Fear Greed RangesFear Greed Ranges Indicator: A Practical Guide to Market Sentiment Analysis

Introduction: Understanding Market Psychology

The "Fear Greed Ranges" indicator is a specialized technical analysis tool designed to visualize market sentiment through the lens of the Relative Strength Index (RSI). Unlike traditional RSI displays that show only a line graph, this indicator transforms raw RSI data into intuitive, color-coded zones that immediately signal whether markets are driven by fear, greed, or balanced sentiment. By providing this visual context, it helps traders identify potential turning points and manage risk more effectively.

Rational Integration: Why RSI Forms the Core

The indicator's foundation rests on the well-established RSI oscillator, chosen for several compelling reasons. First, RSI has stood the test of time since its development by J. Welles Wilder Jr. in 1978, with decades of empirical validation across various asset classes. Second, its mathematical construction—comparing the magnitude of recent gains to recent losses—directly measures momentum, which often precedes price reversals at extremes. Third, RSI's bounded nature (0-100 range) makes it ideal for creating clearly defined zones without subjective interpretation.

The integration transforms this numerical oscillator into a spatial visualization system. Rather than simply reading RSI values, traders can immediately perceive market conditions through color psychology: red triggers caution, green suggests opportunity, and yellow indicates neutrality. This multi-sensory approach reduces cognitive load during fast-moving markets and helps overcome confirmation bias that might occur when interpreting raw numbers.

Component Synergy: How the System Works Together

The indicator comprises three interconnected layers that create a unified analytical framework:

Core Calculation Layer: The traditional RSI calculation processes price data using the specified period length (default 14 periods). This generates the fundamental sentiment metric that drives all subsequent visualizations. The RSI calculation serves as the "brain" of the indicator, continuously analyzing market momentum.

Sentiment Classification Layer: This layer applies threshold logic to categorize each RSI reading into one of three emotional states. Readings above 70 are classified as "Greed" (market potentially overbought), below 30 as "Fear" (market potentially oversold), and between 30-70 as "Neutral" (balanced market conditions). These thresholds are based on the conventional RSI interpretation framework that has been widely adopted in technical analysis.

Visual Translation Layer: The most innovative aspect transforms numerical classifications into immediate visual cues. The colored ribbon area creates a "sentiment atmosphere" around price action, while the background tint provides subtle contextual framing. Horizontal reference lines at 30, 50, and 70 offer precise anchoring points, and the floating label provides real-time status updates. These elements work in concert: the ribbon shows sentiment intensity, the background provides persistent context, and the reference lines offer precise measurement points.

Practical Application: How to Use the Indicator Effectively

For optimal results, traders should incorporate this tool into a comprehensive analysis framework:

Initial Setup: Apply the indicator to any financial chart (stocks, forex, cryptocurrencies, etc.) using the default 14-period setting for general purposes. For shorter timeframes, consider reducing the period to 10; for longer-term analysis, increase to 20-25 periods.

Signal Interpretation:

When the ribbon turns red and the background tints crimson, exercise caution with new long positions and consider profit-taking on existing holdings.

Green zones may indicate accumulation opportunities, particularly if accompanied by bullish divergence (price making lower lows while RSI makes higher lows).

Yellow areas suggest normal market fluctuation where trend-following strategies may be more appropriate than reversal anticipation.

Confirmation Protocol: Always wait for additional confirmation before acting on extreme readings. For greed zone signals, look for bearish candlestick patterns, resistance at key price levels, or decreasing volume. For fear zone signals, watch for bullish reversal patterns, support levels holding, or increasing volume on down moves.

Timeframe Harmony: Analyze multiple timeframes simultaneously. A greed signal on a daily chart carries more weight than one on a 15-minute chart. Look for alignment across timeframes for higher-probability setups.

Alert Utilization: Enable the built-in alert system to receive notifications when sentiment zones change, ensuring you never miss potential opportunities or risk scenarios.

Original Contribution: What Sets This Indicator Apart

While RSI indicators are ubiquitous, the "Fear Greed Ranges" implementation offers several distinctive advantages:

Cognitive Efficiency: By converting numerical data into immediate visual perception, the indicator reduces the mental processing required to assess market conditions. Traders can glance at a chart and instantly understand the sentiment landscape without calculating or interpreting raw values.

Contextual Persistence: The colored background maintains a subtle but constant reminder of the prevailing sentiment, preventing the common pitfall of overlooking extreme conditions that might develop gradually.

Dual-Layer Communication: The system operates on both conscious (reference lines, labels) and subconscious (color psychology) levels, engaging multiple cognitive pathways for more reliable signal recognition.

Integrated Risk Framework: By explicitly naming emotional extremes ("Fear" and "Greed"), the indicator constantly reminds traders of the psychological forces driving markets, encouraging more disciplined decision-making.

Important Considerations and Limitations

No technical indicator guarantees future performance, and this tool should form only one component of a comprehensive trading strategy. Several critical factors require attention:

Market Context Matters: During strong trending markets, RSI can remain in extreme zones for extended periods without immediate reversal. In such conditions, the indicator signals strength rather than imminent reversal.

Volatility Adjustments: Highly volatile instruments may generate frequent zone changes that could lead to overtrading if not filtered appropriately.

Complementary Tools: This indicator works best when combined with price action analysis, volume studies, support/resistance levels, and fundamental factors where applicable.

Personal Adaptation: Traders should backtest the indicator on their preferred markets and timeframes to understand its characteristics before live implementation, potentially adjusting the RSI period or zone thresholds to match specific instrument behaviors.

The "Fear Greed Ranges" indicator serves as a visual translator of market psychology, converting mathematical momentum readings into intuitive emotional landscapes. By making RSI interpretation more immediate and accessible, it helps traders maintain objectivity during emotionally charged market conditions and supports more disciplined execution of their trading strategies. Remember that successful trading involves risk management, continuous learning, and adapting tools to your individual approach—this indicator provides one lens through which to view the markets, not a complete trading system in itself.

Tìm kiếm tập lệnh với "Candlestick"

Pro Volume & Momentum Dashboard [CONFIRMED ENTRY v2.1]🎯 Key Upgrades in This Version:

1. 10-Point Confluence Scoring System

# Factor Description

1 Volume Spike RVOL ≥ threshold with directional candle

2 Volume Delta Buy vs Sell pressure analysis

3 VWAP Position Institutional fair value

4 200 EMA Macro trend alignment

5 EMA Stack 9 > 21 > 50 alignment

6 ADX Trend strength + direction

7 RSI Momentum confirmation

8 MACD Histogram momentum

9 HTF Trend Higher timeframe alignment

10 Candle Quality Strong body, minimal wicks

2. Confirmed Entry Logic

✅ Requires minimum 7/10 confluence score (adjustable)

✅ Waits for candle close to avoid fakeouts

✅ 5-bar cooldown prevents duplicate signals

✅ Potential setups warned when score is 5-6/10

3. Risk Management

Auto-calculated Stop Loss (ATR-based)

Two Take Profit levels (TP1 & TP2)

Visual risk zones on chart

Risk/Reward ratio displayed

4. Higher Timeframe Confirmation

Checks 1H (or custom) timeframe trend

Ensures trade aligns with bigger picture

📌 How to Use:

Wait for ◆ CONFIRMED BUY/SELL label (not triangles)

Check dashboard for 7+/10 score

Entry: On signal candle close

Stop Loss: Red line below/above

Take Profit: Green lines (scale out at TP1, full exit TP2)

🕯️ Candlestick Patterns Added

Bullish Patterns (11 Total)

Pattern Description Strength

Bullish Engulfing Green candle engulfs prior red ⭐⭐⭐ Strong

Hammer Long lower wick at bottom ⭐⭐ Medium

Morning Star 3-candle reversal pattern ⭐⭐⭐ Strong

Bullish Harami Small green inside large red ⭐⭐ Medium

Piercing Line Opens gap down, closes above mid ⭐⭐ Medium

Three White Soldiers 3 consecutive strong green candles ⭐⭐⭐ Strong

Dragonfly Doji Long lower wick, no body ⭐⭐ Medium

Tweezer Bottom Equal lows at support ⭐⭐ Medium

Bullish Marubozu Full body, no wicks ⭐⭐⭐ Strong

Rising Three Continuation after pullback ⭐⭐ Medium

Bearish Patterns (11 Total)

Pattern Description Strength

Bearish Engulfing Red candle engulfs prior green ⭐⭐⭐ Strong

Shooting Star Long upper wick at top ⭐⭐ Medium

Evening Star 3-candle reversal pattern ⭐⭐⭐ Strong

Bearish Harami Small red inside large green ⭐⭐ Medium

Dark Cloud Cover Opens gap up, closes below mid ⭐⭐ Medium

Three Black Crows 3 consecutive strong red candles ⭐⭐⭐ Strong

Gravestone Doji Long upper wick, no body ⭐⭐ Medium

Tweezer Top Equal highs at resistance ⭐⭐ Medium

Bearish Marubozu Full body, no wicks ⭐⭐⭐ Strong

Falling Three Continuation after pullback ⭐⭐ Medium

Hanging Man Long lower wick at top ⭐⭐ Medium

Timeframe Continuity BarsTimeframe Continuity Bars is a script that is extremely simple for good reason

So please, do not remove this post because it seems 'simple'

Now that's over with. Lets dive in to understand what timeframe continuity IS and what this indicator does.

Timeframe continuity is defined by 4 or more timeframes and it is the relationship of the last price traded to those 4 opening prices. Standard timeframe continuity would be using the M,W,D,60min timeframes.

The reason we use MTF analysis is because of the truth of what price is and how it works.

Price movement is SOLELY caused due to aggressive buying / selling. Some may attempt to refute this however at the end of the day. If the price is at 100.00 it is because a buyer is willing to buy there and a seller is willing to sell there. If those market participants did not want to buy or sell at 100.00 price would go up or down to meet the more aggressive participant.

So what does this look like you may ask...

If an aggressive buyer takes the offer we will see prices go up if they were willing to pay more than the last guy who took the offer.

So price may go from 100.00 to 100.01 because you decided to invest in that stock that day at that time with a market order

This same thing occurs when every other institution creates, adds, reduces, or exits a position. They have to buy or sell and they have to either do it aggressively or do it passively by sitting on the bid / ask and waiting.

So since this is true, we know that the relationship to the opening price is extremely important. This is because if price is above it's open that means buyers were willing to take the offer and buy at higher prices. If price is below it's open it means that sellers were willing to sell at the bid and they sold at lower prices.

So any candlestick chart is simply an aggregation of this aggressive buying/selling that is taking place at all times.

By using the timeframe continuity bars indicator we can measure the distance from the current open across 4 or more timeframes.

By doing this we can identify monthly participation groups, weekly participation groups, daily participation groups, and 60min participation groups.

When all those groups align green or red this is considered full timeframe continuity. Where the monthly weekly daily 60min groups are all taking the offer and buying, or all selling at the bid!

When this aligns this is when price is for CERTAIN going in one direction.

However, It is subject to change every 60 minutes as the 60min determines if those monthly weekly daily buyers are present RIGHT NOW.

So if the 60min changes we go into direct conflict against the month/week/day groups.

If we see the 60min and day align we go into direct conflict against the month/week

if the 60min day and week are red we over-take the monthly group for control. At the time of the week day and 60 being red we have ZERO evidence of the previous monthly buyer/seller that was present.

Now that you understand a little bit about continuity.. Check it out on the chart!

P.S Here is some tips

1) it is not about just all timeframes aligning, we want to see long green / red bars!

2) The opens reset on a cyclical basis. Each day, each week, each month... When the new timeframes open we will see timeframes have the SAME open. When the opens are the same price we have LESS evidence versus having all opens seperate.

3) Investors can use the Y Q M W as their 4 timeframes to see when institutional buying is occurring [go do a case study on AMEX:GLD and AMEX:SLV weekly timeframe with these settings]

4) You need to add 4 separate indicators and change the timeframes. It is ideal to then save this layout!

5) The best way to do price analysis is using #TheStrat across all 4 timeframes instead of one timeframe with this indicator. This is soley a tool we use to show changing of control between participation groups!

Linear Regression Market State IndexStandard Deviation Market Structure Indicator

A Comprehensive Multi-Timeframe Market Analysis Tool

🎯 Overview

The Standard Deviation Market Structure (SDMS) indicator is a sophisticated technical analysis tool that integrates multiple proven methodologies to identify market structure, trend direction, and potential reversal zones. By combining price action, statistical analysis, and momentum indicators across multiple timeframes, SDMS provides traders with a comprehensive view of market dynamics.

✨ Key Features

Multi-Timeframe Integration

Primary analysis on current timeframe

1-hour statistical confirmation for support/resistance levels

Order block extension across 500 future bars

Comprehensive Technical Suite

RSI with Deviation Analysis

Dynamic Order Block Detection

Gaussian Filter Channels

Linear Regression with Statistical Bands

Standard deviation to detect price outliers

Directional Movement Index (DMI/ADX)

Bollinger Band % Analysis

Support/Resistance Line System

Visual Clarity

Color-coded signals and zones

Automatic level management

Clean, intuitive display

📊 Core Components Explained

1. Order Block System

What Are Order Blocks?

Order blocks are price zones where institutional activity has occurred, creating future support or resistance levels. SDMS automatically detects these critical zones.

Detection Logic:

Bullish Order Blocks: Form when price breaks above recent highs following bearish candles

Bearish Order Blocks: Form when price breaks below recent lows following bullish candles

Visual Identification:

Green boxes with "BuOB" labels (support zones)

Red boxes with "BeOB" labels (resistance zones)

Each block shows its boundary price for easy reference

Dynamic Management:

Automatically extends 300 bars into the future

Self-cleaning: removes blocks when price breaches their boundaries

Real-time adjustment to changing market structure

2. Statistical Support/Resistance System

How It Works:

SDMS creates support and resistance lines based on statistical extremes confirmed on the 1-hour timeframe.

Trigger Conditions:

Support Lines (Green): Trigger when 1H Bollinger Band % crosses above 0 and bearish momentum subsides.

Resistance Lines (Red): Trigger when 1H Bollinger Band % crosses below 1 and bullish momentum subsides

The Science Behind BB%:

BB% = (Price - Lower Band) / (Upper Band - Lower Band)

BB% <= 0: Price at statistical oversold extreme; also indicated by white candles.

BB% > 1: Price at statistical overbought extreme; also indicated by white candles.

Line Management:

Maximum of 15 active lines

Oldest lines automatically removed

Lines extend across chart for ongoing reference

3. Trend Analysis Suite

Hull Moving Average (HMA):

55-period smoothed trend indicator

Color-coded: Green = bullish, Red = bearish

Visual band shows trend acceleration/deceleration

Gaussian Channel:

Advanced filtering of market noise

Dynamic channel based on true range volatility

Helps identify mean reversion opportunities

Form a yellow band when price is overbought or oversold zones.

Linear Regression System:

Statistical price modeling

Multiple standard deviation bands (up to 3SD)

Regression-based candlestick visualization

Candles turn white when in overbought zones. Yellow candles indicate extremely overbought zones. Blue candles indicate a bullish trend with high volume.

Bearish candles are bluish-purple when volume is high and red when the volume is within normal ranges or low.

4. Momentum & Oscillator Integration

RSI with Deviation Tracking:

21-period RSI with 30-period smoothing

Tracks deviation from moving average based off linear regression

Identifies momentum divergences

Directional Movement Index:

Multi-period DMI/ADX analysis

Used to detect overbought and oversold zones within the indicator calculations.

Combines with RSI for enhanced signals

Momentum confirmation for all entries/exits

🎯 Trading Signals & Alerts

Buy Signals (Yellow "Buy" Labels)

Multi-Condition Confirmation Required:

RSI Oversold Reversal: RSI crosses above 30

Trend Alignment: HMA showing bullish structure

Momentum Confirmation: DMI alignment

Statistical Support: Price at or near support zones

Risk Management: Multiple confirming indicators

Strong Buy Conditions:

Confluence of order block support + BB% support line

Multiple timeframe alignment

Volume confirmation at key levels

Sell Signals (Red/Yellow "Sell" Labels)

Multi-Condition Confirmation Required:

RSI Overbought Reversal: RSI crosses below 70

Trend Exhaustion: HMA showing bearish structure

Momentum Divergence: DMI bearish alignment

Statistical Resistance: Price at or near resistance zones

Timeframe Confirmation: 1H BB% bearish signals

Strong Sell Conditions:

Confluence of order block resistance + BB% resistance line

Multiple timeframe distribution

Volume surge at resistance

Additional Alerts

RSI Divergence Signals: Triangles showing momentum shifts

Extreme Price Alerts: Circles at statistical extremes

Structure Breaks: Visual cues for order block violations

🎨 Visual System Guide

Color Coding System

Green: Bullish conditions, support zones, rising trends

Red: Bearish conditions, resistance zones, falling trends

Blue: Statistical channels, neutral zones

Yellow: Alert conditions, extreme signals

White: Transition zones, neutral signals

Zone Identification

Buying Pressure Zones: Green/blue tinted areas below price or white candles with white dots within the moving average center line

Selling Pressure Zones: Red tinted areas above price with white dots within the moving average center line

Standard Deviation Zones: Gradient colors showing statistical extremes

⚙️ Customization Options

Adjustable Parameters

RSI Settings: Period, oversold/overbought levels, sensitivity

Order Block Detection: Lookback period, ATR multiplier, extension

Statistical Settings: Gaussian filter poles, regression periods

Support/Resistance: Maximum lines, BB% settings

Visual Preferences: Colors, band displays, alert styles

Input Groups

RSI Trading Strategy

Order Block Configuration

Gaussian Channel Settings

Linear Regression Parameters

DMI/ADX Configuration

Bollinger Band % Settings

📈 Practical Trading Applications

For Swing Traders

Identify Key Levels: Use order blocks + BB% lines for entry/exit planning

Trend Confirmation: HMA + Gaussian channel for trend direction

Risk Management: Standard deviation bands for stop placement

Timing Entries: RSI/DMI alignment for optimal entry timing

For Day Traders

Intraday Levels: Order blocks provide immediate S/R for day trading

Momentum Signals: Real-time RSI/DMI signals for quick moves

Statistical Edges: Gaussian channel for mean reversion plays

Breakout Confirmation: Order block breaks with volume

For Position Traders

Higher Timeframe Structure: 1H BB% lines for major levels

Trend Persistence: HMA for long-term trend identification

Accumulation/Distribution Zones: Order blocks show institutional activity

Multi-Timeframe Alignment: Confirmation across timeframes

🔍 How to Use SDMS Effectively

Step 1: Market Structure Assessment

Identify active order blocks (green/red boxes)

Note BB% support/resistance lines (horizontal lines)

Assess HMA and moving average trend direction (color)

Check Gaussian channel position (preferably outside 2SD)

Step 2: Signal Confirmation

Wait for multiple indicator alignment

look for doji candles.

Confirm with green (bullish) or red (bearish) candles

Confirm with volume if available

Check for confluence of levels

Assess risk/reward based on nearby levels

Step 3: Trade Management

Enter at confirmed support/resistance

Place stops beyond opposite levels

Take profits at next statistical level

Monitor for structure changes

Step 4: Risk Management

Use standard deviation bands for volatility assessment

Never risk more than 1-2% per trade

Adjust position size based on confluence strength

Have predefined exit rules

💡 Advanced Strategies

Strategy 1: Confluence Trading

Setup: Order block + BB% line at same level

Entry: Price tests confluence zone with RSI signal

Stop: Beyond the confluence zone

Target: Next statistical level

Strategy 2: Breakout Trading

Setup: Price approaching order block boundary

Entry: Break with volume + RSI/DMI confirmation

Stop: Re-entry into order block

Target: Next BB% line extension

Strategy 3: Mean Reversion

Setup: Price at Gaussian channel extremes

Entry: RSI reversal signal at channel boundary

Stop: Beyond channel extreme

Target: Channel midline or opposite boundary

⚠️ Important Considerations

Best Market Conditions

Trending Markets: Excellent performance in clear trends

Breakout Scenarios: Strong identification of break levels

Range Markets: Works well with defined ranges

Limitations

Choppy Markets: May give false signals in consolidation

News Events: Fundamental shocks can override technical levels

Timeframe Specific: Optimal on 15-minute to daily charts

Risk Management Rules

Always use stops

Never rely on single signals

Consider market context

Adjust for volatility changes

Keep position sizes consistent

🔧 Technical Specifications

Maximum Lines: 500

Maximum Bars Back: 1000

Maximum Boxes: 500

Calculation Efficiency: Optimized for real-time use

🏆 Why SDMS Stands Out

Unique Advantages

Integrated Approach: Combines multiple methodologies into one tool

Self-Adjusting: Automatically adapts to market changes

Multi-Timeframe: Provides both immediate and higher timeframe context

Visual Clarity: Clean, intuitive display of complex data

Professional Grade: Institutional-level analysis accessible to all traders

Educational Value: Learn how different indicators interact

Understand market structure development

See institutional order flow patterns

Develop disciplined trading habits

📚 Learning Resources

Recommended Study Approach

Start Simple: Focus on order blocks and BB% lines first

Add Complexity: Gradually incorporate other indicators

Paper Trade: Practice without risk

Keep Journal: Document setups and outcomes

Review Regularly: Analyze both wins and losses

Common Pitfalls to Avoid

Overtrading: Wait for high-quality setups

Ignoring Context: Consider overall market conditions

Chasing Signals: Enter at planned levels, not after moves

Risk Mismanagement: Always know your risk before entering

Confirmation Bias: Be objective about signals

🤝 Community & Support

Getting the Most from SDMS

Start with Defaults: Use default settings initially

Adjust Gradually: Make small changes as you understand the tool

Combine with Fundamentals: Use for timing within fundamental context

Stay Disciplined: Follow your trading plan consistently

Continuous Improvement

SDMS is designed for continuous learning. As you use the indicator, you'll develop insights into:

Market microstructure

Institutional trading patterns

Statistical edge identification

Risk management optimization

Risk management is more important than signal accuracy

Patience is required for high-quality setups

Success Factors

Discipline: Following your plan consistently

Patience: Waiting for proper setups

Risk Management: Protecting your capital

Continuous Learning: Improving your skills over time

🌟 Final Thoughts

The Standard Deviation Market Structure indicator represents a sophisticated approach to technical analysis, combining the best elements of price action, statistical analysis, and momentum indicators. While powerful, remember that no indicator guarantees success. SDMS is a tool – your skill, discipline, and risk management determine your trading results.

Use SDMS as part of a comprehensive trading plan, combine it with proper risk management, and continue developing your trading skills. The markets are always teaching – stay humble, stay disciplined, and trade well.

Disclaimer: This indicator is for educational purposes only. Past performance does not guarantee future results. Trading involves risk of loss. Always consult with a qualified financial professional before making investment decisions.

Sakata Reversal MatrixThis indicator automatically detects key candlestick reversal patterns based on the traditional Japanese "Sakata Five Methods."

Key Features: Identifies patterns such as Hammer, Engulfing, Harami, Piercing/Dark Cloud, and Gaps (Sanku).

Strict Star Detection: "Morning Star" and "Evening Star" signals are filtered using a strict logic where the second candle (the star) must be visually isolated from the surrounding candles.

High-Accuracy Filter: Combines RSI (below 30 or above 70) with Bollinger Bands to ensure signals appear only during overbought or oversold conditions, reducing false signals.

Bilingual Support: Easily toggle between Japanese and English labels in the settings.

このインジケーターは、日本の伝統的な相場分析法である「酒田五法」をベースに、主要な反転ローソク足パターンを自動検知します。

主な機能: ハンマー(首吊り線)、包み足、はらみ足、切り込み線、三空などを表示。

厳格な明星判定: 「明けの明星」「宵の明星」は、2本目のローソク足の実体が前後の足から窓を開けて孤立している場合のみ検知する厳格なロジックを採用しています。

高精度フィルタ: RSI(35以下/65以上)とボリンジャーバンドを組み合わせ、相場が過熱しているポイントでのみサインを出すことで、騙しを軽減しています。

バイリンガル対応: 設定から日本語と英語の表示を切り替え可能です。

3LL+Baby & 3HH+Baby Pattern3LL+Baby & 3HH+Baby Pattern Indicator

Overview

This indicator identifies powerful reversal patterns based on momentum exhaustion and inside bar formations. It detects two specific candlestick patterns that signal potential trend reversals: the bullish 3LL+Baby and the bearish 3HH+Baby.

Pattern Descriptions

📈 3LL+Baby Pattern (Bullish Reversal)

Conditions:

Three consecutive candles form lower lows (each low is lower than the previous)

The fourth candle is bullish/green (closes higher than it opens)

The fourth candle is completely contained within the third candle's range (both high and low)

Interpretation: After a downward momentum with three lower lows, a bullish inside bar (baby candle) suggests sellers are exhausted and buyers may be taking control. This pattern often precedes upward reversals.

📉 3HH+Baby Pattern (Bearish Reversal)

Conditions:

Three consecutive candles form higher highs (each high is higher than the previous)

The fourth candle is bearish/red (closes lower than it opens)

The fourth candle is completely contained within the third candle's range (both high and low)

Interpretation: After upward momentum with three higher highs, a bearish inside bar indicates buyers are losing strength and sellers may be gaining control. This pattern often signals potential downward reversals.

Features

Visual Signals

Green Triangle (↑): Appears below bars when 3LL+Baby pattern is detected

Red Triangle (↓): Appears above bars when 3HH+Baby pattern is detected

Labels: Clear text labels identifying each pattern type

Background Highlighting: Subtle background colors (green for bullish, red for bearish)

Customization Options

Toggle labels on/off

Toggle arrow signals on/off

Enable/disable bullish patterns independently

Enable/disable bearish patterns independently

How to Use

Add to Chart: Apply the indicator to any timeframe and instrument

Configure Settings: Adjust visibility options based on your preference

Set Alerts: Create alerts for immediate pattern notifications

Trading Strategy:

3LL+Baby : Consider long positions or closing shorts

3HH+Baby: Consider short positions or closing longs

Always confirm with additional analysis and risk management

Best Practices

Use in conjunction with support/resistance levels

Combine with volume analysis for confirmation

Works on all timeframes (higher timeframes generally more reliable)

Apply proper risk management and stop-loss orders

Consider the broader market context and trend

Pinbar MTF - No Repaint# Pinbar MTF - No Repaint Indicator

## Complete Technical Documentation

---

## 📊 Overview

**Pinbar MTF (Multi-Timeframe) - No Repaint** is a professional-grade TradingView Pine Script indicator designed to detect high-probability pinbar reversal patterns with advanced filtering systems. The indicator is specifically engineered to be **100% non-repainting**, making it reliable for both live trading and backtesting.

### Key Features

✅ **Non-Repainting** - Signals only appear AFTER bar closes, never disappear

✅ **Three-Layer Filter System** - ATR, SWING, and RSI filters

✅ **Automatic SL/TP Calculation** - Based on risk:reward ratios

✅ **Real-time Alerts** - TradingView notifications for all signals

✅ **Visual Trade Management** - Lines, labels, and areas for entries, stops, and targets

✅ **Backtesting Ready** - Reliable historical data for strategy testing

---

## 🎯 What is a Pinbar?

A **Pinbar (Pin Bar/Pinocchio Bar)** is a single candlestick pattern that indicates a potential price reversal:

### Bullish Pinbar (BUY Signal)

- **Long lower wick** (rejection of lower prices)

- **Small body at the top** of the candle

- Shows buyers rejected sellers' attempt to push price down

- Forms at support levels or swing lows

- Entry signal for LONG positions

### Bearish Pinbar (SELL Signal)

- **Long upper wick** (rejection of higher prices)

- **Small body at the bottom** of the candle

- Shows sellers rejected buyers' attempt to push price up

- Forms at resistance levels or swing highs

- Entry signal for SHORT positions

---

## 🔧 How the Indicator Works

### 1. **Pinbar Detection Logic**

The indicator analyzes the **previous closed bar ** to identify pinbar patterns:

```

Bullish Pinbar Requirements:

- Lower wick > 72% of total candle range (adjustable)

- Upper wick < 28% of total candle range

- Close > Open (bullish candle body)

Bearish Pinbar Requirements:

- Upper wick > 72% of total candle range (adjustable)

- Lower wick < 28% of total candle range

- Close < Open (bearish candle body)

```

**Why check ?** By analyzing the previous completed bar, we ensure the pattern is fully formed and won't change, preventing repainting.

---

### 2. **Three-Layer Filter System**

#### 🔍 **Filter #1: ATR (Average True Range) Filter**

- **Purpose**: Ensures the pinbar has significant size

- **Function**: Only signals if pinbar range ≥ ATR value

- **Benefit**: Filters out small, insignificant pinbars

- **Settings**:

- Enable/Disable toggle

- ATR Period (default: 7)

**Example**: If ATR = 50 pips, only pinbars with 50+ pip range will signal.

---

#### 🔍 **Filter #2: SWING Filter** (Always Active)

- **Purpose**: Confirms pinbar forms at swing highs/lows

- **Function**: Validates the pinbar is an absolute high/low

- **Benefit**: Identifies true reversal points

- **Settings**:

- Swing Candles (default: 3)

**How it works**:

- For bullish pinbar: Checks if low is lowest of past 3 bars

- For bearish pinbar: Checks if high is highest of past 3 bars

**Example**: With 3 swing candles, a bullish pinbar must have the lowest low among the last 3 bars.

---

#### 🔍 **Filter #3: RSI (Relative Strength Index) Filter**

- **Purpose**: Confirms momentum conditions

- **Function**: Prevents signals in extreme momentum zones

- **Benefit**: Avoids counter-trend trades

- **Settings**:

- Enable/Disable toggle

- RSI Period (default: 7)

- RSI Source (Close, Open, High, Low, HL2, HLC3, OHLC4)

- Overbought Level (default: 70)

- Oversold Level (default: 30)

**Logic**:

- Bullish Pinbar: Only signals if RSI < 70 (not overbought)

- Bearish Pinbar: Only signals if RSI > 30 (not oversold)

---

### 3. **Stop Loss Calculation**

Two methods available:

#### Method A: ATR-Based Stop Loss (Recommended)

```

Bullish Pinbar:

SL = Pinbar Low - (1 × ATR)

Bearish Pinbar:

SL = Pinbar High + (1 × ATR)

```

**Benefit**: Dynamic stops that adapt to market volatility

#### Method B: Fixed Pips Stop Loss

```

Bullish Pinbar:

SL = Pinbar Low - (Fixed Pips)

Bearish Pinbar:

SL = Pinbar High + (Fixed Pips)

```

**Settings**:

- Calculate Stop with ATR (toggle)

- Stop Pips without ATR (default: 5)

---

### 4. **Take Profit Calculation**

Take Profit is calculated based on Risk:Reward ratio:

```

Bullish Trade:

TP = Entry + (Entry - SL) × Risk:Reward Ratio

Bearish Trade:

TP = Entry - (SL - Entry) × Risk:Reward Ratio

```

**Example**:

- Entry: 1.2000

- SL: 1.1950 (50 pip risk)

- RR: 2:1

- TP: 1.2100 (100 pip reward = 50 × 2)

**Settings**:

- Risk:Reward Ratio (default: 1.0, range: 0.1 to 10.0)

---

## 📈 Visual Elements

### On-Chart Displays

1. **Signal Markers**

- 🟢 **Green Triangle Up** = Bullish Pinbar (BUY)

- 🔴 **Red Triangle Down** = Bearish Pinbar (SELL)

- Placed directly on the pinbar candle

2. **Entry Labels**

- Green "BUY" label with entry price

- Red "SELL" label with entry price

- Shows exact entry level

3. **Stop Loss Lines**

- 🔴 Red horizontal line

- "SL" label

- Extends 20 bars forward

4. **Take Profit Lines**

- 🟢 Green horizontal line

- "TP" label

- Extends 20 bars forward

5. **Risk/Reward Areas** (Optional)

- Red shaded box = Risk zone (Entry to SL)

- Green shaded box = Reward zone (Entry to TP)

- Visual risk:reward visualization

6. **Info Table** (Top Right)

- Displays current settings

- Shows filter status (ON/OFF)

- Real-time RSI value

- Quick reference panel

---

## 🔔 Alert System

Three alert types available:

### 1. Combined Alert: "Pinbar Signal (Any Direction)"

- Fires for BOTH bullish and bearish pinbars

- **Best for**: General monitoring

- **Message**: "Pinbar Signal Detected on {TICKER} at {PRICE}"

### 2. Bullish Alert: "Bullish Pinbar Alert"

- Fires ONLY for BUY signals

- **Best for**: Long-only strategies

- **Message**: "BUY Signal on {TICKER} at {PRICE}"

### 3. Bearish Alert: "Bearish Pinbar Alert"

- Fires ONLY for SELL signals

- **Best for**: Short-only strategies

- **Message**: "SELL Signal on {TICKER} at {PRICE}"

---

## ⚙️ Input Parameters Reference

### **Filters Group**

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| ATR Filter on Pinbar Range? | ✅ ON | Boolean | Enable/disable ATR filter |

| ATR Period | 7 | 1+ | Lookback period for ATR calculation |

| Swing Candles | 3 | 1+ | Bars to check for swing high/low |

| RSI Filter on Pinbar? | ❌ OFF | Boolean | Enable/disable RSI filter |

| RSI Period | 7 | 2+ | Lookback period for RSI calculation |

| RSI Source | Close | Multiple | Price data for RSI (Close/Open/High/Low/etc) |

| RSI Overbought Level | 70 | 50-100 | Upper threshold for RSI filter |

| RSI Oversold Level | 30 | 0-50 | Lower threshold for RSI filter |

### **Pinbar Detection Group**

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| Shadow % vs Body | 72 | 50-95 | Minimum wick size as % of total range |

### **Visualization Group**

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| Show SL and TP Lines? | ✅ ON | Boolean | Display stop loss and take profit lines |

| Show SL and TP Area? | ❌ OFF | Boolean | Show shaded risk/reward boxes |

### **Risk Management Group**

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| Risk:Reward Ratio | 1.0 | 0.1-10.0 | Target profit vs risk (1.0 = 1:1, 2.0 = 1:2) |

| Calculate Stop with ATR? | ✅ ON | Boolean | Use ATR for stop calculation |

| Stop Pips without ATR | 5 | 1+ | Fixed pip stop when ATR disabled |

---

## 🚫 Non-Repainting Architecture

### What is Repainting?

**Repainting** occurs when an indicator's historical signals differ from what appeared in real-time. This makes backtesting unreliable and can lead to false confidence in a strategy.

### How This Indicator Prevents Repainting

1. **Closed Bar Analysis**

- All calculations use ` ` offset (previous bar)

- Only analyzes COMPLETED candles

- Signals appear on the bar AFTER the pinbar closes

2. **Confirmed Swing Points**

- Waits for sufficient bar history before signaling

- Only checks historical bars that cannot change

- Prevents premature swing detection

3. **Static Alert Timing**

- Alerts fire only after bar completion

- No conditional logic that changes historically

- Same results in replay mode and live trading

### Verification Method

To verify non-repainting behavior:

1. Apply indicator to chart

2. Note signal locations and prices

3. Refresh browser / reload chart

4. **Signals remain in exact same locations**

---

## 💼 Trading Strategy Guidelines

### Entry Rules

**For Bullish Pinbar (LONG):**

1. Wait for green triangle to appear

2. Enter at close of pinbar (shown in label)

3. Alternative: Enter on break of pinbar high

4. Place stop loss at red SL line

5. Set target at green TP line

**For Bearish Pinbar (SHORT):**

1. Wait for red triangle to appear

2. Enter at close of pinbar (shown in label)

3. Alternative: Enter on break of pinbar low

4. Place stop loss at red SL line

5. Set target at green TP line

### Risk Management

- **Position Sizing**: Risk only 1-2% of account per trade

- **Stop Loss**: Always use the calculated SL (never move it wider)

- **Take Profit**: Use calculated TP or trail stop after 1:1 RR

- **Multiple Timeframes**: Confirm signals on higher timeframe

### Best Practices

✅ **DO:**

- Wait for bar to close before entering

- Trade in direction of higher timeframe trend

- Use on liquid markets with clear support/resistance

- Combine with price action analysis

- Keep a trading journal

❌ **DON'T:**

- Enter before bar closes (prevents seeing full pattern)

- Trade against strong trends

- Ignore the filters (they improve win rate)

- Risk more than 2% per trade

- Trade every signal (be selective)

---

## 📊 Backtesting & Data Export

### Available Data Points

The indicator exports these values for strategy development:

| Output | Description |

|--------|-------------|

| Bullish Signal | 1 = BUY signal, 0 = No signal |

| Bearish Signal | 1 = SELL signal, 0 = No signal |

| Bull SL | Stop loss level for long trades |

| Bull TP | Take profit level for long trades |

| Bull Entry | Entry price for long trades |

| Bear SL | Stop loss level for short trades |

| Bear TP | Take profit level for short trades |

| Bear Entry | Entry price for short trades |

### How to Use in Strategy

These values can be accessed by Pine Script strategies using:

```pine

indicator_values = request.security(syminfo.tickerid, timeframe.period,

)

```

---

## 🎓 Understanding the Filters

### Why Use Multiple Filters?

Single-indicator systems often generate too many false signals. This indicator uses a **confluence approach**:

1. **Pinbar Pattern** = Price rejection detected

2. **+ SWING Filter** = Rejection at key level

3. **+ ATR Filter** = Significant move

4. **+ RSI Filter** = Favorable momentum

**Result**: Higher probability setups with better risk:reward

### Filter Optimization

**Conservative Settings** (Fewer, Higher Quality Signals):

- ATR Filter: ON

- Swing Candles: 5

- RSI Filter: ON

- Shadow %: 75%

**Aggressive Settings** (More Signals, More Noise):

- ATR Filter: OFF

- Swing Candles: 2

- RSI Filter: OFF

- Shadow %: 65%

**Balanced Settings** (Recommended):

- ATR Filter: ON

- Swing Candles: 3

- RSI Filter: OFF (or ON for trending markets)

- Shadow %: 72%

---

## 🔍 Troubleshooting

### "No Signals Appearing"

**Possible Causes:**

1. Filters are too strict

2. No pinbars forming on chart

3. Insufficient bar history

**Solutions:**

- Reduce Shadow % to 65%

- Reduce Swing Candles to 2

- Disable ATR or RSI filters temporarily

- Check that chart has enough data loaded

### "Too Many Signals"

**Solutions:**

- Enable ATR filter

- Increase Swing Candles to 4-5

- Enable RSI filter

- Increase Shadow % to 75-80%

### "Signals Appearing Late"

**This is normal behavior!** The indicator:

- Analyzes previous closed bar

- Signals appear on the bar AFTER the pinbar

- This is what prevents repainting

- Signal latency is 1 bar (by design)

---

## 📝 Technical Specifications

**Indicator Type:** Overlay (displays on price chart)

**Pine Script Version:** 5

**Max Labels:** 500

**Max Lines:** 500

**Repainting:** None (100% non-repainting)

**Data Window Values:** 8 exported values

**Alert Types:** 3 (Combined, Bullish, Bearish)

**Performance:**

- Lightweight script (fast execution)

- Works on all timeframes

- Compatible with all markets (Forex, Crypto, Stocks, Futures)

- No data snooping bias

---

## 🎯 Use Cases

### 1. **Swing Trading**

- Timeframe: Daily, 4H

- Filter Settings: All enabled

- Best for: Catching major reversals

### 2. **Day Trading**

- Timeframe: 15m, 1H

- Filter Settings: ATR + SWING only

- Best for: Intraday reversals

### 3. **Scalping**

- Timeframe: 5m, 15m

- Filter Settings: SWING only (aggressive)

- Best for: Quick reversals (requires experience)

### 4. **Position Trading**

- Timeframe: Weekly, Daily

- Filter Settings: All enabled + high RR (2:1 or 3:1)

- Best for: Long-term trend reversal catches

---

## 🏆 Advantages Over Other Pinbar Indicators

✅ **Guaranteed Non-Repainting** - Many pinbar indicators repaint; this one never does

✅ **Automatic SL/TP** - No manual calculation needed

✅ **Multi-Layer Filtering** - Reduces false signals significantly

✅ **Visual Trade Management** - Clear entry, stop, and target levels

✅ **Flexible Configuration** - Adaptable to any trading style

✅ **Alert System** - Never miss a setup

✅ **Backtesting Ready** - Reliable historical data

✅ **Professional Grade** - Suitable for live trading

---

## 📚 Educational Resources

### Recommended Reading on Pinbars

- "The Pin Bar Trading Strategy" by Nial Fuller

- "Price Action Trading" by Al Brooks

- TradingView Education: Price Action Patterns

### Practice Recommendations

1. Paper trade signals for 20+ trades before live trading

2. Backtest on different timeframes and markets

3. Keep detailed records of all trades

4. Analyze winning vs losing setups

5. Refine filter settings based on results

---

## ⚖️ Disclaimer

This indicator is a tool for technical analysis and does not guarantee profits. Trading involves substantial risk of loss. Past performance is not indicative of future results.

- Always use proper risk management

- Never risk more than you can afford to lose

- Consider your trading experience and objectives

- Seek independent financial advice if needed

---

## 📧 Version Information

**Current Version:** 1.0

**Last Updated:** 2024

**Compatibility:** TradingView Pine Script v5

**Status:** Production Ready

---

## 🔄 Future Enhancements (Potential)

Possible future additions:

- Multi-timeframe confirmation option

- Volume filter integration

- Customizable color schemes

- Win rate statistics display

- Partial profit taking levels

- Trailing stop functionality

---

## 📖 Quick Start Guide

### 5-Minute Setup

1. **Add to Chart**

- Open TradingView

- Go to Pine Editor

- Paste the code

- Click "Add to Chart"

2. **Configure Settings**

- Open indicator settings (gear icon)

- Start with default settings

- Enable "Show SL and TP Lines"

3. **Set Alert**

- Right-click indicator name

- Click "Add Alert"

- Select "Pinbar Signal (Any Direction)"

- Configure notification method

4. **Test**

- Scroll back on chart

- Verify signals make sense

- Check that signals don't repaint

5. **Trade** (After Practice!)

- Wait for alert

- Verify signal quality

- Enter, place SL/TP

- Manage trade

---

## 🎯 Final Thoughts

The **Pinbar MTF - No Repaint** indicator is designed for serious traders who value:

- **Reliability** over flashy signals

- **Quality** over quantity

- **Honesty** over false promises

This indicator will NOT:

- Make you rich overnight

- Win every trade

- Replace proper trading education

This indicator WILL:

- Identify high-probability reversal setups

- Save you analysis time

- Provide consistent, non-repainting signals

- Help you develop a systematic trading approach

**Success in trading comes from:**

1. Proper education (60%)

2. Risk management (30%)

3. Technical tools like this indicator (10%)

Use this tool as part of a complete trading plan, not as a standalone solution.

Monday's Range Superpowerkyu🔔 Settings

You can customize the colors and toggle ON/OFF in the indicator settings.

Works on daily, hourly, and minute charts.

Easily visualize Monday’s high, low, and mid-line range.

📌 1. Support & Resistance with Monday’s Range

Monday High: Acts as the first resistance of the week.

◽ Example: If price breaks above Monday’s high after Tuesday, it signals potential bullish continuation → long setup.

Monday Low: Acts as the first support of the week.

◽ Example: If price breaks below Monday’s low, it signals bearish continuation → short setup.

📌 2. Mid-Line Trend Confirmation

Monday Mid-Line = average price of Monday.

Price above mid-line → bullish bias.

Price below mid-line → bearish bias.

Use mid-line breaks as entry confirmation for long/short positions.

📌 3. Breakout Strategy

Break of Monday’s High = bullish breakout → long entry.

Break of Monday’s Low = bearish breakout → short entry.

Place stop-loss inside Monday’s range for a conservative approach.

📌 4. False Breakout Strategy

If price breaks Monday’s high/low but then falls back inside Monday’s range, it is a False Breakout.

Strategy: Trade in the opposite direction.

◽ False Breakout at High → short.

◽ False Breakout at Low → long.

Stop-loss at the wick (extreme point) of the failed breakout.

📌 5. Range-Based Scalping

Use Monday’s high and low as a trading range.

Sell near Monday’s High, buy near Monday’s Low, repeat until breakout occurs.

📌 6. Weekly Volatility Forecast

Narrow Monday range → higher chance of strong trend later in the week.

Wide Monday range → lower volatility expected during the week.

📌 7. Pattern & Trend Analysis within Monday Range

Look for candlestick patterns around Monday’s High/Low/Mid-Line.

◽ Example: Double Top near Monday’s High = short setup.

◽ Repeated bounce at Mid-Line = strong long opportunity.

✅ Summary

The Monday’s Range (Superpowerkyu) Indicator helps traders:

Identify weekly support & resistance

Confirm trend direction with Mid-Line

Trade breakouts & false breakouts

Apply range scalping strategies

Forecast weekly volatility

⚡ Especially, the False Breakout strategy is powerful as it captures failed moves and sudden sentiment reversals.

Hilly's 0010110 Reversal Scalping Strategy - 5 Min CandlesKey Features and Rationale:

Timeframe: Restricted to 5-minute candles as requested.

Pattern Integration: Includes single (Hammer, Shooting Star, Doji), two (Engulfing, Harami), and three-plus (Morning Star, Evening Star) candlestick patterns, plus reversal patterns based on RSI extremes.

VWAP Cross: Incorporates bullish (price crosses above VWAP) and bearish (price crosses below VWAP) signals, enhanced by trend context.

Volume Analysis: Uses a volume spike threshold to filter noise, with a simple day-start volume comparison for financial environment context.

Financial Environment: Approximates the day's sentiment using early-hour volume compared to current volume, adjusted by trend.

Aggregation: Scores each condition (e.g., 1 for basic patterns, 2 for strong patterns like Engulfing, 3 for three-candle patterns) and decides based on weighted consensus, with trendStrength as a tunable threshold.

Risky Approach: Minimal filtering and a low trendStrength (default 0.5) allow frequent signals, aligning with your $100-to-$200 goal, but expect higher risk.

Suggested Inputs:

EMA Length: 10 (short enough for 5-minute sensitivity).

VWAP Lookback: 1 (uses current session VWAP).

Volume Threshold Multiplier: 1.2 (moderate spike requirement).

RSI Length: 14 (standard, adjustable to 7 for more sensitivity).

Trend Strength Threshold: 0.5 (balance between signals; lower to 0.4 for more trades, raise to 0.6 for fewer).

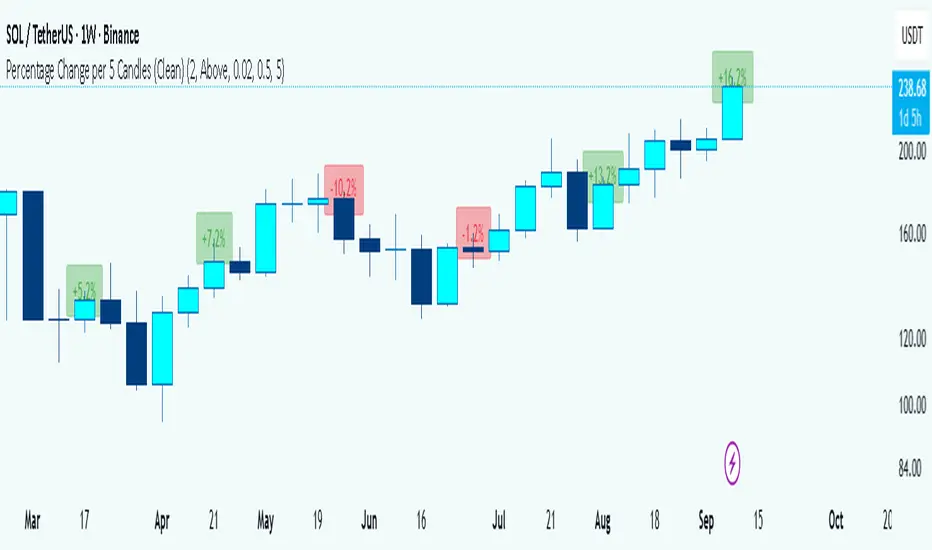

Percentage Change per 5 Candles

🔎 What this indicator does

This indicator calculates and displays the percentage change of each candlestick directly on the chart.

• If a candle closed higher than it opened (bullish candle), it shows a positive % change (green).

• If a candle closed lower than it opened (bearish candle), it shows a negative % change (red).

• Small moves below your chosen threshold (e.g., 0.1%) are ignored to avoid clutter.

• The labels are placed above, below, or in the center of the candle (you choose).

So essentially, every candle “tells you in numbers” exactly how much it changed relative to its opening price.

________________________________________

⚙️ How it operates (the logic inside)

1. Calculate the change

o Formula:

\text{% Change} = \frac{(\text{Close} - \text{Open})}{\text{Open}} \times 100

o Example: If a candle opens at 100 and closes at 105, that’s a +5% change.

2. Round it nicely

o You can control decimals (e.g., show 2 decimals → +5.23%).

3. Filter out noise

o If a candle barely moved (say 0.02%), the label won’t appear unless you reduce the threshold.

4. Style the labels

o Bullish = green text, slightly transparent green background.

o Bearish = red text, slightly transparent red background.

o Neutral (0%) = gray.

5. Place the labels

o Options: above the candle, below the candle, or centered.

o Small vertical offset is applied so labels don’t overlap the candle itself.

________________________________________

📊 How this helps traders

This indicator turns visual candles into quantifiable numbers at a glance. Instead of guessing whether a move was “big” or “small,” you see it clearly.

Key Benefits:

1. Quick volatility analysis

o You can instantly see if candles are making big % swings or just small moves.

o This is especially useful on higher timeframes (daily/weekly) where moves can be large.

2. Pattern confirmation

o For example, you might spot a strong bullish engulfing candle — the % change label helps confirm whether it was truly significant (e.g., +4.5%) or just modest (+0.7%).

3. Noise filtering

o By setting a minimum % threshold, you only see labels when moves are meaningful (say > 0.5%). This keeps focus on important candles.

4. Backtesting & comparison

o You can compare moves across time:

“How strong was this breakout candle compared to the last one?”

“Are today’s bearish candles weaker or stronger than yesterday’s bullish candles?”

5. Better decision-making

o If you’re trading breakouts, reversals, or trend-following, knowing the % size of each candle helps confirm if the move has enough momentum.

________________________________________

✅ In short:

This indicator quantifies price action. Instead of just seeing “green” or “red” candles, you now know exactly how much the price changed in percentage terms, directly on the chart, in real time. It helps you distinguish between strong and weak moves and makes your analysis more precise.

________________________________________

自定义均线系统A customizable Moving Average indicator that lets you freely choose the period values you want, and automatically plots them on the candlestick chart. This flexibility helps traders quickly adjust their analysis style, compare different trends, and fine-tune strategies without switching between multiple fixed indicators.

Custom Buy/Sell Pattern BuilderAre you tired of using trading indicators that only let you follow fixed, pre-designed rules? Do you wish you could build your own “Buy” or “Sell” signals, experiment with your own ideas, or see instantly if your unique pattern works—without learning coding or hiring a developer?

The Custom Buy/Sell Pattern Builder is designed for YOU.

This TradingView indicator lets ANY trader—even a complete beginner—define exactly what kind of price and volume conditions should create a BUY or SELL label on any chart, in any market, at any timeframe.

You don’t need to know programming. You don’t need to know the definition of a hammer, doji, volume spike, or Engulfing pattern.

With a few clicks and easy dropdown choices, you can:

Make your own rules for buying or selling

Choose how many candles your pattern should look at

Decide if you want the biggest body, the lowest volume, the biggest movement, or any combination you can imagine

The result?

You’ll see clear “BUY” or “SELL” labels automatically show up on your chart whenever the exact rule YOU built matches current price action.

No more guessing. No more forced strategies. Just pure control and visual feedback!

Why Is This Powerful?

Traditional indicators (like MACD, RSI, or even classic candlestick scanners) work the same for everyone—and only as their inventors defined.

But every trader, and every market, is unique.

What if you could say:

“Show me a ‘SELL’ every time the newest candle is bigger than the one before, but with LESS volume, while the bar before that had an even smaller body—but more volume than all others?”

With this tool, it’s EASY!

You simply pick which candle you want to compare (most recent, previous, etc), what to compare (body or volume—body means the candle’s “thickness”, from open to close), choose “greater than”, “less than”, or “equal to”, and set a multiplier if you want (like “half as much”, “twice as big”, etc).

After this, if any bar on the chart fits all your rules, it will mark it as a BUY or SELL, depending on your selection.

This means—

Beginners can start experimenting with their intuition or small ideas, without tech hurdles

Experienced traders can visualize and fine-tune any possible logic, before they commit to backtesting or automating a real strategy

Every “what if” or “I wonder” setup is just 2–3 clicks away

How Does It Work? Simple Steps

1. Choose Your Signal Type

“Buy” or “Sell”

This tells the indicator whether to mark the qualifying bars with a green “BUY” or red “SELL” label

2. Pick How Many Candles To Use

“Pattern Candle Count” input (2, 3, or 4)

Example: If you use 4, the pattern will be applied to the most recent 4 candles at every step

3. Define Your Pattern With Inputs

For each candle (from newest “0” to oldest “3”), you can set:

Body Condition (example: “is this candle’s body bigger/smaller/equal to another?”)

Pick which candle to compare against

Pick “>”, “<”, “>=”, “<=”, or “=”

Set a multiplier if needed (like “0.5” to mean “half as big as” or “2” for “twice as big as”)

Volume Condition (exact same choices, but based on trading volume—not the candle’s price body)

For example:

“Candle0 Body > Candle2 Body”

means “the latest candle’s real-body (open–close) is bigger than the one two bars ago.”

“Candle1 Volume <= Candle2 Volume”

means “the previous candle’s volume is less than or equal to the volume of the bar two periods ago.”

You can leave a comparison blank if you don’t want to use it for a particular candle.

What Happens After You Set Your Rules?

Every bar on your chart is checked for your logic:

If ALL body AND volume conditions are true (for each candle you specified),

AND

The signal side (“Buy” or “Sell”) matches your dropdown,

Then a green “BUY” or red “SELL” label will show right on the bar, so you can visually spot exactly where your logic works!

Practical Example:

Suppose you want an entry setup that is:

“Sell whenever the newest candle’s body is bigger than two bars ago, body before that is bigger than three bars ago, AND the newest candle’s volume is less than or equal to two bars ago, AND the candle three bars ago’s volume is less than or equal to half the candle two bars ago’s volume.”

You’d set:

Pattern Candle Count: 4

Side: Sell

Candle0 Body Ref#: 2, Op: >, Mult: 1

Candle1 Body Ref#: 3, Op: >, Mult: 1

Candle0 Vol Ref#: 2, Op: <=, Mult: 1

Candle3 Vol Ref#: 2, Op: <=, Mult: 0.5

And the script will find all “SELL” bars on your chart matching these conditions.

Inputs Section: What Does Each Setting Do?

Let’s break down each input in the indicator’s Settings one by one, so even if you’re new, you’ll understand exactly how to use it!

1. Pattern Candle Count (2–4)

What is it?

This sets how many candles in a row you want your rule to look at.

Example:

“4” means your rules are based on the most recent candle and the 3 before it.

“2” means you are only comparing the current and previous candles.

Tip:

Beginners often use 4 to spot stronger patterns, but you can experiment!

2. Signal Side

What is it?

Choose “Buy” or “Sell”. The word you pick here decides which colored label (green for Buy, red for Sell) appears if your pattern matches.

Example:

Want to spot where “Sell” is likely? Pick “Sell”.

Change to “Buy” if you want bullish signals instead.

3. Body & Volume Comparison Settings (per Candle)

For each candle (#0 is newest/current, #3 is oldest in your pattern window):

Body Comparison

Candle# Body Ref#

Choose which other candle you want to compare this one’s body to.

“0” = newest, “1” = previous, “2” = two bars ago, “3” = three bars ago

Candle# Body Op (Operator; >, <, >=, <=, =)

How do you want to compare?

“>” means “greater than” (is bigger than)

“<” means “less than” (is smaller than)

“=” means “equal to”

Candle# Body Mult (Multiplier)

If you want relative comparisons. For example, with Mult=1:

“Candle0 body > Candle2 body x 1” means just “0 is larger than 2.”

“Candle0 body > Candle2 body x 2” means “0 is more than double 2.”

Volume Comparison

Candle# Vol Ref# / Op / Mult

Exact same logic as body, but works on the “Volume” of each candle (how much was traded during that bar).

How to Set Up a Rule (Step by Step Example)

Say you want to mark a Sell every time:

The most recent candle’s real body is BIGGER than the candle 2 bars ago;

The previous candle’s body is also BIGGER than the candle 3 bars ago;

The current candle’s volume is LESS than or equal to the volume of candle 2;

The previous candle’s volume is LESS than or equal to candle 2’s volume;

The candle 3 bars ago’s volume is LESS than or equal to HALF candle 2’s volume.

You’d set:

Pattern Candle Count: 4

Side: "Sell"

Candle0 Body Ref#: 2, Op: “>”, Mult: 1

Candle1 Body Ref#: 3, Op: “>”, Mult: 1

Candle0 Vol Ref#: 2, Op: “<=”, Mult: 1

Candle1 Vol Ref#: 2, Op: “<=”, Mult: 1

Candle3 Vol Ref#: 2, Op: “<=”, Mult: 0.5

All other comparisons (operators) can be left blank if you don’t want to use them!

When these rules are met, a bright red “SELL” label will appear right above the bar matching all your conditions.

Practical Tips & FAQ for Beginners

What does “body” mean?

It’s the “true range” of the candle: the difference between open and close. This ignores wicks for simple setups.

What does “volume” mean?

This is the total trading activity during that candle/bar. Many traders believe that patterns with different volume “meaning” (such as low-volume up bars, or high-volume down bars) signal a meaningful change.

What if nothing shows on chart?

It just means your current rules are rarely or never matched! Try making your comparisons simpler (maybe just 2-body and 2-volume conditions to start).

You can always hit “Reset Settings” to go back to default.

Can I use this for both buying and selling?

YES! You can detect both bullish (Buy) and bearish (Sell) custom conditions; just switch “Signal Side.”

Do I need to know coding?

Not at all! Everything is in simple input panels.

Creative Use Cases, Example Recipes & Troubleshooting

Creative Ways to Use

Spotting Reversals

Example:

Buy when: the newest candle body is LARGER than the previous 3 bars, but ALL volumes are lower than their neighbors.

Why? Sometimes, a big candle with surprisingly low volume after a sequence of small bars can signal a reversal.

Finding Exhaustion Moves

Example:

Sell when: the current bar body is twice as big as two bars ago, but volume is half.

Why? A very big candle with very little volume compared to similar bars may show the move is “running out of steam.”

Custom “Breakout + Confirmation” Patterns

Example:

Buy when:

Candle 0’s body is greater than Candle 2’s by at least 1.5x,

Candle 0’s volume is greater than Candle 1 and Candle 2,

Candle 1’s volume is less than Candle 0.

Why? This could catch strong breakouts but filter out noisy moves.

Multi-bar Bias/Squeeze Filter

Use “Pattern Candle Count: 4”

Set all 4 volume conditions to “<” and each reference to the previous candle.

Now, a BUY or SELL only marks when each bar is “dryer”/less active than the last — a classic squeeze or low-volatility buildup.

Troubleshooting Guide

“I don’t see any Buy/Sell label; is something broken?”

Most likely, your rules are too strict or rare! Try using only two comparisons and leave other “Op” inputs blank as a test.

Double-check you have enough candles on the chart: you need at least as many bars as your pattern count.

“Why does a label appear but not where I expect?”

Remember, the script checks your rules for every NEW candle. The candle “0” is always the most recent, then “1” is one bar back, etc.

Check the color and type chosen: “Signal Side” must be “Buy” for green, “Sell” for red.

“What if I want a more complex pattern?”

Stack conditions! You can demand the body/volume of each candle in your window meet a different rule or all follow the same rule in sequence.

Mini Glossary — For Newcomers

Candle/Bar: Each bar on the chart, shows price movement during a fixed time (e.g., one minute, one hour, one day).

Body: The colored (or filled) part of the candle — the open-to-close price range.

Volume: How much of the asset was actually traded that candle/bar.

Reference Index: When you pick “2” as a reference, it means “the candle two bars ago in the pattern window.”

Operator (“Op”): The math symbol used to compare (>, <, =, etc).

Signal Side: Whether you want to highlight bullish (“Buy”) or bearish (“Sell”) bars.

Tips for Getting More Value

Start Simple—try just one or two conditions at first. See what lights up. Slowly add more logic as you get comfortable.

Watch the chart live as you change settings. The labels update instantly—this makes strategy design fast and visual!

Try flipping your ideas: If a certain pattern doesn’t work for buys, try reversing the direction for possible “sell” setups.

Remember: There is NO wrong idea. This indicator is only limited by your creativity—it’s a “strategy playground.”

Example Quick-Start Recipes

Classic Sell:

4 candles, side = Sell

Candle0 Body > Candle2; Candle1 Body > Candle3

Candle0 Vol <= Candle2; Candle1 Vol <= Candle2; Candle3 Vol <= Candle2 × 0.5

Simple Buy After Pause:

3 candles, side = Buy

Candle0 Body > Candle1; Candle0 Vol > Candle1

All other Ops blank

Low-Volume Pullback for Entry:

4 candles, side = Buy

Candle0 Body > Candle2

Candle0 Vol < Candle1; Candle1 Vol < Candle2; Candle2 Vol < Candle3

Final Words

Think of this as your “pattern lab.” No code, no guesswork—just experiment, see what the market actually gives, and design your own visual rulebook.

If you’re stuck, reset the script to defaults—it’s always safe to start again!

If you want more ready-made “recipes” for different strategies/styles, just ask and I’ll send some more setups for you.

Happy building—and may your edge always be YOUR edge!

RSI Crossover AlertRSI Crossover Alert Indicator - User Guide

The RSI Crossover Alert Indicator is a comprehensive technical analysis tool that detects multiple types of RSI crossovers and generates real-time alerts. It combines traditional RSI analysis with signal lines, divergence detection, and multi-level crossing alerts.

1. Multiple Crossover Detection

- RSI/Signal Line Cross: Signals a primary trend change.

- RSI/Second Signal Cross: Confirmation signals for stronger trends.

- Level Crossings: Crosses of Overbought 70, Oversold 30, and Midline 50.

- Divergence Detection: Hidden and regular divergences for reversal signals.

2. Alert Types

- Alert: RSI > Signal

Description: Bullish momentum is building.

Signal: Consider long positions.

- Alert: RSI < Signal

Description: Bearish momentum is building.

Signal: Consider short positions.

- Alert: RSI > 70

Description: Entering the overbought zone.

Signal: Prepare for a potential reversal.

- Alert: RSI < 30

Description: Entering the oversold zone.

Signal: Watch for a bounce opportunity.

- Alert: RSI crosses 50

Description: A shift in momentum.

Signal: Trend confirmation.

3. Visual Components

- Lines: RSI blue, Signal orange, Second Signal purple

- Histogram: Visualizes momentum by showing the difference between RSI and the Signal line.

- Background Zones: Red overbought, Green oversold

- Markers: Up/down triangles to indicate crossovers.

- Info Table: Real-time RSI values and status.

Strategy 1: Classic Crossover

- Entry Long: RSI crosses above the Signal Line AND RSI is below 50.

- Entry Short: RSI crosses below the Signal Line AND RSI is above 50.

- Take Profit: On the opposite signal.

- Stop Loss: At the recent swing high/low.

Strategy 2: Extreme Zone Reversal

- Entry Long: RSI is below 30 and crosses above the Signal Line.

- Entry Short: RSI is above 70 and crosses below the Signal Line.

- Risk Management: Higher win rate but fewer signals. Use a minimum 2:1 risk-reward ratio.

Strategy 3: Divergence Trading

- Setup: Enable divergence alerts and look for price/RSI divergence. Wait for an RSI crossover for confirmation.

- Entry: Enter on the crossover after the divergence appears. Place the stop loss beyond the starting point of the divergence.

Strategy 4: Multi-Timeframe Confirmation

1. Check the higher timeframe e.g. Daily to identify the main trend.

2. Use the current timeframe e.g. 4H/1H for your entry.

3. Only enter in the direction of the main trend.

4. Use the RSI crossover as the entry trigger.

Optimal Settings by Market

- Forex Major Pairs

RSI Length: 14, Signal Length: 9, Overbought/Oversold: 70/30

- Crypto High Volatility

RSI Length: 10-12, Signal Length: 6-8, Overbought/Oversold: 75/25

- Stocks Trending

RSI Length: 14-21, Signal Length: 9-12, Overbought/Oversold: 70/30

- Commodities

RSI Length: 14, Signal Length: 9, Overbought/Oversold: 80/20

Risk Management Rules

1. Position Sizing: Never risk more than 1-2% on a single trade. Reduce size in ranging markets.

2. Stop Loss Placement: Place stops beyond the recent swing high/low for crossovers. Using an ATR-based stop is also effective.

3. Profit Taking: Take partial profits at a 1:1 risk-reward ratio. Switch to a trailing stop after reaching 2:1.

1. Filtering Signals

- Combine with volume indicators.

- Confirm the trend on a higher timeframe.

- Wait for candlestick pattern confirmation.

2. Avoid Common Mistakes

- Don't trade every single crossover.

- Avoid taking signals against a strong trend.

- Do not ignore risk management.

3. Market Conditions

- Trending Market: Focus on midline 50 crosses.

- Ranging Market: Look for reversals from overbought/oversold levels.

- Volatile Market: Widen the overbought/oversold levels.

- If you get too many false signals:

Increase the signal line period, add other confirmation indicators, or use a higher timeframe.

- If you are missing major moves:

Decrease the RSI length, shorten the signal line period, or check your alert settings.

Recommended Combinations

1. RSI + MACD: For dual momentum confirmation.

2. RSI + Bollinger Bands: For volatility-adjusted signals.

3. RSI + Volume: To confirm the strength of a signal.

4. RSI + Moving Averages: To use as a trend filter.

This indicator provides a comprehensive RSI analysis. Success depends on proper configuration, risk management, and combining signals with the overall market context. Start with the default settings, then optimize based on your trading style and market conditions.

Rolling Volatility BandsMake sure to view it from the 1D candlestick chart.

The Rolling Volatility Bands indicator provides a statistically-driven approach to visualizing expected daily price movements using true volatility calculations employed by professional options traders. Unlike traditional Bollinger Bands which use price standard deviation around a moving average, this indicator calculates actual daily volatility from log returns over customizable rolling periods (20-day and 60-day), then annualizes the volatility using the standard √252 formula before projecting forward-looking probability bands. The 1 Standard Deviation bands represent a ~68% probability zone where price is expected to trade the following day, while the 2 Standard Deviation bands capture ~95% of expected movements. This methodology mirrors how major exchanges calculate expected moves for earnings and FOMC events, making it invaluable for options strategies like iron condors during low-volatility periods (narrow bands) or directional plays when volatility expands. The indicator works on any timeframe while always utilizing daily candle data via security() calls, ensuring consistent volatility calculations regardless of your chart resolution, and includes real-time annualized volatility percentages plus daily expected range statistics for comprehensive market analysis.

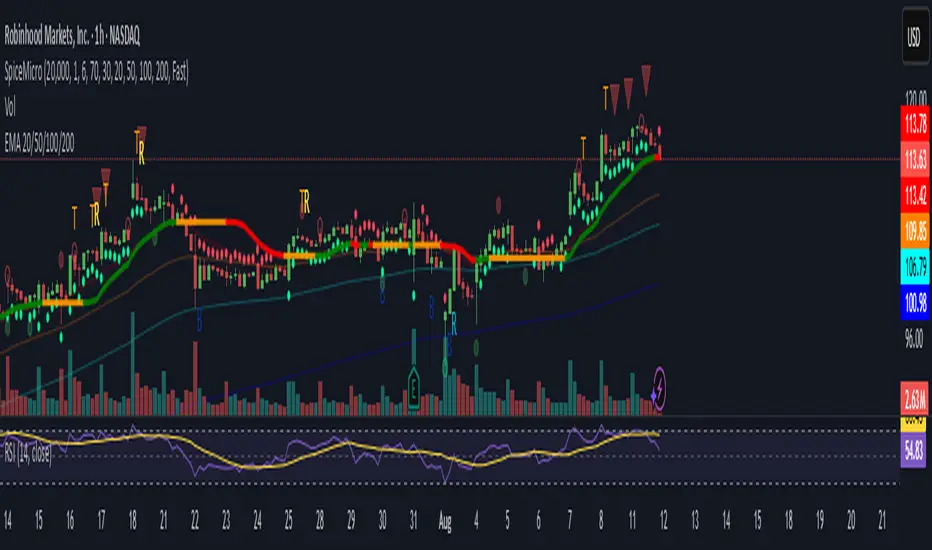

Spice • Micro Suite (T/r & B/r)What it is

A single Pine v5 indicator that stacks:

EMA ribbon + a “special” EMA (11 vs 34) line that flips color on trend.

MTF-RSI “pressure” check with simple up/down arrows.

Bollinger-Band re-entry system with Top/Bottom triggers (T/B) and confirmations (r) in the next N bars.

Classic candlestick add-ons: 3-Line Strike and Leledc exhaustion dots.

Your Micro Dots engine (ATR-based regime + Variable Moving Average filter) + an optional VMA trend line.

Alerts for all the above.

Key signals (what prints on the chart)

EMAs (20/50/100/200): plotted faintly; EMA-34 is drawn and colored by the 11>34 trend.

RSI arrows

Checks RSI(6) on the current TF and (optionally) 5m/15m/30m/1h/4h/1D.

Down arrow: current RSI > 70 and the selected higher TF RSIs are also > 70 (pressure cluster just cooled; barssince(redZone)<2).

Up arrow: current RSI < 30 and selected higher TFs also < 30 (barssince(greenZone)<2).

Bollinger Reversals (your update)

T (Top trigger): first close back inside the upper BB (crossunder(close, upper)).

B (Bottom trigger): first close back inside the lower BB (crossover(close, lower)).

r (Confirm): within the next confirmBars bars (input), price also

closes below the T-bar’s low → top r above bar

closes above the B-bar’s high → bottom r below bar

Bar tinting

Only the T/B trigger bars are tinted (yellow/orange). Everything else stays your normal candle colors (unless you add the optional “trend candles” block I gave you).

3-Line Strike

Prints a small green/red circle when the 3-line strike pattern appears (bull/bear).

Leledc Exhaustion

Calculates a running buy/sell index; prints a small ∘ at major highs/lows when exhaustion conditions hit (major==-1 high, major==1 low).

Micro Dots (your second script, merged)

ATR “micro supertrend” defines regime (up/down).

A fast Variable Moving Average + a simple MA(18) filter.

Green dot below bar when: VMA < price, price > MA(18), regime up, and VMA not pointing down.

Red dot above bar for the bearish mirror.

Separate VMA trend line (length = Fast/Med/Slow) that colors green/red/orange by slope.

Inputs you’ll care about

Top/Bot Reversal → confirmBars (how many bars you allow to confirm the T/B trigger).

RSI Timeframes → toggle which HTFs must agree with the OB/OS condition.

EMAs → show/hide and lengths.

BB → show/hide basis/bands (used for T/B even if hidden).

Micro → show dots, show VMA line, choose intensity (Fast/Med/Slow).

Alerts