Periodic Volume Time Velocity ProfileThis is the Periodic Volume Time Velocity Profile (PVTVP). It is an advanced professional profiling tool that goes beyond standard volume analysis by introducing Time and Velocity (Flow Rate) as profile dimensions.

By analyzing high-resolution intra-bar data, it builds

precise profiles for any custom period (Session, Day, Week, etc.),

helping you understand not just *where* the market traded,

but *how* it traded there.

## The 3 Dimensions of the Market

Unlike standard tools that only show Volume, PVTVP allows you

to switch between three critical metrics:

1. **VOLUME Profile (The "Where"):**

* Shows standard acceptance. High volume nodes (HVN)

are magnets for price.

2. **TIME Profile (The "How Long"):**

* Similar to TPO, it measures how long price spent at each

level.

* **High Time:** True acceptance and fair value.

* **Low Time:** Rejection or rapid movement.

3. **VELOCITY Profile (The "How Fast"):**

* Measures the **speed of trading** (Contracts per Second).

This reveals the hidden intent of market participants.

* **High Velocity (Fast Flow):** Aggression. Initiative

buyers/sellers are hitting market orders rapidly. Often

seen at breakouts or in liquidity vacuums.

* **Low Velocity (Slow Flow):** Absorption. Massive passive

limit orders are slowing price down despite high volume.

Often seen at major reversals ("hitting a brick wall").

## Key Features

1. **Statistical Volume Profile Engine:** For each bar in the selected

period, the indicator builds a complete volume profile on a lower

'Intra-Bar Timeframe'. Instead of simple tick counting, it uses

**statistical models ('PDF' allocation)** to distribute volume

across price levels and **advanced classifiers ('Dynamic' split)**

to determine the buy/sell pressure within that profile.

2. **Flexible Profile Display:** The **finalized profile** (plotted at

the end of each period) can be visualized in three distinct

ways: 'Up/Down' (buy vs. sell), 'Total' (combined volume),

and 'Delta' (net difference).

3. **Developing Key Levels:** The indicator also plots the developing

Point of Control (POC), Value Area (VA), VWAP, and Standard

Deviation bands in real-time as the period unfolds, providing

live insights into the emerging market structure.

4. **Dynamic Row Sizing:** Includes an option ('Rows per Percent')

to automatically adjust the number of profile rows (buckets)

based on the profile's price range, maintaining a consistent

visual density.

5. **Integrated Alerts:** Includes 12 alerts that trigger when the

main price crosses over or under the key developing levels:

POC, VWAP, Value Area High/Low, and the +/- Standard

Deviation bands.

**Caution: Real-Time Data Behavior (Intra-Bar Repainting)**

This indicator uses high-resolution intra-bar data. As a result, the

values on the **current, unclosed bar** (the real-time bar) will

update dynamically as new intra-bar data arrives. This behavior is

normal and necessary for this type of analysis. Signals should only

be considered final **after the main chart bar has closed.**

---

**DISCLAIMER**

1. **For Informational/Educational Use Only:** This indicator is

provided for informational and educational purposes only. It does

not constitute financial, investment, or trading advice, nor is

it a recommendation to buy or sell any asset.

2. **Use at Your Own Risk:** All trading decisions you make based on

the information or signals generated by this indicator are made

solely at your own risk.

3. **No Guarantee of Performance:** Past performance is not an

indicator of future results. The author makes no guarantee

regarding the accuracy of the signals or future profitability.

4. **No Liability:** The author shall not be held liable for any

financial losses or damages incurred directly or indirectly from

the use of this indicator.

5. **Signals Are Not Recommendations:** The alerts and visual signals

(e.g., crossovers) generated by this tool are not direct

recommendations to buy or sell. They are technical observations

for your own analysis and consideration.

Tìm kiếm tập lệnh với "volume"

Smarter Money Volume Rejection Blocks [PhenLabs]📊 Smarter Money Volume Rejection Blocks – Institutional Rejection Zone Detection

The Smarter Money Volume Rejection Blocks indicator combines high-volume analysis with statistical confidence intervals to identify where institutional traders are actively defending price levels through volume spikes and rejection patterns.

🔥 Core Methodology

Volume Spike Detection analyzes when current volume exceeds moving average by configurable multipliers (1.0-5.0x) to identify institutional activity

Rejection Candle Analysis uses dual-ratio system measuring wick percentage (30-90%) and maximum body ratio (10-60%) to confirm genuine rejections

Statistical Confidence Channels create three-level zones (upper, center, lower) based on ATR or Standard Deviation calculations

Smart Invalidation Logic automatically clears zones when price significantly breaches confidence levels to maintain relevance

Dynamic Channel Projection extends confidence intervals forward up to 200 bars with customizable length

Support Zone Identification detects bullish rejections where smart money absorbs selling pressure with high volume and strong lower wicks

Resistance Zone Mapping identifies bearish rejections where institutions defend price levels with volume spikes and pronounced upper wicks

Visual Information Dashboard displays real-time status table showing volume spike conditions and active support/resistance zones

⚙️ Technical Configuration

Dual Confidence Interval Methods: Choose between ATR-Based for trend-following environments or StdDev-Based for range-bound statistical precision

Volume Moving Average: Configurable period (default 20) for baseline volume comparison calculations

Volume Spike Multiplier: Adjustable threshold from 1.0 to 5.0 times average volume to filter institutional activity

Rejection Wick Percentage: Set minimum wick size from 30% to 90% of candle range for valid rejection detection

Maximum Body Ratio: Configure body-to-range ratio from 10% to 60% to ensure genuine rejection structures

Confidence Multiplier: Statistical multiplier (default 1.96) for 95% confidence interval calculations

Channel Projection Length: Extend confidence zones forward from 10 to 200 bars for anticipatory analysis

ATR Period: Customize Average True Range lookback from 5 to 50 bars for volatility-based calculations

StdDev Period: Adjust Standard Deviation period from 10 to 100 bars for statistical precision

🎯 Real-World Trading Applications

Identify high-probability support zones where institutional buyers have historically defended price with significant volume

Map resistance levels where smart money sellers consistently reject higher prices with volume confirmation

Combine with price action analysis to confirm breakout validity when price approaches confidence channel boundaries

Use invalidation signals to exit positions when smart money zones are definitively breached

Monitor the real-time dashboard to quickly assess current market structure and active rejection zones

Adapt strategy based on calculation method: ATR for trending markets, StdDev for ranging conditions

Set alerts on confidence level breaches to catch potential trend reversals or continuation patterns

📈 Visual Interpretation Guide

Green Zones indicate bullish rejection blocks where buyers defended with high volume and lower wicks

Red Zones indicate bearish rejection blocks where sellers defended with high volume and upper wicks

Solid Center Lines represent the core rejection price level where maximum volume activity occurred

Dashed Confidence Boundaries show upper and lower statistical limits based on volatility calculations

Zone Opacity decreases as channels extend forward to indicate decreasing confidence over time

Dashboard Color Coding provides instant visual feedback on active volume spike and zone conditions

⚠️ Important Considerations

Volume-based indicators identify historical rejection zones but cannot predict future price action with certainty

Market conditions change rapidly and institutional activity patterns evolve continuously

High volume does not guarantee level defense as market structure can shift without warning

Confidence intervals represent statistical probabilities, not guaranteed price boundaries

Weis Wave Volume MTF 🎯 Indicator Name

Weis Wave Volume (Multi‑Timeframe) — adapted from the original “Weis Wave Volume by LazyBear.”

This version adds multi‑timeframe (MTF) readings, configurable colors, font size, and screen position for clear dashboard‑style display.

🧠 Concept Background — What is Weis Wave Volume (WWV)?

The Weis Wave Volume indicator originates from Wyckoff and David Weis’ techniques.

Its purpose is to link price movement “waves” with the amount of traded volume to reveal how strong or weak each wave is.

Instead of showing bars one by one, WWV accumulates the total volume while price keeps moving in the same direction.

When price direction changes (up → down or down → up), it:

Finishes the previous wave volume total.

Starts a new wave and begins accumulating again.

Those wave volumes help traders see:

Effort vs Result: Big volume with small price move ⇒ absorption; low volume with big move ⇒ weak participation.

Trend confirmation or exhaustion: High volume waves in trend direction strengthen it, while low‑volume waves hint exhaustion.

⚙️ How this Script Works

Trend & Wave Detection

Compares close with the previous bar to determine up or down movement (mov).

Detects trend reversals (when mov direction changes).

Builds “waves,” each representing a continuous run of bars in one direction.

Volume Accumulation

While price keeps the same direction, the script adds each bar’s volume to the running total (vol).

When direction flips, it resets that total and starts a new wave.

Multi‑Timeframe Computation

Calculates these wave volumes on three timeframes at once, chosen dynamically:

Active Chart Timeframe Displays WWV for:

1 min 1 min

5 min 5 min

15 min 15 min

Any other Chart TF

It uses request.security() to pull each timeframe’s latest WWV value and current wave direction.

Visual Output

Instead of plotting histogram bars, it shows a table with three numeric values:

WWV (1): 25.3 M | (15): 312 M | (240): 2.46 B

Each value is color‑coded:

user‑selected Uptrend Color when price wave = up

user‑selected Downtrend Color when wave = down

You can position this small table in any corner/center (top / bottom × left / center / right).

Font size is user‑adjustable (Tiny → Huge).

📈 How Traders Use It

Quickly gauge buying vs selling effort across multiple horizons.

Compare short‑term wave volume to higher‑timeframe waves to spot:

Alignment → all up and big volumes = strong trend

Divergence → small or opposite‑colored higher‑TF wave = potential reversal or pause

Combine with Wyckoff, VSA, or standard trend analysis to judge if a breakout or pullback has real participation.

🧩 Key Features of This Version

Feature Description

Multi‑Timeframe Panel Displays WWV values for 3 selected TFs at once

Dynamic TF Mapping Auto‑adjusts which TFs to use based on chart

Up/Down Color Coding Customizable colors for wave direction

Adjustable Font and Placement Set font size (Tiny→Huge) and screen corner/center

No Histograms Keeps chart clean; acts as a compact WWV dashboard

RightFlow Universal Volume Profile - Any Market Any TimeframeSummary in one paragraph

RightFlow is a right anchored microstructure volume profile for stocks, futures, FX, and liquid crypto on intraday and daily timeframes. It acts only when several conditions align inside a session window and presents the result as a compact right side profile with value area, POC, a bull bear mix by price bin, and a HUD of profile VWAP and pressure shares. It is original because it distributes each bar’s weight into multiple mid price slices, blends bull bear pressure per bin with a CLV based split, and grows the profile to the right so price action stays readable. Add to a clean chart, read the table, and use the visuals. For conservative workflows read on bar close.

Scope and intent

• Markets. Major FX pairs, index futures, large cap equities and ETFs, liquid crypto.

• Timeframes. One minute to daily.

• Default demo used in the publication. SPY on 15 minute.

• Purpose. See where participation concentrates, which side dominated by price level, and how far price sits from VA and POC.

Originality and usefulness

• Unique fusion. Right anchored growth plus per bar slicing and CLV split, with weight modes Raw, Notional, and DeltaProxy.

• Failure mode addressed. False reads from single bar direction and coarse binning.

• Testability. All parts sit in Inputs and the HUD.

• Portable yardstick. Value Area percent and POC are universal across symbols.

• Protected scripts. Not applicable. Method and use are fully disclosed.

Method overview in plain language

Pick a scope Rolling or Today or This Week. Define a window and number of price bins. For each bar, split its range into small slices, assign each slice a weight from the selected mode, and split that weight by CLV or by bar direction. Accumulate totals per bin. Find the bin with the highest total as POC. Expand left and right until the chosen share of total volume is covered to form the value area. Compute profile VWAP for all, buyers, and sellers and show them with pressure shares.

Base measures

Range basis. High minus low and mid price samples across the bar window.

Return basis. Not used. VWAP trio is price weighted by weights.

Components

• RightFlow Bins. Price histogram that grows to the right.

• Bull Bear Split. CLV based 0 to 1 share or pure bar direction.

• Weight Mode. Raw volume, notional volume times close, or DeltaProxy focus.

• Value Area Engine. POC then outward expansion to target share.

• HUD. Profile VWAP, Buy and Sell percent, winner delta, split and weight mode.

• Session windows optional. Scope resets on day or week.

Fusion rule

Color of each bin is the convex blend of bull and bear shares. Value area shading is lighter inside and darker outside.

Signal rule

This is context, not a trade signal. A strong separation between buy and sell percent with price holding inside VA often confirms balance. Price outside VA with skewed pressure often marks initiative moves.

What you will see on the chart

• Right side bins with blended colors.

• A POC line across the profile width.

• Labels for POC, VAH, and VAL.

• A compact HUD table in the top right.

Table fields and quick reading guide

• VWAP. Profile VWAP.

• Buy and Sell. Pressure shares in percent.

• Delta Winner. Winner side and margin in percent.

• Split and Weight. The active modes.

Reading tip. When Session scope is Today or This Week and Buy minus Sell is clearly positive or negative, that side often controls the day’s narrative.

Inputs with guidance

Setup

• Profile scope. Rolling or session reset. Rolling uses window bars.

• Rolling window bars. Typical 100 to 300. Larger is smoother.

Binning

• Price bins. Typical 32 to 128. More bins increase detail.

• Slices per bar. Typical 3 to 7. Raising it smooths distribution.

Weighting

• Weight mode. Raw, Notional, DeltaProxy. Notional emphasizes expensive prints.

• Bull Bear split. CLV or BarDir. CLV is more nuanced.

• Value Area percent. Typical 68 to 75.

View

• Profile width in bars, color split toggle, value area shading, opacities, POC line, VA labels.

Usage recipes

Intraday trend focus

• Scope Today, bins 64, slices 5, Value Area 70.

• Split CLV, Weight Notional.

Intraday mean reversion

• Scope Today, bins 96, Value Area 75.

• Watch fades back to POC after initiative pushes.

Swing continuation

• Scope Rolling 200 bars, bins 48.

• Use Buy Sell skew with price relative to VA.

Realism and responsible publication

No performance claims. Shapes can move while a bar forms and settle on close. Education only.

Honest limitations and failure modes

Thin liquidity and data gaps can distort bin weights. Very quiet regimes reduce contrast. Session time is the chart venue time.

Open source reuse and credits

None.

Legal

Education and research only. Not investment advice. Test on history and simulation before live use.

Volume Order Block Scanner [BOSWaves]Volume Order Block Scanner - Dynamic Detection of High-Volume Supply and Demand Zones

Overview

The Volume Order Block Scanner introduces a refined approach to institutional zone mapping, combining volume-weighted order flow, structural displacement, and ATR-based proportionality to identify regions of aggressive participation from large entities.

Unlike static zone mapping or simplistic body-size filters, this framework dynamically evaluates each candle through a multi-layer model of relative volume, candle structure, and volatility context to isolate genuine order block formations while filtering out market noise.

Each identified zone represents a potential institutional footprint, defined by significant volume surges and efficient body-to-ATR relationships that indicate purposeful positioning. Once mapped, each order block is dynamically adjusted for volatility and tracked throughout its lifecycle - from creation to mitigation to potential invalidation - producing an evolving liquidity map that adapts with price.

This adaptive behavior allows traders to visualize where liquidity was absorbed and where it remains unfilled, revealing the structural foundation of institutional intent across timeframes.

Theoretical Foundation

At its core, the Volume Order Block Scanner is built on the interaction between volume displacement and structural imbalance. Traditional order block systems often rely on fixed candle formations or simple engulfing logic, neglecting the fundamental driver of institutional activity: volume concentration relative to volatility.

This framework redefines that approach. Each candle is filtered through two comparative ratios:

Relative Volume Ratio (RVR) - the candle’s volume compared to its rolling average, confirming genuine transactional surges.

Body-ATR Ratio (BAR) - a measure of displacement efficiency relative to recent volatility, ensuring structural strength.

Only when both conditions align is an order block validated, marking a displacement event significant enough to create a lasting imbalance.

By embedding this logic within a volatility-adjusted environment, the system maintains scalability across asset classes and volatility regimes - equally effective in crypto, forex, or index markets.

How It Works

The Volume Order Block Scanner operates through a structured multi-stage process:

Displacement Detection - Identifies candles whose body and volume exceed dynamic thresholds derived from ATR and rolling volume averages. These represent the origin points of institutional aggression.

Zone Construction - Each qualified candle generates an order block with ATR-proportional dimensions to ensure consistency across instruments and timeframes. The zone includes two regions: Body Zone (the precise initiation point of displacement) and Wick Imbalance (the residual inefficiency representing unfilled liquidity).

Lifecycle Tracking - Each zone is continuously monitored for market interaction. Reactions within a defined window are classified as respected, mitigated, or invalidated, giving traders a data-driven sense of ongoing institutional relevance.

Volume Confirmation Layer - Reinforces signal integrity by ensuring that all detected blocks correspond with meaningful increases in transactional activity.

Temporal Decay Control - Zones that remain untested beyond a set period gradually lose visual and analytical weight, maintaining chart clarity and contextual precision.

Interpretation

The Volume Order Block Scanner visualizes how institutional participants interact with the market through zones of accumulation and distribution.

Bullish order blocks denote demand imbalances where price displaced upward under high volume; bearish order blocks signify supply regions formed by concentrated selling pressure.

Price revisiting these areas often reflects institutional re-entry or liquidity rebalancing, offering actionable insights for both continuation and reversal scenarios.

By continuously monitoring interaction and expiry, the framework enables traders to distinguish between active institutional footprints and historical liquidity artifacts.

Strategy Integration

The Volume Order Block Scanner integrates naturally into advanced structural and order-flow methodologies:

Liquidity Mapping : Identify high-volume regions that are likely to influence future price reactions.

Break-of-Structure Confirmation : Validate BOS and CHOCH signals through aligned order block behavior.

Volume Confluence : Combine with BOSWaves volume or momentum indicators to confirm real institutional intent.

Smart-Money Frameworks : Utilize order block retests as precision entry zones within SMC-based setups.

Trend Continuation : Filter zones in line with higher-timeframe bias to maintain directional integrity.

Technical Implementation Details

Core Engine : Dual-filter mechanism using Relative Volume Ratio (RVR) and Body-ATR Ratio (BAR).

Volatility Framework : ATR-based scaling for cross-asset proportionality.

Zone Composition : Body and wick regions plotted independently for visual clarity of imbalance.

Lifecycle Logic : Real-time monitoring of reaction, mitigation, and invalidation states.

Directional Coloring : Distinct bullish and bearish shading with adjustable transparency.

Computation Efficiency : Lightweight structure suitable for multi-timeframe or multi-asset environments.

Optimal Application Parameters

Timeframe Guidance:

5m - 15m : Reactive intraday zones for short-term liquidity engagement.

1H - 4H : Medium-term structures for swing or intraday trend mapping.

Daily - Weekly : Macro accumulation and distribution footprints.

Suggested Configuration:

Relative Volume Threshold : 1.5× - 2.0× average volume.

Body-ATR Threshold : 0.8× - 1.2× for valid displacement.

Zone Expiry : 5 - 10 bars for intraday use, 15 - 30 for swing/macro contexts.

Parameter optimization should be asset-specific, tuned to volatility conditions and liquidity depth.

Performance Characteristics

High Effectiveness:

Markets exhibiting clear displacement and directional flow.

Environments with consistent volume expansion and liquidity inefficiencies.

Reduced Effectiveness:

Range-bound markets with frequent false impulses.

Low-volume sessions lacking institutional participation.

Integration Guidelines

Confluence Framework : Pair with structure-based BOS or liquidity tools for validation.

Risk Management : Treat active order blocks as contextual areas of interest, not guaranteed reversal points.

Multi-Timeframe Logic : Derive bias from higher-timeframe blocks and execute from refined lower-timeframe structures.

Volume Verification : Confirm each reaction with concurrent volume acceleration to avoid false liquidity cues.

Disclaimer

The Volume Order Block Scanner is a quantitative mapping framework designed for professional traders and analysts. It is not a predictive or guaranteed system of profit.

Performance depends on correct configuration, market conditions, and disciplined risk management. BOSWaves recommends using this indicator as part of a comprehensive analytical process - integrating structural, volume, and liquidity context for accurate interpretation.

Cumulative Volume Delta Divergence Periodic EMACumulative Volume Delta Divergence Periodic EMA

extended indicator

Nifty 50 Weighted Volume IndicatorThis takes the volume of the cash market as per the composite weighted average of the Nifty 50 Components.

You can use this at your discretion to take calls on Index trades.

Volume Delta Volume Signals by Claudio [hapharmonic]// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © hapharmonic

//@version=6

FV = format.volume

FP = format.percent

indicator('Volume Delta Volume Signals by Claudio ', format = FV, max_bars_back = 4999, max_labels_count = 500)

//------------------------------------------

// Settings |

//------------------------------------------

bool usecandle = input.bool(true, title = 'Volume on Candles',display=display.none)

color C_Up = input.color(#12cef8, title = 'Volume Buy', inline = ' ', group = 'Style')

color C_Down = input.color(#fe3f00, title = 'Volume Sell', inline = ' ', group = 'Style')

// ✅ Nueva entrada para colores de señales

color buySignalColor = input.color(color.new(color.green, 0), "Buy Signal Color", group = "Signals")

color sellSignalColor = input.color(color.new(color.red, 0), "Sell Signal Color", group = "Signals")

string P_ = input.string(position.top_right,"Position",options = ,

group = "Style",display=display.none)

string sL = input.string(size.small , 'Size Label', options = , group = 'Style',display=display.none)

string sT = input.string(size.normal, 'Size Table', options = , group = 'Style',display=display.none)

bool Label = input.bool(false, inline = 'l')

History = input.bool(true, inline = 'l')

// Inputs for EMA lengths and volume confirmation

bool MAV = input.bool(true, title = 'EMA', group = 'EMA')

string volumeOption = input.string('Use Volume Confirmation', title = 'Volume Option', options = , group = 'EMA',display=display.none)

bool useVolumeConfirmation = volumeOption == 'none' ? false : true

int emaFastLength = input(12, title = 'Fast EMA Length', group = 'EMA',display=display.none)

int emaSlowLength = input(26, title = 'Slow EMA Length', group = 'EMA',display=display.none)

int volumeConfirmationLength = input(6, title = 'Volume Confirmation Length', group = 'EMA',display=display.none)

string alert_freq = input.string(alert.freq_once_per_bar_close, title="Alert Frequency",

options= ,group = "EMA",

tooltip="If you choose once_per_bar, you will receive immediate notifications (but this may cause interference or indicator repainting).

\n However, if you choose once_per_bar_close, it will wait for the candle to confirm the signal before notifying.",display=display.none)

//------------------------------------------

// UDT_identifier |

//------------------------------------------

type OHLCV

float O = open

float H = high

float L = low

float C = close

float V = volume

type VolumeData

float buyVol

float sellVol

float pcBuy

float pcSell

bool isBuyGreater

float higherVol

float lowerVol

color higherCol

color lowerCol

//------------------------------------------

// Calculate volumes and percentages |

//------------------------------------------

calcVolumes(OHLCV ohlcv) =>

var VolumeData data = VolumeData.new()

data.buyVol := ohlcv.V * (ohlcv.C - ohlcv.L) / (ohlcv.H - ohlcv.L)

data.sellVol := ohlcv.V - data.buyVol

data.pcBuy := data.buyVol / ohlcv.V * 100

data.pcSell := 100 - data.pcBuy

data.isBuyGreater := data.buyVol > data.sellVol

data.higherVol := data.isBuyGreater ? data.buyVol : data.sellVol

data.lowerVol := data.isBuyGreater ? data.sellVol : data.buyVol

data.higherCol := data.isBuyGreater ? C_Up : C_Down

data.lowerCol := data.isBuyGreater ? C_Down : C_Up

data

//------------------------------------------

// Get volume data |

//------------------------------------------

ohlcv = OHLCV.new()

volData = calcVolumes(ohlcv)

// Plot volumes and create labels

plot(ohlcv.V, color=color.new(volData.higherCol, 90), style=plot.style_columns, title='Total',display = display.all - display.status_line)

plot(ohlcv.V, color=volData.higherCol, style=plot.style_stepline_diamond, title='Total2', linewidth = 2,display = display.pane)

plot(volData.higherVol, color=volData.higherCol, style=plot.style_columns, title='Higher Volume', display = display.all - display.status_line)

plot(volData.lowerVol , color=volData.lowerCol , style=plot.style_columns, title='Lower Volume',display = display.all - display.status_line)

S(D,F)=>str.tostring(D,F)

volStr = S(math.sign(ta.change(ohlcv.C)) * ohlcv.V, FV)

buyVolStr = S(volData.buyVol , FV )

sellVolStr = S(volData.sellVol , FV )

// ✅ MODIFICACIÓN: Porcentaje sin decimales

buyPercentStr = str.tostring(math.round(volData.pcBuy)) + " %"

sellPercentStr = str.tostring(math.round(volData.pcSell)) + " %"

totalbuyPercentC_ = volData.buyVol / (volData.buyVol + volData.sellVol) * 100

sup = not na(ohlcv.V)

if sup

TC = text.align_center

CW = color.white

var table tb = table.new(P_, 6, 6, bgcolor = na, frame_width = 2, frame_color = chart.fg_color, border_width = 1, border_color = CW)

tb.cell(0, 0, text = 'Volume Candles', text_color = #FFBF00, bgcolor = #0E2841, text_halign = TC, text_valign = TC, text_size = sT)

tb.merge_cells(0, 0, 5, 0)

tb.cell(0, 1, text = 'Current Volume', text_color = CW, bgcolor = #0B3040, text_halign = TC, text_valign = TC, text_size = sT)

tb.merge_cells(0, 1, 1, 1)

tb.cell(0, 2, text = 'Buy', text_color = #000000, bgcolor = #92D050, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(1, 2, text = 'Sell', text_color = #000000, bgcolor = #FF0000, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(0, 3, text = buyVolStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(1, 3, text = sellVolStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(0, 5, text = 'Net: ' + volStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.merge_cells(0, 5, 1, 5)

tb.cell(0, 4, text = buyPercentStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(1, 4, text = sellPercentStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

cellCount = 20

filledCells = 0

for r = 5 to 1 by 1

for c = 2 to 5 by 1

if filledCells < cellCount * (totalbuyPercentC_ / 100)

tb.cell(c, r, text = '', bgcolor = C_Up)

else

tb.cell(c, r, text = '', bgcolor = C_Down)

filledCells := filledCells + 1

filledCells

if Label

sp = ' '

l = label.new(bar_index, ohlcv.V,

text=str.format('Net: {0}\nBuy: {1} ({2})\nSell: {3} ({4})\n{5}/\\\n {5}l\n {5}l',

volStr, buyVolStr, buyPercentStr, sellVolStr, sellPercentStr, sp),

style=label.style_none, textcolor=volData.higherCol, size=sL, textalign=text.align_left)

if not History

(l ).delete()

//------------------------------------------

// Draw volume levels on the candlesticks |

//------------------------------------------

float base = na,float value = na

bool uc = usecandle and sup

if volData.isBuyGreater

base := math.min(ohlcv.O, ohlcv.C)

value := base + math.abs(ohlcv.O - ohlcv.C) * (volData.pcBuy / 100)

else

base := math.max(ohlcv.O, ohlcv.C)

value := base - math.abs(ohlcv.O - ohlcv.C) * (volData.pcSell / 100)

barcolor(sup ? color.new(na, na) : ohlcv.C < ohlcv.O ? color.red : color.green,display = usecandle? display.all:display.none)

UseC = uc ? volData.higherCol:color.new(na, na)

plotcandle(uc?base:na, uc?base:na, uc?value:na, uc?value:na,

title='Body', color=UseC, bordercolor=na, wickcolor=UseC,

display = usecandle ? display.all - display.status_line : display.none, force_overlay=true,editable=false)

plotcandle(uc?ohlcv.O:na, uc?ohlcv.H:na, uc?ohlcv.L:na, uc?ohlcv.C:na,

title='Fill', color=color.new(UseC,80), bordercolor=UseC, wickcolor=UseC,

display = usecandle ? display.all - display.status_line : display.none, force_overlay=true,editable=false)

//------------------------------------------------------------

// Plot the EMA and filter out the noise with volume control. |

//------------------------------------------------------------

float emaFast = ta.ema(ohlcv.C, emaFastLength)

float emaSlow = ta.ema(ohlcv.C, emaSlowLength)

bool signal = emaFast > emaSlow

color c_signal = signal ? C_Up : C_Down

float volumeMA = ta.sma(ohlcv.V, volumeConfirmationLength)

bool crossover = ta.crossover(emaFast, emaSlow)

bool crossunder = ta.crossunder(emaFast, emaSlow)

isVolumeConfirmed(source, length, ma) =>

math.sum(source > ma ? source : 0, length) >= math.sum(source < ma ? source : 0, length)

bool ISV = isVolumeConfirmed(ohlcv.V, volumeConfirmationLength, volumeMA)

bool crossoverConfirmed = crossover and (not useVolumeConfirmation or ISV)

bool crossunderConfirmed = crossunder and (not useVolumeConfirmation or ISV)

PF = MAV ? emaFast : na

PS = MAV ? emaSlow : na

p1 = plot(PF, color = c_signal, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 80), linewidth = 10, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 90), linewidth = 20, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 95), linewidth = 30, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 98), linewidth = 45, editable = false, force_overlay = true, display = display.pane)

p2 = plot(PS, color = c_signal, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 80), linewidth = 10, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 90), linewidth = 20, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 95), linewidth = 30, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 98), linewidth = 45, editable = false, force_overlay = true, display = display.pane)

fill(p1, p2, top_value=crossover ? emaFast : emaSlow,

bottom_value =crossover ? emaSlow : emaFast,

top_color =color.new(c_signal, 80),

bottom_color =color.new(c_signal, 95)

)

// ✅ Usar colores configurables para señales

plotshape(crossoverConfirmed and MAV, style=shape.triangleup , location=location.belowbar, color=buySignalColor , size=size.small, force_overlay=true,display =display.pane)

plotshape(crossunderConfirmed and MAV, style=shape.triangledown, location=location.abovebar, color=sellSignalColor, size=size.small, force_overlay=true,display =display.pane)

string msg = '---------\n'+"Buy volume ="+buyVolStr+"\nBuy Percent = "+buyPercentStr+"\nSell volume = "+sellVolStr+"\nSell Percent = "+sellPercentStr+"\nNet = "+volStr+'\n---------'

if crossoverConfirmed

alert("Price (" + str.tostring(close) + ") Crossed over MA\n" + msg, alert_freq)

if crossunderConfirmed

alert("Price (" + str.tostring(close) + ") Crossed under MA\n" + msg, alert_freq)

VSA Volume MonitorDescription

This script provides a clear and adaptable visual representation of volume activity, helping traders understand how current participation compares to recent norms.

It calculates a moving average of volume over a user-defined smoothing window and uses that baseline to classify each bar’s volume into several intensity levels.

Bars are color-coded to reflect these levels:

• Blue for below-average activity

• Green for moderate activity

• Yellow for above-average surges

• Red for exceptionally high or climactic volume

In addition to color-coded bars, the script plots two reference bands that represent the typical (baseline) and elevated (climactic) volume zones.

These bands form a shaded cloud that helps visually separate normal market participation from periods of unusual crowd activity or volatility.

The purpose of this indicator is purely visual and informational — it does not generate buy or sell signals, and it does not predict future price movement.

Instead, it gives traders an at-a-glance view of how market interest is shifting, so they can combine that context with their own analysis or strategy.

This tool is lightweight, easy to read, and designed for use alongside other forms of technical analysis, making it suitable for traders who want to build their own framework for understanding volume behavior.

Prev Day Volume ProfileWhat the script does

Calculates yesterday’s Volume Profile from the bars on your chart (not tick data) and derives:

POC (Point of Control)

VAL (Value Area Low)

VAH (Value Area High)

Draws three horizontal lines for today:

POC in orange

VAL and VAH in purple

Adds labels on the right edge that show the level name and the exact price (e.g., POC 1.2345).

Why it’s bar-based (not tick-based)

Pine Script can’t fetch external tick/aggTrades data. The script approximates a volume profile by distributing each bar’s volume across the price bins that the bar’s high–low range covers. For “yesterday”, this produces a stable, TV-native approximation that’s usually sufficient for intraday trading.

Key inputs

Value Area %: Defaults to 0.70 (70%)—the typical value area range.

TZ Offset vs Exchange (hours): Shifts the day boundary to match your desired session (e.g., Europe/Berlin: +1 winter / +2 summer). This ensures “yesterday” means 00:00–24:00 in your target timezone.

Row Size: Manual? / Manual Row Size: If enabled, you can set the price bin size yourself. Otherwise, the script chooses a TV-like step from syminfo.mintick.

Colors & Line width: POC orange; VAL/VAH purple; configurable width.

High Volume Candles - RVolInspired by Key bars from Option Stalker Pro.

This one is meant to be used on charts where the interval is >=1D.

Highlights candles where RVol is > 1.2.

Helps to not accidentally miss that a candle move happened on high volume (or that it did not happen on high volume...), like potential reversals or resistance/support breaks.

Make sure to move this indicator above the ticker in the Object Tree, so that it is drawn on top of the ticker's candles.

More infos: www.reddit.com

Volume Profile Grid [Alpha Extract]A sophisticated volume distribution analysis system that transforms market activity into institutional-grade visual profiles, revealing hidden support/resistance zones and market participant behavior. Utilizing advanced price level segmentation, bullish/bearish volume separation, and dynamic range analysis, the Volume Profile Grid delivers comprehensive market structure insights with Point of Control (POC) identification, Value Area boundaries, and volume delta analysis. The system features intelligent visualization modes, real-time sentiment analysis, and flexible range selection to provide traders with clear, actionable volume-based market context.

🔶 Dynamic Range Analysis Engine

Implements dual-mode range selection with visible chart analysis and fixed period lookback, automatically adjusting to current market view or analyzing specified historical periods. The system intelligently calculates optimal bar counts while maintaining performance through configurable maximum limits, ensuring responsive profile generation across all timeframes with institutional-grade precision.

// Dynamic period calculation with intelligent caching

get_analysis_period() =>

if i_use_visible_range

chart_start_time = chart.left_visible_bar_time

current_time = last_bar_time

time_span = current_time - chart_start_time

tf_seconds = timeframe.in_seconds()

estimated_bars = time_span / (tf_seconds * 1000)

range_bars = math.floor(estimated_bars)

final_bars = math.min(range_bars, i_max_visible_bars)

math.max(final_bars, 50) // Minimum threshold

else

math.max(i_periods, 50)

🔶 Advanced Bull/Bear Volume Separation

Employs sophisticated candle classification algorithms to separate bullish and bearish volume at each price level, with weighted distribution based on bar intersection ratios. The system analyzes open/close relationships to determine volume direction, applying proportional allocation for doji patterns and ensuring accurate representation of buying versus selling pressure across the entire price spectrum.

🔶 Multi-Mode Volume Visualization

Features three distinct display modes for bull/bear volume representation: Split mode creates mirrored profiles from a central axis, Side by Side mode displays sequential bull/bear segments, and Stacked mode separates volumes vertically. Each mode offers unique insights into market participant behavior with customizable width, thickness, and color parameters for optimal visual clarity.

// Bull/Bear volume calculation with weighted distribution

for bar_offset = 0 to actual_periods - 1

bar_high = high

bar_low = low

bar_volume = volume

// Calculate intersection weight

weight = math.min(bar_high, next_level) - math.max(bar_low, current_level)

weight := weight / (bar_high - bar_low)

weighted_volume = bar_volume * weight

// Classify volume direction

if bar_close > bar_open

level_bull_volume += weighted_volume

else if bar_close < bar_open

level_bear_volume += weighted_volume

else // Doji handling

level_bull_volume += weighted_volume * 0.5

level_bear_volume += weighted_volume * 0.5

🔶 Point of Control & Value Area Detection

Implements institutional-standard POC identification by locating the price level with maximum volume accumulation, providing critical support/resistance zones. The Value Area calculation uses sophisticated sorting algorithms to identify the price range containing 70% of trading volume, revealing the market's accepted value zone where institutional participants concentrate their activity.

🔶 Volume Delta Analysis System

Incorporates real-time volume delta calculation with configurable dominance thresholds to identify significant bull/bear imbalances. The system visually highlights price levels where buying or selling pressure exceeds threshold percentages, providing immediate insight into directional volume flow and potential reversal zones through color-coded delta indicators.

// Value Area calculation using 70% volume accumulation

total_volume_sum = array.sum(total_volumes)

target_volume = total_volume_sum * 0.70

// Sort volumes to find highest activity zones

for i = 0 to array.size(sorted_volumes) - 2

for j = i + 1 to array.size(sorted_volumes) - 1

if array.get(sorted_volumes, j) > array.get(sorted_volumes, i)

// Swap and track indices for value area boundaries

// Accumulate until 70% threshold reached

for i = 0 to array.size(sorted_indices) - 1

accumulated_volume += vol

array.push(va_levels, array.get(volume_levels, idx))

if accumulated_volume >= target_volume

break

❓How It Works

🔶 Weighted Volume Distribution

Implements proportional volume allocation based on the percentage of each bar that intersects with price levels. When a bar spans multiple levels, volume is distributed proportionally based on the intersection ratio, ensuring precise representation of trading activity across the entire price spectrum without double-counting or volume loss.

🔶 Real-Time Profile Generation

Profiles regenerate on each bar close when in visible range mode, automatically adapting to chart zoom and scroll actions. The system maintains optimal performance through intelligent caching mechanisms and selective line updates, ensuring smooth operation even with maximum resolution settings and extended analysis periods.

🔶 Market Sentiment Analysis

Features comprehensive volume analysis table displaying total volume metrics, bullish/bearish percentages, and overall market sentiment classification. The system calculates volume dominance ratios in real-time, providing immediate insight into whether buyers or sellers control the current price structure with percentage-based sentiment thresholds.

🔶 Visual Profile Mapping

Provides multi-layered visual feedback through colored volume bars, POC line highlighting, Value Area boundaries, and optional delta indicators. The system supports profile mirroring for alternative perspectives, line extension for future reference, and customizable label positioning with detailed price information at critical levels.

Why Choose Volume Profile Grid

The Volume Profile Grid represents the evolution of volume analysis tools, combining traditional volume profile concepts with modern visualization techniques and intelligent analysis algorithms. By integrating dynamic range selection, sophisticated bull/bear separation, and multi-mode visualization with POC/Value Area detection, it provides traders with institutional-quality market structure analysis that adapts to any trading style. The comprehensive delta analysis and sentiment monitoring system eliminates guesswork while the flexible visualization options ensure optimal clarity across all market conditions, making it an essential tool for traders seeking to understand true market dynamics through volume-based price discovery.

Piman2077: Previous Day Volume Profile levelsPrevious Day Volume Profile Indicator

Description:

Previous Day Volume Profile Indicator plots the previous trading session’s Volume Profile key levels directly on your chart, providing clear reference points for intraday trading. This indicator calculates the Value Area High (VAH), Value Area Low (VAL), and Point of Control (POC) from the prior session and projects them across the current trading day, helping traders identify potential support, resistance, and high-volume zones.

Features:

Calculates previous day VAH, VAL, and POC based on a user-defined session (default 09:30–16:00).

Uses Volume Profile bins for precise distribution calculation.

Fully customizable line colors for VAH, VAL, and POC.

Lines extend across the current session for easy intraday reference.

Works on any timeframe, optimized for 1-minute charts for precision.

Optional toggles to show/hide VAH, VAL, and POC individually.

Inputs:

Session Time: Define the trading session for which the volume profile is calculated.

Profile Bins: Number of price intervals used to divide the session range.

Value Area %: Percentage of volume to include in the value area (default 68%).

Show POC / VAH & VAL: Toggle visibility of each level.

Line Colors: Customize VAH, VAL, and POC colors.

Use Cases:

Identify previous session support and resistance levels for intraday trading.

Gauge areas of high liquidity and potential market reaction zones.

Combine with other indicators or price action strategies for improved entries and exits.

Recommended Timeframe:

Works on all timeframes; best used on 1-minute or 5-minute charts for precise intraday analysis.

Cumulative Volume Delta with EMA PlotCumulative Delta Volume is a key tool for analyzing the relationship between trading volume and price movement, often referred to as Volume Price Action.

In this indicator, an Exponential Moving Average (EMA) is applied to smooth out short-term noise and reduce volatility, making trends easier to identify. Traders can watch for EMA crossovers as confirmation signals for potential trend reversals, as well as buying or selling opportunities.

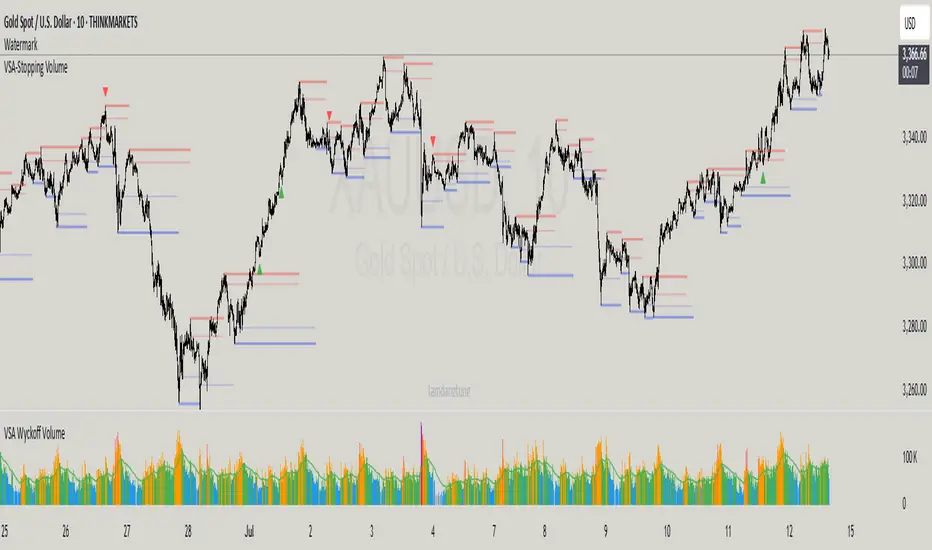

VSA-Stopping VolumeVSA Stopping Volume Indicator

Stopping Volume occurs when candles show decreasing body sizes (narrow spreads) while volume steadily increases.

Example chart:

As you see:

3 consecutive candles in same direction (all green OR all red)

Body sizes (spreads) decreasing progressively: Candle 1 > Candle 2 > Candle 3

Volume increasing progressively: Volume 1 < Volume 2 < Volume 3

This pattern indicates price absorption - increased buying/selling pressure but declining price movement, often signaling exhaustion and potential reversal.

Indicator Features

This indicator detects Stopping Volume candlestick clusters with two signal types:

🔹 BUY/SELL Signals: Generated when pattern occurs at support/resistance zones

🔹 Directional Alerts (▲-green, ▼-red): Generated when pattern occurs outside key levels

Trading Guidelines:

⚠️ Auto-drawn S/R zones are reference only - manual level plotting recommended for accuracy

📊 Best for scalping: M5, M10, M15 timeframes

🛡️ Stop Loss: Place beyond the S/R zone you're trading

🎯 Take Profit: Based on your risk management

Key Concept: Volume expansion + price contraction = potential reversal, especially at SnR levels.

Perfect for scalpers looking to catch reversals at critical zones!

ds-Volume with Flags & Alerts v1.2ds-Volume with Flags & Alerts: User & Training Guide

1. Summary of Features

This indicator is a powerful, all-in-one tool designed to give you a deep and customizable view of market volume. By analyzing volume in multiple ways, it helps you spot unusual activity, confirm trends, and identify potential reversals.

How It Helps a Trader:

Spotting Institutional Activity: The core purpose of the Volume Flags (using either the Multiplier or Standard Deviation method) is to highlight bars with exceptionally high volume. These spikes often signal the entry or exit of large institutional players. A high-volume up-bar can confirm bullish conviction, while a high-volume down-bar can signal significant selling pressure.

Identifying Climactic Events: The HVE (Highest Volume Ever) and HV1 (Highest Volume - 1 Year) labels automatically pinpoint the most significant volume events on the chart. A "blow-off top" at the end of a long uptrend or a "capitulation" event at a market bottom is almost always accompanied by an HVE or HV1 bar. These are critical moments to watch for potential trend reversals.

Gauging Buying vs. Selling Pressure: The Up/Down Volume Ratio gives you a more nuanced view than volume alone. A ratio consistently above 1.2 suggests that buyers are more aggressive, while a ratio below 0.8 suggests sellers are in control. Watching this ratio can help you confirm the strength of a trend or spot divergences where price is rising but the ratio is falling (a potential warning sign).

Visual Confirmation & Customization: With options to color both the volume bars and the main price bars, you can get instant visual confirmation of these events without having to look away from the price action. The ability to toggle features on and off keeps your chart clean and focused on what matters most to you.

Actionable Alerts: The comprehensive alert system ensures you don't miss a key event. You can be notified of everything from a new all-time high volume bar to a subtle shift in the Up/Down Volume Ratio, allowing you to react to market changes in real-time.

2. User-Changeable Options

This indicator is highly customizable. Here is a breakdown of every setting available in the "Inputs" tab.

General Settings

MA Length: The lookback period for the simple moving average (the gray area plot) of the volume.

Volume Flags

Color Price Bars with Flags: If checked, the main price bars on your chart will be colored when a high or low volume flag condition is met.

Color Volume Bars with Flags: If checked, the volume bars in the indicator pane will be colored for flag conditions.

Flag Calculation Method: This is a crucial setting.

Multiplier (Default): Identifies high volume based on a simple multiple of the average volume (e.g., volume is 1.4x its average). It's simple and intuitive.

Standard Deviation: Identifies high volume based on how statistically unusual it is compared to its recent behavior. This method is more adaptive to changing market volatility.

Daily/Weekly Lookback (Multiplier): Sets the lookback period for calculating the average volume when using the "Multiplier" method.

Daily/Weekly High-Vol Multiplier: Sets the multiplier for a high volume event (e.g., 1.4).

STDEV Length (Daily/Weekly): Sets the lookback period for calculating the average and standard deviation when using the "Standard Deviation" method.

STDEV Threshold (Daily/Weekly): Sets the number of standard deviations above the average required to trigger a high volume flag (e.g., 2.0).

Daily/Weekly Low-Vol Multiplier: Sets the threshold for a low volume event (e.g., 0.5 means volume is less than 50% of its average). This is always based on the multiplier method.

Ratios & Stats

Up/Down Ratio Daily/Weekly Lookback: Sets the lookback period for calculating the sum of up volume and down volume for the ratio.

Ratio Calculation Method:

Close vs. Open: Defines an "up volume" bar as one where the close is higher than the open.

Close vs. Previous Close (Default): Defines an "up volume" bar as one where the close is higher than the previous bar's close. This is a common standard.

Up Ratio Arrow Threshold: If the U/D Ratio exceeds this value, a green "up" arrow will appear.

Show Up Ratio Arrow: Toggles the visibility of the green "up" arrow.

Down Ratio Arrow Threshold: If the U/D Ratio falls below this value, a red "down" arrow will appear.

Show Down Ratio Arrow: Toggles the visibility of the red "down" arrow.

Volume Point of Control with Fib Based Profile🍀Description:

This indicator is a comprehensive volume profile analysis tool designed to identify key price levels based on trading activity within user-defined timeframes. It plots the Point of Control (POC), Value Area High (VAH), and Value Area Low (VAL), along with dynamically calculated Fibonacci levels derived from the developing period's range. It offers extensive customization for both historical and developing levels.

🍀Core Features:

Volume Profiling (POC, VAH, VAL):

Calculates and plots the POC (price level with the highest volume), VAH, and VAL for a selected timeframe (e.g., Daily, Weekly).

The Value Area percentage is configurable. 70% is common on normal volume profiles, but this script allows you to configure multiple % levels via the fib levels. I recommend using 2 versions of this indicator on a chart, one has Value Area at 1 (100% - high and low of lookback) and the second is a specified VA area (i.e. 70%) like in the chart snapshot above. See examples at the bottom.

Historical Levels:

Plots POC, VAH, and VAL from previous completed periods.

Optionally displays only "Unbroken" levels – historical levels that price has not yet revisited, which can act as stronger magnets or resistance/support.

The user can manage the number of historical lines displayed to prevent chart clutter.

Developing Levels:

Shows the POC, VAH, and VAL as they form in real-time during the current, incomplete period. This provides insight into intraday/intra-period value migration.

Dynamic Fibonacci Levels:

Calculates and plots Fibonacci retracement/extension levels based dynamically on the range between the developing POC and the developing VAH/VAL.

Offers 8 configurable % levels above and below POC that can be toggled on/off.

Visual Customization:

Extensive options for colors, line styles, and widths for all plotted levels.

Optional gradient fill for the Value Area that visualizes current price distance from POC - option to invert the colors as well.

Labels for developing levels and Fibonacci levels for easy identification.

🍀Characteristics:

Volume-Driven: Levels are derived from actual trading volume, reflecting areas of high participation and price agreement/disagreement.

Timeframe Specific: The results are entirely dependent on the chosen profile timeframe.

Dynamic & Static Elements: Developing levels and Fibs update live, while historical levels remain fixed once their period closes.

Lagging (Historical) & Potentially Leading: Historical levels are based on the past, but are often respected by future price action. Developing levels show current dynamics.

🍀How to Use It:

Identifying Support & Resistance: Historical and developing POCs, VAHs, and VALs are often key areas where price may react. Unbroken levels are particularly noteworthy.

Market Context & Sentiment: Trading above the POC suggests bullish strength/acceptance of higher prices, while trading below suggests bearishness/acceptance of lower prices.

Entry/Exit Zones: Interactions with these levels (rejections, breakouts, tests) can provide potential entry or exit signals, especially when confirming with other analysis methods.

Dynamic Targets: The Fibonacci levels calculated from the developing POC-VA range offer potential intraday/intra-period price targets or areas of interest.

Understanding Value Migration: Observing the movement of the developing POC/VAH/VAL throughout the period reveals where value is currently being established.

🍀Potential Drawbacks:

Input Sensitivity: The choice of timeframe, Value Area percentage, and volume resolution heavily influences the generated levels. Experimentation is needed for optimal settings per instrument/market. (I've found that Range Charts can provide very accurate volume levels on TV since the time element is removed. This helps to refine the accuracy of price levels with high volume.)

Volume Data Dependency: Requires accurate volume data. May be less reliable on instruments with sparse or questionable volume reporting.

Chart Clutter: Enabling all features simultaneously can make the chart busy. Utilize the line management inputs and toggle features as needed.

Not a Standalone Strategy: This indicator provides context and key levels. It should be used alongside other technical analysis tools and price action reading for robust decision-making.

Developing Level Fluctuation: Developing POC/VA/Fib levels can shift considerably, especially early in a new period, before settling down as more volume accumulates and time passes.

🍀Recommendations/Examples:

I recommend have this indicator on your chart twice, one has the VA set at 1 (100%) and has the fib levels plotted. The second has the VA set to 0.7 (70%) to highlight the defined VA.

Here is an example with 3 on a chart. VA of 100%, VA of 80%, and VA of 20%

Volume pressure by GSK-VIZAG-AP-INDIA🔍 Volume Pressure by GSK-VIZAG-AP-INDIA

🧠 Overview

“Volume Pressure” is a multi-timeframe, real-time table-based volume analysis tool designed to give traders a clear and immediate view of buying and selling pressure across custom-selected timeframes. By breaking down buy volume, sell volume, total volume, and their percentages, this indicator helps traders identify demand/supply imbalances and volume momentum in the market.

🎯 Purpose / Trading Use Case

This indicator is ideal for intraday and short-term traders who want to:

Spot aggressive buying or selling activity

Track volume dynamics across multiple timeframes *1 min time frame will give best results*

Use volume pressure as a confirming tool alongside price action or trend-based systems

It helps determine when large buying/selling activity is occurring and whether such behavior is consistent across timeframes—a strong signal of institutional interest or volume-driven trend shifts.

🧩 Key Features & Logic

Real-Time Table Display: A clean, dynamic table showing:

Buy Volume

Sell Volume

Total Volume

Buy % of total volume

Sell % of total volume

Multi-Time frame Analysis: Supports 8 user-selectable custom time frames from 1 to 240 minutes, giving flexibility to analyze volume pressure at various granularities.

Color-Coded Volume Bias:

Green for dominant Buy pressure

Red for dominant Sell pressure

Yellow for Neutral

Intensity-based blinking for extreme values (over 70%)

Dynamic Data Calculation:

Uses volume * (close > open) logic to estimate buy vs sell volumes bar-by-bar, then aggregates by timeframe.

⚙️ User Inputs & Settings

Timeframe Selectors (TF1 to TF8): Choose any 8 timeframes you want to monitor volume pressure across.

Text & Color Settings:

Customize text colors for Buy, Sell, Total volumes

Choose Buy/Sell bias colors

Enable/disable blinking for visual emphasis on extremes

Table Appearance:

Set header color, metric background, and text size

Table positioning: top-right, bottom-right, etc.

Blinking Highlight Toggle: Enable this to visually highlight when Buy/Sell % exceeds 70%—a sign of strong pressure.

📊 Visual Elements Explained

The table has 6 rows and 10 columns:

Row 0: Headers for Today and TF1 to TF8

Rows 1–3: Absolute values (Buy Vol, Sell Vol, Total Vol)

Rows 4–5: Relative percentages (Buy %, Sell %), with dynamic background color

First column shows the metric names (e.g., “Buy Vol”)

Cells blink using alternate background colors if volume pressure crosses thresholds

💡 How to Use It Effectively

Use Buy/Sell % rows to confirm potential breakout trades or identify volume exhaustion zones

Look for multi-timeframe confluence: If 5 or more TFs show >70% Buy pressure, buyers are in control

Combine with price action (e.g., breakouts, reversals) to increase conviction

Suitable for equities, indices, futures, crypto, especially on lower timeframes (1m to 15m)

🏆 What Makes It Unique

Table-based MTF Volume Pressure Display: Most indicators only show volume as bars or histograms; this script summarizes and color-codes volume bias across timeframes in a tabular format.

Customization-friendly: Full control over colors, themes, and timeframes

Blinking Alerts: Rare visual feature to capture user attention during extreme pressure

Designed with performance and readability in mind—even for fast-paced scalping environments.

🚨 Alerts / Extras

While this script doesn’t include TradingView alert functions directly, the visual blinking serves as a strong real-time alert mechanism.

Future versions may include built-in alert conditions for buy/sell bias thresholds.

🔬 Technical Concepts Used

Volume Dissection using close > open logic (to estimate buyer vs seller pressure)

Simple aggregation of volume over custom timeframes

Table plotting using Pine Script table.new, table.cell

Dynamic color logic for bias identification

Custom blinking logic using na(bar_index % 2 == 0 ? colorA : colorB)

⚠️ Disclaimer

This indicator is a tool for analysis, not financial advice. Always backtest and validate strategies before using any indicator for live trading. Past performance is not indicative of future results. Use at your own risk and apply proper risk management.

✍️ Author & Signature

Indicator Name: Volume Pressure

Author: GSK-VIZAG-AP-INDIA

TradingView Username: prowelltraders

Relative Volume Indicator (RVOL)Relative Volume Indicator (RVOL)

The Relative Volume Indicator (RVOL) helps traders identify unusual volume activity by comparing the current volume to the average historical volume. This makes it easier to spot potential breakouts, reversals, or significant market events that are accompanied by volume confirmation.

What This Indicator Shows

This indicator displays volume as a multiple of average volume, where:

- 1.0x means 100% of average volume

- 2.0x means 200% of average volume (twice the average)

- 0.5x means 50% of average volume (half the average)

Color Coding

The volume bars are color-coded based on configurable thresholds:

- Red: Below average volume (< Average Volume Threshold)

- Yellow: Average volume (between Average Volume and Above Average thresholds)

- Green: Above average volume (between Above Average and Extreme thresholds)

- Magenta: Extreme volume (> Extreme Volume Threshold)

Horizontal Reference Lines

Three dotted horizontal reference lines help you visualize the thresholds:

- Lower gray line: Average Volume Threshold (default: 0.8x)

- Upper gray line: Above Average Threshold (default: 1.25x)

- Magenta line: Extreme Volume Threshold (default: 4.0x)

How To Use This Indicator

1. Volume Confirmation: Use green bars to confirm breakouts or trend changes - stronger moves often come with above-average volume.

2. Low Volume Warning: Red bars during price movements may indicate weak conviction and potential reversals.

3. Extreme Volume Events: Magenta bars (extreme volume) often signal major market events or potential exhaustion points that could lead to reversals.

4. Volume Divergence: Look for divergences between price and volume - for example, if price makes new highs but volume is decreasing (more yellow/red bars), the move may be losing strength.

Settings Configuration

- Average Volume Lookback Period: Number of bars used to calculate the average volume (default: 20)

- Average Volume Threshold: Volume below this level is considered below average (default: 0.8x)

- Above Average Threshold: Volume above this level is considered above average (default: 1.25x)

- Extreme Volume Threshold: Volume above this level is considered extreme (default: 4.0x)

- Colors: Customize colors for each volume category

Important Note: Adjust threshold values only through the indicator settings (not in the Style tab). Changing values in the Style tab will not adjust the coloring of the volume bars.

Adjust these settings based on the specific asset being analyzed and your trading timeframe. More volatile assets may require higher thresholds, while less volatile ones might need lower thresholds.

Intraday Volume Indicator for INDICES by TBTPH Pine Script code for an intraday volume indicator with session and lunch break highlights looks great! Here’s a summary of what each part of the script does:

Indicator Settings:

The indicator is set to show on a separate pane (overlay=false).

The SMA Length is adjustable with an input box (default of 20).

Volume and SMA Calculation:

You calculate the Simple Moving Average (SMA) of the volume over the selected length.

The volume color is determined based on whether the close price is higher or lower than the previous close and if the volume is above or below the SMA.

Volume Plot:

Volume is plotted as a histogram with different colors to indicate if the volume is higher or lower than the SMA.

You plot the SMA of the volume with an orange line for easier comparison.

Background Color:

You set a light gray background color to give a subtle contrast.

NYSE and LSE trading sessions are highlighted with green and blue, respectively.

Lunch break periods are highlighted with a white background for both exchanges.

Here are a couple of improvements or suggestions you might consider:

Session Time Overlap Handling:

If the script is applied to a chart where both NYSE and LSE data is visible, they may overlap depending on the time zone of your chart. Ensure the session times align with the active market's timezone, especially if you are using a chart with a different timezone setting.

Color Customization:

The color scheme for bullish/bearish volume could be enhanced further. For example, you could introduce more transparency for low-volume periods to make the histogram appear more subtle during less active trading times.

Handling Different Time Zones:

If your chart is not in the "America/New_York" or "GMT" time zone, be mindful of the session times. The timestamp function depends on the chart’s time zone, so ensuring you're adjusting for different markets is key.

Premarket VolumeTimeframe: Use on intraday charts (e.g., 1-minute, 5-minute) with extended hours enabled.

Behavior: The plot will appear at 4:00 AM, grow as volume accumulates, and disappear at 9:30 AM each day.

Lemon/Lime Volume Lookback IndicatorThe indicator focuses on analyzing volume patterns.

It calculates a relative volume metric by comparing the current volume to a short-term simple moving average of volume.

The code identifies volume spikes when the relative volume exceeds a user-defined threshold.

These volume spikes are visually represented on the chart as small circles:

Yellow circles appear above bars for bearish volume spikes (when price closed lower)

Green circles appear below bars for bullish volume spikes (when price closed higher)

Users can adjust settings such as the lookback period for volume comparison and the percentage increase that defines a volume spike. This would adjust the readings based on incoming volume. Adjust as needed during different market conditions.

This tool essentially helps traders identify and visualize significant increases in trading volume compared to recent average volume, which could potentially signal important price movements or trend changes.

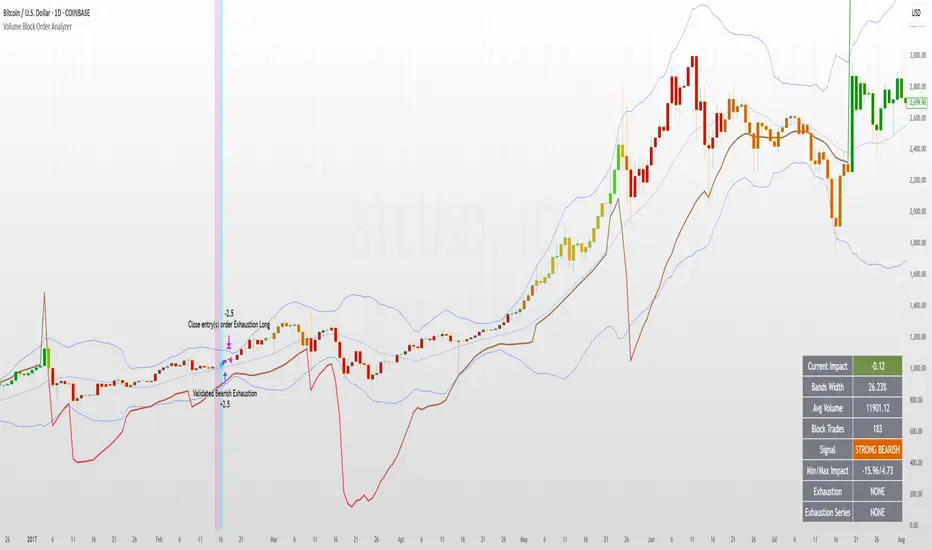

Volume Block Order AnalyzerCore Concept

The Volume Block Order Analyzer is a sophisticated Pine Script strategy designed to detect and analyze institutional money flow through large block trades. It identifies unusually high volume candles and evaluates their directional bias to provide clear visual signals of potential market movements.

How It Works: The Mathematical Model

1. Volume Anomaly Detection

The strategy first identifies "block trades" using a statistical approach:

```

avgVolume = ta.sma(volume, lookbackPeriod)

isHighVolume = volume > avgVolume * volumeThreshold

```

This means a candle must have volume exceeding the recent average by a user-defined multiplier (default 2.0x) to be considered a significant block trade.

2. Directional Impact Calculation

For each block trade identified, its price action determines direction:

- Bullish candle (close > open): Positive impact

- Bearish candle (close < open): Negative impact

The magnitude of impact is proportional to the volume size:

```

volumeWeight = volume / avgVolume // How many times larger than average

blockImpact = (isBullish ? 1.0 : -1.0) * (volumeWeight / 10)

```

This creates a normalized impact score typically ranging from -1.0 to 1.0, scaled by dividing by 10 to prevent excessive values.

3. Cumulative Impact with Time Decay

The key innovation is the cumulative impact calculation with decay:

```

cumulativeImpact := cumulativeImpact * impactDecay + blockImpact

```

This mathematical model has important properties:

- Recent block trades have stronger influence than older ones

- Impact gradually "fades" at rate determined by decay factor (default 0.95)

- Sustained directional pressure accumulates over time

- Opposing pressure gradually counteracts previous momentum

Trading Logic

Signal Generation

The strategy generates trading signals based on momentum shifts in institutional order flow:

1. Long Entry Signal: When cumulative impact crosses from negative to positive

```

if ta.crossover(cumulativeImpact, 0)

strategy.entry("Long", strategy.long)

```

*Logic: Institutional buying pressure has overcome selling pressure, indicating potential upward movement*

2. Short Entry Signal: When cumulative impact crosses from positive to negative

```

if ta.crossunder(cumulativeImpact, 0)

strategy.entry("Short", strategy.short)

```

*Logic: Institutional selling pressure has overcome buying pressure, indicating potential downward movement*

3. Exit Logic: Positions are closed when the cumulative impact moves against the position

```

if cumulativeImpact < 0

strategy.close("Long")

```

*Logic: The original signal is no longer valid as institutional flow has reversed*

Visual Interpretation System

The strategy employs multiple visualization techniques:

1. Color Gradient Bar System:

- Deep green: Strong buying pressure (impact > 0.5)

- Light green: Moderate buying pressure (0.1 < impact ≤ 0.5)

- Yellow-green: Mild buying pressure (0 < impact ≤ 0.1)

- Yellow: Neutral (impact = 0)

- Yellow-orange: Mild selling pressure (-0.1 < impact ≤ 0)

- Orange: Moderate selling pressure (-0.5 < impact ≤ -0.1)

- Red: Strong selling pressure (impact ≤ -0.5)

2. Dynamic Impact Line:

- Plots the cumulative impact as a line

- Line color shifts with impact value

- Line movement shows momentum and trend strength

3. Block Trade Labels:

- Marks significant block trades directly on the chart

- Shows direction and volume amount

- Helps identify key moments of institutional activity

4. Information Dashboard:

- Current impact value and signal direction

- Average volume benchmark

- Count of significant block trades

- Min/Max impact range

Benefits and Use Cases

This strategy provides several advantages:

1. Institutional Flow Detection: Identifies where large players are positioning themselves

2. Early Trend Identification: Often detects institutional accumulation/distribution before major price movements

3. Market Context Enhancement: Provides deeper insight than simple price action alone

4. Objective Decision Framework: Quantifies what might otherwise be subjective observations

5. Adaptive to Market Conditions: Works across different timeframes and instruments by using relative volume rather than absolute thresholds

Customization Options

The strategy allows users to fine-tune its behavior:

- Volume Threshold: How unusual a volume spike must be to qualify

- Lookback Period: How far back to measure average volume

- Impact Decay Factor: How quickly older trades lose influence

- Visual Settings: Labels and line width customization

This sophisticated yet intuitive strategy provides traders with a window into institutional activity, helping identify potential trend changes before they become obvious in price action alone.