Tìm kiếm tập lệnh với "bar"

Internal Bar Strength IndicatorThe internal bar strength or (IBS) is an oscillating indicator which measures the relative position of the close price with respect to the low to high range for the same period.

YK Fuller BarsThe script highlights "Fuller's pins" and generates alerts when these bars are appearing

Higher Resolution Bars on Intraday ChartHi everybody!

With new plotbar and plotcandle functions you may plot somewhat "stretched" daily bars over intraday chart. Enjoy!

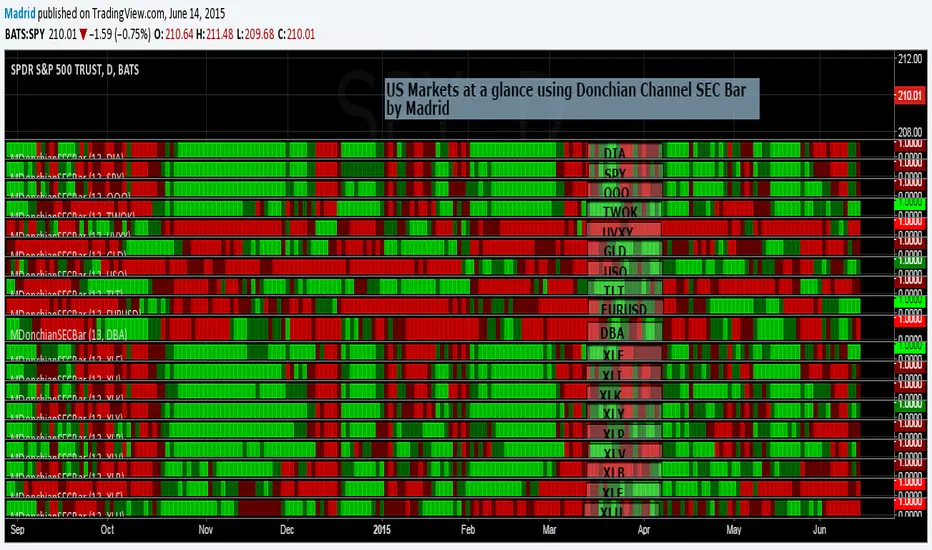

Madrid Donchian SEC barThis study is based on the Donchain Channel Bar indicator but this adds security as a parameter. This allows several instances of this indicator to be used in the same page to create a heat map to take look at a glance at several securities, just like the example where this was implemented.

The only two parameters it requires are the security symbol and the length of the analysis.

Madrid MA Ribbon BarThis study is the companion of the MMAR, displayed here in this publication. This displays the same information as MMAR, but in a linear format. This measures the possibilities of a trend reversal. If the bar fills over 50% of the opposite color from bottom to top then chances are there will be a trend reversal. Otherwise it is just a reentry point.

This study doesn't require but one parameter, and the default is very good. Define if you want to use the standard or the exponential moving average. It is simple, easy to interpret and doesn't require much space on the screen.

It uses only four standard colors

1. Red : A downtrend in progress

2. Green: A short reentry or a trend reversal warning

3. Lime : An uptrend in progress

4. Maroon: A long reentry or a trend reversal warning

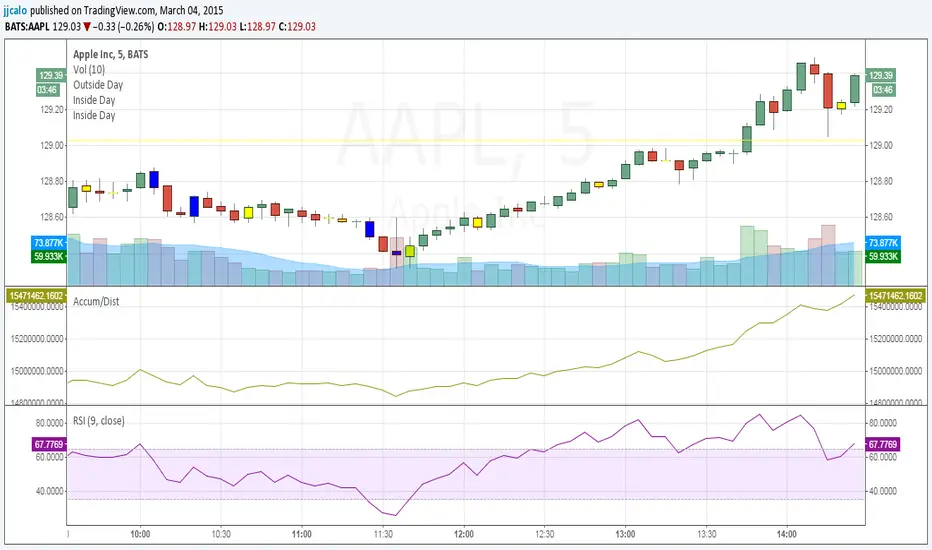

jc-Inside_BarCopyright by jack calo -- v1.0 -- 03/04/2015 -- Paint the bar yellow when it's an inside day. When the full range of a candle is equal or within the full range of the previous bar. Credit to Rob Smith and his In The Black Strategy.

Over ATR Bar highlightScript highlights bars over ATR (20), i use this to look for mazabuzo candles.

FVE Volatility color-coded Volume bar The FVE is a pure volume indicator. Unlike most of the other indicators

(except OBV), price change doesn?t come into the equation for the FVE

(price is not multiplied by volume), but is only used to determine whether

money is flowing in or out of the stock. This is contrary to the current trend

in the design of modern money flow indicators. The author decided against a

price-volume indicator for the following reasons:

- A pure volume indicator has more power to contradict.

- The number of buyers or sellers (which is assessed by volume) will be the same,

regardless of the price fluctuation.

- Price-volume indicators tend to spike excessively at breakouts or breakdowns.

This study is an addition to FVE indicator. Indicator plots different-coloured volume

bars depending on volatility.

Custom Indicator Clearly Shows If Bulls or Bears are in Control!The Two Versions of this Indicator I learned from Two Famous and Highly Successful Traders. This Indicator shows With No Lag Clear Up and Down Trends in Market by Documenting Clearly If Bulls or Bears are in Control. The Version In SubChart 1 Shows Consecutive Closes if the Current Close is Greater than of Less than the Midpoint of the Previous Bar (Why Midpoint Explained in Detail in 1st Post). The Version in SubChart 2 Shows Consecutive Closes that are Greater than or Less Than the Previous Close (Will Discuss Specific Uses in 1st Post). Works on Stocks, Forex, Futures, on All Timeframes.

VWAP filtered MACD Bars with positive MACD histogram value and closing above VWAP are colored, long positions should be taken in areas made of those bars.

Similarly, bars with negative MACD histogram value and closing below VWAP are also colored, short positions should be taken there.

This indicator by default should be a part of your trend following trading system.

In the setting you can change colors

Above grow: positive and rising MACD histogram value

Above fall: positive and falling MACD histogram value

Below fall: negative and falling MACD histogram value

Below grow: negative and rising MACD histogram value

bar color changeThis Pine v5 code allows you to distinguish between candles on the chart. The body/wick/frame of the "live" candle that hasn't yet closed is colored white. When a live candle is present, the body of the immediately preceding candle is colored green with offset = -1. All other candles remain gray (#2e2e2e). plotcandle fixes the wick/frame so that the live and previous candles are selected when following the trend. If there are other conflicting scripts, the most recently added one quickly takes precedence.

Bar RangeI use this to complement the daily ATR bars. It is interesting to see how much the stock has actually moved vs the ATR movement.

MACD Aspray Hybrid Bars (teal/red) = raw momentum (Aspray Histogram).

Teal line = smooth curve of the histogram (Aspray Line).

Orange line = 9-EMA of that line (new signal).

Zero line for reference.

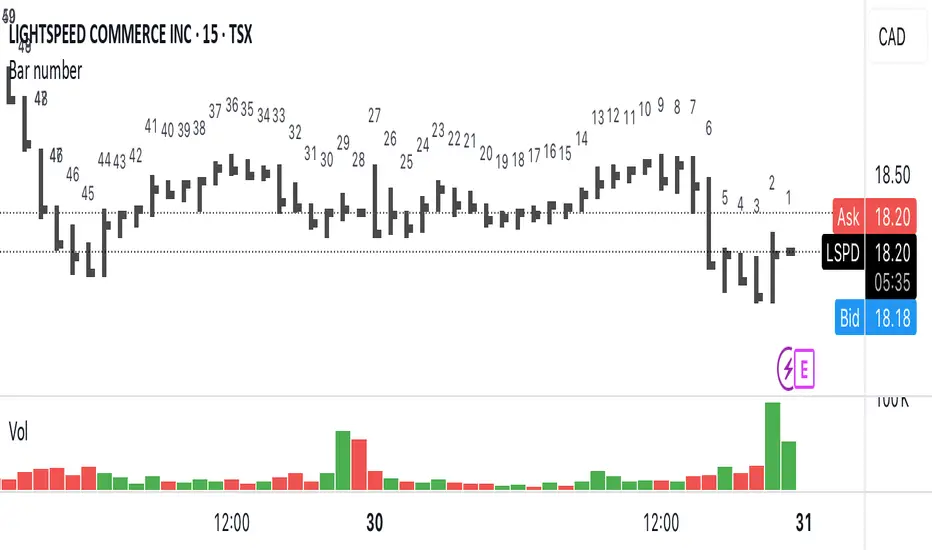

Bar numberAdds a number above the last 50 candles. Candle 1 is always the most recent.

Can be useful when teaching people onlinet. Now they can just ask « what’s candle number 20 » instead of « what’s with that narrow range candle next to the big one to the left… no not that one, the other one »

Bars pattern MLThis script implements a K-Nearest Neighbors (KNN)-based machine learning model to predict future price movements in financial markets. It analyzes past price action using Euclidean distance and selects the most similar historical patterns to estimate future price changes. Unlike traditional KNN implementations, this approach optimizes distance calculations by maintaining a dynamically updated list of the closest neighbors, ensuring efficient selection without the need for sorting. The model generates a forecasted price trajectory based on incremental predictions, which are visualized on the chart using polylines for better interpretability.

Volume HighlightBar colouring: this indicator is simple but effective, it repaints higher than normal candles a certain colour (by default gold/yellow) it helps to know what are valuable areas to trade around for longs and shorts.

Changing the volume multiplier manually helps you to screen volume relevant to the timeframe you are trading on.

For example, some charts 1min the best filter/setting would be 12-35 multiplier where others like btc 1-4 hourly, the filter/setting might be 8-12.

The key is having only the highest/most relevant 3-4 volume candles showing as they often represent supports and resistances.

Pivot Points And Breakout Price Action With LuckyNickVaBar Color Candle Aligned with pivot points swing high and swing lows For Those Who Are Familiar with Trading The Breakouts Of Highs & Lows Of Structure. Pivots are said to be key areas in the market where price shows heavy reaction to where reversals make occur. At these points there are swing Highs & swing lows that traders may be able to find opportunity in the market. This Script is a combination of pivot points and Barcolor signals for the breakout.

Koalafied Volume Extension Bar colours based on extensions from volume Z-Score. Large volume candles can often signal exhaustion or show market strength in reversals or breakouts. Candles not supported by rising volume are coloured black while those that are retain their colouring.