MACD Crossover + AlertMACD Proximity & Crossover Alert Script

This script is designed to help traders stay ahead of MACD crossovers by providing:

Early alerts when the MACD and Signal lines are getting close (within a customizable threshold)

Instant alerts when a bullish or bearish crossover occurs

Whether you're swing trading or scalping, this tool gives you advanced notice to prepare — and a confirmation signal to act on. It works on any timeframe and helps avoid late entries by alerting you when momentum is shifting.

Features:

Customizable MACD settings (fast, slow, signal length)

Adjustable "proximity" threshold

Visual background highlight when lines are close

Built-in alert conditions for:

MACD crossing above Signal (bullish)

MACD crossing below Signal (bearish)

MACD and Signal getting close (early warning)

Perfect for traders who want a heads-up before momentum shifts — not just a reaction afterward.

Dao động trung tâm

Institutional Quantum Momentum Impulse [BullByte]## Overview

The Institutional Quantum Momentum Impulse (IQMI) is a sophisticated momentum oscillator designed to detect institutional-level trend strength, volatility conditions, and market regime shifts. It combines multiple advanced technical concepts, including:

- Quantum Momentum Engine (Hilbert Transform + MACD Divergence + Stochastic Energy)

- Fractal Volatility Scoring (GARCH + Keltner-based volatility)

- Dynamic Adaptive Bands (Self-adjusting thresholds based on efficiency)

- Market Phase Detection (Volume + Momentum alignment)

- Liquidity & Cumulative Delta Analysis

The indicator provides a Z-score normalized momentum reading, making it ideal for mean-reversion and trend-following strategies.

---

## Key Features

### 1. Quantum Momentum Core

- Combines Hilbert Transform, MACD divergence, and Stochastic Energy into a single composite momentum score.

- Normalized using a Z-score for statistical significance.

- Smoothed with EMA/WMA/HMA for cleaner signals.

### 2. Dynamic Adaptive Bands

- Upper/Lower bands adjust based on volatility and efficiency ratio .

- Acts as overbought/oversold zones when momentum reaches extremes.

### 3. Market Phase Detection

- Identifies bullish , bearish , or neutral phases using:

- Volume-Weighted MA alignment

- Fractal momentum extremes

### 4. Volatility & Liquidity Filters

- Fractal Volatility Score (0-100 scale) shows market instability.

- Liquidity Check ensures trades are taken in favorable spread conditions.

### 5. Dashboard & Visuals

- Real-time dashboard with key metrics:

- Momentum strength, volatility, efficiency, cumulative delta, and market regime.

- Gradient coloring for intuitive momentum visualization .

---

## Best Trade Setups

### 1. Trend-Following Entries

- Signal :

- QM crosses above zero + Market Phase = Bullish + ADX > 25

- Cumulative Delta rising (buying pressure)

- Confirmation :

- Efficiency > 0.5 (strong momentum quality)

- Liquidity = High (tight spreads)

### 2. Mean-Reversion Entries

- Signal :

- QM touches upper band + Volatility expanding

- Market Regime = Ranging (ADX < 25)

- Confirmation :

- Efficiency < 0.3 (weak momentum follow-through)

- Cumulative Delta divergence (price high but delta declining)

### 3. Breakout Confirmation

- Signal :

- QM holds above zero after a pullback

- Market Phase shifts to Bullish/Bearish

- Confirmation :

- Volatility rising (expansion phase)

- Liquidity remains high

---

## Recommended Timeframes

- Intraday (5M - 1H): Works well for scalping & swing trades.

- Swing Trading (4H - Daily): Best for trend-following setups.

- Position Trading (Weekly+): Useful for macro trend confirmation.

---

## Input Customization

- Resonance Factor (1.0 - 3.618 ): Adjusts MACD divergence sensitivity.

- Entropy Filter (0.382/0.50/0.618) : Controls stochastic damping.

- Smoothing Type (EMA/WMA/HMA) : Changes momentum responsiveness.

- Normalization Period : Adjusts Z-score lookback.

---

The IQMI is a professional-grade momentum indicator that combines institutional-level concepts into a single, easy-to-read oscillator. It works across all markets (stocks, forex, crypto) and is ideal for traders who want:

✅ Early trend detection

✅ Volatility-adjusted signals

✅ Institutional liquidity insights

✅ Clear dashboard for quick analysis

Try it on TradingView and enhance your trading edge! 🚀

Happy Trading!

- BullByte

BB Breakout + Momentum Squeeze [Strategy]This Strategy is Based on 3 free indicators

- Bollinger Bands Breakout Oscillator: Link

- TTM Squeeze Pro: Link

- Rolling ATR Bands: Link

Bollinger Bands Breakout Oscillator - This tool shows how strong a market trend is by measuring how often prices move outside their normal Bollinger bands range. It helps you see whether prices are strongly moving in one direction or just moving sideways. By looking at how much and how frequently prices push beyond their typical boundaries, you can identify which direction the market is heading over your selected time period.

TM Squeeze Pro - This is a custom version of the TTM Squeeze indicator.

It's designed to help traders spot consolidation phases in the market (when price is coiling or "squeezing") and to catch breakouts early when volatility returns. The logic is based on the relationship between Bollinger Bands and Keltner Channels, combined with a momentum oscillator to show direction and strength.

Rolling ATR Bands - This indicator combines volatility bands (ATR) with momentum and trend signals to show where the market might be breaking out, retesting, or trending. It's highly visual and helpful for traders looking to time entries/exits during trending or volatile moves.

Logic Of the Strategy:

We are going to use the Bollinger Bands Breakout to determine the direction of the market. Than check the Volatility of the price by looking at the TTM Squeeze indicator. And use the ATR Bands to determine dynamic Stop Losses and based on the calculate the Take Profit targets and quantity for each position dynamically.

For the Long Setup:

1. We need to see the that Bull Power (Green line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

For the Short Setup:

1. We need to see the that Bear Power (Red line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

Stop Loss is determined by the Lower ATR Band (for the Long entry) and Upper ATR Band (For the Short entry)

Take Profit is 1:1.5 risk reward ration, which means if the Stop loss is 1% the TP target will be 1.5%

Move stop Loss to Breakeven: If the price will go in the direction of the trade for at least half of the Risk Reward target then the stop will automatically be adjusted to the entry price. For Example: the Stop Loss is 1%, the price has move at least 0.5% in the direction of your trade and that will move the Stop Loss level to the Entry point.

You can Adjust the parameters for each indicator used in that script and also adjust the Risk and Money management block to see how the PnL will change.

Log Regression Oscillator Channel [BigBeluga]

This unique overlay tool blends logarithmic trend analysis with dynamic oscillator behavior. It projects RSI, MFI, or Stochastic lines directly into a log regression channel on the price chart — offering an intuitive way to detect overbought/oversold momentum within the broader price structure.

🔵Key Features:

Logarithmic Regression Channel:

➣ Draws a trend-based channel using logarithmic regression, adapting to price growth curvature over time.

➣ Features upper, lower, and optional midline boundaries to visualize trend flow and range extremes.

Oscillator Overlay (RSI / MFI / Stochastic):

➣ Projects your chosen oscillator inside the channel using dynamic polylines.

➣ Allows switching between RSI, Money Flow Index, or Stochastic for versatile momentum insight.

Threshold-Based Scaling:

➣ The top and bottom of the channel represent traditional oscillator thresholds (e.g., RSI 70/30).

➣ Users can modify the scale in settings to customize what "overbought" or "oversold" means visually.

Signal Line Integration:

➣ Adds a yellow moving average (signal line) for smoother confirmation of oscillator turns.

➣ Helps identify divergence, momentum shifts, and fakeouts with better clarity.

Live Oscillator Readout:

➣ Displays the real-time oscillator value at the right edge of the chart.

➣ Ensures traders stay aware of current momentum levels without switching panels.

🔵Usage:

Momentum Context:

➣ When the oscillator touches the upper regression band, it may signal local overbought pressure.

➣ Touching the lower band may indicate oversold conditions within the current log trend.

Divergence Detection:

➣ Use the oscillator’s behavior relative to the channel slope to spot divergence from price.

➣ For example, RSI rising inside a falling channel can flag early trend shifts.

Trend-Sensitive Entries:

➣ Combine oscillator signals with log channel direction to filter trades in trend alignment.

➣ Signal line crossovers inside the channel act as early warning for momentum turns.

The Log Regression Oscillator Channel transforms how traders view classic momentum tools. By embedding oscillators into a logarithmic trend structure, it offers unmatched clarity on momentum positioning relative to price expansion. Ideal for swing traders, mean-reverters, or trend followers looking to sharpen entries and exits with style.

Rolling ATR Momentum

Rolling ATR Momentum Indicator – User Manual

---

🔍 Overview

The Rolling ATR Momentum Indicator is a simple yet powerful tool designed to detect shifts in market volatility. It compares the current Average True Range (ATR) with the ATR from a previous point in time to measure how market volatility is changing.

This indicator is especially useful for:

- Spotting the beginning or fading of a momentum phase

- Filtering out low-volatility market conditions

- Enhancing timing for entries and exits in trending or breakout trades

---

📊 Key Components

✅ ATR Delta (Rolling)

- Definition: `ATR Delta = Current ATR - Past ATR`

- Inputs:

- ATR Period (default: 14): The base ATR calculation window

- Lookback Period (default: 5): How many bars ago to compare ATR

- Interpretation:

- Positive ATR Delta (Green Line): Market volatility is increasing

- Negative ATR Delta (Red Line): Market volatility is decreasing

📈 Zero Line

- A horizontal baseline at zero helps you easily see when ATR momentum shifts from negative to positive (or vice versa).

🟩/🟥 Background Color

- Green Background: ATR Delta is positive (rising volatility)

- Red Background: ATR Delta is negative (falling volatility)

🔵 Optional: ATR Reference Lines

- You can optionally display raw Current ATR and Past ATR by changing their visibility settings.

---

✅ How to Use It

Entry Timing (Futures/Options)

- Use ATR Delta as a filter:

- Only take trades when ATR Delta is positive → confirms momentum is building

- Avoid trades when ATR Delta is negative → market might be slow, sideways, or losing steam

Breakout Anticipation

- A rising ATR Delta after a tight range or consolidation can suggest that a breakout is underway

Stop-loss Strategy

- Use high ATR periods for wider stops (to avoid noise)

- Use low ATR periods for tighter stops or skip trading

---

🧠 Pro Tips

- This indicator doesn’t predict direction—combine with trend or price structure tools (like EMA, PPMA, candlesticks)

- Works best in trending or breakout environments

- Add it to multi-timeframe layouts to see volatility buildup on higher timeframes

---

⚙️ Settings

| Parameter | Description |

|----------|-------------|

| ATR Period | Length of the ATR calculation (default 14) |

| Lookback Period | How many bars back to compare ATR values |

---

🧭 Best For:

- Index futures (Nifty, BankNifty)

- Option buyers needing volatility confirmation

- Intraday & swing traders looking to trade momentum setups

---

Use the Rolling ATR Momentum indicator as your volatility radar—simple, clean, and highly effective for staying on the right side of market energy.

End of Manual

Rolling ATR Momentum - EnhancedATR Rolling Momentum Indicator – User Manual

---

🔍 Overview

The ATR Rolling Momentum Indicator is a dynamic volatility tool built on the Average True Range (ATR). It not only tracks increasing or decreasing momentum but also provides early warnings and confirmation signals for potential breakout moves. It’s especially powerful for futures and options traders looking to align with expanding price action.

---

📊 Core Components

✅ ATR Delta (Rolling ATR)

- Definition: Difference between current ATR and past ATR (user-defined lookback).

- Use: Tells whether volatility is expanding (positive delta) or contracting (negative delta).

- Visual: Green line for rising momentum, red for declining.

🟣 ATR Delta Slope

- Definition: Measures acceleration in momentum.

- Use: Helps identify early signs of breakout buildup.

- Visual: Purple line. Watch for slope turning up from below.

🟡 Volatility Squeeze (Yellow Dot)

- Definition: Current ATR is significantly lower than its 20-period average.

- Use: Indicates the market is coiling—possible breakout ahead.

🔼 Momentum Start (Green Triangle)

- Definition: ATR Delta slope turns from negative to positive.

- Use: Early warning to prepare for volatility expansion.

🔷 Breakout Confirmation (Blue Label Up)

- Definition: ATR Delta exceeds its high of the last 10 candles.

- Use: Confirms volatility breakout—trade opportunity if direction aligns.

🟩/🟥 Background Color

- Green Background: Momentum rising (positive ATR delta)

- Red Background: Momentum falling (negative ATR delta)

- Yellow Tint: Active squeeze zone

---

✅ How to Use It (Futures/Options Focus)

Step-by-Step:

1. Squeeze Detected (Yellow Dot) → Stay alert. Market is coiling.

2. Green Triangle Appears → Momentum is starting to rise.

3. Background Turns Green → Confirmed rising momentum.

4. Blue Label Appears → Confirmed breakout (enter trade if trend aligns).

Directional Bias:

- Use your main chart setup (price action, EMAs, trendlines, etc.) to decide direction (Call or Put, Long or Short).

- ATR Momentum only tells you how strong the move is—not which way.

---

⚙️ Inputs & Settings

- ATR Period: Default 14 (core volatility measure)

- Rolling Lookback: Used to calculate delta (default 5)

- Slope Length: Used to measure acceleration (default 3)

- Squeeze Factor: Default 0.8 — lower = more sensitive squeeze detection

- Breakout Lookback: Checks ATR delta against last X bars (default 10)

---

🧠 Pro Tips

- Works great when paired with EMA stacks, price structure, or breakout patterns.

- Avoid taking trades based only on squeeze or momentum—combine with chart confirmation.

- If background turns red after a breakout, it may be losing momentum—book partials or tighten stops.

---

🧭 Ideal For:

- Nifty/BankNifty Futures

- Option directional trades (call/put buying)

- Index scalping and momentum swing setups

---

Use this tool as your volatility compass—it won't tell you where to go, but it'll tell you when the wind is strong enough to move fast.

End of Manual

TriTrend Nexus[BullByte]TriTrend Nexus is a comprehensive market analysis tool that consolidates three well-established signals into a single, easy-to-read interface. It is designed to help traders quickly assess the market’s current condition and make more informed decisions about potential trend shifts.

Key Features and Functionality

Composite Signal System

Multi-Faceted Approach :

The indicator combines insights from three distinct market signals into one composite score. This approach provides a more holistic view of market conditions compared to relying on a single indicator.

Clear Classification :

Based on the composite score, TriTrend Nexus categorizes the market into:

Strong Signals : When all three underlying conditions are met, indicating a robust and established trend.

Early Signals : When two out of the three conditions are met, offering an early hint of a potential trend.

Neutral/Choppy : When conditions are ambiguous or conflicting, suggesting a lack of clear market direction.

Trend Qualifiers :

In addition to the composite score, the indicator subtly refines its signal by noting whether a trend is “Rising” or “Fading.” This further aids traders in understanding the momentum behind the signal.

Dynamic Signal Identification

Timely Alerts :

By analyzing the composite data in real time, the indicator quickly identifies when market conditions shift, offering early warning signals that help traders stay ahead of the market.

Adaptive Analysis :

The built-in signal assessment continuously monitors market changes. Whether the market is in the early stages of a move or firmly committed to a trend, TriTrend Nexus adapts its messaging to reflect the evolving conditions.

User-Friendly Dashboard

Integrated Display :

A customizable dashboard provides an at-a-glance summary of key metrics. Users can choose between a detailed view for comprehensive insights or a compact version for a streamlined experience.

Key Metrics Displayed :

Primary Signal : The overall market status, such as “Bullish Strong” or “Bearish Early.”

Composite Nexus Score : A numerical value representing the strength of the current market conditions.

Supporting Data : Essential values that help explain the current signal without overwhelming the trader.

Easy Interpretation :

The dashboard is designed with clarity in mind. Clear labeling and a consistent layout ensure that even traders new to composite indicators can quickly interpret the displayed information.

Visual Clarity and Aesthetic

Color-Coded Signals :

The indicator uses a vibrant color scheme to highlight market conditions:

Bright Green : Signifies a strong bullish trend.

Light Green : Indicates an emerging bullish trend.

Red : Represents a strong bearish trend.

Light Red/Pink : Denotes an early bearish signal.

Gray : Used when market conditions are neutral or choppy.

Graphical Enhancements :

The plotted oscillator visually reinforces the signal classifications with dynamic color transitions. Horizontal markers provide reference points to help traders easily compare the current readings against standard levels.

Customization Options

Adjustable Settings :

Traders can personalize the indicator by modifying input settings such as sensitivity thresholds and period lengths. This flexibility allows the tool to adapt to different market environments and trading styles.

Dashboard Flexibility :

The option to toggle between a full dashboard and a shorter version means that both novice and experienced traders can configure the display to best suit their needs. A more detailed dashboard offers extensive insights, while the compact mode provides a minimalist view for those who prefer simplicity.

Tailored User Experience :

With multiple adjustable parameters, users can fine-tune the indicator to respond precisely to their preferred timeframes and market conditions. This adaptability makes TriTrend Nexus a versatile tool for various trading strategies.

Benefits for Traders

Quick and Informed Decision-Making :

With a single glance at the dashboard and visual cues from the oscillator, traders can quickly gauge whether the market is poised for a strong move, is in the early stages of a trend, or is too volatile for clear signals. This helps in planning timely entries and exits.

Enhanced Market Insight :

By integrating multiple perspectives into one coherent score, the indicator filters out market noise and highlights the prevailing trend more reliably. This can be particularly useful during periods of market uncertainty.

Reduced Analysis Time:

The combination of clear, color-coded signals and an intuitive dashboard reduces the time spent analyzing various individual indicators, allowing traders to focus more on strategy execution.

Customization for Diverse Strategies :

The ability to adjust various input parameters and the dashboard layout ensures that traders can tailor the tool to fit their unique analysis style and market conditions, making it a versatile addition to any trading toolkit.

User-Friendly Interface :

Even for those who are not technically inclined, the clear visual design and straightforward signal descriptions make it easy to understand the current market situation without needing to interpret complex data.

Normalized Mean ReversionA script that can help identify potential mean reversion opportunities using a Simple Moving Average (SMA) as the mean. This script will plot the SMA and highlight when the price deviates significantly from it, which could indicate a potential mean reversion setup.

TTM Squeeze Momentum MTF [Cometreon]TTM Squeeze Momentum MTF combines the core logic of both the Squeeze Momentum by LazyBear and the TTM Squeeze by John Carter into a single, unified indicator. It offers a complete system to analyze the phase, direction, and strength of market movements.

Unlike the original versions, this indicator allows you to choose how to calculate the trend, select from 15 different types of moving averages, customize every parameter, and adapt the visual style to your trading preferences.

If you are looking for a powerful, flexible and highly configurable tool, this is the perfect choice for you.

🔷 New Features and Improvements

🟩 Unified System: Trend Detection + Visual Style

You can decide which logic to use for the trend via the "Show TTM Squeeze Trend" input:

✅ Enabled → Trend calculated using TTM Squeeze

❌ Disabled → Trend based on Squeeze Momentum

You can also customize the visual style of the indicator:

✅ Enable "Show Histogram" for a visual mode using Histogram, Area, or Column

❌ Disable it to display the classic LazyBear-style line

Everything updates automatically and dynamically based on your selection.

🟩 Full Customization

Every base parameter of the original indicator is now fully configurable: lengths, sources, moving average types, and more.

You can finally adapt the squeeze logic to your strategy — not the other way around.

🟩 Multi-MA Engine

Choose from 15 different Moving Averages for each part of the calculation:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

🟩 Dynamic Signal Line

Apply a moving average to the momentum for real-time cross signals, with full control over its length and type.

🟩 Multi-Timeframe & Multi-Ticker Support

You're no longer limited to the chart's current timeframe or ticker. Apply the squeeze to any symbol or timeframe without repainting.

🔷 Technical Details and Customizable Inputs

This indicator offers a fully modular structure with configurable parameters for every component:

1️⃣ Squeeze Momentum Settings – Choose the source, length, and type of moving average used to calculate the base momentum.

2️⃣ Trend Mode Selector – Toggle "Show TTM Squeeze Trend" to select the trend logic displayed on the chart:

✅ Enabled – Shows the trend based on TTM Squeeze (Bollinger Bands inside/outside Keltner Channel)

❌ Disabled – Displays the trend based on Squeeze Momentum logic

🔁 The moving average type for the Keltner Channel is handled automatically, so you don't need to select it manually, even if the custom input is disabled.

3️⃣ Signal Line – Toggle the Signal Line on the Squeeze Momentum. Select its length and MA type to generate visual cross signals.

4️⃣ Bollinger Bands – Configure the length, multiplier, source, and MA type used in the bands.

5️⃣ Keltner Channel – Adjust the length, multiplier, source, and MA type. You can also enable or disable the True Range option.

6️⃣ Advanced MA Parameters – Customize the parameters for advanced MAs (JMA, ALMA, FRAMA, VIDYA), including Phase, Power, Offset, Sigma, and Shift values.

7️⃣ Ticker & Input Source – Select the ticker and manage inputs for alternative chart types like Renko, Kagi, Line Break, and Point & Figure.

8️⃣ Style Settings – Choose how the squeeze is displayed:

Enable "Show Histogram" for Histogram, Area, or Column style

Disable it to show the classic LazyBear-style line

Use Reverse Color to invert line colors

Toggle Show Label to highlight Signal Line cross signals

Customize trend colors to suit your preferences

9️⃣ Multi-Timeframe Options - Timeframe – Use the squeeze on higher timeframes for stronger confirmation

🔟 Wait for Timeframe Closes -

✅ Enabled – Prevents multiple signals within the same candle

❌ Disabled – Displays the indicator smoothly without delay

🔧 Default Settings Reference

To replicate the default settings of the original indicators as they appear when first applied to the chart, use the following configurations:

🟩 TTM Squeeze (John Carter Style)

Squeeze

Length: 20

MA Type: SMA

Show TTM Squeeze Trend: Enabled

Bollinger Bands

Length: 20

Multiplier: 2.0

MA Type: SMA

Keltner Channel

Length: 20

Multiplier: 1.0

Use True Range: ON

MA Type: EMA

Style

Show Histogram: Enabled

Reverse Color: Enabled

🟩 Squeeze Momentum (LazyBear Style)

Squeeze

Length: 10

MA Type: SMA

Show TTM Squeeze Trend: Disabled

Bollinger Bands

Length: 20

Multiplier: 1.5

MA Type: SMA

Keltner Channel

Length: 10

Multiplier: 1.5

Use True Range: ON

MA Type: SMA

Style

Show Histogram: Disabled

Reverse Color: Disabled

⚠️ These values are intended as a starting point. The Cometreon indicator lets you fully customize every input to fit your trading style.

🔷 How to Use Squeeze Momentum Pro

🔍 Identifying Trends

Squeeze Momentum Pro supports two different methods for identifying the trend visually, each based on a distinct logic:

Squeeze Momentum Trend (LazyBear-style):

Displays 3 states based on the position of the Bollinger Bands relative to the Keltner Channel:

🔵 Blue = No Squeeze (BB outside KC and KC outside BB)

⚪️ White = Squeeze Active (BB fully inside KC)

⚫️ Gray = Neutral state (none of the above)

TTM Squeeze Trend (John Carter-style):

Calculates the difference in width between the Bollinger Bands and the Keltner Channel:

🟩 Green = BB width is greater than KC → potential expansion phase

🟥 Red = BB are tighter than KC → possible compression or pre-breakout

📈 Interpreting Signals

Depending on the active configuration, the indicator can provide various signals, including:

Trend color → Reflects the current compression/expansion state (based on selected mode)

Momentum value (above or below 0) → May indicate directional pressure

Signal Line cross → Can highlight momentum shifts

Color change in the momentum → May suggest a potential trend reversal

🛠 Integration with Other Tools

Squeeze Momentum Pro works well alongside other indicators to strengthen market context:

✅ Volume Profile / OBV – Helps confirm accumulation or distribution during squeezes

✅ RSI – Useful to detect divergence between momentum and price

✅ Moving Averages – Ideal for defining primary trend direction and filtering signals

☄️ If you find this indicator useful, leave a Boost to support its development!

Every piece of feedback helps improve the tool and deliver an even better trading experience.

🔥 Share your ideas or feature requests in the comments!

EREMA SignalsOverview

The EREMA Signals indicator is a specialized overlay tool designed to display precise buy and sell signals directly on your price chart. Working as a companion to the main Ehlers Reverse EMA indicator, it brings powerful momentum-based signals to your trading strategy without cluttering your chart with additional indicator panels.

Key Features

On-Chart Signal Visualization: Clear buy/sell arrows appear directly on the price chart

Dynamic Signal Positioning: Signals automatically adjust their distance from price using ATR for optimal visibility

Multiple Signal Types: Choose from three distinct signal generation methods

Clean Chart Interface: Displays only the essential signals, maintaining chart clarity

Signal Types

Zero Cross: Generates signals when the Ehlers Reverse EMA crosses above/below the zero line

MA Cross: Identifies when the Ehlers Reverse EMA crosses its own moving average

Zero & MA Cross: The strictest filter, requiring both zero line and MA crossovers for signal generation

How To Use

Setup

First add the main "Ehlers Reverse EMA" indicator to your chart

Then add this "EREMA Signals" indicator as an overlay

Configure both indicators with identical settings for alpha, MA type, and signal method

Reading Signals

Green Triangles (below price): Buy signals indicating potential upward momentum

Red Triangles (above price): Sell signals indicating potential downward momentum

Trading Applications

Trend Identification: Zero cross signals help identify changes in overall trend direction

Momentum Trading: MA cross signals can identify shorter-term momentum shifts

Confirmation Tool: Use alongside other technical indicators or price action strategies

Multiple Timeframe Analysis: Apply to different timeframes for more robust trading decisions

Best Practices

Consider using longer timeframes (4H, Daily) for more reliable signals

The combined "Zero & MA Cross" setting provides fewer but higher-quality signals

For tighter entries, use the "MA Cross" option in established trends

Adjust the Alpha parameter to match your trading style (lower for longer-term, higher for shorter-term)

This indicator works seamlessly with the main Ehlers Reverse EMA indicator while maintaining a clean chart interface, making it ideal for traders who prefer visual simplicity without sacrificing analytical power.

Ehlers Reverse EMAOverview

The Ehlers Reverse EMA is an advanced momentum indicator designed by John Ehlers and implemented here with additional features for improved trading decision-making. This indicator helps identify trend direction, potential reversals, and generates precise buy/sell signals based on multiple confirmation methods.

What Makes It Unique

Unlike conventional EMAs, the Ehlers Reverse EMA uses a sophisticated reverse-engineering approach to provide smoother, more responsive signals with reduced lag. The indicator combines a proprietary EMA calculation with optional moving average confirmation to filter out market noise and highlight meaningful price movements.

Features

Dynamic Color Coding: Green when momentum is positive, red when negative

Moving Average Overlay: Optional MA with selectable types (SMA, EMA, WMA, VWMA)

Multiple Signal Generation Methods:

Zero-Line Crossovers: Signals when momentum shifts from positive to negative or vice versa

MA Crossovers: Signals when the Ehlers EMA crosses its own moving average

Combined Confirmation: Requires both zero-line and MA crossovers for highest probability signals

On-Chart Signal Visualization: Clear buy/sell arrows directly on the price chart

Customizable Parameters: Adjust alpha value, MA type, and signal generation to suit your trading style

How To Use

Add the main "Ehlers Reverse EMA" indicator to your chart

Add the companion "EREMA Signals" indicator to display buy/sell signals on the price chart

Ensure both indicators have matching settings for consistency

Signal Interpretation

Buy Signals (Green Triangles): Appear below price bars when conditions are met

Sell Signals (Red Triangles): Appear above price bars when conditions are met

Recommended Timeframes

Works well on all timeframes from 5-minute to daily charts. For swing trading, 4H or daily timeframes often provide the most reliable signals.

Strategy Applications

Trend Following: Use zero-line crossovers to enter with the trend

Momentum Trading: Use MA crossovers for entry and exit points

Confirmation Tool: Combine with price action or other indicators for higher-probability trades

Divergence Analysis: Compare indicator movement with price action to spot potential reversals

Parameter Settings

Alpha (Default: 0.1): Lower values create smoother lines but more lag; higher values increase responsiveness but may increase false signals

MA Length (Default: 14): Adjust based on your trading timeframe and style

This versatile indicator helps identify high-probability trading opportunities while filtering out market noise, making it valuable for both novice and experienced traders alike.

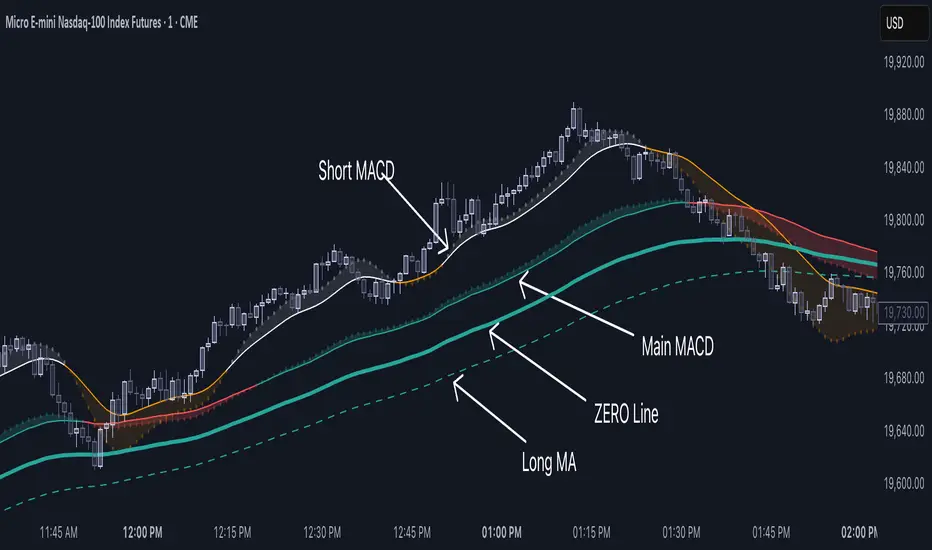

Double MACD Overlay [NLR]This indicator plots two MACD signals directly on your price chart to help you spot trends and shifts in momentum more clearly:

🔹 Main MACD - The classic MACD with customizable Fast, Slow, and Signal lengths. Great for confirming broader trend direction.

🔹 Short MACD - A faster MACD with an option to smooth the input, helping you catch early signals or identify short-term momentum changes.

Each MACD is visualized as:

A line showing the moving average

A colored histogram showing the MACD minus the signal

A zero line for reference

Why use this?

By comparing a short-term MACD with a longer-term one, you get early signals without losing the big picture. Use it for confirmation, divergence spotting, or just cleaner trend visualization.

Best For:

✅ Trend-followers

✅ Momentum traders

✅ Anyone who wants more context from their MACD signals

Recommended Settings:

Here are some ideal settings to get the most out of this indicator:

On a 5-Minute Chart:

Compare your current MACD with the 15-minute MACD.

- MACD Multiplier: 3

On a 1-Minute Chart:

Spot short-term moves while comparing them to the 5-minute MACD.

- MACD Multiplier: 5

- Use Smoothed Source (Short MACD): ON (for a cleaner short MACD signal)

Happy trading! 💹

MACD Volume Strategy (BBO + MACD State, Reversal Type)Overview

MACD Volume Strategy (BBO + MACD State, Reversal Type) is a momentum-based reversal system that combines MACD crossover logic with volume filtering to enhance signal accuracy and minimize noise. It aims to identify structural trend shifts and manage risk using predefined parameters.

※This strategy is for educational and research purposes only. All results are based on historical simulations and do not guarantee future performance.

Strategy Objectives

Identify early trend transitions with high probability

Filter entries using volume dynamics to validate momentum

Maintain continuous exposure using a reversal-style model

Apply a consistent 1:1.5 risk-to-reward ratio per trade

Key Features

Integrated MACD and volume oscillator filtering

Zero repainting (all signals confirmed on closed candles)

Automatic position flipping for seamless direction shifts

Stop-loss and take-profit based on recent structural highs/lows

Trading Rules

Long Entry Conditions

MACD crosses above the zero line (BBO Buy arrow)

Volume oscillator is positive (short EMA > long EMA)

MACD is above the signal line

Close any existing short and enter a new long

Short Entry Conditions

MACD crosses below the zero line (BBO Sell arrow)

Volume oscillator is positive

MACD is below the signal line

Close any existing long and enter a new short

Exit Rules

Take Profit (TP) = Entry ± (risk distance × 1.5)

Stop Loss (SL) = Recent swing low (for long) or high (for short)

Early Exit = Triggered when a reversal signal appears (flip logic)

Risk Management Parameters

Pair: ETH/USD

Timeframe: 10-minute

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted for sustainable practice)

Total Trades: 312 (backtest on selected dataset)

※Risk parameters are fully configurable and should be adjusted to suit each trader's personal setup and broker conditions.

Parameters & Configurations

Volume Short Length: 6

Volume Long Length: 12

MACD Fast Length: 11

MACD Slow Length: 21

Signal Smoothing: 10

Oscillator MA Type: SMA

Signal Line MA Type: SMA

Visual Support

Green arrow = Long entry

Red arrow = Short entry

MACD lines, signal line, and histogram

SL/TP markers plotted directly on the chart

Strategic Advantages & Uniqueness

Volume filtering eliminates low-participation, weak signals

Structurally aligned SL/TP based on recent market pivots

No repainting — decisions are made only on closed candles

Always in the market due to the reversal-style framework

Inspirations & Attribution

This strategy is inspired by the excellent work of:

Bitcoinblockchainonline – “BBO_Roxana_Signals MACD + vol”

Leveraging MACD zero-line cross and volume oscillator for intuitive signal generation.

HasanRifat – “MACD Fake Filter ”

Introduced a signal filter using MACD wave height averaging to reduce false positives.

This strategy builds upon those ideas to create a more automated, risk-aware, and technically adaptive system.

Summary

MACD Volume Strategy is a clean, logic-first automated trading system built for precision-seeking traders. It avoids discretionary bias and provides consistent signal logic under backtested historical conditions.

100% mechanical — no discretionary input required

Designed for high-confidence entries

Can be extended with filters, alerts, or trailing stops

※Strategy performance depends on market context. Past performance is not indicative of future results. Use with proper risk management and careful configuration.

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

Pro Scalper AI [BullByte]The Pro Scalper AI is a powerful, multi-faceted scalping indicator designed to assist active traders in identifying short-term trading opportunities with precision. By combining trend analysis, momentum indicators, dynamic weighting, and optional AI forecasting, this tool provides both immediate and latched trading signals based on confirmed (closed bar) data—helping to avoid repainting issues. Its flexible design includes customizable filters such as a higher timeframe trend filter, and adjustable settings for ADX, ATR, and Hull Moving Average (HMA), giving traders the ability to fine-tune the strategy to different markets and timeframes.

Key Features :

- Confirmed Data Processing :

Utilizes a helper function to lock in price and volume data only from confirmed (closed) bars, ensuring the reliability of signals without the risk of intrabar repainting.

- Trend Analysis :

Employs ADX and Directional Movement (DI) calculations along with a locally computed HMA to detect short-term trends. An optional higher timeframe trend filter can further refine the analysis.

- Flexible Momentum Modes :

Choose between three momentum calculation methods—Stochastic RSI, Fisher RSI, or Williams %R—to match your preferred style of analysis. This versatility allows you to optimize the indicator for different market conditions.

- Dynamic Weighting & Volatility Adjustments :

Adjusts the contribution of trend, momentum, volatility, and volume through dynamic weighting. This ensures that the indicator responds appropriately to varying market conditions by scaling its sensitivity with user-defined maximum factors.

- Optional AI Forecast :

For those who want an extra edge, the built-in AI forecasting module uses linear regression to predict future price moves and adjusts oscillator thresholds accordingly. This feature can be toggled on or off, with smoothing options available for more stable output.

- Latching Mode for Signal Persistenc e:

The script features a latching mechanism that holds signals until a clear reversal is detected, preventing whipsaws and providing more reliable trade entries and exits.

- Comprehensive Visualizations & Dashboard :

- Composite Oscillator & Dynamic Thresholds : The oscillator is plotted with dynamic upper and lower thresholds, and the area between them is filled with a color that reflects the active trading signal (e.g., Strong Buy, Early Sell).

- Signal Markers : Both immediate (non-latching) and stored (latched) signals are marked on the chart with distinct shapes (circles, crosses, triangles, and diamonds) to differentiate between signal types.

- Real-Time Dashboard : A customizable dashboard table displays key metrics including ADX, oscillator value, chosen momentum mode, HMA trend, higher timeframe trend, volume factor, AI bias (if enabled), and more, allowing traders to quickly assess market conditions at a glance.

How to Use :

1. S ignal Interpretation :

- Immediate Signals : For traders who prefer quick entries, the indicator displays immediate signals such as “Strong Buy” or “Early Sell” based on the current market snapshot.

- Latched Signals : When latching is enabled, the indicator holds a signal state until a clear reversal is confirmed, offering sustained trade setups.

2. Trend Confirmation :

- Use the HMA trend indicator and the optional higher timeframe trend filter to confirm the prevailing market direction before acting on signals.

3. Dynamic Thresholds & AI Forecasting :

- Monitor the dynamically adjusted oscillator thresholds and, if enabled, the AI bias to gauge potential shifts in market momentum.

4. Risk Management :

- Combine these signals with additional analysis and sound risk management practices to determine optimal entry and exit points for scalping trades.

Disclaimer :

This script is provided for educational and informational purposes only and does not constitute financial advice. Trading involves risk, and past performance is not indicative of future results. Always perform your own analysis and use proper risk management strategies before trading.

Relative Directional Index (RDI)🔍 Overview

The Relative Directional Index (RDI) is a hybrid tool that fuses the Average Directional and the Relative Strength Indices (ADX and RSI) into a single, highly visual interface. While the former captures trend strength, the latter reveals momentum shifts and potential exhaustion. Together, they can confirm trend structure, anticipate reversals, and sharpen the timing entries and exits.

📌 Why Combine ADX with RSI?

Most indicators focus on either trend-following (like ADX) or momentum detection (like RSI)—but rarely both. Each comes with trade-offs:

- ADX alone confirms trend strength but ignores momentum.

- RSI alone signals overbought/oversold, but lacks trend context.

The RDI resolves this by integrating both, offering:

- Smarter filters for trend entries

- Early warnings of momentum breakdowns

- More confident signal validation

🧠 Design Note: Fibonacci Harmony

All default values—5, 13, 21—are Fibonacci numbers. This is intentional, as these values reflect the natural rhythm of market cycles, and promote harmonic calibration between price action and indicator logic.

🔥 Key Features

✅ ADX Histogram

- Green bars = trend gaining strength

- Red bars = trend weakening

- Adjustable transparency for visual tuning

✅ ADX Line (Orange)

- Measures trend strength over time

- Rising = accelerating trend

- Falling = trend may be fading

✅ RSI Line (Lemon Yellow)

- Captures momentum surges and slowdowns

- Above 50 = bullish control

- Below 50 = bearish pressure

✅ Trend Strength Squares

- Bright green = strong uptrend

- Bright red = strong downtrend

- Faded colors = range-bound or indecisive

✅ ADX/RSI Crossover Markers

- Yellow square = RSI crosses above ADX → momentum building

- Orange square = ADX crosses above RSI → trend still dominant

✅ Customizable Reference Lines

- Yellow (50) = strong trend threshold

- Red (30) = weak trend zone

- Green (70) = overextended, potential exhaustion

_______________________________________________________

🎯 How to Trade with the RDI

The RDI helps traders identify momentum-supported trends, catch early reversals, and avoid false signals during consolidation.

✅ Trend Confirmation Entries

🔼 Bullish → Enter long on pullbacks or resistance breakouts

- ADX rising above 30

- RSI above 50

- Green trend square visible

🔽 Bearish → Enter short on breakdowns or failed retests

- ADX rising

- RSI below 50

- Red trend square visible

🧯 Exit if RSI crosses back against trend direction or ADX flattens

🚨 Reversal Setups Using Divergence

📈 Bullish Divergence → Long entry after confirmation (e.g. engulfing bar, volume spike)

- Price prints lower low

- RSI prints higher low

- Green triangle

📉 Bearish Divergence → Short entry on breakdown

- Price prints higher high

- RSI prints lower high

- Red triangle

Tip: Stronger if ADX is declining (fading trend strength)

🔂 Breakout Detection via Cross Markers

- Yellow square = RSI > ADX → breakout brewing

- Orange square = ADX > RSI → trend continuation likely

⏸️ Avoid Choppy Markets

- RSI between 45–55

- Faded trend squares

- Flat ADX below 20–30

🧠 Pro Tips

- Combine RDI with VWAPs, moving averages and/or pitchforks

- Watch for alignment between trend and momentum

- Use divergence markers as confirmation, not stand-alone triggers

_______________________________________________________

⚠️ Hidden Divergence (Optional)

The RDI includes optional hidden divergence detection. These signals suggest trend continuation but are off by default. Use with discretion—best in established trends, not sideways markets.

🙈 Hidden Bullish

- Price prints higher low

- RSI prints lower low

🙈 Hidden Bearish

- Price prints lower high

- RSI prints higher high

Trend Strength MeterThe Trend Strength Meter (TSM) is a powerful and versatile indicator designed to help traders identify market trends, measure their strength, and detect potential reversals with ease. This indicator combines the power of moving averages, divergence detection, and a clean, customizable dashboard to provide actionable insights for traders of all levels.

How It Works

Trend Strength Calculation:

1. The TSM calculates the trend strength using the difference between two Exponential Moving Averages (EMAs): a fast EMA (default: 20) and a slow EMA (default: 50).

2. The difference is expressed as a percentage of the slow EMA, providing a clear measure of the trend's strength and direction.

Histogram Visualization:

1. A color-coded histogram visually represents the trend strength:

Green: Bullish trend

Red: Bearish trend

Gray: Neutral or no significant trend

2. A smoothed trend strength line (SMA of the trend strength) is also plotted for better clarity.

Divergence Detection:

1. The indicator detects bullish and bearish divergences using the RSI (Relative Strength Index) and price action.

2. Bullish Divergence: Price makes a lower low, but RSI makes a higher low, signaling potential upward momentum.

3. Bearish Divergence: Price makes a higher high, but RSI makes a lower high, signaling potential downward momentum.

=> Divergences are marked with arrows on the chart:

Green Arrow: Bullish divergence

Red Arrow: Bearish divergence

Dashboard:

1. A clean and informative dashboard displays key information:

Trend Strength Value: The current strength of the trend

Trend Direction: Bullish, Bearish, or Neutral

Last Signal: Buy, Sell, or None (based on divergence signals)

The dashboard is fully customizable and can be positioned anywhere on the chart (e.g., top-right, bottom-left, center, etc.).

Key Features

1. Trend Strength Measurement: Quickly identify the strength and direction of the trend.

2. Divergence Detection: Spot potential reversals before they occur with bullish and bearish divergence signals.

3. Customizable Dashboard: Move the dashboard to your preferred location on the chart for better visibility.

4. User-Friendly Design: Clean visuals and intuitive color coding make it easy to interpret market conditions.

5. Actionable Signals: Provides clear Buy/Sell signals based on divergence, helping traders make informed decisions.

How to Use

1. Trend Confirmation:

Use the histogram and trend strength value to confirm the current market trend.

Green bars indicate a bullish trend, while red bars indicate a bearish trend.

2. Divergence Signals:

Look for divergence arrows (green for bullish, red for bearish) to anticipate potential reversals.

Combine divergence signals with other technical analysis tools for higher accuracy.

3. Dashboard Insights:

Monitor the dashboard for real-time updates on trend strength, direction, and the latest signal.

Use the "Last Signal" (Buy/Sell) to validate your trading decisions.

4. Custom Settings:

Adjust the EMA lengths and divergence lookback period to suit your trading style and timeframe.

Position the dashboard anywhere on the chart for convenience.

Best Practices

1. Use the TSM in conjunction with other indicators or price action analysis for confirmation.

2. Test the indicator on different timeframes to find the one that works best for your strategy.

3. Always practice proper risk management when trading.

Disclaimer

This indicator is a tool to assist in technical analysis and should not be used as a standalone trading strategy. Past performance is not indicative of future results. Always conduct your own research and consult with a financial advisor before making trading decisions.

Momentum Shift [Bigbeluga]

This indicator identifies momentum shifts using a smoothed momentum calculation. It plots dynamic shift zones consisting of five levels that expand or contract based on price action. When momentum rises, the indicator creates an upward shift zone, and when momentum falls, it generates a downward shift zone. The shift zones dynamically react to price, stopping extension when a level is crossed.

🔵Key Features:

Smoothed Momentum Calculation:

➣ Utilizes a Hull Moving Average (HMA) to smooth momentum and reduce noise.

➣ Identifies momentum shifts with crossovers between the current momentum value and its previous state.

➣ Uses a gradient color scheme to highlight momentum strength.

Dynamic Shift Zones:

➣ When momentum rises, the indicator plots an upper shift zone with five incremental levels.

➣ When momentum falls, a lower shift zone is formed with five descending levels.

➣ Each level within the shift zone represents a progressively stronger momentum shift.

Level Extension Control:

➣ Shift zones stop extending once a level is crossed by price.

➣ Levels closer to price act as key momentum resistance or support zones.

➣ If price retraces after a shift, the remaining levels stay intact for further reference.

Momentum Direction Indications:

➣ Labels (▲ and ▼) appear at momentum shift points to indicate rising or falling momentum.

🔵Usage:

Momentum-Based Entries: Identify momentum shifts early by using shift zones as confirmation for trade entries.

Trend Continuation & Exhaustion: Observe which shift levels price respects—if momentum shift zones hold, the trend may continue; if they break, momentum may reverse.

Dynamic Support & Resistance: Use the five-level shift zones as temporary support and resistance areas that adapt to momentum shifts.

Momentum Strength Analysis: If price moves through multiple shift levels in one direction, it signals strong momentum in that direction.

Momentum Shift is a powerful tool for traders looking to analyze momentum shifts with structured visual zones. By combining smoothed momentum calculations with dynamic shift zones, this indicator provides a clear view of market momentum and helps traders navigate price action effectively.

MACD Boundary PSA - CoffeeKillerMACD Boundary PSA - CoffeeKiller Indicator Guide

Welcome traders! This guide will walk you through the MACD Boundary PSA indicator, a powerful market analysis tool developed by CoffeeKiller that enhances the traditional MACD with advanced boundary detection and peak signaling features.

🔔 **Warning: This Indicator Has No Signal Line or MACD Line** 🔔 This indicator is my version of the MACD, that I use in conjunction with the Rev&Line indicator.

Core Concept: Enhanced MACD Analysis

The foundation of this indicator builds upon the classic Moving Average Convergence Divergence (MACD) indicator, adding boundary tracking and peak detection systems to provide clearer signals and market insights.

Histogram Bars: Market Momentum

- Positive Green Bars: Bullish momentum

- Negative Red Bars: Bearish momentum

- Color intensity varies based on momentum strength

- Special coloring for new high/low boundaries

Marker Lines: Dynamic Support/Resistance

- High Marker Line (Magenta): Tracks the highest point reached during a bullish phase

- Low Marker Line (Cyan): Tracks the lowest point reached during a bearish phase

- Acts as dynamic boundaries that help identify strength of current moves

Peak Detection System:

- Triangular markers identify significant local maxima and minima

- Background highlighting shows important momentum peaks

- Helps identify potential reversal points and momentum exhaustion

Core Components

1. MACD Calculation

- Customizable fast and slow moving averages

- Signal line smoothing options

- Flexible MA type selection (SMA or EMA)

- Custom source input options

2. Boundary Tracking System

- Automatic detection of highest values in bullish phases

- Automatic detection of lowest values in bearish phases

- Step-line visualization of boundaries

- Color-coded for easy identification

3. Peak Detection System

- Identification of local maxima and minima

- Background highlighting of significant peaks

- Triangle markers for peak visualization

- Zero-line cross detection for trend changes

4. Time Resolution Control

- Normal mode: calculations based on chart timeframe

- Custom resolution mode: calculations based on specified timeframe

Main Features

Time Resolution Settings

- Normal mode: calculations match your chart's timeframe

- Custom resolution mode: calculations based on specified timeframe

- Helps identify stronger signals from other timeframes

Visual Elements

- Color-coded histogram bars

- Dynamic marker lines for boundaries

- Peak triangles for significant turning points

- Background highlighting for peak identification

Signal Generation

- Zero-line crosses for trend change signals

- Boundary breaks for momentum strength

- Peak formation for potential reversals

- Color changes for momentum direction

Customization Options

- MA types and lengths

- Signal smoothing

- Color schemes

- Marker line visibility

- Peak background display options

Trading Applications

1. Trend Identification

- Histogram crossing above zero: bullish trend beginning

- Histogram crossing below zero: bearish trend beginning

- Histogram color: indicates momentum direction

- Consistent color intensity: trend strength

2. Reversal Detection

- Peak triangles after extended trend: potential exhaustion

- Background highlighting: significant reversal points

- Histogram approaching marker lines: potential trend change

- Color shifts from bright to muted: decreasing momentum

3. Momentum Analysis

- Histogram breaking above previous high boundary: accelerating bullish momentum

- Histogram breaking below previous low boundary: accelerating bearish momentum

- Special coloring (magenta/cyan): boundary breaks indicating strength

- Distance from zero line: overall momentum magnitude

4. Market Structure Assessment

- Consecutive higher peaks: strengthening bullish structure

- Consecutive lower troughs: strengthening bearish structure

- Peak comparisons: relative strength of momentum phases

- Boundary line steps: market structure levels

Optimization Guide

1. MACD Settings

- Fast Length: Shorter values (8-12) for responsiveness, longer values (20+) for smoother signals

- Slow Length: Shorter values (21-34) for more signals, longer values (72+) for major moves

- Default settings (22, 72, 9): balanced approach for most timeframes

- Consider using 8, 21, 5 for shorter timeframes and 34, 144, 5 for longer timeframes

2. MA Type Selection

- EMA: More responsive, follows price more closely

- SMA: Smoother, fewer false signals, potentially more lag

- Mix and match for oscillator and signal lines based on your preference

3. Time Resolution

- Match chart timeframe: for aligned analysis

- Use higher timeframe: for filtering signals

- Lower timeframe: for earlier entries but more noise

4. Color Customization

- Normal bullish/bearish colors: represent standard momentum

- High/low marker line colors: customize visibility

- Peak marker colors: adjust for your visual preference

- Consider chart background when selecting colors

Best Practices

1. Signal Confirmation

- Wait for zero-line crosses to confirm trend changes

- Look for peak formations to identify potential reversals

- Check for boundary breaks to confirm strong momentum

- Use custom timeframe option for higher timeframe confirmation

2. Timeframe Selection

- Lower timeframes: more signals, potential noise

- Higher timeframes: cleaner signals, less frequent

- Custom resolution: allows comparison across timeframes

- Consider using multiple timeframes for confirmation

3. Market Context

- Strong bullish phase: positive histogram breaking above marker line

- Strong bearish phase: negative histogram breaking below marker line

- Histogram approaching zero: potential trend change

- Peak formations: potential exhaustion points

4. Combining with Other Indicators

- Use with trend indicators for confirmation

- Pair with oscillators for overbought/oversold conditions

- Combine with volume analysis for validation

- Consider support/resistance levels with boundary lines

Advanced Trading Strategies

1. Boundary Break Strategy

- Enter long when histogram breaks above previous high marker line

- Enter short when histogram breaks below previous low marker line

- Use zero-line as initial stop-loss reference

- Take profits at formation of opposing peaks

2. Peak Trading Strategy

- Identify significant peaks with triangular markers

- Look for consecutive lower peaks in bullish phases for shorting opportunities

- Look for consecutive higher troughs in bearish phases for buying opportunities

- Use zero-line crosses as confirmation

3. Multi-Timeframe Strategy

- Use custom resolution for higher timeframe MACD trend

- Enter trades when both timeframes align

- Higher timeframe for trend direction

- Chart timeframe for precise entry

4. Histogram Color Strategy

- Enter long when histogram turns bright green (increasing momentum)

- Enter short when histogram turns bright red (increasing momentum)

- Exit when color intensity fades (decreasing momentum)

- Use marker lines as dynamic support/resistance

Practical Analysis Examples

Bullish Market Scenario

- Histogram crosses above zero line

- Green bars grow in height and intensity

- High marker line forms steps upward

- Peak triangles appear at local maxima

- Background highlights appear at significant momentum peaks

Bearish Market Scenario

- Histogram crosses below zero line

- Red bars grow in depth and intensity

- Low marker line forms steps downward

- Peak triangles appear at local minima

- Background highlights appear at significant momentum troughs

Consolidation Scenario

- Histogram oscillates around zero line

- Bar colors alternate frequently

- Marker lines remain relatively flat

- Few or no new peak highlights appear

- Histogram values remain small

Understanding Market Dynamics Through MACD Boundary PSA

At its core, this indicator provides a unique lens to visualize market momentum and boundaries:

1. Momentum Strength: The histogram height/depth shows the strength of current momentum, with color intensity providing additional context about acceleration or deceleration.

2. Dynamic Boundaries: The marker lines create a visual representation of the "high water marks" of momentum in both directions, helping to identify when markets are making new momentum extremes.

3. Exhaustion Signals: The peak detection system highlights moments where momentum has reached a local maximum or minimum, often precursors to reversals or consolidations.

4. Trend Confirmation: The histogram color and intensity provide instant feedback about the current trend direction and strength, with special colors highlighting particularly significant moves.

Remember:

- Combine signals from histogram, marker lines, and peak formations

- Use appropriate timeframe settings for your trading style

- Customize the indicator to match your visual preferences

- Consider market conditions and correlate with price action

This indicator works best when:

- Used as part of a comprehensive trading system

- Combined with proper risk management

- Applied with an understanding of current market conditions

- Signals are confirmed by price action and other indicators

**DISCLAIMER**: This indicator and its signals are intended solely for educational and informational purposes. They do not constitute financial advice. Trading involves significant risk of loss. Always conduct your own analysis and consult with financial professionals before making trading decisions.

RSI3M3+ v.1.8RSI3M3+ v.1.8 Indicator

This script is an advanced trading indicator based on Walter J. Bressert's cycle analysis methodology, combined with an RSI (Relative Strength Index) variation. Let me break it down and explain how it works.

Core Concepts

The RSI3M3+ indicator combines:

A short-term RSI (3-period)

A 3-period moving average to smooth the RSI

Bressert's cycle analysis principles to identify optimal trading points

RSI3M3+ Indicator VisualizationImage Walter J. Bressert's Cycle Analysis Concepts

Walter Bressert was a pioneer in cycle analysis trading who believed markets move in cyclical patterns that can be measured and predicted. His key principles integrated into this indicator include:

Trading Cycles: Markets move in cycles with measurable time spans from low to low

Timing Bands: Projected periods when the next cyclical low or high is anticipated

Oscillator Use: Using oscillators like RSI to confirm cycle position

Entry/Exit Rules: Specific rules for trade entry and exit based on cycle position

Key Parameters in the Script

Basic RSI Parameters

Required bars: Minimum number of bars needed (default: 20)

Overbought region: RSI level considered overbought (default: 70)

Oversold region: RSI level considered oversold (default: 30)

Bressert-Specific Parameters

Cycle Detection Length: Lookback period for cycle identification (default: 30)

Minimum/Maximum Cycle Length: Expected cycle duration in days (default: 15-30)

Buy Line: Lower threshold for buy signals (default: 40)

Sell Line: Upper threshold for sell signals (default: 60)

How the Indicator Works

RSI3M3 Calculation:

Calculates a 3-period RSI (sRSI)

Smooths it with a 3-period moving average (sMA)

Cycle Detection:

Identifies bottoms: When the RSI is below the buy line (40) and starting to turn up

Identifies tops: When the RSI is above the sell line (60) and starting to turn down

Records these points to calculate cycle lengths

Timing Bands:

Projects when the next cycle bottom or top should occur

Creates visual bands on the chart showing these expected time windows

Signal Generation:

Buy signals occur when the RSI turns up from below the oversold level (30)

Sell signals occur when the RSI turns down from above the overbought level (70)

Enhanced by Bressert's specific timing rules

Bressert's Five Trading Rules (Implemented in the Script)

Cycle Timing: The low must be 15-30 market days from the previous Trading Cycle bottom

Prior Top Validation: A Trading Cycle high must have occurred with the oscillator above 60

Oscillator Behavior: The oscillator must drop below 40 and turn up

Entry Trigger: Entry is triggered by a rise above the price high of the upturn day

Protective Stop: Place stop slightly below the Trading Cycle low (implemented as 99% of bottom price)

How to Use the Indicator

Reading the Chart

Main Plot Area:

Green line: 3-period RSI

Red line: 3-period moving average of the RSI

Horizontal bands: Oversold (30) and Overbought (70) regions

Dotted lines: Buy line (40) and Sell line (60)

Yellow vertical bands: Projected timing windows for next cycle bottom

Signals:

Green up arrows: Buy signals

Red down arrows: Sell signals

Trading Strategy

For Buy Signals:

Wait for the RSI to drop below the buy line (40)

Look for an upturn in the RSI from below this level

Enter the trade when price rises above the high of the upturn day

Place a protective stop at 99% of the Trading Cycle low

For Sell Signals:

Wait for the RSI to rise above the sell line (60)

Look for a downturn in the RSI from above this level

Consider exiting or taking profits when a sell signal appears

Alternative exit: When price moves below the low of the downturn day

Cycle Timing Enhancement:

Pay attention to the yellow timing bands

Signals occurring within these bands have higher probability of success

Signals outside these bands may be less reliable

Practical Tips for Using RSI3M3+

Timeframe Selection:

The indicator works best on daily charts for intermediate-term trading

Can be used on weekly charts for longer-term position trading

On intraday charts, adjust cycle lengths accordingly

Market Applicability:

Works well in trending markets with clear cyclical behavior

Less effective in choppy, non-trending markets

Consider additional indicators for trend confirmation

Parameter Adjustment:

Different markets may have different natural cycle lengths

You may need to adjust the min/max cycle length parameters

Higher volatility markets may need wider overbought/oversold levels

Trade Management:

Enter trades when all Bressert's conditions are met

Use the protective stop as defined (99% of cycle low)

Consider taking partial profits at the projected cycle high timing

Advanced Techniques

Multiple Timeframe Analysis:

Confirm signals with the same indicator on higher timeframes

Enter in the direction of the larger cycle when smaller and larger cycles align

Divergence Detection:

Look for price making new lows while RSI makes higher lows (bullish)

Look for price making new highs while RSI makes lower highs (bearish)

Confluence with Price Action:

Combine with support/resistance levels

Use with candlestick patterns for confirmation

Consider volume confirmation of cycle turns

This RSI3M3+ indicator combines the responsiveness of a short-term RSI with the predictive power of Bressert's cycle analysis, offering traders a sophisticated tool for identifying high-probability trading opportunities based on market cycles and momentum shifts.

THANK YOU FOR PREVIOUS CODER THAT EFFORT TO CREATE THE EARLIER VERSION THAT MAKE WALTER J BRESSERT CONCEPT IN TRADINGVIEW @ADutchTourist

TR Buy/Sell Signal PanelI scripted this with chatgpt have fun guys

📊 TR Buy/Sell Signal Panel – Smart Trade Signals with Visual Clarity

The TR Buy/Sell Signal Panel is a standalone indicator inspired by the powerful Traders Reality (TR) methodology.

It detects potential long and short trade setups using classic market behavior patterns such as volume spikes, EMA crossovers, and session-based timing – all visualized cleanly and statically on your chart.

✅ Key Features

Buy Signals (LONG):

Green PVSRA candle (strong bullish candle with momentum)

EMA13 crossing above EMA50

Volume spike (current volume exceeds 20-period average × multiplier)

Triggered only during London or New York trading sessions (UTC)

Sell Signals (SHORT):

Red PVSRA candle (strong bearish move)

EMA13 crossing below EMA50

Volume spike

Also restricted to active session times

📌 Visual Components

Green/Red arrows on the chart indicate Buy/Sell entries

A static info panel in the bottom-right corner displays all signal conditions:

PVSRA active ✅

Volume Spike ✅

EMA Crossover ✅

Session Time ✅

Last Signal: 🟢 BUY / 🔴 SELL

Current Direction: 🟢 LONG / 🔴 SHORT / ❌ NONE

⚙️ Fully Customizable

Adjustable volume spike multiplier

Optional toggle for showing/hiding short signals

Extremely user-friendly layout – ideal for both beginners & experienced traders

📦 Best For:

Scalpers & Intraday Traders

Traders who follow the Traders Reality / Market Maker Method

Anyone who values clean, rule-based trade entries

Note: Works across all timeframes with sufficient volume (e.g., 5min – 4hr). Sessions are based on UTC time – adjust if needed based on your timezone or trading hours.

Reversal + Confirm ZonesThis script is written in Pine Script (version 5) for TradingView and creates an indicator called **"Reversal + Confirm Zones"**. It overlays visual zones on a price chart to identify potential reversal points and confirmation signals for trading. The indicator combines **Bollinger Bands** and **RSI** to detect overbought/oversold conditions (reversal zones) and uses **EMA crosses** and **MACD zero-line crosses** to confirm bullish or bearish trends. Below is a detailed explanation:

---

### **1. Purpose**

- The script highlights:

- **Reversal Zones**: Areas where the price might reverse due to being overbought (green) or oversold (red).

- **Confirmation Zones**: Areas where a trend reversal is confirmed using EMA and MACD signals (green for bullish, red for bearish).

- It provides visual backgrounds and alerts to assist traders in spotting potential trade setups.

---

### **2. Components**

The script is divided into two main parts: **Reversal Logic** and **Confirmation Logic**.

---

### **3. Reversal Logic (Red & Green Zones)**

#### **Bollinger Bands**

- **Parameters**:

- Length: 20 periods.

- Source: Closing price (`close`).

- Multiplier: 2.0 (standard deviations).

- **Calculation**:

- `basis`: 20-period Simple Moving Average (SMA).

- `dev`: 2 times the standard deviation of the price over 20 periods.

- `upper`: `basis + dev` (upper band).

- `lower`: `basis - dev` (lower band).

- **Purpose**: Identifies when the price moves outside the normal range (beyond 2 standard deviations).

#### **Relative Strength Index (RSI)**

- **Parameters**:

- Length: 14 periods.

- Low Threshold: 30 (oversold).

- High Threshold: 70 (overbought).

- **Calculation**: `rsiValue = ta.rsi(close, rsiLength)`.

- **Purpose**: Measures momentum to confirm overbought or oversold conditions.

#### **Zone Conditions**

- **Red Zone (Oversold)**:

- Condition: `close < lower` (price below lower Bollinger Band) AND `rsiValue < rsiLowThreshold` (RSI < 30).

- Visual: Light red background (`color.new(color.red, 80)`).

- Alert: "Deep Oversold Signal triggered!".

- **Green Zone (Overbought)**:

- Condition: `close > upper` (price above upper Bollinger Band) AND `rsiValue > rsiHighThreshold` (RSI > 70).

- Visual: Light green background (`color.new(color.green, 80)`).

- Alert: "Deep Overbought Signal triggered!".

#### **Interpretation**