Trendslinger CVDCVD - Cumulative Volume Delta

Cumulative Volume Delta (CVD) tracks the running total of buying versus selling pressure by analyzing volume distribution within each price bar. This indicator visualizes order flow dynamics to help identify accumulation, distribution, and potential trend reversals.

How It Works

CVD calculates the "delta" (difference between buying and selling volume) for each bar and accumulates it over time. Two calculation methods are available:

Close Position: Estimates buy/sell volume based on where price closes within the bar's range. A close near the high suggests more buying pressure; a close near the low suggests more selling pressure.

Polarity: Simple method where green candles count as buy volume and red candles count as sell volume.

Key Features

Multiple Display Types: View CVD as candlesticks, line, histogram, area, or columns

Flexible Reset Options: Reset CVD hourly, daily, or weekly for cleaner intraday analysis

Divergence Detection: Automatically identifies bullish and bearish divergences between price and CVD

Session Tracking: Optional high/low reference lines for the current session

Smoothing Options: Apply SMA, EMA, WMA, or RMA smoothing to reduce noise

Info Table: Real-time display of current CVD value, bar delta, and session extremes

Built-in Alerts: Zero line crosses, divergences, and new session highs/lows

How To Use

Trend Confirmation: Rising CVD confirms bullish price action; falling CVD confirms bearish moves

Divergences: Price making new highs while CVD makes lower highs signals weakening buying pressure (bearish). Price making new lows while CVD makes higher lows signals weakening selling pressure (bullish)

Zero Line: CVD crossing above zero suggests buyers taking control; crossing below suggests sellers dominating

Hourly Resets: Useful for scalping and intraday trading to track momentum within each hour

Biến động

Institutional Options Matrix [Pro]# Institutional Options Matrix – Whale Flow & Gamma Detector

### 🚀 Stop Trading Single Strikes. Start Trading the Matrix.

Most retail traders make a critical mistake: they analyze a single option strike in isolation. **Institutional Desks do not trade this way.** They trade the volatility surface, sweeping liquidity across the ATM (At-The-Money) and OTM (Out-Of-The-Money) strikes simultaneously.

The **Institutional Options Matrix ** is designed to bridge the gap between retail charts and institutional order flow. It does not just look at price; it aggregates **Volume Pressure, Delta Sensitivity, and Implied Volatility** across a cluster of strikes to detect when "Whales" are positioning for a move.

---

### 🧠 The Quant Logic (How it Works)

This indicator moves beyond simple Moving Averages. It employs **Multi-Strike Cluster Analysis**:

1. **Aggregate Volume Pressure:** Instead of watching just the ATM strike, this algorithm sums the volume of the **ATM + OTM1 + OTM2** strikes. This reveals the true "Sector Sentiment." If the ATM volume is low but OTM volume is spiking, the indicator detects "Speculative Accumulation."

2. **Net Order Flow Histogram:** The histogram at the bottom visualizes the net battle between Call Writers and Put Writers.

* **Green Columns:** Net Call Buying Pressure.

* **Red Columns:** Net Put Buying Pressure.

3. **Smoothed Gamma Detector:** Using a custom smoothing algorithm on Spot vs. Option pricing, the script calculates the rate of change (Gamma). When this spikes, it triggers a **"Gamma Zone"** (Yellow Background), indicating that price is accelerating and Market Makers are likely trapped.

4. **Smart Strike Alignment:** The dashboard monitors the live Spot price. If the market moves significantly away from your selected strike, the dashboard alerts you to **"⚠️ SHIFT TO "**, ensuring you are never trading stale data.

---

### 📊 Key Features

* **Whale Flow Histogram:** Visualizes the aggregate pressure of the top 3 strikes.

* **Gamma Squeeze Zones:** Highlights explosive momentum areas with a yellow background.

* **Dynamic Dashboard:** Displays real-time ATM pricing, Aggregated Volume, and Strike status.

* **Speculation Alerts:** Detects when volume is spiking on OTM strikes (a leading indicator of a breakout).

* **Clean Visuals:** Plots Call (Green) and Put (Red) premiums directly on the chart with simple Buy/Sell triangular signals.

---

### 🛠️ How to Use

**1. Setup:**

* **Asset:** Select Index (NIFTY, BANKNIFTY) or Stock.

* **Expiry:** Enter the current expiry in `YYMMDD` format (e.g., `251212`).

* **Strike:** Enter the current ATM strike manually (e.g., `24500`).

* *Note: Check the dashboard! If it says "⚠️ SHIFT TO...", update your inputs.*

**2. Long Entry (Call Buy):**

* **Signal:** Green Triangle (Call Entry).

* **Confirmation:** Net Flow Histogram is **GREEN** (Positive).

* **Price:** Call Premium (Green Line) crosses above its VWAP.

**3. Short Entry (Put Buy):**

* **Signal:** Red Triangle (Put Entry).

* **Confirmation:** Net Flow Histogram is **RED** (Negative).

* **Price:** Put Premium (Red Line) crosses above its VWAP.

**4. The Gamma Boost:**

* If the background turns **YELLOW**, a Gamma Squeeze is active. These are high-probability, high-velocity moves.

---

### ⚠️ Disclaimer

*This tool is for educational purposes only. Options trading involves significant risk and is not suitable for all investors. This script relies on data provided by TradingView (NSE); delayed data may affect signal accuracy. Always manage your risk.*

Consolidation Chopper█ OVERVIEW

Consolidation Chopper is a regime detection indicator designed to identify whether the market is currently in a consolidation (sideways) phase or a trending phase. The indicator uses a proprietary multi-timeframe approach to analyze price action across different windows, providing a more robust classification than single-timeframe methods.

The indicator features an impulse override system that can detect sudden breakouts from consolidation ranges, allowing for faster regime transitions when significant price movement occurs.

█ FEATURES

Three-State Regime Detection

• Sideways — Market is consolidating with no clear directional bias

• Breakout — An impulse move has been detected, signaling a potential regime change

• Trending — Market is exhibiting directional movement

Adaptive Thresholds

The indicator can self-calibrate its detection thresholds based on the instrument's historical behavior, making it adaptable across different markets and asset classes without manual tuning.

Dynamic Range Tracking

During consolidation periods, the indicator tracks the evolving range boundaries:

• Yellow lines show the current range high and low

• Orange lines show the buffered boundaries used for impulse detection

• Range continuously updates as price action develops

Impulse Override System

Multiple configurable conditions can trigger an early exit from consolidation:

• Bar body relative to range size

• Bar range relative to volatility

• Close beyond buffered range boundaries

• Multi-bar cumulative movement

Each condition can be independently enabled or disabled.

Confirmation Layers

Optional confirmation metrics provide additional confidence scoring for the current regime classification. The info panel displays confidence percentage and confirmation status.

Cooldown System

Prevents rapid regime oscillation by enforcing a minimum duration after breakout events before allowing return to sideways classification.

█ HOW TO USE

1 — Add the indicator to your chart. The background color indicates the current regime.

2 — During sideways regimes, observe the yellow range lines to understand the current consolidation boundaries.

3 — Watch for IMP markers which indicate impulse-triggered breakouts.

4 — Use the info panel (top right) to monitor:

Current regime and confidence level

Range boundaries and buffer values

Cooldown status

5 — Adjust impulse detection parameters based on your instrument's volatility characteristics.

Higher values = fewer triggers (more conservative)

Lower values = more triggers (more sensitive)

█ SETTINGS

Threshold Settings

Control the sensitivity of regime classification. Adaptive mode auto-calibrates based on historical data tuned for your instrument.

Impulse Override

Configure which conditions trigger early breakout detection and their respective thresholds.

Multi-Bar Impulse

Settings for detecting breakouts that occur over multiple bars rather than a single impulse candle.

Range Tracking

Configure the establishment period and buffer zone for consolidation range detection.

Cooldown

Set the minimum bars required after a breakout before returning to sideways classification.

█ LIMITATIONS

• The indicator requires sufficient historical data to establish adaptive thresholds.

Initial bars may show less reliable classifications.

• Like all regime detection methods, there is going to be inherent lag in identifying transitions, but this method minimizes it.

The impulse override system helps mitigate this but cannot eliminate it entirely.

• Performance may vary across different timeframes and instruments.

Some parameter tuning is recommended for optimal results.

█ NOTES

This indicator is designed as a filter or context tool to be used alongside other analysis methods. It does not generate trade signals directly but provides market structure context that can inform trading decisions. Typically once a range breaks you can expect directional movement/impulses or higher volatility regimes.

Tập lệnh trả phí

Wick to Body Ratio TableHello, I'm Gomaa if don't know me and if you want to know more about me follow me on my social media accounts which my propose to teach people "How To Learn".

Use this link so you can find me: linktr.ee

Overview

The "Wick to Body Ratio Table" is a comprehensive analytical tool designed to provide traders with detailed insights into candle structure and price movement dynamics. This indicator breaks down each candle into its component parts and displays real-time statistics in an easy-to-read table format.

What It Does

This indicator analyzes the current candle and displays four key metrics for each component:

Ratio to Body - How large each wick is compared to the candle body

Percentage of Total - What portion of the entire candle each component represents

Move Percentage - The actual price movement as a percentage from the opening price

Component breakdown - Upper wick, body, lower wick, and totals

Key Features

Real-Time Analysis:

Updates automatically with every price tick on the current candle

Works seamlessly across ALL timeframes (1 second to monthly charts)

No lag or delay in calculations

Comprehensive Metrics:

Upper Wick: Shows rejection from higher prices and selling pressure

Closed Body: Displays the actual price change from open to close (bullish=green, bearish=red)

Lower Wick: Indicates rejection from lower prices and buying pressure

Total Wick: Combined wick analysis for overall volatility assessment

Whole Candle: Complete range from high to low with total movement percentage

Visual Design:

Color-coded rows for easy identification

Clear headers for each metric column

Positioned at top-right of chart (non-intrusive)

Professional table format with borders and proper spacing

How to Interpret the Data

Ratio to Body Column:

A ratio of 2.0x means that component is twice the size of the body

N/A appears for doji candles (when body = 0)

Higher ratios indicate stronger rejection or indecision

% of Total Column:

Shows what percentage each part contributes to the whole candle

All percentages always add up to 100%

Helps identify if price spent more time in wicks or body

Move % Column:

Calculated from the opening price

Shows actual volatility during the candle period

Example: 0.5% body with 3% total candle = high volatility but little net movement

Trading Applications

1. Rejection Analysis:

Long upper wicks at resistance = strong selling pressure

Long lower wicks at support = strong buying pressure

Wick-to-body ratios above 2:1 suggest significant rejection

2. Volatility Assessment:

Compare body move % to whole candle move %

Large difference indicates choppy price action

Small difference indicates trending movement

3. Candle Patterns:

Identify doji, hammer, shooting star patterns quantitatively

Measure strength of pin bars and rejection candles

Compare current candle structure to historical patterns

4. Market Sentiment:

Body % > 70% = strong directional movement

Wick % > 60% = indecision and rejection

Balanced distribution = consolidation

Settings & Customization

Table position can be modified in the code (top_right, top_left, bottom_right, bottom_left)

Colors can be adjusted for different components

Text size can be changed (size.small, size.normal, size.large)

Decimal precision can be modified in the str.tostring() functions

Best Practices

Use on higher timeframes (15m+) for more reliable signals

Combine with support/resistance levels for context

Look for extreme ratios (>3:1) for high-probability setups

Monitor the move % to gauge true volatility vs. net movement

Technical Details

Written in Pine Script v5

Zero division protection built-in

Handles all edge cases (gaps, doji, extreme wicks)

Lightweight and efficient (minimal CPU usage)

ProCrypto OI Candles (auto symbol) — by ruben_procryptoProCrypto OI Candles (Auto Symbol) visualizes Open Interest in a clear and intuitive way by converting OI data into candles and a smooth trendline.

The script automatically detects the correct OI symbol based on the chart you are viewing, so there is no need to manually change OI tickers when switching between assets.

🔹 Key Features

Automatic Symbol Detection

The indicator automatically selects the appropriate Open Interest data source for the asset on your chart (BTC, SOL, ADA, DOGE, etc.).

OI Candles

Open Interest is displayed as candles to show whether market participation is increasing or decreasing on each bar.

Multi-exchange Support

Users can choose OI data from Binance, Bybit, or OKX. Any combination is supported.

Smooth OI Trendline

An optional EMA-based OI line provides a clear view of the underlying trend in trader activity.

Delta Bars (optional)

Highlights whether Open Interest expanded or contracted within the candle.

🔹 How to Interpret OI

Typical relationships between price and OI:

Price ↑ + OI ↑ → Trend continuation likely

New positions entering the market.

Price ↑ + OI ↓ → Short squeeze / weak move

Shorts closing, not new longs opening.

Price ↓ + OI ↑ → New shorts entering

Often signals bearish pressure.

Price ↓ + OI ↓ → Longs closing

Can indicate capitulation or consolidation.

These concepts help traders understand the strength or weakness behind a price move.

🔹 Inputs

Choose exchange(s) for OI data

Adjust candle opacity

Enable/disable OI line

Smoothing length for OI line

Optional delta bars

Range lookback for line offset

All settings are customizable to suit different styles of analysis.

🔹 Notes

Some assets may not have Open Interest data available on all exchanges.

The indicator uses standard TradingView data sources via request.security().

No trading signals are generated; this script is a visualization tool only.

🔹 Author

Created by ruben_procrypto for traders who analyze liquidity, Open Interest, and market participation.

Percent Change Histogram + MACandle Percent Move Columns with Optional Moving Average

Description:

This indicator calculates the percentage move of each candle over a specified number of bars and displays it as upward-facing columns, regardless of the candle direction. Each column is color-coded based on the candle’s direction—green for bullish, red for bearish. An optional moving average can be overlaid on the percentage values to help visualize trends and smooth out volatility.

Features:

Shows each candle’s percentage move as a column facing upward.

Columns are colored according to candle direction.

Adjustable input for the number of bars used in calculation.

Optional moving average overlay that can be added or removed.

Helps quickly assess volatility and trend strength in percentage terms.

Use Case:

Ideal for traders who want a clear visual representation of individual candle movements in percentage terms, making it easier to spot trends, pullbacks, and volatility patterns across different timeframes.

Pure xATR ProUncover the hidden rhythm of the market with Pure xATR Pro. This indicator is designed for serious traders who need to understand "Price Extension". It calculates the precise distance between the price and the baseline Moving Average (MA) relative to market volatility (ATR). Instead of guessing top and bottom, visualize exactly where the price stands in the cycle—from extreme panic selling to euphoric profit-taking.

Key Features:

4-Stage Market Zoning System:

Panic Zone (Oversold): Identifies extreme price drops (statistically rare deviations). Often presents high-reward mean reversion opportunities.

Buy Zone (Entry): The sweet spot for trend initiation.

Hold / Winner Zone: Detects strong momentum. Keeps you in the trade while the trend is healthy (Ride the trend).

Profit Taking Zone (Overbought): signals when the price is statistically overextended and liable to pullback.

Adaptive Volatility Logic:

Includes a dynamic algorithm that analyzes historical volatility (Lookback Period) to automatically adjust Overbought/Oversold percentiles, adapting to changing market conditions.

Professional Dashboard:

Real-time Status: Displays current Zone, Volatility State (Breakout/Normal), and Actionable Advice.

Risk Management: Auto-calculates Dynamic Stop Loss (based on Supertrend, ATR, or MA) and Fixed % Risk.

Multi-Level Targets: Automatically projects 3 profit targets (TP) based on ATR multiples.

Clean & Customizable Visuals:

Smart Highlighting: Background colors automatically highlight key zones (Panic/Buy/Hold/Profit).

Style Control: Full color customization available directly in the "Style" tab for a clutter-free input menu.

------------------

ค้นพบจังหวะที่แท้จริงของตลาดด้วย Pure xATR Pro อินดิเคเตอร์ระดับมืออาชีพที่ออกแบบมาเพื่อวิเคราะห์ "ระยะการยืดตัวของราคา" (Price Extension) โดยคำนวณระยะห่างระหว่างราคากับเส้นค่าเฉลี่ย (MA) เทียบกับความผันผวน (ATR) ช่วยให้คุณเห็นภาพชัดเจนว่าราคา ณ ปัจจุบันอยู่ในสถานะใด ตั้งแต่จุดที่คนเทขายด้วยความตกใจ (Panic) ไปจนถึงจุดที่ราคาแพงเกินไปและควรขายทำกำไร

ฟีเจอร์หลัก (Key Features):

ระบบแบ่งโซนตลาด 4 ระดับ (4-Stage Zoning):

Panic Zone (โซนของถูก/Oversold): จับจังหวะที่ราคาดิ่งลงแรงผิดปกติ ซึ่งมักเป็นจุดกลับตัวที่ให้ผลตอบแทนสูง (High Reward)

Buy Zone (โซนสะสม): จุดเริ่มต้นของเทรนด์ เป็นระยะปลอดภัยในการเข้าออเดอร์

Hold / Winner Zone (โซนรันเทรนด์): แยกแยะช่วงที่เทรนด์แข็งแกร่ง ให้คุณ "ถือสถานะต่อ" (Let Profit Run) ไม่ขายหมู

Profit Taking Zone (โซนขายทำกำไร): แจ้งเตือนเมื่อราคาวิ่งไปไกลเกินค่าเฉลี่ยทางสถิติ (Overextended) เพื่อพิจารณาขาย

ระบบปรับตัวตามความผันผวน (Adaptive Logic):

อัลกอริทึมอัจฉริยะที่คำนวณค่า Percentile ย้อนหลัง เพื่อปรับระดับ Overbought/Oversold ให้เหมาะสมกับสภาวะตลาดที่เปลี่ยนไปโดยอัตโนมัติ

หน้าปัดสถานะครบวงจร (Professional Dashboard):

แสดงสถานะปัจจุบัน (Action), ระดับความผันผวน, และคำแนะนำแบบ Real-time

Risk Management: คำนวณจุด Stop Loss ให้อัตโนมัติ (เลือกสูตรได้: Supertrend, ATR, หรือ MA)

Target Projection: คำนวณเป้าหมายทำกำไร (TP) ให้ล่วงหน้า 3 ระดับตามระยะ ATR

กราฟสะอาดตา ปรับแต่งง่าย (Clean Visuals):

Smart Highlight: ไฮไลท์สีพื้นหลังตามโซนต่างๆ อัตโนมัติ (Panic/Buy/Hold/Profit) ทำให้ดูเทรนด์ง่ายเพียงกวาดตา

Customizable: ปรับแต่งสีและความโปร่งใสได้อิสระผ่านแถบ "Style" เพื่อกราฟที่ดูเป็นระเบียบและไม่รกสายตา

Volatility Radar [upslidedown]💎 Overview

Volatility Radar visualizes extreme volatility conditions in a clean, intuitive oscillator format.

Unlike traditional momentum oscillators, it transforms average true range (ATR) behavior into a directional volatility structure, making it easier to spot moments when markets may be shifting into expansion, compression, or potential pivot zones.

💎 How to Use

The oscillator highlights moments when the internal volatility condition becomes active as well as when that condition breaks. These events may coincide with structural turning points, breakout conditions, or volatility expansions. While not a prediction tool, Volatility Radar helps traders identify moments worth paying closer attention to.

💎 Signal Markers

■ Square icons on top/bottom identify when the Volatility Radar condition is ACTIVE

▲▼ Triangle icons on top/bottom identify when the Volatility Radar condition BREAKS

📌 Chart Example:

💎 Oscillator Trends

One of the core features of Volatility Radar is its ability to highlight positive or negative volatility trends. The oscillator automatically colors its components to reflect uptrending vs. downtrending volatility structure, making trend context easier to interpret at a glance.

📌 Chart Example:

💎 Histogram Trends

For users who prefer a more compact or traditional visual style, Volatility Radar includes an optional histogram display mode. This mode provides a clean representation of the detected trend and can be helpful for validating price-action concepts within the broader volatility context.

📌 Chart Example:

💎 Volatility Moving Average

The yellow moving average line offers a volatility moving average that can aid in determining longer term trend strength.

Interpret the trend direction by observing whether the average is increasing/decreasing or above/below the zero line.

Reversals may be observed when values move into oversold territories.

Trend continuation may occur during periods when the average is near the zero line.

Evaluate opportunities when the moving average is "touched" or "pinged" by the radar line (setting available to highlight these crosses).

📌 Chart Example:

💎 Backtesting Support

Volatility Radar outputs external signals designed for use with automated backtesting on TradingView. It integrates with @jason5480’s open-source Template Trailing Strategy and its supporting signal libraries.

FX OSINT - Institutional Midnight Intelligence For ForexFX OSINT — Institutional Midnight Intelligence For Forex

See Your FX Charts Like an Intelligence Briefing, Not a Guess

If you’ve ever stared at EURUSD or GBPJPY and thought:

Where is the real liquidity?

Is this move sponsored by smart money or just noise?

Am I buying into premium or discount?

…then FX OSINT is designed for you.

FX OSINT (Forex Open Source Intelligence) treats the FX market the way an analyst treats an investigation:

Collect open‑source signals from price, time, and volatility.

Map out liquidity, structure, and sessions in a repeatable way.

Present them in a clean, non‑cluttered dashboard so you can read context quickly.

No rainbow spaghetti. No 12 indicators stacked on top of each other. Just structured information, midnight visuals, and a clear read on what the market is doing right now.

Why FX OSINT Exists

Many FX traders run into the same problems:

Overloaded charts – multiple indicators fighting for space, none talking to each other.

Signals with no context – arrows that ignore structure, sessions, and liquidity.

Tools not tuned for FX – generic indicators that don’t care what pair you are on.

FX OSINT brings this together into one FX‑focused framework that:

Understands structure : BOS/CHOCH, swings, and trend across multiple timeframes.

Respects liquidity : sweeps, order blocks, and FVGs with controlled visibility.

Reads volatility & ADR : how far today’s range has developed.

Knows the clock : London, New York, and key killzones.

Scores confluence : a 0–100 engine that summarizes how much is lining up.

FX OSINT is built for traders who want structured, institutional‑style logic with a disciplined, midnight‑themed UI —not flashing buy/sell buttons.

1. Midnight Dashboard — Top‑Right Intelligence Panel

This panel acts as your compact “situation room”:

CONFLUENCE — 0–100 score blending trend alignment, volatility regime, sessions, liquidity events, order blocks, FVGs, and ADR context.

REGIME — Low / Building / Normal / Expansion / Extreme, driven by ATR relationships, so you know if you’re in chop, trend, or expansion.

HTF / MTF / LTF TREND — Higher‑, medium‑, and current‑timeframe bias in one place, so you see if you are trading with or against the larger flow.

ADR USED — How much of today’s typical range has already been consumed in percentage terms.

PIP VALUE — Approximate pip size per pair, including JPY‑style pairs.

Everything is bold, legible, and color‑coded, but the layout stays minimal so you can:

Look once → understand the context.

2. Structure, BOS, CHOCH — Smart‑Money‑Style Skeleton

FX OSINT tracks swing highs and lows, then shows how structure evolves:

Trend logic based on evolving swings, not just a moving average cross.

BOS (Break of Structure) when price expands in the direction of trend.

CHOCH (Change of Character) when behavior flips and the market structure changes.

Labels are selective, not spammy . You don’t get a tag on every minor wiggle—only when structure meaningfully shifts, so it’s easier to answer:

"Are we continuing the current leg, or did something actually change here?"

3. Liquidity Sweeps, Order Blocks & FVGs — The OSINT Layer

FX OSINT treats liquidity as a key information layer:

Liquidity sweeps — Detects when price spikes through recent highs/lows and then snaps back, flagging potential stop runs.

Order blocks — The last opposite candle before a displacement move, drawn as controlled boxes with limited lifespan to avoid clutter.

Fair Value Gaps (FVGs) — Three‑candle imbalances rendered as precise zones with a cap on how many can exist at once.

Under the hood, boxes are managed so your chart does not become a wall of old zones:

// Draw Order Blocks with overlap prevention

if isBullishOB and showOrderBlocks

if array.size(obBoxes) >= maxBoxes

oldBox = array.shift(obBoxes)

box.delete(oldBox)

newBox = box.new(bar_index , low , bar_index + obvLength, high ,

border_color = bullColor, bgcolor = bullColorTransp,

border_width = 2, extend = extend.none)

array.push(obBoxes, newBox)

Box limits keep the number of zones under control.

Borders and transparency are tuned so you still see price clearly.

You end up with a curated liquidity map , rather than a chart buried under every level price has ever touched.

4. Volatility, ADR & Sessions — Time and Range Intelligence

FX OSINT runs a Volatility Regime Analyzer and an ADR engine in the background:

Volatility regime — Five states (Low → Extreme) derived from fast vs. slow ATR.

ADR bands — Daily high/mid/low projected from the current daily open.

ADR used % — How far today’s move has traveled relative to its typical range.

On the time side:

Asia, London, New York sessions are softly highlighted with a single active background to avoid overlapping colors.

Killzones (e.g., London and New York opens) can be emphasized when you want to focus on where significant moves often begin.

Together, this helps you answer:

"What time is it in the trading day?"

"How stretched are we?"

"Is expansion just starting, or are we late to the move?"

5. ICT‑Style Add‑Ons — BOS/CHOCH, Premium/Discount, and Confluence

For modern FX / ICT‑inspired workflows, FX OSINT includes:

BOS / CHOCH labels — Clear structural shifts based on swings.

Premium / Discount zones — 25%, 50%, 75% levels of the daily range, so you know if you are buying discount in an uptrend or selling premium in a downtrend.

Confluence score — A single number summarizing how many conditions line up in the current context.

Instead of replacing your plan, FX OSINT compresses your checklist into the chart:

Structure

Liquidity

Session / Time

Volatility / ADR

Higher‑timeframe alignment

When these agree, the dashboard reflects it. When they don’t, it stays neutral and lets you see the conflict.

How To Use FX OSINT

FX OSINT is not a signal bot. It is an information engine that organizes context so you can apply your own plan.

A typical workflow might look like:

Start on higher timeframes (e.g., H4/D1) to form directional bias from structure, volatility regime, and ADR context.

Move to intraday timeframes (e.g., M15/H1) around your chosen sessions (London and/or New York).

Look for confluence :

HTF / MTF / LTF trends aligned.

Price in discount for longs or premium for shorts.

Recent liquidity sweep into a meaningful OB or FVG.

Confluence score at or above a level you consider significant.

Then refine entries using BOS/CHOCH on lower timeframes according to your own risk and execution rules.

FX OSINT aims to make sure you do not enter a trade without seeing:

Where you are in the day (ADR and sessions).

Where you are in the volatility cycle (regime).

Who currently appears in control (structure and trend).

Which liquidity was just targeted (sweeps and zones).

Design Choices and Scope

FX OSINT was designed around a few clear constraints:

FX‑focused — Logic and filters tuned for FX majors, minors, exotics, and metals. It is intended for FX markets, not for every possible asset class.

Open‑source — The full Pine Script code is available so you can read it, learn from it, and adapt it to your own workflow if needed.

Clear themes — Two main visual styles (e.g., dark institutional “midnight” and a lighter accent variant) with a focus on readability, not visual noise.

Chart‑friendly — Panels use fixed areas, session highlights avoid overlapping, and boxes are capped/pruned so the chart remains usable.

FX OSINT is for only Forex pairs, not anything else!

Hope you enjoyed and remember your Open Source Intelligence Matters 😉!

-officialjackofalltrades

Trend Tracer [AlgoAlpha]🟠 OVERVIEW

This tool builds a two-stage trend model that reacts to structure shifts while also showing how strong or weak the move is. It uses a mid-price band (from the highest high and lowest low over a lookback) and applies two Supertrend passes on top of it. The first pass smoothens the basis. The second pass refines that direction and produces the final trail used for signals. A gradient fill between the two trails uses RSI of price-to-trail distance to show when price is stretched or cooling off. The aim is to give traders a simple way to read trend alignment, pressure, and early turns without guessing.

🟠 CONCEPTS

The script starts with a mid-range basis. This is the average of the rolling highest high and lowest low. It acts as a stable structure reference instead of raw close or typical price. From there, two Supertrend layers are applied:

• The first Supertrend uses a shorter ATR period and lower factor. It reacts faster and sets the main regime.

• The second Supertrend uses a slightly longer ATR and higher factor. It filters noise, waits for confirmed continuation, and generates the signal line.

The interaction between these trails matters. The outer Supertrend provides context by defining the broader regime. The inner Supertrend provides timing by flipping earlier and marking possible shifts. The gradient fill uses RSI of (close − supertrend value) to display when price stretches away from the trail. This shows strength, exhaustion, or compression within the trend.

🟠 FEATURES

Bullish and bearish flip markers placed at recent highs/lows

Rejection signals off the trend tracer line

Alerts for bullish and bearish trend changes

🟠 USAGE

Setup : Add the script to your chart. Timeframe is flexible; lower timeframes show more flips while higher ones give cleaner swings. Adjust Length to change how wide the basis range is. Use the two ATR settings and factors to match the volatility of the market you trade.

Read the chart : When the refined trail (stv_) sits above price the regime is bearish; when below, it is bullish. The wide trail (stv) confirms the larger move. Watch the gradient fill: darker colors appear when price is stretched from the trail and lighter colors appear when the move is weakening. Flip markers ▲ or ▼ highlight the first clean shift of the refined trail.

Settings that matter : Increasing the Main Factor slows main-trend flips and filters chop. Increasing the Signal Factor delays the timing trail but reduces noise. Shortening Length makes the basis more reactive. ATR periods change how sensitive each Supertrend pass is to volatility.

ZynIQ Pullback Zones Lite - (Lite Pack)Overview

ZynIQ Pullback Zones Lite identifies dynamic EMA-based retracement areas inside trending markets. These zones highlight where price is most likely to pull back before continuing in the dominant direction. The tool is intentionally simple, visual, and designed to complement the rest of the ZynIQ Lite package without adding noise or complexity.

This is a contextual tool — ideal for timing continuation entries, filtering counter-trend trades, and improving overall trend structure awareness.

Key Features

• Dynamic pullback zones using profile-based EMA + ATR

• Smart trend detection with optional HTF confirmation

• Fresh-touch recognition for potential continuation setups

• Clean ZynIQ-themed visuals (teal/fuchsia zones)

• Lightweight chart footprint for intraday and swing traders

• ZynIQ Lite HUD with profile, trend and HTF status

• Moveable watermark for clear branding on streams and screenshots

• Alerts for long and short pullback opportunities

Use Cases

• Identifying pullback areas within established trends

• Avoiding early entries during retracements

• Timing continuation setups more cleanly

• Filtering false breakouts and counter-trend traps

• Combining with breakout or momentum tools for confluence

• Works on crypto, forex, indices and commodities

Notes

This tool provides structure and context for pullback-based trend trading.

It is not a standalone strategy and should be combined with your preferred confirmations and risk management rules.

Bubbles + Clusters + SweepsIndicator For Bubbles + Clusters + Sweeps

✔ Volume bubbles

✔ Delta coloring (green/red intensity)

✔ Auto supply/demand zones

✔ Volume-profile style blocks inside zones

✔ Liquidity sweep markers

✔ Box drawings extending until filled

✔ Optional bubble filters (min-volume threshold)

Compression / ExpansionI created this Indicator to warn of compression and expansion so I could find the best area to trade I use it In conjunction with VWAP works on any timeframe and any asset where there is Volume

The Indicator produces a Letter C at the Start of Compression and a Letter E at the Start of Expansion you can change the settings to your liking On the chart my Expansion is in Red and compression is is Blue use In Conjunction with your favorite Indicators for Confluence

Average Candle SizeI created this indicator because I couldn't find a simple tool that calculates just the average candle size without additional complexity. Built for traders who want a straightforward volatility measure they can fully understand. How it works:

1. Calculate high-low for each candle

2. Sum all results

3. Divide by the total number of candles

Simple math to get the average candle size of the period specified in Length.

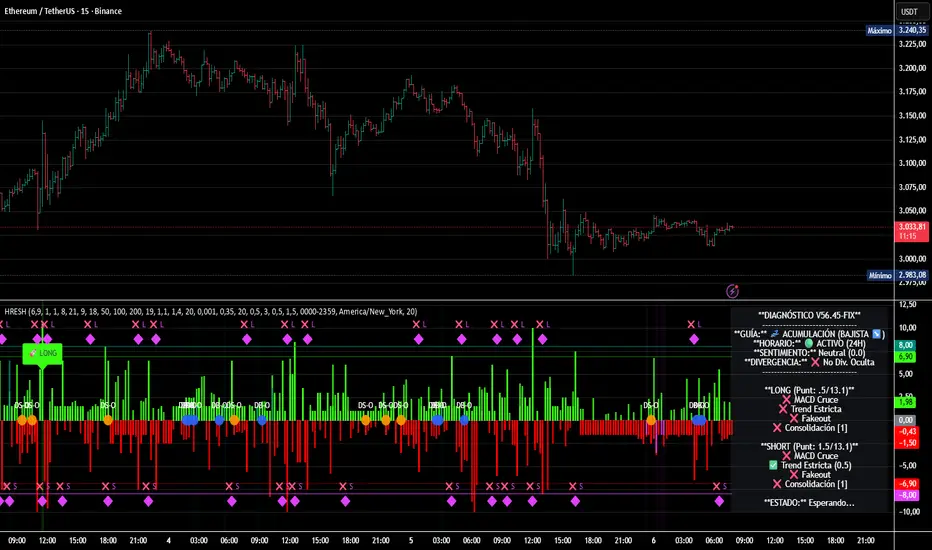

HRESH Pro Dashboard 🦅 HRESH (The Beast) — BTC Specialized System V56.45

This is the fully unlocked, 24-hour version of the HRESH System. It has been mathematically tuned and calibrated specifically for Bitcoin volatility.

🛑 CRITICAL RULES FOR USE (PLEASE READ):

1. STRICT ASSET SELECTION:

BTC (Bitcoin): This is the primary asset for this indicator.

ETH (Ethereum): Allowed ONLY on the 15-Minute timeframe.

❌ DO NOT USE on other assets (Forex, Altcoins, Stocks). The internal logic is unique to BTC/ETH structure.

2. TIMEFRAME STRATEGY:

⏱️ 1 MINUTE (Daily Operations): Use this for intraday scalping.

⏱️ 15 MINUTES (Sniper Mode): Use this for Swing Trading. Expect only 1 or 2 high-precision signals PER MONTH. This mode requires extreme patience.

❌ OTHER TIMEFRAMES: Do not operate. The calculations will be incorrect.

🌍 TRADING SESSIONS & VOLUME: While this version functions 24 hours a day, I strongly advise AGAINST trading during low-volume hours (such as late Asian session or weekends).

✅ RECOMMENDED: London & New York Sessions.

⚠️ HIGH RISK: Trading off-hours increases the risk of market manipulation and fakeouts.

🔴🔴🔴 RISK DISCLAIMER & WARNING 🔴🔴🔴

YOU ARE RESPONSIBLE FOR YOUR CAPITAL. This indicator is a powerful analytical tool, but it does not guarantee profits.

MARKET RISK: Trading cryptocurrency involves substantial risk of loss and is not suitable for every investor.

NO FINANCIAL ADVICE: Always manage your risk properly. If you trade outside the recommended hours or assets, you accept 100% of the risk.

Trade wisely and respect the algorithm.

By Lendrush Margaryan