Tìm kiếm tập lệnh với "session"

NY Session open 9:30 and bond market close at 15:00NY Session open 9.30 and bond market close at 15:00

xmtr's session highs/lowsMarks Asia & London session highs/lows with precision + PDH/PDL for daily context. Fully customizable & perfect for all traders.

NY Session Open Levels This indicator automatically draws horizontal lines at the opening prices of the New York trading session at 08:30, 09:30, and 10:00 AM NY time. Each line is labeled and extended to the right, providing clear reference points for key intraday levels. The lines and labels reset daily and are ideal for identifying reaction zones during the early U.S. trading hours.

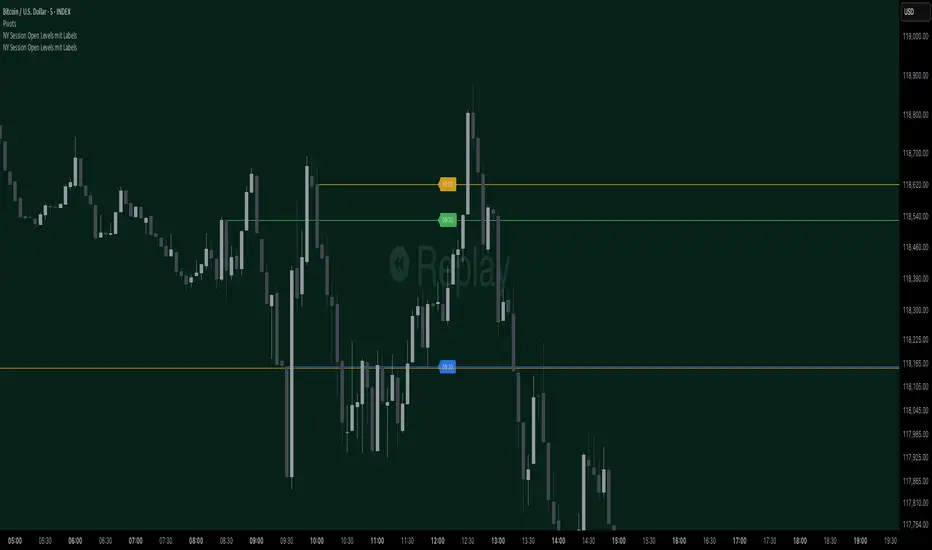

NY Session Open Levels mit LabelsThis indicator automatically draws horizontal lines at the opening prices of the New York trading session at 08:30, 09:30, and 10:00 AM NY time. Each line is labeled and extended to the right, providing clear reference points for key intraday levels. The lines and labels reset daily and are ideal for identifying reaction zones during the early U.S. trading hours.

Nikkei Session Key Levels Lines (with Labels) - Nikkei CFDThis is Nikkei Session Key Levels Lines (with Labels) - Nikkei CFD. shows you all the key level lines that you need to be aware. hope it helps :)

Nikkei Session Prep (RTH only, UTC-4)This is Nikkei Session Prep (RTH only, UTC-4). hope it helps :)

Night Session Highlight (Valehson)Highlights time range from 21:00 to 09:00 with a gray background with 90% transparency.

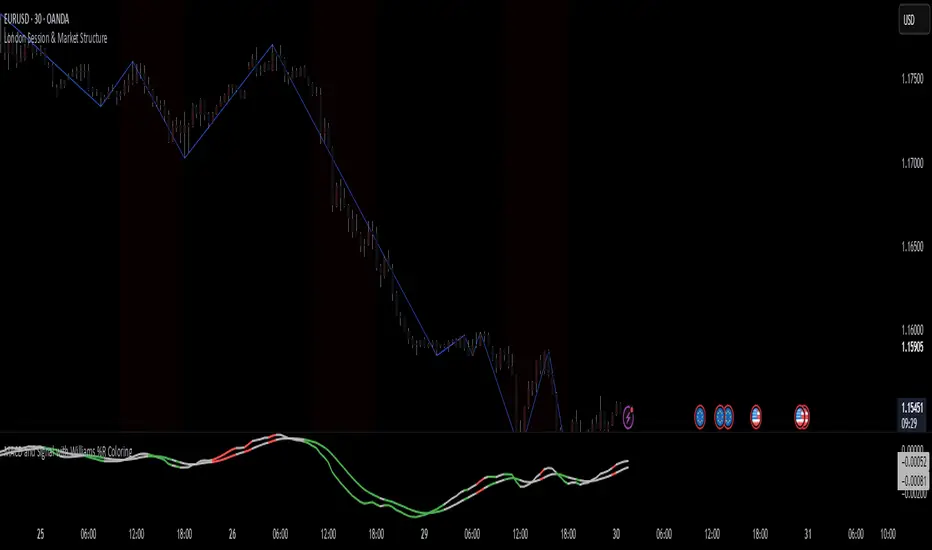

London Session & Market StructureFusion of session indicator with market structure ZigZag line. not my own creation just a fusion of 2 indicators which are publicly available on TV

Asian & London Session Two-Color Candlesthis script use to find the asian and london session with different candle colours.

5m Gold Strategy - Session Break + Previous Day High/LowHere is your complete Pine Script v5 code for TradingView that:

Implements your 5-minute Gold breakout strategy.

Uses previous day high/low levels.

Confirms entry based on 15-minute SMA trend (SMA 9 > SMA 21).

Marks session time.

Filters news time (pause trading 15 minutes before/after major red news from ForexFactory).

PH Night Session HighlightTraders who want to visually separate the night session on their charts. It highlights the period from 8:01 PM to 7:59 AM (Philippine Time), making it easy to distinguish off-hours or pre-market activity, especially when analyzing crypto or 24/7 markets.

The script automatically adjusts server time (UTC) to Philippine Time (UTC+8) and overlays a soft blue background during the specified time window.

Clube 369 LTA Concepts: Session Breaks & NYSE, Sunday OpenThe "Limitless LTA: Session Breaks & Sunday Open" indicator is a simple tool designed to help traders better understand market timing and track the opening price of the trading week. Here's what you need to know:

What It Does:

Displays vertical lines on the chart to mark specific times of interest, usually 18:00 PM UTC-5 over the last four days.

Plots a line representing the price of the first candle of the trading week, typically on a Sunday.

Customization:

Users can customize the appearance of the vertical lines by adjusting style, width, and color preferences.

Benefits:

Provides a visual reference for significant timestamps and the Sunday open price.

Helps traders understand market sentiment and potential trends.

In summary, the "Limitless Timestamp & Sunday Open" indicator is an accessible tool for traders to track important market timings and price movements, enhancing market analysis and decision-making.

Sunday Open Fixed on all timeframes.

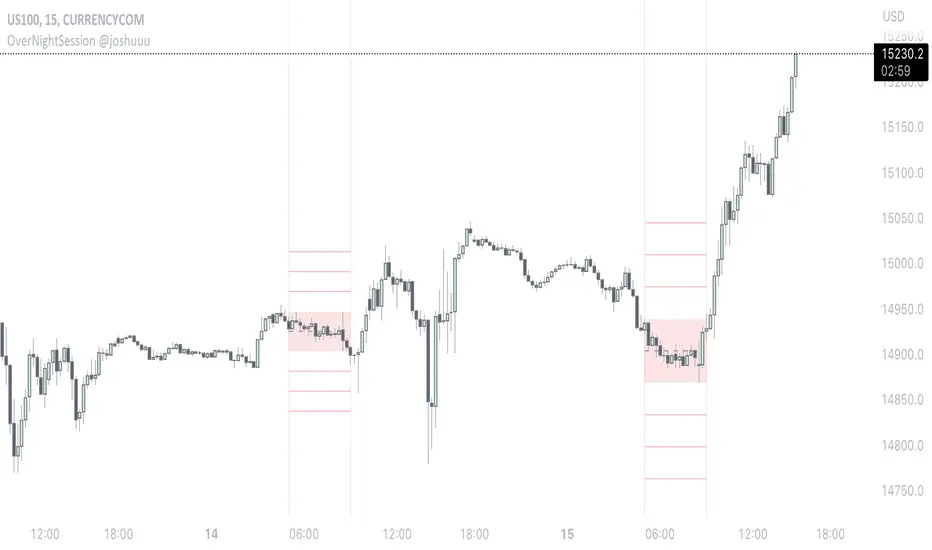

OverNightSession @joshuuuThis indicator highlights the Overnightsession (ONS), taught by TheCurrenyMerchant.

The Overnightsession is from 4-8 am UTC-5. This session can be used to form trades, e.g. after one side has been taken out.

It has the options to display Projection and the equilibrium level. Equilibrium level (50%) can be used to identify if price is currently in premium/discount of the range and the projections (standard deviations of the range) can be used to identify possible targets.

A classic setup he teaches is:

Price trades agressively out of the range taking liquidity. As soon as we trade above the high of the candle that took liquidity, that candle can be considered an orderblock, where the 50% level can be used for long setups.

⚠️ Open Source ⚠️

Coders and TV users are authorized to copy this code base, but a paid distribution is prohibited. A mention to the original author is expected, and appreciated.

⚠️ Terms and Conditions ⚠️

This financial tool is for educational purposes only and not financial advice. Users assume responsibility for decisions made based on the tool's information. Past performance doesn't guarantee future results. By using this tool, users agree to these terms.

Delimited Levels Today Session - Colors as InputsThis script is an alternative to

It was developed to address user feedback / enhancement requests.

The difference is that the 12 color settings are separate input variables, and therefore will retain their values across level input value changes, and support 'default' template saving.

Days and Session

This indicator optionally displays 2 informations:

- The Day of the week

- The New session's Candle

You can turn off/on the displayed information

Disclaimer: Scripts that I post publicly are experimental. They are not financial advices. Always backtest your ideas using your own methodologies.

NY Session in REDNY is Red from UK time 1200 to 1800.

The rest is white, helps distinguish me NY with non NY since I like trading NY session

Time Session Filter - Visual Only - @Davi117 Simple visual adjustable time filter to highlight certain times of the day.

For instance if you only trade between 06:00 and 10:00 etc.

Includes Time Zone Selector using GMT

E.g if you live in London then you time zone will be just GMT, else if you live in Paris it would be GMT+1.

Ensure Trading View's time zone selection in the bottom right to the left of the Auto Scale toggle, is also set also set to your time zone, else it will be misaligned.

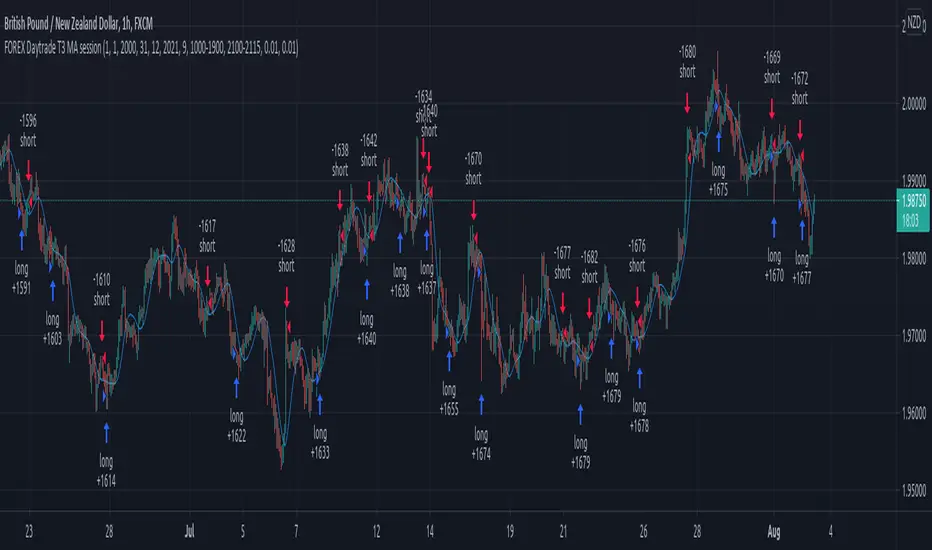

Forex Daytrade T3 MA sessionThis is a simple yet very efficient daytrading strategy for most crosses pairs, like EUR/NZD, EUR/AUD , GBP/NZD, GBP/AUD and so on.

It tends to works best with 1h and 15 min time frame charts.

Its components are :

Entry time = session that we want to trade, where we can combine for example half of London and all of NY using an hour system.

T3 Moving average

Price action.

Rules for entry

For long , we are during the hours we want to trade, current close is price is above previous high and at the same time is above moving average

For short , we are during the hours we want to trade, current close is price is below previous low and at the same time is below moving average

Rules for exit

We exit when either the opposite condition is triggered, if the hours of trading are off or based on a percentage TP/SL system movement.

For this example we use 1% movement both for TP and SL

If you have any questions, let me know !

Delimited Levels Today SessionThis script takes a delimited string of level values (up to 12) and plots them on the chart as per parameters.

Alerts can be set up for crossing, etc, using the Alerts panel as per usual.

Very handy if you have a spreadsheet or list of values to plot.

For example, say your spreadsheet has a list of these 12 levels to plot:

3800

3811

3822

3837

3851

3862

3877

3887

3902

3913

3928

The values could be copied to notepad / text editor, and the line breaks replaced with a delimiter, such as the ';' character (note: no trailing delimiter), to produce a delimited string:

3800;3811;3822;3837;3851;3862;3877;3887;3902;3913;3928

And then simply copy / paste this delimited string into the "Levels Delimited String" parameter.

Note: This script builds upon earlier script:

Enhancements include:

- Plot only for latest day (weekends factored in)

- Plot only for specified session

- Plot as bands or as lines