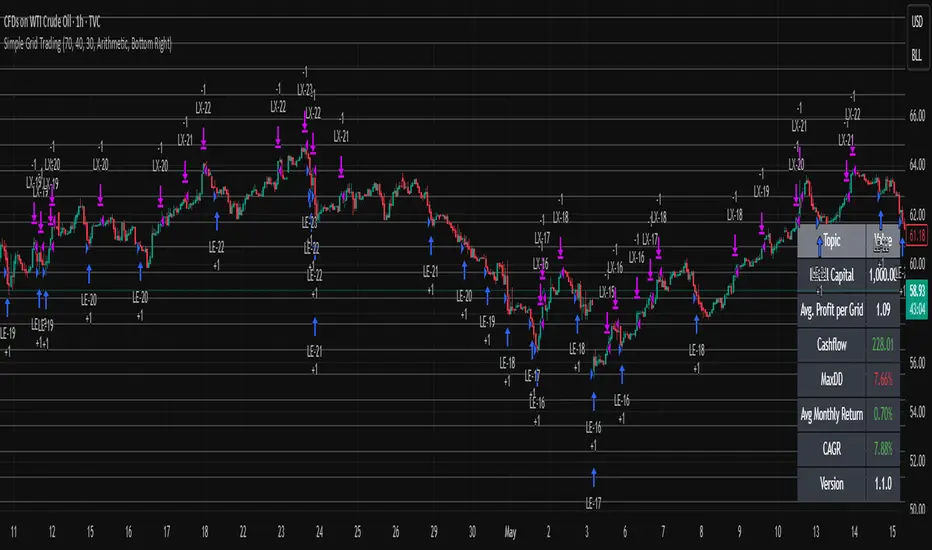

Simple Grid Trading v1.0 [PUCHON]Simple Grid Trading v1.0

Overview

This is a Long-Only Grid Trading Strategy developed in Pine Script v6 for TradingView. It is designed to profit from market volatility by placing a series of Buy Limit orders at predefined price levels. As the price drops, the strategy accumulates positions. As the price rises, it sells these positions at a profit.

Features

Grid Types : Supports both Arithmetic (equal price spacing) and Geometric (equal percentage spacing) grids.

Flexible Order Management : Uses strategy.order for precise control and prevents duplicate orders at the same level.

Performance Dashboard : A real-time table displaying key metrics like Capital, Cashflow, and Drawdown.

Advanced Metrics : Includes Max Drawdown (MaxDD) , Avg Monthly Return , and CAGR calculations.

Customizable : Fully adjustable price range, grid lines, and lot size.

Dashboard Metrics

The dashboard (default: Bottom Right) provides a quick snapshot of the strategy's performance:

Initial Capital : The starting capital defined in the strategy settings.

Lot Size : The fixed quantity of assets purchased per grid level.

Avg. Profit per Grid : The average realized profit for each closed trade.

Cashflow : The total realized net profit (closed trades only).

MaxDD : Maximum Drawdown . The largest percentage drop in equity (realized + unrealized) from a peak.

Avg Monthly Return : The average percentage return generated per month.

CAGR : Compound Annual Growth Rate . The mean annual growth rate of the investment over the specified time period.

Strategy Settings (Inputs)

Grid Settings

Upper Price : The highest price level for the grid.

Lower Price : The lowest price level for the grid.

Number of Grid Lines : The total number of levels (lines) in the grid.

Grid Type :

Arithmetic: Distance between lines is fixed in price terms (e.g., $10, $20, $30).

Geometric: Distance between lines is fixed in percentage terms (e.g., 1%, 2%, 3%).

Lot Size : The fixed amount of the asset to buy at each level.

Dashboard Settings

Show Dashboard : Toggle to hide/show the performance table.

Position : Choose where the dashboard appears on the chart (e.g., Bottom Right, Top Left).

How It Works

Initialization : On the first bar, the script calculates the price levels based on your Upper/Lower price and Grid Type.

Entry Logic :

The strategy places Buy Limit orders at every grid level below the current price.

It checks if a position already exists at a specific level to avoid "stacking" multiple orders on the same line.

Exit Logic :

For every Buy order, a corresponding Sell Limit (Take Profit) order is placed at the next higher grid level.

MaxDD Calculation :

The script continuously tracks the highest equity peak.

It calculates the drawdown on every bar (including intra-bar movements) to ensure accuracy.

Displayed as a percentage (e.g., 5.25%).

Disclaimer

This script is for educational and backtesting purposes only. Grid trading involves significant risk, especially in strong trending markets where the price may move outside your grid range. Always use proper risk management.

Tìm kiếm tập lệnh với "track"

Tradermaap Elite System [Institutional Grade Analysis]Description:

🚀 Institutional Trend Modeling & Automated Risk Engine

Tradermaap Elite is a proprietary quantitative trading system designed for professional scalpers, swing traders, and prop firm challengers. It moves beyond standard indicators by utilizing a Dynamic Mean Reversion Algorithm to identify high-probability structural turning points in the market.

This is NOT just a buy/sell arrow tool. It is a complete Decision Support System that mathematically calculates your risk, entry, and exit zones based on institutional order flow concepts.

🛠️ Key Features

✅ 100% Non-Repainting Engine: Signals are locked on candle close. No disappearing acts. ✅ Institutional Baseline Logic: Uses a proprietary blend of long-term trend filters to avoid false signals in choppy markets. ✅ Auto Risk Guard: Automatically calculates Position Size based on your account balance and defined risk (1% Prop Mode). ✅ Multi-Asset Calibration: Algorithmically tuned for Bitcoin, Gold, Indices (US30/NAS100), and Equities. ✅ Live Dashboard: Tracks real-time Win Rate and Profit Factor directly on your chart. ✅ Dynamic Currency: Switch between USD ($) and INR (₹) in settings.

🧠 How It Works (The Logic)

The system operates on a 3-Stage "Confluence" Mechanism:

Macro Trend Identification: The algorithm scans for the dominant market direction using a Weighted Trend Filter.

Equilibrium Reversion: It identifies when price is "overextended" and waits for it to return to the "Value Zone" (Discount/Premium levels).

Volatility Trigger: A trade is only validated when specific volume and price action conditions are met, filtering out weak moves.

Projected Outcomes:

Protective Stop: Structure-based invalidation levels.

Target 1: Conservative banking zones.

Target 2: Trend-following extensions.

🔒 Access & Licensing

This operates as a Protected Algorithm. It is strictly Invite-Only. To obtain a license key or start a trial, please refer to the link in the signature below.

⚠️ RISK DISCLAIMER: This script is for educational and chart analysis purposes only. It incorporates mathematical modeling to assist in decision-making but does not guarantee profits. Trading is inherently risky. Use responsibly.

EMA Velocity Dual TF Momentum 1h (v2)BINANCE:SOLUSDT

The result is calculated on futures x10

### EMA Velocity Dual TF Momentum (v2) – Public Description

**Overview**

EMA Velocity Dual TF Momentum (v1) is a trend-following momentum strategy that uses the *speed of change* of Exponential Moving Averages (EMA) on two timeframes: the chart timeframe 1h.

The strategy looks for moments when both timeframes point in the same direction and the short‑term momentum is significantly stronger than usual, then manages trades with configurable ATR filtering, stop‑loss / take‑profit and early exit logic.

---

### Core Idea (high level, without formulas)

- On the **lower timeframe** (LTF), the strategy tracks how fast the EMA is moving (its “velocity”) and detects **impulse bars** where this velocity is unusually strong compared to its recent history.

- On the **higher timeframe** (HTF), it also measures EMA velocity and requires that the HTF trend direction is **aligned** with the LTF (both bullish or both bearish), if enabled.

- A **long trade** is opened when:

- LTF EMA velocity is positive (upward momentum),

- LTF momentum is strong enough (impulse),

- HTF EMA velocity is also upwards (if HTF filter is enabled),

- and ATR‑based volatility is above the minimum threshold.

- A **short trade** is opened in the symmetric situation (downward momentum on both timeframes).

- Positions are closed using configurable stop‑loss and take‑profit, and can be partially exited, moved to break‑even and trailed using early‑exit options.

---

### Inputs and Parameters

#### Trend & Momentum (Lower Timeframe)

- **`LTF EMA length (emaLenLTF)`**

Length of the EMA on the chart timeframe used to measure short‑term trend and momentum. Smaller values react faster; larger values are smoother and slower.

- **`LTF velocity lookback (velKLTF)`**

Lookback for computing EMA “velocity” on LTF. Controls how sensitive the momentum calculation is to recent price changes.

- **`LTF impulse lookback bars (impLookback)`**

Window size used to estimate the “normal” average absolute velocity. The strategy compares current momentum against this baseline to detect strong impulse moves.

- **`LTF |velocity| multiplier vs average (impMult)`**

Multiplier for defining what counts as a strong impulse. Higher values = fewer but stronger signals; lower values = more frequent, weaker impulses.

#### Trend & Momentum (Higher Timeframe)

- **`Use higher timeframe alignment (useHTF)`**

If enabled, trades are only taken when the higher‑timeframe EMA velocity confirms the same direction as the lower timeframe.

- **`HTF timeframe (htf_tf)`**

Higher timeframe used for confirmation (e.g. 60 minutes). Defines the “macro” context above the chart timeframe.

- **`HTF EMA length (emaLenHTF)`**

Length of the EMA on the higher timeframe. Controls how smooth and slow the higher‑timeframe trend filter is.

- **`HTF velocity lookback (velKHTF)`**

Lookback for the EMA velocity on HTF. Smaller values react quicker to changes in the higher‑timeframe trend.

#### Volatility / ATR Filter

- **`Use ATR filter (useAtrFilter)`**

Enables a volatility filter based on Average True Range. When active, trades are allowed only if market volatility is not too low.

- **`ATR Period (atrPeriod)`**

Lookback period for ATR calculation. Shorter periods react faster to recent volatility shifts; longer ones are more stable.

- **`ATR Min % for trading (atrMinPerc)`**

Minimum ATR as a percentage of price required to trade. Filters out very quiet, choppy periods where the strategy is more likely to be whipsawed.

#### Risk Management

- **`Use stops (SL/TP) (useStops)`**

Enables fixed stop‑loss and take‑profit exits. If disabled, positions are managed only by early exit logic and manual closing.

- **`Stop Loss % (stopLossPerc)`**

Distance of the protective stop from entry, in percent. Higher values give trades more room but increase risk per trade.

- **`Take Profit % (takeProfitPerc)`**

Distance of the primary profit target from entry, in percent. Controls the reward‑to‑risk profile of each trade.

#### Early Exit / Break‑Even / Trailing

- **`Enable early exit module (useEarlyExit)`**

Master switch for all early exit features: partial profit taking, break‑even stops and trailing exits.

- **`Take partial profit at +% (close 50%) (partialTP)`**

Profit level (in %) at which the strategy closes a partial portion of the position (e.g. 50%), locking in gains while leaving a runner.

- **`Trailing TP distance (%) (trailTP)`**

Distance (in %) for dynamic trailing stop after entry. When positive, the strategy trails the price to protect profits as the move extends.

- **`Break-even stop after +% profit (useBreakEven)`**

Enables automatic move of the stop to the entry price once a certain profit threshold is reached.

- **`Break-even activation (+%) (breakEvenPerc)`**

Profit level (in %) at which the stop is moved to break‑even. Higher values require a larger unrealized profit before break‑even protection kicks in.

#### Visuals

- **`Show labels (showLabels)`**

Toggles on‑chart labels that mark long and short entry signals for easier visual analysis.

- **`Label offset (labelOffset)`**

Horizontal offset (in bars) for placing labels relative to the signal bar. Used only for visual clarity; does not affect trading logic.

---

Если нужно, могу на основе этого текста сразу подготовить компактную версию (ограниченную по символам) специально под поле описания публичного скрипта в TradingView.

Alpha VWAP Regime🔥 Alpha VWAP Regime — Institutional VWAP Strategy (Closed Source)

Alpha VWAP Regime is a multi-layered VWAP trading system that identifies the active market regime and adapts its signals based on institutional liquidity behavior.

This strategy is closed-source because it uses a proprietary combination of VWAP structures, anchored pivot logic, band deviations, and regime detection filters that are not publicly available.

🧠 How the Strategy Works (Conceptual Explanation)

This strategy does not rely on a single VWAP line.

Instead, it builds a VWAP matrix consisting of:

1) Session VWAP

Defines fair value for the current session.

Used to detect intraday directional bias.

2) Anchored VWAP (AVWAP)

Automatically anchored to swing highs and lows (pivot-based).

Tracks where large players accumulated or distributed positions.

3) VWAP Bands (±1σ and ±2σ)

Used as dynamic volatility envelopes:

±1σ = fair-value zone / no-trade area

±2σ = mean-reversion extremes

4) Market Regime Classification (ADX-based)

The strategy determines which environment the market is in:

Trending Regime: ADX above threshold

Ranging Regime: ADX below threshold

Breakout Regime: Volume-based breakout of AVWAP

Each regime activates a different entry model.

📌 Entry Logic (High-Level Overview)

Trend Mode

Triggered only when ADX confirms a trend.

Entries occur near VWAP or −1σ using price-action confirmation.

Mean Reversion Mode

Activated when the market is ranging.

Entries target the ±2σ deviation bands.

Breakout Mode

Triggered by price crossing AVWAP with above-average volume.

Used to catch institutional continuation moves.

ALL Mode

Combines the three models for a full adaptive system.

📉 Exits & Risk Management

All stops and targets use ATR-based volatility sizing

Trend trades aim for larger targets

Mean-reversion trades aim for smaller snapback moves

Breakouts use wider stops but high R:R

🔍 How to Use the Strategy

Load the script on a clean chart

Choose your preferred regime mode (Trend / MR / Breakout / ALL)

Optionally hide VWAP indicators and display signals only

Use realistic position sizing and commissions

Evaluate performance across multiple assets and timeframes

🔒 Why It Is Closed-Source

The code uses:

A custom anchoring engine

Multi-layered regime filters

Dynamic VWAP matrix

Prop logic for bias scoring

These components were built from scratch and form a unique decision model, so the source is protected.

🇸🇦 الشرح العربي لاستراتيجية Alpha VWAP Regime

Alpha VWAP Regime هي استراتيجية تداول مؤسسية متقدمة تعتمد على تحليل السيولة، وتحديد حالة السوق (Market Regime)، ودمج عدة طبقات من VWAP داخل نموذج واحد متكيف.

الهدف من الاستراتيجية هو التداول في المناطق التي يتواجد فيها المال الذكي، وتجنب التداول في المناطق العشوائية أو منخفضة الجودة.

________________________________________

🧠 كيف تعمل الاستراتيجية؟

الاستراتيجية لا تعتمد على VWAP واحد، بل تستخدم “مصفوفة VWAP” كاملة تتكوّن من:

1) VWAP اليومي (Session VWAP)

يُستخدم لتحديد القيمة العادلة خلال الجلسة، وتحديد الاتجاه اللحظي (Intraday Bias).

________________________________________

2) VWAP المثبّت (Anchored VWAP)

يتم تثبيته تلقائيًا على:

• القمم المهمة (Swing Highs)

• القيعان المهمة (Swing Lows)

ويساعد في تحديد مناطق تمركز المؤسسات، ومناطق الانعكاس أو الاختراقات الحقيقية.

________________________________________

3) نطاقات VWAP (±1σ و ±2σ)

تُستخدم كأغلفة ديناميكية للسيولة والتقلب:

• ±1σ = منطقة القيمة العادلة (Fair-Value Zone)

→ غالبًا منطقة غير مناسبة للتداول (No-Trade Zone)

• ±2σ = مناطق التشبّع الحركي (Extremes)

→ مناسبة لاستراتيجيات الانعكاس (Mean Reversion)

________________________________________

4) تصنيف حالة السوق Market Regimes

الاستراتيجية تستخدم مؤشر ADX لتحديد حالة السوق الحالية:

حالة السوق الوصف

Trending اتجاه واضح وقوي

Ranging تذبذب بدون اتجاه

Breakout اختراق مدعوم بحجم تداول

كل Regime يفعّل نموذج دخول مختلف داخل الاستراتيجية.

________________________________________

🎯 نماذج الدخول داخل الاستراتيجية

1) نموذج الاتجاه (Trend Mode)

يعمل فقط عندما يكون السوق في اتجاه حقيقي.

يعتمد على دخول Pullbacks قرب VWAP أو نطاق −1σ مع تأكيد شموعي.

________________________________________

2) نموذج الانعكاس (Mean Reversion Mode)

يعمل فقط عندما يكون السوق متذبذبًا (Range).

الدخول عند لمس ±2σ بهدف العودة نحو VWAP.

________________________________________

3) نموذج الاختراق (Breakout Mode)

يستخدم اختراقات Anchored VWAP

ولكن بشرط وجود حجم تداول أعلى من المتوسط (Volume Confirmation).

________________________________________

4) وضع الدمج (ALL Mode)

يجمع بين النماذج الثلاثة ويجعل الاستراتيجية متكيفة تلقائيًا مع كل حالات السوق.

________________________________________

📉 الخروج وإدارة المخاطر

تستخدم الاستراتيجية نظامًا ديناميكيًا لإدارة المخاطر:

• وقف الخسارة مبني على ATR

• الأهداف مبنية على طبيعة النموذج

• الصفقات الاتجاهية تستهدف R:R أعلى

• صفقات MR أقصر وأسرع

• صفقات Breakout أوسع ولكن مدعومة بزخم قوي

________________________________________

🧩 كيفية استخدام الاستراتيجية

1. ضع الاستراتيجية على رسم بياني نظيف بدون مؤشرات إضافية

2. اختر نموذج الدخول المناسب من الإعدادات

3. فعّل أو أخفِ خطوط VWAP حسب الحاجة

4. استخدم إعدادات مخاطرة واقعية

5. اختبر الاستراتيجية على عدة أسواق وفريمات

________________________________________

🔒 سبب إغلاق الكود

تم إغلاق الكود لأنها تعتمد على:

• محرك تثبيت AVWAP خاص

• نظام Regime Detection متقدم

• مصفوفة VWAP متعددة الطبقات

• منطق دخول/خروج خاص تم تطويره بالكامل

كل ذلك يتطلب حماية الملكية الفكرية، لذا تم نشرها Closed-Source.

GOLDM Dow Theory – 1H Trend + 5m Pullback1. Strategy Overview

Instrument: MCX GOLDM

Chart timeframe: 5 minutes

Side: Long-only

Position size: Fixed 3 lots

Core idea:

Trade only in 1H uptrend, enter after a 5m pullback and breakout, with basic volume/volatility filters and ATR-based SL/TP.

2. High-Level Logic Flow (Per Bar)

On every 5-minute bar, the script does this:

Update session/time, volume, and ATR filters

Read 1H trend from higher timeframe

Update 5m pullback state (whether a valid dip happened)

Check if there is a valid breakout back in the direction of the 1H trend

If all filters + conditions align → enter Long (3 lots)

While in a trade:

Manage SL/TP using ATR

Close trade if 1H trend flips down or price closes below 5m EMA

Everything else (plots, alerts) is just for visibility and convenience.

3. Inputs & Configuration

Main inputs:

pullbackLookback – how many 5m bars to look back to detect a pullback

breakoutLookback – how many bars to consider for recent swing high

emaLenTrendFast / emaLenTrendSlow – 1H EMAs (50/200) for trend

emaLenPullback – 5m EMA used for pullback logic (default 20)

tradeSession – default "0900-2315" (you can change)

volLookback, volMult – volume filter

atrLen, atrSmaLen – ATR filter

slATRmult (1.4), tpATRmult (3.0) – ATR multiples → ~1.4 : 3 RR

4. Session / Time Filter

tradeSession = "0900-2315"

inSession = not useSessionFilter or not na(time(timeframe.period, tradeSession))

Only allows entries when the current bar’s time is inside 09:00–23:15.

If useSessionFilter is false, this filter is ignored.

No trade opens outside this window, but existing trades can still exit.

5. Volume & Volatility Filters

Volume Filter

avgVol = ta.sma(volume, volLookback)

highVolume = not useVolumeFilter or (volume > avgVol * volMult)

If enabled, current bar’s volume must be greater than average volume × multiplier.

Purpose: avoid thin, illiquid periods.

ATR Filter

atr5 = ta.atr(atrLen)

atrSma = ta.sma(atr5, atrSmaLen)

goodATR = not useATRFilter or (atr5 > atrSma)

If enabled, current ATR must be above its own moving average.

Purpose: avoid flat / extremely low-volatility periods.

Only if both highVolume and goodATR are true, the system considers entering.

6. Higher Timeframe Trend (1H)

emaFast1h = request.security(syminfo.tickerid, "60", ta.ema(close, emaLenTrendFast), ...)

emaSlow1h = request.security(syminfo.tickerid, "60", ta.ema(close, emaLenTrendSlow), ...)

trendUp = emaFast1h > emaSlow1h

trendDown = emaFast1h < emaSlow1h

On the 1-hour timeframe:

If EMA Fast (50) > EMA Slow (200) → trendUp = true

If EMA Fast (50) < EMA Slow (200) → trendDown = true

This is the core trend filter:

We only look for longs when trendUp is true.

7. 5-Minute Structure Logic (Dow-style)

7.1 Pullback Detection

emaPull = ta.ema(close, emaLenPullback)

pulledBackLong = ta.lowest(close, pullbackLookback) < emaPull

A pullback is defined as:

In the last pullbackLookback bars, price closed below the 5m EMA (emaPull) at least once.

This indicates a dip against the 1H uptrend.

A state flag tracks this:

var bool hadLongPullback = false

hadLongPullback := trendUp and pulledBackLong ? true : (not trendUp ? false : hadLongPullback)

When:

trendUp AND pulledBackLong → hadLongPullback = true.

If the trend stops being up (trendUp = false), flag resets to false.

So the system remembers:

“There has been a proper dip while the 1H uptrend is active.”

7.2 Breakout Confirmation

recentHigh = ta.highest(high, pullbackLookback)

breakoutUp = close > recentHigh

After a pullback, we wait for price to close above the highest high of recent bars (excluding the current one).

This mimics:

“Higher high after a higher low” → breakout in Dow Theory terms.

8. Final Long Entry Logic

The base entry condition:

baseLongEntry =

trendUp and

hadLongPullback and

breakoutUp and

close > emaPull

Translated:

1H trend is up (trendUp).

A valid pullback happened recently (hadLongPullback).

Current candle broke above the recent swing high (breakoutUp).

Price is now back above the 5m EMA (pullback is resolving, not deepening).

Then filters are applied:

longEntryCond =

baseLongEntry and

inSession and

highVolume and

goodATR and

not isLong

So a long entry only occurs if:

Core structure conditions (baseLongEntry) are true

Time is within session

Volume is high enough

ATR is healthy

You are not already in a long

When longEntryCond is true:

if longEntryCond

strategy.entry("Long", strategy.long, comment = "Dow Long: Trend+PB+BO")

hadLongPullback := false

Enters 3 lots long (as per default_qty_type + default_qty_value).

Resets hadLongPullback so we don’t re-use the same pullback.

9. Exit Logic

There are two exit layers:

9.1 Logical Exit (Trend or Structure Change)

exitLongTrendFlip = trendDown

exitLongEMA = ta.crossunder(close, emaPull)

longExitCond = isLong and (exitLongTrendFlip or exitLongEMA)

If in a long:

Exit when trend flips down (1H EMA50 < EMA200), OR

Price crosses below 5m EMA (pullback may be turning into reversal).

Then:

if longExitCond

strategy.close("Long", comment = "Exit Long: Trend flip / EMA break")

This closes the position at market (on bar close).

9.2 ATR-based Stop Loss & Take Profit

if useSLTP and isLong

longStop = strategy.position_avg_price - atr5 * slATRmult

longLimit = strategy.position_avg_price + atr5 * tpATRmult

strategy.exit("Long SLTP", "Long", stop = longStop, limit = longLimit)

SL = entry price – 1.4 × ATR(14, 5m)

TP = entry price + 3.0 × ATR(14, 5m)

This gives roughly 1.4 : 3 RR.

If SL or TP is hit, strategy.exit will close the trade.

So exits can come from:

Hitting Stop Loss

Hitting Take Profit

OR logic-based exit (trend flip / EMA break)

10. Alerts

Two alertconditions:

alertcondition(longEntryCond, title="Long Entry Signal",

message="GOLDM LONG: 1H Uptrend + 5m Pullback Breakout + Filters OK")

alertcondition(longExitCond, title="Long Exit Signal",

message="GOLDM LONG EXIT: Trend flip or EMA break")

You can set TradingView alerts based on:

“Long Entry Signal” → tells you when all entry conditions align.

“Long Exit Signal” → tells you when the logic-based exit triggers.

(ATR SL/TP exits won’t auto-alert unless you separately set price alerts or add extra conditions.)

11. Mental Model Summary (How YOU should think about it)

For every trade, the system is basically doing this:

Is GOLDM in an uptrend on 1H?

→ If no: do nothing

Did we get a clear dip below 5m EMA in that uptrend?

→ If no: wait

Did price then break above recent highs and reclaim EMA20?

→ If yes: this is our Dow-style continuation entry

Is market liquid and moving (volume + ATR)?

→ If yes: go Long with 3 lots

Manage with:

ATR SL & TP

Exit early if 1H trend flips or price falls back below EMA20

FVG Session Break Strategy with ATR RR🧠 FVG Session Break Strategy with ATR RR — Timezone-Aware, Session-Savvy, and Risk-Calibrated

This strategy captures high-probability reversals and continuations by combining Fair Value Gap (FVG) imbalances with session-based breakout logic and ATR-calibrated risk management. It’s designed for traders who want to exploit structural inefficiencies during key market sessions — with precision and portability across global exchanges.

🔍 Core Logic:

Fair Value Gap Detection: Identifies bullish and bearish FVGs using a 3-bar displacement pattern.

Session Breakout Engine: Tracks session highs and lows (Asian, London, NY) and triggers trades only when price breaks these levels — ensuring trades occur at meaningful inflection points.

ATR-Based RR Control: Dynamically sizes stop-loss and take-profit levels using ATR × multiplier, maintaining consistent risk across volatility regimes.

🌐 Timezone-Aware Session Logic:

Session boundaries are defined in UTC-5 (e.g., NY: 0930–1600) but automatically converted to the exchange’s local timezone using timestamp("Etc/GMT+5", ...). This ensures:

Accurate session detection across all markets and assets

No manual timezone adjustments needed

Robust performance on crypto, forex, and global equities

📈 Visuals:

Session highs and lows plotted in orange

Bullish and bearish FVGs marked with green and red triangles

Strategy entries and exits shown on chart with full RR logic

This strategy is ideal for traders who want to combine structural edge with session context and disciplined risk.

nOI + Funding + CVD • strategynOI + Funding + CVD Strategy

Overview

This strategy is designed for cryptocurrency trading on platforms like TradingView, focusing on perpetual futures markets. It combines three key indicators—Normalized Open Interest (nOI), Funding Rate, and Cumulative Volume Delta (CVD)—to generate buy and sell signals for long and short positions. The strategy aims to capitalize on market imbalances, such as overextended open interest, funding rate extremes, and volume deltas, which often signal potential reversals or continuations in trending markets.

The script supports pyramiding (up to 10 positions), uses percentage-based position sizing (default 10% of equity per trade), and allows customization of trade directions (longs and shorts can be enabled/disabled independently). It includes multiple signal systems for entries, various exit mechanisms (including stop-loss, take-profit, time-based exits, and conditional closes based on indicators), a Martingale add-on system for averaging positions during drawdowns, and handling of opposite signals (ignore, close, or reverse).

This strategy is not financial advice; backtest thoroughly and use at your own risk. It requires data sources for Open Interest (OI) and Funding Rates, which are fetched via TradingView's security functions (e.g., from Binance for funding premiums).

Key Indicators

1. Normalized Open Interest (nOI)

Group: Open Interest

Purpose: Measures the relative level of open interest over a lookback window to identify overbought (high OI) or oversold (low OI) conditions, which can indicate potential exhaustion in trends.

Calculation:

Fetches OI data (close) from the symbol's standard ticker (e.g., "{symbol}_OI").

Normalizes OI within a user-defined window (default: 500 bars) using min-max scaling: (OI - min_OI) / (max_OI - min_OI) * 100.

Upper threshold (default: 70%): Signals potential short opportunities when crossed from above.

Lower threshold (default: 30%): Signals potential long opportunities when crossed from below.

Visualization: Plotted as a line (teal above upper, red below lower, gray in between). Horizontal lines at upper, mid (50%), lower, and a separator at 102%.

Notes: Handles non-crypto symbols by adjusting timeframe to daily if intraday. Errors if no OI data available.

2. Funding Rate

Group: Funding Rate

Purpose: Tracks the average funding rate (premium index) to detect market sentiment extremes. Positive funding suggests bull bias (longs pay shorts), negative suggests bear bias.

Calculation:

Fetches premium index data from Binance (e.g., "binance:{base}usdt_premium").

Supports lower timeframe aggregation (default: enabled, using 1-min TF) for smoother data.

Averages open and close premiums, clamps values, and scales/shifts for plotting (base: 150, scale: 1000x).

Upper threshold (default: 1.0%): Overheat for shorts.

Lower threshold (default: 1.0%): Overcool for longs.

Ultra level (default: 1.8%): Extreme for additional short signals.

Smoothing: Uses inverse weighted moving average (IWMA) or lower-TF aggregation to reduce noise.

Visualization: Shifted plot (green positive, red negative) with filled areas. Horizontal lines for overheat, overcool, base (0%), and ultra.

Notes: Custom ticker option for non-standard symbols.

3. Cumulative Volume Delta (CVD)

Group: CVD (Cumulative Volume Delta)

Purpose: Measures net buying/selling pressure via volume delta, normalized to identify divergences or confirmations with price.

Calculation:

Delta: +volume if close > open, -volume if close < open.

Cumulative: Rolling cumsum over a window (default: 500 bars), smoothed with EMA (default: 20).

Normalized: Scaled by absolute max in window (-1 to 1 range).

Scaled/shifted for plotting (base: 300 or 0 if anchored, scale: 120x).

Upper threshold (default: 1.0%): Over for shorts.

Lower threshold (default: 1.0%): Under for longs.

Visualization: Shifted plot (aqua positive, purple negative) with filled areas. Horizontal lines for over, under, and separator (default: 252).

Filter Options (for Signal A):

Enable filter (default: false).

Require sign match (Long ≥0, Short ≤0).

Require extreme zones.

Require momentum (rising/falling over N bars, default: 3).

Signal Logics for Entries

Entries are triggered by buy/sell signals from multiple systems (A, B, C, D), filtered by direction toggles and entry conditions.

Signal System A: OI + Funding (with optional CVD filter)

Enabled: Default true.

Sell (Short): nOI > upper threshold, falling over N bars (default: 3), delta ≥ threshold (default: 3%), funding > overheat, and CVD filter OK.

Buy (Long): nOI < lower threshold, rising over N bars (default: 3), delta ≥ threshold (default: 3%), funding < overcool, and CVD filter OK.

Signal System B: Short - Funding Crossunder + Filters

Enabled: Default true.

Sell (Short): Funding crosses under overheat level, optional: CVD > over, nOI < upper.

Signal System C: Short - Ultra Funding

Enabled: Default false.

Sell (Short): Funding crosses ultra level (up or down, both default true).

Signal System D: Long - Funding Crossover + Filters

Enabled: Default true.

Buy (Long): Funding crosses over overcool level, optional: CVD < under, nOI > lower.

Combined: Sell if A/B/C active; Buy if A/D active.

Entry Filters

Cooldown: Optional pause between entries (default: false, 3 bars).

Max Entries: Limit pyramiding (default: true, 6 max).

Entries only if both filters pass and direction allowed.

Opposite Signal Handling

Mode: Ignore (default), Reverse (close and enter opposite), or Close (exit only).

Processed before regular entries.

Position Management

Martingale (3 Steps):

Enabled per step (default: all true).

Triggers add-ons at loss levels (defaults: 5%, 8%, 11%) by adding % to position (default: 100% each).

Resets on position close.

Break Even:

Enabled (default: true).

Activates at profit threshold (default: 5%), sets SL better by offset (default: 0.1%).

Exit Systems

Multiple exits checked in sequence.

Exit 1: SL/TP

Enabled: Separate for long/short (default: true).

SL: % from avg price (defaults: 1% long/short).

TP: % from avg price (defaults: 2% long/short).

Exit 2: Funding

Enabled: Separate for long (up) / short (down) (default: true).

Long Exit: Funding > upper exit threshold (default: 0.8%).

Short Exit: Funding < lower exit threshold (default: 0.8%).

Exit 3: nOI

Enabled: Separate for long (up) / short (down) (default: true).

Long Exit: nOI > upper exit (default: 85%).

Short Exit: nOI < lower exit (default: 15%).

Exit 4: Global SL

Enabled: Default true.

Exit: If position loss ≥ % (default: 7%).

Exit 5: Break Even (integrated in position block)

Exit 6: Time Limit

Enabled: Separate for long/short (default: true).

Exit: After N bars in trade (defaults: 30 each).

Timer updates on add-ons if enabled (default: true).

Visual Elements

Buy/Sell Labels: Small labels ("BUY"/"SELL") on bars with signals, limited to last 30.

All indicators plotted on a separate pane (overlay=false).

Usage Notes

Backtesting: Adjust parameters based on asset/timeframe. Test on historical data.

Data Requirements: Works best on crypto perps with OI and funding data.

Risk Management: Incorporates SL/TP and global SL; monitor drawdowns with Martingale.

Customization: All thresholds, enables, and scales are inputs for fine-tuning.

Version: Pine Script v6.

For questions or improvements, contact the author. Happy trading!

Turtles StrategyBorn from the 1980s "Turtle" experiment, this method of trading captures breakouts and places or closes trades with intrabar entries or exits and realized-equity risk controls.

How It Works

The strategy buys/sells on breakouts from recent highs/lows, using ATR for volatility-adjusted stops and sizing. It risks a fixed % (default 1%) of realized equity per trade—initial capital plus closed P&L, ignoring open positions for conservatism. Drawdown protection auto-reduces risk by 20% at 10% drops (up to three times), resetting only on full peak recovery. Single positions only, with 1-tick slippage simulated for realistic fills. Best for trending assets like forex,commodities, crypto, stocks. Backtest for optimal parameters.

Main Operations

The strategy works on any timeframe but it's meant to be used on daily charts.

Entry Signals:

Long: Buy-stop 1 tick above 20-bar high (default "Entry Period") when no position—enters intrabar on breakout.

Short: Sell-stop 1 tick below 20-bar low. OCA cancels opposites.

Size: (Realized equity × adjusted risk %) ÷ (2× ATR stop distance), scaled by point value.

Exit Signals:

Longs: Stop at tighter of (entry - 2× ATR) or (10-bar low - 1 tick trailing, default "Exit Period").

Shorts: Stop at tighter of (entry + 2× ATR) or (10-bar high + 1 tick trailing).

Locks profits in trends, exits fast on fades.

Risk Controls:

Tracks realized equity peak.

10% drawdown: Risk ×0.8; 20%/30%: Further ×0.8 (max 3x).

Full reset above peak—preserves capital in slumps.

Enhanced MA Crossover Pro📝 Strategy Summary: Enhanced MA Crossover Pro

This strategy is an advanced, highly configurable moving average (MA) crossover system designed for algorithmic trading. It uses the crossover of two customizable MAs (a "Fast" MA 1 and a "Slow" MA 2) as its core entry signal, but aggressively integrates multiple technical filters, time controls, and dynamic position management to create a robust and comprehensive trading system.

💡 Core Logic

Entry Signal: A bullish crossover (MA1 > MA2) generates a Long signal, and a bearish crossover (MA1 < MA2) generates a Short signal. Users can opt to use MA crossovers from a Higher Timeframe (HTF) for the entry signal.

Confirmation/Filters: The basic MA cross signal is filtered by several optional indicators (see Filters section below) to ensure trades align with a broader trend or momentum context.

Position Management: Trades are managed with a sophisticated system of Stop Loss, Take Profit, Trailing Stops, and Breakeven stops that can be fixed, ATR-based, or dynamically adjusted.

Risk Management: Daily limits are enforced for maximum profit/loss and maximum trades per day.

⚙️ Key Features and Customization

1. Moving Averages

Primary MAs (MA1 & MA2): Highly configurable lengths (default 8 & 20) and types: EMA, WMA, SMA, or SMMA/RMA.

Higher Timeframe (HTF) MAs: Optional MAs calculated on a user-defined resolution (e.g., "60" for 1-hour) for use as an entry signal or as a trend confirmation filter.

2. Multi-Filter System

The entry signal can be filtered by the following optional conditions:

SMA Filter: Price must be above a 200-period SMA for long trades, and below it for short trades.

VWAP Filter: Price must be above VWAP for long trades, and below it for short trades.

RSI Filter: Long trades are blocked if RSI is overbought (default 70); short trades are blocked if RSI is oversold (default 30).

MACD Filter: Requires the MACD Line to be above the Signal Line for long trades (and vice versa for short trades).

HTF Confirmation: Requires the HTF MA1 to be above HTF MA2 for long entries (and vice versa).

3. Dynamic Stop and Target Management (S/L & T/P)

The strategy provides extensive control over exits:

Stop Loss Methods:

Fixed: Fixed tick amount.

ATR: Based on a multiple of the Average True Range (ATR).

Capped ATR: ATR stop limited by a maximum fixed tick amount.

Exit on Close Cross MA: Position is closed if the price crosses back over the chosen MA (MA1 or MA2).

Breakeven Stop: A stop can be moved to the entry price once a trigger distance (fixed ticks or Adaptive Breakeven based on ATR%) is reached.

Trailing Stop: Can be fixed or ATR-based, with an optional feature to auto-tighten the trailing multiplier after the breakeven condition is met.

Profit Target: Can be a fixed tick amount or a dynamic target based on an ATR multiplier.

4. Time and Session Control

Trading Session: Trades are only taken between defined Start/End Hours and Minutes (e.g., 9:30 to 16:00).

Forced Close: All open positions are closed near the end of the session (e.g., 15:45).

Trading Days: Allows specific days of the week to be enabled or disabled for trading.

5. Risk and Position Limits

Daily Profit/Loss Limits: The strategy tracks daily realized and unrealized PnL in ticks and will close all positions and block new entries if the user-defined maximum profit or maximum loss is hit.

Max Trades Per Day: Limits the number of executed trades in a single day.

🎨 Outputs and Alerts

Plots: Plots the MA1, MA2, SMA, VWAP, and HTF MAs (if enabled) on the chart.

Shapes: Plots visual markers (BUY/SELL labels) on the bar where the MA crossover occurs.

Trailing Stop: Plots the dynamic trailing stop level when a position is open.

Alerts: Generates JSON-formatted alerts for entry ({"action":"buy", "price":...}) and exit ({"action":"exit", "position":"long", "price":...}).

Basic DCA Strategy by Wongsakon KhaisaengThe Core Principle and Philosophy Behind the Basic DCA Strategy

1. Introduction

The Basic DCA Strategy (Dollar-Cost Averaging) represents one of the most fundamental and enduring investment methodologies in the realm of systematic accumulation. The philosophy underpinning DCA is rooted not in speculation or prediction, but in disciplined participation. It assumes that the consistent act of investing a fixed amount of capital over time—regardless of short-term price volatility—can yield superior long-term outcomes through the natural smoothing effect of cost averaging.

This strategy, expressed through the Pine Script code above, formalizes the DCA concept into a fully systematic trading framework, enabling quantitative backtesting and objective evaluation of long-term accumulation efficiency.

2. Mechanism of Operation

At its technical core, the strategy executes a fixed-value buy order at every predefined interval within a specific accumulation period.

Each DCA event invests a constant “Investment Amount (USD)” irrespective of price fluctuations. When prices decline, this constant investment buys a larger quantity of the asset; when prices rise, it purchases fewer units. Over time, this behavior lowers the average cost basis of the accumulated position, effectively neutralizing short-term timing risks.

Mathematically, this is represented as:

Units Purchased = Investment Amount / Closing Price

Cost Basis = Total Invested USD / Total Units Acquired

Portfolio Value = Total Units Acquired × Current Price

The algorithm tracks cumulative investment, acquired units, and commissions dynamically, continuously recalculating key portfolio metrics such as total profit/loss (PnL), CAGR (Compound Annual Growth Rate), and maximum drawdown (peak-to-trough equity decline).

Furthermore, the script juxtaposes DCA results with a Buy & Hold benchmark, where the entire initial capital is invested at once. This comparison highlights the behavioral resilience and volatility resistance of the DCA method relative to market-timing strategies.

3. The Essence of DCA Philosophy

At its philosophical core, DCA is not a trading system, but a behavioral framework for rational capital deployment under uncertainty. It embodies the principle that time in the market often outweighs timing the market.

The DCA approach rejects the illusion of precision forecasting and embraces probabilistic humility—the recognition that even the most skilled investors cannot consistently predict short-term market fluctuations. Instead, it focuses on controlling what is controllable: the frequency, consistency, and size of investment actions.

This mindset reflects a broader principle of risk dispersion through temporal diversification. Rather than concentrating entry risk into a single price point (as in lump-sum investing), DCA spreads exposure across multiple time intervals, thereby converting volatility into opportunity.

In essence, volatility—often perceived as risk—is reframed as a mechanism for mean reversion advantage. The strategy thrives precisely because markets oscillate; each fluctuation provides a chance to accumulate at varied price levels, improving the weighted-average entry over time.

4. Long-Term Rationality Over Short-Term Emotion

DCA’s endurance stems from its ability to neutralize emotional biases inherent in human decision-making. Investors tend to overreact to market euphoria or panic—buying high out of greed and selling low out of fear. By automating purchases through predefined intervals, the DCA model enforces mechanical discipline, detaching decision-making from sentiment.

This transforms investing from an emotional endeavor into a systematic, algorithmic routine governed by rules rather than reactions. In doing so, DCA serves not only as a financial model but also as a psychological safeguard—aligning investor behavior with long-term compounding logic rather than short-term speculation.

5. Comparative Insight: DCA vs. Buy & Hold

While both DCA and Buy & Hold share a long-term investment horizon, they diverge in their treatment of entry timing. The Buy & Hold model assumes full deployment of capital at the beginning, maximizing exposure to growth but also to volatility. Conversely, DCA smooths the entry curve, trading off short-term returns for long-term stability and improved average entry price.

In environments characterized by volatility and cyclical corrections, DCA tends to outperform in terms of risk-adjusted returns, lower drawdowns, and improved investor adherence—since it reduces the psychological pain of entering at local peaks.

6. Conclusion

The Basic DCA Strategy exemplifies the synthesis of mathematical rigor and behavioral discipline. Its algorithmic construction in Pine Script transforms a classical investment philosophy into a quantifiable, testable, and transparent framework.

By automating fixed-amount purchases across time, the system operationalizes the central axiom of DCA: consistency over conviction. It is not concerned with predicting future prices but with ensuring persistent participation—trusting that the market’s upward bias and the power of compounding will reward patience more than precision.

Ultimately, DCA embodies the timeless principle that successful investing is less about forecasting markets, and more about designing behavior that can endure them.

OneHolo-TGAPSNRTGAPSNR: Multi time frame - Trend Gap Stop And Reverse strategy/Study PnL. This script outlines a systematic approach to generating buy and sell signals by combining Fair Value Gaps (FVGs), specific market structures, and three different trend direction methods (Swing, Gravity, and FVG Inverse direction). The strategy incorporates multiple entry modes, such as Hyper Mode, Swiper Mode, and a Custom mode, allowing users to tailor signal conditions, alongside extensive logic for trade management, higher time frame analysis, and various visual indicators for plotting trend, pivots, and profit and loss information.

I. Core Trend Direction Consensus (The Three-Pillar System)

The primary method for determining market bias is a three-pillar consensus model, requiring all directional methods to align before the overall Trend Direction is established (up or down). This ensures high conviction for trend signals.

• Pillar 1: Swing Direction: Determines market direction based on classic price action, specifically checking for continuous higher highs and higher lows for an upward bias, or lower lows and lower highs for a downward bias.

• Pillar 2: Gravity Direction (Peak and Valley): This uses specific market structure pivots. Direction is set based on whether the close price successfully crosses the established recent Peak High (indicating upward momentum) or crosses under the recent Valley Low (indicating downward pressure).

• Pillar 3: FVG Inverse Direction: This relies on Fair Value Gaps (FVGs), defined as a gap between the current bar's price and the price two bars prior. Direction shifts occur when the Close price crosses the midpoint of the last relevant FVG. For instance, crossing above the midpoint of the last FVG Down signals a potential inverse long trade.

II. Flexible Signal Generation Modes

The strategy offers several pre-configured and highly detailed entry modes, plus a powerful Custom Mode:

• Session Open Range Break (ORB) Mode: Uses the high/low of the session's first bar to generate initial signals, then defaults to the Three-Pillar Trend Direction after the ORB session concludes.

• Swiper Mode: Designed to identify continuations, combining a confirmed Trend Direction with a Stop and Reverse signal (SnR) while actively avoiding confirmed pivot breaks.

• Hyper/Aggressive Modes: These modes use broad combinations of signals, allowing for earlier entry based on momentum and structural breaks (like PeakCrossLong, SnRtrapLong, or FVG signals).

• Custom Query Mode (The Seven-Slot Logic): This non-redundant system allows the user to define complex, tailored entry conditions by selecting any combination of 14 core patterns across seven distinct slots.

◦ AND/OR Combination: For each of the seven slots, the user determines if the chosen pattern must be met (AND component) or if it can serve as an alternative trigger (OR component).

◦ The final signal requires that all configured AND conditions are true and then integrates the result of the OR conditions, allowing for highly specific "hook queries" (e.g., "Condition A AND Condition B, OR Condition C").

III. Advanced PnL and Mobile App Diagnostics

A key proprietary element is the implementation of a dual PnL system and customized visualization features:

• Dual PnL Display (Strategy PnL vs. Study PnL): Users can choose to view either the native platform's strategy performance data or the script's internal, proprietary Study PnL. The Study PnL calculates profits/losses based strictly on the close price and tracks performance using Pine Script® arrays, providing a transparent, diagnostic view of performance independent of broker/platform simulation biases.

• Lower Panel Visualization: Both PnL types are displayed on the lower panel using detailed bar plots (style=plot.style_columns), which color according to profitability, and include labels that show current open profit and total net profit.

• Detailed Trade Labels: The script generates detailed, customizable labels on both the chart (above/below bars) and the lower PnL panel, providing historical PnL, number of trades, and real-time profit information for each entry or exit.

IV. Higher Time Frame (HTF) Context and Lookahead Prevention

The strategy integrates multi-time frame analysis using strict methodology to prevent lookahead bias:

• HTF Bias Filtering: When enabled, the strategy uses the position calculated on a user-defined higher time frame (HTF) as a mandatory filter. A long signal on the current chart is only executed if the HTF is also in a long position, and vice-versa.

• Lookahead Prevention: To maintain integrity, all HTF data requests use a mandatory lookback index (often ) to ensure the script only accesses confirmed data from the prior completed bar on the higher timeframe.

• HTF Visual Mode: The user can opt to display key structural elements—such as the Gravity Pivots and the Trend Direction blocks—as calculated on the HTF, overlaying this higher-level context onto the current chart for visual analysis.

The TGAPSNR: Multi time frame - Trend Gap Stop And Reverse strategy/Study PnL script, despite its complexity, intentionally excludes realistic considerations such as fees, slippage, and explicit risk management settings (like fixed stop-loss or take-profit rules) from its primary logic.

Here is an explanation of why these elements are omitted in the strategy's current implementation and why they must be applied by the user for real-world application, drawing on the context of the sources:

1. Absence of Realistic Fees, Commissions, and Slippage

The primary function of the TGAPSNR script is to execute intricate signal generation and diagnostic PnL calculation based on its three-pillar trend system and Custom Mode logic.

However, the strategy's backtesting results, particularly those displayed by the internal Study PnL feature, are based purely on price difference (e.g., (close - lse) * syminfo.pointvalue * IUnits).

• Strategy Result Requirements: TradingView explicitly states that strategies published publicly should strive to use realistic commission AND slippage when calculating backtesting results to avoid misleading traders.

• User Responsibility: Since the script currently focuses on signal integrity and uses a fixed contract size (IUnits = 1) without configurable commission/slippage inputs shown in the source, the user must manually configure these fees within the Pine Script® Strategy Tester settings (Properties tab) to ensure the strategy results are reflective of actual trading costs.

2. Omission of Built-in Risk Management (Stop-Loss and Take-Profit)

The TGAPSNR strategy's core focuses on entry signals and trend confirmation. Exits are primarily governed by:

• Reversal signals (BuyStop or SellStop).

• End-of-Day (EOD) session closures (EODStop).

• HTF bias opposition.

What is Missing: The script does not include explicit, hard-coded risk management parameters for traditional stop-loss (SL) or take-profit (TP) levels (e.g., risk percentage or ATR-based exits).

• Viable Risk: TradingView guidelines stipulate that strategies should generally risk sustainable amounts of equity, usually not exceeding 5-10% on a single trade, and trade size must be appropriate.

• User Application: To ensure the strategy operates within realistic risk boundaries, users must apply their own risk management rules. This includes:

◦ Implementing realistic stops and profit targets, which can be added via Pine Script® code or manually managed during live trading.

◦ Sizing trades to only risk sustainable amounts of equity. The current default unit size (IUnits = 1) is unrealistic for risk assessment unless the symbol is micro-sized.

3. Execution Quality (Fills)

The strategy is set to fill_orders_on_standard_ohlc = true and operates on confirmed bar closes (barstate.isconfirmed).

• Fill Assumption: This suggests the strategy primarily uses close price or the HTF close price (EntryPrice = HTFClose) for execution.

• Real-World Limitation: In volatile markets, obtaining a fill price equal to the close of the bar is rare. The user must be aware that the simulated fill price shown in backtesting may differ significantly from actual execution prices due to market action and chosen order type, reinforcing the importance of applying slippage settings.

In summary, while the script provides highly detailed and unique signal generation and internal PnL diagnostics, users must exercise caution and apply their own realistic parameters for fees, slippage, and explicit risk controls to prevent misleading performance results and ensure viable trading

AVGO Advanced Day Trading Strategy📈 Overview

The AVGO Advanced Day Trading Strategy is a comprehensive, multi-timeframe trading system designed for active day traders seeking consistent performance with robust risk management. Originally optimized for AVGO (Broadcom), this strategy adapts well to other liquid stocks and can be customized for various trading styles.

🎯 Key Features

Multiple Entry Methods

EMA Crossover: Classic trend-following signals using fast (9) and medium (16) EMAs

MACD + RSI Confluence: Momentum-based entries combining MACD crossovers with RSI positioning

Price Momentum: Consecutive price action patterns with EMA and RSI confirmation

Hybrid System: Advanced multi-trigger approach combining all methodologies

Advanced Technical Arsenal

When enabled, the strategy analyzes 8+ additional indicators for confluence:

Volume Price Trend (VPT): Measures volume-weighted price momentum

On-Balance Volume (OBV): Tracks cumulative volume flow

Accumulation/Distribution Line: Identifies institutional money flow

Williams %R: Momentum oscillator for entry timing

Rate of Change Suite: Multi-timeframe momentum analysis (5, 14, 18 periods)

Commodity Channel Index (CCI): Cyclical turning points

Average Directional Index (ADX): Trend strength measurement

Parabolic SAR: Dynamic support/resistance levels

🛡️ Risk Management System

Position Sizing

Risk-based position sizing (default 1% per trade)

Maximum position limits (default 25% of equity)

Daily loss limits with automatic position closure

Multiple Profit Targets

Target 1: 1.5% gain (50% position exit)

Target 2: 2.5% gain (30% position exit)

Target 3: 3.6% gain (20% position exit)

Configurable exit percentages and target levels

Stop Loss Protection

ATR-based or percentage-based stop losses

Optional trailing stops

Dynamic stop adjustment based on market volatility

📊 Technical Specifications

Primary Indicators

EMAs: 9 (Fast), 16 (Medium), 50 (Long)

VWAP: Volume-weighted average price filter

RSI: 6-period momentum oscillator

MACD: 8/13/5 configuration for faster signals

Volume Confirmation

Volume filter requiring 1.6x average volume

19-period volume moving average baseline

Optional volume confirmation bypass

Market Structure Analysis

Bollinger Bands (20-period, 2.0 multiplier)

Squeeze detection for breakout opportunities

Fractal and pivot point analysis

⏰ Trading Hours & Filters

Time Management

Configurable trading hours (default: 9:30 AM - 3:30 PM EST)

Weekend and holiday filtering

Session-based trade management

Market Condition Filters

Trend alignment requirements

VWAP positioning filters

Volatility-based entry conditions

📱 Visual Features

Information Dashboard

Real-time display of:

Current entry method and signals

Bullish/bearish signal counts

RSI and MACD status

Trend direction and strength

Position status and P&L

Volume and time filter status

Chart Visualization

EMA plots with customizable colors

Entry signal markers

Target and stop level lines

Background color coding for trends

Optional Bollinger Bands and SAR display

🔔 Alert System

Entry Alerts

Customizable alerts for long and short entries

Method-specific alert messages

Signal confluence notifications

Advanced Alerts

Strong confluence threshold alerts

Custom alert messages with signal counts

Risk management alerts

⚙️ Customization Options

Strategy Parameters

Enable/disable long or short trades

Adjustable risk parameters

Multiple entry method selection

Advanced indicator on/off toggle

Visual Customization

Color schemes for all indicators

Dashboard position and size options

Show/hide various chart elements

Background color preferences

📋 Default Settings

Initial Capital: $100,000

Commission: 0.1%

Default Position Size: 10% of equity

Risk Per Trade: 1.0%

RSI Length: 6 periods

MACD: 8/13/5 configuration

Stop Loss: 1.1% or ATR-based

🎯 Best Use Cases

Day Trading: Designed for intraday opportunities

Swing Trading: Adaptable for longer-term positions

Momentum Trading: Excellent for trending markets

Risk-Conscious Trading: Built-in risk management protocols

⚠️ Important Notes

Paper Trading Recommended: Test thoroughly before live trading

Market Conditions: Performance varies with market volatility

Customization: Adjust parameters based on your risk tolerance

Educational Purpose: Use as a learning tool and customize for your needs

🏆 Performance Features

Detailed performance metrics

Trade-by-trade analysis capability

Customizable risk/reward ratios

Comprehensive backtesting support

This strategy is for educational purposes. Past performance does not guarantee future results. Always practice proper risk management and consider your financial situation before trading.

Small-Cap — Sell Every Spike (Rendon1) Small-Cap — Sell Every Spike v6 — Strict, No Look-Ahead

Educational use only. This is not financial advice or a signal service.

This strategy targets low/ mid-float runners (≤ ~20M) that make parabolic spikes. It shorts qualified spikes and scales out into flushes. Logic is deliberately simple and transparent to avoid curve-fit.

What the strategy does

Detects a parabolic up move using:

Fast ROC over N bars

Big range vs ATR

Volume spike vs SMA

Fresh higher high (no stale spikes)

Enters short at bar close when conditions are met (no same-bar fills).

Manages exits with ATR targets and optional % covers.

Tracks float rotation intraday (manual float input) and blocks trades above a hard limit.

Draws daily spike-high resistance from confirmed daily bars (no repaint / no look-ahead).

Timeframes & market

Designed for 1–5 minute charts.

Intended for US small-caps; turn Premarket on.

Works intraday; avoid illiquid tickers or names with constant halts.

Entry, Exit, Risk (short side)

Entry: parabolic spike (ROC + Range≥ATR×K + Vol≥SMA×K, new HH).

Optional confirmations (OFF by default to “sell every spike”): upper-wick and VWAP cross-down.

Stop: ATR stop above entry (default 1.2× ATR).

Targets: TP1 = 1.0× ATR, TP2 = 2.0× ATR + optional 10/20/30% covers.

Safety: skip trades if RVOL is low or Float Rotation exceeds your limit (default warn 5×, hard 7×).

Inputs (Balanced defaults)

Price band: $2–$10

Float Shares: set per ticker (from Finviz).

RVOL(50) ≥ 1.5×

ROC(5) ≥ 1.0%, Range ≥ 1.6× ATR, Vol ≥ 1.8× SMA

Cooldown: 10 bars; Max trades/day: 6

Optional: Require wick (≥35%) and/or Require VWAP cross-down.

Presets suggestion:

• Balanced (defaults above)

• Safer: wick+VWAP ON, Range≥1.8×, trades/day 3–4

• Micro-float (<5M): ROC 1.4–1.8%, Range≥1.9–2.2×, Vol≥2.2×, RVOL≥2.0, wick 40–50%

No look-ahead / repaint notes

Daily spike-highs use request.security(..., lookahead_off) and shifted → only closed daily bars.

Orders arm next bar after entry; entries execute at bar close.

VWAP/ATR/ROC/Vol/RVOL are computed on the chart timeframe (no HTF peeking).

How to use

Build a watchlist: Float <20M, RelVol >2, Today +20% (Finviz).

Open 1–5m chart, enter Float Shares for the ticker.

Start with Balanced, flip to Safer on halty/SSR names or repeated VWAP reclaims.

Scale out into flushes; respect the stop and rotation guard.

Limitations & risk

Backtests on small-caps can be optimistic due to slippage, spreads, halts, SSR, and limited premarket data. Always use conservative sizing. Low-float stocks can squeeze violently.

Alerts

Parabolic UP (candidate short)

SHORT Armed (conditions met; entry at bar close)

Hazel nut BB Strategy, volume base- lite versionHazel nut BB Strategy, volume base — lite version

Having knowledge and information in financial markets is only useful when a trader operates with a well-defined trading strategy. Trading strategies assist in capital management, profit-taking, and reducing potential losses.

This strategy is built upon the core principle of supply and demand dynamics. Alongside this foundation, one of the widely used technical tools — the Bollinger Bands — is employed to structure a framework for profit management and risk control.

In this strategy, the interaction of these tools is explained in detail. A key point to note is that for calculating buy and sell volumes, a lower timeframe function is used. When applied with a tick-level resolution, this provides the most precise measurement of buyer/seller flows. However, this comes with a limitation of reduced historical depth. Users should be aware of this trade-off: if precise tick-level data is required, shorter timeframes should be considered to extend historical coverage .

The strategy offers multiple configuration options. Nevertheless, it should be treated strictly as a supportive tool rather than a standalone trading system. Decisions must integrate personal analysis and other instruments. For example, in highly volatile assets with narrow ranges, it is recommended to adjust profit-taking and stop-loss percentages to smaller values.

◉ Volume Settings

• Buyer and seller volume (up/down volume) are requested from a lower timeframe, with an option to override the automatic resolution.

• A global lookback period is applied to calculate moving averages and cumulative sums of buy/sell/delta volumes.

• Ratios of buyers/sellers to total volume are derived both on the current bar and across the lookback window.

◉ Bollinger Band

• Bands are computed using configurable moving averages (SMA, EMA, RMA, WMA, VWMA).

• Inputs allow control of length, standard deviation multiplier, and offset.

• The basis, upper, and lower bands are plotted, with a shaded background between them.

◉ Progress & Proximity

• Relative position of the price to the Bollinger basis is expressed as percentages (qPlus/qMinus).

• “Near band” conditions are triggered when price progress toward the upper or lower band exceeds a user-defined threshold (%).

• A signed score (sScore) represents how far the close has moved above or below the basis relative to band width.

◉ Info Table

• Optional compact table summarizing:

• - Upper/lower band margins

• - Buyer/seller volumes with moving averages

• - Delta and cumulative delta

• - Buyer/seller ratios per bar and across the window

• - Money flow values (buy/sell/delta × price) for bar-level and summed periods

• The table is neutral-colored and resizable for different chart layouts.

◉ Zone Event Gate

• Tracks entry into and exit from “near band” zones.

• Arming logic: a side is armed when price enters a band proximity zone.

• Trigger logic: on exit, a trade event is generated if cumulative buyer or seller volume dominates over a configurable window.

◉ Trading Logic

• Orders are placed only on zone-exit events, conditional on volume dominance.

• Position sizing is defined as a fixed percentage of strategy equity.

• Long entries occur when leaving the lower zone with buyer dominance; short entries occur when leaving the upper zone with seller dominance.

◉ Exit Rules

• Open positions are managed by a strict priority sequence:

• 1. Stop-loss (% of entry price)

• 2. Take-profit (% of entry price)

• 3. Opposite-side event (zone exit with dominance in the other direction)

• Stop-loss and take-profit levels are configurable

◉ Notes

• This lite version is intended to demonstrate the interaction of Bollinger Bands and volume-based dominance logic.

• It provides a framework to observe how price reacts at band boundaries under varying buy/sell pressure, and how zone exits can be systematically converted into entry/exit signals.

When configuring this strategy, it is essential to carefully review the settings within the Strategy Tester. Ensure that the chosen parameters and historical data options are correctly aligned with the intended use. Accurate back testing depends on applying proper configurations for historical reference. The figure below illustrates sample result and configuration type.

Lavender Multi-Signal Momentum StrategyOverview

The Lavender strategy is a sophisticated momentum-based trading system specifically optimized for Tesla (TSLA) on the 15-minute timeframe. It combines multiple technical signals to identify high-probability long entries during strong trending conditions.

Key Features

🎯 Multi-Signal Entry System

The strategy uses 4 distinct signal types that can be enabled/disabled individually:

Supertrend Pullback (Default: ON)

Identifies pullbacks in uptrends using Supertrend (ATR: 9, Factor: 0.5)

Enters when price retests EMA9-20 zone during bullish Supertrend

Donchian Breakout + Z-Score Momentum (Default: ON)

53-period Donchian channel breakouts

Combined with 35-period Z-Score momentum filter

Only triggers with positive momentum confirmation

Keltner Squeeze Expansion (Default: OFF)

Detects volatility squeeze conditions

Enters on breakout above Keltner Channel after compression

Opening Range Breakout (ORB) (Default: ON)

Tracks first hour range (9:30-10:30 AM)

Triggers on breakout above opening range high

🧭 Trend Regime Filter

EMA Trend Filter: 20 EMA > 100 EMA (Default: ON)

ADX Strength Filter: ADX > 22 with 15/13 smoothing (Default: ON)

Only trades when both trend conditions align

💵 Advanced Risk Management

Risk per Trade: 2.0% of capital (Default)

ATR-Based Stop Loss: 15-period ATR × 1.6 multiplier

Risk/Reward Ratio: 4:1 (Default)

Position Sizing: Automatic based on stop distance

Capital Options: Dynamic equity or fixed capital ($200,000 default)

⚙️ Execution Control

Candle Close Entries: Prevents intrabar noise (Default: ON)

Candle Close Exits: Stop loss and take profit only at bar close (Default: ON)

Trading Session: 9:00 AM - 4:00 PM (Default)

Trading Days: Monday-Saturday (Default: 123456)

Default Settings Summary

ParameterDefault ValuePurposeRisk per Trade2.0%Capital risk percentageATR Length15Stop loss calculationATR Multiplier1.6Stop distance factorRisk/Reward4.0Take profit multiplierEMA Fast20Short-term trendEMA Slow100Long-term trendADX Threshold22Minimum trend strengthMin Signals Required1Entry trigger thresholdInitial Capital$200,000Backtesting capital

How It Works

Trend Confirmation: Checks EMA alignment and ADX strength

Signal Generation: Scans for active momentum signals

Entry Execution: Enters when minimum signal threshold is met

Risk Management: Calculates position size based on ATR stop

Exit Management: Manages trades with 4:1 risk/reward ratio

Best Use Cases

Tesla (TSLA) on 15-minute charts

Trending market conditions

Intraday momentum trading

Markets with clear directional bias

Visual Indicators

Blue Line: 100-period EMA (trend filter)

Green/Red Line: Supertrend indicator

Teal Line: Donchian channel high

Purple Triangles: Keltner breakout signals

Orange Arrows: Opening range breakouts

Green Dots: Combined entry signals

Red/Green Lines: Active stop loss and take profit levels

Risk Disclaimer

This strategy is optimized for Tesla's specific price behavior on 15-minute timeframes. Past performance does not guarantee future results. Always test thoroughly and manage risk appropriately.

Created by kevloewe - Specialized for TSLA 15M momentum trading

Master Arb Recipes – 3 Commas signal Bot integration Master Arb Recipes – 3 Commas signal Bot integration

Purpose

A systematic arbitrage/accumulation framework with pre-tuned “recipes” for BTC/ETH/XRP/SUI/SOL plus a fully manual mode. It automates signal generation for external execution bots (via alert() JSON), while showing on-chart panels for goals, active parameters, DCA position, and P&L/ROI/CAGR. Backtests simulate market orders with optional slippage and TradingView commissions.

Key ideas

Entries: Intrabar trigger when price drops by the recipe’s Entry drop % from the previous close.

Exits: Profit-taking when price rises by the recipe’s Exit rise % (optionally requiring price above average cost).

DCA accounting: Tracks running quantity, average cost, realized (cash) P&L, and unrealized (coin) P&L.

Capital planning: “ReqCap” column estimates capital = Entry $ × Allowed entries (UI only; does not affect orders).

Alerts (live only): Sends minimal Custom Signal JSON for enter_long / exit_long to your execution bot.

What’s included on chart

Top-Right: Strategy Goals Table

Describes the objective for each preset. Auto-filters by the chart’s base (optional).

Bottom-Left: Active Recipe Panel (with 3C UI column)

Shows the active preset (or custom) with: timeframe, Sell-Above-Cost state, Entry/Exit %, Exit-as-%-of-Entry, min bars between entries, once-per-bar gate, and 3Commas UI guidance for optional filters and per-order dollars.

Top-Left: DCA Panel

Current base quantity, average cost, and realized P&L.

Bottom-Right: P&L + ROI/CAGR Panel

Cash P&L (realized), Coin P&L (unrealized), Total P&L, ROI since first fill, and annualized CAGR. Displays denominators for both StartCap (strategy.initial_capital) and ReqCap (planning).

Presets

BTC: STH1_D, LTH1_6H, LTH2_D, LTH3_W, LTH4_6H

ETH: STH1_D, STH2_D, LTH1_D

XRP: STH1_D, STH2_6H, LTH1_6H, LTH2_1H

SUI: STH1_D, STH2_D, STH3_D

SOL: STH1_D, LTH1_D

Each preset sets Entry drop %, Exit rise %, default Entry $, Exit-as-%-of-Entry, Sell-Above-Cost flag, and a reference timeframe (display only). Custom mode lets you define these manually.

Inputs you’ll use

3Commas Custom Signal: secret, bot_uuid, max_lag_sec.

Start Window: Exact date/time + timezone to begin trading/signals.

Entry/Exit Parameters: Entry drop %, Exit rise %, Sell Above Avg Cost toggle, Exit as % of Entry.

Capital Planning: Allowed entries (for ReqCap), Entry $ override (panel only).

Execution/Sim: Simulated slippage %, once-per-bar gate, minimum bars between entries, TradingView commission.

Panels: Toggles + positions for each table.

Alert / Bot integration

Alerts fire only in realtime (barstate.isrealtime) on order submission.

Create one alert on this script using “Any alert() function call”.

Payload (Custom Signal style) includes:

secret, bot_uuid, max_lag, timestamp, trigger_price, tv_exchange, tv_instrument, action where action ∈ {enter_long, exit_long}.

Sizing: This script does not include per-order sizing in the JSON; size in your bot UI. The on-chart Entry $ / Exit $ values are for planning/backtest display.

3Commas optional filter mapping (shown in the panel’s “3C UI” column):

Entry filters:

Same order: set to –EntryDrop% (ON)

From average entry: set to –EntryDrop% (ON)

Exit filters:

If Sell Above Cost = ON → From average entry +ExitRise% (ON); Same order OFF

If Sell Above Cost = OFF → Same order +ExitRise% (ON); From average entry OFF

Per-order volume: Use your bot’s UI. Panel shows the dollars you planned (Entry $ and Exit $).

Backtest notes & limitations

Uses calc_on_every_tick=true and intrabar checks against the previous close for entry drops; historical behavior won’t perfectly match exchange microstructure.

process_orders_on_close=false; fills are simulated at bar prices with your slippage setting and TV commission.

Alerts and webhook timing depend on TradingView + broker/exchange latencies; use max_lag_sec accordingly.

Required Capital (ReqCap) is for planning only and does not reserve funds or constrain orders.

Recommended markets/timeframes

Crypto spot or futures charts that trade 24/7. Preset labels (D/6H/1H/W) are reference rhythms for volatility; the script runs on any timeframe but results will vary.

Change log (04092025)

Added 3C UI guidance column in Active Recipe panel (dynamic % per recipe).

Restored Goals (top-right) and P&L/ROI/CAGR (bottom-right with StartCap & ReqCap).

Minor UI clarifications; trading logic unchanged.

Disclaimer

This script is for research and education. It is not financial advice and makes no performance promises. Backtests are hypothetical and subject to substantial limitations. Markets involve risk; you can lose capital. Test on paper first and deploy at your own discretion. Licensed under the Mozilla Public License 2.0.

BDNS ORB Strategy v3BDNS Opening Range Breakout Strategy

What This Strategy Does This strategy implements an Opening Range Breakout (ORB) system that identifies the high and low prices during a customizable opening period, then trades breakouts above or below these levels with momentum confirmation. The strategy goes beyond basic ORB concepts by incorporating ADX momentum filtering, VWAP directional bias, dynamic position sizing, and sophisticated exit management including breakeven moves and trailing stops.

Core Strategy Logic

Opening Range Definition: The strategy tracks price action during a user-defined opening period (default: 9:30-9:35 AM ET for 5 minutes). During this time, blue horizontal lines appear marking the session high and low. A yellow background highlights this opening range period.

Breakout Detection: After the opening range completes, green and red horizontal lines appear showing the actual entry levels - these are offset from the range boundaries by a configurable number of ticks (default: 24 ticks) to filter out false breakouts and ensure committed moves.

Entry Conditions: Trades trigger when price breaks through these offset levels during the trading window (green background, default until 10:30 AM ET), but only when:

ADX momentum indicator exceeds threshold (default 24.0) in the breakout direction

Price relationship to VWAP confirms directional bias (when VWAP filter enabled)

Daily trade limits haven't been reached

Large range filtering conditions are met

Visual Elements and Usage

Range Lines: Blue lines show the actual opening range boundaries. These appear immediately when the opening session begins.

Entry Levels: Green (long) and red (short) lines show where trades will trigger, appearing after the opening range completes.

Information Table: A data table appears in the top-right showing real-time strategy status including range size in ticks, ADX readings, filter status, trade counts, and momentum conditions.

Position Management:

When in a trade, colored circles appear showing:

Lime circles: Long position targets (T1, T2, T3)

Orange circles: Short position targets

Red circles: Stop loss levels

Blue crosses: Breakeven levels (when that feature activates)

Purple lines: Trailing stop levels (when position 3 trailing activates)

Background Colors:

Yellow: Opening range session active

Green: Trading window active

Purple: Large range day detected

Gray: Large range day being skipped

Position Management System

The strategy uses a three-tier exit approach:

Position 1: Takes partial profits at first target (default 50% of range size)

Position 2: Exits at second target (default 100% of range size)

Position 3: Either exits at third target or uses trailing stop after Position 2 wins

Breakeven Feature: When enabled and price reaches the breakeven trigger level, all stop losses move to a more favorable breakeven level instead of the original stop, protecting against giving back profits.

Trailing Stop System: After Position 2 hits its target, Position 3 automatically switches to a trailing stop that moves in the trader's favor as price continues trending.

Customization for Different Instruments