Sigmoid Risk AllocatorThe Sigmoid Risk Allocator is a dynamic position sizing indicator that tells you how much of your capital to allocate based on current market conditions. Unlike simple "risk-on/risk-off" signals, this indicator gives you smooth, gradual transitions based on a sigmoid function.

Why a Sigmoid Curve?

Most position sizing approaches use fixed thresholds: "If drawdown > 20%, buy. Otherwise, don't." This creates all-or-nothing decisions.

Using the sigmoid (S-curve) makes this decision different. It creates a smooth transition where:

Small drawdowns → Stay near your baseline allocation

Moderate drawdowns → Gradually increase exposure

Large drawdowns → Approach maximum allocation

The sigmoid curve naturally "saturates" at the extremes, preventing you from going all-in too early or panicking out too fast. This is very useful to meek traders psychology and risk management in check.

What's a Sigmoid Function?

The sigmoid function is a mathematical S-curve defined as:

σ(x) = 1 / (1 + e^(-x))

This formula takes any input value and smoothly maps it to a number between 0 and 1. The curve has three key properties that make it ideal for position sizing in investing:

Smooth transitions: No sudden jumps. Allocation changes gradually.

Saturation at extremes: The curve flattens near 0 and 1, preventing overreaction and overexposure.

Sensitive in the middle: Most of the action happens around the midpoint.

To convert this into an allocation percentage, the indicator uses:

Allocation = α_min + (α_max - α_min) × σ(k × (Risk - Midpoint))

Where:

- `α_min` = Your minimum allocation (default 50%)

- `α_max` = Your maximum allocation (default 100%)

- `Risk` = Current risk metric (drawdown %, volatility, or Kelly %)

- `Midpoint` = The risk level where allocation sits halfway between min and max (default 15%)

- `k` = Steepness—how quickly allocation changes around the midpoint

Example : With defaults, if drawdown hits 15% (the midpoint), your allocation will be 75% (halfway between 50% and 100%). As the drawdown increases beyond 15%, the allocation curves toward 100%. As it decreases toward 0%, allocation curves toward 50%.

Cool, isn't it?

Asymmetric Response: Fast In, Slow Out

The indicator uses different steepness values for scaling in vs. scaling out. This is great to increase trend following. This is something I'm proud of too in this indicator.

k_increase = 30 (steep curve): When drawdowns appear, allocation ramps up quickly to catch the opportunity

k_decrease = 5 (slower curve): When conditions normalize, allocation decreases slowly to avoid selling the rebound

This asymmetry reflects how markets behave—drawdowns often overshoot fundamentals (rewarding quick entries), while recoveries tend to be more orderly (rewarding patience on exits).

Three Risk Metrics

You can choose what drives your allocation:

Drawdown (Default)

Volatility - Scales your position inversely to current market volatility.

Kelly Criterion - Automatically calculates optimal position size. The indicator applies a conservative "half Kelly" by default.

Use Cases

Position sizing for swing trading or trend following

Risk management overlay for any existing strategy

Drawdown-based DCA (dollar cost averaging) decisions

Volatility-adjusted exposure management

Feel free to provide feedback and share your thoughts!

- Henrique Centieiro

Statistical

Sigmoid Allocation Indicator & DashboardTL;DR This sigmoid-based allocation indicator tells you percentage of your portfolio to invest based on how much the market has dropped.

Market at all-time high? → Stay defensive, invest less (e.g., 30%)

Market crashed hard? → Get aggressive, invest more (e.g., 100%)

The "sigmoid" part just means the transition between these two extremes follows a smooth S-shaped curve.

Description

This indicator is a sigmoid-based allocation system that dynamically adjusts a portfolio exposure based on market drawdown.

It compares multiple steepness curves (K values) to find your optimal risk profile for leveraged ETF strategies, but it can also be used to scale in-out from stocks, crypto and to understand whether to use leverage or not.

The Sigmoid Allocation Dashboard helps you to dynamically adjust a portfolio allocation based on how much a market has dropped from its all-time high.

I've implemented it using a sigmoid (S-curve) function, that dynamically calculates the optimal allocation percentages. Depending on the market conditions, the S curves transition between defensive and aggressive allocations.

The Math Behind It (if you are a geek like me)

This indicator uses the sigmoid function to create smooth S-curve transitions:

α(D) = α_min + (α_max - α_min) × σ(k × (D - D_mid))

Where:

σ(x) = 1 / (1 + e^(-x)) ← Standard sigmoid function

You can also check it here:

// Sigmoid function: σ(x) = 1 / (1 + e^(-x))

sigmoid(float x) =>

1.0 / (1.0 + math.exp(-x))

// Alpha calculation: α(D) = α_min + (α_max - α_min) × σ(k × (D - D_mid))

calcAlpha(float drawdown, float k, float a_min, float a_max, float d_midpoint) =>

sig_input = k * (drawdown - d_midpoint) / 100.0

a_min + (a_max - a_min) * sigmoid(sig_input)

User parameters (you can tweak this):

Allocation Min (%): Your baseline allocation when markets are at ATH (default: 30%)

Allocation Max (%): Your maximum allocation during deep drawdowns (default: 100%)

D_mid (%): The drawdown level where you want to be at the midpoint (default: 25%)

Why do I like sigmoid and not a linear line?

Unlike linear models, the sigmoid creates "floors" and "ceilings" for your allocation. It transitions smoothly, no sudden jumps, and you never exceed your defined min/max bounds.

Understand the K Values (Steepness)

The K parameter controls how quickly your allocation shifts from defensive to aggressive.

Lower K (for example K=5) will give you a gradual transition, but at 0% drawdown you are already at a 46% allocation.

A higher like (like K=40) will give you a sharp transition, but at 0% drawdown you are close to the minimum allocation. On the other hand, a higher K will give close to 100% allocation when the markets are at new lows.

The example below illustrates this well, then the S&P 500 reached new lows in October 2022:

Different K values will affect the sigmoid curves (and you allocations differently). The chart below illustrates well how K affects the sigmoid curves:

Read the Dashboard

The main dashboard shows:

Current drawdown from ATH

Allocation % for each K value

Suggested action (Defensive → MAX LONG)

Use the Reference Chart

The static reference panel shows what your allocation would be at various drawdown levels (0%, 10%, 20%, 30%, 40%, 50%), helping you plan ahead.

Identify Zones

The color-coded chart background shows:

- 🟢 Green Zone: Aggressive positioning - "Buy the Dip"

- 🟡 Yellow Zone: Transition zone - Scaling in/out

- 🔴 Red Zone: Defensive positioning - Protect ya gains

Use Cases

Use case 1: Leveraged ETF Portfolio Management (this is my main use case)

When holding leveraged ETFs like TQQQ or UPRO, volatility makes it important to:

- Reduce exposure near all-time highs (when crashes hurt most)

- Increase exposure during drawdowns (when recovery potential is highest)

Example Strategy:

- At ATH: Hold 30% TQQQ, 70% cash/bonds or other uncorrelated assets

- At 25% drawdown: Hold 65% TQQQ, 35% cash/bonds

- At 40%+ drawdown: Hold 100% TQQQ

Use case 2: Diversified Leveraged Portfolio

Compare different K values for different assets:

- Use K = 10 for broad market (QQQ/SPY exposure via TQQQ/UPRO)

- Use K = 25 for sector bets (TECL, SOXL, TMF) that you want to scale into faster

Use case 3: Systematic Rebalancing Signals

Use the alerts to trigger rebalancing:

- Alert when K3 allocation crosses above 90% (time to add)

- Alert when drawdown exceeds your D_mid threshold

- Alert when market returns to within 5% of ATH

Tips for Best Results

It works best in longer time frames

Adjust the ATR lookback window

Match your risk tolerance level

I use this for index investing and stocks and haven't tried with crypto

Thanks for using the indicator and let me know if you have any feedback :)

- Henrique Centieiro

Monthly Seasonality AnalyzerThis indicator analyzes historical performance/seasonality of a chosen month, from date of inception to present. Users can choose any calendar month via dropdown menu.

For each historical month selected, it will calculate the monthly percentage gain/loss, range(volatility), and average gain/loss percentage, average range percentage across all recorded years. Positive returns are colored green and negative returns are red. Also, calculates if the selected month was bullish(open>close) or bearish.

When current chart month matches the selected month, it shows the in-progress range as well.

Data is collected from 1930 to present. Results are shown in vertical and horizontal tables. If the vertical table exceeds a 36 years, the script automatically switches to horizontal table to display all the data, with option to change table position.

Overall this tool is valuable for seasonality research, such as Santa Rally, May Go Away and swing trading/ position trading to capture the monthly PO3 range.

Most seasonality indicators show all 12 months at once or use daily bars. This one zooms in deeply on one month only, providing detailed per-year breakdowns, accurate completed-month stats, and a practical live range display.

The script uses arrays to store years, gains, and ranges. Uses table.new(), table.cell(), table.merge_cells() for easily readable result display. Code handles the current in-progress month separately (shows live range without including it in historical averages).

**Script will not run on any timeframe other than monthly and displays error otherwise. Script is best used on spot and not futures.

CUSUM Volatility BreakoutCUSUM Volatility Breakout A statistical trend-detection and volatility-breakout indicator that identifies subtle momentum shifts earlier than traditional tools.

OVERVIEW

The CUSUM control chart is a statistical tool designed to detect small, gradual shifts from a target value. In trading, it helps identify the early stages of a trend, giving traders a heads-up before momentum becomes obvious on standard price charts. By spotting these subtle movements, the CUSUM Volatility Breakout indicator (CUSUM VB) can highlight potential breakout opportunities earlier than traditional indicators. In other words, a statistical trend detection & breakout indicator.

Copyright © 2025 CoinOperator

HOW IT WORKS

CUSUM VB uses a combination of differenced price series, volume normalization, and dynamic control limits:

CUSUM Principle: Tracks cumulative deviations of price from a zero reference. Signals occur when cumulative deviations exceed a control limit shown on the chart and clears any enabled filters.

Adaptive Volatility: H adjusts automatically based on short- vs long-term ATR ratios, allowing faster detection during volatile periods and reduced false signals in calm markets.

Volume Weighting (optional): Amplifies price CUSUM values during high-volume bars to prioritize market participation strength.

ATR Confirmation (optional): Ensures breakouts are accompanied by expanded volatility.

Bollinger Band Squeeze Integration (optional): Confirms trend breakouts by detecting volatility contraction and release shown on the chart as triangles.

Signals:

Arrows on the price chart mark the bars where trades are actually filled, based on conditions detected on the prior signal bar.

Long Entry: Confirmed positive CUSUM breach (price & volume) with BB breakout (signal bar).

Short Entry: Confirmed negative CUSUM breach (price & volume) with BB breakout (signal bar).

Exit Signals: Triggered automatically by opposite-side signals.

Alerts, when created, fire on the bars where fills occur.

CHART COMPONENTS

CUSUM Upper Price (CU Price) and CUSUM Lower Price (CL Price) are green/red circles for confirmed signals.

● Rapid upward accumulation of CU Price indicates a developing bullish trend.

● Rapid downward accumulation of CL Price indicates a developing bearish trend.

Decision/Control limits (UCL/LCL, red)

Zero line (reference for the differenced price series baseline)

Optional BB triangles and volume CUSUM

SETUP AND CONFIGURATION

Differenced Price Series

Differenced Price Length and Lag

Increase differencing lag or window length → Increases variance of residuals → Wider control limits (UCL/LCL) → Slower to trigger.

Decrease lag or window → Tighter limits, more responsive to short-term regime shifts.

CUSUM Parameters

Volume-Weighted CUSUM

NOTE : Uses price length if 'Confirm Price with Volume' is disabled, otherwise will use volume length.

Amplifies CUSUM price responses during high-volume bars and reduces them during low-volume bars. This links trend detection to market participation strength.

Volume-Weighted CUSUM doesn’t replace price confirmation with volume; it modulates it by volume intensity, amplifying price signals when participation is strong and suppressing them when weak.

Recommended when analyzing assets with consistent volume patterns (e.g., stocks, major futures).

Disable for low-liquidity or irregular-volume instruments (e.g., crypto pairs, small-cap stocks).

ATR Confirmation

Enable this feature to confirm CUSUM signals only when price deviations are accompanied by higher-than-normal volatility. The indicator compares current ATR to a smoothed ATR to detect volatility expansion. This helps distinguish true breakouts from low-volatility noise and reduces false signals during quiet periods.

Adjust the ATR lookback length, smoothing length, and expansion factor to control sensitivity. Rule of thumb:

ATR Length ≈ 0.5 × differenced price length to 1.5 × differenced price length gives balanced sensitivity.

ATR Smoothing 5–10 bars.

ATR Expansion 5% to 50%.

CUSUM Input Mode

Select how CUSUM processes differenced price and log-normalized volume — either directly (Txfrm Data) or as deviations from a short-term EMA baseline (Residuals):

Txfrm Data = transformed input: differenced price & log-normalized volume as input for CUSUM (larger swings, more frequent control limit breaches)

Residuals = deviation from short-term EMA baseline (smaller swings, fewer control limit breaches, but higher signal quality).

Residual EMA Length: Defines how quickly the residual baseline adapts to recent differenced price moves. Shorter = more reactive; longer = smoother baseline. Keep EMA length moderate; over-smoothing can distort timing.

Control Sensitivity (K)

Increase K → Less sensitive → CUSUM accumulates slower → Fewer signals, captures only major trends.

Decrease K → More sensitive → CUSUM accumulates faster → More signals, captures minor swings too.

Reset Mode : Method of resetting CUSUM values.

Immediate Reset: Reset both immediately after any signal breach. Traditional SPC.

Opposite-Side Reset: Reset only the opposite side when a valid signal fires. Best for ongoing trend tracking.

Decay Reset: Gradually reduce CUSUM values toward zero with a decay factor each bar. Maintains trend memory but allows slow “forgetting.”

Threshold Reset: Reset only if CUSUM returns below a small threshold (10 % of H). Filters noise without full wipe.

No Reset / Continuous: Never reset; instead track running totals. Long-term cumulative bias measurement.

Conflict Handling : Method of handling conflicting signals.

Ignore Both: Discards both when overlap occurs.

Prioritize Latest: Chooses the direction implied by the most recent close.

Prioritize Stronger: Compares absolute magnitudes of CU Price vs CL Price.

Average Resolve: Looks at the difference; small overlap → ignore, otherwise pick direction by sign.

Sequential Confirm: Requires N consecutive same-direction signals before confirmation.

Volume Parameters (Optional)

Amplification Factor

Adjusts volume sensitivity and effectively rescales the log series of volume to a comparable magnitude with price changes.

Since price and volume are normalized in a compatible way, the amplification factor is used instead of independent K and H values for volume.

Bollinger Bands (Optional)

Lookback Synchronization

BB Lookback (for CUSUM): Number of bars that define a window for the BB signal to look back for the CUSUM signal.

CUSUM Lookback (for BB): Number of bars that define a window for the CUSUM signal to look back for the BB signal.

Both can be enabled for stricter alignment.

Relationship Between K, H, ARL₀ and ARL₁

H (max) is usually the only H you need to adjust. With everything else being constant, increasing either K or H (max) generally increases both ARL₀ and ARL₁ : higher thresholds reduce false alarms but slow detection, and lower thresholds do the opposite.

Increase Min Target ARL ratio →

ARL₀ increases (safer, fewer false alarms)

ARL₁ decreases or stays small (faster detection)

Control limits slightly expand to achieve separation

Strategy becomes more selective and stable

Decrease Min Target ARL ratio →

ARL₀ decreases (more false alarms tolerated)

ARL₁ increases (slower detection tolerated)

Control limits tighten

Strategy becomes more sensitive but lower quality

The ARL Ratio of ARL₀ / ARL₁ is typically between 3 and 8. This implies you want your ARL₀ (false-alarm interval) ≈ 'Min Target ARL ratio' × differenced price length window.

Example:

"Min Target ARL ratio = 4.0"

⇒ implies you want your ARL₀ (false-alarm interval) ≈ 4 × differenced price length.

Assume price length = 50 (typical differencing window).

ARL ratio = 4.0 → target ARL = 4 × 50 = 200 bars.

● On a 6-hour chart (≈4 bars/day) → ~50 days between expected false alarms (on average).

● On a daily chart → ~200 trading days between false alarms (very conservative).

ARL ratio = 8.0 → target ARL = 400 bars → twice as infrequent signals vs ratio=4.

ARL ratio = 2.0 → target ARL = 100 bars → about half the inter-signal interval.

Another way to think about it: probability of a false alarm on any bar ≈ 1 / target ARL. If you want ~1% of bars producing alarms, target ARL ≈ 100.

QUICK START

Start with the defaults.

Set price series → length/order/lag

Configure CUSUM thresholds → K, H min/max

1. Adjust the price differencing lag/window.

2. Verify that it captures real price inflection points without overreacting to bar noise.

Enable optional filters → Volume, ATR, BB

The optional Bollinger Bands squeeze usually works best if used with CUSUM Input Mode = Txfrm Data.

Monitor CUSUM chart → CU Price, CL Price, thresholds, zero line

Act on signals → data window / chart triangles

Adjust sensitivity → H (max), K, lengths

Monitor ARL ratio and CUSUM behavior for fine-tuning

Note : When you’ve finalized the length, lag, and order of the Price Difference, as well as the Ln(Vol) Series of “Confirm Price with Volume” if enabled, then pass both through the Augmented Dickey–Fuller (ADF) mean reversion test to ensure they are stationary, i.e., mean reverting. You can find a ready-made indicator for such use at . Many thanks to tbtkg for this indicator.

SUMMARY

CUSUM VB combines CUSUM statistical control, volatility-adaptive thresholds, volume weighting, and optional BB breakout confirmation to provide robust, actionable signals across a wide variety of trading instruments.

Why traders use it : Fast detection of shifts, reduced false alarms, versatile across markets.

Ideal for : Futures (continuous contracts), forex, crypto, stocks, ETFs, and commodity/index CFDs, especially where:

● Price and volume data exist

● Breakouts and volatility shifts are tradable

● There’s enough liquidity for meaningful signals

Visualization : Upper/lower CUSUM circles, UCL/LCL thresholds, optional highlight traded background, optional volume and BB overlays on the chart, optional entry/exit labels on the price chart, as well as entry/exit signals in the data window.

Alerts : For entry/exit labels when trades are actually filled.

CUSUM VB is designed for traders who want statistically grounded trend detection with configurable sensitivity, visual clarity, and multi-market versatility.

DISCLAIMER

This software and documentation are provided “as is” without any warranties of any kind, express or implied. CoinOperator assumes no responsibility or liability for any errors, omissions, or losses arising from the use or interpretation of this software or its outputs. Trading and investing carry inherent risks, and users are solely responsible for their own decisions and results.

Max Pain Options [QuantLabs] v5 (Balanced)Institutional Grade Options Analysis: Max Pain, Gamma & Pin Risk

For years, TradingView users have been flying blind without access to Options Chain data. QuantLabs: Max Pain & Gamma Exposure changes that. This is not just a support/resistance indicator—it is a sophisticated, algorithmic model that reverse-engineers the incentives of Market Makers using synthetic Black-Scholes logic.

This tool visualizes the "invisible hand" of the market: the hedging requirements of large dealers who are forced to buy or sell to keep their books neutral.

CORE FEATURES:

🔴 Max Pain Gravity Model The bright red line represents the "Max Pain" strike—the price level where the maximum amount of Options Open Interest (Calls + Puts) expires worthless.

Theory: As OpEx (Expiration) approaches, Market Makers maximize profits by pinning the price to this level.

Strategy: Use this as a mean-reversion target. If price is far away, look for a snap-back to the red line.

🟣 Gamma Exposure Profiles (The Purple Lines) These neon histograms show you the estimated "Gamma Walls."

Long Gamma: Dealers trade against the trend (stabilizing price).

Short Gamma: Dealers trade with the trend (accelerating volatility).

Visual: The larger the purple bar, the harder it will be for price to break through that level.

📦 Algorithmic "Pin Risk" Zones The dashed red box highlights the "Kill Zone." When price enters this area near expiration, volatility often dies as dealers pin the asset to kill retail premiums.

Warning: Do not expect breakouts while inside the Pin Zone.

📊 Institutional HUD A clean, non-intrusive dashboard provides real-time Greeks and risk analysis:

Pin Risk: High/Medium/Low probability of a pinned close.

Exp Mode: Detects if the market is in "Short Gamma" (Squeeze territory) or "Long Gamma" (Chop territory).

HOW IT WORKS (The Math): Since live options data is not available via Pine Script, this engine uses a proprietary Synthetic OI Distribution Model. It inputs Volume, Volatility (IV), and Time-to-Expiry into a modified Black-Scholes equation to probability-map where the heavy open interest likely sits.

SETTINGS & CUSTOMIZATION:

Responsiveness: Tuned for the "Goldilocks Zone" (Spread: 12, Decay: 22) to catch local liquidity walls without over-fitting.

Visuals: Designed for Dark Mode. High-contrast Neon aesthetics for maximum readability.

Friday Statistical Zones - Last 30 Fridays Only BTC 📊 Friday Statistical Zones (Pre / Dump / After)

This indicator highlights statistical risk zones for Fridays, based on the last 30 completed Fridays.

It analyzes historical price and volume behavior to determine:

• When a Pre-Dump phase typically starts

• When selling pressure statistically peaks

• When the After-Dump phase usually occurs

The result is a time-based overlay with three zones:

🟡 Pre-Dump · 🔴 Dump · 🟡 After-Dump

⚠️ This is not a signal indicator.

It does not predict price direction.

It provides risk-timing context only.

Best used for risk management and situational awareness on Fridays, not as a standalone trading strategy.

Arbitrage Detector [LuxAlgo]The Arbitrage Detector unveils hidden spreads in the crypto and forex markets. It compares the same asset on the main crypto exchanges and forex brokers and displays both prices and volumes on a dashboard, as well as the maximum spread detected on a histogram divided by four user-selected percentiles. This allows traders to detect unusual, high, typical, or low spreads.

This highly customizable tool features automatic source selection (crypto or forex) based on the asset in the chart, as well as current and historical spread detection. It also features a dashboard with sortable columns and a historical histogram with percentiles and different smoothing options.

🔶 USAGE

Arbitrage is the practice of taking advantage of price differences for the same asset across different markets. Arbitrage traders look for these discrepancies to profit from buying where it’s cheaper and selling where it’s more expensive to capture the spread.

For begginers this tool is an easy way to understand how prices can vary between markets, helping you avoid trading at a disadvantage.

For advanced traders it is a fast tool to spot arbitrage opportunities or inefficiencies that can be exploited for profit.

Arbitrage opportunities are often short‑lived, but they can be highly profitable. By showing you where spreads exist, this tool helps traders:

Understand market inefficiencies

Avoid trading at unfavorable prices

Identify potential profit opportunities across exchanges

As we can see in the image, the tool consists of two main graphics: a dashboard on the main chart and a histogram in the pane below.

Both are useful for understanding the behavior of the same asset on different crypto exchanges or forex brokers.

The tool's main goal is to detect and categorize spread activity across the major crypto and forex sources. The comparison uses data from up to 19 crypto exchanges and 13 forex brokers.

🔹 Forex or Crypto

The tool selects the appropriate sources (crypto exchanges or forex brokers) based on the asset in the chart. Traders can choose which one to use.

The image shows the prices and volumes for Bitcoin and the euro across the main sources, sorted by descending average price over the last 20 days.

🔹 Dashboard

The dashboard displays a list of all sources with four main columns: last price, average price, volume, and total volume.

All four columns can be sorted in ascending or descending order, or left unsorted. A background gradient color is displayed for the sorted column.

Price and volume delta information between the chart asset and each exchange can be enabled or disabled from the settings panel.

🔹 Histogram

The histogram is excellent for visualizing historical values and comparing them with the asset price.

In this case, we have the Euro/U.S. Dollar daily chart. As we can see, the unusual spread activity detected since 2016, with values at or above 98%, is usually a good indication of increased trader activity, which may result in a key price area where the market could turn around.

By default, the histogram has the gradient and smoothing auto features enabled.

The differences are visible in the chart above. On top is an adaptive moving average with higher values for unusual activity. At the bottom is an exponential moving average with a length of 9.

The differences between the gradient and solid colors are evident. In the first case, the colors are in sync with the data values, becoming more yellow with higher values and more green with lower values. In the second case, the colors are solid and only distinguish data above or below the defined percentiles.

🔶 SETTINGS

Sources: Choose between crypto exchanges, forex brokers, or automatic selection based on the asset in the chart.

Average Length: Select the length for the price and volume averages.

🔹 Percentiles

Percentile Length: Select the length for the percentile calculation, or enable the use of the full dataset. Enabling this option may result in runtime errors due to exceeding the allotted resources.

Unusual % >: Select the unusual percentile.

High % >: Select the high percentile.

Typical % >: Select the typical percentile.

🔹 Dashboard

Dashboard: Enable or disable the dashboard.

Sorting: Select the sorting column and direction.

Position: Select the dashboard location.

Size: Select the dashboard size.

Price Delta: Show the price difference between each exchange and the asset on the chart.

Volume Delta: Show the volume difference between each exchange and the asset on the chart.

🔹 Style

Unusual: Enable the plot of the unusual percentile and select its color.

High: Enable the plot of the high percentile and select its color.

Typical: Enable the plot of the typical percentile and select its color.

Low: Select the color for the low percentile.

Percentiles Auto Color: Enable auto color for all plotted percentiles.

Histogram Gradient: Enable the gradient color for the histogram.

Histogram Smoothing: Select the length of the EMA smoothing for the histogram or enable the Auto feature. The Auto feature uses an adaptive moving average with the data percent rank as the efficiency ratio.

OTT Volatility [RunRox]📊 OTT Volatility is an indicator developed by the RunRox team to pinpoint the most optimal time to trade across different markets.

OTT stands for Optimal Trade Time Volatility and is designed primarily for markets without a fixed trading session, such as cryptocurrencies that trade 24/7. At the same time, it works equally well on any other market.

🔶 The concept is straightforward. The indicator takes a specified number of historical periods (Samples) and statistically evaluates which hours of the day or which days show the highest volatility for the selected asset.

As a result, it highlights time windows with elevated volatility where traders can focus on searching for trade setups and building positions.

🔶 As the core volatility metric, the indicator uses ATR (Average True Range) to measure intraday volatility. Then it calculates the average ATR value over the last N Samples, creating a statistically stable estimate of typical volatility for the selected asset.

🔶 Statistically, during these highlighted periods the market shows higher-than-average volatility.

This means that in these time windows price is more likely to be subject to stronger moves and potential manipulation, making them attractive for active trade execution and position management.

⚠️ However, historical behavior does not guarantee future results.

These periods should be treated only as zones where volatility has a higher probability of being above normal, not as a promise of movement.

As shown in the screenshot above, the indicator also projects potential future volatility based on historical data. This helps you better plan your trading hours and align your activity with periods where volatility is statistically expected to be higher or lower.

🔶 Current Volatility – as shown in the screenshot above, you can also monitor the real-time volatility of the market without any statistical averaging.

On top of that, you can overlay the current volatility on top of the statistical volatility levels, which makes it easy to see whether the market is now trading in a high- or low-volatility regime relative to its usual behavior.

4 display modes – you can choose any visualization style that fits your trading workflow:

Absolute – displays the raw volatility values.

Relative – shows volatility relative to its typical levels.

Average Centered – centers volatility around its average value.

Trim Low Value – filters out low-volatility noise and highlights only more significant moves.

This indicator helps you define the most effective trading hours on any market by relying on historical volatility statistics.

Use it to quickly see when your market tends to be more active and to structure your trading sessions around those periods.

✅ We hope this tool becomes a useful part of your trading toolkit and helps you improve the quality of your decisions and timing.

Liquidity ThermometerThis is a universal indicator that assesses market liquidity based on five key market parameters: volume, volatility, candlestick range, body size, and price momentum.

The indicator does not use open interest data and is suitable for all markets, including spot, futures, and Forex.

This indicator normalizes each metric historically and creates a composite index between 0 and 1, where higher values correspond to a stable and calm market environment, and lower values indicate periods of increased risk and potential liquidity stress.

LT generates an integral liquidity index in the range based on five normalized components:

-nVol — normalized volume, reflecting trading density and activity.

-nATR — the volatility component (ATR), inverted, as high volatility is typically associated with declining liquidity.

-nRange — the normalized candlestick range, also inverted to assess the structural narrowness of the price movement.

-nBody — the normalized candlestick body size (|close − open|), inverted to assess the balance of supply and demand.

-nMove — the normalized value of the price impulse movement (|Δclose|), reflecting short-term price spikes.

Each metric is linearly normalized over a sliding window (200 bars) using the formula:

norm(x) = (x − min) / (max − min),

where at max = min, the value is fixed at 0.5 to ensure stability.

The ALT index is calculated as a weighted combination:

ALT = 0.35 nVol + 0.20 (1 − nATR) + 0.20 (1 − nRange) + 0.15 (1 − nBody) + 0.10 (1 − nMove)

The result is further smoothed using EMA(3) to reduce micronoise.

Red Zone (MLI < 0.25) — Risk, Thin Liquidity

When the indicator falls into the red zone, it means the market is extremely volatile:

Characteristics:

Low volume — small trades have a strong impact on the price.

High volatility — candlesticks rise or fall sharply.

Wide candlestick range — the market is "breathing heavily," easily breaking price extremes.

Impulsive movements — small market shocks lead to sharp spikes.

Thin liquidity — few orders in the order book, large orders "eat up" the market.

What this means for a trader:

🔥 High risk of spikes and false breakouts.

⚠ Possible series of liquidations on leverage.

❌ It is not recommended to enter long or short positions without a filter or protection.

✅ Can be used for short scalping strategies if you know the entry point, but very carefully.

Green Zone (MLI > 0.75) — High Liquidity, Safe Zone

When the indicator rises into the green zone, it means the market is stable and balanced:

Characteristics:

High volume — the market is deep, orders are executed without a strong impact on the price.

Low volatility — candlesticks are stable, no sharp spikes.

Narrow candlestick range — price moves calmly.

Weak impulse movements — no sharp surges.

Sufficient liquidity — the market can handle large orders.

What this means for a trader:

✅ Safe zone for opening positions.

🔄 Easier to set stop-loss and take-profit orders.

💡 You can trade both up and down, the risk of sharp movements is minimal.

⚡ Under these conditions, there is a lower risk of spikes and accidental liquidations.

It does not predict price movements or guarantee results. It is an analytical tool intended for additional research into market structure.

Price Drop CounterThe Price Drop Counter is a very basic statistical indicator.

See it as an analytical tool that tracks how many times an asset's price has dropped by a specified percentage from its recent peak within a defined date range.

The indicator monitors the highest price reached and counts each occurrence when the price falls by your chosen threshold, then resets its peak tracking point after each drop is registered.

Uses

Volatility Assessment: Measure how frequently significant price corrections occur during specific periods

Market Behavior Analysis: Compare drop frequency across different timeframes or market conditions

Risk Evaluation: Identify assets or periods with higher downside volatility

Historical Pattern Recognition: Study how often major pullbacks happened during bull or bear markets

Backtesting Support: Analyze how your strategy would perform based on the frequency of drawdowns

How to use it

Add the indicator to your TradingView chart

Configure the Percent Drop (%) to define your threshold (default: 10%). The indicator will count each time price falls by this percentage from the most recent high

IMPORTANT Set your Start Date and End Date to analyze a specific period of interest

The blue step-line plot shows the cumulative count of drops within your date range

Adjust the percentage threshold based on your analysis needs - use smaller values (2-5%) for more frequent signals or larger values (15-20%) for major corrections only

The counter resets its high-water mark after each qualifying drop, allowing it to track multiple sequential drops within the same period.

Percentile Rank Oscillator (Price + VWMA)A statistical oscillator designed to identify potential market turning points using percentile-based price analytics and volume-weighted confirmation.

What is PRO?

Percentile Rank Oscillator measures how extreme current price behavior is relative to its own recent history. It calculates a rolling percentile rank of price midpoints and VWMA deviation (volume-weighted price drift). When price reaches historically rare levels – high or low percentiles – it may signal exhaustion and potential reversal conditions.

How it works

Takes midpoint of each candle ((H+L)/2)

Ranks the current value vs previous N bars using rolling percentile rank

Maps percentile to a normalized oscillator scale (-1..+1 or 0–100)

Optionally evaluates VWMA deviation percentile for volume-confirmed signals

Highlights extreme conditions and confluence zones

Why percentile rank?

Median-based percentiles ignore outliers and read the market statistically – not by fixed thresholds. Instead of guessing “overbought/oversold” values, the indicator adapts to current volatility and structure.

Key features

Rolling percentile rank of price action

Optional VWMA-based percentile confirmation

Adaptive, noise-robust structure

User-selectable thresholds (default 95/5)

Confluence highlighting for price + VWMA extremes

Optional smoothing (RMA)

Visual extreme zone fills for rapid signal recognition

How to use

High percentile values –> statistically extreme upward deviation (potential top)

Low percentile values –> statistically extreme downward deviation (potential bottom)

Price + VWMA confluence strengthens reversal context

Best used as part of a broader trading framework (market structure, order flow, etc.)

Tip: Look for percentile spikes at key HTF levels, after extended moves, or where liquidity sweeps occur. Strong moves into rare percentile territory may precede mean reversion.

Suggested settings

Default length: 100 bars

Thresholds: 95 / 5

Smoothing: 1–3 (optional)

Important note

This tool does not predict direction or guarantee outcomes. It provides statistical context for price extremes to help traders frame probability and timing. Always combine with sound risk management and other tools.

Statistical Price Deviation Index (MAD/VWMA)SPDI is a statistical oscillator designed to detect potential price reversal zones by measuring how far price deviates from its typical behavior within a defined rolling window.

Instead of using momentum or moving averages like traditional indicators, SPDI applies robust statistics - a rolling median and Mean Absolute Deviation (MAD) - to calculate a normalized measure of price displacement. This normalization keeps the output bounded (from −1 to +1 by default), producing a stable and consistent oscillator that adapts to changing volatility conditions.

The second line in SPDI uses a Volume-Weighted Moving Average (VWMA) instead of a simple price median. This creates a complementary oscillator showing statistically weighted deviations based on traded volume. When both oscillators align in their extremes, strong confluence reversal signals are generated.

How It Works

For each bar, SPDI calculates the median price of the last N bars (default 100).

It then measures how far the current bar’s midpoint deviates from that rolling median.

The Mean Absolute Deviation (MAD) of those distances defines a “normal” range of fluctuation.

The deviation is normalized and compressed via a tanh mapping, keeping the oscillator in fixed boundaries (−1 to +1).

The same logic is applied to the VWMA line to gauge volume-weighted deviations.

How to Use

The blue line (Price MAD) represents pure price deviation.

The green line (VWMA Disp) shows the volume-weighted deviation.

Overbought (red) zones indicate statistically extreme upward deviation -> potential short-term overextension.

Oversold (green) zones indicate statistically extreme downward deviation -> potential rebound area.

Confluence signals (both lines hitting the same extreme) often mark strong reversal points.

Settings Tips

Lookback length controls how much historical data defines “normal” behavior. Larger = smoother, smaller = more sensitive.

Smoothing (RMA length) can reduce noise without changing the overall statistical logic.

Output scale can be set to either −1..+1 or 0..100, depending on your visual preference.

Alerts and color fills are fully customizable in the Style tab.

Summary:

SPDI transforms raw price and volume data into a statistically bounded deviation index. When both Price MAD and VWMA Disp reach joint extremes, it highlights probable market turning points - offering traders a clean, data-driven way to spot potential reversals ahead of time.

Aggregated Scores Oscillator [Alpha Extract]A sophisticated risk-adjusted performance measurement system that combines Omega Ratio and Sortino Ratio methodologies to create a comprehensive market assessment oscillator. Utilizing advanced statistical band calculations with expanding and rolling window analysis, this indicator delivers institutional-grade overbought/oversold detection based on risk-adjusted returns rather than traditional price movements. The system's dual-ratio aggregation approach provides superior signal accuracy by incorporating both upside potential and downside risk metrics with dynamic threshold adaptation for varying market conditions.

🔶 Advanced Statistical Framework

Implements dual statistical methodologies using expanding and rolling window calculations to create adaptive threshold bands that evolve with market conditions. The system calculates cumulative statistics alongside rolling averages to provide both historical context and current market regime sensitivity with configurable window parameters for optimal performance across timeframes.

🔶 Dual Ratio Integration System

Combines Omega Ratio analysis measuring excess returns versus deficit returns with Sortino Ratio calculations focusing on downside deviation for comprehensive risk-adjusted performance assessment. The system applies configurable smoothing to both ratios before aggregation, ensuring stable signal generation while maintaining sensitivity to regime changes.

// Omega Ratio Calculation

Excess_Return = sum((Daily_Return > Target_Return ? Daily_Return - Target_Return : 0), Period)

Deficit_Return = sum((Daily_Return < Target_Return ? Target_Return - Daily_Return : 0), Period)

Omega_Ratio = Deficit_Return ≠ 0 ? (Excess_Return / Deficit_Return) : na

// Sortino Ratio Framework

Downside_Deviation = sqrt(sum((Daily_Return < Target_Return ? (Daily_Return - Target_Return)² : 0), Period) / Period)

Sortino_Ratio = (Mean_Return / Downside_Deviation) * sqrt(Annualization_Factor)

// Aggregated Score

Aggregated_Score = SMA(Omega_Ratio, Omega_SMA) + SMA(Sortino_Ratio, Sortino_SMA)

🔶 Dynamic Band Calculation Engine

Features sophisticated threshold determination using both expanding historical statistics and rolling window analysis to create adaptive overbought/oversold levels. The system incorporates configurable multipliers and sensitivity adjustments to optimize signal timing across varying market volatility conditions with automatic band convergence logic.

🔶 Signal Generation Framework

Generates overbought conditions when aggregated score exceeds adjusted upper threshold and oversold conditions below lower threshold, with neutral zone identification for range-bound markets. The system provides clear binary signal states with background zone highlighting and dynamic oscillator coloring for intuitive market condition assessment.

🔶 Enhanced Visual Architecture

Provides modern dark theme visualization with neon color scheme, dynamic oscillator line coloring based on signal states, and gradient band fills for comprehensive market condition visualization. The system includes zero-line reference, statistical band plots, and background zone highlighting with configurable transparency levels.

snapshot

🔶 Risk-Adjusted Performance Analysis

Utilizes target return parameters for customizable risk assessment baselines, enabling traders to evaluate performance relative to specific return objectives. The system's focus on downside deviation through Sortino analysis provides superior risk-adjusted signals compared to traditional volatility-based oscillators that treat upside and downside movements equally.

🔶 Multi-Timeframe Adaptability

Features configurable calculation periods and rolling windows to optimize performance across various timeframes from intraday to long-term analysis. The system's statistical foundation ensures consistent signal quality regardless of timeframe selection while maintaining sensitivity to market regime changes through adaptive band calculations.

🔶 Performance Optimization Framework

Implements efficient statistical calculations with optimized variable management and configurable smoothing parameters to balance responsiveness with signal stability. The system includes automatic band adjustment mechanisms and rolling window management for consistent performance across extended analysis periods.

This indicator delivers sophisticated risk-adjusted market analysis by combining proven statistical ratios in a unified oscillator framework. Unlike traditional overbought/oversold indicators that rely solely on price movements, the ASO incorporates risk-adjusted performance metrics to identify genuine market extremes based on return quality rather than price volatility alone. The system's adaptive statistical bands and dual-ratio methodology provide institutional-grade signal accuracy suitable for systematic trading approaches across cryptocurrency, forex, and equity markets with comprehensive visual feedback and configurable risk parameters for optimal strategy integration.

Expected Value Monte CarloI created this indicator after noticing that there was no Expected Value indicator here on TradingView.

The EVMC provides statistical Expected Value to what might happen in the future regarding the asset you are analyzing.

It uses 2 quantitative methods:

Historical Backtest to ground your analysis in long-term, factual data.

Monte Carlo Simulation to project a cone of probable future outcomes based on recent market behavior.

This gives you a data-driven edge to quantify risk, and make more informed trading decisions.

The indicator includes:

Dual analysis: Combines historical probability with forward-looking simulation.

Quantified projections: Provides the Expected Value ($ and %), Win Rate, and Sharpe Ratio for both methods.

Asset-aware: Automatically adjusts its calculations for Stocks (252 trading days) and Crypto (365 days) for mathematical accuracy.

The projection cone shows the mean expected path and the +/- 1 standard deviation range of outcomes.

No repainting

Calculation:

1. Historical Expected Value:

This is a systematic backtest over thousands of bars. It calculates the return Rᵢ for N past trades (buy-and-hold). The Historical EV is the simple average of these returns, giving a baseline performance measure.

Historical EV % = (Σ Rᵢ) / N

2. Monte Carlo Projection:

This projection uses the Geometric Brownian Motion (GBM) model to simulate thousands of future price paths based on the market's recent behavior.

It first measures the drift (μ), or recent trend, and volatility (σ), or recent risk, from the Projection Lookback period. It then projects a final return for each simulation using the core GBM formula:

Projected Return = exp( (μ - σ²/2)T + σ√T * Z ) - 1

(Where T is the time horizon and Z is a random variable for the simulation.)

The purple line on the chart is the average of all simulated outcomes (the Monte Carlo EV). The cone represents one standard deviation of those outcomes.

The dashed lines represent one standard deviation (+/- 1σ) from the average, forming a cone of probable outcomes. Roughly 68% of the simulated paths ended within this cone.

This projection answers the question: "If the recent trend and volatility continue, where is the price most likely to go?"

Here's how to read the indicator

Expected Value ($/%): Is my average trade profitable?

Win Rate: How often can I expect to be right?

Sharpe Ratio: Am I being adequately compensated for the risk I'm taking?

User Guide

Max trade duration (bars): This is your analysis timeframe. Are you interested in the probable outcome over the next month (21 bars), quarter (63 bars), or year (252 bars)?

Position size ($): Set this to your typical trade size to see the Expected Value in real dollar terms.

Projection lookback (bars): This is the most important input for the Monte Carlo model. A short lookback (e.g., 50) makes the projection highly sensitive to recent momentum. Use this to identify potential recency bias. A long lookback (e.g., 252) provides a more stable, long-term projection of trend and volatility.

Historical Lookback (bars): For the historical backtest, more data is always better. Use the maximum that your TradingView plan allows for the most statistically significant results.

Use TP/SL for Historical EV: Check this box to see how the historical performance would have changed if you had used a simple Take Profit and Stop Loss, rather than just holding for the full duration.

I hope you find this indicator useful and please let me know if you have any suggestions. 😊

Stop Loss vs Take Profit Probability and EVThis stop loss and take profit calculator uses a Monte Carlo simulation to calculate the probability of hitting your Stop Loss or Take Profit levels across different time horizons (expressed in bars).

It provides data-driven insights to optimize your risk management and position sizing by showing Expected Value for each scenario.

As a quant, I love using statistical data to help my decisions and get better EV from my trades.

🔬 How It's Calculated

Monte Carlo Simulation: Runs 1,000-10,000 price simulations using a random walk model

Volatility Analysis: Combines ATR-based and Historical Volatility for accurate price movement modeling

Expected Value: Calculates profit/loss expectation using formula: (TP_Probability × Reward) - (SL_Probability × Risk)

Time Horizons: Tests multiple timeframes (1, 5, 10, 20, 50 bars) to find optimal holding periods

Risk/Reward Ratios: Automatically calculates and displays R:R ratios for quick assessment

💡 Use Cases

Position Sizing - Determine optimal risk per trade based on Expected Value

Time Horizon Optimization - Find the best holding period for your strategy

Stop Loss Placement - Validate SL levels using probability analysis

Take Profit Optimization - Set TP levels with statistical backing

Strategy Backtesting - Compare different R:R setups before entering trades

Risk Management - Avoid trades with negative Expected Value

Swing vs Day Trading - Choose timeframes with highest success probability

🎯 How to Use

Setup Trade: Enter your entry price, stop loss, and take profit levels

You can add or remove time horizons denominated in bars. Say you are looking at 1h candles, adding a 24-bar time horizon means you are looking into 24 hours

Choose Direction: Select Long or Short position

Review Table

Analyze Expected Value: Focus on positive EV scenarios (green background)

Optimize Timing: Select time horizons with best risk/reward profile

Adjust Parameters: Modify volatility calculation method and simulation count if needed

Examples

Here's how you can read the tables.

Example 1:

In this chart, we are analyzing the TP and SL probabilities as well as the EV (expected value) for a stock. I want to check what the likelihood is that my SL and TP get triggered over the next 5 days. The stock market is open for 6.5 hours per day, which is 13 bars in this 30-minute bar chart. 26 bars is 2 days, 39 bars is 3 days and so on.

Although this trade is more likely to trigger my SL than my TP, in some of the time horizons we have a positive expected value because of the risk/reward of our trade (i.e. distance of the SL and TP from the price) and the probability of hitting SL and TP.

Example 2:

In this example, we have applied the indicator to gold. Because the TP is much closer to the price, the probability of hitting the TP is much higher.

We can also observe that the expected Value in the shorter time frames is better than in the longer ones. This can give us some clues to set up our trade. If we know that the EV is positive, we can allocate more to that specific trade.

Enjoy, and please let me know your feedback! 😊🥂

Forecasting Quadratic Regression [UPDATED V6] Forecasting Quadratic Regression applies a second-degree polynomial regression model to price data, offering a non-linear alternative to traditional linear regression. By fitting a quadratic curve of the form:

y=a+bx+cx2

the indicator captures both directional trend and curvature, allowing traders to detect momentum shifts earlier than with straight-line models.

🔹 Core Features

Fits a quadratic regression curve to user-defined lookback periods

Extends the fitted curve forward to generate forecast projections

Calculates slope curvature to highlight trend acceleration or deceleration

Adapts dynamically as new bars are added

🔹 Trading Applications

Identify potential reversal zones when the curve inflects (2nd derivative sign change)

Forecast near-term mean reversion targets or extended trend continuations

Filter trades by measuring momentum curvature rather than linear slope

Visualize higher-order structure in price beyond standard regression lines

⚠️ Note: This model is statistical and assumes past curvature informs short-term future price paths. It should be combined with confirmation signals (volume, oscillators, support/resistance) to reduce false inflection points.

Markov Chain Trend ProbabilityA Markov Chain is a mathematical model that predicts future states based on the current state, assuming that the future depends only on the present (not the past). Originally developed by Russian mathematician Andrey Markov, this concept is widely used in:

Finance: Risk modeling, portfolio optimization, credit scoring, algorithmic trading

Weather Forecasting: Predicting sunny/rainy days, temperature patterns, storm tracking

Here's an example of a Markov chain: If the weather is sunny, the probability that will be sunny 30 min later is say 90%. However, if the state changes, i.e. it starts raining, how the probability that will be raining 30 min later is say 70% and only 30% sunny.

Similar concept can be applied to markets price action and trends.

Mathematical Foundation

The core principle follows the Markov Property: P(X_{t+1}|X_t, X_{t-1}, ..., X_0) = P(X_{t+1}|X_t)

Transition Matrix :

-------------Next State

Current----

--------P11 P12

-----P21 P22

Probability Calculations:

P(Up→Up) = Count(Up→Up) / Count(Up states)

P(Down→Down) = Count(Down→Down) / Count(Down states)

Steady-state probability: π = πP (where π is the stationary distribution)

State Definition:

State = UPTREND if (Price_t - Price_{t-n})/ATR > threshold

State = DOWNTREND if (Price_t - Price_{t-n})/ATR < -threshold

How It Works in Trading

This indicator applies Markov Chain theory to market trends by:

Defining States: Classifies market conditions as UPTREND or DOWNTREND based on price movement relative to ATR (Average True Range)

Learning Transitions: Analyzes historical data to calculate probabilities of moving from one state to another

Predicting Probabilities: Estimates the likelihood of future trend continuation or reversal

How to Use

Parameters:

Lookback Period: Number of bars to analyze for trend detection (default: 14)

ATR Threshold: Sensitivity multiplier for state changes (default: 0.5)

Historical Periods: Sample size for probability calculations (default: 33)

Trading Applications:

Trend confirmation for entry/exit decisions

Risk assessment through probability analysis

Market regime identification

Early warning system for potential trend reversals

The indicator works on any timeframe and asset class. Enjoy!

Statistical Pairs Trading IndicatorZ-Score Stat Trading — Statistical Pairs Trading Indicator

📊🔗

---

What is it?

Z-Score Stat Trading is a powerful indicator for statistical pairs trading and quantitative analysis of two correlated assets.

It calculates the Z-Score of the log-price spread between any two symbols you choose, providing both long-term and short-term Z-Score signals.

You’ll also see real-time correlation, volatility, spread, and the number of long/short signals in a handy on-chart table!

---

How to Use 🛠️

1. Add the indicator to your chart.

2. Select two assets (symbols) to analyze in the settings.

3. Watch the Z-Score plots (blue and orange lines) and threshold levels (+2, -2 by default).

4. Check the info table for:

- Correlation

- Volatility

- Spread

- Number of long (NL) and short (NS) signals in the last 1000 bars

5. Set up alerts for signal generation or threshold crossings if you want to be notified automatically.

---

Trading Strategy 💡

- This indicator is designed for statistical arbitrage (mean reversion) strategies.

- Long Signal (🟢):

When both Z-Scores drop below the negative threshold (e.g., -2), a long signal is generated.

→ Buy Symbol A, Sell Symbol B, expecting the spread to revert to the mean.

- Short Signal (🔴):

When both Z-Scores rise above the positive threshold (e.g., +2), a short signal is generated.

→ Sell Symbol A, Buy Symbol B, again expecting mean reversion.

- The info table helps you quickly assess the frequency of signals and the current statistical relationship between your chosen assets.

---

Best Practices & Warnings 🚦

- Avoid high leverage! Pairs trading can be risky, especially during periods of divergence. Use conservative position sizing.

- Check for cointegration: Before using this indicator, make sure both assets are cointegrated or have a strong historical relationship. This increases the reliability of mean reversion signals.

- Check correlation: Only use asset pairs with a high correlation (preferably 0.8–0.9 or higher) for best results. The correlation value is shown in the info table.

- Scale in and out gradually: When entering or exiting positions, consider doing so in parts rather than all at once. This helps manage slippage and risk, especially in volatile markets.

---

⚠️ Note on Performance:

This indicator may work a bit slowly, especially on large timeframes or long chart histories, because the calculation of NL and NS (number of long/short signals) is computationally intensive.

---

Disclaimer ⚠️

This script is provided for educational and informational purposes only .

It is not financial advice or a recommendation to buy or sell any asset.

Use at your own risk. The author assumes no responsibility for any trading decisions or losses.

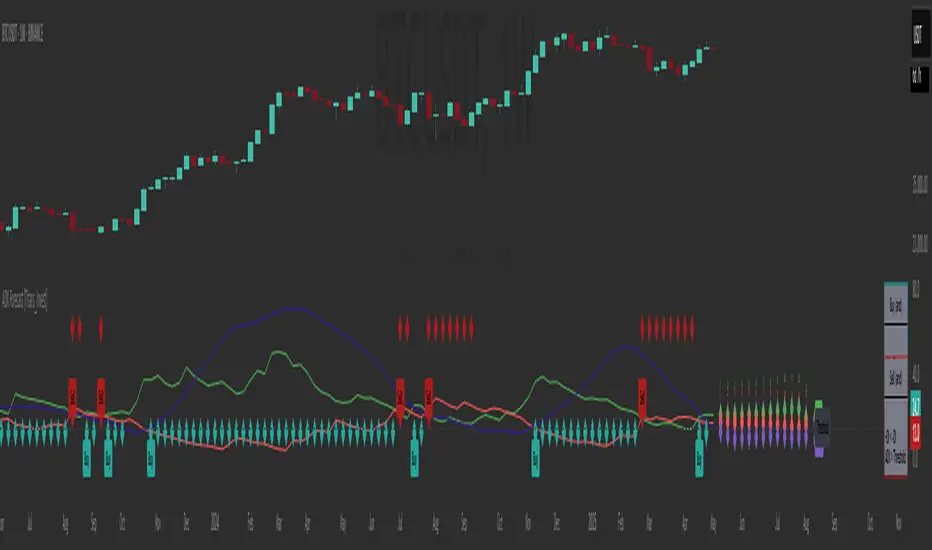

ADX Forecast [Titans_Invest]ADX Forecast

This isn’t just another ADX indicator — it’s the most powerful and complete ADX tool ever created, and without question the best ADX indicator on TradingView, possibly even the best in the world.

ADX Forecast represents a revolutionary leap in trend strength analysis, blending the timeless principles of the classic ADX with cutting-edge predictive modeling. For the first time on TradingView, you can anticipate future ADX movements using scientifically validated linear regression — a true game-changer for traders looking to stay ahead of trend shifts.

1. Real-Time ADX Forecasting

By applying least squares linear regression, ADX Forecast projects the future trajectory of the ADX with exceptional accuracy. This forecasting power enables traders to anticipate changes in trend strength before they fully unfold — a vital edge in fast-moving markets.

2. Unmatched Customization & Precision

With 26 long entry conditions and 26 short entry conditions, this indicator accounts for every possible ADX scenario. Every parameter is fully customizable, making it adaptable to any trading strategy — from scalping to swing trading to long-term investing.

3. Transparency & Advanced Visualization

Visualize internal ADX dynamics in real time with interactive tags, smart flags, and fully adjustable threshold levels. Every signal is transparent, logic-based, and engineered to fit seamlessly into professional-grade trading systems.

4. Scientific Foundation, Elite Execution

Grounded in statistical precision and machine learning principles, ADX Forecast upgrades the classic ADX from a reactive lagging tool into a forward-looking trend prediction engine. This isn’t just an indicator — it’s a scientific evolution in trend analysis.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the ADX, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an ADX time series like this:

Time →

ADX →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted ADX, which can be crossed with the actual ADX to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public ADX with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining ADX with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

ADX Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_______________________________________________________________________

🥇 This is the world’s first ADX indicator with: Linear Regression for Forecasting 🥇_______________________________________________________________________

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE ADX❓

The Average Directional Index (ADX) is a technical analysis indicator developed by J. Welles Wilder. It measures the strength of a trend in a market, regardless of whether the trend is up or down.

The ADX is an integral part of the Directional Movement System, which also includes the Plus Directional Indicator (+DI) and the Minus Directional Indicator (-DI). By combining these components, the ADX provides a comprehensive view of market trend strength.

⯁ HOW TO USE THE ADX❓

The ADX is calculated based on the moving average of the price range expansion over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and has three main zones:

• Strong Trend: When the ADX is above 25, indicating a strong trend.

• Weak Trend: When the ADX is below 20, indicating a weak or non-existent trend.

• Neutral Zone: Between 20 and 25, where the trend strength is unclear.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔹 +DI > -DI

🔹 +DI < -DI

🔹 +DI > ADX

🔹 +DI < ADX

🔹 -DI > ADX

🔹 -DI < ADX

🔹 ADX > Threshold

🔹 ADX < Threshold

🔹 +DI > Threshold

🔹 +DI < Threshold

🔹 -DI > Threshold

🔹 -DI < Threshold

🔹 +DI (Crossover) -DI

🔹 +DI (Crossunder) -DI

🔹 +DI (Crossover) ADX

🔹 +DI (Crossunder) ADX

🔹 +DI (Crossover) Threshold

🔹 +DI (Crossunder) Threshold

🔹 -DI (Crossover) ADX

🔹 -DI (Crossunder) ADX

🔹 -DI (Crossover) Threshold

🔹 -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔸 +DI > -DI

🔸 +DI < -DI

🔸 +DI > ADX

🔸 +DI < ADX

🔸 -DI > ADX

🔸 -DI < ADX

🔸 ADX > Threshold

🔸 ADX < Threshold

🔸 +DI > Threshold

🔸 +DI < Threshold

🔸 -DI > Threshold

🔸 -DI < Threshold

🔸 +DI (Crossover) -DI

🔸 +DI (Crossunder) -DI

🔸 +DI (Crossover) ADX

🔸 +DI (Crossunder) ADX

🔸 +DI (Crossover) Threshold

🔸 +DI (Crossunder) Threshold

🔸 -DI (Crossover) ADX

🔸 -DI (Crossunder) ADX

🔸 -DI (Crossover) Threshold

🔸 -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : ADX Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

RSI Full Forecast [Titans_Invest]RSI Full Forecast

Get ready to experience the ultimate evolution of RSI-based indicators – the RSI Full Forecast, a boosted and even smarter version of the already powerful: RSI Forecast

Now featuring over 40 additional entry conditions (forecasts), this indicator redefines the way you view the market.

AI-Powered RSI Forecasting:

Using advanced linear regression with the least squares method – a solid foundation for machine learning - the RSI Full Forecast enables you to predict future RSI behavior with impressive accuracy.

But that’s not all: this new version also lets you monitor future crossovers between the RSI and the MA RSI, delivering early and strategic signals that go far beyond traditional analysis.

You’ll be able to monitor future crossovers up to 20 bars ahead, giving you an even broader and more precise view of market movements.

See the Future, Now:

• Track upcoming RSI & RSI MA crossovers in advance.

• Identify potential reversal zones before price reacts.

• Uncover statistical behavior patterns that would normally go unnoticed.

40+ Intelligent Conditions:

The new layer of conditions is designed to detect multiple high-probability scenarios based on historical patterns and predictive modeling. Each additional forecast is a window into the price's future, powered by robust mathematics and advanced algorithmic logic.

Full Customization:

All parameters can be tailored to fit your strategy – from smoothing periods to prediction sensitivity. You have complete control to turn raw data into smart decisions.

Innovative, Accurate, Unique:

This isn’t just an upgrade. It’s a quantum leap in technical analysis.

RSI Full Forecast is the first of its kind: an indicator that blends statistical analysis, machine learning, and visual design to create a true real-time predictive system.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION