Ichimoku BarsThis script follows off the principles of the Ichimoku Cloud indicator. The green zones display optimal time to buy according to the Ichimoku model. The red zones show optimal time to sell according to the Ichimoku model inverse. The yellow zones show where the conversion line meets the base line (potential up or down movement at this point). Feel free to contact me to fix any problems or add additional info.

Tìm kiếm tập lệnh với "Ichimoku Cloud"

Trend Indicators CollectionAnalyses MACD crosses with Ichimoku cloud direction and state

General idea:

- MACD crosses usually point to a change in trend direction and Kumo state and direction often act as a confirmation as well as a trend strength indicator. Using this, the script points out where there were was or can be a point where the trend change may have the strength to carry on.

Buy warnings:

- This warning will be triggered in two ways, both of them only if MACD is above EMA and the current close price is over Kumo:

- Senku span A crosses over Senku B (Kumo turns positive) when MACD is already positive

- MACD turns positive when Kumo is already positive

Sell warnings

- Triggered in two ways:

- Kumo turns negative when the current close price is bellow EMA

- The inverse of the above, the current close price falls bellow EMA when the Kumo is already negative

Trend Indicators Collection (TIC) contains:

- MACD, EMA, ADX, Mass index, Ichimoku Cloud, and Pivot points

- Best suited for monthly charts with 30m bars

Multi StrategyDuring the course of a trade, we can find ourselves changing strategies depending on the market. Instead of using many different templates, I have a simple indicator that clearly says "Buy", "Sell" or "Stay Out". The great thing about this approach, is we instantly observe the majority are in agreement and that decides which way to place our trade.

This indicator includes the following strategies:

- QQE

- Ichimoku using much faster settings.

- Parabolic SAR

- Supertrend

- TTM Oscillator

- The Squeeze strategy

- The Alligator Strategy

Using this indicator is simple, if the lines are mainly green then buy, if mainly red then sell OR don't trade. So...

Green Line - This strategy is in a buy position

Orange or Black Line - This strategy is undecided

Red Line - This strategy is in a sell position

There are also some green and red circles for reference that appear showing when that bar has broken through the Ichimoku cloud.

The trader's approach is simple, when all indicators are green or red, then take the trade. As soon as one indicator changes, then re-evaluate using your normal process, such as price action, to determine whether to close the trade or continue.

I can customise this further or add other strategies, please message me.

Gator RibbonThere's nothing fancy here--I just like the look of this one. And it works pretty well. This started out as the standard Alligator indicator. There I reset all the offsets to 0 and added an Ichimoku Cloudish fill.

Astute observers will notice a fourth line has been added at 34 SMA. It's a bit of a cheat. 34 SMA is the zero line of another classic B. Williams indicator, the Awesome Oscillator. When the green line crosses over 34 SMA, it's quite likely the Awesome Oscillator will have changed sentiment as well. It also makes a nice loose trailing stop loss reference if you're hoping to get into some long trends.

Ichimoku Bollinger BandsThis indicator is a standard set of Bollinger Bands with some functionality borrowed from Ichimoku Kinko Hyo. There's an added SMA (9) that gets shaded green when it's above the basis line of the Bollinger Bands (SMA 20) and turns red when it falls below. No, it's not remotely where the Ichimoku Cloud would appear, but it's a decent trend indicator regardless.

You also get Ichimoku's Lagging Span to help verify the strength of the trend. When the Lagging Span rises above the price history, the trend is up. When the Lagging Span rises above the Bollinger Bands, the uptrend is super strong. And the opposite conditions signal downtrends.

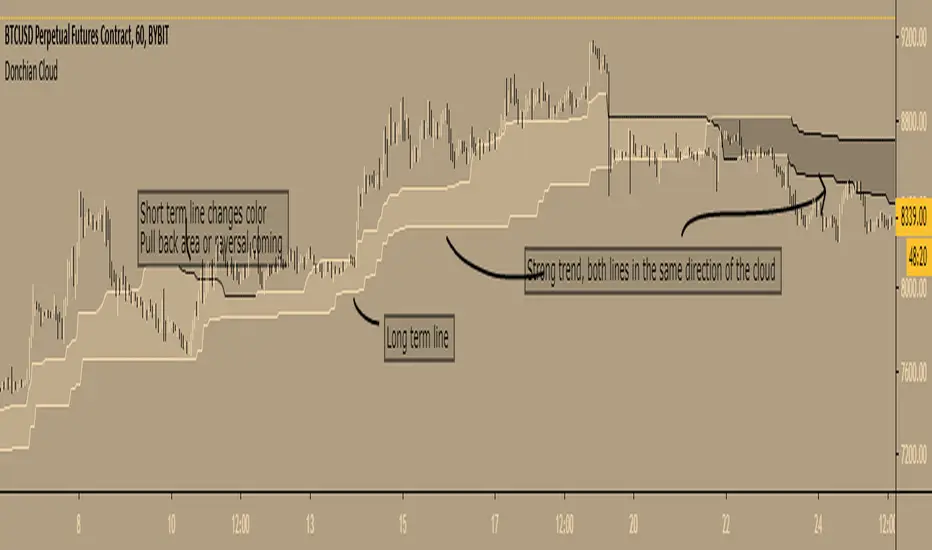

Donchian Cloud - evoA cloud based on the highest high and lowest low of a given period (Donchian), same lines used in Ichimoku Cloud (Conversion line or Base line).

Short term line is based on current time frame, long term line is based on your given multiple of current time frame.

The color of the lines is based on up or down movement.

I stole a piece of code from PineCoders for the multiple time frame:

I have not used this in my trades (yet) so I don't know how good it is, just posting because it looks nice :)

Feel free to share your settings if you can find good ones.

Auto IchimokuA strategy where entries are calculated for you using the Ichimoku Cloud. The IC isn't plotted though, just a heads up.

ULTIMATE ICHIMOKU TRADING SUITEThis is an update of "Uncle Mo's Ultimate Ichimoku V1"

Main features:

2 x Ichimoku Cloud

5 x EMA

2 x MA

1 x HullMA

Williams Fractal

Bollinger Bands - ***NEW***

ATR - ***NEW***

PSAR - ***NEW***

Candlestick Patterns - ***NEW***

Price Action Bars- ***NEW***

List of credits:

@br0qn for the Ichimoku

@RicardoSantos for the Bill Williams Fractal

@EmilianoMesa for the EMAs/MAs

@mohamed982 for the HullMA

@ymaheshreddy4u for the Bollinger Bands

@ChrisMoody for the Price Action Bars and PSAR

@HPotter for the ATR

@repo32 for the Candlestick Patterns

The script is open source and free to use. Feel free to change it around to suit your needs.

***If you copy & paste code from other traders to make your own script, please do remember to give them credit for their amazing work.***

Happy trading!

Crypto optimized Ichimoku and 5 variable SMA / EMAThis script has the option for showing up to 5 moving averages with options to toggle between SMA / EMA. Also includes crypto optimized Ichimoku cloud.

********This script was pieced together from various other's contributions from this site, and I cannot remember who the original authors are*******

Im just combining them to help others with free accounts and limited indicator availability like myself.

I hope this can help someone! Thank you and enjoy.

Crypto optimized Ichimoku and 5 variable SMA / EMAThis script has the option for showing up to 5 moving averages with options to toggle between SMA / EMA. Also includes crypto optimized Ichimoku cloud.

********This script was pieced together from various other's contributions from this site, and I cannot remember who the original authors are*******

Im just combining them to help others with free accounts and limited indicator availability like myself.

I hope this can help someone! Thank you and enjoy.

TSP Ichimoku Clouds x2 MTFDouble Ichimoku

Use a Multiple of current time frame :

15m * 4 = 1h

1h*24 = 1d

Oscars Simple Trend Ichimoku Kijun-senThis super simple Kijun-sen line borrowed from Ichimoku Clouds for trend following.

Ichimoku EMA BandsSome find Ichimoku Clouds bit complicated. This simplified version is combined with EMA Bands may be profitable. Give a try!. I recommend hourly timeframe for good results. Aye! :D

The Rumpy CloudSimilar basic principle to Ichimoku cloud, more sophisticated implementation.

I've exposed cloud width multipliers in the setting in case anyone wants to experiment with them, there are likely to be other widths of significance.

Lots of lines so settings includes easy batch way of altering color settings.

--------------------------------------

If you find it useful please consider a tip/donation :

BTC - 3BMEXEDyWJ58eXUEALYPadbn1wwWKmf6sA

--------------------------------------

Uncle Mo's Ultimate Ichimoku V1Main features:

2 x Ichimoku Cloud

5 x EMA

2 x MA

1 x HullMA

Williams Fractals

Study is based around trader @br0qn 's Ichimoku script.

Credits also go to:

@RicardoSantos for the Bill Williams Fractals

@EmilianoMesa for the EMAs/MAs

@mohamed982 for the HullMA

The script is open source so please feel free to change it around. I'd greatly appreciate it if you could suggest ways to improve it.

Happy trading!

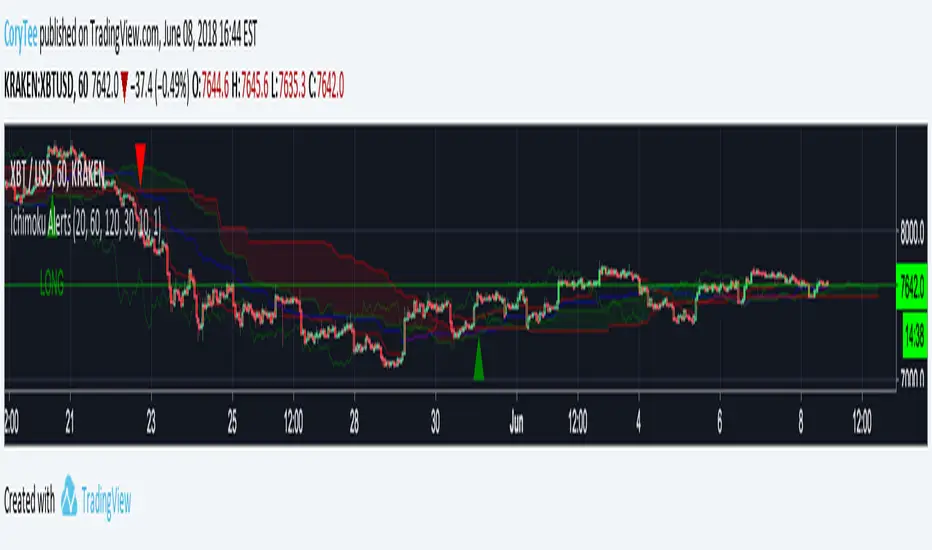

CoryT's Noro's Ichimoku AlertsA few months ago I took Noro's Ichimoku Cloud and used the AV bot template to throw stops on it. I took some code from JustUncleL

to make it not so hideous. Trailing Stops are turned off, stop losses are turned off (you really don't need them with this), and this is currently a Long/Short strategy, the Longs Only and Shorts Only options are broken right now, I'm tired and you guys can either fix it yourselves or deal with it like this for now.

Hint: If you wanna use this as a long-only strategy just have AV close your buy orders whenever a short is triggered.

CoryT's Noro's IchimokuA few months ago I took Noro's Ichimoku Cloud and used the AV bot template to throw stops on it. I took some code from JustUncleL

to make it not so hideous. Trailing Stops are turned off, stop losses are turned off (you really don't need them with this), and this is currently a Long/Short strategy, the Longs Only and Shorts Only options are broken right now, I'm tired and you guys can either fix it yourselves or deal with it like this for now.

Hint: If you wanna use this as a long-only strategy just have AV close your buy orders whenever a short is triggered.

Ichimoku Kumo Twist Strategy with Presets [Krypt]A simple strategy for testing Ichimoku settings used in the following indicator:

Ichimoku OscillatorIchimoku trading signals mapped to an oscillator.

Primarily to indicate bullish and bearish trends.

Forked from:

Crypto-Optimized Ichimoku Cloud [Public]Made public and open since I didn't really do anything unique here.

Uses 'Double Crypto' ichimokou settings, and adds a couple new visual features over regular ichimokou.

Made the leading spans' cloud much more visible, and added a new cloud between the base and conversion lines hinting at the trend as well as resistance/support.