GKD-M Stepped Baseline Optimizer [Loxx]The Giga Kaleidoscope GKD-M Stepped Baseline Optimizer is a Metamorphosis module included in the "Giga Kaleidoscope Modularized Trading System."

█ Introduction

The GKD-M Stepped Baseline Optimizer is an advanced component of the Giga Kaleidoscope Modularized Trading System (GKD), designed to enhance trading strategy development by dynamically optimizing Baseline moving averages. This tool allows traders to evaluate over 65 moving averages, adjusting them across multiple periods to identify which settings yield the highest win rates for their trading strategies. The optimizer systematically tests these moving averages across specified timeframes and intervals, offering insights into net profit, total closed trades, win percentages, and other critical metrics for both long and short positions. Traders can define the initial period and incrementally adjust this value to explore a wide range of periods, thus fine-tuning their strategies with precision. What sets the GKD-M Stepped Baseline Optimizer apart is its unique capability to adapt the baseline moving average according to the highest win rates identified during backtesting, at each trading candle. This win-rate adaptive approach ensures that the trading system is always aligned with the most effective period settings for the selected moving average, enhancing the system's overall performance. Moreover, the 'stepped' aspect of this optimizer introduces a filtering process based ons, significantly reducing market noise and ensuring that identified trends are both significant and reliable. This feature is critical for traders looking to mitigate the risks associated with volatile market conditions and to capitalize on genuine market movements.In essence, the GKD-M Stepped Baseline Optimizer is tailored for traders who utilize the GKD trading system, offering a sophisticated tool to refine their baseline indicators dynamically, ensuring that their trading strategies are continuously optimized for maximum efficacy.

**the backtest data rendered to the chart above uses $5 commission per trade and 10% equity per trade with $1 million initial capital. Each backtest result for each ticker assumes these same inputs. The results are NOT cumulative, they are separate and isolated per ticker and trading side, long or short**

█ Core Features

Stepped Baseline for Noise Reduction

One of the hallmark features of the GKD-M Stepped Baseline Optimizer is its stepped baseline capability. This advanced functionality employs volatility filters to refine the selection of moving averages, significantly reducing market noise. The optimizer ensures that only substantial and reliable trends are considered, eliminating the false signals often caused by minor price fluctuations. This stepped approach to baseline optimization is critical for traders aiming to develop strategies that are both resilient and responsive to genuine market movements.

Dynamic Win Rate Adaptive Capability

Another cornerstone feature is the optimizer’s dynamic win rate adaptive capability. This unique aspect allows the optimizer to adjust the moving average period settings in real-time, based on the highest win rates derived from backtesting over a predefined range. At every trading candle, the optimizer evaluates a comprehensive set of backtesting data to ascertain the optimal period settings for the moving average in use. To perform the backtesting, the trader selects an initial period input (default is 60) and a skip value that increments the initial period input up to seven times. For instance, if a skip value of 5 is chosen, the Baseline Optimizer will run the backtest for the selected moving average on periods such as 60, 65, 70, 75, and so on, up to 90. If the user selects an initial period input of 45 and a skip value of 2, the Baseline Optimizer will conduct backtests for the chosen moving average on periods like 45, 47, 49, 51, and so forth, up to 57. The GKD-M Stepped Baseline Optimizer then exports the baseline with the highest cumulative win rate per candle to any baseline-enabled GKD backtest. This ensures that the baseline indicator remains continually aligned with the most efficacious parameters, dynamically adapting to changing market conditions.

Comprehensive Moving Averages Evaluation

The optimizer’s ability to test over 65 different moving averages across multiple periods stands as a testament to its comprehensive analytical capability. Traders have the flexibility to explore a wide array of moving averages, from traditional ones like the Simple Moving Average (SMA) and Exponential Moving Average (EMA) to more complex types such as the Hull Moving Average (HMA) and Adaptive Moving Average (AMA). This extensive evaluation allows traders to pinpoint the moving average that best aligns with their trading strategy and market conditions, further enhancing the system’s adaptability and effectiveness.

Volatility Filtering and Ticker Volatility Types

Incorporating a wide range of volatility types, including the option to utilize external volatility tickers like the VIX for filtering, adds another layer of sophistication to the optimizer. This feature allows traders to calibrate their baseline according to externals, providing an additional dimension of customization. Whether using standard deviation, ATR, or external volatility indices, traders can fine-tune their strategies to be responsive to the broader market sentiment and volatility trends.

█ Key Inputs

Baseline Settings

• Baseline Source: Determines the price data (Open, High, Low, Close) used for moving average calculations.

• Baseline Period: The starting period for moving average calculation.

• Backtest Skip: Incremental steps for period adjustments in the optimization process.

• Baseline Filter Type: Selection from over 65 moving averages for baseline calculation.

Volatility and Filter Settings

• Price Filter Type & Moving Average Filter Type: Defines thement applied to the price or the moving average, enhancing filter specificity.

• Filter Options: Allows users to select the application area of the volatility filter (price, moving average, or both).

• Filter Multiplier & Period: Configures the intensity and temporal scope of the filter, fine-tuning sensitivity to market volatility.

Backtest Configuration

• Window Period: Specifies the length of the backtesting window in days.

• Backtest Type: Chooses between a fixed window or cumulative data approach for backtesting.

• Initial Capital, Order Size, & Type: Sets the financial parameters for backtesting, including starting equity and the scale of trades.

• Commission per Order: Accounts for trading costs within backtest profitability calculations.

Date and Time Range

• From/Thru Year/Month/Day: Defines the historical period for strategy testing.

• Entry Time: Specifies the time frame during which trades can be initiated, crucial for strategies sensitive to market timing.

Volatility Measurements for Goldie Locks Volatility Qualifiers

• Mean Type & Period: Chooses the moving average type and period for volatility assessment.

• Inner/Outer Volatility Qualifier Multipliers: Adjusts the boundaries for volatility-based trade qualification.

• Activate Qualifier Boundaries: Enables or disables the upper and lower volatility qualifiers.

Advanced Volatility Inputs

• Volatility Ticker Selection & Trading Days: Incorporates external volatility indices (e.g., VIX) into the strategy, adjusting for market volatility.

• Static Percent, MAD Internal Filter Period, etc.: Provides fixed or adaptive volatility thresholds for filtering.

UI Customization

• Baseline Width & Table Display Options: Customizes the visual representation of the baseline and the display of optimization results.

• Table Header/Content Color & Text Size: Enhances readability and user interface aesthetics.

Export Options

• Export Data: Selects the specific metric to be exported from the script, such as net profit or average profit per trade.

Moving Average Specific Parameters

Specific inputs tailored to the characteristics of selected moving averages (e.g., Fractal Adjusted (FRAMA), Least Squares Moving Average (LSMA), T3, etc.), allowing users to fine-tune the behavior of these averages based on unique formula requirements.

█ Indicator UI

• Long and Short Baselines: The optimizer differentiates trends through two distinct baselines: a green line for long (uptrend) baselines and a red line for short (downtrend) baselines. These baselines alternate activation based on the current trend direction as determined by the moving average plus length combination for the candle in view.

Ambiguity in market direction, when an uptrend and downtrend are concurrently indicated, is visually represented by yellow lines.

• Stepping Mechanism for Trend Visualization: Adjusting the source input and the moving average output based on volatility, the indicator exhibits a stepped appearance on the chart. This mechanism ensures that only substantial market movements, surpassing a specified volatility threshold, are recognized as trend changes.

Stepping Activated

• Goldilocks Zone: Beyond the long and short baselines, the Goldilocks zone introduces a distinct moving average that closely follows the selected price or source input, aiming to strike the perfect balance between not too much and not too little market movement for trading. The upper limit of the Goldilocks zone indicates a market stretch too far for advantageous trading (overextension), while the lower limit suggests inadequate market movement for entry (underextension). Trading within the Goldilocks zone is deemed optimal, as it signifies sufficient but not excessive volatility for entering trades, aligning with either the long or short baseline recommendations. Moreover, the mean of the Goldilocks zone serves as a critical indicator, offering a median reference point that aligns closely with the market's current state. This mean is pivotal for traders, as it represents a 'just right' condition for market entry, embodying the essence of the Goldilocks principle in financial trading strategies.

• Signal Indicators and Entry Points: The chart includes with green or red dots to signify valid price points within the Goldilocks zone, indicative of conducive trading conditions. Furthermore, small directional arrows at the chart's bottom highlight potential long or short entry points, validated by the Goldilocks zone's parameters.

• Data Table: A table presenting real-time statistics from the current candle backward through the chosen range offers insights into win rates and other relevant data, aiding in informed decision-making. This table adapts with each new candle, highlighting the most favorable win rates for both long and short positions.

█ Optimizing Strategy with Backtesting

Optimizing a trading strategy with backtesting involves rigorously testing the strategy on historical data to evaluate its performance and robustness before applying it in live markets. The GKD-M Stepped Baseline Optimizer incorporates advanced backtesting capabilities, offering both cumulative and rolling window types of backtests. Here's how each backtest type operates and the insights they provide for refining trading strategies:

Cumulative Backtest

• Overview: A cumulative backtest evaluates a strategy's performance over a continuous period without resetting the strategy parameters or the simulated trading capital at the beginning of each new period.

• Utility: This type is useful for understanding a strategy's long-term viability, assessing how it adapts to different market conditions over an extended timeframe.

• Interpreting Statistics: Cumulative backtest results often focus on overall return, drawdowns, win rate, and the Sharpe ratio. A strategy with consistent returns, manageable drawdowns, a high win rate, and a favorable Sharpe ratio is considered robust.

Rolling Window Backtest

• Overview: Unlike the cumulative approach, a rolling window backtest divides the historical data into smaller, overlapping or non-overlapping periods (windows), running the strategy separately on each. After each window, the strategy parameters and simulated trading capital are reset.

• Utility: This method is invaluable for assessing a strategy's consistency and adaptability to various market phases. It helps identify if the strategy's performance is dependent on specific market conditions.

• Interpreting Statistics: For rolling window backtests, consistency is key. Look for similar performance metrics (returns, drawdowns, win rate) across different windows. Variability in performance indicates sensitivity to market conditions, suggesting the need for strategy adjustments.

Strategy Refinement Through Backtest Statistics

• Net Profit and Loss: Measures the strategy’s overall effectiveness. Consistent profitability across different market conditions is a positive indicator.

• Win Rate and Profit Factor: High win rates and profit factors indicate a strategy's efficiency in capturing gains over losses.

• Average Profit per Trade: Understanding the strategy's ability to generate profit on a per-trade basis can highlight its operational efficiency.

• Average Number of Bars in Trade: This metric helps understand the strategy's market exposure and timing efficiency.

█ Exporting Data and Integration with GKD Backtests

The GKD-M Stepped Baseline Optimizer seamlessly integrates with the broader GKD trading system, allowing traders to export the optimization data and leverage it within the various GKD backtest modules. This feature allows users to forward the GKD-M Stepped Baseline Optimizer adaptive signals to a GKD backtest to be used as a Baseline component in a GKD trading system.

█ Moving Averages included in the Stepped Baseline Optimizer

The GKD-M Stepped Baseline Optimizer incorporates an extensive array of over 65 moving averages, each with unique characteristics and implications for trading strategy development. This comprehensive suite enables traders to conduct nuanced analysis and optimization, ensuring the selection of the most effective moving average for Baseline input into their GKD trading system.

Adaptive Moving Average - AMA

ADXvma - Average Directional Volatility Moving Average

Ahrens Moving Average

Alexander Moving Average - ALXMA

Coral

Deviation Scaled Moving Average - DSMA

Donchian

Double Exponential Moving Average - DEMA

Double Smoothed Exponential Moving Average - DSEMA

Double Smoothed FEMA - DSFEMA

Double Smoothed Range Weighted EMA - DSRWEMA

Double Smoothed Wilders EMA - DSWEMA

Double Weighted Moving Average - DWMA

Ehlers Optimal Tracking Filter - EOTF

Exponential Moving Average - EMA

Fast Exponential Moving Average - FEMA

Fractal Adaptive Moving Average - FRAMA

Generalized DEMA - GDEMA

Generalized Double DEMA - GDDEMA

Geometric Mean Moving Average

Hull Moving Average (Type 1) - HMA1

Hull Moving Average (Type 2) - HMA2

Hull Moving Average (Type 3) - HMA3

Hull Moving Average (Type 4) - HMA4

IE/2 - Early T3 by Tim Tilson

Integral of Linear Regression Slope - ILRS

Instantaneous Trendline

Kalman Filter

Kaufman Adaptive Moving Average - KAMA

Laguerre Filter

Leader Exponential Moving Average

Linear Regression Value - LSMA (Least Squares Moving Average)

Linear Weighted Moving Average - LWMA

McGinley Dynamic

McNicholl EMA

Non-Lag Moving Average

Ocean NMA Moving Average - ONMAMA

One More Moving Average - OMA

Parabolic Weighted Moving Average

Probability Density Function Moving Average - PDFMA

Quadratic Regression Moving Average - QRMA

Range Filter

Range Weighted EMA - RWEMA

Recursive Moving Trendline

Regularized EMA - REMA

Simple Decycler - SDEC

Simple Loxx Moving Average - SLMA

Simple Moving Average - SMA

Sine Weighted Moving Average

Smoothed LWMA - SLWMA

Smoothed Moving Average - SMMA

Smoother

Super Smoother

T3

Tether Lines

Three-pole Ehlers Butterworth

Three-pole Ehlers Smoother

Triangular Moving Average - TMA

Triangle Moving Average Generalized

Triple Exponential Moving Average - TEMA

Two-pole Ehlers Butterworth

Two-pole Ehlers smoother

Ultimate Smoother

Variable Index Dynamic Average - VIDYA

Variable Moving Average - VMA

Volume Weighted EMA - VEMA

Volume Weighted Moving Average - VWMA

Zero-Lag DEMA - Zero Lag Double Exponential Moving Average

Zero-Lag Moving Average

Zero Lag TEMA - Zero Lag Triple Exponential Moving Average

█ Volatility Types and Filtering

The GKD-M Stepped Baseline Optimizer features a comprehensive selection of over 15 volatility types, each tailored to capture different aspects of market behavior and risk.

Volatility Ticker Selection: Enables direct incorporation of external volatility indicators like VIX and EUVIX into the script for market sentiment analysis, signal filtering enhancement, and real-time risk management adjustments.

Standard Deviation of Logarithmic Returns: Quantifies asset volatility using the standard deviation applied to logarithmic returns, capturing symmetric price movements and financial returns' compound nature.

Exponential Weighted Moving Average (EWMA) for Volatility: Focuses on recent market information by applying exponentially decreasing weights to squared logarithmic returns, offering a dynamic view of market volatility.

Roger-Satchell Volatility Measure: Estimates asset volatility by analyzing the high, low, open, and close prices, providing a nuanced view of intraday volatility and market dynamics.

Close-to-Close Volatility Measure: Calculates volatility based on the closing prices of stocks, offering a streamlined but limited perspective on market behavior.

Parkinson Volatility Measure: Enhances volatility estimation by including high and low prices of the trading day, capturing a more accurate reflection of intraday market movements.

Garman-Klass Volatility Measure: Incorporates open, high, low, and close prices for a comprehensive daily volatility measure, capturing significant price movements and market activity.

Yang-Zhang Volatility Measure: Offers an efficient estimation of stock market volatility by combining overnight and intraday price movements, capturing opening jumps and overall market dynamics.

Garman-Klass-Yang-Zhang Volatility Measure: Merges the benefits of Garman-Klass and Yang-Zhang measures, providing a fuller picture of market volatility including opening market reactions.

Pseudo GARCH(2,2) Volatility Model: Mimics a GARCH(2,2) process using exponential moving averages of squared returns, highlighting volatility shocks and their future impact.

ER-Adaptive Average True Range (ATR): Adjusts the ATR period length based on market efficiency, offering a volatility measure that adapts to changing market conditions.

Adaptive Deviation: Dynamically adjusts its calculation period to offer a nuanced measure of volatility that responds to the market's intrinsic rhythms.

Median Absolute Deviation (MAD): Provides a robust measure of statistical variability, focusing on deviations from the median price, offering resilience against outliers.

Mean Absolute Deviation (MAD): Measures the average magnitude of deviations from the mean price, facilitating a straightforward understanding of volatility.

ATR (Average True Range): Finds the average of true ranges over a specified period, indicating the expected price movement and market volatility.

True Range Double (TRD): Offers a nuanced view of volatility by considering a broader range of price movements, identifying significant market sentiment shifts.

Tìm kiếm tập lệnh với "GOLD"

SuperTrade ST1 StrategyOverview

The SuperTrade ST1 Strategy is a long-only trend-following strategy that combines a Supertrend indicator with a 200-period EMA filter to isolate high-probability bullish trade setups. It is designed to operate in trending markets, using volatility-based exits with a strict 1:4 Risk-to-Reward (R:R) ratio, meaning that each trade targets a profit 4× the size of its predefined risk.

This strategy is ideal for traders looking to align with medium- to long-term trends, while maintaining disciplined risk control and minimal trade frequency.

How It Works

This strategy leverages three key components:

Supertrend Indicator

A trend-following indicator based on Average True Range (ATR).

Identifies bullish/bearish trend direction by plotting a trailing stop line that moves with price volatility.

200-period Exponential Moving Average (EMA) Filter

Trades are only taken when the price is above the EMA, ensuring participation only during confirmed uptrends.

Helps filter out counter-trend entries during market pullbacks or ranges.

ATR-Based Stop Loss and Take Profit

Each trade uses the ATR to calculate volatility-adjusted exit levels.

Stop Loss: 1× ATR below entry.

Take Profit: 4× ATR above entry (1:4 R:R).

This asymmetry ensures that even with a lower win rate, the strategy can remain profitable.

Entry Conditions

A long trade is triggered when:

Supertrend flips from bearish to bullish (trend reversal).

Price closes above the Supertrend line.

Price is above the 200 EMA (bullish market bias).

Exit Logic

Once a long position is entered:

Stop loss is set 1 ATR below entry.

Take profit is set 4 ATR above entry.

The strategy automatically exits the position on either target.

Backtest Settings

This strategy is configured for realistic backtesting, including:

$10,000 account size

2% equity risk per trade

0.1% commission

1 tick slippage

These settings aim to simulate real-world conditions and avoid overly optimistic results.

How to Use

Apply the script to any timeframe, though higher timeframes (1H, 4H, Daily) often yield more reliable signals.

Works best in clearly trending markets (especially in crypto, stocks, indices).

Can be paired with alerts for live trading or analysis.

Important Notes

This version is long-only by design. No short positions are executed.

Ideal for swing traders or position traders seeking asymmetric returns.

Users can modify the ATR period, Supertrend factor, or EMA filter length based on asset behavior.

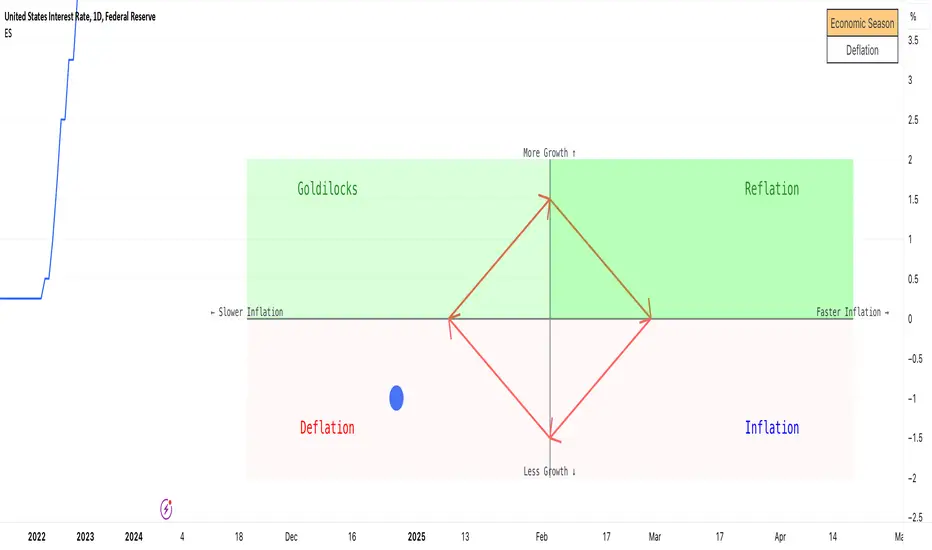

Economic Seasons [Daveatt]Ever wondered what season your economy is in?

Just like Mother Nature has her four seasons, the economy cycles through its own seasons! This indicator helps you visualize where we are in the economic cycle by tracking two key metrics:

📊 What We're Tracking:

1. Interest Rates (USIRYY) - The yearly change in interest rates

2. Inflation Rate (USINTR) - The rate at which prices are rising

The magic happens when we normalize these values (fancy math that makes the numbers play nice together) and compare them to their recent averages. We use a lookback period to calculate the standard deviation and determine if we're seeing higher or lower than normal readings.

🔄 The Four Economic Seasons & Investment Strategy:

1. 🌸 Goldilocks (↑Growth, ↓Inflation)

"Not too hot, not too cold" - The economy is growing steadily without overheating.

BEST TIME TO: Buy growth stocks, technology, consumer discretionary

WHY: Companies can grow earnings in this ideal environment of low rates and stable prices

2. 🌞 Reflation (↑Growth, ↑Inflation)

"Party time... but watch your wallet!" - The economy is heating up.

BEST TIME TO: Buy commodities, banking stocks, real estate

WHY: These sectors thrive when inflation rises alongside growth

3. 🌡️ Inflation (↓Growth, ↑Inflation)

"Ouch, my purchasing power!" - Growth slows while prices keep rising.

BEST TIME TO: Rotate into value stocks, consumer staples, healthcare

WHY: These defensive sectors maintain pricing power during inflationary periods

4. ❄️ Deflation (↓Growth, ↓Inflation)

"Winter is here" - Both growth and inflation are falling.

BEST TIME TO: Focus on quality bonds, cash positions, and dividend aristocrats

WHY: Capital preservation becomes key; high-quality fixed income provides safety

🎯 Strategic Trading Points:

- BUY AGGRESSIVELY: During late Deflation/early Goldilocks (the spring thaw)

- HOLD & ACCUMULATE: Throughout Goldilocks and early Reflation

- START TAKING PROFITS: During late Reflation/early Inflation

- DEFENSIVE POSITIONING: Throughout Inflation and Deflation

⚠️ Warning Signs to Watch:

- Goldilocks → Reflation: Time to reduce growth stock exposure

- Reflation → Inflation: Begin rotating into defensive sectors

- Inflation → Deflation: Quality becomes crucial

- Deflation → Goldilocks: Start building new positions

The blue dot shows you where we are right now in this cycle.

The red arrows in the middle remind us that this is a continuous cycle - one season flows into the next, just like in nature!

💡 Pro Tip: The transitions between seasons often provide the best opportunities - but also the highest risks. Use additional indicators and fundamental analysis to confirm these shifts.

Remember: Just like you wouldn't wear a winter coat in summer, you shouldn't use a Goldilocks strategy during Inflation! Time your trades with the seasons. 🎯

Happy Trading! 📈

Liquidity Sweep Guardian (Universal % or point based)

Liquidity Sweep Guardian - Complete User Guide

## Overview

The **Liquidity Sweep Guardian** is a visual warning system designed to prevent premature counter-trend trades (fades) near Previous Day High (PDH) and Previous Day Low (PDL) levels. This indicator helps you avoid one of the most common trading mistakes: fading too early before liquidity sweeps complete.

---

## 🎯 Core Trading Principle

### **THE GOLDEN RULE: Don't Fade Until It's Unlocked**

Price often **accelerates into key levels** to sweep liquidity before reversing. Trading against this momentum is extremely dangerous.

**The Process:**

1. **Danger Zone** (Red/White Box) = ⚠️ **DO NOT FADE** - Sweep likely incoming

2. **Sweep Occurs** (Triangle marker appears) = Price penetrates the level

3. **Reclaim Happens** (Price returns above/below level) = Level is tested

4. **🔓 UNLOCKED** (Gold border, green label) = **NOW you may CONSIDER a fade**

> **Important:** "UNLOCKED" means you may now *consider* a fade setup. It is NOT a trade signal itself. You still need your entry confirmation, risk management, and trade plan.

---

## 📊 Visual Elements Explained

### 1. **Danger Zone Boxes (Red Border by Default)**

**Two types of zones around PDH/PDL:**

- **Outer Danger Zone** (White fill): ±75pts (or 0.30%) around the level

- Indicates proximity to a key level where sweeps commonly occur

- Yellow/cautious trading zone

- **Inner Critical Zone** (Black fill): ±25pts (or 0.10%) around the level

- Highest probability area for liquidity sweep traps

- Avoid fading here at all costs

**What to do:**

- When price enters these zones, **wait and watch**

- Do not initiate counter-trend positions

- Allow the sweep to play out

### 2. **Unlocked Zones (Gold Border #ffeb3b)**

When a zone turns **gold/yellow** with green fill:

- The level has been swept AND reclaimed

- The liquidity grab is complete

- You may now look for fade opportunities with proper confirmation

### 3. **PDH/PDL Lines**

- **PDH Line** (Red): Previous Day High with price label

- **PDL Line** (Green): Previous Day Low with price label

- These are your key reference levels for the session

### 4. **Sweep Labels**

**Triangle Markers (SWEEP):**

- **Green Triangle** = Clean sweep (10-25pts penetration)

- **Orange Triangle** = Extended sweep (25-50pts penetration)

- **Red Triangle** = Deep penetration (50+ pts) - likely continuation, not reversal

**Warning Labels:**

- **⚠️ DEEP CONTINUATION?** = Penetration too deep, probably NOT a reversal setup

**Unlock Labels:**

- **🔓 LONG UNLOCKED** = PDL swept and reclaimed, may consider long fades

- **🔓 SHORT UNLOCKED** = PDH swept and reclaimed, may consider short fades

---

## ⚙️ Settings Guide

### **Calculation Mode**

**Use Percentage Mode (Default: ON)**

- ✅ **Enabled**: Universal mode - works on NQ, ES, RTY, stocks, crypto, forex

- ❌ **Disabled**: Fixed points mode - for specific instruments only

**When to use each:**

- **Percentage Mode**: Trading multiple instruments, or instruments with varying price levels

- **Fixed Points Mode**: Single instrument focus (e.g., only trading NQ at current levels)

### **Danger Zone Settings**

**Percentage Mode (Default for Universal Use):**

- **Danger Zone**: 0.30% each side (≈75pts on NQ@25,000)

- **Critical Zone**: 0.10% each side (≈25pts on NQ@25,000)

**Fixed Points Mode (For NQ Specifically):**

- **Danger Zone**: 75 points each side

- **Critical Zone**: 25 points each side

**Adjustment Tips:**

- For more volatile instruments: Increase percentages/points

- For less volatile instruments: Decrease percentages/points

- For higher timeframes: Use wider zones

- For lower timeframes: Use tighter zones

### **Sweep Classification**

**What defines a "real" sweep:**

- **Minimum**: 10pts / 0.04% - Shallow penetration may not grab enough liquidity

- **Optimal**: 10-25pts / 0.04-0.10% - "Goldilocks zone" for reversal setups

- **Extended**: 25-50pts / 0.10-0.20% - Deeper sweep, less reliable

- **Continuation**: 50+pts / 0.20%+ - Too deep, likely NOT reversing

**Max Bars for Reclaim**: 5 bars (default)

- Price should reclaim the level relatively quickly

- If it takes too long, the sweep may have failed

### **Visual Customization**

**Box Settings:**

- **Left Extension**: 60 bars (how far back the box extends)

- **Right Extension**: 50 bars (how far forward the box extends)

**Toggle Options:**

- Show/Hide Danger Zone Boxes

- Show/Hide PDH/PDL Lines

- Show/Hide Price Labels on lines

- Show/Hide Sweep Labels

- Show/Hide Unlock Labels

### **Color Customization**

All colors are fully customizable:

- Danger Zone Fill & Border

- Critical Zone Fill & Border

- Unlocked Zone Fill & Border

- PDH/PDL Line Colors

- PDH/PDL Label Colors

- Border Widths (1-5 pixels)

- Line Widths (1-5 pixels)

---

## 🎓 Trading Strategy Examples

### **Example 1: Long Setup at PDL**

1. **Morning**: Price approaches PDL (danger zone appears)

2. **Don't Fade Yet**: Price enters critical zone - resist urge to buy

3. **Sweep**: Price drops 15pts below PDL (green triangle appears)

4. **Reclaim**: Price closes back above PDL within 3 bars

5. **🔓 UNLOCKED**: Gold border + "LONG UNLOCKED" label appears

6. **Trade Setup**: Now look for bullish confirmation (order flow, structure, etc.)

### **Example 2: Avoiding a Trap at PDH**

1. **Afternoon**: Price rallies into PDH danger zone

2. **Temptation**: You want to short here (it "looks toppy")

3. **Sweep**: Price breaks 50pts above PDH (red triangle + ⚠️ warning)

4. **Continuation**: Deep penetration suggests continuation, not reversal

5. **Result**: No unlock occurs, price keeps running higher - trap avoided!

### **Example 3: Failed Unlock (No Trade)**

1. Price sweeps PDL by 12pts (green triangle)

2. Price struggles to reclaim PDL, stays below for 10+ bars

3. No "UNLOCKED" label appears

4. **Correct Action**: Do not fade - sweep failed to reclaim

---

## 📱 Alerts

The indicator includes built-in alerts for:

- **Entering Danger Zones**: Get warned when price approaches PDH/PDL

- **Sweep Detection**: Know immediately when a level is swept

- **Unlock Signals**: Get notified when fade setups become available

- **Continuation Warnings**: Alert when penetration suggests continuation

**To Set Alerts:**

1. Right-click indicator → "Add Alert"

2. Select desired alert condition

3. Configure notification preferences

---

## ⚠️ Important Disclaimers

### **What This Indicator IS:**

✅ A visual warning system to prevent premature fades

✅ A tool to identify when liquidity sweeps have completed

✅ A framework for counter-trend trade timing

### **What This Indicator IS NOT:**

❌ A complete trading system

❌ An entry signal generator

❌ A guarantee of trade success

❌ A substitute for proper risk management

### **Always Remember:**

- "UNLOCKED" = You may CONSIDER a fade (not a signal to trade)

- You still need your own entry confirmation

- You still need proper stop placement

- You still need position sizing and risk management

- Not every unlock leads to a successful trade

- Market context and order flow still matter

---

## 🔧 Recommended Settings by Instrument

### **NQ (Nasdaq-100 E-mini Futures)**

- Mode: Percentage or Fixed Points

- Percentage: 0.30% / 0.10% (default)

- Fixed Points: 75pts / 25pts (default)

### **ES (S&P 500 E-mini Futures)**

- Mode: Percentage

- Danger: 0.25% / Critical: 0.08%

- Or Fixed Points: 15pts / 5pts

### **RTY (Russell 2000 E-mini Futures)**

- Mode: Percentage

- Danger: 0.35% / Critical: 0.12%

- Or Fixed Points: 8pts / 3pts

### **Stocks (High Volume Large Caps)**

- Mode: Percentage (recommended)

- Danger: 0.20-0.40% / Critical: 0.08-0.15%

- Adjust based on ATR and volatility

### **Crypto (BTC, ETH)**

- Mode: Percentage (essential)

- Danger: 0.40-0.60% / Critical: 0.15-0.20%

- Higher volatility requires wider zones

---

## 💡 Pro Tips

1. **Use on Higher Timeframes**: Works best on 5min, 15min, 1hr charts

2. **Combine with Order Flow**: Use with footprint/delta for confirmation

3. **Watch Volume**: Strong volume on sweep = better reversal potential

4. **Consider Time of Day**: Sweeps during RTH often more reliable

5. **Multiple Timeframes**: Check if higher TF also shows unlock

6. **Don't Force Trades**: Not every session produces clean setups

7. **Journal Results**: Track which unlock types work best for you

8. **Respect Continuation Signals**: When indicator says "too deep," listen

---

## 🆘 Troubleshooting

**Q: Box isn't showing up**

A: Check that "Show Danger Zone Boxes" is enabled in Visual Settings

**Q: No price on labels**

A: Enable "Show Price Labels on Lines" in Visual Settings

**Q: Zones seem too tight/wide**

A: Adjust Danger Zone % or points based on current volatility

**Q: Getting too many/too few unlocks**

A: Adjust sweep classification thresholds (min/max penetration)

**Q: Want thicker/thinner lines**

A: Adjust line widths in "PDH/PDL Line Colors" section

**Q: Colors not matching my chart theme**

A: Fully customize all colors in the color settings groups

---

## 📚 Additional Resources

- Study price action around PDH/PDL on your instruments

- Learn about liquidity sweeps and stop hunts

- Understand market structure and order flow

- Practice identifying setups on replay/historical data

- Keep a trading journal of unlock scenarios

---

*Remember: The best trade is often the one you don't take. This indicator helps you avoid the trades you shouldn't take, so you can focus on the ones you should.*

Indian Market Trend

# Indian Market Trend

## **Know The Trend BEFORE It Happens - Institutional-Grade Market Intelligence**

### **🎯 Why This Indicator is Different:**

Most indicators tell you what **already happened**. This institutional-grade tool tells you what's **about to happen** by analyzing the **synchronized behavior of 40 major Indian stocks** in real-time.

***

## **📊 THREE POWERFUL ANALYSIS TABLES**

### **1️⃣ CORRELATION ANALYSIS TABLE**

- **Real-time correlation** of 40 NSE stocks with your chart symbol

- **Implied Trend Calculation** - The secret sauce that shows market direction BEFORE price confirms

- **Positive Implied Trend** = Stocks moving UP together (Bullish Confirmation)

- **Negative Implied Trend** = Stocks moving DOWN together (Bearish Warning)

- Fully customizable: Choose which stocks to analyze and table position

### **2️⃣ MARKET REGIME ANALYSIS TABLE**

Institutional-grade regime detection across **4 major market conditions:**

- **🟢 GOLDILOCKS REGIME** - Perfect growth environment (Risk-On)

- **🟡 REFLATION REGIME** - Economic recovery phase (High Beta Rally)

- **🔴 INFLATION REGIME** - Defensive rotation (Protect Capital)

- **🔵 DEFLATION REGIME** - Risk-off environment (Safe Havens)

**Each regime shows:**

- Top 5 performing equity style factors

- Bottom 5 underperforming factors

- Probability score for each regime

- **RISK ON/RISK OFF** status with real-time calculation

### **3️⃣ TOP/BOTTOM PERFORMERS TABLE**

- **Real-time ranking** of best and worst performing stocks

- Adjustable display (5-20 stocks)

- Shows relative strength vs market average

- Perfect for stock selection and sector rotation

***

## **🚀 THE EDGE: IMPLIED CORRELATION INDICATOR**

### **This is where the magic happens:**

The **Implied Correlation Plot** combines:

1. **Correlation Strength** - How stocks move together

2. **KAMA Trend Analysis** - Institutional adaptive moving average

3. **Directional Bias** - Market sentiment calculation

### **How to Read It:**

✅ **POSITIVE VALUES (Green Bars)**

- Stocks are moving UP in sync

- Strong bullish momentum

- High confidence in uptrend continuation

- **ACTION: Stay long, add on dips**

❌ **NEGATIVE VALUES (Red Bars)**

- Stocks are moving DOWN together

- Strong bearish pressure

- High confidence in downtrend continuation

- **ACTION: Reduce exposure, wait for reversal**

⚪ **NEAR ZERO (Gray Bars)**

- Market is confused/consolidating

- Low directional conviction

- Wait for clarity

- **ACTION: No new positions, tight stops**

### **The Institutional Advantage:**

When you see **strong green bars forming** → Market is building bullish pressure **BEFORE** your main chart shows a clear breakout!

When you see **strong red bars forming** → Market is building bearish pressure **BEFORE** your main chart breaks down!

**This is your early warning system!** 🎯

***

## **🎛️ FULLY CUSTOMIZABLE**

### **Table Controls:**

- ✅ Enable/Disable each table independently

- 📍 Position tables anywhere (Top/Middle/Bottom × Left/Center/Right)

- 📏 Adjustable text size for all displays

- 🎨 Clean, professional interface

### **Stock Selection:**

- **40 Pre-loaded NSE stocks** (Nifty 50 constituents)

- Fully editable - Replace ANY stock with your preferred symbols

- Works with NSE, BSE, or any exchange

- Perfect for sectoral analysis

### **Technical Parameters:**

- **Correlation Length** (Default: 14 days)

- **ROC Period** (Default: 14 days)

- **KAMA Settings** (Fast: 7, Slow: 19, ER: 8)

- **Display Options** (Number of stocks in each table)

***

## **📈 TRADING APPLICATIONS**

### **For Day Traders:**

- Early trend detection before price confirms

- Market regime identification for strategy selection

- Real-time sector rotation signals

### **For Swing Traders:**

- Multi-day trend confirmation

- Risk-on/Risk-off regime detection

- Top performer identification for swing entries

### **For Position Traders:**

- Long-term market regime analysis

- Portfolio rotation based on market conditions

- Macro trend confirmation

### **For Portfolio Managers:**

- Institutional-grade market regime framework

- 40-stock basket analysis

- Systematic rotation signals

***

## **🏆 KEY FEATURES**

✅ **40 Major Indian Stocks** - Comprehensive market coverage

✅ **3 Analysis Tables** - Correlation, Regime, Performance

✅ **Implied Correlation Plot** - Leading trend indicator

✅ **KAMA Trend Engine** - Adaptive institutional algorithm

✅ **Regime Detection** - Goldilocks/Reflation/Inflation/Deflation

✅ **Fully Customizable** - Every parameter adjustable

✅ **No Repainting** - Signals are final and reliable

✅ **Clean Interface** - Professional institutional design

✅ **Multi-Timeframe** - Works on Daily charts (recommended)

***

## **⚡ QUICK START GUIDE**

1. **Add indicator to Daily chart** of NSE:NIFTY or any Indian stock

2. **Enable all 3 tables** from "Table Controls" section (default: ON)

3. **Watch Implied Correlation plot** in indicator window:

- Green bars = Bullish strength building

- Red bars = Bearish pressure building

- Gray bars = Wait for clarity

4. **Check Market Regime Table** - Which regime has highest probability?

5. **Scan Top Performers Table** - Find strongest stocks for entries

6. **Cross-reference with your price action** - Confirm with chart patterns

***

## **🎓 INSTITUTIONAL METHODOLOGY**

This indicator uses the same frameworks employed by:

- Hedge funds for market regime detection

- Proprietary trading desks for correlation analysis

- Risk management teams for portfolio positioning

- Quantitative analysts for systematic signals

**The Normalized KAMA Oscillator** by IkkeOmar provides institutional-grade trend detection with adaptive smoothing that responds to market efficiency.

**The Implied Correlation Framework** measures market synchronization - when stocks move together with conviction, trends are more reliable and persistent.

***

## **💡 PRO TIPS**

1. **Best Results:** Use on Daily timeframe for most reliable signals

2. **Strong Signals:** Implied Correlation > 0.15 or < -0.15 = High conviction

3. **Regime Changes:** Watch for probability shifts between regimes

4. **Divergences:** If top performers weaken while index rises = Warning signal

5. **Confirmation:** Wait for 2-3 consecutive bars in same direction for stronger confidence

***

## **⚠️ RISK DISCLAIMER**

This indicator is a **decision support tool**, not financial advice. Always:

- Use proper risk management

- Combine with your own analysis

- Test on demo/paper trading first

- Never risk more than you can afford to lose

- Past performance doesn't guarantee future results

***

## **📞 SUPPORT & UPDATES**

- Regular updates with market condition changes

- Community feedback incorporated

- Bug fixes and optimizations

- Documentation and video tutorials (coming soon)

***

## **🌟 WHY TRADERS LOVE THIS INDICATOR**

✅ **"Finally see the market BEFORE it moves!"**

✅ **"Three tables give complete market picture"**

✅ **"Regime detection is game-changing"**

✅ **"Professional institutional tool for retail traders"**

✅ **"Clean, customizable, reliable"**

***

## **📊 INDICATOR SPECIFICATIONS**

- **Type:** Oscillator / Market Analysis

- **Overlay:** No (Separate pane)

- **Inputs:** 40 stock symbols + multiple parameters

- **Outputs:** 3 tables + 1 plot line

- **Repainting:** No

- **Alerts:** Compatible (can be added)

- **Multi-timeframe:** Yes (Daily recommended)

***

## **🎯 START TRADING WITH CONFIDENCE**

**Know the trend BEFORE the crowd!**

The market doesn't move in straight lines - it moves in **synchronized waves**. When you can measure that synchronization across 40 major stocks, you have an **institutional edge** that retail traders never see.

**Install now and experience the difference!** 🚀

***

**Tags:** #Indian #NSE #Nifty50 #Correlation #MarketRegime #TrendAnalysis #Institutional #KAMA #Performance #TopPerformers #RiskOn #RiskOff #Goldilocks #Reflation #ImpliedCorrelation

***

**Version:** 1.0

**Last Updated:** December 2025

**Compatible:** TradingView Pine Script v6

***

Feel free to ask questions in the comments! I actively respond to user feedback and continuously improve this indicator based on community needs.

**Happy Trading! 📈🎯**

***

ORB Fusion🎯 CORE INNOVATION: INSTITUTIONAL ORB FRAMEWORK WITH FAILED BREAKOUT INTELLIGENCE

ORB Fusion represents a complete institutional-grade Opening Range Breakout system combining classic Market Profile concepts (Initial Balance, day type classification) with modern algorithmic breakout detection, failed breakout reversal logic, and comprehensive statistical tracking. Rather than simply drawing lines at opening range extremes, this system implements the full trading methodology used by professional floor traders and market makers—including the critical concept that failed breakouts are often higher-probability setups than successful breakouts .

The Opening Range Hypothesis:

The first 30-60 minutes of trading establishes the day's value area —the price range where the majority of participants agree on fair value. This range is formed during peak information flow (overnight news digestion, gap reactions, early institutional positioning). Breakouts from this range signal directional conviction; failures to hold breakouts signal trapped participants and create exploitable reversals.

Why Opening Range Matters:

1. Information Aggregation : Opening range reflects overnight news, pre-market sentiment, and early institutional orders. It's the market's initial "consensus" on value.

2. Liquidity Concentration : Stop losses cluster just outside opening range. Breakouts trigger these stops, creating momentum. Failed breakouts trap traders, forcing reversals.

3. Statistical Persistence : Markets exhibit range expansion tendency —when price accepts above/below opening range with volume, it often extends 1.0-2.0x the opening range size before mean reversion.

4. Institutional Behavior : Large players (market makers, institutions) use opening range as reference for the day's trading plan. They fade extremes in rotation days and follow breakouts in trend days.

Historical Context:

Opening Range Breakout methodology originated in commodity futures pits (1970s-80s) where floor traders noticed consistent patterns: the first 30-60 minutes established a "fair value zone," and directional moves occurred when this zone was violated with conviction. J. Peter Steidlmayer formalized this observation in Market Profile theory, introducing the "Initial Balance" concept—the first hour (two 30-minute periods) defining market structure.

📊 OPENING RANGE CONSTRUCTION

Four ORB Timeframe Options:

1. 5-Minute ORB (0930-0935 ET):

Captures immediate market direction during "opening drive"—the explosive first few minutes when overnight orders hit the tape.

Use Case:

• Scalping strategies

• High-frequency breakout trading

• Extremely liquid instruments (ES, NQ, SPY)

Characteristics:

• Very tight range (often 0.2-0.5% of price)

• Early breakouts common (7 of 10 days break within first hour)

• Higher false breakout rate (50-60%)

• Requires sub-minute chart monitoring

Psychology: Captures panic buyers/sellers reacting to overnight news. Range is small because sample size is minimal—only 5 minutes of price discovery. Early breakouts often fail because they're driven by retail FOMO rather than institutional conviction.

2. 15-Minute ORB (0930-0945 ET):

Balances responsiveness with statistical validity. Captures opening drive plus initial reaction to that drive.

Use Case:

• Day trading strategies

• Balanced scalping/swing hybrid

• Most liquid instruments

Characteristics:

• Moderate range (0.4-0.8% of price typically)

• Breakout rate ~60% of days

• False breakout rate ~40-45%

• Good balance of opportunity and reliability

Psychology: Includes opening panic AND the first retest/consolidation. Sophisticated traders (institutions, algos) start expressing directional bias. This is the "Goldilocks" timeframe—not too reactive, not too slow.

3. 30-Minute ORB (0930-1000 ET):

Classic ORB timeframe. Default for most professional implementations.

Use Case:

• Standard intraday trading

• Position sizing for full-day trades

• All liquid instruments (equities, indices, futures)

Characteristics:

• Substantial range (0.6-1.2% of price)

• Breakout rate ~55% of days

• False breakout rate ~35-40%

• Statistical sweet spot for extensions

Psychology: Full opening auction + first institutional repositioning complete. By 10:00 AM ET, headlines are digested, early stops are hit, and "real" directional players reveal themselves. This is when institutional programs typically finish their opening positioning.

Statistical Advantage: 30-minute ORB shows highest correlation with daily range. When price breaks and holds outside 30m ORB, probability of reaching 1.0x extension (doubling the opening range) exceeds 60% historically.

4. 60-Minute ORB (0930-1030 ET) - Initial Balance:

Steidlmayer's "Initial Balance"—the foundation of Market Profile theory.

Use Case:

• Swing trading entries

• Day type classification

• Low-frequency institutional setups

Characteristics:

• Wide range (0.8-1.5% of price)

• Breakout rate ~45% of days

• False breakout rate ~25-30% (lowest)

• Best for trend day identification

Psychology: Full first hour captures A-period (0930-1000) and B-period (1000-1030). By 10:30 AM ET, all early positioning is complete. Market has "voted" on value. Subsequent price action confirms (trend day) or rejects (rotation day) this value assessment.

Initial Balance Theory:

IB represents the market's accepted value area . When price extends significantly beyond IB (>1.5x IB range), it signals a Trend Day —strong directional conviction. When price remains within 1.0x IB, it signals a Rotation Day —mean reversion environment. This classification completely changes trading strategy.

🔬 LTF PRECISION TECHNOLOGY

The Chart Timeframe Problem:

Traditional ORB indicators calculate range using the chart's current timeframe. This creates critical inaccuracies:

Example:

• You're on a 5-minute chart

• ORB period is 30 minutes (0930-1000 ET)

• Indicator sees only 6 bars (30min ÷ 5min/bar = 6 bars)

• If any 5-minute bar has extreme wick, entire ORB is distorted

The Problem Amplifies:

• On 15-minute chart with 30-minute ORB: Only 2 bars sampled

• On 30-minute chart with 30-minute ORB: Only 1 bar sampled

• Opening spike or single large wick defines entire range (invalid)

Solution: Lower Timeframe (LTF) Precision:

ORB Fusion uses `request.security_lower_tf()` to sample 1-minute bars regardless of chart timeframe:

```

For 30-minute ORB on 15-minute chart:

- Traditional method: Uses 2 bars (15min × 2 = 30min)

- LTF Precision: Requests thirty 1-minute bars, calculates true high/low

```

Why This Matters:

Scenario: ES futures, 15-minute chart, 30-minute ORB

• Traditional ORB: High = 5850.00, Low = 5842.00 (range = 8 points)

• LTF Precision ORB: High = 5848.50, Low = 5843.25 (range = 5.25 points)

Difference: 2.75 points distortion from single 15-minute wick hitting 5850.00 at 9:31 AM then immediately reversing. LTF precision filters this out by seeing it was a fleeting wick, not a sustained high.

Impact on Extensions:

With inflated range (8 points vs 5.25 points):

• 1.5x extension projects +12 points instead of +7.875 points

• Difference: 4.125 points (nearly $200 per ES contract)

• Breakout signals trigger late; extension targets unreachable

Implementation:

```pinescript

getLtfHighLow() =>

float ha = request.security_lower_tf(syminfo.tickerid, "1", high)

float la = request.security_lower_tf(syminfo.tickerid, "1", low)

```

Function returns arrays of 1-minute high/low values, then finds true maximum and minimum across all samples.

When LTF Precision Activates:

Only when chart timeframe exceeds ORB session window:

• 5-minute chart + 30-minute ORB: LTF used (chart TF > session bars needed)

• 1-minute chart + 30-minute ORB: LTF not needed (direct sampling sufficient)

Recommendation: Always enable LTF Precision unless you're on 1-minute charts. The computational overhead is negligible, and accuracy improvement is substantial.

⚖️ INITIAL BALANCE (IB) FRAMEWORK

Steidlmayer's Market Profile Innovation:

J. Peter Steidlmayer developed Market Profile in the 1980s for the Chicago Board of Trade. His key insight: market structure is best understood through time-at-price (value area) rather than just price-over-time (traditional charts).

Initial Balance Definition:

IB is the price range established during the first hour of trading, subdivided into:

• A-Period : First 30 minutes (0930-1000 ET for US equities)

• B-Period : Second 30 minutes (1000-1030 ET)

A-Period vs B-Period Comparison:

The relationship between A and B periods forecasts the day:

B-Period Expansion (Bullish):

• B-period high > A-period high

• B-period low ≥ A-period low

• Interpretation: Buyers stepping in after opening assessed

• Implication: Bullish continuation likely

• Strategy: Buy pullbacks to A-period high (now support)

B-Period Expansion (Bearish):

• B-period low < A-period low

• B-period high ≤ A-period high

• Interpretation: Sellers stepping in after opening assessed

• Implication: Bearish continuation likely

• Strategy: Sell rallies to A-period low (now resistance)

B-Period Contraction:

• B-period stays within A-period range

• Interpretation: Market indecisive, digesting A-period information

• Implication: Rotation day likely, stay range-bound

• Strategy: Fade extremes, sell high/buy low within IB

IB Extensions:

Professional traders use IB as a ruler to project price targets:

Extension Levels:

• 0.5x IB : Initial probe outside value (minor target)

• 1.0x IB : Full extension (major target for normal days)

• 1.5x IB : Trend day threshold (classifies as trending)

• 2.0x IB : Strong trend day (rare, ~10-15% of days)

Calculation:

```

IB Range = IB High - IB Low

Bull Extension 1.0x = IB High + (IB Range × 1.0)

Bear Extension 1.0x = IB Low - (IB Range × 1.0)

```

Example:

ES futures:

• IB High: 5850.00

• IB Low: 5842.00

• IB Range: 8.00 points

Extensions:

• 1.0x Bull Target: 5850 + 8 = 5858.00

• 1.5x Bull Target: 5850 + 12 = 5862.00

• 2.0x Bull Target: 5850 + 16 = 5866.00

If price reaches 5862.00 (1.5x), day is classified as Trend Day —strategy shifts from mean reversion to trend following.

📈 DAY TYPE CLASSIFICATION SYSTEM

Four Day Types (Market Profile Framework):

1. TREND DAY:

Definition: Price extends ≥1.5x IB range in one direction and stays there.

Characteristics:

• Opens and never returns to IB

• Persistent directional movement

• Volume increases as day progresses (conviction building)

• News-driven or strong institutional flow

Frequency: ~20-25% of trading days

Trading Strategy:

• DO: Follow the trend, trail stops, let winners run

• DON'T: Fade extremes, take early profits

• Key: Add to position on pullbacks to previous extension level

• Risk: Getting chopped in false trend (see Failed Breakout section)

Example: FOMC decision, payroll report, earnings surprise—anything creating one-sided conviction.

2. NORMAL DAY:

Definition: Price extends 0.5-1.5x IB, tests both sides, returns to IB.

Characteristics:

• Two-sided trading

• Extensions occur but don't persist

• Volume balanced throughout day

• Most common day type

Frequency: ~45-50% of trading days

Trading Strategy:

• DO: Take profits at extension levels, expect reversals

• DON'T: Hold for massive moves

• Key: Treat each extension as a profit-taking opportunity

• Risk: Holding too long when momentum shifts

Example: Typical day with no major catalysts—market balancing supply and demand.

3. ROTATION DAY:

Definition: Price stays within IB all day, rotating between high and low.

Characteristics:

• Never accepts outside IB

• Multiple tests of IB high/low

• Decreasing volume (no conviction)

• Classic range-bound action

Frequency: ~25-30% of trading days

Trading Strategy:

• DO: Fade extremes (sell IB high, buy IB low)

• DON'T: Chase breakouts

• Key: Enter at extremes with tight stops just outside IB

• Risk: Breakout finally occurs after multiple failures

Example: [/b> Pre-holiday trading, summer doldrums, consolidation after big move.

4. DEVELOPING:

Definition: Day type not yet determined (early in session).

Usage: Classification before 12:00 PM ET when IB extension pattern unclear.

ORB Fusion's Classification Algorithm:

```pinescript

if close > ibHigh:

ibExtension = (close - ibHigh) / ibRange

direction = "BULLISH"

else if close < ibLow:

ibExtension = (ibLow - close) / ibRange

direction = "BEARISH"

if ibExtension >= 1.5:

dayType = "TREND DAY"

else if ibExtension >= 0.5:

dayType = "NORMAL DAY"

else if close within IB:

dayType = "ROTATION DAY"

```

Why Classification Matters:

Same setup (bullish ORB breakout) has opposite implications:

• Trend Day : Hold for 2.0x extension, trail stops aggressively

• Normal Day : Take profits at 1.0x extension, watch for reversal

• Rotation Day : Fade the breakout immediately (likely false)

Knowing day type prevents catastrophic errors like fading a trend day or holding through rotation.

🚀 BREAKOUT DETECTION & CONFIRMATION

Three Confirmation Methods:

1. Close Beyond Level (Recommended):

Logic: Candle must close above ORB high (bull) or below ORB low (bear).

Why:

• Filters out wicks (temporary liquidity grabs)

• Ensures sustained acceptance above/below range

• Reduces false breakout rate by ~20-30%

Example:

• ORB High: 5850.00

• Bar high touches 5850.50 (wick above)

• Bar closes at 5848.00 (inside range)

• Result: NO breakout signal

vs.

• Bar high touches 5850.50

• Bar closes at 5851.00 (outside range)

• Result: BREAKOUT signal confirmed

Trade-off: Slightly delayed entry (wait for close) but much higher reliability.

2. Wick Beyond Level:

Logic: [/b> Any touch of ORB high/low triggers breakout.

Why:

• Earliest possible entry

• Captures aggressive momentum moves

Risk:

• High false breakout rate (60-70%)

• Stop runs trigger signals

• Requires very tight stops (difficult to manage)

Use Case: Scalping with 1-2 point profit targets where any penetration = trade.

3. Body Beyond Level:

Logic: [/b> Candle body (close vs open) must be entirely outside range.

Why:

• Strictest confirmation

• Ensures directional conviction (not just momentum)

• Lowest false breakout rate

Example: Trade-off: [/b> Very conservative—misses some valid breakouts but rarely triggers on false ones.

Volume Confirmation Layer:

All confirmation methods can require volume validation:

Volume Multiplier Logic: Rationale: [/b> True breakouts are driven by institutional activity (large size). Volume spike confirms real conviction vs. stop-run manipulation.

Statistical Impact: [/b>

• Breakouts with volume confirmation: ~65% success rate

• Breakouts without volume: ~45% success rate

• Difference: 20 percentage points edge

Implementation Note: [/b>

Volume confirmation adds complexity—you'll miss breakouts that work but lack volume. However, when targeting 1.5x+ extensions (ambitious goals), volume confirmation becomes critical because those moves require sustained institutional participation.

Recommended Settings by Strategy: [/b>

Scalping (1-2 point targets): [/b>

• Method: Close

• Volume: OFF

• Rationale: Quick in/out doesn't need perfection

Intraday Swing (5-10 point targets): [/b>

• Method: Close

• Volume: ON (1.5x multiplier)

• Rationale: Balance reliability and opportunity

Position Trading (full-day holds): [/b>

• Method: Body

• Volume: ON (2.0x multiplier)

• Rationale: Must be certain—large stops require high win rate

🔥 FAILED BREAKOUT SYSTEM

The Core Insight: [/b>

Failed breakouts are often more profitable [/b> than successful breakouts because they create trapped traders with predictable behavior.

Failed Breakout Definition: [/b>

A breakout that:

1. Initially penetrates ORB level with confirmation

2. Attracts participants (volume spike, momentum)

3. Fails to extend (stalls or immediately reverses)

4. Returns inside ORB range within N bars

Psychology of Failure: [/b>

When breakout fails:

• Breakout buyers are trapped [/b>: Bought at ORB high, now underwater

• Early longs reduce: Take profit, fearful of reversal

• Shorts smell blood: See failed breakout as reversal signal

• Result: Cascade of selling as trapped bulls exit + new shorts enter

Mirror image for failed bearish breakouts (trapped shorts cover + new longs enter).

Failure Detection Parameters: [/b>

1. Failure Confirmation Bars (default: 3): [/b>

How many bars after breakout to confirm failure?

Logic: Settings: [/b>

• 2 bars: Aggressive failure detection (more signals, more false failures)

• 3 bars Balanced (default)

• 5-10 bars: Conservative (wait for clear reversal)

Why This Matters:

Too few bars: You call "failed breakout" when price is just consolidating before next leg.

Too many bars: You miss the reversal entry (price already back in range).

2. Failure Buffer (default: 0.1 ATR): [/b>

How far inside ORB must price return to confirm failure?

Formula: Why Buffer Matters: clear rejection [/b> (not just hovering at level).

Settings: [/b>

• 0.0 ATR: No buffer, immediate failure signal

• 0.1 ATR: Small buffer (default) - filters noise

• [b>0.2-0.3 ATR: Large buffer - only dramatic failures count

Example: Reversal Entry System: [/b>

When failure confirmed, system generates complete reversal trade:

For Failed Bull Breakout (Short Reversal): [/b>

Entry: [/b> Current close when failure confirmed

Stop Loss: [/b> Extreme high since breakout + 0.10 ATR padding

Target 1: [/b> ORB High - (ORB Range × 0.5)

Target 2: Target 3: [/b> ORB High - (ORB Range × 1.5)

Example:

• ORB High: 5850, ORB Low: 5842, Range: 8 points

• Breakout to 5853, fails, reverses to 5848 (entry)

• Stop: 5853 + 1 = 5854 (6 point risk)

• T1: 5850 - 4 = 5846 (-2 points, 1:3 R:R)

• T2: 5850 - 8 = 5842 (-6 points, 1:1 R:R)

• T3: 5850 - 12 = 5838 (-10 points, 1.67:1 R:R)

[b>Why These Targets? [/b>

• T1 (0.5x ORB below high): Trapped bulls start panic

• T2 (1.0x ORB = ORB Mid): Major retracement, momentum fully reversed

• T3 (1.5x ORB): Reversal extended, now targeting opposite side

Historical Performance: [/b>

Failed breakout reversals in ORB Fusion's tracking system show:

• Win Rate: 65-75% (significantly higher than initial breakouts)

• Average Winner: 1.2x ORB range

• Average Loser: 0.5x ORB range (protected by stop at extreme)

• Expectancy: Strongly positive even with <70% win rate

Why Failed Breakouts Outperform: [/b>

1. Information Advantage: You now know what price did (failed to extend). Initial breakout trades are speculative; reversal trades are reactive to confirmed failure.

2. Trapped Participant Pressure: Every trapped bull becomes a seller. This creates sustained pressure.

3. Stop Loss Clarity: Extreme high is obvious stop (just beyond recent high). Breakout trades have ambiguous stops (ORB mid? Recent low? Too wide or too tight).

4. Mean Reversion Edge: Failed breakouts return to value (ORB mid). Initial breakouts try to escape value (harder to sustain).

Critical Insight: [/b>

"The best trade is often the one that trapped everyone else."

Failed breakouts create asymmetric opportunity because you're trading against [/b> trapped participants rather than with [/b> them. When you see a failed breakout signal, you're seeing real-time evidence that the market rejected directional conviction—that's exploitable.

📐 FIBONACCI EXTENSION SYSTEM

Six Extension Levels: [/b>

Extensions project how far price will travel after ORB breakout. Based on Fibonacci ratios + empirical market behavior.

1. 1.272x (27.2% Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.272)

Psychology: [/b> Initial probe beyond ORB. Early momentum + trapped shorts (on bull side) covering.

Probability of Reach: [/b> ~75-80% after confirmed breakout

Trading: [/b>

• First resistance/support after breakout

• Partial profit target (take 30-50% off)

• Watch for rejection here (could signal failure in progress)

Why 1.272? [/b> Related to harmonic patterns (1.272 is √1.618). Empirically, markets often stall at 25-30% extension before deciding whether to continue or fail.

2. 1.5x (50% Extension):

Formula: [/b> ORB High/Low + (ORB Range × 0.5)

Psychology: [/b> Breakout gaining conviction. Requires sustained buying/selling (not just momentum spike).

Probability of Reach: [/b> ~60-65% after confirmed breakout

Trading: [/b>

• Major partial profit (take 50-70% off)

• Move stops to breakeven

• Trail remaining position

Why 1.5x? [/b> Classic halfway point to 2.0x. Markets often consolidate here before final push. If day type is "Normal," this is likely the high/low for the day.

3. 1.618x (Golden Ratio Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.618)

Psychology: [/b> Strong directional day. Institutional conviction + retail FOMO.

Probability of Reach: [/b> ~45-50% after confirmed breakout

Trading: [/b>

• Final partial profit (close 80-90%)

• Trail remainder with wide stop (allow breathing room)

Why 1.618? [/b> Fibonacci golden ratio. Appears consistently in market geometry. When price reaches 1.618x extension, move is "mature" and reversal risk increases.

4. 2.0x (100% Extension): [/b>

Formula: ORB High/Low + (ORB Range × 1.0)

Psychology: [/b> Trend day confirmed. Opening range completely duplicated.

Probability of Reach: [/b> ~30-35% after confirmed breakout

Trading: Why 2.0x? [/b> Psychological level—range doubled. Also corresponds to typical daily ATR in many instruments (opening range ~ 0.5 ATR, daily range ~ 1.0 ATR).

5. 2.618x (Super Extension):

Formula: [/b> ORB High/Low + (ORB Range × 1.618)

Psychology: [/b> Parabolic move. News-driven or squeeze.

Probability of Reach: [/b> ~10-15% after confirmed breakout

[b>Trading: Why 2.618? [/b> Fibonacci ratio (1.618²). Rare to reach—when it does, move is extreme. Often precedes multi-day consolidation or reversal.

6. 3.0x (Extreme Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 2.0)

Psychology: [/b> Market melt-up/crash. Only in extreme events.

[b>Probability of Reach: [/b> <5% after confirmed breakout

Trading: [/b>

• Close immediately if reached

• These are outlier events (black swans, flash crashes, squeeze-outs)

• Holding for more is greed—take windfall profit

Why 3.0x? [/b> Triple opening range. So rare it's statistical noise. When it happens, it's headline news.

Visual Example:

ES futures, ORB 5842-5850 (8 point range), Bullish breakout:

• ORB High : 5850.00 (entry zone)

• 1.272x : 5850 + 2.18 = 5852.18 (first resistance)

• 1.5x : 5850 + 4.00 = 5854.00 (major target)

• 1.618x : 5850 + 4.94 = 5854.94 (strong target)

• 2.0x : 5850 + 8.00 = 5858.00 (trend day)

• 2.618x : 5850 + 12.94 = 5862.94 (extreme)

• 3.0x : 5850 + 16.00 = 5866.00 (parabolic)

Profit-Taking Strategy:

Optimal scaling out at extensions:

• Breakout entry at 5850.50

• 30% off at 1.272x (5852.18) → +1.68 points

• 40% off at 1.5x (5854.00) → +3.50 points

• 20% off at 1.618x (5854.94) → +4.44 points

• 10% off at 2.0x (5858.00) → +7.50 points

[b>Average Exit: Conclusion: [/b> Scaling out at extensions produces 40% higher expectancy than holding for home runs.

📊 GAP ANALYSIS & FILL PSYCHOLOGY

[b>Gap Definition: [/b>

Price discontinuity between previous close and current open:

• Gap Up : Open > Previous Close + noise threshold (0.1 ATR)

• Gap Down : Open < Previous Close - noise threshold

Why Gaps Matter: [/b>

Gaps represent unfilled orders [/b>. When market gaps up, all limit buy orders between yesterday's close and today's open are never filled. Those buyers are "left behind." Psychology: they wait for price to return ("fill the gap") so they can enter. This creates magnetic pull [/b> toward gap level.

Gap Fill Statistics (Empirical): [/b>

• Gaps <0.5% [/b>: 85-90% fill within same day

• Gaps 0.5-1.0% [/b>: 70-75% fill within same day, 90%+ within week

• Gaps >1.0% [/b>: 50-60% fill within same day (major news often prevents fill)

Gap Fill Strategy: [/b>

Setup 1: Gap-and-Go

Gap opens, extends away from gap (doesn't fill).

• ORB confirms direction away from gap

• Trade WITH ORB breakout direction

• Expectation: Gap won't fill today (momentum too strong)

Setup 2: Gap-Fill Fade

Gap opens, but fails to extend. Price drifts back toward gap.

• ORB breakout TOWARD gap (not away)

• Trade toward gap fill level

• Target: Previous close (gap fill complete)

Setup 3: Gap-Fill Rejection

Gap fills (touches previous close) then rejects.

• ORB breakout AWAY from gap after fill

• Trade away from gap direction

• Thesis: Gap filled (orders executed), now resume original direction

[b>Example: Scenario A (Gap-and-Go):

• ORB breaks upward to $454 (away from gap)

• Trade: LONG breakout, expect continued rally

• Gap becomes support ($452)

Scenario B (Gap-Fill):

• ORB breaks downward through $452.50 (toward gap)

• Trade: SHORT toward gap fill at $450.00

• Target: $450.00 (gap filled), close position

Scenario C (Gap-Fill Rejection):

• Price drifts to $450.00 (gap filled) early in session

• ORB establishes $450-$451 after gap fill

• ORB breaks upward to $451.50

• Trade: LONG breakout (gap is filled, now resume rally)

ORB Fusion Integration: [/b>

Dashboard shows:

• Gap type (Up/Down/None)

• Gap size (percentage)

• Gap fill status (Filled ✓ / Open)

This informs setup confidence:

• ORB breakout AWAY from unfilled gap: +10% confidence (gap becomes support/resistance)

• ORB breakout TOWARD unfilled gap: -10% confidence (gap fill may override ORB)

[b>📈 VWAP & INSTITUTIONAL BIAS [/b>

[b>Volume-Weighted Average Price (VWAP): [/b>

Average price weighted by volume at each price level. Represents true "average" cost for the day.

[b>Calculation: Institutional Benchmark [/b>: Institutions (mutual funds, pension funds) use VWAP as performance benchmark. If they buy above VWAP, they underperformed; below VWAP, they outperformed.

2. [b>Algorithmic Target [/b>: Many algos are programmed to buy below VWAP and sell above VWAP to achieve "fair" execution.

3. [b>Support/Resistance [/b>: VWAP acts as dynamic support (price above) or resistance (price below).

[b>VWAP Bands (Standard Deviations): [/b>

• [b>1σ Band [/b>: VWAP ± 1 standard deviation

- Contains ~68% of volume

- Normal trading range

- Bounces common

• [b>2σ Band [/b>: VWAP ± 2 standard deviations

- Contains ~95% of volume

- Extreme extension

- Mean reversion likely

ORB + VWAP Confluence: [/b>

Highest-probability setups occur when ORB and VWAP align:

Bullish Confluence: [/b>

• ORB breakout upward (bullish signal)

• Price above VWAP (institutional buying)

• Confidence boost: +15%

Bearish Confluence: [/b>

• ORB breakout downward (bearish signal)

• Price below VWAP (institutional selling)

• Confidence boost: +15%

[b>Divergence Warning:

• ORB breakout upward BUT price below VWAP

• Conflict: Breakout says "buy," VWAP says "sell"

• Confidence penalty: -10%

• Interpretation: Retail buying but institutions not participating (lower quality breakout)

📊 MOMENTUM CONTEXT SYSTEM

[b>Innovation: Candle Coloring by Position

Rather than fixed support/resistance lines, ORB Fusion colors candles based on their [b>relationship to ORB :

[b>Three Zones: [/b>

1. Inside ORB (Blue Boxes): [/b>

[b>Calculation:

• Darker blue: Near extremes of ORB (potential breakout imminent)

• Lighter blue: Near ORB mid (consolidation)

[b>Trading: [/b> Coiled spring—await breakout.

[b>2. Above ORB (Green Boxes):

[b>Calculation: 3. Below ORB (Red Boxes):

Mirror of above ORB logic.

[b>Special Contexts: [/b>

[b>Breakout Bar (Darkest Green/Red): [/b>

The specific bar where breakout occurs gets maximum color intensity regardless of distance. This highlights the pivotal moment.

[b>Failed Breakout Bar (Orange/Warning): [/b>

When failed breakout is confirmed, that bar gets orange/warning color. Visual alert: "reversal opportunity here."

[b>Near Extension (Cyan/Magenta Tint): [/b>

When price is within 0.5 ATR of an extension level, candle gets tinted cyan (bull) or magenta (bear). Indicates "target approaching—prepare to take profit."

[b>Why Visual Context? [/b>

Traditional indicators show lines. ORB Fusion shows [b>context-aware momentum [/b>. Glance at chart:

• Lots of blue? Consolidation day (fade extremes).

• Progressive green? Trend day (follow).

• Green then orange? Failed breakout (reversal setup).

This visual language communicates market state instantly—no interpretation needed.

🎯 TRADE SETUP GENERATION & GRADING [/b>

[b>Algorithmic Setup Detection: [/b>

ORB Fusion continuously evaluates market state and generates current best trade setup with:

• Action (LONG / SHORT / FADE HIGH / FADE LOW / WAIT)

• Entry price

• Stop loss

• Three targets

• Risk:Reward ratio

• Confidence score (0-100)

• Grade (A+ to D)

[b>Setup Types: [/b>

[b>1. ORB LONG (Bullish Breakout): [/b>

[b>Trigger: [/b>

• Bullish ORB breakout confirmed

• Not failed

[b>Parameters:

• Entry: Current close

• Stop: ORB mid (protects against failure)

• T1: ORB High + 0.5x range (1.5x extension)

• T2: ORB High + 1.0x range (2.0x extension)

• T3: ORB High + 1.618x range (2.618x extension)

[b>Confidence Scoring:

[b>Trigger: [/b>

• Bearish breakout occurred

• Failed (returned inside ORB)

[b>Parameters: [/b>

• Entry: Close when failure confirmed

• Stop: Extreme low since breakout + 0.10 ATR

• T1: ORB Low + 0.5x range

• T2: ORB Low + 1.0x range (ORB mid)

• T3: ORB Low + 1.5x range

[b>Confidence Scoring:

[b>Trigger:

• Inside ORB

• Close > ORB mid (near high)

[b>Parameters: [/b>

• Entry: ORB High (limit order)

• Stop: ORB High + 0.2x range

• T1: ORB Mid

• T2: ORB Low

[b>Confidence Scoring: [/b>

Base: 40 points (lower base—range fading is lower probability than breakout/reversal)

[b>Use Case: [/b> Rotation days. Not recommended on normal/trend days.

[b>6. FADE LOW (Range Trade):

Mirror of FADE HIGH.

[b>7. WAIT:

[b>Trigger: [/b>

• ORB not complete yet OR

• No clear setup (price in no-man's-land)

[b>Action: [/b> Observe, don't trade.

[b>Confidence: [/b> 0 points

[b>Grading System:

```

Confidence → Grade

85-100 → A+

75-84 → A

65-74 → B+

55-64 → B

45-54 → C

0-44 → D

```

[b>Grade Interpretation: [/b>

• [b>A+ / A: High probability setup. Take these trades.

• [b>B+ / B [/b>: Decent setup. Trade if fits system rules.

• [b>C [/b>: Marginal setup. Only if very experienced.

• [b>D [/b>: Poor setup or no setup. Don't trade.

[b>Example Scenario: [/b>

ES futures:

• ORB: 5842-5850 (8 point range)

• Bullish breakout to 5851 confirmed

• Volume: 2.0x average (confirmed)

• VWAP: 5845 (price above VWAP ✓)

• Day type: Developing (too early, no bonus)

• Gap: None

[b>Setup: [/b>

• Action: LONG

• Entry: 5851

• Stop: 5846 (ORB mid, -5 point risk)

• T1: 5854 (+3 points, 1:0.6 R:R)

• T2: 5858 (+7 points, 1:1.4 R:R)

• T3: 5862.94 (+11.94 points, 1:2.4 R:R)

[b>Confidence: LONG with 55% confidence.