Curved Radius Supertrend [BOSWaves]Curved Radius Supertrend — Adaptive Parabolic Trend Framework with Dynamic Acceleration Geometry

Overview

The Curved Radius Supertrend introduces an evolution of the classic Supertrend indicator - engineered with a dynamic curvature engine that replaces rigid ATR bands with parabolic, radius-based motion. Traditional Supertrend systems rely on static band displacement, reacting linearly to volatility and often lagging behind emerging price acceleration. The Curved Radius Supertend model redefines this by integrating controlled acceleration and curvature geometry, allowing the trend bands to adapt fluidly to both velocity and duration of price movement.

The result is a smoother, more organic trend flow that visually captures the momentum curve of price action - not just its direction. Instead of sharp pivots or whipsaws, traders experience a structurally curved trajectory that mirrors real market inertia. This makes it particularly effective for identifying sustained directional phases, detecting early trend rotations, and filtering out noise that plagues standard Supertrend methodologies.

Unlike conventional band-following systems, the Curved Radius framework is time-reactive and velocity-aware, providing a nuanced signal structure that blends geometric precision with volatility sensitivity.

Theoretical Foundation

The Curved Radius Supertrend draws from the intersection of mathematical curvature dynamics and adaptive volatility processing. Standard Supertrend algorithms extend from Average True Range (ATR) envelopes - a linear measure of volatility that moves proportionally with price deviation. However, markets do not expand or contract linearly. Trend velocity typically accelerates and decelerates in nonlinear arcs, forming natural parabolas across price phases.

By embedding a radius-based acceleration function, the indicator models this natural behavior. The core variable, radiusStrength, controls how aggressively curvature accelerates over time. Instead of simply following price distance, the band now evolves according to temporal acceleration - each bar contributes incremental velocity, bending the trend line into a radius-like curve.

This structural design allows the indicator to anticipate rather than just respond to price action, capturing momentum transitions as curved accelerations rather than binary flips. In practice, this eliminates the stutter effect typical of standard Supertrends and replaces it with fluid directional motion that better reflects actual trend geometry.

How It Works

The Curved Radius Supertrend is constructed through a multi-stage process designed to balance price responsiveness with geometric stability:

1. Baseline Supertrend Core

The framework begins with a standard ATR-derived upper and lower band calculation. These define the volatility envelope that constrains potential price zones. Directional bias is determined through crossover logic - prices above the lower band confirm an uptrend, while prices below the upper band confirm a downtrend.

2. Curvature Acceleration Engine

Once a trend direction is established, a curvature engine is activated. This system uses radiusStrength as a coefficient to simulate acceleration per bar, incrementally increasing velocity over time. The result is a parabolic displacement from the anchor price (the price level at trend change), creating a curved motion path that dynamically widens or tightens as the trend matures.

Mathematically, this acceleration behaves quadratically - each new bar compounds the previous velocity, forming an exponential rate of displacement that resembles curved inertia.

3. Adaptive Smoothing Layer

After the radius curve is applied, a smoothing stage (defined by the smoothness parameter) uses a simple moving average to regulate curve noise. This ensures visual coherence without sacrificing responsiveness, producing flowing arcs rather than jagged band steps.

4. Directional Visualization and Outer Envelope

Directional state (bullish or bearish) dictates both the color gradient and band displacement. An outer envelope is plotted one ATR beyond the curved band, creating a layered trend visualization that shows the extent of volatility expansion.

5. Signal Events and Alerts

Each directional transition triggers a 'BUY' or 'SELL' signal, clearly labeling phase shifts in market structure. Alerts are built in for automation and backtesting.

Interpretation

The Curved Radius Supertrend reframes how traders visualize and confirm trends. Instead of simply plotting a trailing stop, it maps the dynamic curvature of trend development.

Uptrend Phases : The band curves upward with increasing acceleration, reflecting the market’s growing directional velocity. As curvature steepens, conviction strengthens.

Downtrend Phases : The band bends downward in a mirrored acceleration pattern, indicating sustained bearish momentum.

Trend Change Points : When the direction flips and a new anchor point forms, the curve resets - providing a clean, early visual confirmation of structural reversal.

Smoothing and Radius Interplay : A lower radius strength produces a tighter, more reactive curve ideal for scalping or short timeframes. Higher values generate broad, sweeping arcs optimized for swing or positional analysis.

Visually, this curvature system translates market inertia into shape - revealing how trends bend, accelerate, and ultimately exhaust.

Strategy Integration

The Curved Radius Supertrend is versatile enough to integrate seamlessly into multiple trading frameworks:

Trend Following : Use BUY/SELL flips to identify emerging directional bias. Strong curvature continuation confirms sustained momentum.

Momentum Entry Filtering : Combine with oscillators or volume tools to filter entries only when the curve slope accelerates (high momentum conditions).

Pullback and Re-entry Timing : The smooth curvature of the radius band allows traders to identify shallow retracements without premature exits. The band acts as a dynamic, self-adjusting support/resistance arc.

Volatility Compression and Expansion : Flattening curvature indicates volatility compression - a potential pre-breakout zone. Rapid re-steepening signals expansion and directional conviction.

Stop Placement Framework : The curved band can serve as a volatility-adjusted trailing stop. Because the curve reflects acceleration, it adapts naturally to market rhythm - widening during momentum surges and tightening during stagnation.

Technical Implementation Details

Curved Radius Engine : Parabolic acceleration algorithm that applies quadratic velocity based on bar count and radiusStrength.

Anchor Logic : Resets curvature at each trend change, establishing a new reference base for directional acceleration.

Smoothing Layer : SMA-based curve smoothing for noise reduction.

Outer Envelope : ATR-derived band offset visualizing volatility extension.

Directional Coloring : Candle and band coloration tied to current trend state.

Signal Engine : Built-in BUY/SELL markers and alert conditions for automation or script integration.

Optimal Application Parameters

Timeframe Guidance :

1-5 min (Scalping) : 0.08–0.12 radius strength, minimal smoothing for rapid responsiveness.

15 min : 0.12–0.15 radius strength for intraday trends.

1H : 0.15–0.18 radius strength for structured short-term swing setups.

4H : 0.18–0.22 radius strength for macro-trend shaping.

Daily : 0.20–0.25 radius strength for broad directional curves.

Weekly : 0.25–0.30 radius strength for smooth macro-level cycles.

The suggested radius strength ranges provide general structural guidance. Optimal values may vary across assets and volatility regimes, and should be refined through empirical testing to account for instrument-specific behavior and prevailing market conditions.

Asset Guidance :

Cryptocurrency : Higher radius and multiplier values to stabilize high-volatility environments.

Forex : Midrange settings (0.12-0.18) for clean curvature transitions.

Equities : Balanced curvature for trending sectors or momentum rotation setups.

Indices/Futures : Moderate radius values (0.15-0.22) to capture cyclical macro swings.

Performance Characteristics

High Effectiveness :

Trending environments with directional expansion.

Markets exhibiting clean momentum arcs and low structural noise.

Reduced Effectiveness :

Range-bound or low-volatility conditions with repeated false flips.

Ultra-short-term timeframes (<1m) where curvature acceleration overshoots.

Integration Guidelines

Confluence Framework : Combine with structure tools (order blocks, BOS, liquidity zones) for entry validation.

Risk Management : Trail stops along the curved band rather than fixed points to align with adaptive market geometry.

Multi-Timeframe Confirmation : Use higher timeframe curvature as a trend filter and lower timeframe curvature for execution timing.

Curve Compression Awareness : Treat flattening arcs as potential exhaustion zones - ideal for scaling out or reducing exposure.

Disclaimer

The Curved Radius Supertrend is a geometric trend model designed for professional traders and analysts. It is not a predictive system or a guaranteed profit method. Its performance depends on correct parameter calibration and sound risk management. BOSWaves recommends using it as part of a comprehensive analytical framework, incorporating volume, liquidity, and structural context to validate directional signals.

Tìm kiếm tập lệnh với "sweep"

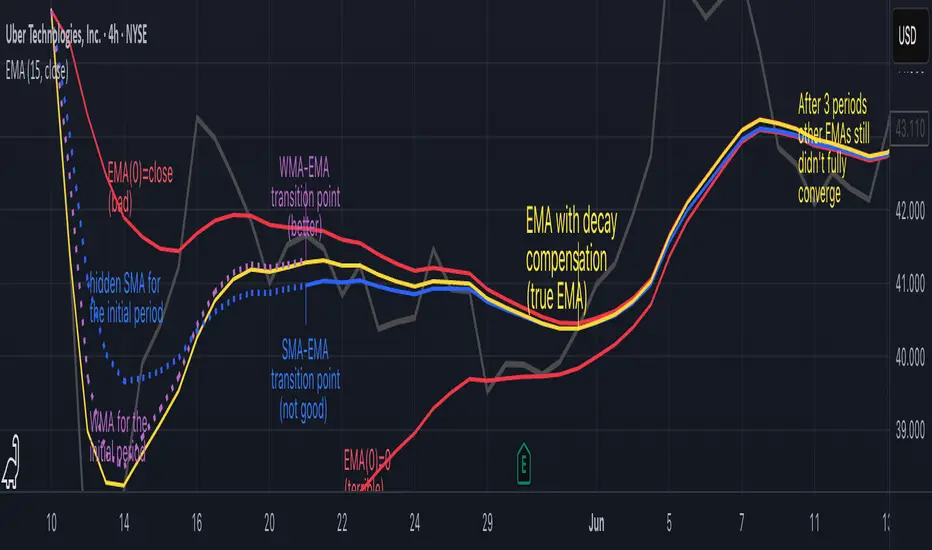

Why EMA Isn't What You Think It IsMany new traders adopt the Exponential Moving Average (EMA) believing it's simply a "better Simple Moving Average (SMA)". This common misconception leads to fundamental misunderstandings about how EMA works and when to use it.

EMA and SMA differ at their core. SMA use a window of finite number of data points, giving equal weight to each data point in the calculation period. This makes SMA a Finite Impulse Response (FIR) filter in signal processing terms. Remember that FIR means that "all that we need is the 'period' number of data points" to calculate the filter value. Anything beyond the given period is not relevant to FIR filters – much like how a security camera with 14-day storage automatically overwrites older footage, making last month's activity completely invisible regardless of how important it might have been.

EMA, however, is an Infinite Impulse Response (IIR) filter. It uses ALL historical data, with each past price having a diminishing - but never zero - influence on the calculated value. This creates an EMA response that extends infinitely into the past—not just for the last N periods. IIR filters cannot be precise if we give them only a 'period' number of data to work on - they will be off-target significantly due to lack of context, like trying to understand Game of Thrones by watching only the final season and wondering why everyone's so upset about that dragon lady going full pyromaniac.

If we only consider a number of data points equal to the EMA's period, we are capturing no more than 86.5% of the total weight of the EMA calculation. Relying on he period window alone (the warm-up period) will provide only 1 - (1 / e^2) weights, which is approximately 1−0.1353 = 0.8647 = 86.5%. That's like claiming you've read a book when you've skipped the first few chapters – technically, you got most of it, but you probably miss some crucial early context.

▶️ What is period in EMA used for?

What does a period parameter really mean for EMA? When we select a 15-period EMA, we're not selecting a window of 15 data points as with an SMA. Instead, we are using that number to calculate a decay factor (α) that determines how quickly older data loses influence in EMA result. Every trader knows EMA calculation: α = 1 / (1+period) – or at least every trader claims to know this while secretly checking the formula when they need it.

Thinking in terms of "period" seriously restricts EMA. The α parameter can be - should be! - any value between 0.0 and 1.0, offering infinite tuning possibilities of the indicator. When we limit ourselves to whole-number periods that we use in FIR indicators, we can only access a small subset of possible IIR calculations – it's like having access to the entire RGB color spectrum with 16.7 million possible colors but stubbornly sticking to the 8 basic crayons in a child's first art set because the coloring book only mentioned those by name.

For example:

Period 10 → alpha = 0.1818

Period 11 → alpha = 0.1667

What about wanting an alpha of 0.17, which might yield superior returns in your strategy that uses EMA? No whole-number period can provide this! Direct α parameterization offers more precision, much like how an analog tuner lets you find the perfect radio frequency while digital presets force you to choose only from predetermined stations, potentially missing the clearest signal sitting right between channels.

Sidenote: the choice of α = 1 / (1+period) is just a convention from 1970s, probably started by J. Welles Wilder, who popularized the use of the 14-day EMA. It was designed to create an approximate equivalence between EMA and SMA over the same number of periods, even thought SMA needs a period window (as it is FIR filter) and EMA doesn't. In reality, the decay factor α in EMA should be allowed any valye between 0.0 and 1.0, not just some discrete values derived from an integer-based period! Algorithmic systems should find the best α decay for EMA directly, allowing the system to fine-tune at will and not through conversion of integer period to float α decay – though this might put a few traditionalist traders into early retirement. Well, to prevent that, most traditionalist implementations of EMA only use period and no alpha at all. Heaven forbid we disturb people who print their charts on paper, draw trendlines with rulers, and insist the market "feels different" since computers do algotrading!

▶️ Calculating EMAs Efficiently

The standard textbook formula for EMA is:

EMA = CurrentPrice × alpha + PreviousEMA × (1 - alpha)

But did you know that a more efficient version exists, once you apply a tiny bit of high school algebra:

EMA = alpha × (CurrentPrice - PreviousEMA) + PreviousEMA

The first one requires three operations: 2 multiplications + 1 addition. The second one also requires three ops: 1 multiplication + 1 addition + 1 subtraction.

That's pathetic, you say? Not worth implementing? In most computational models, multiplications cost much more than additions/subtractions – much like how ordering dessert costs more than asking for a water refill at restaurants.

Relative CPU cost of float operations :

Addition/Subtraction: ~1 cycle

Multiplication: ~5 cycles (depending on precision and architecture)

Now you see the difference? 2 * 5 + 1 = 11 against 5 + 1 + 1 = 7. That is ≈ 36.36% efficiency gain just by swapping formulas around! And making your high school math teacher proud enough to finally put your test on the refrigerator.

▶️ The Warmup Problem: how to start the EMA sequence right

How do we calculate the first EMA value when there's no previous EMA available? Let's see some possible options used throughout the history:

Start with zero : EMA(0) = 0. This creates stupidly large distortion until enough bars pass for the horrible effect to diminish – like starting a trading account with zero balance but backdating a year of missed trades, then watching your balance struggle to climb out of a phantom debt for months.

Start with first price : EMA(0) = first price. This is better than starting with zero, but still causes initial distortion that will be extra-bad if the first price is an outlier – like forming your entire opinion of a stock based solely on its IPO day price, then wondering why your model is tanking for weeks afterward.

Use SMA for warmup : This is the tradition from the pencil-and-paper era of technical analysis – when calculators were luxury items and "algorithmic trading" meant your broker had neat handwriting. We first calculate an SMA over the initial period, then kickstart the EMA with this average value. It's widely used due to tradition, not merit, creating a mathematical Frankenstein that uses an FIR filter (SMA) during the initial period before abruptly switching to an IIR filter (EMA). This methodology is so aesthetically offensive (abrupt kink on the transition from SMA to EMA) that charting platforms hide these early values entirely, pretending EMA simply doesn't exist until the warmup period passes – the technical analysis equivalent of sweeping dust under the rug.

Use WMA for warmup : This one was never popular because it is harder to calculate with a pencil - compared to using simple SMA for warmup. Weighted Moving Average provides a much better approximation of a starting value as its linear descending profile is much closer to the EMA's decay profile.

These methods all share one problem: they produce inaccurate initial values that traders often hide or discard, much like how hedge funds conveniently report awesome performance "since strategy inception" only after their disastrous first quarter has been surgically removed from the track record.

▶️ A Better Way to start EMA: Decaying compensation

Think of it this way: An ideal EMA uses an infinite history of prices, but we only have data starting from a specific point. This creates a problem - our EMA starts with an incorrect assumption that all previous prices were all zero, all close, or all average – like trying to write someone's biography but only having information about their life since last Tuesday.

But there is a better way. It requires more than high school math comprehension and is more computationally intensive, but is mathematically correct and numerically stable. This approach involves compensating calculated EMA values for the "phantom data" that would have existed before our first price point.

Here's how phantom data compensation works:

We start our normal EMA calculation:

EMA_today = EMA_yesterday + α × (Price_today - EMA_yesterday)

But we add a correction factor that adjusts for the missing history:

Correction = 1 at the start

Correction = Correction × (1-α) after each calculation

We then apply this correction:

True_EMA = Raw_EMA / (1-Correction)

This correction factor starts at 1 (full compensation effect) and gets exponentially smaller with each new price bar. After enough data points, the correction becomes so small (i.e., below 0.0000000001) that we can stop applying it as it is no longer relevant.

Let's see how this works in practice:

For the first price bar:

Raw_EMA = 0

Correction = 1

True_EMA = Price (since 0 ÷ (1-1) is undefined, we use the first price)

For the second price bar:

Raw_EMA = α × (Price_2 - 0) + 0 = α × Price_2

Correction = 1 × (1-α) = (1-α)

True_EMA = α × Price_2 ÷ (1-(1-α)) = Price_2

For the third price bar:

Raw_EMA updates using the standard formula

Correction = (1-α) × (1-α) = (1-α)²

True_EMA = Raw_EMA ÷ (1-(1-α)²)

With each new price, the correction factor shrinks exponentially. After about -log₁₀(1e-10)/log₁₀(1-α) bars, the correction becomes negligible, and our EMA calculation matches what we would get if we had infinite historical data.

This approach provides accurate EMA values from the very first calculation. There's no need to use SMA for warmup or discard early values before output converges - EMA is mathematically correct from first value, ready to party without the awkward warmup phase.

Here is Pine Script 6 implementation of EMA that can take alpha parameter directly (or period if desired), returns valid values from the start, is resilient to dirty input values, uses decaying compensator instead of SMA, and uses the least amount of computational cycles possible.

// Enhanced EMA function with proper initialization and efficient calculation

ema(series float source, simple int period=0, simple float alpha=0)=>

// Input validation - one of alpha or period must be provided

if alpha<=0 and period<=0

runtime.error("Alpha or period must be provided")

// Calculate alpha from period if alpha not directly specified

float a = alpha > 0 ? alpha : 2.0 / math.max(period, 1)

// Initialize variables for EMA calculation

var float ema = na // Stores raw EMA value

var float result = na // Stores final corrected EMA

var float e = 1.0 // Decay compensation factor

var bool warmup = true // Flag for warmup phase

if not na(source)

if na(ema)

// First value case - initialize EMA to zero

// (we'll correct this immediately with the compensation)

ema := 0

result := source

else

// Standard EMA calculation (optimized formula)

ema := a * (source - ema) + ema

if warmup

// During warmup phase, apply decay compensation

e *= (1-a) // Update decay factor

float c = 1.0 / (1.0 - e) // Calculate correction multiplier

result := c * ema // Apply correction

// Stop warmup phase when correction becomes negligible

if e <= 1e-10

warmup := false

else

// After warmup, EMA operates without correction

result := ema

result // Return the properly compensated EMA value

▶️ CONCLUSION

EMA isn't just a "better SMA"—it is a fundamentally different tool, like how a submarine differs from a sailboat – both float, but the similarities end there. EMA responds to inputs differently, weighs historical data differently, and requires different initialization techniques.

By understanding these differences, traders can make more informed decisions about when and how to use EMA in trading strategies. And as EMA is embedded in so many other complex and compound indicators and strategies, if system uses tainted and inferior EMA calculatiomn, it is doing a disservice to all derivative indicators too – like building a skyscraper on a foundation of Jell-O.

The next time you add an EMA to your chart, remember: you're not just looking at a "faster moving average." You're using an INFINITE IMPULSE RESPONSE filter that carries the echo of all previous price actions, properly weighted to help make better trading decisions.

EMA done right might significantly improve the quality of all signals, strategies, and trades that rely on EMA somewhere deep in its algorithmic bowels – proving once again that math skills are indeed useful after high school, no matter what your guidance counselor told you.

Fibonacci Circle Zones🟩 The Fibonacci Circle Zones indicator is a technical visualization tool, building upon the concept of traditional Fibonacci circles. It provides configurable options for analyzing geometric relationships between price and time, used to identify potential support and resistance zones derived from circle-based projections. The indicator constructs these Fibonacci circles based on two user-selected anchor points (Point A and Point B), which define the foundational price range and time duration for the geometric analysis.

Key features include multiple mathematical Circle Formulas for radius scaling and several options for defining the circle's center point, enabling exploration of complex, non-linear geometric relationships between price and time distinct from traditional linear Fibonacci analysis. Available formulas incorporate various mathematical constants (π, e, φ variants, Silver Ratio) alongside traditional Fibonacci ratios, facilitating investigation into different scaling hypotheses. Furthermore, selecting the Center point relative to the A-B anchors allows these circular time-price patterns to be constructed and analyzed from different geometric perspectives. Analysis can be further tailored through detailed customization of up to 12 Fibonacci levels, including their mathematical values, colors, and visibility..

📚 THEORY and CONCEPT 📚

Fibonacci circles represent an application of Fibonacci principles within technical analysis, extending beyond typical horizontal price levels by incorporating the dimension of time. These geometric constructions traditionally use numerical proportions, often derived from the Fibonacci sequence, to project potential zones of price-time interaction, such as support or resistance. A theoretical understanding of such geometric tools involves considering several core components: the significance of the chosen geometric origin or center point , the mathematical principles governing the proportional scaling of successive radii, and the fundamental calculation considerations (like chart scale adjustments and base radius definitions) that influence the resulting geometry and ensure its accurate representation.

⨀ Circle Center ⨀

The traditional construction methodology for Fibonacci circles begins with the selection of two significant anchor points on the chart, usually representing a key price swing, such as a swing low (Point A) and a subsequent swing high (Point B), or vice versa. This defined segment establishes the primary vector—representing both the price range and the time duration of that specific market move. From these two points, a base distance or radius is derived (this calculation can vary, sometimes using the vertical price distance, the time duration, or the diagonal distance). A center point for the circles is then typically established, often at the midpoint (time and price) between points A and B, or sometimes anchored directly at point B.

Concentric circles are then projected outwards from this center point. The radii of these successive circles are calculated by multiplying the base distance by key Fibonacci ratios and other standard proportions. The underlying concept posits that markets may exhibit harmonic relationships or cyclical behavior that adheres to these proportions, suggesting these expanding geometric zones could highlight areas where future price movements might decelerate, reverse, or find equilibrium, reflecting a potential proportional resonance with the initial defining swing in both price and time.

The Fibonacci Circle Zones indicator enhances traditional Fibonacci circle construction by offering greater analytical depth and flexibility: it addresses the origin point of the circles: instead of being limited to common definitions like the midpoint or endpoint B, this indicator provides a selection of distinct center point calculations relative to the initial A-B swing. The underlying idea is that the geometric source from which harmonic projections emanate might vary depending on the market structure being analyzed. This flexibility allows for experimentation with different center points (derived algorithmically from the A, B, and midpoint coordinates), facilitating exploration of how price interacts with circular zones anchored from various perspectives within the defining swing.

Potential Center Points Setup : This view shows the anchor points A and B , defined by the user, which form the basis of the calculations. The indicator dynamically calculates various potential Center points ( C through N , and X ) based on the A-B structure, representing different geometric origins available for selection in the settings.

Point X holds particular significance as it represents the calculated midpoint (in both time and price) between A and B. This 'X' point corresponds to the default 'Auto' center setting upon initial application of the indicator and aligns with the centering logic used in TradingView's standard Fibonacci Circle tool, offering a familiar starting point.

The other potential center points allow for exploring circles originating from different geometric anchors relative to the A-B structure. While detailing the precise calculation for each is beyond the scope of this overview, they can be broadly categorized: points C through H are derived from relationships primarily within the A-B time/price range, whereas points I through N represent centers projected beyond point B, extrapolating the A-B geometry. Point J, for example, is calculated as a reflection of the A-X midpoint projected beyond B. This variety provides a rich set of options for analyzing circle patterns originating from historical, midpoint, and extrapolated future anchor perspectives.

Default Settings (Center X, FibCircle) : Using the default Center X (calculated midpoint) with the default FibCircle . Although circles begin plotting only after Point B is established, their curvature shows they are geometrically centered on X. This configuration matches the standard TradingView Fib Circle tool, providing a baseline.

Centering on Endpoint B : Using Point B, the user-defined end of the swing, as the Center . This anchors the circular projections directly to the swing's termination point. Unlike centering on the midpoint (X) or start point (A), this focuses the analysis on geometric expansion originating precisely from the conclusion of the measured A-B move.

Projected Center J : Using the projected Point J as the Center . Its position is calculated based on the A-B swing (conceptually, it represents a forward projection related to the A-X midpoint relationship) and is located chronologically beyond Point B. This type of forward projection often allows complete circles to be visualized as price develops into the corresponding time zone.

Time Symmetry Projection (Center L) : Uses the projected Point L as the Center . It is located at the price level of the start point (A), projected forward in time from B by the full duration of the A-B swing . This perspective focuses analysis on temporal symmetry , exploring geometric expansions from a point representing a full time cycle completion anchored back at the swing's origin price level.

⭕ Circle Formula

Beyond the center point , the expansion of the projected circles is determined by the selected Circle Formula . This setting provides different mathematical methods, or scaling options , for scaling the circle radii. Each option applies a distinct mathematical constant or relationship to the base radius derived from the A-B swing, allowing for exploration of various geometric proportions.

eScaled

Mathematical Basis: Scales the radius by Euler's number ( e ≈ 2.718), the base of natural logarithms. This constant appears frequently in processes involving continuous growth or decay.

Enables investigation of market geometry scaled by e , exploring relationships potentially based on natural exponential growth applied to time-price circles, potentially relevant for analyzing phases of accelerating momentum or volatility expansion.

FibCircle

Mathematical Basis: Scales the radius to align with TradingView’s built-in Fibonacci Circle Tool.

Provides a baseline circle size, potentially emulating scaling used in standard drawing tools, serving as a reference point for comparison with other options.

GoldenFib

Mathematical Basis: Scales the radius by the Golden Ratio (φ ≈ 1.618).

Explores the fundamental Golden Ratio proportion, central to Fibonacci analysis, applied directly to circular time-price geometry, potentially highlighting zones reflecting harmonic expansion or retracement patterns often associated with φ.

GoldenContour

Mathematical Basis: Scales the radius by a factor derived from Golden Ratio geometry (√(1 + φ²) / 2 ≈ 0.951). It represents a specific geometric relationship derived from φ.

Allows analysis using proportions linked to the geometry of the Golden Rectangle, scaled to produce circles very close to the initial base radius. This explores structural relationships often associated with natural balance or proportionality observed in Golden Ratio constructions.

SilverRatio

Mathematical Basis: Scales the radius by the Silver Ratio (1 + √2 ≈ 2.414). The Silver Ratio governs relationships in specific regular polygons and recursive sequences.

Allows exploration using the proportions of the Silver Ratio, offering a significant expansion factor based on another fundamental metallic mean for comparison with φ-based methods.

PhiDecay

Mathematical Basis: Scales the radius by φ raised to the power of -φ (φ⁻ᵠ ≈ 0.53). This unique exponentiation explores a less common, non-linear transformation involving φ.

Explores market geometry scaled by this specific phi-derived factor which is significantly less than 1.0, offering a distinct contractile proportion for analysis, potentially relevant for identifying zones related to consolidation phases or decaying momentum.

PhiSquared

Mathematical Basis: Scales the radius by φ squared, normalized by dividing by 3 (φ² / 3 ≈ 0.873).

Enables investigation of patterns related to the φ² relationship (a key Fibonacci extension concept), visualized at a scale just below 1.0 due to normalization. This scaling explores projections commonly associated with significant trend extension targets in linear Fibonacci analysis, adapted here for circular geometry.

PiScaled

Mathematical Basis: Scales the radius by Pi (π ≈ 3.141).

Explores direct scaling by the fundamental circle constant (π), investigating proportions inherent to circular geometry within the market's time-price structure, potentially highlighting areas related to natural market cycles, rotational symmetry, or full-cycle completions.

PlasticNumber

Mathematical Basis: Scales the radius by the Plastic Number (approx 1.3247), the third metallic mean. Like φ and the Silver Ratio, it is the solution to a specific cubic equation and relates to certain geometric forms.

Introduces another distinct fundamental mathematical constant for geometric exploration, comparing market proportions to those potentially governed by the Plastic Number.

SilverFib

Mathematical Basis: Scales the radius by the reciprocal Golden Ratio (1/φ ≈ 0.618).

Explores proportions directly related to the core 0.618 Fibonacci ratio, fundamental within Fibonacci-based geometric analysis, often significant for identifying primary retracement levels or corrective wave structures within a trend.

Unscaled

Mathematical Basis: No scaling applied.

Provides the base circle defined by points A/B and the Center setting without any additional mathematical scaling, serving as a pure geometric reference based on the A-B structure.

🧪 Advanced Calculation Settings

Two advanced settings allow further refinement of the circle calculations: matching the chart's scale and defining how the base radius is calculated from the A-B swing.

The Chart Scale setting ensures geometric accuracy by aligning circle calculations with the chart's vertical axis display. Price charts can use either a standard (linear) or logarithmic scale, where vertical distances represent price changes differently. The setting offers two options:

Standard : Select this option when the price chart's vertical axis is set to a standard linear scale.

Logarithmic : It is necessary to select this option if the price chart's vertical axis is set to a logarithmic scale. Doing so ensures the indicator adjusts its calculations to maintain correct geometric proportions relative to the visual price action on the log-scaled chart.

The Radius Calc setting determines how the fundamental base radius is derived from the A-B swing, offering two primary options:

Auto : This is the default setting and represents the traditional method for radius calculation. This method bases the radius calculation on the vertical price range of the A-B swing, focusing the geometry on the price amplitude.

Geometric : This setting provides an alternative calculation method, determining the base radius from the diagonal distance between Point A and Point B. It considers both the price change and the time duration relative to the chart's aspect ratio, defining the radius based on the overall magnitude of the A-B price-time vector.

This choice allows the resulting circle geometry to be based either purely on the swing's vertical price range ( Auto ) or on its combined price-time movement ( Geometric ).

🖼️ CHART EXAMPLES 🖼️

Default Behavior (X Center, FibCircle Formula) : This configuration uses the midpoint ( Center X) and the FibCircle scaling Formula , representing the indicator's effective default setup when 'Auto' is selected for both options initially. This is designed to match the output of the standard TradingView Fibonacci Circle drawing tool.

Center B with Unscaled Formula : This example shows the indicator applied to an uptrend with the Center set to Point B and the Circle Formula set to Unscaled . This configuration projects the defined levels (0.236, 0.382, etc.) as arcs originating directly from the swing's termination point (B) without applying any additional mathematical scaling from the formulas.

Visualization with Projected Center J : Here, circles are centered on the projected point J, calculated from the A-B structure but located forward in time from point B. Notice how using this forward-projected origin allows complete inner circles to be drawn once price action develops into that zone, providing a distinct visual representation of the expanding geometric field compared to using earlier anchor points. ( Unscaled formula used in this example).

PhiSquared Scaling from Endpoint B : The PhiSquared scaling Formula applied from the user-defined swing endpoint (Point B). Radii expand based on a normalized relationship with φ² (the square of the Golden Ratio), creating a unique geometric structure and spacing between the circle levels compared to other formulas like Unscaled or GoldenFib .

Centering on Swing Origin (Point A) : Illustrates using Point A, the user-defined start of the swing, as the circle Center . Note the significantly larger scale and wider spacing of the resulting circles. This difference occurs because centering on the swing's origin (A) typically leads to a larger base radius calculation compared to using the midpoint (X) or endpoint (B). ( Unscaled formula used).

Center Point D : Point D, dynamically calculated from the A-B swing, is used as the origin ( Center =D). It is specifically located at the price level of the swing's start point (A) occurring precisely at the time coordinate of the swing's end point (B). This offers a unique perspective, anchoring the geometric expansion to the initial price level at the exact moment the defining swing concludes. ( Unscaled formula shown).

Center Point G : Point G, also dynamically calculated from the A-B swing, is used as the origin ( Center =G). It is located at the price level of the swing's endpoint (B) occurring at the time coordinate of the start point (A). This provides the complementary perspective to Point D, anchoring the geometric expansion to the final price level achieved but originating from the moment the swing began . As observed in the example, using Point G typically results in very wide circle projections due to its position relative to the core A-B action. ( Unscaled formula shown).

Center Point I: Half-Duration Projection : Using the dynamically calculated Point I as the Center . Located at Point B's price level but projected forward in time by half the A-B swing duration , Point I's calculated time coordinate often falls outside the initially visible chart area. As the chart progresses, this origin point will appear, revealing large, sweeping arcs representing geometric expansions based on a half-cycle temporal projection from the swing's endpoint price. ( Unscaled formula shown).

Center Point M : Point M, also dynamically calculated from the A-B swing, serves as the origin ( Center =M). It combines the midpoint price level (derived from X) with a time coordinate projected forward from Point B by the full duration of the A-B swing . This perspective anchors the geometric expansion to the swing's balance price level but originates from the completion point of a full temporal cycle relative to the A-B move. Like other projected centers, using M allows for complete circles to be visualized as price progresses into its time zone. ( SilverFib formula shown).

Geometric Validation & Functionality : Comparing the indicator (red lines), using its default settings ( Center X, FibCircle Formula ), against TradingView's standard Fib Circle tool (green lines/white background). The precise alignment, particularly visible at the 1.50 and 2.00 levels shown, validates the core geometry calculation.

🛠️ CONFIGURATION AND SETTINGS 🛠️

The Fibonacci Circle Zones indicator offers a range of configurable settings to tailor its functionality and visual representation. These options allow customization of the circle origin, scaling method, level visibility, visual appearance, and input points.

Center and Formula

Settings for selecting the circle origin and scaling method.

Center : Dropdown menu to select the origin point for the circles.

Auto : Automatically uses point X (the calculated midpoint between A and B).

Selectable points including start/end (A, B), midpoint (X), plus various points derived from or projected beyond the A-B swing (C-N).

Circle Formula : Dropdown menu to select the mathematical method for scaling circle radii.

Auto : Automatically selects a default formula ('FibCircle' if Center is 'X', 'Unscaled' otherwise).

Includes standard Fibonacci scaling ( FibCircle, GoldenFib ), other mathematical constants ( PiScaled, eScaled ), metallic means ( SilverRatio ), phi transformations ( PhiDecay, PhiSquared ), and others.

Fib Levels

Configuration options for the 12 individual Fibonacci levels.

Advanced Settings

Settings related to core calculation methods.

Radius Calc : Defines how the base radius is calculated (e.g., 'Auto' for vertical price range, 'Geometric' for diagonal price-time distance).

Chart Scale : Aligns circle calculations with the chart's vertical axis setting ('Standard' or 'Logarithmic') for accurate visual proportions.

Visual Settings

Settings controlling the visual display of the indicator elements.

Plots : Dropdown controlling which parts of the calculated circles are displayed ( Upper , All , or Lower ).

Labels : Dropdown controlling the display of the numerical level value labels ( All , Left , Right , or None ).

Setup : Dropdown controlling the visibility of the initial setup graphics ( Show or Hide ).

Info : Dropdown controlling the visibility of the small information table ( Show or Hide ).

Text Size : Adjusts the font size for all text elements displayed by the indicator (Value ranges from 0 to 36).

Line Width : Adjusts the width of the circle plots (1-10).

Time/Price

Inputs for the anchor points defining the base swing.

These settings define the start (Point A) and end (Point B) of the price swing used for all calculations.

Point A (Time, Price) : Input fields for the exact time coordinate and price level of the swing's starting point (A).

Point B (Time, Price) : Input fields for the exact time coordinate and price level of the swing's ending point (B).

Interactive Adjustment : Points A and B can typically be adjusted directly by clicking and dragging their markers on the chart (if 'Setup' is set to 'Show'). Changes update settings automatically.

📝 NOTES 📝

Fibonacci circles begin plotting only once the time corresponding to Point B has passed and is confirmed on the chart. While potential center locations might be visible earlier (as shown in the setup graphic), the final circle calculations require the complete geometry of the A-B swing. This approach ensures that as new price bars form, the circles are accurately rendered based on the finalized A-B relationship and the chosen center and scaling.

The indicator's calculations are anchored to user-defined start (A) and end (B) points on the chart. When switching between charts with significantly different price scales (e.g., from an index at 5,000 to a crypto asset at $0.50), it is typically necessary to adjust these anchor points to ensure the circle elements are correctly positioned and scaled.

⚠️ DISCLAIMER ⚠️

The Fibonacci Circle Zones indicator is a visual analysis tool designed to illustrate Fibonacci relationships through geometric constructions incorporating curved lines, providing a structured framework for identifying potential areas of price interaction. Like all technical and visual indicators, these visual representations may visually align with key price zones in hindsight, reflecting observed price dynamics. It is not intended as a predictive or standalone trading signal indicator.

The indicator calculates levels and projections using user-defined anchor points and Fibonacci ratios. While it aims to align with TradingView’s standard Fibonacci circle tool by employing mathematical and geometric formulas, no guarantee is made that its calculations are identical to TradingView's proprietary methods.

🧠 BEYOND THE CODE 🧠

The Fibonacci Circle Zones indicator, like other xxattaxx indicators , is designed with education and community collaboration in mind. Its open-source nature encourages exploration, experimentation, and the development of new Fibonacci and grid calculation indicators and tools. We hope this indicator serves as a framework and a starting point for future Innovation and discussions.

Day Open vs Previous Day CloseThe concept of comparing the **Day Open** to the **Previous Day Close** is used frequently in technical analysis to gauge the sentiment or momentum at the start of a new trading day.

### Key Terms:

- **Day Open**: The first traded price of an asset when the market opens for the day.

- **Previous Day Close**: The last traded price of an asset when the market closed on the previous day.

### Importance of Day Open vs. Previous Day Close

1. **Market Sentiment Indicator**:

- If the **Day Open** is **higher** than the **Previous Day Close**, it suggests **bullish** sentiment (buyers are willing to pay more than yesterday's closing price).

- If the **Day Open** is **lower** than the **Previous Day Close**, it suggests **bearish** sentiment (sellers are driving prices down compared to the last price from the previous day).

2. **Potential Gaps**:

- A **gap** occurs when there is a significant difference between the Day Open and Previous Day Close, often due to events or news released after the market closed. This gap can indicate strong momentum in either direction.

- **Gap Up**: Open > Close (bullish).

- **Gap Down**: Open < Close (bearish).

3. **Trend Continuation or Reversal**:

- If the market opens above the previous day’s close and continues to rise, it often signals a **continuation of an upward trend**.

- Conversely, if the market opens below and keeps falling, it suggests **downward momentum** is still strong.

4. **Trading Strategies**:

- **Opening Range Breakout**: Traders may look for the price to break above or below the opening range (the price range between the Day Open and the first few candles) to confirm a strong bullish or bearish move.

- **Reversals**: Some traders look for price reversals if the price spikes far above or below the previous day's close, expecting that the market might correct itself and return towards the previous day’s closing levels.

In the context of your **Opening Range Indicator**, the concept of the Day Open sweeping and closing above or below the Previous Day Close is used to identify whether the new day is setting up for a **buy (bullish)** or **sell (bearish)** opportunity.

Radius Trend [ChartPrime]RADIUS TREND

⯁ OVERVIEW

The Radius Trend [ ChartPrime ] indicator is an innovative technical analysis tool designed to visualize market trends using a dynamic, radius-based approach. By incorporating adaptive bands that adjust based on price action and volatility, this indicator provides traders with a unique perspective on trend direction, strength, and potential reversal points.

The Radius Trend concept involves creating a dynamic trend line that adjusts its angle and position based on market movements, similar to a radius sweeping across a chart. This approach allows for a more fluid and adaptive trend analysis compared to traditional linear trend lines.

◆ KEY FEATURES

Dynamic Trend Band: Calculates and plots a main trend band that adapts to market conditions.

Radius-Based Adjustment: Uses a step-based radius approach to adjust the trend band angle.

// Apply step angle to trend lines

if bar_index % n == 0 and trend

multi1 := 0

multi2 += step

band += distance1 * multi2

if bar_index % n == 0 and not trend

multi1 += step

multi2 := 0

band -= distance1 * multi1

Volatility-Adjusted Calculations: Incorporates price range volatility for more accurate band placement.

Trend Direction Visualization: Provides clear color-coding to distinguish between uptrends and downtrends.

Flexible Parameters: Allows users to adjust the radius step and initial distance for customized analysis.

◆ USAGE

Trend Identification: Use the color and direction of the main band to determine the current market trend.

Trend Strength Analysis: Observe the angle and consistency of the band for insights into trend strength.

Reversal Detection: Watch for price crossing the main band or crossing a dashed band as a potential trend reversal signal.

Volatility Assessment: The distance between price and bands can provide insights into market volatility.

⯁ USER INPUTS

Radius Step: Controls the rate of angle adjustment for the trend band (default: 0.15, step: 0.001).

Start Points Distance: Sets the initial distance multiplier for band calculations (default: 2, step: 0.1).

The Radius Trend indicator offers traders a unique and dynamic approach to trend analysis. By combining radius-based trend adjustments with volatility-sensitive calculations, it provides a fluid representation of market trends. This indicator is particularly useful for traders looking to identify trend persistence, potential reversal points, and adaptive support/resistance levels across various market conditions and timeframes.

Any Oscillator Underlay [TTF]We are proud to release a new indicator that has been a while in the making - the Any Oscillator Underlay (AOU) !

Note: There is a lot to discuss regarding this indicator, including its intent and some of how it operates, so please be sure to read this entire description before using this indicator to help ensure you understand both the intent and some limitations with this tool.

Our intent for building this indicator was to accomplish the following:

Combine all of the oscillators that we like to use into a single indicator

Take up a bit less screen space for the underlay indicators for strategies that utilize multiple oscillators

Provide a tool for newer traders to be able to leverage multiple oscillators in a single indicator

Features:

Includes 8 separate, fully-functional indicators combined into one

Ability to easily enable/disable and configure each included indicator independently

Clearly named plots to support user customization of color and styling, as well as manual creation of alerts

Ability to customize sub-indicator title position and color

Ability to customize sub-indicator divider lines style and color

Indicators that are included in this initial release:

TSI

2x RSIs (dubbed the Twin RSI )

Stochastic RSI

Stochastic

Ultimate Oscillator

Awesome Oscillator

MACD

Outback RSI (Color-coding only)

Quick note on OB/OS:

Before we get into covering each included indicator, we first need to cover a core concept for how we're defining OB and OS levels. To help illustrate this, we will use the TSI as an example.

The TSI by default has a mid-point of 0 and a range of -100 to 100. As a result, a common practice is to place lines on the -30 and +30 levels to represent OS and OB zones, respectively. Most people tend to view these levels as distance from the edges/outer bounds or as absolute levels, but we feel a more way to frame the OB/OS concept is to instead define it as distance ("offset") from the mid-line. In keeping with the -30 and +30 levels in our example, the offset in this case would be "30".

Taking this a step further, let's say we decided we wanted an offset of 25. Since the mid-point is 0, we'd then calculate the OB level as 0 + 25 (+25), and the OS level as 0 - 25 (-25).

Now that we've covered the concept of how we approach defining OB and OS levels (based on offset/distance from the mid-line), and since we did apply some transformations, rescaling, and/or repositioning to all of the indicators noted above, we are going to discuss each component indicator to detail both how it was modified from the original to fit the stacked-indicator model, as well as the various major components that the indicator contains.

TSI:

This indicator contains the following major elements:

TSI and TSI Signal Line

Color-coded fill for the TSI/TSI Signal lines

Moving Average for the TSI

TSI Histogram

Mid-line and OB/OS lines

Default TSI fill color coding:

Green : TSI is above the signal line

Red : TSI is below the signal line

Note: The TSI traditionally has a range of -100 to +100 with a mid-point of 0 (range of 200). To fit into our stacking model, we first shrunk the range to 100 (-50 to +50 - cut it in half), then repositioned it to have a mid-point of 50. Since this is the "bottom" of our indicator-stack, no additional repositioning is necessary.

Twin RSI:

This indicator contains the following major elements:

Fast RSI (useful if you want to leverage 2x RSIs as it makes it easier to see the overlaps and crosses - can be disabled if desired)

Slow RSI (primary RSI)

Color-coded fill for the Fast/Slow RSI lines (if Fast RSI is enabled and configured)

Moving Average for the Slow RSI

Mid-line and OB/OS lines

Default Twin RSI fill color coding:

Dark Red : Fast RSI below Slow RSI and Slow RSI below Slow RSI MA

Light Red : Fast RSI below Slow RSI and Slow RSI above Slow RSI MA

Dark Green : Fast RSI above Slow RSI and Slow RSI below Slow RSI MA

Light Green : Fast RSI above Slow RSI and Slow RSI above Slow RSI MA

Note: The RSI naturally has a range of 0 to 100 with a mid-point of 50, so no rescaling or transformation is done on this indicator. The only manipulation done is to properly position it in the indicator-stack based on which other indicators are also enabled.

Stochastic and Stochastic RSI:

These indicators contain the following major elements:

Configurable lengths for the RSI (for the Stochastic RSI only), K, and D values

Configurable base price source

Mid-line and OB/OS lines

Note: The Stochastic and Stochastic RSI both have a normal range of 0 to 100 with a mid-point of 50, so no rescaling or transformations are done on either of these indicators. The only manipulation done is to properly position it in the indicator-stack based on which other indicators are also enabled.

Ultimate Oscillator (UO):

This indicator contains the following major elements:

Configurable lengths for the Fast, Middle, and Slow BP/TR components

Mid-line and OB/OS lines

Moving Average for the UO

Color-coded fill for the UO/UO MA lines (if UO MA is enabled and configured)

Default UO fill color coding:

Green : UO is above the moving average line

Red : UO is below the moving average line

Note: The UO naturally has a range of 0 to 100 with a mid-point of 50, so no rescaling or transformation is done on this indicator. The only manipulation done is to properly position it in the indicator-stack based on which other indicators are also enabled.

Awesome Oscillator (AO):

This indicator contains the following major elements:

Configurable lengths for the Fast and Slow moving averages used in the AO calculation

Configurable price source for the moving averages used in the AO calculation

Mid-line

Option to display the AO as a line or pseudo-histogram

Moving Average for the AO

Color-coded fill for the AO/AO MA lines (if AO MA is enabled and configured)

Default AO fill color coding (Note: Fill was disabled in the image above to improve clarity):

Green : AO is above the moving average line

Red : AO is below the moving average line

Note: The AO is technically has an infinite (unbound) range - -∞ to ∞ - and the effective range is bound to the underlying security price (e.g. BTC will have a wider range than SP500, and SP500 will have a wider range than EUR/USD). We employed some special techniques to rescale this indicator into our desired range of 100 (-50 to 50), and then repositioned it to have a midpoint of 50 (range of 0 to 100) to meet the constraints of our stacking model. We then do one final repositioning to place it in the correct position the indicator-stack based on which other indicators are also enabled. For more details on how we accomplished this, read our section "Binding Infinity" below.

MACD:

This indicator contains the following major elements:

Configurable lengths for the Fast and Slow moving averages used in the MACD calculation

Configurable price source for the moving averages used in the MACD calculation

Configurable length and calculation method for the MACD Signal Line calculation

Mid-line

Note: Like the AO, the MACD also technically has an infinite (unbound) range. We employed the same principles here as we did with the AO to rescale and reposition this indicator as well. For more details on how we accomplished this, read our section "Binding Infinity" below.

Outback RSI (ORSI):

This is a stripped-down version of the Outback RSI indicator (linked above) that only includes the color-coding background (suffice it to say that it was not technically feasible to attempt to rescale the other components in a way that could consistently be clearly seen on-chart). As this component is a bit of a niche/special-purpose sub-indicator, it is disabled by default, and we suggest it remain disabled unless you have some pre-defined strategy that leverages the color-coding element of the Outback RSI that you wish to use.

Binding Infinity - How We Incorporated the AO and MACD (Warning - Math Talk Ahead!)

Note: This applies only to the AO and MACD at time of original publication. If any other indicators are added in the future that also fall into the category of "binding an infinite-range oscillator", we will make that clear in the release notes when that new addition is published.

To help set the stage for this discussion, it's important to note that the broader challenge of "equalizing inputs" is nothing new. In fact, it's a key element in many of the most popular fields of data science, such as AI and Machine Learning. They need to take a diverse set of inputs with a wide variety of ranges and seemingly-random inputs (referred to as "features"), and build a mathematical or computational model in order to work. But, when the raw inputs can vary significantly from one another, there is an inherent need to do some pre-processing to those inputs so that one doesn't overwhelm another simply due to the difference in raw values between them. This is where feature scaling comes into play.

With this in mind, we implemented 2 of the most common methods of Feature Scaling - Min-Max Normalization (which we call "Normalization" in our settings), and Z-Score Normalization (which we call "Standardization" in our settings). Let's take a look at each of those methods as they have been implemented in this script.

Min-Max Normalization (Normalization)

This is one of the most common - and most basic - methods of feature scaling. The basic formula is: y = (x - min)/(max - min) - where x is the current data sample, min is the lowest value in the dataset, and max is the highest value in the dataset. In this transformation, the max would evaluate to 1, and the min would evaluate to 0, and any value in between the min and the max would evaluate somewhere between 0 and 1.

The key benefits of this method are:

It can be used to transform datasets of any range into a new dataset with a consistent and known range (0 to 1).

It has no dependency on the "shape" of the raw input dataset (i.e. does not assume the input dataset can be approximated to a normal distribution).

But there are a couple of "gotchas" with this technique...

First, it assumes the input dataset is complete, or an accurate representation of the population via random sampling. While in most situations this is a valid assumption, in trading indicators we don't really have that luxury as we're often limited in what sample data we can access (i.e. number of historical bars available).

Second, this method is highly sensitive to outliers. Since the crux of this transformation is based on the max-min to define the initial range, a single significant outlier can result in skewing the post-transformation dataset (i.e. major price movement as a reaction to a significant news event).

You can potentially mitigate those 2 "gotchas" by using a mechanism or technique to find and discard outliers (e.g. calculate the mean and standard deviation of the input dataset and discard any raw values more than 5 standard deviations from the mean), but if your most recent datapoint is an "outlier" as defined by that algorithm, processing it using the "scrubbed" dataset would result in that new datapoint being outside the intended range of 0 to 1 (e.g. if the new datapoint is greater than the "scrubbed" max, it's post-transformation value would be greater than 1). Even though this is a bit of an edge-case scenario, it is still sure to happen in live markets processing live data, so it's not an ideal solution in our opinion (which is why we chose not to attempt to discard outliers in this manner).

Z-Score Normalization (Standardization)

This method of rescaling is a bit more complex than the Min-Max Normalization method noted above, but it is also a widely used process. The basic formula is: y = (x – μ) / σ - where x is the current data sample, μ is the mean (average) of the input dataset, and σ is the standard deviation of the input dataset. While this transformation still results in a technically-infinite possible range, the output of this transformation has a 2 very significant properties - the mean (average) of the output dataset has a mean (μ) of 0 and a standard deviation (σ) of 1.

The key benefits of this method are:

As it's based on normalizing the mean and standard deviation of the input dataset instead of a linear range conversion, it is far less susceptible to outliers significantly affecting the result (and in fact has the effect of "squishing" outliers).

It can be used to accurately transform disparate sets of data into a similar range regardless of the original dataset's raw/actual range.

But there are a couple of "gotchas" with this technique as well...

First, it still technically does not do any form of range-binding, so it is still technically unbounded (range -∞ to ∞ with a mid-point of 0).

Second, it implicitly assumes that the raw input dataset to be transformed is normally distributed, which won't always be the case in financial markets.

The first "gotcha" is a bit of an annoyance, but isn't a huge issue as we can apply principles of normal distribution to conceptually limit the range by defining a fixed number of standard deviations from the mean. While this doesn't totally solve the "infinite range" problem (a strong enough sudden move can still break out of our "conceptual range" boundaries), the amount of movement needed to achieve that kind of impact will generally be pretty rare.

The bigger challenge is how to deal with the assumption of the input dataset being normally distributed. While most financial markets (and indicators) do tend towards a normal distribution, they are almost never going to match that distribution exactly. So let's dig a bit deeper into distributions are defined and how things like trending markets can affect them.

Skew (skewness): This is a measure of asymmetry of the bell curve, or put another way, how and in what way the bell curve is disfigured when comparing the 2 halves. The easiest way to visualize this is to draw an imaginary vertical line through the apex of the bell curve, then fold the curve in half along that line. If both halves are exactly the same, the skew is 0 (no skew/perfectly symmetrical) - which is what a normal distribution has (skew = 0). Most financial markets tend to have short, medium, and long-term trends, and these trends will cause the distribution curve to skew in one direction or another. Bullish markets tend to skew to the right (positive), and bearish markets to the left (negative).

Kurtosis: This is a measure of the "tail size" of the bell curve. Another way to state this could be how "flat" or "steep" the bell-shape is. If the bell is steep with a strong drop from the apex (like a steep cliff), it has low kurtosis. If the bell has a shallow, more sweeping drop from the apex (like a tall hill), is has high kurtosis. Translating this to financial markets, kurtosis is generally a metric of volatility as the bell shape is largely defined by the strength and frequency of outliers. This is effectively a measure of volatility - volatile markets tend to have a high level of kurtosis (>3), and stable/consolidating markets tend to have a low level of kurtosis (<3). A normal distribution (our reference), has a kurtosis value of 3.

So to try and bring all that back together, here's a quick recap of the Standardization rescaling method:

The Standardization method has an assumption of a normal distribution of input data by using the mean (average) and standard deviation to handle the transformation

Most financial markets do NOT have a normal distribution (as discussed above), and will have varying degrees of skew and kurtosis

Q: Why are we still favoring the Standardization method over the Normalization method, and how are we accounting for the innate skew and/or kurtosis inherent in most financial markets?

A: Well, since we're only trying to rescale oscillators that by-definition have a midpoint of 0, kurtosis isn't a major concern beyond the affect it has on the post-transformation scaling (specifically, the number of standard deviations from the mean we need to include in our "artificially-bound" range definition).

Q: So that answers the question about kurtosis, but what about skew?

A: So - for skew, the answer is in the formula - specifically the mean (average) element. The standard mean calculation assumes a complete dataset and therefore uses a standard (i.e. simple) average, but we're limited by the data history available to us. So we adapted the transformation formula to leverage a moving average that included a weighting element to it so that it favored recent datapoints more heavily than older ones. By making the average component more adaptive, we gained the effect of reducing the skew element by having the average itself be more responsive to recent movements, which significantly reduces the effect historical outliers have on the dataset as a whole. While this is certainly not a perfect solution, we've found that it serves the purpose of rescaling the MACD and AO to a far more well-defined range while still preserving the oscillator behavior and mid-line exceptionally well.

The most difficult parts to compensate for are periods where markets have low volatility for an extended period of time - to the point where the oscillators are hovering around the 0/midline (in the case of the AO), or when the oscillator and signal lines converge and remain close to each other (in the case of the MACD). It's during these periods where even our best attempt at ensuring accurate mirrored-behavior when compared to the original can still occasionally lead or lag by a candle.

Note: If this is a make-or-break situation for you or your strategy, then we recommend you do not use any of the included indicators that leverage this kind of bounding technique (the AO and MACD at time of publication) and instead use the Trandingview built-in versions!

We know this is a lot to read and digest, so please take your time and feel free to ask questions - we will do our best to answer! And as always, constructive feedback is always welcome!

0DTE Watchlist0DTE Watchlist – Intraday Momentum Scanner

This script is a real-time multi-symbol intraday watchlist designed for 0DTE options and high-conviction day trades. It continuously scans up to 10 large-cap symbols for clean Opening Range Breakout (ORB) continuation setups using structure, VWAP alignment, and controlled risk parameters.

The indicator automatically:

Defines the Opening Range (customizable minutes after the open)

Detects bullish and bearish structure (higher highs/lows or lower lows/highs)

Confirms momentum with ORB breaks, retests, and liquidity sweeps

Applies an optional VWAP filter to avoid low-quality trades

Calculates ATR-based stop loss, TP1, and TP2 levels

Manages trades with break-even logic, cooldown periods, and session resets

All signals are displayed in a clean table dashboard, showing:

Current trade status (Call / Put / In Trade / Cooldown / Closed)

Live price, entry, stop loss, TP1, TP2

ORB high and low levels per symbol

How to use:

Add your preferred large-cap symbols (SPY, NVDA, META, etc.)

Use a 1–5 min chart for 0DTE scalping

Wait for the table to show “BUY CALL” or “BUY PUT”

Execute via your options platform and manage risk using the provided levels

Avoid trades during cooldown or outside regular market hours

This tool is optimized for clean trend days, institutional momentum, and continuation moves—not chop or mean-reversion noise.

SA Range Rank NQ 1.13.2026 PM SESSION15 MINUTE — PREPARE / POSITION MODE

Developer Note: Bias & Position Framing

This daily view is preparatory, not executable.

The purpose of the Daily timeframe is to define directional bias, not entries.

It helps frame which side of the market deserves attention and which activity should be ignored.

The goal here is context, not action.

________________________________________

Purpose on Daily

The Daily timeframe is used to:

• Define directional bias for the week

• Prepare position-building zones

• Identify environments where participation is unnecessary or elevated-risk

• Reduce overtrading by narrowing focus

Daily charts answer one question only:

“If I participate this week, which side makes sense?”

________________________________________

What Matters Most (Public View)

SA Range Indicator (RI):

→ Is the market transitioning or trending?

→ Is energy building, releasing, or rotating?

SA ZoneEngine (visual context only):

→ Are daily moves aligned with higher-timeframe structure?

→ Is price operating with or against dominant bias?

These visuals explain environment, not decisions.

________________________________________

How to Interpret Public Daily Posts

• Daily is not timing

• Daily is not execution

• Daily is not a signal

Daily charts prepare the trader mentally and structurally by clarifying:

• what deserves patience

• what deserves caution

• what deserves no attention at all

________________________________________

Messaging Line

“Daily charts prepare the trade — they don’t execute it.”

________________________________________

SEO Intent

daily equity bias, position preparation, market structure analysis

________________________________________

🤝 For Those Who Find Value

If these daily posts help you see the market more clearly:

• Follow, boost, and share my scripts, Ideas, and MINDS posts

• Feel free to message me directly with questions or build requests

• Constructive feedback and collaboration are always welcome

For traders who want to go deeper, optional memberships may include:

• Additional signal access

• Early previews

• Occasional free tools and upgrades

🔗 Membership & Signals

trianchor.gumroad.com

________________________________________

________________________________________

⏱ 15-MIN — PREPARE / POSITION MODE

Developer Note: Setup Formation Phase

The 15-minute timeframe is where setups begin to form, not where they are acted on.

This view exists to separate developing structure from noise.

________________________________________

Purpose on 15-Minute

The 15-minute timeframe is used to:

• Spot trap-prone conditions

• Identify developing structure

• Observe compression, rotation, or early expansion

• Prepare for execution — without acting

This timeframe answers a different question:

“Is something forming — or is this noise?”

________________________________________

What Matters Most (Public View)

SA Range Indicator (RI):

→ Compression → expansion transitions

→ Energy buildup vs premature release

SA CloudRegimes (visual only):

→ Whether price behavior reflects continuation, pullback, or contraction

→ Whether movement is controlled or impulsive

These visuals describe behavior, not entries.

________________________________________

How to Interpret Public 15-Minute Posts

• 15m is setup formation

• 15m is environmental awareness

• 15m is not execution

Most errors occur when traders act before structure has finished forming.

This timeframe exists to slow that impulse down.

________________________________________

Messaging Line

“Preparation happens before the move — not during it.”

________________________________________

________________________________________

🤝 For Those Who Find Value

If these posts help you better recognize developing structure:

• Follow, boost, and share my scripts, Ideas, and MINDS posts

• Feel free to message me directly with questions or build requests

• Constructive feedback and collaboration are always welcome

For traders who want to go deeper, optional memberships may include:

• Additional signal access

• Early previews

• Occasional free tools and upgrades

🔗 Membership & Signals

trianchor.gumroad.com

15 Minute (15m) — Tactical Entry Alignment / “Permission + Timing”

Goal: Convert higher-timeframe permission into tradable timing.

How to use:

• Trade the first clean reclaim after a pullback.

• Avoid taking a reclaim if price is already extended far beyond the wake edge (late reclaim).

Best conditions:

• Works extremely well when:

o 1H agrees

o session structure is active (open/close windows)

o reclaim occurs near VWAP or a key level you already respect

Settings:

• dispMult 0.75–1.05

• reclaimWindow 6–14

• cooldown 3–6

🟠 15-MINUTE — Intraday Structure & Session Logic

1️⃣ Range Indicator (RI)

• Session compression → impulse likely

• Expansion → follow, don’t fade

Use:

Defines session behavior.

________________________________________

2️⃣ ZoneEngine (Structure)

• Filters session traps

• Explains failed breakouts

Use:

Keeps you aligned with real participation.

________________________________________

3️⃣ Cloud / Reclaim (Behavior)

• Identifies pullback vs continuation

• Reclaim confirms acceptance

Use:

Contextual confirmation.

________________________________________

4️⃣ Stop-Hunt Proxy

• Session liquidity sweeps

• Common near opens and transitions

Use:

Stop-hunt + compression = likely session impulse.

Range Indicator Golden Pocket, Liquidity, FairValueGapOverview

This indicator is a comprehensive institutional market structure toolkit. It is designed to identify high-probability reversal zones by merging three powerful technical analysis concepts: Fibonacci Golden Pockets (61.8% - 65%), Liquidity Pool Analysis (Swing Failure Patterns), and Fair Value Gaps (FVG). By automating the detection of price inefficiencies and "stop runs," it helps traders navigate complex price action with objective, rule-based confirmation.

What the Script Does

The script continuously monitors a user-defined lookback period to define a trading range. Within this range, it dynamically plots:

Golden Pockets: High-confluence retracement zones (calculated as 0.35 - 0.382 internal range levels).

Liquidity Zones: Highlighted regions at the absolute high and low (Top/Bottom 5%) where institutional orders and retail stops are typically concentrated.

Swing Failure Patterns (SFP): Real-time detection of liquidity grabs where price breaches a range extreme but fails to close outside, signaling a potential trap.

Fair Value Gaps (FVG): Visualizes 3-candle price imbalances, showing areas of aggressive buying or selling that often act as future magnets or support/resistance.

2-Candle Confirmation: A momentum-based filter requiring a candle-close confirmation before a reversal signal is generated.

For Whom is it?

Smart Money Concepts (SMC) & ICT Students: Traders looking for automated liquidity sweeps and market inefficiencies.

Fibonacci & Mean Reversion Traders: Those seeking a clean, professional visualization of the Golden Pocket across multiple timeframes.

Systematic Day Traders: Who require strict price-action confirmation (SFP and 2-candle rules) to remove emotional bias from their entries.

Functions and Input Options

1. Market Structure & Visuals

Lookback Period (Default: 100): Defines the window for calculating the range extremes.

Box Offset Right (Default: 50): Extends all zones into the future for better anticipatory trading.