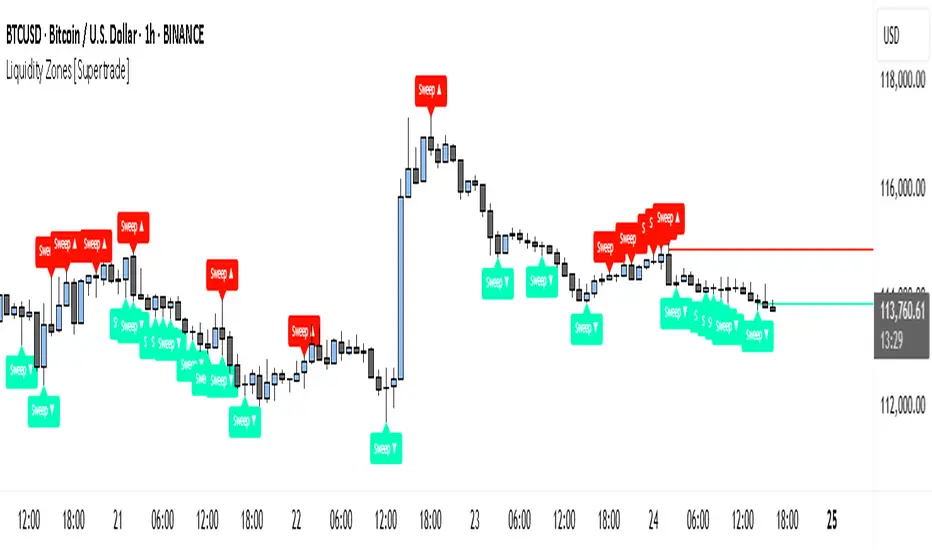

Simple Liquidity Zones [Supertrade]🔎 What this indicator does

This indicator is designed to highlight liquidity sweep zones on the chart.

• A liquidity sweep occurs when price briefly breaks above a recent swing high or below a recent swing low, but fails to close beyond it.

• Such behavior often indicates that price has taken liquidity (stop orders resting above highs or below lows) and may reverse.

The indicator marks these events as bullish or bearish liquidity zones:

• Bullish Zone (green) → Price swept a swing low and closed back above it (possible bullish reversal area).

• Bearish Zone (red) → Price swept a swing high and closed back below it (possible bearish reversal area).

These zones are drawn as shaded horizontal bands that extend forward in time, providing visual areas where liquidity grabs occurred.

________________________________________

⚙️ How calculations are made

The indicator does not use moving averages or smoothing.

Instead, it works with raw price action:

1. Swing Detection → It checks the highest high and lowest low of the past N bars (swing length).

2. Sweep Logic →

o A bearish sweep happens if the high breaks above the previous swing high, but the close returns below that level.

o A bullish sweep happens if the low breaks below the previous swing low, but the close returns above that level.

3. Zone Creation → When a sweep is detected, a shaded zone is drawn just above/below the swing level.

4. Persistence → Zones extend into the future until replaced by new ones (or optionally until price fully trades through them).

This makes the calculations simple, transparent, and responsive to actual market structure without lag.

________________________________________

📈 How it helps traders

This tool helps traders by:

• Visualizing liquidity areas → Shows where price previously swept liquidity and may act as support/resistance.

• Identifying reversals → Helps spot potential turning points after liquidity grabs.

• Risk management → Zones highlight areas where stops may be targeted, useful for positioning stop-loss orders.

• Confluence tool → Works best when combined with other strategies such as order blocks, trendlines, or volume analysis.

⚠️ Note: Like all indicators, this should not be used in isolation. It provides context, not guaranteed trade signals.

________________________________________

🏦 Markets & Timeframes

• Works across all markets (crypto, forex, stocks, indices, commodities).

• Particularly effective in high-liquidity environments where stop-hunting is common (e.g., forex majors, BTC/ETH, S&P500).

• Timeframes:

o Lower timeframes (1m–15m) → Scalpers can spot intraday liquidity sweeps.

o Higher timeframes (1H–1D) → Swing traders can identify major liquidity pools.

________________________________________

Tìm kiếm tập lệnh với "liquidity"

[c3s] CWS - M2 Global Liquidity Index & BTC Correlation CWS - M2 Global Liquidity Index with Offset BTC Correlation

This custom indicator visualizes and analyzes the relationship between the global M2 money supply and Bitcoin (BTC) price movements. It calculates the correlation between these two variables to provide insights into how changes in global liquidity may impact Bitcoin’s price over time.

Key Features:

Global M2 Liquidity Index Calculation:

Fetches M2 money supply data from multiple economies (China, US, EU, Japan, UK) and normalizes using currency exchange rates (e.g., CNY/USD, EUR/USD).

Combines all M2 data points and normalizes by dividing by 1 trillion (1e12) for easier visualization.

Offset for M2 Data:

The offset parameter allows users to shift the M2 data by a specified number of days, helping track the influence of past global liquidity on Bitcoin.

BTC Price Correlation:

Computes the correlation between shifted global M2 liquidity and Bitcoin (BTC) price, using a 52-day lookback period by default.

Correlation Quality Display:

Categorizes correlation quality as:

Excellent : Correlation >= 0.8

Good : Correlation >= 0.6 and < 0.8

Weak : Correlation >= 0.4 and < 0.6

Very Weak : Correlation < 0.4

Displays correlation quality as a label on the chart for easy assessment.

Visual Enhancements:

Labels : Displays dynamic labels on the chart with metrics like M2 value and correlation.

Plot Shapes : Uses shapes to indicate data availability for global M2 and correlation.

Data Table : Optionally shows a data table in the top-right corner summarizing:

Global M2 value (in trillions)

The correlation between global M2 and BTC

The correlation quality

Optional Debugging:

Debug plots help identify when data is missing for M2 or correlation, ensuring transparency and accurate functionality.

Inputs:

Offset: Shift the M2 data (in days) to see past liquidity effects on Bitcoin.

Lookback Period: Number of periods (default 52) used to calculate the correlation.

Show Labels: Toggle to show or hide labels for M2 and correlation values.

Show Table: Toggle to show or hide the data table in the top-right corner.

Usage:

Ideal for traders and analysts seeking to understand the relationship between global liquidity and Bitcoin price. The offset and lookback period can be adjusted to explore different timeframes and correlation strengths, aiding more informed trading decisions.

Trishul Tap Signals (v6) — Liquidity Sweep + Imbalanced RetestTrishul Tap Signals — Liquidity Sweep + Imbalanced Retest

Type: Signal-only indicator (non-repainting)

Style: Price-action + Liquidity + Trend-following

Best for: Intraday & Swing Trading — any liquid market (stocks, futures, crypto, FX)

Timeframes: Any (5m–1D recommended)

Concept

The Trishul Tap setup is a liquidity-driven retest play inspired by order-flow and Smart Money Concepts.

It identifies one-sided impulse candles that also sweep liquidity (grab stops above/below a recent swing), then waits for price to retest the origin of that candle to enter in the trend direction.

Think of it as the three points of a trident:

Trend filter — Only signals with the prevailing trend.

Liquidity sweep — Candle takes out a recent swing high/low (stop-hunt).

Imbalanced retest — Price taps the candle’s open/low (bull) or open/high (bear).

Bullish Setup

Trend Filter: Price above EMA(200).

Impulse Candle:

Green close.

Upper wick ≥ (wickRatio × lower wick).

Lower wick ≤ (oppWickMaxFrac × full range).

Liquidity Sweep: Candle’s high exceeds the highest high of the last sweepLookback bars (excluding current).

Tap Entry: Buy signal triggers when price later taps the candle’s low or open (user choice) within expireBars.

Bearish Setup

Trend Filter: Price below EMA(200).

Impulse Candle:

Red close.

Lower wick ≥ (wickRatio × upper wick).

Upper wick ≤ (oppWickMaxFrac × full range).

Liquidity Sweep: Candle’s low breaks the lowest low of the last sweepLookback bars (excluding current).

Tap Entry: Sell signal triggers when price later taps the candle’s high or open (user choice) within expireBars.

Inputs

Trend EMA Length: Default 200.

Sweep Lookback: Number of bars for liquidity sweep check (default 20).

Wick Ratio: Required size ratio of dominant wick to opposite wick (default 2.0).

Opposite Wick Max %: Opposite wick must be ≤ this fraction of the candle’s range (default 25%).

Tap Tolerance (ticks): How close price must come to the level to count as a tap.

Expire Bars: Max bars after setup to allow a valid tap.

One Signal per Level: If ON, a base is “consumed” after first signal.

Plot Tap Levels: Show horizontal lines for active bases.

Show Setup Labels: Mark the origin sweep candle.

Plots & Visuals

EMA Trend Line — trend filter reference.

Tap Levels —

Green = bullish base (origin candle’s low/open).

Red = bearish base (origin candle’s high/open).

Labels — Show where the setup candle formed.

Signals —

BUY: triangle-up below bar at bullish tap.

SELL: triangle-down above bar at bearish tap.

Alerts

Two built-in conditions:

BUY Signal (Trishul Tap) — triggers on bullish tap.

SELL Signal (Trishul Tap) — triggers on bearish tap.

Set via Alerts panel → Condition = this indicator → Choose signal type.

How to Trade It

Use in liquid markets with clean price structure.

Confirm with HTF structure, volume spikes, or other confluence if desired.

Place stop just beyond the tap level (or ATR-based).

Target 1–2R or trail behind structure.

Why It Works

Liquidity sweep traps traders entering late (breakout buyers or panic sellers) and forces them to exit in the opposite direction, fueling your entry.

Wick imbalance confirms directional aggression by one side.

Trend filter keeps you aligned with the market’s dominant flow.

Retest entry lets you enter at a better price with reduced risk.

Non-Repainting

Setups form only on confirmed bar closes.

Signals trigger only on later bars that tap the stored level.

No lookahead functions are used.

Disclaimer

This script is for educational purposes only and does not constitute financial advice. Test thoroughly in a simulator or demo before using in live markets. Trading involves risk.

SulLaLuna — HTF M2 x Ultimate BB (Fusion) 🌕 **SulLaLuna — HTF M2 x Ultimate BB (Fusion)** 🚀💵

**By SulLaLuna Trading**

(Portions of the Bollinger Band logic adapted with permission/credit from the *Ultimate Buy & Sell Indicator* by its original author — thank you for the brilliance!)

---

🧭 **What This Is**

This is not just another price-following tool.

This is **a macro liquidity detector** — a **Daily Higher Timeframe Hull Moving Average of the Global M2 Money Supply**, smoothed via lower timeframe candles (default 5m, 48 Hull length), overlaid with **Ultimate-style double Bollinger Bands** to reveal *over-extension & mean reversion zones*.

It doesn’t chase candles.

It watches the tides beneath the market — the **money supply currents** that have a **direct correlation** to asset price behavior.

When liquidity expands → risk-on assets tend to rise.

When liquidity contracts → risk-off waves hit.

We ride those waves.

---

🔍 **What It Does**

* **Tracks Global M2** across major economies, FX-adjusted, and scales it to your chart’s price.

* **HTF Hull MA** (Daily, smoothed via 5m base) → gives you the macro liquidity trend.

* **Ultimate BB logic** applied to the HTF M2 Hull → inner/outer bands for volatility envelopes.

* **Pivot Labels** → ideal entry/exit zones on macro turns.

* **Over-Extension Alerts** → when HTF M2 Hull pushes outside the outer bands.

* **Re-Entry Alerts** → mean reversion triggers when liquidity moves back inside the range.

* **Background Paint** from chart TF M2 slope → for confluence on your entry timeframe.

---

📜 **Suggested How-To**

1. **Choose your execution chart** — e.g., 1–15m for scalps, 1H–4H for swings.

2. **Use the background paint** as your *local tide check* (chart TF M2 slope).

3. **Trade in the direction of the HTF M2 Hull** — green line = liquidity rising, red line = liquidity falling.

4. **Watch pivot labels** — these are potential “macro inflection” points.

5. **Confluence stack** — pair with ZLSMA, WaveTrend divergences, VWAP volume, or your favorite price-action setups.

6. **Size down** when HTF M2 Hull is flat/gray (chop zone).

7. **Scale in/out** on over-extension + re-entry alerts for higher probability swings.

---

⚠️ **Important Note**

This indicator **does not predict price** — it tracks macro liquidity flows that *influence* price.

Think of it as your market’s **tide chart**: when the water’s coming in, you can swim out; when it’s going out, you’d better be ready for the undertow.

---

📢 **Alerts Available**

* HTF Pivot HIGH / LOW

* Over-Extension (HTF Hull outside outer BB)

* Re-Entry (return from overbought/oversold)

---

🤝 **Join the SulLaLuna Tribe**

If this indicator helps you capture better entries, follow & share so more traders can learn to trade *math, not emotion*.

We rise together — **and we’ll meet you on the Moon** 🌕🚀💵.

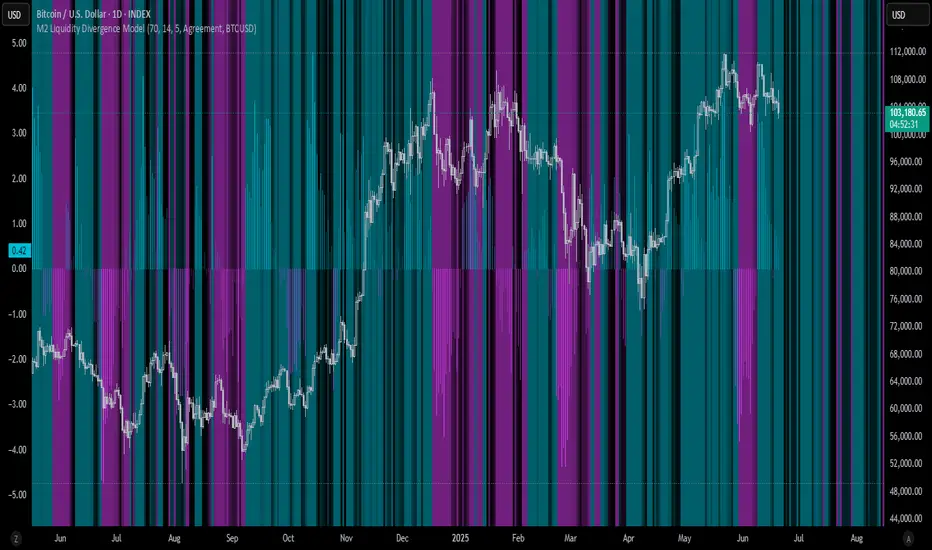

M2 Liquidity Divergence ModelM2 Liquidity Divergence Model

The M2 Liquidity Divergence Model is a macro-aware visualization tool designed to compare shifts in global liquidity (M2) against the performance of a benchmark asset (default: Bitcoin). This script captures liquidity flows across major global economies and highlights whether price action is aligned ("Agreement") or diverging ("Divergence") from macro trends.

🔍 Core Features

M2 Global Liquidity Index (GLI):

Aggregates M2 money supply from major global economies, FX-adjusted, including extended contributors like India, Brazil, and South Africa. The slope of this composite is used to infer macro liquidity trends.

Lag Offset Control:

Allows the M2 signal to lead benchmark asset price by a configurable number of days (Lag Offset), useful for modeling the forward-looking nature of macro flows.

Gradient Macro Context (Background):

Displays a color-gradient background—aqua for expansionary liquidity, fuchsia for contraction—based on the slope and volatility of M2. This contextual backdrop helps users visually anchor price action within macro shifts.

Divergence Histogram (Optional):

Plots a histogram showing dynamic correlation or divergence between the liquidity index and the selected benchmark.

Agreement Mode: M2 and asset are moving together.

Divergence Mode: Highlights break in expected macro-asset alignment.

Adaptive Transparency Scaling:

Histogram and background gradients scale their visual intensity based on statistical deviation to emphasize stronger signals.

Toggle Options:

Show/hide the M2 Liquidity Index line.

Show/hide divergence histogram.

Enable/disable visual offset of M2 to benchmark.

🧠 Suggested Usage

Macro Positioning: Use the background context to align directional trades with macro liquidity flows.

Disagreement as Signal: Use divergence plots to identify when price moves against macro expectations—potential reversal or exhaustion zones.

Time-Based Alignment: Adjust Lag Offset to synchronize M2 signals with asset price behavior across different market conditions.

⚠️ Disclaimer

This indicator is designed for educational and analytical purposes only. It does not constitute financial advice or an investment recommendation. Always conduct your own research and consult a licensed financial advisor before making trading decisions.

BSL & SSL - Liquidity Zones

BSL & SSL - Liquidity Zones

Indicator Description (for TradingView)

Concept

The BSL & SSL - Liquidity Zones indicator is a simple yet powerful visual tool that helps traders identify key liquidity zones in the market by tracking prominent highs and lows on the chart.

It is based on the concept that the Highest High (Buy Side Liquidity - BSL) and Lowest Low (Sell Side Liquidity - SSL) represent zones where stop-loss orders and pending orders accumulate — often attracting future price movements.

Purpose

This indicator helps traders spot hidden liquidity levels which may act as targets or potential reversal points. It is especially useful for traders who apply Smart Money Concepts (SMC) or institutional trading models.

Great for detecting potential stop hunts and understanding market structure shifts.

How It Works

The indicator calculates the Highest High and Lowest Low over a user-defined period (default: 20 candles).

When a new Higher High forms, it marks a new BSL.

When a new Lower Low forms, it marks a new SSL.

These zones are likely to attract price in the future — either as targets or traps.

Visualization

The indicator draws static horizontal lines (Stepline style) at BSL and SSL levels.

These lines remain in place until broken or a new level is formed.

Visual Labels enhance clarity:

🟢 Green Label → BSL

🔴 Red Label → SSL

Trading Insights / Practical Use

When price approaches a BSL or SSL zone, ask yourself:

✅ Will price break the level to grab liquidity?

✅ Will there be a reversal after liquidity is taken?

The indicator does not provide signals by itself — it serves as a valuable confirmation tool when combined with:

Price Action

Support & Resistance

Momentum Indicators

SMC Tools

Key Benefits

✅ Easy to use

✅ Enhances liquidity analysis

✅ Highlights zones targeted by institutional players

✅ Simple calculation — no complex formulas

Limitations

🚫 Does NOT generate buy/sell signals

🚫 Should be used as part of a complete trading framework

Conclusion

BSL & SSL - Liquidity Zones is a versatile and intuitive tool for any trader looking to better understand where liquidity is positioned on the chart.

It works across all timeframes and complements any trading strategy, especially Smart Money-based approaches.

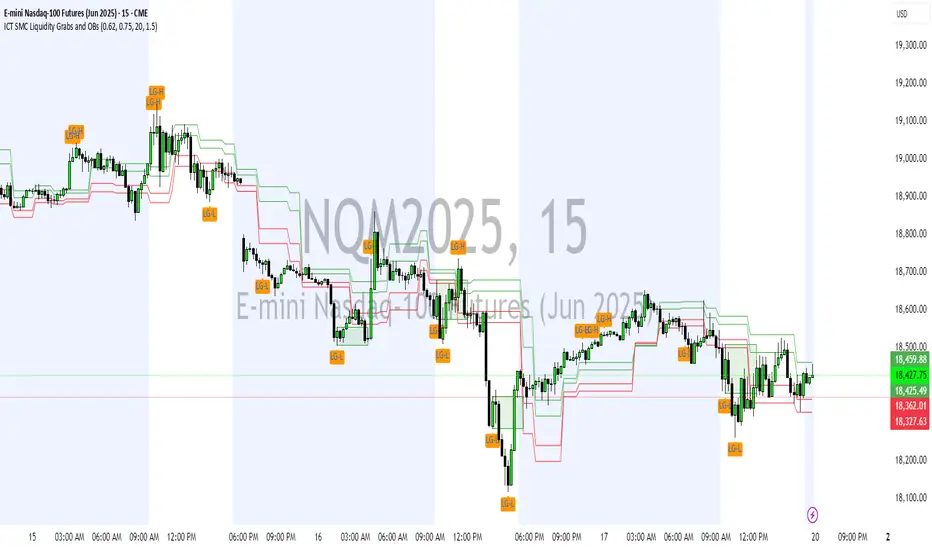

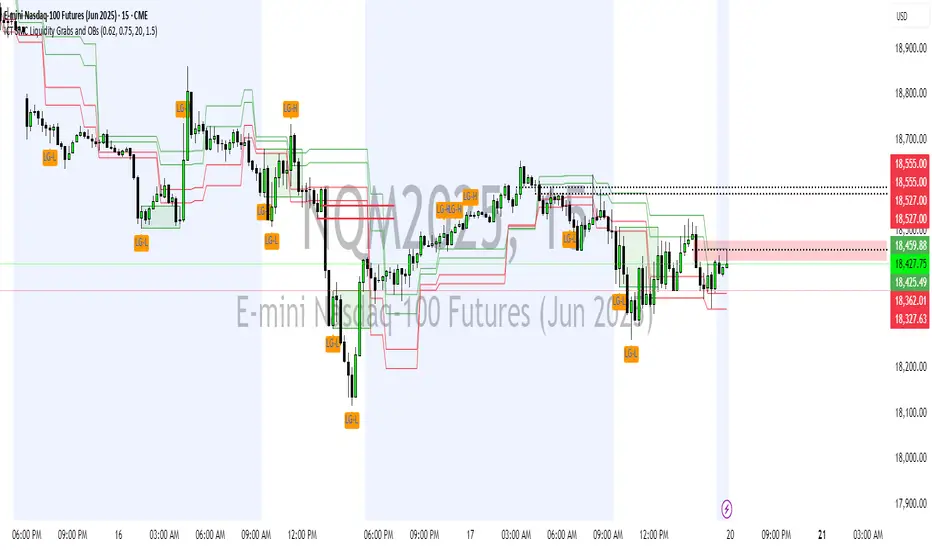

ICT SMC Liquidity Grabs and OBsICT SMC Liquidity Grabs + Order Blocks + Fibonacci OTE Levels

A High-Probability Entry Engine for Smart Money Concept Traders

This script combines three powerful Smart Money Concepts (SMC) into a single tool: Liquidity Grabs, Order Block Zones, and Fibonacci OTE Levels, allowing traders to identify institutional entry models with clean, rule-based visual signals.

It’s designed to simplify SMC trading by highlighting confluence zones where price is likely to reverse or continue — with clear visual zones, entry arrows, and take profit projections.

🔍 What This Script Does:

Detects Liquidity Grabs

Identifies when price sweeps above/below the highest high or lowest low within a user-defined lookback period and closes back inside.

Plots orange labels on the chart to signal potential liquidity events (LG-H / LG-L).

Plots Order Blocks After Liquidity Grabs

After a liquidity grab, the script looks for displacement candles (strong bullish or bearish moves) and draws highlighted OB zones extending several bars to the right.

These zones represent potential institutional footprints for price reversals.

Draws Fibonacci OTE Levels (Optimal Trade Entry)

Uses recent swing high and low pivots to automatically calculate OTE zones (default: 62% and 75% retracement levels).

Draws these retracement zones for both bullish and bearish setups.

Marks Valid OTE Entry Zones

Buy/Sell zones only trigger when:

A liquidity grab occurs,

Price enters the OTE zone,

And a strong confirming candle is present.

Plots green/red arrows for valid buy/sell OTE entries.

Auto-Draws Take Profit Zones

TP1 = Previous swing high/low

TP2 = Risk-based R-multiplied extension (e.g., 1.5R — customizable)

Alerts

Triggers alerts when valid buy or sell OTE setups are detected.

⚙️ Customization Features:

Toggle each feature: Liquidity Grabs, Order Blocks, Fibonacci OTE levels

Set Fibonacci retracement percentages (e.g., 0.62 / 0.75)

Adjust lookback window for liquidity detection

Customize the take-profit multiplier (R-based)

Full control over visuals: colors, labels, and lines

💡 How to Use:

Use this script to scan for high-confluence trade setups based on Smart Money principles.

Combine with session timing (e.g., New York open), major swing structure, or Kill Zone windows for maximum edge.

Look for arrows inside OB zones or OTE levels following liquidity sweeps for cleaner entries.

🔗 Works Best With:

✅ First FVG — Opening Range Fair Value Gap Detector: Identify early inefficiencies to set the narrative for the day.

✅ Liquidity Levels — Smart Swing Lows: Spot key structural lows that can fuel stop hunts and reversals.

✅ ICT Turtle Soup — Liquidity Reversal: Add a classic reversal pattern to your toolkit to catch fakeouts cleanly.

Together, these tools build a complete Smart Money ecosystem for entry precision, risk management, and price behavior forecasting.

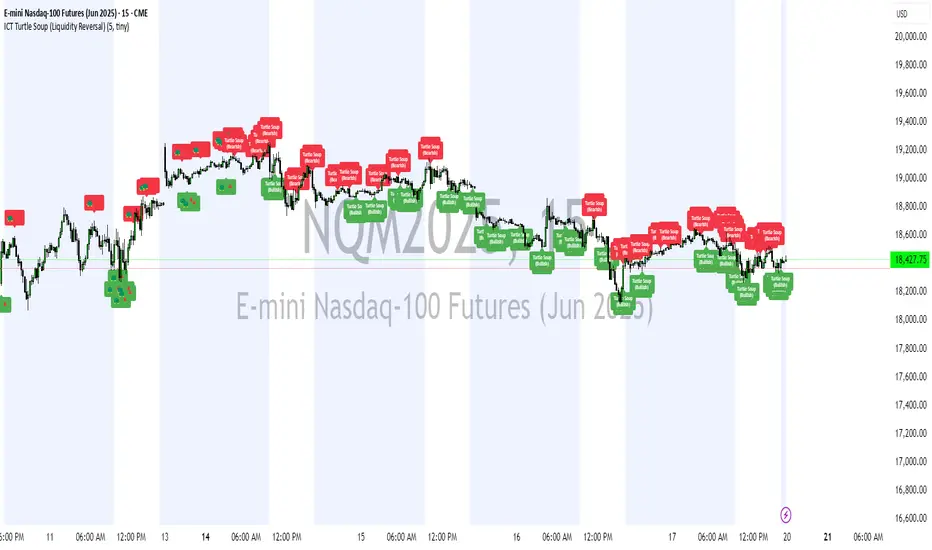

ICT Turtle Soup (Liquidity Reversal)ICT Turtle Soup — Liquidity Reversal Detection

Trap the Trap: A Precision Reversal Strategy from the Inner Circle Trader Playbook

This indicator implements the Turtle Soup liquidity reversal setup — a widely used ICT (Inner Circle Trader) concept that targets false breakouts beyond recent swing highs or lows. These patterns typically occur when price grabs liquidity above or below a known level, then snaps back, trapping retail traders and creating a high-probability reversal scenario.

🔍 What This Script Does:

Detects Liquidity Sweeps Above/Below Key Swing Levels

Uses a customizable swing lookback to identify recent swing highs and lows.

Triggers a Bearish Turtle Soup when price runs above a previous swing high and closes back below.

Triggers a Bullish Turtle Soup when price sweeps below a prior swing low and closes back above.

Plots Clear Visual Signals

Reversal signals appear as 🐢🔻 (Bearish) or 🐢🔺 (Bullish) markers directly on your chart.

Optional labels can be enabled for enhanced journaling and review.

Real-Time Alerts

Receive alert notifications when a Turtle Soup setup is detected — ideal for scalpers or intraday traders watching for reversals around liquidity pools.

⚙️ Customization Options:

Set the swing lookback sensitivity (default: 5)

Enable or disable labels

Choose label font size

Customize colors for bullish and bearish signals

💡 How to Use:

Deploy on intraday timeframes (e.g. 5m–15m) for high-resolution liquidity analysis.

Watch for signals at key highs/lows, session extremes, or zones where liquidity is likely resting.

Combine with tools like FVGs, Order Blocks, and OTE zones for layered confirmation.

🔗 Combine With These Tools for a Complete SMC Edge:

✅ First FVG — Opening Range Fair Value Gap Detector

✅ ICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

✅ Liquidity Levels — Smart Swing Lows

Together, these tools form a high-precision Smart Money toolkit — helping traders map, anticipate, and act on institutional-level liquidity events with clarity and confidence.

ICT Turtle Soup (Liquidity Reversal)ICT Turtle Soup — Liquidity Reversal Detection

Classic Liquidity Trap Reversal Strategy for Smart Money Traders

This indicator implements the ICT Turtle Soup concept — a classic liquidity-based reversal pattern — which occurs when price runs above or below a recent swing level to grab liquidity, then sharply reverses. This pattern is commonly used in Smart Money Concepts (SMC) and Inner Circle Trader (ICT) strategies to anticipate false breakouts and high-probability reversals.

🔍 What This Script Does:

Identifies Swing Highs & Lows

Detects recent swing highs and lows using a customizable lookback period.

Tracks Liquidity Grabs

A bearish Turtle Soup setup is triggered when price breaks above a recent swing high but closes back below it.

A bullish Turtle Soup setup is triggered when price breaks below a recent swing low but closes back above it.

These conditions often signal liquidity traps, where price sweeps resting orders before reversing.

Plots Signals Directly on the Chart

Turtle Soup setups are marked with 🐢🔻 (bearish) and 🐢🔺 (bullish) labels.

Optional full-text labels can also be displayed for clarity and journaling.

Includes Alert Conditions

Alerts can be enabled to notify you of bullish or bearish Turtle Soup reversals in real-time.

⚙️ Customization Features:

Adjustable swing lookback period

Enable/disable Turtle Soup labels

Set label font size

Choose your preferred bullish/bearish signal colors

💡 How to Use:

Add this script to your chart (ideally on intraday timeframes such as 5m–15m).

Wait for a Turtle Soup signal near a key swing high/low or liquidity zone.

Combine with other confirmation tools (e.g., FVGs, Order Blocks, OTE) for stronger setups.

Use alerts to stay ahead of fast-moving reversals.

🧠 Why It Works:

Turtle Soup setups are rooted in liquidity theory — they exploit the market’s tendency to sweep obvious swing levels before reversing. These moves often trap retail traders and mark the beginning of Smart Money entries.

🔗 Best Used With:

Maximize the edge by combining this with other SMC tools:

✅ First FVG — Opening Range Fair Value Gap Detector

✅ ICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

✅ Liquidity Levels — Smart Swing Lows

Together, they create a complete ecosystem for identifying, confirming, and executing liquidity-driven trade setups with precision.

Global M2 Liquidity [TheAlchimist]🌍 Global M2 Liquidity – Navigating the Quantum Field of Markets 🌍

Category: Macroeconomic Indicators 📊

"In quantum physics, the observer effect states that the mere act of observation changes the system being observed. Similarly, in financial markets, global liquidity acts as a quantum field that permeates all market states simultaneously. Just as Heisenberg’s uncertainty principle suggests we cannot precisely measure both position and momentum, the M2 money supply’s influence on market dynamics creates a complex web of cause and effect across multiple timeframes."

📈 Overview

The Global M2 Liquidity indicator is a powerful tool that tracks the combined M2 money supply from five major economies (US, EU, China, Japan, UK), converted to USD 💵, offering a panoramic view of global liquidity conditions. With multi-timeframe analysis and a customizable forward-shift feature, it empowers traders to anticipate market movements driven by liquidity trends.

✨ Features

- Global Coverage 🌎: Monitors M2 money supply from 5 major economic regions (US, EU, China, Japan, UK).

- Real-Time Conversion 💱: Converts all data to USD for consistent analysis.

- Multi-Timeframe Analysis ⏰: Tracks liquidity from 15-minute to weekly charts.

- Forward-Shift Capability 🔮: Aligns M2 data with future price action for predictive insights.

- Color-Coded Trends 🎨: Visualizes liquidity trends (🟢 Expansion, 🔴 Contraction).

🚀 How to Use

1. Main Line 📉: Displays total global M2 liquidity in trillions of USD.

2. Golden Moving Average ⭐: Identifies the overall trend direction.

3. Trend Colors 🟢🔴:

- Green: Liquidity expanding above the moving average (bullish for risk assets).

- Red: Liquidity contracting below the moving average (bearish signal).

4. Forward Shift ⏩: Use the shift parameter to align M2 data with price action for predictive analysis.

5. Combine with Price Action 🔍: Correlate liquidity trends with assets like Bitcoin, stocks, or forex for strategic entries/exits.

⚙️ Settings

- MA Period 📏: Length of the moving average (default: 50).

- Shift ⏳: Number of days to shift data forward (default: 60).

🏷️ Tags

#Trading #Macroeconomic #M2Liquidity #GlobalLiquidity #MoneySupply #MultiTimeframe #TrendAnalysis #PredictiveAnalysis #Forex #Stocks #Crypto #Bitcoin #RiskAssets #CentralBanks #USD #TheAlchimist #QuantumTrading #AlgoTrading #DayTrading #SwingTrading

ICT SMC Liquidity Grabs and OBsICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

Smart Money Concepts Trading Assistant

This script is built for traders who follow ICT (Inner Circle Trader) and Smart Money Concepts. It intelligently combines three critical components of SMC trading: Liquidity Grabs, Order Blocks, and Fibonacci-based Optimal Trade Entry (OTE) zones — giving traders visual cues for potential high-probability reversals and entry points.

🔍 What This Script Does:

Detects Liquidity Grabs

Identifies swing highs/lows where price sweeps liquidity, then immediately reverses.

Labels them with orange markers when price takes out previous highs/lows but closes back inside.

Draws Order Blocks

After a liquidity grab, the script looks for strong bullish or bearish candles and automatically highlights the OB zone.

These OB zones are visualized with transparent colored boxes extending several bars forward.

Plots Fibonacci OTE Levels

Uses recent swing high/low pivots to dynamically draw customizable OTE retracement levels (e.g., 62% and 75%) for both long and short setups.

Highlights Optimal Entry Zones

Marks valid OTE-based buy/sell opportunities only when:

Liquidity has been taken,

Price enters the OTE zone,

And a strong confirming candle appears.

Adds visual zones, trade labels, and optional alerts for each qualified entry.

Includes Take Profit Targets

Automatically calculates take-profit levels based on previous structure and risk-reward ratios.

TP1 is the previous swing, and TP2 is an extended R-multiple (customizable by user).

⚙️ Customization Options:

Toggle each feature (Liquidity Grabs, OBs, Fibonacci Levels)

Adjust Fibonacci levels (default: 62% and 75%)

Set lookback period for liquidity checks

Customize the R-multiple for TP2 levels

💡 How to Use:

Enable desired features from the input panel.

Watch for Buy/Sell OTE zones highlighted in green/red.

Confirm with liquidity sweep and OB support for stronger signals.

Use the automatically generated TP levels to manage risk.

🚀 What Makes It Unique:

Unlike other open-source mashups, this script synchronizes multiple SMC concepts into a single tool that:

Waits for high-confidence conditions (not just blind fib or OB detection)

Validates entries using multiple confluences

Visually marks actionable setups

Automates trade management zones

Whether you're trend-trading, scalping, or swing trading ICT-style, this tool offers a streamlined, smart-money-aligned workflow directly on your chart.

ICT SMC Liquidity Grabs and OBsICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

Smart Money Concepts Trading Assistant

This script is built for traders who follow ICT (Inner Circle Trader) and Smart Money Concepts. It intelligently combines three critical components of SMC trading: Liquidity Grabs, Order Blocks, and Fibonacci-based Optimal Trade Entry (OTE) zones — giving traders visual cues for potential high-probability reversals and entry points.

🔍 What This Script Does:

Detects Liquidity Grabs

Identifies swing highs/lows where price sweeps liquidity, then immediately reverses.

Labels them with orange markers when price takes out previous highs/lows but closes back inside.

Draws Order Blocks

After a liquidity grab, the script looks for strong bullish or bearish candles and automatically highlights the OB zone.

These OB zones are visualized with transparent colored boxes extending several bars forward.

Plots Fibonacci OTE Levels

Uses recent swing high/low pivots to dynamically draw customizable OTE retracement levels (e.g., 62% and 75%) for both long and short setups.

Highlights Optimal Entry Zones

Marks valid OTE-based buy/sell opportunities only when:

Liquidity has been taken,

Price enters the OTE zone,

And a strong confirming candle appears.

Adds visual zones, trade labels, and optional alerts for each qualified entry.

Includes Take Profit Targets

Automatically calculates take-profit levels based on previous structure and risk-reward ratios.

TP1 is the previous swing, and TP2 is an extended R-multiple (customizable by user).

⚙️ Customization Options:

Toggle each feature (Liquidity Grabs, OBs, Fibonacci Levels)

Adjust Fibonacci levels (default: 62% and 75%)

Set lookback period for liquidity checks

Customize the R-multiple for TP2 levels

💡 How to Use:

Enable desired features from the input panel.

Watch for Buy/Sell OTE zones highlighted in green/red.

Confirm with liquidity sweep and OB support for stronger signals.

Use the automatically generated TP levels to manage risk.

🚀 What Makes It Unique:

Unlike other open-source mashups, this script synchronizes multiple SMC concepts into a single tool that:

Waits for high-confidence conditions (not just blind fib or OB detection)

Validates entries using multiple confluences

Visually marks actionable setups

Automates trade management zones

Whether you're trend-trading, scalping, or swing trading ICT-style, this tool offers a streamlined, smart-money-aligned workflow directly on your chart.

M2 Global Liquidity Index - 10 Week Lead

M2 Global Liquidity Index - Forward Projection (10 Weeks)

This indicator provides a 10-week forward projection of the M2 Global Liquidity Index, offering traders insight into potential future market conditions based on global money supply trends.

What This Indicator Shows

The M2 Global Liquidity Index aggregates M2 money stock data from five major economies:

- China (CNY)

- United States (USD)

- European Union (EUR)

- Japan (JPY)

- Great Britain (GBP)

All values are converted to USD and presented as a unified global liquidity metric, providing a comprehensive view of worldwide monetary conditions.

Forward Projection Feature

This adaptation displays the indicator 10 weeks ahead of the current price, allowing you to visualize potential future liquidity conditions that might influence market behavior. The projection maintains data integrity while providing an advanced view of the liquidity landscape.

Trading Applications

- Anticipate potential market reactions to changing global liquidity conditions

- Identify divergences between projected liquidity and current price action

- Develop longer-term strategic positions based on forward liquidity projections

- Enhance your macro-economic analysis toolkit

Credit

This indicator is an adaptation of the original "M2 Global Liquidity Index" created by Mik3Christ3ns3n. Full credit for the original concept and implementation goes to the original author. This version simply adds a 10-week forward projection to the existing calculations.

Disclaimer

This indicator is for informational purposes only and should be used as one of many tools in your analysis. Past performance and projections are not guarantees of future results.

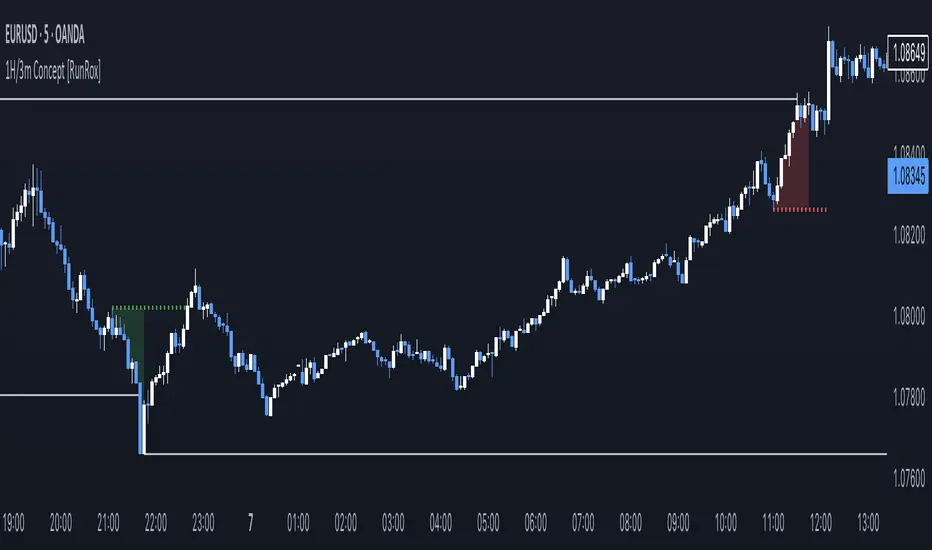

1H/3m Concept [RunRox]🕘 1H/3m Concept is a versatile trading methodology based on liquidity sweeps from fractal points identified on higher timeframes, followed by price reversals at these key moments.

Below, I will explain this concept in detail and provide clear examples demonstrating its practical application.

⁉️ WHAT IS A FRACTALS?

In trading, a fractal is a technical analysis pattern composed of five consecutive candles, typically highlighting local market turning points. Specifically, a fractal high is formed when a candle’s high is higher than the highs of the two candles on either side, whereas a fractal low occurs when a candle’s low is lower than the lows of the two adjacent candles on both sides.

Traders use fractals as reference points for identifying significant support and resistance levels, potential reversal areas, and liquidity zones within price action analysis. Below is a screenshot illustrating clearly formed fractals on the chart.

📌 ABOUT THE CONCEPT

The 1H/3m Concept involves marking Higher Timeframe (HTF) fractals directly onto a Lower Timeframe (LTF) chart. When a liquidity sweep occurs at an HTF fractal level, we remain on the same LTF chart (since all HTF fractals are already plotted on this lower timeframe) and wait for a clear Market Structure Shift (MSS) to identify our potential entry point.

Below is a schematic illustration clearly demonstrating how this concept works in practice.

Below is another 💡 real-chart example , showing liquidity in the form of a 1H fractal, swept by a rapid impulse move. Immediately afterward, a clear Market Structure Shift (MSS) occurs, signaling a potential entry point into the trade.

Another example is shown below, where we see our hourly fractal, from which price clearly reacts, providing an opportunity to search for an entry point.

As illustrated on the chart, the fractal levels from the higher timeframe are clearly displayed, but we’re working directly on the 5-minute chart. This allows us to remain on one timeframe without needing to switch back and forth between charts to spot such trading setups.

🔍 MTF FRACTALS

This concept can be applied across various HTF-LTF timeframe combinations. Although our examples illustrate 1H fractals used on a 5-minute chart, you can effectively utilize many other timeframe combinations, such as:

30m HTF fractals on 1m chart

1H HTF fractals on 3m chart

4H HTF fractals on 15m chart

1D HTF fractals on 1H chart

The key idea behind this concept is always the same: identify liquidity at fractal levels on the higher timeframe (HTF), then wait for a clear Market Structure Shift (MSS) on the lower timeframe (LTF) to enter trades.

⚙️ SETTINGS

🔷 Trade Direction – Select the preferred trading direction (Long, Short, or Both).

🔷 HTF – Choose the higher timeframe from which fractals will be displayed on the current chart.

🔷 HTF Period – Number of candles required on both sides of a fractal candle (before and after) to confirm fractal formation on the HTF.

🔷 Current TF Period – Sensitivity to the impulse that sweeps liquidity, used for identifying and forming the MSS line.

🔷 Show HTF – Enable or disable displaying HTF fractal lines on your chart. You can also customize line style and color.

🔷 Max Age (Bars) – Number of recent bars within which fractals from the selected HTF will be displayed.

🔷 Show Entry – Enable or disable displaying the MSS line on the chart.

🔷 Enable Alert – Activates TradingView alerts whenever the MSS line is crossed.

You can also enable 🔔 alerts, which notify you whenever price crosses the MSS line. This significantly simplifies the process of identifying these setups on your charts. Simply configure your preferred timeframes and wait for notifications when the MSS line is crossed.

🔶 We greatly appreciate your feedback and suggestions for improving the indicator!

Killzones & Previous High-Low Liquidity [odnac]This indicator is designed for use in intraday trading to visualize key "Killzones" (specific time windows during different global market sessions) and highlight liquidity levels based on previous highs and lows from the previous day and week.

It helps traders identify potential market entry and exit points based on time-based trading zones and price action levels.

Key Features:

Killzone (Market Session Timeframes):

Asia (2000-0000 UTC): Displays a shaded box over the Asia trading session.

Europe (0200-0500 UTC): Highlights the European trading session.

New York AM (0830-1100 UTC): Represents the morning session of the NY market.

New York PM (1330-1600 UTC): Represents the afternoon session of the NY market.

Each of these timeframes can be customized in terms of session start and end times, and the shaded areas will help identify high liquidity periods when the market tends to be more active.

Previous High-Low Liquidity Zones:

Previous Week's High/Low: Displays lines at the high and low of the previous week.

These are important liquidity levels that can influence price action.

Previous Day's High/Low: Shows the high and low from the previous trading day.

These are also significant levels to watch for potential support and resistance.

Filters and Customization:

Position Filtering: The indicator allows users to filter out previous highs or lows if the current price doesn't align with those levels.

For example, it can filter out previous week highs if the current price is lower than that level.

Vertical Lines: Optional vertical lines to highlight key time points such as the start and end of the previous week and day.

How It Works:

The indicator visually draws "killzones" as shaded regions on the chart, indicating periods of increased market activity.

This can help traders align their strategies with the most liquid periods of the day.

The previous high and low lines (both for the previous week and the previous day) are drawn as solid lines and can be toggled on/off in the settings.

Labels are added to indicate the specific levels and periods.

The indicator provides clear visual cues, helping traders assess if the price is near important liquidity levels and whether the current market conditions align with those levels.

Customizable Settings:

You can control whether each Killzone and liquidity level is shown on the chart.

Color customization for the various zones and lines is also available.

The indicator also lets you decide whether to hide weekend data, set time-frame limits, and choose whether or not to show vertical lines at the beginning and end of each trading session.

This indicator is aimed at traders who want to trade based on high-liquidity periods and understand where key support and resistance levels are likely to emerge based on previous price action.

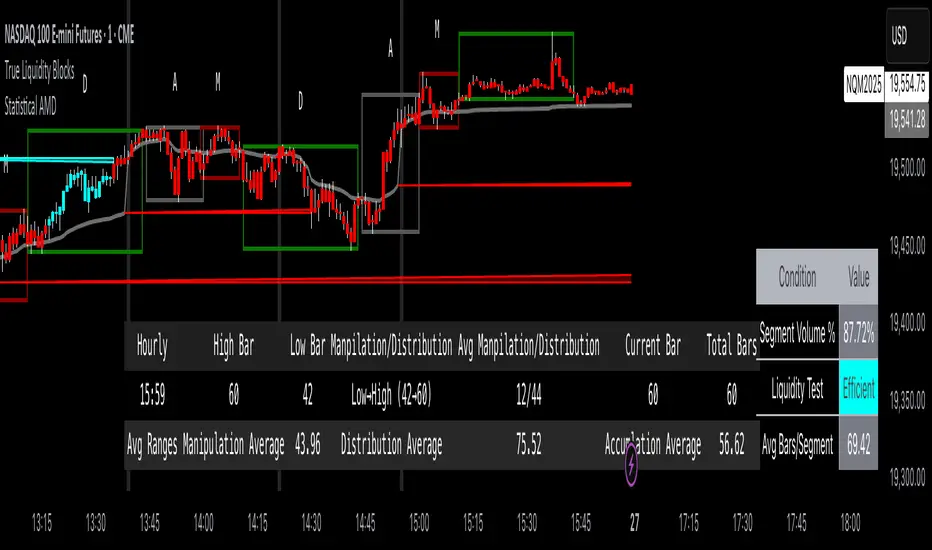

True Liquidity BlocksSo basically I've been deep diving into liquidity trading concepts similar to ICT (Inner Circle Trader) and developed an indicator that breaks down market movement through a volume-centric lens.

Key Concept:

Markets move not just by price, but by resolving trapped positions

Volume segments, not time intervals, show true market dynamics

VWAP (Volume Weighted Average Price) becomes a key structural reference

What Makes This Different:

Tracks volume segments instead of fixed time frames

Identifies "trapped" trader positions

Measures liquidity level efficiency

Color-codes bars based on nearest liquidity zone

Indicator Features:

Cyan/Red liquidity levels showing buy/sell pressure

Efficiency tracking for each level

Dynamic volume-based segmentation

Bar coloring to show nearest liquidity zone

Theoretical Inspiration: Viewed markets as energy systems where:

Positions create potential energy

Price movement resolves this energy

Trends form through systematic position liquidation

VWAP Recalculation in Each Segment:

Segment Start:

VWAP resets when volume threshold User Inputtable (600,000) is reached

Uses the last 4 price values (High, Low, Close, Close) for calculation

Weighted by volume traded during that segment

Calculation Method:

pineCopy = ta.vwap(hlcc4, na(segment_start) ? true : na, 1)

hlcc4: Combines high, low, close prices

na(segment_start): Ensures reset at new segment

Weighted by volume, not equal time intervals

Key Points:

Dynamic recalculation each segment

Reflects most recent trading activity

Provides real-time fair price reference

Tracks positioning

Essentially, VWAP resets and recalculates with each new volume segment, creating a rolling, volume-weighted average price that maps trader positioning.

BSL (Buy Side Liquidity) and SSL (Sell Side Liquidity) Explained:

When a volume segment closes relative to VWAP, it creates natural positioning traps:

BSL (Cyan) - Created when price closes BELOW THAT SEGMENT'S VWAP:

Bulls are positioned BELOW VWAP (trapped)

Shorts are positioned ABOVE VWAP (In Profit)

SSL (Red) - Created when price closes ABOVE THAT SEGMENT"S VWAP:

Bulls are positioned ABOVE VWAP (trapped)

Shorts are positioned BELOW VWAP (trapped)

Core Mechanism:

VWAP acts as a reference point for trader positioning

Trapped positions create inherent market tension

Levels expand to show accumulating pressure

Color-coded for quick identification of potential move direction

The goal: Visualize where traders are likely "stuck" and must eventually resolve their positions or liquidate other's, driving market movement.

It was just a fun experiment but If ya'll have any thoughts on it or what I could do to improve it, I would appreciate it.

Just a little note, It's optimized for futures, but if u uncheck the "Rest at Futures Open ?" setting, it allow full reign of any asset with volume data.

SMC Order Block & Liquidity EntryThe SMC Order Block and Liquidity Trap Entry Strategy script uses Smart Money Concepts (SMC), which analyze institutional actions in the market, to assist traders in identifying high-probability trades. In order to help traders match their entry with institutional activity, this script highlights important regions of interest, including order blocks, liquidity zones, and indications for Break of Structure (BOS) or Change of Character (CHoCH).

The fundamental ideas of this approach, which focuses on regions where institutions frequently make sizable orders or sweep liquidity, are based on SMC principles. Order blocks, which are frequently important support or resistance zones when institutions are involved, are the final bullish or bearish candle before a significant price move in the other direction. There are liquidity zones that show where retail stop-loss orders build up (above recent highs or below recent lows), such as Buy-Side Liquidity (BSL) and Sell-Side Liquidity (SSL). Before changing the direction of the price, institutions could target these zones, giving traders possible chances.

The script depicts liquidity levels above or below recent highs and lows, automatically finds order blocks within a specified lookback time, and looks for BOS (a continuation signal) or CHoCH (a reversal signal). When liquidity retests inside an order block coincide with BOS or CHoCH circumstances, entry signals are produced. While short entries are triggered when the price breaks below the order block and SSL, long entry alerts are triggered when the price breaks above the order block and BSL.

Night Low Liquidity Congestions with 4 Trading SessionsThis indicator is designed to help traders visualize and analyze key market periods of low liquidity during the night and identify high-activity zones in the morning. It also includes customizable time sessions for major global markets, including the European and American sessions, as well as the London Close session.

T he main functionalities include:

- Night Low Liquidity Phase: This highlights periods with typically low market activity during the night (default: 20:01–5:59). It also displays the total range (in pips) during this phase, allowing traders to identify potential price consolidations.

- Morning Hot Zone: This focuses on high-activity periods in the early morning (default: 6:00–7:59), providing visual cues without altering bar colors.

- European Trading Session: Displays the European market’s open hours (default: 8:00–12:00), shaded in blue, to mark increased volatility typically seen during this period.

- American Trading Session: Marks the active hours of the U.S. market (default: 12:01–16:59), where market activity tends to peak.

- London Close Area: Highlights the closing hours of the London market (default: 17:00–20:00), allowing traders to track potential liquidity shifts.

Key Features:

1. Customizable Time Sessions:

- The indicator allows for full customization of the start and end times for each market session, making it adaptable to different instruments and trading style.

- Traders can choose their preferred color and opacity for each time zone to suit their charting preferences.

2. Night Low Liquidity Pip Range Calculation:

- Automatically calculates and displays the pip range for the Night Low Liquidity phase.

- The range is colored red if it exceeds the specified threshold and green if it remains below it.

3. Alarm System:

- Customizable alerts for H1, M15, and M5 timeframes.

- Traders can set alerts to trigger just before a bar closes during specific sessions (European, American, or London Close) and on selected days of the week (Monday–Friday).

- The alarm system allows for full customization of active hours and days, giving traders full control over their notifications.

4. Clear Visual Cues:

- The indicator uses transparent shading to differentiate market sessions, making it easy to spot different phases of the trading day.

- Each session is visually distinct and can be toggled on or off based on trader preferences.

Ideal For:

- Traders who focus on intraday strategies and want to understand how market sessions affect liquidity and volatility.

- Those looking to trade during specific time windows like the Night Low Liquidity or Morning Hot Zones.

- Traders who need to automate their alerts based on specific market hours and close events for major timeframes.

Global Liquidity Index and DEMA1001. Global Liquidity Index:

The code calculates global liquidity from economic data from multiple countries and regions. Specifically, it aggregates money supply data from major economies such as the United States, Europe, China, and Japan, and sums and adjusts them to get a global liquidity index.

This index is calculated by summing data from different sources and subtracting the impact of some financial instruments (such as reverse repurchase agreements, etc.), and then converting the result into a number in trillions. This can help analyze the liquidity conditions in global money markets.

2. ROC SMA (Simple Moving Average of Rate of Change):

The code calculates the rate of change (ROC) of the global liquidity index, which is a way to measure the speed of change of the index.

Then, a simple moving average (SMA) is applied to the rate of change, which helps smooth the data and identify trends.

The ROC SMA curve is displayed in yellow to help users observe the trend of liquidity changes.

3. DEMA (Double Exponential Moving Average):

DEMA is a more complex moving average that attempts to reduce the lag of the moving average and provide a more sensitive trend response.

The calculation method is to first calculate a standard exponential moving average (EMA), then calculate the EMA of this EMA, and use these two results to calculate DEMA.

The code allows users to set the period length of DEMA (default is 100), which can adjust the speed of DEMA's response to price changes.

The DEMA curve is displayed in blue, helping users to more accurately capture the trends and changes of global liquidity indicators.

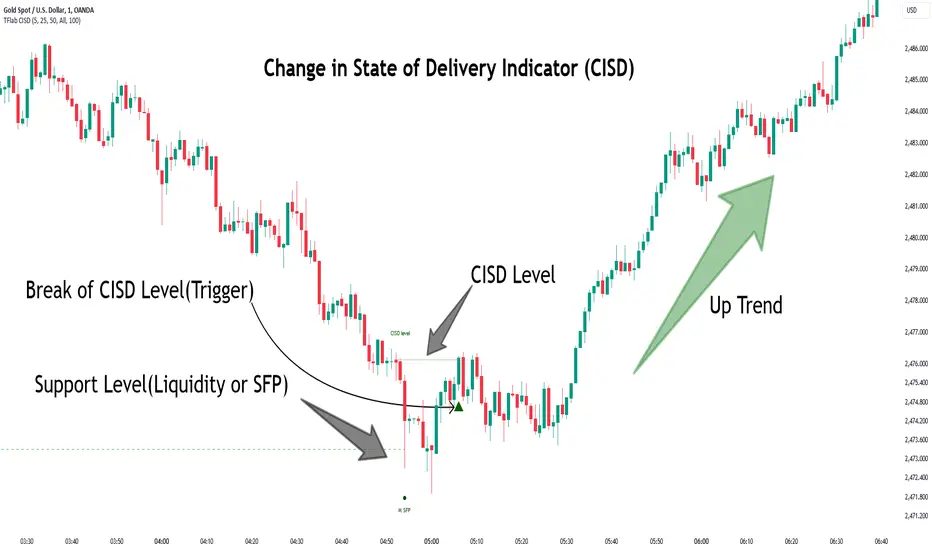

Change in State of Delivery CISD ICT [TradingFinder] Liquidity 1🔵 Introduction

🟣 What is CISD ?

Change in State of Delivery (CISD) is a key concept in technical analysis, similar to Change of Character (ChoCh) and Market Structure Shift (MSS) in the ICT (Inner Circle Trader) and Smart Money trading styles. Like ChoCh and MSS, CISD helps traders identify critical changes in market structure and make timely entries into trades.

To determine the CISD Level, traders typically review the last 1 to 4 candles to identify the first positive or negative candle. The CISD Level is then set using the opening price of the next candle.

In this version of the indicator, support and resistance levels are defined based on liquidity, which includes patterns such as SFP (Swing Failure Pattern), fake breakout, and false breakout.

Bullish CISD :

Bearish CISD :

🔵 How to Use

🟣 Bullish CISD (Change in State of Delivery Upward)

In Bullish CISD, the trend shifts from bearish to bullish after the price hits a liquidity zone, typically indicated by patterns such as SFP, fake breakout, or false breakout.

The steps to identify Bullish CISD are as follow s:

Identify the liquidity zone (SFP, fake breakout).

Review the candles and find the first positive candle.

Set the CISD Level using the opening price of the next candle after the positive candle.

Confirm the change in state of delivery when the price closes above the CISD Level.

Enter the trade after CISD confirmation.

🟣 Bearish CISD (Change in State of Delivery Downward)

In Bearish CISD, the trader looks for a shift from a bullish to a bearish trend. This change typically occurs when the price hits a liquidity level, indicated by patterns such as SFP or false breakout.

The steps to identify Bearish CISD are :

Identify the liquidity zone.

Review the candles and find the first negative candle.

Set the CISD Level using the opening price of the next candle after the negative candle.

Confirm the change in state of delivery when the price closes below the CISD Level.

Enter a short trade after CISD confirmation.

🟣 CISD Compared to ChoCh and MSS (CISD Vs ChoCh/ MSS)

CISD, ChoCh, and MSS are all tools for identifying trend changes in the market, but they have some differences :

CISD: Focuses on a change in the state of delivery and uses liquidity patterns (SFP, fake breakout) and key candles to confirm trend reversals.

ChoCh: Identifies a change in the market’s character, often signaling rapid shifts in trend direction.

MSS: Focuses on changes in market structure and identifies the breaking of key levels as a signal of trend shifts.

🔵 Settings

🟣 CISD Logical settings

Bar Back Check : Determining the return of candles to identify the CISD level.

CISD Level Validity : CISD level validity period based on the number of candles.

🟣 SFP Logical settings

Swing period : You can set the swing detection period.

Max Swing Back Method : It is in two modes "All" and "Custom". If it is in "All" mode, it will check all swings, and if it is in "Custom" mode, it will check the swings to the extent you determine.

Max Swing Back : You can set the number of swings that will go back for checking.

🟣 CISD Display settings

Displaying or not displaying swings and setting the color of labels and lines.

🟣 SFP Display settings

Displaying or not displaying swings and setting the color of labels and lines.

🔵 Conclusion

CISD is a powerful tool for identifying trend reversals using liquidity patterns and key candle analysis. Traders can use the CISD Level to detect trend changes and find optimal entry and exit points.

This concept is similar to ChoCh and MSS but stands out with its focus on confirming trend changes through liquidity and specific patterns. With the right approach, CISD helps traders capitalize on market movements more effectively.

M2 Global Liquidity Index (Candles)M2 Global Liquidity Index (Candles)

In this enhanced version of the original M2 Global Liquidity Index script by Mik3Christ3ns3n , I've taken the foundational concept and expanded its capabilities for more in-depth analysis and user flexibility. This updated script aggregates M2 money supply data from major global economies—China, the U.S., the Eurozone, Japan, and the U.K.—adjusted by their respective exchange rates, into a customizable global liquidity index.

Key Enhancements:

Candlestick Visualization:

• Instead of a simple line chart, I've implemented a candlestick chart, providing a more detailed representation of liquidity trends with open, high, low, and close values for each period. This allows traders to analyze the index with the same technical tools used for price charts.

Customizable Components:

• Users can now select which components (M2 data and exchange rates) to include in the index calculation, giving you the flexibility to tailor the index to specific economic factors or regions of interest.

Dynamic Color Coding:

• Candles are color-coded based on their performance (bullish or bearish), with customized wick and border colors to enhance visual clarity, making it easier to spot liquidity trends at a glance.

Overlay Option:

• This script is designed to be an overlay, allowing you to plot the Global Liquidity Index directly on your price charts, facilitating comparison between liquidity trends and asset prices.

This enhanced script is ideal for traders and analysts who want a deeper understanding of global liquidity trends and their impact on financial markets.

God's of LiquidityHere’s a detailed description for your script, following the guidelines for clarity and originality:

---

**Title:** God's of Liquidity

**Description:**

The "Gods of Liquidity" script is a comprehensive trading tool designed to help traders identify high-probability buy and sell opportunities based on a combination of liquidity levels, RSI-based sentiment analysis, and session-specific filters.

**Key Features:**

1. **Liquidity Zones Identification:**

- The script dynamically calculates the previous day's high and low levels, which serve as critical liquidity zones. Traders can use these levels to spot potential breakout points and reversals.

2. **RSI-Based Sentiment Analysis:**

- The script incorporates a sophisticated RSI-based sentiment model that differentiates between institutional (Banker) and retail (Hot Money) activity. This dual RSI approach allows traders to gauge market sentiment and anticipate shifts in momentum.

- **Banker RSI:** Measures the sentiment of institutional traders, with customizable sensitivity and period parameters.

- **Hot Money RSI:** Measures retail trader sentiment, with its own adjustable settings to tailor the script to various market conditions.

3. **Session and Day Filters:**

- Traders can restrict signals to specific trading sessions and days of the week, providing greater control and precision in executing trades. This feature is particularly useful for aligning trading activity with market conditions that best suit the strategy.

4. **Breakout and Reversal Signals:**

- The script generates buy signals when the price breaks above the previous day's high, accompanied by bullish RSI sentiment from institutional traders. Conversely, sell signals are generated when the price breaks below the previous day's low, with bearish institutional sentiment.

- These signals are visually marked on the chart, making it easier for traders to identify potential trading opportunities.

5. **Customizable Moving Averages:**

- The script allows users to customize the moving averages used in the RSI calculations, giving traders the flexibility to adapt the tool to their specific trading style and market conditions.

6. **Alert System:**

- Alerts are integrated to notify traders when buy or sell conditions are met, ensuring that traders can react promptly to potential trading opportunities without constantly monitoring the charts.

**How It Works:**

- The script uses the previous day's high and low as key liquidity levels. The price crossing these levels, combined with RSI-based signals, indicates potential buy or sell opportunities.

- The sentiment analysis is derived from the RSI values, with separate calculations for institutional and retail activities. The crossover points of these RSI values against their respective moving averages trigger buy or sell signals.

- The session and day filters allow traders to focus on the most relevant times for trading, enhancing the effectiveness of the strategy.

**Usage:**

- This indicator is designed for Forex traders who want to integrate liquidity zones and sentiment analysis into their trading strategy. It is particularly effective on daily or higher timeframes where liquidity levels and RSI-based sentiment analysis can provide strong indications of market direction.

- The script's flexibility in adjusting session times, days, and RSI parameters makes it suitable for a wide range of trading styles, from day trading to swing trading.

---

**License:**

This source code is subject to the terms of the Mozilla Public License 2.0 at (mozilla.org).

© bankbaguitarcrazy

---

This description should provide sufficient detail to comply with the publication guidelines, offering clear insight into how the script works and its unique features.

Daily Liquidity Peaks and Troughs [ST]Daily Liquidity Peaks and Troughs

Description in English:

This indicator identifies peaks and troughs of highest liquidity on a daily timeframe by analyzing volume data. It helps traders visualize key points of high buying or selling pressure, which could indicate potential reversal or continuation areas.

Detailed Explanation:

Configuration:

Lookback Length: This input defines the period over which the highest high and lowest low are calculated. The default value is 14. This means the script will look at the past 14 bars to determine if the current high or low is a pivot point.

Volume Threshold Multiplier: This input defines the multiplier for the average volume. For example, a multiplier of 1.5 means the volume needs to be 1.5 times the average volume to be considered a significant peak or trough.

Peak Color: This input sets the color for liquidity peaks. The default color is red.

Trough Color: This input sets the color for liquidity troughs. The default color is green.

Volume Calculation:

Average Volume: The script calculates the simple moving average (SMA) of the volume over the lookback period. This helps to identify periods of significantly higher volume.

Volume Threshold: The threshold is determined by multiplying the average volume by the volume threshold multiplier. Only volumes exceeding this threshold are considered significant.

Identifying Peaks and Troughs:

Liquidity Peak: A peak is identified when the current high is the highest high over the lookback period and the current volume exceeds the volume threshold. This indicates a potential area of strong selling pressure.

Liquidity Trough: A trough is identified when the current low is the lowest low over the lookback period and the current volume exceeds the volume threshold. This indicates a potential area of strong buying pressure.

These peaks and troughs are marked on the chart with labels and shapes for easy visualization.

Plotting Peaks and Troughs:

Labels: The script uses labels to mark peaks and troughs on the chart. Peaks are marked with a red label and troughs with a green label.

Shapes: The script plots triangles above peaks and below troughs to highlight these areas visually.

Indicator Benefits:

Liquidity Identification: Helps traders identify key areas of high liquidity, indicating strong buying or selling pressure.

Visual Cues: Provides clear visual signals for potential reversal or continuation points, aiding in making informed trading decisions.

Customizable Parameters: Allows traders to adjust the lookback length and volume threshold to suit different trading strategies and market conditions.

Justification of Component Combination:

Peaks and Troughs Identification: Combining pivot points with volume analysis provides a robust method to identify significant liquidity areas. This helps in detecting potential market reversals or continuations.

Volume Analysis: Utilizing average volume and volume threshold ensures that only significant volume spikes are considered, enhancing the accuracy of identified peaks and troughs.

How Components Work Together:

The script first calculates the average volume over the specified lookback period.

It then checks each bar to see if it qualifies as a liquidity peak or trough based on the highest high, lowest low, and volume threshold.

When a peak or trough is identified, it is marked on the chart with a label and a shape, providing clear visual cues for traders.

Título: Picos e Fundos de Liquidez Diários

Descrição em Português:

Este indicador identifica picos e fundos de maior liquidez no gráfico diário, analisando os dados de volume. Ele ajuda os traders a visualizar pontos-chave de alta pressão de compra ou venda, o que pode indicar áreas potenciais de reversão ou continuação.

Explicação Detalhada:

Configuração:

Comprimento de Retrocesso: Este input define o período sobre o qual a máxima e mínima são calculadas. O valor padrão é 14. Isso significa que o script analisará os últimos 14 candles para determinar se a máxima ou mínima atual é um ponto de pivô.

Multiplicador de Limite de Volume: Este input define o multiplicador para o volume médio. Por exemplo, um multiplicador de 1.5 significa que o volume precisa ser 1.5 vezes o volume médio para ser considerado um pico ou fundo significativo.

Cor do Pico: Este input define a cor para os picos de liquidez. A cor padrão é vermelha.

Cor do Fundo: Este input define a cor para os fundos de liquidez. A cor padrão é verde.

Cálculo do Volume:

Volume Médio: O script calcula a média móvel simples (SMA) do volume ao longo do período de retrocesso. Isso ajuda a identificar períodos de volume significativamente mais alto.

Limite de Volume: O limite é determinado multiplicando o volume médio pelo multiplicador de limite de volume. Apenas volumes que excedem esse limite são considerados significativos.

Identificação de Picos e Fundos:

Pico de Liquidez: Um pico é identificado quando a máxima atual é a máxima mais alta no período de retrocesso e o volume atual excede o limite de volume. Isso indica uma potencial área de forte pressão de venda.

Fundo de Liquidez: Um fundo é identificado quando a mínima atual é a mínima mais baixa no período de retrocesso e o volume atual excede o limite de volume. Isso indica uma potencial área de forte pressão de compra.

Esses picos e fundos são marcados no gráfico com etiquetas e formas para fácil visualização.

Plotagem de Picos e Fundos:

Etiquetas: O script usa etiquetas para marcar picos e fundos no gráfico. Os picos são marcados com uma etiqueta vermelha e os fundos com uma etiqueta verde.

Formas: O script plota triângulos acima dos picos e abaixo dos fundos para destacar essas áreas visualmente.

Benefícios do Indicador:

Identificação de Liquidez: Ajuda os traders a identificar áreas-chave de alta liquidez, indicando forte pressão de compra ou venda.

Cues Visuais: Fornece sinais visuais claros para pontos potenciais de reversão ou continuação, auxiliando na tomada de decisões informadas.

Parâmetros Personalizáveis: Permite que os traders ajustem o comprimento de retrocesso e o limite de volume para se adequar a diferentes estratégias de negociação e condições de mercado.

Justificação da Combinação de Componentes:

Identificação de Picos e Fundos: A combinação de pontos de pivô com análise de volume fornece um método robusto para identificar áreas significativas de liquidez. Isso ajuda na detecção de potenciais reversões ou continuações de mercado.

Análise de Volume: Utilizar o volume médio e o limite de volume garante que apenas picos de volume significativos sejam considerados, aumentando a precisão dos picos e fundos identificados.

Como os Componentes Funcionam Juntos:

O script primeiro calcula o volume médio ao longo do período especificado de retrocesso.

Em seguida, verifica cada barra para ver se ela se qualifica como um pico ou fundo de liquidez com base