AlgoIndex NQ/MNQ FuturesAlgoIndex Futures v3.15 - NQ/MNQ (10-Minute RTH)

This strategy is specifically tailored for trading CME Nasdaq futures - NQ and MNQ, including continuous symbols such as NQ1!/MNQ1!. It is optimized for a 10-minute chart during U.S. Regular Trading Hours (RTH), utilizing session settings defined in the Inputs. This strategy is not intended for other futures contracts or markets.

Core Concept

The strategy employs an ATR-based trend-band model similar to Supertrend for identifying directional mechanism changes in NQ/MNQ. Trade signals are evaluated at the bar close, incorporating session and time-based safety techniques to mitigate lower-quality trading opportunities near session boundaries.

Recommended Use (Optimized Defaults)

The default input parameters are fine-tuned for NQ/MNQ on the 10-minute chart. Users are encouraged to utilize these defaults initially and to make incremental adjustments to one variable at a time to understand the impact on the strategy's performance, trading frequency, and risk profile.

Configurable Inputs

- Take Profit / Stop Loss Settings:

- Enable Stop Loss and define Stop Loss (Points)

- Enable Take Profit and define Take Profit (Points)

- Enable Trailing Stop and set both Trailing Stop (Points) and Trailing Offset (Points)

- Time Avoidance Filter:

- Enable Time Avoidance

- Avoid First X Minutes

- Avoid Last X Minutes

- Display Avoidance Zones (visual overlay)

- Session Filter and End-of-Day Management:

- Enable Session Filter

- Define Trading Session (default: 09:30-16:00)

- Select Session Timezone

- Option to Close Positions at Session End

- Specify EOD Close Minutes Before (default: 20)

- Safety Controls:

- Option to Close Before Holidays (when enabled, this feature allows the strategy to flatten positions prior to holiday or early close conditions)

- Automation Settings (Optional):

- Ticker Override (optional)

- Define Contracts (position size)

- Strategy Configuration:

- Trade Direction: Both / Long Only / Short Only

- Visual Configuration:

- Option to Show Buy/Sell Signals

- Highlight Trend Zones

- Display Info Table

- Customizable Bull/Bear Colors

Alerts and Automation (Optional)

This strategy can generate order-fill alert payloads for hooking into webhook-based automation solutions. Keep in mind to validate your alert type and your bridge/broker configuration during Replay and paper trading. Note that reversals may trigger two sequential actions (e.g., exit followed by new entry).

Backtest Notes (Optional)

For more precise historical fill data, consider enabling TradingView’s Bar Magnifier in Strategy Properties. Always apply consistent assumptions for commission and slippage when comparing backtest results.

Disclaimer

This script is intended for informational and educational purposes only and does not constitute investment advice. Trading futures carries significant risk and may result in losses that exceed the initial deposit. Backtested results are hypothetical and do not guarantee future performance.

Futures

Quantellics: NQ Reverse From EMA [Strategy]//@version=5

// © 2025 Quantellics. All rights reserved.

strategy("Quantellics: NQ Reverse From EMA ", overlay = true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, pyramiding = 0)

// Inputs

emaLen = input.int(60, "EMA Length", minval = 1)

rsiLen = input.int(14, "RSI Length", minval = 1)

lb = input.int(10, "Lookback Candles", minval = 1)

entryOff = input.float(75.0, "Entry Offset ($)", minval = 0, step = 1)

slDollar = input.float(50.0, "Stop Loss ($)", minval = 0, step = 1)

tpDollar = input.float(50.0, "Take Profit ($)", minval = 0, step = 1)

trailAct = input.float(30.0, "Trail Activation ($)", minval = 0, step = 1)

trailOff = input.float(30.0, "Trail Offset ($)", minval = 0, step = 1)

trailDelay = input.int(2, "Trail Delay (Candles)", minval = 0, step = 1)

ssH = input.int(9, "Session Start Hour (ET)", minval = 0, maxval = 23)

ssM = input.int(30, "Session Start Minute (ET)", minval = 0, maxval = 59)

seH = input.int(12, "Session End Hour (ET)", minval = 0, maxval = 23)

seM = input.int(0, "Session End Minute (ET)", minval = 0, maxval = 59)

// Session calc

int h = hour(time, "America/New_York")

int m = minute(time, "America/New_York")

sStart = ssH * 60 + ssM

sEnd = seH * 60 + seM

nowMin = h * 60 + m

inSess = nowMin >= sStart and nowMin < sEnd

eos = nowMin >= sEnd

// Indicators

ema60 = ta.ema(close, emaLen)

rsi = ta.rsi(close, rsiLen)

hiN = ta.highest(high, lb)

loN = ta.lowest(low, lb)

// Levels

longLvl = hiN - entryOff

shortLvl = loN + entryOff

// Conditions

longOk = high > ema60 and rsi > 50 and strategy.position_size == 0 and inSess and not eos

shortOk = low < ema60 and rsi < 50 and strategy.position_size == 0 and inSess and not eos

// State

var float ePrice = na

var float slLvl = na

var float tpLvl = na

var int bars = 0

if strategy.position_size != 0

bars += 1

else

bars := 0

// Orders

if longOk

strategy.entry("Long", strategy.long, limit = longLvl)

else

strategy.cancel("Long")

if shortOk

strategy.entry("Short", strategy.short, limit = shortLvl)

else

strategy.cancel("Short")

if strategy.position_size > 0

if bars > trailDelay

strategy.exit("Long Exit", "Long", stop = strategy.position_avg_price - slDollar, limit = strategy.position_avg_price + tpDollar, trail_points = trailAct, trail_offset = trailOff)

else

strategy.exit("Long Exit", "Long", stop = strategy.position_avg_price - slDollar, limit = strategy.position_avg_price + tpDollar)

if strategy.position_size < 0

if bars > trailDelay

strategy.exit("Short Exit", "Short", stop = strategy.position_avg_price + slDollar, limit = strategy.position_avg_price - tpDollar, trail_points = trailAct, trail_offset = trailOff)

else

strategy.exit("Short Exit", "Short", stop = strategy.position_avg_price + slDollar, limit = strategy.position_avg_price - tpDollar)

// EOS flat

if eos and strategy.position_size != 0

strategy.close_all(comment = "EOS Exit")

if eos

strategy.cancel_all()

// Tracking

if strategy.position_size > 0 and strategy.position_size <= 0

ePrice := strategy.position_avg_price

slLvl := ePrice - slDollar

tpLvl := ePrice + tpDollar

if strategy.position_size < 0 and strategy.position_size >= 0

ePrice := strategy.position_avg_price

slLvl := ePrice + slDollar

tpLvl := ePrice - tpDollar

// Plots

plot(ema60, color = color.blue, title = "EMA 60", linewidth = 2)

plot(hiN, color = color.new(color.green, 50), title = "Lookback High", linewidth = 1, style = plot.style_stepline)

plot(loN, color = color.new(color.red, 50), title = "Lookback Low", linewidth = 1, style = plot.style_stepline)

plot(longLvl, color = color.new(color.orange, 30), title = "Long Entry", linewidth = 2)

plot(shortLvl, color = color.new(color.purple, 30), title = "Short Entry", linewidth = 2)

Robrechtian Long-Medium Breakout Trend SystemRobrechtian Long–Medium-Term Breakout Trend System

A professional, rule-based trend-following strategy designed to capture large, sustained price movements using pure price action and breakouts.

This system follows long-established trend-following philosophy: no prediction, no volatility targeting, and no profit targets. Only disciplined entries, position additions, and exits driven entirely by trend structure.

Core Principles

Breakout-driven entries: Initial positions are taken only when price breaks above/below the 80-day Donchian channel, confirming a long–medium-term trend shift.

Short-term confirmation: Breakouts must also exceed the 20-day channel, reducing false positives.

Trend-direction filter: A 50-day moving average slope filter ensures alignment with the broader trend.

Explosive bar filter: Entries avoid excessively large, single-candle expansions (>2.5× ATR(20)) to prevent chasing exhaustion spikes.

Pyramiding into strength: Additional units are added only when price makes fresh 20-day breakouts in the direction of the trend. No scaling out. No adding on dips.

Exit only on trend violation: Positions are closed exclusively when price breaks the opposite 80-day channel. This preserves unlimited upside while enforcing disciplined exits.

Pure trend philosophy: No volatility targeting, no smoothing, no discretionary overrides, no optimization for short-term performance.

Intended Use

This system is designed primarily for diversified futures portfolios, where diversification across dozens of globally liquid markets creates robustness and stability. However, it may also be used on individual assets for educational and analytical purposes.

The system embraces the core trend-following logic:

Small losses, big winners, and unlimited upside when trends persist.

⚠️ WARNINGS / DISCLAIMERS

⚠️ Warning 1 — This strategy is not optimized for single stocks

The Robrechtian Trend System is designed for multi-asset futures portfolios, not single equities.

Performance on individual tickers may vary greatly due to lack of diversification.

⚠️ Warning 2 — Trend following includes substantial drawdowns

Deep drawdowns are a normal and expected feature of all long-term trend-following systems.

The strategy does not attempt to smooth returns or manage volatility.

If you seek steady, low-volatility equity curves, this system is not suitable.

⚠️ Warning 3 — No volatility targeting or risk smoothing

This system intentionally avoids volatility-based position sizing.

Trades may experience larger fluctuations than systems using risk parity or vol targeting.

⚠️ Warning 4 — Not financial advice

This script is for educational and research purposes only.

Past performance does not guarantee future results.

Use at your own risk.

⚠️ Warning 5 — TradingView backtests have known limitations

TradingView does not simulate:

futures contract roll logic

slippage

real bid/ask spreads

liquidity conditions

limit-up/limit-down behavior

Results may vary from live market execution.

Qullamagi EMA Breakout Autotrade (Crypto Futures L+S)Title: Qullamagi EMA Breakout – Crypto Autotrade

Overview

A crypto-focused, Qullamagi-style EMA breakout strategy built for autotrading on futures and perpetual swaps.

It combines a 5-MA trend stack (EMA 10/20, SMA 50/100/200), volatility contraction boxes, volume spikes and an optional higher-timeframe 200-MA filter. The script supports both long and short trades, partial take profit, trailing MA exits and percent-of-equity position sizing for automated crypto futures trading.

Key Features (Crypto)

Qullamagi MA Breakout Engine – trades only when price is aligned with a strong EMA/SMA trend and breaks out of a tight consolidation range. Longs use: Close > EMA10 > EMA20 > SMA50 > SMA100 > SMA200. Shorts are the mirror condition with all MAs sloping in the trend direction.

Strict vs Loose Modes – Strict (Daily) is designed for cleaner swing trades on 1H–4H (full MA stack, box+ATR and volume filters, optional HTF filter). Loose (Intraday) focuses on 10/20/50 alignment with relaxed filters for more frequent 15m–30m signals.

Volatility & Volume Filters for Crypto – ATR-based box height limit to detect volatility contraction, wide-candle filter to avoid chasing exhausted breakouts, and a volume spike condition requiring current volume to exceed an SMA of volume.

Higher-Timeframe Trend Filter (Optional) – uses a 200-period SMA on a higher timeframe (default: 1D). Longs only when HTF close is above the HTF 200-SMA, shorts only when it is below, helping avoid trading against dominant crypto trends.

Autotrade-Oriented Trade Management – position size as % of equity, initial stop anchored to a chosen MA (EMA10 / EMA20 / SMA50) with optional buffer, partial take profit at a configurable R-multiple, trailing MA exit for the remainder, and an optional cooldown after a full exit.

Markets & Timeframes

Best suited for BTC, ETH and major altcoin futures/perpetuals (Binance, Bybit, OKX, etc.).

Strict preset: 1H–4H charts for classic Qullamagi-style trend structure and fewer fake breakouts.

Loose preset: 15m–30m charts for higher trade frequency and more active intraday trading.

Always retune ATR length, box length, volume multiplier and position size for each symbol and exchange.

Strategy Logic (Quick Summary)

Long (Strict): MA stack in bullish alignment with all MAs sloping up → tight volatility box (ATR-based) → volume spike above SMA(volume) × multiplier → breakout above box high (close or intrabar) → optional HTF close above 200-SMA.

Short: Mirror logic: bearish MA stack, tight box, volume spike and breakdown below box low with optional HTF downtrend.

Best Practices for Crypto

Backtest on each symbol and timeframe you plan to autotrade, including commissions and slippage.

Start on higher timeframes (1H/4H) to learn the behavior, then move to 15m–30m if you want more signals.

Use the higher-timeframe filter when markets are strongly trending to reduce counter-trend trades.

Keep position-size percentage conservative until you fully understand the drawdowns.

Forward-test / paper trade before connecting to live futures accounts.

Webhook / Autotrade Integration

Designed to work with TradingView webhooks and external crypto trading bots.

Alert messages include structured fields such as: EVENT=ENTRY / SCALE_OUT / EXIT, SIDE=LONG / SHORT, STRATEGY=Qullamagi_MA.

Map each EVENT + SIDE combination to your bot logic (open long/short, partial close, full close, etc.) on your preferred exchange.

Important Notes & Disclaimer

Crypto markets are highly volatile and can change regime quickly. Backtest and forward-test thoroughly before using real capital. Higher timeframes generally produce cleaner MA structures and fewer fake breakouts.

This strategy is for educational and informational purposes only and does not constitute financial advice. Trading leveraged crypto products involves substantial risk of loss. Always do your own research, manage risk carefully, and never trade with money you cannot afford to lose.

EMA Cross + RSI + ADX - Autotrade Strategy V2Overview

A versatile trend-following strategy combining EMA 9/21 crossovers with RSI momentum filtering and optional ADX trend strength confirmation. Designed for both cryptocurrency and traditional futures/options markets with built-in stop loss management and automated position reversals.

Key Features

Multi-Market Compatibility: Works on both crypto futures (Bitcoin, Ethereum) and traditional markets (NIFTY, Bank NIFTY, S&P 500 futures, equity options)

Triple Confirmation System: EMA crossover + RSI filter + ADX strength (optional)

Automated Risk Management: 2% stop loss with wick-touch detection

Position Auto-Reversal: Opposite signals automatically close and reverse positions

Webhook Ready: Six distinct alert messages for automation (Entry Buy/Sell, Close Long/Short, SL Hit Long/Short)

Performance Metrics

NIFTY Futures (15min): 50%+ win rate with ADX filter OFF

Crypto Markets: Requires extensive backtesting before live deployment

Optimal Timeframes: 15-minute to 1-hour charts (patience required for higher timeframes)

Strategy Logic

Entry Signals:

LONG: EMA 9 crosses above EMA 21 + RSI > 55 + ADX > 20 (if enabled)

SHORT: EMA 9 crosses below EMA 21 + RSI < 45 + ADX > 20 (if enabled)

Exit Signals:

Opposite EMA crossover (auto-closes current position)

Stop loss hit at 2% from entry price (tracks candle wicks)

Technical Indicators:

Fast EMA: 9-period (short-term trend)

Slow EMA: 21-period (primary trend)

RSI: 14-period with 55/45 thresholds (momentum confirmation)

ADX: 14-period with 20 threshold (trend strength filter - optional)

Market-Specific Settings

Traditional Markets (NIFTY, Bank NIFTY, S&P Futures, Options)

Recommended Settings:

ADX Filter: Turn OFF (less choppy, cleaner trends)

Timeframe: 15-minute chart

Win Rate: 50%+ on NIFTY Futures

Why No ADX: Traditional markets have more institutional participation and smoother price action, making ADX unnecessary

Cryptocurrency Markets (BTC, ETH, Altcoins)

Recommended Settings:

ADX Filter: Turn ON (ADX > 20)

Timeframe: 15-minute to 1-hour

Extensive backtesting required before live trading

Why ADX: Crypto markets are highly volatile and prone to false breakouts; ADX filters low-quality chop

Best Practices

✅ Backtest thoroughly on your specific instrument and timeframe

✅ Use larger timeframes (1H, 4H) for higher quality signals and better risk/reward

✅ Adjust RSI thresholds based on market volatility (try 52/48 for more signals, 60/40 for fewer but stronger)

✅ Monitor ADX effectiveness - disable for traditional markets, enable for crypto

✅ Proper position sizing - adjust default_qty_value based on your capital and instrument price

✅ Paper trade first - test for 2-4 weeks before risking real capital

Risk Management

Fixed 2% stop loss per trade (adjustable)

Stop loss tracks candle wicks for accurate execution

Positions auto-reverse on opposite signals (no manual intervention needed)

0.075% commission built into backtest (adjust for your broker)

Customization Options

All parameters are adjustable via inputs:

EMA periods (default: 9/21)

RSI length and thresholds (default: 14-period, 55/45 levels)

ADX length and threshold (default: 14-period, 20 threshold)

Stop loss percentage (default: 2%)

Webhook Automation

This strategy includes six distinct alert messages for automated trading:

"Entry Buy" - Long position opened

"Entry Sell" - Short position opened

"Close Long" - Long position closed on opposite crossover

"Close Short" - Short position closed on opposite crossover

"SL Hit Long" - Long stop loss triggered

"SL Hit Short" - Short stop loss triggered

Compatible with Delta Exchange, Binance Futures, 3Commas, Alertatron, and other webhook platforms.

Important Notes

⚠️ Crypto markets require extensive backtesting - volatility patterns differ significantly from traditional markets

⚠️ Higher timeframes = better results - 15min works but 1H/4H provide cleaner signals

⚠️ ADX toggle is critical - OFF for traditional markets, ON for crypto

⚠️ Not financial advice - always conduct your own research and use proper risk management

⚠️ Past performance ≠ future results - backtest results may not reflect live trading conditions

Disclaimer

This strategy is for educational and informational purposes only. Trading futures and options involves substantial risk of loss. Always backtest thoroughly, start with paper trading, and never risk more than you can afford to lose. The author assumes no responsibility for any trading losses incurred using this strategy.

AlgoIndexOS-ES-FuturesAlgoIndexOS — ES Futures Strategy v2.0 (5-Minute RTH)

Scope (read first)

ES on 5-minute only, RTH session. The strategy operates on U.S. Regular Trading Hours (09:30–16:00 ET) using a 5-minute ES chart. It builds an Opening Session Range (OSR) from the RTH open, then runs a breakout engine when internal quality conditions are met. Exits are target-based with an intrabar touch-to-flat safety. Positions are flattened at the RTH session end by default. Alerts can post JSON to your Webhook URL for automation.

What this is

One intraday engine with four curated presets (“Stages”) tuned for distinct segments of the NY session. Stages keep the core logic consistent while applying time-of-day context and conservative governors. Single invite-only listing; not a multi-post suite.

How it trades (high-level)

Range context: Builds and locks the OSR from the opening bell; entries only arm after the range is set.

Quality gating: Trades only when internal trend/volatility/confirmation conditions align (no parameter disclosure).

Breakout execution: Signals at bar close; bracket exits manage take-profit (limit) with an intrabar “TP-touch” safety to avoid phantom fills; optional stop-loss.

Session safety: Positions flat at RTH close by default (time exit).

(No settings or thresholds are disclosed; presets encapsulate research choices.)

Stages (session templates; one engine)

A single Stage selector chooses among four presets optimized for different parts of the RTH session (morning vs mid-day; long/short focus). Internal parameters remain fixed to preserve tested behavior.

Public inputs (kept minimal)

Stage (choose your preset)

TP / SL (points) shown for transparency; effective values are governed by the selected preset to maintain consistency with research.

Optional display overlays (status line/markers) for readability.

Alerts (how to use)

Create an alert on the strategy and choose Strategy → Order fills. Use a webhook if you want automation. The payload includes the exact chart symbol so it works on ES1! or a specific ES contract:

{

"tv_symbol": "{{ticker}}",

"tv_exchange": "{{exchange}}",

"action": "buy|sell|exit",

"price": {{close}},

"time": "{{timenow}}"

}

If your receiver needs a fixed root (e.g., “ES”), map it on your server using tv_symbol for context.

Backtest & assumptions

Backtest assumptions (initial capital, commission, slippage, margin) are user-configurable in TradingView. Results on your chart reflect your settings. This script evaluates ES fills on 5-minute RTH bars; live execution will differ.

Operating notes

Use on ES only, 5-minute timeframe, RTH session.

If you run multiple Stages, use separate charts/tabs and coordinate net exposure in your own tooling if needed.

Publish with a clean chart for clarity.

Disclosures (compliance)

No investment advice. This script is for research/education and tooling only. It does not provide investment, legal, tax, or accounting advice and does not recommend any security, instrument, or strategy. Use at your own risk.

Hypothetical performance (CFTC 4.41). Hypothetical or simulated results have many limitations, and no representation is made that any account will achieve similar outcomes. Past performance is not necessarily indicative of future results.

Futures risk. Trading futures involves substantial risk of loss and is not suitable for all investors. Leverage, gaps, slippage, and connectivity can cause losses exceeding initial investment.

Backtesting limitations. Results depend on data quality, chart resolution, session filters, and user assumptions; live execution will differ.

Intellectual property. © 2025 AlgoIndex. All Rights Reserved. Redistribution, resale, or decompilation prohibited without written consent.

Futures Fighter MO: Multi-Confluence Day Trading System ADX/SMI👋 Strategy Overview: The Multi-Confluence Mashup

The Futures Fighter MO is a comprehensive, multi-layered day trading strategy designed for experienced traders focusing on high-liquidity futures contracts (e.g., NQ, ES, R2K).

This strategy is a sophisticated mashup that uses the 1-minute chart for surgical entries while enforcing strict environmental filtering through higher-timeframe data. We aim to capture high-conviction moves only when multiple, uncorrelated signals align.

🧠 How the Logic Works (Concepts & Confluence)

Our logic is built on four pillars, which must align for a trade to be executed:

Primary Trend Filter

Indicators :

ADX/DMI (15-Minute Lookback)

Role :

Price action is filtered to ensure the ADX (17/14) is above 25, confirming a strong, prevailing market trend (Bullish or Bearish). Trades are strictly rejected during "Flat" (sideways) market regimes.

Entry Signal Types

The system uses multiple entry types:

- 🟢 Trend Long/Short: A breakout/rejection near the 200-Period EMA is confirmed by the primary ADX trend.

- 🔴 Engulfing Rejection: A strong signal when a Bullish/Bearish Engulfing or Doji prints near the long-term 500-Period EMA (emaGOD) while the Stochastic Momentum Index (SMI on 30M) is in an extreme overbought/oversold state (below $-40$ or above $40$).

Volatility & Volume Confirmation

Indicators: Average True Range (ATR) and 20-Period SMA of Volume

Role: Every entry requires a volume spike (Current Volume $> 1.5 \times$ SMA Volume) to confirm that the move is supported by significant liquidity. Volatility is tracked via ATR to define bar range and stop boundaries.

Structural Guardrails

Indicators: Daily Pivot Points (PP, S1-S3, R1-R3)

Role: Trades are disabled if the current bar's price range intersects with a Daily Pivot Point. This is a critical filter to avoid high-chop consolidation zones near key structural levels.

📊 Strategy Results & Required Disclosures

I strive to publish backtesting results that are transparent and realistic for the retail futures trader.

- Initial Capital: $50,000 - A realistic base for Mini/Micro futures contracts.

- Order Size: 1 Contract (Pyramiding up to 3) - Conservative risk relative to the account size.

- Commission: $0.11 USD per order - Represents realistic costs for low-cost brokers.

- Slippage: 2 Ticks - Accounts for expected market friction.

⚠️ Risk Management & Deviations

Stop-Loss: The strategy uses a dynamic stop-loss system where positions are closed upon a reversal (e.g., breaking the 50-Period EMA or failure to hold a Pivot Point), rather than a fixed tick-based stop. This is suited for experienced traders using a low relative risk (single Micro-contract entry) on a larger account. Users must confirm that the first entry's maximum potential loss remains below $10\%$ of their capital for compliance.

Trade Sample Size: Due to data limitations of the TradingView Essential plan (showing $\approx 50$ trades over 2 weeks), the sample size is under the ideal $100+$ target. Justification: This system is designed to generate signals across a portfolio of correlated futures markets (NQ, ES, R2K, Gold, Crude), meaning the real sample size for a user tracking the portfolio is significantly higher.

Drawdown Control: This strategy is designed for manual management. It requires the user to turn the script/alerts OFF after a significant drawdown and only reactivate it once a recovery trend is established externally.

The strategy uses a combination of dynamic trailing stops, structural support/resistance zones, and a fixed profit target to manage open positions.

🛑 Strategy Exit Logic

1. General Stop-Loss (Dynamic Trailing Stop)

These conditions act as the primary dynamic stop, closing the position if the market reverses past a key Moving Average (MA):

- Long Positions Closed When: The current bar's close crosses under the 50-Period EMA (emaLong).

- Short Positions Closed When: The current bar's close crosses above the 50-Period EMA (emaLong).

2. Profit Target (Fixed Percentage)

The script includes a general exit based on a user-defined profit percentage:

Take Profit Trigger: The position is closed when the currentProfitPercent meets or exceeds the input Profit Target (%) (default is 1.0% of the entry price).

3. Structural Exits (Daily Pivot Points)

These exits are high-priority, "close all" orders that trigger when the price fails to hold or reclaims a recent Daily Pivot Point, suggesting a failure of the current move.

- VR Close All - Long ($\sym{size} > 0$) - Price crosses under a Daily Resistance Level (R1, R2, or R3) minus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Resistance as support.

- VS Close All - Short ($\sym{size} < 0$) - Price crosses above a Daily Support Level (S1, S2, or S3) plus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Support as resistance.

4. Trend Failure Exit (Trend-Following Signals Only)

This exit protects against holding a position when the primary high-timeframe trend used for the entry has failed:

- Long Positions Closed When: The primary trend is no longer "bullish" for more than 2 consecutive bars (i.e., it turned "bearish" or "flat").

- Short Positions Closed When: The primary trend is no longer "bearish" for more than 2 consecutive bars (i.e., it turned "bullish" or "flat").

5. End of Day (EOD) Session Control

The final hard exits based on time:

- End of Session (EoS): At 11:30 AM, new trades are disabled (TradingDay := false). Open positions are kept.

- End of Day (EoD): At 1:30 PM, all remaining open positions are closed (strategy.close_all).

🤝 Development & Disclaimer

This script and description were created with assistance from Gemini and GitHub Copilot. My focus is on helping fellow real estate investors and day traders develop mechanically sound systems.

Disclaimer: This is for educational purposes only and does not constitute financial advice. Always abide by the Realtor Code and manage your own risk.

NY VIX Channel Trend US Futures Day Trade StrategyNY VIX Channel Trend Strategy

Summary in one paragraph

Session anchored intraday strategy for index futures such as ES and NQ on one to fifteen minute charts. It acts only after the first configurable window of New York Regular Trading Hours and uses a VIX derived daily implied move to form a realistic channel from the session open. Originality comes from using a pure implied volatility yardstick as portable support and resistance, then committing in the direction of the first window close relative to the open. Add it to a clean chart and trade the simple visuals. For conservative alerts use on bar close.

Scope and intent

• Markets. Index futures ES and NQ

• Timeframes. One to thirty minutes

• Default demo. ES1 on five minutes

• Purpose. Provide a portable intraday yardstick for entries and exits without curve fitting

• Limits. This is a strategy. Orders are simulated on standard candles

Originality and usefulness

• Unique concept. A VIX only channel anchored at 09:30 New York plus a single window trend test

• Addresses. False urgency at session open and unrealistic bands from arbitrary multipliers

• Testability. Every input is visible and the channel is plotted so users can audit behavior

• Portable yardstick. Daily implied move equals VIX percent divided by square root of two hundred fifty two

• Protected status. None. Method and use are fully disclosed

Method overview in plain language

Take the daily VIX or VIX9D value, convert it to a daily fraction by dividing by square root of two hundred fifty two, then anchor a symmetric channel at the New York session open. Observe the first N minutes. If that window closes above the open the bias is long. If it closes below the open the bias is short. One trade per session. Exits occur at the channel boundary or at a bracket based on a user selected VIX factor. Positions are closed a set number of minutes before the session ends.

Base measures

Return basis. The daily implied move unit equals VIX percent divided by square root of two hundred fifty two and serves as the distance unit for targets and stops.

Components

• VIX Channel. Top, mid, bottom lines anchored at 09:30 New York. No extra multipliers

• Window Trend. Close of the first N minutes relative to the session open sets direction

• Risk Bracket. Take profit and stop loss equal to VIX unit times user factor

• Session Window. Uses the exchange time of the chart

Fusion rule

Minimum gates count equals one. The trade only arms after the window has elapsed and a direction exists. One entry per session.

Signal rule

• Long when the window close is above the session open and the window has completed

• Short when the window close is below the session open and the window has completed

• Exit on channel touch. Long exits at the top. Short exits at the bottom

• Flat thirty minutes before the session close or at the user setting

Inputs with guidance

Setup

• Use VIX9D. Width source. Typical true for fast tone or false for baseline

• Use daily OPEN. Toggle for sensitivity to overnight changes

Logic

• Window minutes. Five to one hundred twenty. Larger values delay entries and reduce whipsaw

• VIX factor for TP. Zero point five to two. Raising it widens the profit target

• VIX factor for SL. Zero point five to two. Raising it widens the stop

• Exit minutes before close. Fifteen to ninety. Raising it exits earlier

Properties visible in this publication

• Initial capital one hundred thousand USD

• Base currency USD

• request.security uses lookahead off

• Commission cash per contract two point five $ per each contract. Slippage one tick

• Default order size method FIXED with value one contract. Pyramiding zero. Process orders on close ON. Bar magnifier OFF. Recalculate after order is filled OFF. Calc on every tick ON

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Fills and slippage vary by venue. Shapes can move while a bar forms and settle on close. Strategy uses standard candles.

Honest limitations and failure modes

Economic releases and thin liquidity can break the channel. Very quiet regimes can reduce signal contrast. Session windows follow the exchange time of the chart. If both stop and target can be hit within one bar, assume stop first for conservative reading without bar magnifier.

Works best in liquid hours of New York RTH. Very large gaps and surprise news may exceed the implied channel. Always validate on the symbols you trade.

Entries and exits

• Entry logic. After the first window, go long if the window close is above the session open, go short if below

• Exit logic. Long exits at the channel top or at the take profit or stop. Short exits at the channel bottom or at the take profit or stop. Flat before session close by the configured minutes

• Risk model. Initial stop and target based on the VIX unit times user factors. No trail and no break even. No cooldown

• Tie handling. Treat as stop first for conservative interpretation

Position sizing

Fixed size one contract per trade. Target risk per trade should generally remain near one percent of account equity. Risk is based on the daily volatility value, the max loss from the tests for one year duration with 5min chart was 4%, while the avg loss was below <1% of the total capital.

If you have any questions please let me know. Thank you for coming by !

Kz GC1! ORBStrategy that trades breakouts on GC1! futures on the 5min timeframe. It also works on MGC1! for lower drawdown and to manage Apex and Top Step accounts with the lower risk.

Risk Disclaimer:

Past results as well as strategy tester reports do not indicate future performance. Guarantees do not exist in trading. By using this strategy you risk losing all your money.

Important:

It trades all days that markets are open. Set times may be seen on settings. Trades multiple times a day sometimes.

It works on the 5 and 15min timeframe only. Results are better on 5min timeframe.

The settings are optimized already for GC1! on the 5min timeframe.

How it works:

Every trading day it measures the range of the first 15min candle of pre-selected hours. As soon as price closes above or below on the 15min timeframe, it will trade the breakout targeting a set risk to reward ratio. SL on the opposite side of the range.

Settings:

Hourly Trading Hours: These are the times that worked best for this strategy. All boxes should be checked for best results. Excluded times were when it performed bad which is why those times have been left out.

ORB Formation Period: This setting determines on which timeframe candle has to close outside the opening range box in order to take a trade. It's set to 15min by default because this is what worked by far the best

Entry Type: Entries are immediate instead of waiting for a pull back to enter on a limit order.

Limit Orders: If enabled, the strategy will place a pending order x points from the current price, instead of a market order. Immediate orders are enabled by default for a better performance. Important: It doesn't actually place a limit order. The strategy will just wait for a pullback and then enter with a market order. It's more like a hidden limit order.

Limit Order Offset Points: If you have limit orders enabled, this setting determines how many points from the current price the limit order will be placed.

FVG Detection Type: How fast it detects the fair value gaps. Standard detection over immediate had better performance

Risk Type: You can chose either between Fixed USD Amount, Risk per Trade in % or Fixed Contract Size. By default it's set to fixed contract size.

Risk Amount (USD or Contracts): This setting is to set how many USD or how many contracts you want to risk per trade. Make sure to check which risk type you have selected before you choose the risk amount.

Take Profit Multiplier: This is simply the total SL size in points multiplied by x.

Example: If you put 2, you get a 2:1 Risk to Reward Ratio. By Default it's set to 2.5 because this gave the best results in backtests.

Stop Loss Padding: This is simply the buffer in points that is added to the SL for safety reasons. If you have it on 0, the SL will be at the exact price of the opposite side of the range. By default it's set to 5 because this is what delivered the best results in backtests.

Stop Loss Placement: This determines where the stop loss gets placed for the order. It has been set to ORB Range by default as this delivered the best results.

Max Trades Per Hour: This allows the user to decide how many trades are taken an hour. 1 is been set to default for best results

Visual Settings: Check boxes to show orb range, FVG's, Entry points, and trade visualization boxes.

Backtest Settings:

For the backtest the commissions were set to 1.29USD per contract and .35USD for micros which is the highest amount Tradovate charges Margin was not accounted for because typically on prop accounts you can use way more contracts than you need for the extremely low max drawdown. Margin would be important on personal accounts but even there typically it's not an issue at all especially because this strategy runs on the 15min timeframe so it won't use a lot of contracts anyways.

Why the source code is hidden:

The source code is hidden because I invested a lot of time and money into developing this strategy and optimizing it with paid 3rd party software.

AlgoAIDESIGNED FOR HEIKEN ASHI BARS

Gain Access here: algoai.store

AlgoAI

The Dark Edge of Trading

An AI-powered TradingView strategy that thrives across all markets. Short altcoin pumps. Ride NAS100 waves. Dominate gold, FX, stocks, and futures — all with one AI brain.

#1

Semi-Automatic Trading (Recommended)

Set up alerts on AlgoAI signals. As they come in, grade the setups and choose to enter manually. This gives you full control while leveraging AI precision.

#2

Fully Automated Trading

Pass signals via webhooks to TradersPost for futures or PineConnector for FX. Note: When running fully automated, it's suggested to use long-only or short-only mode to avoid side swiping and potential unintended drawdown.

BITSTAMP:BTCUSD

BOCS Channel Scalper Strategy - Automated Mean Reversion System# BOCS Channel Scalper Strategy - Automated Mean Reversion System

## WHAT THIS STRATEGY DOES:

This is an automated mean reversion trading strategy that identifies consolidation channels through volatility analysis and executes scalp trades when price enters entry zones near channel boundaries. Unlike breakout strategies, this system assumes price will revert to the channel mean, taking profits as price bounces back from extremes. Position sizing is fully customizable with three methods: fixed contracts, percentage of equity, or fixed dollar amount. Stop losses are placed just outside channel boundaries with take profits calculated either as fixed points or as a percentage of channel range.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This strategy is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Version**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the scalper ideal for active day traders who want continuous opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased trade frequency also means higher commission costs and requires tighter risk management.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The strategy normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The strategy tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The strategy uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. This captures mean reversion opportunities as price reaches channel extremes.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents signal spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long signal will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The strategy includes a multi-timeframe ATR filter to avoid trading during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while trading on 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Trading enabled

- If ATR < threshold: No signals fire

This prevents entries during dead zones where mean reversion is unreliable due to insufficient price movement.

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. Larger percentages aim for opposite channel edge.

### Stop Loss Placement:

Stop losses are placed just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. If price breaks through, the range is no longer valid and position exits.

### Trade Execution Logic:

When entry conditions are met (price in zone, cooldown satisfied, ATR filter passed, no existing position):

1. Calculate entry price at zone boundary

2. Calculate TP and SL based on selected method

3. Execute strategy.entry() with calculated position size

4. Place strategy.exit() with TP limit and SL stop orders

5. Update info table with active trade details

The strategy enforces one position at a time by checking strategy.position_size == 0 before entry.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

### Position Sizing System:

Three methods calculate position size:

**Fixed Contracts**:

- Uses exact contract quantity specified in settings

- Best for futures traders (e.g., "trade 2 NQ contracts")

**Percentage of Equity**:

- position_size = (strategy.equity × equity_pct / 100) / close

- Dynamically scales with account growth

**Cash Amount**:

- position_size = cash_amount / close

- Maintains consistent dollar exposure regardless of price

## INPUT PARAMETERS:

### Position Sizing:

- **Position Size Type**: Choose Fixed Contracts, % of Equity, or Cash Amount

- **Number of Contracts**: Fixed quantity per trade (1-1000)

- **% of Equity**: Percentage of account to allocate (1-100%)

- **Cash Amount**: Dollar value per position ($100+)

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long entries on/off

- **Enable Short Scalps**: Toggle short entries on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between signals (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for trade enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time strategy status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Color Settings**: Customize long/short/TP/SL colors

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short entries

- **Active TP/SL lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing position status, channel state, last signal, entry/TP/SL prices, and ATR status

## HOW TO USE:

### For 1-3 Minute Scalping (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars

- Position Size: 1-2 contracts

### For 5-15 Minute Day Trading:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- Position Size: Fixed contracts or 5-10% equity

### For 30-60 Minute Swing Scalping:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- Position Size: % of equity recommended

## BACKTEST CONSIDERATIONS:

- Strategy performs best in ranging, mean-reverting markets

- Strong trending markets produce more stop losses as price breaks channels

- ATR filter significantly reduces trade count but improves quality during low volatility

- Cooldown period trades signal quantity for signal quality

- Commission and slippage materially impact sub-5-minute timeframe performance

- Shorter timeframes require tighter entry zones (15-20%) to catch quick reversions

- % of Channel TP adapts better to varying channel sizes than fixed points

- Fixed contract sizing recommended for consistent risk per trade in futures

**Backtesting Parameters Used**: This strategy was developed and tested using realistic commission and slippage values to provide accurate performance expectations. Recommended settings: Commission of $1.40 per side (typical for NQ futures through discount brokers), slippage of 2 ticks to account for execution delays on fast-moving scalp entries. These values reflect real-world trading costs that active scalpers will encounter. Backtest results without proper cost simulation will significantly overstate profitability.

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features require data feed with volume information but are optional for core functionality.

## KNOWN LIMITATIONS:

- Immediate touch entry can fire multiple times in choppy zones without adequate cooldown

- Channel deletion at 10-tick breaks may be too aggressive or lenient depending on instrument tick size

- ATR filter from lower timeframes requires higher-tier TradingView subscription (request.security limitation)

- Mean reversion logic fails in strong breakout scenarios leading to stop loss hits

- Position sizing via % of equity or cash amount calculates based on close price, may differ from actual fill price

- No partial closing capability - full position exits at TP or SL only

- Strategy does not account for gap openings or overnight holds

## RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance does not guarantee future results. This strategy is for educational purposes and backtesting only. Mean reversion strategies can experience extended drawdowns during trending markets. Stop losses may not fill at intended levels during extreme volatility or gaps. Thoroughly test on historical data and paper trade before risking real capital. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Automated trading systems can malfunction - monitor all live positions actively.

## ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based signals, multi-timeframe ATR volatility filtering, flexible position sizing (fixed/percentage/cash), cooldown period filtering, dual TP methods (fixed points vs channel percentage), automated strategy execution with exit management, and real-time position monitoring table.

FlowStateTrader FlowState Trader - Advanced Time-Filtered Strategy

## Overview

FlowState Trader is a sophisticated algorithmic trading strategy that combines precision entry signals with intelligent time-based filtering and adaptive risk management. Built for traders seeking to achieve their optimal performance state, FlowState identifies high-probability trading opportunities within user-defined time windows while employing dynamic trailing stops and partial position management.

## Core Strategy Philosophy

FlowState Trader operates on the principle that peak trading performance occurs when three elements align: **Focus** (precise entry signals), **Flow** (optimal time windows), and **State** (intelligent position management). This strategy excels at finding reversal opportunities at key support and resistance levels while filtering out suboptimal trading periods to keep traders in their optimal flow state.

## Key Features

### 🎯 Focus Entry System

**Support/Resistance Zone Trading**:

- Dynamic identification of key price levels using configurable lookback periods

- Entry signals triggered when price interacts with these critical zones

- Volume confirmation ensures genuine breakout/reversal momentum

- Trend filter alignment prevents counter-trend disasters

**Entry Conditions**:

- **Long Signals**: Price closes above support buffer, touches support level, with above-average volume

- **Short Signals**: Price closes below resistance buffer, touches resistance level, with above-average volume

- Optional trend filter using EMA or SMA for directional bias confirmation

### ⏰ FlowState Time Filtering System

**Comprehensive Time Controls**:

- **12-Hour Format Trading Windows**: User-friendly AM/PM time selection

- **Multi-Timezone Support**: UTC, EST, PST, CST with automatic conversion

- **Day-of-Week Filtering**: Trade only weekdays, weekends, or both

- **Lunch Hour Avoidance**: Automatically skips low-volume lunch periods (12-1 PM)

- **Visual Time Indicators**: Background coloring shows active/inactive trading periods

**Smart Time Features**:

- Handles overnight trading sessions seamlessly

- Prevents trades during historically poor performance periods

- Customizable trading hours for different market sessions

- Real-time trading window status in dashboard

### 🛡️ Adaptive Risk Management

**Multi-Level Take Profit System**:

- **TP1**: First profit target with optional partial position closure

- **TP2**: Final profit target for remaining position

- **Flexible Scaling**: Choose number of contracts to close at each level

**Dynamic Trailing Stop Technology**:

- **Three Operating Modes**:

- **Conservative**: Earlier activation, tighter trailing (protect profits)

- **Balanced**: Optimal risk/reward balance (recommended)

- **Aggressive**: Later activation, wider trailing (let winners run)

- **ATR-Based Calculations**: Adapts to current market volatility

- **Automatic Activation**: Engages when position reaches profitability threshold

### 📊 Intelligent Position Sizing

**Contract-Based Management**:

- Configurable entry quantity (1-1000 contracts)

- Partial close quantities for profit-taking

- Clear position tracking and P&L monitoring

- Real-time position status updates

### 🎨 Professional Visualization

**Enhanced Chart Elements**:

- **Entry Zone Highlighting**: Clear visual identification of trading opportunities

- **Dynamic Risk/Reward Lines**: Real-time TP and SL levels with price labels

- **Trailing Stop Visualization**: Live tracking of adaptive stop levels

- **Support/Resistance Lines**: Key level identification

- **Time Window Background**: Visual confirmation of active trading periods

**Dual Dashboard System**:

- **Strategy Dashboard**: Real-time position info, settings status, and current levels

- **Performance Scorecard**: Live P&L tracking, win rates, and trade statistics

- **Customizable Sizing**: Small, Medium, or Large display options

### ⚙️ Comprehensive Customization

**Core Strategy Settings**:

- **Lookback Period**: Support/resistance calculation period (5-100 bars)

- **ATR Configuration**: Period and multipliers for stops/targets

- **Reward-to-Risk Ratios**: Customizable profit target calculations

- **Trend Filter Options**: EMA/SMA selection with adjustable periods

**Time Filter Controls**:

- **Trading Hours**: Start/end times in 12-hour format

- **Timezone Selection**: Four major timezone options

- **Day Restrictions**: Weekend-only, weekday-only, or unrestricted

- **Session Management**: Lunch hour avoidance and custom periods

**Risk Management Options**:

- **Trailing Stop Modes**: Conservative/Balanced/Aggressive presets

- **Partial Close Settings**: Enable/disable with custom quantities

- **Alert System**: Comprehensive notifications for all trade events

### 📈 Performance Tracking

**Real-Time Metrics**:

- Net profit/loss calculation

- Win rate percentage

- Profit factor analysis

- Maximum drawdown tracking

- Total trade count and breakdown

- Current position P&L

**Trade Analytics**:

- Winner/loser ratio tracking

- Real-time performance scorecard

- Strategy effectiveness monitoring

- Risk-adjusted return metrics

### 🔔 Alert System

**Comprehensive Notifications**:

- Entry signal alerts with price and quantity

- Take profit level hits (TP1 and TP2)

- Stop loss activations

- Trailing stop engagements

- Position closure notifications

## Strategy Logic Deep Dive

### Entry Signal Generation

The strategy identifies high-probability reversal points by combining multiple confirmation factors:

1. **Price Action**: Looks for price interaction with key support/resistance levels

2. **Volume Confirmation**: Ensures sufficient market interest and liquidity

3. **Trend Alignment**: Optional filter prevents counter-trend positions

4. **Time Validation**: Only trades during user-defined optimal periods

5. **Zone Analysis**: Entry occurs within calculated buffer zones around key levels

### Risk Management Philosophy

FlowState Trader employs a three-tier risk management approach:

1. **Initial Protection**: ATR-based stop losses set at strategy entry

2. **Profit Preservation**: Trailing stops activate once position becomes profitable

3. **Scaled Exit**: Partial profit-taking allows for both security and potential

### Time-Based Edge

The time filtering system recognizes that not all trading hours are equal:

- Avoids low-volume, high-spread periods

- Focuses on optimal liquidity windows

- Prevents trading during news events (lunch hours)

- Allows customization for different market sessions

## Best Practices and Optimization

### Recommended Settings

**For Scalping (1-5 minute charts)**:

- Lookback Period: 10-20

- ATR Period: 14

- Trailing Stop: Conservative mode

- Time Filter: Major session hours only

**For Day Trading (15-60 minute charts)**:

- Lookback Period: 20-30

- ATR Period: 14-21

- Trailing Stop: Balanced mode

- Time Filter: Extended trading hours

**For Swing Trading (4H+ charts)**:

- Lookback Period: 30-50

- ATR Period: 21+

- Trailing Stop: Aggressive mode

- Time Filter: Disabled or very broad

### Market Compatibility

- **Forex**: Excellent for major pairs during active sessions

- **Stocks**: Ideal for liquid stocks during market hours

- **Futures**: Perfect for index and commodity futures

- **Crypto**: Effective on major cryptocurrencies (24/7 capability)

### Risk Considerations

- **Market Conditions**: Performance varies with volatility regimes

- **Timeframe Selection**: Lower timeframes require tighter risk management

- **Position Sizing**: Never risk more than 1-2% of account per trade

- **Backtesting**: Always test on historical data before live implementation

## Educational Value

FlowState serves as an excellent learning tool for:

- Understanding support/resistance trading

- Learning proper time-based filtering

- Mastering trailing stop techniques

- Developing systematic trading approaches

- Risk management best practices

## Disclaimer

This strategy is for educational and informational purposes only. Past performance does not guarantee future results. Trading involves substantial risk of loss and is not suitable for all investors. Users should thoroughly backtest the strategy and understand all risks before live trading. Always use proper position sizing and never risk more than you can afford to lose.

---

*FlowState Trader represents the evolution of systematic trading - combining classical technical analysis with modern risk management and intelligent time filtering to help traders achieve their optimal performance state through systematic, disciplined execution.*

Spread Mean Reversion Strategy [SciQua]╭───────────────────────────────────────╮

Spread Mean Reversion Strategy

╰───────────────────────────────────────╯

This invite-only futures spread strategy applies a statistical mean reversion framework, executing limit orders exclusively at calculated Z-score thresholds for precise, rules-based entries and exits. It is designed for CME-style spreads and synthetic instruments with well-defined reversion tendencies.

╭────────────╮

Core Concept

╰────────────╯

The strategy calculates a rolling mean and standard deviation of a chosen spread or synthetic price series, then computes the Z-score to measure deviation from the mean in standard deviation units.

Long entries trigger when Z crosses upward through a negative entry threshold (`-devEnter`). A buy limit is placed exactly at the price corresponding to that Z-score, optionally offset by a configurable tick amount.

Short entries trigger when Z crosses downward through a positive entry threshold (`+devEnter`). A sell limit is placed at the corresponding threshold price, also with optional offset.

Exits use the same threshold method, with an independent `Close Limit Offset` to fine-tune exit placement.

╭────────────╮

Key Features

╰────────────╯

Persistence filter – Requires the Z-score to remain beyond threshold for a configurable number of bars before entry.

Cooldown after exits – Prevents immediate re-entry to reduce over-trading.

Daily and weekend flattening – Force-flattens positions via limit orders before exchange maintenance breaks and weekend closes.

Auto-rollover detection with persistence – Detects when the second contract month’s daily volume exceeds the first for a set number of days, then blocks new entries (optional).

Configurable tick offsets – Independently adjust entry and exit levels relative to threshold prices.

Minimum spread width filter – Blocks trades when long/short entry thresholds are too close together.

Contract multiplier override – Allows correct sizing for synthetic symbols where `syminfo.pointvalue` is incorrect or missing.

Limit-only execution – All entries, exits, and forced-flat actions are executed with limit orders for price control.

╭────────────────────╮

Entry Blocking Rules

╰────────────────────╯

New trades are blocked:

During daily maintenance break pre-windows

During weekend close pre-windows

After rollover triggers, if `Block After Roll` is enabled

╭────────────────────────╮

Intended Markets & Usage

╰────────────────────────╯

Built for futures spreads and synthetic instruments , including calendar spreads.

Performs best in markets with clear seasonal or statistical mean-reverting tendencies.

Not designed for strongly trending, non-reverting markets.

╭──────────────────────────╮

Risk Management & Defaults

╰──────────────────────────╯

Fixed default position size of 1 contract (qty calc function available for customization).

Realistic commission and slippage assumptions pre-set.

Pyramiding disabled by default.

Default Z-score levels: Entry at ±2.0, Exit at ±0.5.

Separate tick offset controls for entries and exits.

Note: This strategy is for research and backtesting purposes only. Past performance does not guarantee future results. All use is subject to explicit written permission from the author.

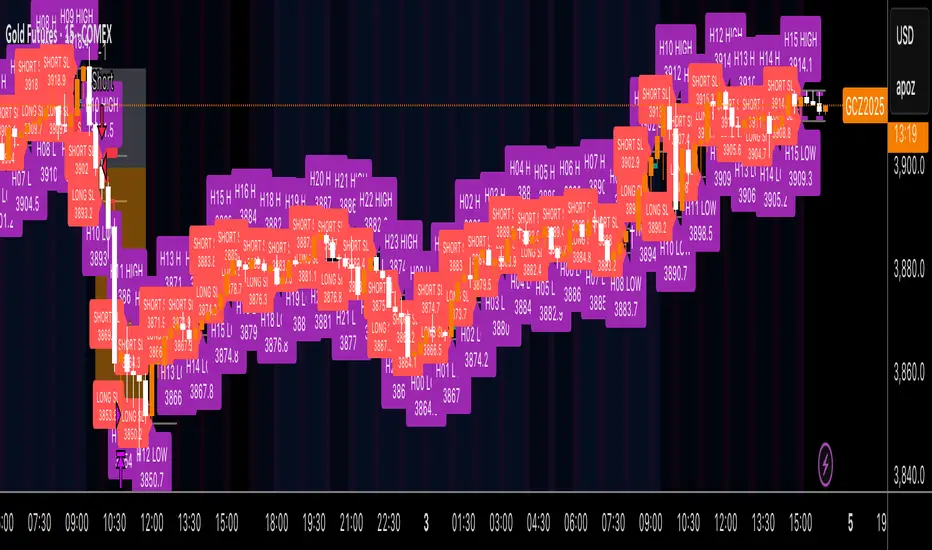

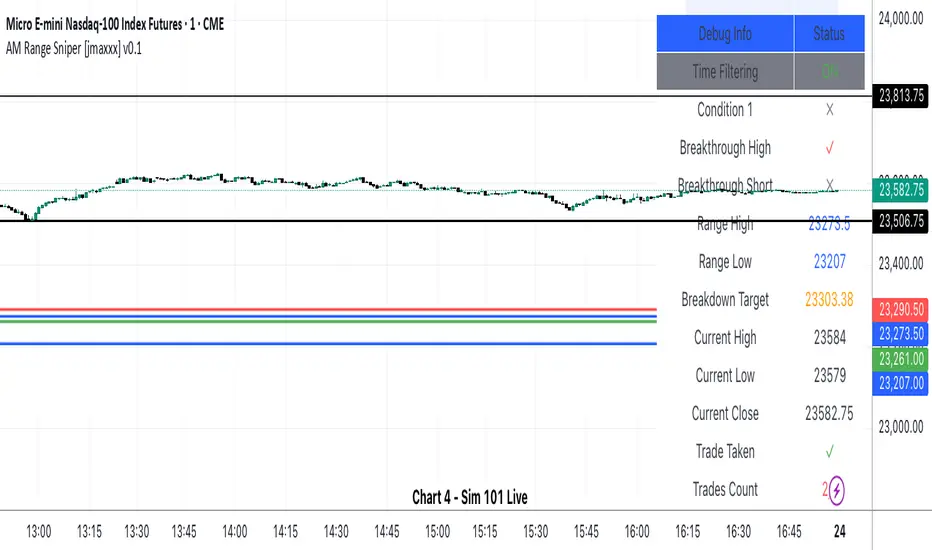

AM Range Sniper [jmaxxx]AM Range Sniper

Overview

AM Range Sniper is a sophisticated morning session trading strategy designed for Micro E-mini Nasdaq-100 Index Futures (MNQ). This strategy capitalizes on the critical 8:30-9:30 AM EST range formation period, implementing precise entry and exit mechanics with advanced risk management.

Key Features

🕐 Time-Based Range Analysis

Range Definition: Automatically identifies and tracks the 8:30-9:30 AM EST range

Trading Window: Active trading from 9:30 AM to 11:00 AM EST (extended for second chance trades)

Session Management: Daily reset ensures clean state for each trading session

🎯 Multiple Entry Patterns

Breakthrough/Retest: Captures price breakthroughs above range with retest opportunities

Long/Short Opportunities: Comprehensive coverage of both directional moves

Breakdown: Identifies bearish breakdowns below range support

Break Up: Detects bullish breakups above range resistance

Range Sweeps: Monitors for range high/low sweeps with reversal entries

⚡ Advanced Risk Management

Configurable Stop Losses: Tick-based stop losses for each trade type

Take Profit Targets: Automatic target calculations based on range size

Hard Close Protection: Automatic position closure at 4 PM EST

Second Chance Feature: Optional second trade opportunity if first trade loses

🔧 Professional Features

Visual Stop Loss Lines: Real-time stop loss visualization on chart

Debug Information Panel: Comprehensive status monitoring

Alert Integration: Customizable alert messages for entries/exits

Flexible Time Settings: Adjustable for different timezones

Strategy Logic

Range Formation (8:30-9:30 AM)

The strategy monitors the first hour of trading to establish the day's range. This range serves as the foundation for all subsequent trading decisions.

Entry Conditions

Breakthrough: Price breaks above range high with retest rejection

Breakdown: Price breaks below range low with confirmed bearish momentum

Break Up: Price breaks above range high with strong bullish confirmation

Sweep Entries: Range high/low sweeps followed by reversal signals

Risk Management

Stop Loss: Configurable tick-based stops for each trade type

Take Profit: 1.5x range size targets for breakdown/breakup trades

Position Sizing: Percentage-based position sizing

Session Limits: Maximum 2 trades per session (with second chance feature)

Settings & Customization

Core Parameters

Enable/disable individual entry patterns

Configurable stop loss levels (1-500 ticks)

Second chance feature toggle

Previous day level integration

Visual Customization

Customizable stop loss colors and widths

Debug panel visibility

Range line styling

Alert Configuration

Custom entry/exit alert messages

***** Automate With *****

APEX

NinjaTrader

Crosstrade.io ( promo code JMAXXX )

Performance & Reliability

Precision Focused: Waits for high-probability setups

Risk-Aware: Comprehensive stop loss and position management

Session-Based: Clean daily resets prevent carryover issues

Professional Grade: Designed for serious traders

Ideal For

Day Traders: Morning session specialists

Futures Traders: MNQ and similar instruments

Range Traders: Traders who capitalize on range breakouts

Risk-Conscious Traders: Those who prioritize risk management

Disclaimer

This strategy is for educational and informational purposes. Past performance does not guarantee future results. Always test thoroughly on historical data and paper trading before live implementation. Risk management is crucial - never risk more than you can afford to lose.

Created by jmaxxx - Professional trading strategy developer

For questions, feedback, or customization requests, please leave a comment below.

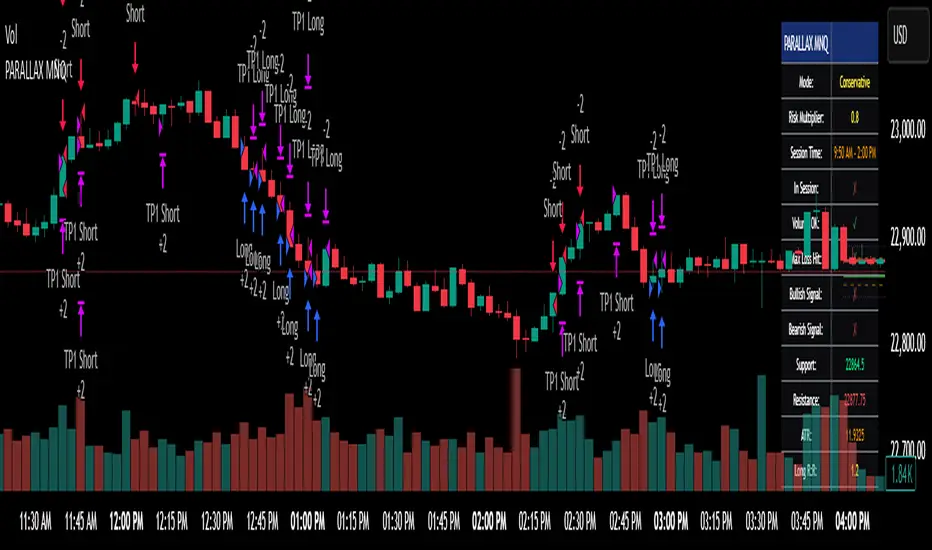

Parallax Momentum MNQ Strategy# 📈 Parallax Momentum MNQ Strategy

## Overview

The Parallax Momentum MNQ Strategy is a sophisticated support/resistance breakout system specifically designed for Micro Nasdaq futures (MNQ) trading (also works on minis). This strategy combines dynamic level detection with momentum confirmation to identify high-probability entry opportunities while maintaining strict risk management protocols.

## 🎯 Key Features

### Core Strategy Logic

- **Dynamic Support/Resistance Detection**: Automatically identifies key levels using configurable lookback periods

- **Momentum Confirmation**: Volume-based filtering ensures trades align with market momentum

- **ATR-Based Risk Management**: Adaptive stop losses and take profits based on market volatility

- **Dual Entry System**: Both long and short opportunities with limit order execution

### Risk Management

- **ATR-Adaptive Stops**: Stop losses and take profits automatically adjust to market volatility

- **Reward-to-Risk Ratios**: Configurable R:R ratios with default 2:1 minimum

- **Maximum Loss Protection**: Optional daily loss limits to prevent overtrading

- **Session Time Filtering**: Trade only during specified market hours

### Strategy Modes

- **Conservative Mode**: 0.8x risk multiplier for cautious trading

- **Balanced Mode**: Standard 1.0x risk multiplier (default)

- **Aggressive Mode**: 1.2x risk multiplier for active trading

## 📊 Visual Features

### Dashboard Display

- Real-time strategy status and performance metrics

- Current support/resistance levels and ATR values

- Live risk-to-reward ratios for potential trades

- Win rate, profit factor, and drawdown statistics

- Adjustable dashboard size and positioning

### Chart Indicators

- Support and resistance lines with labels

- ATR-based levels (+/-1 ATR and +/-2 ATR)

- Dynamic visual updates as levels change

- Configurable line extensions and styling

## ⚙️ Configuration Options

### Entry Filters

- **Volume Filter**: Optional volume confirmation above SMA

- **Session Time Filter**: 12-hour format time restrictions

- **ATR vs Fixed Stops**: Choose between adaptive or fixed tick-based exits

### Risk Controls

- **ATR Period**: Default 14-period ATR calculation

- **Stop Loss Multiplier**: ATR-based stop distance (default 1.5x)

- **Take Profit Multiplier**: ATR-based target distance (default 1.5x)

- **Secondary Take Profit**: Optional TP2 with position scaling

## 📋 How It Works

### Entry Conditions

**Long Trades**: Triggered when price closes above support buffer but low touches support level, with volume and session confirmation

**Short Trades**: Triggered when price closes below resistance buffer but high touches resistance level, with volume and session confirmation

### Exit Strategy

- **Primary Take Profit**: ATR-based target with 2:1 R:R minimum

- **Stop Loss**: ATR-based protective stop

- **Optional TP2**: Extended target for partial profit taking

- **One Trade at a Time**: No overlapping positions

## 🎛️ Default Settings

- **Lookback Period**: 20 bars for support/resistance detection

- **ATR Period**: 14 bars for volatility calculation

- **Stop Loss**: 1.5x ATR from entry

- **Take Profit**: 1.5x ATR with 2:1 reward-to-risk ratio

- **Session**: 7:30 AM - 2:00 PM (configurable)

## ⚠️ Important Notes

### Risk Disclaimer

- This strategy is for educational and informational purposes only

- Past performance does not guarantee future results

- Always use proper position sizing and risk management

- Test thoroughly on historical data before live trading

- Consider market conditions and volatility when using

### Best Practices

- Backtest on sufficient historical data

- Start with conservative mode for new users

- Monitor performance regularly and adjust parameters as needed

- Use appropriate position sizing for your account

- Consider broker commissions and slippage in live trading

## 🔧 Customization

The strategy offers extensive customization options including:

- Adjustable time sessions with AM/PM format

- Configurable ATR and risk parameters

- Optional maximum daily loss limits

- Dashboard size and position controls

- Visual element toggles and styling

## 📈 Ideal For

- MNQ (Micro Nasdaq) futures traders

- Intraday momentum strategies

- Traders seeking systematic entry/exit rules

- Risk-conscious traders wanting automated stops

- Both beginner and experienced algorithmic traders

---

**Version**: Pine Script v5 Compatible

**Timeframe**: Works on multiple timeframes (test on 1m, 3m, 5m, 15m)

**Market**: Optimized for MNQ but adaptable to other instruments

**Strategy Type**: Trend following with momentum confirmation

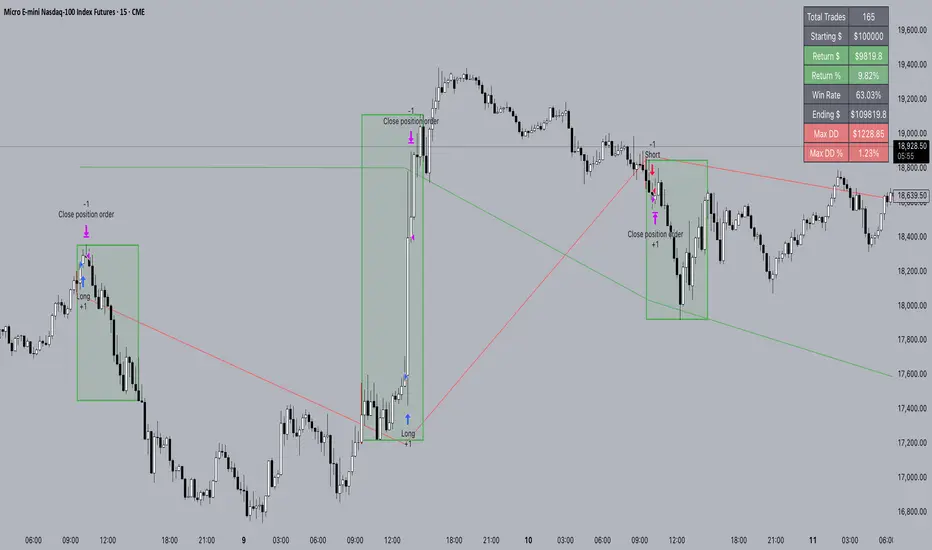

Opening-Range BreakoutNote: Default trading date range looks mediocre. Set date range to "Entire History" to see full effect of the strategy. 50.91% profitable trades, 1.178 profit factor, steady profits and limited drawdown. Total P&L: $154,141.18, Max Drawdown: $18,624.36. High R^2

█ Overview

The Opening-Range Breakout strategy is a mechanical, session‑based day‑trading system designed to capture the initial burst of directional momentum immediately following the market open. It defines a user‑configurable “opening range” window, measures its high and low boundaries, then places breakout stop orders at those levels once the range closes. Built‑in filters on minimum range width, reward‑to‑risk ratios, and optional reversal logic help refine entries and manage risk dynamically.

█ How It Works

Opening‑Range Formation

Between 9:30–10:15 AM ET (configurable), the script tracks the highest high and lowest low to form the day’s opening range box.

On the first bar after the range window closes, the range high (OR_high) and low (OR_low) are “locked in.”

Range‑Width Filter

To avoid false breakouts in low‑volatility mornings, the range must be at least X% of the current price (default 0.35%).

If the measured opening-range width < minimum threshold, no orders are placed that day.

Entry & Order Placement

Long: a stop‑buy order at the opening‑range high.

Short: a stop‑sell order at the opening‑range low.

Only one side can trigger (or both if reverse logic is enabled after a losing trade).

Risk Management

Once triggered, each trade uses an ATR‑style stop-loss defined as a percentage retracement of the range (default 50% of range width).

Profit target is set at a configurable Reward/Risk Ratio (default 1.1×).

Optional: Reverse on Stop‑Loss – if the initial breakout loses, immediately reverse into the opposite side on the same day.

Session Exit

Any open positions are closed at the end of the regular trading day (default 3:45 PM ET window end, with hard flat at session close).

Visual cues are provided via green (range high) and red (range low) step‑line plots directly on the chart, allowing you to see the range box and breakout triggers in real time.

█ Why It Works

Early Momentum Capture: The first 15 – 60 minutes of trading encapsulate overnight news digestion and institutional order flow, creating a well‑defined volatility “range.”

Mechanical Discipline: Clear, rule‑based entries and exits remove emotional guesswork, ensuring consistency.

Volatility Filtering: By requiring a minimum range width, the system avoids choppy, low‑range days where false breakouts are common.

Dynamic Sizing: Stops and targets scale with the opening range, adapting automatically to each day’s volatility environment.

█ How to Use

Set Your Instruments & Timeframe

-Apply to any futures contract on a 1‑ to 5‑minute chart.