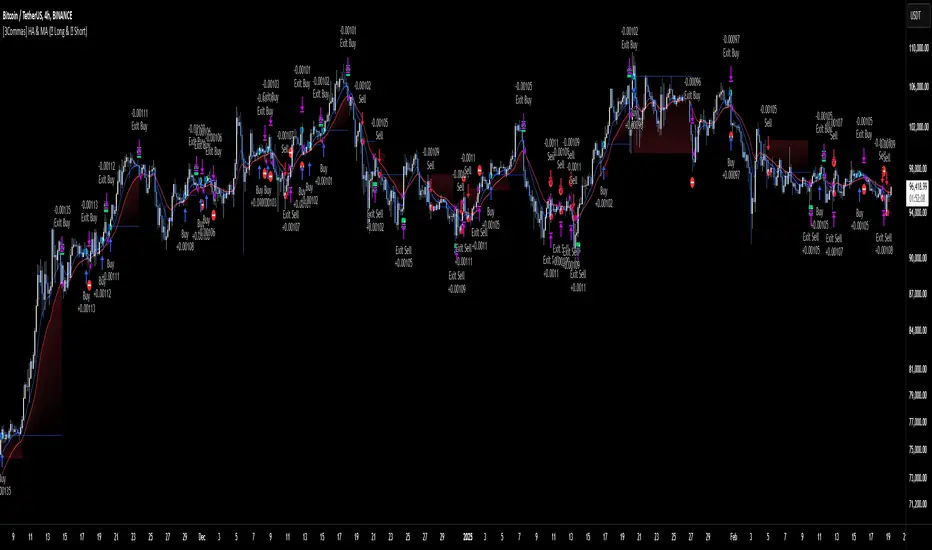

Trendline Breaks with Multi Fibonacci Supertrend StrategyTMFS Strategy: Advanced Trendline Breakouts with Multi-Fibonacci Supertrend

Elevate your algorithmic trading with institutional-grade signal confluence

Strategy Genesis & Evolution

This advanced trading system represents the culmination of a personal research journey, evolving from my custom " Multi Fibonacci Supertrend with Signals " indicator into a comprehensive trading strategy. Built upon the exceptional trendline detection methodology pioneered by LuxAlgo in their " Trendlines with Breaks " indicator, I've engineered a systematic framework that integrates multiple technical factors into a cohesive trading system.

Core Fibonacci Principles

At the heart of this strategy lies the Fibonacci sequence application to volatility measurement:

// Fibonacci-based factors for multiple Supertrend calculations

factor1 = input.float(0.618, 'Factor 1 (Weak/Fibonacci)', minval = 0.01, step = 0.01)

factor2 = input.float(1.618, 'Factor 2 (Medium/Golden Ratio)', minval = 0.01, step = 0.01)

factor3 = input.float(2.618, 'Factor 3 (Strong/Extended Fib)', minval = 0.01, step = 0.01)

These precise Fibonacci ratios create a dynamic volatility envelope that adapts to changing market conditions while maintaining mathematical harmony with natural price movements.

Dynamic Trendline Detection

The strategy incorporates LuxAlgo's pioneering approach to trendline detection:

// Pivotal swing detection (inspired by LuxAlgo)

pivot_high = ta.pivothigh(swing_length, swing_length)

pivot_low = ta.pivotlow(swing_length, swing_length)

// Dynamic slope calculation using ATR

slope = atr_value / swing_length * atr_multiplier

// Update trendlines based on pivot detection

if bool(pivot_high)

upper_slope := slope

upper_trendline := pivot_high

else

upper_trendline := nz(upper_trendline) - nz(upper_slope)

This adaptive trendline approach automatically identifies key structural market boundaries, adjusting in real-time to evolving chart patterns.

Breakout State Management

The strategy implements sophisticated state tracking for breakout detection:

// Track breakouts with state variables

var int upper_breakout_state = 0

var int lower_breakout_state = 0

// Update breakout state when price crosses trendlines

upper_breakout_state := bool(pivot_high) ? 0 : close > upper_trendline ? 1 : upper_breakout_state

lower_breakout_state := bool(pivot_low) ? 0 : close < lower_trendline ? 1 : lower_breakout_state

// Detect new breakouts (state transitions)

bool new_upper_breakout = upper_breakout_state > upper_breakout_state

bool new_lower_breakout = lower_breakout_state > lower_breakout_state

This state-based approach enables precise identification of the exact moment when price breaks through a significant trendline.

Multi-Factor Signal Confluence

Entry signals require confirmation from multiple technical factors:

// Define entry conditions with multi-factor confluence

long_entry_condition = enable_long_positions and

upper_breakout_state > upper_breakout_state and // New trendline breakout

di_plus > di_minus and // Bullish DMI confirmation

close > smoothed_trend // Price above Supertrend envelope

// Execute trades only with full confirmation

if long_entry_condition

strategy.entry('L', strategy.long, comment = "LONG")

This strict requirement for confluence significantly reduces false signals and improves the quality of trade entries.

Advanced Risk Management

The strategy includes sophisticated risk controls with multiple methodologies:

// Calculate stop loss based on selected method

get_long_stop_loss_price(base_price) =>

switch stop_loss_method

'PERC' => base_price * (1 - long_stop_loss_percent)

'ATR' => base_price - long_stop_loss_atr_multiplier * entry_atr

'RR' => base_price - (get_long_take_profit_price() - base_price) / long_risk_reward_ratio

=> na

// Implement trailing functionality

strategy.exit(

id = 'Long Take Profit / Stop Loss',

from_entry = 'L',

qty_percent = take_profit_quantity_percent,

limit = trailing_take_profit_enabled ? na : long_take_profit_price,

stop = long_stop_loss_price,

trail_price = trailing_take_profit_enabled ? long_take_profit_price : na,

trail_offset = trailing_take_profit_enabled ? long_trailing_tp_step_ticks : na,

comment = "TP/SL Triggered"

)

This flexible approach adapts to varying market conditions while providing comprehensive downside protection.

Performance Characteristics

Rigorous backtesting demonstrates exceptional capital appreciation potential with impressive risk-adjusted metrics:

Remarkable total return profile (1,517%+)

Strong Sortino ratio (3.691) indicating superior downside risk control

Profit factor of 1.924 across all trades (2.153 for long positions)

Win rate exceeding 35% with balanced distribution across varied market conditions

Institutional Considerations

The strategy architecture addresses execution complexities faced by institutional participants with temporal filtering and date-range capabilities:

// Time Filter settings with flexible timezone support

import jason5480/time_filters/5 as time_filter

src_timezone = input.string(defval = 'Exchange', title = 'Source Timezone')

dst_timezone = input.string(defval = 'Exchange', title = 'Destination Timezone')

// Date range filtering for precise execution windows

use_from_date = input.bool(defval = true, title = 'Enable Start Date')

from_date = input.time(defval = timestamp('01 Jan 2022 00:00'), title = 'Start Date')

// Validate trading permission based on temporal constraints

date_filter_approved = time_filter.is_in_date_range(

use_from_date, from_date, use_to_date, to_date, src_timezone, dst_timezone

)

These capabilities enable precise execution timing and market session optimization critical for larger market participants.

Acknowledgments

Special thanks to LuxAlgo for the pioneering work on trendline detection and breakout identification that inspired elements of this strategy. Their innovative approach to technical analysis provided a valuable foundation upon which I could build my Fibonacci-based methodology.

This strategy is shared under the same Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license as LuxAlgo's original work.

Past performance is not indicative of future results. Conduct thorough analysis before implementing any algorithmic strategy.

Tìm kiếm tập lệnh với "profit factor"

Market Regime# MARKET REGIME IDENTIFICATION & TRADING SYSTEM

## Complete User Guide

---

## 📋 TABLE OF CONTENTS

1. (#overview)

2. (#regimes)

3. (#indicator-usage)

4. (#entry-signals)

5. (#exit-signals)

6. (#regime-strategies)

7. (#confluence)

8. (#backtesting)

9. (#optimization)

10. (#examples)

---

## OVERVIEW

### What This System Does

This is a **complete market regime identification and trading system** that:

1. **Identifies 6 distinct market regimes** automatically

2. **Adapts trading tactics** to each regime

3. **Provides high-probability entry signals** with confluence scoring

4. **Shows optimal exit points** for each trade

5. **Can be backtested** to validate performance

### Two Components Provided

1. **Indicator** (`market_regime_indicator.pine`)

- Visual regime identification

- Entry/exit signals on chart

- Dynamic support/resistance

- Info tables with live data

- Use for manual trading

2. **Strategy** (`market_regime_strategy.pine`)

- Fully automated backtestable version

- Same logic as indicator

- Position sizing and risk management

- Performance metrics

- Use for backtesting and automation

---

## THE 6 MARKET REGIMES

### 1. 🟢 BULL TRENDING

**Characteristics:**

- Strong uptrend

- Price above SMA50 and SMA200

- ADX > 25 (strong trend)

- Higher highs and higher lows

- DI+ > DI- (bullish momentum)

**What It Means:**

- Market has clear upward direction

- Buyers in control

- Pullbacks are buying opportunities

- Strongest regime for long positions

**How to Trade:**

- ✅ **BUY dips to EMA20 or SMA20**

- ✅ Enter when RSI < 60 on pullback

- ✅ Hold through minor corrections

- ❌ Don't short against the trend

- ❌ Don't sell too early

**Expected Behavior:**

- Pullbacks are shallow (5-10%)

- Bounces are strong

- Support at moving averages holds

- Volume increases on rallies

---

### 2. 🔴 BEAR TRENDING

**Characteristics:**

- Strong downtrend

- Price below SMA50 and SMA200

- ADX > 25 (strong trend)

- Lower highs and lower lows

- DI- > DI+ (bearish momentum)

**What It Means:**

- Market has clear downward direction

- Sellers in control

- Rallies are selling opportunities

- Strongest regime for short positions

**How to Trade:**

- ✅ **SELL rallies to EMA20 or SMA20**

- ✅ Enter when RSI > 40 on bounce

- ✅ Hold through minor bounces

- ❌ Don't buy against the trend

- ❌ Don't cover shorts too early

**Expected Behavior:**

- Rallies are weak (5-10%)

- Selloffs are strong

- Resistance at moving averages holds

- Volume increases on declines

---

### 3. 🔵 BULL RANGING

**Characteristics:**

- Bullish bias but consolidating

- Price near or above SMA50

- ADX < 20 (weak trend)

- Trading in range

- Choppy price action

**What It Means:**

- Uptrend is pausing

- Accumulation phase

- Support and resistance zones clear

- Lower volatility

**How to Trade:**

- ✅ **BUY at support zone**

- ✅ Enter when RSI < 40

- ✅ Take profits at resistance

- ⚠️ Smaller position sizes

- ⚠️ Tighter stops

**Expected Behavior:**

- Range-bound oscillations

- Support bounces repeatedly

- Resistance rejections common

- Eventually breaks higher (usually)

---

### 4. 🟠 BEAR RANGING

**Characteristics:**

- Bearish bias but consolidating

- Price near or below SMA50

- ADX < 20 (weak trend)

- Trading in range

- Choppy price action

**What It Means:**

- Downtrend is pausing

- Distribution phase

- Support and resistance zones clear

- Lower volatility

**How to Trade:**

- ✅ **SELL at resistance zone**

- ✅ Enter when RSI > 60

- ✅ Take profits at support

- ⚠️ Smaller position sizes

- ⚠️ Tighter stops

**Expected Behavior:**

- Range-bound oscillations

- Resistance holds repeatedly

- Support bounces are weak

- Eventually breaks lower (usually)

---

### 5. ⚪ CONSOLIDATION

**Characteristics:**

- No clear direction

- Range compression

- Very low ADX (< 15 often)

- Price inside tight range

- Neutral sentiment

**What It Means:**

- Market is coiling

- Building energy for next move

- Indecision between buyers/sellers

- Calm before the storm

**How to Trade:**

- ✅ **WAIT for breakout direction**

- ✅ Enter on high-volume breakout

- ✅ Direction becomes clear

- ❌ Don't trade inside the range

- ❌ Avoid choppy scalping

**Expected Behavior:**

- Narrow range

- Low volume

- False breakouts possible

- Explosive move when it breaks

---

### 6. 🟣 CHAOS (High Volatility)

**Characteristics:**

- Extreme volatility

- No clear direction

- Erratic price swings

- ATR > 2x average

- Unpredictable

**What It Means:**

- Market panic or euphoria

- News-driven moves

- Emotion dominates logic

- Highest risk environment

**How to Trade:**

- ❌ **STAY OUT!**

- ❌ No positions

- ❌ Wait for stability

- ✅ Protect existing positions

- ✅ Reduce risk

**Expected Behavior:**

- Large intraday swings

- Gaps up/down

- Stop hunts

- Whipsaws

- Eventually calms down

---

## INDICATOR USAGE

### Visual Elements

#### 1. Background Colors

- **Light Green** = Bull Trending (go long)

- **Light Red** = Bear Trending (go short)

- **Light Teal** = Bull Ranging (buy dips)

- **Light Orange** = Bear Ranging (sell rallies)

- **Light Gray** = Consolidation (wait)

- **Purple** = Chaos (stay out!)

#### 2. Regime Labels

- Appear when regime changes

- Show new regime name

- Positioned at highs (bullish) or lows (bearish)

#### 3. Entry Signals

- **Green "LONG"** labels = Buy here

- **Red "SHORT"** labels = Sell here

- Number shows confluence score (X/5 signals)

- Hover for details (stop, target, RSI, etc.)

#### 4. Exit Signals

- **Orange "EXIT LONG"** = Close long position

- **Orange "EXIT SHORT"** = Close short position

- Shows exit reason in tooltip

#### 5. Support/Resistance Lines

- **Green line** = Dynamic support (buy zone)

- **Red line** = Dynamic resistance (sell zone)

- Adapts to regime automatically

#### 6. Moving Averages

- **Blue** = SMA 20 (short-term trend)

- **Orange** = SMA 50 (medium-term trend)

- **Purple** = SMA 200 (long-term trend)

### Information Tables

#### Top Right Table (Main Info)

Shows real-time market conditions:

- **Current Regime** - What regime we're in

- **Bias** - Long, Short, Breakout, or Stay Out

- **ADX** - Trend strength (>25 = strong)

- **Trend** - Strong, Moderate, or Weak

- **Volatility** - High or Normal

- **Vol Ratio** - Current vs average volatility

- **RSI** - Momentum (>70 overbought, <30 oversold)

- **vs SMA50/200** - Price position relative to MAs

- **Support/Resistance** - Exact price levels

- **Long/Short Signals** - Confluence scores (X/5)

#### Bottom Right Table (Regime Guide)

Quick reference for each regime:

- What action to take

- What strategy to use

- Color-coded for quick identification

---

## ENTRY SIGNALS EXPLAINED

### Confluence Scoring System (5 Factors)

Each entry signal is scored 0-5 based on how many factors align:

#### For LONG Entries:

1. ✅ **Regime Alignment** - In Bull Trending or Bull Ranging

2. ✅ **RSI Pullback** - RSI between 35-50 (not overbought)

3. ✅ **Near Support** - Price within 2% of dynamic support

4. ✅ **MACD Turning Up** - Momentum shifting bullish

5. ✅ **Volume Confirmation** - Above average volume

#### For SHORT Entries:

1. ✅ **Regime Alignment** - In Bear Trending or Bear Ranging

2. ✅ **RSI Rejection** - RSI between 50-65 (not oversold)

3. ✅ **Near Resistance** - Price within 2% of dynamic resistance

4. ✅ **MACD Turning Down** - Momentum shifting bearish

5. ✅ **Volume Confirmation** - Above average volume

### Confluence Requirements

**Minimum Confluence** (default = 2):

- 2/5 = Entry signal triggered

- 3/5 = Good signal

- 4/5 = Strong signal

- 5/5 = Excellent signal (rare)

**Higher confluence = Higher probability = Better trades**

### Specific Entry Patterns

#### 1. Bull Trending Entry

```

Requirements:

- Regime = Bull Trending

- Price pulls back to EMA20

- Close above EMA20 (bounce)

- Up candle (close > open)

- RSI < 60

- Confluence ≥ 2

```

#### 2. Bear Trending Entry

```

Requirements:

- Regime = Bear Trending

- Price rallies to EMA20

- Close below EMA20 (rejection)

- Down candle (close < open)

- RSI > 40

- Confluence ≥ 2

```

#### 3. Bull Ranging Entry

```

Requirements:

- Regime = Bull Ranging

- RSI < 40 (oversold)

- Price at or below support

- Up candle (reversal)

- Confluence ≥ 1 (more lenient)

```

#### 4. Bear Ranging Entry

```

Requirements:

- Regime = Bear Ranging

- RSI > 60 (overbought)

- Price at or above resistance

- Down candle (rejection)

- Confluence ≥ 1 (more lenient)

```

#### 5. Consolidation Breakout

```

Requirements:

- Regime = Consolidation

- Price breaks above/below range

- Volume > 1.5x average (explosive)

- Strong directional candle

```

---

## EXIT SIGNALS EXPLAINED

### Three Types of Exits

#### 1. Regime Change Exits (Automatic)

- **Long Exit**: Regime changes to Bear Trending or Chaos

- **Short Exit**: Regime changes to Bull Trending or Chaos

- **Reason**: Market character changed, strategy no longer valid

#### 2. Support/Resistance Break Exits

- **Long Exit**: Price breaks below support by 2%

- **Short Exit**: Price breaks above resistance by 2%

- **Reason**: Key level violated, trend may be reversing

#### 3. Momentum Exits

- **Long Exit**: RSI > 70 (overbought) AND down candle

- **Short Exit**: RSI < 30 (oversold) AND up candle

- **Reason**: Overextension, take profits

### Stop Loss & Take Profit

**Stop Loss** (Automatic in strategy):

- Placed at Entry - (ATR × 2)

- Adapts to volatility

- Protected from whipsaws

- Typically 2-4% for stocks, 5-10% for crypto

**Take Profit** (Automatic in strategy):

- Placed at Entry + (Stop Distance × R:R Ratio)

- Default 2.5:1 reward:risk

- Example: $2 risk = $5 reward target

- Allows winners to run

---

## TRADING EACH REGIME

### BULL TRENDING - Most Profitable Long Environment

**Strategy: Buy Every Dip**

**Entry Rules:**

1. Wait for pullback to EMA20 or SMA20

2. Look for RSI < 60

3. Enter when candle closes above MA

4. Confluence should be 2+

**Stop Loss:**

- Below the recent swing low

- Or 2 × ATR below entry

**Take Profit:**

- At previous high

- Or 2.5:1 R:R minimum

**Position Size:**

- Can use full size (2% risk)

- High win rate regime

**Example Trade:**

```

Price: $100, pulls back to $98 (EMA20)

Entry: $98.50 (close above EMA)

Stop: $96.50 (2 ATR)

Target: $103.50 (2.5:1)

Risk: $2, Reward: $5

```

---

### BEAR TRENDING - Most Profitable Short Environment

**Strategy: Sell Every Rally**

**Entry Rules:**

1. Wait for bounce to EMA20 or SMA20

2. Look for RSI > 40

3. Enter when candle closes below MA

4. Confluence should be 2+

**Stop Loss:**

- Above the recent swing high

- Or 2 × ATR above entry

**Take Profit:**

- At previous low

- Or 2.5:1 R:R minimum

**Position Size:**

- Can use full size (2% risk)

- High win rate regime

**Example Trade:**

```

Price: $100, rallies to $102 (EMA20)

Entry: $101.50 (close below EMA)

Stop: $103.50 (2 ATR)

Target: $96.50 (2.5:1)

Risk: $2, Reward: $5

```

---

### BULL RANGING - Buy Low, Sell High

**Strategy: Range Trading (Long Bias)**

**Entry Rules:**

1. Wait for price at support zone

2. Look for RSI < 40

3. Enter on reversal candle

4. Confluence should be 1-2+

**Stop Loss:**

- Below support zone

- Tighter than trending (1.5 ATR)

**Take Profit:**

- At resistance zone

- Don't hold through resistance

**Position Size:**

- Reduce to 1-1.5% risk

- Lower win rate than trending

**Example Trade:**

```

Range: $95-$105

Entry: $96 (at support, RSI 35)

Stop: $94 (below support)

Target: $104 (at resistance)

Risk: $2, Reward: $8 (4:1)

```

---

### BEAR RANGING - Sell High, Buy Low

**Strategy: Range Trading (Short Bias)**

**Entry Rules:**

1. Wait for price at resistance zone

2. Look for RSI > 60

3. Enter on rejection candle

4. Confluence should be 1-2+

**Stop Loss:**

- Above resistance zone

- Tighter than trending (1.5 ATR)

**Take Profit:**

- At support zone

- Don't hold through support

**Position Size:**

- Reduce to 1-1.5% risk

- Lower win rate than trending

**Example Trade:**

```

Range: $95-$105

Entry: $104 (at resistance, RSI 65)

Stop: $106 (above resistance)

Target: $96 (at support)

Risk: $2, Reward: $8 (4:1)

```

---

### CONSOLIDATION - Wait for Breakout

**Strategy: Breakout Trading**

**Entry Rules:**

1. Identify consolidation range

2. Wait for VOLUME SURGE (1.5x+ avg)

3. Enter on close outside range

4. Direction must be clear

**Stop Loss:**

- Opposite side of range

- Or 2 ATR

**Take Profit:**

- Measure range height, project it

- Example: $10 range = $10 move expected

**Position Size:**

- Reduce to 1% risk

- 50% false breakout rate

**Example Trade:**

```

Consolidation: $98-$102 (4-point range)

Breakout: $102.50 (high volume)

Entry: $103

Stop: $100 (back in range)

Target: $107 (4-point range projected)

Risk: $3, Reward: $4

```

---

### CHAOS - STAY OUT!

**Strategy: Preservation**

**What to Do:**

- ❌ NO new positions

- ✅ Close existing positions if near entry

- ✅ Tighten stops on profitable trades

- ✅ Reduce position sizes dramatically

- ✅ Wait for regime to stabilize

**Why It's Dangerous:**

- Stop hunts are common

- Whipsaws everywhere

- News-driven volatility

- No technical reliability

- Even "perfect" setups fail

**When Does It End:**

- Volatility ratio drops < 1.5

- ADX starts rising (direction appears)

- Price respects support/resistance again

- Usually 1-5 days

---

## CONFLUENCE SYSTEM

### How It Works

The system scores each potential entry on 5 factors. More factors aligning = higher probability.

### Confluence Requirements by Regime

**Trending Regimes** (strictest):

- Minimum 2/5 required

- 3/5 = Good

- 4-5/5 = Excellent

**Ranging Regimes** (moderate):

- Minimum 1-2/5 required

- 2/5 = Good

- 3+/5 = Excellent

**Consolidation** (breakout only):

- Volume is most critical

- Direction confirmation

- Less confluence needed

### Adjusting Minimum Confluence

**If too few signals:**

- Lower from 2 to 1

- More trades, lower quality

**If too many false signals:**

- Raise from 2 to 3

- Fewer trades, higher quality

**Recommendation:**

- Start at 2

- Adjust based on win rate

- Aim for 55-65% win rate

---

## STRATEGY BACKTESTING

### Loading the Strategy

1. Copy `market_regime_strategy.pine`

2. Open Pine Editor in TradingView

3. Paste and "Add to Chart"

4. Strategy Tester tab opens at bottom

### Initial Settings

```

Risk Per Trade: 2%

ATR Stop Multiplier: 2.0

Reward:Risk Ratio: 2.5

Trade Longs: ✓

Trade Shorts: ✓

Trade Trending Only: ✗ (test both)

Avoid Chaos: ✓

Minimum Confluence: 2

```

### What to Look For

**Good Results:**

- Win Rate: 50-60%

- Profit Factor: 1.8-2.5

- Net Profit: Positive

- Max Drawdown: <20%

- Consistent equity curve

**Warning Signs:**

- Win Rate: <45% (too many losses)

- Profit Factor: <1.5 (barely profitable)

- Max Drawdown: >30% (too risky)

- Erratic equity curve (unstable)

### Testing Different Regimes

**Test 1: Trending Only**

```

Trade Trending Only: ✓

Result: Higher win rate, fewer trades

```

**Test 2: All Regimes**

```

Trade Trending Only: ✗

Result: More trades, potentially lower win rate

```

**Test 3: Long Only**

```

Trade Longs: ✓

Trade Shorts: ✗

Result: Works in bull markets

```

**Test 4: Short Only**

```

Trade Longs: ✗

Trade Shorts: ✓

Result: Works in bear markets

```

---

## SETTINGS OPTIMIZATION

### Key Parameters to Adjust

#### 1. Risk Per Trade (Most Important)

- **0.5%** = Very conservative

- **1.0%** = Conservative (recommended for beginners)

- **2.0%** = Moderate (recommended)

- **3.0%** = Aggressive

- **5.0%** = Very aggressive (not recommended)

**Impact:** Higher risk = higher returns BUT bigger drawdowns

#### 2. Reward:Risk Ratio

- **2:1** = More wins needed, hit target faster

- **2.5:1** = Balanced (recommended)

- **3:1** = Fewer wins needed, hold longer

- **4:1** = Very patient, best in trending

**Impact:** Higher R:R = can have lower win rate

#### 3. Minimum Confluence

- **1** = More signals, lower quality

- **2** = Balanced (recommended)

- **3** = Fewer signals, higher quality

- **4** = Very selective

- **5** = Almost never triggers

**Impact:** Higher = fewer but better trades

#### 4. ADX Thresholds

- **Trending: 20-30** (default 25)

- Lower = detect trends earlier

- Higher = only strong trends

- **Ranging: 15-25** (default 20)

- Lower = identify ranging earlier

- Higher = only weak trends

#### 5. Trend Period (SMA)

- **20-50** = Short-term trends

- **50** = Medium-term (default, recommended)

- **100-200** = Long-term trends

**Impact:** Longer period = slower regime changes, more stable

### Optimization Workflow

**Step 1: Baseline**

- Use all default settings

- Test on 3+ years

- Record: Win Rate, PF, Drawdown

**Step 2: Risk Optimization**

- Test 1%, 1.5%, 2%, 2.5%

- Find best risk-adjusted return

- Balance profit vs drawdown

**Step 3: R:R Optimization**

- Test 2:1, 2.5:1, 3:1

- Check which maximizes profit factor

- Consider holding time

**Step 4: Confluence Optimization**

- Test 1, 2, 3

- Find sweet spot for win rate

- Aim for 55-65% win rate

**Step 5: Regime Filter**

- Test with/without trend filter

- Test with/without chaos filter

- Find what works for your asset

---

## REAL TRADING EXAMPLES

### Example 1: Bull Trending - SPY

**Setup:**

- Regime: BULL TRENDING

- Price pulls back from $450 to $445

- EMA20 at $444

- RSI drops to 45

- Confluence: 4/5

**Entry:**

- Price closes at $445.50 (above EMA20)

- LONG signal appears

- Enter at $445.50

**Risk Management:**

- Stop: $443 (2 ATR = $2.50)

- Target: $451.75 (2.5:1 = $6.25)

- Risk: $2.50 per share

- Position: 80 shares (2% of $10k = $200 risk)

**Outcome:**

- Price rallies to $452 in 3 days

- Target hit

- Profit: $6.50 × 80 = $520

- Return: 2.6 × risk (excellent)

---

### Example 2: Bear Ranging - AAPL

**Setup:**

- Regime: BEAR RANGING

- Range: $165-$175

- Price rallies to $174

- Resistance at $175

- RSI at 68

- Confluence: 3/5

**Entry:**

- Rejection candle at $174

- SHORT signal appears

- Enter at $173.50

**Risk Management:**

- Stop: $176 (above resistance)

- Target: $166 (support)

- Risk: $2.50

- Position: 80 shares

**Outcome:**

- Price drops to $167 in 2 days

- Target hit

- Profit: $6.50 × 80 = $520

- Return: 2.6 × risk

---

### Example 3: Consolidation Breakout - BTC

**Setup:**

- Regime: CONSOLIDATION

- Range: $28,000 - $30,000

- Compressed for 2 weeks

- Volume declining

**Breakout:**

- Price breaks $30,000

- Volume surges 200%

- Close at $30,500

- LONG signal

**Entry:**

- Enter at $30,500

**Risk Management:**

- Stop: $29,500 (back in range)

- Target: $32,000 (range height = $2k)

- Risk: $1,000

- Position: 0.2 BTC ($200 risk on $10k)

**Outcome:**

- Price runs to $33,000

- Target exceeded

- Profit: $2,500 × 0.2 = $500

- Return: 2.5 × risk

---

### Example 4: Avoiding Chaos - Tesla

**Setup:**

- Regime: BULL TRENDING

- LONG position from $240

- Elon tweets something crazy

- Regime changes to CHAOS

**Action:**

- EXIT signal appears

- Close position immediately

- Current price: $242 (small profit)

**Outcome:**

- Next 3 days: wild swings

- High $255, Low $230

- By staying out, avoided:

- Potential stop out

- Whipsaw losses

- Stress

**Result:**

- Small profit preserved

- Capital protected

- Re-enter when regime stabilizes

---

## ALERTS SETUP

### Available Alerts

1. **Bull Trending Regime** - Market goes bullish

2. **Bear Trending Regime** - Market goes bearish

3. **Chaos Regime** - High volatility, stay out

4. **Long Entry Signal** - Buy opportunity

5. **Short Entry Signal** - Sell opportunity

6. **Long Exit Signal** - Close long

7. **Short Exit Signal** - Close short

### How to Set Up

1. Click **⏰ (Alert)** icon in TradingView

2. Select **Condition**: Choose indicator + alert type

3. **Options**: Popup, Email, Webhook, etc.

4. **Message**: Customize notification

5. Click **Create**

### Recommended Alert Strategy

**For Active Traders:**

- Long Entry Signal

- Short Entry Signal

- Long Exit Signal

- Short Exit Signal

**For Position Traders:**

- Bull Trending Regime (enter longs)

- Bear Trending Regime (enter shorts)

- Chaos Regime (exit all)

**For Conservative:**

- Only regime change alerts

- Manually review entries

- More selective

---

## TIPS FOR SUCCESS

### 1. Start Small

- Paper trade first

- Then 0.5% risk

- Build to 1-2% over time

### 2. Follow the Regime

- Don't fight it

- Adapt your style

- Different tactics for each

### 3. Trust the Confluence

- 4-5/5 = Best trades

- 2-3/5 = Good trades

- 1/5 = Skip unless desperate

### 4. Respect Exits

- Don't hope and hold

- Cut losses quickly

- Take profits at targets

### 5. Avoid Chaos

- Seriously, just stay out

- Protect your capital

- Wait for clarity

### 6. Keep a Journal

- Record every trade

- Note regime and confluence

- Review weekly

- Learn patterns

### 7. Backtest Thoroughly

- 3+ years minimum

- Multiple market conditions

- Different assets

- Walk-forward test

### 8. Be Patient

- Best setups are rare

- 1-3 trades per week is normal

- Quality over quantity

- Compound over time

---

## COMMON QUESTIONS

**Q: How many trades per month should I expect?**

A: Depends on timeframe and settings. Daily chart: 5-15 trades/month. 4H chart: 15-30 trades/month.

**Q: What's a good win rate?**

A: 55-65% is excellent. 50-55% is good. Below 50% needs adjustment.

**Q: Should I trade all regimes?**

A: Beginners: Only trending. Intermediate: Trending + ranging. Advanced: All except chaos.

**Q: Can I use this on any timeframe?**

A: Best on Daily and 4H. Works on 1H with more noise. Not recommended <1H.

**Q: What if I'm in a trade and regime changes?**

A: Exit immediately (if using indicator) or let strategy handle it automatically.

**Q: How do I know if I'm over-optimizing?**

A: If results are perfect on one period but fail on another. Use walk-forward testing.

**Q: Should I always take 5/5 confluence trades?**

A: Yes, but they're rare (1-2/month). Don't wait only for these.

**Q: Can I combine this with other indicators?**

A: Yes, but keep it simple. RSI, MACD already included. Maybe add volume profile.

**Q: What assets work best?**

A: Liquid stocks, major crypto, futures. Avoid forex spot (use futures), penny stocks.

**Q: How long to hold positions?**

A: Trending: Days to weeks. Ranging: Hours to days. Breakout: Days. Let the regime guide you.

---

## FINAL THOUGHTS

This system gives you:

- ✅ Clear market context (regime)

- ✅ High-probability entries (confluence)

- ✅ Defined exits (automatic signals)

- ✅ Adaptable tactics (regime-specific)

- ✅ Backtestable results (strategy version)

**Success requires:**

- 📚 Understanding each regime

- 🎯 Following the signals

- 💪 Discipline to wait

- 🧠 Emotional control

- 📊 Proper risk management

**Start your journey:**

1. Load the indicator

2. Watch for 1 week (no trading)

3. Identify regime patterns

4. Paper trade for 1 month

5. Go live with small size

6. Scale up as you gain confidence

**Remember:** The market will always be here. There's no rush. Master one regime at a time, and you'll be profitable in all conditions!

Good luck! 🚀

Adaptive Genesis Engine [AGE]ADAPTIVE GENESIS ENGINE (AGE)

Pure Signal Evolution Through Genetic Algorithms

Where Darwin Meets Technical Analysis

🧬 WHAT YOU'RE GETTING - THE PURE INDICATOR

This is a technical analysis indicator - it generates signals, visualizes probability, and shows you the evolutionary process in real-time. This is NOT a strategy with automatic execution - it's a sophisticated signal generation system that you control .

What This Indicator Does:

Generates Long/Short entry signals with probability scores (35-88% range)

Evolves a population of up to 12 competing strategies using genetic algorithms

Validates strategies through walk-forward optimization (train/test cycles)

Visualizes signal quality through premium gradient clouds and confidence halos

Displays comprehensive metrics via enhanced dashboard

Provides alerts for entries and exits

Works on any timeframe, any instrument, any broker

What This Indicator Does NOT Do:

Execute trades automatically

Manage positions or calculate position sizes

Place orders on your behalf

Make trading decisions for you

This is pure signal intelligence. AGE tells you when and how confident it is. You decide whether and how much to trade.

🔬 THE SCIENCE: GENETIC ALGORITHMS MEET TECHNICAL ANALYSIS

What Makes This Different - The Evolutionary Foundation

Most indicators are static - they use the same parameters forever, regardless of market conditions. AGE is alive . It maintains a population of competing strategies that evolve, adapt, and improve through natural selection principles:

Birth: New strategies spawn through crossover breeding (combining DNA from fit parents) plus random mutation for exploration

Life: Each strategy trades virtually via shadow portfolios, accumulating wins/losses, tracking drawdown, and building performance history

Selection: Strategies are ranked by comprehensive fitness scoring (win rate, expectancy, drawdown control, signal efficiency)

Death: Weak strategies are culled periodically, with elite performers (top 2 by default) protected from removal

Evolution: The gene pool continuously improves as successful traits propagate and unsuccessful ones die out

This is not curve-fitting. Each new strategy must prove itself on out-of-sample data through walk-forward validation before being trusted for live signals.

🧪 THE DNA: WHAT EVOLVES

Every strategy carries a 10-gene chromosome controlling how it interprets market data:

Signal Sensitivity Genes

Entropy Sensitivity (0.5-2.0): Weight given to market order/disorder calculations. Low values = conservative, require strong directional clarity. High values = aggressive, act on weaker order signals.

Momentum Sensitivity (0.5-2.0): Weight given to RSI/ROC/MACD composite. Controls responsiveness to momentum shifts vs. mean-reversion setups.

Structure Sensitivity (0.5-2.0): Weight given to support/resistance positioning. Determines how much price location within swing range matters.

Probability Adjustment Genes

Probability Boost (-0.10 to +0.10): Inherent bias toward aggressive (+) or conservative (-) entries. Acts as personality trait - some strategies naturally optimistic, others pessimistic.

Trend Strength Requirement (0.3-0.8): Minimum trend conviction needed before signaling. Higher values = only trades strong trends, lower values = acts in weak/sideways markets.

Volume Filter (0.5-1.5): Strictness of volume confirmation. Higher values = requires strong volume, lower values = volume less important.

Risk Management Genes

ATR Multiplier (1.5-4.0): Base volatility scaling for all price levels. Controls whether strategy uses tight or wide stops/targets relative to ATR.

Stop Multiplier (1.0-2.5): Stop loss tightness. Lower values = aggressive profit protection, higher values = more breathing room.

Target Multiplier (1.5-4.0): Profit target ambition. Lower values = quick scalping exits, higher values = swing trading holds.

Adaptation Gene

Regime Adaptation (0.0-1.0): How much strategy adjusts behavior based on detected market regime (trending/volatile/choppy). Higher values = more reactive to regime changes.

The Magic: AGE doesn't just try random combinations. Through tournament selection and fitness-weighted crossover, successful gene combinations spread through the population while unsuccessful ones fade away. Over 50-100 bars, you'll see the population converge toward genes that work for YOUR instrument and timeframe.

📊 THE SIGNAL ENGINE: THREE-LAYER SYNTHESIS

Before any strategy generates a signal, AGE calculates probability through multi-indicator confluence:

Layer 1 - Market Entropy (Information Theory)

Measures whether price movements exhibit directional order or random walk characteristics:

The Math:

Shannon Entropy = -Σ(p × log(p))

Market Order = 1 - (Entropy / 0.693)

What It Means:

High entropy = choppy, random market → low confidence signals

Low entropy = directional market → high confidence signals

Direction determined by up-move vs down-move dominance over lookback period (default: 20 bars)

Signal Output: -1.0 to +1.0 (bearish order to bullish order)

Layer 2 - Momentum Synthesis

Combines three momentum indicators into single composite score:

Components:

RSI (40% weight): Normalized to -1/+1 scale using (RSI-50)/50

Rate of Change (30% weight): Percentage change over lookback (default: 14 bars), clamped to ±1

MACD Histogram (30% weight): Fast(12) - Slow(26), normalized by ATR

Why This Matters: RSI catches mean-reversion opportunities, ROC catches raw momentum, MACD catches momentum divergence. Weighting favors RSI for reliability while keeping other perspectives.

Signal Output: -1.0 to +1.0 (strong bearish to strong bullish)

Layer 3 - Structure Analysis

Evaluates price position within swing range (default: 50-bar lookback):

Position Classification:

Bottom 20% of range = Support Zone → bullish bounce potential

Top 20% of range = Resistance Zone → bearish rejection potential

Middle 60% = Neutral Zone → breakout/breakdown monitoring

Signal Logic:

At support + bullish candle = +0.7 (strong buy setup)

At resistance + bearish candle = -0.7 (strong sell setup)

Breaking above range highs = +0.5 (breakout confirmation)

Breaking below range lows = -0.5 (breakdown confirmation)

Consolidation within range = ±0.3 (weak directional bias)

Signal Output: -1.0 to +1.0 (bearish structure to bullish structure)

Confluence Voting System

Each layer casts a vote (Long/Short/Neutral). The system requires minimum 2-of-3 agreement (configurable 1-3) before generating a signal:

Examples:

Entropy: Bullish, Momentum: Bullish, Structure: Neutral → Signal generated (2 long votes)

Entropy: Bearish, Momentum: Neutral, Structure: Neutral → No signal (only 1 short vote)

All three bullish → Signal generated with +5% probability bonus

This is the key to quality. Single indicators give too many false signals. Triple confirmation dramatically improves accuracy.

📈 PROBABILITY CALCULATION: HOW CONFIDENCE IS MEASURED

Base Probability:

Raw_Prob = 50% + (Average_Signal_Strength × 25%)

Then AGE applies strategic adjustments:

Trend Alignment:

Signal with trend: +4%

Signal against strong trend: -8%

Weak/no trend: no adjustment

Regime Adaptation:

Trending market (efficiency >50%, moderate vol): +3%

Volatile market (vol ratio >1.5x): -5%

Choppy market (low efficiency): -2%

Volume Confirmation:

Volume > 70% of 20-bar SMA: no change

Volume below threshold: -3%

Volatility State (DVS Ratio):

High vol (>1.8x baseline): -4% (reduce confidence in chaos)

Low vol (<0.7x baseline): -2% (markets can whipsaw in compression)

Moderate elevated vol (1.0-1.3x): +2% (trending conditions emerging)

Confluence Bonus:

All 3 indicators agree: +5%

2 of 3 agree: +2%

Strategy Gene Adjustment:

Probability Boost gene: -10% to +10%

Regime Adaptation gene: scales regime adjustments by 0-100%

Final Probability: Clamped between 35% (minimum) and 88% (maximum)

Why These Ranges?

Below 35% = too uncertain, better not to signal

Above 88% = unrealistic, creates overconfidence

Sweet spot: 65-80% for quality entries

🔄 THE SHADOW PORTFOLIO SYSTEM: HOW STRATEGIES COMPETE

Each active strategy maintains a virtual trading account that executes in parallel with real-time data:

Shadow Trading Mechanics

Entry Logic:

Calculate signal direction, probability, and confluence using strategy's unique DNA

Check if signal meets quality gate:

Probability ≥ configured minimum threshold (default: 65%)

Confluence ≥ configured minimum (default: 2 of 3)

Direction is not zero (must be long or short, not neutral)

Verify signal persistence:

Base requirement: 2 bars (configurable 1-5)

Adapts based on probability: high-prob signals (75%+) enter 1 bar faster, low-prob signals need 1 bar more

Adjusts for regime: trending markets reduce persistence by 1, volatile markets add 1

Apply additional filters:

Trend strength must exceed strategy's requirement gene

Regime filter: if volatile market detected, probability must be 72%+ to override

Volume confirmation required (volume > 70% of average)

If all conditions met for required persistence bars, enter shadow position at current close price

Position Management:

Entry Price: Recorded at close of entry bar

Stop Loss: ATR-based distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit: ATR-based distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Position: +1 (long) or -1 (short), only one at a time per strategy

Exit Logic:

Check if price hit stop (on low) or target (on high) on current bar

Record trade outcome in R-multiples (profit/loss normalized by ATR)

Update performance metrics:

Total trades counter incremented

Wins counter (if profit > 0)

Cumulative P&L updated

Peak equity tracked (for drawdown calculation)

Maximum drawdown from peak recorded

Enter cooldown period (default: 8 bars, configurable 3-20) before next entry allowed

Reset signal age counter to zero

Walk-Forward Tracking:

During position lifecycle, trades are categorized:

Training Phase (first 250 bars): Trade counted toward training metrics

Testing Phase (next 75 bars): Trade counted toward testing metrics (out-of-sample)

Live Phase (after WFO period): Trade counted toward overall metrics

Why Shadow Portfolios?

No lookahead bias (uses only data available at the bar)

Realistic execution simulation (entry on close, stop/target checks on high/low)

Independent performance tracking for true fitness comparison

Allows safe experimentation without risking capital

Each strategy learns from its own experience

🏆 FITNESS SCORING: HOW STRATEGIES ARE RANKED

Fitness is not just win rate. AGE uses a comprehensive multi-factor scoring system:

Core Metrics (Minimum 3 trades required)

Win Rate (30% of fitness):

WinRate = Wins / TotalTrades

Normalized directly (0.0-1.0 scale)

Total P&L (30% of fitness):

Normalized_PnL = (PnL + 300) / 600

Clamped 0.0-1.0. Assumes P&L range of -300R to +300R for normalization scale.

Expectancy (25% of fitness):

Expectancy = Total_PnL / Total_Trades

Normalized_Expectancy = (Expectancy + 30) / 60

Clamped 0.0-1.0. Rewards consistency of profit per trade.

Drawdown Control (15% of fitness):

Normalized_DD = 1 - (Max_Drawdown / 15)

Clamped 0.0-1.0. Penalizes strategies that suffer large equity retracements from peak.

Sample Size Adjustment

Quality Factor:

<50 trades: 1.0 (full weight, small sample)

50-100 trades: 0.95 (slight penalty for medium sample)

100 trades: 0.85 (larger penalty for large sample)

Why penalize more trades? Prevents strategies from gaming the system by taking hundreds of tiny trades to inflate statistics. Favors quality over quantity.

Bonus Adjustments

Walk-Forward Validation Bonus:

if (WFO_Validated):

Fitness += (WFO_Efficiency - 0.5) × 0.1

Strategies proven on out-of-sample data receive up to +10% fitness boost based on test/train efficiency ratio.

Signal Efficiency Bonus (if diagnostics enabled):

if (Signals_Evaluated > 10):

Pass_Rate = Signals_Passed / Signals_Evaluated

Fitness += (Pass_Rate - 0.1) × 0.05

Rewards strategies that generate high-quality signals passing the quality gate, not just profitable trades.

Final Fitness: Clamped at 0.0 minimum (prevents negative fitness values)

Result: Elite strategies typically achieve 0.50-0.75 fitness. Anything above 0.60 is excellent. Below 0.30 is prime candidate for culling.

🔬 WALK-FORWARD OPTIMIZATION: ANTI-OVERFITTING PROTECTION

This is what separates AGE from curve-fitted garbage indicators.

The Three-Phase Process

Every new strategy undergoes a rigorous validation lifecycle:

Phase 1 - Training Window (First 250 bars, configurable 100-500):

Strategy trades normally via shadow portfolio

All trades count toward training performance metrics

System learns which gene combinations produce profitable patterns

Tracks independently: Training_Trades, Training_Wins, Training_PnL

Phase 2 - Testing Window (Next 75 bars, configurable 30-200):

Strategy continues trading without any parameter changes

Trades now count toward testing performance metrics (separate tracking)

This is out-of-sample data - strategy has never seen these bars during "optimization"

Tracks independently: Testing_Trades, Testing_Wins, Testing_PnL

Phase 3 - Validation Check:

Minimum_Trades = 5 (configurable 3-15)

IF (Train_Trades >= Minimum AND Test_Trades >= Minimum):

WR_Efficiency = Test_WinRate / Train_WinRate

Expectancy_Efficiency = Test_Expectancy / Train_Expectancy

WFO_Efficiency = (WR_Efficiency + Expectancy_Efficiency) / 2

IF (WFO_Efficiency >= 0.55): // configurable 0.3-0.9

Strategy.Validated = TRUE

Strategy receives fitness bonus

ELSE:

Strategy receives 30% fitness penalty

ELSE:

Validation deferred (insufficient trades in one or both periods)

What Validation Means

Validated Strategy (Green "✓ VAL" in dashboard):

Performed at least 55% as well on unseen data compared to training data

Gets fitness bonus: +(efficiency - 0.5) × 0.1

Receives priority during tournament selection for breeding

More likely to be chosen as active trading strategy

Unvalidated Strategy (Orange "○ TRAIN" in dashboard):

Failed to maintain performance on test data (likely curve-fitted to training period)

Receives 30% fitness penalty (0.7x multiplier)

Makes strategy prime candidate for culling

Can still trade but with lower selection probability

Insufficient Data (continues collecting):

Hasn't completed both training and testing periods yet

OR hasn't achieved minimum trade count in both periods

Validation check deferred until requirements met

Why 55% Efficiency Threshold?

If a strategy earned 10R during training but only 5.5R during testing, it still proved an edge exists beyond random luck. Requiring 100% efficiency would be unrealistic - market conditions change between periods. But requiring >50% ensures the strategy didn't completely degrade on fresh data.

The Protection: Strategies that work great on historical data but fail on new data are automatically identified and penalized. This prevents the population from being polluted by overfitted strategies that would fail in live trading.

🌊 DYNAMIC VOLATILITY SCALING (DVS): ADAPTIVE STOP/TARGET PLACEMENT

AGE doesn't use fixed stop distances. It adapts to current volatility conditions in real-time.

Four Volatility Measurement Methods

1. ATR Ratio (Simple Method):

Current_Vol = ATR(14) / Close

Baseline_Vol = SMA(Current_Vol, 100)

Ratio = Current_Vol / Baseline_Vol

Basic comparison of current ATR to 100-bar moving average baseline.

2. Parkinson (High-Low Range Based):

For each bar: HL = log(High / Low)

Parkinson_Vol = sqrt(Σ(HL²) / (4 × Period × log(2)))

More stable than close-to-close volatility. Captures intraday range expansion without overnight gap noise.

3. Garman-Klass (OHLC Based):

HL_Term = 0.5 × ²

CO_Term = (2×log(2) - 1) × ²

GK_Vol = sqrt(Σ(HL_Term - CO_Term) / Period)

Most sophisticated estimator. Incorporates all four price points (open, high, low, close) plus gap information.

4. Ensemble Method (Default - Median of All Three):

Ratio_1 = ATR_Current / ATR_Baseline

Ratio_2 = Parkinson_Current / Parkinson_Baseline

Ratio_3 = GK_Current / GK_Baseline

DVS_Ratio = Median(Ratio_1, Ratio_2, Ratio_3)

Why Ensemble?

Takes median to avoid outliers and false spikes

If ATR jumps but range-based methods stay calm, median prevents overreaction

If one method fails, other two compensate

Most robust approach across different market conditions

Sensitivity Scaling

Scaled_Ratio = (Raw_Ratio) ^ Sensitivity

Sensitivity 0.3: Cube root - heavily dampens volatility impact

Sensitivity 0.5: Square root - moderate dampening

Sensitivity 0.7 (Default): Balanced response to volatility changes

Sensitivity 1.0: Linear - full 1:1 volatility impact

Sensitivity 1.5: Exponential - amplified response to volatility spikes

Safety Clamps: Final DVS Ratio always clamped between 0.5x and 2.5x baseline to prevent extreme position sizing or stop placement errors.

How DVS Affects Shadow Trading

Every strategy's stop and target distances are multiplied by the current DVS ratio:

Stop Loss Distance:

Stop_Distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit Distance:

Target_Distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Example Scenario:

ATR = 10 points

Strategy's ATR_Mult gene = 2.5

Strategy's Stop_Mult gene = 1.5

Strategy's Target_Mult gene = 2.5

DVS_Ratio = 1.4 (40% above baseline volatility - market heating up)

Stop = 10 × 2.5 × 1.5 × 1.4 = 52.5 points (vs. 37.5 in normal vol)

Target = 10 × 2.5 × 2.5 × 1.4 = 87.5 points (vs. 62.5 in normal vol)

Result:

During volatility spikes: Stops automatically widen to avoid noise-based exits, targets extend for bigger moves

During calm periods: Stops tighten for better risk/reward, targets compress for realistic profit-taking

Strategies adapt risk management to match current market behavior

🧬 THE EVOLUTIONARY CYCLE: SPAWN, COMPETE, CULL

Initialization (Bar 1)

AGE begins with 4 seed strategies (if evolution enabled):

Seed Strategy #0 (Balanced):

All sensitivities at 1.0 (neutral)

Zero probability boost

Moderate trend requirement (0.4)

Standard ATR/stop/target multiples (2.5/1.5/2.5)

Mid-level regime adaptation (0.5)

Seed Strategy #1 (Momentum-Focused):

Lower entropy sensitivity (0.7), higher momentum (1.5)

Slight probability boost (+0.03)

Higher trend requirement (0.5)

Tighter stops (1.3), wider targets (3.0)

Seed Strategy #2 (Entropy-Driven):

Higher entropy sensitivity (1.5), lower momentum (0.8)

Slight probability penalty (-0.02)

More trend tolerant (0.6)

Wider stops (1.8), standard targets (2.5)

Seed Strategy #3 (Structure-Based):

Balanced entropy/momentum (0.8/0.9), high structure (1.4)

Slight probability boost (+0.02)

Lower trend requirement (0.35)

Moderate risk parameters (1.6/2.8)

All seeds start with WFO validation bypassed if WFO is disabled, or must validate if enabled.

Spawning New Strategies

Timing (Adaptive):

Historical phase: Every 30 bars (configurable 10-100)

Live phase: Every 200 bars (configurable 100-500)

Automatically switches to live timing when barstate.isrealtime triggers

Conditions:

Current population < max population limit (default: 8, configurable 4-12)

At least 2 active strategies exist (need parents)

Available slot in population array

Selection Process:

Run tournament selection 3 times with different seeds

Each tournament: randomly sample active strategies, pick highest fitness

Best from 3 tournaments becomes Parent 1

Repeat independently for Parent 2

Ensures fit parents but maintains diversity

Crossover Breeding:

For each of 10 genes:

Parent1_Fitness = fitness

Parent2_Fitness = fitness

Weight1 = Parent1_Fitness / (Parent1_Fitness + Parent2_Fitness)

Gene1 = parent1's value

Gene2 = parent2's value

Child_Gene = Weight1 × Gene1 + (1 - Weight1) × Gene2

Fitness-weighted crossover ensures fitter parent contributes more genetic material.

Mutation:

For each gene in child:

IF (random < mutation_rate):

Gene_Range = GENE_MAX - GENE_MIN

Noise = (random - 0.5) × 2 × mutation_strength × Gene_Range

Mutated_Gene = Clamp(Child_Gene + Noise, GENE_MIN, GENE_MAX)

Historical mutation rate: 20% (aggressive exploration)

Live mutation rate: 8% (conservative stability)

Mutation strength: 12% of gene range (configurable 5-25%)

Initialization of New Strategy:

Unique ID assigned (total_spawned counter)

Parent ID recorded

Generation = max(parent generations) + 1

Birth bar recorded (for age tracking)

All performance metrics zeroed

Shadow portfolio reset

WFO validation flag set to false (must prove itself)

Result: New strategy with hybrid DNA enters population, begins trading in next bar.

Competition (Every Bar)

All active strategies:

Calculate their signal based on unique DNA

Check quality gate with their thresholds

Manage shadow positions (entries/exits)

Update performance metrics

Recalculate fitness score

Track WFO validation progress

Strategies compete indirectly through fitness ranking - no direct interaction.

Culling Weak Strategies

Timing (Adaptive):

Historical phase: Every 60 bars (configurable 20-200, should be 2x spawn interval)

Live phase: Every 400 bars (configurable 200-1000, should be 2x spawn interval)

Minimum Adaptation Score (MAS):

Initial MAS = 0.10

MAS decays: MAS × 0.995 every cull cycle

Minimum MAS = 0.03 (floor)

MAS represents the "survival threshold" - strategies below this fitness level are vulnerable.

Culling Conditions (ALL must be true):

Population > minimum population (default: 3, configurable 2-4)

At least one strategy has fitness < MAS

Strategy's age > culling interval (prevents premature culling of new strategies)

Strategy is not in top N elite (default: 2, configurable 1-3)

Culling Process:

Find worst strategy:

For each active strategy:

IF (age > cull_interval):

Fitness = base_fitness

IF (not WFO_validated AND WFO_enabled):

Fitness × 0.7 // 30% penalty for unvalidated

IF (Fitness < MAS AND Fitness < worst_fitness_found):

worst_strategy = this_strategy

worst_fitness = Fitness

IF (worst_strategy found):

Count elite strategies with fitness > worst_fitness

IF (elite_count >= elite_preservation_count):

Deactivate worst_strategy (set active flag = false)

Increment total_culled counter

Elite Protection:

Even if a strategy's fitness falls below MAS, it survives if fewer than N strategies are better. This prevents culling when population is generally weak.

Result: Weak strategies removed from population, freeing slots for new spawns. Gene pool improves over time.

Selection for Display (Every Bar)

AGE chooses one strategy to display signals:

Best fitness = -1

Selected = none

For each active strategy:

Fitness = base_fitness

IF (WFO_validated):

Fitness × 1.3 // 30% bonus for validated strategies

IF (Fitness > best_fitness):

best_fitness = Fitness

selected_strategy = this_strategy

Display selected strategy's signals on chart

Result: Only the highest-fitness (optionally validated-boosted) strategy's signals appear as chart markers. Other strategies trade invisibly in shadow portfolios.

🎨 PREMIUM VISUALIZATION SYSTEM

AGE includes sophisticated visual feedback that standard indicators lack:

1. Gradient Probability Cloud (Optional, Default: ON)

Multi-layer gradient showing signal buildup 2-3 bars before entry:

Activation Conditions:

Signal persistence > 0 (same directional signal held for multiple bars)

Signal probability ≥ minimum threshold (65% by default)

Signal hasn't yet executed (still in "forming" state)

Visual Construction:

7 gradient layers by default (configurable 3-15)

Each layer is a line-fill pair (top line, bottom line, filled between)

Layer spacing: 0.3 to 1.0 × ATR above/below price

Outer layers = faint, inner layers = bright

Color transitions from base to intense based on layer position

Transparency scales with probability (high prob = more opaque)

Color Selection:

Long signals: Gradient from theme.gradient_bull_mid to theme.gradient_bull_strong

Short signals: Gradient from theme.gradient_bear_mid to theme.gradient_bear_strong

Base transparency: 92%, reduces by up to 8% for high-probability setups

Dynamic Behavior:

Cloud grows/shrinks as signal persistence increases/decreases

Redraws every bar while signal is forming

Disappears when signal executes or invalidates

Performance Note: Computationally expensive due to linefill objects. Disable or reduce layers if chart performance degrades.

2. Population Fitness Ribbon (Optional, Default: ON)

Histogram showing fitness distribution across active strategies:

Activation: Only draws on last bar (barstate.islast) to avoid historical clutter

Visual Construction:

10 histogram layers by default (configurable 5-20)

Plots 50 bars back from current bar

Positioned below price at: lowest_low(100) - 1.5×ATR (doesn't interfere with price action)

Each layer represents a fitness threshold (evenly spaced min to max fitness)

Layer Logic:

For layer_num from 0 to ribbon_layers:

Fitness_threshold = min_fitness + (max_fitness - min_fitness) × (layer / layers)

Count strategies with fitness ≥ threshold

Height = ATR × 0.15 × (count / total_active)

Y_position = base_level + ATR × 0.2 × layer

Color = Gradient from weak to strong based on layer position

Line_width = Scaled by height (taller = thicker)

Visual Feedback:

Tall, bright ribbon = healthy population, many fit strategies at high fitness levels

Short, dim ribbon = weak population, few strategies achieving good fitness

Ribbon compression (layers close together) = population converging to similar fitness

Ribbon spread = diverse fitness range, active selection pressure

Use Case: Quick visual health check without opening dashboard. Ribbon growing upward over time = population improving.

3. Confidence Halo (Optional, Default: ON)

Circular polyline around entry signals showing probability strength:

Activation: Draws when new position opens (shadow_position changes from 0 to ±1)

Visual Construction:

20-segment polyline forming approximate circle

Center: Low - 0.5×ATR (long) or High + 0.5×ATR (short)

Radius: 0.3×ATR (low confidence) to 1.0×ATR (elite confidence)

Scales with: (probability - min_probability) / (1.0 - min_probability)

Color Coding:

Elite (85%+): Cyan (theme.conf_elite), large radius, minimal transparency (40%)

Strong (75-85%): Strong green (theme.conf_strong), medium radius, moderate transparency (50%)

Good (65-75%): Good green (theme.conf_good), smaller radius, more transparent (60%)

Moderate (<65%): Moderate green (theme.conf_moderate), tiny radius, very transparent (70%)

Technical Detail:

Uses chart.point array with index-based positioning

5-bar horizontal spread for circular appearance (±5 bars from entry)

Curved=false (Pine Script polyline limitation)

Fill color matches line color but more transparent (88% vs line's transparency)

Purpose: Instant visual probability assessment. No need to check dashboard - halo size/brightness tells the story.

4. Evolution Event Markers (Optional, Default: ON)

Visual indicators of genetic algorithm activity:

Spawn Markers (Diamond, Cyan):

Plots when total_spawned increases on current bar

Location: bottom of chart (location.bottom)

Color: theme.spawn_marker (cyan/bright blue)

Size: tiny

Indicates new strategy just entered population

Cull Markers (X-Cross, Red):

Plots when total_culled increases on current bar

Location: bottom of chart (location.bottom)

Color: theme.cull_marker (red/pink)

Size: tiny

Indicates weak strategy just removed from population

What It Tells You:

Frequent spawning early = population building, active exploration

Frequent culling early = high selection pressure, weak strategies dying fast

Balanced spawn/cull = healthy evolutionary churn

No markers for long periods = stable population (evolution plateaued or optimal genes found)

5. Entry/Exit Markers

Clear visual signals for selected strategy's trades:

Long Entry (Triangle Up, Green):

Plots when selected strategy opens long position (position changes 0 → +1)

Location: below bar (location.belowbar)

Color: theme.long_primary (green/cyan depending on theme)

Transparency: Scales with probability:

Elite (85%+): 0% (fully opaque)

Strong (75-85%): 10%

Good (65-75%): 20%

Acceptable (55-65%): 35%

Size: small

Short Entry (Triangle Down, Red):

Plots when selected strategy opens short position (position changes 0 → -1)

Location: above bar (location.abovebar)

Color: theme.short_primary (red/pink depending on theme)

Transparency: Same scaling as long entries

Size: small

Exit (X-Cross, Orange):

Plots when selected strategy closes position (position changes ±1 → 0)

Location: absolute (at actual exit price if stop/target lines enabled)

Color: theme.exit_color (orange/yellow depending on theme)

Transparency: 0% (fully opaque)

Size: tiny

Result: Clean, probability-scaled markers that don't clutter chart but convey essential information.

6. Stop Loss & Take Profit Lines (Optional, Default: ON)

Visual representation of shadow portfolio risk levels:

Stop Loss Line:

Plots when selected strategy has active position

Level: shadow_stop value from selected strategy

Color: theme.short_primary with 60% transparency (red/pink, subtle)

Width: 2

Style: plot.style_linebr (breaks when no position)

Take Profit Line:

Plots when selected strategy has active position

Level: shadow_target value from selected strategy

Color: theme.long_primary with 60% transparency (green, subtle)

Width: 2

Style: plot.style_linebr (breaks when no position)

Purpose:

Shows where shadow portfolio would exit for stop/target

Helps visualize strategy's risk/reward ratio

Useful for manual traders to set similar levels

Disable for cleaner chart (recommended for presentations)

7. Dynamic Trend EMA

Gradient-colored trend line that visualizes trend strength:

Calculation:

EMA(close, trend_length) - default 50 period (configurable 20-100)

Slope calculated over 10 bars: (current_ema - ema ) / ema × 100

Color Logic:

Trend_direction:

Slope > 0.1% = Bullish (1)

Slope < -0.1% = Bearish (-1)

Otherwise = Neutral (0)

Trend_strength = abs(slope)

Color = Gradient between:

- Neutral color (gray/purple)

- Strong bullish (bright green) if direction = 1

- Strong bearish (bright red) if direction = -1

Gradient factor = trend_strength (0 to 1+ scale)

Visual Behavior:

Faint gray/purple = weak/no trend (choppy conditions)

Light green/red = emerging trend (low strength)

Bright green/red = strong trend (high conviction)

Color intensity = trend strength magnitude

Transparency: 50% (subtle, doesn't overpower price action)

Purpose: Subconscious awareness of trend state without checking dashboard or indicators.

8. Regime Background Tinting (Subtle)

Ultra-low opacity background color indicating detected market regime:

Regime Detection:

Efficiency = directional_movement / total_range (over trend_length bars)

Vol_ratio = current_volatility / average_volatility

IF (efficiency > 0.5 AND vol_ratio < 1.3):

Regime = Trending (1)

ELSE IF (vol_ratio > 1.5):

Regime = Volatile (2)

ELSE:

Regime = Choppy (0)

Background Colors:

Trending: theme.regime_trending (dark green, 92-93% transparency)

Volatile: theme.regime_volatile (dark red, 93% transparency)

Choppy: No tint (normal background)

Purpose:

Subliminal regime awareness

Helps explain why signals are/aren't generating

Trending = ideal conditions for AGE

Volatile = fewer signals, higher thresholds applied

Choppy = mixed signals, lower confidence

Important: Extremely subtle by design. Not meant to be obvious, just subconscious context.

📊 ENHANCED DASHBOARD

Comprehensive real-time metrics in single organized panel (top-right position):

Dashboard Structure (5 columns × 14 rows)

Header Row:

Column 0: "🧬 AGE PRO" + phase indicator (🔴 LIVE or ⏪ HIST)

Column 1: "POPULATION"

Column 2: "PERFORMANCE"

Column 3: "CURRENT SIGNAL"

Column 4: "ACTIVE STRATEGY"

Column 0: Market State

Regime (📈 TREND / 🌊 CHAOS / ➖ CHOP)

DVS Ratio (current volatility scaling factor, format: #.##)

Trend Direction (▲ BULL / ▼ BEAR / ➖ FLAT with color coding)

Trend Strength (0-100 scale, format: #.##)

Column 1: Population Metrics

Active strategies (count / max_population)

Validated strategies (WFO passed / active total)

Current generation number

Total spawned (all-time strategy births)

Total culled (all-time strategy deaths)

Column 2: Aggregate Performance

Total trades across all active strategies

Aggregate win rate (%) - color-coded:

Green (>55%)

Orange (45-55%)

Red (<45%)

Total P&L in R-multiples - color-coded by positive/negative

Best fitness score in population (format: #.###)

MAS - Minimum Adaptation Score (cull threshold, format: #.###)

Column 3: Current Signal Status

Status indicator:

"▲ LONG" (green) if selected strategy in long position

"▼ SHORT" (red) if selected strategy in short position

"⏳ FORMING" (orange) if signal persisting but not yet executed

"○ WAITING" (gray) if no active signal

Confidence percentage (0-100%, format: #.#%)

Quality assessment:

"🔥 ELITE" (cyan) for 85%+ probability

"✓ STRONG" (bright green) for 75-85%

"○ GOOD" (green) for 65-75%

"- LOW" (dim) for <65%

Confluence score (X/3 format)

Signal age:

"X bars" if signal forming

"IN TRADE" if position active

"---" if no signal

Column 4: Selected Strategy Details

Strategy ID number (#X format)

Validation status:

"✓ VAL" (green) if WFO validated

"○ TRAIN" (orange) if still in training/testing phase

Generation number (GX format)

Personal fitness score (format: #.### with color coding)

Trade count

P&L and win rate (format: #.#R (##%) with color coding)

Color Scheme:

Panel background: theme.panel_bg (dark, low opacity)

Panel headers: theme.panel_header (slightly lighter)

Primary text: theme.text_primary (bright, high contrast)

Secondary text: theme.text_secondary (dim, lower contrast)

Positive metrics: theme.metric_positive (green)

Warning metrics: theme.metric_warning (orange)

Negative metrics: theme.metric_negative (red)

Special markers: theme.validated_marker, theme.spawn_marker

Update Frequency: Only on barstate.islast (current bar) to minimize CPU usage

Purpose:

Quick overview of entire system state

No need to check multiple indicators

Trading decisions informed by population health, regime state, and signal quality

Transparency into what AGE is thinking

🔍 DIAGNOSTICS PANEL (Optional, Default: OFF)

Detailed signal quality tracking for optimization and debugging:

Panel Structure (3 columns × 8 rows)

Position: Bottom-right corner (doesn't interfere with main dashboard)

Header Row:

Column 0: "🔍 DIAGNOSTICS"

Column 1: "COUNT"

Column 2: "%"

Metrics Tracked (for selected strategy only):

Total Evaluated:

Every signal that passed initial calculation (direction ≠ 0)

Represents total opportunities considered

✓ Passed:

Signals that passed quality gate and executed

Green color coding

Percentage of evaluated signals

Rejection Breakdown:

⨯ Probability:

Rejected because probability < minimum threshold

Most common rejection reason typically

⨯ Confluence:

Rejected because confluence < minimum required (e.g., only 1 of 3 indicators agreed)

⨯ Trend:

Rejected because signal opposed strong trend

Indicates counter-trend protection working

⨯ Regime:

Rejected because volatile regime detected and probability wasn't high enough to override

Shows regime filter in action

⨯ Volume:

Rejected because volume < 70% of 20-bar average

Indicates volume confirmation requirement

Color Coding:

Passed count: Green (success metric)

Rejection counts: Red (failure metrics)

Percentages: Gray (neutral, informational)

Performance Cost: Slight CPU overhead for tracking counters. Disable when not actively optimizing settings.

How to Use Diagnostics

Scenario 1: Too Few Signals

Evaluated: 200

Passed: 10 (5%)

⨯ Probability: 120 (60%)

⨯ Confluence: 40 (20%)

⨯ Others: 30 (15%)

Diagnosis: Probability threshold too high for this strategy's DNA.

Solution: Lower min probability from 65% to 60%, or allow strategy more time to evolve better DNA.

Scenario 2: Too Many False Signals

Evaluated: 200

Passed: 80 (40%)

Strategy win rate: 45%

Diagnosis: Quality gate too loose, letting low-quality signals through.

Solution: Raise min probability to 70%, or increase min confluence to 3 (all indicators must agree).

Scenario 3: Regime-Specific Issues

⨯ Regime: 90 (45% of rejections)

Diagnosis: Frequent volatile regime detection blocking otherwise good signals.

Solution: Either accept fewer trades during chaos (recommended), or disable regime filter if you want signals regardless of market state.

Optimization Workflow:

Enable diagnostics

Run 200+ bars

Analyze rejection patterns

Adjust settings based on data

Re-run and compare pass rate

Disable diagnostics when satisfied

⚙️ CONFIGURATION GUIDE

🧬 Evolution Engine Settings

Enable AGE Evolution (Default: ON):

ON: Full genetic algorithm (recommended for best results)

OFF: Uses only 4 seed strategies, no spawning/culling (static population for comparison testing)

Max Population (4-12, Default: 8):

Higher = more diversity, more exploration, slower performance

Lower = faster computation, less exploration, risk of premature convergence

Sweet spot: 6-8 for most use cases

4 = minimum for meaningful evolution

12 = maximum before diminishing returns

Min Population (2-4, Default: 3):

Safety floor - system never culls below this count

Prevents population extinction during harsh selection

Should be at least half of max population

Elite Preservation (1-3, Default: 2):

Top N performers completely immune to culling

Ensures best genes always survive

1 = minimal protection, aggressive selection

2 = balanced (recommended)

3 = conservative, slower gene pool turnover

Historical: Spawn Interval (10-100, Default: 30):

Bars between spawning new strategies during historical data

Lower = faster evolution, more exploration

Higher = slower evolution, more evaluation time per strategy

30 bars = ~1-2 hours on 15min chart

Historical: Cull Interval (20-200, Default: 60):

Bars between culling weak strategies during historical data

Should be 2x spawn interval for balanced churn

Lower = aggressive selection pressure

Higher = patient evaluation

Live: Spawn Interval (100-500, Default: 200):

Bars between spawning during live trading

Much slower than historical for stability

Prevents population chaos during live trading

200 bars = ~1.5 trading days on 15min chart

Live: Cull Interval (200-1000, Default: 400):

Bars between culling during live trading

Should be 2x live spawn interval

Conservative removal during live trading

Historical: Mutation Rate (0.05-0.40, Default: 0.20):

Probability each gene mutates during breeding (20% = 2 out of 10 genes on average)

Higher = more exploration, slower convergence

Lower = more exploitation, faster convergence but risk of local optima

20% balances exploration vs exploitation

Live: Mutation Rate (0.02-0.20, Default: 0.08):

Mutation rate during live trading

Much lower for stability (don't want population to suddenly degrade)

8% = mostly inherits parent genes with small tweaks

Mutation Strength (0.05-0.25, Default: 0.12):

How much genes change when mutated (% of gene's total range)

0.05 = tiny nudges (fine-tuning)

0.12 = moderate jumps (recommended)

0.25 = large leaps (aggressive exploration)

Example: If gene range is 0.5-2.0, 12% strength = ±0.18 possible change

📈 Signal Quality Settings

Min Signal Probability (0.55-0.80, Default: 0.65):

Quality gate threshold - signals below this never generate

0.55-0.60 = More signals, accept lower confidence (higher risk)

0.65 = Institutional-grade balance (recommended)

0.70-0.75 = Fewer but higher-quality signals (conservative)

0.80+ = Very selective, very few signals (ultra-conservative)

Min Confluence Score (1-3, Default: 2):

Required indicator agreement before signal generates

1 = Any single indicator can trigger (not recommended - too many false signals)

2 = Requires 2 of 3 indicators agree (RECOMMENDED for balance)

3 = All 3 must agree (very selective, few signals, high quality)

Base Persistence Bars (1-5, Default: 2):

Base bars signal must persist before entry

System adapts automatically:

High probability signals (75%+) enter 1 bar faster

Low probability signals (<68%) need 1 bar more

Trending regime: -1 bar (faster entries)

Volatile regime: +1 bar (more confirmation)

1 = Immediate entry after quality gate (responsive but prone to whipsaw)

2 = Balanced confirmation (recommended)

3-5 = Patient confirmation (slower but more reliable)

Cooldown After Trade (3-20, Default: 8):

Bars to wait after exit before next entry allowed

Prevents overtrading and revenge trading

3 = Minimal cooldown (active trading)

8 = Balanced (recommended)

15-20 = Conservative (position trading)

Entropy Length (10-50, Default: 20):