QTALibrary "QTA"

This is simple library for basic Quantitative Technical Analysis for retail investors. One example of it being used can be seen here ().

calculateKellyRatio(returns)

Parameters:

returns (array) : An array of floats representing the returns from bets.

Returns: The calculated Kelly Ratio, which indicates the optimal bet size based on winning and losing probabilities.

calculateAdjustedKellyFraction(kellyRatio, riskTolerance, fedStance)

Parameters:

kellyRatio (float) : The calculated Kelly Ratio.

riskTolerance (float) : A float representing the risk tolerance level.

fedStance (string) : A string indicating the Federal Reserve's stance ("dovish", "hawkish", or neutral).

Returns: The adjusted Kelly Fraction, constrained within the bounds of .

calculateStdDev(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The standard deviation of the returns, or 0 if insufficient data.

calculateMaxDrawdown(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The maximum drawdown as a percentage.

calculateEV(avgWinReturn, winProb, avgLossReturn)

Parameters:

avgWinReturn (float) : The average return from winning bets.

winProb (float) : The probability of winning a bet.

avgLossReturn (float) : The average return from losing bets.

Returns: The calculated Expected Value of the bet.

calculateTailRatio(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The Tail Ratio, or na if the 5th percentile is zero to avoid division by zero.

calculateSharpeRatio(avgReturn, riskFreeRate, stdDev)

Parameters:

avgReturn (float) : The average return of the investment.

riskFreeRate (float) : The risk-free rate of return.

stdDev (float) : The standard deviation of the investment's returns.

Returns: The calculated Sharpe Ratio, or na if standard deviation is zero.

calculateDownsideDeviation(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The standard deviation of the downside returns, or 0 if no downside returns exist.

calculateSortinoRatio(avgReturn, downsideDeviation)

Parameters:

avgReturn (float) : The average return of the investment.

downsideDeviation (float) : The standard deviation of the downside returns.

Returns: The calculated Sortino Ratio, or na if downside deviation is zero.

calculateVaR(returns, confidenceLevel)

Parameters:

returns (array) : An array of floats representing the returns.

confidenceLevel (float) : A float representing the confidence level (e.g., 0.95 for 95% confidence).

Returns: The Value at Risk at the specified confidence level.

calculateCVaR(returns, varValue)

Parameters:

returns (array) : An array of floats representing the returns.

varValue (float) : The Value at Risk threshold.

Returns: The average Conditional Value at Risk, or na if no returns are below the threshold.

calculateExpectedPriceRange(currentPrice, ev, stdDev, confidenceLevel)

Parameters:

currentPrice (float) : The current price of the asset.

ev (float) : The expected value (in percentage terms).

stdDev (float) : The standard deviation (in percentage terms).

confidenceLevel (float) : The confidence level for the price range (e.g., 1.96 for 95% confidence).

Returns: A tuple containing the minimum and maximum expected prices.

calculateRollingStdDev(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling standard deviation of returns.

calculateRollingVariance(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling variance of returns.

calculateRollingMean(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling mean of returns.

calculateRollingCoefficientOfVariation(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling coefficient of variation of returns.

calculateRollingSumOfPercentReturns(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling sum of percent returns.

calculateRollingCumulativeProduct(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling cumulative product of returns.

calculateRollingCorrelation(priceReturns, volumeReturns, window)

Parameters:

priceReturns (array) : An array of floats representing the price returns.

volumeReturns (array) : An array of floats representing the volume returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling correlation.

calculateRollingPercentile(returns, window, percentile)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

percentile (int) : An integer representing the desired percentile (0-100).

Returns: An array of floats representing the rolling percentile of returns.

calculateRollingMaxMinPercentReturns(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: A tuple containing two arrays: rolling max and rolling min percent returns.

calculateRollingPriceToVolumeRatio(price, volData, window)

Parameters:

price (array) : An array of floats representing the price data.

volData (array) : An array of floats representing the volume data.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling price-to-volume ratio.

determineMarketRegime(priceChanges)

Parameters:

priceChanges (array) : An array of floats representing the price changes.

Returns: A string indicating the market regime ("Bull", "Bear", or "Neutral").

determineVolatilityRegime(price, window)

Parameters:

price (array) : An array of floats representing the price data.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the calculated volatility.

classifyVolatilityRegime(volatility)

Parameters:

volatility (array) : An array of floats representing the calculated volatility.

Returns: A string indicating the volatility regime ("Low" or "High").

method percentPositive(thisArray)

Returns the percentage of positive non-na values in this array.

This method calculates the percentage of positive values in the provided array, ignoring NA values.

Namespace types: array

Parameters:

thisArray (array)

_candleRange()

_PreviousCandleRange(barsback)

Parameters:

barsback (int) : An integer representing how far back you want to get a range

redCandle()

greenCandle()

_WhiteBody()

_BlackBody()

HighOpenDiff()

OpenLowDiff()

_isCloseAbovePreviousOpen(length)

Parameters:

length (int)

_isCloseBelowPrevious()

_isOpenGreaterThanPrevious()

_isOpenLessThanPrevious()

BodyHigh()

BodyLow()

_candleBody()

_BodyAvg(length)

_BodyAvg function.

Parameters:

length (simple int) : Required (recommended is 6).

_SmallBody(length)

Parameters:

length (simple int) : Length of the slow EMA

Returns: a series of bools, after checking if the candle body was less than body average.

_LongBody(length)

Parameters:

length (simple int)

bearWick()

bearWick() function.

Returns: a SERIES of FLOATS, checks if it's a blackBody(open > close), if it is, than check the difference between the high and open, else checks the difference between high and close.

bullWick()

barlength()

sumbarlength()

sumbull()

sumbear()

bull_vol()

bear_vol()

volumeFightMA()

volumeFightDelta()

weightedAVG_BullVolume()

weightedAVG_BearVolume()

VolumeFightDiff()

VolumeFightFlatFilter()

avg_bull_vol(userMA)

avg_bull_vol(int) function.

Parameters:

userMA (int)

avg_bear_vol(userMA)

avg_bear_vol(int) function.

Parameters:

userMA (int)

diff_vol(userMA)

diff_vol(int) function.

Parameters:

userMA (int)

vol_flat(userMA)

vol_flat(int) function.

Parameters:

userMA (int)

_isEngulfingBullish()

_isEngulfingBearish()

dojiup()

dojidown()

EveningStar()

MorningStar()

ShootingStar()

Hammer()

InvertedHammer()

BearishHarami()

BullishHarami()

BullishBelt()

BullishKicker()

BearishKicker()

HangingMan()

DarkCloudCover()

MATH

IndicatorsLibrary "Indicators"

cmf(lookback, n_to_smooth)

Calculates the Chaikin's Money Flow.

Parameters:

lookback (simple int)

n_to_smooth (simple int)

Returns: float The Money Flow value.

cmma(lookback, atr_length)

Calculates the CMMA (Close Minus Moving Average) indicator.

Parameters:

lookback (simple int)

atr_length (simple int)

Returns: float The CMMA value.

macd(fast_length, slow_length, n_to_smooth)

Calculates the normalized and scaled MACD.

Parameters:

fast_length (simple int)

slow_length (simple int)

n_to_smooth (simple int)

Returns: A tuple containing .

stochK(length, n_to_smooth)

Calculates a simplified Stochastic Oscillator.

Uses: 100 * ta.sma((close - lowest_low) / (highest_high - lowest_low), n_to_smooth)

Parameters:

length (simple int)

n_to_smooth (simple int)

Returns: float The Stochastic %K value.

williamsR(length)

Calculates the Williams %R using the stochK function.

Uses: -1 * (100 - stoch(length, 1))

Parameters:

length (simple int)

Returns: float The Williams %R value.

lib_kernelLibrary "lib_kernel"

Library "lib_kernel"

This is a tool / library for developers, that contains several common and adapted kernel functions as well as a kernel regression function and enum to easily select and embed a list into the settings dialog.

How to Choose and Modify Kernels in Practice

Compact Support Kernels (e.g., Epanechnikov, Triangular): Use for localized smoothing and emphasizing nearby data.

Oscillatory Kernels (e.g., Wave, Cosine): Ideal for detecting periodic patterns or mean-reverting behavior.

Smooth Tapering Kernels (e.g., Gaussian, Logistic): Use for smoothing long-term trends or identifying global price behavior.

kernel_Epanechnikov(u)

Parameters:

u (float)

kernel_Epanechnikov_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Triangular(u)

Parameters:

u (float)

kernel_Triangular_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Rectangular(u)

Parameters:

u (float)

kernel_Uniform(u)

Parameters:

u (float)

kernel_Uniform_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Logistic(u)

Parameters:

u (float)

kernel_Logistic_alt(u)

Parameters:

u (float)

kernel_Logistic_alt2(u, sigmoid_steepness)

Parameters:

u (float)

sigmoid_steepness (float)

kernel_Gaussian(u)

Parameters:

u (float)

kernel_Gaussian_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Silverman(u)

Parameters:

u (float)

kernel_Quartic(u)

Parameters:

u (float)

kernel_Quartic_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Biweight(u)

Parameters:

u (float)

kernel_Triweight(u)

Parameters:

u (float)

kernel_Sinc(u)

Parameters:

u (float)

kernel_Wave(u)

Parameters:

u (float)

kernel_Wave_alt(u)

Parameters:

u (float)

kernel_Cosine(u)

Parameters:

u (float)

kernel_Cosine_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel(u, select, alt_modificator)

wrapper for all standard kernel functions, see enum Kernel comments and function descriptions for usage szenarios and parameters

Parameters:

u (float)

select (series Kernel)

alt_modificator (float)

kernel_regression(src, bandwidth, kernel, exponential_distance, alt_modificator)

wrapper for kernel regression with all standard kernel functions, see enum Kernel comments for usage szenarios. performance optimized version using fixed bandwidth and target

Parameters:

src (float) : input data series

bandwidth (simple int) : sample window of nearest neighbours for the kernel to process

kernel (simple Kernel) : type of Kernel to use for processing, see Kernel enum or respective functions for more details

exponential_distance (simple bool) : if true this puts more emphasis on local / more recent values

alt_modificator (float) : see kernel functions for parameter descriptions. Mostly used to pronounce emphasis on local values or introduce a decay/dampening to the kernel output

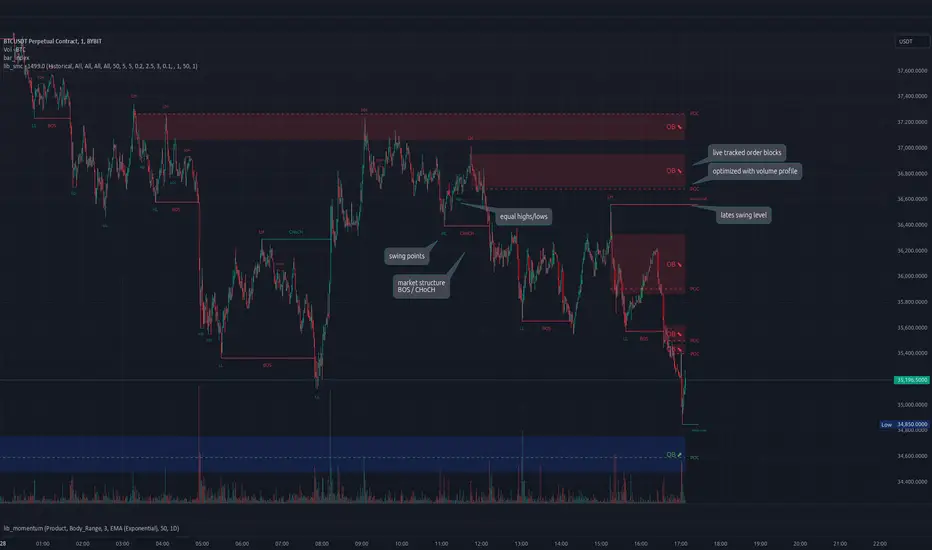

lib_smcLibrary "lib_smc"

This is an adaptation of LuxAlgo's Smart Money Concepts indicator with numerous changes. Main changes include integration of object based plotting, plenty of performance improvements, live tracking of Order Blocks, integration of volume profiles to refine Order Blocks, and many more.

This is a library for developers, if you want this converted into a working strategy, let me know.

buffer(item, len, force_rotate)

Parameters:

item (float)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (int)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (Profile type from robbatt/lib_profile/32)

len (int)

force_rotate (bool)

swings(len)

INTERNAL: detect swing points (HH and LL) in given range

Parameters:

len (simple int) : range to check for new swing points

Returns: values are the price level where and if a new HH or LL was detected, else na

method init(this)

Namespace types: OrderBlockConfig

Parameters:

this (OrderBlockConfig)

method delete(this)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

method clear_broken(this, broken_buffer)

INTERNAL: delete internal order blocks box coordinates if top/bottom is broken

Namespace types: map

Parameters:

this (map)

broken_buffer (map)

Returns: any_bull_ob_broken, any_bear_ob_broken, broken signals are true if an according order block was broken/mitigated, broken contains the broken block(s)

create_ob(id, mode, start_t, start_i, top, end_t, end_i, bottom, break_price, early_confirmation_price, config, init_plot, force_overlay)

INTERNAL: set internal order block coordinates

Parameters:

id (int)

mode (int) : 1: bullish, -1 bearish block

start_t (int)

start_i (int)

top (float)

end_t (int)

end_i (int)

bottom (float)

break_price (float)

early_confirmation_price (float)

config (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

Returns: signals are true if an according order block was broken/mitigated

method align_to_profile(block, align_edge, align_break_price)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

align_edge (bool)

align_break_price (bool)

method create_profile(block, opens, tops, bottoms, closes, values, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

opens (array)

tops (array)

bottoms (array)

closes (array)

values (array)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

method create_profile(block, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

track_obs(swing_len, hh, ll, top, btm, bull_bos_alert, bull_choch_alert, bear_bos_alert, bear_choch_alert, min_block_size, max_block_size, config_bull, config_bear, init_plot, force_overlay, enabled, extend_blocks, clear_broken_buffer_before, align_edge_to_value_area, align_break_price_to_poc, profile_args_bull, profile_args_bear, use_soft_confirm, soft_confirm_offset, use_retracements_with_FVG_out)

Parameters:

swing_len (int)

hh (float)

ll (float)

top (float)

btm (float)

bull_bos_alert (bool)

bull_choch_alert (bool)

bear_bos_alert (bool)

bear_choch_alert (bool)

min_block_size (float)

max_block_size (float)

config_bull (OrderBlockConfig)

config_bear (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

enabled (bool)

extend_blocks (simple bool)

clear_broken_buffer_before (simple bool)

align_edge_to_value_area (simple bool)

align_break_price_to_poc (simple bool)

profile_args_bull (ProfileArgs type from robbatt/lib_profile/32)

profile_args_bear (ProfileArgs type from robbatt/lib_profile/32)

use_soft_confirm (simple bool)

soft_confirm_offset (float)

use_retracements_with_FVG_out (simple bool)

method draw(this, config, extend_only)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

config (OrderBlockConfig)

extend_only (bool)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: array

Parameters:

blocks (array)

config (OrderBlockConfig)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: map

Parameters:

blocks (map)

config (OrderBlockConfig)

method cleanup(this, ob_bull, ob_bear)

removes all Profiles that are older than the latest OrderBlock from this profile buffer

Namespace types: array

Parameters:

this (array type from robbatt/lib_profile/32)

ob_bull (OrderBlock)

ob_bear (OrderBlock)

_plot_swing_points(mode, x, y, show_swing_points, linecolor_swings, keep_history, show_latest_swings_levels, trail_x, trail_y, trend)

INTERNAL: plot swing points

Parameters:

mode (int) : 1: bullish, -1 bearish block

x (int) : x-coordingate of swing point to plot (bar_index)

y (float) : y-coordingate of swing point to plot (price)

show_swing_points (bool) : switch to enable/disable plotting of swing point labels

linecolor_swings (color) : color for swing point labels and lates level lines

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

show_latest_swings_levels (bool)

trail_x (int) : x-coordinate for latest swing point (bar_index)

trail_y (float) : y-coordinate for latest swing point (price)

trend (int) : the current trend 1: bullish, -1: bearish, to determine Strong/Weak Low/Highs

_pivot_lvl(mode, trend, hhll_x, hhll, super_hhll, filter_insignificant_internal_breaks)

INTERNAL: detect whether a structural level has been broken and if it was in trend direction (BoS) or against trend direction (ChoCh), also track the latest high and low swing points

Parameters:

mode (simple int) : detect 1: bullish, -1 bearish pivot points

trend (int) : current trend direction

hhll_x (int) : x-coordinate of newly detected hh/ll (bar_index)

hhll (float) : y-coordinate of newly detected hh/ll (price)

super_hhll (float) : level/y-coordinate of superior hhll (if this is an internal structure pivot level)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: coordinates of internal structure that has been broken (x,y): start of structure, (trail_x, trail_y): tracking hh/ll after structure break, (bos_alert, choch_alert): signal whether a structural level has been broken

_plot_structure(x, y, is_bos, is_choch, line_color, line_style, label_style, label_size, keep_history)

INTERNAL: plot structural breaks (BoS/ChoCh)

Parameters:

x (int) : x-coordinate of newly broken structure (bar_index)

y (float) : y-coordinate of newly broken structure (price)

is_bos (bool) : whether this structural break was in trend direction

is_choch (bool) : whether this structural break was against trend direction

line_color (color) : color for the line connecting the structural level and the breaking candle

line_style (string) : style (line.style_dashed/solid) for the line connecting the structural level and the breaking candle

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the structural level and the breaking candle

label_size (string) : size (size.small/tiny) for the label above/below the line connecting the structural level and the breaking candle

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure_values(length, super_hh, super_ll, filter_insignificant_internal_breaks)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: trend: direction 1:bullish -1:bearish, (bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up): whether and which level broke in a bullish direction, trailing high, (bbear_bos_alert, bear_choch_alert, tm_x, btm_y, trail_dn_x, trail_dn): same in bearish direction

structure_plot(trend, bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up, hh, bear_bos_alert, bear_choch_alert, btm_x, btm_y, trail_dn_x, trail_dn, ll, color_bull, color_bear, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history)

detect (and plot) structural breaks and the resulting new trend

Parameters:

trend (int) : crrent trend 1: bullish, -1: bearish

bull_bos_alert (bool) : if there was a bullish bos alert -> plot it

bull_choch_alert (bool) : if there was a bullish choch alert -> plot it

top_x (int) : latest shwing high x

top_y (float) : latest swing high y

trail_up_x (int) : trailing high x

trail_up (float) : trailing high y

hh (float) : if there was a higher high

bear_bos_alert (bool) : if there was a bearish bos alert -> plot it

bear_choch_alert (bool) : if there was a bearish chock alert -> plot it

btm_x (int) : latest swing low x

btm_y (float) : latest swing low y

trail_dn_x (int) : trailing low x

trail_dn (float) : trailing low y

ll (float) : if there was a lower low

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure(length, color_bull, color_bear, super_hh, super_ll, filter_insignificant_internal_breaks, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history, enabled)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

enabled (bool)

_check_equal_level(mode, len, eq_threshold, enabled)

INTERNAL: detect equal levels (double top/bottom)

Parameters:

mode (int) : detect 1: bullish/high, -1 bearish/low pivot points

len (int) : lookback period for equal level (swing point) detection

eq_threshold (float) : maximum price offset for a level to be considered equal

enabled (bool)

Returns: eq_alert whether an equal level was detected and coordinates of the first and the second level/swing point

_plot_equal_level(show_eq, x1, y1, x2, y2, label_txt, label_style, label_size, line_color, line_style, keep_history)

INTERNAL: plot equal levels (double top/bottom)

Parameters:

show_eq (bool) : whether to plot the level or not

x1 (int) : x-coordinate of the first level / swing point

y1 (float) : y-coordinate of the first level / swing point

x2 (int) : x-coordinate of the second level / swing point

y2 (float) : y-coordinate of the second level / swing point

label_txt (string) : text for the label above/below the line connecting the equal levels

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the equal levels

label_size (string) : size (size.tiny) for the label above/below the line connecting the equal levels

line_color (color) : color for the line connecting the equal levels (and it's label)

line_style (string) : style (line.style_dotted) for the line connecting the equal levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

equal_levels_values(len, threshold, enabled)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

enabled (bool) : whether detection is enabled

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels_plot(eqh_x1, eqh_y1, eqh_x2, eqh_y2, eql_x1, eql_y1, eql_x2, eql_y2, color_eqh, color_eql, show, keep_history)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

eqh_x1 (int) : coordinates of first point of equal high

eqh_y1 (float) : coordinates of first point of equal high

eqh_x2 (int) : coordinates of second point of equal high

eqh_y2 (float) : coordinates of second point of equal high

eql_x1 (int) : coordinates of first point of equal low

eql_y1 (float) : coordinates of first point of equal low

eql_x2 (int) : coordinates of second point of equal low

eql_y2 (float) : coordinates of second point of equal low

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels(len, threshold, color_eqh, color_eql, enabled, show, keep_history)

detect (and plot) equal levels (double top/bottom)

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

enabled (bool) : whether detection is enabled

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert) whether an equal high was detected, (eql_alert) same for equal lows

_detect_fvg(mode, enabled, o, h, l, c, filter_insignificant_fvgs, change_tf)

INTERNAL: detect FVG (fair value gap)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

enabled (bool) : whether detection is enabled

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

Returns: whether a new FVG was detected and its top/mid/bottom levels

_clear_broken_fvg(mode, upper_boxes, lower_boxes)

INTERNAL: clear mitigated FVGs (fair value gaps)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

upper_boxes (array) : array that stores the upper parts of the FVG boxes

lower_boxes (array) : array that stores the lower parts of the FVG boxes

_plot_fvg(mode, show, top, mid, btm, border_color, extend_box)

INTERNAL: plot (and clear broken) FVG (fair value gap)

Parameters:

mode (int) : plot 1: bullish, -1 bearish gap

show (bool) : whether plotting is enabled

top (float) : top level of fvg

mid (float) : center level of fvg

btm (float) : bottom level of fvg

border_color (color) : color for the FVG box

extend_box (int) : how many bars into the future the FVG box should be extended after detection

fvgs_values(o, h, l, c, filter_insignificant_fvgs, change_tf, enabled)

detect (and plot / clear broken) FVGs (fair value gaps), and return alerts and level values

Parameters:

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

enabled (bool) : whether detection is enabled

Returns: (bullish_fvg_alert, bull_top, bull_mid, bull_btm): whether a new bullish FVG was detected and its top/mid/bottom levels, (bearish_fvg_alert, bear_top, bear_mid, bear_btm): same for bearish FVGs

fvgs_plot(bullish_fvg_alert, bull_top, bull_mid, bull_btm, bearish_fvg_alert, bear_top, bear_mid, bear_btm, color_bull, color_bear, extend_box, show)

Parameters:

bullish_fvg_alert (bool)

bull_top (float)

bull_mid (float)

bull_btm (float)

bearish_fvg_alert (bool)

bear_top (float)

bear_mid (float)

bear_btm (float)

color_bull (color) : color for bullish FVG boxes

color_bear (color) : color for bearish FVG boxes

extend_box (int) : how many bars into the future the FVG box should be extended after detection

show (bool) : whether plotting is enabled

Returns: (bullish_fvg_alert, bull_top, bull_mid, bull_btm): whether a new bullish FVG was detected and its top/mid/bottom levels, (bearish_fvg_alert, bear_top, bear_mid, bear_btm): same for bearish FVGs

fvgs(o, h, l, c, filter_insignificant_fvgs, change_tf, color_bull, color_bear, extend_box, enabled, show)

detect (and plot / clear broken) FVGs (fair value gaps)

Parameters:

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

color_bull (color) : color for bullish FVG boxes

color_bear (color) : color for bearish FVG boxes

extend_box (int) : how many bars into the future the FVG box should be extended after detection

enabled (bool) : whether detection is enabled

show (bool) : whether plotting is enabled

Returns: (bullish_fvg_alert): whether a new bullish FVG was detected, (bearish_fvg_alert): same for bearish FVGs

OrderBlock

Fields:

id (series int)

dir (series int)

left_top (chart.point)

right_bottom (chart.point)

break_price (series float)

early_confirmation_price (series float)

ltf_high (array)

ltf_low (array)

ltf_volume (array)

plot (Box type from robbatt/lib_plot_objects/49)

profile (Profile type from robbatt/lib_profile/32)

trailing (series bool)

extending (series bool)

awaiting_confirmation (series bool)

touched_break_price_before_confirmation (series bool)

soft_confirmed (series bool)

has_fvg_out (series bool)

hidden (series bool)

broken (series bool)

OrderBlockConfig

Fields:

show (series bool)

show_last (series int)

show_id (series bool)

show_profile (series bool)

args (BoxArgs type from robbatt/lib_plot_objects/49)

txt (series string)

txt_args (BoxTextArgs type from robbatt/lib_plot_objects/49)

delete_when_broken (series bool)

broken_args (BoxArgs type from robbatt/lib_plot_objects/49)

broken_txt (series string)

broken_txt_args (BoxTextArgs type from robbatt/lib_plot_objects/49)

broken_profile_args (ProfileArgs type from robbatt/lib_profile/32)

use_profile (series bool)

profile_args (ProfileArgs type from robbatt/lib_profile/32)

FibRatiosLibrary "FibRatios"

Library with calculation logic for fib retracement, extension and ratios

retracement(a, b, ratio, logScale, precision)

Calculates the retracement for points a, b with given ratio and scale

Parameters:

a (float) : Starting point a

b (float) : Second point b

ratio (float) : Ratio for which we need to calculate retracement c

logScale (bool) : Flag to get calculations in log scale. Default is false

precision (int) : rounding precision. If set to netagive number, round_to_mintick is applied. Default is -1

Returns: retracement point c for points a,b with given ratio and scale

retracementRatio(a, b, c, logScale, precision)

Calculates the retracement ratio for points a, b, c with given scale

Parameters:

a (float) : Starting point a

b (float) : Second point b

c (float) : Retracement point. c should be placed between a and b

logScale (bool) : Flag to get calculations in log scale. Default is false

precision (int) : rounding precision. If set to netagive number, round_to_mintick is applied. Default is 3

Returns: retracement ratio for points a,b,c on given scale

extension(a, b, c, ratio, logScale, precision)

Calculates the extensions for points a, b, c with given ratio and scale

Parameters:

a (float) : Starting point a

b (float) : Second point b

c (float) : Retracement point. c should be placed between a and b

ratio (float) : Ratio for which we need to calculate extension d

logScale (bool) : Flag to get calculations in log scale. Default is false

precision (int) : rounding precision. If set to netagive number, round_to_mintick is applied. Default is -1

Returns: extensoin point d for points a,b,c with given ratio and scale

extensionRatio(a, b, c, d, logScale, precision)

Calculates the extension ratio for points a, b, c, d with given scale

Parameters:

a (float) : Starting point a

b (float) : Second point b

c (float) : Retracement point. c should be placed between a and b

d (float) : Extension point. d should be placed beyond a, c. But, can be with b,c or beyond b

logScale (bool) : Flag to get calculations in log scale. Default is false

precision (int) : rounding precision. If set to netagive number, round_to_mintick is applied. Default is 3

Returns: extension ratio for points a,b,c,d on given scale

MathHelpersLibrary "MathHelpers"

Overview

A collection of helper functions for designing indicators and strategies.

calculateATR(length, log)

Calculates the Average True Range (ATR) or Log ATR based on the 'log' parameter. Sans Wilder's Smoothing

Parameters:

length (simple int)

log (simple bool)

Returns: float The calculated ATR value. Returns Log ATR if `log` is true, otherwise returns standard ATR.

CDF(z)

Computes the Cumulative Distribution Function (CDF) for a given value 'z', mimicking the CDF function in "Statistically Sound Indicators" by Timothy Masters.

Parameters:

z (simple float)

Returns: float The CDF value corresponding to the input `z`, ranging between 0 and 1.

logReturns(lookback)

Calculates the logarithmic returns over a specified lookback period.

Parameters:

lookback (simple int)

Returns: float The calculated logarithmic return. Returns `na` if insufficient data is available.

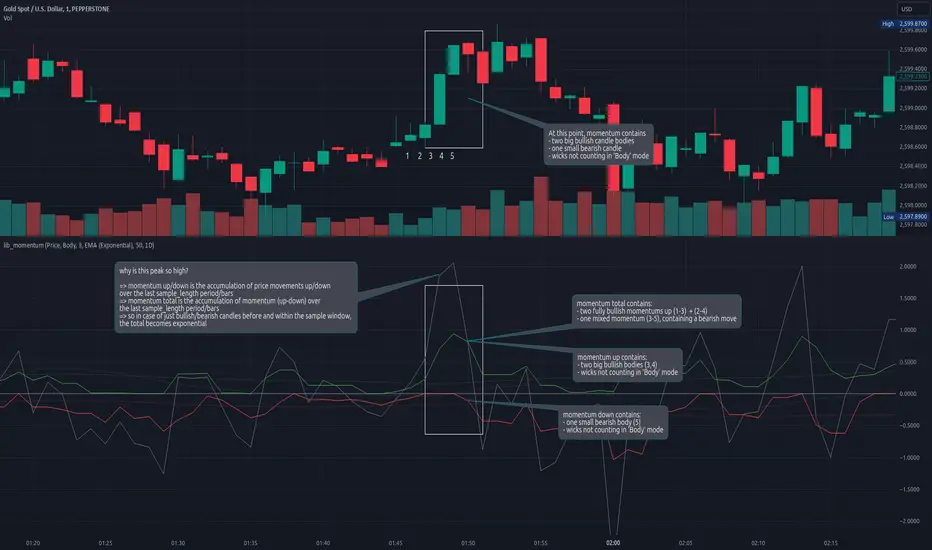

lib_momentumLibrary "lib_momentum"

This library calculates the momentum, derived from a sample range of prior candles. Depending on set MomentumType it either deduces the momentum from the price, volume, or a product of both. If price/product are selected, you can choose from SampleType if only candle body, full range from high to low or a combination of both (body counts full, wicks half for each direction) should be used. Optional: You can choose to normalize the results, dividing each value by its average (normalization_ma_length, normalization_ma). This will allow comparison between different instruments. For the normalization Moving Average you can choose any currently supported in my lib_no_delay.

get_momentum(momentum_type, sample_type, sample_length, normalization_ma_length, normalization_ma)

Parameters:

momentum_type (series MomentumType) : select one of MomentumType. to sample the price, volume or a product of both

sample_type (series SampleType) : select one of SampleType. to sample the body, total range from high to low or a combination of both (body count full, wicks half for each direction)

sample_length (simple int) : how many candles should be sampled (including the current)

normalization_ma_length (simple int) : if you want to normalize results (momentum / momentum average) this sets the period for the average. (default = 0 => no normalization)

normalization_ma (simple MovingAverage enum from robbatt/lib_no_delay/9) : is the type of moving average to normalize / compare with

Returns: returns the current momentum where the total line is not just (up - down) but also sampled over the sample_length and can therefore be used as trend indicator. If up/down fail to reach total's level it's a sign of decreasing momentum, if up/down exceed total the trend it's a sign of increasing momentum.

analytics_tablesLibrary "analytics_tables"

📝 Description

This library provides the implementation of several performance-related statistics and metrics, presented in the form of tables.

The metrics shown in the afforementioned tables where developed during the past years of my in-depth analalysis of various strategies in an atempt to reason about the performance of each strategy.

The visualization and some statistics where inspired by the existing implementations of the "Seasonality" script, and the performance matrix implementations of @QuantNomad and @ZenAndTheArtOfTrading scripts.

While this library is meant to be used by my strategy framework "Template Trailing Strategy (Backtester)" script, I wrapped it in a library hoping this can be usefull for other community strategy scripts that will be released in the future.

🤔 How to Guide

To use the functionality this library provides in your script you have to import it first!

Copy the import statement of the latest release by pressing the copy button below and then paste it into your script. Give a short name to this library so you can refer to it later on. The import statement should look like this:

import jason5480/analytics_tables/1 as ant

There are three types of tables provided by this library in the initial release. The stats table the metrics table and the seasonality table.

Each one shows different kinds of performance statistics.

The table UDT shall be initialized once using the `init()` method.

They can be updated using the `update()` method where the updated data UDT object shall be passed.

The data UDT can also initialized and get updated on demend depending on the use case

A code example for the StatsTable is the following:

var ant.StatsData statsData = ant.StatsData.new()

statsData.update(SideStats.new(), SideStats.new(), 0)

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var statsTable = ant.StatsTable.new().init(ant.getTablePos('TOP', 'RIGHT'))

statsTable.update(statsData)

A code example for the MetricsTable is the following:

var ant.StatsData statsData = ant.StatsData.new()

statsData.update(ant.SideStats.new(), ant.SideStats.new(), 0)

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var metricsTable = ant.MetricsTable.new().init(ant.getTablePos('BOTTOM', 'RIGHT'))

metricsTable.update(statsData, 10)

A code example for the SeasonalityTable is the following:

var ant.SeasonalData seasonalData = ant.SeasonalData.new().init(Seasonality.monthOfYear)

seasonalData.update()

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var seasonalTable = ant.SeasonalTable.new().init(seasonalData, ant.getTablePos('BOTTOM', 'LEFT'))

seasonalTable.update(seasonalData)

🏋️♂️ Please refer to the "EXAMPLE" regions of the script for more advanced and up to date code examples!

Special thanks to @Mrcrbw for the proposal to develop this library and @DCNeu for the constructive feedback 🏆.

getTablePos(ypos, xpos)

Get table position compatible string

Parameters:

ypos (simple string) : The position on y axise

xpos (simple string) : The position on x axise

Returns: The position to be passed to the table

method init(this, pos, height, width, positiveTxtColor, negativeTxtColor, neutralTxtColor, positiveBgColor, negativeBgColor, neutralBgColor)

Initialize the stats table object with the given colors in the given position

Namespace types: StatsTable

Parameters:

this (StatsTable) : The stats table object

pos (simple string) : The table position string

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts height. By default, 0 auto-adjusts the width based on the text inside the cells

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

neutralTxtColor (simple color) : The text color when neutral

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

method init(this, pos, height, width, neutralBgColor)

Initialize the metrics table object with the given colors in the given position

Namespace types: MetricsTable

Parameters:

this (MetricsTable) : The metrics table object

pos (simple string) : The table position string

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts width. By default, 0 auto-adjusts the width based on the text inside the cells

neutralBgColor (simple color) : The background color with transparency when neutral

method init(this, seas)

Initialize the seasonal data

Namespace types: SeasonalData

Parameters:

this (SeasonalData) : The seasonal data object

seas (simple Seasonality) : The seasonality of the matrix data

method init(this, data, pos, maxNumOfYears, height, width, extended, neutralTxtColor, neutralBgColor)

Initialize the seasonal table object with the given colors in the given position

Namespace types: SeasonalTable

Parameters:

this (SeasonalTable) : The seasonal table object

data (SeasonalData) : The seasonality data of the table

pos (simple string) : The table position string

maxNumOfYears (simple int) : The maximum number of years that fit into the table

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts width. By default, 0 auto-adjusts the width based on the text inside the cells

extended (simple bool) : The seasonal table with extended columns for performance

neutralTxtColor (simple color) : The text color when neutral

neutralBgColor (simple color) : The background color with transparency when neutral

method update(this, wins, losses, numOfInconclusiveExits)

Update the strategy info data of the strategy

Namespace types: StatsData

Parameters:

this (StatsData) : The strategy statistics object

wins (SideStats)

losses (SideStats)

numOfInconclusiveExits (int) : The number of inconclusive trades

method update(this, stats, positiveTxtColor, negativeTxtColor, negativeBgColor, neutralBgColor)

Update the stats table object with the given data

Namespace types: StatsTable

Parameters:

this (StatsTable) : The stats table object

stats (StatsData) : The stats data to update the table

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

method update(this, stats, buyAndHoldPerc, positiveTxtColor, negativeTxtColor, positiveBgColor, negativeBgColor)

Update the metrics table object with the given data

Namespace types: MetricsTable

Parameters:

this (MetricsTable) : The metrics table object

stats (StatsData) : The stats data to update the table

buyAndHoldPerc (float) : The buy and hold percetage

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

method update(this)

Update the seasonal data based on the season and eon timeframe

Namespace types: SeasonalData

Parameters:

this (SeasonalData) : The seasonal data object

method update(this, data, positiveTxtColor, negativeTxtColor, neutralTxtColor, positiveBgColor, negativeBgColor, neutralBgColor, timeBgColor)

Update the seasonal table object with the given data

Namespace types: SeasonalTable

Parameters:

this (SeasonalTable) : The seasonal table object

data (SeasonalData) : The seasonal cell data to update the table

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

neutralTxtColor (simple color) : The text color when neutral

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

timeBgColor (simple color) : The background color of the time gradient

SideStats

Object that represents the strategy statistics data of one side win or lose

Fields:

numOf (series int)

sumFreeProfit (series float)

freeProfitStDev (series float)

sumProfit (series float)

profitStDev (series float)

sumGain (series float)

gainStDev (series float)

avgQuantityPerc (series float)

avgCapitalRiskPerc (series float)

avgTPExecutedCount (series float)

avgRiskRewardRatio (series float)

maxStreak (series int)

StatsTable

Object that represents the stats table

Fields:

table (series table) : The actual table

rows (series int) : The number of rows of the table

columns (series int) : The number of columns of the table

StatsData

Object that represents the statistics data of the strategy

Fields:

wins (SideStats)

losses (SideStats)

numOfInconclusiveExits (series int)

avgFreeProfitStr (series string)

freeProfitStDevStr (series string)

lossFreeProfitStDevStr (series string)

avgProfitStr (series string)

profitStDevStr (series string)

lossProfitStDevStr (series string)

avgQuantityStr (series string)

MetricsTable

Object that represents the metrics table

Fields:

table (series table) : The actual table

rows (series int) : The number of rows of the table

columns (series int) : The number of columns of the table

SeasonalData

Object that represents the seasonal table dynamic data

Fields:

seasonality (series Seasonality)

eonToMatrixRow (map)

numOfEons (series int)

mostRecentMatrixRow (series int)

balances (matrix)

returnPercs (matrix)

maxDDs (matrix)

eonReturnPercs (array)

eonCAGRs (array)

eonMaxDDs (array)

SeasonalTable

Object that represents the seasonal table

Fields:

table (series table) : The actual table

headRows (series int) : The number of head rows of the table

headColumns (series int) : The number of head columns of the table

eonRows (series int) : The number of eon rows of the table

seasonColumns (series int) : The number of season columns of the table

statsRows (series int)

statsColumns (series int) : The number of stats columns of the table

rows (series int) : The number of rows of the table

columns (series int) : The number of columns of the table

extended (series bool) : Whether the table has additional performance statistics

BinaryInsertionSortLibrary "BinaryInsertionSort"

Library containing functions which can help create sorted array based on binary insertion sort.

This sorting will be quicker than array.sort function if the sorting needs to be done on every bar and the size of the array is comparatively big.

method binary_search_basic(sortedArray, item, order)

binary_search_basic - finds the closest index of the value

Namespace types: array

Parameters:

sortedArray (array) : array which is assumed to be sorted in the requested order

item (float) : float item which needs to be searched in the sorted array

order (int) : Sort order - positive number means ascending order whereas negative number represents descending order

Returns: int index at which the item can be inserted into sorted array

method binary_search_basic(sortedArray, item, order)

binary_search_basic - finds the closest index of the value

Namespace types: array

Parameters:

sortedArray (array) : array which is assumed to be sorted in the requested order

item (int) : int item which needs to be searched in the sorted array

order (int) : Sort order - positive number means ascending order whereas negative number represents descending order

Returns: int index at which the item can be inserted into sorted array

method binary_insertion_sort(sortedArray, item, order)

binary insertion sort - inserts item into sorted array while maintaining sort order

Namespace types: array

Parameters:

sortedArray (array) : array which is assumed to be sorted in the requested order

item (float) : float item which needs to be inserted into sorted array

order (int) : Sort order - positive number means ascending order whereas negative number represents descending order

Returns: int index at which the item is inserted into sorted array

method binary_insertion_sort(sortedArray, item, order)

binary insertion sort - inserts item into sorted array while maintaining sort order

Namespace types: array

Parameters:

sortedArray (array) : array which is assumed to be sorted in the requested order

item (int) : int item which needs to be inserted into sorted array

order (int) : Sort order - positive number means ascending order whereas negative number represents descending order

Returns: int index at which the item is inserted into sorted array

update_sort_indices(sortIndices, newItemIndex)

adds the sort index of new item added to sorted array and also updates existing sort indices.

Parameters:

sortIndices (array) : array containing sort indices of an array.

newItemIndex (int) : sort index of new item added to sorted array

Returns: void

get_array_of_series(item, order)

Converts series into array and sorted array.

Parameters:

item (float) : float series

order (int) : Sort order - positive number means ascending order whereas negative number represents descending order

Returns:

get_array_of_series(item, order)

Converts series into array and sorted array.

Parameters:

item (int) : int series

order (int) : Sort order - positive number means ascending order whereas negative number represents descending order

Returns:

get_sorted_arrays(item, order)

Converts series into array and sorted array. Also calculates the sort order of the value array

Parameters:

item (float) : float|int series

order (int) : Sort order - positive number means ascending order whereas negative number represents descending order

Returns:

get_sorted_arrays(item, order)

Converts series into array and sorted array. Also calculates the sort order of the value array

Parameters:

item (int) : int series

order (int) : Sort order - positive number means ascending order whereas negative number represents descending order

Returns:

lib_no_delayLibrary "lib_no_delay"

This library contains modifications to standard functions that return na before reaching the bar of their 'length' parameter.

That is because they do not compromise speed at current time for correct results in the past. This is good for live trading in short timeframes but killing applications on Monthly / Weekly timeframes if instruments, like in crypto, do not have extensive history (why would you even trade the monthly on a meme coin ... not my decision).

Also, some functions rely on source (value at previous bar), which is not available on bar 1 and therefore cascading to a na value up to the last bar ... which in turn leads to a non displaying indicator and waste of time debugging this)

Anyway ... there you go, let me know if I should add more functions.

sma(source, length)

Parameters:

source (float) : Series of values to process.

length (simple int) : Number of bars (length).

Returns: Simple moving average of source for length bars back.

ema(source, length)

Parameters:

source (float) : Series of values to process.

length (simple int) : Number of bars (length).

Returns: (float) The exponentially weighted moving average of the source.

rma(source, length)

Parameters:

source (float) : Series of values to process.

length (simple int) : Number of bars (length).

Returns: Exponential moving average of source with alpha = 1 / length.

atr(length)

Function atr (average true range) returns the RMA of true range. True range is max(high - low, abs(high - close ), abs(low - close )). This adapted version extends ta.atr to start without delay at first bar and deliver usable data instead of na by averaging ta.tr(true) via manual SMA.

Parameters:

length (simple int) : Number of bars back (length).

Returns: Average true range.

rsi(source, length)

Relative strength index. It is calculated using the ta.rma() of upward and downward changes of source over the last length bars. This adapted version extends ta.rsi to start without delay at first bar and deliver usable data instead of na.

Parameters:

source (float) : Series of values to process.

length (simple int) : Number of bars back (length).

Returns: Relative Strength Index.

Time Zone CorrectorThe Time Zone Corrector library provides a utility function designed to adjust time based on the user's current time zone. This library supports a wide range of time zones across the Americas, Europe, Asia, and Oceania, making it highly versatile for traders around the world. It simulates a switch-case structure using ternary operators to output the appropriate time offset relative to UTC.

Whether you're dealing with market sessions in New York, Tokyo, London, or other major trading hubs, this library helps ensure your trading algorithms can accurately account for time differences. The library is particularly useful for strategies that rely on precise timing, as it dynamically adjusts the time zone offset depending on the symbol being traded.

iteratorThe "Iterator" library is designed to provide a flexible way to work with sequences of values. This library offers a set of functions to create and manage iterators for various data types, including integers, floats, and more. Whether you need to generate an array of values with specific increments or iterate over elements in reverse order, this library has you covered.

Key Features:

Array Creation: Easily generate arrays of integers or floats with customizable steps, both inclusive and exclusive of the end values.

Flexible Iteration: Includes methods to iterate over arrays of different types, such as booleans, integers, floats, strings, colors, and drawing objects like lines and labels.

Reverse Iteration: Support for reverse iteration, giving you control over the order in which elements are processed.

Automatic Loop Control: One of the key advantages of this library is that when using the .iterate() method, it only loops over the array when there are values present. This means you don’t have to manually check if the array is populated before iterating, simplifying your code and reducing potential errors.

Versatile Use Cases: Ideal for scenarios where you need to loop over an array without worrying about empty arrays or checking conditions manually.

This library is particularly useful in cases where you need to perform operations on each element in an array, ensuring that your loops are efficient and free from unnecessary checks.

Library "iterator"

The "iterator" library provides a versatile and efficient set of functions for creating and managing iterators.

It allows you to generate arrays of integers or floats with customizable steps, both inclusive and exclusive of the end values.

The library also includes methods for iterating over various types, including booleans, integers, floats, strings, colors,

and drawing objects like lines and labels. With support for reverse iteration and flexible customization options.

iterator(stop, start, step)

Creates an array of integers from start to stop with a specified step, excluding the stop value.

Parameters:

stop (int) : The end value of the iterator, exclusive.

start (int) : The starting value of the iterator. Default is 0.

step (int) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of integers incremented by the step value from start to stop. Will return and empty array if start = stop.

iterator(stop, start, step)

Creates an array of floats from start to stop with a specified step, excluding the stop value.

Parameters:

stop (float) : The end value of the iterator, exclusive.

start (float) : The starting value of the iterator. Default is 0.

step (float) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of floats incremented by the step value from start to stop. Will return and empty array if start = stop.

iterator_inclusive(stop, start, step)

Creates an array of integers from start to stop with a specified step, including the stop value.

Parameters:

stop (int) : The end value of the iterator, inclusive.

start (int) : The starting value of the iterator. Default is 0.

step (int) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of integers incremented by the step value from start to stop, including the stop value.

iterator_inclusive(stop, start, step)

Creates an array of floats from start to stop with a specified step, including the stop value.

Parameters:

stop (float) : The end value of the iterator, inclusive.

start (float) : The starting value of the iterator. Default is 0.

step (float) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of floats incremented by the step value from start to stop, including the stop value.

itr(stop, start, step)

Creates an array of integers from start to stop with a specified step, excluding the stop value.

Parameters:

stop (int) : The end value of the iterator, exclusive.

start (int) : The starting value of the iterator. Default is 0.

step (int) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of integers incremented by the step value from start to stop.

itr(stop, start, step)

Creates an array of floats from start to stop with a specified step, excluding the stop value.

Parameters:

stop (float) : The end value of the iterator, exclusive.

start (float) : The starting value of the iterator. Default is 0.

step (float) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of floats incremented by the step value from start to stop.

itr_in(stop, start, step)

Creates an array of integers from start to stop with a specified step, including the stop value.

Parameters:

stop (int) : The end value of the iterator, inclusive.

start (int) : The starting value of the iterator. Default is 0.

step (int) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of integers incremented by the step value from start to stop, including the stop value.

itr_in(stop, start, step)

Creates an array of floats from start to stop with a specified step, including the stop value.

Parameters:

stop (float) : The end value of the iterator, inclusive.

start (float) : The starting value of the iterator. Default is 0.

step (float) : The increment value for each step in the iterator. Default is 1. Must be greater than 0.

Returns: An array of floats incremented by the step value from start to stop, including the stop value.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

method iterate(self, reverse)

Creates an iterator array for the indices of ana array, with an option to reverse the order.

Namespace types: array

Parameters:

self (array) : The array to iterate over.

reverse (bool) : A boolean flag indicating whether to reverse the iterator order. Default is false.

Returns: An array of integers representing the indices of the array. The order can be reversed if specified.

LibraryBitwiseOperandsLibrary "LibraryBitwiseOperands"

Description: When you need more space for your data you can use bitwise operations. For example if you are creating an Order Block indicator and you have multiple types then you can define variables for each type with only one bit set like these:

const int TYPE_OB = 1

const int TYPE_HH = 2

const int TYPE_LH = 4

const int TYPE_HL = 8

const int TYPE_LL = 16

const int TYPE_BOS = 32

const int TYPE_CHOCH = 64

bitwise_shift_left(x, y)

bitwise_shift_left(): Bitwise left shift: x << y

Parameters:

x (int)

y (int)

Returns: : The left operand’s value is moved toward left by the number of bits specified by the right operand.

bitwise_shift_right(x, y)

bitwise_shift_right(): Bitwise right shift: x >> y

Parameters:

x (int)

y (int)

Returns: : The left operand’s value is moved toward right by the number of bits specified by the right operand.

bitwise_not(x)

bitwise_not(): Bitwise NOT: ~x

Parameters:

x (int)

Returns: : Inverts individual bits.

bitwise_and(x, y)

bitwise_and(): Bitwise AND: x & y

Parameters:

x (int)

y (int)

Returns: : Result bit 1, if both operand bits are 1; otherwise results bit 0.

bitwise_or(x, y)

bitwise_or(): Bitwise OR: x | y

Parameters:

x (int)

y (int)

Returns: : Result bit 1, if any of the operand bit is 1; otherwise results bit 0.

bitwise_xor(x, y)

bitwise_xor(): Bitwise (exclusive OR) XOR: x ^ y

Parameters:

x (int)

y (int)

Returns: : Result bit 1, if any of the operand bit is 1 but not both, otherwise results bit 0.

logical_xor(x, y)

logical_xor(): Logical (exclusive OR) XOR: x xor y

Parameters:

x (bool)

y (bool)

Returns: : Result true, if any of the operand bit are different, otherwise results bit 0.

bit_check(x, y)

bit_check(): Bitwise Checks the specified bit

Parameters:

x (int)

y (int)

Returns: : Returns True if the bit is set.

bit_set(x, y)

bit_set(): Bitwise Sets the specified bit

Parameters:

x (int)

y (int)

Returns: : Returns a value with the bit set.

bit_clear(x, y)

bit_clear(): Bitwise Clears the specified bit

Parameters:

x (int)

y (int)

Returns: : Returns a value with the bit cleared.

bit_flip(x, y)

bit_flip(): Bitwise Inverts the specified bit

Parameters:

x (int)

y (int)

Returns: : Returns a value with the bit inverted.

bitmask_check(x, mask)

bitmask_check(): Bitwise Checks the specified Mask

Parameters:

x (int)

mask (int)

Returns: : Returns True if the mask is set.

bitmask_set(x, mask)

bitmask_set(): Bitwise Sets the specified Mask

Parameters:

x (int)

mask (int)

Returns: : Returns a value with the mask set.

bitmask_clear(x, mask)

bitmask_clear(): Bitwise Clears the specified Mask

Parameters:

x (int)

mask (int)

Returns: : Returns a value with the mask cleared.

bitmask_flip(x, mask)

bitmask_flip(): Inverts the specified Mask

Parameters:

x (int)

mask (int)

Returns: : Returns a value with the mask inverted.

math_bit_check(x, y)

math_bit_check(): Fast arithmetic bitwise Checks the specified Mask

Parameters:

x (int)

y (int)

Returns: : Returns True if the mask is set.

math_bit_set(x, y)

math_bit_set(): Fast arithmetic bitwise Sets the specified bit

Parameters:

x (int)

y (int)

Returns: : Returns a value with the bit set.

math_bit_clear(x, y)

math_bit_clear(): Fast arithmetic bitwise Clears the specified bit

Parameters:

x (int)

y (int)

Returns: : Returns a value with the bit cleared.

math_bitmask_check(x, y)

math_bitmask_check(): Fast arithmetic bitwise Checks the specified Mask

Parameters:

x (int)

y (int)

Returns: : Returns True if the mask is set.

math_bitmask_set(x, y)

math_bitmask_set(): Fast arithmetic bitwise Sets the specified Mask

Parameters:

x (int)

y (int)

Returns: : Returns a value with the mask set.

math_bitmask_clear(x, y)

math_bitmask_clear(): Fast arithmetic bitwise Clears the specified Mask

Parameters:

x (int)

y (int)

Returns: : Returns a value with the mask cleared.

SpectrumLibrary "Spectrum"

This library includes spectrum analysis tools such as the Fast Fourier Transform (FFT).

method toComplex(data, polar)

Creates an array of complex type objects from a float type array.

Namespace types: array

Parameters:

data (array) : The float type array of input data.

polar (bool) : Initialization coordinates; the default is false (cartesian).

Returns: The complex type array of converted data.

method sAdd(data, value, end, start, step)

Performs scalar addition of a given float type array and a simple float value.

Namespace types: array

Parameters:

data (array) : The float type array of input data.

value (float) : The simple float type value to be added.

end (int) : The last index of the input array (exclusive) on which the operation is performed.

start (int) : The first index of the input array (inclusive) on which the operation is performed; the default value is 0.

step (int) : The step by which the function iterates over the input data array between the specified boundaries; the default value is 1.

Returns: The modified input array.

method sMult(data, value, end, start, step)

Performs scalar multiplication of a given float type array and a simple float value.

Namespace types: array

Parameters:

data (array) : The float type array of input data.

value (float) : The simple float type value to be added.