it by setting.

""=None,

"M"=1Month, "2W"=2Weeks, "W"=1Week,

"3D"=3Days, "2D"=2Days, "D"=1Day,

"720"=12Hours, "480"=4Hours, "240"=4Hours, "180"=3Hours, "120"=2Hours,

"60"=60Minutes, "30"=30Minutes, "15"=15Minutes, "5"=5Minutes, "1"=1Minute

Default Configurate of RSI Timeframe (for a time frame of 1 hour to 1 day)

"W"= Timeframe 1 month shown in line 90-100 --> Represent Long Trend of RSI

---------------------------------------

"D2"= Timeframe 2 days shown in line 70-80 --> Represent Trend of RSI

"D"= Timeframe 1 day shown in line 60-70 --> Represent Trend of RSI

---------------------------------------

"240"= Timeframe 3 hours shown in line 40-50 --> Represent Signal Up/Signal Down/Divergence of RSI

"120"= Timeframe 2 hours shown in line 30-40 --> Represent Signal Up/Signal Down/Divergence of RSI

"60"= Timeframe 1 hour shown in line 20-30 --> Represent Signal Up/Signal Down/Divergence of RSI

"30"= Timeframe 30 minutes shown in line 10-20 --> Represent Signal Up/Signal Down/Divergence of RSI

"15"= Timeframe 15 minutes shown in line 00-10 --> Represent Signal Up/Signal Down/Divergence of RSI

Description of Colors

Dark Bule = Extreme Uptrend / Overbought / Bull Market (RSI > 67)

Light Bule = Uptrend (RSI between 50-52 .. 67)

Yellow = Sideways Trend / Trend Reversal (RSI between 48 .. 52) ** You can change it by setting.

Light Red = Downtrend (RSI between 33 .. 48-50)

Dark Red = Extreme Downtrend / Oversold / Bear Market (RSI < 33)

How to use

1. You must first know what the main trend of the RSI is (look at the 60-80 line). If it is red, it is a downtrend. and if it's blue shows that it is an uptrend

2. Throughout the period of the main trend There will always be a reversal of the sub-trend. (Can see from the 0-50 line), but eventually will return to follow the main trend.

3. Unless the sub trend persists for a long time until the main trend changes.

ICT Index Futures Session LinesICT Index Futures Session Lines

Description:

The script is based on one of ICT's concepts on trading Index Futures. The script lays out the daily range from an intraday basis.

Range:

00:00 - New York Midnight

08:30 – New York Open (News events come out)

12:00/13:00 - New York Lunch (No trade time period)

13:30 - (Algorithm)

16:30 - Close

* The open, high and low lines are plotted from 00:00 to 08:30

How To Use:

You will need to check the daily bias. Prior to 8:30 you are to look for previous swing points where liquidity may exist. During the open you want to see if a high or low is taken out, and then wait for an energetic break/displacement for a potential FVG/imbalance retracement entry.

Strategy is for LTF (1 to 15m)

Default time zone is set to America/New_York (UTC New York), so lines will be plotted correctly regardless of user’s local UTC chart setting.

RSI Levels, Multi-TimeframeThe relative strength index (RSI) is a momentum indicator that measures the magnitude of recent price changes to evaluate overbought or oversold conditions. RSI is normally displayed as an oscillator separately from price and can have a reading from 0 to 100. This indicator takes the RSI and plots the 30 & 70 levels onto the price chart so you can see when price is going to meet the 30 or 70 levels. The reason the 30 & 70 levels are important is because many traders (and bots) use those as signals to buy (at 30 RSI) or sell (at 70 RSI). Additionally, this indicator allows you to display not just the RSI levels of your currently viewed timeframe on the chart, but also shows the RSI levels of up to 6 different timeframes on the same chart. This allows you to quickly see if multiple RSI levels are aligning across different timelines, which is an even stronger indication that price is going to change direction when it meets those levels on the chart. There are a lot of nice configuration options, like:

Style customization (color, thickness, size)

Labels on the chart so you can tell which plots are the RSI levels

Optionally display the plot as a horizontal line if all you care about is the RSI level right now

Toggle overbought (RSI 70) or oversold (RSI 30) on/off completely

Hotch v1.02 RSI+Fractals/VWAP Bands/Smoothed Moving Average. In this script the RSI is used the limit number of displayed fractals to only those fractals that are triggered in the RSI Overbought and Oversold areas. This helps keep the chart cleaner looking when combined with other indicators so other icons that are plotted above and below candles are not covered up.

For example if the RSI drops below 30 the next fractal would be displayed.

If the RSI stays below 30 each fractal would be displayed.

If the RSI dips below 30 and returns above 30 before there is a fractal is displayed, the next valid fractal would still be displayed.

With optimization of the RSI values this indicator can be used in confluence with the included VWAP bands and Moving average to find trend reversal entry points for trades. Also recommended is to use a divergence identifying lower indicator as a secondary confirmation of trade entry.

Example of a potential long entry using the displayed chart.

1) RSI under 30

2) Price was recently outside of your chosen VWAP multiple.

3) a fractal was triggered.

Additionaly:

4) Use other indicators or other confluences for a stronger trade signal.

5) Use your preferred method of determining entry price stop loss and take profit.

NOTE: Fractals normally paint two bars behind the current bar. In this code, with the combination of the RSI and Fractal Trigger, the fractal paints an icon on the current bar.

User-Inputed Time Range & FibsGreetings Traders! I have decided to release a few scripts as open-source as I'm sure others can benefit from them and perhaps make them better.(Be sure to check my Profile for the other scripts as well: www.tradingview.com).

This one is called User-Inputed Time Range & Fibs.

The idea behind this script is to record the Range Highs and Lows of a User Defined Period, and plot potential Targets based on either Fibonacci Extensions or a Multiple of the Range Size. I created this originally for use with the US Session Initial Balance(From 9:30-10:30AM EST), however it can be set to any time period.

What is Initial Balance? In simple words, Initial Balance (IB) is the price data, which are formed during the first hour of a trading session. Activity of traders forms the so-called Initial Balance at this time. This concept was introduced for the first time by Peter Steidlmayer when he presented the market profile to traders(atas.net).

The IB is monitored as a break-out area for Range Extension traders. The IB High is also seen as an area of resistance and the IB Low as an area of support until it is broken(www.mypivots.com).

As a note, depending on the Time Zone you are in, you may need to manually add or subtract from the Timed Range to match the desired Time. For example in NY Eastern Time, I have to use 8:30-9:30AM to Capture the 9:30-10-30AM IB for ES and NQ. Similarly, I must use 14:30-15:30PM to Capture the 9:30-10-30AM IB for BTC. You will need to make adjustments based on the Time Zone you are located in.

I wanted to give a Special Thanks to @PineCoders for the Custom Rounding Function from Backtesting/Trading Engine--> (), Pinecoders.com for help with Tracking the Highs/Lows--> (www.pinecoders.com), and @TradeChartist for allowing me to use some of the code for the Fibonacci Extensions from his script here--> ().

If you like User-Inputed Time Range & Fibs, be sure to Like, Follow, and if you have any questions, don't be afraid to drop a comment below.

Realized VolatilityRealized / Historical Volatility

Calculates historical, i.e. realized volatility of any underlying. If frequency is not the daily, but for example 6h, 30min, weeks or months, it scales the initial setting to be suitable for the different time frame.

Examples with default settings (30 day volatility, 365 days per year):

A) Frequency = Daily:

Returns 30 day historical volatility, under the assumption that there are 365 trading days in a year.

B) Frequency = 6h:

Still returns 30 day historical volatility, under the assumption that there are 365 trading days in a year. However, since 6h granularity fits 4 times in 24 hours, it rescales the look back period to rather 30*4 = 120 units to still reflect 30 day historical volatility.

RSI3graf. 3 RSI in one window[wozdux] Three RSI indicator charts in one window. Plus, the resale area (green) and overbought area ( red) are highlighted. Indicator settings are periods of calculation of the RSI indicator (24, 14, 9). The fourth parameter (30) is the critical levels, which are at a distance of 30 units from the edges. If the parameter is 30, then the oversold level is 30 and the overbought level is 70 (100-30).

Levels from NY Open and SettlementThis indicator draws a line from the high and low of the 30 second candle at 14:59:30CT, and extends the lines for 24 hours.

It draws another high low from the 8:30CT 30 second opening candle and extends them for the full 24 to the next NY open, plus another 6.5 hours until the next settlement time at 14:59:30CT.

This gives a very long liquidity box starting from the 30 second candle of the NY open, and a shorter liquidity box starting from the 30 second candle of settlement time.

Impulse Reactor RSI-SMA Trend Indicator [ApexLegion]Impulse Reactor RSI-SMA Trend Indicator

Introduction and Theoretical Background

Design Rationale

Standard indicators frequently generate binary 'BUY' or 'SELL' signals without accounting for the broader market context. This often results in erratic "Flip-Flop" behavior, where signals are triggered indiscriminately regardless of the prevailing volatility regime.

Impulse Reactor was engineered to address this limitation by unifying two critical requirements: Quantitative Rigor and Execution Flexibility.

The Solution

Composite Analytical Framework This script is not a simple visual overlay of existing indicators. It is an algorithmic synthesis designed to function as a unified decision-making engine. The primary objective was to implement rigorous quantitative analysis (Volatility Normalization, Structural Filtering) directly within an alert-enabled framework. This architecture is designed to process signals through strict, multi-factor validation protocols before generating real-time notifications, allowing users to focus on structurally validated setups without manual monitoring.

How It Works

This is not a simple visual mashup. It utilizes a cross-validation algorithm where the Trend Structure acts as a gatekeeper for Momentum signals:

Logic over Lag: Unlike simple moving average crossovers, this script uses a 15-layer Gradient Ribbon to detect "Laminar Flow." If the ribbon is knotted (Compression), the system mathematically suppresses all signals.

Volatility Normalization: The core calculation adapts to ATR (Average True Range). This means the indicator automatically expands in volatile markets and contracts in quiet ones, maintaining accuracy without constant manual tweaking.

Adaptive Signal Thresholding: It incorporates an 'Anti-Greed' algorithm (Dynamic Thresholding) that automatically adjusts entry criteria based on trend duration. This logic aims to mitigate the risk of entering positions during periods of statistical trend exhaustion.

Why Use It?

Market State Decoding: The gradient Ribbon visualizes the underlying trend phase in real-time.

◦ Cyan/Blue Flow: Strong Bullish Trend (Laminar Flow).

◦ Magenta/Pink Flow: Strong Bearish Trend.

◦ Compressed/Knotted: When the ribbon lines are tightly squeezed or overlapping, it signals Consolidation. The system filters signals here to avoid chop.

Noise Reduction: The goal is not to catch every pivot, but to isolate high-confidence setups. The logic explicitly filters out minor fluctuations to help maintain position alignment with the broader trend.

⚖️ Chapter 1: System Architecture

Introduction: Composite Analytical Framework

System Overview

Impulse Reactor serves as a comprehensive technical analysis engine designed to synthesize three distinct market dimensions—Momentum, Volatility, and Trend Structure—into a unified decision-making framework. Unlike traditional methods that analyze these metrics in isolation, this system functions as a central processing unit that integrates disparate data streams to construct a coherent model of market behavior.

Operational Objective

The primary objective is to transition from single-dimensional signal generation to a multi-factor assessment model. By fusing data from the Impulse Core (Volatility), Gradient Oscillator (Momentum), and Structural Baseline (Trend), the system aims to filter out stochastic noise and identify high-probability trade setups grounded in quantitative confluence.

Market Microstructure Analysis: Limitations of Conventional Models

Extensive backtesting and quantitative analysis have identified three critical inefficiencies in standard oscillator-based strategies:

• Bounded Oscillator Limitations (The "Oscillation Trap"): Traditional indicators such as RSI or Stochastics are mathematically constrained between fixed values (0 to 100). In strong trending environments, these metrics often saturate in "overbought" or "oversold" zones. Consequently, traders relying on static thresholds frequently exit structurally valid positions prematurely or initiate counter-trend trades against prevailing momentum, resulting in suboptimal performance.

• Quantitative Blindness to Quality: Standard moving averages and trend indicators often fail to distinguish the qualitative nature of price movement. They treat low-volume drift and high-velocity expansion identically. This inability to account for "Volatility Quality" leads to delayed responsiveness during critical market events.

• Fractal Dissonance (Timeframe Disconnect): Financial markets exhibit fractal characteristics where trends on lower timeframes may contradict higher timeframe structures. Manual integration of multi-timeframe analysis increases cognitive load and susceptibility to human error, often resulting in conflicting biases at the point of execution.

Core Design Principles

To mitigate the aforementioned systemic inefficiencies, Impulse Reactor employs a modular architecture governed by three foundational principles:

Principle A:

Volatility Precursor Analysis Market mechanics demonstrate that volatility expansion often functions as a leading indicator for directional price movement. The system is engineered to detect "Volatility Deviation" — specifically, the divergence between short-term and long-term volatility baselines—prior to its manifestation in price action. This allows for entry timing aligned with the expansion phase of market volatility.

Principle B:

Momentum Density Visualization The system replaces singular momentum lines with a "Momentum Density" model utilizing a 15-layer Simple Moving Average (SMA) Ribbon.

• Concept: This visualization represents the aggregate strength and consistency of the trend.

• Application: A fully aligned and expanded ribbon indicates a robust trend structure ("Laminar Flow") capable of withstanding minor counter-trend noise, whereas a compressed ribbon signals consolidation or structural weakness.

Principle C:

Adaptive Confluence Protocols Signal validity is strictly governed by a multi-dimensional confluence logic. The system suppresses signal generation unless there is synchronized confirmation across all three analytical vectors:

1. Volatility: Confirmed expansion via the Impulse Core.

2. Momentum: Directional alignment via the Hybrid Oscillator.

3. Structure: Trend validation via the Baseline. This strict filtering mechanism significantly reduces false positives in non-trending (choppy) environments while maintaining sensitivity to genuine breakouts.

🔍 Chapter 2: Core Modules & Algorithmic Logic

Module A: Impulse Core (Normalized Volatility Deviation)

Operational Logic The Impulse Core functions as a volatility-normalized momentum gauge rather than a standard oscillator. It is designed to identify "Volatility Contraction" (Squeeze) and "Volatility Expansion" phases by quantifying the divergence between short-term and long-term volatility states.

Volatility Z-Score Normalization

The formula implements a custom normalization algorithm. Unlike standard oscillators that rely on absolute price changes, this logic calculates the Z-Score of the Volatility Spread.

◦ Numerator: (atr_f - atr_s) captures the raw momentum of volatility expansion.

◦ Denominator: (std_f + 1e-6) standardizes this value against historical variance.

◦ Result: This allows the indicator scales consistently across assets (e.g., Bitcoin vs. Euro) without manual recalibration.

f_impulse() =>

atr_f = ta.atr(fastLen) // Fast Volatility Baseline

atr_s = ta.atr(slowLen) // Slow Volatility Baseline

std_f = ta.stdev(atr_f, devLen) // Volatility Standard Deviation

(atr_f - atr_s) / (std_f + 1e-6) // Normalized Differential Calculation

Algorithmic Framework

• Differential Calculation: The system computes the spread between a Fast Volatility Baseline (ATR-10) and a Slow Volatility Baseline (ATR-30).

• Normalization Protocol: To standardize consistency across diverse asset classes (e.g., Forex vs. Crypto), the raw differential is divided by the standard deviation of the volatility itself over a 30-period lookback.

• Signal Generation:

◦ Contraction (Squeeze): When the Fast ATR compresses below the Slow ATR, it registers a potential volatility buildup phase.

◦ Expansion (Release): A rapid divergence of the Fast ATR above the Slow ATR signals a confirmed volatility expansion, validating the strength of the move.

Module B: Gradient Oscillator (RSI-SMA Hybrid)

Design Rationale To mitigate the "noise" and "false reversal" signals common in single-line oscillators (like standard RSI), this module utilizes a 15-Layer Gradient Ribbon to visualize momentum density and persistence.

Technical Architecture

• Ribbon Array: The system generates 15 sequential Simple Moving Averages (SMA) applied to a volatility-adjusted RSI source. The length of each layer increases incrementally.

• State Analysis:

Momentum Alignment (Laminar Flow): When all 15 layers are expanded and parallel, it indicates a robust trend where buying/selling pressure is distributed evenly across multiple timeframes. This state helps filter out premature "overbought/oversold" signals.

• Consolidation (Compression): When the distance between the fastest layer (Layer 1) and the slowest layer (Layer 15) approaches zero or the layers intersect, the system identifies a "Non-Tradable Zone," preventing entries during choppy market conditions.

// Laminar Flow Validation

f_validate_trend() =>

// Calculate spread between Ribbon layers

ribbon_spread = ta.stdev(ribbon_array, 15)

// Only allow signals if Ribbon is expanded (Laminar Flow)

is_flowing = ribbon_spread > min_expansion_threshold

// If compressed (Knotted), force signal to false

is_flowing ? signal : na

Module C: Adaptive Signal Filtering (Behavioral Bias Mitigation)

This subsystem, operating as an algorithmic "Anti-Greed" Mechanism, addresses the statistical tendency for signal degradation following prolonged trends.

Dynamic Threshold Adjustment

• Win Streak Detection: The algorithm internally tracks the outcome of closed trade cycles.

• Sensitivity Multiplier: Upon detecting consecutive successful signals in the same direction, a Penalty_Factor is applied to the entry logic.

• Operational Impact: This effectively raises the Required_Slope threshold for subsequent signals. For example, after three consecutive bullish signals, the system requires a 30% steeper trend angle to validate a fourth entry. This enforces stricter discipline during extended trends to reduce the probability of entering at the point of trend exhaustion.

Anti-Greed Logic: Dynamic Threshold Calculation

f_adjust_threshold(base_slope, win_streak) =>

// Adds a 10% penalty to the difficulty for every consecutive win

penalty_factor = 0.10

risk_scaler = 1 + (win_streak * penalty_factor)

// Returns the new, harder-to-reach threshold

base_slope * risk_scaler

Module D: Trend Baseline (Triple-Smoothed Structure)

The Trend Baseline serves as the structural filter for all signals. It employs a Triple-Smoothed Hybrid Algorithm designed to balance lag reduction with noise filtration.

Smoothing Stages

1. Volatility Banding: Utilizes a SuperTrend-based calculation to establish the upper and lower boundaries of price action.

2. Weighted Filter: Applies a Weighted Moving Average (WMA) to prioritize recent price data.

3. Exponential Smoothing: A final Exponential Moving Average (EMA) pass is applied to create a seamless baseline curve.

Functionality

This "Heavy" baseline resists minor intraday volatility spikes while remaining responsive to sustained structural shifts. A signal is only considered valid if the price action maintains structural integrity relative to this baseline

🚦 Chapter 3: Risk Management & Exit Protocols

Quantitative Risk Management (TP/SL & Trailing)

Foundational Architecture: Volatility-Adjusted Geometry Unlike strategies relying on static nominal values, Impulse Reactor establishes dynamic risk boundaries derived from quantitative volatility metrics. This design aligns trade invalidation levels mathematically with the current market regime.

• ATR-Based Dynamic Bracketing:

The protocol calculates Stop-Loss and Take-Profit levels by applying Fibonacci coefficients (Default: 0.786 for SL / 1.618 for TP) to the Average True Range (ATR).

◦ High Volatility Environments: The risk bands automatically expand to accommodate wider variance, preventing premature exits caused by standard market noise.

◦ Low Volatility Environments: The bands contract to tighten risk parameters, thereby dynamically adjusting the Risk-to-Reward (R:R) geometry.

• Close-Validation Protocol ("Soft Stop"):

Institutional algorithms frequently execute liquidity sweeps—driving prices briefly below key support levels to accumulate inventory.

◦ Mechanism: When the "Soft Stop" feature is enabled, the system filters out intraday volatility spikes. The stop-loss is conditional; execution is triggered only if the candle closes beyond the invalidation threshold.

◦ Strategic Advantage: This logic distinguishes between momentary price wicks and genuine structural breakdowns, preserving positions during transient volatility.

• Step-Function Trailing Mechanism:

To protect unrealized PnL while allowing for normal price breathing, a two-phase trailing methodology is employed:

◦ Phase 1 (Activation): The trailing function remains dormant until the price advances by a pre-defined percentage threshold.

◦ Phase 2 (Dynamic Floor): Once armed, the stop level creates a moving floor, adjusting relative to price action while maintaining a volatility-based (ATR) buffer to systematically protect unrealized PnL.

• Algorithmic Exit Protocols (Dynamic Liquidity Analysis)