Swing Z | Zillennial Technologies Inc.Swing Z by Zillennial Technologies Inc. is an advanced algorithmic framework built specifically for cryptocurrency markets. It integrates multiple layers of technical analysis into a single decision-support tool, generating buy and sell signals only when several independent confirmations align.

Core Concept

Swing Z fuses trend structure, momentum oscillators, volatility signals, and price action tools to capture high-probability trading opportunities in volatile crypto environments.

Trend Structure (EMA 9, 21, 50, 200)

Short-term EMAs (9 & 21) detect immediate momentum shifts.

Longer-term EMAs (50 & 200) define the broader trend and dynamic support/resistance.

Momentum & Confirmation Layer

RSI measures relative strength and market conditions.

MACD crossovers confirm momentum shifts and trend continuations.

Volatility & Market Pressure

TTM Squeeze highlights compression zones likely to precede breakouts.

Volume analysis confirms conviction behind directional moves.

VWAP (Volume Weighted Average Price) establishes intraday value zones and institutional benchmarks.

Price Action Filters

Fibonacci retracements are integrated to identify key reversal and continuation levels.

Signals are produced only when multiple conditions agree, reducing noise and improving reliability in fast-moving crypto markets.

Features

Tailored for cryptocurrency trading across major pairs (BTC, ETH, and altcoins).

Works effectively on swing and trend-based timeframes (1H–1D).

Combines trend, momentum, volatility, and price action into a single framework.

Generates clear Buy/Sell markers and integrates with TradingView alerts.

How to Use

Apply to a clean chart for the clearest visualization.

Use Swing Z as a swing trading tool, aligning entries with both trend structure and momentum confirmation.

Combine with your own stop-loss, take-profit, and position sizing rules.

Avoid application on non-standard chart types such as Renko, Heikin Ashi, or Point & Figure, which may distort results.

Disclaimer

Swing Z is designed as a decision-support tool, not financial advice.

All backtesting should use realistic risk, commission, and slippage assumptions.

Past results do not guarantee future performance.

Signals do not repaint but may adjust as new data develops in real-time.

Why Swing Z is original & useful:

Swing Z unifies EMA trend structure, RSI, MACD, TTM Squeeze, VWAP, Fibonacci retracements, and volume analysis into a single algorithmic framework. This multi-confirmation approach improves accuracy by requiring consensus across trend, momentum, volatility, and price action — a design made specifically for the challenges and volatility of cryptocurrency markets.

Tìm kiếm tập lệnh với "Volatility"

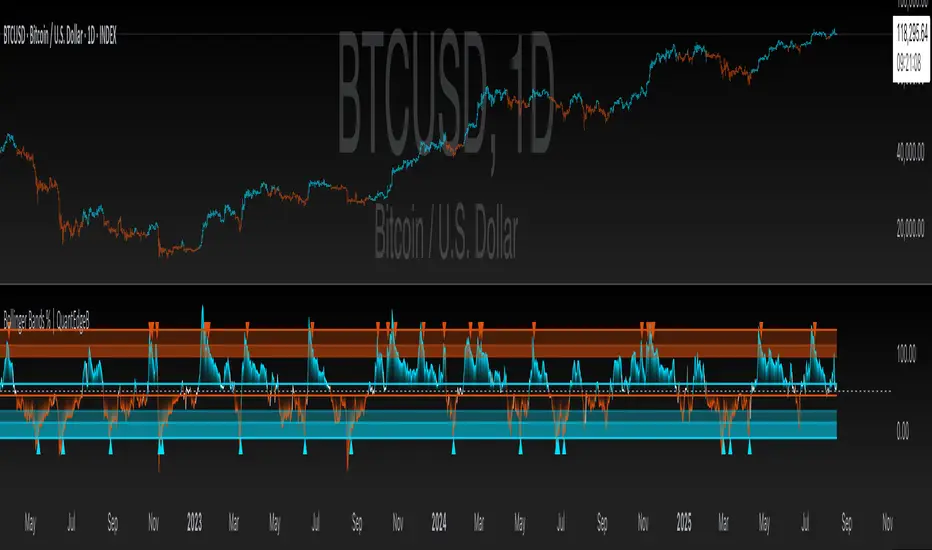

Bollinger Bands % | QuantEdgeB📊 Introducing Bollinger Bands % (BB%) by QuantEdgeB

🛠️ Overview

BB% | QuantEdgeB is a volatility-aware momentum tool that maps price within a Bollinger envelope onto a normalized scale. By letting you choose the base moving average (SMA, EMA, DEMA, TEMA, HMA, ALMA, EHMA, THMA, RMA, WMA, VWMA, T3, LSMA) and even Heikin-Ashi sources, it adapts to your style while keeping readings consistent across symbols and timeframes. Clear thresholds and color-coded visuals make it easy to spot emerging strength, fading moves, and potential mean-reversions.

✨ Key Features

• 🔹 Flexible Baseline

Pick from 12 MA types (plus Heikin-Ashi source option) to tailor responsiveness and smoothness.

• 🔹 Normalized Positioning

Price is expressed as a percentage of the band range, yielding an intuitive 0–100 style read (can exceed in extreme trends).

• 🔹 Actionable Thresholds

Default Long 55 / Short 45 levels provide simple, objective triggers.

• 🔹 Visual Clarity

Color-coded candles, shaded OB/OS zones, and adaptive color themes speed up decision-making.

• 🔹 Ready-to-Alert

Built-in alerts for long/short transitions.

📐 How It Works

1️⃣ Band Construction

A moving average (your choice) defines the midline; volatility (standard deviation) builds upper/lower bands.

2️⃣ Normalization

The indicator measures where price sits between the lower and upper band, scaling that into a bounded oscillator (BB%).

3️⃣ Signal Logic

• ✅ Long when BB% rises above 55 (strength toward the top of the envelope).

• ❌ Short when BB% falls below 45 (weakness toward the bottom).

4️⃣ OB/OS Context

Shaded regions above/below typical ranges highlight exhaustion and potential snap-backs.

⚙️ Custom Settings

• Base MA Type: SMA, EMA, DEMA, TEMA, HMA, ALMA, EHMA, THMA, RMA, WMA, VWMA, T3, LSMA

• Source Mode: Classic price or Heikin-Ashi (close/open/high/hlc3)

• Base Length: default 40

• Band Width: standard deviation-based (2× SD by default)

• Long / Short Thresholds: defaults 55 / 45

• Color Mode: Alpha, MultiEdge, TradingSuite, Premium, Fundamental, Classic, Warm, Cold, Strategy

• Candles & Labels: optional candle coloring and signal markers

👥 Ideal For

✅ Trend Followers — Ride strength as price compresses near the upper band.

✅ Swing/Mean-Reversion Traders — Fade extremes when BB% stretches into OB/OS zones.

✅ Multi-Timeframe Analysts — Compare band position consistently across periods.

✅ System Builders — Use BB% as a normalized feature for strategies and filters.

📌 Conclusion

BB% | QuantEdgeB delivers a clean, normalized read of price versus its volatility envelope—adaptable via rich MA/source options and easy to automate with thresholds and alerts.

🔹 Key Takeaways:

1️⃣ Normalized view of price inside the volatility bands

2️⃣ Flexible baseline (12+ MA choices) and Heikin-Ashi support

3️⃣ Straightforward 55/45 triggers with clear visual context

📌 Disclaimer: Past performance is not indicative of future results. No strategy guarantees success.

📌 Strategic Advice: Always backtest, tune parameters, and align with your risk profile before live trading.

New RSI📌 New RSI

The New RSI is a modern, enhanced version of the classic RSI created in 1978 — redesigned for today’s fast-moving markets, where algorithmic trading and AI dominate price action.

This indicator combines:

Adaptive RSI: Adjusts its calculation length in real time based on market volatility, making it more responsive during high volatility and smoother during calm periods.

Dynamic Bands: Upper and lower bands calculated from historical RSI volatility, helping you spot overbought/oversold conditions with greater accuracy.

Trend & Regime Filters: EMA and ADX-based detection to confirm signals only in favorable market conditions.

Volume Confirmation: Signals appear only when high trading volume supports the move — green volume for bullish setups and red volume for bearish setups — filtering out weak and unreliable trades.

💡 How it works:

A LONG signal appears when RSI crosses above the lower band and the volume is high with a bullish candle.

A SHORT signal appears when RSI crosses below the upper band and the volume is high with a bearish candle.

Trend and higher timeframe filters (optional) can help improve precision and adapt to different trading styles.

✅ Best Use Cases:

Identify high-probability reversals or pullbacks with strong momentum confirmation.

Avoid false signals by trading only when volume validates the move.

Combine with your own support/resistance or price action strategy for even higher accuracy.

⚙️ Fully Customizable:

Adjustable RSI settings (length, volatility adaptation, smoothing)

Dynamic band sensitivity

Volume threshold multiplier

Higher timeframe RSI filter

Color-coded background for market regime visualization

This is not just another RSI — it’s a complete, next-gen momentum tool designed for traders who want accuracy, adaptability, and confirmation in every signal.

Volatility Wick Trap — Smart Reversal EngineThe Volatility Wick Trap — Smart Reversal Engine is a precision reversal detection tool designed for traders who rely on smart money footprints, volatility compression, and liquidity wick exhaustion to time entries near market turns.

💡 Core Components:

Volatility Squeeze Detection: Identifies candles where range compresses significantly compared to the 14-period average true range, highlighting potential breakout zones.

Liquidity Wick Exhaustion: Detects candles with dominant upper or lower wicks, signaling failed liquidity grabs or stop hunts.

Contextual EMA Filter: Uses a 21-period EMA to filter signals, improving accuracy by aligning with market structure bias.

🔍 How It Works:

Green diamond lines mark bullish hidden reversal zones.

Red diamond lines mark bearish hidden reversal traps.

These lines only appear when volatility compresses and wick traps are confirmed within the trend context.

✅ Clean. Minimal. Tactical.

Ideal for scalpers, swing traders, and smart money enthusiasts looking to fade emotional price spikes.

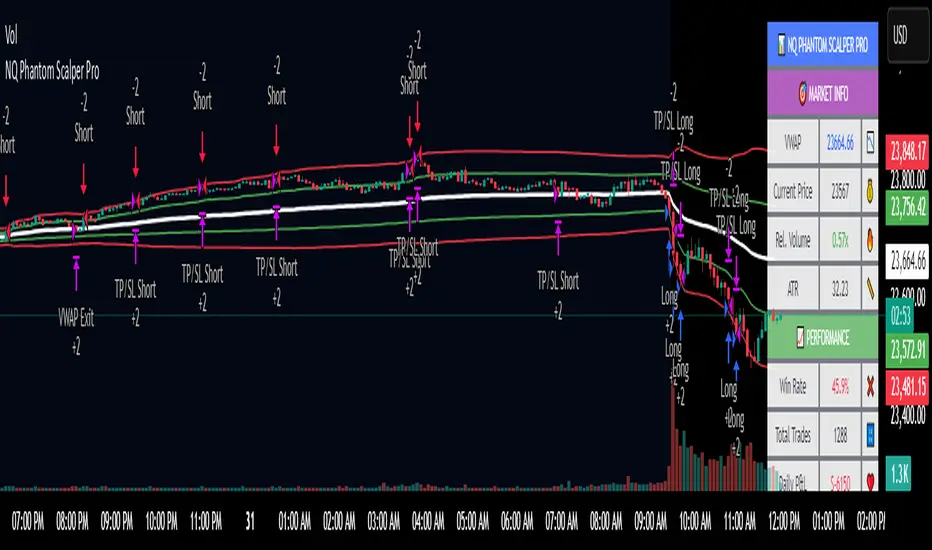

NQ Phantom Scalper Pro# 👻 NQ Phantom Scalper Pro

**Advanced VWAP Mean Reversion Strategy with Volume Confirmation**

## 🎯 Strategy Overview

The NQ Phantom Scalper Pro is a sophisticated mean reversion strategy designed specifically for Nasdaq 100 (NQ) futures scalping. This strategy combines Volume Weighted Average Price (VWAP) bands with intelligent volume spike detection to identify high-probability reversal opportunities during optimal market hours.

## 🔧 Key Features

### VWAP Band System

- **Dynamic VWAP Bands**: Automatically adjusting standard deviation bands based on intraday volatility

- **Multiple Band Levels**: Configurable Band #1 (entry trigger) and Band #2 (profit target reference)

- **Flexible Anchoring**: Choose from Session, Week, Month, Quarter, or Year-based VWAP calculations

### Volume Intelligence

- **Volume Spike Detection**: Only triggers entries when volume exceeds SMA by configurable multiplier

- **Relative Volume Display**: Real-time volume strength indicator in info panel

- **Optional Volume Filter**: Can be disabled for testing alternative setups

### Advanced Time Management

- **12-Hour Format**: User-friendly time inputs (9 AM - 4 PM default)

- **Lunch Filter**: Automatically avoids low-liquidity lunch period (12-2 PM)

- **Visual Time Zones**: Color-coded background for active/inactive periods

- **Market Hours Focus**: Optimized for peak NQ trading sessions

### Smart Risk Management

- **ATR-Based Stops**: Volatility-adjusted stop losses using Average True Range

- **Dual Exit Strategy**: VWAP mean reversion + fixed profit targets

- **Adjustable Risk-Reward**: Configurable target ratio to opposite VWAP band

- **Position Sizing**: Percentage-based equity allocation

### Optional Trend Filter

- **EMA Trend Alignment**: Optional trend filter to avoid counter-trend trades

- **Configurable Period**: Adjustable EMA length for trend determination

- **Toggle Functionality**: Enable/disable based on market conditions

## 📊 How It Works

### Entry Logic

**Long Entries**: Triggered when price touches lower VWAP band + volume spike during active hours

**Short Entries**: Triggered when price touches upper VWAP band + volume spike during active hours

### Exit Strategy

1. **VWAP Mean Reversion**: Early exit when price returns to VWAP center line

2. **Profit Target**: Fixed target based on percentage to opposite VWAP band

3. **Stop Loss**: ATR-based protective stop

### Visual Elements

- **VWAP Center Line**: Blue line showing volume-weighted fair value

- **Green Bands**: Entry trigger levels (Band #1)

- **Red Bands**: Extended levels for target reference (Band #2)

- **Orange EMA**: Trend filter line (when enabled)

- **Background Colors**: Yellow (lunch), Gray (after hours), Clear (active trading)

- **Info Panel**: Real-time metrics display

## ⚙️ Recommended Settings

### Timeframes

- **Primary**: 1-5 minute charts for scalping

- **Validation**: Test on 15-minute for swing applications

### Market Conditions

- **Best Performance**: Ranging/choppy markets with good volume

- **Trend Markets**: Enable trend filter to avoid counter-trend trades

- **High Volatility**: Increase ATR multiplier for stops

### Session Optimization

- **Pre-Market**: Generally avoided (low volume)

- **Morning Session**: 9:30 AM - 12:00 PM (high activity)

- **Lunch Period**: 12:00 PM - 2:00 PM (filtered by default)

- **Afternoon Session**: 2:00 PM - 4:00 PM (good volume)

- **After Hours**: Generally avoided (wide spreads)

## ⚠️ Risk Disclaimer

This strategy is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Trading futures involves substantial risk of loss and is not suitable for all investors. Users should:

- Thoroughly backtest on historical data

- Start with small position sizes

- Understand the risks of leveraged trading

- Consider transaction costs and slippage

- Never risk more than you can afford to lose

## 📈 Performance Tips

1. **Volume Threshold**: Adjust volume multiplier based on average NQ volume patterns

2. **Band Sensitivity**: Modify band multipliers for different volatility regimes

3. **Time Filters**: Customize trading hours based on your timezone and preferences

4. **Trend Alignment**: Use trend filter during strong directional markets

5. **Risk Management**: Always maintain consistent position sizing and risk parameters

**Version**: 6.0 Compatible

**Asset**: Optimized for NASDAQ 100 Futures (NQ)

**Style**: Mean Reversion Scalping

**Frequency**: High-Frequency Trading Ready

ATR Circle PlotTitle: ATR Circle Plot

Short Title: ATR Circle Plot

Description:

ATR Circle Plot is a dynamic overlay indicator that visualizes volatility-based levels around the open price of each bar, using the Average True Range (ATR). It plots two customizable levels—Upper and Lower ATR—calculated by multiplying the ATR by a user-defined factor (default: 1.0) and adding/subtracting it from the open price. These levels are displayed as colored circles on the chart, ideal for identifying potential breakout or stop-loss zones. A movable table summarizes the ATR value, Upper Level, and Lower Level with tick precision, and a new toggleable label feature displays these values directly on the chart for quick reference.

Perfect for traders in volatile markets like forex, futures, or stocks, this indicator helps set risk parameters or spot key price levels. Users can adjust the ATR timeframe, length, multiplier, table position, and circle colors to suit their strategy. The optional chart labels enhance usability by overlaying ATR metrics at the latest price levels, reducing the need to check the table during fast-moving markets.

Key Features:

Plots Upper and Lower ATR levels as colored circles around the open price.

Toggleable table (top/bottom, left/right) showing ATR and level values in ticks.

Optional chart labels for ATR, Upper, and Lower levels, toggleable via input.

Customizable ATR length, multiplier, timeframe, and colors for flexibility.

Lightweight and compatible with any chart timeframe.

How to Use:

Add the indicator to your chart and adjust the ATR length, multiplier, and timeframe as needed. Enable/disable the table or labels based on your preference. Use the Upper and Lower ATR levels as dynamic support/resistance or stop-loss guides. For example, place stops beyond the Upper/Lower levels or target breakouts when price crosses them. Combine with trend or momentum indicators for a robust setup.

Note: Leave the ATR Timeframe input empty to use the chart’s timeframe, or specify a higher timeframe (e.g., “D” for daily) for broader volatility context. Ensure your chart’s tick size aligns with the asset for accurate table values.

Tags: ATR, volatility, support resistance, stop loss, table, labels, breakout

Category: Volatility

Risk Context + Position SizingWhat This Indicator Does (And Doesn't Do)

This is NOT a buy/sell signal indicator. Instead, it's a risk management tool that helps you understand two critical things:

How volatile the market is right now (compared to recent history)

How much you should risk on your next trade based on that volatility

The Core Problem It Solves

Imagine you always risk the same amount on every trade - say $100. But sometimes the market is calm and predictable, other times it's wild and unpredictable. This indicator says: "Hey, the market is going crazy right now - maybe only risk $70 instead of your usual $100."

How It Works

Measures Market "Nervousness"

Uses ATR (Average True Range) to measure how much prices typically move each day

Compares today's volatility to the past 100 days

Shows you a percentile (0-100%) - higher = more volatile

Categorizes Risk Environment

LOW (green): Market is calm, you can size up slightly

NORMAL: Standard conditions, use your normal position size

HIGH (red): Market is jumpy, reduce your position size

EXTREME (dark red): Market is in chaos, significantly reduce size

Important Disclaimers

This doesn't predict price direction - it only measures current market stress

You still need a trading strategy - this just helps you size it properly

Past volatility doesn't guarantee future volatility

Always combine with proper stop losses and risk management

Sri_Momentum Burst Histogram📝 Description :

🌀 Sri_Momentum Burst Histogram — A Custom Momentum and Volatility Fusion Tool

The Sri_Momentum Burst Histogram is a unique technical analysis tool designed to visualize sudden changes in price momentum in the form of a dynamic, color-coded histogram. This indicator helps traders identify trend accelerations, early momentum shifts, and potential exhaustion in real time.

By combining a MACD-like momentum engine with a volatility-sensitive Bollinger Band range, this script offers an enhanced view of market bursts — moments where momentum "pops" beyond typical ranges. The result is a refined perspective on market sentiment, helping traders to anticipate reversals, follow breakouts, and assess the relative strength of ongoing trends.

🧠 Core Methodology

The indicator calculates the difference between a fast and slow EMA (Exponential Moving Average), similar to a MACD histogram.

This difference is then compared across candles to gauge the rate of change in momentum — referred to here as a “momentum burst.”

A sensitivity multiplier allows you to scale the response based on your preferred timeframe and trading style.

A volatility band, derived from Bollinger Band logic, is used to frame the relative intensity of the momentum change.

The histogram is divided into two parts:

Green/Lime Bars represent increasing and decreasing bullish momentum.

Red/Orange Bars represent increasing and decreasing bearish momentum.

⚙️ Customizable Inputs

Momentum Sensitivity: Adjust the responsiveness of the burst detection mechanism.

Short EMA Period: Sets the lookback period for the fast EMA.

Long EMA Period: Sets the lookback period for the slow EMA.

Volatility Band Length: Controls the length used for Bollinger Band calculations.

Band Std Dev Multiplier: Adjusts how wide the volatility range should be, based on price dispersion.

📈 How to Use It

Use the green/red histogram bars to visually gauge momentum strength and direction.

Watch for transitions in color intensity (e.g., green to lime, red to orange) as early warning signs of trend exhaustion or reversal.

Combine with other indicators like RSI, MACD, ADX, or volume profiles to confirm entry/exit points.

Useful in both trending and ranging markets, especially on lower timeframes for scalping or intraday setups.

✅ Key Features

Easy-to-read histogram with intuitive color coding.

Fully customizable settings for fine-tuned signal control.

Can be used on any asset class — stocks, forex, crypto, commodities.

Optimized for real-time use with minimal lag.

🔐 This script is an original creation, developed independently by adapting publicly known mathematical concepts into a unique visualization tool. All function and variable names have been customized for originality and compliance with TradingView’s publishing and community standards.

💡 Developed by: @venkat_27

🧩 For educational purposes only — not financial advice.

Navier-Cauchy Market Elasticity [PhenLabs]📊 Navier-Cauchy Market Elasticity

Version: PineScript™ v6

📌 Description

The Navier-Cauchy Market Elasticity (NCME) indicator takes a new step into technical analysis by applying materials science principles to financial markets. Similar to last weeks release utilizing Navier-Stokes dynamics equation this indicator focuses on the elastic interaction of virtual “solids”. Based on elasticity theory used in engineering, NCME treats price movements as material deformations, calculating market stress and strain using proven physics formulas. This unique approach reveals hidden market dynamics invisible to traditional indicators.

By implementing Lamé parameters and Young’s modulus calculations, NCME identifies critical stress points where markets exhibit extreme tension or compression. These zones often precede significant price movements, providing traders with advanced warning of potential reversals or breakouts.

🚀 Points of Innovation

• First indicator to apply Navier-Cauchy elasticity equations to market analysis

• Dynamic stress tensor calculations adapted for one-dimensional price movements

• Real-time Poisson ratio adjustments for market-specific elasticity modeling

• Gradient-based coloring system that visualizes stress intensity variations

• Advanced display modes with customizable visual layers for professional analysis

• Physics-based volatility normalization using Young’s modulus principles

🔧 Core Components

• Elasticity Engine: Calculates market elasticity using volatility-adjusted Young’s modulus

• Stress Tensor System: Computes normal stress values using Lamé parameters (λ and μ)

• Strain Measurement: Tracks price displacement relative to historical movement patterns

• Dynamic Bands: Statistical deviation bands that adapt to market elasticity changes

🔥 Key Features

• Four Display Modes: Choose between Histogram, Line, Both, or Advanced visualization

• Five Color Schemes: Modern, Classic, Neon, Ocean, and Fire themes with gradient support

• Background Stress Zones: Five distinct zones showing market stress levels visually

• Customizable Smoothing: Adjustable period for noise reduction without signal lag

• Extreme Value Detection: Automatic marking of critical stress points with visual alerts

• Advanced Mode Options: Glow effects, momentum ribbon, and extreme dots toggles

🎨 Visualization

• Stress Line: Primary indicator showing real-time market stress with gradient coloring

• Histogram Bars: Normalized stress values with dynamic opacity based on magnitude

• Reference Bands: Primary and secondary deviation bands for context

• Background Zones: Color-coded regions indicating stress intensity levels

• Signal Dots: Markers appearing at extreme stress points for easy identification

📖 Usage Guidelines

Display Settings

• Display Style

○ Default: Advanced

○ Options: Histogram, Line, Both, Advanced

○ Description: Controls visual presentation mode. Advanced offers the most comprehensive view with multiple layers

• Smoothing Period

○ Default: 3

○ Range: 1-50

○ Description: Moving average periods for noise reduction. Higher values create smoother signals but may introduce lag

Elasticity Parameters

• Displacement Length

○ Default: 14

○ Range: 1-100

○ Description: Lookback period for strain calculation. Shorter periods detect rapid stress changes

• Elasticity Length

○ Default: 30

○ Range: 1-200

○ Description: Period for volatility-based elasticity calculation. Longer periods provide more stable readings

• Poisson Ratio

○ Default: 0.3

○ Range: 0-0.5

○ Description: Theoretical elasticity ratio. 0.3 works well for most markets; adjust for specific asset classes

✅ Best Use Cases

• Identifying market tension before major breakouts

• Detecting compression zones during accumulation phases

• Confirming trend strength through stress persistence

• Timing reversals at extreme stress levels

• Multi-timeframe stress analysis for comprehensive market view

⚠️ Limitations

• Requires sufficient price history for accurate elasticity calculations

• May produce false signals during unprecedented market events

• Works best in liquid markets with consistent volume

• Not suitable as a standalone trading system

💡 What Makes This Unique

• Physics-Based Foundation: First indicator to properly implement elasticity theory

• Academic Rigor: Based on proven Navier-Cauchy equations from materials science

• Visual Innovation: Multiple display modes with professional-grade aesthetics

• Adaptive Technology: Self-adjusting parameters based on market conditions

🔬 How It Works

1. Strain Calculation:

• Measures price displacement over specified period

• Normalizes displacement relative to price level

2. Elasticity Determination:

• Calculates Young’s modulus using inverse volatility

• Updates Lamé parameters based on Poisson ratio

3. Stress Computation:

• Applies elasticity theory formula: σ = (λ + 2μ) × ε

• Scales result for visual clarity

• Applies smoothing to reduce noise

💡 Note: NCME represents a breakthrough in applying physics principles to market analysis. While based on proven scientific formulas, remember that markets are complex systems influenced by human psychology and external factors. Use NCME as part of a comprehensive trading strategy with proper risk management.

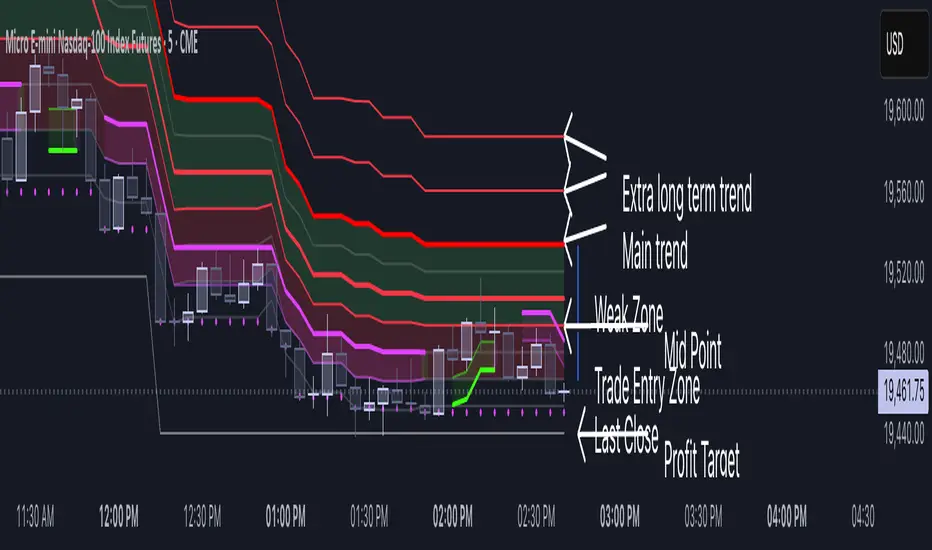

Volatility Layered Supertrend [NLR]We’ve all used Supertrend, but do you know where to actually enter a trade? Volatility Layered Supertrend (VLS) is here to solve that! This advanced trend-following indicator builds on the classic Supertrend by not only identifying trends and their strength but also guiding you to the best trade entry points. VLS divides the main long-term trend into “Strong” and “Weak” Zones, with a clear “Trade Entry Zone” to help you time your trades with precision. With layered trends, dynamic profit targets, and volatility-adaptive bands, VLS delivers actionable signals for any market.

Why I Created VLS Over a Plain Supertrend

I built VLS to address the gaps in traditional Supertrend usage and make trade entries clearer:

Single-Line Supertrend Issues: The default Supertrend sets stop-loss levels that are too wide, making it impractical for most traders to use effectively.

Unclear Entry Points: Standard Supertrend doesn’t tell you where to enter a trade, often leaving you guessing or entering too early or late.

Multi-Line Supertrend Enhancement: Many traders use short, medium, and long Supertrends, which is helpful but can lack focus. In VLS, I include Short, Medium, and Long trends (using multipliers 1 to 3), and add multipliers 4 and 5 to track extra long-term trends—helping to avoid fakeouts that sometimes occur with multiplier 3.

My Solution: I focused on the main long-term Supertrend and split it into “Weak Zone” and “Strength Zone” to show the trend’s reliability. I also defined a “Trade Entry Zone” (starting from the Mid Point, with the first layer’s background hidden for clarity) to guide you on where to enter trades. The zones include Short, Medium, and Long Trend layers for precise entries, exits, and stop-losses.

Practical Trading: This approach provides realistic stop-loss levels, clear entry points, and a “Profit Target” line that aligns with your risk tolerance, while filtering out false signals with longer-term trends.

Key Features

Layered Trend Zones: Short, Medium, Long, and Extra Long Trend layers (up to multipliers 4 and 5) for timing entries and exits.

Strong & Weak Zones: See when the trend is reliable (Strength Zone) or needs caution (Weak Zone).

Trade Entry Zone: A dedicated zone starting from the Mid Point (first layer’s background hidden) to show the best entry points.

Dynamic Profit Targets: A “Profit Target” line that adjusts with the trend for clear goals.

Volatility-Adaptive: Uses ATR to adapt to market conditions, ensuring reliable signals.

Color-Coded: Green for uptrends, red for downtrends—simple and clear.

How It Works

VLS enhances the main long-term Supertrend by dividing it into two zones:

Weak Zone: Indicates a less reliable trend—use tighter stop-losses or wait for the price to reach the Trade Entry Zone.

Strength Zone: Signals a strong trend—ideal for entries with wider stop-losses for bigger moves.

The “Trade Entry Zone” starts at the Mid Point (last layer’s background hidden for clarity), showing you the best area to enter trades. Each zone includes Short, Medium, Long, and Extra Long Trend sublevels (up to multipliers 4 and 5) for precise trade timing and to filter out fakeouts. The “Profit Target” updates dynamically based on trend direction and volatility, giving you a clear goal.

How to Use

Spot the Trend: Green bands = buy, red bands = sell.

Check Strength: Price in Strength Zone? Trend’s reliable—trade confidently. In Weak Zone? Use tighter stops or wait.

Enter Trades: Use the “Trade Entry Zone” (from the Mid Point upward) for the best entry points.

Use Sublevels: Short, Medium, Long, and Extra Long layers in each zone help fine-tune entries and exits.

Set Targets: Follow the Profit Target line for goals—it updates automatically.

Combine Tools: Pair with RSI, MACD, or support/resistance for added confirmation.

Settings

ATR Length: Adjust the ATR period (default 10) to change sensitivity.

Up/Down Colors: Customize colors—green for up, red for down, by default.

Volatility Momentum Breakout StrategyDescription:

Overview:

The Volatility Momentum Breakout Strategy is designed to capture significant price moves by combining a volatility breakout approach with trend and momentum filters. This strategy dynamically calculates breakout levels based on market volatility and uses these levels along with trend and momentum conditions to identify trade opportunities.

How It Works:

1. Volatility Breakout:

• Methodology:

The strategy computes the highest high and lowest low over a defined lookback period (excluding the current bar to avoid look-ahead bias). A multiple of the Average True Range (ATR) is then added to (or subtracted from) these levels to form dynamic breakout thresholds.

• Purpose:

This method helps capture significant price movements (breakouts) while ensuring that only past data is used, thereby maintaining realistic signal generation.

2. Trend Filtering:

• Methodology:

A short-term Exponential Moving Average (EMA) is applied to determine the prevailing trend.

• Purpose:

Long trades are considered only when the current price is above the EMA, indicating an uptrend, while short trades are taken only when the price is below the EMA, indicating a downtrend.

3. Momentum Confirmation:

• Methodology:

The Relative Strength Index (RSI) is used to gauge market momentum.

• Purpose:

For long entries, the RSI must be above a mid-level (e.g., above 50) to confirm upward momentum, and for short entries, it must be below a similar threshold. This helps filter out signals during overextended conditions.

Entry Conditions:

• Long Entry:

A long position is triggered when the current closing price exceeds the calculated long breakout level, the price is above the short-term EMA, and the RSI confirms momentum (e.g., above 50).

• Short Entry:

A short position is triggered when the closing price falls below the calculated short breakout level, the price is below the EMA, and the RSI confirms momentum (e.g., below 50).

Risk Management:

• Position Sizing:

Trades are sized to risk a fixed percentage of account equity (set here to 5% per trade in the code, with each trade’s stop loss defined so that risk is limited to approximately 2% of the entry price).

• Stop Loss & Take Profit:

A stop loss is placed a fixed ATR multiple away from the entry price, and a take profit target is set to achieve a 1:2 risk-reward ratio.

• Realistic Backtesting:

The strategy is backtested using an initial capital of $10,000, with a commission of 0.1% per trade and slippage of 1 tick per bar—parameters chosen to reflect conditions faced by the average trader.

Important Disclaimers:

• No Look-Ahead Bias:

All breakout levels are calculated using only past data (excluding the current bar) to ensure that the strategy does not “peek” into future data.

• Educational Purpose:

This strategy is experimental and provided solely for educational purposes. Past performance is not indicative of future results.

• User Responsibility:

Traders should thoroughly backtest and paper trade the strategy under various market conditions and adjust parameters to fit their own risk tolerance and trading style before live deployment.

Conclusion:

By integrating volatility-based breakout signals with trend and momentum filters, the Volatility Momentum Breakout Strategy offers a unique method to capture significant price moves in a disciplined manner. This publication provides a transparent explanation of the strategy’s components and realistic backtesting parameters, making it a useful tool for educational purposes and further customization by the TradingView community.

India VIXThe VIX chart represents the Volatility Index, commonly referred to as the "Fear Gauge" of the stock market. It measures the market's expectations of future volatility over the next 30 days, based on the implied volatility of NSE index options. The VIX is often used as an indicator of investor sentiment, reflecting the level of fear or uncertainty in the market.

Here’s a breakdown of what you might observe on a typical VIX chart:

VIX Value: The y-axis typically represents the VIX index value, with higher values indicating higher levels of expected market volatility (more fear or uncertainty), and lower values signaling calm or stable market conditions.

VIX Spikes: Large spikes in the VIX often correspond to market downturns or periods of heightened uncertainty, such as during financial crises or major geopolitical events. A high VIX is often associated with a drop in the stock market.

VIX Drops: A decline in the VIX indicates a reduction in expected market volatility, usually linked with periods of market calm or rising stock prices.

Trend Analysis: Technical traders might use moving averages or other indicators on the VIX chart to assess the potential for future market movements.

Inverse Relationship with the Stock Market: Typically, there is an inverse correlation between the VIX and the stock market. When stocks fall sharply, volatility increases, and the VIX tends to rise. Conversely, when the stock market rallies or remains stable, the VIX tends to fall.

A typical interpretation would be that when the VIX is low, the market is relatively stable, and when the VIX is high, the market is perceived to be uncertain or volatile.

VIX Spike StrategyThis script implements a trading strategy based on the Volatility Index (VIX) and its standard deviation. It aims to enter a long position when the VIX exceeds a certain number of standard deviations above its moving average, which is a signal of a volatility spike. The position is then exited after a set number of periods.

VIX Symbol (vix_symbol): The input allows the user to specify the symbol for the VIX index (typically "CBOE:VIX").

Standard Deviation Length (stddev_length): The number of periods used to calculate the standard deviation of the VIX. This can be adjusted by the user.

Standard Deviation Multiplier (stddev_multiple): This multiplier is used to determine how many standard deviations above the moving average the VIX must exceed to trigger a long entry.

Exit Periods (exit_periods): The user specifies how many periods after entering the position the strategy will exit the trade.

Strategy Logic:

Data Loading: The script loads the VIX data, both for the current timeframe and as a rescaled version for calculation purposes.

Standard Deviation Calculation: It calculates both the moving average (SMA) and the standard deviation of the VIX over the specified period (stddev_length).

Entry Condition: A long position is entered when the VIX exceeds the moving average by a specified multiple of its standard deviation (calculated as vix_mean + stddev_multiple * vix_stddev).

Exit Condition: After the position is entered, it will be closed after the user-defined number of periods (exit_periods).

Visualization:

The VIX is plotted in blue.

The moving average of the VIX is plotted in orange.

The threshold for the VIX, which is the moving average plus the standard deviation multiplier, is plotted in red.

The background turns green when the entry condition is met, providing a visual cue.

Sources:

The VIX is often used as a measure of market volatility, with high values indicating increased uncertainty in the market.

Standard deviation is a statistical measure of the variability or dispersion of a set of data points. In financial markets, it is used to measure the volatility of asset prices.

References:

Bollerslev, T. (1986). "Generalized Autoregressive Conditional Heteroskedasticity." Journal of Econometrics.

Black, F., & Scholes, M. (1973). "The Pricing of Options and Corporate Liabilities." Journal of Political Economy.

[KVA] KATRThe KATR indicator enhances the traditional ATR by leveraging the most common candle body percentage range, tailoring volatility measurement to specific market contexts. This advanced tool provides more relevant insights tailored to current market conditions.

Key Features:

Configurable ATR Length : Allows users to set the period for the ATR calculation, providing flexibility to adapt to different trading strategies and timeframes.

Multiple Smoothing Options : Offers a choice of RMA, SMA, EMA, and WMA for smoothing the ATR, enabling traders to select the method that best suits their analysis style.

Histogram Visualization for ATR Differences: The histogram visually represents the difference between the ATR and its moving average. This difference, or "dif," is calculated and smoothed, then multiplied by a user-defined factor. The histogram color indicates market conditions:

Light Red: Increasing but below zero, signaling potential weakening.

Light Green: Increasing and above zero, indicating strengthening.

Dark Green: Decreasing but above zero, showing potential weakening.

Dark Red: Decreasing and below zero, indicating strong weakening.

Ideal for Traders:

This indicator is perfect for traders seeking precise, context-sensitive volatility assessments to optimize trade timing and risk management strategies. Integrated seamlessly with other technical indicators, the KATR enhances your trading dashboard by adding depth to volatility analysis.

Detailed Explanation:

ATR Calculation: The ATR is derived by taking the average true range over a specified period, multiplied by the most common body percentage found in historical data.

Smoothing: Users can smooth the ATR using different methods, adding flexibility and customization to suit various trading styles.

Histogram: The histogram's primary function is to visualize the difference between the current ATR and its smoothed average. This provides clear, visual signals for potential volatility expansions or contractions, aiding in better decision-making.

Whether you're a day trader or a long-term investor, the KATR helps you stay ahead of market trends with reliable and easy-to-interpret insights. Elevate your trading strategy with the KATR's innovative approach to volatility measurement.

Chervolinos-Wave-PM-ForecastThe Wave PM (Whistler Active Volatility Energy – Price Mass) indicator is an oscillator described in Mark Whistler's book, Volatility Illuminated.

The Wave PM is specifically designed to help read volatility cycles. When we visualize volatility cycles as a chart, we can get a clear view of the market volatility phases in multiple time frames. This indicator forms an arithmetic mean over 30 observed periods. Traders can thus get a better insight into "potential" volatility from up to pent-up energy, the different zones give strong help to predict future price developments.

Possible interpretation patterns:

You are at the end of a long uptrend and you want to know if the price is going to go down, if the indicator shows red and the value is above 25, it is likely to do so.

You're in a downtrend and there's a bit of a recovery phase, so you might be wondering if it's going to continue when the indicator shows green. It would go further with yellow, but with green it can be assumed that it is going down rapidly.

Special thanks to sourcey who programmed the 3D Wave-PM.

This variant of sourcey looks very nice, but was too confusing for me. In order to get a strong overview, forming an arithmetic mean is very useful.

I hope you and the Mods like my version

Best regards, Chervolino

Elder Impulse System + ATR BandsDisregard the above chart, I am not sure why it isn't showing the one I want, which is linked below:

This is as far as I can tell the closest representation to Dr. Alexander Elder's updated "Elder Impulse System" that has added ATR-volatility bands up to 3x deviations from price. I got the idea from watching this recent video (www.youtube.com) of Dr. Elder reviewing some recent trades and noticed he had updated his system from his original books. The Impulse System colour coding was inspired by AstralLoverFlow and LazyBear. ATR Bands are pre-programmed Keltner Channels with some modifications such as filing in the ATR Zones with user-selected colour bands and modifying the ATR value to better suit the volatility of the market being traded.

The script has several components, which I will detail below:

Exponential Moving Averages:

1) A 13-period EMA that is used as a staple in all of Dr. Elder's technical analysis. He uses this EMA as the basis for all of his indicators and why it is included here.

2) A 26-period EMA which can be used as a base-line of sorts to filter when to go long or when to go short. For instance, price over the 26-EMA, price is strong and the rally upwards is likely to continue, underneath it, price is weak and likely to continue downwards for a time.

Volatility Bands:

By definition these are nothing more than 3 separate Keltner Channels of a 13-period EMA each set to one additional multiplier from the moving average. This gives us a 1x, 2x, and 3x multiplier of average volatility from the 13-period EMA based on a 14-period Average True Range (ATR) reading. The ATR was chosen as it accommodates price gaps and also is the standard formula calculation in TradingView. The values of the bands cannot be adjusted but the colour coding of them can be.

Elder Impulse System:

These colour-coded bars show you the strength and direction of the current chart resolution, calculated by the slope of a 13-period EMA and the slope of a MACD histogram. These are used not as a buying or selling recommendation alone but as trend filters, as per Dr. Elder's own description of them.

Green Bars = The 13-period EMA is sloping positively and the MACD histogram is rising compared to previous bars. The trader should only consider buying/long opportunities when a green bar is most recent.

Red Bars = The 13-period EMA is sloping negatively and the MACD histogram is falling compared to previous bars. The trader should only consider selling/short opportunities when a red bar is most recent.

Blue Bars = The 13-period EMA and the MACD histogram are not aligned. One of the indicators is sloping opposite to the other indicator. These are known as indecision bars and are typically seen near the end of a previously established trend. The trader can choose to wait for either a green or red bar to shape their trading bias if they are more risk-averse while a counter-trend trader may decide to try opening a position against the currently-established trend.

How To Trade the System:

This system is unique in that it is so versatile and will fit the styles of many traders, be it trend following traders (generally the original Elder Impulse System design) or mean-reversion/counter-trend trading (the original Keltner Channel design). None of the examples below or in the chart above are financial advice and are just there for demonstration purposes only.

1) The most basic signal given would be the moving average cross up or down. A cross of the 13-EMA over the 26-EMA signals upward trend strength and the trader could look for buying opportunities. Conversely, the 13-EMA under the 26-EMA shows downward trend strength and the trader could look for selling opportunities.

2) Following the Elder Impulse system in conjunction with the EMAs. Look for long opportunities when a green bar is printed and price is over both of the 13- and 26-period EMAs. Look for short opportunities when a red bar is printed and price is below both of the 13- and 26-period EMAs. Keep in mind this does not necessarily need a moving average cross to be viable, a green or red bar over both EMAs is a valid signal in this system, usually. Examine price more closely for better entry signals when a blue bar is printed and price is either above or below both EMAs if you are a trend trader. This is how Dr. Elder originally intended the system to be used in conjunction with his famous Triple Screen Trading System. I am not going into detail here as it is a deep subject but I would suggest an interested trader to examine this Triple Screen System further as it is widely accepted as a strong strategy.

3) Mean Reversion and Counter-Trend Trading. Dr. Elder mentions that the zone between the two EMAs is called the Value Zone. A mean reversion trader could look for buying opportunities if price has generally been in an uptrend and falls back to value, conversely, they could look for shorting opportunities if price has generally been in a downtrend and rises back to value. These are your very basic pull backs found in trends that create your higher lows in an uptrend or your lower highs in a downtrend. A mean reversion/scalper trader may also look to use the upper and lower most ATR bands as an indication of price being overbought or oversold and could look to enter a counter-trend trade here once a blue indecision bar is printed and to ride that move back down to the Value Zone.

Taking Profits and Risk Management

This system again is very versatile and will fit a wide range of trading styles. It has built in take profit levels and risk management depending on your style of trading.

1a) In original Triple Screen Trading (and the original Elder Impulse system), a trader was to place a buy order one tick above a newly printed green bar with a stop loss one tick below the most recent 2-day low, and vice-versa for red bars on short selling. as long as other criteria were met, that I will not go into. It is all over YouTube and in his books and on Investopedia if you want more information. The general idea is to continue the trend in the direction if price is strong and you are bought into that move with a close stop, or if price falls back a little bit, you can get in at a better price. This would be a system typically better suited to a scalper.

1b) The updated risk management according to the above video is to place a stop loss at least 2ATR away from price. These bands already have calculated these values so a trader can place a stop one tick below the 2 or even 3ATR zones depending on their risk appetite. This is assuming you have already received a strong buy signal based on the system you follow. This would be a system typically better suited to a trend-trader.

2a) Taking profits if you are a trend trader has several possibilities. The first, as Dr. Elder suggests, is to place a price target 2ATR values away from your entry giving you approximately a 1:1 risk-reward ratio.

2b) The second possibility if the trade is successful is to ride the trend upwards until a blue bar is printed, suggesting indecision in the market. A modified version of this that could let a winning trade run longer is to wait for the price to close under the 13-EMA in fast markets, or close under the 26-EMA in slightly slower markets to maximize potential winnings.

2c) A scalper trader may wish to have a target at either the value zone if they are playing an extended buy/short back to the mean, or if they are being at the mean, to sell or cover when price extends back out to the 2x or 3x zone.

3) Trend traders can additionally use the ATR zones as a sort of safety guidelines for entering a trade. Anything within the 1ATR zone is typically a safer entry as the market is less volatile at this time. Entering when price has gone into the 2ATR zone is signaled as a strong momentum move and can signal a stronger move in the direction of the current closing bar. While not always the case, it is suggested by Dr. Elder to not enter trend trades at the 3ATR zone as this is where you will be likely looking for a counter-trend retracement back to value and a trader entering here in the direction of the trade has a higher chance of being stopped out or not getting in at the best possible price.

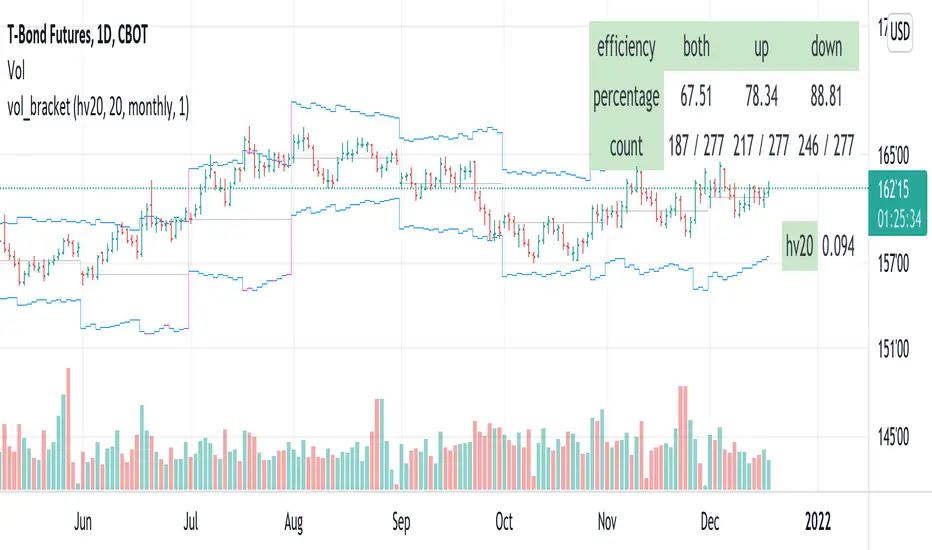

vol_bracketThis simple script shows an "N" standard deviation volatility bracket, anchored at the opening price of the current month, week, or quarter. This anchor is meant to coincide roughly with the expiration of options issued at the same interval. You can choose between a manually-entered IV or the hv30 volatility model.

Unlike my previous scripts, which all show the volatility bracket as a rolling figure, the anchor helps to visualize the volatility estimate in relation to price as it ranges over the (approximate) lifetime of a single, real contract.

Standard Error of the Estimate -Jon Andersen- V2Original implementation idea of bands by:

Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

Standard Error Bands are quite different than Bollinger's.

First, they are bands constructed around a linear regression curve.

Second, the bands are based on two standard errors above and below this regression line.

The error bands measure the standard error of the estimate around the linear regression line.

Therefore, as a price series follows the course of the regression line the bands will narrow , showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands .

Thanks to the work of @glaz & @XeL_arjona

In this version you can change the type of moving averages and the source of the bands.

Add a few studies of @dgtrd

1- ADX Colored Directional Movement Line

Directional Movement (DMI) (created by J. Welles Wilder ) consists of the Average Directional Index ( ADX ), to define whether or not there is a trend present, and Plus Directional Indicator (+D I) and Minus Directional Indicator (-D I) serve the purpose of determining trend direction

ADX Colored Directional Movement Line is custom interpretation of Directional Movement (DMI) with aim to present all 3 DMI indicator components with SINGLE line and ability to be added on top of the price chart (main chart)

How to interpret :

* triangle shapes:

▲- bullish : diplus >= diminus

▼- bearish : diplus < diminus

* colors:

green - bullish trend : adx >= strongTrend and di+ > di-

red - bearish trend : adx >= strongTrend and di+ < di-

gray - no trend : weekTrend < adx < strongTrend

yellow - week trend : adx < weekTrend

* color density:

darker : adx growing

lighter : adx falling

2- Volatility Colored Price/MA Line

Custom interpretation of the idea “Prices high above the moving average (MA) or low below it are likely to be remedied in the future by a reverse price movement”. Further details can be found under study “Price Distance to its MA by DGT”

How to interpret :

-▲ – Bullish , Price Action above Moving Average

-▼ – Bearish , Price Action below Moving Average

-Gray/Black - Low Volatility

-Green/Red – Price Action in Threshold Bands

-Dark Green/Red – Price Action Exceeds Threshold Bands

3- Volume Weighted Bar s

Volume Weighted Bars, a study of Kıvanç Özbilgiç, aims to present whether volume supports price movements. Volume Weighted Bars are calculated based on volume moving average.

How to interpret :

-Volume high above the volume moving average be displayed with red/green colors

-Average volume values will remain as they are and

-Volume low below the volume moving average will be indicated with darker colors

4- Fear & Greed index value, using technical anlysis approach calculated based on :

⮩1 - Price Momentum : Price Distance to its Moving Average

⮩2 - Strenght : Rate of Return, price movement over a period of time

⮩3 - Money Flow : Chaikin Money Flow, quantify changes in buying and selling pressure. CMF calculations is based on Accumulation/Distribution

⮩4 - Market Volatility : CBOE Volatility Index ( VIX ), the Volatility Index, or VIX , is a real-time market index that represents the market's expectation. It provides a measure of market risk and investors' sentiments

⮩5 -Safe Haven Demand: in this study GOLD demand is assumed

Williams Vix Fix BB + RVI + LinReg & Squeeze (Keltner) BBW + %BLegend:

Entery signal: When line color turns to lime (lighter green) after a blue dot appears

Exit signal: When line color turns to red (darker red) after a red dot appears

Note: it is more affective as an entry signal (Bottom is stronger)

- When line touches or crosses red band it is Top signal (Williams Vix Fix)

- When line touches or crosses blue band it is Bottom signal (Williams Vix Fix)

- Red dot at the top of indicator is a Top signal (Relative Volatility Index)

- Blue dot at the top of indicator is a Bottom signal (Relative Volatility Index)

- Gray dot at the bottom of indicator is a Keltner Squeeze signal (filtered by either BBW or %B)

- Silver dot at the bottom of indicator is a weaker Keltner Squeeze signal (Doesn't meet either BBW or %B filter)

- Purple is a 'Half Squeeze' only 1 Bollinger Band crossed the Keltner Channel

This is an attempt to make use of the main features of all 6 of these Volatility tools:

- Williams Vix Fix + Bollinger Bands

- Relative Volatility Index (RVI)

- Linear Regression (detects Vix Fix starts to rise or fall to a certain degree in order to help validate bottom/top)

Note : There is also added precision on Linear Regression entry by dividing WVF by square roots of basis.

- The crossing of Keltner Channel by the Bollinger Bands (Squeeze)

Conditions to Help Filter Keltner Squeeze:

- When the Bollinger Bands Width (BBW) value is lower than the lowest value within a period plus a margin of error (percentage)

- When the %B value goes up or down by the impulse value (threshold value in setting) detailed in LazyBears indicator. (www.tradingview.com)

If it meets one of these 2 filters and there is a Keltner Channel Squeeze than gray color or else if the squeeze doesn’t meet one of the 2 filters than silver color (weaker Squeeze).

The goal is to find the best tool to find bottoms and top relative to volatility and filter squeeze.

Note: You can also change the threshold for RVI top and bottom.

And this work builds on my last indicators:

- Williams Vix Fix + BB & RVI (Top/Bottom) & Squeeze ()

- Williams Vix Fix BB + RVI & Squeeze (Keltner) filtered BBW + %B ()

If you have ideas on this work or have ideas on potential combinations please message me, I always want to learn or get perspective on how it can be improved.

Sharing is how we get better (Parameter tuning, ideas, discussion)

I don’t reinvent the wheel, just trying to make the wheel better.

BBW, Squeeze, and EMAThis indicator helps traders to identify low volatility areas by using the "Bollinger Bands Squeeze" method. The idea is to look for the lowest values in the Bollinger bands width to judge the lowest volatility readings.

By default the squeeze period is 125, as suggested by John Bollinger.

The indicator is a variation on the BB Squeeze indicator by @danarm. It adds:

* A lowest volatility print, named "Squeeze Line". This shows traders the lowest BBW reads.

* A moving average on top of BBW. This helps traders gauge volatility expansion. I'd use is like this: once you identify volatility contraction, an expansion would be when BBW crosses its average upwards.

* The blue background color indicates where BBW crossed its lowest 125 value, indicating further volatility contraction.

BankNifty Multi-TimeFrames Price Panel [MaestroTrader]█ OVERVIEW

Price Panel provides Nifty /BankNifty Index comprehensive Price Insights on different time intervals. It helps to determine the trend of Index using top Index Heavy Weights along with Dow, India VIX & Index Spot Prices. It helps to determine the price behavior of the underlying Index/stock to make informed decisions while trading.

█ FEATURES

a) Displays Price in Multi Time Frames for Multi time frame analysis

b) Displays Weighted Securities price for Weighted INDEX price analysis.

c) Displays INDIA VIX and DOW for Combined INDIX VOLATALITY Analysis

█ MUTLI TIME FRAME ANALYSIS

How to use Multiple time frame analysis?

Multiple time frame analysis follows a top-down approach when trading and allows traders to gauge the longer-term trend while spotting ideal entries on a smaller time frame. Traders can then conduct technical analysis using multiple time frames to confirm or reject their trading bias.

Multiple time frame analysis, is the process of viewing the same symbols under different time frames. Usually, the larger time frame is used to establish a longer-term trend, while a shorter time frame is used to spot ideal entries into the market.

Let’s Say 75 & 15 TF’s Trend is up, then shorter time 5M is used to spot ideal entries on long side.

█ WEIGHTED INDEXS PRICE ANALYSIS

How to use Weighted Index Price Movement in Multi timeframes?

The index future trading price is based on the trading prices of the individual securities (stocks) that comprise the index basket. In other words, the stocks with higher weights will have more impact on the movement of the index. Price Panel provides the insights of these heavy weight stock price movement in different time frames, that can help you confirm or reject your trading bias.

HDFC Bank (28% Weight) will have more impact on the BankNifty Movement. By looking the top 4 bank's price movement in different timeframes, you can derive the BankNifty price trend.

█ VOLATALITY ANALYSIS

India VIX is a short form for India Volatility Index. It is the volatility index that measures the market’s expectation of volatility over the near term.

A lower VIX level usually implies that the market is confident about the movement and is expecting lower volatility and a stable range.

A higher VIX level usually signals high volatility and lower trader confidence about the current range of the market. A major directional move can be expected in the market and a quick broadening of range can be expected.

█ SETTINGS

• Time Frame Settings: Configure Time Frames 5 Min, 15 Min, 75 Min

• Table Settings: Configure Table Styles- Position- Font Color

• Symbol Settings: Configure Securities. Toggle (on/Off) Securities display.

• Index Settings: Display Bank Nifty or Nifty Heavy Weights.

█ PANEL DISPLAY VARIATIONS

BANK NIFTY VIEW

NIFTY VIEW

WITHOUT STOCKS - ONLY INDEX, VIX, DOW

█ THANKS

Thanks to Pine Team for this new great feature tables & Thanks to PineCoders for the `f_strRightOf` function.

█ DISCLIAMER

Indicator is built for educational purposes. Test it before use.

Hope - These features help you get quick insights of the price movement to take informed trades.

You are free to use the code, please share the credit for reuse.

Happy Trading !!

Bollinger Band Calculation ToolIntroducing the Bollinger Band Calculation Tool

What are Bollinger Bands ?

According to Investopedia ....

"In the 1980s, John Bollinger, a long-time technician of the markets, developed the technique of using a moving average with two trading bands above and below it.

Unlike a percentage calculation from a normal moving average, Bollinger Bands® simply add and subtract a standard deviation calculation.

Standard deviation is a mathematical formula that measures volatility, showing how the stock price can vary from its true value.

By measuring price volatility, Bollinger Bands® adjust themselves to market conditions.

This is what makes them so handy for traders; they can find almost all of the price data needed between the two bands."

Classic interpretations of Bollinger bands from Fidelity Investments....

"When the bands tighten during a period of low volatility, it raises the likelihood of a sharp price move in either direction.

This may begin a trending move. Watch out for a false move in opposite direction which reverses before the proper trend begins.

When the bands separate by an unusual large amount, volatility increases and any existing trend may be ending.

Prices have a tendency to bounce within the bands' envelope, touching one band then moving to the other band.

You can use these swings to help identify potential profit targets.

For example, if a price bounces off the lower band and then crosses above the moving average, the upper band then becomes the profit target.

Price can exceed or hug a band envelope for prolonged periods during strong trends.

On divergence with a momentum oscillator, you may want to do additional research to determine if taking additional profits is appropriate for you.

A strong trend continuation can be expected when the price moves out of the bands.

However, if prices move immediately back inside the band, then the suggested strength is negated."

This indicator contains a standard set of Bollinger Bands with the addition of a Test Closing Price calculation function.

It displays a standard set of Bollinger Bands by default.

How do I use the Test Closing Price function ?

Enter a test price in the Test Closing Price box in the settings, and then click the "Use Test Price" button.

The indicator will then replace the current Bollinger upper, lower and basis-lines with plots showing the resultant lines if price were to close at the Test Closing Price.

An information panel will appear which displays the test closing price and the resulting Bollinger-upper, Bollinger-lower and basis-line prices.

Can display up to 10 decimal places and has adjustable label offset.

It will also plot lines outlining the resultant closed candle body for clarity.

To return to "Standard Bollingers" just click off the "Use Test Price" button.

Knowing exactly what the Bollinger bands and Basis will do if a particular closing price is met can be useful in a variety of ways to traders who use Bollinger Bands® in their trading.

It is possible to work out exactly what closing price is required to get above or below a Bollinger band which is normally difficult as Bollingers react to the change in price.

Users can also experiment with different Test Closing Prices [/i to see exactly what effect this would have on the Basis moving average and on the Bollinger bands themselves.

MOVE/VXTLT CorrelationMany know of the VIX for equity trading. Yet, many are unaware that there is the same kind of volatility measure for trading bonds, called the MOVE Index.

"The Merrill Lynch Option Volatility Estimate (MOVE) Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options which are weighted on the 2, 5, 10, and 30 year contracts."

With this script one can see the the correlation and divergences between bonds and its volatility measure to make educated decisions in trading or hedging.

The idea of this script comes from NicTheMajestic.