LuxAlgo - Backtester (OSC)The OSC Backtester is an innovative strategy script that allows users to create a wide variety of strategies using various unique oscillators.

By utilizing our 'Step' and 'Match' algorithms, users can create custom and complex strategy entries from each of the supported oscillators and included conditions, as well as any external sources, allowing users to create entries from a sequence of conditions and/or multiple matching conditions.

We included a complete alert system that will send a notification for each action taken by the strategy and we also allow users to set custom messages for each action taken by a strategy.

🔶 Features

🔹 Step & Match Algorithm

More complex entry rules can be created by using multiple conditions together, this is done thanks to the Step dropdown setting on the right of each condition.

The Step setting is directly related to the Step & Match algorithm and works in two ways:

When two or more conditions have the same step number, both conditions are evaluated. Used to test matching conditions.

When two or more conditions have different step numbers, each conditions will be evaluated in order, testing for the first step and switching to the next step once the previous one is true. When the final step is true the strategy will open a market order. Used to create sequence of conditions.

This operation is complementary, as you can create a sequence of conditions with one step consisting of two or more matching conditions as long as they have the same step number.

🔹 Fully Customizable Entries From Various Oscillators And Conditions

We allow the users to set entries using our unique HyperWave, Smart Money Flow, and their derived conditions as entries.

The Hyper Wave is a normalized adaptive oscillator aiming to reflect price trends without returning a high amount of noise.

The Smart Money Flow aims to detect trends based on market activity, by doing a comparative analysis between current volume and historical volume. A Smart Money Flow above 50 suggest market participants are bullish, else bearish. Derived from this oscillator we have Overflow indications, this indicator detects when market is overbought or oversold based on participants activity.

Other entries include proprietary reversal signals, real-time divergence detection, oscillator confluence (indicating how aligned each oscillator is), as well as entries using external sources.

🔹 Complete Alert System

Users can get alerted for any action executed by a strategy, from opening positions to closing them.

The message field in the Alert Messages setting section allows for the strategy to send a custom alert message depending on the action taken by the strategy, if no messages are set the strategy will send default messages.

🔶 Usage

Users can create a wide variety of strategies from this script, whether they are trend-following or contrarian traders.

Let's see a contrarian (revesal-based) strategy example using the following entry conditions:

Long: Hyperwave bullish divergence and oversold Hyperwave (lower than 20).

Short: Hyperwave bearish divergence and overbought Hyperwave (greater than 20).

We can also introduce take-profit and stop-loss exit conditions based on external indicators, allowing more control over exits in our strategy. For example:

Long: Hyperwave crossing over 50 while money flow is bearish.

Short: Hyperwave crossing under 50 while money flow is bullish.

Exit Long on a profit (long exit tp): Hyperwave crossing 80.

Exit Short on a profit (short exit tp): Hyperwave crossing 20.

While this strategy script can be used as a standalone, we recommend using other indicators creatively to assist with entries and exits as well as TP/SLs.

Our Step & Match algorithm can magnify interoperability, allowing for way more complete strategies through complex conditions, let's demonstrate this using the following entries:

Long: Any bullish reversal occurring after the price crosses over the lowest upper reversal zone of the Signals & Overlays™.

Short: Any bearish reversal occurring after the price crosses under the highest lower reversal zone of the Signals & Overlays™.

Long TP/SL: 5 ATR's away from the entry price.

Short TP/SL: 5 ATR's away from the entry price.

🔶 Strategy Properties (Important)

This script backtest is done on daily EURGBP, using the following backtesting properties:

Balance (default): 10 000 (default base currency)

Order Size: 10% of the equity

Comission: 3.4 pips (average spread for EURGBP)

Slippage: 3 tick

Stop Loss: 0.02 points away from entry price

We use these properties to ensure a realistic preview of the backtesting system, do note that default properties can be different for various reasons described below:

Order Size: 1 contract by default, this is to allow the strategy to run properly on most instruments such as futures.

Comission: Comission can vary depending on the market and instrument, there is no default value that might return realistic results.

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from the strategies built are realistic.

🔶 How To Access

You can see the Author's Instructions below to learn how to get access.

Tìm kiếm tập lệnh với "alert"

LuxAlgo - Backtester (PAC)The PAC Backtester is an innovative strategy script that allows users to create a wide variety of strategies derived from price action-related concepts for a data-driven approach to discretionary trading strategies.

Thanks to our 'Step' and 'Match' algorithm, users can create custom and complex strategy entries and exits from features such as market structure, order blocks, imbalances, as well as any external indicators, allowing users to create entries from a sequence of conditions and/or multiple matching conditions.

We included a complete alert system that will send a notification for each action taken by the strategy and we also allow users to set custom messages for each action taken by a strategy.

🔶 Features

🔹 Step & Match Algorithm

More complex entry rules can be created by using multiple conditions together, this is done thanks to the Step dropdown setting on the right of each condition.

The Step setting is directly related to the Step & Match algorithm and works in two ways:

When two or more conditions have the same step number, both conditions are evaluated. Used to test matching conditions.

When two or more conditions have different step numbers, each condition will be evaluated in order, testing for the first step and switching to the next step once the previous one is true. When the final step is true the strategy will open a market order. Used to create a sequence of conditions.

This operation is complementary, as you can create a sequence of conditions with one step consisting of two or more matching conditions as long as they have the same step number.

🔹 Fully Customizable Price Action Concepts As Entries

We allow the users to use market structures, order blocks, imbalances, and external sources together to set their custom entry and exit conditions.

Market structures are commonly used to determine trend direction by indicating when prices break prior swing points. Their occurrence can be used as entry conditions.

Order blocks highlight areas where institutional market participants open positions, one can use order blocks to determine confirmation entries or potential targets as we can expect there is a large amount of liquidity at these order blocks. Price entering, being within, or mitigating an order block can be used as an entry condition.

Market imbalances highlight areas where there is a disparity between supply and demand. Price entering, being within, or mitigating an imbalance can be used as an entry condition.

This system also allows the use of external sources to create entry and exit conditions, such as moving averages, bands, trailing stops...etc.

🔹 Complete Alert System

Users can get alerted for any action executed by a strategy, from opening positions to closing them.

The message field in the Alert Messages setting section allows for the strategy to send a custom alert message depending on the action taken by the strategy, if no messages are set the strategy will send default messages.

🔶 Usage

Users can create complete price action strategies from this script, let's see an example using the following entry conditions:

Long: Mitigated bearish order block occurring during the New York session after a mitigated bearish imbalance.

Short: Mitigated bullish order block occurring during the New York session after a mitigated bullish imbalance.

Take Profit: 2 points away from the entry price.

Stop Loss: 1 point away from the entry price.

We can also use features from Price Action Concepts™ to construct custom exit conditions, leading to the following strategy conditions:

Long: Bullish CHoCH and price mitigates bearish FVG.

Short: Bearish CHoCH and price mitigates bullish FVG.

Exit Long: Price mitigates bearish order block.

Exit Short: Price mitigates bullish order block.

Users can achieve a wide variety of results by using external indicators as an input source for entries and exits, combining the best from price action and technical indicators. We might for example be interested in exiting a position when the RSI oscillator is overbought or oversold.

🔶 Strategy Properties (Important)

This script backtest is done on daily EURGBP, using the following backtesting properties:

Balance (default): 10 000 (default base currency)

Order Size: 10% of the equity

Comission: 3.4 pips (average spread for EURGBP)

Slippage: 1 tick

Stop Loss: 0.01 points away from entry price

We use these properties to ensure a realistic preview of the backtesting system, do note that default properties can be different for various reasons described below:

Order Size: 1 contract by default, this is to allow the strategy to run properly on most instruments such as futures.

Comission: Comission can vary depending on the market and instrument, there is no default value that might return realistic results.

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from strategies built are realistic.

🔶 How to access

You can see the Author's Instructions below to learn how to get access.

Long-Only Opening Range Breakout (ORB) with Pivot PointsIntraday Trading Strategy: Long-Only Opening Range Breakout (ORB) with Pivot Points

Background:

Opening Range Breakout (ORB) is a popular long-only trading strategy that capitalizes on the early morning volatility in financial markets. It's based on the idea that the initial price movements during the first few minutes or hours of the trading day can set the tone for the rest of the session. The strategy involves identifying a price range within which the asset trades during the opening period and then taking long positions when the price breaks out to the upside of this range.

Pivot Points are a widely used technical indicator in trading. They represent potential support and resistance levels based on the previous day's price action. Pivot points are calculated using the previous day's high, low, and close prices and can help traders identify key price levels for making trading decisions.

How to Use the Script:

Initialization: This script is written in Pine Script, a domain-specific language for trading strategies on the TradingView platform. To use this script, you need to have access to TradingView.

Apply the Script: You can do this by adding it to your favorites, then selecting the script in the indicators list under favorites or by searching for it by name under community scripts.

Customize Settings: The script allows you to customize various settings through the TradingView interface. These settings include:

Opening Session: You can set the time frame for the opening session.

Max Trades per Day: Specify the maximum number of long trades allowed per trading day.

Initial Stop Loss Type: Choose between using a percentage-based stop loss or the previous candles low for stop loss calculations.

Stop Loss Percentage: If you select the percentage-based stop loss, specify the percentage of the entry price for the stop loss.

Backtesting Start and End Time: Set the time frame for backtesting the strategy.

Strategy Signals:

The script will display pivot points in blue (R1, R2, R3, R4, R5) and half-pivot points in gray (R0.5, R1.5, R2.5, R3.5, R4.5) on your chart.

The green line represents the opening range.

The script generates long (buy) signals based on specific conditions:

---The open price is below the opening range high (h).

---The current high price is above the opening range high.

---Pivot point R1 is above the opening range high.

---It's a long-only strategy designed to capture upside breakouts.

---It also respects the maximum number of long trades per day.

The script manages long positions, calculates stop losses, and adjusts long positions according to the defined rules.

Trailing Stop Mechanism

The script incorporates a dynamic trailing stop mechanism designed to protect and maximize profits for long positions. Here's how it works:

1. Initialization:

The script allows you to choose between two types of initial stop loss:

---Percentage-based: This option sets the initial stop loss as a percentage of the entry price.

---Previous day's low: This option sets the initial stop loss at the previous day's low.

2. Setting the Initial Stop Loss (`sl_long0`):

The initial stop loss (`sl_long0`) is calculated based on the chosen method:

---If "Percentage" is selected, it calculates the stop loss as a percentage of the entry price.

---If "Previous Low" is selected, it sets the stop loss at the previous day's low.

3. Dynamic Trailing Stop (`trail_long`):

The script then monitors price movements and uses a dynamic trailing stop mechanism (`trail_long`) to adjust the stop loss level for long positions.

If the current high price rises above certain pivot point levels, the trailing stop is adjusted upwards to lock in profits.

The trailing stop levels are calculated based on pivot points (`r1`, `r2`, `r3`, etc.) and half-pivot points (`r0.5`, `r1.5`, `r2.5`, etc.).

The script checks if the high price surpasses these levels and, if so, updates the trailing stop accordingly.

This dynamic trailing stop allows traders to secure profits while giving the position room to potentially capture additional gains.

4. Final Stop Loss (`sl_long`):

The script calculates the final stop loss level (`sl_long`) based on the following logic:

---If no position is open (`pos == 0`), the stop loss is set to zero, indicating there is no active stop loss.

---If a position is open (`pos == 1`), the script calculates the maximum of the initial stop loss (`sl_long0`) and the dynamic trailing stop (`trail_long`).

---This ensures that the stop loss is always set to the more conservative of the two values to protect profits.

5. Plotting the Stop Loss:

The script plots the stop loss level on the chart using the `plot` function.

It will only display the stop loss level if there is an open position (`pos == 1`) and it's not a new trading day (`not newday`).

The stop loss level is shown in red on the chart.

By combining an initial stop loss with a dynamic trailing stop based on pivot points and half-pivot points, the script aims to provide a comprehensive risk management mechanism for long positions. This allows traders to lock in profits as the price moves in their favor while maintaining a safeguard against adverse price movements.

End of Day (EOD) Exit:

The script includes an "End of Day" (EOD) exit mechanism to automatically close any open positions at the end of the trading day. This feature is designed to manage and control positions when the trading day comes to a close. Here's how it works:

1. Initialization:

At the beginning of each trading day, the script identifies a new trading day using the `is_newbar('D')` condition.

When a new trading day begins, the `newday` variable becomes `true`, indicating the start of a new trading session.

2. Plotting the "End of Day" Signal:

The script includes a plot on the chart to visually represent the "End of Day" signal. This is done using the `plot` function.

The plot is labeled "DayEnd" and is displayed as a comment on the chart. It signifies the EOD point.

3. EOD Exit Condition:

When the script detects that a new trading day has started (`newday == true`), it triggers the EOD exit condition.

At this point, the script proceeds to close all open positions that may have been active during the trading day.

4. Closing Open Positions:

The `strategy.close_all` function is used to close all open positions when the EOD exit condition is met.

This function ensures that any remaining long positions are exited, regardless of their current profit or loss.

The function also includes an `alert_message`, which can be customized to send an alert or notification when positions are closed at EOD.

Purpose of EOD Exit

The "End of Day" exit mechanism serves several essential purposes in the trading strategy:

Risk Management: It helps manage risk by ensuring that positions are not left open overnight when markets can experience increased volatility.

Capital Preservation: Closing positions at EOD can help preserve trading capital by avoiding potential adverse overnight price movements.

Rule-Based Exit: The EOD exit is rule-based and automatic, ensuring that it is consistently applied without emotions or manual intervention.

Scalability: It allows the strategy to be applied to various markets and timeframes where EOD exits may be appropriate.

By incorporating an EOD exit mechanism, the script provides a comprehensive approach to managing positions, taking profits, and minimizing risk as each trading day concludes. This can be especially important in volatile markets like cryptocurrencies, where overnight price swings can be significant.

Backtesting: The script includes a backtesting feature that allows you to test the strategy's performance over historical data. Set the start and end times for backtesting to see how the long-only strategy would have performed in the past.

Trade Execution: If you choose to use this script for live trading, make sure you understand the risks involved. It's essential to set up proper risk management, including position sizing and stop loss orders.

Monitoring: Monitor the long-only strategy's performance over time and be prepared to make adjustments as market conditions change.

Disclaimer: Trading carries a risk of capital loss. This script is provided for educational purposes and as a starting point for your own long-only strategy development. Always do your own research and consider seeking advice from a qualified financial professional before making trading decisions.

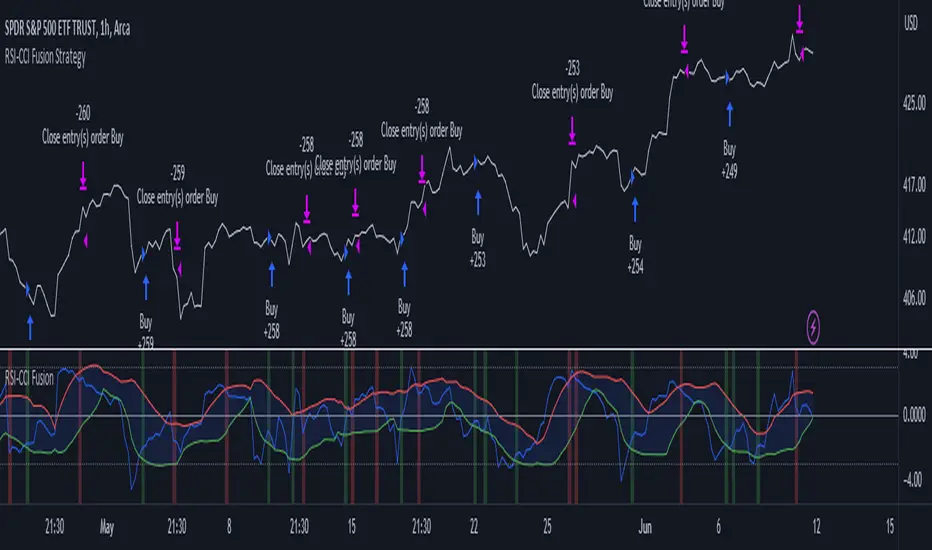

RSI-CCI Fusion StrategyRSI-CCI Fusion Strategy: Harnessing the Power of RSI and CCI

The "RSI-CCI Fusion Strategy" is a powerful trading approach that combines the strengths of the Relative Strength Index (RSI) and the Commodity Channel Index (CCI) to provide enhanced trading insights. This strategy is based on the popular "RSI & CCI Fusion + Alerts" indicator, which utilizes the RSI and CCI indicators from TradingView .

1. Overview of RSI and CCI:

The Relative Strength Index (RSI) is a widely used momentum oscillator that measures the speed and change of price movements. It helps traders identify overbought and oversold conditions in the market. On the other hand, the Commodity Channel Index (CCI) is a versatile indicator that identifies cyclical trends and provides insights into overbought and oversold levels.

2. The RSI-CCI Fusion Strategy:

The RSI-CCI Fusion Strategy harnesses the combined power of the RSI and CCI indicators to generate robust trading signals. By blending the RSI and CCI, this strategy captures both momentum and cyclical trend dynamics, offering a more comprehensive view of the market.

3. Utilizing the RSI-CCI Fusion Indicator + Alerts:

The "RSI & CCI Fusion + Alerts" indicator serves as the backbone of the RSI-CCI Fusion Strategy. It integrates the RSI and CCI indicators from TradingView, providing traders with a clear and actionable trading signal.

4. How it Works:

- The indicator calculates the RSI and CCI values, standardizes them using z-score, and combines them with a weighted fusion approach.

- The resulting RSI-CCI Fusion indicator is plotted on the chart, accompanied by dynamic upper and lower bands, which help identify potential overbought and oversold conditions.

- Traders can customize alerts based on their preferred thresholds and timeframes, enabling them to receive timely notifications for potential buy and sell signals.

5. Implementing the RSI-CCI Fusion Strategy:

Traders following the RSI-CCI Fusion Strategy can utilize the buy and sell signals generated by the RSI-CCI Fusion indicator. When the indicator crosses below the upper band, it may signal a potential selling opportunity. Conversely, when it crosses above the lower band, it may indicate a potential buying opportunity. Traders can also consider additional factors and technical analysis tools to validate the signals before making trading decisions.

Conclusion: The RSI-CCI Fusion Strategy provides traders with a robust approach to analyze the market and make well-informed trading decisions. By incorporating the RSI and CCI indicators through the "RSI & CCI Fusion + Alerts" indicator, traders can take advantage of the combined strengths of these indicators. However, it is important to remember that no strategy guarantees success, and traders should always practice risk management and conduct thorough analysis before executing trades using this strategy.

Disclaimer: Trading involves risks, and it is important to conduct your own research and consult with a financial advisor before making any investment decisions.

Note: The RSI-CCI Fusion Strategy serves as a general guide, and individual traders may have different preferences and trading styles.

Cyatophilum Universal Oscillator TraderAn indicator to backtest and create an infinite number of strategies using any external indicator.

═════════════════════════════════════════════════════════════════════════

█ HOW IT WORKS

The indicator allows you to create your oscillator strategy and get backtest results from the Strategy Tester.

You can also create alerts for each of the strategy events.

█ HOW TO USE

Choose a strategy direction long or short that you want to create.

Always use regular candle type.

Configure your entry condition . To use any other indicator as source, it needs to be added to the chart first.

If you have the basic (free) TradingView plan, you can only have 1 indicator on your chart, and cannot use this external source feature. For this case, the indicator has a list of built-in oscillator (that can be increased upon request).

Then choose your condition: Cross over, Greater than, Pullback, Turning up, etc.

You now have your entry and should already see trades on the chart!

Next you can fine tune your entry condition or move to the risk management and filters.

Configure your stop loss

Use the stop loss feature to exit a trade at a certain loss.

You can also create a trailing stop using price % movement or ATR.

Configure your profit target

Use the Take Profit feature to set a target in percentage of price. You can also make it trail.

Configure your safety orders

This indicator has a safety orders feature to reduce the risk of your trade. See more below.

Check your backtest parameters

Make sure that the initial capital and order size make sense. Since it is a pyramiding strategy with safety orders, the sum of all deals should not be bigger than the initial capital.

If you use % equity as order size, please note that it will create compounding.

Check the fees, by default they are set to 0.1%.

I also recommend to set a slippage that corresponds to your exchange's spread.

█ FEATURES

• Strategy direction

Configure to go long or short.

• Entry Conditions

- External Oscillator source

- Built-in Oscillator (for basic plans)

- Base Condition for entry (Less/Greater than, Crossing Up/Down, Pullback Bull/Bear, Turning Up/Down, etc. More can be added later on)

- Additional Momentum Condition: Oscillator should be rising/falling for x number of bars

- Addition Threshold Condition: Oscillator should be Greater/Lowser than x

• Trend Filter

Filter Trades using 1 or 2 moving averages (MTF), based on Slop Change or Price Cross. Trend line is green = only longs, red = only shorts.

• Entry Filters

- Volume filter to remove low volume entries

- Overbought/Oversold filters

- Flat market Filter

• Stop Loss and Take Profit

Configure your stop loss and take profit for long and short trades.

You can also make a trailing take profit and trailing stop.

• DCA (Safety orders)

Create up to 100 safety orders with configurable options for step and volume scaling, take profit from total volume, base and safety order size.

• Backtest Settings

Choose a backtest period, longs or shorts, wether to use limit orders or not.

Graphics

A Backtest Results panel with additional information from the strategy tester.

A lightweight mode to remove background plots and make the indicator load faster.

█ ALERTS

The indicator is using the alert() calls: it only uses 1 alert slot to send order messages for each event (Long/Short entry, stop loss, take profit, safety order, exit timer). This means basic-free TV plans can create 1 complete strategy.

To set your alert messages, open the indicator settings and scroll to the bottom of the "inputs" tab.

Create your alert after you set the messages in the indicator settings, and make sure "Any alert() function call" is set in the alert option.

Use placeholders to automatically replace values in your alert messages like price, target profit, order size etc. (see the indicator inputs).

█ BACKTEST RESULTS

The backtest settings can be seen in the 'Properties' tab of the backtest report below.

Please read the author instructions below for access.

Cyatophilum 3Commas DCA Bot BacktesterAn indicator to backtest and automate 3Commas DCA Bots.

═════════════════════════════════════════════════════════════════════════

█ HOW IT WORKS

The indicator allows you to replicate your bot settings and get backtest results from the Strategy Tester and also a backtest panel with additional information on the safety orders.

You can also create alerts for each of the strategy events.

█ HOW TO USE

Choose a symbol that corresponds to your bot pair and exchange.

Pick a chart time frame as small as possible, usually 1 minute. The timeframe should always be smaller or equal to the deal start conditions timeframes.

Always use regular candle type.

Configure your deal start condition . You can combine several technical indicators to trigger an entry using a AND logical gate.

Configure your profit target

Use the Take Profit feature to set a target in percentage of price. You can also make it trail.

There is also a Stop Loss feature that is turned off by default.

Configure your safety orders

Replicate the safety orders from your bot into the indicator inputs.

Check your backtest parameters

Make sure that the initial capital and order size make sense. Since it is a pyramiding strategy with safety orders, the sum of all deals should not be bigger than the initial capital.

In this example: Initial capital is 0.02 BTC, which around 600$. I used 1000$ to be safe.

If you use % equity as order size, please note that it will create compounding.

Check the fees, by default they are set to 0.1%.

I also recommend to set a slippage that corresponds to your exchange's spread.

█ FEATURES

• Strategy direction

Configure wether to go long or short.

• Deal Start Conditions

The current conditions available are:

- Up to 4 MTF Trading View ratings conditions (Buy/Sell, Strong Buy/Sell)

- Up to 4 MTF RSI with configurable start conditions (Less/Greater than, Crossing Up/Down)

- Up to 2 MTF Ultimate Oscillator with configurable start conditions (Less/Greater than, Crossing Up/Down)

- MTF BB%-20-1 (length-deviation) with configurable start conditions (Less/Greater than, Crossing Up/Down)

- MTF BB%-20-2 (length-deviation) with configurable start conditions (Less/Greater than, Crossing Up/Down)

- Up to 2 MTF TA presets with the following options (Bollinger Bands, MFI, CCI, MACD, PSAR, SMA crosses, Heikin Ashi)

• Stop Loss and Take Profit

Configure your stop loss and take profit for long and short trades.

You can also make a trailing take profit.

• DCA (Safety orders)

Create up to 100 safety orders with configurable options for step and volume scaling, take profit from total volume, base and safety order size.

• Backtest Settings

Choose a backtest period, longs or shorts, wether to use limit orders or not.

Graphics

A Configuration panel with all the indicator settings, useful for sharing/saving a strategy.

A Backtest Results panel with additional information from the strategy tester.

█ ALERTS

The indicator is using the alert() calls: it only uses 1 alert slot to send order messages for each event (Long/Short entry, stop loss, take profit, safety order). This means free TV plans can create 1 complete strategy.

To set your alert messages, open the indicator settings and scroll to the bottom of the "inputs" tab.

Create your alert after you set the messages in the indicator settings, and make sure "Any alert() function call" is set in the alert option.

█ BACKTEST RESULTS

The backtest settings used in this snapshot are the following:

Initial Capital: 1000€

Order size: 0.003 BTC

Commission: 0.1 % per order

Slippage : 1 tick

Please read the author instructions below for access.

DCA Bot for ProfitViewThe base for this strategy is the "Backtesting 3commas DCA Bot v2" script by rouxam. I have made some additions, edits, and fixes, as well as tailored it for usage with ProfitView.

The strategy works in such a way that you select one or multiple rules together, in order to determine when a trade should be initiated.

The selectable rules are:

RSI-7: Initiate trading when the 7 period RSI goes below a specified threshold.

Technicals: This is essentially the TradingView screener strength. A multitude of technical indicators combined that range from Strong Sell - Sell - Buy - Strong Buy.

QFL: Find a support/resistance line on a specified timeframe, and initiate trading only when the price is below a certain point from this line.

Once the deal start rule is met, trading will initiate, and a series of additional orders will be placed and spaced out according to the order settings set in the indicator. These orders includes Take Profit, Stoploss, Trailing Take Profit, and specified additional entry orders to DCA your way into a position.

The indicator is set up so that by hooking this up to ProfitView, all of the signals should automatically be replicated to your assigned exchange, along with discord/telegram notifications for when the deals start and end, and the resulting pnl.

If you want to use it for spot markets, while technically possible, you will need to significantly edit the PV Alert syntax that i have supplied below.

Run this on your testnet of choice, it is likely that there are undiscovered issues at this point.

The strategy currently only works with 'Longs' at the time of publishing, but may be subject to change.

==ProfitView Setup==

!!Important!!

The assigned PV Alert name must contain the keyword 'Long', fex "DCA Long"

Uncheck the Once per Bar advanced filter option on the PV Alert you use for this.

Copy/Paste the text into the PV Alert: pastebin.com

Indicators & Conditions Test Framework [DTU]Hello All,

This script is a framework to build strategies by combining indicators and conditions (long, short, exits). You are able to analyze your strategies in realtime by changing the input parameters related to indicators, conditions and their combinations.

OVERVIEW

With this Study/Strategy framework, you will be able to create strategy conditions, display them on the chart, and test them using existing indicators as well as external and custom indicators that you can add.

The main purpose of the Framework is to choose your indicators to be used in the conditions and test your strategy by producing your "Long, short, Exit long, Exit short" combinations.

Although may be, it can be a bit difficult and complicated at first start, but you can understand the logic on its use in a very short time.

Notes:

I removed external links off descriptive images and video to be comply with Trading view violation House Rules

Since I am new in the community and still trying to understand the pine script language I can make errors and violations on my script. Please Inform me on any issue that I made..

HOW TO

STEP 1: SETTINGS ______________________________________________________________________________________________________

SOURCE, TIMEFRAME, SECURITY

Select the Source, timeframe and Secure type that your indicators will use.

Here, the Secure entry consists of 3 parts and the f_security function is used to determine it.

a)Secure

This option is defined as reducing repaint in tradingview calculations as much as possible. The following function is used.

request.security(_symbol, _res, _src , lookahead=barmerge.lookahead_on)

b)Semi Secure

While this option can reduce repaint in tradingview calculations as much as possible, it is less secure. The following function is used.

request.security(_symbol, _res, _src )

c)Repaint

This option turns on the repaint feature. The following function is used.

request.security(_symbol, _res, _src ) : na

Ind Source:

You can the source that indicators will use their own calculations

Ext Source:

You can import external Indicator sources from here . It appears on condition/combination area as "EXT".

To export the External indicator plot it with a title. It will be visible in source dropdown input

PERIOD , ALERTS...

Period:

Determine your strategy testing period by selecting start and end date/time

(!!! According to your tradingview subscription, it takes the last 5000, 10000.. bars.

The extra bar option may cause problems such as not appearing in the calculations or errors).

Plot Alerts:

Plot condition result as alerts arrows on the chart's bottom for "LONG" and the top for "SHORT" entries, exits

Close on opposite:

When selected, a long entry gets closed when a short entry opens and vice versa

Show Profit:

It appears if script is in strategy mode (not in study) this can display current or open profit for better reanalyzing your strategy entry exit points. (Currently under development)

PLOT TYPE OPERATIONS

This option has 4 entries

a) Mult

Sets the multiplier for the selected Plot Type (stochastic, Percentrank, Org Range (-1,1) ) except for "Original" in the range (-1,1).

EXAMPLE: When 1000 is selected, the indicator in the range of (-1,1) will appear in the range of (-1000, 1000) on the screen.

b) Shift

It determines the shift that will appear on the screen for the selected Plot Type (stochastic, Percentrank,Org Range (-1,1) ) in the range (-1,1) other than "Original".

EXAMPLE: When Shift:35000 and mult:1000 are selected, the indicator will appear in the range (34000, 36000) on the screen.

c) Smooth

This option (only for Stochastic & PercentRank) allows to smooth the indicator to be displayed.

Here, tradinview ta.swma function is used.

b) hline

Adjusts the horizontal lines to appear on the screen according to the mult factor for the range (-1,1)

The lines represent the values (-1, -05, 0, 05, 1)

STEP 2: INDICATORS ______________________________________________________________________________________________________

You need to choose indicators that you can use in strategy conditions.

Here, the indicators come from the dturkuler/lib_Indicators_DT open script library defined in the code

In addition, you can add the indicators that you will create in the area defined in the code to this list..

You can also import external indicators and test them with other variables on the system..

You can choose a maximum of 5 indicators that you can use in total. (can be increased in new versions)

Indicators are categorized in 3 main sections

Indicator Selection:

You can select your indicators from this area

a)Moving Averages

These are indicators such as EMA, SMA that you can show on the stock. They come from the library.

These indicators are fed from Settings/source. Only the length value can be used as a parameter.

In addition, line colors can be changed..

As of now, there are 28 indicators in the library in total and 5 indicators are left as future use for this field for now.

b)Other Indicators

These are different indicators from the stock value such as RSI, COG. They come from the library. These indicators are fed from Settings/source.

Only the length value can be used as a parameter. In addition, line colors can be changed.

As of now, there are 24 indicators in the library in total and 5 indicators are left as a future use for this field for now.

c)Custom Indicators

These indicators are the ones you can create by programming yourself in the source code..

The area at the bottom of the settings screen is reserved for the parameters of this type of indicators.

Indicator Length:

You can update your selected indicator length value from here. (Not: it doesn't work for custom indicators since they have their parameter on cust. Ind. input screen )

Indicator Plot Type:

Next to the indicators, there is an input selection field about how they will be displayed on the screen.

a)Original

The indicator is displayed on the screen with its current values. It is an ideal solution for displaying moving average indicators such as (EMA, SMA) over current stock.

Since the values of indicators such as (RSI, COB) are low (-100,100 : -1.1), they appear at the bottom of the screen and make analysis difficult.

For this reason, other options may be more suitable for these.

b)Stochastic

The indicator is displayed on the screen with stochastic calculation in the range of -1.1.

It uses the stochastic(50) calculation method to spread indicators such as (RSI, COB) over the range (-1,1).

Indicators in this selection can be fixed and monitored under stock on the screen with the parameters under the Plot Type section.

You can see the original values of the relevant indicator on the Data Window screen.

(!!! Do not use the values on the chart in your condition calculations. Instead, get the values from Data Window)

c)PercentRank

The indicator is displayed on the screen with stochastic calculation in the range of -1.1. .

Since the values of indicators such as (RSI, COB) are low (-100,100 : -1.1), they appear at the bottom of the screen and make analysis difficult.

Indicators in this selection can be fixed and monitored under stock on the screen with the parameters under the Plot Type section.

You can see the original values of the relevant indicator on the Data Window screen

((!!! Do not use the values on the chart in your condition calculations. Instead, get the values from Data Window)

d)Org Range (-1,1)

If your indicator is in the range of -1.1, your indicator will be displayed on the screen with its original calculation in the range of -1.1.

Indicators in this selection can be fixed and monitored under stock on the screen with the parameters under the Plot Type section.

You can see the original values of the relevant indicator on the Data Window screen.

(!!! Do not use the values on the chart in your fitness calculations. Instead, get the values from Data Window)

STEP 2 NOTES:

STEP 3: CONDITIONS ______________________________________________________________________________________________________

After choosing the indicators you will use in the conditions, you move on to the "CONDITIONS" section.

There are 4 conditions type here.

• LONG ENTRY CONDITION

• SHORT ENTRY CONDITION

• LONG CLOSE CONDITION

• SHORT CLOSE CONDITION

The use of each condition is the same.

There are 3 combinations you can use in each condition. (can be increased in new versions)

a)COMBINATIONS

There are 3 combinations you can use in each condition. (can be increased in new versions)

Each combination are build from 4 parts

1)1st Indicator

If set to "NONE" this combination will not be used on calculations. You can select

IND1-5: from indicators (See above),

EXT: value from externally imported indicator

Stock built-in values: close, open...

2)Operator

Selected Operator compares 1st Indicator with the 2nd one. You can select different operators such as

crossover, crossunder, cross,>,<,=....

3)2nd Indicator

This indicator will be compared with the 1st one via selected Operator. You can select

IND1-5: from indicators (See above),

VALUE: a float value defined in the combinations value parameter

EXT: value from externally imported indicator

Stock builtin values: close,open...

4)Value

When the 2nd indicator field is "VALUE", value area compares the entered value.

ex: 1st indicator="open", op=">", 2nd indicator="VALUE", value=3000.12 means is(close>3000.12)

In other conditions, it compares the previous values of the indicator.

ex: 1st indicator="open", op=">" 2nd indicator is "close" and value is 2 means is(open>close )

EXAMPLES:

indicator 1= "IND1", Operator=">", indicator 2= "IND2" => is(IND1>IND2)

indicator 1= "IND1", Operator=">", indicator 2= "VALUE", "0.1" => is(IND1>0.9)

indicator 1= "IND2", Operator="crossover", indicator 2= "IND1" => is(IND2 crossover IND1) : like a=ta.crossover(IND2, IND1)

indicator 1= "IND1", Operator="<", indicator 2= "close" => is(IND1>close)

indicator 1= "IND1", Operator="<", indicator 2= "EXT" => is(IND1>EXT) , EXT mean external imported indicator that define on settings section

indicator 1= "IND1", Operator="<", indicator 2= "IND1", Value="1" => is (IND1>IND1 )

b)JOIN COMBINATIONS

Each combination in Condition is compared with the next one via JOIN operator

The join operator can be selected as AND or OR.

Examples:

1st combination= is(IND1>0.9) true

2nd combination= is(IND2 crossover IND1) false

1st combination "AND" 2ndcombination" => false (is(IND1>0.9) AND is(IND2 crossover IND1))

1st combination "OR" 2nd combination" => true (is(IND1>0.9) OR is(IND2 crossover IND1))

STEP 3 NOTES:

When the 2nd indicator field is "VALUE", value area compares the entered value. In other conditions, it compares the previous values of the indicator.

In cases where "VALUE" is not selected, integer values must be entered in this field. (float should not be entered. ie 1, 2 should be entered)

!!!If the 1st indicator is "NONE" in the combination, that combination is cancelled.

Each combination returns true/false, allowing the selected value to be compared with another value

Example: EMA(21)>EMA(50) returns true under all conditions or (EMA(21) crossover EMA(50)) returns true when passed.

You can use , Value of 5 indicators (IND1-IND5) or (VALUE) that you have defined in combinations or import indicator (EXT) or stock values (close, open, high...) in your calculations.

combination Compares the 1st indicator with 2nd indicator via the operator.

STEP 4: CUSTOM INDICATORS ______________________________________________________________________________________________________

There is an area in the code for designing Custom Indicators.

Here you can design your own indicators and use them in the framework.

You can also create unlimited parameters for your indicators in the SETTINGS custom indicator field.

For now, only 3 Custom indicators have been defined.

Examples are entered in the code for custom indicators.

STEP 4 NOTES:

Including / updating custom to the code is explained in the source code

• LIMITATIONS:

!!! According to your tradingview subscription, it takes the last 5000, 10000.. bars. More bar options may cause problems such as not appearing in the calculations or errors.

• RAMBLINGS:

• NOTES [ /i]

This Script can be used as an indicator if the last strategy parts in the code are commented out and converted to the initial strategy study.

It was originally prepared for my use with my own strategy framework and has export functions accordingly.

When integrated to my own strategy framework it brings many more features over strategy definition of trades.

• TODO [ /i]

TODO: Add tooltips to the settings screen

TODO: Add double triple, Quatr factor for all indicators (convert any indicator to factor2-4 facotr. ex: EMA to DEMA, TEMA, QEMA...)

TODO: Add factorized Fibo avg range indicator (good for trend definition and entry exit points)

TODO: Add bands to the indicator and conditions

TODO: Add debug window for exporting indicator's parameters

TODO: Add isRising(value) isFalling(value), is...(value) .... to combinations (they can be used as custom indicator also

TODO: Reassess condition entry screen for user friendly GUI

TODO: Increase # conditions from 3 to 4

TODO: Reassess strategy entries, exit and close (should be improved)

TODO: Add Alerts, Condiional alerts for indicator (study) part

TODO: Create export function v3 for Pinecoders Indicator framework

• THANKS:

For Pine script format docs RicardoSantos .

For Pine script coding standards Pinecoders .

For moving average script used on library s RodrigoKazuma .

Multi-Market Swing Trader Webhook Ready [HullBuster]

Introduction

This is an all symbol swing trading strategy intended for webhook integration to live accounts. This script employs an adjustable bandwidth ping pong algorithm which can be run in long only, short only or bidirectional modes. Additionally, this script provides advanced features such as pyramiding and DCA. It has been in development for nearly three years and exposes over 90 inputs to accommodate varying risk reward ratios. Equipped with a proper configuration it is suitable for professional traders seeking quality trades from a cloud based platform. This is my most advanced Pine Script to date which combines my RangeV3 and TrendV2 scripts. Using this combination it tries to bridge the gap between range bound and trending markets. I have put a lot of time into creating a system that could transition by itself so as to require less human intervention and thus be able to withstand long periods in full automation mode.

As a Pine strategy, hypothetical performance can be easily back-tested. Allowing you to Iron out the configuration of your target instrument. Now with recent advancements from the Pine development team this same script can be connected to a webhook through the alert mechanism. The requirement of a separate study script has been completely removed. This really makes things a lot easier to get your trading system up and running. I would like to also mention that TradingView has made significant advancements to the back-end over the last year. Notably, compile times are much faster now permitting more complex algorithms to be implemented. Thank you TradingView!

I used QuantConnect as my role model and strived to produce a base script which could compete with higher end cloud based platforms while being attractive to similarly experienced traders. The versatility of the Pine Language combined with the greater selection of end point execution systems provides a powerful alternative to other cloud based platforms. At the very least, with the features available today, a modular trading system for everyday use is a reality. I hope you'll agree.

This is a swing trading strategy so the behavior of this script is to buy on weakness and sell on strength. In trading parlance this is referred to as Support and Resistance Trading. Support being the point at which prices stop falling and start rising. Resistance being the point at which prices stop rising and fall. The chart real estate between these two points being defined as the range. This script seeks to implement strategies to profit from placing trades within this region. Short positions at resistance and long positions at support. Just to be clear, the range as well as trends are merely illusions as the chart only receives prices. However, this script attempts to calculate pivot points from the price stream. Rising pivots are shorts and falling pivots are longs. I refer to pivots as a vertex in this script which adds structural components to the chart formation (point, sides and a base). When trading in “Ping Pong” mode long and short positions are interleaved continuously as long as there exists a detectable vertex.

This is a non-hedging script so those of us subject to NFA FIFO Rule 2-43(b) should be generally safe to webhook into signals emitted from this script. However, as covered later in this document, there are some technical limitations to this statement. I have tested this script on various instruments for over two years and have configurations for forex, crypto and stocks. This script along with my TrendV2 script are my daily trading vehicles as a webhook into my forex and crypto accounts. This script employs various high risk features that could wipe out your account if not used judiciously. You should absolutely not use this script if you are a beginner or looking for a get-rich-quick strategy. Also please see my CFTC RULE 4.41 disclosure statement at the end of the document. Really!

Does this script repaint? The short answer is yes, it does, despite my best efforts to the contrary. EMAs are central to my strategy and TradingView calculates from the beginning of the series so there is just no getting around this. However, Pine is improving everyday and I am hopeful that this issue will be address from an architectural level at some point in the future. I have programmed my webhook to compensate for this occurrence so, in the mean time, this my recommended way to handle it (at the endpoint and before the broker).

Design

This strategy uses a ping pong algorithm of my own design. Basically, trades bounce off each other along the price stream. Trades are produced as a series of reversals. The point at which a trade reverses is a pivot calculation. A measurement is made between the recent valley to peak which results in a standard deviation value. This value is an input to implied probability calculation.Yes, the same implied probability used in sports betting. Odds are then calculated to determine the likelihood of price action continuing or retracing to the pivot. Based on where the account is at alert time, the action could be an entry, take profit or pyramid signal. In this design, trades must occur in alternating sequence. A long followed by a short then another long followed by a short and so on. In range bound price action trades appear along the outer bands of the channel in the aforementioned sequence. Shorts on the top and longs at the bottom. Generally speaking, the widths of the trading bands can be adjusted using the vertex dynamics in Section 2. There are a dozen inputs in this section used to describe the trading range. It is not a simple adjustment. If pyramids are enabled the strategy overrides the ping pong reversal pattern and begins an accumulation sequence. In this case you will see a series of same direction trades.

This script uses twelve indicators on a single time frame. The original trading algorithms are a port from a C++ program on proprietary trading platform. I’ve converted some of the statistical functions to use standard indicators available on TradingView. The setups make heavy use of the Hull Moving Average in conjunction with EMAs that form the Bill Williams Alligator as described in his book “New Trading Dimensions” Chapter 3. Lag between the Hull and the EMAs play a key role in identifying the pivot points. I really like the Hull Moving Average. I use it in all my systems, including 3 other platforms. It’s is an excellent leading indicator and a relatively light calculation.

The trend detection algorithms rely on several factors:

1. Smoothed EMAs in a Willams Alligator pattern.

2. Number of pivots encountered in a particular direction.

3. Which side debt is being incurred.

4. Settings in Section 4 and 5 (long and short)

The strategy uses these factors to determine the probability of prices continuing in the most recent direction. My TrendV2 script uses a higher time frame to determine trend direction. I can’t use that method in this script without exceeding various TradingView limitations on code size. However, the higher time frame is the best way to know which trend is worth pursuing or better to bet against.

The entire script is around 2400 lines of Pine code which pushes the limits of what can be created on this platform given the TradingView maximums for: local scopes, run-time duration and compile time. The module has been through numerous refactoring passes and makes extensive use of ternary statements. As such, It takes a full minute to compile after adding it to a chart. Please wait for the hovering dots to disappear before attempting to bring up the input dialog box. Scrolling the chart quickly may bring up an hour glass.

Regardless of the market conditions: range or trend. The behavior of the script is governed entirely by the 91 inputs. Depending on the settings, bar interval and symbol, you can configure a system to trade in small ranges producing a thousand or more trades. If you prefer wider ranges with fewer trades then the vertex detection settings in Section 2 should employ stiffer values. To make the script more of a trend follower, adjustments are available in Section 4 and 5 (long and short respectively). Overall this script is a range trader and the setups want to get in that way. It cannot be made into a full blown trend trading system. My TrendV2 is equipped for that purpose. Conversely, this script cannot be effectively deployed as a scalper either. The vertex calculation require too much data for high frequency trading. That doesn’t work well for retail customers anyway. The script is designed to function in bar intervals between 5 minutes and 4 hours. However, larger intervals require more backtest data in order to create reliable configurations. TradingView paid plans (Pro) only provide 10K bars which may not be sufficient. Please keep that in mind.

The transition from swing trader to trend follower typically happens after a stop is hit. That means that your account experiences a loss first and usually with a pyramid stack so the loss could be significant. Even then the script continues to alternate trades long and short. The difference is that the strategy tries to be more long on rising prices and more short on falling prices as opposed to simply counter trend trading. Otherwise, a continuous period of rising prices results in a distinctly short pyramid stack. This is much different than my TrendV2 script which stays long on peaks and short on valleys. Basically, the plan is to be profitable in range bound markets and just lose less when a trend comes along. How well this actually plays out will depend largely on the choices made in the sectioned input parameters.

Sections

The input dialog for this script contains 91 inputs separated into six sections.

Section 1: Global settings for the strategy including calculation model, trading direction, exit levels, pyramid and DCA settings. This is where you specify your minimum profit and stop levels. You should setup your Properties tab inputs before working on any of the sections. It’s really important to get the Base Currency right before doing any work on the strategy inputs. It is important to understand that the “Minimum Profit” and “Limit Offset” are conditional exits. To exit at a profit, the specified value must be exceeded during positive price pressure. On the other hand, the “Stop Offset” is a hard limit.

Section 2: Vertex dynamics. The script is equipped with four types of pivot point indicators. Histogram, candle, fractal and transform. Despite how the chart visuals may seem. The chart only receives prices. It’s up to the strategy to interpret patterns from the number stream. The quality of the feed and the symbol’s bar characteristics vary greatly from instrument to instrument. Each indicator uses a fundamentally different pattern recognition algorithm. Use trial and error to determine the best fit for your configuration. After selecting an indicator type, there are eight analog fields that must be configured for that particular indicator. This is the hardest part of the configuration process. The values applied to these fields determine how the range will be measured. They have a big effect on the number of trades your system will generate. To see the vertices click on the “Show Markers” check box in this section. Red markers are long positions and blue markers are short. This will give you an idea of where trades will be placed in natural order.

Section 3: Event thresholds. Price spikes are used to enter and exit trades. The magnitude which define these spikes are configured here. The rise and fall events are primarily for pyramid placement. The rise and fall limits determine the exit threshold for the conditional “Limit Offset” field found in Section 1. These fields should be adjusted one at a time. Use a zero value to disengage every one but the one you are working on. Use the fill colors found in Section 6 to get a visual on the values applied to these fields. To make it harder for pyramids to enter stiffen the Event values. This is more of a hack as the formal pyramid parameters are in Section 1.

Section 4 and 5: Long and short settings. These are mirror opposite settings with all opposing fields having the same meaning. Its really easy to introduce data mining bias into your configuration through these fields. You must combat against this tendency by trying to keep your settings as uniform as possible. Wildly different parameters for long and short means you have probably fitted the chart. There are nine analog and thirteen Boolean fields per trade direction. This section is all about how the trades themselves will be placed along the range defined in Section 2. Generally speaking, more restrictive settings will result in less trades but higher quality. Remember that this strategy will enter long on falling prices and short on rising prices. So getting in the trade too early leads to a draw-down. However, this could be what you want if pyramiding is enabled. I, personally, have found that the best configurations come from slightly skewing one side. I just accept that the other side will be sub-par.

Section 6: Chart rendering. This section contains one analog and four Boolean fields. More or less a diagnostic tool. Of particular interest is the “Symbol Debt Sequence” field. This field contains a whole number which paints regions that have sustained a run of bad trades equal or greater than specified value. It is useful when DCA is enabled. In this script Dollar Cost Averaging on new positions continues only until the symbol debt is recouped. To get a better understanding on how this works put a number in this field and activate DCA. You should notice how the trade size increases in the colored regions. The “Summary Report” checkbox displays a blue information box at the live end of the chart. It exposes several metrics which you may find useful if manually trading this strategy from audible alerts or text messages.

Pyramids

This script features a downward pyramiding strategy which increases your position size on losing trades. On purely margin trades, this feature can be used to, hypothetically, increase the profit factor of positions (not individual trades). On long only markets, such as crypto, you can use this feature to accumulate coins at depressed prices. The way it works is the stop offset, applied in the Section 1 inputs, determines the maximum risk you intend to bear. Additional trades will be placed at pivot points calculated all the way down to the stop price. The size of each add on trade is increased by a multiple of its interval. The maximum number of intervals is limited by the “Pyramiding” field in the properties tab. The rate at which pyramid positions are created can be adjusted in Section 1. To see the pyramids click on the “Mark Pyramid Levels” check box in the same section. Blue triangles are painted below trades other than the primary.

Unlike traditional Martingale strategies, the result of your trade is not dependent on the profit or loss from the last trade. The position must recover the R1 point in order to close. Alternatively, you can set a “Pyramid Bale Out Offset” in Section 1 which will terminate the trade early. However, the bale out must coincide with a pivot point and result in a profitable exit in order to actually close the trade. Should the market price exceed the stop offset set in Section 1, the full value of the position, multiplied by the accepted leverage, will be realized as a loss to the trading account. A series of such losses will certainly wipe out your account.

Pyramiding is an advanced feature intended for professional traders with well funded accounts and an appropriate mindset. The availability of this feature is not intended to endorse or promote my use of it. Use at your own risk (peril).

DCA

In addition to pyramiding this script employs DCA which enables users to experiment with loss recovery techniques. This is another advanced feature which can increase the order size on new trades in response to stopped out or winning streak trades. The script keeps track of debt incurred from losing trades. When the debt is recovered the order size returns to the base amount specified in the properties tab. The inputs for this feature are found in section 3 and include a limiter to prevent your account from depleting capital during runaway markets. The main difference between DCA and pyramids is that this implementation of DCA applies to new trades while pyramids affect open positions. DCA is a popular feature in crypto trading but can leave you with large “bags” if your not careful. In other markets, especially margin trading, you’ll need a well funded account and much experience.

To be sure pyramiding and dollar cost averaging is as close to gambling as you can get in respectable trading exchanges. However, if you are looking to compete in a spot trading contest or just want to add excitement to your trading life style those features could find a place in your strategies. Although your backtest may show spectacular gains don’t expect your live trading account to do the same. Every backtest has some measure of data mining bias. Please remember that.

Webhook Integration

The TradingView alerts dialog provides a way to connect your script to an external system which could actually execute your trade. This is a fantastic feature that enables you to separate the data feed and technical analysis from the execution and reporting systems. Using this feature it is possible to create a fully automated trading system entirely on the cloud. Of course, there is some work to get it all going in a reliable fashion. To that end this script has several things going for it. First off, it is a strategy type script. That means that the strategy place holders such as {{strategy.position_size}} can be embedded in the alert message text. There are more than 10 variables which can write internal script values into the message for delivery to the specified endpoint. Additionally, my scripts output the current win streak and debt loss counts in the {{strategy.order.alert_message}} field. Depending on the condition, this script will output other useful values in the JSON “comment” field of the alert message. Here is an excerpt of the fields I use in my webhook signal:

"broker_id": "kraken",

"account_id": "XXX XXXX XXXX XXXX",

"symbol_id": "XMRUSD",

"action": "{{strategy.order.action}}",

"strategy": "{{strategy.order.id}}",

"lots": "{{strategy.order.contracts}}",

"price": "{{strategy.order.price}}",

"comment": "{{strategy.order.alert_message}}",

"timestamp": "{{time}}"

Though TradingView does a great job in dispatching your alert this feature does come with a few idiosyncrasies. Namely, a single transaction call in your script may cause multiple transmissions to the endpoint. If you are using placeholders each message describes part of the transaction sequence. A good example is closing a pyramid stack. Although the script makes a single strategy.close() call, the endpoint actually receives a close message for each pyramid trade. The broker, on the other hand, only requires a single close. The incongruity of this situation is exacerbated by the possibility of messages being received out of sequence. Depending on the type of order designated in the message, a close or a reversal. This could have a disastrous effect on your live account. This broker simulator has no idea what is actually going on at your real account. Its just doing the job of running the simulation and sending out the computed results. If your TradingView simulation falls out of alignment with the actual trading account lots of really bad things could happen. Like your script thinks your are currently long but the account is actually short. Reversals from this point forward will always be wrong with no one the wiser. Human intervention will be required to restore congruence. But how does anyone find out this is occurring? In closed systems engineering this is known as entropy. In practice your webhook logic should be robust enough to detect these conditions. Be generous with the placeholder usage and give the webhook code plenty of information to compare states. Both issuer and receiver. Don’t blindly commit incoming signals without verifying system integrity.

Operation

This is a swing trading strategy so the fundamental behavior of this script is to buy on weakness and sell on strength. As such trade orders are placed in a counter direction to price pressure. What you will see on the chart is a short position on peaks and a long position on valleys. This is slightly misleading since a range as well as a trend are best recognized, in hindsight, after the patterns occur on the chart. In the middle of a trade, one never knows how deep valleys will drop or how high peaks will rise. For certain, long trades will continue to trigger as the market prices fall and short trades on rising prices. This means that the maximum efficiency of this strategy is achieved in choppy markets where the price doesn’t extend very far from its adjacent pivot point. Conversely, this strategy will be the least efficient when market conditions exhibit long continuous single direction price pressure. Especially, when measured in weeks. Translation, the trend is not your friend with this strategy. Internally, the script attempts to recognize prolonged price pressure and changes tactics accordingly. However, at best, the goal is to weather the trend until the range bound market returns. At worst, trend detection fails and pyramid trades continue to be placed until the limit specified in the Properties tab is reached. In all likelihood this could trigger a margin call and if it hits the stop it could wipe out your account.

This script has been in beta test four times since inception. During all that time no one has been successful in creating a configuration from scratch. Most people give up after an hour or so. To be perfectly honest, the configuration process is a bear. I know that but there is no way, currently, to create libraries in Pine. There is also no way specify input parameters other than the flattened out 2-D inputs dialog. And the publish rules clearly state that script variations addressing markets or symbols (suites) are not permitted. I suppose the problem is systemic to be-all-end-all solutions like my script is trying to be. I needed a cloud strategy for all the symbols that I trade and since Pine does not support library modules, include files or inter process communication this script and its unruly inputs are my weapon of choice in the war against the market forces. It takes me about six hours to configure a new symbol. Also not all the symbols I configure are equally successful. I should mention that I have a facsimile of this strategy written in another platform which allows me to run a backtest on 10 years of historical data. The results provide me a sanity check on the inputs I select on this platform.

My personal configurations use a 10 minute bar interval on forex instruments and 15 minutes on crypto. I try to align my TradingView scripts to employ standard intervals available from the broker so that I can backtest longer durations than those available on TradingView. For example, Bitcoin at 15 minute bars is downloadable from several sources. I really like the 10 minute bar. It provides lots of detectable patterns and is easy to store many years in an SQL database.

The following steps provide a very brief set of instructions that will get you started but will most certainly not produce the best backtest. A trading system that you are willing to risk your hard earned capital will require a well crafted configuration that involves time, expertise and clearly defined goals. As previously mentioned, I have several example configurations that I use for my own trading that I can share with you if you like. To get hands on experience in setting up your own symbol from scratch please follow the steps below.

Step 1. Setup the Base currency and order size in the properties tab.

Step 2. Select the calculation presets in the Instrument Type field.

Step 3. Select “No Trade” in the Trading Mode field

Step 4. Select the Histogram indicator from Section 2. You will be experimenting with different ones so it doesn’t matter which one you try first.

Step 5. Turn on Show Markers in Section 2.

Step 6. Go to the chart and checkout where the markers show up. Blue is up and red is down. Long trades show up along the red markers and short trades on the blue.

Step 7. Make adjustments to “Base To Vertex” and “Vertex To Base” net change and ROC in Section 2. Use these fields to move the markers to where you want trades to be.

Step 8. Try a different indicator from Section 2 and repeat Step 7 until you find the best match for this instrument on this interval. This step is complete when the Vertex settings and indicator combination produce the most favorable results.

Step 9. Go to Section 4 and enable “Apply Red Base To Base Margin”.

Step 10. Go to Section 5 and enable “Apply Blue Base To Base Margin”.

Step 11. Go to Section 2 and adjust “Minimum Base To Base Blue” and “Minimum Base To Base Red”. Observe the chart and note where the markers move relative to each other. Markers further apart will produce less trades but will reduce cutoffs in “Ping Pong” mode.

Step 12. Turn off Show Markers in Section 2.

Step 13. Put in your Minimum Profit and Stop Loss in the first section. This is in pips or currency basis points (chart right side scale). Percentage is not currently supported. Note that the profit is taken as a conditional exit on a market order not a fixed limit. The actual profit taken will almost always be greater than the amount specified. The stop loss, on the other hand, is indeed a hard number which is executed by the TradingView broker simulator when the threshold is breached.

Step 14. Return to step 3 and select a Trading Mode (Long, Short, BiDir, Ping Pong). If you are planning to trade bidirectionally its best to configure long first then short. Combine them with “BiDir” or “Ping Pong” after setting up both sides of the trade individually. The difference between “BiDir” and “Ping Pong” is that “Ping Pong” uses position reversal and can cut off opposing trades less than the specified minimum profit. As a result “Ping Pong” mode produces the greatest number of trades.

Step 15. Take a look at the chart. Trades should be showing along the markers plotted earlier.

Step 16. Make adjustments to the Vertex fields in Section 2 until the TradingView performance report is showing a profit. This includes the “Minimum Base To Base” fields. If a profit cannot be achieved move on to Step 17.

Step 17. Improve the backtest profitability by adjusting the “Entry Net Change” and “Entry ROC” in Section 4 and 5.

Step 18. Enable the “Mandatory Snap” checkbox in Section 4 and 5 and adjust the “Snap Candle Delta” and “Snap Fractal Delta” in Section 2. This should reduce some chop producing unprofitable reversals.

Step 19. Increase the distance between opposing trades by adding an “Interleave Delta” in Sections 4 and 5. This is a floating point value which starts at 0.01 and typically does not exceed 2.0.

Step 20. Increase the distance between opposing trades even further by adding a “Decay Minimum Span” in Sections 4 and 5. This is an absolute value specified in the symbol’s quote currency (right side scale of the chart). This value is similar to the minimum profit and stop loss fields in Section 1.

Step 21. The “Buy Composite Strength” input works in tandem with “Long Decay Minimum Span” in Section 4. Try enabling and see if it improves the performance. This field is only relevant when there is a value in “Long Decay Minimum Span”.

Step 22. The “Sell Composite Weakness” input works in tandem with “Short Decay Minimum Span” in Section 5. Try enabling and see if it improves the performance. This field is only relevant when there is a value in “Short Decay Minimum Span”.

Step 23. Improve the backtest profitability by adjusting the “Adherence Delta” in Section 4 and 5. This field requires the “Adhere to Rising Trend” checkbox to be enabled.

Step 24. At this point your strategy should be more or less working. Experiment with the remaining check boxes in Section 4 and 5. Keep the ones which seem to improve the performance.

Step 25. Examine the chart and see that trades are being placed in accordance with your desired trading goals. This is an important step. If your desired model requires multiple trades per day then you should be seeing hundreds of trades on the chart. Alternatively, you may be looking to trade fewer steep peaks and deep valleys in which case you should see trades at major turning points. Don’t simply settle for what the backtest serves you. Work your configuration until the system aligns with your desired model. Try changing indicators and even intervals if you cannot reach your simulation goals. Generally speaking, the histogram and Candle indicators produce the most trades. The Fractal indicator captures the tallest peaks and valleys. The Transform indicator is the most reliable but doesn’t well work on all instruments.

Example Settings

To reproduce the performance shown on the chart please use the following configuration:

1. Select XBTUSD Kraken as the chart symbol.

2. On the properties tab set the Order Size to: 0.01 Bitcoin

3. On the properties tab set the Pyramiding to: 10

4. In Section 1: Select “Forex” for the Instrument Type

5. In Section 1: Select “Ping Pong” for the Trading Mode

6. In Section 1: Input 1200 for the Minimum Profit

7. In Section 1: Input 15000 for the Stop Offset

8. In Section 1: Input 1200 for the Pyramid Minimum Span

9. In Section 1: Check mark the Ultra Wide Pyramids

10. In Section 2: Check mark the Use Transform Indicator

So to be clear, I used a base position size of one - one hundredth of a Bitcoin and allow the script to add up to 10 downward pyramids. The example back-test did hit eight downward pyramids. That means the account would have to be able to withstand a base position size (0.01) times 28. The resulting position size is 0.28 of a Bitcoin. If the price of Bitcoin is 35K then the draw down amount (not including broker fees) would be $9800 dollars. Since I have a premium subscription my backtest chart includes 20K historical bars. That's roughly six months of data. As of today, pro accounts only get 10K bars so the performance cannot be exactly matched with such a difference in historical data. Please keep that in mind.

There are, of course, various ways to reduce the risk incurred from accumulating pyramids. You can increase the “Pyramid Minimum Span” input found in Section 2 which increases the space between each pyramid trade. Also you can set a “Pyramid Bale Out Offset” in the same input section. This lets you out of the trade faster on position recovery. For example: Set a value of 8000 into this input and the number of trades increase to 178 from 157. Since the positions didn’t go full term, more trades were created at less profit each. The total brute force approach would be to simply limit the number of pyramids in the Properties tab.