Doji strategyThis is a simple strategy based on Doji star candlestick.

It places two orders: buy stop at doji star high or previous candle high and sell stop at doji star low or previous candle low.

Exit rules are with take profit and fixed stop loss or take profit and stop loss at doji min or max.

This strategy works very well with high time frames like Daily and Weekly because those are without noise in doji formation.

Each currency pair has its own optimal setting for TP and SL: it's up to user find the best ones.

I could implement SL based on ATR, maybe in next revision.

Please use comment section for any feedback.

Next improvement (only to whom is interested to this script and follows me): study with alerts on multiple tickers all at one. Leave a comment if you want to have access to study.

Tìm kiếm tập lệnh với "profit"

ATR and VIX For Profit Target and RSI LimitThe red line, based on ATR, should be used as a percentage gain goal. So I will set my profit targets based on this percentage.

The grey line is based on William's VIX and I use it to judge what RSI I should sell at.

RSI Multi Time Frame - Spot Panic Sell Moments and profit!Union of three RSI indicators: 1h, 4h and daily. In order to show 1h RSI, you have to set it as active time frame on the chart.

Purpose: spot "triple oversold" moments, where all the three RSI are under the threshold, which is 30 by default but editable.

Target Market: Cryptocurrencies. Didn't try it on other ones, may work as well. Fits Crypto well as, by experience, I can tell it usually doesn't stay oversold for long.

When the market panics and triple oversold occurs, the spot is highlighted by a green vertical bar on the indicator.

The indicator highlights triple overbought conditions as well (usually indicating strong FOMO), but I usually don't use it as a signal.

I suggest to edit the oversold threshold in order to make it fit the coin you're studying, minimizing false positives.

Special thanks to Heavy91, a Discord user, for inspiring me in this indicator.

Any editing proposal is welcome!

I reposted this script, as the first time I wrote it in Italian. Sorry for that.

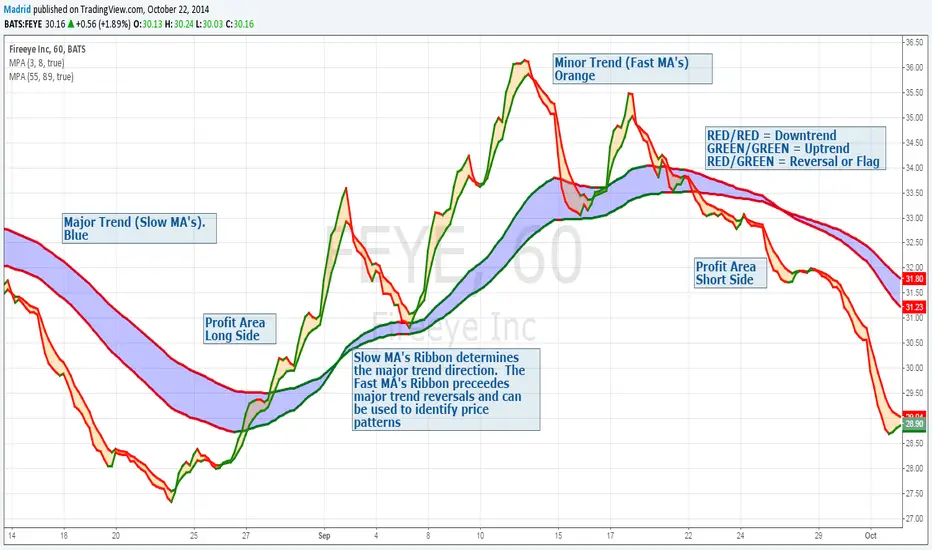

Madrid Profit AreaThis study displays a ribbon made of two moving averages identified by a filled Area. This provides visual aids to determine the trend direction and pivot points. The moving average will be Red if its value is decreasing, and green if it is increasing. When both MA's are the same color we have a trend direction. If those are different then we have a trend reversal and a pivot point.

If combined with another ribbon then it can be configured so we have a pair of slow MA's and another pair of fast MA's , this can visually determine if the price is in bull or bear territory following the basic rules:

1. Fast MA pair above the slow MA Pair = Bullish

2. Fast MA pair below the slow MA Pair = Bearish

3. If the fast MA crosses over the slow MA it is a Bullish reversal

4. If the fast MA crosses below the the slow MA, it is a Bearish reversal.

The use of the ribbons without the price bars or line reduces the noise inherent to the price

Opening Range Breakout with 2 Profit Targets.Opening Range Breakout with 2 Profit Targets.

Updated Indicator now works on all Symbols with Many Different Session Options.

***Known PineScript Issue…While the Opening Range is being Formed the lines only adjust for that individual bar. Just reset Indicator after Opening Range Completes.

***All Times are Based on New York Time

Session Options Forex U.S. Banks Open (8:00), Gold U.S. Open (8:20), Oil U.S. Open (9:00), U.S. Cash Session - Stocks (9:30), NY Forex Open (17:00) , Europe Open (02:00), or if you choose Setting 0 the Session Runs from 00:00 to 00:00 (Midnight to Midnight).

***Ability to use 60 minute Opening Range, 30 minute, 15 minute, and many other options.

***However you can manually change the times in the Inputs Tab to adjust for any session you prefer. This is useful for Day Light Savings Adjustments. Also the default times work if your charts are set to EST Time. If you use A different time zone in your settings you need to Adjust the times in the inputs tab.

Initially Opening Range High and Low plot as Yellow Lines. If Price Goes Above Opening Range then Line Turns Green. If Price Goes Below Opening Range Line Turns Red.

By default the First Profit Target is 1/2 the Width of the Opening Range and the 2nd Profit Target is 1 Times the Opening Range. However these are Adjustable in the Inputs Tab.

By Default the Opening Range Length is 1 Hour. However, you can Change the Opening Range Length to 15 min, 30 min, 2 hours etc. in the Inputs Tab.

Plots a 1 Above or Below Candle when 1st Profit Target is Achieved, and a 2 when 2nd Profit Target is Achieved.

ES/NQ Price Action Sync See when ES & NQ move in syncSee when ES & NQ move in sync — revealing real market momentum at a glance.”

⚖️ ES/NQ Price Action Sync

Discover when the market moves as one.

This indicator tracks when S&P 500 Futures (ES1!) and Nasdaq Futures (NQ1!) align in momentum — helping you spot broad-market confirmation or early divergence in real time.

🧠 Concept

The ES/NQ relationship often reveals the market’s underlying strength or hesitation. When both indices turn bullish or bearish together with meaningful movement, that’s a sign of true market alignment.

When they disagree — expect mixed momentum and possible reversals.

⚙️ Features

✅ Highlights new bullish and bearish syncs on chart

✅ Dynamic info table showing % change and direction for each index

✅ Optional triangle markers for clean visual cues

✅ Alert conditions for new sync events

✅ Adjustable lookback and minimum-move filters

💡 How to Use

Use this as a market-context tool, not a direct buy/sell signal.

When both indices sync, intraday trends often hold better; when they diverge, momentum may fade.

Combine it with your own system or higher-time-frame analysis for confirmation.

📊 Why Traders Love It

Simple idea — powerful insight.

This tool helps traders instantly see when “the market machine” is running in harmony… or pulling in opposite directions.

⚠️ Disclaimer:

This script is for educational and analytical purposes only.

It does not provide financial advice or trading signals. Always perform your own research before making trading decisions.

DIP BUYING by HAZEREAL BUY THE DIP - Educational Price Movement Indicator

This technical indicator is designed for educational purposes to help traders identify potential price reversal opportunities in equity markets, particularly focusing on NASDAQ-100 index tracking instruments and technology sector ETFs.

Key Features:

Monitors price movements relative to recent highs over customizable lookback periods

Identifies two distinct price decline thresholds: standard (5%+) and extreme (12.3%+)

Visual signals with triangular markers and background color zones

Real-time data table showing current metrics and status

Customizable alert system with webhook-ready JSON formatting

Clean overlay design that doesn't obstruct price action

How It Works:

The indicator tracks the highest price within a specified lookback period and calculates the percentage decline from that high. When price drops below the minimum threshold, it generates visual buy signals. The extreme threshold triggers enhanced alerts for more significant market movements.

Best Use Cases:

Educational analysis of market volatility patterns

Identifying potential support levels during market corrections

Studying historical price behavior around significant declines

Risk management and position sizing education

Important Note: This is a technical analysis tool for educational purposes only. All trading decisions should be based on comprehensive analysis and appropriate risk management. Past performance does not guarantee future results.

[ProfitTrailer:Feeder] VWAP %This script will help you create a strategy bases on VWAP % on BaseCoin & Top xx coin settings.

Enjoy & Like and follow if you like this kind of content.

[ProfitTrailer:Feeder] Market Trends Top X / BTCThis script will help you determine your MarketConditions Grouping for PtFeeder. You're able to input the specific top 10/20/xx pairs you want to use to fine-tune your groupings as well as specific BasePairs, there values will be automatically printed on the chart!

When measuring top coins trend, this is how many top coins to check by volume from the exchanges that you have configured PT Feeder for. For, the top 50 coins will be checked and their price change over the MeasureTimes property and the average change calculated. This average is used for the MaxTopCoinAverageChange property

If you like this kind of content, please 'like' and 'follow' and I'll continue publishing these kind of scripts!

Enjoy!

Profitable L 1800 Candle Highlight [Beta]

Certainly! Here's a user guide for the provided Pine Script code:

User Guide: 1800 Candle Highlight Indicator

Overview:

The "1800 Candle Highlight" indicator is designed to visually emphasize the 18:00 (6:00 PM) candle on the chart, providing clarity on its open and close prices, and highlighting its timeframe with a distinctive color.

Key Features:

Candle Highlighting: The indicator identifies the candle that opens at 18:00 and visually distinguishes it from other candles on the chart.

Open and Close Prices: The indicator plots the open and close prices of the 18:00 candle as step lines, making it easy to identify price movements during that timeframe.

Background Color: It colors the background within the 18:00 candle's timeframe with a transparent blue shade, providing further emphasis on that period.

Start Marker: A downward triangle shape marks the start of the 18:00 candle, aiding in identifying the beginning of the highlighted timeframe.

Usage:

Overlay: The indicator is designed to be overlaid on the price chart, allowing users to visualize the highlighted candle alongside price movements.

Interpretation: Traders can observe the open and close prices of the 18:00 candle relative to previous and subsequent candles, aiding in analysis and decision-making.

Timeframe Focus: The highlighted candle's timeframe can serve as a reference point for analyzing price action during specific hours, such as the end of a trading day.

Installation:

Access: Users can access the Pine Script editor within the TradingView platform to create a new indicator.

Copy and Paste: Copy the provided Pine Script code and paste it into the editor.

Save and Apply: Save the indicator and apply it to the desired chart, adjusting settings as needed.

Customization:

Color Scheme: Users can customize the colors used for highlighting, open/close prices, and background to suit their preferences and chart aesthetics.

Styling: Adjustments can be made to line styles, widths, and marker sizes to enhance visibility and clarity.

Compatibility:

The indicator is compatible with TradingView's Pine Script version 5 and can be applied to various financial instruments and timeframes supported by the platform.

Disclaimer:

The "1800 Candle Highlight" indicator is provided for informational purposes only and should not be considered as financial advice. Users are encouraged to conduct thorough analysis and consider multiple factors before making trading decisions.

Profitable Supertrend v0.1 - AlphaThis a script to try detect the best combination of supertrend parameters in a space of time. Sadly the script is slow. Evaluate all possibilities params is hard for a pinescript and my knowledge too. In some cases, when you want evaluate many time could be the script fails for timeout. Perhaps with time I could enhance. For this problem of speed the calculate of combinatios it's not complete: In factor use a increment of 0.2 in each param (0.1, 0.3, 0.5 ...) in period the increment for each value is 3. The range for factor it's from 3.0 to 12.0. The range of period it's from 10 to 43

My knowledge don't let me go more far. Perhaps with time I can enhance the script.

PMax on RSI with Tillson T3Profit Maximizer Indicator on RSI with Tillson T3 Moving Average:

PMax uses ATR calculation inside, for this reason users couldn't manage to use PMax on RSI because RSI indicator doesn't have High and Low values in bars, but ATR needs that values. So I personally calculate RSI in a different way to have High and Low values of RSI wrt price bars.

IMPORTANT:

Because of the sudden movements and divergences on RSI, this indicator must firstly optimized for the charts before using. Optimization can be held by users for the meaningful parameters for each chart.

3 parameters are critical when optimizing:

First: Multiplier

Second: Tillson T3 Length

Third: T3 Volume Factor

Here are some information about Profit Maximizer:

PMax Indicator:

PMax Screener and Strategy:

PMax Explorer STRATEGY & SCREENERProfit Maximizer - PMax Explorer STRATEGY & SCREENER screens the BUY and SELL signals (trend reversals) for 20 user defined different tickers in Tradingview charts.

Simply input the name of the ticker in Tradingview that you want to screen.

Terminology explanation:

Confirmed Reversal: PMax reversal that happened in the last bar and cannot be repainted.

Potential Reversal: PMax reversal that might happen in the current bar but can also not happen depending upon the timeframe closing price.

Downtrend: Tickers that are currently in the sell zone

Uptrend: Tickers that are currently in the buy zone

Screener has also got a built in PMax indicator which users can confirm the reversals on graphs.

Screener explores the 20 tickers in current graph's time frame and also in desired parameters of the SuperTrend indicator.

Also you can optimize the parameters manually with the built in STRATEGY version.

PMax indicator :

Profit Maximizer - PMax is a brand new indicator developed by me.

It's a combination of two trailing stop loss indicators;

One is Anıl Özekşi's MOST (Moving Stop Loss) Indicator

and the other one is well known ATR based SuperTrend

Profit Maximizer - PMax tries to solve this problem. PMax combines the powerful sides of MOST (Moving Average Trend Changer) and SuperTrend (ATR price detection) in one indicator.

Backtest and optimization results of PMax are far better when compared to its ancestors MOST and SuperTrend. It reduces the number of false signals in sideways and give more reliable trade signals.

PMax is easy to determine the trend and can be used in any type of markets and instruments. It does not repaint.

The first parameter in the PMax indicator set by the three parameters is the period/length of ATR.

The second Parameter is the Multiplier of ATR which would be useful to set the value of distance from the built in Moving Average.

I personally think the most important parameter is the Moving Average Length and type.

PMax will be much sensitive to trend movements if Moving Average Length is smaller. And vice versa, will be less sensitive when it is longer.

As the period increases it will become less sensitive to little trends and price actions.

In this way, your choice of period, will be closely related to which of the sort of trends you are interested in.

We are under the effect of the uptrend in cases where the Moving Average is above PMax;

conversely under the influence of a downward trend, when the Moving Average is below PMax.

Built in Moving Average type defaultly set as EMA but users can choose from 8 different Moving Average types like:

SMA : Simple Moving Average

EMA : Exponential Movin Average

WMA : Weighted Moving Average

TMA : Triangular Moving Average

VAR : Variable Index Dynamic Moving Average aka VIDYA

WWMA : Welles Wilder's Moving Average

ZLEMA : Zero Lag Exponential Moving Average

TSF : True Strength Force

Tip: In sideways VAR would be a good choice

You can use PMax default alarms and Buy Sell signals like:

1-

BUY when Moving Average crosses above PMax

SELL when Moving Average crosses under PMax

2-

BUY when prices jumps over PMax line.

SELL when prices go under PMax line.

McGinley Dynamic debugged🔍 McGinley Dynamic Debugged (Adaptive Moving Average)

This indicator plots the McGinley Dynamic, a mathematically adaptive moving average designed to reduce lag and better track price action during both trends and consolidations.

✅ Key Features:

Adaptive smoothing: The McGinley Dynamic adjusts itself based on the speed of price changes.

Lag reduction: Compared to traditional moving averages like EMA or SMA, McGinley provides smoother yet responsive tracking.

Stability fix: This version includes a robust fix for rare recursive calculation issues, particularly on low-priced historical assets (e.g., Wipro pre-2000).

⚙️ What’s Different in This Debugged Version?

Implements manual clamping on the source / previous value ratio to prevent mathematical spikes that could cause flattening or distortion in the plotted line.

Ensures more stable behavior across all instruments and timeframes, especially those with historically low price points or volatile early data.

💡 Use Case:

Ideal for:

Trend confirmation

Entry filtering

Adaptive support/resistance visualization

Improving signal precision in low-volatility or high-noise environments

⚠️ Notes:

Works best when combined with volume filters or other trend indicators for validation.

This version is optimized for visual use—for signal generation, consider pairing it with additional logic or thresholds.

PROFIT INDICATORFirst let me tell you which indicators have been used in this script so that you have the confidence while taking the trade:

(a) Bollinger Band with 20 SMA Inside it - Currently it is off, you can turn it on from settings.

(b) HMA 33, I have added the option of using two HMA's simultaneously. You can use HMA, EMA, SMA as per your settings and it would be color trending.

(c) VWAP- you can turn it on from settings

(d) CPR- you can turn it on from settings

(e) EMA's 20, 50, 200. Currently off, you can turn it on from settings.

(d) SMA's 50 and 200. Currently off, yu can turn it on from settings, if you want to use 20 SMA you can use bollinger band basis that is 20 period SMA.

(f) Trend bar at bottom on the basis of 50 EMA.

(g) Half Trend

(h) Trend strength Detector

(d) EMA 50 high and low to show the pac channel. I am not using this however as per request I have added this. Currently, it is trun on and you can turn it off from settings.

(f) Auto Fib levels

Please use a stick note for few days and mention imp notes before taking trade to check if all the conditions are matching to take the trade.

Buy Condition:-

1. Bolling band should be widely open.

2. Check the support and resistance from CPR. Candle should close above support in green.

3. Check the trend bar at bottom, it should be green, if it is grey in colour dont enter in trade.

4. Candle should be closing above EMA 50 and its upto you if you need additional confirmation, you can use EMA 20, 50, 200 and SMA 50 and 200, this is optional.

5. You can use VWAP as support or resistance and you can turn it on from settings.

6. Trending HMA of 33 should be in green for buy.

7. Half trend Indicator should give buy signal.

8. Trend Strength Indicator for checking the strength of the trend, if the arrow is big upside, you can go for buy.

9. Exit from buy trade when it start showing very small arrow which means trend is about to change.

10.Exit buy trade at 61.8 Fib level

Sell Condition:-

1. Bolling band should be widely open.

2. Check the support and resistance from CPR. Candle should close below resistance in red.

3. Check the trend bar at bottom, it should be red, if it is grey in colour dont enter in trade.

4. Candle should be closing below EMA 50 and its upto you if you need additional confirmation, you can use EMA 20, 50, 200 and SMA 50 and 200, this is optional.

5. You can use VWAP as support or resistance and you can turn it on from settings.

6. Trending HMA of 33 should be in red for sell.

7. Half trend Indicator should give sell signal.

8. Trend Strength Indicator for checking the strength of the trend, if the arrow is big downside, you can go for sell.

9. Exit from sell trade when down arrows start showing very small in size which means trend is about to change.

10.Exit sell trade at 61.8 Fib level

PMax on Rsi w/T3 *Strategy*Profit Maximizer Indicator on RSI with Tillson T3 Moving Average:

PMax uses ATR calculation inside, for this reason users couldn't manage to use PMax on RSI because RSI indicator doesn't have High and Low values in bars, but ATR needs that values. So I personally calculate RSI in a different way to have High and Low values of RSI wrt price bars.

IMPORTANT:

Because of the sudden movements and divergences on RSI , this indicator must firstly optimized for the charts before using. Optimization can be held by users for the meaningful parameters for each chart.

3 parameters are critical when optimizing:

First: Multiplier

Second: Tillson T3 Length

Third: T3 Volume Factor

Says, Kıvanç Özbilgiç. Here's the strategy version for you to backtest & optimize properly.

Enjoy.

$EURUSD 1 Minute Chart StrategyYou must be using the renko chart with traditional settings with the block size set at .0001. This can be done by going to settings. Style at the bottom should be changed from ATR to traditional. The set the block size as .0001.

Profit target areaUpdate.

- you can specify count of bars used to detect reversal pattern

- you can specify count of bars used to determine lowest or highest price to place support or resistance

- area between lines is filled by green - ascending, red - descending trend

To trade:

- open position using stop command on S/R

- close position using limit command on retracement line

- close position when background colour indicates trend change

(erratum: last balloon on right should say "buy limit")

XAUUSD 1-Minute Scalping Strategy - Advanced Strategy for ExitsThis is a **mean-reversion scalping strategy** optimized for **XAUUSD on the 1-minute (or the 5-minute) timeframe**. It combines a classic **RSI(14)** oscillator with an optional **200-period EMA trend filter** to identify short-term overextended conditions in gold price action, while enforcing fixed, conservative exits to maintain strict risk control.

### Core Logic & Why This Combination:

The strategy enters counter-trend when RSI reaches extreme levels (below 30 for longs, above 70 for shorts), capturing quick snap-backs that frequently occur in gold's intraday volatility.

- **RSI(14)** acts as the primary momentum filter — detecting oversold/overbought exhaustion.

- The **200 EMA trend filter** (enabled by default) adds directional context: longs are allowed only when price is above the EMA (overall uptrend bias), shorts only below it (downtrend bias). This reduces whipsaws in strong trending sessions and improves trade quality without overly restricting opportunities.

- Disabling the trend filter allows pure mean-reversion trading (useful in ranging/Asian sessions), but enabling it is strongly recommended for better expectancy in most market conditions.

Entries occur only when flat (no pyramiding), keeping the system clean and directional.

### Exit Rules (Fixed at Entry):

- **Take Profit**: +10 pips (0.10 in XAUUSD price terms)

- **Stop Loss**: -5 pips (0.05 in price terms)

- **Risk:Reward** = 1:2

Exits are **set once on the entry bar** using limit/stop orders — this prevents dynamic recalculation and mimics real broker behavior more closely. The 2:1 RR gives the strategy mathematical edge even with moderate win rates.

### Performance & Realism Guidelines:

This strategy is tuned for **high-frequency scalping** on gold, which typically produces hundreds to thousands of trades per year on 1-minute data.

Recommended **backtest/publication settings** (update these in the strategy properties before publishing):

- **Initial Capital**: $10,000 – $50,000 (realistic for retail prop/swing traders; the script defaults to $1,000,000 only for visual scaling — change it!)

- **Order Size**: Fixed 0.10–0.50 lots (adjust according to account size)

- **Commission**: 3–7 USD per round-turn lot (typical ECN/raw-spread gold commission on brokers like IC Markets, Pepperstone, etc.)

- **Slippage**: 2–5 ticks (≈0.02–0.05 in price) — gold can be slippery during news/volatility spikes on 1-minute charts

- **Pyramiding**: 1 (default — no stacking)

- **Dataset**: At minimum 1–3 years of 1-minute data (aim for >500–1000 closed trades for statistical significance)

With realistic costs applied, expect win rate ≈55–70%, profit factor >1.4–1.8 in favorable periods, but results vary significantly across trending vs. ranging regimes and news events.

**Risk per trade** remains very controlled (typically <0.5–1.5% depending on SL distance and position sizing) — never exceeds sustainable levels.

### Important Usage Notes:

- Check thoroughly the curve-fitted back tests.

- Gold is extremely volatile on 1-minute charts; check major news (NFP, FOMC, FED) unless you widen SL/TP dynamically (you can manually implement it here).

- Always forward-test on demo first and use proper position sizing.

- The built-in dashboard shows live stats (net P&L, win rate, profit factor, current RSI, position status, etc.) for quick monitoring.

- Restricted Sample Size for Precision

Happy scalping — trade responsibly! 🚀

Supertrend Advance Pullback StrategyHandbook for the Supertrend Advance Strategy

1. Introduction

Purpose of the Handbook:

The main purpose of this handbook is to serve as a comprehensive guide for traders and investors who are looking to explore and harness the potential of the Supertrend Advance Strategy. In the rapidly changing financial market, having the right tools and strategies at one's disposal is crucial. Whether you're a beginner hoping to dive into the world of trading or a seasoned investor aiming to optimize and diversify your portfolio, this handbook offers the insights and methodologies you need. By the end of this guide, readers should have a clear understanding of how the Supertrend Advance Strategy works, its benefits, potential pitfalls, and practical application in various trading scenarios.

Overview of the Supertrend Advance Pullback Strategy:

At its core, the Supertrend Advance Strategy is an evolution of the popular Supertrend Indicator. Designed to generate buy and sell signals in trending markets, the Supertrend Indicator has been a favorite tool for many traders around the world. The Advance Strategy, however, builds upon this foundation by introducing enhanced mechanisms, filters, and methodologies to increase precision and reduce false signals.

1. Basic Concept:

The Supertrend Advance Strategy relies on a combination of price action and volatility to determine the potential trend direction. By assessing the average true range (ATR) in conjunction with specific price points, this strategy aims to highlight the potential starting and ending points of market trends.

2. Methodology:

Unlike the traditional Supertrend Indicator, which primarily focuses on closing prices and ATR, the Advance Strategy integrates other critical market variables, such as volume, momentum oscillators, and perhaps even fundamental data, to validate its signals. This multidimensional approach ensures that the generated signals are more reliable and are less prone to market noise.

3. Benefits:

One of the main benefits of the Supertrend Advance Strategy is its ability to filter out false breakouts and minor price fluctuations, which can often lead to premature exits or entries in the market. By waiting for a confluence of factors to align, traders using this advanced strategy can increase their chances of entering or exiting trades at optimal points.

4. Practical Applications:

The Supertrend Advance Strategy can be applied across various timeframes, from intraday trading to swing trading and even long-term investment scenarios. Furthermore, its flexible nature allows it to be tailored to different asset classes, be it stocks, commodities, forex, or cryptocurrencies.

In the subsequent sections of this handbook, we will delve deeper into the intricacies of this strategy, offering step-by-step guidelines on its application, case studies, and tips for maximizing its efficacy in the volatile world of trading.

As you journey through this handbook, we encourage you to approach the Supertrend Advance Strategy with an open mind, testing and tweaking it as per your personal trading style and risk appetite. The ultimate goal is not just to provide you with a new tool but to empower you with a holistic strategy that can enhance your trading endeavors.

2. Getting Started

Navigating the financial markets can be a daunting task without the right tools. This section is dedicated to helping you set up the Supertrend Advance Strategy on one of the most popular charting platforms, TradingView. By following the steps below, you'll be able to integrate this strategy into your charts and start leveraging its insights in no time.

Setting up on TradingView:

TradingView is a web-based platform that offers a wide range of charting tools, social networking, and market data. Before you can apply the Supertrend Advance Strategy, you'll first need a TradingView account. If you haven't set one up yet, here's how:

1. Account Creation:

• Visit TradingView's official website.

• Click on the "Join for free" or "Sign up" button.

• Follow the registration process, providing the necessary details and setting up your login credentials.

2. Navigating the Dashboard:

• Once logged in, you'll be taken to your dashboard. Here, you'll see a variety of tools, including watchlists, alerts, and the main charting window.

• To begin charting, type in the name or ticker of the asset you're interested in the search bar at the top.

3. Configuring Chart Settings:

• Before integrating the Supertrend Advance Strategy, familiarize yourself with the chart settings. This can be accessed by clicking the 'gear' icon on the top right of the chart window.

• Adjust the chart type, time intervals, and other display settings to your preference.

Integrating the Strategy into a Chart:

Now that you're set up on TradingView, it's time to integrate the Supertrend Advance Strategy.

1. Accessing the Pine Script Editor:

• Located at the top-center of your screen, you'll find the "Pine Editor" tab. Click on it.

• This is where custom strategies and indicators are scripted or imported.

2. Loading the Supertrend Advance Strategy Script:

• Depending on whether you have the script or need to find it, there are two paths:

• If you have the script: Copy the Supertrend Advance Strategy script, and then paste it into the Pine Editor.

• If searching for the script: Click on the “Indicators” icon (looks like a flame) at the top of your screen, and then type “Supertrend Advance Strategy” in the search bar. If available, it will show up in the list. Simply click to add it to your chart.

3. Applying the Strategy:

• After pasting or selecting the Supertrend Advance Strategy in the Pine Editor, click on the “Add to Chart” button located at the top of the editor. This will overlay the strategy onto your main chart window.

4. Configuring Strategy Settings:

• Once the strategy is on your chart, you'll notice a small settings ('gear') icon next to its name in the top-left of the chart window. Click on this to access settings.

• Here, you can adjust various parameters of the Supertrend Advance Strategy to better fit your trading style or the specific asset you're analyzing.

5. Interpreting Signals:

• With the strategy applied, you'll now see buy/sell signals represented on your chart. Take time to familiarize yourself with how these look and behave over various timeframes and market conditions.

3. Strategy Overview

What is the Supertrend Advance Strategy?

The Supertrend Advance Strategy is a refined version of the classic Supertrend Indicator, which was developed to aid traders in spotting market trends. The strategy utilizes a combination of data points, including average true range (ATR) and price momentum, to generate buy and sell signals.

In essence, the Supertrend Advance Strategy can be visualized as a line that moves with the price. When the price is above the Supertrend line, it indicates an uptrend and suggests a potential buy position. Conversely, when the price is below the Supertrend line, it hints at a downtrend, suggesting a potential selling point.

Strategy Goals and Objectives:

1. Trend Identification: At the core of the Supertrend Advance Strategy is the goal to efficiently and consistently identify prevailing market trends. By recognizing these trends, traders can position themselves to capitalize on price movements in their favor.

2. Reducing Noise: Financial markets are often inundated with 'noise' - short-term price fluctuations that can mislead traders. The Supertrend Advance Strategy aims to filter out this noise, allowing for clearer decision-making.

3. Enhancing Risk Management: With clear buy and sell signals, traders can set more precise stop-loss and take-profit points. This leads to better risk management and potentially improved profitability.

4. Versatility: While primarily used for trend identification, the strategy can be integrated with other technical tools and indicators to create a comprehensive trading system.

Type of Assets/Markets to Apply the Strategy:

1. Equities: The Supertrend Advance Strategy is highly popular among stock traders. Its ability to capture long-term trends makes it particularly useful for those trading individual stocks or equity indices.

2. Forex: Given the 24-hour nature of the Forex market and its propensity for trends, the Supertrend Advance Strategy is a valuable tool for currency traders.

3. Commodities: Whether it's gold, oil, or agricultural products, commodities often move in extended trends. The strategy can help in identifying and capitalizing on these movements.

4. Cryptocurrencies: The volatile nature of cryptocurrencies means they can have pronounced trends. The Supertrend Advance Strategy can aid crypto traders in navigating these often tumultuous waters.

5. Futures & Options: Traders and investors in derivative markets can utilize the strategy to make more informed decisions about contract entries and exits.

It's important to note that while the Supertrend Advance Strategy can be applied across various assets and markets, its effectiveness might vary based on market conditions, timeframe, and the specific characteristics of the asset in question. As always, it's recommended to use the strategy in conjunction with other analytical tools and to backtest its effectiveness in specific scenarios before committing to trades.

4. Input Settings

Understanding and correctly configuring input settings is crucial for optimizing the Supertrend Advance Strategy for any specific market or asset. These settings, when tweaked correctly, can drastically impact the strategy's performance.

Grouping Inputs:

Before diving into individual input settings, it's important to group similar inputs. Grouping can simplify the user interface, making it easier to adjust settings related to a specific function or indicator.

Strategy Choice:

This input allows traders to select from various strategies that incorporate the Supertrend indicator. Options might include "Supertrend with RSI," "Supertrend with MACD," etc. By choosing a strategy, the associated input settings for that strategy become available.

Supertrend Settings:

1. Multiplier: Typically, a default value of 3 is used. This multiplier is used in the ATR calculation. Increasing it makes the Supertrend line further from prices, while decreasing it brings the line closer.

2. Period: The number of bars used in the ATR calculation. A common default is 7.

EMA Settings (Exponential Moving Average):

1. Period: Defines the number of previous bars used to calculate the EMA. Common periods are 9, 21, 50, and 200.

2. Source: Allows traders to choose which price (Open, Close, High, Low) to use in the EMA calculation.

RSI Settings (Relative Strength Index):

1. Length: Determines how many periods are used for RSI calculation. The standard setting is 14.

2. Overbought Level: The threshold at which the asset is considered overbought, typically set at 70.

3. Oversold Level: The threshold at which the asset is considered oversold, often at 30.

MACD Settings (Moving Average Convergence Divergence):

1. Short Period: The shorter EMA, usually set to 12.

2. Long Period: The longer EMA, commonly set to 26.

3. Signal Period: Defines the EMA of the MACD line, typically set at 9.

CCI Settings (Commodity Channel Index):

1. Period: The number of bars used in the CCI calculation, often set to 20.

2. Overbought Level: Typically set at +100, denoting overbought conditions.

3. Oversold Level: Usually set at -100, indicating oversold conditions.

SL/TP Settings (Stop Loss/Take Profit):

1. SL Multiplier: Defines the multiplier for the average true range (ATR) to set the stop loss.

2. TP Multiplier: Defines the multiplier for the average true range (ATR) to set the take profit.

Filtering Conditions:

This section allows traders to set conditions to filter out certain signals. For example, one might only want to take buy signals when the RSI is below 30, ensuring they buy during oversold conditions.

Trade Direction and Backtest Period:

1. Trade Direction: Allows traders to specify whether they want to take long trades, short trades, or both.

2. Backtest Period: Specifies the time range for backtesting the strategy. Traders can choose from options like 'Last 6 months,' 'Last 1 year,' etc.

It's essential to remember that while default settings are provided for many of these tools, optimal settings can vary based on the market, timeframe, and trading style. Always backtest new settings on historical data to gauge their potential efficacy.

5. Understanding Strategy Conditions

Developing an understanding of the conditions set within a trading strategy is essential for traders to maximize its potential. Here, we delve deep into the logic behind these conditions, using the Supertrend Advance Strategy as our focal point.

Basic Logic Behind Conditions:

Every strategy is built around a set of conditions that provide buy or sell signals. The conditions are based on mathematical or statistical methods and are rooted in the study of historical price data. The fundamental idea is to recognize patterns or behaviors that have been profitable in the past and might be profitable in the future.

Buy and Sell Conditions:

1. Buy Conditions: Usually formulated around bullish signals or indicators suggesting upward price momentum.

2. Sell Conditions: Centered on bearish signals or indicators indicating downward price momentum.

Simple Strategy:

The simple strategy could involve using just the Supertrend indicator. Here:

• Buy: When price closes above the Supertrend line.

• Sell: When price closes below the Supertrend line.

Pullback Strategy:

This strategy capitalizes on price retracements:

• Buy: When the price retraces to the Supertrend line after a bullish signal and is supported by another bullish indicator.

• Sell: When the price retraces to the Supertrend line after a bearish signal and is confirmed by another bearish indicator.

Indicators Used:

EMA (Exponential Moving Average):

• Logic: EMA gives more weight to recent prices, making it more responsive to current price movements. A shorter-period EMA crossing above a longer-period EMA can be a bullish sign, while the opposite is bearish.

RSI (Relative Strength Index):

• Logic: RSI measures the magnitude of recent price changes to analyze overbought or oversold conditions. Values above 70 are typically considered overbought, and values below 30 are considered oversold.

MACD (Moving Average Convergence Divergence):

• Logic: MACD assesses the relationship between two EMAs of a security’s price. The MACD line crossing above the signal line can be a bullish signal, while crossing below can be bearish.

CCI (Commodity Channel Index):

• Logic: CCI compares a security's average price change with its average price variation. A CCI value above +100 may mean the price is overbought, while below -100 might signify an oversold condition.

And others...

As the strategy expands or contracts, more indicators might be added or removed. The crucial point is to understand the core logic behind each, ensuring they align with the strategy's objectives.

Logic Behind Each Indicator:

1. EMA: Emphasizes recent price movements; provides dynamic support and resistance levels.

2. RSI: Indicates overbought and oversold conditions based on recent price changes.

3. MACD: Showcases momentum and direction of a trend by comparing two EMAs.

4. CCI: Measures the difference between a security's price change and its average price change.

Understanding strategy conditions is not just about knowing when to buy or sell but also about comprehending the underlying market dynamics that those conditions represent. As you familiarize yourself with each condition and indicator, you'll be better prepared to adapt and evolve with the ever-changing financial markets.

6. Trade Execution and Management

Trade execution and management are crucial aspects of any trading strategy. Efficient execution can significantly impact profitability, while effective management can preserve capital during adverse market conditions. In this section, we'll explore the nuances of position entry, exit strategies, and various Stop Loss (SL) and Take Profit (TP) methodologies within the Supertrend Advance Strategy.

Position Entry:

Effective trade entry revolves around:

1. Timing: Enter at a point where the risk-reward ratio is favorable. This often corresponds to confirmatory signals from multiple indicators.

2. Volume Analysis: Ensure there's adequate volume to support the movement. Volume can validate the strength of a signal.

3. Confirmation: Use multiple indicators or chart patterns to confirm the entry point. For instance, a buy signal from the Supertrend indicator can be confirmed with a bullish MACD crossover.

Position Exit Strategies:

A successful exit strategy will lock in profits and minimize losses. Here are some strategies:

1. Fixed Time Exit: Exiting after a predetermined period.

2. Percentage-based Profit Target: Exiting after a certain percentage gain.

3. Indicator-based Exit: Exiting when an indicator gives an opposing signal.

Percentage-based SL/TP:

• Stop Loss (SL): Set a fixed percentage below the entry price to limit potential losses.

• Example: A 2% SL on an entry at $100 would trigger a sell at $98.

• Take Profit (TP): Set a fixed percentage above the entry price to lock in gains.

• Example: A 5% TP on an entry at $100 would trigger a sell at $105.

Supertrend-based SL/TP:

• Stop Loss (SL): Position the SL at the Supertrend line. If the price breaches this line, it could indicate a trend reversal.

• Take Profit (TP): One could set the TP at a point where the Supertrend line flattens or turns, indicating a possible slowdown in momentum.

Swing high/low-based SL/TP:

• Stop Loss (SL): For a long position, set the SL just below the recent swing low. For a short position, set it just above the recent swing high.

• Take Profit (TP): For a long position, set the TP near a recent swing high or resistance. For a short position, near a swing low or support.

And other methods...

1. Trailing Stop Loss: This dynamic SL adjusts with the price movement, locking in profits as the trade moves in your favor.

2. Multiple Take Profits: Divide the position into segments and set multiple TP levels, securing profits in stages.

3. Opposite Signal Exit: Exit when another reliable indicator gives an opposite signal.

Trade execution and management are as much an art as they are a science. They require a blend of analytical skill, discipline, and intuition. Regularly reviewing and refining your strategies, especially in light of changing market conditions, is crucial to maintaining consistent trading performance.

7. Visual Representations

Visual tools are essential for traders, as they simplify complex data into an easily interpretable format. Properly analyzing and understanding the plots on a chart can provide actionable insights and a more intuitive grasp of market conditions. In this section, we’ll delve into various visual representations used in the Supertrend Advance Strategy and their significance.

Understanding Plots on the Chart:

Charts are the primary visual aids for traders. The arrangement of data points, lines, and colors on them tell a story about the market's past, present, and potential future moves.

1. Data Points: These represent individual price actions over a specific timeframe. For instance, a daily chart will have data points showing the opening, closing, high, and low prices for each day.

2. Colors: Used to indicate the nature of price movement. Commonly, green is used for bullish (upward) moves and red for bearish (downward) moves.

Trend Lines:

Trend lines are straight lines drawn on a chart that connect a series of price points. Their significance:

1. Uptrend Line: Drawn along the lows, representing support. A break below might indicate a trend reversal.

2. Downtrend Line: Drawn along the highs, indicating resistance. A break above might suggest the start of a bullish trend.

Filled Areas:

These represent a range between two values on a chart, usually shaded or colored. For instance:

1. Bollinger Bands: The area between the upper and lower band is filled, giving a visual representation of volatility.

2. Volume Profile: Can show a filled area representing the amount of trading activity at different price levels.

Stop Loss and Take Profit Lines:

These are horizontal lines representing pre-determined exit points for trades.

1. Stop Loss Line: Indicates the level at which a trade will be automatically closed to limit losses. Positioned according to the trader's risk tolerance.

2. Take Profit Line: Denotes the target level to lock in profits. Set according to potential resistance (for long trades) or support (for short trades) or other technical factors.

Trailing Stop Lines:

A trailing stop is a dynamic form of stop loss that moves with the price. On a chart:

1. For Long Trades: Starts below the entry price and moves up with the price but remains static if the price falls, ensuring profits are locked in.

2. For Short Trades: Starts above the entry price and moves down with the price but remains static if the price rises.

Visual representations offer traders a clear, organized view of market dynamics. Familiarity with these tools ensures that traders can quickly and accurately interpret chart data, leading to more informed decision-making. Always ensure that the visual aids used resonate with your trading style and strategy for the best results.

8. Backtesting

Backtesting is a fundamental process in strategy development, enabling traders to evaluate the efficacy of their strategy using historical data. It provides a snapshot of how the strategy would have performed in past market conditions, offering insights into its potential strengths and vulnerabilities. In this section, we'll explore the intricacies of setting up and analyzing backtest results and the caveats one must be aware of.

Setting Up Backtest Period:

1. Duration: Determine the timeframe for the backtest. It should be long enough to capture various market conditions (bullish, bearish, sideways). For instance, if you're testing a daily strategy, consider a period of several years.

2. Data Quality: Ensure the data source is reliable, offering high-resolution and clean data. This is vital to get accurate backtest results.

3. Segmentation: Instead of a continuous period, sometimes it's helpful to backtest over distinct market phases, like a particular bear or bull market, to see how the strategy holds up in different environments.

Analyzing Backtest Results:

1. Performance Metrics: Examine metrics like the total return, annualized return, maximum drawdown, Sharpe ratio, and others to gauge the strategy's efficiency.

2. Win Rate: It's the ratio of winning trades to total trades. A high win rate doesn't always signify a good strategy; it should be evaluated in conjunction with other metrics.

3. Risk/Reward: Understand the average profit versus the average loss per trade. A strategy might have a low win rate but still be profitable if the average gain far exceeds the average loss.

4. Drawdown Analysis: Review the periods of losses the strategy could incur and how long it takes, on average, to recover.

9. Tips and Best Practices

Successful trading requires more than just knowing how a strategy works. It necessitates an understanding of when to apply it, how to adjust it to varying market conditions, and the wisdom to recognize and avoid common pitfalls. This section offers insightful tips and best practices to enhance the application of the Supertrend Advance Strategy.

When to Use the Strategy:

1. Market Conditions: Ideally, employ the Supertrend Advance Strategy during trending market conditions. This strategy thrives when there are clear upward or downward trends. It might be less effective during consolidative or sideways markets.

2. News Events: Be cautious around significant news events, as they can cause extreme volatility. It might be wise to avoid trading immediately before and after high-impact news.

3. Liquidity: Ensure you are trading in assets/markets with sufficient liquidity. High liquidity ensures that the price movements are more reflective of genuine market sentiment and not due to thin volume.

Adjusting Settings for Different Markets/Timeframes:

1. Markets: Each market (stocks, forex, commodities) has its own characteristics. It's essential to adjust the strategy's parameters to align with the market's volatility and liquidity.

2. Timeframes: Shorter timeframes (like 1-minute or 5-minute charts) tend to have more noise. You might need to adjust the settings to filter out false signals. Conversely, for longer timeframes (like daily or weekly charts), you might need to be more responsive to genuine trend changes.

3. Customization: Regularly review and tweak the strategy's settings. Periodic adjustments can ensure the strategy remains optimized for the current market conditions.

10. Frequently Asked Questions (FAQs)

Given the complexities and nuances of the Supertrend Advance Strategy, it's only natural for traders, both new and seasoned, to have questions. This section addresses some of the most commonly asked questions regarding the strategy.

1. What exactly is the Supertrend Advance Strategy?

The Supertrend Advance Strategy is an evolved version of the traditional Supertrend indicator. It's designed to provide clearer buy and sell signals by incorporating additional indicators like EMA, RSI, MACD, CCI, etc. The strategy aims to capitalize on market trends while minimizing false signals.

2. Can I use the Supertrend Advance Strategy for all asset types?

Yes, the strategy can be applied to various asset types like stocks, forex, commodities, and cryptocurrencies. However, it's crucial to adjust the settings accordingly to suit the specific characteristics and volatility of each asset type.

3. Is this strategy suitable for day trading?

Absolutely! The Supertrend Advance Strategy can be adjusted to suit various timeframes, making it versatile for both day trading and long-term trading. Remember to fine-tune the settings to align with the timeframe you're trading on.

4. How do I deal with false signals?

No strategy is immune to false signals. However, by combining the Supertrend with other indicators and adhering to strict risk management protocols, you can minimize the impact of false signals. Always use stop-loss orders and consider filtering trades with additional confirmation signals.

5. Do I need any prior trading experience to use this strategy?

While the Supertrend Advance Strategy is designed to be user-friendly, having a foundational understanding of trading and market analysis can greatly enhance your ability to employ the strategy effectively. If you're a beginner, consider pairing the strategy with further education and practice on demo accounts.

6. How often should I review and adjust the strategy settings?

There's no one-size-fits-all answer. Some traders adjust settings weekly, while others might do it monthly. The key is to remain responsive to changing market conditions. Regular backtesting can give insights into potential required adjustments.

7. Can the Supertrend Advance Strategy be automated?

Yes, many traders use algorithmic trading platforms to automate their strategies, including the Supertrend Advance Strategy. However, always monitor automated systems regularly to ensure they're operating as intended.

8. Are there any markets or conditions where the strategy shouldn't be used?

The strategy might generate more false signals in markets that are consolidative or range-bound. During significant news events or times of unexpected high volatility, it's advisable to tread with caution or stay out of the market.

9. How important is backtesting with this strategy?

Backtesting is crucial as it allows traders to understand how the strategy would have performed in the past, offering insights into potential profitability and areas of improvement. Always backtest any new setting or tweak before applying it to live trades.

10. What if the strategy isn't working for me?

No strategy guarantees consistent profits. If it's not working for you, consider reviewing your settings, seeking expert advice, or complementing the Supertrend Advance Strategy with other analysis methods. Remember, continuous learning and adaptation are the keys to trading success.

Other comments

Value of combining several indicators in this script and how they work together

Diversification of Signals: Just as diversifying an investment portfolio can reduce risk, using multiple indicators can offer varied perspectives on potential price movements. Each indicator can capture a different facet of the market, ensuring that traders are not overly reliant on a single data point.

Confirmation & Reduced False Signals: A common challenge with many indicators is the potential for false signals. By requiring confirmation from multiple indicators before acting, the chances of acting on a false signal can be significantly reduced.

Flexibility Across Market Conditions: Different indicators might perform better under different market conditions. For example, while moving averages might excel in trending markets, oscillators like RSI might be more useful during sideways or range-bound conditions. A mashup strategy can potentially adapt better to varying market scenarios.

Comprehensive Analysis: With multiple indicators, traders can gauge trend strength, momentum, volatility, and potential market reversals all at once, providing a holistic view of the market.

How do the different indicators in the Supertrend Advance Strategy work together?

Supertrend: This is primarily a trend-following indicator. It provides traders with buy and sell signals based on the volatility of the price. When combined with other indicators, it can filter out noise and give more weight to strong, confirmed trends.

EMA (Exponential Moving Average): EMA gives more weight to recent price data. It can be used to identify the direction and strength of a trend. When the price is above the EMA, it's generally considered bullish, and vice versa.

RSI (Relative Strength Index): An oscillator that measures the magnitude of recent price changes to evaluate overbought or oversold conditions. By cross-referencing with other indicators like EMA or MACD, traders can spot potential reversals or confirmations of a trend.

MACD (Moving Average Convergence Divergence): This indicator identifies changes in the strength, direction, momentum, and duration of a trend in a stock's price. When the MACD line crosses above the signal line, it can be a bullish sign, and when it crosses below, it can be bearish. Pairing MACD with Supertrend can provide dual confirmation of a trend.

CCI (Commodity Channel Index): Initially developed for commodities, CCI can indicate overbought or oversold conditions. It can be used in conjunction with other indicators to determine entry and exit points.

In essence, the synergy of these indicators provides a balanced, comprehensive approach to trading. Each indicator offers its unique lens into market conditions, and when they align, it can be a powerful indication of a trading opportunity. This combination not only reduces the potential drawbacks of each individual indicator but leverages their strengths, aiming for more consistent and informed trading decisions.

Backtesting and Default Settings

• This indicator has been optimized to be applied for 1 hour-charts. However, the underlying principles of this strategy are supply and demand in the financial markets and the strategy can be applied to all timeframes. Daytraders can use the 1min- or 5min charts, swing-traders can use the daily charts.

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The combination of the qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

• Default properties: RSI on (length 14, RSI buy level 50, sell level 50), EMA, RSI, MACD on, type of strategy pullback, SL/TP type: ATR (length 10, factor 3), trade direction both, quantity 5, take profit swing hl 5.1, highest / lowest lookback 2, enable ATR trail (ATR length 10, SL ATR multiplier 1.4, TP multiplier 2.1, lookback = 4, trade direction = both).