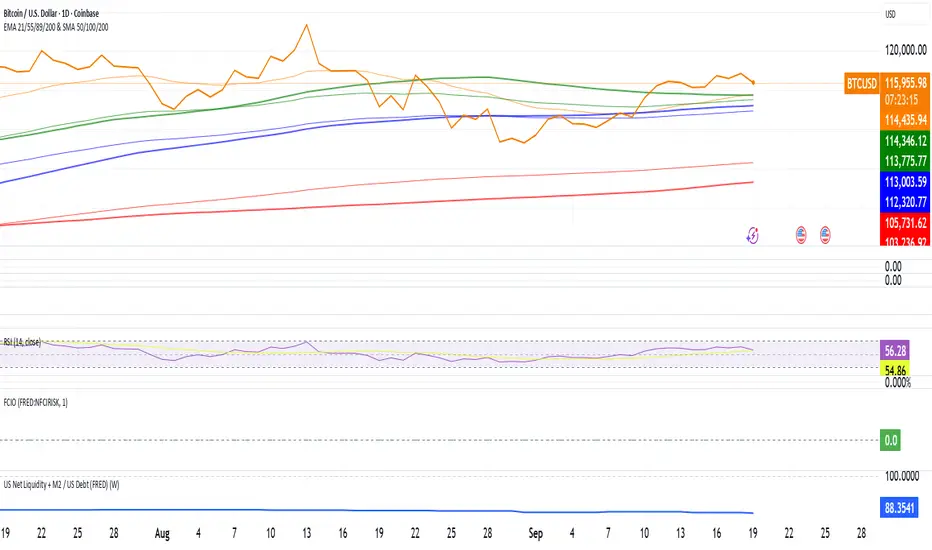

US Net Liquidity + M2 / US Debt (FRED)US Net Liquidity + M2 / US Debt

🧩 What this chart shows

This indicator plots the ratio of US Net Liquidity + M2 Money Supply divided by Total Public Debt.

US Net Liquidity is defined here as the Federal Reserve Balance Sheet (WALCL) minus the Treasury General Account (TGA) and the Overnight Reverse Repo facility (ON RRP).

M2 Money Supply represents the broad pool of liquid money circulating in the economy.

US Debt uses the Federal Government’s total outstanding debt.

By combining net liquidity with M2, then dividing by total debt, this chart provides a structural view of how much monetary “fuel” is in the system relative to the size of the federal debt load.

🧮 Formula

Ratio

=

(

Fed Balance Sheet

−

(

TGA

+

ON RRP

)

)

+

M2

Total Public Debt

Ratio=

Total Public Debt

(Fed Balance Sheet−(TGA+ON RRP))+M2

An optional normalization feature scales the ratio to start at 100 on the first valid bar, making long-term trends easier to compare.

🔎 Why it matters

Liquidity vs. Debt Growth: The numerator (Net Liquidity + M2) captures the monetary resources available to markets, while the denominator (Debt) reflects the expanding obligation of the federal government.

Market Signal: Historically, shifts in net liquidity and money supply relative to debt have coincided with major turning points in risk assets like equities and Bitcoin.

Context: A rising ratio may suggest that liquidity conditions are improving relative to debt expansion, which can be supportive for risk assets. Conversely, a falling ratio may highlight tightening conditions or debt outpacing liquidity growth.

⚙️ How to use it

Overlay this chart against S&P 500, Bitcoin, or gold to analyze correlations with asset performance.

Watch for trend inflections—does the ratio bottom before equities rally, or peak before risk-off periods?

Use normalization for long historical comparisons, or raw values to see the absolute ratio.

📊 Data sources

This indicator pulls from FRED (Federal Reserve Economic Data) tickers available in TradingView:

WALCL: Fed balance sheet

RRPONTSYD: Overnight Reverse Repo

WTREGEN: Treasury General Account

M2SL: M2 money stock

GFDEBTN: Total federal public debt

⚠️ Notes

Some FRED series are updated weekly, others monthly—set your chart timeframe accordingly.

If any ticker is unavailable in your plan, replace it with the equivalent FRED symbol provided in TradingView.

This indicator is intended for macro analysis, not short-term trading signals.

Phân tích Cơ bản

Grand Master's Candlestick Dominance (ATR Enhanced)### Grand Master's Candlestick Dominance (ATR Enhanced)

**Overview**

Unleash the ancient wisdom of Japanese candlestick charting with a modern twist! This comprehensive Pine Script v5 strategy and indicator scans for over 75 classic and advanced candlestick patterns (bullish, bearish, and neutral), assigning dynamic strength scores (1-10) to each for precise signal filtering. Enhanced with Average True Range (ATR) for volatility-aware body size validation, it dominates the markets by combining timeless pattern recognition with robust confirmation layers. Whether used as a backtestable strategy or visual indicator, it empowers traders to spot high-probability reversals, continuations, and indecision setups with surgical accuracy.

Inspired by Steve Nison's *Japanese Candlestick Charting Techniques*, this tool elevates pattern analysis beyond basics—think Hammers, Engulfing patterns, Morning Stars, and rare gems like Abandoned Baby or Concealing Baby Swallow—all consolidated into intelligent arrays for real-time averaging and prioritization.

**Key Features**

- **Extensive Pattern Library**:

- **Bullish (25+ patterns)**: Hammer (8.0), Bullish Engulfing (10.0), Morning Star (7.0), Three White Soldiers (9.0), Dragonfly Doji (8.0), and more (e.g., Rising Three, Unique Three River Bottom).

- **Bearish (25+ patterns)**: Hanging Man (8.0), Bearish Engulfing (10.0), Evening Star (7.0), Three Black Crows (9.0), Gravestone Doji (8.0), and exotics like Upside Gap Two Crows or Stalled Pattern.

- **Neutral/Indecision (34+ patterns)**: Doji variants (Long-Legged, Four Price), Spinning Tops, Harami Crosses, and multi-bar setups like Upside Tasuki Gap or Advancing Block.

Each pattern includes duration tracking (1-5 bars) and ATR-adjusted body/shadow criteria for relevance in volatile conditions.

- **Smart Confirmation Filters** (All Toggleable):

- **Trend Alignment**: 20-period SMA (customizable) ensures entries align with the prevailing trend; optional higher timeframe (e.g., Daily) MA crossover for multi-timeframe confluence.

- **Support/Resistance (S/R)**: Pivot-based levels with 0.01% tolerance to confirm bounces or breaks.

- **Volume Surge**: 20-period volume MA with 1.5x spike multiplier to validate momentum.

- **ATR Body Sizing**: Filters small bodies (<0.3x ATR) and long bodies (>0.8x ATR) for context-aware pattern reliability.

- **Follow-Through**: Ensures post-pattern confirmation via bullish/bearish closes or closes beyond prior bars.

Minimum average strength (default 7.0) and individual pattern thresholds (5.0) prevent weak signals.

- **Entry & Exit Logic**:

- **Long Entry**: Bullish average strength ≥7.0 (outweighing bearish), uptrend, volume spike, near support, follow-through, and HTF alignment.

- **Short Entry**: Mirror for bearish dominance in downtrends near resistance.

- **Exits**: Bearish/neutral shift, or fixed TP (5%) / SL (2%)—pyramiding disabled, 10% equity sizing.

- Backtest range: Jan 1, 2020 – Dec 31, 2025 (editable). Initial capital: $10,000.

- **Interactive Dashboard** (Top-Right Panel):

Real-time insights including:

- Market phase (e.g., "Bullish Phase (Avg Str: 8.2)"), active pattern (e.g., "BULLISH: Bullish Engulfing (Str: 10.0, Bars: 2)"), and trend status.

- Strength breakdowns (Bull/Bear/Neutral counts & averages).

- Filter status (e.g., "Volume: ✔ Spike", "ATR: Enabled (L:0.8, S:0.3)").

- Backtest stats: Total trades, win rate, streak, and last entry/exit details (price & timestamp).

Toggle mode: Strategy (live trades) or Indicator (signals only).

- **Advanced Alerts** (15+ Toggleable Types):

Set up via TradingView's "Any alert() function call" for bar-close triggers:

- Entry/Exit signals with strength & pattern details.

- Strong patterns (≥2 bullish/bearish), neutral indecision, volume spikes.

- S/R breakouts, HTF reversals, high-confidence singles (≥8.0 strength).

- Conflicting signals, MA crossovers, ATR volatility bursts, multi-bar completions.

Example: "STRONG BULLISH PATTERN detected! Strength: 9.5 | Top Pattern: Three White Soldiers | Trend: Up".

**Customization & Usage Tips**

- **Inputs Groups**: Strategy toggles, confirmations, exits, backtest dates, and 15+ alert switches—all intuitively grouped.

- **Optimization**: Tune min strengths for aggressive (lower) or conservative (higher) trading; enable/disable filters to suit your style (e.g., disable S/R for scalping).

- **Best For**: Forex, stocks, crypto on 1H–Daily charts. Test on historical data to refine TP/SL.

- **Limitations**: No external data installs; relies on built-in TA functions. Patterns are probabilistic—combine with your risk management.

Master the candles like a grandmaster. Deploy on TradingView, backtest relentlessly, and let dominance begin! Questions? Drop a comment.

*Version: 1.0 | Updated: September 2025 | Credits: Built on Pine Script v5 with nods to Nison's timeless techniques.*

Stock Valuation Models - Professional Investment Analysis Tool📊 Overview

Stock Valuation Models is a comprehensive financial analysis indicator that combines multiple valuation methodologies to calculate intrinsic stock value. This professional-grade tool implements 7 different valuation methods , risk assessment framework, and financial health metrics to provide data-driven investment decisions.

🎯 Key Features

📈 Multiple Valuation Methods

Graham's Valuation - Conservative asset-based approach by Benjamin Graham

Multiples Valuation - Market-based P/E and P/B ratios from sector peers

Discounted Cash Flow (DCF) - Future cash flow projections with present value calculation

Dividend Discount Model - Gordon Growth Model for dividend-paying stocks

FCFF Model - Enterprise-level Free Cash Flow to Firm analysis

EVA Model - Economic Value Added measurement above cost of capital

Advanced Multiples - Enterprise Value ratios (EV/EBITDA, EV/Sales)

🏥 Financial Health Metrics

Altman Z-Score - Bankruptcy prediction and financial distress assessment

Piotroski F-Score - 9-point fundamental strength evaluation

Beneish M-Score - Earnings manipulation detection system

Magic Formula - Joel Greenblatt's combined quality and value scoring

⚖️ Risk Assessment Framework

Multi-Factor Risk Scoring - Fundamental, market, quality, and data quality risks

Risk-Adjusted Margin of Safety - Dynamic safety thresholds based on risk level

Position Sizing Guidance - Risk-appropriate investment allocation recommendations

🔍 Data Quality System

Real-Time Quality Tracking - Visual warnings for insufficient data

Fallback Methodology - Alternative calculations when primary data unavailable

Confidence Scoring - Method agreement and data quality assessment

⚙️ Settings & Parameters

Main Settings

Margin of Safety (%) - Minimum discount required before buying (Default: 15%)

Table Font Size - Choose between "Small" and "Normal" text size

Valuation Methods

Graham's Valuation - Best for mature, stable companies with strong fundamentals

Multiples Valuation - Compares to industry peers using dynamic sector ratios

Discounted Cash Flow - Ideal for growth companies with predictable cash flows

Dividend Discount Model - For consistent dividend-paying stocks (disabled by default)

FCFF Model - Enterprise approach for leveraged companies and M&A analysis

EVA Model - Measures value creation above cost of capital

Advanced Multiples - Wall Street standard EV ratios for professional analysis

Additional Metrics

Magic Formula - Combined quality and value scoring system

Altman Z-Score - Bankruptcy risk assessment (Safe >2.99, Distress <1.81)

Piotroski F-Score - Fundamental quality score (Excellent ≥8, Poor <4)

Beneish M-Score - Manipulation detector (High Risk >-2.22, Low Risk ≤-2.22)

🔧 How It Works

Dynamic Calculations

Sector-Based Ratios - Automatically detects company sector and applies appropriate valuation multiples

Economic Integration - Uses real-time risk-free rates, VIX volatility, and GDP growth data

Quality Weighting - Adjusts method weights based on company type (growth/mature/distressed) and market conditions

Negative Value Handling - Shows actual calculated values but excludes negative results from weighted average

Risk-Adjusted Analysis

VIX Integration - Higher market volatility increases required margin of safety

Sector Risk Premiums - Energy and Financial sectors get higher risk multipliers

Quality Adjustments - High Piotroski F-Score companies get lower risk ratings

Data Quality Impact - Insufficient data increases risk score and safety requirements

Visual Display

Horizontal Table Layout - Organized by method groups (Valuation → Results → Risk → Health)

Color-Coded Results - Green/Yellow/Red indicators for risk levels and recommendations

Warning Symbols - ⚠️ for data quality issues, ❌ for excluded negative values

Dollar Amounts - Both percentage and dollar-based margin of safety calculations

📈 Interpretation Guide

💎 Intrinsic Value Results

Weighted Average - Combines all enabled methods based on intelligent weighting

Confidence Level - High/Medium/Low based on method agreement and data quality

Method Count - Number of successful valuation calculations

🎯 Margin of Safety

Percentage - Current discount/premium to calculated intrinsic value

Dollar Amount - Absolute dollar difference per share

Buy Price - Risk-adjusted target purchase price

⚖️ Risk Assessment

Low Risk (Green) - Normal position sizing (3-5%)

Medium Risk (Yellow) - Reduced position sizing (1-3%)

High Risk (Red) - Minimal position sizing (<1%)

📊 Recommendations

STRONG BUY - Low risk + adequate margin + high confidence

BUY - Meets risk-adjusted margin requirements

HOLD - Positive margin but higher risk

SELL - Insufficient margin for risk level

🎓 Educational Tooltips

Every parameter includes detailed explanations accessible by hovering over the setting. Learn about:

When to use each valuation method

How different metrics are calculated

Interpretation thresholds and ratings

Risk factors and quality indicators

💡 Best Practices

🚀 For Growth Stocks

Enable DCF and Advanced Multiples

Focus on Piotroski F-Score for quality assessment

Use higher margin of safety due to volatility

💰 For Value Stocks

Enable Graham's and Multiples Valuation

Check Altman Z-Score for financial stability

Consider Magic Formula rating

📈 For Dividend Stocks

Enable Dividend Discount Model

Focus on sustainable dividend coverage

Check for consistent dividend history

⚠️ For Distressed Situations

Prioritize Graham's asset-based approach

Monitor Altman Z-Score closely

Use higher risk-adjusted margins

⚠️ Important Notes & Data Limitations

📅 Data Timing Considerations

Fundamental Data Lag - Company financial data (earnings, cash flows, balance sheet items) may be 1-3 months behind current market conditions

Quarterly Reporting Delays - Most recent available data reflects the company's situation as of the last filed quarterly/annual report

Market vs. Fundamentals Gap - Stock prices react instantly to news, while fundamental data updates occur periodically

Accuracy Impact - Recent business changes, market events, or company developments may not be reflected in current calculations

🔧 Technical Limitations

Data Dependencies - Requires fundamental data availability from TradingView

Quality Warnings - Pay attention to ⚠️ symbols indicating insufficient data

Risk Context - Always consider risk score in investment decisions

Market Conditions - Tool automatically adjusts for market volatility (VIX)

Sector Specificity - Ratios automatically adjust based on company's sector

💡 Best Practice Recommendations

Supplement with Current Analysis - Always combine with recent news, earnings calls, and management guidance

Monitor Data Quality - Check when the underlying financial data was last updated

Consider Market Context - Factor in recent market events that may affect company performance

Use as Starting Point - Treat calculations as baseline analysis requiring additional research

🔗 Methodology

Based on established academic research and professional practices:

Benjamin Graham - Security Analysis principles

Joel Greenblatt - Magic Formula methodology

Edward Altman - Z-Score bankruptcy prediction

Joseph Piotroski - Fundamental analysis scoring

Messod Beneish - Earnings manipulation detection

Modern Portfolio Theory - Risk-adjusted decision making

This indicator is designed for educational and analytical purposes. Always conduct additional research and consider consulting with financial professionals before making investment decisions.

VIX Price BoxVIX Price Box (Customizable Colors)

This indicator displays the current VIX (CBOE Volatility Index) value in a fixed box on the top-right corner of the chart. It’s designed to give traders a quick, at-a-glance view of market volatility without needing to switch tickers.

Features

Pulls the live VIX price and updates automatically on every bar.

Displays the value inside a table box that stays fixed in the top-right corner.

Threshold-based coloring: the text color changes depending on whether the VIX is below, between, or above your chosen threshold levels.

5 built-in color modes:

Custom mode – choose your own colors for low, medium, and high volatility zones.

Adjustable threshold levels, background color, and frame color.

Use Cases

Monitor overall market risk sentiment while trading other instruments.

Identify periods of low vs. high volatility at a glance.

Pair with strategies that rely on volatility (options trading, hedging, breakout setups, etc.).

Higher High Lower Low Higher High Lower Low 🦉{Phanchai} — TradingView Description

Structure detector with dynamic Support/Resistance, customizable labels, and ready-made alerts (Pine v6).

This script marks market structure turning points — HH (Higher High), HL (Higher Low), LH (Lower High), LL (Lower Low) — and builds segmented Support/Resistance lines from those turns. Labels and colors are fully customizable and the script ships with multiple alert conditions.

What it does

Detects swing pivots using left/right bar windows, then classifies each confirmed swing as HH/HL/LH/LL.

Plots compact labels at the confirmed pivot bars with tooltips (English).

Derives dynamic Support / Resistance : every time structure flips, the previous level is closed and a new segment starts, extending to the right .

Provides alert conditions for any label and for specific first-occurrence shifts (e.g., first HH after a bearish label).

How it works (in short)

A pivot high/low confirms only after Right Bars candles have closed; labels and S/R appear at that confirmation bar.

An internal backbone (zigzag-like) is built from confirmed pivots, with light consistency checks to avoid contradictory sequences.

Structure rules compare the recent five pivots (A…E) to decide HH/HL/LH/LL.

S/R is updated from structure: e.g., in an up leg, new HLs refresh Support; in a down leg, new LHs refresh Resistance.

Alerts included

Any structure label (HH/HL/LH/LL) — Fires on any new label.

First LL after HL/HH — First bearish break after a bullish label.

First HH after LL/LH — First bullish break after a bearish label.

LL or HL formed — Any low-side label.

LH or HH formed — Any high-side label.

HL formed

HH formed

LL formed

LH formed

How to use (quick start)

Add the indicator to your chart.

Choose Left/Right Bars for your timeframe (e.g., 5–10 for intraday; larger for higher timeframes).

Pick your label colors/sizes and S/R style.

Right-click the chart → Add alert… → Condition: this indicator → select the desired alert.

Notes & tips

Because pivots require Right Bars to confirm, labels and S/R appear with a natural delay of that many bars. This avoids repainting.

Raising Left/Right Bars reduces noise and increases the average distance between pivots; lowering them increases sensitivity.

Structure is strict: sometimes you may see two HL (or two LH) in a row if the intermediate opposite swing didn’t qualify as HH/LH (or LL/HL).

S/R segments are drawn with line objects ; they are controlled via Inputs (style/width/color), not the Style tab.

This tool highlights structure; it’s not a standalone entry/exit system. Combine with volume, trend, or risk management rules.

Built with Pine v6. Clean, compact labels; segmented S/R that updates only on confirmed changes; comprehensive alerts ready for automation.

Fundamentals PanelFundamentals Panel Description

The Fundamentals Panel is a versatile Pine Script indicator that displays key financial metrics—Market Cap, P/E Ratio, P/S Ratio, and PEG Ratio—in a clean, customizable table on your TradingView chart. Designed for investors and traders, this tool brings essential company fundamentals directly to your chart, saving time and enhancing decision-making.

Quick Insights: View critical valuation metrics (Market Cap, P/E, P/S, PEG) at a glance without leaving your chart, ideal for fundamental analysis or screening stocks.

Customizable Display: Toggle each metric on or off via input settings to focus on what matters most to your strategy.

Adjustable Font Size: Choose from Small, Normal, or Large text sizes to ensure readability suits your chart setup and screen preferences.

Reliable Data: Pulls data directly from TradingView’s financial database, using diluted shares and trailing metrics for accuracy across most stocks.

Debugging Support: Includes hidden plots (visible in the Data Window) to verify raw data like shares outstanding, revenue, and PEG, helping you trust the numbers.

How It Works

The indicator fetches:

Market Cap: Calculated using diluted shares outstanding and current price.

P/E Ratio: Price divided by trailing twelve-month (TTM) diluted EPS.

P/S Ratio: Market cap divided by TTM total revenue.

PEG Ratio: Trailing PEG from TradingView’s data, with an additional calculated PEG for cross-checking.

Optimized SMC Dashboard - by MinkyJuiceSMC - all in one

all SMC confluences are included, fully automated and customisable

enjoy, made by MinkyJuice

No Turd Burglars, please

FOMC Fund Rate 2022–2025(0.1)This indicator visualizes the Federal Open Market Committee (FOMC) meetings from 2022 through 2025.

It plots vertical lines on the announcement dates and attaches labels showing:

The decision (rate hike ⭡, cut ⭣, or hold ⭤).

The size of the rate change in percentage points.

The cumulative Federal Funds Rate path in parentheses.

Features:

Accurate timestamps for each FOMC meeting (UTC+1).

Customizable line style, width, and color.

Label color and text color options.

Placeholder labels for future meetings to maintain the timeline.

Use this script to keep track of historical Fed policy decisions and visualize the rate path over time directly on your chart.

Value Investing IndicatorThis is based on PeterNagy Indicator. I just update it from v.4 to v.6 and modify. Open for tweak

PE Rating by The Noiseless TraderPE Rating by The Noiseless Trader

This script analyzes a symbol’s Price-to-Earnings (P/E) ratio, using Diluted EPS (TTM) fundamentals directly from TradingView.

The script calculates the Price-to-Earnings ratio (P/E) using Diluted EPS (TTM) fundamentals. It then identifies:

PE High → the highest valuation point over a 3-year historical range.

PE Low → the lowest valuation point over a 3-year historical range.

PE Median → the midpoint between the two extremes, offering a fair-value benchmark.

PE (Int) → an additional intermediate low to track more recent undervaluation points. This is calculated based on lowest valuation point over a 1-year historical range

These levels are plotted directly on the chart as horizontal references, with markers showing the exact bars/dates when the extremes occurred. Candles corresponding to those days are also highlighted for context.

Bars corresponding to these extremes are highlighted (red = PE High, green = PE Low).

How it helps

Provides a historical valuation framework that complements technical analysis. We look for long opportunity or base formation near the PE Low and be cautious when stocks tends to trade near High PE.

We do not short the stock at High PE infact be cautious with long trades.

Helps identify whether current price action is happening near overvalued or undervalued zones.

Adds a long-term perspective to support swing trading and investing decisions. If a stock is coming from Low PE to Median PE and along with that if we get entry based on Classical strategies like Darvas Box, or HH-HL based on Dow Theory.

Offers a simple visual map of how far the market has moved from “cheap” to “expensive.”

This tool is best suited for long-term investors and swing traders who want to merge fundamentals with technical setups.

This indicator is designed as an educational tool to illustrate how valuation metrics (like earnings multiples) can be viewed alongside price action, helping traders connect fundamental context with technical execution in real market conditions.

ATR Future Movement Range Projection

The "ATR Future Movement Range Projection" is a custom TradingView Pine Script indicator designed to forecast potential price ranges for a stock (or any asset) over short-term (1-month) and medium-term (3-month) horizons. It leverages the Average True Range (ATR) as a measure of volatility to estimate how far the price might move, while incorporating recent momentum bias based on the proportion of bullish (green) vs. bearish (red) candles. This creates asymmetric projections: in bullish periods, the upside range is larger than the downside, and vice versa.

The indicator is overlaid on the chart, plotting horizontal lines for the projected high and low prices for both timeframes. Additionally, it displays a small table in the top-right corner summarizing the projected prices and the percentage change required from the current close to reach them. This makes it useful for traders assessing potential targets, risk-reward ratios, or option strategies, as it combines volatility forecasting with directional sentiment.

Key features:

- **Volatility Basis**: Uses weekly ATR to derive a stable daily volatility estimate, avoiding noise from shorter timeframes.

- **Momentum Adjustment**: Analyzes recent candle colors to tilt projections toward the prevailing trend (e.g., more upside if more green candles).

- **Time Horizons**: Fixed at 1 month (21 trading days) and 3 months (63 trading days), assuming ~21 trading days per month (excluding weekends/holidays).

- **User Adjustable**: The ATR length/lookback (default 50) can be tweaked via inputs.

- **Visuals**: Green/lime lines for highs, red/orange for lows; a semi-transparent table for quick reference.

- **Limitations**: This is a probabilistic projection based on historical volatility and momentum—it doesn't predict direction with certainty and assumes volatility persists. It ignores external factors like news, earnings, or market regimes. Best used on daily charts for stocks/ETFs.

The indicator doesn't generate buy/sell signals but helps visualize "expected" ranges, similar to how implied volatility informs option pricing.

### How It Works Step-by-Step

The script executes on each bar update (typically daily timeframe) and follows this logic:

1. **Input Configuration**:

- ATR Length (Lookback): Default 50 bars. This controls both the ATR calculation period and the candle count window. You can adjust it in the indicator settings.

2. **Calculate Weekly ATR**:

- Fetches the ATR from the weekly timeframe using `request.security` with a length of 50 weeks.

- ATR measures average price range (high-low, adjusted for gaps), representing volatility.

3. **Derive Daily ATR**:

- Divides the weekly ATR by 5 (approximating 5 trading days per week) to get an equivalent daily volatility estimate.

- Example: If weekly ATR is $5, daily ATR ≈ $1.

4. **Define Projection Periods**:

- 1 Month: 21 trading days.

- 3 Months: 63 trading days (21 × 3).

- These are hardcoded but based on standard trading calendar assumptions.

5. **Compute Base Projections**:

- Base projection = Daily ATR × Days in period.

- This gives the total expected movement (range) without direction: e.g., for 3 months, $1 daily ATR × 63 = $63 total range.

6. **Analyze Candle Momentum (Win Rate)**:

- Counts green candles (close > open) and red candles (close < open) over the last 50 bars (ignores dojis where close == open).

- Total colored candles = green + red.

- Win rate = green / total colored (as a fraction, e.g., 0.7 for 70%). Defaults to 0.5 if no colored candles.

- This acts as a simple momentum proxy: higher win rate implies bullish bias.

7. **Adjust Projections Asymmetrically**:

- Upside projection = Base projection × Win rate.

- Downside projection = Base projection × (1 - Win rate).

- This skews the range: e.g., 70% win rate means 70% of the total range allocated to upside, 30% to downside.

8. **Calculate Projected Prices**:

- High = Current close + Upside projection.

- Low = Current close - Downside projection.

- Done separately for 1M and 3M.

9. **Plot Lines**:

- 3M High: Solid green line.

- 3M Low: Solid red line.

- 1M High: Dashed lime line.

- 1M Low: Dashed orange line.

- Lines extend horizontally from the current bar onward.

10. **Display Table**:

- A 3-column table (Projection, Price, % Change) in the top-right.

- Rows for 1M High/Low and 3M High/Low, color-coded.

- % Change = ((Projected price - Close) / Close) × 100.

- Updates dynamically with new data.

The entire process repeats on each new bar, so projections evolve as volatility and momentum change.

### Examples

Here are two hypothetical examples using the indicator on a daily chart. Assume it's applied to a stock like AAPL, but with made-up data for illustration. (In TradingView, you'd add the script to see real outputs.)

#### Example 1: Bullish Scenario (High Win Rate)

- Current Close: $150.

- Weekly ATR (50 periods): $10 → Daily ATR: $10 / 5 = $2.

- Last 50 Candles: 35 green, 15 red → Total colored: 50 → Win Rate: 35/50 = 0.7 (70%).

- Base Projections:

- 1M: $2 × 21 = $42.

- 3M: $2 × 63 = $126.

- Adjusted Projections:

- 1M Upside: $42 × 0.7 = $29.4 → High: $150 + $29.4 = $179.4 (+19.6%).

- 1M Downside: $42 × 0.3 = $12.6 → Low: $150 - $12.6 = $137.4 (-8.4%).

- 3M Upside: $126 × 0.7 = $88.2 → High: $150 + $88.2 = $238.2 (+58.8%).

- 3M Downside: $126 × 0.3 = $37.8 → Low: $150 - $37.8 = $112.2 (-25.2%).

- On the Chart: Green/lime lines skewed higher; table shows bullish % changes (e.g., +58.8% for 3M high).

- Interpretation: Suggests stronger potential upside due to recent bullish momentum; useful for call options or long positions.

#### Example 2: Bearish Scenario (Low Win Rate)

- Current Close: $50.

- Weekly ATR (50 periods): $3 → Daily ATR: $3 / 5 = $0.6.

- Last 50 Candles: 20 green, 30 red → Total colored: 50 → Win Rate: 20/50 = 0.4 (40%).

- Base Projections:

- 1M: $0.6 × 21 = $12.6.

- 3M: $0.6 × 63 = $37.8.

- Adjusted Projections:

- 1M Upside: $12.6 × 0.4 = $5.04 → High: $50 + $5.04 = $55.04 (+10.1%).

- 1M Downside: $12.6 × 0.6 = $7.56 → Low: $50 - $7.56 = $42.44 (-15.1%).

- 3M Upside: $37.8 × 0.4 = $15.12 → High: $50 + $15.12 = $65.12 (+30.2%).

- 3M Downside: $37.8 × 0.6 = $22.68 → Low: $50 - $22.68 = $27.32 (-45.4%).

- On the Chart: Red/orange lines skewed lower; table highlights larger downside % (e.g., -45.4% for 3M low).

- Interpretation: Indicates bearish risk; might prompt protective puts or short strategies.

#### Example 3: Neutral Scenario (Balanced Win Rate)

- Current Close: $100.

- Weekly ATR: $5 → Daily ATR: $1.

- Last 50 Candles: 25 green, 25 red → Win Rate: 0.5 (50%).

- Projections become symmetric:

- 1M: Base $21 → Upside/Downside $10.5 each → High $110.5 (+10.5%), Low $89.5 (-10.5%).

- 3M: Base $63 → Upside/Downside $31.5 each → High $131.5 (+31.5%), Low $68.5 (-31.5%).

- Interpretation: Pure volatility-based range, no directional bias—ideal for straddle options or range trading.

In real use, test on historical data: e.g., if past projections captured actual moves ~68% of the time (1 standard deviation for ATR), it validates the volatility assumption. Adjust the lookback for different assets (shorter for volatile cryptos, longer for stable blue-chips).

KT_Global Bond Yields by CountryGlobal Bond Yields Indicator Summary

The Global Bond Yields by Country indicator, developed for Trading View (Pine Script v5), provides a comprehensive tool for visualizing and analyzing government bond yields across multiple countries and maturities. Below are its key features:

Features

Country Selection: Choose from 20 countries, including the United States, China, Japan, Germany, United Kingdom, and more, to display their respective bond yields.

Multiple Maturities: Supports 18 bond maturities ranging from 1 month to 40 years, allowing users to analyze short-term to long-term yield trends.

Customizable Display:

Toggle visibility for each maturity (1M, 3M, 6M, 1Y, 2Y, 3Y, 4Y, 5Y, 6Y, 7Y, 8Y, 9Y, 10Y, 15Y, 20Y, 25Y, 30Y, 40Y) individually.

Option to show or hide all maturities with a single toggle for streamlined analysis.

10Y-2Y Yield Spread: Plots the difference between 10-year and 2-year bond yields, a key indicator of yield curve dynamics, with an option to enable/disable.

Zero Line Reference: Displays a dashed grey horizontal line at zero for clear visual reference.

Color-Coded Plots: Each maturity is plotted with a distinct color, ranging from lighter shades (short-term) to darker shades (long-term), for easy differentiation.

Country Label: Displays the selected country's name as a large, prominent label on the chart for quick identification.

Error Handling: Alerts users if an invalid country is selected, ensuring robust operation.

Data Integration: Fetches bond yield data from Trading View's database (e.g., TVC:US10Y) with support for ignoring invalid symbols to prevent errors.

This indicator is ideal for traders and analysts monitoring global fixed-income markets, yield curve shapes, and cross-country comparisons.

Futures Forward Price [NeoButane]In futures markets, the theoretical value of a futures contract can be derived from its underlying price and cost of carry. By baking in the costs and potential yields, the theoretical forward price then be used in basis against futures prices in place of the underlying spot price.

Usage

The script creates plots on the main chart and a separate window pane. Both are meant to be used to visualize dislocations in the market.

By using a futures vs. forward basis instead of futures vs. spot basis, discounts in the market are clearer.

Last month, the gold futures market GCZ2025 traded >1% above forward price when tariffs were announced and fell back in line once the tariffs were verbally retracted.

View roll spreads over a back-adjusted continuous chart. I guess. I don't think spread traders only look at one chart. This is as educational for me as it is you.

Configuration

The underlying reference needs to be changed to match the futures contract you are using.

The Risk-Free Rate defaults to FRED:SOFR. I found the contract month matched 3-Month SOFR Futures to be the closest for forward price.

Risk-Free Rate: The interest rate source for forward price.

Constant Risk-Free Rate: a static interest rate that can be used in advance of future changes in risk-free rate.

Underlying Reference: spot or index price. Some examples include TVC:SPX, TVC:GOLD, CRYPTO:BTCUSD, TVC:USOIL.

Forward Price Compounding: determines which formula to use. They're similar and become closer as the contract matures.

Alternative Contract: enable and select a futures contract to use it on a chart different than the main.

Storage Cost and Yield: for use with commodities. I haven't found a proper use for them yet but enabling is simple if you are able to.

The following are meant to be used with the continuous formula as they are compounded. However the rate sources don't differ much for the purpose of futures prices.

3-Month CME SOFR Futures

3-Month ICEEUR SONIA Futures

3-Month Osaka TONA Futures

The other rate sources are either meant for futures contracts shorter than quarterly such as monthly crypto futures or were meant to help myself understand how different rates would align with futures prices, like inflation.

What this script does

It uses the cost of carry formula to output the forward price (red line). The underlying reference (green line) is plotted alongside and a futures-derived reference (blue line) can be displayed to see how it looks next to the real reference price.

The data pane displays either the nominal difference or percentage difference between the real futures price and the calculated forward price.

Further reading

www.investopedia.com

www.cmegroup.com

www.oxfordenergy.org

www-2.rotman.utoronto.ca

www.cmegroup.com

3-month rate futures

www.cmegroup.com

www.ice.com

www.bankofengland.co.uk

www.jpx.co.jp

Trend FriendTrend Friend — What it is and how to use it

I built Trend Friend to stop redrawing the same trendlines all day. It automatically connects confirmed swing points (fractals) and keeps the most relevant lines in front of you. The goal: give you clean, actionable structure without the guesswork.

What it does (in plain English)

Finds swing highs/lows using a Fractal Period you choose.

Draws auto-trendlines between the two most recent confirmed highs and the two most recent confirmed lows.

Colours by intent:

Lines drawn from highs (potential resistance / bearish) = Red

Lines drawn from lows (potential support / bullish) = Green

Keeps the chart tidy: The newest lines are styled as “recent,” older lines are dimmed as “historical,” and it prunes anything beyond your chosen limit.

Optional crosses & alerts: You can highlight when price closes across the most recent line and set alerts for new lines formed and upper/lower line crosses.

Structure labels: It tags HH, LH, HL, LL at the swing points, so you can quickly read trend/rotation.

How it works (under the hood)

A “fractal” here is a confirmed pivot: the highest high (or lowest low) with n bars on each side. That means pivots only confirm after n bars, so signals are cleaner and less noisy.

When a new pivot prints, the script connects it to the prior pivot of the same type (high→high, low→low). That gives you one “bearish” line from highs and one “bullish” line from lows.

The newest line is marked as recent (brighter), and the previous recent line becomes historical (dimmed). You can keep as many pairs as you want, but I usually keep it tight.

Inputs you’ll actually use

Fractal Period (n): this is the big one. It controls how swingy/strict the pivots are.

Lower n → more swings, more lines (faster, noisier)

Higher n → fewer swings, cleaner lines (slower, swing-trade friendly)

Max pair of lines: how many pairs (up+down) to keep on the chart. 1–3 is a sweet spot.

Extend: extend lines Right (my default) or Both ways if you like the context.

Line widths & colours: recent vs. historical are separate so you can make the active lines pop.

Show crosses: toggle the X markers when price crosses a line. I turn this on when I’m actively hunting breakouts/retests.

Reading the chart

Red lines (from highs): I treat these as potential resistance. A clean break + hold above a red line often flips me from “fade” to “follow.”

Green lines (from lows): Potential support. Same idea in reverse: break + hold below and I stop buying dips until I see structure reclaim.

HH / LH / HL / LL dots: quick read on structure.

HH/HL bias = uptrend continuation potential

LH/LL bias = downtrend continuation potential

Mixed prints = rotation/chop—tighten risk or wait for clarity.

My H1 guidance (fine-tuning Fractal Period)

If you’re mainly on H1 (my use case), tune like this:

Fast / aggressive: n = 6–8 (lots of signals, good for momentum days; more chop risk)

Balanced (recommended): n = 9–12 (keeps lines meaningful but responsive)

Slow / swing focus: n = 13–21 (filters noise; better for trend days and higher-TF confluence)

Rule of thumb: if you’re getting too many touches and whipsaws, increase n. If you’re late to obvious breaks, decrease n.

How I trade it (example workflow)

Pick your n for the session (H1: start at 9–12).

Mark the recent red & green lines. That’s your immediate structure.

Look for interaction:

Rejections from a line = fade potential back into the range.

Break + close across a line = watch the retest for continuation.

Confirm with context: session bias, HTF structure, and your own tools (VWAP, RSI, volume, FVG/OB, etc.).

Plan the trade: enter on retest or reclaim, stop beyond the line/last swing, target the opposite side or next structure.

Alerts (set and forget)

“New trendline formed” — fires when a new high/low pivot confirms and a fresh line is drawn.

“Upper/lower trendline crossed” — fires when price crosses the most recent red/green line.

Use these to track structure shifts without staring at the screen.

Good to know (honest limitations)

Confirmation lag: pivots need n bars on both sides, so signals arrive after the swing confirms. That’s by design—less noise, fewer fake lines.

Lines update as structure evolves: when a new pivot forms, the previous “recent” line becomes “historical,” and older ones can be removed based on your max setting.

Not an auto trendline crystal ball: it won’t predict which line holds or breaks—it just keeps the most relevant structure clean and up to date.

Final notes

Works on any timeframe; I built it with H1 in mind and scale to H4/D1 by increasing n.

Pairs nicely with session tools and VWAP for intraday, or with supply/demand / FVGs for swing planning.

Risk first: lines are structure, not guarantees. Manage position size and stops as usual.

Not financial advice. Trade your plan. Stay nimble.

Volumatic Fair Value Gaps [BigBeluga]🔵 OVERVIEW

The Volumatic Fair Value Gaps indicator detects and plots size-filtered Fair Value Gaps (FVGs) and immediately analyzes the bullish vs. bearish volume composition inside each gap. When an FVG forms, the tool samples volume from a 10× lower timeframe , splits it into Buy and Sell components, and overlays two compact bars whose percentages always sum to 100%. Each gap also shows its total traded volume . A live dashboard (top-right) summarizes how many bullish and bearish FVGs are currently active and their cumulative volumes—offering a quick read on directional participation and trend pressure.

🔵 CONCEPTS

FVGs (Fair Value Gaps) : Imbalance zones between three consecutive candles where price “skips” trading. The script plots bullish and bearish gaps and extends them until mitigated.

Size Filtering : Only significant gaps (by relative size percentile) are drawn, reducing noise and emphasizing meaningful imbalances.

// Gap Filters

float diff = close > open ? (low - high ) / low * 100 : (low - high) / high *100

float sizeFVG = diff / ta.percentile_nearest_rank(diff, 1000, 100) * 100

bool filterFVG = sizeFVG > 15

Volume Decomposition : For each FVG, the indicator inspects a 10× lower timeframe and aggregates volume of bullish vs. bearish candles inside the gap’s span.

100% Split Bars : Two inline bars per FVG display the % Bull and % Bear shares; their total is always 100%.

Total Gap Volume : A numeric label at the right edge of the FVG shows the total traded volume associated with that gap.

Mitigation Logic : Gaps are removed when price closes through (or touches via high/low—user-selectable) the opposite boundary.

Dashboard Summary : Counts and sums the active bullish/bearish FVGs and their total volumes to gauge directional dominance.

🔵 FEATURES

Bullish & Bearish FVG plotting with independent color controls and visibility toggles.

Adaptive size filter (percentile-based) to keep only impactful gaps.

Lower-TF volume sampling at 10× faster resolution for more granular Buy/Sell breakdown.

Per-FVG volume bars : two horizontal bars showing Bull % and Bear % (sum = 100%).

Per-FVG total volume label displayed at the right end of the gap’s body.

Mitigation source option : choose close or high/low for removing/invalidating gaps.

Overlap control : older overlapped gaps are cleaned to avoid clutter.

Auto-extension : active gaps extend right until mitigated.

Dashboard : shows count of bullish/bearish gaps on chart and cumulative volume totals for each side.

Performance safeguards : caps the number of active FVG boxes to maintain responsiveness.

🔵 HOW TO USE

Turn on/off FVG types : Enable Bullish FVG and/or Bearish FVG depending on your focus.

Tune the filter : The script already filters by relative size; if you need fewer (stronger) signals, increase the percentile threshold in code or reduce the number of displayed boxes.

Choose mitigation source :

close — stricter; gap is removed when a closing price crosses the boundary.

high/low — more sensitive; a wick through the boundary mitigates the gap.

Read the per-FVG bars :

A higher Bull % inside a bullish gap suggests constructive demand backing the imbalance.

A higher Bear % inside a bearish gap suggests supply is enforcing the imbalance.

Use total gap volume : Larger totals imply more meaningful interest at that imbalance; confluence with structure/HTF levels increases relevance.

Watch the dashboard : If bullish counts and cumulative volume exceed bearish, market pressure is likely skewed upward (and vice versa). Combine with trend tools or market structure for entries/exits.

Optional: hide volume bars : Disable Volume Bars when you want a cleaner FVG map while keeping total volume labels and the dashboard.

🔵 CONCLUSION

Volumatic Fair Value Gaps blends precise FVG detection with lower-timeframe volume analytics to show not only where imbalances exist but also who powers them. The per-gap Bull/Bear % bars, total volume labels, and the cumulative dashboard together provide a fast, high-signal read on directional participation. Use the tool to prioritize higher-quality gaps, align with trend bias, and time mitigations or continuations with greater confidence.

Trajectory Channel (VWAP Highs/Lows) [Euler-Inspired]VPWA higha nd low Euler trajectory inspired script

Monthly VWAPDescription

This indicator identifies potential mean reversion opportunities by tracking price deviations from monthly VWAP with dynamic volatility-adjusted thresholds.

Core Logic:

The indicator monitors when price moves significantly away from monthly VWAP and looks for potential reversal opportunities. It uses ATR-based dynamic thresholds that adapt to current market volatility, combined with volume confirmation to filter out weak signals.

Key Features:

Adaptive Thresholds: ATR-based bands that adjust to market volatility

Volume Confirmation: Requires average volume spike to validate signals

Monthly Reset: VWAP anchors reset each month for fresh reference levels

Visual Clarity: Color-coded deviation line with background highlights for active signals

Info Panel: Shows days from anchor and current price context vs fair value

Signal Generation:

Buy Signal: Price below monthly VWAP by threshold amount with elevated volume

Sell Signal: Price above monthly VWAP by threshold amount with elevated volume

Neutral: Price within threshold range or insufficient volume

Best Used For:

Mean reversion strategies in ranging markets

Identifying potential oversold/overbought conditions

Understanding price position relative to monthly fair value

Swing Guardrail — 30-sec Midterm Check (EBITDA Margin & EV/EBITDWhat it does

Before a short-term swing entry, this indicator right-sizes positions by a quick midterm (3–12m) durability screen using two fundamentals:

EBITDA Margin (TTM) → earning power / operational resilience

EV/EBITDA (TTM) → price tag vs earning capacity (payback feel)

A high-contrast table (top-right) shows both metrics and a verdict:

PASS — both meet thresholds → normal size

HALF — only one meets → reduce size

FAIL — neither meets → avoid

Why check “midterm” for a short-term trade?

Short swings still face earnings/news gaps, failed breakouts, and regime shifts. Names with weak margins or stretched valuation tend to break faster and deeper. A 30-sec durability check helps you:

Filter fragile setups (avoid expensive + weakening names)

Stabilize drawdowns (size down when quality/price don’t align)

Keep timing unchanged while improving risk-adjusted returns

Inputs (defaults)

Min EBITDA Margin % (TTM): 8%

Max EV/EBITDA (TTM): 12

Dark chart? High-contrast colors

How to use with a swing system

Get your entry from price/volume (e.g., Ichimoku cloud break, Kijun reclaim, Tenkan>Kijun; or your A/B/C rules).

Run this check only to set size (not timing).

Optional alerts: Once per bar close for PASS / HALF / FAIL.

Size mapping & event guard

PASS → 100% of your planned size

HALF → ~50% size / tighter stops

FAIL → watchlist only

If earnings < ~10 JP business days, drop one tier; ≤3 days → avoid.

Sector guides (tweak as needed)

Software/Internet: Margin ≥ 15%, EV/EBITDA ≤ 18

Industrials/Consumer: Margin ≥ 8%, EV/EBITDA ≤ 12

Retail: Margin ≥ 5–7%, EV/EBITDA ≤ 10–12

Edge cases / substitutions

Banks/Insurers/REITs or net-cash/negative EBITDA: EV/EBITDA may mislead → consider Net Debt/EBITDA or sector metrics (CET1/LTV/DSCR).

Sparse data / fresh listings: numbers may be NA until updates.

Notes & limitations

Data via request.financial() (TTM/most-recent). Some tickers/regions can show NA until fundamentals refresh.

This is a risk-screen / sizing tool, not a buy/sell signal.

Disclaimer

Educational use only. Not investment advice.

日本語

タイトル

スイング用ガードレール―中期“壊れにくさ”30秒チェック(EBITDAマージン & EV/EBITDA, TTM)

概要

短期スイングのエントリー前に、中期(3〜12か月)の耐久性を2指標で素早く確認し、ポジションサイズを決めるためのツールです。

EBITDAマージン(TTM):事業の稼ぐ力・体力

EV/EBITDA(TTM):その体力に対する“値札”(回収年数の感覚)

右上の高コントラスト表に数値と判定を表示:

PASS:両方クリア → 通常サイズ

HALF:片方のみ → サイズ半分

FAIL:両方NG → 見送り

なぜ短期でも“中期”を確認?

短期でも決算・ニュースのギャップ、ブレイク失敗、地合い転換は起きます。マージンが弱い/割高すぎる銘柄は崩れやすく、戻りも鈍い傾向。30秒の耐久性チェックで

脆いセットアップを回避

ドローダウンを平準化(サイズで吸収)

タイミングは変えずに、リスク調整後リターンの改善を狙えます。

入力(既定)

最低EBITDAマージン:8%

最大EV/EBITDA:12

黒背景向け:高コントラスト表示

使い方(スイング手法と併用)

まずは価格シグナル(一目の雲上抜け/基準線回復/転換線>基準線、またはA/B/Cルール)。

本インジの判定でサイズのみ決定(エントリーのタイミングは出しません)。

任意でバー確定アラート(PASS/HALF/FAIL)を設定。

サイズ目安 & イベント抑制

PASS:計画サイズ100%

HALF:約50%(ストップもタイトに)

FAIL:見送り

決算まで≦10営業日なら1段階サイズダウン、≦3営業日は原則見送り。

セクター目安(調整推奨)

ソフト/ネット:マージン 15%以上、EV/EBITDA 18以下

工業/一般消費:マージン 8%以上、EV/EBITDA 12以下

小売:マージン 5〜7%以上、EV/EBITDA 10〜12以下

例外・代替

銀行・保険・REIT/ネットキャッシュ・EBITDAマイナス:EV/EBITDAは適さない場合 → Net Debt/EBITDAやCET1/LTV/DSCR等で補助。

新規上場・データ薄:更新までNAのことあり。

注意

データは request.financial() を使用。更新前はNAの可能性。

本ツールはリスク確認/サイズ調整用で、売買シグナルではありません。

免責

情報提供のみ。投資判断は自己責任で。

Total Return (divi reivested)Total Return (Dividends Reinvested) — Price Scale

This indicator overlays a Total Return price line on the chart. It shows how the stock would have performed if all dividends had been reinvested back into the stock (buying fractional shares) rather than taken as cash.

The line starts exactly at the price level of the first visible bar on your chart and moves in the same price units as the chart (not indexed to 100).

Until the first dividend inside the visible window, the Total Return line is identical to the price. From the first dividend onward, it gradually diverges upwards, reflecting the effect of reinvested payouts.

Settings:

Reinvest at Open / Close — Choose whether reinvestment uses the bar’s open or close price.

Apply effect on the next bar — If enabled, reinvestment shows up from the bar after the dividend date (common in practice).

Show dividend markers — Optionally plots labels where dividend events occur.

Line width — Adjusts the thickness of the plotted Total Return line.

Use case:

This tool is useful if you want to compare plain price performance with true shareholder returns including dividends. It helps evaluate dividend stocks (like BTI, T, XOM, etc.) more realistically.

Stock Scoring SystemThe EMA Scoring System is designed to help traders quickly assess market trend strength and decide portfolio allocation. It compares price vs. key EMAs (21, 50, 100) and also checks the relative strength between EMAs. Based on these conditions, it assigns a score (-6 to +6) and a corresponding allocation percentage.

+6 Score = 100% allocation (strong bullish trend)

-6 Score = 10% allocation (strong bearish trend)

Scores in between represent intermediate trend strength.

📌 Key Features

✅ Scoring Model: Evaluates price vs. EMA alignment and EMA cross relationships.

✅ Allocation % Display: Converts score into suggested portfolio allocation.

✅ Background Highlighting: Green shades for bullish conditions, red shades for bearish.

✅ Customizable Table Position: Choose between Top Right, Top Center, Bottom Right, or Bottom Center.

✅ Toggleable EMAs: Show/Hide 21 EMA, 50 EMA, and 100 EMA directly from indicator settings.

✅ Simple & Intuitive: One glance at the chart tells you trend strength and suggested allocation.

📈 How It Works

Score Calculation:

Price above an EMA = +1, below = -1

Faster EMA above slower EMA = +1, else -1

Maximum score = +6, minimum = -6

Allocation Mapping:

+6 → 100% allocation

+4 to +5 → 100% allocation

+2 to +3 → 75% allocation

0 to +1 → 50% allocation

-1 to -2 → 30% allocation

-3 to -4 → 20% allocation

-5 to -6 → 10% allocation

Visual Output:

Table shows SCORE + Allocation %

Background color shifts with score (green for bullish, red for bearish)

⚠️ Disclaimer

This indicator is for educational purposes only. It does not constitute financial advice. Always backtest and combine with your own analysis before making trading decisions.

MS - Çoklu Onay Stratejisi (AL-SAT)"VOLUME, MA50, RSI, DMI, ATR

5 conditions, all turning positive at the same time gives a buy signal; one of them turning negative gives a sell signal. This should be evaluated with weekly data. Not financial advice."