Reversal WaveThis is the type of quantitative system that can get you hated on investment forums, now that the Random Walk Theory is back in fashion. The strategy has simple price action rules, zero over-optimization, and is validated by a historical record of nearly a century on both Gold and the S&P 500 index.

Recommended Markets

SPX (Weekly, Monthly)

SPY (Monthly)

Tesla (Weekly)

XAUUSD (Weekly, Monthly)

NVDA (Weekly, Monthly)

Meta (Weekly, Monthly)

GOOG (Weekly, Monthly)

MSFT (Weekly, Monthly)

AAPL (Weekly, Monthly)

System Rules and Parameters

Total capital: $10,000

We will use 10% of the total capital per trade

Commissions will be 0.1% per trade

Condition 1: Previous Bearish Candle (isPrevBearish) (the closing price was lower than the opening price).

Condition 2: Midpoint of the Body The script calculates the exact midpoint of the body of that previous bearish candle.

• Formula: (Previous Open + Previous Close) / 2.

Condition 3: 50% Recovery (longCondition) The current candle must be bullish (green) and, most importantly, its closing price must be above the midpoint calculated in the previous step.

Once these parameters are met, the system executes a long entry and calculates the exit parameters:

Stop Loss (SL): Placed at the low of the candle that generated the entry signal.

Take Profit (TP): Calculated by projecting the risk distance upward.

• Calculation: Entry Price + (Risk * 1).

Risk:Reward Ratio of 1:1.

About the Profit Factor

In my experience, TradingView calculates profits and losses based on the percentage of movement, which can cause returns to not match expectations. This doesn’t significantly affect trending systems, but it can impact systems with a high win rate and a well-defined risk-reward ratio. It only takes one large entry candle that triggers the SL to translate into a major drop in performance.

For example, you might see a system with a 60% win rate and a 1:1 risk-reward ratio generating losses, even though commissions are under control relative to the number of trades.

My recommendation is to manually calculate the performance of systems with a well-defined risk-reward ratio, assuming you will trade using a fixed amount per trade and limit losses to a fixed percentage.

Remember that, even if candles are larger or smaller in size, we can maintain a fixed loss percentage by using leverage (in cases of low volatility) or reducing the capital at risk (when volatility is high).

Implementing leverage or capital reduction based on volatility is something I haven’t been able to incorporate into the code, but it would undoubtedly improve the system’s performance dramatically, as it would fix a consistent loss percentage per trade, preventing losses from fluctuating with volatility swings.

For example, we can maintain a fixed loss percentage when volatility is low by using the following formula:

Leverage = % of SL you’re willing to risk / % volatility from entry point to exit or SL

And if volatility is high and exceeds the fixed percentage we want to expose per trade (if SL is hit), we could reduce the position size.

For example, imagine we only want to risk 15% per SL on Tesla, where volatility is high and would cause a 23.57% loss. In this case, we subtract 23.57% from 15% (the loss percentage we’re willing to accept per trade), then subtract the result from our usual position size.

23.57% - 15% = 8.57%

Suppose I use $200 per trade.

To calculate 8.57% of $200, simply multiply 200 by 8.57/100. This simple calculation shows that 8.57% equals about $17.14 of the $200. Then subtract that value from $200:

$200 - $17.14 = $182.86

In summary, if we reduced the position size to $182.86 (from the usual $200, where we’re willing to lose 15%), no matter whether Tesla moves up or down 23.57%, we would still only gain or lose 15% of the $200, thus respecting our risk management.

Final Notes

The code is extremely simple, and every step of its development is detailed within it.

If you liked this strategy, which complements very well with others I’ve already published, stay tuned. Best regards.

Tìm kiếm tập lệnh với "META股价历史数据"

Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!

Golden Cross 50/200 EMATrend-following systems are characterized by having a low win rate, yet in the right circumstances (trending markets and higher timeframes) they can deliver returns that even surpass those of systems with a high win rate.

Below, I show you a simple bullish trend-following system with clear execution rules:

System Rules

-Long entries when the 50-period EMA crosses above the 200-period EMA.

-Stop Loss (SL) placed at the lowest low of the 15 candles prior to the entry candle.

-Take Profit (TP) triggered when the 50-period EMA crosses below the 200-period EMA.

Risk Management

-Initial capital: $10,000

-Position size: 10% of capital per trade

-Commissions: 0.1% per trade

Important Note:

In the code, the stop loss is defined using the swing low (15 candles), but the position size is not adjusted based on the distance to the stop loss. In other words, 10% of the equity is risked on each trade, but the actual loss on the trade is not controlled by a maximum fixed percentage of the account — it depends entirely on the stop loss level. This means the loss on a single trade could be significantly higher or lower than 10% of the account equity, depending on volatility.

Implementing leverage or reducing position size based on volatility is something I haven’t been able to include in the code, but it would dramatically improve the system’s performance. It would fix a consistent percentage loss per trade, preventing losses from fluctuating wildly with changes in volatility.

For example, we can maintain a fixed loss percentage when volatility is low by using the following formula:

Leverage = % of SL you’re willing to risk / % volatility from entry point to stop loss

And when volatility is high and would exceed the fixed percentage we want to expose per trade (if the SL is hit), we could reduce the position size accordingly.

Practical example:

Imagine we only want to risk 15% of the position value if the stop loss is triggered on Tesla (which has high volatility), but the distance to the SL represents a potential 23.57% drop. In this case, we subtract the desired risk (15%) from the actual volatility-based loss (23.57%):

23.57% − 15% = 8.57%

Now suppose we normally use $200 per trade.

To calculate 8.57% of $200:

200 × (8.57 / 100) = $17.14

Then subtract that amount from the original position size:

$200 − $17.14 = $182.86

In summary:

If we reduce the position size to $182.86 (instead of the usual $200), even if Tesla moves 23.57% against us and hits the stop loss, we would still only lose approximately 15% of the original $200 position — exactly the risk level we defined. This way, we strictly respect our risk management rules regardless of volatility swings.

I hope this clearly explains the importance of capping losses at a fixed percentage per trade. This keeps risk under control while maintaining a consistent percentage of capital invested per trade — preventing both statistical distortion of the system and the potential destruction of the account.

About the code:

Strategy declaration:

The strategy is named 'Golden Cross 50/200 EMA'.

overlay=true means it will be drawn directly on the price chart.

initial_capital=10000 sets the initial capital to $10,000.

default_qty_type=strategy.percent_of_equity and default_qty_value=10 means each trade uses 10% of available equity.

margin_long=0 indicates no margin is used for long positions (this is likely for simulation purposes only; in real trading, margin would be required).

commission_type=strategy.commission.percent and commission_value=0.1 sets a 0.1% commission per trade.

Indicators:

Calculates two EMAs: a 50-period EMA (ema50) and a 200-period EMA (ema200).

Crossover detection:

bullCross is triggered when the 50-period EMA crosses above the 200-period EMA (Golden Cross).

bearCross is triggered when the 50-period EMA crosses below the 200-period EMA (Death Cross).

Recent swing:

swingLow calculates the lowest low of the previous 15 periods.

Stop Loss:

entryStopLoss is a variable initialized as na (not available) and is updated to the current swingLow value whenever a bullCross occurs.

Entry and exit conditions:

Entry: When a bullCross occurs, the initial stop loss is set to the current swingLow and a long position is opened.

Exit on opposite signal: When a bearCross occurs, the long position is closed.

Exit on stop loss: If the price falls below entryStopLoss while a position is open, the position is closed.

Visualization:

Both EMAs are plotted (50-period in blue, 200-period in red).

Green triangles are plotted below the bar on a bullCross, and red triangles above the bar on a bearCross.

A horizontal orange line is drawn that shows the stop loss level whenever a position is open.

Alerts:

Alerts are created for:Long entry

Exit on bearish crossover (Death Cross)

Exit triggered by stop loss

Favorable Conditions:

Tesla (45-minute timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $12,458.73 or +124.59%

Maximum drawdown: $1,210.40 or 8.29%

Total trades: 107

Winning trades: 27.10% (29/107)

Profit factor: 3.141

Tesla (1-hour timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $7,681.83 or +76.82%

Maximum drawdown: $993.36 or 7.30%

Total trades: 75

Winning trades: 29.33% (22/75)

Profit factor: 3.157

Netflix (45-minute timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,380.73 or +113.81%

Maximum drawdown: $699.45 or 5.98%

Total trades: 134

Winning trades: 36.57% (49/134)

Profit factor: 2.885

Netflix (1-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,689.05 or +116.89%

Maximum drawdown: $844.55 or 7.24%

Total trades: 107

Winning trades: 37.38% (40/107)

Profit factor: 2.915

Netflix (2-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $12,807.71 or +128.10%

Maximum drawdown: $866.52 or 6.03%

Total trades: 56

Winning trades: 41.07% (23/56)

Profit factor: 3.891

Meta (45-minute timeframe)

May 18, 2012 – November 17, 2025

Total net profit: $2,370.02 or +23.70%

Maximum drawdown: $365.27 or 3.50%

Total trades: 83

Winning trades: 31.33% (26/83)

Profit factor: 2.419

Apple (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,232.55 or +80.59%

Maximum drawdown: $581.11 or 3.16%

Total trades: 140

Winning trades: 34.29% (48/140)

Profit factor: 3.009

Apple (1-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $9,685.89 or +94.93%

Maximum drawdown: $374.69 or 2.26%

Total trades: 118

Winning trades: 35.59% (42/118)

Profit factor: 3.463

Apple (2-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,001.28 or +77.99%

Maximum drawdown: $755.84 or 7.56%

Total trades: 67

Winning trades: 41.79% (28/67)

Profit factor: 3.825

NVDA (15-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $11,828.56 or +118.29%

Maximum drawdown: $1,275.43 or 8.06%

Total trades: 466

Winning trades: 28.11% (131/466)

Profit factor: 2.033

NVDA (30-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $12,203.21 or +122.03%

Maximum drawdown: $1,661.86 or 10.35%

Total trades: 245

Winning trades: 28.98% (71/245)

Profit factor: 2.291

NVDA (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $16,793.48 or +167.93%

Maximum drawdown: $1,458.81 or 8.40%

Total trades: 172

Winning trades: 33.14% (57/172)

Profit factor: 2.927

ECG PRICE - mauricioofsousa📉 ECG PRICE – The Price Electrocardiogram

(explained for traders, scientists, and complete beginners)

🔍 1. WHAT IS THE ECG PRICE?

The ECG PRICE protocol is a market-reading system based on the RSI, but with a surgical twist:

👉 You don’t just calculate RSI from price.

👉 You adjust the price using the RSI, and then calculate RSI over this adjusted price.

This creates a filtered, amplified signal that behaves like a heart monitor for price, detecting micro-impulses and subtle market movements long before they show up in the standard RSI.

🧬 2. CORE IDEA

Just like a real ECG amplifies and reveals electrical rhythms hidden inside the heartbeat,

the ECG PRICE amplifies micro-deformations hidden inside the price’s momentum.

It works in three stages:

Compute the regular RSI

Use the RSI to adjust the price (creating an electrocardiographic price)

Compute a second RSI over this modified price

The result is a meta-derived oscillator—more sensitive, more precise, and better at detecting structural changes.

🧩 3. TECHNICAL BREAKDOWN

3.1. First RSI (classic)

The script calculates:

average gains

average losses

relative strength (RS)

and then the standard 0–100 RSI

This is the “normal heart rate monitor” everyone uses.

3.2. Creating the “Adjusted Price”

adjustedPrice = close * (rsi / 100)

This means:

➡️ When RSI is high (strong buying momentum), price is amplified.

➡️ When RSI is low (strong selling momentum), price is compressed.

This converts raw price into a bio-electrical signal, where the price itself is modulated by its own internal momentum.

It’s the financial equivalent of ECG gain adjustment.

3.3. RSI of the Adjusted Price

Now the script calculates a new RSI from this modified price.

That is the actual ECG PRICE.

This second-order oscillator becomes extremely sensitive to:

micro-momentum shifts

early trend fading

volatility shocks

micro-divergences

institutional pressure waves

It reads the electrical pattern behind the price rather than the superficial movement.

🟩🟥 4. Diagnostic Lines of the Protocol

35 (green dotted)

Pre-oversold fatigue zone.

65 (red dotted)

Pre-overbought exhaustion zone.

30 (white solid)

Classic oversold.

70 (white solid)

Classic overbought.

Together they create two diagnostic corridors:

1. Medical corridor (30–70):

Standard RSI clinical range.

2. Electrical corridor (35–65):

The ECG-sensitive zone where micro-shifts appear first.

🧠 5. In Engineering Language (MGO style)

The ECG PRICE is essentially:

A nonlinear second-order oscillator where the RSI feeds back into price, creating a recursive momentum-modulated signal.

It functions like a:

bioinformational modulator

feedback-driven wave processor

impulse amplifier

micro-PID sensitivity enhancer

Very similar to the informational-wave transformations inside the MGO pipeline.

👨⚕️📉 6. Explained for a Total Beginner

Imagine the price is a heart.

The normal RSI shows if the heart is beating fast or slow.

But the ECG PRICE takes that heartbeat…

feeds it back into the heart…

and then measures the new heartbeat.

This creates a much more sensitive exam that detects problems before the normal test would.

💡 7. What It Gives You in Practice

earlier reversal signals

better trend-fatigue detection

clearer micro-divergences

a clean RSI with reduced noise

a smoother momentum curve

advanced behavioral readings before breakouts

It’s an upgrade.

A second-layer RSI that “hears” the inner electrical impulses of price.

Algorithm Predator - ML-liteAlgorithm Predator - ML-lite

This indicator combines four specialized trading agents with an adaptive multi-armed bandit selection system to identify high-probability trade setups. It is designed for swing and intraday traders who want systematic signal generation based on institutional order flow patterns , momentum exhaustion , liquidity dynamics , and statistical mean reversion .

Core Architecture

Why These Components Are Combined:

The script addresses a fundamental challenge in algorithmic trading: no single detection method works consistently across all market conditions. By deploying four independent agents and using reinforcement learning algorithms to select or blend their outputs, the system adapts to changing market regimes without manual intervention.

The Four Trading Agents

1. Spoofing Detector Agent 🎭

Detects iceberg orders through persistent volume at similar price levels over 5 bars

Identifies spoofing patterns via asymmetric wick analysis (wicks exceeding 60% of bar range with volume >1.8× average)

Monitors order clustering using simplified Hawkes process intensity tracking (exponential decay model)

Signal Logic: Contrarian—fades false breakouts caused by institutional manipulation

Best Markets: Consolidations, institutional trading windows, low-liquidity hours

2. Exhaustion Detector Agent ⚡

Calculates RSI divergence between price movement and momentum indicator over 5-bar window

Detects VWAP exhaustion (price at 2σ bands with declining volume)

Uses VPIN reversals (volume-based toxic flow dissipation) to identify momentum failure

Signal Logic: Counter-trend—enters when momentum extreme shows weakness

Best Markets: Trending markets reaching climax points, over-extended moves

3. Liquidity Void Detector Agent 💧

Measures Bollinger Band squeeze (width <60% of 50-period average)

Identifies stop hunts via 20-bar high/low penetration with immediate reversal and volume spike

Detects hidden liquidity absorption (volume >2× average with range <0.3× ATR)

Signal Logic: Breakout anticipation—enters after liquidity grab but before main move

Best Markets: Range-bound pre-breakout, volatility compression zones

4. Mean Reversion Agent 📊

Calculates price z-scores relative to 50-period SMA and standard deviation (triggers at ±2σ)

Implements Ornstein-Uhlenbeck process scoring (mean-reverting stochastic model)

Uses entropy analysis to detect algorithmic trading patterns (low entropy <0.25 = high predictability)

Signal Logic: Statistical reversion—enters when price deviates significantly from statistical equilibrium

Best Markets: Range-bound, low-volatility, algorithmically-dominated instruments

Adaptive Selection: Multi-Armed Bandit System

The script implements four reinforcement learning algorithms to dynamically select or blend agents based on performance:

Thompson Sampling (Default - Recommended):

Uses Bayesian inference with beta distributions (tracks alpha/beta parameters per agent)

Balances exploration (trying underused agents) vs. exploitation (using proven winners)

Each agent's win/loss history informs its selection probability

Lite Approximation: Uses pseudo-random sampling from price/volume noise instead of true random number generation

UCB1 (Upper Confidence Bound):

Calculates confidence intervals using: average_reward + sqrt(2 × ln(total_pulls) / agent_pulls)

Deterministic algorithm favoring agents with high uncertainty (potential upside)

More conservative than Thompson Sampling

Epsilon-Greedy:

Exploits best-performing agent (1-ε)% of the time

Explores randomly ε% of the time (default 10%, configurable 1-50%)

Simple, transparent, easily tuned via epsilon parameter

Gradient Bandit:

Uses softmax probability distribution over agent preference weights

Updates weights via gradient ascent based on rewards

Best for Blend mode where all agents contribute

Selection Modes:

Switch Mode: Uses only the selected agent's signal (clean, decisive)

Blend Mode: Combines all agents using exponentially weighted confidence scores controlled by temperature parameter (smooth, diversified)

Lock Agent Feature:

Optional manual override to force one specific agent

Useful after identifying which agent dominates your specific instrument

Only applies in Switch mode

Four choices: Spoofing Detector, Exhaustion Detector, Liquidity Void, Mean Reversion

Memory System

Dual-Layer Architecture:

Short-Term Memory: Stores last 20 trade outcomes per agent (configurable 10-50)

Long-Term Memory: Stores episode averages when short-term reaches transfer threshold (configurable 5-20 bars)

Memory Boost Mechanism: Recent performance modulates agent scores by up to ±20%

Episode Transfer: When an agent accumulates sufficient results, averages are condensed into long-term storage

Persistence: Manual restoration of learned parameters via input fields (alpha, beta, weights, microstructure thresholds)

How Memory Works:

Agent generates signal → outcome tracked after 8 bars (performance horizon)

Result stored in short-term memory (win = 1.0, loss = 0.0)

Short-term average influences agent's future scores (positive feedback loop)

After threshold met (default 10 results), episode averaged into long-term storage

Long-term patterns (weighted 30%) + short-term patterns (weighted 70%) = total memory boost

Market Microstructure Analysis

These advanced metrics quantify institutional order flow dynamics:

Order Flow Toxicity (Simplified VPIN):

Measures buy/sell volume imbalance over 20 bars: |buy_vol - sell_vol| / (buy_vol + sell_vol)

Detects informed trading activity (institutional players with non-public information)

Values >0.4 indicate "toxic flow" (informed traders active)

Lite Approximation: Uses simple open/close heuristic instead of tick-by-tick trade classification

Price Impact Analysis (Simplified Kyle's Lambda):

Measures market impact efficiency: |price_change_10| / sqrt(volume_sum_10)

Low values = large orders with minimal price impact ( stealth accumulation )

High values = retail-dominated moves with high slippage

Lite Approximation: Uses simplified denominator instead of regression-based signed order flow

Market Randomness (Entropy Analysis):

Counts unique price changes over 20 bars / 20

Measures market predictability

High entropy (>0.6) = human-driven, chaotic price action

Low entropy (<0.25) = algorithmic trading dominance (predictable patterns)

Lite Approximation: Simple ratio instead of true Shannon entropy H(X) = -Σ p(x)·log₂(p(x))

Order Clustering (Simplified Hawkes Process):

Tracks self-exciting event intensity (coordinated order activity)

Decays at 0.9× per bar, spikes +1.0 when volume >1.5× average

High intensity (>0.7) indicates clustering (potential spoofing/accumulation)

Lite Approximation: Simple exponential decay instead of full λ(t) = μ + Σ α·exp(-β(t-tᵢ)) with MLE

Signal Generation Process

Multi-Stage Validation:

Stage 1: Agent Scoring

Each agent calculates internal score based on its detection criteria

Scores must exceed agent-specific threshold (adjusted by sensitivity multiplier)

Agent outputs: Signal direction (+1/-1/0) and Confidence level (0.0-1.0)

Stage 2: Memory Boost

Agent scores multiplied by memory boost factor (0.8-1.2 based on recent performance)

Successful agents get amplified, failing agents get dampened

Stage 3: Bandit Selection/Blending

If Adaptive Mode ON:

Switch: Bandit selects single best agent, uses only its signal

Blend: All agents combined using softmax-weighted confidence scores

If Adaptive Mode OFF:

Traditional consensus voting with confidence-squared weighting

Signal fires when consensus exceeds threshold (default 70%)

Stage 4: Confirmation Filter

Raw signal must repeat for consecutive bars (default 3, configurable 2-4)

Minimum confidence threshold: 0.25 (25%) enforced regardless of mode

Trend alignment check: Long signals require trend_score ≥ -2, Short signals require trend_score ≤ 2

Stage 5: Cooldown Enforcement

Minimum bars between signals (default 10, configurable 5-15)

Prevents over-trading during choppy conditions

Stage 6: Performance Tracking

After 8 bars (performance horizon), signal outcome evaluated

Win = price moved in signal direction, Loss = price moved against

Results fed back into memory and bandit statistics

Trading Modes (Presets)

Pre-configured parameter sets:

Conservative: 85% consensus, 4 confirmations, 15-bar cooldown

Expected: 60-70% win rate, 3-8 signals/week

Best for: Swing trading, capital preservation, beginners

Balanced: 70% consensus, 3 confirmations, 10-bar cooldown

Expected: 55-65% win rate, 8-15 signals/week

Best for: Day trading, most traders, general use

Aggressive: 60% consensus, 2 confirmations, 5-bar cooldown

Expected: 50-58% win rate, 15-30 signals/week

Best for: Scalping, high-frequency trading, active management

Elite: 75% consensus, 3 confirmations, 12-bar cooldown

Expected: 58-68% win rate, 5-12 signals/week

Best for: Selective trading, high-conviction setups

Adaptive: 65% consensus, 2 confirmations, 8-bar cooldown

Expected: Varies based on learning

Best for: Experienced users leveraging bandit system

How to Use

1. Initial Setup (5 Minutes):

Select Trading Mode matching your style (start with Balanced)

Enable Adaptive Learning (recommended for automatic agent selection)

Choose Thompson Sampling algorithm (best all-around performance)

Keep Microstructure Metrics enabled for liquid instruments (>100k daily volume)

2. Agent Tuning (Optional):

Adjust Agent Sensitivity multipliers (0.5-2.0):

<0.8 = Highly selective (fewer signals, higher quality)

0.9-1.2 = Balanced (recommended starting point)

1.3 = Aggressive (more signals, lower individual quality)

Monitor dashboard for 20-30 signals to identify dominant agent

If one agent consistently outperforms, consider using Lock Agent feature

3. Bandit Configuration (Advanced):

Blend Temperature (0.1-2.0):

0.3 = Sharp decisions (best agent dominates)

0.5 = Balanced (default)

1.0+ = Smooth (equal weighting, democratic)

Memory Decay (0.8-0.99):

0.90 = Fast adaptation (volatile markets)

0.95 = Balanced (most instruments)

0.97+ = Long memory (stable trends)

4. Signal Interpretation:

Green triangle (▲): Long signal confirmed

Red triangle (▼): Short signal confirmed

Dashboard shows:

Active agent (highlighted row with ► marker)

Win rate per agent (green >60%, yellow 40-60%, red <40%)

Confidence bars (█████ = maximum confidence)

Memory size (short-term buffer count)

Colored zones display:

Entry level (current close)

Stop-loss (1.5× ATR)

Take-profit 1 (2.0× ATR)

Take-profit 2 (3.5× ATR)

5. Risk Management:

Never risk >1-2% per signal (use ATR-based stops)

Signals are entry triggers, not complete strategies

Combine with your own market context analysis

Consider fundamental catalysts and news events

Use "Confirming" status to prepare entries (not to enter early)

6. Memory Persistence (Optional):

After 50-100 trades, check Memory Export Panel

Record displayed alpha/beta/weight values for each agent

Record VPIN and Kyle threshold values

Enable "Restore From Memory" and input saved values to continue learning

Useful when switching timeframes or restarting indicator

Visual Components

On-Chart Elements:

Spectral Layers: EMA8 ± 0.5 ATR bands (dynamic support/resistance, colored by trend)

Energy Radiance: Multi-layer glow boxes at signal points (intensity scales with confidence, configurable 1-5 layers)

Probability Cones: Projected price paths with uncertainty wedges (15-bar projection, width = confidence × ATR)

Connection Lines: Links sequential signals (solid = same direction continuation, dotted = reversal)

Kill Zones: Risk/reward boxes showing entry, stop-loss, and dual take-profit targets

Signal Markers: Triangle up/down at validated entry points

Dashboard (Configurable Position & Size):

Regime Indicator: 4-level trend classification (Strong Bull/Bear, Weak Bull/Bear)

Mode Status: Shows active system (Adaptive Blend, Locked Agent, or Consensus)

Agent Performance Table: Real-time win%, confidence, and memory stats

Order Flow Metrics: Toxicity and impact indicators (when microstructure enabled)

Signal Status: Current state (Long/Short/Confirming/Waiting) with confirmation progress

Memory Panel (Configurable Position & Size):

Live Parameter Export: Alpha, beta, and weight values per agent

Adaptive Thresholds: Current VPIN sensitivity and Kyle threshold

Save Reminder: Visual indicator if parameters should be recorded

What Makes This Original

This script's originality lies in three key innovations:

1. Genuine Meta-Learning Framework:

Unlike traditional indicator mashups that simply display multiple signals, this implements authentic reinforcement learning (multi-armed bandits) to learn which detection method works best in current conditions. The Thompson Sampling implementation with beta distribution tracking (alpha for successes, beta for failures) is statistically rigorous and adapts continuously. This is not post-hoc optimization—it's real-time learning.

2. Episodic Memory Architecture with Transfer Learning:

The dual-layer memory system mimics human learning patterns:

Short-term memory captures recent performance (recency bias)

Long-term memory preserves historical patterns (experience)

Automatic transfer mechanism consolidates knowledge

Memory boost creates positive feedback loops (successful strategies become stronger)

This architecture allows the system to adapt without retraining , unlike static ML models that require batch updates.

3. Institutional Microstructure Integration:

Combines retail-focused technical analysis (RSI, Bollinger Bands, VWAP) with institutional-grade microstructure metrics (VPIN, Kyle's Lambda, Hawkes processes) typically found in academic finance literature and professional trading systems, not standard retail platforms. While simplified for Pine Script constraints, these metrics provide insight into informed vs. uninformed trading , a dimension entirely absent from traditional technical analysis.

Mashup Justification:

The four agents are combined specifically for risk diversification across failure modes:

Spoofing Detector: Prevents false breakout losses from manipulation

Exhaustion Detector: Prevents chasing extended trends into reversals

Liquidity Void: Exploits volatility compression (different regime than trending)

Mean Reversion: Provides mathematical anchoring when patterns fail

The bandit system ensures the optimal tool is automatically selected for each market situation, rather than requiring manual interpretation of conflicting signals.

Why "ML-lite"? Simplifications and Approximations

This is the "lite" version due to necessary simplifications for Pine Script execution:

1. Simplified VPIN Calculation:

Academic Implementation: True VPIN uses volume bucketing (fixed-volume bars) and tick-by-tick buy/sell classification via Lee-Ready algorithm or exchange-provided trade direction flags

This Implementation: 20-bar rolling window with simple open/close heuristic (close > open = buy volume)

Impact: May misclassify volume during ranging/choppy markets; works best in directional moves

2. Pseudo-Random Sampling:

Academic Implementation: Thompson Sampling requires true random number generation from beta distributions using inverse transform sampling or acceptance-rejection methods

This Implementation: Deterministic pseudo-randomness derived from price and volume decimal digits: (close × 100 - floor(close × 100)) + (volume % 100) / 100

Impact: Not cryptographically random; may have subtle biases in specific price ranges; provides sufficient variation for agent selection

3. Hawkes Process Approximation:

Academic Implementation: Full Hawkes process uses maximum likelihood estimation with exponential kernels: λ(t) = μ + Σ α·exp(-β(t-tᵢ)) fitted via iterative optimization

This Implementation: Simple exponential decay (0.9 multiplier) with binary event triggers (volume spike = event)

Impact: Captures self-exciting property but lacks parameter optimization; fixed decay rate may not suit all instruments

4. Kyle's Lambda Simplification:

Academic Implementation: Estimated via regression of price impact on signed order flow over multiple time intervals: Δp = λ × Δv + ε

This Implementation: Simplified ratio: price_change / sqrt(volume_sum) without proper signed order flow or regression

Impact: Provides directional indicator of impact but not true market depth measurement; no statistical confidence intervals

5. Entropy Calculation:

Academic Implementation: True Shannon entropy requires probability distribution: H(X) = -Σ p(x)·log₂(p(x)) where p(x) is probability of each price change magnitude

This Implementation: Simple ratio of unique price changes to total observations (variety measure)

Impact: Measures diversity but not true information entropy with probability weighting; less sensitive to distribution shape

6. Memory System Constraints:

Full ML Implementation: Neural networks with backpropagation, experience replay buffers (storing state-action-reward tuples), gradient descent optimization, and eligibility traces

This Implementation: Fixed-size array queues with simple averaging; no gradient-based learning, no state representation beyond raw scores

Impact: Cannot learn complex non-linear patterns; limited to linear performance tracking

7. Limited Feature Engineering:

Advanced Implementation: Dozens of engineered features, polynomial interactions (x², x³), dimensionality reduction (PCA, autoencoders), feature selection algorithms

This Implementation: Raw agent scores and basic market metrics (RSI, ATR, volume ratio); minimal transformation

Impact: May miss subtle cross-feature interactions; relies on agent-level intelligence rather than feature combinations

8. Single-Instrument Data:

Full Implementation: Multi-asset correlation analysis (sector ETFs, currency pairs, volatility indices like VIX), lead-lag relationships, risk-on/risk-off regimes

This Implementation: Only OHLCV data from displayed instrument

Impact: Cannot incorporate broader market context; vulnerable to correlated moves across assets

9. Fixed Performance Horizon:

Full Implementation: Adaptive horizon based on trade duration, volatility regime, or profit target achievement

This Implementation: Fixed 8-bar evaluation window

Impact: May evaluate too early in slow markets or too late in fast markets; one-size-fits-all approach

Performance Impact Summary:

These simplifications make the script:

✅ Faster: Executes in milliseconds vs. seconds (or minutes) for full academic implementations

✅ More Accessible: Runs on any TradingView plan without external data feeds, APIs, or compute servers

✅ More Transparent: All calculations visible in Pine Script (no black-box compiled models)

✅ Lower Resource Usage: <500 bars lookback, minimal memory footprint

⚠️ Less Precise: Approximations may reduce statistical edge by 5-15% vs. academic implementations

⚠️ Limited Scope: Cannot capture tick-level dynamics, multi-order-book interactions, or cross-asset flows

⚠️ Fixed Parameters: Some thresholds hardcoded rather than dynamically optimized

When to Upgrade to Full Implementation:

Consider professional Python/C++ versions with institutional data feeds if:

Trading with >$100K capital where precision differences materially impact returns

Operating in microsecond-competitive environments (HFT, market making)

Requiring regulatory-grade audit trails and reproducibility

Backtesting with tick-level precision for strategy validation

Need true real-time adaptation with neural network-based learning

For retail swing/day trading and position management, these approximations provide sufficient signal quality while maintaining usability, transparency, and accessibility. The core logic—multi-agent detection with adaptive selection—remains intact.

Technical Notes

All calculations use standard Pine Script built-in functions ( ta.ema, ta.atr, ta.rsi, ta.bb, ta.sma, ta.stdev, ta.vwap )

VPIN and Kyle's Lambda use simplified formulas optimized for OHLCV data (see "Lite" section above)

Thompson Sampling uses pseudo-random noise from price/volume decimal digits for beta distribution sampling

No repainting: All calculations use confirmed bar data (no forward-looking)

Maximum lookback: 500 bars (set via max_bars_back parameter)

Performance evaluation: 8-bar forward-looking window for reward calculation (clearly disclosed)

Confidence threshold: Minimum 0.25 (25%) enforced on all signals

Memory arrays: Dynamic sizing with FIFO queue management

Limitations and Disclaimers

Not Predictive: This indicator identifies patterns in historical data. It cannot predict future price movements with certainty.

Requires Human Judgment: Signals are entry triggers, not complete trading strategies. Must be confirmed with your own analysis, risk management rules, and market context.

Learning Period Required: The adaptive system requires 50-100 bars minimum to build statistically meaningful performance data for bandit algorithms.

Overfitting Risk: Restoring memory parameters from one market regime to a drastically different regime (e.g., low volatility to high volatility) may cause poor initial performance until system re-adapts.

Approximation Limitations: Simplified calculations (see "Lite" section) may underperform academic implementations by 5-15% in highly efficient markets.

No Guarantee of Profit: Past performance, whether backtested or live-traded, does not guarantee future performance. All trading involves risk of loss.

Forward-Looking Bias: Performance evaluation uses 8-bar forward window—this creates slight look-ahead for learning (though not for signals). Real-time performance may differ from indicator's internal statistics.

Single-Instrument Limitation: Does not account for correlations with related assets or broader market regime changes.

Recommended Settings

Timeframe: 15-minute to 4-hour charts (sufficient volatility for ATR-based stops; adequate bar volume for learning)

Assets: Liquid instruments with >100k daily volume (forex majors, large-cap stocks, BTC/ETH, major indices)

Not Recommended: Illiquid small-caps, penny stocks, low-volume altcoins (microstructure metrics unreliable)

Complementary Tools: Volume profile, order book depth, market breadth indicators, fundamental catalysts

Position Sizing: Risk no more than 1-2% of capital per signal using ATR-based stop-loss

Signal Filtering: Consider external confluence (support/resistance, trendlines, round numbers, session opens)

Start With: Balanced mode, Thompson Sampling, Blend mode, default agent sensitivities (1.0)

After 30+ Signals: Review agent win rates, consider increasing sensitivity of top performers or locking to dominant agent

Alert Configuration

The script includes built-in alert conditions:

Long Signal: Fires when validated long entry confirmed

Short Signal: Fires when validated short entry confirmed

Alerts fire once per bar (after confirmation requirements met)

Set alert to "Once Per Bar Close" for reliability

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

LibVPrfLibrary "LibVPrf"

This library provides an object-oriented framework for volume

profile analysis in Pine Script®. It is built around the `VProf`

User-Defined Type (UDT), which encapsulates all data, settings,

and statistical metrics for a single profile, enabling stateful

analysis with on-demand calculations.

Key Features:

1. **Object-Oriented Design (UDT):** The library is built around

the `VProf` UDT. This object encapsulates all profile data

and provides methods for its full lifecycle management,

including creation, cloning, clearing, and merging of profiles.

2. **Volume Allocation (`AllotMode`):** Offers two methods for

allocating a bar's volume:

- **Classic:** Assigns the entire bar's volume to the close

price bucket.

- **PDF:** Distributes volume across the bar's range using a

statistical price distribution model from the `LibBrSt` library.

3. **Buy/Sell Volume Splitting (`SplitMode`):** Provides methods

for classifying volume into buying and selling pressure:

- **Classic:** Classifies volume based on the bar's color (Close vs. Open).

- **Dynamic:** A specific model that analyzes candle structure

(body vs. wicks) and a short-term trend factor to

estimate the buy/sell share at each price level.

4. **Statistical Analysis (On-Demand):** Offers a suite of

statistical metrics calculated using a "Lazy Evaluation"

pattern (computed only when requested via `get...` methods):

- **Central Tendency:** Point of Control (POC), VWAP, and Median.

- **Dispersion:** Value Area (VA) and Population Standard Deviation.

- **Shape:** Skewness and Excess Kurtosis.

- **Delta:** Cumulative Volume Delta, including its

historical high/low watermarks.

5. **Structural Analysis:** Includes a parameter-free method

(`getSegments`) to decompose a profile into its fundamental

unimodal segments, allowing for modality detection (e.g.,

identifying bimodal profiles).

6. **Dynamic Profile Management:**

- **Auto-Fitting:** Profiles set to `dynamic = true` will

automatically expand their price range to fit new data.

- **Manipulation:** The resolution, price range, and Value Area

of a dynamic profile can be changed at any time. This

triggers a resampling process that uses a **linear

interpolation model** to re-bucket existing volume.

- **Assumption:** Non-dynamic profiles are fixed and will throw

a `runtime.error` if `addBar` is called with data

outside their initial range.

7. **Bucket-Level Access:** Provides getter methods for direct

iteration and analysis of the raw buy/sell volume and price

boundaries of each individual price bucket.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

create(buckets, rangeUp, rangeLo, dynamic, valueArea, allot, estimator, cdfSteps, split, trendLen)

Construct a new `VProf` object with fixed bucket count & range.

Parameters:

buckets (int) : series int number of price buckets ≥ 1

rangeUp (float) : series float upper price bound (absolute)

rangeLo (float) : series float lower price bound (absolute)

dynamic (bool) : series bool Flag for dynamic adaption of profile ranges

valueArea (int) : series int Percentage of total volume to include in the Value Area (1..100)

allot (series AllotMode) : series AllotMode Allocation mode `classic` or `pdf` (default `classic`)

estimator (series PriceEst enum from AustrianTradingMachine/LibBrSt/1) : series LibBrSt.PriceEst PDF model when `model == PDF`. (deflault = 'uniform')

cdfSteps (int) : series int even #sub-intervals for Simpson rule (default 20)

split (series SplitMode) : series SplitMode Buy/Sell determination (default `classic`)

trendLen (int) : series int Look‑back bars for trend factor (default 3)

Returns: VProf freshly initialised profile

method clone(self)

Create a deep copy of the volume profile.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object to copy

Returns: VProf A new, independent copy of the profile

method clear(self)

Reset all bucket tallies while keeping configuration intact.

Namespace types: VProf

Parameters:

self (VProf) : VProf profile object

Returns: VProf cleared profile (chaining)

method merge(self, srcABuy, srcASell, srcRangeUp, srcRangeLo, srcCvd, srcCvdHi, srcCvdLo)

Merges volume data from a source profile into the current profile.

If resizing is needed, it performs a high-fidelity re-bucketing of existing

volume using a linear interpolation model inferred from neighboring buckets,

preventing aliasing artifacts and ensuring accurate volume preservation.

Namespace types: VProf

Parameters:

self (VProf) : VProf The target profile object to merge into.

srcABuy (array) : array The source profile's buy volume bucket array.

srcASell (array) : array The source profile's sell volume bucket array.

srcRangeUp (float) : series float The upper price bound of the source profile.

srcRangeLo (float) : series float The lower price bound of the source profile.

srcCvd (float) : series float The final Cumulative Volume Delta (CVD) value of the source profile.

srcCvdHi (float) : series float The historical high-water mark of the CVD from the source profile.

srcCvdLo (float) : series float The historical low-water mark of the CVD from the source profile.

Returns: VProf `self` (chaining), now containing the merged data.

method addBar(self, offset)

Add current bar’s volume to the profile (call once per realtime bar).

classic mode: allocates all volume to the close bucket and classifies

by `close >= open`. PDF mode: distributes volume across buckets by the

estimator’s CDF mass. For `split = dynamic`, the buy/sell share per

price is computed via context-driven piecewise s(u).

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

offset (int) : series int To offset the calculated bar

Returns: VProf `self` (method chaining)

method setBuckets(self, buckets)

Sets the number of buckets for the volume profile.

Behavior depends on the `isDynamic` flag.

- If `dynamic = true`: Works on filled profiles by re-bucketing to a new resolution.

- If `dynamic = false`: Only works on empty profiles to prevent accidental changes.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

buckets (int) : series int The new number of buckets

Returns: VProf `self` (chaining)

method setRanges(self, rangeUp, rangeLo)

Sets the price range for the volume profile.

Behavior depends on the `dynamic` flag.

- If `dynamic = true`: Works on filled profiles by re-bucketing existing volume.

- If `dynamic = false`: Only works on empty profiles to prevent accidental changes.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

rangeUp (float) : series float The new upper price bound

rangeLo (float) : series float The new lower price bound

Returns: VProf `self` (chaining)

method setValueArea(self, valueArea)

Set the percentage of volume for the Value Area. If the value

changes, the profile is finalized again.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

valueArea (int) : series int The new Value Area percentage (0..100)

Returns: VProf `self` (chaining)

method getBktBuyVol(self, idx)

Get Buy volume of a bucket.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

idx (int) : series int Bucket index

Returns: series float Buy volume ≥ 0

method getBktSellVol(self, idx)

Get Sell volume of a bucket.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

idx (int) : series int Bucket index

Returns: series float Sell volume ≥ 0

method getBktBnds(self, idx)

Get Bounds of a bucket.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

idx (int) : series int Bucket index

Returns:

up series float The upper price bound of the bucket.

lo series float The lower price bound of the bucket.

method getPoc(self)

Get POC information.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

Returns:

pocIndex series int The index of the Point of Control (POC) bucket.

pocPrice. series float The mid-price of the Point of Control (POC) bucket.

method getVA(self)

Get Value Area (VA) information.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

Returns:

vaUpIndex series int The index of the upper bound bucket of the Value Area.

vaUpPrice series float The upper price bound of the Value Area.

vaLoIndex series int The index of the lower bound bucket of the Value Area.

vaLoPrice series float The lower price bound of the Value Area.

method getMedian(self)

Get the profile's median price and its bucket index. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns:

medianIndex series int The index of the bucket containing the Median.

medianPrice series float The Median price of the profile.

method getVwap(self)

Get the profile's VWAP and its bucket index. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns:

vwapIndex series int The index of the bucket containing the VWAP.

vwapPrice series float The Volume Weighted Average Price of the profile.

method getStdDev(self)

Get the profile's volume-weighted standard deviation. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns: series float The Standard deviation of the profile.

method getSkewness(self)

Get the profile's skewness. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns: series float The Skewness of the profile.

method getKurtosis(self)

Get the profile's excess kurtosis. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns: series float The Kurtosis of the profile.

method getSegments(self)

Get the profile's fundamental unimodal segments. Calculates on-demand if stale.

Uses a parameter-free, pivot-based recursive algorithm.

Namespace types: VProf

Parameters:

self (VProf) : VProf The profile object.

Returns: matrix A 2-column matrix where each row is an pair.

method getCvd(self)

Cumulative Volume Delta (CVD) like metric over all buckets.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns:

cvd series float The final Cumulative Volume Delta (Total Buy Vol - Total Sell Vol).

cvdHi series float The running high-water mark of the CVD as volume was added.

cvdLo series float The running low-water mark of the CVD as volume was added.

VProf

VProf Bucketed Buy/Sell volume profile plus meta information.

Fields:

buckets (series int) : int Number of price buckets (granularity ≥1)

rangeUp (series float) : float Upper price range (absolute)

rangeLo (series float) : float Lower price range (absolute)

dynamic (series bool) : bool Flag for dynamic adaption of profile ranges

valueArea (series int) : int Percentage of total volume to include in the Value Area (1..100)

allot (series AllotMode) : AllotMode Allocation mode `classic` or `pdf`

estimator (series PriceEst enum from AustrianTradingMachine/LibBrSt/1) : LibBrSt.PriceEst Price density model when `model == PDF`

cdfSteps (series int) : int Simpson integration resolution (even ≥2)

split (series SplitMode) : SplitMode Buy/Sell split strategy per bar

trendLen (series int) : int Look‑back length for trend factor (≥1)

maxBkt (series int) : int User-defined number of buckets (unclamped)

aBuy (array) : array Buy volume per bucket

aSell (array) : array Sell volume per bucket

cvd (series float) : float Final Cumulative Volume Delta (Total Buy Vol - Total Sell Vol).

cvdHi (series float) : float Running high-water mark of the CVD as volume was added.

cvdLo (series float) : float Running low-water mark of the CVD as volume was added.

poc (series int) : int Index of max‑volume bucket (POC). Is `na` until calculated.

vaUp (series int) : int Index of upper Value‑Area bound. Is `na` until calculated.

vaLo (series int) : int Index of lower value‑Area bound. Is `na` until calculated.

median (series float) : float Median price of the volume distribution. Is `na` until calculated.

vwap (series float) : float Profile VWAP (Volume Weighted Average Price). Is `na` until calculated.

stdDev (series float) : float Standard Deviation of volume around the VWAP. Is `na` until calculated.

skewness (series float) : float Skewness of the volume distribution. Is `na` until calculated.

kurtosis (series float) : float Excess Kurtosis of the volume distribution. Is `na` until calculated.

segments (matrix) : matrix A 2-column matrix where each row is an pair. Is `na` until calculated.

Leveraged ETF Volume Ratio3x/2x Long/short etf pairs for popular tickers, including TSLA, QQQ, META, PLTR... Extreme values indicate bullish/bearish sentiment.

Macro & Earnings Dashboard — NY Fed CalendarMacro & Earnings Dashboard — NY Fed Calendar

This is an overlay indicator designed to provide a quick, real-time overview of the most critical upcoming US economic data releases and corporate earnings reports directly on your TradingView chart. It functions as a dynamic dashboard, removing the need to constantly check external calendars.

Key Features

1. Real-Time Economic Calendar (Bottom-Right Table)

The dashboard tracks the time remaining until the next release of five major, high-impact economic indicators. The data for these dates is pre-loaded directly from the New York Fed Economic Indicators Calendar (currently loaded for October through December 2025).

The tracked events include:

CPI (Consumer Price Index)

PPI (Producer Price Index)

Employment Situation (Non-Farm Payrolls / Unemployment Rate)

Interest Rate Decision (FOMC Meetings)

Consumer Sentiment (University of Michigan Survey)

2. Corporate Earnings Tracker (Top-Right Table)

This table uses TradingView's built-in data to calculate the estimated days remaining until the next Earnings Per Share (EPS) report for a curated list of high-profile NASDAQ tickers:

AAPL, NVDA, GOOG, TSLA, MSFT, AMZN, META

3. Color-Coded Urgency

The "Days" column for both macro and earnings tables uses a traffic light system to instantly communicate how soon the event is:

Red: The event is scheduled for Today or Tomorrow (0–1 day away).

Orange: The event is scheduled for the current week (within 6 days).

Teal: The event is more than a week away.

Gray: The date is currently unavailable or outside the loaded calendar range.

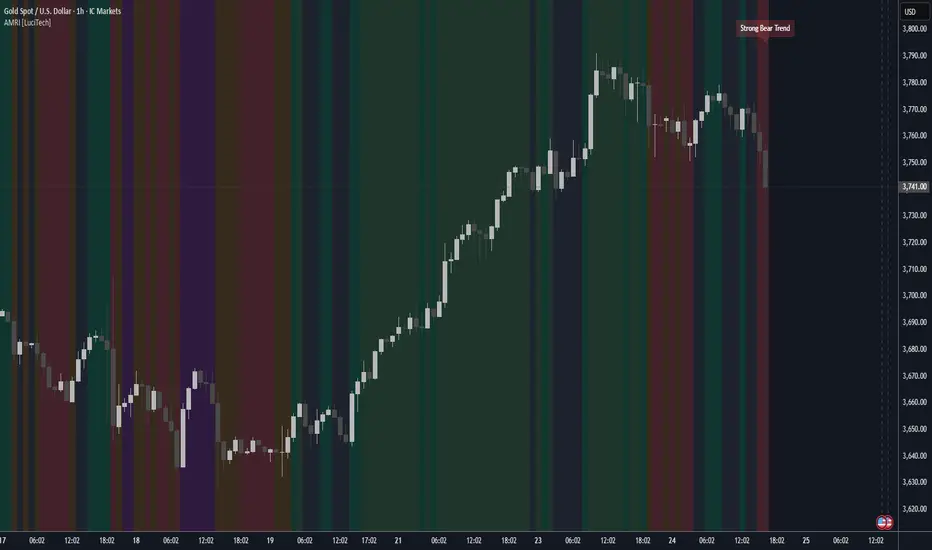

Adaptive Market Regime Identifier [LuciTech]What it Does:

AMRI visually identifies and categorizes the market into six primary regimes directly on your chart using a color-coded background. These regimes are:

-Strong Bull Trend: Characterized by robust upward momentum and low volatility.

-Weak Bull Trend: Indicates upward momentum with less conviction or higher volatility.

-Strong Bear Trend: Defined by powerful downward momentum and low volatility.

-Weak Bear Trend: Suggests downward momentum with less force or increased volatility.

-Consolidation: Periods of low volatility and sideways price action.

-Volatile Chop: High volatility without clear directional bias, often seen during transitions or indecision.

By clearly delineating these states, AMRI helps traders quickly grasp the overarching market context, enabling them to apply strategies best suited for the current conditions (e.g., trend-following in strong trends, range-bound strategies in consolidation, or caution in volatile chop).

How it Works (The Adaptive Edge)

AMRI achieves its adaptive classification by continuously analyzing three core market dimensions, with each component dynamically adjusting to current market conditions:

1.Adaptive Moving Average (KAMA): The indicator utilizes the Kaufman Adaptive Moving Average (KAMA) to gauge trend direction and strength. KAMA is unique because it adjusts its smoothing period based on market efficiency (noise vs. direction). In trending markets, it becomes more responsive, while in choppy markets, it smooths out noise, providing a more reliable trend signal than static moving averages.

2.Adaptive Average True Range (ATR): Volatility is measured using an adaptive version of the Average True Range. Similar to KAMA, this ATR dynamically adjusts its sensitivity to reflect real-time changes in market volatility. This helps AMRI differentiate between calm, ranging markets and highly volatile, directional moves or chaotic periods.

3.Normalized Slope Analysis: The slope of the KAMA is normalized against the Adaptive ATR. This normalization provides a robust measure of trend strength that is relative to the current market volatility, making the thresholds for strong and weak trends more meaningful across different instruments and timeframes.

These adaptive components work in concert to provide a nuanced and responsive classification of the market regime, minimizing lag and reducing false signals often associated with fixed-parameter indicators.

Key Features & Originality:

-Dynamic Regime Classification: AMRI stands out by not just indicating trend or range, but by classifying the type of market regime, offering a higher-level analytical framework. This is a meta-indicator that provides context for all other trading tools.

-Adaptive Core Metrics: The use of KAMA and an Adaptive ATR ensures that the indicator remains relevant and responsive across diverse market conditions, automatically adjusting to changes in volatility and trend efficiency. This self-adjusting nature is a significant advantage over indicators with static lookback periods.

-Visual Clarity: The color-coded background provides an immediate, at-a-glance understanding of the current market regime, reducing cognitive load and allowing for quicker decision-making.

-Contextual Trading: By identifying the prevailing regime, AMRI empowers traders to select and apply strategies that are most effective for that specific environment, helping to avoid costly mistakes of using a trend-following strategy in a ranging market, or vice-versa.

-Originality: While components like KAMA and ATR are known, their adaptive integration into a comprehensive, multi-regime classification system, combined with normalized slope analysis for trend strength, offers a novel approach to market analysis not commonly found in publicly available indicators.

FNGAdataCloseClose prices for FNGA ETF (Dec 2018–May 2025)

The Close prices for FNGA ETF (December 2018 – May 2025) represent the final trading price recorded at the end of each regular U.S. market session (4:00 p.m. Eastern Time) over the entire lifespan of this leveraged exchange-traded note. Initially issued under the ticker FNGU and later rebranded as FNGA in March 2025 before its redemption in May 2025, the product was designed to provide 3x daily leveraged exposure to the MicroSectors FANG+™ Index, which tracks a concentrated group of large-cap technology and tech-enabled growth leaders such as Apple, Amazon, Meta (Facebook), Netflix, and Alphabet (Google).

Close prices are widely regarded as the most important reference point in market data because they establish the official end-of-day valuation of a security. For leveraged products like FNGA, the closing price is especially critical, since it directly determines the reset value for the following trading session. This daily compounding effect means that FNGA’s closing levels often diverged significantly from the long-term performance of its underlying index, creating both opportunities and risks for traders.

FNGAdataLow“Low prices for FNGA ETF (Dec 2018–May 2025)

The Low prices for FNGA ETF (December 2018 – May 2025) capture the lowest trading price reached during each regular U.S. market session over the entire lifespan of this leveraged exchange-traded note. Initially launched under the ticker FNGU, and later rebranded as FNGA in March 2025 before its eventual redemption, the fund was structured to deliver 3x daily leveraged exposure to the MicroSectors FANG+™ Index. This index concentrated on a small basket of leading technology and tech-enabled growth companies such as Meta (Facebook), Amazon, Apple, Netflix, and Alphabet (Google), along with a few other innovators.

The Low price is particularly important in the study of FNGA because it highlights the intraday downside extremes of a highly volatile, leveraged product. Since FNGA was designed to reset leverage daily, its lows often reflected moments of amplified market stress, when declines in the underlying FANG+™ stocks were multiplied through the 3x leverage structure.

FNGAdataHighHigh prices for FNGA ETF (Dec 2018–May 2025)

The High prices for FNGA ETF (December 2018 – May 2025) represent the maximum trading price reached during each regular U.S. market session over the entire trading lifespan of this leveraged exchange-traded note. Originally issued under the ticker FNGU, and later rebranded as FNGA in March 2025 before its redemption, the fund was designed to deliver 3x daily leveraged exposure to the MicroSectors FANG+™ Index. This index focused on a concentrated group of large-cap technology and technology-enabled companies such as Facebook (Meta), Amazon, Apple, Netflix, and Google (Alphabet), along with a few other growth leaders.

The High price data from December 2018 through May 2025 is crucial for understanding how FNGA behaved during intraday trading sessions. Because FNGA was a daily resetting 3x leveraged product, its intraday highs often displayed extreme sensitivity to movements in the underlying FANG+™ stocks, resulting in sharp upward spikes during bullish days and pronounced volatility during broader market rallies.

S&P 500 Weighted Advance Decline LineS&P 500 Weighted Advance Decline Line Indicator

Overview

This indicator creates a market cap weighted advance/decline line for the S&P 500 that tracks breadth based on actual index weights rather than treating all stocks equally. By weighting each stock's contribution according to its true S&P 500 impact, it provides more accurate market breadth analysis and better insights into underlying market strength and potential turning points.

Key Features

Market Cap Weighted: Each stock contributes based on its actual S&P 500 weight

Top 40 Stocks: Covers ~51% of the index with the largest companies

(limited by TradingView's 40 security call maximum for Premium accounts)

Real-Time Updates: Cumulative line shows long-term breadth trends

Visual Indicators: Background coloring, moving average option, and data table

Stock Coverage

Sector Breakdown:

Technology (29.8%) - Dominates the coverage as expected

Financials (5.8%) - Major banking and payment companies

Consumer/Retail (3.7%) - Consumer staples and retail giants

Healthcare (3.2%) - Pharma and healthcare services

Communication (1.97%) - Telecom and tech services

Energy (1.35%) - Oil and gas majors

Industrial (0.9%) - Aerospace and industrial equipment

Other Sectors (4.6%) - Miscellaneous including software and payments

Includes the 40 largest S&P 500 companies by weight, featuring:

Tech Leaders (29.8%): AAPL (7.0%), MSFT (6.5%), NVDA (4.5%), AMZN (3.5%), META (2.5%), GOOGL/GOOG (3.8%), AVGO (1.5%), ORCL (1.22%), AMD (0.51%), plus others

Financials (5.8%): BRK.B (1.8%), JPM (1.2%), V (1.0%), MA (0.8%), BAC (0.63%), WFC (0.46%)

Healthcare (3.2%): LLY (1.2%), UNH (1.2%), JNJ (1.1%), ABBV (0.8%), PG (0.9%)

Consumer/Retail (3.7%): WMT (0.8%), HD (0.8%), COST (0.7%), KO (0.6%), PEP (0.6%), NKE (0.4%)

Communication (1.97%): TMUS (0.47%), CSCO (0.47%), DIS (0.5%), CRM (0.5%)

Energy** (1.35%): XOM (0.8%), CVX (0.55%)

Industrial** (0.9%): GE (0.5%), BA (0.4%)

Other Sectors (4.6%): PLTR (0.65%), ADBE (0.6%), PYPL (0.3%), plus others

How to Interpret

Trend Signals

Rising A/D Line: Broad market strength, more weighted buying than selling

Falling A/D Line: Market weakness, more weighted selling pressure

Flat A/D Line: Balanced market conditions

Divergence Analysis

Bullish Divergence: S&P 500 makes new lows but A/D Line holds higher

Bearish Divergence: S&P 500 makes new highs but A/D Line fails to confirm

Confirmation

Strong trends occur when both price and A/D Line move in the same direction

Weak trends show when price moves but breadth doesn't follow

Settings

Lookback Period: Days for advance/decline comparison (default: 1)

Show Moving Average: Optional trend smoothing

MA Length: Moving average period (default: 20)

Limitations

Covers ~51% of S&P 500 (not complete market breadth)

Optimized for TradingView Premium accounts (40 security limit)

Heavy weighting toward mega-cap technology stocks

Dependent on real-time data quality

Primitive Delta DivergencePrimitive Delta Divergence

This indicator detects volume-price divergences by analyzing the relationship between price direction and volume bias over a rolling lookback period, revealing potential momentum shifts before they become apparent in price action alone.

Instead of relying solely on price movements, you can identify moments when volume sentiment contradicts price direction — a core concept borrowed from footprint chart analysis, adapted for traditional bar charts.

For example, when price moves higher but volume is predominantly bearish, or when price declines while volume shows bullish accumulation.

🔹 How it works

Lookback Period (n) → defines the rolling window for analyzing price and volume relationships

Creates a "meta-candle" from the lookback period, comparing its open vs. close for price bias

Volume classification → separates each bar's volume into bullish (green candles), bearish (red candles), or neutral (doji candles)

Volume bias calculation → generates a continuous score (-1 to +1) representing the directional volume pressure

Plots divergence signals when price direction and volume bias disagree

🔹 Use cases

Spot early momentum exhaustion when price and volume move in opposite directions

Identify potential reversal zones where volume suggests underlying weakness or strength

Enhance entry/exit timing by incorporating volume-based confirmation alongside price action

Apply footprint-style analysis to any timeframe without specialized charting tools

✨ Primitive Delta Divergence reveals the hidden story volume tells about price, uncovering divergences that traditional indicators might miss.

NAS100 Component Sentiment Scanner# NAS100 Component Sentiment Scanner

## 🎯 Overview

The NAS100 Component Sentiment Scanner analyzes the top-weighted stocks in the NASDAQ-100 index to provide real-time bullish/bearish sentiment signals that can help predict NAS100 price movements. This indicator combines multiple technical analysis methods to give traders a comprehensive view of underlying market sentiment.

## 📊 How It Works

The indicator calculates sentiment scores for major NASDAQ-100 components (AAPL, MSFT, NVDA, GOOGL, AMZN, META, TSLA, AVGO, COST, NFLX) using:

- **RSI Analysis**: Identifies overbought/oversold conditions

- **Moving Average Trends**: Compares fast vs slow MA positioning

- **Volume Confirmation**: Validates moves with volume thresholds

- **Price Momentum**: Analyzes recent price direction

- **Market Cap Weighting**: Uses actual NASDAQ-100 weightings for accuracy

## 🚀 Key Features

### Real-Time Sentiment Analysis

- Weighted composite score based on individual stock analysis

- Color-coded sentiment line (Green = Bullish, Red = Bearish)

- Dynamic background coloring for strong signals

### Interactive Data Table

- Shows individual stock scores and signals

- Bullish/Bearish stock count summary

- Customizable position and size

### Smart Signal System

- **Bullish Signals**: Green triangle up when sentiment crosses threshold

- **Bearish Signals**: Red triangle down when sentiment falls below threshold

- **Alert Conditions**: Automatic notifications for signal changes

## ⚙️ Customization Options

### Technical Analysis Settings

- **RSI Period**: Adjust lookback period (default: 14)

- **RSI Levels**: Set overbought/oversold thresholds

- **Moving Averages**: Configure fast/slow MA periods

- **Volume Threshold**: Set volume confirmation multiplier

### Signal Thresholds

- **Bullish/Bearish Levels**: Customize trigger points

- **Strong Signal Levels**: Set extreme sentiment thresholds

- Fine-tune sensitivity to market conditions

### Display Options

- **Toggle Table**: Show/hide sentiment data table

- **Table Position**: 6 position options (Top/Bottom/Middle + Left/Right)

- **Table Size**: Choose from Tiny, Small, Normal, or Large

- **Background Colors**: Enable/disable signal backgrounds

- **Signal Arrows**: Show/hide buy/sell indicators

### Stock Selection

- **Individual Control**: Enable/disable any of the 10 major stocks

- **Dynamic Weighting**: Automatically adjusts calculations based on selected stocks

- **Flexible Analysis**: Focus on specific sectors or market leaders

## 📈 How to Use

### 1. Basic Setup

1. Add the indicator to your NAS100 chart

2. Default settings work well for most traders

3. Observe the sentiment line and signals

### 2. Signal Interpretation

- **Score > 30**: Bullish bias for NAS100

- **Score > 50**: Strong bullish signal

- **Score -30 to 30**: Neutral/consolidation

- **Score < -30**: Bearish bias for NAS100

- **Score < -50**: Strong bearish signal

### 3. Trading Strategies

**Trend Following:**

- Buy NAS100 when bullish signals appear

- Sell/short when bearish signals trigger

- Use background colors for quick visual confirmation

**Divergence Trading:**

- Watch for sentiment/price divergences

- Strong sentiment with weak NAS100 price = potential breakout

- Weak sentiment with strong NAS100 price = potential reversal

**Consensus Trading:**

- Monitor bullish/bearish stock counts in table

- 8+ stocks aligned = strong directional bias

- Mixed signals = wait for clearer consensus

### 4. Advanced Usage

- Combine with your existing NAS100 trading strategy

- Use multiple timeframes for confirmation

- Adjust thresholds based on market volatility

- Focus on specific stocks by disabling others

## 🔔 Alert Setup

The indicator includes built-in alert conditions:

1. Go to TradingView Alerts

2. Select "NAS100 Component Sentiment Scanner"

3. Choose from available alert types:

- NAS100 Bullish Signal

- NAS100 Bearish Signal

- Strong Bullish Consensus

- Strong Bearish Consensus

## 💡 Pro Tips

### Optimization

- **High Volatility**: Increase signal thresholds (±40, ±60)

- **Low Volatility**: Decrease thresholds (±20, ±40)

- **Day Trading**: Use smaller table, focus on real-time signals

- **Swing Trading**: Enable background colors, larger thresholds

### Best Practices

- Don't use as a standalone system - combine with price action

- Check individual stock table for context

- Monitor during market open for most reliable signals

- Consider earnings seasons for individual stock impacts

### Market Conditions

- **Trending Markets**: Higher accuracy, use with trend following

- **Ranging Markets**: Watch for false signals, increase thresholds

- **News Events**: Individual stock news can skew sentiment temporarily

## 🎨 Visual Guide

- **Green Line Above Zero**: Bullish sentiment building

- **Red Line Below Zero**: Bearish sentiment building

- **Background Color Changes**: Strong signal confirmation

- **Triangle Arrows**: Entry/exit signal points

- **Table Colors**: Quick sentiment overview

## ⚠️ Important Notes

- This indicator analyzes component stocks, not NAS100 directly

- Market cap weightings approximate real NASDAQ-100 weightings