Moving Average TransformThe MAT is essentially a different kind of smoothed moving average. It is made to filter out data sets that deviate from the specified absolute threshold and the result becomes a smoothing function. The goal here, inspired by time series analysis within mathematical study, is to eliminate data anomalies and generate a more accurate trendline.

Functionality:

This script calculates a filtered average by:

Determining the mean of the entire data series.

Initializing sum and count variables.

Iterating through the data to filter values that deviate from the mean beyond the threshold.

Calculating a filtered mean based on the filtered data.

The filtered mean is then passed through a moving average function, where various types of moving averages like SMA, EMA, DEMA, TEMA, and ALMA can be applied. Some popular averages such as the HMA were omitted due to their heavy dependency on weighing specific data points.

Some information from "Time Series Analysis" regarding deviations

Definition of Anomaly: An anomaly or outlier is a data point that differs significantly from other observations in the dataset. It can be caused by various reasons such as measurement errors, data entry errors, or genuine extreme observations.

Impact on Mean: The mean (or average) of a dataset is calculated by summing all the values and dividing by the number of values. Since the mean is sensitive to extreme values, even a single outlier can significantly skew the mean.

Example: Consider a simple time series dataset: . The value "150" is an anomaly in this context. If we calculate the mean with this outlier, it is (10 + 12 + 11 + 9 + 150) / 5 = 38.4. However, if we exclude the outlier, the mean becomes (10 + 12 + 11 + 9) / 4 = 10.5. The presence of the outlier has substantially increased the mean.

Accuracy and Representativeness: While the mean calculated without outliers might be more "accurate" in the sense of being more representative of the central tendency of the bulk of the data, it's essential to note that anomalies might convey important information about the system being studied. Blindly removing or ignoring them might lead to overlooking significant events or phenomena.

Approaches to Handle Anomalies?

Detection and Removal

Robust Statistics

Transformation

Tìm kiếm tập lệnh với "电力行业+股票+11年涨幅"

ICT Silver Bullet [LuxAlgo]The ICT Silver Bullet indicator is inspired from the lectures of "The Inner Circle Trader" (ICT) and highlights the Silver Bullet (SB) window which is a specific 1-hour interval where a Fair Value Gap (FVG) pattern can be formed.

When a FVG is formed during the Silver Bullet window, Support & Resistance lines will be drawn at the end of the SB session.

There are 3 different Silver Bullet windows (New York local time):

The London Open Silver Bullet (3 AM — 4 AM ~ 03:00 — 04:00)

The AM Session Silver Bullet (10 AM — 11 AM ~ 10:00 — 11:00)

The PM Session Silver Bullet (2 PM — 3 PM ~ 14:00 — 15:00)

🔶 USAGE

The ICT Silver Bullet indicator aims to provide users a comprehensive display as similar as possible to how anyone would manually draw the concept on their charts.

It's important to use anything below the 15-minute timeframe to ensure proper setups can display. In this section, we are purely using the 3-minute timeframe.

In the image below, we can see a bullish setup whereas a FVG was successfully retested during the Silver Bullet session. This was then followed by a move upwards to liquidity as our target.

Alternatively, you can also see below a bearish setup utilizing the ICT Silver Bullet indicator outlined.

At this moment, the indicator has removed all other FVGs within the Silver Bullet session & has confirmed this FVG as the retested one.

There is also a support level marked below to be used as a liquidity target as per the ICT Silver Bullet concept suggests.

In the below chart we can see 4 separate consecutive examples of bullish & bearish setups on the 3-minute chart.

🔶 CONCEPTS

This technique can visualize potential support/resistance lines, which can be used as targets.

The script contains 2 main components:

• forming of a Fair Value Gap (FVG)

• drawing support/resistance (S/R) lines

🔹 Forming of FVG

1 basic principle: when a FVG at the end of the SB session is not retraced, it will be made invisible.

Dependable on the settings, different FVG's will be shown.

• 'All FVG': all FVG's are shown, regardless the trend

• 'Only FVG's in the same direction of trend': Only FVG's are shown that are similar to the trend at that moment (trend can be visualized by enabling ' Show ' -> ' Trend ')

-> only bearish FVG when the trend is bearish vs. bullish FVG when trend is bullish

• 'strict': Besides being similar to the trend, only FVG's are shown when the closing price at the end of the SB session is:

– below the top of the FVG box (bearish FVG)

– above bottom of the FVG box (bullish FVG)

• 'super-strict': Besides being similar to the trend, only FVG's are shown when the FVG box is NOT broken

in the opposite direction AND the closing price at the end of the SB session is:

– below bottom of the FVG box (bearish FVG)

– above the top of the FVG box (bullish FVG)

' Super-Strict ' mode resembles ICT lectures the most.

🔹 Drawing support/resistance lines

When the SB session has ended, the script draws potential support/resistance lines, again, dependable on the settings.

• Previous session (any): S/R lines are fetched between current and previous session.

For example, when current session is ' AM SB Session (10 AM — 11 AM) ', then previous session is

' London Open SB (3 AM — 4 AM) ', S/R lines between these 2 sessions alone will be included.

• Previous session (similar): S/R lines are fetched between current and previous - similar - session.

For example, when current session is ' London Open SB (3 AM — 4 AM)' , only S/R lines between

current session and previous ' London Open SB (3 AM — 4 AM) ' session are included.

When a new session starts, S/R lines will be removed, except when enabling ' Keep lines (only in strict mode) '

This is not possible in ' All FVG ' or ' Only FVG's in the same direction of trend ' mode, since the chart would be cluttered.

Note that in ' All FVG ' or ' Only FVG's in the same direction of trend ' mode, both, Support/Resistance lines will be shown,

while in Strict/Super-Strict mode:

• only Support lines will be shown if a bearish FVG appears

• only Resistance lines if a bullish FVG is shown

The lines will still be drawn the the end of the SB session, when a valid FVG appears,

but the S/R lines will remain visible and keep being updated until price reaches that line.

This publication contains a "Minimum Trade Framework (mTFW)", which represents the best-case expected price delivery, this is not your actual trade entry - exit range.

• 40 ticks for index futures or indices

• 15 pips for Forex pairs.

When on ' Strict/Super-Strict ' mode, only S/R lines will be shown which are:

• higher than the lowest FVG bottom + mTFW, in a bullish scenario

• lower than the highest FVG bottom - mTFW, in a bearish scenario

When on ' All FVG/Only FVG's in the same direction of trend ' mode, or on non-Forex/Futures/Indices symbols, S/R needs to be higher/lower than SB session high/low.

🔶 SETTINGS

(Check CONCEPTS for deeper insights and explanation)

🔹 Swing settings (left): Sets the length, which will set the lookback period/sensitivity of the Zigzag patterns (which directs the trend)

🔹 Silver Bullet Session; Show SB session: show lines and labels of SB session

Labels can be disabled separately in the ' Style ' section, color is set at the ' Inputs ' section.

🔹 FVG

– Mode

• All FVG

• Only FVG's in the same direction of trend

• Strict

• Super-Strict

– Colors

– Extend: extend till last bar of SB session

🔹 Targets – support/resistance lines

– Previous session (any): S/R lines fetched between current and previous SB session

– Previous session (similar): S/R lines fetched between current and previous similar SB session

– Colors

– Keep lines (only in strict mode)

🔹 Show

– MSS ~ Session: Show Market Structure Shift , only when this happens during a SB session

– Trend: Show trend (Zigzag, colored ~ trend)

Variety N-Tuple Moving Averages w/ Variety Stepping [Loxx]Variety N-Tuple Moving Averages w/ Variety Stepping is a moving average indicator that allows you to create 1- 30 tuple moving average types; i.e., Double-MA, Triple-MA, Quadruple-MA, Quintuple-MA, ... N-tuple-MA. This version contains 2 different moving average types. For example, using "50" as the depth will give you Quinquagintuple Moving Average. If you'd like to find the name of the moving average type you create with the depth input with this indicator, you can find a list of tuples here: Tuples extrapolated

Due to the coding required to adapt a moving average to fit into this indicator, additional moving average types will be added as they are created to fit into this unique use case. Since this is a work in process, there will be many future updates of this indicator. For now, you can choose from either EMA or RMA.

This indicator is also considered one of the top 10 forex indicators. See details here: forex-station.com

Additionally, this indicator is a computationally faster, more streamlined version of the following indicators with the addition of 6 stepping functions and 6 different bands/channels types.

STD-Stepped, Variety N-Tuple Moving Averages

STD-Stepped, Variety N-Tuple Moving Averages is the standard deviation stepped/filtered indicator of the following indicator

Last but not least, a big shoutout to @lejmer for his help in formulating a looping solution for this streamlined version. this indicator is speedy even at 50 orders deep. You can find his scripts here: www.tradingview.com

How this works

Step 1: Run factorial calculation on the depth value,

Step 2: Calculate weights of nested moving averages

factorial(depth) / (factorial(depth - k) * factorial(k); where depth is the depth and k is the weight position

Examples of coefficient outputs:

6 Depth: 6 15 20 15 6

7 Depth: 7 21 35 35 21 7

8 Depth: 8 28 56 70 56 28 8

9 Depth: 9 36 34 84 126 126 84 36 9

10 Depth: 10 45 120 210 252 210 120 45 10

11 Depth: 11 55 165 330 462 462 330 165 55 11

12 Depth: 12 66 220 495 792 924 792 495 220 66 12

13 Depth: 13 78 286 715 1287 1716 1716 1287 715 286 78 13

Step 3: Apply coefficient to each moving average

For QEMA, which is 5 depth EMA , the calculation is as follows

ema1 = ta. ema ( src , length)

ema2 = ta. ema (ema1, length)

ema3 = ta. ema (ema2, length)

ema4 = ta. ema (ema3, length)

ema5 = ta. ema (ema4, length)

In this new streamlined version, these MA calculations are packed into an array inside loop so Pine doesn't have to keep all possible series information in memory. This is handled with the following code:

temp = array.get(workarr, k + 1) + alpha * (array.get(workarr, k) - array.get(workarr, k + 1))

array.set(workarr, k + 1, temp)

After we pack the array, we apply the coefficients to derive the NTMA:

qema = 5 * ema1 - 10 * ema2 + 10 * ema3 - 5 * ema4 + ema5

Stepping calculations

First off, you can filter by both price and/or MA output. Both price and MA output can be filtered/stepped in their own way. You'll see two selectors in the input settings. Default is ATR ATR. Here's how stepping works in simple terms: if the price/MA output doesn't move by X deviations, then revert to the price/MA output one bar back.

ATR

The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.

Standard Deviation

Standard deviation is a statistic that measures the dispersion of a dataset relative to its mean and is calculated as the square root of the variance. The standard deviation is calculated as the square root of variance by determining each data point's deviation relative to the mean. If the data points are further from the mean, there is a higher deviation within the data set; thus, the more spread out the data, the higher the standard deviation.

Adaptive Deviation

By definition, the Standard Deviation (STD, also represented by the Greek letter sigma σ or the Latin letter s) is a measure that is used to quantify the amount of variation or dispersion of a set of data values. In technical analysis we usually use it to measure the level of current volatility .

Standard Deviation is based on Simple Moving Average calculation for mean value. This version of standard deviation uses the properties of EMA to calculate what can be called a new type of deviation, and since it is based on EMA , we can call it EMA deviation. And added to that, Perry Kaufman's efficiency ratio is used to make it adaptive (since all EMA type calculations are nearly perfect for adapting).

The difference when compared to standard is significant--not just because of EMA usage, but the efficiency ratio makes it a "bit more logical" in very volatile market conditions.

See how this compares to Standard Devaition here:

Adaptive Deviation

Median Absolute Deviation

The median absolute deviation is a measure of statistical dispersion. Moreover, the MAD is a robust statistic, being more resilient to outliers in a data set than the standard deviation. In the standard deviation, the distances from the mean are squared, so large deviations are weighted more heavily, and thus outliers can heavily influence it. In the MAD, the deviations of a small number of outliers are irrelevant.

Because the MAD is a more robust estimator of scale than the sample variance or standard deviation, it works better with distributions without a mean or variance, such as the Cauchy distribution.

For this indicator, I used a manual recreation of the quantile function in Pine Script. This is so users have a full inside view into how this is calculated.

Efficiency-Ratio Adaptive ATR

Average True Range (ATR) is widely used indicator in many occasions for technical analysis . It is calculated as the RMA of true range. This version adds a "twist": it uses Perry Kaufman's Efficiency Ratio to calculate adaptive true range

See how this compares to ATR here:

ER-Adaptive ATR

Mean Absolute Deviation

The mean absolute deviation (MAD) is a measure of variability that indicates the average distance between observations and their mean. MAD uses the original units of the data, which simplifies interpretation. Larger values signify that the data points spread out further from the average. Conversely, lower values correspond to data points bunching closer to it. The mean absolute deviation is also known as the mean deviation and average absolute deviation.

This definition of the mean absolute deviation sounds similar to the standard deviation (SD). While both measure variability, they have different calculations. In recent years, some proponents of MAD have suggested that it replace the SD as the primary measure because it is a simpler concept that better fits real life.

For Pine Coders, this is equivalent of using ta.dev()

Bands/Channels

See the information above for how bands/channels are calculated. After the one of the above deviations is calculated, the channels are calculated as output +/- deviation * multiplier

Signals

Green is uptrend, red is downtrend, yellow "L" signal is Long, fuchsia "S" signal is short.

Included:

Alerts

Loxx's Expanded Source Types

Bar coloring

Signals

6 bands/channels types

6 stepping types

Related indicators

3-Pole Super Smoother w/ EMA-Deviation-Corrected Stepping

STD-Stepped Fast Cosine Transform Moving Average

ATR-Stepped PDF MA

STD-Stepped, Variety N-Tuple Moving Averages [Loxx]STD-Stepped, Variety N-Tuple Moving Averages is the standard deviation stepped/filtered indicator of the following indicator

Variety N-Tuple Moving Averages is a moving average indicator that allows you to create 1- 30 tuple moving average types; i.e., Double-MA, Triple-MA, Quadruple-MA, Quintuple-MA, ... N-tuple-MA. This version contains 5 different moving average types including T3. A list of tuples can be found here if you'd like to name the order of the moving average by depth: Tuples extrapolated

STD-Stepped, You'll notice that this is a lot of code and could normally be packed into a single loop in order to extract the N-tuple MA, however due to Pine Script limitations and processing paradigm this is not possible ... yet.

If you choose the EMA option and select a depth of 2, this is the classic DEMA ; EMA with a depth of 3 is the classic TEMA , and so on and so forth this is to help you understand how this indicator works. This version of NTMA is restricted to a maximum depth of 30 or less. Normally this indicator would include 50 depths but I've cut this down to 30 to reduce indicator load time. In the future, I'll create an updated NTMA that allows for more depth levels.

This is considered one of the top ten indicators in forex. You can read more about it here: forex-station.com

How this works

Step 1: Run factorial calculation on the depth value,

Step 2: Calculate weights of nested moving averages

factorial(nemadepth) / (factorial(nemadepth - k) * factorial(k); where nemadepth is the depth and k is the weight position

Examples of coefficient outputs:

6 Depth: 6 15 20 15 6

7 Depth: 7 21 35 35 21 7

8 Depth: 8 28 56 70 56 28 8

9 Depth: 9 36 34 84 126 126 84 36 9

10 Depth: 10 45 120 210 252 210 120 45 10

11 Depth: 11 55 165 330 462 462 330 165 55 11

12 Depth: 12 66 220 495 792 924 792 495 220 66 12

13 Depth: 13 78 286 715 1287 1716 1716 1287 715 286 78 13

Step 3: Apply coefficient to each moving average

For QEMA, which is 5 depth EMA , the caculation is as follows

ema1 = ta. ema ( src , length)

ema2 = ta. ema (ema1, length)

ema3 = ta. ema (ema2, length)

ema4 = ta. ema (ema3, length)

ema5 = ta. ema (ema4, length)

qema = 5 * ema1 - 10 * ema2 + 10 * ema3 - 5 * ema4 + ema5

Included:

Alerts

Loxx's Expanded Source Types

Bar coloring

Signals

Standard deviation stepping

Variety N-Tuple Moving Averages [Loxx]Variety N-Tuple Moving Averages is a moving average indicator that allows you to create 1- 30 tuple moving average types; i.e., Double-MA, Triple-MA, Quadruple-MA, Quintuple-MA, ... N-tuple-MA. This version contains 5 different moving average types including T3. A list of tuples can be found here if you'd like to name the order of the moving average by depth: Tuples extrapolated

You'll notice that this is a lot of code and could normally be packed into a single loop in order to extract the N-tuple MA, however due to Pine Script limitations and processing paradigm this is not possible ... yet.

If you choose the EMA option and select a depth of 2, this is the classic DEMA; EMA with a depth of 3 is the classic TEMA, and so on and so forth this is to help you understand how this indicator works. This version of NTMA is restricted to a maximum depth of 30 or less. Normally this indicator would include 50 depths but I've cut this down to 30 to reduce indicator load time. In the future, I'll create an updated NTMA that allows for more depth levels.

This is considered one of the top ten indicators in forex. You can read more about it here: forex-station.com

How this works

Step 1: Run factorial calculation on the depth value,

Step 2: Calculate weights of nested moving averages

factorial(nemadepth) / (factorial(nemadepth - k) * factorial(k); where nemadepth is the depth and k is the weight position

Examples of coefficient outputs:

6 Depth: 6 15 20 15 6

7 Depth: 7 21 35 35 21 7

8 Depth: 8 28 56 70 56 28 8

9 Depth: 9 36 34 84 126 126 84 36 9

10 Depth: 10 45 120 210 252 210 120 45 10

11 Depth: 11 55 165 330 462 462 330 165 55 11

12 Depth: 12 66 220 495 792 924 792 495 220 66 12

13 Depth: 13 78 286 715 1287 1716 1716 1287 715 286 78 13

Step 3: Apply coefficient to each moving average

For QEMA, which is 5 depth EMA, the caculation is as follows

ema1 = ta.ema(src, length)

ema2 = ta.ema(ema1, length)

ema3 = ta.ema(ema2, length)

ema4 = ta.ema(ema3, length)

ema5 = ta.ema(ema4, length)

qema = 5 * ema1 - 10 * ema2 + 10 * ema3 - 5 * ema4 + ema5

Included:

Alerts

Loxx's Expanded Source Types

Bar coloring

Weighted percentile nearest rankYo, posting it for the whole internet, took the whole day to find / to design the actual working solution for weighted percentile 'nearest rank' algorithm, almost no reliable info online and a lot of library-style/textbook-style solutions that don't provide on real world production level.

The principle:

0) initial data

data = 22, 33, 11, 44, 55

weights = 5 , 3 , 2 , 1 , 4

array(s) size = 5

1) sort data array, apply the sorting pattern to the weights array, resulting:

data = 11, 22, 33, 44, 55

weights = 2 , 5 , 3 , 1 , 4

2) get weights cumsum and sum:

weights = 2, 5, 3 , 1 , 4

weights_cum = 2, 7, 10, 11, 15

weights_sum = 15

3) say we wanna find 50th percentile, get a threshold value:

n = 50

thres = weights_sum / 100 * n

7.5 = 15 / 100 * 50

4) iterate through weights_cum until you find a value that >= the threshold:

for i = 0 to size - 1

2 >= 7.5 ? nah

7 >= 7.5 ? nah

10 >= 7.5 ? aye

5) take the iteration index that resulted "aye", and find the data value with the same index, that's gonna be the resulting percentile.

i = 2

data = 33

This one is not an approximation, not an estimator, it's the actual weighted percentile nearest rank as it is.

I tested the thing extensively and it works perfectly.

For the skeptics, check lines 40, 41, 69 in the code, you can comment/uncomment dem to switch for unit (1) weights, resulting in the usual non-weighted percentile nearest rank that ideally matches the TV's built-in function.

Shoutout for @wallneradam for the sorting function mane

...

Live Long and Prosper

z_score_bgd

Z-score indicator for volatile currency pairs, showing STRONG BUY, BUY, SELL, STRONG SELL zones by shading the chart background.

---------------------------------

Background

---------------------------------

Based on mean reversion, a theory that after a swing in price the price will tend back to the mean. This offers some ability to predict future trends.

The formula for calculating a z-score is is z = (x-μ)/σ, where x is the pair price, μ is the mean for a population, and σ is the population standard deviation.

---------------------------------

Set up

---------------------------------

The user can define their own value for the "window" or population, which is the number of preceding days to evaluate. This value will affect the frequency and magnitude of trades, with higher "window" values reducing the frequency of reversions but increasing their magnitude.

Where the value for "window" is left at 99, the default values below will be applied in the background. Otherwise the user's selection will be in effect.

atombtc 18

avaxbtc 21

ethbtc 18

ftmbtc 11

maticbtc 11

solbtc 11

soleth 16

The default values above are intended for the daily time-frame.

---------------------------------

Interpreting the indicator

---------------------------------

Dark green -> large deviation below mean price (strong buy)

Green -> moderate deviation below mean price (buy)

Red -> moderate deviation below mean price (sell)

Dark red -> large deviation below mean price (strong sell)

Z-score is an imperfect indicator, as with all indiciators and trading decisions must be confirmed by multiple indicators and consider other factors.

SuperTrend OptimizerHello!

This indicator attempts to optimize Supertrend parameters. To achieve this, 102 parameter combinations are tested concurrently - the top three performers are listed in descending order.

Parameters,

Factor: Changes to this parameter shifts the tested factor range. For instance, increasing the factor measure from 3.00 to 3.01 (+0.01) will remove 3.00 from the tested range - this setting controls the lower threshold of the range. The upper threshold, in all instances, is the lower Factor threshold + 3.3 (i.e. 3.0(lower) - 6.3(upper), 4.0(lower) - 7.3(upper), 2.5(lower) - 5.8(upper))

ATR period: Changes to this parameter shifts the tested ATR period range. For instance, increasing the ATR measure from 10 to 11 (+1) will remove 10 from the tested range - this setting controls the lower threshold of the range. The upper threshold, in all instances, is the lower threshold + 2 (i.e. 10(lower) - 12(upper), 11(lower) - 13(upper), 9(lower), - 11(upper))

The Factor parameter is modifiable to any positive decimal number; the ATR parameter is modifiable to any positive integer. Changing either parameter shifts the tested parameter combination range. Both parameters can be changed in the settings, to which you control the lower threshold of the range. If, for instance, you were to change the Factor measurement from 3.0 to 4.1 (+1.1) the 4.0 Factor measurement, and all Factor measures less than 4.0, will be excluded from the performance test.

Consequently, a Supertrend test will be performed with a Factor of 4.1 and an ATR period of 10 (default). This test repeats at 0.1 Factor intervals and 1.0 ATR intervals.

Therefore, assume you modify the Factor lower threshold to 3.1 and the ATR lower threshold to 10. The indicator will test three Supertrend systems with a Factor of 3.1 and an ATR period of 10.. then 11.. 12, then three systems with a Factor of 3.2 and an ATR period of 10.. then 11.. 12... until (lower Factor threshold + 3.3) and (lower ATR threshold + 2) are tested... which in this example is... a Factor of 6.4 and an ATR period of 12.

The tested Factor range and ATR range are displayed in a bottom right table alongside the top performing parameter combinations.

Of course, you can change the the lower thresholds, which means you can test numerous Supertrend parameter combinations! However, no greater than 102 parameter combinations will be tested simultaneously; the best performing Supertrend parameters are plotted on the chart automatically.

I will be working on this indicator more tomorrow! Let me know if you have questions or anything you would like included!

(I of course added something fun in the script. Be sure to try it with bar replay!)

Bear & Bull Zone Signal StrategySince I love to mix and match, here is something fresh and that actually works on the breakout of Ethereum without losing your ass on lagging indicators.

It blends some of the nice parts of my previous scripts while moving to big boy pants with a twist on the Fibonacci retracement using SMA and EMA at multiple levels to do a sanity check.

Is it too good to be true? Nope, just what happens when a Solution Architect starts messing around with crypto and applies engineering and mathematics to the mix. You get a strategy that really doesn't have high profit losses when you tweak it just the right way.

What's the right tweak you ask?

1. Start with a 30 minute timeframe and set your window start date to the date the market began the bear or bull run

2. Make sure you can see your strategy performance window (not the graph one)

3. Set Stop Loss and Target Profit to 50%

4. Use your mouse wheel or up and down arrows and mess around with the RSI, go down one at a time but no lower than 7. Whichever value displayed the highest long or short gain is the one to pick.

5. Now select long or short only based on whichever one shows the highest gain.

6. Now go to K and D, leave K as 3 and check what happens when D is 4 or 5. Leave D at the value that gives you the highest gain.

7. Now go to EMA Fast and Slow Lengths. Leave Fast at 5 and check what happens when the Slow is moved up to 11 or 12, do the gains go up. If not, check what happens when Slow is moved down to 9, 8, or 7. Whichever gives you the highest gain, leave it there. Now go mess with the fast length, keep in mind that fast must always be less than slow. So check values down to 3 and up to 6. Same concept, mo money...leave it be.

8. Now go mess with the Target Profit, I start at 5, hit enter, then go to 7, hit enter, then 9...up by 2 until I get to 21 to make sure I don't hastily pick a low one and always keep in mind between which values the gain switched from high to low. For example, in this example I published at 11 it was $5k and at 13 it was $3700 for the gains. So after I got up to 21 I went back to 11 and started going up by 0.01 steps until the value dropped, which was at 11.19 so I set it at 11.18.

9. Now stop loss is trickier, you've maximized the gains, which means if you set the stop loss at a low value you will sacrifice gains. Typically by this point your loss is less than 10% with this script. So, my approach is to find the value where the stop loss doesn't change what I've tweaked already. In this example, I did the same start at 5 and go up by 2 and saw that when I went to 17 it stopped changing. So I started going back down by 0.5 and saw at 15.5 the gains went lower again. Now I started going back up in steps of 0.01 and at 15.98 it went back to the high gain I already tweaked for. I kept stop loss there and unleashed the strategy on ETH.

So far so good, no bad trades and it's been behaving pretty well.

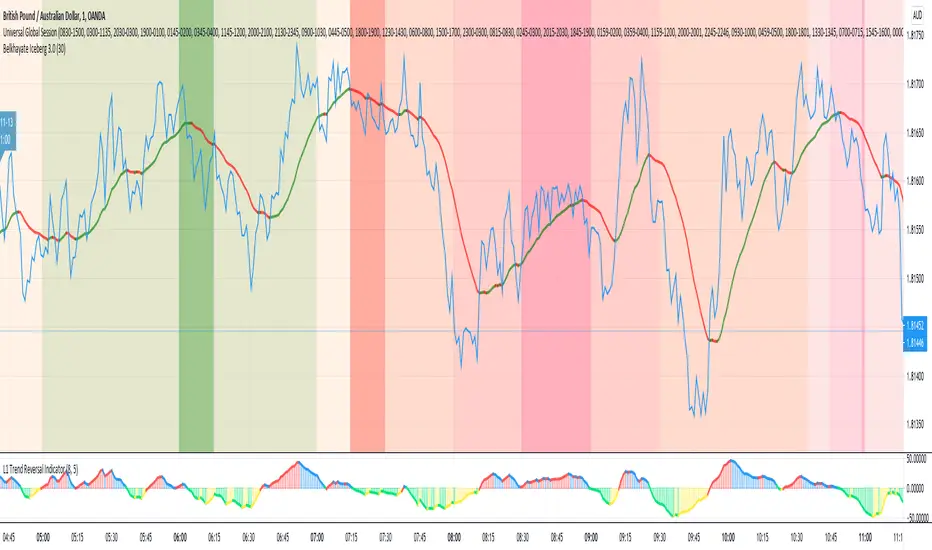

Universal Global SessionUniversal Global Session

This Script combines the world sessions of: Stocks, Forex, Bitcoin Kill Zones, strategic points, all configurable, in a single Script, to capitalize the opening and closing times of global exchanges as investment assets, becoming an Universal Global Session .

It is based on the great work of @oscarvs ( BITCOIN KILL ZONES v2 ) and the scripts of @ChrisMoody. Thank you Oscar and Chris for your excellent judgment and great work.

At the end of this writing you can find all the internet references of the extensive documentation that I present here. To maximize your benefits in the use of this Script, I recommend that you read the entire document to create an objective and practical criterion.

All the hours of the different exchanges are presented at GMT -6. In Market24hClock you can adjust it to your preferences.

After a deep investigation I have been able to show that the different world sessions reveal underlying investment cycles, where it is possible to find sustained changes in the nominal behavior of the trend before the passage from one session to another and in the natural overlaps between the sessions. These underlying movements generally occur 15 minutes before the start, close or overlap of the session, when the session properly starts and also 15 minutes after respectively. Therefore, this script is designed to highlight these particular trending behaviors. Try it, discover your own conclusions and let me know in the notes, thank you.

Foreign Exchange Market Hours

It is the schedule by which currency market participants can buy, sell, trade and speculate on currencies all over the world. It is open 24 hours a day during working days and closes on weekends, thanks to the fact that operations are carried out through a network of information systems, instead of physical exchanges that close at a certain time. It opens Monday morning at 8 am local time in Sydney —Australia— (which is equivalent to Sunday night at 7 pm, in New York City —United States—, according to Eastern Standard Time), and It closes at 5pm local time in New York City (which is equivalent to 6am Saturday morning in Sydney).

The Forex market is decentralized and driven by local sessions, where the hours of Forex trading are based on the opening range of each active country, becoming an efficient transfer mechanism for all participants. Four territories in particular stand out: Sydney, Tokyo, London and New York, where the highest volume of operations occurs when the sessions in London and New York overlap. Furthermore, Europe is complemented by major financial centers such as Paris, Frankfurt and Zurich. Each day of forex trading begins with the opening of Australia, then Asia, followed by Europe, and finally North America. As markets in one region close, another opens - or has already opened - and continues to trade in the currency market. The seven most traded currencies in the world are: the US dollar, the euro, the Japanese yen, the British pound, the Australian dollar, the Canadian dollar, and the New Zealand dollar.

Currencies are needed around the world for international trade, this means that operations are not dominated by a single exchange market, but rather involve a global network of brokers from around the world, such as banks, commercial companies, central banks, companies investment management, hedge funds, as well as retail forex brokers and global investors. Because this market operates in multiple time zones, it can be accessed at any time except during the weekend, therefore, there is continuously at least one open market and there are some hours of overlap between the closing of the market of one region and the opening of another. The international scope of currency trading means that there are always traders around the world making and satisfying demands for a particular currency.

The market involves a global network of exchanges and brokers from around the world, although time zones overlap, the generally accepted time zone for each region is as follows:

Sydney 5pm to 2am EST (10pm to 7am UTC)

London 3am to 12 noon EST (8pm to 5pm UTC)

New York 8am to 5pm EST (1pm to 10pm UTC)

Tokyo 7pm to 4am EST (12am to 9am UTC)

Trading Session

A financial asset trading session refers to a period of time that coincides with the daytime trading hours for a given location, it is a business day in the local financial market. This may vary according to the asset class and the country, therefore operators must know the hours of trading sessions for the securities and derivatives in which they are interested in trading. If investors can understand market hours and set proper targets, they will have a much greater chance of making a profit within a workable schedule.

Kill Zones

Kill zones are highly liquid events. Many different market participants often come together and perform around these events. The activity itself can be event-driven (margin calls or option exercise-related activity), portfolio management-driven (asset allocation rebalancing orders and closing buy-in), or institutionally driven (larger players needing liquidity to complete the size) or a combination of any of the three. This intense cross-current of activity at a very specific point in time often occurs near significant technical levels and the established trends emerging from these events often persist until the next Death Zone approaches or enters.

Kill Zones are evolving with time and the course of world history. Since the end of World War II, New York has slowly invaded London's place as the world center for commercial banking. So much so that during the latter part of the 20th century, New York was considered the new center of the financial universe. With the end of the cold war, that leadership appears to have shifted towards Europe and away from the United States. Furthermore, Japan has slowly lost its former dominance in the global economic landscape, while Beijing's has increased dramatically. Only time will tell how these death zones will evolve given the ever-changing political, economic, and socioeconomic influences of each region.

Financial Markets

New York

New York (NYSE Chicago, NASDAQ)

7:30 am - 2:00 pm

It is the second largest currency platform in the world, followed largely by foreign investors as it participates in 90% of all operations, where movements on the New York Stock Exchange (NYSE) can have an immediate effect (powerful) on the dollar, for example, when companies merge and acquisitions are finalized, the dollar can instantly gain or lose value.

A. Complementary Stock Exchanges

Brazil (BOVESPA - Brazilian Stock Exchange)

07:00 am - 02:55 pm

Canada (TSX - Toronto Stock Exchange)

07:30 am - 02:00 pm

New York (NYSE - New York Stock Exchange)

08:30 am - 03:00 pm

B. North American Trading Session

07:00 am - 03:00 pm

(from the beginning of the business day on NYSE and NASDAQ, until the end of the New York session)

New York, Chicago and Toronto (Canada) open the North American session. Characterized by the most aggressive trading within the markets, currency pairs show high volatility. As the US markets open, trading is still active in Europe, however trading volume generally decreases with the end of the European session and the overlap between the US and Europe.

C. Strategic Points

US main session starts in 1 hour

07:30 am

The euro tends to drop before the US session. The NYSE, CHX and TSX (Canada) trading sessions begin 1 hour after this strategic point. The North American session begins trading Forex at 07:00 am.

This constitutes the beginning of the overlap of the United States and the European market that spans from 07:00 am to 10:35 am, often called the best time to trade EUR / USD, it is the period of greatest liquidity for the main European currencies since it is where they have their widest daily ranges.

When New York opens at 07:00 am the most intense trading begins in both the US and European markets. The overlap of European and American trading sessions has 80% of the total average trading range for all currency pairs during US business hours and 70% of the total average trading range for all currency pairs during European business hours. The intersection of the US and European sessions are the most volatile overlapping hours of all.

Influential news and data for the USD are released between 07:30 am and 09:00 am and play the biggest role in the North American Session. These are the strategically most important moments of this activity period: 07:00 am, 08:00 am and 08:30 am.

The main session of operations in the United States and Canada begins

08:30 am

Start of main trading sessions in New York, Chicago and Toronto. The European session still overlaps the North American session and this is the time for large-scale unpredictable trading. The United States leads the market. It is difficult to interpret the news due to speculation. Trends develop very quickly and it is difficult to identify them, however trends (especially for the euro), which have developed during the overlap, often turn the other way when Europe exits the market.

Second hour of the US session and last hour of the European session

09:30 am

End of the European session

10:35 am

The trend of the euro will change rapidly after the end of the European session.

Last hour of the United States session

02:00 pm

Institutional clients and very large funds are very active during the first and last working hours of almost all stock exchanges, knowing this allows to better predict price movements in the opening and closing of large markets. Within the last trading hours of the secondary market session, a pullback can often be seen in the EUR / USD that continues until the opening of the Tokyo session. Generally it happens if there was an upward price movement before 04:00 pm - 05:00 pm.

End of the trade session in the United States

03:00 pm

D. Kill Zones

11:30 am - 1:30 pm

New York Kill Zone. The United States is still the world's largest economy, so by default, the New York opening carries a lot of weight and often comes with a huge injection of liquidity. In fact, most of the world's marketable assets are priced in US dollars, making political and economic activity within this region even more important. Because it is relatively late in the world's trading day, this Death Zone often sees violent price swings within its first hour, leading to the proven adage "never trust the first hour of trading in America. North.

---------------

London

London (LSE - London Stock Exchange)

02:00 am - 10:35 am

Britain dominates the currency markets around the world, and London is its main component. London, a central trading capital of the world, accounts for about 43% of world trade, many Forex trends often originate from London.

A. Complementary Stock Exchange

Dubai (DFM - Dubai Financial Market)

12:00 am - 03:50 am

Moscow (MOEX - Moscow Exchange)

12:30 am - 10:00 am

Germany (FWB - Frankfurt Stock Exchange)

01:00 am - 10:30 am

Afríca (JSE - Johannesburg Stock Exchange)

01:00 am - 09:00 am

Saudi Arabia (TADAWUL - Saudi Stock Exchange)

01:00 am - 06:00 am

Switzerland (SIX - Swiss Stock Exchange)

02:00 am - 10:30 am

B. European Trading Session

02:00 am - 11:00 am

(from the opening of the Frankfurt session to the close of the Order Book on the London Stock Exchange / Euronext)

It is a very liquid trading session, where trends are set that start during the first trading hours in Europe and generally continue until the beginning of the US session.

C. Middle East Trading Session

12:00 am - 06:00 am

(from the opening of the Dubai session to the end of the Riyadh session)

D. Strategic Points

European session begins

02:00 am

London, Frankfurt and Zurich Stock Exchange enter the market, overlap between Europe and Asia begins.

End of the Singapore and Asia sessions

03:00 am

The euro rises almost immediately or an hour after Singapore exits the market.

Middle East Oil Markets Completion Process

05:00 am

Operations are ending in the European-Asian market, at which time Dubai, Qatar and in another hour in Riyadh, which constitute the Middle East oil markets, are closing. Because oil trading is done in US dollars, and the region with the trading day coming to an end no longer needs the dollar, consequently, the euro tends to grow more frequently.

End of the Middle East trading session

06:00 am

E. Kill Zones

5:00 am - 7:00 am

London Kill Zone. Considered the center of the financial universe for more than 500 years, Europe still has a lot of influence in the banking world. Many older players use the European session to establish their positions. As such, the London Open often sees the most significant trend-setting activity on any trading day. In fact, it has been suggested that 80% of all weekly trends are set through the London Kill Zone on Tuesday.

F. Kill Zones (close)

2:00 pm - 4:00 pm

London Kill Zone (close).

---------------

Tokyo

Tokyo (JPX - Tokyo Stock Exchange)

06:00 pm - 12:00 am

It is the first Asian market to open, receiving most of the Asian trade, just ahead of Hong Kong and Singapore.

A. Complementary Stock Exchange

Singapore (SGX - Singapore Exchange)

07:00 pm - 03:00 am

Hong Kong (HKEx - Hong Kong Stock Exchange)

07:30 pm - 02:00 am

Shanghai (SSE - Shanghai Stock Exchange)

07:30 pm - 01:00 am

India (NSE - India National Stock Exchange)

09:45 pm - 04:00 am

B. Asian Trading Session

06:00 pm - 03:00 am

From the opening of the Tokyo session to the end of the Singapore session

The first major Asian market to open is Tokyo which has the largest market share and is the third largest Forex trading center in the world. Singapore opens in an hour, and then the Chinese markets: Shanghai and Hong Kong open 30 minutes later. With them, the trading volume increases and begins a large-scale operation in the Asia-Pacific region, offering more liquidity for the Asian-Pacific currencies and their crosses. When European countries open their doors, more liquidity will be offered to Asian and European crossings.

C. Strategic Points

Second hour of the Tokyo session

07:00 pm

This session also opens the Singapore market. The commercial dynamics grows in anticipation of the opening of the two largest Chinese markets in 30 minutes: Shanghai and Hong Kong, within these 30 minutes or just before the China session begins, the euro usually falls until the same moment of the opening of Shanghai and Hong Kong.

Second hour of the China session

08:30 pm

Hong Kong and Shanghai start trading and the euro usually grows for more than an hour. The EUR / USD pair mixes up as Asian exporters convert part of their earnings into both US dollars and euros.

Last hour of the Tokyo session

11:00 pm

End of the Tokyo session

12:00 am

If the euro has been actively declining up to this time, China will raise the euro after the Tokyo shutdown. Hong Kong, Shanghai and Singapore remain open and take matters into their own hands causing the growth of the euro. Asia is a huge commercial and industrial region with a large number of high-quality economic products and gigantic financial turnover, making the number of transactions on the stock exchanges huge during the Asian session. That is why traders, who entered the trade at the opening of the London session, should pay attention to their terminals when Asia exits the market.

End of the Shanghai session

01:00 am

The trade ends in Shanghai. This is the last trading hour of the Hong Kong session, during which market activity peaks.

D. Kill Zones

10:00 pm - 2:00 am

Asian Kill Zone. Considered the "Institutional" Zone, this zone represents both the launch pad for new trends as well as a recharge area for the post-American session. It is the beginning of a new day (or week) for the world and as such it makes sense that this zone often sets the tone for the remainder of the global business day. It is ideal to pay attention to the opening of Tokyo, Beijing and Sydney.

--------------

Sidney

Sydney (ASX - Australia Stock Exchange)

06:00 pm - 12:00 am

A. Complementary Stock Exchange

New Zealand (NZX - New Zealand Stock Exchange)

04:00 pm - 10:45 pm

It's where the global trading day officially begins. While it is the smallest of the megamarkets, it sees a lot of initial action when markets reopen Sunday afternoon as individual traders and financial institutions are trying to regroup after the long hiatus since Friday afternoon. On weekdays it constitutes the end of the current trading day where the change in the settlement date occurs.

B. Pacific Trading Session

04:00 pm - 12:00 am

(from the opening of the Wellington session to the end of the Sydney session)

Forex begins its business hours when Wellington (New Zealand Exchange) opens local time on Monday. Sydney (Australian Stock Exchange) opens in 2 hours. It is a session with a fairly low volatility, configuring itself as the calmest session of all. Strong movements appear when influential news is published and when the Pacific session overlaps the Asian Session.

C. Strategic Points

End of the Sydney session

12:00 am

---------------

Conclusions

The best time to trade is during overlaps in trading times between open markets. Overlaps equate to higher price ranges, creating greater opportunities.

Regarding press releases (news), it should be noted that these in the currency markets have the power to improve a normally slow trading period. When a major announcement is made regarding economic data, especially when it goes against the predicted forecast, the coin can lose or gain value in a matter of seconds. In general, the more economic growth a country produces, the more positive the economy is for international investors. Investment capital tends to flow to countries that are believed to have good growth prospects and subsequently good investment opportunities, leading to the strengthening of the country's exchange rate. Also, a country that has higher interest rates through its government bonds tends to attract investment capital as foreign investors seek high-yield opportunities. However, stable economic growth and attractive yields or interest rates are inextricably intertwined. It's important to take advantage of market overlaps and keep an eye out for press releases when setting up a trading schedule.

References:

www.investopedia.com

www.investopedia.com

www.investopedia.com

www.investopedia.com

market24hclock.com

market24hclock.com

Back to zero: Understanding seriestype: pine series basic example

time required: 10 minutes

level: medium (need to know the "array" data variable as a generic programming concept, basic Pine syntax)

tl;dr how variables and series work in Pine

Pine is an array/vector language. That's something that twists how it behaves, and how we have to think about it. A lot of misunderstandings come from forgetting this fact. This example tries to clear that concept.

First, you need to know what an array is, and how it works in a programmig language. Also, having javascript under your belt helps too. If you don't, google "javascript array basic tutorial" is your friend :)

So, in pine arrays are called "series". Every variable is an array with values for each candle in the chart. if we do:

myVar = true

this is not a constant. It is a series of values for each candle, { true, true,....., true }

In practice, the result is the same, but we can access each of the values in the series, like myVar{0}, myVar{7}, myVar{anyNumber}....

Again, it is not a constant, since you can access/modify the each value individually

so, lets show it:

plot (myVar, clolor = gray)

this plots an horizontal line of value 1 ( 1 is equal to true ) so it's all good.

On to a more usual series:

tipicalSeries = close > open ? true : false

plot(tipicalSeries, color= blue)

This gives the expected result, a tipical up and down line with values at 1 or 0. Naturally, "tipicalSeries" is an array, the "ups" and "downs" are all stored under the same variable, indexed by the candles.

In Pine, the ZERO position in the array is the last one, which corresponds to the last candle on the right. Say you have a chart with 12 candles. The close would be the closing value of what we intuitively think as first candle, the one on the left. then close ... and so on.... until close , the value of the "last" candle, the one on the right. It actually helps to start thinking of the positions backwards, counting down to zero, rocket launch style :)

And back to our series. The myVar will also be the same size, from myVar to myVar .

When we do some operation with them, something simple like

if ( myVar == tipicalSeries)

what is really happening is that internally, Pine is checking each of the indexes, as in myVar == tipicalSeries , myVar == tipicalSeries .... myVar == tipicalSeries

And we can store that stuff to check it. simply:

result = (myVar == tipicalSeries) ? true : false //yes, this is the same as tipicalSeries, but we're not in a boolean logic tut ;)

plot (result)

The reason we can plot the result is that it is an array, not a single value. The example indicator i provide shows a plot where the values are obtained from different places in the array, this line here:

mySeries3 = mySeries2 and mySeries1

this creates a series that is the result of the PREVIOUS values stored (the zero index is the one most at the right, or the "current" one), which here just causes a shift in the plotted line by one candle.

Go ahead, grab a copy of my code, try to change the indexes and see the results. Understanding this stuff is critical to go deeper into Pine :)

TRZigZagLibLibrary "TRZigZagLib"

method directionName(this)

Gets pivot direction as string

Namespace types: Pivot

Parameters:

this (Pivot) : Pivot instance

Returns: "HIGH" or "LOW"

method isHigh(this)

Checks if pivot is a high

Namespace types: Pivot

Parameters:

this (Pivot) : Pivot instance

Returns: true if pivot is a high

method isLow(this)

Checks if pivot is a low

Namespace types: Pivot

Parameters:

this (Pivot) : Pivot instance

Returns: true if pivot is a low

method newSettings(minLength, minBarSize, maxBarSize)

Creates default ZigZag settings

Namespace types: series int, simple int, input int, const int

Parameters:

minLength (int) : Minimum pivot length (default: 10)

minBarSize (int) : Minimum bars between pivots (default: 5)

maxBarSize (int) : Maximum bars to lookback (default: 300)

Returns: New ZigZagSettings instance

method setLineStyle(this, lineColor, lineWidth, lineStyle)

Sets line appearance

Namespace types: ZigZagSettings

Parameters:

this (ZigZagSettings) : Settings instance

lineColor (color)

lineWidth (int)

lineStyle (string)

Returns: Modified settings instance

method newZigZag(settings, depth)

Creates a new ZigZag instance

Namespace types: ZigZagSettings

Parameters:

settings (ZigZagSettings) : ZigZag settings

depth (int) : Depth value for this ZigZag

Returns: New ZigZag instance

method calculate(this)

Calculates ZigZag using LuxAlgo-style pivot detection

Namespace types: ZigZag

Parameters:

this (ZigZag) : ZigZag instance

method getLastPivots(this, count)

Gets the last N pivots

Namespace types: ZigZag

Parameters:

this (ZigZag) : ZigZag instance

count (int) : Number of pivots to get (default: 5)

Returns: Array of pivots

method getPivot(this, index)

Gets pivot at index

Namespace types: ZigZag

Parameters:

this (ZigZag) : ZigZag instance

index (int) : Index (0 = most recent)

Returns: Pivot or na

method truncate(this, maxBars)

Truncates old pivots beyond lookback window

Namespace types: ZigZag

Parameters:

this (ZigZag) : ZigZag instance

maxBars (int) : Maximum bars to keep

method newMultiZigZag(settings, minDepth, maxDepth, count)

Creates a new MultiZigZag manager

Namespace types: ZigZagSettings

Parameters:

settings (ZigZagSettings) : Base settings for all ZigZags

minDepth (int) : Minimum depth value

maxDepth (int) : Maximum depth value

count (int) : Number of ZigZag instances (max 11)

Returns: New MultiZigZag instance

method calculateAll(this)

Updates all ZigZag instances

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

method getZigZag(this, index)

Gets ZigZag at index

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

index (int) : Index (0 to count-1)

Returns: ZigZag instance or na

method getDepth(this, index)

Gets depth value at index

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

index (int) : Index (0 to count-1)

Returns: Depth value

method size(this)

Gets total number of ZigZag instances

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

Returns: Count of ZigZag instances

method truncateAll(this, maxBars)

Truncates all ZigZag instances

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

maxBars (int) : Maximum bars to keep

method distance(p1, p2)

Calculates distance between two pivots

Namespace types: Pivot

Parameters:

p1 (Pivot) : First pivot

p2 (Pivot) : Second pivot

Returns: Price distance (absolute)

method barSpan(p1, p2)

Calculates bar span between two pivots

Namespace types: Pivot

Parameters:

p1 (Pivot) : First pivot

p2 (Pivot) : Second pivot

Returns: Bar span (absolute)

method isAlternating(pivots)

Checks if pivots are alternating (high-low-high or low-high-low)

Namespace types: array

Parameters:

pivots (array) : Array of pivots

Returns: true if alternating pattern exists

Pivot

Pivot point in the chart

Fields:

d (series int) : Direction: 1=high, -1=low

x (series int) : Bar index

y (series float) : Price

confirmed (series bool) : Pivot confirmation flag

ZigZagSettings

ZigZag configuration settings

Fields:

minLength (series int) : Minimum pivot detection length

minBarSize (series int) : Minimum bars between pivots

maxBarSize (series int) : Maximum bars to lookback

lineColor (series color) : ZigZag line color

lineWidth (series int) : ZigZag line width

lineStyle (series string) : ZigZag line style

ZigZag

Single ZigZag instance

Fields:

settings (ZigZagSettings) : Configuration settings

pivots (array) : Array of pivot points (max 25 for patterns)

lastUpdateBar (series int) : Last bar index when updated

depth (series int) : Current depth value

MultiZigZag

Multi-depth ZigZag manager

Fields:

zigzags (array) : Array of ZigZag instances (max 11)

depthValues (array) : Array of depth values being used

currentBar (series int) : Current bar index being processed

SMC N-Gram Probability Matrix [PhenLabs]📊 SMC N-Gram Probability Matrix

Version: PineScript™ v6

📌 Description

The SMC N-Gram Probability Matrix applies computational linguistics methodology to Smart Money Concepts trading. By treating SMC patterns as a discrete “alphabet” and analyzing their sequential relationships through N-gram modeling, this indicator calculates the statistical probability of which pattern will appear next based on historical transitions.

Traditional SMC analysis is reactive—traders identify patterns after they form and then anticipate the next move. This indicator inverts that approach by building a transition probability matrix from up to 5,000 bars of pattern history, enabling traders to see which SMC formations most frequently follow their current market sequence.

The indicator detects and classifies 11 distinct SMC patterns including Fair Value Gaps, Order Blocks, Liquidity Sweeps, Break of Structure, and Change of Character in both bullish and bearish variants, then tracks how these patterns transition from one to another over time.

🚀 Points of Innovation

First indicator to apply N-gram sequence modeling from computational linguistics to SMC pattern analysis

Dynamic transition matrix rebuilds every 50 bars for adaptive probability calculations

Supports bigram (2), trigram (3), and quadgram (4) sequence lengths for varying analysis depth

Priority-based pattern classification ensures higher-significance patterns (CHoCH, BOS) take precedence

Configurable minimum occurrence threshold filters out statistically insignificant predictions

Real-time probability visualization with graphical confidence bars

🔧 Core Components

Pattern Alphabet System: 11 discrete SMC patterns encoded as integers for efficient matrix indexing and transition tracking

Swing Point Detection: Uses ta.pivothigh/pivotlow with configurable sensitivity for non-repainting structure identification

Transition Count Matrix: Flattened array storing occurrence counts for all possible pattern sequence transitions

Context Encoder: Converts N-gram pattern sequences into unique integer IDs for matrix lookup

Probability Calculator: Transforms raw transition counts into percentage probabilities for each possible next pattern

🔥 Key Features

Multi-Pattern SMC Detection: Simultaneously identifies FVGs, Order Blocks, Liquidity Sweeps, BOS, and CHoCH formations

Adjustable N-Gram Length: Choose between 2-4 pattern sequences to balance specificity against sample size

Flexible Lookback Range: Analyze anywhere from 100 to 5,000 historical bars for matrix construction

Pattern Toggle Controls: Enable or disable individual SMC pattern types to customize analysis focus

Probability Threshold Filtering: Set minimum occurrence requirements to ensure prediction reliability

Alert Integration: Built-in alert conditions trigger when high-probability predictions emerge

🎨 Visualization

Probability Table: Displays current pattern, recent sequence, sample count, and top N predicted patterns with percentage probabilities

Graphical Probability Bars: Visual bar representation (█░) showing relative probability strength at a glance

Chart Pattern Markers: Color-coded labels placed directly on price bars identifying detected SMC formations

Pattern Short Codes: Compact notation (F+, F-, O+, O-, L↑, L↓, B+, B-, C+, C-) for quick pattern identification

Customizable Table Position: Place probability display in any corner of your chart

📖 Usage Guidelines

N-Gram Configuration

N-Gram Length: Default 2, Range 2-4. Lower values provide more samples but less specificity. Higher values capture complex sequences but require more historical data.

Matrix Lookback Bars: Default 500, Range 100-5000. More bars increase statistical significance but may include outdated market behavior.

Min Occurrences for Prediction: Default 2, Range 1-10. Higher values filter noise but may reduce prediction availability.

SMC Detection Settings

Swing Detection Length: Default 5, Range 2-20. Controls pivot sensitivity for structure analysis.

FVG Minimum Size: Default 0.1%, Range 0.01-2.0%. Filters insignificant gaps.

Order Block Lookback: Default 10, Range 3-30. Bars to search for OB formations.

Liquidity Sweep Threshold: Default 0.3%, Range 0.05-1.0%. Minimum wick extension beyond swing points.

Display Settings

Show Probability Table: Toggle the probability matrix display on/off.

Show Top N Probabilities: Default 5, Range 3-10. Number of predicted patterns to display.

Show SMC Markers: Toggle on-chart pattern labels.

✅ Best Use Cases

Anticipating continuation or reversal patterns after liquidity sweeps

Identifying high-probability BOS/CHoCH sequences for trend trading

Filtering FVG and Order Block signals based on historical follow-through rates

Building confluence by comparing predicted patterns with other technical analysis

Studying how SMC patterns typically sequence on specific instruments or timeframes

⚠️ Limitations

Predictions are based solely on historical pattern frequency and do not account for fundamental factors

Low sample counts produce unreliable probabilities—always check the Samples display

Market regime changes can invalidate historical transition patterns

The indicator requires sufficient historical data to build meaningful probability matrices

Pattern detection uses standardized parameters that may not capture all institutional activity

💡 What Makes This Unique

Linguistic Modeling Applied to Markets: Treats SMC patterns like words in a language, analyzing how they “flow” together

Quantified Pattern Relationships: Transforms subjective SMC analysis into objective probability percentages

Adaptive Learning: Matrix rebuilds periodically to incorporate recent pattern behavior

Comprehensive SMC Coverage: Tracks all major Smart Money Concepts in a unified probability framework

🔬 How It Works

1. Pattern Detection Phase

Each bar is analyzed for SMC formations using configurable detection parameters

A priority hierarchy assigns the most significant pattern when multiple detections occur

2. Sequence Encoding Phase

Detected patterns are stored in a rolling history buffer of recent classifications

The current N-gram context is encoded into a unique integer identifier

3. Matrix Construction Phase

Historical pattern sequences are iterated to count transition occurrences

Each context-to-next-pattern transition increments the appropriate matrix cell

4. Probability Calculation Phase

Current context ID retrieves corresponding transition counts from the matrix

Raw counts are converted to percentages based on total context occurrences

5. Visualization Phase

Probabilities are sorted and the top N predictions are displayed in the table

Chart markers identify the current detected pattern for visual reference

💡 Note:

This indicator performs best when used as a confluence tool alongside traditional SMC analysis. The probability predictions highlight statistically common pattern sequences but should not be used as standalone trading signals. Always verify predictions against price action context, higher timeframe structure, and your overall trading plan. Monitor the sample count to ensure predictions are based on adequate historical data.

Borna's ZonesBorna's Zones marks two important time-based zones on the chart: the 08:00 zone and the 09:00 zone.

The 08:00 zone identifies initial liquidity. This zone sets the range where early market participants create significant activity.

The 09:00 zone serves as a reference for confirmation. After 09:00, the indicator helps you identify whether the 08:00 zone should be considered cleared.

Both zones are automatically extended until 11:00, providing clear visual references for potential market reactions.

No trading is recommended after 11:00, as the early morning zones lose relevance.

This indicator is useful for traders who focus on pre-market and early session liquidity, helping to visualize key levels where price may react.

BuLLzEyE_MNQ FVG/IFVG SystemFVG Boxes

These are the main trading zones. The indicator automatically detects Fair Value Gaps and draws boxes on your chart:

• GREEN boxes = Bullish FVG (potential buy zone)

• RED boxes = Bearish FVG (potential sell zone)

• YELLOW boxes = IFVG (Inverse FVG - filled gaps that now act as support/resistance)

• GRAY boxes = Mitigated FVG (gap has been filled)

• WHITE dashed line = 50% level (optimal entry point within the FVG)

Session Boxes

Session boxes show you the high/low range of each major trading session. This helps identify where liquidity sits:

• PURPLE = Asia Session (6:00 PM - 3:00 AM ET)

• BLUE = London Session (3:00 AM - 12:00 PM ET)

• ORANGE = New York Session (9:30 AM - 4:00 PM ET)

• TEAL = Sydney Session (5:00 PM - 2:00 AM ET)

• LIME GREEN = Kill Zone / London-NY Overlap (8:00 AM - 11:00 AM ET) - BEST TRADING TIME

Entry Signals

• GREEN triangle pointing UP = Long entry signal at a Bullish FVG (not 100% reliable)

• RED triangle pointing DOWN = Short entry signal at a Bearish FVG (not 100% reliable)

Liquidity Sweeps

• RED X with 'SWEEP' = Previous Day High (PDH) was swept

• GREEN X with 'SWEEP' = Previous Day Low (PDL) was swept

• Dotted lines = PDH (red) and PDL (green) levels

Information Tables

HTF Bias Table (Top Right): Shows whether the higher timeframe (default 15m) is bullish or bearish, the number of active FVGs, and whether you're in the trading session.

Risk Calculator Table (Bottom Right): Shows your risk amount and calculates how many contracts you can trade for different stop loss sizes (5pt, 10pt, 15pt).

How It Works

What is a Fair Value Gap?

A Fair Value Gap (FVG) is a 3-candle pattern where aggressive buying or selling creates a price void. Specifically, it's when the wick of the first candle doesn't overlap with the wick of the third candle, leaving a gap in between. Price tends to return to these gaps to 'rebalance' before continuing in the original direction.

What is an Inverse FVG?

When an FVG gets filled (price returns and closes through the gap), it becomes an Inverse FVG (IFVG). These zones flip their polarity - a filled Bullish FVG becomes resistance, and a filled Bearish FVG becomes support. The indicator automatically converts mitigated FVGs to yellow IFVG boxes.

The 50% Entry Level

The dashed white line in each FVG represents the 50% level (also called Consequent Encroachment). This is considered the optimal entry point - it's the middle of the imbalance where price is most likely to react.

Suggested Trading Strategy

1. Check HTF Bias (top right table) - only trade in that direction

2. Wait for a liquidity sweep (SWEEP label appears)

3. Look for an FVG to form AFTER the sweep

4. Enter when price returns to the 50% level (dashed line)

5. Place stop loss below/above the FVG (add 2 ticks buffer)

6. Take profit at 1:2 or 1:3 risk-to-reward ratio

Settings Explained

FVG Settings

• Min FVG Size: Minimum gap size in points to be considered valid (default: 2.0)

• Max FVG Age: How many bars until an FVG is removed from chart (default: 50)

• Show 50% Entry Level: Toggle the dashed entry line on/off

Session Settings

• Show Session Boxes: Toggle all session boxes on/off

• Max Sessions to Show: How many historical sessions to display (default: 5)

• Individual Session Toggles: Turn each session (Asia/London/NY/Sydney/Kill Zone) on or off

Risk Calculator Settings

• Account Size: Your trading account balance

• Risk Per Trade: Percentage of account to risk per trade (default: 0.5%)

• Tick Value/Size: Contract specifications for MNQ ($0.50 per tick, 0.25 point tick size)

Tips for Best Results

1. Trade during the Kill Zone (8:00-11:00 AM ET) for best volatility and liquidity

2. Always align trades with HTF bias - don't fight the trend

3. Wait for liquidity sweeps before entering - this confirms smart money activity

4. Use the 50% level for entries - it offers the best risk-to-reward

5. Watch for IFVG zones as additional confluence for entries

6. Use the risk calculator to size positions properly - never risk more than you can afford

7. Session boxes help identify where stops are clustered - sweeps of these levels often precede reversals

Available Alerts

• New FVG Formed (Bullish or Bearish)

• Price Touching 50% Entry Level

• FVG Mitigated (gap filled)

• Long Entry Signal

• Short Entry Signal

• PDH/PDL Liquidity Sweep

─────────────────────────────────────

Created by BullyTrading

Designed for MNQ Prop Firm Trading

Self-Organized Criticality - Avalanche DistributionHere's all you need to know: This indicator applies Self-Organized Criticality (SOC) theory to financial markets, measuring the power-law exponent (alpha) of price drawdown distributions. It identifies whether markets are in stable Gaussian regimes or critical states where large cascading moves become more probable.

Self-Organized Criticality

SOC theory, introduced by Per Bak, Tang, and Wiesenfeld (1987), describes how complex systems naturally evolve toward critical (fragile) states. An example is a sand pile: adding grains creates avalanches whose sizes follow a power-law distribution rather than a normal distribution.

Financial markets exhibit similar behavior. Price movements aren't purely random walks—they display:

Fat-tailed distributions (more extreme events than Gaussian models predict)

Scale invariance (no characteristic avalanche size)

Intermittent dynamics (periods of calm punctuated by large cascades)

Power-Law Distributions

When a system is in a critical state, the probability of an avalanche of size s follows:

P(s) ∝ s^(-α)

Where:

α (alpha) is the power-law exponent

Higher α → distribution resembles Gaussian (large events rare)

Lower α → heavy tails dominate (large events common)

This indicator estimates α from the empirical distribution of price drawdowns.

Mathematical Method

1. Avalanche Detection

The indicator identifies local price peaks (highest point in a lookback window), then measures the percentage drawdown to the next trough. A dynamic ATR-based threshold filters out noise—small drops in calm markets count, but the bar rises in volatile periods.

2. Logarithmic Binning

Avalanche sizes are sorted into logarithmically-spaced bins (e.g., 1-2%, 2-4%, 4-8%) rather than linear bins. This captures power-law behavior across multiple scales - a 2% drop and 20% crash both matter. The indicator creates 12 adaptive bins spanning from your smallest to largest observed avalanche.

3. Bin-to-Bin Ratio Estimation

For each pair of adjacent bins, we calculate:

α ≈ log(N₁/N₂) / log(s₂/s₁)

Where N₁ and N₂ are avalanche counts, s₁ and s₂ are bin sizes.

Example: If 2% drops happen 4× more often than 4% drops, then α ≈ log(4)/log(2) ≈ 2.0.

We get 8-11 independent estimates and average them. This is more robust than fitting one line through all points—outliers can't dominate.

4. Rolling Window Analysis

Alpha recalculates using only recent avalanches (default: last 500 bars). Old data drops out as new avalanches occur, so the indicator tracks regime shifts in real-time.

Regime Classification

🟢 Gaussian α ≥ 2.8 Normal distribution behavior; large moves are rare outliers

🟡 Transitional 1.8 ≤ α < 2.8 Moderate fat tails; system approaching criticality

🟠 Critical 1.0 ≤ α < 1.8 Heavy tails; large avalanches increasingly common

🔴 Super-Critical α < 1.0 Extreme tail risk; system prone to cascading failures

What Alpha Tells You

Declining alpha → Market moving toward criticality; tail risk increasing

Rising alpha → Market stabilizing; returns to normal distribution

Persistent low alpha → Sustained fragility; heightened crash probability

Supporting Metrics

Heavy Tail %: Concentration of total drawdown in largest 10% of events

Populated Bins: Data coverage quality (11-12 out of 12 is ideal)

Avalanche Count: Sample size for statistical reliability

Limitations

This is a distributional measure, not a timing indicator. Low alpha indicates increased systemic risk but doesn't predict when a cascade will occur. Only that the probability distribution has shifted toward larger events.

How This Differs from the Per Bak Fragility Index

The SOC Avalanche Distribution calculates the power-law exponent (alpha) directly from price drawdown distributions - a pure mathematical analysis requiring only price data. The Per Bak Fragility Index aggregates external stress indicators (VIX, SKEW, credit spreads, put/call ratios) into a weighted composite score.

Technical Notes

Default settings optimized for daily and weekly timeframes on major indices

Requires minimum 200 bars of history for stable estimates

ATR-based dynamic sizing prevents scale-dependent bias

Alerts available for regime transitions and super-critical entry

References

Bak, P., Tang, C., & Wiesenfeld, K. (1987). Self-organized criticality: An explanation of the 1/f noise. Physical Review Letters.

Sornette, D. (2003). Why Stock Markets Crash: Critical Events in Complex Financial Systems. Princeton University Press.

Relative Strength Heatmap [BackQuant]Relative Strength Heatmap

A multi-horizon RSI matrix that compresses 20 different lookbacks into a single panel, turning raw momentum into a visual “pressure gauge” for overbought and oversold clustering, trend exhaustion, and breadth of participation across time horizons.

What this is

This indicator builds a strip-style heatmap of 20 RSIs, each with a different length, and stacks them vertically as colored tiles in a single pane. Every tile is colored by its RSI value using your chosen palette, so you can see at a glance:

How many “fast” versus “slow” RSIs are overbought or oversold.

Whether momentum is concentrated in the short lookbacks or spread across the whole curve.

When momentum extremes cluster, signalling strong market pressure or exhaustion.

On top of the tiles, the script plots two simple breadth lines:

A white line that counts how many RSIs are above 70 (overbought cluster).

A black line that counts how many RSIs are below 30 (oversold cluster).

This turns a single symbol’s RSI ladder into a compact “market pressure gauge” that shows not only whether RSI is overbought or oversold, but how many different horizons agree at the same time.

Core idea

A single RSI looks at one length and one timescale. Markets, however, are driven by flows that operate on multiple horizons at once. By computing RSI over a ladder of lengths, you approximate a “term structure” of strength:

Short lengths react to immediate swings and very recent impulses.

Medium lengths reflect swing behaviour and local trends.

Long lengths reflect structural bias and higher timeframe regime.

When many lengths agree, for example 10 or more RSIs all above 70, it suggests broad participation and strong directional pressure. When only a few fast lengths stretch to extremes while longer ones stay neutral, the move is more fragile and more likely to mean-revert.

This script makes that structure visible as a heatmap instead of forcing you to run many separate RSI panes.

How it works

1) Generating RSI lengths

You control three parameters in the calculation settings:

RS Period – the base RSI length used for the shortest strip.

RSI Step – the amount added to each successive RSI length.

RSI Multiplier – a global scaling factor applied after the step.

Each of the 20 RSIs uses:

RSI length = round((base_length + step × index) × multiplier) , where the index goes from 0 to 19.

That means:

RSI 1 uses (len + step × 0) × mult.

RSI 2 uses (len + step × 1) × mult.

…