Cointegration Heatmap & Spread Table [EdgeTerminal]The Cointegration Heatmap is a powerful visual and quantitative tool designed to uncover deep, statistically meaningful relationships between assets.

Unlike traditional indicators that react to price movement, this tool analyzes the underlying statistical relationship between two time series and tracks when they diverge from their long-term equilibrium — offering actionable signals for mean-reversion trades .

What Is Cointegration?

Most traders are familiar with correlation, which measures how two assets move together in the short term. But correlation is shallow — it doesn’t imply a stable or predictable relationship over time.

Cointegration, however, is a deeper statistical concept: Two assets are cointegrated if a linear combination of their prices or returns is stationary , even if the individual series themselves are non-stationary.

Cointegration is a foundational concept in time series analysis, widely used by hedge funds, proprietary trading firms, and quantitative researchers. This indicator brings that institutional-grade concept into an easy-to-use and fully visual TradingView indicator.

This tool helps answer key questions like:

“Which stocks tend to move in sync over the long term?”

“When are two assets diverging beyond statistical norms?”

“Is now the right time to short one and long the other?”

Using a combination of regression analysis, residual modeling, and Z-score evaluation, this indicator surfaces opportunities where price relationships are stretched and likely to snap back — making it ideal for building low-risk, high-probability trade setups.

In simple terms:

Cointegrated assets drift apart temporarily, but always come back together over time. This behavior is the foundation of successful pairs trading.

How the Indicator Works

Cointegration Heatmap indicator works across any market supported on TradingView — from stocks and ETFs to cryptocurrencies and forex pairs.

You enter your list of symbols, choose a timeframe, and the indicator updates every bar with live cointegration scores, spread signals, and trade-ready insights.

Indicator Settings:

Symbol list: a customizable list of symbols separated by commas

Returns timeframe: time frame selection for return sampling (Weekly or Monthly)

Max periods: max periods to limit the data to a certain time and to control indicator performance

This indicator accomplishes three major goals in one streamlined package:

Identifies stable long-term relationships (cointegration) between assets, using a heatmap visualization.

Tracks the spread — the difference between actual prices and the predicted linear relationship — between each pair.

Generates trade signals based on Z-score deviations from the mean spread, helping traders know when a pair is statistically overextended and likely to mean revert.

The math:

Returns are calculated using spread tickers to ensure alignment in time and adjust for dividends, splits, and other inconsistencies.

For each unique pair of symbols, we perform a linear regression

Yt=α+βXt+ε

Then we compute the residuals (errors from the regression):

Spreadt=Yt−(α+βXt)

Calculate the standard deviation of the spread over a moving window (default: 100 samples) and finally, define the Cointegration Score:

S=1/Standard Deviation of Residuals

This means, the lower the deviation, the tighter the relationship, so higher scores indicate stronger cointegration.

Always remember that cointegration can break down so monitor the asset over time and over multiple different timeframes before making a decision.

How to use the indicator

The heatmap table:

The indicator displays 2 very important tables, one in the middle and one on the right side. After entering your symbols, the first table to pay attention to is the middle heatmap table.

Any assets with a cointegration value of 25% is something to pay attention to and have a strong and stable relationship. Anything below is weak and not tradable.

Additionally, the 40% level is another important line to cross. Assets that have a cointegration score of over 40% will most likely have an extremely strong relationship.

Think about it this way, the higher the percentage, the tighter and more statistically reliable the relationship is.

The spread table:

After finding a good asset pair using heatmap, locate the same pair in the spread table (right side).

Here’s what you’ll see on the table:

Spread: Current difference between the two symbols based on the regression fit

Mean: Historical average of that spread

Z-score: How far current spread is from the mean in standard deviations

Signal: Trade suggestion: Short, Long, or Neutral

Since you’re expecting mean reversion, the idea is that the spread will return to the average. You want to take a trade when the z-score is either over +2 or below -2 and exit when z-score returns to near 0.

You will usually see the trade suggestion on the spread chart but you can make your own decision based on your risk level.

Keep in mind that the Z-score for each pair refers to how off the first asset is from the mean compared to the second one, so for example if you see STOCKA vs STOCKB with a Z-score of -1.55, we are regressing STOCKB (Y) on STOCKA (X).

In this case, STOCKB is the quoted asset and STOCKA is the base asset.

In this case, this means that STOCKB is much lower than expected relative to STOCKA, so the trade would be a long position on stock B and short position on stock A.

Regressions

Index Futures vs Cash ArbitrageThis indicator measures the statistical spread between major stock index futures and their corresponding cash indices (e.g., ES vs SPX, NQ vs NDX) using Z-score normalization. It automatically detects commonly traded index pairs (S&P 500, Nasdaq, Dow Jones, Russell 2000) and calculates a smoothed spread between futures and spot prices. A Z-score is then derived from this spread to highlight potential overpricing or underpricing conditions.

Traders can use customizable thresholds to identify mean-reversion opportunities where the futures contract may be temporarily overvalued or undervalued relative to the index. The histogram highlights the direction of the Z-score (green = futures > index, red = futures < index), while built-in alerts notify users of key threshold breaches or zero-line crosses.

This tool is designed for discretionary traders, pairs traders, or anyone exploring statistical arbitrage strategies between futures and spot markets. It is not a buy/sell signal by itself and should be used with additional confluence or risk management techniques.

PolyBand Convergence System (PBCS)PolyBand Convergence System (PBCS)

The PolyBand Convergence System (PBCS) is an advanced technical analysis indicator that combines multiple polynomial regressions with statistical bands to identify trend strength and potential reversal zones.

Key Features

Multi-Degree Polynomial Analysis: Combines 1st, 2nd, 3rd, and 4th degree polynomial regressions into a composite regression line

Adaptive Statistical Bands: Uses percentile-based bands enhanced with standard deviation multipliers

Asymmetric Volatility Measurement: Separately calculates upside and downside volatility for more accurate band placement

Smart Trend Detection: Identifies bullish, bearish, or neutral market conditions based on price position relative to bands

How It Works

PBCS creates a composite regression line from multiple polynomial fits to better capture the underlying price structure. This line is then surrounded by adaptive bands that represent statistical thresholds for price movement. When price breaks above the upper band, a bullish trend is signaled; when it breaks below the lower band, a bearish trend is indicated.

Customization Options

Regression Settings: Adjust source data, lookback period, and smoothing parameters

Percentile Controls: Fine-tune the statistical thresholds for upper and lower bands

Volatility Sensitivity: Modify standard deviation multipliers to control band width

Visual Preferences: Choose from multiple color schemes to match your trading platform

Disclaimer

This indicator is provided for educational and informational purposes only and does not constitute investment advice. Trading involves risk and may result in financial loss. Always perform your own research and consult with a qualified financial advisor before making any trading decisions.

Kernel Regression Bands SuiteMulti-Kernel Regression Bands

A versatile indicator that applies kernel regression smoothing to price data, then dynamically calculates upper and lower bands using a wide variety of deviation methods. This tool is designed to help traders identify trend direction, volatility, and potential reversal zones with customizable visual styles.

Key Features

Multiple Kernel Types: Choose from 17+ kernel regression styles (Gaussian, Laplace, Epanechnikov, etc.) for smoothing.

Flexible Band Calculation: Select from 12+ deviation types including Standard Deviation, Mean/Median Absolute Deviation, Exponential, True Range, Hull, Parabolic SAR, Quantile, and more.

Adaptive Bands: Bands are calculated around the kernel regression line, with a user-defined multiplier.

Signal Logic: Trend state is determined by crossovers/crossunders of price and bands, coloring the regression line and band fills accordingly.

Custom Color Modes: Six unique color palettes for visual clarity and personal preference.

Highly Customizable Inputs: Adjust kernel type, lookback, deviation method, band source, and more.

How to Use

Trend Identification: The regression line changes color based on the detected trend (up/down)

Volatility Zones: Bands expand/contract with volatility, helping spot breakouts or mean-reversion opportunities.

Visual Styling: Use color modes to match your chart theme or highlight specific market states.

Credits:

Kernel regression logic adapted from:

ChartPrime | Multi-Kernel-Regression-ChartPrime (Link in the script)

Disclaimer

This script is for educational and informational purposes only. Not financial advice. Use at your own risk.

Open-Close / High-Low RibbonThis indicator visualizes smoothed Open, Close, High, and Low price levels as continuous lines, helping users observe underlying price structure with reduced noise. The Open and Close values are shaded to highlight bullish (green) or bearish (red) zones based on their relationship. Smoothing is applied using a simple moving average (SMA) over a user-defined length to make trends easier to interpret. This tool can be useful for identifying directional bias, trend shifts, or areas of support and resistance on any timeframe.

Linear Regression Volume | Lyro RSLinear Regression Volume | Lyro RS

⚠️Disclaimer⚠️

Always combine this indicator with other forms of analysis and risk management. Please do your own research before making any trading decisions.

The LR Volume | 𝓛𝔂𝓻𝓸 𝓡𝓢 indicator blends linear regression with volume-adjusted moving average s to dynamically outline price equilibrium and trend intensity. By integrating volume into its regression model, it highlights meaningful price movement relative to trading activity.

📌 How It Works:

Volume-Weighted Regression Baseline

Price is filtered through one of four volume-adjusted moving averages (SMA, RMA, HMA, ALMA) before being passed through a linear regression model, forming a dynamic fair value line.

Deviation Bands

The indicator plots 1x, 2x, and 3x standard deviation zones above and below the baseline, helping identify potential extremes, volatility spikes, and mean reversion areas.

Slope-Based Color Logic

The baseline and fill areas are dynamically colored:

- 🟢 Green for positive slope (uptrend)

- 🔴 Red for negative slope (downtrend)

- ⚪ Gray for neutral movement

⚙️ Inputs & Options:

Regression Length – Controls how many bars are used in the moving average and regression calculation.

Deviation Multiplier – Adjusts the width of the bands surrounding the regression baseline.

MA Type – Choose from 4 types:

SMA (Simple Moving Average)

RMA (Relative Moving Average)

HMA (Hull Moving Average)

ALMA (Arnaud Legoux Moving Average)

Band Colors – Customizable upper/lower band colors to match your visual style.

🔔 Alerts:

Long Signal – Triggers when the regression slope turns positive.

Short Signal – Triggers when the regression slope turns negative.

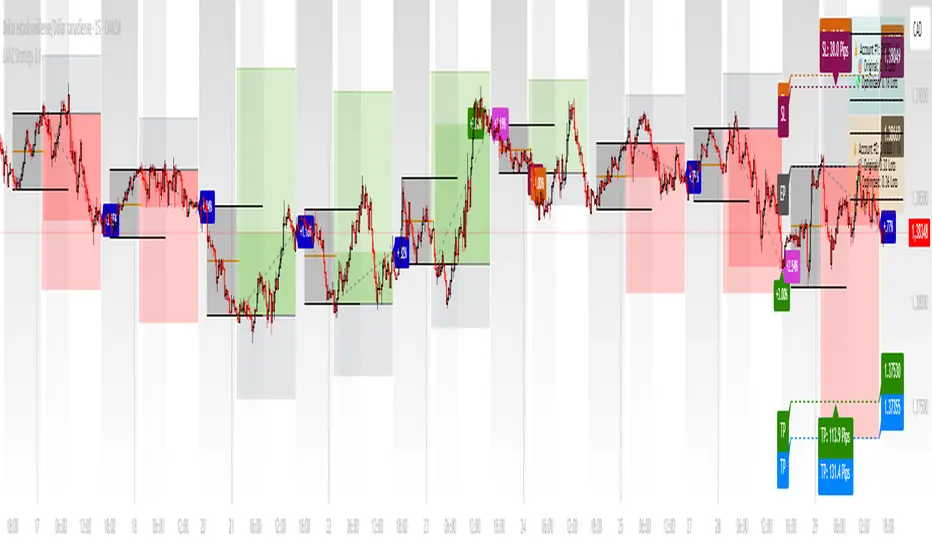

LANZ Strategy 3.0🔷 LANZ Strategy 3.0 — Asian Range Fibonacci Strategy with Execution Window Logic

LANZ Strategy 3.0 is a rule-based trading system that utilizes the Asian session range to project Fibonacci levels and manage entries during a defined execution window. Designed for Forex and index traders, this strategy focuses on structured price behavior around key levels before the New York session.

🧠 Core Components:

Asian Session Range Mapping: Automatically detects the high, low, and midpoint during the Asian session.

Fibonacci Level Projection: Projects configurable Fibonacci retracement and extension levels based on the Asian range.

Execution Window Logic: Uses the 01:15 NY candle as a reference to validate potential reversals or continuation setups.

Conditional Entry System: Includes logic for limit order entries (buy or sell) at specific Fib levels, with reversal logic if price breaks structure before execution.

Risk Management: Entry orders are paired with dynamic SL and TP based on Fibonacci-based distances, maintaining a risk-reward ratio consistent with intraday strategies.

📊 Visual Features:

Asian session high/low/mid lines.

Fibonacci levels: Original (based on raw range) and Optimized (user-adjustable).

Session background coloring for Asia, Execution Window, and NY session.

Labels and lines for entry, SL, and TP targets.

Dynamic deletion of untriggered orders after execution window expires.

⚙️ How It Works:

The script calculates the Asian session range.

Projects Fibonacci levels from the range.

Waits for the 01:15 NY candle to close to validate a signal.

If valid, a limit entry order (BUY or SELL) is plotted at the selected level.

If price structure changes (e.g., breaks the high/low), reversal logic may activate.

If no trade is triggered, orders are cleared before the NY session.

🔔 Alerts:

Alerts trigger when a valid setup appears after 01:15 NY candle.

Optional alerts for order activation, SL/TP hit, or trade cancellation.

📝 Notes:

Intended for semi-automated or discretionary trading.

Best used on highly liquid markets like Forex majors or indices.

Script parameters include session times, Fib ratios, SL/TP settings, and reversal logic toggle.

Credits:

Developed by LANZ, this script merges traditional session-based analysis with Fibonacci tools and structured execution timing, offering a unique framework for morning volatility plays.

Machine Learning: ARIMA + SARIMADescription

The ARIMA (Autoregressive Integrated Moving Average) and SARIMA (Seasonal ARIMA) are advanced statistical models that use machine learning to forecast future price movements. It uses autoregression to find the relationship between observed data and its lagged observations. The data is differenced to make it more predictable. The MA component creates a dependency between observations and residual errors. The parameters are automatically adjusted to market conditions.

Differences

ARIMA - This excels at identifying trends in the form of directions

SARIMA - Incorporates seasonality. It's better at capturing patterns previously seen

How To Use

1. Model: Determine if you want to use ARIMA (better for direction) or SARIMA (better for overall prediction). You can click on the 'Show Historic Prediction' to see the direction of the previous candles. Green = forecast ending up, red = forecast ending down

2. Metrics: The RMSE% and MAPE are 10 day moving averages of the first 10 predictions made at candle close. They're error metrics that compare the observed data with the predicted data. It is better to use them when they're below 8%. Higher timeframes will be higher, as these models are partly mean-reverting and higher TFs tend to trend more. Better to compare RMSE% and MAPE with similar timeframes. They naturally lag as data is being collected

3. Parameter selection: The simpler, the better. Both are used for ARIMA(1,1,1) and SARIMA(1,1,1)(1,1,1)5. Increasing may cause overfitting

4. Training period: Keep at 50. Because of limitations in pine, higher values do not make for more powerful forecasts. They will only criminally lag. So best to keep between 20 and 80

BTC vs ALT Lag Detector [MEXC Overlay]This indicator monitors the price movement of Bitcoin (BTC) and compares it in real time to a customizable list of major altcoins on the MEXC exchange.

It helps you identify lagging altcoins — tokens that are underperforming or overperforming BTC’s price action over a selected timeframe. These temporary deviations can offer profitable entry or rotation opportunities, especially for scalpers, day traders, and arbitrage-style strategies.

Key Features:

- Real-time deviation detection between BTC and altcoins

- Customizable comparison timeframe: 1m, 6m, 12m, 30m, 1h, 4h, or 1d

- Deviation threshold alert: Highlights coins that lag BTC by more than 0.5%, 1%, 2%, or 3%

- Compact stats table embedded in the price chart

- Fully adjustable layout: Table position (Top/Bottom/Center + Left/Right), Font size (Tiny, Small, Medium)

- Built-in alert system when deviation exceeds your chosen threshold

How to Use It:

Set your desired timeframe for comparison (e.g., 1 hour).

Select a deviation threshold (e.g., 1.0%).

The table will show:

Each altcoin’s % change

BTC’s % change

The delta (deviation) vs BTC

Red highlights indicate alts whose deviation exceeded the threshold.

When at least one alt lags beyond your threshold, the indicator can trigger an alert — helping you capitalize on potential catch-up trades.

Please provide any feedback on it.

Market Manipulation Index (MMI)The Composite Manipulation Index (CMI) is a structural integrity tool that quantifies how chaotic or orderly current market conditions are, with the aim of detecting potentially manipulated or unstable environments. It blends two distinct mathematical models that assess price behavior in terms of both structural rhythm and predictability.

1. Sine-Fit Deviation Model:

This component assumes that ideal, low-manipulation price behavior resembles a smooth oscillation, such as a sine wave. It generates a synthetic sine wave using a user-defined period and compares it to actual price movement over an adaptive window. The error between the real price and this synthetic wave—normalized by price variance—forms the Sine-Based Manipulation Index. A high error indicates deviation from natural rhythm, suggesting structural disorder.

2. Predictability-Based Model:

The second component estimates how well current price can be predicted using recent price lags. A two-variable rolling linear regression is computed between the current price and two lagged inputs (close and close ). If the predicted price diverges from the actual price, this error—also normalized by price variance—reflects unpredictability. High prediction error implies a more manipulated or erratic environment.

3. Adaptive Mechanism:

Both components are calculated using an adaptive smoothing window based on the Average True Range (ATR). This allows the indicator to respond proportionally to market volatility. During high volatility, the analysis window expands to avoid over-sensitivity; during calm periods, it contracts for better responsiveness.

4. Composite Output:

The two normalized metrics are averaged to form the final CMI value, which is then optionally smoothed further. The output is scaled between 0 and 1:

0 indicates a highly structured, orderly market.

1 indicates complete structural breakdown or randomness.

Suggested Interpretation:

CMI < 0.3: Market is clean and structured. Trend-following or breakout strategies may perform better.

CMI > 0.7: Market is structurally unstable. Choppy price action, fakeouts, or manipulative behavior may dominate.

CMI 0.3–0.7: Transitional zone. Caution or reduced risk may be warranted.

This indicator is designed to serve as a contextual filter, helping traders assess whether current market conditions are conducive to structured strategies, or if discretion and defense are more appropriate.

Liquidity Trap Reversal Pro (Radar v2)Liquidity Trap Reversal Pro (Radar v2) is a non-repainting indicator designed to detect hidden liquidity traps at key swing highs and lows. It combines wick analysis, volume spike detection, and optional trend and exhaustion filters to identify high-probability reversal setups.

🔷 Features:

Non-Repainting: Pivots confirmed after lookback period, no future leaking.

Volume Spike Detection: Filters traps that occur during major liquidity events.

EMA Trend Filter (Optional): Focus on traps aligned with the prevailing trend.

Higher Timeframe Trend Filter (Optional): Confirm traps using a higher timeframe EMA bias.

Exhaustion Guard (Optional): Prevents traps after overextended moves based on ATR stretch.

Clean Visuals: Distinct plots for raw trap points vs confirmed traps.

Alerts Included: Set alerts for confirmed high/low liquidity traps.

📚 How to Use:

Watch for Trap Signals:

A Trap High signal suggests a potential bearish reversal.

A Trap Low signal suggests a potential bullish reversal.

Use Confirmed Signals for Best Entries:

Confirmed traps fire only after price moves opposite to the trap direction, adding reliability.

Use Trend Filters to Improve Accuracy:

In an uptrend (price above EMA), prefer Trap Lows (buy setups).

In a downtrend (price below EMA), prefer Trap Highs (sell setups).

Use the Exhaustion Guard to Avoid Bad Trades:

This filter blocks signals when price has moved too far from trend, helping avoid late entries.

Recommended Settings:

Best used on 15-minute, 1-hour, or 4-hour charts.

Trend filter ON for trending markets.

Exhaustion guard ON for volatile or stretched markets.

📈 Important Notes:

This script does not repaint once a pivot is confirmed.

Alerts trigger only on confirmed trap signals.

Always combine signals with sound risk management and trading strategy.

Disclaimer:

This script is for educational purposes only. It is not investment advice or a guarantee of results. Always do your own research before trading.

Auto Trend Channel + Buy/Sell AlertsThis indicator automatically detects trend channels using a linear regression line, and dynamically plots upper and lower channel boundaries based on standard deviation. It helps traders identify potential Buy and Sell zones with clear visual signals and customizable alerts.

💡 How It Works:

🧠 Regression-Based Channel: Calculates the central trend line using ta.linreg() over a user-defined length.

📏 Dynamic Boundaries: Upper and lower channel lines are offset by a multiplier of the standard deviation for precision volatility tracking.

✅ Buy Signals: Triggered when price crosses above the lower boundary — potential bounce entry.

❌ Sell Signals: Triggered when price crosses below the upper boundary — potential reversal exit.

🔔 Alerts Enabled: Get real-time alerts when price touches the channel lines.

Pullback SARPullback SAR - Parabolic SAR with Pullback Detection

Description: The "Pullback SAR" is an advanced indicator built on the classic Parabolic SAR but with additional functionality for detecting pullbacks. It helps identify moments when the price pulls back from the main trend, offering potential entry signals. Perfect for traders looking to enter the market after a correction.

Key Features:

SAR (Parabolic SAR): The Parabolic SAR indicator is used to determine potential trend reversal points. It marks levels where the price could reverse its direction.

Pullback Detection: The indicator catches periods when the price moves away from the main trend and then returns, which may suggest a re-entry opportunity.

Long and Short Signals: Once a pullback in the direction of the main trend is identified, the indicator generates signals that could be used to open positions.

Simple and Clear Construction: The indicator is based on the classic SAR, with added pullback detection logic to enhance the accuracy of the signals.

Parameters:

Start (SAR Step): Determines the initial step for the SAR calculation, which controls the rate of change in the indicator at the beginning.

Increment (SAR Increment): Defines the maximum step size for SAR, allowing traders to adjust the indicator’s sensitivity to market volatility.

Max Value (SAR Max): Sets the upper limit for the SAR value, controlling its volatility.

Usage:

Swing Trading: Ideal for swing strategies, aiming to capture larger price moves while maintaining a safe margin.

Scalping: Due to its precise pullback detection, it can also be used in scalping, especially when the price quickly returns to the main trend.

Risk Management: The combination of SAR and pullback detection allows traders to adjust their positions according to changing market conditions.

Special Notes:

Adjusting Parameters: Depending on the market and trading style, users can adjust the SAR parameters (Start, Increment, Max Value) to fit their needs.

Combination with Other Indicators: It's recommended to use the indicator alongside other technical analysis tools (e.g., EMA, RSI) to enhance the accuracy of the signals.

Link to the script: This open-source version of the indicator is available on TradingView, enabling full customization and adjustments to meet your personal trading strategy. Share your experiences and suggestions!

ML Deep Regression Pro (TechnoBlooms)ML Deep Regression Pro is a machine-learning-inspired trading indicator that integrates Polynomial Regression, Linear Regression and Statistical Deviation models to provide a powerful, data-driven approach to market trend analysis.

Designed for traders, quantitative analysts and developers, this tool transforms raw market data into predictive trend insights, allowing for better decision-making and trend validation.

By leveraging statistical regression techniques, ML Deep Regression Pro eliminates market noise and identifies key trend shifts, making it a valuable addition to both manual and algorithmic trading strategies.

REGRESSION ANALYSIS

Regression is a statistical modeling technique used in machine learning and data science to identify patterns and relationships between variables. In trading, it helps detect price trends, reversals and volatility changes by fitting price data into a predictive model.

1. Linear Regression -

The most widely used regression model in trading, providing a best-fit plotted line to track price trends.

2. Polynomial Regression -

A more advanced form of regression that fits curved price structures, capturing complex market cycles and improving trend forecasting accuracy.

3. Standard Deviation Bands -

Based on regression calculations, these bands measure price dispersion and identify overbought/ oversold conditions, similar to Bollinger Bands. By default, these lines are hidden and user can make it visible through Settings.

KEY FEATURES :-

✅ Hybrid Regression Engine – Combines Linear and Polynomial Regression to detect market trends with greater accuracy.

✅ Dynamic Trend Bias Analysis – Identifies bullish & bearish market conditions using real-time regression models.

✅ Standard Deviation Bands – Measures price volatility and potential reversals with an advanced deviation model.

✅ Adaptive EMA Crossover Signals – Generates buy/sell signals when price momentum shifts relative to the regression trend.

Adaptive Trend FinderAdaptive Trend Finder - The Ultimate Trend Detection Tool

Introducing Adaptive Trend Finder, the next evolution of trend analysis on TradingView. This powerful indicator is an enhanced and refined version of Adaptive Trend Finder (Log), designed to offer even greater flexibility, accuracy, and ease of use.

What’s New?

Unlike the previous version, Adaptive Trend Finder allows users to fully configure and adjust settings directly within the indicator menu, eliminating the need to modify chart settings manually. A major improvement is that users no longer need to adjust the chart's logarithmic scale manually in the chart settings; this can now be done directly within the indicator options, ensuring a smoother and more efficient experience. This makes it easier to switch between linear and logarithmic scaling without disrupting the analysis. This provides a seamless user experience where traders can instantly adapt the indicator to their needs without extra steps.

One of the most significant improvements is the complete code overhaul, which now enables simultaneous visualization of both long-term and short-term trend channels without needing to add the indicator twice. This not only improves workflow efficiency but also enhances chart readability by allowing traders to monitor multiple trend perspectives at once.

The interface has been entirely redesigned for a more intuitive user experience. Menus are now clearer, better structured, and offer more customization options, making it easier than ever to fine-tune the indicator to fit any trading strategy.

Key Features & Benefits

Automatic Trend Period Selection: The indicator dynamically identifies and applies the strongest trend period, ensuring optimal trend detection with no manual adjustments required. By analyzing historical price correlations, it selects the most statistically relevant trend duration automatically.

Dual Channel Display: Traders can view both long-term and short-term trend channels simultaneously, offering a broader perspective of market movements. This feature eliminates the need to apply the indicator twice, reducing screen clutter and improving efficiency.

Fully Adjustable Settings: Users can customize trend detection parameters directly within the indicator settings. No more switching chart settings – everything is accessible in one place.

Trend Strength & Confidence Metrics: The indicator calculates and displays a confidence score for each detected trend using Pearson correlation values. This helps traders gauge the reliability of a given trend before making decisions.

Midline & Channel Transparency Options: Users can fine-tune the visibility of trend channels, adjusting transparency levels to fit their personal charting style without overwhelming the price chart.

Annualized Return Calculation: For daily and weekly timeframes, the indicator provides an estimate of the trend’s performance over a year, helping traders evaluate potential long-term profitability.

Logarithmic Adjustment Support: Adaptive Trend Finder is compatible with both logarithmic and linear charts. Traders who analyze assets like cryptocurrencies, where log scaling is common, can enable this feature to refine trend calculations.

Intuitive & User-Friendly Interface: The updated menu structure is designed for ease of use, allowing quick and efficient modifications to settings, reducing the learning curve for new users.

Why is this the Best Trend Indicator?

Adaptive Trend Finder stands out as one of the most advanced trend analysis tools available on TradingView. Unlike conventional trend indicators, which rely on fixed parameters or lagging signals, Adaptive Trend Finder dynamically adjusts its settings based on real-time market conditions. By combining automatic trend detection, dual-channel visualization, real-time performance metrics, and an intuitive user interface, this indicator offers an unparalleled edge in trend identification and trading decision-making.

Traders no longer have to rely on guesswork or manually tweak settings to identify trends. Adaptive Trend Finder does the heavy lifting, ensuring that users are always working with the strongest and most reliable trends. The ability to simultaneously display both short-term and long-term trends allows for a more comprehensive market overview, making it ideal for scalpers, swing traders, and long-term investors alike.

With its state-of-the-art algorithms, fully customizable interface, and professional-grade accuracy, Adaptive Trend Finder is undoubtedly one of the most powerful trend indicators available.

Try it today and experience the future of trend analysis.

This indicator is a technical analysis tool designed to assist traders in identifying trends. It does not guarantee future performance or profitability. Users should conduct their own research and apply proper risk management before making trading decisions.

// Created by Julien Eche - @Julien_Eche

CAPM Alpha & BetaThe CAPM Alpha & Beta indicator is a crucial tool in finance and investment analysis derived from the Capital Asset Pricing Model (CAPM) . It provides insights into an asset's risk-adjusted performance (Alpha) and its relationship to broader market movements (Beta). Here’s a breakdown:

1. How Does It Work?

Alpha:

Definition: Alpha measures the portion of an investment's return that is not explained by market movements, i.e., the excess return over and above what the market is expected to deliver.

Purpose: It represents the value a fund manager or strategy adds (or subtracts) from an investment’s performance, adjusting for market risk.

Calculation:

Alpha is derived from comparing actual returns to expected returns predicted by CAPM:

Alpha = Actual Return − (Risk-Free Rate + β × (Market Return − Risk-Free Rate))

Alpha = Actual Return − (Risk-Free Rate + β × (Market Return − Risk-Free Rate))

Interpretation:

Positive Alpha: The investment outperformed its CAPM prediction (good performance for additional value/risk).

Negative Alpha: The investment underperformed its CAPM prediction.

Beta:

Definition: Beta measures the sensitivity of an asset's returns relative to the overall market's returns. It quantifies systematic risk.

Purpose: Indicates how volatile or correlated an investment is relative to the market benchmark (e.g., S&P 500).

Calculation:

Beta is computed as the ratio of the covariance of the asset and market returns to the variance of the market returns:

β = Covariance (Asset Return, Market Return) / Variance (Market Return)

β = Variance (Market Return) Covariance (Asset Return, Market Return)

Interpretation:

Beta = 1: The asset’s price moves in line with the market.

Beta > 1: The asset is more volatile than the market (higher risk/higher potential reward).

Beta < 1: The asset is less volatile than the market (lower risk/lower reward).

Beta < 0: The asset moves inversely to the market.

2. How to Use It?

Using Alpha:

Portfolio Evaluation: Investors use Alpha to gauge whether a portfolio manager or a strategy has successfully outperformed the market on a risk-adjusted basis.

If Alpha is consistently positive, the portfolio may deliver higher-than-expected returns for the given level of risk.

Stock/Asset Selection: Compare Alpha across multiple securities. Positive Alpha signals that the asset may be a good addition to your portfolio for excess returns.

Adjusting Investment Strategy: If Alpha is negative, reassess the asset's role in the portfolio and refine strategies.

Using Beta:

Risk Management:

A high Beta (e.g., 1.5) indicates higher sensitivity to market movements. Use such assets if you want to take on more risk during bullish market phases or expect higher returns.

A low Beta (e.g., 0.7) indicates stability and is useful in diversifying risk in volatile or bearish markets.

Portfolio Diversification: Combine assets with varying Betas to achieve the desired level of market responsiveness and smooth out portfolio volatility.

Monitoring Systematic Risk: Beta helps identify whether an investment aligns with your risk tolerance. For example, high-Beta stocks may not be suitable for conservative investors.

Practical Application:

Use both Alpha and Beta together:

Assess performance with Alpha (excess returns).

Assess risk exposure with Beta (market sensitivity).

Example: A stock with a Beta of 1.2 and a highly positive Alpha might suggest a solid performer that is slightly more volatile than the market, making it a suitable pick for risk-tolerant, return-maximizing investors.

In conclusion, the CAPM Alpha & Beta indicator gives a comprehensive view of an asset's performance and risk. Alpha enables performance evaluation on a risk-adjusted basis, while Beta reveals the level of market risk. Together, they help investors make informed decisions, build optimal portfolios, and align investments with their risk-return preferences.

Ethereum Logarithmic Regression Bands (Fine-Tuned)This indicator, "Ethereum Logarithmic Regression Bands (Fine-Tuned)," is my attempt to create a tool for estimating long-term trends in Ethereum (ETH/USD) price action using logarithmic regression bands. Please note that I am not an expert in financial modeling or coding—I developed this as a personal project to serve as a rough estimation rather than a precise or professional trading tool. The data was fitted to non-bubble periods of Ethereum's history to provide a general trendline, but it’s far from perfect.

I’m sharing this because I couldn’t find a similar indicator available, and I thought it might be useful for others who are also exploring ETH’s long-term behavior. The bands start from Ethereum’s launch price and are adjustable via input parameters, but they are based on my best effort to align with historical data. With some decent coding experience, I’m sure someone could refine this further—perhaps by optimizing the coefficients or incorporating more advanced fitting techniques. Feel free to tweak the code, suggest improvements, or use it as a starting point for your own projects!

How to Use:

** THIS CHART IS SPECIFICALLY CODED FOR ETH/USD (KRAKEN) ON THE WEEKLY TIMEFRAME IN LOG VIEW**

The main band (blue) represents the logarithmic regression line.

The upper (red) and lower (green) bands provide a range around the main trend, adjustable with multipliers.

Adjust the "Launch Price," "Base Coefficient," "Growth Coefficient," and other inputs to experiment with different fits.

Disclaimer:

This is not financial advice. Use at your own risk, and always conduct your own research before making trading decisions.

ICT Session by LasinsName: ICT Session by Lasins

Purpose: To visually identify and differentiate between the Asian, London, and New York trading sessions on the chart.

Features:

Highlights the background of the chart during each session.

Includes a mini dashboard in the top-right corner to show the active session.

Allows customization of time zones (exchange timezone or UTC).

Displays copyright and author information.

Key Components

Inputs:

useExchangeTimezone: A boolean input to toggle between using the exchange timezone or UTC for session times.

showDashboard: A boolean input to toggle the visibility of the mini dashboard.

Session Times:

The script defines three trading sessions:

Asian Session: 2000-0000 UTC (or adjusted for exchange timezone).

London Session: 0200-0500 UTC (or adjusted for exchange timezone).

New York Session: 0700-1000 UTC (or adjusted for exchange timezone).

Session Detection:

The is_session function checks if the current time falls within a specified session using the time function.

Background Coloring:

The bgcolor function is used to highlight the chart background during each session:

Asian Session: Red background.

London Session: Green background.

New York Session: Blue background.

Mini Dashboard:

A table is created in the top-right corner of the chart to display the active session and its corresponding color.

The dashboard includes:

A header row with "Session" and "Color".

Rows for each session (Asian, London, New York) with their respective colors.

Copyright and Author Information:

A label is added to the chart to display the copyright and author information ("© ICT Session by Lasins Raj").

How It Works

The script checks the current time and compares it to the predefined session times.

If the current time falls within a session, the chart background is highlighted with the corresponding color.

The mini dashboard updates to reflect the active session.

The copyright and author information is displayed at the bottom of the chart.

Customization

You can adjust the session times in the script to match your preferred timezone or trading hours.

The useExchangeTimezone input allows you to switch between UTC and the exchange timezone.

The showDashboard input lets you toggle the visibility of the mini dashboard.

Example Use Case

Traders who follow the ICT (Inner Circle Trader) methodology can use this indicator to identify key trading sessions and plan their trades accordingly.

The visual representation of sessions helps traders quickly recognize when major markets are open and active.

TASC 2025.03 A New Solution, Removing Moving Average Lag█ OVERVIEW

This script implements a novel technique for removing lag from a moving average, as introduced by John Ehlers in the "A New Solution, Removing Moving Average Lag" article featured in the March 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers explains that the average price in a time series represents a statistical estimate for a block of price values, where the estimate is positioned at the block's center on the time axis. In the case of a simple moving average (SMA), the calculation moves the analyzed block along the time axis and computes an average after each new sample. Because the average's position is at the center of each block, the SMA inherently lags behind price changes by half the data length.

As a solution to removing moving average lag, Ehlers proposes a new projected moving average (PMA) . The PMA smooths price data while maintaining responsiveness by calculating a projection of the average using the data's linear regression slope.

The slope of linear regression on a block of financial time series data can be expressed as the covariance between prices and sample points divided by the variance of the sample points. Ehlers derives the PMA by adding this slope across half the data length to the SMA, creating a first-order prediction that substantially reduces lag:

PMA = SMA + Slope * Length / 2

In addition, the article includes methods for calculating predictions of the PMA and the slope based on second-order and fourth-order differences. The formulas for these predictions are as follows:

PredictPMA = PMA + 0.5 * (Slope - Slope ) * Length

PredictSlope = 1.5 * Slope - 0.5 * Slope

Ehlers suggests that crossings between the predictions and the original values can help traders identify timely buy and sell signals.

█ USAGE

This indicator displays the SMA, PMA, and PMA prediction for a specified series in the main chart pane, and it shows the linear regression slope and prediction in a separate pane. Analyzing the difference between the PMA and SMA can help to identify trends. The differences between PMA or slope and its corresponding prediction can indicate turning points and potential trade opportunities.

The SMA plot uses the chart's foreground color, and the PMA and slope plots are blue by default. The plots of the predictions have a green or red hue to signify direction. Additionally, the indicator fills the space between the SMA and PMA with a green or red color gradient based on their differences:

Users can customize the source series, data length, and plot colors via the inputs in the "Settings/Inputs" tab.

█ NOTES FOR Pine Script® CODERS

The article's code implementation uses a loop to calculate all necessary sums for the slope and SMA calculations. Ported into Pine, the implementation is as follows:

pma(float src, int length) =>

float PMA = 0., float SMA = 0., float Slope = 0.

float Sx = 0.0 , float Sy = 0.0

float Sxx = 0.0 , float Syy = 0.0 , float Sxy = 0.0

for count = 1 to length

float src1 = src

Sx += count

Sy += src

Sxx += count * count

Syy += src1 * src1

Sxy += count * src1

Slope := -(length * Sxy - Sx * Sy) / (length * Sxx - Sx * Sx)

SMA := Sy / length

PMA := SMA + Slope * length / 2

However, loops in Pine can be computationally expensive, and the above loop's runtime scales directly with the specified length. Fortunately, Pine's built-in functions often eliminate the need for loops. This indicator implements the following function, which simplifies the process by using the ta.linreg() and ta.sma() functions to calculate equivalent slope and SMA values efficiently:

pma(float src, int length) =>

float Slope = ta.linreg(src, length, 0) - ta.linreg(src, length, 1)

float SMA = ta.sma(src, length)

float PMA = SMA + Slope * length * 0.5

To learn more about loop elimination in Pine, refer to this section of the User Manual's Profiling and optimization page.

UM-Optimized Linear Regression ChannelDESCRIPTION

This indicator was inspired by Dr. Stoxx at drstoxx.com. Shout out to him and his services for introducing me to this idea. This indicator is a slightly different take on the standard linear regression indicator.

It uses two standard deviations to draw bands and dynamically attempts to best-fit the data lookback period using an R-squared statistical measure. The R-squared value ranges between zero and one with zero being no fit to the data at all and 1 being a 100% match of the data to linear regression line. The R-squared calculation is weighted exponentially to give more weight to the most recent data.

The label provides the number of periods identified as the optimal best-fit period, the type of loopback period determination (Manual or Auto) and the R-squared value (0-100, 100% being a perfect fit). >=90% is a great fit of the data to the regression line. <50% is a difficult fit and more or less considered random data.

The lookback mode can also be set manually and defaults to a value of 100 periods.

DEFAULTS

The defaults are 1.5 and 2.0 for standard deviation. This creates 2 bands above and below the regression line. The default mode for best-fit determination with "Auto" selected in the dropdown. When manual mode is selected, the default is 100. The modes, manual lookback periods, colors, and standard deviations are user-configurable.

HOW TO USE

Overlay this indicator on any chart of any timeframe. Look for turning points at extremes in the upper and lower bands. Look for crossovers of the centerline. Look at the Auto-determination for best fit. Compare this to your favorite Manual mode setting (Manual Mode is set to 100 by default lookback periods.)

When price is at an extreme, look for turnarounds or reversals. Use your favorite indicators, in addition to this indicator, to determine reversals. Try this indicator against your favorite securities and timeframes.

CHART EXAMPLE

The chart I used for an example is the daily chart of IWM. I illustrated the extremes with white text. This is where I consider proactively exiting an existing position and/or begin looking for a reversal.

CandelaCharts - Fib Retracement (OTE) 📝 Overview

The CandelaCharts Fib Retracement (OTE) indicator is a precision tool designed to help traders identify Optimal Trade Entry (OTE) levels based on Fibonacci retracement principles, as taught in ICT (Inner Circle Trader) methodology.

This indicator automatically plots Fibonacci retracement levels between a selected swing high and swing low, highlighting the key OTE zone between the 61.8% and 78.6% retracement levels—a prime area for potential reversals in trending markets.

📦 Features

Automatic & Custom lookback modes

Customizable fib levels

Dynamic coloring

Reverse & extend

⚙️ Settings

Lookback: Controls the number of bars to look back. You can choose between **Automatic** or **Custom** mode.

Line Style: Sets the line style for the Fibonacci levels.

Levels: 0, 0.236, 0.0.382, 0.500, 0.620, 0.705, 0.790, 0.886, 1.000. Allows you to toggle the visibility of Fibonacci levels.

Dynamic Coloring: Colors Fibonacci levels according to trend direction.

Show Labels: Shows the price value at each Fibonacci level.

Reverse: Flips the Fibonacci levels in the opposite direction.

Extend Left: Extends the Fibonacci levels to the left.

⚡️ Showcase

Dynamic Coloring

Manual Coloring

Fib Retracement

Extended

Custom Length

📒 Usage

Using the CandelaCharts Fib Retracement (OTE) is pretty straightforward—just follow these steps to spot high-probability trade setups and refine your entries.

Identify the Trend – Determine whether the market is in an uptrend or downtrend.

Select Swing Points – The indicator automatically plots from the most recent swing high to swing low (or vice versa).

Wait for Price to Enter OTE Zone – Look for price action confirmation within the optimal entry zone (61.8%-78.6%).

Enter the Trade – Consider longs in an uptrend at the OTE zone, and shorts in a downtrend.

Set Stop & Target – Place stops below/above the swing low/high and target extension levels (127.2%, 161.8%).

🎯 Key takeways

The CandelaCharts Fib Retracement (OTE) is a must-have tool for traders looking to refine their entries and maximize risk-reward potential with precision-based ICT trading strategies. 🚀

🚨 Alerts

The indicator does not provide any alerts!

⚠️ Disclaimer

Trading involves significant risk, and many participants may incur losses. The content on this site is not intended as financial advice and should not be interpreted as such. Decisions to buy, sell, hold, or trade securities, commodities, or other financial instruments carry inherent risks and are best made with guidance from qualified financial professionals. Past performance is not indicative of future results.

MOKI V1The "MOKI V1" script is a trading strategy on the TradingView platform that uses a combination of two key indicators to identify buy and sell signals:

EMA200 (Exponential Moving Average 200): Used to determine the overall market trend. This line helps ensure that trades are made in the direction of the primary market trend.

RSI (Relative Strength Index): Used to measure the strength or weakness of a trend. In this strategy, a reading above 50 for the RSI indicates stronger buy signals.

Engulfing Pattern: This candlestick pattern occurs when a green (bullish) candle completely engulfs the previous red (bearish) candle. It is used as a buy signal when combined with the other indicators.

Pearson Correlation CoefficientDescription: The Pearson Correlation Coefficient measures the strength and direction of the linear relationship between two data series. Its value ranges from -1 to +1, where:

+1 indicates a perfect positive linear correlation: as one asset increases, the other asset increases proportionally.

0 indicates no linear correlation: variations in one asset have no relation to variations in the other asset.

-1 indicates a perfect negative linear correlation: as one asset increases, the other asset decreases proportionally.

This measure is widely used in technical analysis to assess the degree of correlation between two financial assets. The "Pearson Correlation (Manual Compare)" indicator allows users to manually select two assets and visually display their correlation relationship on a chart.

Features:

Correlation Period: The time period used for calculating the correlation can be adjusted (default: 50).

Comparison Asset: Users can select a secondary asset for comparison.

Visual Plots: The chart includes reference lines for perfect correlations (+1 and -1) and strong correlations (+0.7 and -0.7).

Alerts: Set alerts for when the correlation exceeds certain threshold values (e.g., +0.7 for strong positive correlation).

How to Select the Second Asset:

Primary Asset Selection: The primary asset is the one you select for viewing on the chart. This can be done by simply opening the chart for the desired asset.

Secondary Asset Selection: To select the secondary asset for comparison, use the input field labeled "Comparison Asset" in the script settings. You can manually enter the ticker symbol of the secondary asset you want to compare with the primary asset.

This indicator is ideal for traders looking to identify relationships and correlations between different financial assets to make informed trading decisions.