Crude Oil Time + Fix Catalyst StrategyHybrid Workflow: Event-Driven Macro + Market DNA Micro

1. Macro Catalyst Layer (Your Overlays)

Event Mapping: Fed decisions, LBMA fixes, EIA releases, OPEC+ meetings.

Regime Filters: Risk-on/off, volatility regimes, macro bias (hawkish/dovish).

Volatility Scaling: ATR-based position sizing, adaptive overlays for London/NY sessions.

Governance: Max trades/day, cool-down logic, session boundaries.

👉 This layer answers when and why to engage.

2. Micro Execution Layer (Market DNA)

Order Flow Confirmation: Tape reading (Level II, time & sales, bid/ask).

Liquidity Zones: Identify support/resistance pools where buyers/sellers cluster.

Imbalance Detection: Aggressive buyers/sellers overwhelming the other side.

Precision Entry: Only trigger trades when order flow confirms macro catalyst bias.

Risk Discipline: Tight stops beyond liquidity zones, conviction-based scaling.

👉 This layer answers how and where to engage.

3. Unified Playbook

Step Macro Overlay (Your Edge) Market DNA (Jay’s Edge) Result

Event Trigger Fed/LBMA/OPEC+ catalyst flagged — Volatility window opens

Bias Filter Hawkish/dovish regime filter — Directional bias set

Sizing ATR volatility scaling — Position size calibrated

Execution — Tape confirms liquidity imbalance Precision entry

Risk Control Governance rules (cool-down, max trades) Tight stops beyond liquidity zones Disciplined exits

4. Gold & Silver Use Case

Gold (Fed Day):

Overlay flags volatility window → bias hawkish.

Market DNA shows sellers hitting bids at resistance.

Enter short with volatility-scaled size, stop just above liquidity zone.

Silver (LBMA Fix):

Overlay highlights fix window → bias neutral.

Market DNA shows buyers stepping in at support.

Enter long with adaptive size, HUD displays risk metrics.

5. HUD Integration

Macro Dashboard: Catalyst timeline, regime filter status, volatility bands.

Micro Dashboard: Live tape imbalance meter, liquidity zone map, conviction score.

Unified View: Macro tells you when to look, micro tells you when to pull the trigger.

⚡ This hybrid workflow gives you macro awareness + micro precision. Your overlays act as the radar, Jay’s Market DNA acts as the laser scope. Together, they create a disciplined, event-aware, volatility-scaled playbook for gold and silver.

Antonio — do you want me to draft this into a compile-safe Pine Script v6 template that embeds the macro overlay logic, while leaving hooks for Market DNA-style execution (order flow confirmation)? That way you’d have a production-ready skeleton to extend across TradingView, TradeStation, and NinjaTrader.

Antonio — do you want me to draft this into a compile-safe Pine Script v6 template that embeds the macro overlay logic, while leaving hooks for Market DNA-style execution (order flow confirmation)? That way you’d have a production-ready skeleton to extend across TradingView, TradeStation, and NinjaTrader.

Chỉ báo và chiến lược

Liquidity Sweep + BOS Retest System — Prop Firm Edition🟦 Liquidity Sweep + BOS Retest System — Prop Firm Edition

A High-Probability Smart Money Strategy Built for NQ, ES, and Funding Accounts

🚀 Overview

The Liquidity Sweep + BOS Retest System (Prop Firm Edition) is a precision-engineered SMC strategy built specifically for prop firm traders. It mirrors institutional liquidity behavior and combines it with strict account-safe entry rules to help traders pass and maintain funding accounts with consistency.

Unlike typical indicators, this system waits for three confirmations — liquidity sweep, displacement, and a clean retest — before executing any trade. Every component is optimized for low drawdown, high R:R, and prop-firm-approved risk management.

Whether you’re trading Apex, TakeProfitTrader, FFF, or OneUp Trader, this system gives you a powerful mechanical framework that keeps you within rules while identifying the market’s highest-probability reversal zones.

🔥 Key Features

1. Liquidity Sweep Detection (Stop Hunt Logic)

Automatically identifies when price clears a previous swing high/low with a sweep confirmation candle.

✔ Filters noise

✔ Eliminates early entries

✔ Locks onto true liquidity grabs

2. Automatic Break of Structure (BOS) Confirmation

Price must show true displacement by breaking structure opposite the sweep direction.

✔ Confirms momentum shift

✔ Removes fake reversals

✔ Ensures institutional intent

3. Precision Retest Entry Model

The strategy enters only when price retests the BOS level at premium/discount pricing.

✔ Zero chasing

✔ Extremely tight stop loss placement

✔ Prop-firm-friendly controlled risk

4. Built-In Risk & Trade Management

SL set at swept liquidity

TP set by user-defined R:R multiplier

Optional session filter (NY Open by default)

One trade at a time (no pyramiding)

Automatically resets logic after each trade

This prevents overtrading — the #1 cause of evaluation and account breaches.

5. Designed for Prop Firm Futures Trading

This script is optimized for:

Trailing/static drawdown accounts

Micro contract precision

Funding evaluations

Low-risk, high-probability setups

Structured, rule-based execution

It reduces randomness and emotional trading by automating the highest-quality SMC sequence.

🎯 The Trading Model Behind the System

Step 1 — Liquidity Sweep

Price must take out a recent high/low and close back inside structure.

This confirms stop-hunting behavior and marks the beginning of a potential reversal.

Step 2 — BOS (Break of Structure)

Price must break the opposite side swing with a displacement candle. This validates a directional shift.

Step 3 — Retest Entry

The system waits for price to retrace into the BOS level and signal continuation.

This creates optimal R:R entry with minimal drawdown.

📈 Best Markets

NQ (NASDAQ Futures) – Highly recommended

ES, YM, RTY

Gold (XAUUSD)

FX majors

Crypto (with high volatility)

Works best on 1m, 2m, 5m, or 15m depending on your trading style.

🧠 Why Traders Love This System

✔ No signals until all confirmations align

✔ Reduces overtrading and emotional decisions

✔ Follows market structure instead of random indicators

✔ Perfect for maintaining long-term funded accounts

✔ Built around institutional-grade concepts

✔ Makes your trading consistent, calm, and rules-based

⚙️ Recommended Settings

Session: 06:30–08:00 MST (NY Open)

R:R: 1.5R – 3R

Contracts: Start with 1–2 micros

Markets: NQ for best structure & volume

📦 What’s Included

Complete strategy logic

All plots, labels, sweep markers & BOS alerts

BOS retest entry automation

Session filtering

Stop loss & take profit system

Full SMC logic pipeline

🏁 Summary

The Liquidity Sweep + BOS Retest System is a complete, prop-firm-ready, structure-based strategy that automates one of the cleanest and most reliable SMC entry models. It is designed to keep you safe, consistent, and rule-compliant while capturing premium institutional setups.

If you want to trade with confidence, discipline, and prop-firm precision — this system is for you.

Good Luck -BG

Rasta Long/Short — StrategyThe Rasta Long/Short Strategy is a visual and educational framework designed to help traders study momentum shifts that appear when a fast EMA interacts with a slower smoothed baseline.

It is not a signal service. Instead, it is a research tool that helps you observe transitions, structure, and behavior across different market conditions and smoothing contexts.

The script plots:

A primary EMA line (fast reaction wave).

A Smoothed line (your chosen smoothing method).

Color-coded fog regions showing directional bias.

Optional DNA rung connections between the two lines for structural comparison.

Together, these allow a deeper study of how momentum pushes, volatility compression, expansions, and drift emerge around fast/slow EMA interactions.

✦ Core Idea

The Rasta Long/Short mechanism studies how price behaves when the fast EMA crosses above or below a smoothed anchor.

Rather than predicting price, it reveals where transitions occur across different structures, timeframes, and smoothing techniques.

The Long/Short logic simply highlights flips in directional structure.

It is not intended for real-time signals or automated execution; it is intended for understanding market movement.

✦ Smoothing Types (Explained)

The strategy allows experimenting with several smoothing families to observe how they transform the fast EMA:

SMA (Simple Moving Average)

Averaged, slower response. Good for stability comparisons.

EMA (Exponential)

Faster reaction, more responsive, smoother behavior during momentum.

RMA (Wilder’s)

Used in RSI calculations; steady, well-balanced response.

WMA (Weighted)

More weight to recent bars; bridges SMA and EMA dynamics.

None

Raw EMA vs EMA interaction with no secondary smoothing.

Each smoothing type provides unique structural information and can lead to different interpretations.

✦ Modes of Study

Designed for multi-timeframe research:

1H / 4H — Momentum flow mapping and structural identification.

Daily / Weekly — Higher-timeframe rotations, macro structure transitions.

1–15m — Microstructure studies, noise vs trend emergence.

Use the built-in Strategy Tester to explore entry/exit context, but treat results as research, not predictive performance.

✦ Components (Visual Study Tools)

EMA Line (Fast)

Primary reactive wave. Shows fast directional shifts.

Smoothed Line (Slow)

Trend baseline / reference structure.

Fog Region

Highlights fast-vs-smoothed directional alignment.

DNA Rungs (Optional)

Structural “bridges” showing the exact relationship between waves on each bar.

Useful for studying separation, compression, and expansions.

✦ Educational Insights

This strategy helps illuminate:

How fast and slow EMAs interact dynamically.

How structure changes precede trend emergence.

Where volatility compresses before expansion.

How noise, drift, and clean reversals differ.

How different smoothers alter the interpretation of the same price data.

The goal is clarity — not prediction.

✦ How to Use

Apply to any timeframe or instrument.

Enable or disable fog depending on preferred visibility.

Use DNA rungs for close structural comparison.

Observe long/short flips as educational reference points — not signals.

Study transitions visually, then backtest using the Strategy Tester for pattern research.

✦ Disclaimer

This script is provided for educational and research purposes only.

It does not provide trading signals, financial advice, or recommendations.

Past behavior does not indicate future performance.

Always practice risk-aware study and consult qualified financial professionals when needed.

✦ Author

Michael Culpepper (mikeyc747)

Creator of the Rasta framework and related market structure studies.

Faraz Perfect Structure XL / XS (Trend-Filtered)Faraz’s Perfect Structure XL/XS identifies premium trend continuation and reversal setups using a three-filter system:

structural breakouts using dynamic swing-based support/resistance,

trend confirmation via 200-EMA slope,

momentum validation through RSI and MACD.

Signals only trigger when all factors align, eliminating noise, chop, and false signals.

Designed for traders who want clean, high-probability long (XL) and short (XS) entries.

EMA 50/200 Pullback + RSI (BTC/USDT 15m - 2 Bar Logic)I recognize that combining indicators requires clear justification on how the components interact Therefore the new scripts description will explicitly detail the strategys operational logic

Objective The strategy is a Trend Following Pullback System designed for high frequency time frames 15m

Synergy The EMA50 EMA200 defines the primary Trend Direction Trend Filter It then utilizes a 2 Bar Pullback Logic to find an entry point where the price has momentarily reversed against the trendline and the RSI 14 serves as a Momentum Filter RSI greater than 50 for Long RSI less than 50 for Short to minimize false signals

EMA Cross Strategy v5 (30 lots) (15 min candle only)- safe flip🚀 EMA Cross Strategy v5 (30 Lots) (15 min candle only)— Safe Flip Edition

Fully Automated | Fast | Reliable | Battle-tested

Welcome to a clean, powerful, and automation-friendly EMA crossover system.

This strategy is built for traders who want consistent trend-based entries without the risk of unwanted pyramiding or doubled positions.

🔥 How It Works

This strategy uses a fast EMA (10) crossing a slow EMA (20) to detect trend shifts:

Bullish Crossover → LONG (30 lots)

Bearish Crossover → SHORT (30 lots)

Every opposite signal safely flips the position by first closing the current trade, then opening a fresh position of exactly 30 lots.

No doubling.

No runaway position size.

No surprises.

Just clean, mechanical trend-following.

📈 Why This Strategy Stands Out

Unlike basic EMA crossbots, this version:

✔ Prevents unintended pyramiding

✔ Never over-allocates capital

✔ Works perfectly with webhook-based automation

✔ Produces stable, systematic entries

✔ Executes directional flips with precision

🔍 Backtest Highlights (1-Year)

(Backtests will vary by instrument/timeframe)

1,500+ trades executed

Profit factor above 1.27

Strong trend performance

Balanced long/short behavior

No margin calls

Consistent trade execution

This strategy thrives in trending markets and maintains strict discipline even in choppy conditions.

⚙️ Automation Ready

Designed for automated execution via webhook and API setups on supported platforms.

Just connect, run, and let the bot follow the rules without hesitation.

No emotions.

No overtrading.

No fear or greed.

Pure logic.

XiaoJiu_RSI_5m_Drop1_DCA✔ Automatic buy when RSI < 30

✔ Automatic averaging down for every 1 point drop in RSI (maximum 21 times)

✔ Automatic liquidation when RSI > 70

✔ 28U per average averaging down

✔ Automatically calculates weighted average cost

✔ Automatically displays actual profit

✔ Can be tested on any coin and at any time

✔ Complete DCA model

Golden Cross 50/200 EMATrend-following systems are characterized by having a low win rate, yet in the right circumstances (trending markets and higher timeframes) they can deliver returns that even surpass those of systems with a high win rate.

Below, I show you a simple bullish trend-following system with clear execution rules:

System Rules

-Long entries when the 50-period EMA crosses above the 200-period EMA.

-Stop Loss (SL) placed at the lowest low of the 15 candles prior to the entry candle.

-Take Profit (TP) triggered when the 50-period EMA crosses below the 200-period EMA.

Risk Management

-Initial capital: $10,000

-Position size: 10% of capital per trade

-Commissions: 0.1% per trade

Important Note:

In the code, the stop loss is defined using the swing low (15 candles), but the position size is not adjusted based on the distance to the stop loss. In other words, 10% of the equity is risked on each trade, but the actual loss on the trade is not controlled by a maximum fixed percentage of the account — it depends entirely on the stop loss level. This means the loss on a single trade could be significantly higher or lower than 10% of the account equity, depending on volatility.

Implementing leverage or reducing position size based on volatility is something I haven’t been able to include in the code, but it would dramatically improve the system’s performance. It would fix a consistent percentage loss per trade, preventing losses from fluctuating wildly with changes in volatility.

For example, we can maintain a fixed loss percentage when volatility is low by using the following formula:

Leverage = % of SL you’re willing to risk / % volatility from entry point to stop loss

And when volatility is high and would exceed the fixed percentage we want to expose per trade (if the SL is hit), we could reduce the position size accordingly.

Practical example:

Imagine we only want to risk 15% of the position value if the stop loss is triggered on Tesla (which has high volatility), but the distance to the SL represents a potential 23.57% drop. In this case, we subtract the desired risk (15%) from the actual volatility-based loss (23.57%):

23.57% − 15% = 8.57%

Now suppose we normally use $200 per trade.

To calculate 8.57% of $200:

200 × (8.57 / 100) = $17.14

Then subtract that amount from the original position size:

$200 − $17.14 = $182.86

In summary:

If we reduce the position size to $182.86 (instead of the usual $200), even if Tesla moves 23.57% against us and hits the stop loss, we would still only lose approximately 15% of the original $200 position — exactly the risk level we defined. This way, we strictly respect our risk management rules regardless of volatility swings.

I hope this clearly explains the importance of capping losses at a fixed percentage per trade. This keeps risk under control while maintaining a consistent percentage of capital invested per trade — preventing both statistical distortion of the system and the potential destruction of the account.

About the code:

Strategy declaration:

The strategy is named 'Golden Cross 50/200 EMA'.

overlay=true means it will be drawn directly on the price chart.

initial_capital=10000 sets the initial capital to $10,000.

default_qty_type=strategy.percent_of_equity and default_qty_value=10 means each trade uses 10% of available equity.

margin_long=0 indicates no margin is used for long positions (this is likely for simulation purposes only; in real trading, margin would be required).

commission_type=strategy.commission.percent and commission_value=0.1 sets a 0.1% commission per trade.

Indicators:

Calculates two EMAs: a 50-period EMA (ema50) and a 200-period EMA (ema200).

Crossover detection:

bullCross is triggered when the 50-period EMA crosses above the 200-period EMA (Golden Cross).

bearCross is triggered when the 50-period EMA crosses below the 200-period EMA (Death Cross).

Recent swing:

swingLow calculates the lowest low of the previous 15 periods.

Stop Loss:

entryStopLoss is a variable initialized as na (not available) and is updated to the current swingLow value whenever a bullCross occurs.

Entry and exit conditions:

Entry: When a bullCross occurs, the initial stop loss is set to the current swingLow and a long position is opened.

Exit on opposite signal: When a bearCross occurs, the long position is closed.

Exit on stop loss: If the price falls below entryStopLoss while a position is open, the position is closed.

Visualization:

Both EMAs are plotted (50-period in blue, 200-period in red).

Green triangles are plotted below the bar on a bullCross, and red triangles above the bar on a bearCross.

A horizontal orange line is drawn that shows the stop loss level whenever a position is open.

Alerts:

Alerts are created for:Long entry

Exit on bearish crossover (Death Cross)

Exit triggered by stop loss

Favorable Conditions:

Tesla (45-minute timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $12,458.73 or +124.59%

Maximum drawdown: $1,210.40 or 8.29%

Total trades: 107

Winning trades: 27.10% (29/107)

Profit factor: 3.141

Tesla (1-hour timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $7,681.83 or +76.82%

Maximum drawdown: $993.36 or 7.30%

Total trades: 75

Winning trades: 29.33% (22/75)

Profit factor: 3.157

Netflix (45-minute timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,380.73 or +113.81%

Maximum drawdown: $699.45 or 5.98%

Total trades: 134

Winning trades: 36.57% (49/134)

Profit factor: 2.885

Netflix (1-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,689.05 or +116.89%

Maximum drawdown: $844.55 or 7.24%

Total trades: 107

Winning trades: 37.38% (40/107)

Profit factor: 2.915

Netflix (2-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $12,807.71 or +128.10%

Maximum drawdown: $866.52 or 6.03%

Total trades: 56

Winning trades: 41.07% (23/56)

Profit factor: 3.891

Meta (45-minute timeframe)

May 18, 2012 – November 17, 2025

Total net profit: $2,370.02 or +23.70%

Maximum drawdown: $365.27 or 3.50%

Total trades: 83

Winning trades: 31.33% (26/83)

Profit factor: 2.419

Apple (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,232.55 or +80.59%

Maximum drawdown: $581.11 or 3.16%

Total trades: 140

Winning trades: 34.29% (48/140)

Profit factor: 3.009

Apple (1-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $9,685.89 or +94.93%

Maximum drawdown: $374.69 or 2.26%

Total trades: 118

Winning trades: 35.59% (42/118)

Profit factor: 3.463

Apple (2-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,001.28 or +77.99%

Maximum drawdown: $755.84 or 7.56%

Total trades: 67

Winning trades: 41.79% (28/67)

Profit factor: 3.825

NVDA (15-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $11,828.56 or +118.29%

Maximum drawdown: $1,275.43 or 8.06%

Total trades: 466

Winning trades: 28.11% (131/466)

Profit factor: 2.033

NVDA (30-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $12,203.21 or +122.03%

Maximum drawdown: $1,661.86 or 10.35%

Total trades: 245

Winning trades: 28.98% (71/245)

Profit factor: 2.291

NVDA (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $16,793.48 or +167.93%

Maximum drawdown: $1,458.81 or 8.40%

Total trades: 172

Winning trades: 33.14% (57/172)

Profit factor: 2.927

RSI BREAKOUT SIGNALSThis BB + RSI Breakout indicator is designed to help traders identify potential buy and sell opportunities based on price movements relative to the Donchian channel (or Bollinger-type channel) and momentum conditions. It calculates the highest high and lowest low over a user-defined length to form a dynamic channel, and then it checks whether the current price breaks above the upper band (for a buy signal) or below the lower band (for a sell signal). To avoid repeated signals in a row, the indicator uses a state system: after a buy signal occurs, it will not generate another buy until a sell occurs, and vice versa. When a buy signal is triggered, it automatically calculates a take-profit price a certain percentage above the buy candle and displays this price below the candle as a “TP” label. Sell signals are displayed above the candle, and any previous TP label is cleared. The indicator updates in real time, so the signals move with the chart, giving a clear and lag-free visualization of entry points and potential profit targets.

BTC EMA 5-9 Flip Strategy AutobotThis strategy is designed for fast and accurate trend-following trades on Bitcoin.

It uses a crossover between EMA 5 and EMA 9 to detect instant trend reversals and automatically flips between Long and Short positions.

How the strategy works

EMA 5 crossing above EMA 9 → Long

EMA 5 crossing below EMA 9 → Short

Automatically closes the opposite trade during a flip

Executes trades only on candle close

Prevents double entries with internal position-state logic

Fully compatible with automated trading via webhooks (Delta Exchange)

Why this strategy works

EMA 5–9 is extremely responsive for BTC’s volatility

Captures trend reversals early

Works best on 15-minute timeframe

Clean, simple logic without over-filtering reduces missed opportunities

Performs well in both uptrends and downtrends

Automation Ready

This strategy includes alert conditions and webhook-ready JSON for automated execution.

This is a fast-reacting BTC bot designed for intraday and swing crypto trend trading.

SP500 Session Gap Fade StrategySummary in one paragraph

SPX Session Gap Fade is an intraday gap fade strategy for index futures, designed around regular cash sessions on five minute charts. It helps you participate only when there is a full overnight or pre session gap and a valid intraday session window, instead of trading every open. The original part is the gap distance engine which anchors both stop and optional target to the previous session reference close at a configurable flat time, so every trade’s risk scales with the actual gap size rather than a fixed tick stop.

Scope and intent

• Markets. Primarily index futures such as ES, NQ, YM, and liquid index CFDs that exhibit overnight gaps and regular cash hours.

• Timeframes. Intraday timeframes from one minute to fifteen minutes. Default usage is five minute bars.

• Default demo used in the publication. Symbol CME:ES1! on a five minute chart.

• Purpose. Provide a simple, transparent way to trade opening gaps with a session anchored risk model and forced flat exit so you are not holding into the last part of the session.

• Limits. This is a strategy. Orders are simulated on standard candles only.

Originality and usefulness

• Unique concept or fusion. The core novelty is the combination of a strict “full gap” entry condition with a session anchored reference close and a gap distance based TP and SL engine. The stop and optional target are symmetric multiples of the actual gap distance from the previous session’s flat close, rather than fixed ticks.

• Failure mode it addresses. Fixed sized stops do not scale when gaps are unusually small or unusually large, which can either under risk or over risk the account. The session flat logic also reduces the chance of holding residual positions into late session liquidity and news.

• Testability. All key pieces are explicit in the Inputs: session window, minutes before session end, whether to use gap exits, whether TP or SL are active, and whether to allow candle based closes and forced flat. You can toggle each component and see how it changes entries and exits.

• Portable yardstick. The main unit is the absolute price gap between the entry bar open and the previous session reference close. tp_mult and sl_mult are multiples of that gap, which makes the risk model portable across contracts and volatility regimes.

Method overview in plain language

The strategy first defines a trading session using exchange time, for example 08:30 to 15:30 for ES day hours. It also defines a “flat” time a fixed number of minutes before session end. At the flat bar, any open position is closed and the bar’s close price is stored as the reference close for the next session. Inside the session, the strategy looks for a full gap bar relative to the prior bar: a gap down where today’s high is below yesterday’s low, or a gap up where today’s low is above yesterday’s high. A full gap down generates a long entry; a full gap up generates a short entry. If the gap risk engine is enabled and a valid reference close exists, the strategy measures the distance between the entry bar open and that reference close. It then sets a stop and optional target as configurable multiples of that gap distance and manages them with strategy.exit. Additional exits can be triggered by a candle color flip or by the forced flat time.

Base measures

• Range basis. The main unit is the absolute difference between the current entry bar open and the stored reference close from the previous session flat bar. That value is used as a “gap unit” and scaled by tp_mult and sl_mult to build the target and stop.

Components

• Component one: Gap Direction. Detects full gap up or full gap down by comparing the current high and low to the previous bar’s high and low. Gap down signals a long fade, gap up signals a short fade. There is no smoothing; it is a strict structural condition.

• Component two: Session Window. Only allows entries when the current time is within the configured session window. It also defines a flat time before the session end where positions are forced flat and the reference close is updated.

• Component three: Gap Distance Risk Engine. Computes the absolute distance between the entry open and the stored reference close. The stop and optional target are placed as entry ± gap_distance × multiplier so that risk scales with gap size.

• Optional component: Candle Exit. If enabled, a bullish bar closes short positions and a bearish bar closes long positions, which can shorten holding time when price reverses quickly inside the session.

• Session windows. Session logic uses the exchange time of the chart symbol. When changing symbols or venues, verify that the session time string still matches the new instrument’s cash hours.

Fusion rule

All gates are hard conditions rather than weighted scores. A trade can only open if the session window is active and the full gap condition is true. The gap distance engine only activates if a valid reference close exists and use_gap_risk is on. TP and SL are controlled by separate booleans so you can use SL only, TP only, or both. Long and short are symmetric by construction: long trades fade full gap downs, short trades fade full gap ups with mirrored TP and SL logic.

Signal rule

• Long entry. Inside the active session, when the current bar shows a full gap down relative to the previous bar (current high below prior low), the strategy opens a long position. If the gap risk engine is active, it places a gap based stop below the entry and an optional target above it.

• Short entry. Inside the active session, when the current bar shows a full gap up relative to the previous bar (current low above prior high), the strategy opens a short position. If the gap risk engine is active, it places a gap based stop above the entry and an optional target below it.

• Forced flat. At the configured flat time before session end, any open position is closed and the close price of that bar becomes the new reference close for the following session.

• Candle based exit. If enabled, a bearish bar closes longs, and a bullish bar closes shorts, regardless of where TP or SL sit, as long as a position is open.

What you will see on the chart

• Markers on entry bars. Standard strategy entry markers labeled “long” and “short” on the gap bars where trades open.

• Exit markers. Standard exit markers on bars where either the gap stop or target are hit, or where a candle exit or forced flat close occurs. Exit IDs “long_gap” and “short_gap” label gap based exits.

• Reference levels. Horizontal lines for the current long TP, long SL, short TP, and short SL while a position is open and the gap engine is enabled. They update when a new trade opens and disappear when flat.

• Session background. This version does not add background shading for the session; session logic runs internally based on time.

• No on chart table. All decisions are visible through orders and exit levels. Use the Strategy Tester for performance metrics.

Inputs with guidance

Session Settings

• Trading session (sess). Session window in exchange time. Typical value uses the regular cash session for each contract, for example “0830-1530” for ES. Adjust if your broker or symbol uses different hours.

• Minutes before session end to force exit (flat_before_min). Minutes before the session end where positions are forced flat and the reference close is stored. Typical range is 15 to 120. Raising it closes trades earlier in the day; lowering it allows trades later in the session.

Gap Risk

• Enable gap based TP/SL (use_gap_risk). Master switch for the gap distance exit engine. Turning it off keeps entries and forced flat logic but removes automatic TP and SL placement.

• Use TP limit from gap (use_gap_tp). Enables gap based profit targets. Typical values are true for structured exits or false if you want to manage exits manually and only keep a stop.

• Use SL stop from gap (use_gap_sl). Enables gap based stop losses. This should normally remain true so that each trade has a defined initial risk in ticks.

• TP multiplier of gap distance (tp_mult). Multiplier applied to the gap distance for the target. Typical range is 0.5 to 2.0. Raising it places the target further away and reduces hit frequency.

• SL multiplier of gap distance (sl_mult). Multiplier applied to the gap distance for the stop. Typical range is 0.5 to 2.0. Raising it widens the stop and increases risk per trade; lowering it tightens the stop and may increase the number of small losses.

Exit Controls

• Exit with candle logic (use_candle_exit). If true, closes shorts on bullish candles and longs on bearish candles. Useful when you want to react to intraday reversal bars even if TP or SL have not been reached.

• Force flat before session end (use_forced_flat). If true, guarantees you are flat by the configured flat time and updates the reference close. Turn this off only if you understand the impact on overnight risk.

Filters

There is no separate trend or volatility filter in this version. All trades depend on the presence of a full gap bar inside the session. If you need extra filtering such as ATR, volume, or higher timeframe bias, they should be added explicitly and documented in your own fork.

Usage recipes

Intraday conservative gap fade

• Timeframe. Five minute chart on ES regular session.

• Gap risk. use_gap_risk = true, use_gap_tp = true, use_gap_sl = true.

• Multipliers. tp_mult around 0.7 to 1.0 and sl_mult around 1.0.

• Exits. use_candle_exit = false, use_forced_flat = true. Focus on the structured TP and SL around the gap.

Intraday aggressive gap fade

• Timeframe. Five minute chart.

• Gap risk. use_gap_risk = true, use_gap_tp = false, use_gap_sl = true.

• Multipliers. sl_mult around 0.7 to 1.0.

• Exits. use_candle_exit = true, use_forced_flat = true. Entries fade full gaps, stops are tight, and candle color flips flatten trades early.

Higher timeframe gap tests

• Timeframe. Fifteen minute or sixty minute charts on instruments with regular gaps.

• Gap risk. Keep use_gap_risk = true. Consider slightly higher sl_mult if gaps are structurally wider on the higher timeframe.

• Note. Expect fewer trades and be careful with sample size; multi year data is recommended.

Properties visible in this publication

• On average our risk for each position over the last 200 trades is 0.4% with a max intraday loss of 1.5% of the total equity in this case of 100k $ with 1 contract ES. For other assets, recalculations and customizations has to be applied.

• Initial capital. 100 000.

• Base currency. USD.

• Default order size method. Fixed with size 1 contract.

• Pyramiding. 0.

• Commission. Flat 2 USD per order in the Strategy Tester Properties. (2$ buying + 2$selling)

• Slippage. One tick in the Strategy Tester Properties.

• Process orders on close. ON.

Realism and responsible publication

• No performance claims are made. Past results do not guarantee future outcomes.

• Costs use a realistic flat commission and one tick of slippage per trade for ES class futures.

• Default sizing with one contract on a 100 000 reference account targets modest per trade risk. In practice, extreme slippage or gap through events can exceed this, so treat the one and a half percent risk target as a design goal, not a guarantee.

• All orders are simulated on standard candles. Shapes can move while a bar is forming and settle on bar close.

Honest limitations and failure modes

• Economic releases, thin liquidity, and limit conditions can break the assumptions behind the simple gap model and lead to slippage or skipped fills.

• Symbols with very frequent or very large gaps may require adjusted multipliers or alternative risk handling, especially in high volatility regimes.

• Very quiet periods without clean gaps will produce few or no trades. This is expected behavior, not a bug.

• Session windows follow the exchange time of the chart. Always confirm that the configured session matches the symbol.

• When both the stop and target lie inside the same bar’s range, the TradingView engine decides which is hit first based on its internal intrabar assumptions. Without bar magnifier, tie handling is approximate.

Legal

Education and research only. This strategy is not investment advice. You remain responsible for all trading decisions. Always test on historical data and in simulation with realistic costs before considering any live use.

Moving Average Band StrategyOverview

The Moving Average Band Strategy is a fully customizable breakout and trend-continuation system designed for traders who need both simplicity and control.

The strategy creates adaptive bands around a user-selected moving average and executes trades when price breaks out of these bands, with advanced risk-management settings including optional Risk:Reward targets.

This script is suitable for intraday, swing, and positional traders across all markets — equities, futures, crypto, and forex.

Key Features

✔ Six Moving Average Types

Choose the MA that best matches your trading style:

SMA

EMA

WMA

HMA

VWMA

RMA

✔ Dynamic Bands

Upper Band built from MA of highs

Lower Band built from MA of lows

Adjustable band offset (%)

Color-coded band fill indicating price position

✔ Configurable Strategy Preferences

Toggle Long and/or Short trades

Toggle Risk:Reward Take-Profit

Adjustable Risk:Reward Ratio

Default position sizing: % of equity (configurable via strategy settings)

Entry Conditions

Long Entry

A long trade triggers when:

Price crosses above the Upper Band

Long trades are enabled

No existing long position is active

Short Entry

A short trade triggers when:

Price crosses below the Lower Band

Short trades are enabled

No existing short position is active

Clear entry markers and price labels appear on the chart.

Risk Management

This strategy includes a complete set of risk-controls:

Stop-Loss (Fixed at Entry)

Long SL: Lower Band

Short SL: Upper Band

These levels remain constant for the entire trade.

Optional Risk:Reward Take-Profit

Enabled/disabled using a toggle switch.

When enabled:

Long TP = Entry + (Risk × Risk:Reward Ratio)

Short TP = Entry – (Risk × Risk:Reward Ratio)

When disabled:

Exits are handled by reverse crossover signals.

Exit Conditions

Long Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Short Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Exit markers and price labels are plotted automatically.

Visual Tools

To improve clarity:

Upper & Lower Band (blue, adjustable width)

Middle Line

Dynamic band fill (green/red/yellow)

SL & TP line plotting when in position

Entry/Exit markers

Price labels for all executed trades

These are built to help users visually follow the strategy logic.

Alerts Included

Every trading event is covered:

Long Entry

Short Entry

Long SL / TP / Cross Exit

Short SL / TP / Cross Exit

Combined Alert for webhook/automation (JSON-formatted)

Perfect for algo trading, Discord bots, or automation platforms.

Best For

This strategy performs best in:

Trending markets

Breakout environments

High-momentum instruments

Clean intraday swings

Works seamlessly on:

Stocks

Index futures

Commodities

Crypto

Forex

⚠️ Important Disclaimer

This script is for educational purposes only.

Trading involves risk. Backtest results are not indicative of future performance.

Always validate settings and use proper position sizing.

MOMO – Imbalance Trend (SIMPLE BUY/SELL)MOMO – Imbalance Trend (SIMPLE BUY/SELL)

This strategy combines trend breaks, imbalance detection, and first-tap supply/demand entries to create a clean and disciplined trading model.

It automatically highlights imbalance candles, draws fresh zones, and waits for the first retest to deliver precise BUY and SELL signals.

Performance

On optimized settings, this strategy shows an estimated 57%–70% win-rate, depending on the asset and timeframe.

Actual performance may vary, but the model is built for consistency, discipline, and improved decision-making.

How it works

Detects trend structure shifts (BOS / Break of Trend)

Identifies displacement (imbalance) candles

Creates supply and demand zones from imbalance origin

Waits for first tap only (no second chances)

Confirms direction using trend logic

Generates clean BUY/SELL arrows

Automatic SL/TP based on user settings

Features

Clean BUY/SELL markers

Auto-drawn supply & demand zones

Trend break markers

Imbalance tags

Smart first-tap confirmation

Customizable stop loss & take profit

Works on crypto, gold, forex, indices

Best on M5–H1 for day trading

Note

This strategy is designed for day traders who want clarity, structure, and zero emotional trading.

Use it with discipline — and it will serve you well.

Good luck, soldier.

Positional Supertrend Strategy (1D Filter + 2H Entry)Positional Supertrend Strategy (1D Filter + 2H Entry)

ASHOK 15 Novashok trial 15 nov 1845h

I have created this strategy to convert my chart pattern and MACD, EMA observations to tradeable logic.

Any Strategy BacktestA simple script for backtesting your strategies with TP and SL settings. For this to work, your indicators must have sources for long and short conditions.

Qullamagi EMA Breakout Autotrade (Crypto Futures L+S)Title: Qullamagi EMA Breakout – Crypto Autotrade

Overview

A crypto-focused, Qullamagi-style EMA breakout strategy built for autotrading on futures and perpetual swaps.

It combines a 5-MA trend stack (EMA 10/20, SMA 50/100/200), volatility contraction boxes, volume spikes and an optional higher-timeframe 200-MA filter. The script supports both long and short trades, partial take profit, trailing MA exits and percent-of-equity position sizing for automated crypto futures trading.

Key Features (Crypto)

Qullamagi MA Breakout Engine – trades only when price is aligned with a strong EMA/SMA trend and breaks out of a tight consolidation range. Longs use: Close > EMA10 > EMA20 > SMA50 > SMA100 > SMA200. Shorts are the mirror condition with all MAs sloping in the trend direction.

Strict vs Loose Modes – Strict (Daily) is designed for cleaner swing trades on 1H–4H (full MA stack, box+ATR and volume filters, optional HTF filter). Loose (Intraday) focuses on 10/20/50 alignment with relaxed filters for more frequent 15m–30m signals.

Volatility & Volume Filters for Crypto – ATR-based box height limit to detect volatility contraction, wide-candle filter to avoid chasing exhausted breakouts, and a volume spike condition requiring current volume to exceed an SMA of volume.

Higher-Timeframe Trend Filter (Optional) – uses a 200-period SMA on a higher timeframe (default: 1D). Longs only when HTF close is above the HTF 200-SMA, shorts only when it is below, helping avoid trading against dominant crypto trends.

Autotrade-Oriented Trade Management – position size as % of equity, initial stop anchored to a chosen MA (EMA10 / EMA20 / SMA50) with optional buffer, partial take profit at a configurable R-multiple, trailing MA exit for the remainder, and an optional cooldown after a full exit.

Markets & Timeframes

Best suited for BTC, ETH and major altcoin futures/perpetuals (Binance, Bybit, OKX, etc.).

Strict preset: 1H–4H charts for classic Qullamagi-style trend structure and fewer fake breakouts.

Loose preset: 15m–30m charts for higher trade frequency and more active intraday trading.

Always retune ATR length, box length, volume multiplier and position size for each symbol and exchange.

Strategy Logic (Quick Summary)

Long (Strict): MA stack in bullish alignment with all MAs sloping up → tight volatility box (ATR-based) → volume spike above SMA(volume) × multiplier → breakout above box high (close or intrabar) → optional HTF close above 200-SMA.

Short: Mirror logic: bearish MA stack, tight box, volume spike and breakdown below box low with optional HTF downtrend.

Best Practices for Crypto

Backtest on each symbol and timeframe you plan to autotrade, including commissions and slippage.

Start on higher timeframes (1H/4H) to learn the behavior, then move to 15m–30m if you want more signals.

Use the higher-timeframe filter when markets are strongly trending to reduce counter-trend trades.

Keep position-size percentage conservative until you fully understand the drawdowns.

Forward-test / paper trade before connecting to live futures accounts.

Webhook / Autotrade Integration

Designed to work with TradingView webhooks and external crypto trading bots.

Alert messages include structured fields such as: EVENT=ENTRY / SCALE_OUT / EXIT, SIDE=LONG / SHORT, STRATEGY=Qullamagi_MA.

Map each EVENT + SIDE combination to your bot logic (open long/short, partial close, full close, etc.) on your preferred exchange.

Important Notes & Disclaimer

Crypto markets are highly volatile and can change regime quickly. Backtest and forward-test thoroughly before using real capital. Higher timeframes generally produce cleaner MA structures and fewer fake breakouts.

This strategy is for educational and informational purposes only and does not constitute financial advice. Trading leveraged crypto products involves substantial risk of loss. Always do your own research, manage risk carefully, and never trade with money you cannot afford to lose.

GMH : Tech Bubble Good Morning Holding

Simulating How to Ride the Bubble — and Jump Out Before the Crash

Be careful! Most simulation results show that this strategy sometimes underperforms a simple buy-and-hold, because it gives away positions during deep retracements and buys back at higher thresholds.

Humans often struggle with cutting losses. When the pain becomes too much, they lose the confidence needed to execute even a reasonable strategy.

But in terms of mentality, this approach reduces long-term portfolio volatility. It helps investors feel more at peace, especially during real market crashes like the tech bubble in 2021.

How to use : Select TimeFrame 4HR on trading view

QQQ Momentum Regime Rider (EMA + VWAP + ADX + Vol Pullback)My strategy catches intraday momentum, has a phenomenal return of 18% annually

Range Oscillator Strategy + Stoch Confirm🔹 Short summary

This is a free, educational long-only strategy built on top of the public “Range Oscillator” by Zeiierman (used under CC BY-NC-SA 4.0), combined with a Stochastic timing filter, an EMA-based exit filter and an optional risk-management layer (SL/TP and R-multiple exits). It is NOT financial advice and it is NOT a magic money machine. It’s a structured framework to study how range-expansion + momentum + trend slope can be combined into one rule-based system, often with intentionally RARE trades.

────────────────────────

0. Legal / risk disclaimer

────────────────────────

• This script is FREE and public. I do not charge any fee for it.

• It is for EDUCATIONAL PURPOSES ONLY.

• It is NOT financial advice and does NOT guarantee profits.

• Backtest results can be very different from live results.

• Markets change over time; past performance is NOT indicative of future performance.

• You are fully responsible for your own trades and risk.

Please DO NOT use this script with money you cannot afford to lose. Always start in a demo / paper trading environment and make sure you understand what the logic does before you risk any capital.

────────────────────────

1. About default settings and risk (very important)

────────────────────────

The script is configured with the following defaults in the `strategy()` declaration:

• `initial_capital = 10000`

→ This is only an EXAMPLE account size.

• `default_qty_type = strategy.percent_of_equity`

• `default_qty_value = 100`

→ This means 100% of equity per trade in the default properties.

→ This is AGGRESSIVE and should be treated as a STRESS TEST of the logic, not as a realistic way to trade.

TradingView’s House Rules recommend risking only a small part of equity per trade (often 1–2%, max 5–10% in most cases). To align with these recommendations and to get more realistic backtest results, I STRONGLY RECOMMEND you to:

1. Open **Strategy Settings → Properties**.

2. Set:

• Order size: **Percent of equity**

• Order size (percent): e.g. **1–2%** per trade

3. Make sure **commission** and **slippage** match your own broker conditions.

• By default this script uses `commission_value = 0.1` (0.1%) and `slippage = 3`, which are reasonable example values for many crypto markets.

If you choose to run the strategy with 100% of equity per trade, please treat it ONLY as a stress-test of the logic. It is NOT a sustainable risk model for live trading.

────────────────────────

2. What this strategy tries to do (conceptual overview)

────────────────────────

This is a LONG-ONLY strategy designed to explore the combination of:

1. **Range Oscillator (Zeiierman-based)**

- Measures how far price has moved away from an adaptive mean.

- Uses an ATR-based range to normalize deviation.

- High positive oscillator values indicate strong price expansion away from the mean in a bullish direction.

2. **Stochastic as a timing filter**

- A classic Stochastic (%K and %D) is used.

- The logic requires %K to be below a user-defined level and then crossing above %D.

- This is intended to catch moments when momentum turns up again, rather than chasing every extreme.

3. **EMA Exit Filter (trend slope)**

- An EMA with configurable length (default 70) is calculated.

- The slope of the EMA is monitored: when the slope turns negative while in a long position, and the filter is enabled, it triggers an exit condition.

- This acts as a trend-protection exit: if the medium-term trend starts to weaken, the strategy exits even if the oscillator has not yet fully reverted.

4. **Optional risk-management layer**

- Percentage-based Stop Loss and Take Profit (SL/TP).

- Risk/Reward (R-multiple) exit based on the distance from entry to SL.

- Implemented as OCO orders that work *on top* of the logical exits.

The goal is not to create a “holy grail” system but to serve as a transparent, configurable framework for studying how these concepts behave together on different markets and timeframes.

────────────────────────

3. Components and how they work together

────────────────────────

(1) Range Oscillator (based on “Range Oscillator (Zeiierman)”)

• The script computes a weighted mean price and then measures how far price deviates from that mean.

• Deviation is normalized by an ATR-based range and expressed as an oscillator.

• When the oscillator is above the **entry threshold** (default 100), it signals a strong move away from the mean in the bullish direction.

• When it later drops below the **exit threshold** (default 30), it can trigger an exit (if enabled).

(2) Stochastic confirmation

• Classic Stochastic (%K and %D) is calculated.

• An entry requires:

- %K to be below a user-defined “Cross Level”, and

- then %K to cross above %D.

• This is a momentum confirmation: the strategy tries to enter when momentum turns up from a pullback rather than at any random point.

(3) EMA Exit Filter

• The EMA length is configurable via `emaLength` (default 70).

• The script monitors the EMA slope: it computes the relative change between the current EMA and the previous EMA.

• If the slope turns negative while the strategy holds a long position and the filter is enabled, it triggers an exit condition.

• This is meant to help protect profits or cut losses when the medium-term trend starts to roll over, even if the oscillator conditions are not (yet) signalling exit.

(4) Risk management (optional)

• Stop Loss (SL) and Take Profit (TP):

- Defined as percentages relative to average entry price.

- Both are disabled by default, but you can enable them in the Inputs.

• Risk/Reward Exit:

- Uses the distance from entry to SL to project a profit target at a configurable R-multiple.

- Also optional and disabled by default.

These exits are implemented as `strategy.exit()` OCO orders and can close trades independently of oscillator/EMA conditions if hit first.

────────────────────────

4. Entry & Exit logic (high level)

────────────────────────

A) Time filter

• You can choose a **Start Year** in the Inputs.

• Only candles between the selected start date and 31 Dec 2069 are used for backtesting (`timeCondition`).

• This prevents accidental use of tiny cherry-picked windows and makes tests more honest.

B) Entry condition (long-only)

A long entry is allowed when ALL the following are true:

1. `timeCondition` is true (inside the backtest window).

2. If `useOscEntry` is true:

- Range Oscillator value must be above `entryLevel`.

3. If `useStochEntry` is true:

- Stochastic condition (`stochCondition`) must be true:

- %K < `crossLevel`, then %K crosses above %D.

If these filters agree, the strategy calls `strategy.entry("Long", strategy.long)`.

C) Exit condition (logical exits)

A position can be closed when:

1. `timeCondition` is true AND a long position is open, AND

2. At least one of the following is true:

- If `useOscExit` is true: Oscillator is below `exitLevel`.

- If `useMagicExit` (EMA Exit Filter) is true: EMA slope is negative (`isDown = true`).

In that case, `strategy.close("Long")` is called.

D) Risk-management exits

While a position is open:

• If SL or TP is enabled:

- `strategy.exit("Long Risk", ...)` places an OCO stop/limit order based on the SL/TP percentages.

• If Risk/Reward exit is enabled:

- `strategy.exit("RR Exit", ...)` places an OCO order using a projected R-multiple (`rrMult`) of the SL distance.

These risk-based exits can trigger before the logical oscillator/EMA exits if price hits those levels.

────────────────────────

5. Recommended backtest configuration (to avoid misleading results)

────────────────────────

To align with TradingView House Rules and avoid misleading backtests:

1. **Initial capital**

- 10 000 (or any value you personally want to work with).

2. **Order size**

- Type: **Percent of equity**

- Size: **1–2%** per trade is a reasonable starting point.

- Avoid risking more than 5–10% per trade if you want results that could be sustainable in practice.

3. **Commission & slippage**

- Commission: around 0.1% if that matches your broker.

- Slippage: a few ticks (e.g. 3) to account for real fills.

4. **Timeframe & markets**

- Volatile symbols (e.g. crypto like BTCUSDT, or major indices).

- Timeframes: 1H / 4H / **1D (Daily)** are typical starting points.

- I strongly recommend trying the strategy on **different timeframes**, for example 1D, to see how the behaviour changes between intraday and higher timeframes.

5. **No “caution warning”**

- Make sure your chosen symbol + timeframe + settings do not trigger TradingView’s caution messages.

- If you see warnings (e.g. “too few trades”), adjust timeframe/symbol or the backtest period.

────────────────────────

5a. About low trade count and rare signals

────────────────────────

This strategy is intentionally designed to trade RARELY:

• It is **long-only**.

• It uses strict filters (Range Oscillator threshold + Stochastic confirmation + optional EMA Exit Filter).

• On higher timeframes (especially **1D / Daily**) this can result in a **low total number of trades**, sometimes WELL BELOW 100 trades over the whole backtest.

TradingView’s House Rules mention 100+ trades as a guideline for more robust statistics. In this specific case:

• The **low trade count is a conscious design choice**, not an attempt to cherry-pick a tiny, ultra-profitable window.

• The goal is to study a **small number of high-conviction long entries** on higher timeframes, not to generate frequent intraday signals.

• Because of the low trade count, results should NOT be interpreted as statistically strong or “proven” – they are only one sample of how this logic would have behaved on past data.

Please keep this in mind when you look at the equity curve and performance metrics. A beautiful curve with only a handful of trades is still just a small sample.

────────────────────────

6. How to use this strategy (step-by-step)

────────────────────────

1. Add the script to your chart.

2. Open the **Inputs** tab:

- Set the backtest start year.

- Decide whether to use Oscillator-based entry/exit, Stochastic confirmation, and EMA Exit Filter.

- Optionally enable SL, TP, and Risk/Reward exits.

3. Open the **Properties** tab:

- Set a realistic account size if you want.

- Set order size to a realistic % of equity (e.g. 1–2%).

- Confirm that commission and slippage are realistic for your broker.

4. Run the backtest:

- Look at Net Profit, Max Drawdown, number of trades, and equity curve.

- Remember that a low trade count means the statistics are not very strong.

5. Experiment:

- Tweak thresholds (`entryLevel`, `exitLevel`), Stochastic settings, EMA length, and risk params.

- See how the metrics and trade frequency change.

6. Forward-test:

- Before using any idea in live trading, forward-test on a demo account and observe behaviour in real time.

────────────────────────

7. Originality and usefulness (why this is more than a mashup)

────────────────────────

This script is not intended to be a random visual mashup of indicators. It is designed as a coherent, testable strategy with clear roles for each component:

• Range Oscillator:

- Handles mean vs. range-expansion states via an adaptive, ATR-normalized metric.

• Stochastic:

- Acts as a timing filter to avoid entering purely on extremes and instead waits for momentum to turn.

• EMA Exit Filter:

- Trend-slope-based safety net to exit when the medium-term direction changes against the position.

• Risk module:

- Provides practical, rule-based exits: SL, TP, and R-multiple exit, which are useful for structuring risk even if you modify the core logic.

It aims to give traders a ready-made **framework to study and modify**, not a black box or “signals” product.

────────────────────────

8. Limitations and good practices

────────────────────────

• No single strategy works on all markets or in all regimes.

• This script is long-only; it does not short the market.

• Performance can degrade when market structure changes.

• Overfitting (curve fitting) is a real risk if you endlessly tweak parameters to maximise historical profit.

Good practices:

- Test on multiple symbols and timeframes.

- Focus on stability and drawdown, not only on how high the profit line goes.

- View this as a learning tool and a basis for your own research.

────────────────────────

9. Licensing and credits

────────────────────────

• Core oscillator idea & base code:

- “Range Oscillator (Zeiierman)”

- © Zeiierman, licensed under CC BY-NC-SA 4.0.

• Strategy logic, Stochastic confirmation, EMA Exit Filter, and risk-management layer:

- Modifications by jokiniemi.

Please respect both the original license and TradingView House Rules if you fork or republish any part of this script.

────────────────────────

10. No payments / no vendor pitch

────────────────────────

• This script is completely FREE to use on TradingView.

• There is no paid subscription, no external payment link, and no private signals group attached to it.

• If you have questions, please use TradingView’s comment system or private messages instead of expecting financial advice.

Use this script as a tool to learn, experiment, and build your own understanding of markets.

────────────────────────

11. Example backtest settings used in screenshots

────────────────────────

To avoid any confusion about how the results shown in screenshots were produced, here is one concrete example configuration:

• Symbol: BTCUSDT (or similar major BTC pair)

• Timeframe: 1D (Daily)

• Backtest period: from 2018 to the most recent data

• Initial capital: 10 000

• Order size type: Percent of equity

• Order size: 2% per trade

• Commission: 0.1%

• Slippage: 3 ticks

• Risk settings: Stop Loss and Take Profit disabled by default, Risk/Reward exit disabled by default

• Filters: Range Oscillator entry/exit enabled, Stochastic confirmation enabled, EMA Exit Filter enabled

If you change any of these settings (symbol, timeframe, risk per trade, commission, slippage, filters, etc.), your results will look different. Please always adapt the configuration to your own risk tolerance, market, and trading style.

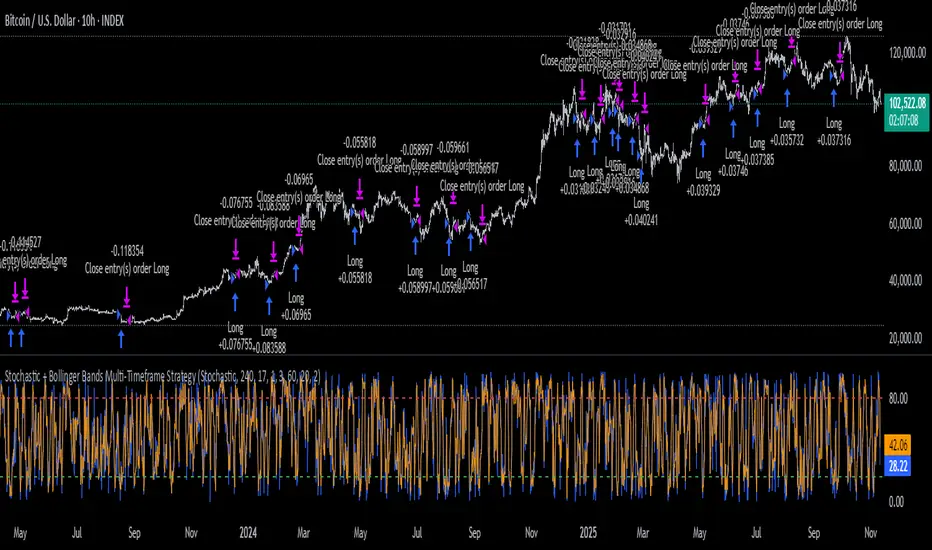

Stochastic + Bollinger Bands Multi-Timeframe StrategyThis strategy fuses the Stochastic Oscillator from the 4-hour timeframe with Bollinger Bands from the 1-hour timeframe, operating on a 10-hour chart to capture a unique volatility rhythm and temporal alignment discovered through observational alpha.

By blending momentum confirmation from the higher timeframe with short-term volatility extremes, the strategy leverages what some traders refer to as “rotating volatility” — a phenomenon where multi-timeframe oscillations sync to reveal hidden trade opportunities.

🧠 Strategy Logic

✅ Long Entry Condition:

Stochastic on the 4H timeframe:

%K crosses above %D

Both %K and %D are below 20 (oversold zone)

Bollinger Bands on the 1H timeframe:

Price crosses above the lower Bollinger Band, indicating a potential reversal

→ A long trade is opened when both momentum recovery and volatility reversion align.

✅ Long Exit Condition:

Stochastic on the 4H:

%K crosses below %D

Both %K and %D are above 80 (overbought zone)

Bollinger Bands on the 1H:

Price reaches or exceeds the upper Bollinger Band, suggesting exhaustion

→ The long trade is closed when either signal suggests a potential reversal or overextension.

🧬 Temporal Structure & Alpha

This strategy is deployed on a 10-hour chart — a non-standard timeframe that may align more effectively with multi-timeframe mean reversion dynamics.

This subtle adjustment exploits what some traders identify as “temporal drift” — the desynchronization of volatility across timeframes that creates hidden rhythm in price action.

→ For example, Stochastic on 4H (lookback 17) and Bollinger Bands on 1H (lookback 20) may periodically sync around 10H intervals, offering unique alpha windows.

📊 Indicator Components

🔹 Stochastic Oscillator (4H, Length 17)

Detects momentum reversals using %K and %D crossovers

Helps define overbought/oversold zones from a mid-term view

🔹 Bollinger Bands (1H, Length 20, ±2 StdDev)

Measures price volatility using standard deviation around a moving average

Entry occurs near lower band (support), exits near upper band (resistance)

🔹 Multi-Timeframe Logic

Uses request.security() to safely reference 4H and 1H indicators from a 10H chart

Avoids repainting by using closed higher-timeframe candles only

📈 Visualization

A plot selector input allows toggling between:

Stochastic Plot (%K & %D, with overbought/oversold levels)

Bollinger Bands Plot (Upper, Basis, Lower from 1H data)

This helps users visually confirm entry/exit triggers in real time.

🛠 Customization

Fully configurable Stochastic and BB settings

Timeframes are independently adjustable

Strategy settings like position sizing, slippage, and commission are editable

⚠️ Disclaimer

This strategy is intended for educational and informational purposes only.

It does not constitute financial advice or a recommendation to buy or sell any asset.

Market conditions vary, and past performance does not guarantee future results.

Always test any trading strategy in a simulated environment and consult a licensed financial advisor before making real-world investment decisions.