High & Low Of Custom Session - Breakout True Open [cognyto]This indicator is based on the High & Low Of Custom Session - OpeningRange Breakout (Expo) created by Zeiierman.

It adds new functionality and enhances existing settings, targeting ES, NQ, and YM:

Manages session defaults to 12:00 to 13:00

New true opening fully customizable (default 13:00)

Manages timeframe visualization (default 15m and below)

Manages session draw length until the end of the current session (default NY)

Manages previous sessions, allowing the to be hidden

Improves timezone selection (default NY)

Following the strategy called Paradox detailed by DayTradingRauf, it works with indices like ES, NQ, and YM.

The rules consider three possible profiles:

First

AM session as consolidation (08:00-12:00)

Lunch hour range as consolidation (less than 100 points)

PM session breaking either side of the session range

Second

AM session trending lower (08:00-12:00)

Lunch hour range as consolidation (less than 100 points)

PM session trending higher

Third

AM session trending higher (08:00-12:00)

Lunch hour range as consolidation (less than 100 points)

PM session trending lower

After the session ends, the opening price at 13:00 is automatically drawn as it is a key point for the entry strategy.

The strategy can be monitored using a 5-minute or 15-minute timeframe as follows:

- Wait for a liquidity hunt (either the high or low of the lunch session range or AM is taken).

- If liquidity is taken, switch to the 1-minute timeframe and wait for a CISD (change in the state of delivery), where the price closes below an OB, or consider a breaker block or iFVG to enter the trade.

- Bullish entries should happen below the opening price at 13:00, and bearish entries should happen above.

- Consider a 1:2 reward ratio. However, runners can target the opposite side of the range that was not yet taken.

This indicator is for informational purposes only and you should not rely on any information it provides as legal, tax, investment, financial or other advice. Nothing provided by this indicator constitutes a solicitation, recommendation, endorsement or offer by cognyto or any third party service provider to buy or sell any securities or other financial instruments in this or any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.

Tìm kiếm tập lệnh với "TAKE"

TrailingTakeProfit exampleQuite recently I came upon a concept of Trailing Take Profit and I couldn't find a PineScript which implements it for the fastest possible execution, so here it is :)

Everybody knows Trailing StopLoss - an invisible mechanism follows the price and exits the trade once the price retreats too much from its recent most extended favourable value. Trailing TakeProfit does the similar thing, but at the opposite end - the trade gets closed if a price moves too well, in too favourable extent.

Why close the trade if it is going so good? Well, whatever goes up, must go down and vice versa. It is expected, that after fast rally a market will soon fall and after a dump it will go up. So Trailing TakeProfit's role is to secure profits.

But how does Trailing TakeProfit differ from the standard one? "Trailing" means, the exit level is moving. Its role is to be executed only after a rapid favourable move within 1-2 candles, not more. We never know when a rapid move happens, but when it does, we wanna catch those pips and quickly exit without looking back.

Visually Trailing TakeProfit levels are... bands. In this script example these are ATR multiplied bands (aka Keltner Channel), but they could also be Bollinger Bands or something else.

The code is simple just to focus on this single functionality, so you can quickly copy-paste it into your script. Entries are triggered by default SMA crosses.

P.S. I wouldn't be myself, if I didn't add alert messages compatible with the syntax of recently revamped TradingConnector - both in the code already and in the table showing them.

All Candlestick Patterns on Backtest [By MUQWISHI]▋ INTRODUCTION :

The “All Candlestick Patterns on Backtest” indicator generates a table that offers a clear visualization of the historical return percentages for each candlestick pattern strategy over a specified time period. This table serves as an organized resource, serving as a launching point for in-depth research into candle formations. It may help to rectify any misconceptions surrounding candlestick patterns, refine trading approaches, and it could be foundation to make informed decisions in trading journey.

_______________________

▋ OVERVIEW:

_______________________

▋ CREDIT:

Credit to public technical “*All Candlestick Patterns*” indicator.

_______________________

▋ TABLE:

_______________________

▋ CHART:

_______________________

▋ INDICATOR SETTINGS:

#Section One: Table Setting

#Section Two: Backtest Setting

(1) Backtest Starting Period.

Note: If the datetime of the first candle on the chart is after the entreated datetime, the calculation will start from the first candle on the chart.

(2) Initial Equity ($).

(3) Leverage: Current Equity x Leverage Value.

(4) Entry Mode:

- “At Close”: Execute entry order as soon as the candle confirmed.

- “Breakout High (Low for Short)”: Stop limit buy order, entry order will be executed as soon as the next candle breakout the high of last pattern’s candle (low for short)

(5) Cancel Entry Within Bars: This option is applicable with {Entry Mode = Breakout High (Low for Short)}, to cancel the Entry Order if it's not executed within certain selected number of bars.

(6) Stoploss Range: the range refers to high of pattern - low of pattern.

(7) Risk:Reward: the calculation of risk:reward range start from entry price level. For example: A pattern triggered with range 10 points, and entry price is 100.

- For 1:1~risk:reward would the stoploss at 90 and takeprofit at 110.

- For 1:3~risk:reward would the stoploss at 90 and takeprofit at 130.

#Section Three: Technical & Candle Patterns

_______________________

▋ Comments:

This table was developed for research and educational purposes.

Candlestick patterns are almost similar as seen in “*All Candlestick Patterns*” indicator.

The table results should not be taken as a major concept to build a trading decision.

Personally, I see candlestick patterns as a means to comprehend the psychology of the market, and help to follow the price action.

Please let me know if you have any questions.

Thank you.

Ehlers Two-Pole Predictor [Loxx]Ehlers Two-Pole Predictor is a new indicator by John Ehlers . The translation of this indicator into PineScript™ is a collaborative effort between @cheatcountry and I.

The following is an excerpt from "PREDICTION" , by John Ehlers

Niels Bohr said “Prediction is very difficult, especially if it’s about the future.”. Actually, prediction is pretty easy in the context of technical analysis . All you have to do is to assume the market will behave in the immediate future just as it has behaved in the immediate past. In this article we will explore several different techniques that put the philosophy into practice.

LINEAR EXTRAPOLATION

Linear extrapolation takes the philosophical approach quite literally. Linear extrapolation simply takes the difference of the last two bars and adds that difference to the value of the last bar to form the prediction for the next bar. The prediction is extended further into the future by taking the last predicted value as real data and repeating the process of adding the most recent difference to it. The process can be repeated over and over to extend the prediction even further.

Linear extrapolation is an FIR filter, meaning it depends only on the data input rather than on a previously computed value. Since the output of an FIR filter depends only on delayed input data, the resulting lag is somewhat like the delay of water coming out the end of a hose after it supplied at the input. Linear extrapolation has a negative group delay at the longer cycle periods of the spectrum, which means water comes out the end of the hose before it is applied at the input. Of course the analogy breaks down, but it is fun to think of it that way. As shown in Figure 1, the actual group delay varies across the spectrum. For frequency components less than .167 (i.e. a period of 6 bars) the group delay is negative, meaning the filter is predictive. However, the filter has a positive group delay for cycle components whose periods are shorter than 6 bars.

Figure 1

Here’s the practical ramification of the group delay: Suppose we are projecting the prediction 5 bars into the future. This is fine as long as the market is continued to trend up in the same direction. But, when we get a reversal, the prediction continues upward for 5 bars after the reversal. That is, the prediction fails just when you need it the most. An interesting phenomenon is that, regardless of how far the extrapolation extends into the future, the prediction will always cross the signal at the same spot along the time axis. The result is that the prediction will have an overshoot. The amplitude of the overshoot is a function of how far the extrapolation has been carried into the future.

But the overshoot gives us an opportunity to make a useful prediction at the cyclic turning point of band limited signals (i.e. oscillators having a zero mean). If we reduce the overshoot by reducing the gain of the prediction, we then also move the crossing of the prediction and the original signal into the future. Since the group delay varies across the spectrum, the effect will be less effective for the shorter cycles in the data. Nonetheless, the technique is effective for both discretionary trading and automated trading in the majority of cases.

EXPLORING THE CODE

Before we predict, we need to create a band limited indicator from which to make the prediction. I have selected a “roofing filter” consisting of a High Pass Filter followed by a Low Pass Filter. The tunable parameter of the High Pass Filter is HPPeriod. Think of it as a “stone wall filter” where cycle period components longer than HPPeriod are completely rejected and cycle period components shorter than HPPeriod are passed without attenuation. If HPPeriod is set to be a large number (e.g. 250) the indicator will tend to look more like a trending indicator. If HPPeriod is set to be a smaller number (e.g. 20) the indicator will look more like a cycling indicator. The Low Pass Filter is a Hann Windowed FIR filter whose tunable parameter is LPPeriod. Think of it as a “stone wall filter” where cycle period components shorter than LPPeriod are completely rejected and cycle period components longer than LPPeriod are passed without attenuation. The purpose of the Low Pass filter is to smooth the signal. Thus, the combination of these two filters forms a “roofing filter”, named Filt, that passes spectrum components between LPPeriod and HPPeriod.

Since working into the future is not allowed in EasyLanguage variables, we need to convert the Filt variable to the data array XX. The data array is first filled with real data out to “Length”. I selected Length = 10 simply to have a convenient starting point for the prediction. The next block of code is the prediction into the future. It is easiest to understand if we consider the case where count = 0. Then, in English, the next value of the data array is equal to the current value of the data array plus the difference between the current value and the previous value. That makes the prediction one bar into the future. The process is repeated for each value of count until predictions up to 10 bars in the future are contained in the data array. Next, the selected prediction is converted from the data array to the variable “Prediction”. Filt is plotted in Red and Prediction is plotted in yellow.

The Predict Extrapolation indicator is shown below for the Emini S&P Futures contract using the default input parameters. Filt is plotted in red and Predict is plotted in yellow. The crossings of the Predict and Filt lines provide reliable buy and sell timing signals. There is some overshoot for the shorter cycle periods, for example in February and March 2021, but the only effect is a late timing signal. Further reducing the gain and/or reducing the BarsFwd inputs would provide better timing signals during this period.

Figure 2. Predict Extrapolation Provides Reliable Timing Signals

I have experimented with other FIR filters for predictions, but found none that had a significant advantage over linear extrapolation.

MESA

MESA is an acronym for Maximum Entropy Spectral Analysis. Conceptually, it removes spectral components until the residual is left with maximum entropy. It does this by forming an all-pole filter whose order is determined by the selected number of coefficients. It maximally addresses the data within the selected window and ignores all other data. Its resolution is determined only by the number of filter coefficients selected. Since the resulting filter is an IIR filter, a prediction can be formed simply by convolving the filter coefficients with the data. MESA is one of the few, if not the only way to practically determine the coefficients of a higher order IIR filter. Discussion of MESA is beyond the scope of this article.

TWO POLE IIR FILTER

While the coefficients of a higher order IIR filter are difficult to compute without MESA, it is a relatively simple matter to compute the coefficients of a two pole IIR filter.

(Skip this paragraph if you don’t care about DSP) We can locate the conjugate pole positions parametrically in the Z plane in polar coordinates. Let the radius be QQ and the principal angle be 360 / P2Period. The first order component is 2*QQ*Cosine(360 / P2Period) and the second order component is just QQ2. Therefore, the transfer response becomes:

H(z) = 1 / (1 - 2*QQ*Cosine(360 / P2Period)*Z-1 + QQ2*Z-2)

By mixing notation we can easily convert the transfer response to code.

Output / Input = 1 / (1 - 2*QQ*Cosine(360 / P2Period)* + QQ2* )

Output - 2*QQ*Cosine(360 / P2Period)*Output + QQ2*Output = Input

Output = Input + 2*QQ*Cosine(360 / P2Period)*Output - QQ2*Output

The Two Pole Predictor starts by computing the same “roofing filter” design as described for the Linear Extrapolation Predictor. The HPPeriod and LPPeriod inputs adjust the roofing filter to obtain the desired appearance of an indicator. Since EasyLanguage variables cannot be extended into the future, the prediction process starts by loading the XX data array with indicator data up to the value of Length. I selected Length = 10 simply to have a convenient place from which to start the prediction. The coefficients are computed parametrically from the conjugate pole positions and are normalized to their sum so the IIR filter will have unity gain at zero frequency.

The prediction is formed by convolving the IIR filter coefficients with the historical data. It is easiest to see for the case where count = 0. This is the initial prediction. In this case the new value of the XX array is formed by successively summing the product of each filter coefficient with its respective historical data sample. This process is significantly different from linear extrapolation because second order curvature is introduced into the prediction rather than being strictly linear. Further, the prediction is adaptive to market conditions because the degree of curvature depends on recent historical data. The prediction in the data array is converted to a variable by selecting the BarsFwd value. The prediction is then plotted in yellow, and is compared to the indicator plotted in red.

The Predict 2 Pole indicator is shown above being applied to the Emini S&P Futures contract for most of 2021. The default parameters for the roofing filter and predictor were used. By comparison to the Linear Extrapolation prediction of Figure 2, the Predict 2 Pole indicator has a more consistent prediction. For example, there is little or no overshoot in February or March while still giving good predictions in April and May.

Input parameters can be varied to adjust the appearance of the prediction. You will find that the indicator is relatively insensitive to the BarsFwd input. The P2Period parameter primarily controls the gain of the prediction and the QQ parameter primarily controls the amount of prediction lead during trending sections of the indicator.

TAKEAWAYS

1. A more or less universal band limited “roofing filter” indicator was used to demonstrate the predictors. The HPPeriod input parameter is used to control whether the indicator looks more like a trend indicator or more like a cycle indicator. The LPPeriod input parameter is used to control the smoothness of the indicator.

2. A linear extrapolation predictor is formed by adding the difference of the two most recent data bars to the value of the last data bar. The result is considered to be a real data point and the process is repeated to extend the prediction into the future. This is an FIR filter having a one bar negative group delay at zero frequency, but the group delay is not constant across the spectrum. This variable group delay causes the linear extrapolation prediction to be inconsistent across a range of market conditions.

3. The degree of prediction by linear extrapolation can be controlled by varying the gain of the prediction to reduce the overshoot to be about the same amplitude as the peak swing of the indicator.

4. I was unable to experimentally derive a higher order FIR filter predictor that had advantages over the simple linear extrapolation predictor.

5. A Two Pole IIR predictor can be created by parametrically locating the conjugate pole positions.

6. The Two Pole predictor is a second order filter, which allows curvature into the prediction, thus mitigating overshoot. Further, the curvature is adaptive because the prediction depends on previously computed prediction values.

7. The Two Pole predictor is more consistent over a range of market conditions.

ADDITIONS

Loxx's Expanded source types:

Library for expanded source types:

Explanation for expanded source types:

Three different signal types: 1) Prediction/Filter crosses; 2) Prediction middle crosses; and, 3) Filter middle crosses.

Bar coloring to color trend.

Signals, both Long and Short.

Alerts, both Long and Short.

Rob Booker - ADX Breakout updated to pinescript V5Rob Booker - ADX Breakout. The strategy remains unchanged but the code has been updated to pinescript V5. This enables compatibility with all new Tradingview features. Additonally, indicators have been made more easily visible, default cash settings as well as input descriptions have been added.

Rob Booker - ADX Breakout: (Directly taken from the official Tradingview V1 version of the script)

Definition

Rob Booker’s Average Directional Index (ADX) Breakout is a trend strength indicator that affirms the belief that trading in the direction of a trend and continuing to follow its pull is more profitable for traders, while simultaneously reducing risk.

History

ADX was traditionally used and developed to determine a price’s trend strength. It is commonly known as a tool from the arsenal of Rob Booker, experienced entrepreneur and currency trader.

Calculations

Calculations for the ADX Breakout indicator are based on a moving average of price range expansion over a specific period of time. By default, the setting rests at 14 bars, this however is not mandatory, as other periods are routinely used for analysis as well.

Takeaways

The ADX line is used to measure and determine the strength of a trend, and so the direction of this line and its interpretation are crucial in a trader’s analysis. As the ADX line rises, a trend increases in strength and price moves in the trend’s direction. Similarly, if the ADX line is falling, a trend decreases in strength and price then enters a period of consolidation, or retracement.

Traditionally, the ADX is plotted on the chart as a single line that consists of values that range from 0-100. The line is non-directional, meaning that it always measures trend strength regardless of the position of a price’s trend (up or down). Essentially, ADX quantifies trend strength by presenting in both uptrends and downtrends of the line.

What to look for

The values associated with the ADX line help traders determine the most profitable trades and where risk lies in the current trend. It is important to know how to quantify trend strength and distinguish between the varying values in order to understand the differences in trending vs. non-trending conditions. Let’s take a look at ADX values and what they mean for trend strength.

ADX Value:

0-25: Signifies an absent of weak trend

25-50: Signifies a strong trend

50-75: Signifies a very strong trend

75-100: Signifies an extremely strong trend

To delve into this a bit further, let’s assess the meaning of ADX if it is valued below 25. If the ADX line remains below 25 for more than 30 or so bars, price then enters range conditions, making price patterns more distinguishable and visible to traders. Price will move up and down between resistance and support in order to determine selling and buying interest and may then eventually break out into a trend or pattern.

The way in which ADX peaks, ebs, and flows is also a signifier of its overall pattern and trend momentum. The line can clearly indicate to the trader when trend strength is strong versus when it is weak. When ADX peaks are pictured as higher, it points towards an increase in trend momentum. If ADX peaks are pictured as lower - you guessed it - it points towards a decrease in trend momentum. A trend of lower ADX peaks could be a warning for traders to watch prices and manage and assess risk before a trade gets out of hand. Similarly, whenever there is a sudden move that seems out of place or a change in trend character that goes against what you’ve seen before, this should be a clear sign to watch prices and assess risk.

Summary

The ADX Breakout indicator is a trend strength indicator that analyzes price movements relative to trend strength to signal a user when is best for a trade and when is best to manage risk and assess patterns. As long as a trader recognizes strong trends and assesses the risk of each trade properly, they should have no problem using this indicator and utilizing it to work in their favor. In addition, the ADX helps identify trending conditions, but while doing so, also aids traders in finding strong trends to trade. The indicator can even alert traders to specific changes in trend momentum, allowing them to be primed for risk management.

OBV MA StrategyThe On Balance Volume + Moving Average Strategy

Parameters: 1H candles, ETHUSDT on BINANCEUS, commission percent uses Binance's maker/taker fees of 0.075%

Strategy: I create a 30 day moving average of the On Balance Volume "obvSma = ta.sma(ta.obv, 30)." Then I use the following buy conditions:

OBV crosses above the OBV moving average

The obv drops x% below the OBV moving average (buy a dip)

The OBV moving average is rising, the OBV is greater than the OBV moving average and the OBV is rising

The first buy condition is attempting to buy into an uptrend. When the OBV rises above the OBV moving average, people are buying and it's a good time to enter the trade.

The idea behind the second buy condition is to buy a dip so make sure you are careful to not set it too shallow or you'll end up buying the dip before the dip before the dip. :) I recommend 10% or more.

The third buy condition is there in case our trailing stop takes us out of a trade but the trend is still rising, we don't want to miss out on that profit so if the OBV is above the OBV moving average, the average is rising and the OBV is rising, we are likely in the middle of an uptrend and we should buy in.

Gap RiderThis Indicator allows you to make statistics on the performance of any underlying on the days in which an opening gap occurs.

Specifically, the indicator was designed for "0 dte" options trades. In fact, it is possible to find parameters that give a good statistical advantage by opening a spread in the direction of the gap, creating a trade that has a risk-return ratio of 1: 1.

The indicator shows flags on the graph (green in case of gap up, red in case of gap down) and colored boxes (green in case the stock closed in the direction of the gap, red in case the stock closed in the opposite direction to the gap, yellow in the event that the stock closed at a distance that did not allow the spread in options to close in maximum loss or maximum profit, and therefore in breakeven)

The statistics panel, on the other hand, contains all the information necessary to search for parameters that give the trader a good statistical advantage.

In the settings you can filter the days of the week, only gap up or only gap down, ATR thresholds (volatility), points or minimum percentage for which a gap is taken into account, measure of the breakeven (which for options traders should represent the half the width of the spread to open), large gaps filter that takes into consideration only gaps that open out of range compared to the previous session. The Lookback parameter of course is used to set how many bars to take into account for the statistics.

Parameters and recommended strategy:

TODAY 31/08/2021 - Lookback 500 bars (2 years)

UNDERLYING: SPX

FILTERS: only Monday and Wednesday, only gap up, only gap> 0.01%

STRATEGY: exactly at opening, cover an ATM spread in the direction of the gap (example: gap up, I open a long call spread) that has the opening price as a break even, with a risk-return ratio of 1: 1 and leave it open until closing session, or set take profit at 90-95%. It is advisable to take into consideration the SPX statistics but to operate on the ES future so as to be able to open the spread a couple of minutes before the opening of the cash session and prevent the trade from "running away" due to too sudden movements of the opening. .

RESULTS:

124 Trade

70% profitable trades

30% losing trades

Max drawdown 3 trades

So assuming a spread on ES 10 points wide, each trade would gain or lose $ 250, applying the described strategy we would have in two years, investing only $ 250, a profit of $ 12500, with a max drawdown of $ 750. We would therefore have a profit of 5000%, or rather 2500% per year on the invested capital, with a drawdown of a much lower proportion of the profit ($ 750 compared to $ 6250 of annual profit).

The strategy is infinitely scalable by increasing the options contracts used and the impact of the commissions is almost zero.

MONEY MANAGEMENT: Example on a 50K account, with a spread that earns or loses $ 500, in two years it earns $ 25,000, therefore about 12500 per year, with a max drawdown of $ 1500, therefore 25% per year on the ENTIRE ACCOUNT with a maximum drawdown of 3%.

Note: the test was performed without a break even parameter, so the actual result will be more moderate, but of the same explosive nature.

** BUG STILL LOOKING FOR SOLUTION **

only in case the filters are set to take into account ONLY the gap down, the drawdown count in the statistics panel shows an incorrect result "

Fib Thermometer - S&P500Fib Retracement is such an amazing tool 😎 , and when u incorporate it onto a chart, no matter a forex , stock or future one, you will always secure some important and meaningful levels for your trading. I am not a huge fan of it actually 😵, but I would say it is an eye opener for me, because sometimes things don't fully make sense will make you money. I can't deny its popularity in our community and also in the trading world.

In this script, I am not intending to give a brand new version of auto drawing fib levels, but to catch the optimal timings to buy the upcoming rally after a crash 😊. Buying the dips is the approach to get rich , right? But more wisely, we can instead to buy the higher lows , not the lowest lows in order to avoid the bankruptcy risk. Nothing advanced to teach here, doing so just takes your extra patience and willingness to seek confirmation. 🕵

To cut it short, I have utilized 52-week highs and lows and two important fib levels (0.236 and 0.618) , with ten most heavily weighted stocks in s&p500 index to create some awesome signals. The rationale is first defining two fib levels with the 52-week-high-low range, then if those stocks rebounded just higher than 0.236 levels, we can confirm the trend has changed and start our buying . For the 0.618 level, you can use it as a profit taker , or a sell signal during the bull run. What decides a trend continuation or a trend change is the degree of the retracement , and 0.236 would be an ideal level to confirm the trend has changed.😃

For your own convenience, you can amend or diy the script to make it work for you by simply put your favorite stocks or indexes on the list. Hope you find it really helpful and HAPPY TRADING!!! 😃

If you find my scripts useful, please click the FOLLOW button and I am VERY VERY GRATEFUL.😘

Historical Volatility EstimatorsHistorical volatility is a statistical measure of the dispersion of returns for a given security or market index over a given period. This indicator provides different historical volatility model estimators with percentile gradient coloring and volatility stats panel.

█ OVERVIEW There are multiple ways to estimate historical volatility. Other than the traditional close-to-close estimator. This indicator provides different range-based volatility estimators that take high low open into account for volatility calculation and volatility estimators that use other statistics measurements instead of standard deviation. The gradient coloring and stats panel provides an overview of how high or low the current volatility is compared to its historical values.

█ CONCEPTS We have mentioned the concepts of historical volatility in our previous indicators, Historical Volatility, Historical Volatility Rank, and Historical Volatility Percentile. You can check the definition of these scripts. The basic calculation is just the sample standard deviation of log return scaled with the square root of time. The main focus of this script is the difference between volatility models.

Close-to-Close HV Estimator: Close-to-Close is the traditional historical volatility calculation. It uses sample standard deviation. Note: the TradingView build in historical volatility value is a bit off because it uses population standard deviation instead of sample deviation. N – 1 should be used here to get rid of the sampling bias.

Pros:

• Close-to-Close HV estimators are the most commonly used estimators in finance. The calculation is straightforward and easy to understand. When people reference historical volatility, most of the time they are talking about the close to close estimator.

Cons:

• The Close-to-close estimator only calculates volatility based on the closing price. It does not take account into intraday volatility drift such as high, low. It also does not take account into the jump when open and close prices are not the same.

• Close-to-Close weights past volatility equally during the lookback period, while there are other ways to weight the historical data.

• Close-to-Close is calculated based on standard deviation so it is vulnerable to returns that are not normally distributed and have fat tails. Mean and Median absolute deviation makes the historical volatility more stable with extreme values.

Parkinson Hv Estimator:

• Parkinson was one of the first to come up with improvements to historical volatility calculation. • Parkinson suggests using the High and Low of each bar can represent volatility better as it takes into account intraday volatility. So Parkinson HV is also known as Parkinson High Low HV. • It is about 5.2 times more efficient than Close-to-Close estimator. But it does not take account into jumps and drift. Therefore, it underestimates volatility. Note: By Dividing the Parkinson Volatility by Close-to-Close volatility you can get a similar result to Variance Ratio Test. It is called the Parkinson number. It can be used to test if the market follows a random walk. (It is mentioned in Nassim Taleb's Dynamic Hedging book but it seems like he made a mistake and wrote the ratio wrongly.)

Garman-Klass Estimator:

• Garman Klass expanded on Parkinson’s Estimator. Instead of Parkinson’s estimator using high and low, Garman Klass’s method uses open, close, high, and low to find the minimum variance method.

• The estimator is about 7.4 more efficient than the traditional estimator. But like Parkinson HV, it ignores jumps and drifts. Therefore, it underestimates volatility.

Rogers-Satchell Estimator:

• Rogers and Satchell found some drawbacks in Garman-Klass’s estimator. The Garman-Klass assumes price as Brownian motion with zero drift.

• The Rogers Satchell Estimator calculates based on open, close, high, and low. And it can also handle drift in the financial series.

• Rogers-Satchell HV is more efficient than Garman-Klass HV when there’s drift in the data. However, it is a little bit less efficient when drift is zero. The estimator doesn’t handle jumps, therefore it still underestimates volatility.

Garman-Klass Yang-Zhang extension:

• Yang Zhang expanded Garman Klass HV so that it can handle jumps. However, unlike the Rogers-Satchell estimator, this estimator cannot handle drift. It is about 8 times more efficient than the traditional estimator.

• The Garman-Klass Yang-Zhang extension HV has the same value as Garman-Klass when there’s no gap in the data such as in cryptocurrencies.

Yang-Zhang Estimator:

• The Yang Zhang Estimator combines Garman-Klass and Rogers-Satchell Estimator so that it is based on Open, close, high, and low and it can also handle non-zero drift. It also expands the calculation so that the estimator can also handle overnight jumps in the data.

• This estimator is the most powerful estimator among the range-based estimators. It has the minimum variance error among them, and it is 14 times more efficient than the close-to-close estimator. When the overnight and daily volatility are correlated, it might underestimate volatility a little.

• 1.34 is the optimal value for alpha according to their paper. The alpha constant in the calculation can be adjusted in the settings. Note: There are already some volatility estimators coded on TradingView. Some of them are right, some of them are wrong. But for Yang Zhang Estimator I have not seen a correct version on TV.

EWMA Estimator:

• EWMA stands for Exponentially Weighted Moving Average. The Close-to-Close and all other estimators here are all equally weighted.

• EWMA weighs more recent volatility more and older volatility less. The benefit of this is that volatility is usually autocorrelated. The autocorrelation has close to exponential decay as you can see using an Autocorrelation Function indicator on absolute or squared returns. The autocorrelation causes volatility clustering which values the recent volatility more. Therefore, exponentially weighted volatility can suit the property of volatility well.

• RiskMetrics uses 0.94 for lambda which equals 30 lookback period. In this indicator Lambda is coded to adjust with the lookback. It's also easy for EWMA to forecast one period volatility ahead.

• However, EWMA volatility is not often used because there are better options to weight volatility such as ARCH and GARCH.

Adjusted Mean Absolute Deviation Estimator:

• This estimator does not use standard deviation to calculate volatility. It uses the distance log return is from its moving average as volatility.

• It’s a simple way to calculate volatility and it’s effective. The difference is the estimator does not have to square the log returns to get the volatility. The paper suggests this estimator has more predictive power.

• The mean absolute deviation here is adjusted to get rid of the bias. It scales the value so that it can be comparable to the other historical volatility estimators.

• In Nassim Taleb’s paper, he mentions people sometimes confuse MAD with standard deviation for volatility measurements. And he suggests people use mean absolute deviation instead of standard deviation when we talk about volatility.

Adjusted Median Absolute Deviation Estimator:

• This is another estimator that does not use standard deviation to measure volatility.

• Using the median gives a more robust estimator when there are extreme values in the returns. It works better in fat-tailed distribution.

• The median absolute deviation is adjusted by maximum likelihood estimation so that its value is scaled to be comparable to other volatility estimators.

█ FEATURES

• You can select the volatility estimator models in the Volatility Model input

• Historical Volatility is annualized. You can type in the numbers of trading days in a year in the Annual input based on the asset you are trading.

• Alpha is used to adjust the Yang Zhang volatility estimator value.

• Percentile Length is used to Adjust Percentile coloring lookbacks.

• The gradient coloring will be based on the percentile value (0- 100). The higher the percentile value, the warmer the color will be, which indicates high volatility. The lower the percentile value, the colder the color will be, which indicates low volatility.

• When percentile coloring is off, it won’t show the gradient color.

• You can also use invert color to make the high volatility a cold color and a low volatility high color. Volatility has some mean reversion properties. Therefore when volatility is very low, and color is close to aqua, you would expect it to expand soon. When volatility is very high, and close to red, you would it expect it to contract and cool down.

• When the background signal is on, it gives a signal when HVP is very low. Warning there might be a volatility expansion soon.

• You can choose the plot style, such as lines, columns, areas in the plotstyle input.

• When the show information panel is on, a small panel will display on the right.

• The information panel displays the historical volatility model name, the 50th percentile of HV, and HV percentile. 50 the percentile of HV also means the median of HV. You can compare the value with the current HV value to see how much it is above or below so that you can get an idea of how high or low HV is. HV Percentile value is from 0 to 100. It tells us the percentage of periods over the entire lookback that historical volatility traded below the current level. Higher HVP, higher HV compared to its historical data. The gradient color is also based on this value.

█ HOW TO USE If you haven’t used the hvp indicator, we suggest you use the HVP indicator first. This indicator is more like historical volatility with HVP coloring. So it displays HVP values in the color and panel, but it’s not range bound like the HVP and it displays HV values. The user can have a quick understanding of how high or low the current volatility is compared to its historical value based on the gradient color. They can also time the market better based on volatility mean reversion. High volatility means volatility contracts soon (Move about to End, Market will cooldown), low volatility means volatility expansion soon (Market About to Move).

█ FINAL THOUGHTS HV vs ATR The above volatility estimator concepts are a display of history in the quantitative finance realm of the research of historical volatility estimations. It's a timeline of range based from the Parkinson Volatility to Yang Zhang volatility. We hope these descriptions make more people know that even though ATR is the most popular volatility indicator in technical analysis, it's not the best estimator. Almost no one in quant finance uses ATR to measure volatility (otherwise these papers will be based on how to improve ATR measurements instead of HV). As you can see, there are much more advanced volatility estimators that also take account into open, close, high, and low. HV values are based on log returns with some calculation adjustment. It can also be scaled in terms of price just like ATR. And for profit-taking ranges, ATR is not based on probabilities. Historical volatility can be used in a probability distribution function to calculated the probability of the ranges such as the Expected Move indicator. Other Estimators There are also other more advanced historical volatility estimators. There are high frequency sampled HV that uses intraday data to calculate volatility. We will publish the high frequency volatility estimator in the future. There's also ARCH and GARCH models that takes volatility clustering into account. GARCH models require maximum likelihood estimation which needs a solver to find the best weights for each component. This is currently not possible on TV due to large computational power requirements. All the other indicators claims to be GARCH are all wrong.

The Strat - Levels [rdjxyz]◆ OVERVIEW

The Strat - Levels dynamically displays key levels used in The Strat trading methodology, developed by Rob Smith. The level colors are dynamically determined by their Strat classification (1, 2 up, failed 2 up, 2 down, failed 2 down, 3)—making it easy to recognize higher timeframe Strat candle classifications from any lower timeframe.

◆ DETAILS

If you're unfamiliar with The Strat, there are 3 universal scenarios regarding candle behavior:

SCENARIO ONE

The 1 Bar - Inside Bar: A candle that doesn't take out the highs or the lows of the previous candle; aka consolidation.

SCENARIO TWO

The 2 Bar - Directional Bar: A candle that takes out one side of the previous candle; aka trending (or at least attempting to trend).

These can be broken down even further as follows:

2 Up: A candle that takes out the high of the previous candle and closes bullish

Failed 2 Up: A candle that takes out the high of the previous candle and closes bearish

2 Down: A candle that takes out the low of the previous candle and closes bearish

Failed 2 Down: A candle that takes out the low of the previous candle and closes bullish

SCENARIO THREE

The 3 Bar - Outside Bar: A candle that takes out both sides of the previous candle; aka broadening formation.

◇ HOW THE DYNAMIC LEVEL COLORING WORKS

PREVIOUS LEVELS

Previous Day High/Low

Previous Week High/Low

Previous Month High/Low

Previous Quarter High/Low

Previous Year High/Low

Each period's levels are compared to their previous period's levels and colored according to the 3 universal scenarios, which are fixed based on historical data. (No repainting)

CURRENT LEVELS

Current Day Open

Current Week Open

Current Month Open

Current Quarter Open

Current Year Open

Each current period's levels (high, low, and current price) are compared to the previous period's levels and current period's open on every tick—changing colors in real-time as their Strat classification changes. (Will repaint as price action evolves)

E.g. When a new day opens inside of the previous day's range (high/low) the Day Open line will be gray (default for inside bars). When the current day trades above the previous day's range, the Day Open line will become aqua (default for 2 up). If price trades back below the current day's open, the Day Open line will become fuchsia (default for failed 2 up). And if price trades below the previous day's range, the Day Open line will become dark purple (default for 3s).

◆ SETTINGS

Current Day Open

Previous Day High/Low

Current Week Open

Previous Week High/Low

Current Month Open

Previous Month High/Low

Current Quarter Open

Previous Quarter High/Low

Current Year Open

Previous Year High/Low

Strat Colors

Each Current Level Open has 4 inputs:

Show/Hide Checkbox

Line Style

Line Width

Label Offset (Integer)

Each Previous Level High/Low has 5 inputs:

Show/Hide High Checkbox

Show/Hide Low Checkbox

Line Style

Line Width

Label Offset (Integer)

And each Strat scenario can be custom colored:

1-Bar Color - Default Gray

2-Up Color - Default Aqua

Failed 2-Up Color - Default Fuchsia

2-Down Color - Default White

Failed 2-Down Color - Default Teal

3-Bar Color - Default Dark Purple

◆ USAGE

There are 3 ways to look at these levels:

Potential continuation (e.g. Previous Day's 2-Up High being broken by Current Day's Price)

Potential reversal (e.g. Previous Day's 2-Down High being broken by Current Day's Price)

Potential exhaustion risk (e.g. Previous Month's Low is broken by Current Day's Price but trades back up into the Previous Month's range)

It's best to use this indicator with a separate indicator that color codes your chart's candles according to their Strat Scenario (1, 2, 3) and use top-down analysis to gauge whether to view levels as a sign of continuation, reversal, or exhaustion risk.

◆ WRAP UP

As demonstrated, The Strat - Levels offers Strat Scenario color-coded key levels, making it easy to identify the previous period's Strat Scenario (1, 2-Up, Failed 2-Up, 2-Down, Failed 2-Down, or 3) without needing to manually plot levels or refer to higher timeframes.

◆ DISCLAIMER

This indicator is a tool for visual analysis and is intended to assist traders who follow The Strat methodology. As with any trading methodology, there's no guarantee of profits; trading involves a high degree of risk and you could lose all of your invested capital. Use of this indicator is not indicative of future results and does not constitute and should not be construed as investment advice. All trading decisions and investments made by you are at your own discretion and risk. Under no circumstances shall the author be liable for any direct, indirect, or incidental damages. You should only risk capital you can afford to lose.

Liquidity Sweep + BOS Retest System — Prop Firm Edition🟦 Liquidity Sweep + BOS Retest System — Prop Firm Edition

A High-Probability Smart Money Strategy Built for NQ, ES, and Funding Accounts

🚀 Overview

The Liquidity Sweep + BOS Retest System (Prop Firm Edition) is a precision-engineered SMC strategy built specifically for prop firm traders. It mirrors institutional liquidity behavior and combines it with strict account-safe entry rules to help traders pass and maintain funding accounts with consistency.

Unlike typical indicators, this system waits for three confirmations — liquidity sweep, displacement, and a clean retest — before executing any trade. Every component is optimized for low drawdown, high R:R, and prop-firm-approved risk management.

Whether you’re trading Apex, TakeProfitTrader, FFF, or OneUp Trader, this system gives you a powerful mechanical framework that keeps you within rules while identifying the market’s highest-probability reversal zones.

🔥 Key Features

1. Liquidity Sweep Detection (Stop Hunt Logic)

Automatically identifies when price clears a previous swing high/low with a sweep confirmation candle.

✔ Filters noise

✔ Eliminates early entries

✔ Locks onto true liquidity grabs

2. Automatic Break of Structure (BOS) Confirmation

Price must show true displacement by breaking structure opposite the sweep direction.

✔ Confirms momentum shift

✔ Removes fake reversals

✔ Ensures institutional intent

3. Precision Retest Entry Model

The strategy enters only when price retests the BOS level at premium/discount pricing.

✔ Zero chasing

✔ Extremely tight stop loss placement

✔ Prop-firm-friendly controlled risk

4. Built-In Risk & Trade Management

SL set at swept liquidity

TP set by user-defined R:R multiplier

Optional session filter (NY Open by default)

One trade at a time (no pyramiding)

Automatically resets logic after each trade

This prevents overtrading — the #1 cause of evaluation and account breaches.

5. Designed for Prop Firm Futures Trading

This script is optimized for:

Trailing/static drawdown accounts

Micro contract precision

Funding evaluations

Low-risk, high-probability setups

Structured, rule-based execution

It reduces randomness and emotional trading by automating the highest-quality SMC sequence.

🎯 The Trading Model Behind the System

Step 1 — Liquidity Sweep

Price must take out a recent high/low and close back inside structure.

This confirms stop-hunting behavior and marks the beginning of a potential reversal.

Step 2 — BOS (Break of Structure)

Price must break the opposite side swing with a displacement candle. This validates a directional shift.

Step 3 — Retest Entry

The system waits for price to retrace into the BOS level and signal continuation.

This creates optimal R:R entry with minimal drawdown.

📈 Best Markets

NQ (NASDAQ Futures) – Highly recommended

ES, YM, RTY

Gold (XAUUSD)

FX majors

Crypto (with high volatility)

Works best on 1m, 2m, 5m, or 15m depending on your trading style.

🧠 Why Traders Love This System

✔ No signals until all confirmations align

✔ Reduces overtrading and emotional decisions

✔ Follows market structure instead of random indicators

✔ Perfect for maintaining long-term funded accounts

✔ Built around institutional-grade concepts

✔ Makes your trading consistent, calm, and rules-based

⚙️ Recommended Settings

Session: 06:30–08:00 MST (NY Open)

R:R: 1.5R – 3R

Contracts: Start with 1–2 micros

Markets: NQ for best structure & volume

📦 What’s Included

Complete strategy logic

All plots, labels, sweep markers & BOS alerts

BOS retest entry automation

Session filtering

Stop loss & take profit system

Full SMC logic pipeline

🏁 Summary

The Liquidity Sweep + BOS Retest System is a complete, prop-firm-ready, structure-based strategy that automates one of the cleanest and most reliable SMC entry models. It is designed to keep you safe, consistent, and rule-compliant while capturing premium institutional setups.

If you want to trade with confidence, discipline, and prop-firm precision — this system is for you.

Good Luck -BG

indicator CalibrationIndicator Calibration - Multi-Indicator Consensus System

Overview

Indicator Calibration is a powerful consensus-based trading indicator that leverages the MyIndicatorLibrary (NormalizedIndicators) to combine multiple trend-following indicators into a single, actionable signal. By averaging the normalized outputs of up to 8 different trend indicators, this tool provides traders with a clear consensus view of market direction, reducing noise and false signals inherent in single-indicator approaches.

The indicator outputs a value between -1 (strong bearish) and +1 (strong bullish), with 0 representing a neutral market state. This creates an intuitive, easy-to-read oscillator that synthesizes multiple analytical perspectives into one coherent signal.

🎯 Core Concept

Consensus Trading Philosophy

Rather than relying on a single indicator that may give conflicting or premature signals, Indicator Calibration employs a democratic voting system where multiple indicators contribute their normalized opinion:

Each enabled indicator votes: +1 (bullish), -1 (bearish), or 0 (neutral)

The votes are averaged to create a consensus signal

Strong consensus (closer to ±1) indicates high agreement among indicators

Weak consensus (closer to 0) indicates market indecision or transition

Key Benefits

Reduced False Signals: Multiple indicators must agree before strong signals appear

Noise Filtering: Individual indicator quirks are smoothed out by averaging

Customizable: Enable/disable indicators and adjust parameters to suit your trading style

Universal Application: Works across all timeframes and asset classes

Clear Visualization: Simple line oscillator with clear bull/bear zones

📊 Included Indicators

The system can utilize up to 8 normalized trend-following indicators from the library:

1. BBPct - Bollinger Bands Percent

Parameters: Length (default: 20), Factor (default: 2)

Type: Stationary oscillator

Strength: Mean reversion and volatility detection

2. NorosTrendRibbonEMA

Parameters: Length (default: 20)

Type: Non-stationary trend follower

Strength: Breakout detection with momentum confirmation

3. RSI - Relative Strength Index

Parameters: Length (default: 9), SMA Length (default: 4)

Type: Stationary momentum oscillator

Strength: Overbought/oversold with smoothing

4. Vidya - Variable Index Dynamic Average

Parameters: Length (default: 30), History Length (default: 9)

Type: Adaptive moving average

Strength: Volatility-adjusted trend following

5. HullSuite

Parameters: Length (default: 55), Multiplier (default: 1)

Type: Fast-response moving average

Strength: Low-lag trend identification

6. TrendContinuation

Parameters: MA Length 1 (default: 50), MA Length 2 (default: 25)

Type: Dual HMA system

Strength: Trend quality assessment with neutral states

7. LeonidasTrendFollowingSystem

Parameters: Short Length (default: 21), Key Length (default: 10)

Type: Dual EMA crossover

Strength: Simple, reliable trend tracking

8. TRAMA - Trend Regularity Adaptive Moving Average

Parameters: Length (default: 50)

Type: Adaptive trend follower

Strength: Adjusts to trend stability

⚙️ Input Parameters

Source Settings

Source: Choose your price input (default: close)

Can be modified to: open, high, low, close, hl2, hlc3, ohlc4, hlcc4

Indicator Selection

Each indicator can be enabled or disabled via checkboxes:

use_bbpct: Enable/disable Bollinger Bands Percent

use_noros: Enable/disable Noro's Trend Ribbon

use_rsi: Enable/disable RSI

use_vidya: Enable/disable VIDYA

use_hull: Enable/disable Hull Suite

use_trendcon: Enable/disable Trend Continuation

use_leonidas: Enable/disable Leonidas System

use_trama: Enable/disable TRAMA

Parameter Customization

Each indicator has its own parameter group where you can fine-tune:

val 1: Primary period/length parameter

val 2: Secondary parameter (multiplier, smoothing, etc.)

📈 Signal Interpretation

Output Line (Orange)

The main output oscillates between -1 and +1:

+1.0 to +0.5: Strong bullish consensus (all or most indicators agree on uptrend)

+0.5 to +0.2: Moderate bullish bias (bullish indicators outnumber bearish)

+0.2 to -0.2: Neutral zone (mixed signals or transition phase)

-0.2 to -0.5: Moderate bearish bias (bearish indicators outnumber bullish)

-0.5 to -1.0: Strong bearish consensus (all or most indicators agree on downtrend)

Reference Lines

Green line (+1): Maximum bullish consensus

Red line (-1): Maximum bearish consensus

Gray line (0): Neutral midpoint

💡 Trading Strategies

Strategy 1: Consensus Threshold Trading

Entry Rules:

- Long: Output crosses above +0.5 (strong bullish consensus)

- Short: Output crosses below -0.5 (strong bearish consensus)

Exit Rules:

- Exit Long: Output crosses below 0 (consensus lost)

- Exit Short: Output crosses above 0 (consensus lost)

Strategy 2: Zero-Line Crossover

Entry Rules:

- Long: Output crosses above 0 (bullish shift in consensus)

- Short: Output crosses below 0 (bearish shift in consensus)

Exit Rules:

- Exit on opposite crossover

Strategy 3: Divergence Trading

Look for divergences between:

- Price making higher highs while indicator makes lower highs (bearish divergence)

- Price making lower lows while indicator makes higher lows (bullish divergence)

Strategy 4: Extreme Reading Reversal

Entry Rules:

- Long: Output reaches -0.8 or below (extreme bearish consensus = potential reversal)

- Short: Output reaches +0.8 or above (extreme bullish consensus = potential reversal)

Use with caution - best combined with other reversal signals

🔧 Optimization Tips

For Trending Markets

Enable trend-following indicators: Noro's, VIDYA, Hull Suite, Leonidas

Use higher threshold levels (±0.6) to filter out minor retracements

Increase indicator periods for smoother signals

For Range-Bound Markets

Enable oscillators: BBPct, RSI

Use zero-line crossovers for entries

Decrease indicator periods for faster response

For Volatile Markets

Enable adaptive indicators: VIDYA, TRAMA

Use wider threshold levels to avoid whipsaws

Consider disabling fast indicators that may overreact

Custom Calibration Process

Start with all indicators enabled using default parameters

Backtest on your chosen timeframe and asset

Identify which indicators produce the most false signals

Disable or adjust parameters for problematic indicators

Test different threshold levels for entry/exit

Validate on out-of-sample data

📊 Visual Guide

Color Scheme

Orange Line: Main consensus output

Green Horizontal: Bullish extreme (+1)

Red Horizontal: Bearish extreme (-1)

Gray Horizontal: Neutral zone (0)

Reading the Chart

Line above 0: Net bullish sentiment

Line below 0: Net bearish sentiment

Line near extremes: Strong consensus

Line fluctuating near 0: Indecision or transition

Smooth line movement: Stable consensus

Erratic line movement: Conflicting signals

⚠️ Important Considerations

Lag Characteristics

This is a lagging indicator by design (consensus takes time to form)

Best used for trend confirmation rather than early entry

May miss the first portion of strong moves

Reduces false entries at the cost of delayed entries

Number of Active Indicators

More indicators = smoother but slower signals

Fewer indicators = faster but potentially noisier signals

Minimum recommended: 4 indicators for reliable consensus

Optimal: 6-8 indicators for balanced performance

Market Conditions

Best: Strong trending markets (up or down)

Good: Volatile markets with clear directional moves

Poor: Choppy, sideways markets with no clear trend

Worst: Low-volume, range-bound conditions

Complementary Tools

Consider combining with:

Volume analysis for confirmation

Support/resistance levels for entry/exit points

Market structure analysis (higher timeframe trends)

Risk management tools (ATR-based stops)

🎓 Example Use Cases

Swing Trading

Timeframe: Daily or 4H

Enable: All 8 indicators with default parameters

Entry: Consensus > +0.5 or < -0.5

Hold: Until consensus reverses to opposite extreme

Day Trading

Timeframe: 15m or 1H

Enable: Faster indicators (RSI, BBPct, Noro's, Hull Suite)

Entry: Zero-line crossover with volume confirmation

Exit: Opposite crossover or profit target

Position Trading

Timeframe: Weekly or Daily

Enable: Slower indicators (TRAMA, VIDYA, Trend Continuation)

Entry: Strong consensus (±0.7) with higher timeframe confirmation

Hold: Months until consensus weakens significantly

🔬 Technical Details

Calculation Method

1. Each enabled indicator calculates its normalized signal (-1, 0, or +1)

2. All active signals are stored in an array

3. Array.avg() computes the arithmetic mean

4. Result is plotted as a continuous line

Output Range

Theoretical: -1.0 to +1.0

Practical: Typically ranges between -0.8 to +0.8

Rare: All indicators perfectly aligned at ±1.0

Performance

Lightweight calculation (simple averaging)

No repainting (all indicators are non-repainting)

Compatible with all Pine Script features

Works on all TradingView plans

📋 License

This code is subject to the Mozilla Public License 2.0 at mozilla.org

🚀 Quick Start Guide

Add to Chart: Apply indicator to your chart

Choose Timeframe: Select appropriate timeframe for your trading style

Enable Indicators: Start with all 8 enabled

Observe Behavior: Watch how consensus forms during different market conditions

Calibrate: Adjust parameters and indicator selection based on observations

Backtest: Validate your settings on historical data

Trade: Apply with proper risk management

🎯 Key Takeaways

✅ Consensus beats individual indicators - Multiple perspectives reduce errors

✅ Customizable to your style - Enable/disable and tune to preference

✅ Simple interpretation - One line tells the story

✅ Works across markets - Stocks, crypto, forex, commodities

✅ Reduces emotional trading - Clear, objective signal generation

✅ Professional-grade - Built on proven technical analysis principles

Indicator Calibration transforms complex multi-indicator analysis into a single, actionable signal. By harnessing the collective wisdom of multiple proven trend-following systems, traders gain a powerful edge in identifying high-probability trade setups while filtering out market noise.

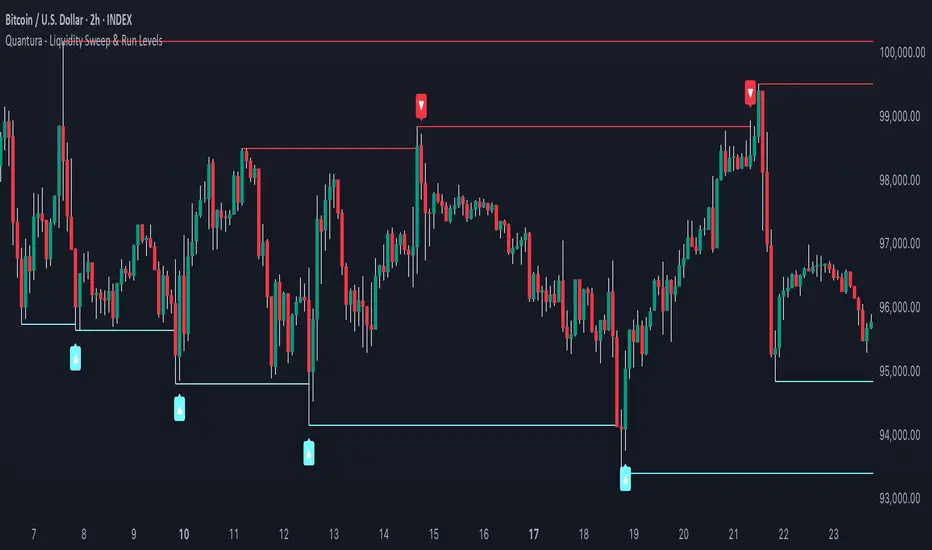

Quantura - Liquidity Sweep & Run LevelsIntroduction

“Quantura – Liquidity Sweep & Run Levels” is a structural price-action indicator designed to automatically detect swing-based liquidity zones and visualize potential sweep and run events. It helps traders identify areas where liquidity has likely been taken (sweep) or released (run), improving precision in market structure analysis and timing of entries or exits.

Originality & Value

This tool translates institutional liquidity concepts into an automated visual framework. Instead of simply marking highs and lows, it dynamically monitors swing points, tracks their breaches, and identifies subsequent reactions. The indicator is built to highlight the liquidity dynamics that often precede reversals or continuations.

Its originality lies in:

Automatic identification and tracking of swing highs and lows.

Real-time detection of broken levels and liquidity sweeps.

Distinction between “Run” and “Sweep” modes for different market behaviors.

Persistent historical visualization of liquidity levels using clean line structures.

Configurable signal markers for bullish and bearish sweep confirmations.

Functionality & Core Logic

Detects swing highs and lows using a user-defined Swing Length parameter.

Stores and updates all swing levels dynamically with arrays for efficient memory handling.

Draws horizontal lines from each detected swing point to visualize potential liquidity zones.

Monitors when price breaks a swing level and marks that event as “broken.”

Generates signals when the market either sweeps above/below or runs away from those levels, depending on the chosen mode.

Provides optional visual signal markers (“▲” for bullish sweeps, “▼” for bearish sweeps).

Parameters & Customization

Mode: Choose between “Sweep” (detects liquidity grabs) or “Run” (detects breakout continuations).

Swing Length: Sets the sensitivity for detecting swing highs/lows. A higher value focuses on larger structures, while smaller values detect micro liquidity points.

Bullish Color / Bearish Color: Customize color themes for sweep/run lines and signal markers.

Signals: Enables or disables visual up/down markers for confirmed events.

Visualization & Display

Horizontal lines represent potential liquidity levels (unbroken swing highs/lows).

Once broken, lines automatically stop extending, marking the moment liquidity is taken.

Depending on the selected mode:

“Sweep” mode identifies false breaks or stop-hunt behavior.

“Run” mode highlights breakouts that continue the trend.

Colored arrows indicate the direction and type of liquidity reaction.

Clean, non-intrusive visualization suitable for overlaying on price charts.

Use Cases

Detect liquidity sweeps before major reversals.

Identify breakout continuations after liquidity runs.

Combine with Supply/Demand or FVG indicators for multi-layered confirmation.

Validate liquidity bias in algorithmic or discretionary strategies.

Analyze market manipulation patterns and institutional stop-hunting behavior.

Limitations & Recommendations

This indicator identifies structural behavior but does not guarantee trade direction or profitability.

Works best on liquid markets with clear swing structures (e.g., crypto, forex, indices).

Signal interpretation should be combined with confluence tools such as volume, order flow, or structure-based filters.

Excessively small swing settings may cause over-signaling in volatile markets.

Markets & Timeframes

Optimized for all major asset classes — including crypto, Forex, indices, and equities — and for intraday to higher-timeframe structural analysis (5-minute up to daily charts).

Author & Access

Developed 100% by Quantura. Published as a Open-source script indicator. Access is free.

Compliance Note

This description fully complies with TradingView’s Script Publishing Rules and House Rules . It avoids performance claims, provides transparency on methodology, and clearly describes indicator behavior and limitations.

Luxy Momentum, Trend, Bias and Breakout Indicators V7

TABLE OF CONTENTS

This is Version 7 (V7) - the latest and most optimized release. If you are using any older versions (V6, V5, V4, V3, etc.), it is highly recommended to replace them with V7.

Why This Indicator is Different

Who Should Use This

Core Components Overview

The UT Bot Trading System

Understanding the Market Bias Table

Candlestick Pattern Recognition

Visual Tools and Features

How to Use the Indicator

Performance and Optimization

FAQ

---

### CREDITS & ATTRIBUTION

This indicator implements proven trading concepts using entirely original code developed specifically for this project.

### CONCEPTUAL FOUNDATIONS

• UT Bot ATR Trailing System

- Original concept by @QuantNomad: (search "UT-Bot-Strategy"

- Our version is a complete reimplementation with significant enhancements:

- Volume-weighted momentum adjustment

- Composite stop loss from multiple S/R layers

- Multi-filter confirmation system (swing, %, 2-bar, ZLSMA)

- Full integration with multi-timeframe bias table

- Visual audit trail with freeze-on-touch

- NOTE: No code was copied - this is a complete reimplementation with enhancements.

• Standard Technical Indicators (Public Domain Formulas):

- Supertrend: ATR-based trend calculation with custom gradient fills

- MACD: Gerald Appel's formula with separation filters

- RSI: J. Welles Wilder's formula with pullback zone logic

- ADX/DMI: Custom trend strength formula inspired by Wilder's directional movement concept, reimplemented with volume weighting and efficiency metrics

- ZLSMA: Zero-lag formula enhanced with Hull MA and momentum prediction

### Custom Implementations

- Trend Strength: Inspired by Wilder's ADX concept but using volume-weighted pressure calculation and efficiency metrics (not traditional +DI/-DI smoothing)

- All code implementations are original

### ORIGINAL FEATURES (70%+ of codebase)

- Multi-Timeframe Bias Table with live updates

- Risk Management System (R-multiple TPs, freeze-on-touch)

- Opening Range Breakout tracker with session management

- Composite Stop Loss calculator using 6+ S/R layers

- Performance optimization system (caching, conditional calcs)

- VIX Fear Index integration

- Previous Day High/Low auto-detection

- Candlestick pattern recognition with interactive tooltips

- Smart label and visual management

- All UI/UX design and table architecture

### DEVELOPMENT PROCESS

**AI Assistance:** This indicator was developed over 2+ months with AI assistance (ChatGPT/Claude) used for:

- Writing Pine Script code based on design specifications

- Optimizing performance and fixing bugs

- Ensuring Pine Script v6 compliance

- Generating documentation

**Author's Role:** All trading concepts, system design, feature selection, integration logic, and strategic decisions are original work by the author. The AI was a coding tool, not the system designer.

**Transparency:** We believe in full disclosure - this project demonstrates how AI can be used as a powerful development tool while maintaining creative and strategic ownership.

---

1. WHY THIS INDICATOR IS DIFFERENT

Most traders use multiple separate indicators on their charts, leading to cluttered screens, conflicting signals, and analysis paralysis. The Suite solves this by integrating proven technical tools into a single, cohesive system.

Key Advantages:

All-in-One Design: Instead of loading 5-10 separate indicators, you get everything in one optimized script. This reduces chart clutter and improves TradingView performance.

Multi-Timeframe Bias Table: Unlike standard indicators that only show the current timeframe, the Bias Table aggregates trend signals across multiple timeframes simultaneously. See at a glance whether 1m, 5m, 15m, 1h are aligned bullish or bearish - no more switching between charts.

Smart Confirmations: The indicator doesn't just give signals - it shows you WHY. Every entry has multiple layers of confirmation (MA cross, MACD momentum, ADX strength, RSI pullback, volume, etc.) that you can toggle on/off.

Dynamic Stop Loss System: Instead of static ATR stops, the SL is calculated from multiple support/resistance layers: UT trailing line, Supertrend, VWAP, swing structure, and MA levels. This creates more intelligent, price-action-aware stops.

R-Multiple Take Profits: Built-in TP system calculates targets based on your initial risk (1R, 1.5R, 2R, 3R). Lines freeze when touched with visual checkmarks, giving you a clean audit trail of partial exits.

Educational Tooltips Everywhere: Every single input has detailed tooltips explaining what it does, typical values, and how it impacts trading. You're not guessing - you're learning as you configure.

Performance Optimized: Smart caching, conditional calculations, and modular design mean the indicator runs fast despite having 15+ features. Turn off what you don't use for even better performance.

No Repainting: All signals respect bar close. Alerts fire correctly. What you see in history is what you would have gotten in real-time.

What Makes It Unique:

Integrated UT Bot + Bias Table: No other indicator combines UT Bot's ATR trailing system with a live multi-timeframe dashboard. You get precision entries with macro trend context.

Candlestick Pattern Recognition with Interactive Tooltips: Patterns aren't just marked - hover over any emoji for a full explanation of what the pattern means and how to trade it.

Opening Range Breakout Tracker: Built-in ORB system for intraday traders with customizable session times and real-time status updates in the Bias Table.

Previous Day High/Low Auto-Detection: Automatically plots PDH/PDL on intraday charts with theme-aware colors. Updates daily without manual input.

Dynamic Row Labels in Bias Table: The table shows your actual settings (e.g., "EMA 10 > SMA 20") not generic labels. You know exactly what's being evaluated.

Modular Filter System: Instead of forcing a fixed methodology, the indicator lets you build your own strategy. Start with just UT Bot, add filters one at a time, test what works for your style.

---

2. WHO WHOULD USE THIS

Designed For:

Intermediate to Advanced Traders: You understand basic technical analysis (MAs, RSI, MACD) and want to combine multiple confirmations efficiently. This isn't a "one-click profit" system - it's a professional toolkit.

Multi-Timeframe Traders: If you trade one asset but check multiple timeframes for confirmation (e.g., enter on 5m after checking 15m and 1h alignment), the Bias Table will save you hours every week.

Trend Followers: The indicator excels at identifying and following trends using UT Bot, Supertrend, and MA systems. If you trade breakouts and pullbacks in trending markets, this is built for you.

Intraday and Swing Traders: Works equally well on 5m-1h charts (day trading) and 4h-D charts (swing trading). Scalpers can use it too with appropriate settings adjustments.

Discretionary Traders: This isn't a black-box system. You see all the components, understand the logic, and make final decisions. Perfect for traders who want tools, not automation.

Works Across All Markets:

Stocks (US, international)

Cryptocurrency (24/7 markets supported)

Forex pairs

Indices (SPY, QQQ, etc.)

Commodities

NOT Ideal For :

Complete Beginners: If you don't know what a moving average or RSI is, start with basics first. This indicator assumes foundational knowledge.

Algo Traders Seeking Black Box: This is discretionary. Signals require context and confirmation. Not suitable for blind automated execution.

Mean-Reversion Only Traders: The indicator is trend-following at its core. While VWAP bands support mean-reversion, the primary methodology is trend continuation.

---

3. CORE COMPONENTS OVERVIEW

The indicator combines these proven systems:

Trend Analysis:

Moving Averages: Four customizable MAs (Fast, Medium, Medium-Long, Long) with six types to choose from (EMA, SMA, WMA, VWMA, RMA, HMA). Mix and match for your style.

Supertrend: ATR-based trend indicator with unique gradient fill showing trend strength. One-sided ribbon visualization makes it easier to see momentum building or fading.

ZLSMA : Zero-lag linear-regression smoothed moving average. Reduces lag compared to traditional MAs while maintaining smooth curves.

Momentum & Filters:

MACD: Standard MACD with separation filter to avoid weak crossovers.

RSI: Pullback zone detection - only enter longs when RSI is in your defined "buy zone" and shorts in "sell zone".

ADX/DMI: Trend strength measurement with directional filter. Ensures you only trade when there's actual momentum.

Volume Filter: Relative volume confirmation - require above-average volume for entries.

Donchian Breakout: Optional channel breakout requirement.

Signal Systems:

UT Bot: The primary signal generator. ATR trailing stop that adapts to volatility and gives clear entry/exit points.

Base Signals: MA cross system with all the above filters applied. More conservative than UT Bot alone.

Market Bias Table: Multi-timeframe dashboard showing trend alignment across 7 timeframes plus macro bias (3-day, weekly, monthly, quarterly, VIX).

Candlestick Patterns: Six major reversal patterns auto-detected with interactive tooltips.

ORB Tracker: Opening range high/low with breakout status (intraday only).

PDH/PDL: Previous day levels plotted automatically on intraday charts.

VWAP + Bands : Session-anchored VWAP with up to three standard deviation band pairs.

---

4. THE UT BOT TRADING SYSTEM

The UT Bot is the heart of the indicator's signal generation. It's an advanced ATR trailing stop that adapts to market volatility.

Why UT Bot is Superior to Fixed Stops:

Traditional ATR stops use a fixed multiplier (e.g., "stop = entry - 2×ATR"). UT Bot is smarter:

It TRAILS the stop as price moves in your favor

It WIDENS during high volatility to avoid premature stops

It TIGHTENS during consolidation to lock in profits

It FLIPS when price breaks the trailing line, signaling reversals

Visual Elements You'll See:

Orange Trailing Line: The actual UT stop level that adapts bar-by-bar

Buy/Sell Labels: Aqua triangle (long) or orange triangle (short) when the line flips

ENTRY Line: Horizontal line at your entry price (optional, can be turned off)

Suggested Stop Loss: A composite SL calculated from multiple support/resistance layers:

- UT trailing line

- Supertrend level

- VWAP

- Swing structure (recent lows/highs)

- Long-term MA (200)

- ATR-based floor

Take Profit Lines: TP1, TP1.5, TP2, TP3 based on R-multiples. When price touches a TP, it's marked with a checkmark and the line freezes for audit trail purposes.

Status Messages: "SL Touched ❌" or "SL Frozen" when the trade leg completes.

How UT Bot Differs from Other ATR Systems:

Multiple Filters Available: You can require 2-bar confirmation, minimum % price change, swing structure alignment, or ZLSMA directional filter. Most UT implementations have none of these.

Smart SL Calculation: Instead of just using the UT line as your stop, the indicator suggests a better SL based on actual support/resistance. This prevents getting stopped out by wicks while keeping risk controlled.

Visual Audit Trail: All SL/TP lines freeze when touched with clear markers. You can review your trades weeks later and see exactly where entries, stops, and targets were.

Performance Options: "Draw UT visuals only on bar close" lets you reduce rendering load without affecting logic or alerts - critical for slower machines or 1m charts.

Trading Logic:

UT Bot flips direction (Buy or Sell signal appears)

Check Bias Table for multi-timeframe confirmation

Optional: Wait for Base signal or candlestick pattern

Enter at signal bar close or next bar open

Place stop at "Suggested Stop Loss" line

Scale out at TP levels (TP1, TP2, TP3)