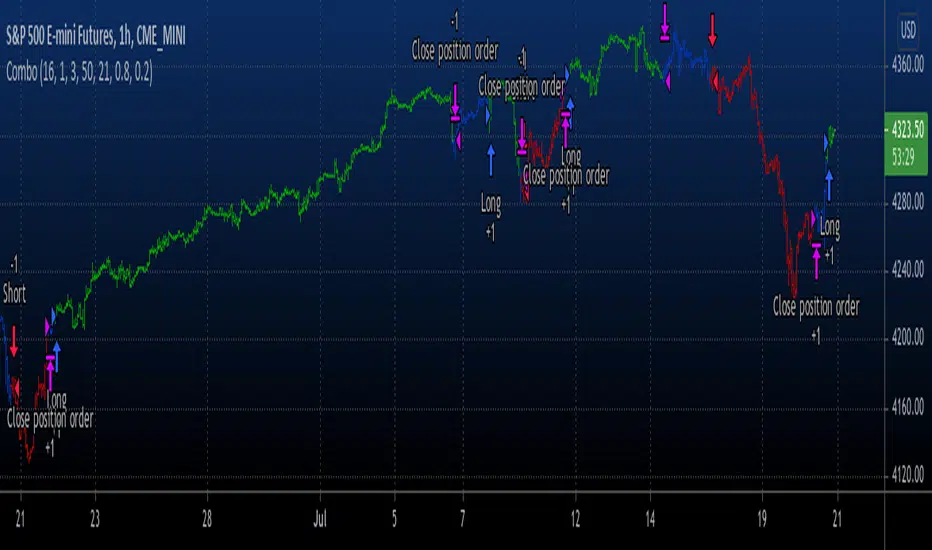

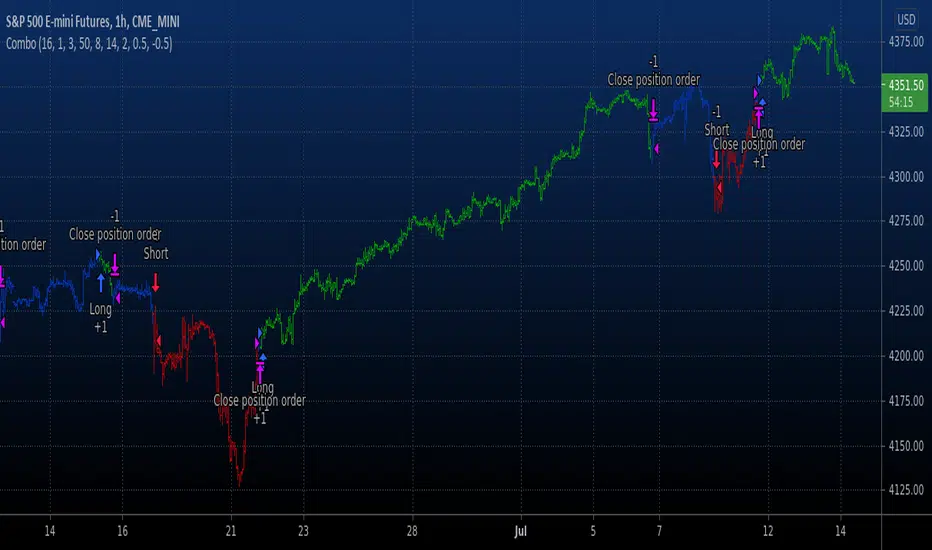

Dynamic Support and Resistance Pivot Strategy The Dynamic Support and Resistance Pivot Strategy is a flexible and adaptive tool designed to identify short-term support and resistance levels using the concept of price pivots.

### Key Elements of the Strategy

1. Pivot points as support and resistance levels

Pivots are significant turning points on the price chart, often marking local highs and lows where the price has reversed direction. A pivot high occurs when the price forms a local peak, while a pivot low occurs when the price forms a local trough. When a new pivot high is formed, it creates a resistance level. Conversely, when a new pivot low is formed, it creates a support level.

The strategy continuously updates these levels as new pivots are detected, ensuring they remain relevant to the current market conditions. By identifying these price levels, the strategy dynamically adjusts to market conditions, allowing it to adapt to both trending and ranging markets, since it has a long target and can perform reversal operations.

2. Entry Criteria

- Buy (Long): A long position is triggered when the price is near the support level and then crosses it from below to above. This suggests that the price has found support and may start moving upwards.

- Sell (Short): A short position is triggered when the price is near the resistance level and then crosses it from above to below. This indicates that the price may be reversing and moving downward.

3. Support/Resistance distance (%)

- This parameter establishes a percentage range around the identified support and resistance level. For example, if the Support Resistance Distance is 0.4% (default), the closing price must be within a range of 0.4% above support or below the resistance to be considered "close" and trigger a trade.

4. Exit criteria

- Take profit = 27 %

- Stop loss = 10 %

- Reversal if a new entry point is identified in the opposite direction

5. No Repainting

- The Dynamic Support and Resistance Pivot Strategy is not subject to repainting.

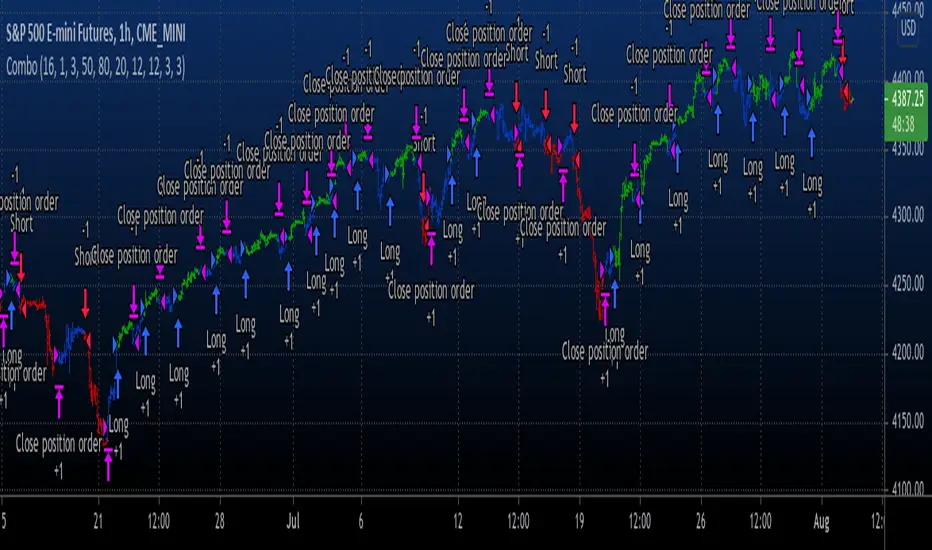

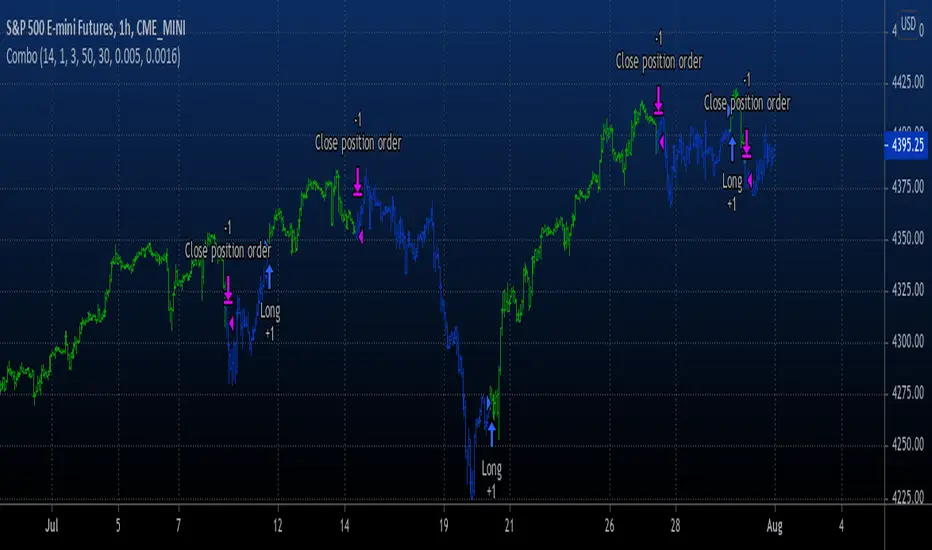

6. Position Sizing by Equity and risk management

- This strategy has a default configuration to operate with 35% of the equity. The stop loss is set to 10% from the entry price. This way, the strategy is putting at risk about 10% of 35% of equity, that is, around 3.5% of equity for each trade. The percentage of equity and stop loss can be adjusted by the user according to their risk management.

7. Backtest results

- This strategy was subjected to backtest and operations in replay mode on **1000000MOGUSDT.P**, with the inclusion of transaction fees at 0.12% and slipagge of 5 ticks, and the past results have shown consistent profitability. Past results are no guarantee of future results. The strategy's backtest results may even be due to overfitting with past data.

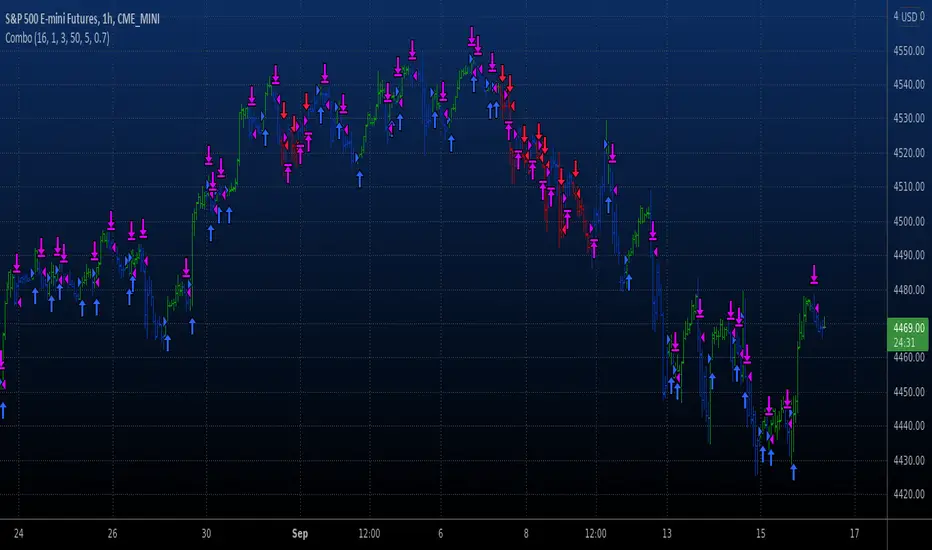

8. Chart Visualization

- Support and resistance levels are displayed as green (support) and red (resistance) lines.

- Pivot prices are displayed as green (pivot low) and red (pivot high) labels.

In this image above, the Support/Resistance distance (%) parameter was set to 0.8.

9. Default Configuration

Chart Timeframe: 1h

Pivot Lengh: 2

Support/Resistance distance (%): 0.4*

Stop Loss: 10 %

Take Profit: 27 %

* This parameter can alternatively be set to 0.8.

10. Alternative Configuration

Chart Timeframe: 20 min

Pivot Lengh: 4

Support/Resistance distance (%): 0.1

Stop Loss: 10 %

Take Profit: 25 %

BYBIT:1000000MOGUSDT.P

Reversal

Price Action StrategyThe **Price Action Strategy** is a tool designed to capture potential market reversals by utilizing classic reversal candlestick patterns such as Hammer, Shooting Star, Doji, and Pin Bar near dinamic support and resistance levels.

***Note to moderators

- The moving average was removed from the strategy because it was not suitable for the strategy and not participating in the entry or exit criteria.

- The moving average length has been replaced/renamed by the support/resistance lenght.

- The bullish engulfing and bearish engulfing patterns were also removed because in practice they were not working as entry criteria, since the candle price invariably closes far from the support/resistance level even considering the sensitivity range. There was no change in the backtest results after removing these patterns.

### Key Elements of the Strategy

1. Support and Resistance Levels

- Support and resistance are pivotal price levels where the asset has previously struggled to move lower (support) or higher (resistance). These levels act as psychological barriers where buying interest (at support) or selling interest (at resistance) often increases, potentially causing price reversals.

- In this strategy, support is calculated as the lowest low and resistance as the highest high over a 16-period length. When the price nears these levels, it indicates possible zones for a reversal, and the strategy looks for specific candlestick patterns to confirm an entry.

2. Candlestick Patterns

- This strategy uses classic reversal patterns, including:

- **Hammer**: Indicates a buy signal, suggesting rejection of lower prices.

- **Shooting Star**: Suggests a sell signal, showing rejection of higher prices.

- **Doji**: Reflects indecision and potential reversal.

- **Pin Bar**: Represents price rejection with a long shadow, often signaling a reversal.

By combining these reversal patterns with the proximity to dinamic support or resistance levels, the strategy aims to capture potential reversal movements.

3. Sensitivity Level

- The sensitivity parameter adjusts the acceptable range (Default 0.018 = 1.8%) around support and resistance levels within which reversal patterns can trigger trades (i.e. the closing price of the candle must occur within the specified range defined by the sensitivity parameter). A higher sensitivity value expands this range, potentially leading to less accurate signals, as it may allow for more false positives.

4. Entry Criteria

- **Buy (Long)**: A Hammer, Doji, or Pin Bar pattern near support.

- **Sell (Short)**: A Shooting Star, Doji, or Pin Bar near resistance.

5. Exit criteria

- Take profit = 9.5%

- Stop loss = 16%

6. No Repainting

- The Price Action Strategy is not subject to repainting.

7. Position Sizing by Equity and risk management

- This strategy has a default configuration to operate with 35% of the equity. The stop loss is set to 16% from the entry price. This way, the strategy is putting at risk about 16% of 35% of equity, that is, around 5.6% of equity for each trade. The percentage of equity and stop loss can be adjusted by the user according to their risk management.

8. Backtest results

- This strategy was subjected to deep backtest and operations in replay mode on **1000000MOGUSDT.P**, with the inclusion of transaction fees at 0.12% and slipagge of 5 ticks, and the past results have shown consistent profitability. Past results are no guarantee of future results. The strategy's backtest results may even be due to overfitting with past data.

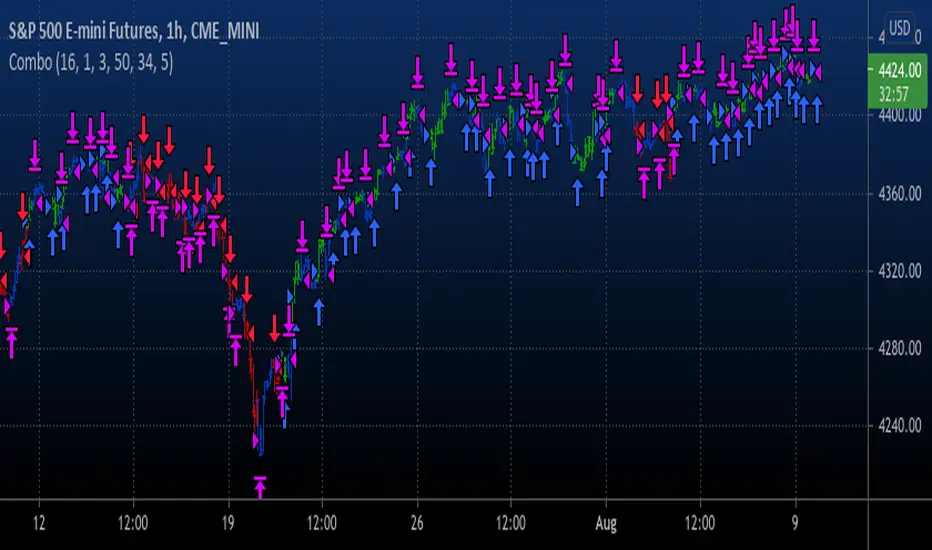

9. Chart Visualization

- Support and resistance levels are displayed as green (support) and red (resistance) lines.

- Only the candlestick pattern that generated the entry signal to triger the trade is identified and labeled on the chart. During the operation, the occurrence of new Doji, Pin Bar, Hammer and Shooting Star patterns will not be demonstrated on the chart, since the exit criteria are based on percentage take profit and stop loss.

Doji:

Pin Bar and Doji

Shooting Star and Doji

Hammer

10. Default settings

Chart timeframe: 20 min

Moving average lenght: 16

Sensitivity: 0.018

Stop loss (%): 16

Take Profit (%): 9.5

BYBIT:1000000MOGUSDT.P

I11L - Reversal Trading Ideas by Larry ConnorsThis is my own Twist on Larry Connors Simple Tradingideas.

It Combines the RSI, Averaging In and the Lowest Bars in a Single System.

The current Configuration is designed for the Daily Timeframe.

Feel free to play with the Parameters and keep in mind that Larry Intended to buy fear and sell the greed!

The Rules are the following:

---Buy---

Buy, if the lowest Bar of your Configuration has been hit (default is set to 7).

---Average Down--

Buy, if the lowest Bar of your Configuration * Your open trades has been hit AND only if the buyin is atleast 1% cheaper.

---Close---

Close, if the RSI closes above a certain level (default is set to 70).

---TP---

There is no TP

---SL---

There is no SL, so be cautions of your tail Risk!

Rob Booker Reversal Tabs StrategyRob Booker Reversal Tabs Strategy is an updated version of Rob Bookers Reversal Tab study: Rob Booker Reversal Tabs

While the original is a Pinescript study, this version can be switched between strategy and indicator mode.

Rob Bookers script generates reversal signal based on MACD and Stochastics, it is not a true reversal system, default pyramiding value is set to 5.

Inputs determine MACD and Stochastics settings. The only additional input is the "Strategy Mode" checkbox.

This script works well on its own for some tickers, but like any reversal pattern generating scripts, traders will profit from looking at overall price action and trend strength before making a trade.

From the original:

A simple reversal pattern indicator that uses MACD and Stochastics.

Created by Rob Booker and programmed by Andrew Palladino.

Please note that I only updated the original to V5 and edited it to be a strategy, which was a grand total of 5 minutes of work. I updated it because I wanted to see how the script performs as a strategy and I'm publishing it in case others would like to use it. I take no credit whatsoever for the original and WILL take this version down if Rob Booker or his Team ask me to or decide to release their own strategy version of the original.

Check out Rob Bookers scripts and ideas on his Tradingview account: robbooker

Range Strat - MACD/RSIThis strategy uses a trend based indicator (MACD) for entry/exit signals with a momentum oscillator (RSI) to act as confirmation. Although relying on a trend based indicator this has been created for range bound crypto markets, which have been in a period of chop since June 2022.

Long/Short signals are generated from MACD with the RSI oscillator thresholds suppressing entries at price extremes. This is not a mean reversion RSI strategy! As the indicators are contrary to each other you will need to be generous with the RSI settings in order for signals to trigger.

Strategy is designed for use on the 4h timeframe, it may work well on higher timeframes, but lower time frames will lead to false signals. Use fixed percentage of equity for order size to capture the compounding effect. As a reversal strategy bear in mind that should market trend strongly in either direction stops will be required.

The RSI thresholds can be tailored to provide higher frequency or safer signals. Similarly tweaking MACD settings will provide earlier/more frequent or safer signals. As this is intended to enter near range high / low you should check the visual cues to ensure a ping-pong effect is observed, so that peaks and troughs are captured. Once an observable range is established the strategy works well across a range of crypto markets,

The script is open source, so feel free to amend as you wish. Using a different momentum oscillator may provide better results. I have prior coding experience, but first time using PineScript was last night, so it's not very tidy. I will update this with some additional customisation and TP/SL in the near future.

Usage: Range bound markets

Markets: Cryptocurrency Alts/BTC/ETH

Timeframe: 4h

Triple RSI strategyThis strategy is commonly used both in forex and stock markets for reversal trading. when the rsi line reaches and crosses simultaneously at 3 rsi setups i.e at 7, 14, and 21, a signal is generated.

This strategy works best in 1-hour timeframe. It provides over 60 to 80 percent accuracy in 1-hour timeframe.

In the stock market, this strategy provides an excellent entry point, if one is seeking small profits.

One can expect to make around 10 to 50 pips in the forex market easily. However, I advise seeking support from price action from the lower timeframe in the forex market.

I hope you like it.

Follow for more strategies and scripts like this.

3C QFL Mean reversalWhat is QFL trading strategy?

QFL stands for Quickfingersluc, and sometimes it is referred to as the Base Strategy or Mean Reversals. Its main idea is about identifying the moment of panic selling and buying below the base level and utilizing Safety orders.

What is Base level or Support Level?

Base level or Support Level refers to the lowest price level that was reached before the moment the price started increasing again. At that level, you can notice that buyers of some cryptocurrencies make a strong reaction.

In this strategy we can also reverse the strategy and go short. But i must warn you that that is alot riskier.

QFL is meant to be used on higher TF's like 1hr, 2hr and 4hr. But this strategy also work well on lower Timeframes.

The script also simulates DCA strategy with parameters used in 3commas DCA bots for futures trading.

Experiment with parameters to find your trading setup.

Beware how large your total leveraged position is and how far can market go before you get liquidated!

Do that with the help of futures liquidation calculators you can find online!

Included:

An internal average price and profit calculating, instead of TV`s native one, which is subject to severe slippage.

A graphic interface, so levels are clearly visible and back-test analyzing made easier.

Long & Short direction of the strategy.

Table display a summary of past trades

Vertical colored lines appear when the new maximum deviation from the original price has

been reached

All the trading happens with total account capital, and all order sizes inputs are expressed in percent.

Swing Failure Reversal StrategyThis strategy is using Swing Failure Patterns as a reversion indicator.

The strategy automatically adapts itself to the timeframe of the current chart.

Swing Failure Pattern occurs when the price trend fails to set new highs in uptrend or meet new lows in a downtrend. This pattern helps traders decide when to enter and exit the market. Usually, traders enter in the downtrend i.e. lower price highs and lower price lows, and exit in the uptrend situation i.e. higher price highs and higher price lows. Thus, traders go against the current trend. This helps the traders take advantage of early trend reversal indicators.

Types of Failure Swing :

Failure Swing Top: This occurs when the stock price goes higher whereas the RSI fails to make a higher high and falls below the recent fail point. The Fail Point is where the RSI line is below the recent swing low. This Failure Swing indicates a short position.

Failure Swing Bottom: This occurs when the stock price gets lower whereas RSI fails to make a lower low and rises over the recent fail point. Fail point is the point where the RSI line is above the recent swing high. This Failure Swing indicates a long position.

Combo Backtest 123 Reversal & TEMA1This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This study plots the TEMA1 indicator. TEMA1 ia s triple MA (Moving Average),

and is calculated as 3*MA - (3*MA(MA)) + (MA(MA(MA)))

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & T3 Averages This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the moving average described in the January, 1998 issue

of S&C, p.57, "Smoothing Techniques for More Accurate Signals", by Tim Tillson.

This indicator plots T3 moving average presented in Figure 4 in the article.

T3 indicator is a moving average which is calculated according to formula:

T3(n) = GD(GD(GD(n))),

where GD - generalized DEMA (Double EMA) and calculating according to this:

GD(n,v) = EMA(n) * (1+v)-EMA(EMA(n)) * v,

where "v" is volume factor, which determines how hot the moving average’s response

to linear trends will be. The author advises to use v=0.7.

When v = 0, GD = EMA, and when v = 1, GD = DEMA. In between, GD is a less aggressive

version of DEMA. By using a value for v less than1, trader cure the multiple DEMA

overshoot problem but at the cost of accepting some additional phase delay.

In filter theory terminology, T3 is a six-pole nonlinear Kalman filter. Kalman

filters are ones that use the error — in this case, (time series - EMA(n)) —

to correct themselves. In the realm of technical analysis, these are called adaptive

moving averages; they track the time series more aggres-sively when it is making large

moves. Tim Tillson is a software project manager at Hewlett-Packard, with degrees in

mathematics and computer science. He has privately traded options and equities for 15 years.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Stochastic Crossover This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This back testing strategy generates a long trade at the Open of the following

bar when the %K line crosses below the %D line and both are above the Overbought level.

It generates a short trade at the Open of the following bar when the %K line

crosses above the %D line and both values are below the Oversold level.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & RSIThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The RSI is a very popular indicator that follows price activity.

It calculates an average of the positive net changes, and an average

of the negative net changes in the most recent bars, and it determines

the ratio between these averages. The result is expressed as a number

between 0 and 100. Commonly it is said that if the RSI has a low value,

for example 30 or under, the symbol is oversold. And if the RSI has a

high value, 70 for example, the symbol is overbought.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Awesome Oscillator (AO) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator is based on Bill Williams` recommendations from his book

"New Trading Dimensions". We recommend this book to you as most useful reading.

The wisdom, technical expertise, and skillful teaching style of Williams make

it a truly revolutionary-level source. A must-have new book for stock and

commodity traders.

The 1st 2 chapters are somewhat of ramble where the author describes the

"metaphysics" of trading. Still some good ideas are offered. The book references

chaos theory, and leaves it up to the reader to believe whether "supercomputers"

were used in formulating the various trading methods (the author wants to come across

as an applied mathemetician, but he sure looks like a stock trader). There isn't any

obvious connection with Chaos Theory - despite of the weak link between the title and

content, the trading methodologies do work. Most readers think the author's systems to

be a perfect filter and trigger for a short term trading system. He states a goal of

10%/month, but when these filters & axioms are correctly combined with a good momentum

system, much more is a probable result.

There's better written & more informative books out there for less money, but this author

does have the "Holy Grail" of stock trading. A set of filters, axioms, and methods which are

the "missing link" for any trading system which is based upon conventional indicators.

This indicator plots the oscillator as a histogram where periods fit for buying are marked

as blue, and periods fit for selling as red. If the current value of AC (Awesome Oscillator)

is over the previous, the period is deemed fit for buying and the indicator is marked blue.

If the AC values is not over the previous, the period is deemed fir for selling and the indicator

is marked red.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Awesome Oscillator (AC) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the oscillator as a histogram where blue denotes

periods suited for buying and red . for selling. If the current value

of AO (Awesome Oscillator) is above previous, the period is considered

suited for buying and the period is marked blue. If the AO value is not

above previous, the period is considered suited for selling and the

indicator marks it as red.

WARNING:

- For purpose educate only

- This script to change bars colors.

Pivot Reversal strategy long onlyPivot Point Reversal Strategy

Pivot point reversal strategy is based on the first support level’s price action during the bullish trend and the first resistance level during the bearish trend . Traders follow the main trend and enter into the trade after reversal analyzing pivot point levels.

This version is an upgraded version, combining the initial pivot point reversal strategy together with one of the most accuracy moving average in my opinion for day trade, the Least square moving average.

At the same time I applied an option to backtest using a date range and a leverage calculator.

The default options are optimized for BTC /USDT 2H charts, using 0.1% comission fee.

If you have any questions, let me know

Combo Backtest 123 Reversal & 2/20 Exponential MA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots 2/20 exponential moving average. For the Mov

Avg X 2/20 Indicator, the EMA bar will be painted when the Alert criteria is met.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Stochastic RSIThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This strategy used to calculate the Stochastic RSI

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Statistical Volatility This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator used to calculate the statistical volatility, sometime

called historical volatility, based on the Extreme Value Method.

Please use this link to get more information about Volatility.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & STARC BandsThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

A type of technical indicator that is created by plotting two bands around

a short-term simple moving average (SMA) of an underlying asset's price.

The upper band is created by adding a value of the average true range

(ATR) - a popular indicator used by technical traders - to the moving average.

The lower band is created by subtracting a value of the ATR from the SMA.

STARC is an acronym for Stoller Average Range Channels. The indicator is

named after its creator, Manning Stoller.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Smoothed Williams ADThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Accumulation is a term used to describe a market controlled by buyers;

whereas distribution is defined by a market controlled by sellers.

Williams recommends trading this indicator based on divergences:

Distribution of the security is indicated when the security is making

a new high and the A/D indicator is failing to make a new high. Sell.

Accumulation of the security is indicated when the security is making

a new low and the A/D indicator is failing to make a new low. Buy.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Smoothed RSIThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is new version of RSI oscillator indicator, developed by John Ehlers.

The main advantage of his way of enhancing the RSI indicator is smoothing

with minimum of lag penalty.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & SMI Ergodic Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The SMI Ergodic Indicator is the same as the True Strength Index (TSI) developed by

William Blau, except the SMI includes a signal line. The SMI uses double moving averages

of price minus previous price over 2 time frames. The signal line, which is an EMA of the

SMI, is plotted to help trigger trading signals. Adjustable guides are also given to fine

tune these signals. The user may change the input (close), method (EMA), period lengths

and guide values.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Smart Money Index (SMI) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Smart money index (SMI) or smart money flow index is a technical analysis indicator demonstrating investors sentiment.

The index was invented and popularized by money manager Don Hays. The indicator is based on intra-day price patterns.

The main idea is that the majority of traders (emotional, news-driven) overreact at the beginning of the trading day

because of the overnight news and economic data. There is also a lot of buying on market orders and short covering at the opening.

Smart, experienced investors start trading closer to the end of the day having the opportunity to evaluate market performance.

Therefore, the basic strategy is to bet against the morning price trend and bet with the evening price trend. The SMI may be calculated

for many markets and market indices (S&P 500, DJIA, etc.)

The SMI sends no clear signal whether the market is bullish or bearish. There are also no fixed absolute or relative readings signaling

about the trend. Traders need to look at the SMI dynamics relative to that of the market. If, for example, SMI rises sharply when the

market falls, this fact would mean that smart money is buying, and the market is to revert to an uptrend soon. The opposite situation

is also true. A rapidly falling SMI during a bullish market means that smart money is selling and that market is to revert to a downtrend

soon. The SMI is, therefore, a trend-based indicator.

Some analysts use the smart money index to claim that precious metals such as gold will continually maintain value in the future.

WARNING:

- For purpose educate only

- This script to change bars colors.