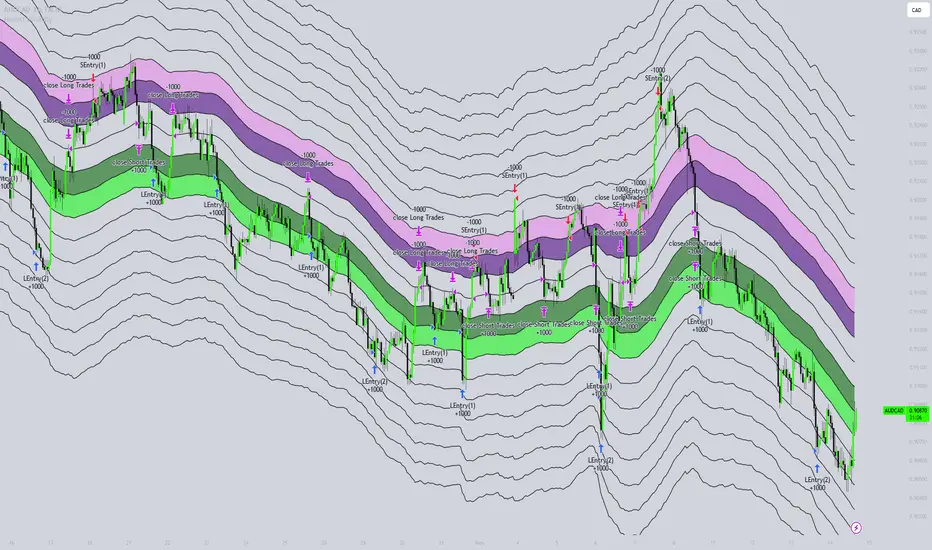

MACDouble & StochRSI w/ safeties and variable time interval v0.3UPDATE:

IMPORTANT!!! MAKE SURE "RECALCULATE AFTER ORDER FILLED" IS CHECKED. I will have it on by default in the future.

This is a continuation of my previous scripts of two MACD indicators with a Stochastic RSI indicator.

New features:

- Alternate MACD time interval

You can now set the time interval for the second MACD indicator to a different resolution than the displayed chart.

Uncheck the box and select the desired interval. For example, if your chart is set to 15min then first MACD will be set at 15 min and you can select 5 min for the second MACD.

- Alternate StoRSI time interval

You can (and should) set the StochRSI to a different time interval as well. StochRSI hasn't worked great with previous versions. Now you can set it to a different time resolution as well. I strongly recommend you set it at a higher (slower) resolution; for example if your chart is set at 15min then you should test setting the StochRSI at 30 or 45min.

- ' True" StochRSI logic

Trading logic for StochRSI is now a true StochRSI, instead of just reading "k" and ignoring "d", K now has to be greater than D to buy and less than to sell.

- Safeties

A primitive but low risk safety in the form of an uptrend/downtrend price safety. If current close+high isn't greater than the previous close and high then the buy order will not be executed. The same applies for sell orders.

- Cap on losses from short positions

A stop loss safety set to 9000 for exiting sell positions. This will need refinement in the future but this puts a cap on losses from any sell position. At an initial currency of 10,000 this translates to 90.00. If it is giving you problems simply delete line 78 from the source code.

Please feel free to ask any questions or send me suggestions. This is still very much a work in progress and I'll try to polish up the rough spots but it is fully functional. With a slower StochRSI and the safeties I have gotten it to consistently outperform the old 2x MACD strategy script---typically by 3-fold.

Tìm kiếm tập lệnh với "order"

Outsidebar vs Insidebar, Illusion Strategy (by ChartArt)WARNING: This strategy does not work! Please don't trade with this strategy

I'm sharing this strategy for the following three educational reasons:

1. You can easily find 100% strategies, but if they only seem to work 100% on one asset, they actually don't work at all. Therefore never backtest your strategy only on one asset, especially forward testing is useless, because it tends to repeat the old patterns. Your strategy has to work on as many different assets as possible.

2. The pyramiding of orders can have an impact on the strategy. In this case if you manually change the strategy settings by increasing it from 1 to 100 pyramiding orders changes the percent profitable on "UKOIL" monthly from 100% to 90% profitable. On other assets you can see very different results. Allowing much more pyramiding orders in this case results in opening orders where the background color highlights appear.

3. The Tradingview backtest beta version currently does not close the last open trade during the backtest. In this case going long on "UKOIL" near the top in 2011 as this strategy did would result in a big loss in 2015. But since the trade is still open and not canceled out by a new short order it still appears as if this strategy works 100% profitable. Which it doesn't.

Kalman VWAP Filter [BackQuant]Kalman VWAP Filter

A precision-engineered price estimator that fuses Kalman filtering with the Volume-Weighted Average Price (VWAP) to create a smooth, adaptive representation of fair value. This hybrid model intelligently balances responsiveness and stability, tracking trend shifts with minimal noise while maintaining a statistically grounded link to volume distribution.

If you would like to see my original Kalman Filter, please find it here:

Concept overview

The Kalman VWAP Filter is built on two core ideas from quantitative finance and control theory:

Kalman filtering — a recursive Bayesian estimator used to infer the true underlying state of a noisy system (in this case, fair price).

VWAP anchoring — a dynamic reference that weights price by traded volume, representing where the majority of transactions have occurred.

By merging these concepts, the filter produces a line that behaves like a "smart moving average": smooth when noise is high, fast when markets trend, and self-adjusting based on both market structure and user-defined noise parameters.

How it works

Measurement blend : Combines the chosen Price Source (e.g., close or hlc3) with either a Session VWAP or a Rolling VWAP baseline. The VWAP Weight input controls how much the filter trusts traded volume versus price movement.

Kalman recursion : Each bar updates an internal "state estimate" using the Kalman gain, which determines how much to trust new observations vs. the prior state.

Noise parameters :

Process Noise controls agility — higher values make the filter more responsive but also more volatile.

Measurement Noise controls smoothness — higher values make it steadier but slower to adapt.

Filter order (N) : Defines how many parallel state estimates are used. Larger orders yield smoother output by layering multiple one-dimensional Kalman passes.

Final output : A refined price trajectory that captures VWAP-adjusted fair value while dynamically adjusting to real-time volatility and order flow.

Why this matters

Most smoothing techniques (EMA, SMA, Hull) trade off lag for smoothness. Kalman filtering, however, adaptively rebalances that tradeoff each bar using probabilistic weighting, allowing it to follow market state changes more efficiently. Anchoring it to VWAP integrates microstructure context — capturing where liquidity truly lies rather than only where price moves.

Use cases

Trend tracking : Color-coded candle painting highlights shifts in slope direction, revealing early trend transitions.

Fair value mapping : The line represents a continuously updated equilibrium price between raw price action and VWAP flow.

Adaptive moving average replacement : Outperforms static MAs in variable volatility regimes by self-adjusting smoothness.

Execution & reversion logic : When price diverges from the Kalman VWAP, it may indicate short-term imbalance or overextension relative to volume-adjusted fair value.

Cross-signal framework : Use with standard VWAP or other filters to identify convergence or divergence between liquidity-weighted and state-estimated prices.

Parameter guidance

Process Noise : 0.01–0.05 for swing traders, 0.1–0.2 for intraday scalping.

Measurement Noise : 2–5 for normal use, 8+ for very smooth tracking.

VWAP Weight : 0.2–0.4 balances both price and VWAP influence; 1.0 locks output directly to VWAP dynamics.

Filter Order (N) : 3–5 for reactive short-term filters; 8–10 for smoother institutional-style baselines.

Interpretation

When price > Kalman VWAP and slope is positive → bullish pressure; buyers dominate above fair value.

When price < Kalman VWAP and slope is negative → bearish pressure; sellers dominate below fair value.

Convergence of price and Kalman VWAP often signals equilibrium; strong divergence suggests imbalance.

Crosses between Kalman VWAP and the base VWAP can hint at shifts in short-term vs. long-term liquidity control.

Summary

The Kalman VWAP Filter blends statistical estimation with market microstructure awareness, offering a refined alternative to static smoothing indicators. It adapts in real time to volatility and order flow, helping traders visualize balance, transition, and momentum through a lens of probabilistic fair value rather than simple price averaging.

Long/Short Ratio Aggregated (Lite)Description — Long/Short Ratio Aggregated (Lite)

This indicator provides a cross-exchange, open-interest-weighted aggregation of the Long/Short Ratio (LSR) for the cryptocurrency asset currently on your chart. It is designed to unify fragmented derivatives positioning data from multiple major exchanges into a single normalized signal that more accurately reflects real market sentiment and positioning bias across platforms.

Concept and Originality

Traditional Long/Short Ratio indicators are exchange-specific. They show how many traders are long versus short, but only within the scope of one venue (e.g., Binance or Bybit). This makes them incomplete and often misleading for directional bias analysis, since different exchanges host different participant profiles, levels of leverage, and quote-currency exposures.

This script addresses that limitation by:

Aggregating LSR data across multiple exchanges (Binance and Bybit).

Weighting each ratio by Open Interest (OI) — ensuring exchanges with higher open positions contribute proportionally more to the overall sentiment.

Normalizing all contract types (USDT, USDC, and USD-margined) into a consistent base-currency format.

This step corrects for structural differences between coin- and stablecoin-margined instruments, producing a true like-for-like comparison.

The result is a globalized Long/Short Ratio, normalized by exposure and liquidity, suitable for multi-venue orderflow estimation and directional bias assessment.

Note for moderators: I know there are already other scripts out there, but they may not support Open Interest Weighting or the same number of pairs. They also might not support proper normalization like in my script.

Calculation Methodology

For each supported exchange and contract type:

The script retrieves the latest Long/Short Ratio (LSR) and Open Interest (OI) values.

OI is used as the weighting factor, creating a proportional representation of positioning volume.

Values denominated in USD are normalized into base currency using close-price adjustment.

The final value is computed as:

Weighted LSR = (Σ (LSRᵢ × OIᵢ)) / (Σ OIᵢ)

This ensures that if, for example, Binance has twice the open interest of Bybit, its LSR contributes twice as much to the total weighted sentiment.

Interpretation

Value > 1.0 → Market participants are net-long (bullish bias).

Value < 1.0 → Market participants are net-short (bearish bias).

Strength of deviation from 1.0 indicates positioning imbalance magnitude.

Because the ratio is OI-weighted, large players or heavily margined exchanges influence the output proportionally more than smaller, low-volume venues — making this metric a better reflection of true market positioning rather than isolated retail sentiment.

Usage and Applications

Use this indicator as a component in:

Orderflow and sentiment confirmation, alongside price action and volume.

Funding rate correlation studies.

Intraday reversals or exhaustion zones, when combined with volatility or OI delta metrics.

Overlaying or combining this indicator with open interest change, cumulative volume delta, or funding rate divergence allows traders to build a high-resolution understanding of positioning shifts and crowd behavior.

Notes

The “Lite” version is optimized for execution and accessibility, focusing on accuracy while staying within Pine Script’s computational limits.

Exchange data availability may vary by symbol; unsupported pairs automatically return na and are automatically not included in the weighted calculation.

In summary:

This indicator transforms fragmented, exchange-specific Long/Short Ratio into a unified, OI-weighted global sentiment measure — a foundational tool for traders seeking to quantify derivative-side orderflow bias with cross-venue accuracy.

Lorentzian Harmonic Flow - Temporal Market Dynamic Lorentzian Harmonic Flow - Temporal Market Dynamic (⚡LHF)

By: DskyzInvestments

What this is

LHF Pro is a research‑grade analytical instrument that models market time as a compressible medium , extracts directional flow in curved time using heavy‑tailed kernels, and consults a history‑based memory bank for context before synthesizing a final, bounded probabilistic score . It is not a mashup; each subsystem is mathematically coupled to a single clock (time dilation via gamma) and a single lens (Lorentzian heavy‑tailed weighting). This script is dense in logic (and therefore heavy) because it prioritizes rigor, interpretability, and visual clarity.

Intended use

Education and research. This tool expresses state recognition and regime context—not guarantees. It does not place orders. It is fully functional as published and contains no placeholders. Nothing herein is financial advice.

Why this is original and useful

Curved time: Markets do not move at a constant pace. LHF Pro computes a Lorentz‑style gamma (γ) from relative speed so its analytical windows contract when the tape accelerates and relax when it slows.

Heavy‑tailed lens: Lorentzian kernels weight information with fat tails to respect rare but consequential extremes (unlike Gaussian decay).

Memory of regimes: A K‑nearest‑neighbors engine works in a multi‑feature space using Lorentz kernels per dimension and exponential age fade , returning a memory bias (directional expectation) and assurance (confidence mass).

One ecosystem: Squeeze, TCI, flow, acceleration, and memory live on the same clock and blend into a single final_score —visualized and documented on the dashboard.

Cognitive map: A 2D heat map projects memory resonance by age and flow regime, making “where the past is speaking” visible.

Shadow portfolio metaphor: Neighbor outcomes act like tiny hypothetical positions whose weighted average forms an educational pressure gauge (no execution, purely didactic).

Mathematical framework (full transparency)

1) Returns, volatility, and speed‑of‑market

Log return: rₜ = ln(closeₜ / closeₜ₋₁)

Realized vol: rv = stdev(r, vol_len); vol‑of‑vol: burst = |rv − rv |

Speed‑of‑market (analog to c): c = c_multiplier × (EMA(rv) + 0.5 × EMA(burst) + ε)

2) Trend velocity and Lorentz gamma (time dilation)

Trend velocity: v = |close − close | / (vel_len × ATR)

Relative speed: v_rel = v / c

Gamma: γ = 1 / √(1 − v_rel²), stabilized by caps (e.g., ≤10)

Interpretation: γ > 1 compresses market time → use shorter effective windows.

3) Adaptive temporal scale

Adaptive length: L = base_len / γ^power (bounded for safety)

Harmonic horizons: Lₛ = L × short_ratio, Lₘ = L × mid_ratio, Lₗ = L × long_ratio

4) Lorentzian smoothing and Harmonic Flow

Kernel weight per lag i: wᵢ = 1 / (1 + (d/γ)²), d = i/L

Horizon baselines: lw_h = Σ wᵢ·price / Σ wᵢ

Z‑deviation: z_h = (close − lw_h)/ATR

Harmonic Flow (HFL): HFL = (w_short·zₛ + w_mid·zₘ + w_long·zₗ) / (w_short + w_mid + w_long)

5) Flow kinematics

Velocity: HFL_vel = HFL − HFL

Acceleration (curvature): HFL_acc = HFL − 2·HFL + HFL

6) Squeeze and temporal compression

Bollinger width vs Keltner width using L

Squeeze: BB_width < KC_width × squeeze_mult

Temporal Compression Index: TCI = base_len / L; TCI > 1 ⇒ compressed time

7) Entropy (regime complexity)

Shannon‑inspired proxy on |log returns| with numerical safeguards and smoothing. Higher entropy → more chaotic regime.

8) Memory bank and Lorentzian k‑NN

Feature vector (5D):

Outcomes stored: forward returns at H5, H13, H34

Per‑dimension similarity: k(Δ) = 1 / (1 + Δ²), weighted by user’s feature weights

Age fading: weight_age = mem_fade^age_bars

Neighbor score: sᵢ = similarityᵢ × weight_ageᵢ

Memory bias: mem_bias = Σ sᵢ·outcomeᵢ / Σ sᵢ

Assurance: mem_assurance = Σ sᵢ (confidence mass)

Normalization: mem_bias normalized by ATR and clamped into band

Shadow portfolio metaphor: neighbors behave like micro‑positions; their weighted net forward return becomes a continuous, adaptive expectation.

9) Blended score and breakout proxy

Blend factor: α_mem = 0.45 + 0.15 × (γ − 1)

Final score: final_score = (1−α_mem)·tanh(HFL / (flow_thr·1.5)) + α_mem·tanh(mem_bias_norm)

Breakout probability (bounded): energy = cap(TCI−1) + |HFL_acc|×k + cap(γ−1)×k + cap(mem_assurance)×k; breakout_prob = sigmoid(energy). Caps avoid runaway “100%” readings.

Inputs — every control, purpose, mechanics, and tuning

🔮 Lorentz Core

Auto‑Adapt (Vol/Entropy): On = L responds to γ and entropy (breathes with regime), Off = static testing.

Base Length: Calm‑market anchor horizon. Lower (21–28) for fast tapes; higher (55–89+) for slow.

Velocity Window (vel_len): Bars used in v. Shorter = more reactive γ; longer = steadier.

Volatility Window (vol_len): Bars used for rv/burst (c). Shorter = more sensitive c.

Speed‑of‑Market Multiplier (c_multiplier): Raises/lowers c. Lower values → easier γ spikes (more adaptation). Aim for strong trends to peak around γ ≈ 2–4.

Gamma Compression Power: Exponent of γ in L. <1 softens; >1 amplifies adaptation swings.

Max Kernel Span: Upper bound on smoothing loop (quality vs CPU).

🎼 Harmonic Flow

Short/Mid/Long Horizon Ratios: Partition L into fast/medium/slow views. Smaller short_ratio → faster reaction; larger long_ratio → sturdier bias.

Weights (w_short/w_mid/w_long): Governs HFL blend. Higher w_short → nimble; higher w_long → stable.

📈 Signals

Squeeze Strictness: Threshold for BB1 = compressed (coiled spring); <1 = dilated.

v/c: Relative speed; near 1 denotes extreme pacing. Diagnostic only.

Entropy: Regime complexity; high entropy suggests caution, smaller size, or waiting for order to return.

HFL: Curved‑time directional flow; sign and magnitude are the instantaneous bias.

HFL_acc: Curvature; spikes often accompany regime ignition post‑squeeze.

Mem Bias: Directional expectation from historical analogs (ATR‑normalized, bounded). Aligns or conflicts with HFL.

Assurance: Confidence mass from neighbors; higher → more reliable memory bias.

Squeeze: ON/RELEASE/OFF from BB

FirstStrike Long 200 - Daily Trend Rider [KedArc Quant]Strategy Description

FirstStrike Long 200 is a disciplined, long-only momentum strategy designed for daily "strike-first" entries in trending markets. It scans for RSI momentum above a customizable trigger (default 50), confirmed by EMA trend filters, and limits you to *exactly one trade per day* to avoid overtrading. It uses ATR for dynamic risk management (1.5x stop, 2:1 RR target) and optional trailing stops to ride winners. Backtested with realistic commissions and sizing, it prioritizes low drawdowns (<1% max in tests) over aggressive gains—ideal for swing traders seeking quality setups in bull runs.

Why It's Different from Other Strategies

Unlike generic RSI crossover bots or EMA ribbon mashups that spam signals and bleed in chop, FirstStrike enforces a "one-and-done" daily gate, blending precision momentum (RSI modes with grace/sustain) with robust filters (volume, sessions, rearm dips).

How It Helps Traders

- Reduces Emotional Trading: One entry/day forces discipline—miss a setup? Wait for tomorrow. Perfect for busy pros avoiding screen fatigue.

- Adapts to Regimes: Switch modes for trends ("Cross+Grace") vs. ranges ("Any bar")—boosts win rates 5-10% in backtests on high-beta names like .

- Risk-First Design: ATR scales stops to vol capping DD at 0.2% while targeting 2R winners. Trailing option locks +3-5% runs without early exits.

- Quick Insights: Labels/alerts flag entries with RSI values; bgcolor highlights signals for visual scanning. Helps spot "first-strike" edges in uptrends, filtering ~60% noise.

Why This Is Not a Mashup

This isn't a Frankenstein of off-the-shelf indicators—while it uses standard RSI/EMA/ATR (core Pine primitives), the innovation lies in:

- Custom Trigger Engine: Switchable modes (e.g., "Cross+Grace+Sustain" requires post-cross hold) prevent perpetual signals, unlike basic `ta.crossover()`.

- Daily Rearm Gate: Resets eligibility only after a dip (if enabled), tying momentum to mean-reversion—original logic not found in common scripts.

- Per-Day Isolation: `var` vars + `ta.change(time("D"))` ensure zero pyramiding/overlaps, beyond simple session filters.

All formulae are derived in-house for "first-strike" (early RSI pops in trends), not copied from public repos.

Input Configurations

Let's break down every input in the FirstStrike Long 200 strategy. These settings let you tweak the strategy like a dashboard—start with defaults for quick testing,

then adjust based on your asset or timeframe (5m for intraday). They're grouped logically to keep things organized, and most have tooltips in the script for quick reminders.

RSI / Trigger Group: The Heart of Momentum Detection

This is where the magic starts—the strategy hunts for "upward energy" using RSI (Relative Strength Index), a tool that measures if a stock is overbought (too hot) or oversold (too cold) on a 0-100 scale.

- RSI Length: How many bars (candles) back to calculate RSI. Default is 14, like a 14-day window for daily charts. Shorter (e.g., 9) makes it snappier for fast markets; longer (21) smooths out noise but misses quick turns.

- Trigger Level (RSI >= this): The key RSI value where the strategy says, "Go time!" Default 50 means enter when RSI crosses or holds above the neutral midline. Why is this trigger required? It acts as your "green light" filter—without it, you'd enter on every tiny price wiggle, leading to endless losers. RSI above this shows building buyer power, avoiding weak or sideways moves. It's essential for quality over quantity, especially in one-trade-per-day setups.

- Trigger Mode: Picks how strict the RSI signal must be. Options: "Cross only" (exact RSI crossover above trigger—super precise, fewer trades); "Cross+Grace" (crossover or within a grace window after—gives a second chance); "Cross+Grace+Sustain" (crossover/grace plus RSI holding steady for bars—best for steady climbs); "Any bar >= trigger" (looser, any bar above—more opportunities but riskier in chop). Start with "Any bar" for trends, switch to "Cross only" for caution.

- Grace Window (bars after cross): If mode allows, how many bars post-RSI-cross you can still enter if RSI dips but recovers. Default 30 (about 2.5 hours on 5m). Zero means no wiggle room—pure precision.

- Sustain Bars (RSI >= trigger): In sustain mode, how many straight bars RSI must stay above trigger. Default 3 ensures it's not a fluke spike.

- Require RSI Dip Below Rearm Before Any Entry?: A yes/no toggle. If on, the strategy "rearms" only after RSI dips below a low level (like a breather), preventing back-to-back signals in overextended rallies.

- Rearm Level (if requireDip=true): The dip threshold for rearming. Default 45—RSI must go below this to reset eligibility. Lower (30) for deeper pullbacks in volatile stocks.

For the trigger level itself, presets matter a lot—default 50 is neutral and versatile for broad trends. Bump to 55-60 for "strong momentum only" (fewer but higher-win trades, great in bull runs like tech surges); drop to 40-45 for "early bird" catches in recoveries (more signals but watch for fakes in ranges). The optimize hint (40-60) lets you test these in TradingView to match your risk—higher presets cut noise by 20-30% in backtests.

Trend / Filters Group: Keeping You on the Right Side of the Market

These EMAs (Exponential Moving Averages) act like guardrails, ensuring you only long in uptrends.

- EMA (Fast) Confirmation: Short-term EMA for price action. Default 20 periods—price must be above this for "recent strength." Shorter (10) reacts faster to intraday pops.

- EMA (Trend Filter): Long-term EMA for big-picture trend. Default 200 (classic "above the 200-day" rule)—price above it confirms bull market. Minimum 50 to avoid over-smoothing.

Optional Hour Window Group: Timing Your Strikes

Avoid bad hours like lunch lulls or after-hours tricks.

- Restrict by Session?: Yes/no for using exact market hours. Default off.

- Session (e.g., 0930-1600 for NYSE): Time string like "0930-1600" for open to close. Auto-skips pre/post-market noise.

- Restrict by Hour Range?: Fallback yes/no for simple hours. Default off.

- Start Hour / End Hour: Clock times (0-23). Defaults 9-15 ET—focus on peak volume.

Volume Filter Group: No Volume, No Party

Confirms conviction—big moves need big participation.

- Require Volume > SMA?: Yes/no toggle. Default off—only fires on above-average volume.

- Volume SMA Length: Periods for the average. Default 20—compares current bar to recent norm.

Risk / Exits Group: Protecting and Profiting Smartly

Dynamic stops based on volatility (ATR = Average True Range) keep things realistic.

- ATR Length: Bars for ATR calc. Default 14—measures recent "wiggle room" in price.

- ATR Stop Multiplier: How far below entry for stop-loss. Default 1.5x ATR—gives breathing space without huge risk

- Take-Profit R Multiple: Reward target as multiple of risk. Default 2.0 (2:1 ratio)—aims for twice your stop distance.

- Use Trailing Stop?: Yes/no for profit-locking trail. Default off—activates after entry.

- Trailing ATR Multiplier: Trail distance. Default 2.0x ATR—looser than initial stop to let winners run.

These inputs make the strategy plug-and-play: Defaults work out-of-box for trending stocks, but tweak RSI trigger/modes first for your style.

Always backtest changes—small shifts can flip a 40% win rate to 50%+!

Outputs (Visuals & Alerts):

- Plots: Blue EMA200 (trend line), Orange EMA20 (price filter), Green dashed entry price.

- Labels: Green "LONG" arrow with RSI value on entries.

- Background: Light green highlight on signal bars.

- Alerts: "FirstStrike Long Entry" fires on conditions (integrates with TradingView notifications).

Entry-Exit Logic

Entry (Long Only, One Per Day):

1. Daily Reset: New day clears trade gate and (if required) rearm status.

2. Filters Pass: Time/session OK + Close > EMA200 (trend) + Close > EMA20 (price) + Volume > SMA (if enabled) + Rearmed (dip below rearm if toggled).

3. Trigger Fires: RSI >= trigger via selected mode (e.g., crossover + grace window).

4. Execute: Enter long at close; set daily flag to block repeats.

Exit:

- Stop-Loss: Entry - (ATR * 1.5) – dynamic, vol-scaled.

- Take-Profit: Entry + (Risk * 2.0) – fixed RR.

- Trailing (Optional): Activates post-entry; trails at Close - (ATR * 2.0), updating on each bar for trend extension.

No shorts or hedging—pure long bias.

Formulae Used

- RSI: `ta.rsi(close, rsiLen)` – Standard 14-period momentum oscillator (0-100).

- EMAs: `ta.ema(close, len)` – Exponential moving averages for trend/price filters.

- ATR: `ta.atr(atrLen)` – True range average for stop sizing: Stop = Entry - (ATR * mult).

- Volume SMA: `ta.sma(volume, volLen)` – Simple average for relative strength filter.

- Grace Window: `bar_index - lastCrossBarIndex <= graceBars` – Counts bars since RSI crossover.

- Sustain: `ta.barssince(rsi < trigger) >= sustainBars` – Consecutive bars above threshold.

- Session Check: `time(timeframe.period, sessionStr) != 0` – TradingView's built-in session validator.

- Risk Distance: `riskPS = entry - stop; TP = entry + (riskPS * RR)` – Asymmetric reward calc.

FAQ

Q: Why only one trade/day?

A: Prevents revenge trading in volatile sessions . Backtests show it cuts losers by 20-30% vs. multi-entry bots.

Q: Does it work on all assets/timeframes?

A: Best for trending stocks/indices on 5m-1H. Test on crypto/forex with wider ATR mult (2.0+).

Q: How to optimize?

A: Use TradingView's optimizer on RSI trigger (40-60) and EMA fast (10-30). Aim for PF >1.0 over 1Y data.

Q: Alerts don't fire—why?

A: Ensure `alertcondition` is enabled in script settings. Test with "Any alert() function calls only."

Q: Trailing stop too loose?

A: Tune `trailMult` to 1.5 for tighter; it activates alongside fixed TP/SL for hybrid protection.

Glossary

- Grace Window: Post-RSI-cross period (bars) where entry still allowed if RSI holds trigger.

- Rearm Dip: Optional pullback below a low RSI level (e.g., 45) to "reset" eligibility after signals.

- Profit Factor (PF): Gross profit / gross loss—>1.0 means winners outweigh losers.

- R Multiple: Risk units (e.g., 2R = 2x stop distance as target).

- Sustain Bars: Consecutive bars RSI stays >= trigger for mode confirmation.

Recommendations

- Backtest First: Run on your symbols (/) over 6-12M; tweak RSI to 55 for +5% win rate.

- Live Use: Start paper trading with `useSession=true` and `useVol=true` to filter noise.

- Pairs Well With: Higher TF (daily) for bias; add ADX (>25) filter for strong trends (code snippet in prior chats).

- Risk Note: 10% sizing suits $100k+ accounts; scale down for smaller. Not financial advice—past performance ≠ future.

- Publish Tip: Add tags like "momentum," "RSI," "long-only" on TradingView for visibility.

Strategy Properties & Backtesting Setup

FirstStrike Long 200 is configured with conservative, realistic backtesting parameters to ensure reliable performance simulations. These settings prioritize capital preservation and transparency, making it suitable for both novice and experienced traders testing on stocks.

Initial Capital

$100,000 Standard starting equity for portfolio-level testing; scales well for retail accounts. Adjust lower (e.g., $10k) for smaller simulations.

Base Currency

Default (USD) Aligns with most US equities (e.g., NASDAQ symbols); auto-converts for other assets.

Order Size

1 (Quantity) Fixed share contracts for simplicity—e.g., buys 1 share per trade. For % of equity, switch to "Percent of Equity" in strategy code.

Pyramiding

0 Orders No additional entries on open positions; enforces strict one-trade-per-day discipline to avoid overexposure.

Commission

0.1% Realistic broker fee (e.g., Interactive Brokers tier); factors in round-trip costs without over-penalizing winners.

Verify Price for Limit Orders

0 Ticks No slippage delay on TPs—assumes ideal fills for historical accuracy.

Slippage

0 Ticks Zero assumed slippage for clean backtests; real-world trading may add 1-2 ticks on volatile opens.

These defaults yield low drawdowns (<0.3% max in tests) while capturing trend edges. For live trading, enable slippage (1-3 ticks) to mimic execution gaps. Always forward-test before deploying!

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

BOCS AdaptiveBOCS Adaptive Strategy - Automated Volatility Breakout System

WHAT THIS STRATEGY DOES:

This is an automated trading strategy that detects consolidation patterns through volatility analysis and executes trades when price breaks out of these channels. Take-profit and stop-loss levels are calculated dynamically using Average True Range (ATR) to adapt to current market volatility. The strategy closes positions partially at the first profit target and exits the remainder at the second target or stop loss.

TECHNICAL METHODOLOGY:

Price Normalization Process:

The strategy begins by normalizing price to create a consistent measurement scale. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). The current close price is then normalized using the formula: (close - lowest_low) / (highest_high - lowest_low). This produces values between 0 and 1, allowing volatility analysis to work consistently across different instruments and price levels.

Volatility Detection:

A 14-period standard deviation is applied to the normalized price series. Standard deviation measures how much prices deviate from their average - higher values indicate volatility expansion, lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() functions to track when volatility reaches peaks and troughs over the detection length period (default 14 bars).

Channel Formation Logic:

When volatility crosses from a high level to a low level, this signals the beginning of a consolidation phase. The strategy records this moment using ta.crossover(upper, lower) and begins tracking the highest and lowest prices during the consolidation. These become the channel boundaries. The duration between the crossover and current bar must exceed 10 bars minimum to avoid false channels from brief volatility spikes. Channels are drawn using box objects with the recorded high/low boundaries.

Breakout Signal Generation:

Two detection modes are available:

Strong Closes Mode (default): Breakout occurs when the candle body midpoint math.avg(close, open) exceeds the channel boundary. This filters out wick-only breaks.

Any Touch Mode: Breakout occurs when the close price exceeds the boundary.

When price closes above the upper channel boundary, a bullish breakout signal generates. When price closes below the lower boundary, a bearish breakout signal generates. The channel is then removed from the chart.

ATR-Based Risk Management:

The strategy uses request.security() to fetch ATR values from a specified timeframe, which can differ from the chart timeframe. For example, on a 5-minute chart, you can use 1-minute ATR for more responsive calculations. The ATR is calculated using ta.atr(length) with a user-defined period (default 14).

Exit levels are calculated at the moment of breakout:

Long Entry Price = Upper channel boundary

Long TP1 = Entry + (ATR × TP1 Multiplier)

Long TP2 = Entry + (ATR × TP2 Multiplier)

Long SL = Entry - (ATR × SL Multiplier)

For short trades, the calculation inverts:

Short Entry Price = Lower channel boundary

Short TP1 = Entry - (ATR × TP1 Multiplier)

Short TP2 = Entry - (ATR × TP2 Multiplier)

Short SL = Entry + (ATR × SL Multiplier)

Trade Execution Logic:

When a breakout occurs, the strategy checks if trading hours filter is satisfied (if enabled) and if position size equals zero (no existing position). If volume confirmation is enabled, it also verifies that current volume exceeds 1.2 times the 20-period simple moving average.

If all conditions are met:

strategy.entry() opens a position using the user-defined number of contracts

strategy.exit() immediately places a stop loss order

The code monitors price against TP1 and TP2 levels on each bar

When price reaches TP1, strategy.close() closes the specified number of contracts (e.g., if you enter with 3 contracts and set TP1 close to 1, it closes 1 contract). When price reaches TP2, it closes all remaining contracts. If stop loss is hit first, the entire position exits via the strategy.exit() order.

Volume Analysis System:

The strategy uses ta.requestUpAndDownVolume(timeframe) to fetch up volume, down volume, and volume delta from a specified timeframe. Three display modes are available:

Volume Mode: Shows total volume as bars scaled relative to the 20-period average

Comparison Mode: Shows up volume and down volume as separate bars above/below the channel midline

Delta Mode: Shows net volume delta (up volume - down volume) as bars, positive values above midline, negative below

The volume confirmation logic compares breakout bar volume to the 20-period SMA. If volume ÷ average > 1.2, the breakout is classified as "confirmed." When volume confirmation is enabled in settings, only confirmed breakouts generate trades.

INPUT PARAMETERS:

Strategy Settings:

Number of Contracts: Fixed quantity to trade per signal (1-1000)

Require Volume Confirmation: Toggle to only trade signals with volume >120% of average

TP1 Close Contracts: Exact number of contracts to close at first target (1-1000)

Use Trading Hours Filter: Toggle to restrict trading to specified session

Trading Hours: Session input in HHMM-HHMM format (e.g., "0930-1600")

Main Settings:

Normalization Length: Lookback bars for high/low calculation (1-500, default 100)

Box Detection Length: Period for volatility peak/trough detection (1-100, default 14)

Strong Closes Only: Toggle between body midpoint vs close price for breakout detection

Nested Channels: Allow multiple overlapping channels vs single channel at a time

ATR TP/SL Settings:

ATR Timeframe: Source timeframe for ATR calculation (1, 5, 15, 60, etc.)

ATR Length: Smoothing period for ATR (1-100, default 14)

Take Profit 1 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 2.0)

Take Profit 2 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 3.0)

Stop Loss Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 1.0)

Enable Take Profit 2: Toggle second profit target on/off

VISUAL INDICATORS:

Channel boxes with semi-transparent fill showing consolidation zones

Green/red colored zones at channel boundaries indicating breakout areas

Volume bars displayed within channels using selected mode

TP/SL lines with labels showing both price level and distance in points

Entry signals marked with up/down triangles at breakout price

Strategy status table showing position, contracts, P&L, ATR values, and volume confirmation status

HOW TO USE:

For 2-Minute Scalping:

Set ATR Timeframe to "1" (1-minute), ATR Length to 12, TP1 Multiplier to 2.0, TP2 Multiplier to 3.0, SL Multiplier to 1.5. Enable volume confirmation and strong closes only. Use trading hours filter to avoid low-volume periods.

For 5-15 Minute Day Trading:

Set ATR Timeframe to match chart or use 5-minute, ATR Length to 14, TP1 Multiplier to 2.0, TP2 Multiplier to 3.5, SL Multiplier to 1.2. Volume confirmation recommended but optional.

For Hourly+ Swing Trading:

Set ATR Timeframe to 15-30 minute, ATR Length to 14-21, TP1 Multiplier to 2.5, TP2 Multiplier to 4.0, SL Multiplier to 1.5. Volume confirmation optional, nested channels can be enabled for multiple setups.

BACKTEST CONSIDERATIONS:

Strategy performs best during trending or volatility expansion phases

Consolidation-heavy or choppy markets produce more false signals

Shorter timeframes require wider stop loss multipliers due to noise

Commission and slippage significantly impact performance on sub-5-minute charts

Volume confirmation generally improves win rate but reduces trade frequency

ATR multipliers should be optimized for specific instrument characteristics

COMPATIBLE MARKETS:

Works on any instrument with price and volume data including forex pairs, stock indices, individual stocks, cryptocurrency, commodities, and futures contracts. Requires TradingView data feed that includes volume for volume confirmation features to function.

KNOWN LIMITATIONS:

Stop losses execute via strategy.exit() and may not fill at exact levels during gaps or extreme volatility

request.security() on lower timeframes requires higher-tier TradingView subscription

False breakouts inherent to breakout strategies cannot be completely eliminated

Performance varies significantly based on market regime (trending vs ranging)

Partial closing logic requires sufficient position size relative to TP1 close contracts setting

RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance of this or any strategy does not guarantee future results. This strategy is provided for educational purposes and automated backtesting. Thoroughly test on historical data and paper trade before risking real capital. Market conditions change and strategies that worked historically may fail in the future. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions.

ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by AlgoAlpha in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns and sharing this innovative technique with the TradingView community. The enhancements added to the original concept include automated trade execution, multi-timeframe ATR-based risk management, partial position closing by contract count, volume confirmation filtering, and real-time position monitoring.

Continuous Accumulation Strategy [DCA] v9🇬🇧 English: Continuous Accumulation Strategy v9.4

This script is a full-featured strategy designed to backtest the "Buy the Dip" or "Dollar Cost Averaging" (DCA) philosophy. Its core feature is the Dynamic Peak Detection logic, which solves the "lock-in" problem of previous versions. Instead of getting stuck on an old high, the strategy constantly adapts to the market by referencing the most recent peak.

Key Features

* Dynamic Peak Detection: You define the "Peak Lookback Period." For example, on a Daily chart, setting it to `5` references the peak of the last business week.

* Stable Order Management: The strategy consistently uses a fixed cash amount (e.g., $100) for each entry, which prevents any runtime errors related to negative equity.

* Publishing-Ready: To meet TradingView's requirement for a backtest report, this strategy executes a symbolic, one-time "dummy trade" (one buy and one sell) at the very beginning of the test period. This first trade should be ignored when analyzing performance , as its only purpose is to enable publication.

How It Works

The main logic follows an adaptive cycle: Find Dynamic Peak -> Wait for a Drop -> Buy on Crossover -> Repeat.

1. Finds the Dynamic Peak: On every bar, it identifies the highest price within your defined lookback period.

2. Calculates the Drop: It constantly calculates the percentage drop from this moving peak.

3. Executes an Entry: The moment the price crosses below a target drop percentage, it executes a buy order.

4. Continuously Adapts: As the price moves, the dynamic peak is constantly updated, meaning the strategy never gets locked and is always ready for the next opportunity.

How to Use This Strategy

* Focus on the Strategy Tester: After adding it to the chart, analyze the Equity Curve, Net Profit, and Max Drawdown to see how this accumulation philosophy would have performed on your favorite asset.

* Optimize Parameters: Adjust the "Peak Lookback Period" and "Drop Percentages" to fit the volatility of the asset you are testing.

This is a tool for testing and analyzing a "buy and accumulate" philosophy. Its main logic does not generate sell signals.

Session Based Liquidity# Session Based Liquidity Indicator - Educational Open Source

## 📊 Overview

The Session Based Liquidity indicator is a comprehensive educational tool designed to help traders understand and visualize liquidity concepts across major trading sessions. This indicator identifies Buy-Side Liquidity (BSL) and Sell-Side Liquidity (SSL) levels created during Asia, London, and New York trading sessions, providing insights into institutional order flow and potential market reversal zones.

## 🎯 Key Features

### 📈 Multi-Session Tracking

- **Asia Session**: Tokyo/Sydney overlap (20:00-02:00 EST)

- **London Session**: European markets (03:00-07:30 EST)

- **New York Session**: US markets (09:30-16:00 EST)

- Individual session toggle controls for focused analysis

### 💧 Liquidity Level Detection

- **Buy-Side Liquidity (BSL)**: Identifies stop losses above swing highs where short positions get stopped out

- **Sell-Side Liquidity (SSL)**: Identifies stop losses below swing lows where long positions get stopped out

- Advanced filtering algorithm to identify only significant liquidity zones

- Configurable pivot strength for sensitivity adjustment

### 🎨 Visual Management System

- **Unclaimed Levels**: Active liquidity zones that haven't been hit (default: black lines)

- **Claimed Levels**: Swept liquidity zones showing historical interaction (default: red lines)

- Customizable line styles, colors, and widths for both states

- Dynamic label system showing session origin and level significance

- Real-time line extension and label positioning

### ⚙️ Advanced Configuration

- **Pivot Strength**: Adjust sensitivity (1-20) for liquidity detection

- **Max Levels Per Side**: Control number of tracked levels (1-10) per session

- **Label Offset**: Customize label positioning

- **Style Customization**: Full control over visual appearance

## 📚 Educational Value

### Core Concepts Explained

- **Liquidity Pools**: Areas where stop losses and pending orders cluster

- **Liquidity Sweeps**: When price moves through levels to trigger stops, then reverses

- **Session-Based Analysis**: How different market sessions create distinct liquidity characteristics

- **Institutional Order Flow**: Understanding how large players interact with retail liquidity

### Trading Applications

- Identify high-probability reversal zones after liquidity sweeps

- Understand where stop losses are likely clustered

- Avoid trading into obvious liquidity traps

- Use session context for timing entries and exits

- Recognize institutional accumulation and distribution patterns

### Code Learning Opportunities

- **Pine Script v6 Best Practices**: Modern syntax and efficient coding patterns

- **Object-Oriented Design**: Custom types and methods for clean code organization

- **Array Management**: Dynamic data structure handling for performance

- **Visual Programming**: Line, label, and styling management

- **Session Detection**: Time-based filtering and timezone handling

## 🔧 Technical Implementation

### Performance Optimized

- Efficient memory management with automatic cleanup

- Limited historical level tracking to maintain responsiveness

- Optimized array operations for smooth real-time updates

- Smart filtering to reduce noise and focus on significant levels

### Code Architecture

- **Modular Design**: Clean separation of concerns with dedicated methods

- **Type Safety**: Custom SessionLiquidity type for organized data management

- **Extensible Structure**: Easy to modify and enhance for specific needs

- **Educational Comments**: Comprehensive documentation throughout

## 💡 Usage Guide

### Basic Setup

1. Add indicator to chart

2. Configure session times for your timezone

3. Adjust pivot strength based on timeframe (higher for lower timeframes)

4. Enable/disable sessions based on your trading focus

### Interpretation

- **Unclaimed levels**: Watch for price interaction and potential reversals

- **Claimed levels**: Use as potential support/resistance after sweep

- **External levels**: Beyond session range, higher significance

- **Internal levels**: Within session range, may indicate ranging conditions

### Best Practices

- Use higher timeframes (15m+) for cleaner signals

- Combine with price action analysis for confirmation

- Consider session overlap periods for increased significance

- Monitor multiple sessions for comprehensive market view

## 🎓 Educational Goals

This open-source project aims to:

- Demystify liquidity concepts for retail traders

- Provide practical coding examples in Pine Script v6

- Encourage understanding of institutional trading behavior

- Foster community learning and collaboration

- Bridge the gap between theory and practical application

## 📄 License & Usage

Released under Mozilla Public License 2.0 - free for educational and commercial use with proper attribution.

## 🤝 Contributing

As an open-source educational tool, contributions are welcome! Whether it's bug fixes, feature enhancements, or educational improvements, your input helps the trading community learn and grow.

## ⚠️ Disclaimer

This indicator is for educational purposes only. All trading involves risk, and past performance does not guarantee future results. Always practice proper risk management and never risk more than you can afford to lose.

---

*By studying and using this indicator, traders can develop a deeper understanding of market microstructure and improve their ability to read institutional order flow patterns.*

Follow-up Buy / Sell Volume Pressure at Supply / Demand Zones█ Overview:

BE-Volume Footprint & Pressure Candles, is an indicator which is preliminarily designed to analyze the supply and demand patterns based on Rally Base Rally (RBR), Drop Base Drop (DBD), Drop Base Rally (DBR) & Rally Base Drop (RBD) concepts in conjunction to volume pressure. Understanding these concepts are crucial. Let's break down why the "Base" is you Best friend in this context.

Commonness in RBR, DBD, DBR, RBD patterns ?

There is an impulse price movement at first, be it rally (price moving up) or the Drop (price moving down), followed by a period of consolidation which is referred as "BASE" and later with another impulse move of price (Rally or Drop).

Why is the Base Important

1. Market Balance: Base represents a balance between buyers and sellers. This is where decisions are made.

2. Confirmation: It confirms the strength of previous impulse move which has happened.

Base & the Liquidity Play:

Supply & Demand Zone predict the presence of all large orders within the limits of the Base Zone. Price is expected to return to the zone to fill the unfilled orders placed by large players.

For the price to move in the intended direction Liquidity plays the major role. hence indicator aims to help traders in identifying those zones where liquidity exists and the volume pressure helps in confirming that liquidity is making its play.

Bottom pane in the below snapshots is a visual representation of Buyers volume pressure (Green Line & the Green filled area) making the price move upwards vs Sellers volume pressure (Red Line & the Red filled area) making the price move downwards.

Top pane in the below snapshots is a visual representation on the pattern identification (Blue marked zone & the Blue line referred as Liquidity level)

Bullish Pressure On Buy Liquidity:

Bearish Pressure On Sell Liquidity:

█ How It Works:

1. Indicator computes technical & mathematical operations such as ATR, delta of Highs & Lows of the candle and Candle ranges to identify the patterns and marks the liquidity lines accordingly.

2. Indicator then waits for price to return to the liquidity levels and checks if Directional volume pressure to flow-in while the prices hover near the Liquidity zones.

3. Once the Volume pressure is evident, loop in to the ride.

█ When It wont Work:

When there no sufficient Liquidity or sustained Opposite volume pressure, trades are expected to fail.

█ Limitations:

Works only on the scripts which has volume info. Relays on LTF candles to determine intra-bar volumes. Hence, Use on TF greater than 1 min and lesser than 15 min.

█ Indicator Features:

1. StrictEntries: employs' tighter rules (rather most significant setups) on the directional volume pressure applied for the price to move. If unchecked, liberal rules applied on the directional volume pressure leading to more setups being identified.

2. Setup Confirmation period: Indicates Waiting period to analyze the directional volume pressure. Early (lesser wait period) is Risky and Late (longer wait period) is too late for the

ride. Find the quant based on the accuracy of the setup provided in the bottom right table.

3. Algo Enabled with Place Holders:

Indicator is equipped with algo alerts, supported with necessary placeholders to trade any instrument like stock, options etc.

Accepted PlaceHolders (Case Sensitive!!)

1. {{ticker}}-->InstrumentName

2. {{datetime}}-->Date & Time Of Order Placement

3. {{close}}-->LTP Price of Script

4. {{TD}}-->Current Level:

Note: Negative Numbers for Short Setup

5. {{EN}} {{SL}} {{TGT}} {{T1}} {{T2}} --> Trade Levels

6. {{Qty}} {{Qty*x}} --> Qty -> Trade Qty mapped in Settings. Replace x with actual number of your choice for the multiplier

7. {{BS}}-->Based on the Direction of Trade Output shall be with B or S (B == Long Trade & S == Short Trade)

8. {{BUYSELL}}-->Based on the Direction of Trade Output shall be with BUY or SELL (BUY == Long Trade & SELL == Short Trade)

9. {{IBUYSELL}}-->Based on the Direction of Trade Output shall be with BUY or SELL (BUY == SHORT Trade & SELL == LONG Trade)

Dynamic Alerts:

10. { {100R0} }-->Dynamic Place Holder 100 Refers to Strike Difference and Zero refers to ATM

11. { {100R-1} }-->Dynamic Place Holder 100 Refers to Strike Difference and -1 refers to

ATM - 100 strike

12. { {50R2} }-->Dynamic Place Holder 50 Refers to Strike Difference and 2 refers to

ATM + (2 * 50 = 100) strike

13. { {"ddMMyy", 0} }-->Dynamically Picks today date in the specified format.

14. { {"ddMMyy", n} }-->replace n with actual number of your choice to Pick date post today date in the specified format.

15. { {"ddMMyy", "MON"} }-->dynamically pick Monday date (coming Monday, if today is not Monday)

Note. for the 2nd Param-->you can choose to specify either Number OR any letter from =>

16. {{CEPE}} {{ICEPE}} {{CP}} {{ICP}} -> Dynamic Option Side CE or C refers to Calls and PE or P refers to Puts. If "I" is used in PlaceHolder text, On long entries PUTs shall be used

Indicator is equipped with customizable Trade & Risk management settings like multiple Take profit levels, Trailing SL.

Size & LeverageSize and Leverage calculator for trading, using market orders. It will calculate maximum possible leverage by default in order to prioritize capital efficiency. If you wish to use manual leverage you need to manually enter it in the settings. The script rounds both auto leverage and size to your liking. Entry price is always last price. Size is the actual size you need to input, adjusted to your leverage, cost means the margin required to open the trade. I made this indicator as a binance futures user.

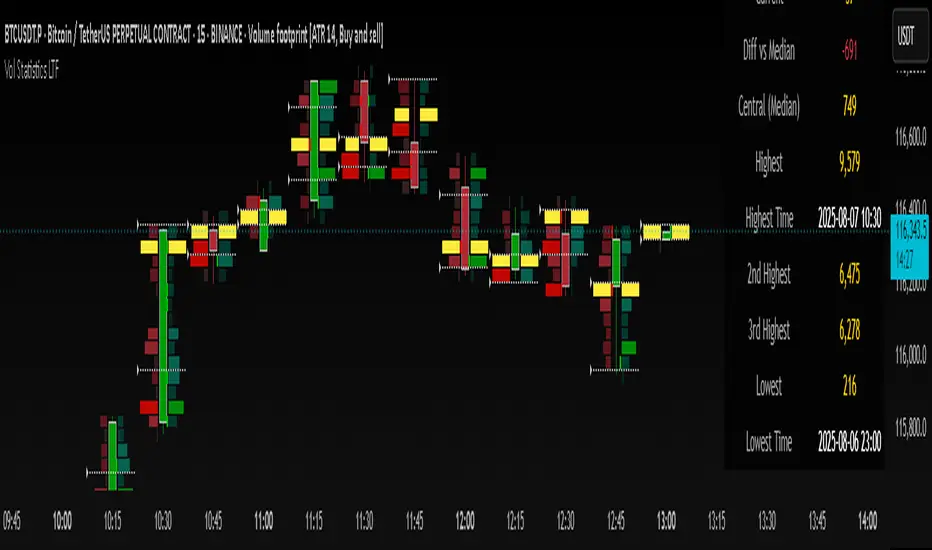

Volume Statistics - IntraweekVolume Statistics - Intraweek: For Orderflow Traders

This tool is designed for traders using volume footprint charts and orderflow methods.

Why it matters:

In orderflow trading, you care about the quality of volume behind each move. You’re not just watching price; you’re watching how much aggression is behind that price move. That’s where this indicator helps.

What to look at:

* Current Volume shows you how much volume is trading right now.

* Central Volume (median or average over 24h or 7D) gives you a baseline for what's normal volume VS abnormal volume.

* The Diff vs Central tells you immediately if current volume is above or below normal.

How this helps:

* If volume is above normal, it suggested elevated levels of buyer or seller aggression. Look for strong follow-through or continuation.

* If volume is below normal, it may signal low interest, passive participation, a lack of conviction, or a fake move.

* Use this context to decide if what you're seeing in the footprint (imbalances, absorption, traps) is actually worth acting on.

Extra context:

* The highest and lowest volume levels and their timestamps help you spot prior key reactions.

* Second and third highest bars help you see other major effort points in the recent window.

Comment with any suggestions on how to improve this indicator.

Volumetric Expansion/Contraction### Indicator Title: Volumetric Expansion/Contraction

### Summary

The Volumetric Expansion/Contraction (PCC) indicator is a comprehensive momentum oscillator designed to identify high-conviction price moves. Unlike traditional oscillators that only look at price, the PCC integrates four critical dimensions of market activity: **Price Change**, **Relative Volume (RVOL)**, **Cumulative Volume Delta (CVD)**, and **Average True Range (ATR)**.

Its primary purpose is to help traders distinguish between meaningful, volume-backed market expansions and noisy, unsustainable price action. It gives more weight to moves that occur in a controlled, low-volatility environment, highlighting potential starts of new trends or significant shifts in market sentiment.

### Key Concepts & Purpose

The indicator's unique formula synthesizes the following concepts:

1. **Price Change:** Measures the magnitude and direction of the primary move.

2. **Relative Volume (RVOL):** Confirms that the move is backed by significant volume compared to its recent average, indicating institutional participation.

3. **Cumulative Volume Delta (CVD):** Measures the underlying buying and selling pressure, confirming that the price move is aligned with the net flow of market orders.

4. **Inverse Volatility (ATR):** This is the indicator's unique twist. It normalizes the signal by the inverse of the Average True Range. This means the indicator's value is **amplified** when volatility (ATR) is low (signifying a controlled, confident expansion) and **dampened** when volatility is high (filtering out chaotic, less predictable moves).

The goal is to provide a single, easy-to-read oscillator that signals when price, volume, and order flow are all in alignment, especially during a breakout from a period of contraction.

### Features

* **Main Oscillator Line:** A single line plotted in a separate pane that represents the calculated strength of the volumetric expansion or contraction.

* **Zero Line:** A dotted reference line to easily distinguish between bullish (above zero) and bearish (below zero) regimes.

* **Visual Threshold Zones:** The background automatically changes color to highlight periods of significant strength:

* **Bright Green:** Indicates a "Strong Up Move" when the oscillator crosses above the user-defined upper threshold.

* **Bright Fuchsia:** Indicates a "Strong Down Move" when the oscillator crosses below the user-defined lower threshold.

### Configurable Settings & Filters

The indicator is fully customizable to allow for extensive testing and adaptation to different assets and timeframes.

#### Main Calculation Inputs

* **Price Change Lookback:** Sets the period for calculating the primary price change.

* **CVD Normalization Length:** The lookback period for normalizing the Cumulative Volume Delta.

* **RVOL Avg Volume Length:** The lookback for the simple moving average of volume, used to calculate RVOL.

* **RVOL Normalization Length:** The lookback period for normalizing the RVOL score.

* **ATR Length & Normalization Length:** Sets the periods for calculating the ATR and its longer-term average for normalization.

#### Weights

* Fine-tune the impact of each core component on the final calculation, allowing you to emphasize what matters most to your strategy (e.g., give more weight to CVD or RVOL).

#### External Market Filter (Powerful Feature)

* **Enable SPY/QQQ Filter for Up Moves?:** A checkbox to activate a powerful regime filter.

* **Symbol:** A dropdown to choose whether to filter signals based on the trend of **SPY** or **QQQ**.

* **SMA Period:** Sets the lookback period for the Simple Moving Average (default is 50).

* **How it works:** When enabled, this filter will **only allow "Strong Up Move" signals to appear if the chosen symbol (SPY or QQQ) is currently trading above its specified SMA**. This is an excellent tool for aligning your signals with the broader market trend and avoiding bullish entries in a bearish market.

#### Visuals

* **Upper/Lower Threshold:** Allows you to define what level the oscillator must cross to trigger the colored background zones, letting you customize the indicator's sensitivity.

***

**Disclaimer:** This tool is designed for market analysis and confluence. It is not a standalone trading system. Always use this indicator in conjunction with your own trading strategy, risk management, and other forms of analysis.

MirPapa:ICT:HTF: FVG OB Threeple# MirPapa:ICT:HTF: FVG OB (Fair Value Gap Order Block)

**Version:** Pine Script® v6

**Author:** © goodia

**License:** MPL-2.0 (Mozilla Public License 2.0)

---

## Overview

“FVG OB” (Fair Value Gap Order Block) identifies higher-timeframe candle ranges where a gap (imbalance) exists between two non-consecutive candles, signaling potential institutional order blocks. This module draws bullish or bearish FVG OB boxes on your lower-timeframe chart, extends them until price interacts a specified number of times, and then finalizes (recolors) the box.

---

## Inputs

- **Enable FVG OB Boxes** (`bool`)

Toggle drawing of HTF FVG OB boxes on the chart.

- **Enable FVG OB Midlines** (`bool`)

Toggle drawing of a midpoint line inside each FVG OB box.

- **FVG OB Close Count** (`int` 1–10)

Number of HTF closes beyond the FVG range required to finalize (recolor) the box.

- **FVG OB Bull Color** (`color`)

Fill & border color for bullish FVG OB boxes.

- **FVG OB Bear Color** (`color`)

Fill & border color for bearish FVG OB boxes.

- **FVG OB Box Transparency** (`int` 1–100)

Opacity level for FVG OB box fills (higher = more transparent).

---

## How It Works

1. **HTF Data Retrieval**

- The script uses `request.security()` (via `GetHTFrevised()`) to fetch HTF OHLC and historical values:

- `_htfHigh3` (high three bars ago) and `_htfLow1` (low one bar ago) for bullish FVG OB.

- `_htfLow3` (low three bars ago) and `_htfHigh1` (high one bar ago) for bearish FVG OB.

- It also tracks the HTF `bar_index` on the lower timeframe to align drawing.

2. **FVG OB Detection**

- **Bullish FVG OB**: Occurs when the HTF low of the previous bar (`low `) is strictly above the HTF high of three bars ago (`high `), creating a gap.

- **Bearish FVG OB**: Occurs when the HTF high of the previous bar (`high `) is strictly below the HTF low of three bars ago (`low `), creating a gap.

3. **Box Creation**

- On each new HTF bar (`ta.change(time(HTF)) != 0`), if a bullish or bearish FVG OB condition is met, the script calls `CreateBoxData()` with:

- **Bullish**: `bottom = HTF low `, `top = HTF high `, `_isBull = true`.

- **Bearish**: `bottom = HTF low `, `top = HTF high `, `_isBull = false`.

- Midline toggled by input.

- A `BoxData` struct is created and stored in either the Bull or Bear array.

4. **Box Extension & Finalization**

- On **every LTF bar**, `ProcessBoxDatas(...)` iterates over all active FVG OB boxes:

1. **Extend Right Edge**: `box.set_right(bar_index)` ensures the box follows the latest bar.

2. **Record Volume Delta**: Tracks buy/sell volume inside the box.

3. **Touch Stage Update**: `modBoxUpdateStage()` increments `_stage` when price touches its “basePoint” (for FVG OB, the basePrice is one side of the gap).

4. **Finalize**: `setBoxFinalize()` checks if the configured number of closes beyond the FVG gap (`FVG OB Close Count`) has occurred. If so:

- `_isActive := false`

- Border and background colors are changed to the “Box Close Color” (input).

- Finalized boxes remain on screen semi-transparent, indicating that the FVG OB zone has been tested.

5. **Midline (Optional)**

- If “Enable FVG OB Midlines” is checked, `ProcessBoxDatas()` also extends a horizontal midpoint line inside the box with `line.set_x2(bar_index)`.

---

## Usage Instructions

1. **Installation**

- Copy the FVG OB section of the Pine Script into TradingView’s Pine Editor (ensure the library import is included).

- Click “Add to Chart.”

2. **Configure Inputs**

- Choose a Higher Time Frame via the dropdown (e.g., “4시간” maps to a 4H timeframe).

- Toggle “Enable FVG OB Boxes” and “Enable FVG OB Midlines.”

- Select colors for bullish and bearish boxes and set transparency.

- Adjust “FVG OB Close Count” to control how many closes beyond the gap finalize the box.

3. **Interpretation**

- **Active FVG OB Boxes** extend to the right until price closes beyond the gap range the specified number of times.

- When finalized, each box changes to the “Box Close Color,” signaling that institutional orders in that gap have likely been filled.

Enjoy precise visualization of higher-timeframe Fair Value Gap Order Blocks on your lower-timeframe chart!

Super Arma Institucional PRO v6.3Super Arma Institucional PRO v6.3

Description

Super Arma Institucional PRO v6.3 is a multifunctional indicator designed for traders looking for a clear and objective analysis of the market, focusing on trends, key price levels and high liquidity zones. It combines three essential elements: moving averages (EMA 20, SMA 50, EMA 200), dynamic support and resistance, and volume-based liquidity zones. This integration offers an institutional view of the market, ideal for identifying strategic entry and exit points.

How it Works

Moving Averages:

EMA 20 (orange): Sensitive to short-term movements, ideal for capturing fast trends.

SMA 50 (blue): Represents the medium-term trend, smoothing out fluctuations.

EMA 200 (red): Indicates the long-term trend, used as a reference for the general market bias.

Support and Resistance: Calculated based on the highest and lowest prices over a defined period (default: 20 bars). These dynamic levels help identify zones where the price may encounter barriers or supports.

Liquidity Zones: Purple rectangles are drawn in areas of significantly above-average volume, indicating regions where large market participants (institutional) may be active. These zones are useful for anticipating price movements or order absorption.

Purpose

The indicator was developed to provide a clean and institutional view of the market, combining classic tools (moving averages and support/resistance) with modern liquidity analysis. It is ideal for traders operating swing trading or position trading strategies, allowing to identify:

Short, medium and long-term trends.

Key support and resistance levels to plan entries and exits.

High liquidity zones where institutional orders can influence the price.

Settings

Show EMA 20 (true): Enables/disables the 20-period EMA.

Show SMA 50 (true): Enables/disables the 50-period SMA.

Show EMA 200 (true): Enables/disables the 200-period EMA.

Support/Resistance Period (20): Sets the period for calculating support and resistance levels.

Liquidity Sensitivity (20): Period for calculating the average volume.

Minimum Liquidity Factor (1.5): Multiplier of the average volume to identify high liquidity zones.

How to Use

Moving Averages:

Crossovers between the EMA 20 and SMA 50 may indicate short/medium-term trend changes.

The EMA 200 serves as a reference for the long-term bias (above = bullish, below = bearish).

Support and Resistance: Use the red (resistance) and green (support) lines to identify reversal or consolidation zones.

Liquidity Zones: The purple rectangles highlight areas of high volume, where the price may react (reversal or breakout). Consider these zones to place orders or manage risks.

Adjust the parameters according to the asset and timeframe to optimize the analysis.

Notes

The chart should be configured only with this indicator to ensure clarity.

Use on timeframes such as 1 hour, 4 hours or daily for better visualization of liquidity zones and support/resistance levels.

Avoid adding other indicators to the chart to keep the script output easily identifiable.

The indicator is designed to be clean, without explicit buy/sell signals, following an institutional approach.

This indicator is perfect for traders who want a visually clear and powerful tool to trade based on trends, key levels and institutional behavior.

Grid Tendence V1The “Grid Tendence V1” strategy is based on the classic Grid strategy, only in this case the entries and exits are made in favor of the trend, which allows to take advantage of large movements to maximize profits, since it is also possible to enter and exit with the balance with a controlled risk, because precisely the distance between each Grid works as a natural and adaptable stop loss and take profit. This fact helps to avoid overlapping entries and exits that would result from using stop loss and take profit as limit orders.

In this version of the script the entries and exits are always at market, and based on the percentage change of the price, not on the profit or loss of the current position.

The user will notice that the strategy setup is based on a controlled risk, risking 5% on each trade, a fairly standard commission and a modest initial capital, all this in order to protect the user of the strategy from unexpected or unrealistic results.

However, it is always recommended to optimize the parameters so that the strategy is effective for each asset and for each time frame.

Quadruple EMA (QEMA)The Quadruple Exponential Moving Average (QEMA) is an advanced technical indicator that extends the concept of lag reduction beyond TEMA (Triple Exponential Moving Average) to a fourth order. By applying a sophisticated four-stage EMA cascade with optimized coefficient distribution, QEMA provides the ultimate evolution in EMA-based lag reduction techniques.

Unlike traditional compund moving averages like DEMA and TEMA, QEMA implements a progressive smoothing system that strategically distributes alphas across four EMA stages and combines them with balanced coefficients (4, -6, 4, -1). This approach creates an indicator that responds extremely quickly to price changes while still maintaining sufficient smoothness to be useful for trading decisions. QEMA is particularly valuable for traders who need the absolute minimum lag possible in trend identification.

▶️ **Core Concepts**

Fourth-order processing: Extends the EMA cascade to four stages for maximum possible lag reduction while maintaining a useful signal

Progressive alpha system: Uses mathematically derived ratio-based alpha progression to balance responsiveness across all four EMA stages

Optimized coefficients: Employs calculated weights (4, -6, 4, -1) to effectively eliminate lag while preserving compound signal stability

Numerical stability control: Implements initialization and alpha distribution to ensure consistent results from the first calculation bar

QEMA achieves its exceptional lag reduction by combining four progressive EMAs with mathematically optimized coefficients. The formula is designed to maximize responsiveness while minimizing the overshoot problems that typically occur with aggressive lag reduction techniques. The implementation uses a ratio-based alpha progression that ensures each EMA stage contributes appropriately to the final result.

▶️ **Common Settings and Parameters**

Period: Default: 15| Base smoothing period | When to Adjust: Decrease for extremely fast signals, increase for more stable output

Alpha: Default: auto | Direct control of base smoothing factor | When to Adjust: Manual setting allows precise tuning beyond standard period settings

Source: Default: Close | Data point used for calculation | When to Adjust: Change to HL2 or HLC3 for more balanced price representation

Pro Tip: Professional traders often use QEMA with longer periods than other moving averages (e.g., QEMA(20) instead of EMA(10)) since its extreme lag reduction provides earlier signals even with longer periods.

▶️ **Calculation and Mathematical Foundation**

Simplified explanation:

QEMA works by calculating four EMAs in sequence, with each EMA taking the previous one as input. It then combines these EMAs using balancing weights (4, -6, 4, -1) to create a moving average with extremely minimal lag and high level of smoothness. The alpha factors for each EMA are progressively adjusted using a mathematical ratio to ensure balanced responsiveness across all stages.

Technical formula:

QEMA = 4 × EMA₁ - 6 × EMA₂ + 4 × EMA₃ - EMA₄

Where:

EMA₁ = EMA(source, α₁)

EMA₂ = EMA(EMA₁, α₂)

EMA₃ = EMA(EMA₂, α₃)

EMA₄ = EMA(EMA₃, α₄)

α₁ = 2/(period + 1) is the base smoothing factor

r = (1/α₁)^(1/3) is the derived ratio

α₂ = α₁ × r, α₃ = α₂ × r, α₄ = α₃ × r are the progressive alphas

Mathematical Rationale for the Alpha Cascade:

The QEMA indicator employs a specific geometric progression for its smoothing factors (alphas) across the four EMA stages. This design is intentional and aims to optimize the filter's performance. The ratio between alphas is **r = (1/α₁)^(1/3)** - derived from the cube root of the reciprocal of the base alpha.

For typical smoothing (α₁ < 1), this results in a sequence of increasing alpha values (α₁ < α₂ < α₃ < α₄), meaning that subsequent EMAs in the cascade are progressively faster (less smoothed). This specific progression, when combined with the QEMA coefficients (4, -6, 4, -1), is chosen for the following reasons:

1. Optimized Frequency Response:

Using the same alpha for all EMA stages (as in a naive multi-EMA approach) can lead to an uneven frequency response, potentially causing over-shooting of certain frequencies or creating undesirable resonance. The geometric progression of alphas in QEMA helps to create a more balanced and controlled filter response across a wider range of movement frequencies. Each stage's contribution to the overall filtering characteristic is more harmonized.

2. Minimized Phase Lag:

A key goal of QEMA is extreme lag reduction. The specific alpha cascade, particularly the relationship defined by **r**, is designed to minimize the cumulative phase lag introduced by the four smoothing stages, while still providing effective noise reduction. Faster subsequent EMAs contribute to this reduced lag.

🔍 Technical Note: The ratio-based alpha progression is crucial for balanced response. The ratio r is calculated as the cube root of 1/α₁, ensuring that the combined effect of all four EMAs creates a mathematically optimal response curve. All EMAs are initialized with the first source value rather than using progressive initialization, eliminating warm-up artifacts and providing consistent results from the first bar.

▶️ **Interpretation Details**

QEMA provides several key insights for traders:

When price crosses above QEMA, it signals the beginning of an uptrend with minimal delay

When price crosses below QEMA, it signals the beginning of a downtrend with minimal delay

The slope of QEMA provides immediate insight into trend direction and momentum

QEMA responds to price reversals significantly faster than other moving averages

Multiple QEMA lines with different periods can identify immediate support/resistance levels

QEMA is particularly valuable in fast-moving markets and for short-term trading strategies where speed of signal generation is critical. It excels at capturing the very beginning of trends and identifying reversals earlier than any other EMA-derived indicator. This makes it especially useful for breakout trading and scalping strategies where getting in early is essential.

▶️ **Limitations and Considerations**

Market conditions: Can generate excessive signals in choppy, sideways markets due to its extreme responsiveness

Overshooting: The aggressive lag reduction can create some overshooting during sharp reversals

Calculation complexity: Requires four separate EMA calculations plus coefficient application, making it computationally more intensive

Parameter sensitivity: Small changes in the base alpha or period can significantly alter behavior

Complementary tools: Should be used with momentum indicators or volatility filters to confirm signals and reduce false positives

▶️ **References**

Mulloy, P. (1994). "Smoothing Data with Less Lag," Technical Analysis of Stocks & Commodities .

Ehlers, J. (2001). Rocket Science for Traders . John Wiley & Sons.

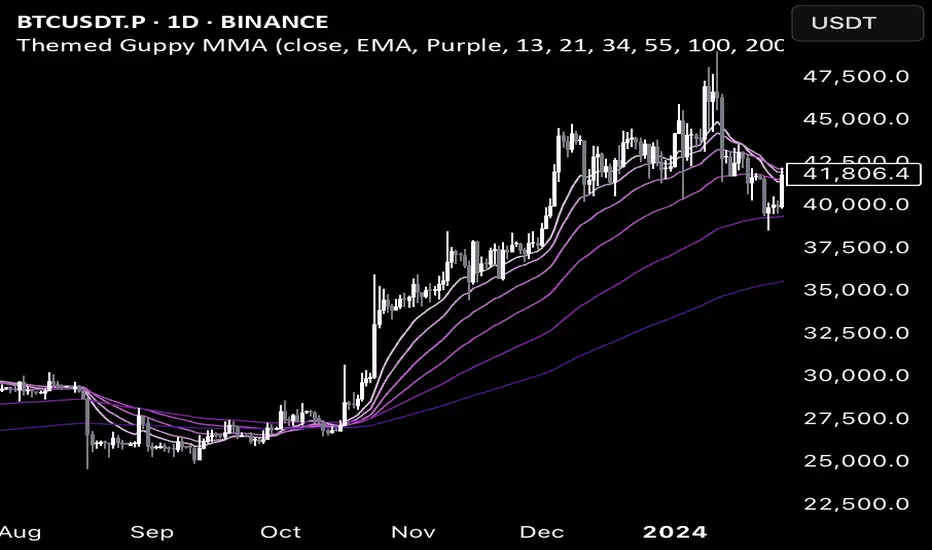

Color Themed Guppy Multiple Moving Average

========== TLDR ==========

The "Color Themed Guppy Multiple Moving Average" plots a group of 6 Moving Averages on your chart with a selection of color themes to automatically style the different length Moving Average lines. As someone who struggles with screens and colors on a busy chart, this indicator has helped me a lot in quickly identifying which Moving Average price is respecting the most - giving me better signals for trade entries and trend loss.

========== Key Features and Advantages ==========

- Show different length Moving Averages with a single indicator

- quickly make your chart more readable with 12 different color themes

- The themes will color the Moving Averages with a gradient (light - dark), with a lighter color indicating a shorter length or 'faster' Moving Average

- Select the type of Moving Average you would like to use

========== Use Cases ==========

Identify Specific Length Moving Averages That are Acting as Support or Resistance:

Having each Moving Average coloured by a theme makes it easier to track each individual line with your eyes, making it easier to quickly find the Moving Averages that price is respecting the most for a given asset and/or trend.

Get Bias Quickly:

When all 6 of the Moving Averages are 'stacked' on top of each other in order, and all are angled either up or down, it can provide a useful bias for the market on your timeframe.