Ultimate Bollinger Bands by @DaviddTechThis strategy uses the Ultimate Bollinger and Aroon indicator.

The logic behind the code is

* Enter long :

Aroon up is below the 20 or lower line in settings.

Aroon down is above 70 or above line in settings.

When close crossover the lower Bollinger Band we take an entry

SL is %

TP is % of if Aroon up is below the 70 or lower line in settings.

Aroon down is above 20 or above line in settings.

When close crossover the upper Bollinger Band

* Short :

Aroon down is below the 20 or lower line in settings.

Aroon up is above 70 or above line in settings.

When close crossunder the upper Bollinger Band we take an entry

SL is %

TP is % of if Aroon up is below the 20 or lower line in settings.

Aroon down is above 70 or above line in settings.

When close crossover the lower Bollinger Band

Settings I used to get the results below :

====================

** Ultimate Bollinger Bands by @DaviddTech **

====================

Enable Repainting? = False

Enable LONG entries? = True

Enable SHORT entries? = True

lengthBB = 20

Source = close

StdDev = 2

Offset = 0

Aroon Length = 14

Aroon Enter upper band = 85

Aroon Enter lower band = 5

Aroon Exit upper band = 70

Aroon Exit lower band = 20

Restrict Entries to Date Range? = False

From : = 1611100800000

To : = 1613779200000

Show Liquadation line (BETA) = False

Leverage Amount = 25

Maintenance Margin Rate = 0.5

Type of Exit / Entry = Enter New Trade Only if NO running Trades

Type of Take Profit = Custom Stoploss

Type of Stoploss = Custom Stoploss

Stop Loss % = 4

Take Profit % = 6

Highest High lookback = 50

Lowest Low Lookback = 60

Profitfactor Long (Risk to Reward) = 2

Profitfactor Short (Risk to Reward) = 0.5

Stoploss Factor: LONG = 4

SHORT = 4

Profit Factor: LONG = 2

SHORT = 2

ATR Length = 11

Length = 200

Source = hlc3

Multiplier = 3

Level = 764

Take Multi Profit X3 = False

% to take at First TP = 33

% to take at Second TP = 33

% to take at Third TP = 100

Use Strategy Alerts? - Please read the tooltip = False

Show S/R Levels = False

Use MFI + RSI = False

RSI Source = close

RSI Length = 14

RSI Oversold = 30

RSI Overbought = 60

MFI Period = 60

MFI Area multiplier = 150

MFI Area Y Pos = 2.5

Use vWap = False

vWap Source = close

vWap2 Source = close

Vwap Length = 3

EMA Breakout = False

EMA Length = 100

Use MTF EMA cross = False

MTF = 5

EMA Period = 5

MTF = 5

EMA Period = 30

WARNING:

- For purpose educate only - My mission is to debunk fake strategies with code to find THE ONE.

- Plots EMAs and other values on chart.

- This script to change bars colors.

If you have any questions or feedback, please let me know in the comments.

Tìm kiếm tập lệnh với "rsi"

3Commas DCA Bot Strategy v1.0Introduction

The strategy attempts to implement a majority all of the settings found on the 3Commas DCA Bot setting page that can be implemented within a TradingView indicator. Specifically, it will implement the "Open new trade ASAP" and "Trading View Custom Signal" deal start conditions. In this way, you can leverage the power of TradingView's backtester to model your settings and analysis past performance as well as leverage TradingView's alert notification subsystem to send Deal Start and Close signals to 3Commas using almost any of the thousands of scripts found in the Public Library (see "What does it do and how does it do it?" section below for more information on how to do this using the RSI indicator as an example).

How is it original and useful?

This strategy is unique in that it's the only one (as of the initial publications) that can handle 28 out of 32 bot settings (88% coverage) that are found on the 3Commas bot settings page. In addition, because it is a TradingView script, you will benefit from the following:

Model your bot's configuration using the backtester on any timeframe and evaluate its performance using the chart's history.

View a table of detailed statistics pertaining to deals started and completed, win/loss rates, daily P&L, true max drawdown, and detailed statistics on bars in deal along with safety orders filled.

View a table of "Used amount for each step" as presented in 3Commas as well.

Ability to link to almost any TradingView chart indicator that provides a single data point for buy/sell signals.

Make use of the 3Commas TA Start Conditions indicator to emulate the 3Commas built-in indicators for further performance evaluation with the backtester.

How does it compare to other scripts in the Public Library?

This strategy offers a very detailed, comprehensive settings and maybe the only one (as of the initial publication) that can handle 28 out of the 32 bot settings that are found on the 3Commas bot settings page (that can be handled within TradingView, because some cannot be modeled due to chart and language constraints). Specifically, the following 3Commas bot settings and inputs are addressed with asterisks denoting specific limitation due to TradingView's platform architecture and/or constraints:

Main settings

✅ Name

❌ Exchange* (Not handled since it is inherited from chart)

⚠ Bot type* (Only Single-pair because you simply apply the indicator to as many pairs you desire in separate charts to simulate a Multi-pair setting)

Pairs

❌ Pairs* (Not handled since it is inheriting the symbol from the chart)

Strategy

✅ Strategy

❌ Profit currency* (Not handled since there is no equivalence in TradingView)

✅ Base order size / unit

✅ Safety order size / unit

✅ Start order type

Deal start condition

⚠ TradingView* (You can modify the "Technical Rating" indicator by TradingView to output a signal yourself like @TheTradingParrot has done in the TV signal for DCA backtest script)

⚠ QFL* (See Quickfingers Luc's Base Breaking Strategy v2.5 - 3Commas Edition for an alternative)

❌ Manually/API* (Not handled since there is no equivalence in TradingView)

✅ Trading View custom signal

✅ Open new trade asap

Take profit

✅ Take profit (%)

✅ Take profit type

✅ Trailing

⚠ Trailing deviation* (modified to handle TradingView's broker emulator properly)

Stop loss

✅ Stop Loss (%)

✅ Stop Loss action

⚠ Stop Loss timeout* (modified to use "bars" as the unit of measure)

Safety orders

✅ Max safety trades count (a total of 100 safety orders are supported!)

⚠ Max active safety trades count* (Not handled since there is no equivalence in TradingView)

✅ Price deviation to open safety orders (% from initial order)

✅ Safety order volume scale

✅ Safety order step scale

Advanced settings

✅ Don't start deal(s) if the daily volume is less than

✅ Minimum price to open deal

✅ Maximum price to open deal

⚠ Deal start delay (QFL and standard TV signals only)* (modified to use "bars" as the unit of measure)

✅ Cooldown between deals

✅ Open deals & stop

Close deal after timeout

⚠ The time after which, deal will be closed automatically* (modified to use "bars" as the unit of measure)

In addition to the above inputs, the script will also support the same output data points that are found on the bot settings page, which are:

Assistant

✅ Balance

✅ Max amount for bot usage (Based on current rate)

✅ Max safety order price deviation

✅ % of available balance to be used by the bot

Table (Used amount for each step)

✅ Order No.

✅ Deviation %

✅ Order Size (Base currency)

✅ Order Volume (Quote currency)

✅ Price

✅ Average price

✅ Required price

✅ Required change

✅ Total Size (Base currency)

✅ Total Volume (Quote currency)

What does it do and how does it do it?

When applied to the chart for the first time, the default settings will work to execute the "Open new trade asap" deal start condition using a take profit of 4%, a base order size of 1.335% of equity (initial capital + net profit), a safety order size of 2.003% of equity (initial capital + net profit), a safety order volume scale of 1.5, a safety order step scale of 1.21, and a max safety trades count of 8. With these settings, as you scroll through the chart's history you should see price action crossing the DCA layers (denoted with blue triangles), and a green take-profit price line will render (with green triangle denoting the crossings). Lastly, in the upper-right corner of the chart the table of DCA statistics will render showing you all the gathered data that took place since the chart's starting history until the current time.

Using the "TV Custom Signal" section will allow you to "link" other chart indicators to supply "Start" and "Close" signals for the script. For example, here's how you can use the standard RSI indicator to generate an entry signal:

1) Add the stock RSI indicator and configure it to your desire.

2) Select the "RSI" indicator in the "Chart/Indicator Data Point" input.

3) Select "Chart/Indicator Data Point" in the "Start Deal When" input.

4) Select "Less Than" in the "Is" input.

5) Select "Custom Value(s)" in the "The Value Of" input.

6) Enter "25" in the "Custom Value 1 (Single or Lower Bound)" input.

7) Select "Trading View Custom Signal" in the "Open new trade" input (in the DEAL START CONDITION section).

8) Lastly, check the checkbox with a horizontal straight line above the "Start Deal When" input.

This means that the indicator will start a deal when the "RSI indicator" is "Less Than" the value of "25".

Strategy Results

The default settings are designed to ensure that the indicator will render chart elements when first loaded as well as to allow the backtester to gather order executions and display performance summary. The chart above is is using $10,000 initial capital, a commission rate of 0.1% for both entries and exits, and a 1 tick slippage setting. It is also using 3.22581% of the equity for the Base Order Size, 6.45161% of equity for the first Safety Order Size. The Maximum Safety Trade Count is 4 with a Safety Order Volume Scale of 2, a Safety Order Step Scale of 1.53, Price Deviation To Option Safety Orders at 5.3, and a take profit of 4.5% with Trailing turned on at a deviation of 1.5%. All other settings are defaults.

It is recommended that the indicator be "tuned" for your specific market in order to best implement the strategy and obtain better desirable results. You do so by using the backtester and statistics table and observe the output values and learn how the indicator is performing in the chart history. Using this information, you can adjust the settings accordingly until you find the settings acceptable to your trading goals and risk tolerance.

Always keep in mind that past performance may not be indicative of future results. Settings that seem favorable for one market may be found to be disastrous in another. Therefore, do take the time needed to understand how the settings will behave with the given chart symbol.

Enjoy! 😊👍

How to obtain access to the script?

You have two choices:

Use the "Website" link below to obtain access to this indicator, or

Send us a private message (PM) in TradingView itself.

Nick Rypock Trailing Reverse (by everget)Hello.

Research (NRTR) from the author (Evergrt) made into strategy.

The idea of the indicator is similar to the Chandelier Exit , but doesn't involve ATR component and uses a percentage instead.

A dynamic price channel is used to calculate the NRTR. The calculations involve only those prices that are included in the current trend and exclude the extremes related to the previous trend. The indicator is always at the same distance (in percent) from the extremes reached by prices (below the maximum peak for the current uptrend, above the minimum bottom for the current downtrend)

I also added filter output, rsi /% output, and backtesting to the strategy. Below in order:

1) Logic entry:

% - distance as a percentage of extreme values

2)Filter settings

If the checkbox is checked, the rsi/wma filter will be used. If at the moment of triggering a buy signal in a long line, the rsi line is under the lower line, then a buy will be made, and if not, ignored. With the short position, on the contrary, the upper line border is responsible for it.

3)Exit settings

-exit by rsi, if the conditions are triggered, but the position is in the red, then there will be no exit.

- percentage output

If there is a tick on the rsi and%, then the position will be closed, which will be the first.

4)Darta range

backtesting for any period of time

Rainbow Strategy BacktestingRainbow Strategy Backtesting base on "Rainbow Moving Average" Strategy as below:

1.Rainbow Moving Average setup

- Source: source of 1st MA

- Type: SMA/EMA

- Period: period of 1st MA

- Displacement: period of 2nd MA to 7th MA with source is previous MA

2.Trend Define

- Up Trend: Main MA moving at the top of Rainbow

- Down Trend: Main MA moving at the bottom of Rainbow

- Sideway: Main MA moving between the top and the bottom of Rainbow

3.Signal

- Buy Signal: When Rainbow change to Up Trend.

- Sell Signal: When Rainbow change to Down Trend.

- Exit: When Rainbow change to Sideway.

4.RSI Filter

- "Enable": Only signals have 1st RSI moving between Overbought and Oversold and 2nd RSI moving outside Middle Channel are accepted.

- The filter may help trader avoid bull trap, bear trap and choppy market.

5.Backtesting Infomation

- Ticker: BTCUSDT

- Timeframe: H1

- Rainbow parameter:

+ Source: hlc3

+ Type: SMA

+ Period: 12

+ Displacement: 3

- RSI Filter parameter:

+ Enable

+ 1st RSI filter: period 12, overbought 65, oversold 35

+ 2nd RSI filter: period 9, upper middle 56, lower middle 44

3x SuperTrend Strategy (Mel0nTek) V1This is a triple SuperTrend based strategy for lower time frame trades such as day trades and scalping. I have not seen many strategies that combine multiple SuperTrends so I thought I would publish this one since I put it together and have been quite happy with the results. I have found through testing that the best results are on currency exchange markets such as Crypto or Forex on 1-15 min time frames.

The core idea was inspired by a youtube video put out by Trade Pro:

"Trade Pro - HIGHEST PROFIT Triple Supertrend Trading Strategy Proven 100 Trade Results"

I went ahead and set the defaults to the ones he uses in his video for anyone who wants to try a configuration similar to his. They work pretty well in general, however the EMA, SuperTrend ATR multipliers, and P/L ratio can be tuned/optimized to fit the timeframe/market desired. The video is quite good but not a required watch as I will explain below.

The 200EMA is used as a medium-term trend direction indicator.

- Price closing consistently above the 200EMA means that only long positions should be entered.

- Price closing consistently below 200EMA means that only short positions should be entered.

The 3 SuperTrend indicators should be used as direction confirmation for entries. Typically, price above SuperTrend indicates bullish movement, while price below SuperTrend indicates Bearish movement. However by itself, it is not a great indication to enter/exit positions in my experience. By combining 3 of them with slightly longer periods and increased ATR multipliers, we can get much stronger confirmation of trend direction/strength.

The way they are used in this strategy is such that:

- We only want to enter a position if at least 2 out of 3 SuperTrends are on our side.

- 3/3 SuperTrends on our side is the best case, since we are taking trades WITH momentum/price strength.

- The second farthest SuperTrend from entry price is used as a Stop Loss

SuperTrend being on our side is not the only requirement for an entry however. The probability of success is increased with SuperTrend, and a longer EMA on our side, but we want to be sure that we aren't getting in too late/after the movement has already happened.

So we use Stoch RSI to pick our entries where price is oversold/overbought and reversing. That means the Stoch RSI is above 80, or below 20, and our indication to enter the trade is when the 2 lines cross/begin reversing direction.

So with trend direction on our side, we can get really good entries at these oversold/overbought extremes, especially as it's reversing (Stoch RSI K and D are crossing). This allows us to use the SuperTrend as a support/stop loss on our entry since price should be above it.

Then we just target 1.5x our max loss so that even if we only win 50% of the time, we still make a profit.

The explicit rules of this strategy are as follows:

=== Rules ===

long only

- price above EMA200

short only

- price below EMA200

Stop Loss = 2nd SuperTrend line above (short) or below(long) entry candle

Profit = 1.5x SL/risk (Profit Ratio x Max Loss)

=== Entry Setup ===

LONG

- Stoch RSI below 20, cross up

- at least 2 SuperTrend lines below close

SHORT

- Stoch RSI above 80, cross down

- at least 2 SuperTrend lines above close

P.S. Special thanks to Trade Pro for producing so many quality videos, putting strategy claims to the test, and providing me with so many good ideas I apply to my own strategies.

Bot go_up strategyHello. This strategy is based on go_up alerts.

Our task is to find the local minimum. The trade is entered on the basis of RSI and SMA according to a specific formula, which is embedded in the code. When the RSI crosses the SMA upside down, a long position is entered. You can change the length of the RSI . The longer the length, the less frequent, but more accurate the entrance, and vice versa. You can use a different time frame.

The settings have:

1) RSI length, the lower the length, the more often the entry.

2) Testing results for any period of time

3) Take profit for any percentage

4) Stop order for any percentage

5) If there is a check mark ✅, then purchases will always be made, and if not, then purchases will be made, BUT, if the next payback is lower than the previous one, it does not matter by what percentage.

6) If there is a check mark ✅, then each trace of the purchase will be made provided that it is lower by the percentage specified, even if the conditions of the purchase are triggered.

7) The filled area is made for visual display of consolidation zones

Default settings:

RSI length 15, step 1.5, take profit 15, stop order 30.

Also in the settings there is a pyramid of the order, keep this in mind. Enter a deal for a small part of the deposit, and not for all the money at once! You can remove pyramiding and see the results with one entry.

For a more visual understanding, overlay the go_up script.

You can choose a strategy for yourself based on history! If you need examples of strategies, then write to me, my contacts are in the column: instructions from the author.

Successful trades, dear friends, I am glad that you trust me!

stratRsi_MiguelThis strategy was created with the aim of trying to predict upper moves and to protect from falling prices. It is intended to out perform going from bottom to top and to bottom again (ex: BTC from 10k to 20k to 10k again and remain with substancial profit from the rise). It will not outperform from bottom to top. It is advised to do not enter short positions with this strategy. Only long and close.

Adjust "Period in minutes" to your time frame. ex: 60 for 1h, 240 for 4h, 1440 for 1D.

This will adjust the lengh of ema (RSI).

Default value is 1440 for 1D time frame.

Long condition is triggered when a FastEma(RSI) is bigger then a MeddiumEma(RSI), the MeddiumRSI is bigger than the SlowerEma(RSI), the FastRSI is larger then the Highest(FastRSI) with a length equal to input "High Length"(default value=6) and ema(close) is rising.

The short Condition is triggered when rsi(close,14) is lower then lowest(FastRSI) with a lenght equal to input "Low Length" (default value=3) and ema(close) is falling.

You can set up the time range to evaluate the strategy from "Start date" (default: year=2018, month=1, day=1) to "End date" (default: year=2050, month=1, day=1). Default commission=0.075%. Default Initial capital = 100 USD

Jigga - Nifty Bank JuniorHello Investors !!

We have seen many indicators for trading, But I was looking for indicator which can be use for long term investment, which gives less trade and yet result in profit.

1) We know trend is our friend. And best way to be in trend is to follow trend indicator. I have picked RSI to find out trend.

2) It’s difficult to handle volatility of stocks and hence I choose to make indicator which works only on Index. Especially Nifty, BankNifty and Nifty Junior.

Logic is simple

Bullish when RSI level > 55

Bearish when RSI level < 45

In this indicator you can change RSI look back period as per your convenience. Also, you can check back testing output by selecting “Back Testing” option.

General guideline to use this study

1) Use only on Nifty, Bank Nifty, Junior Nifty

2) ‘Daily’ period gives good result.

Please note this study may not be useful for Trading purpose. Kindly request to check RSI related others study on Trading View.

Happy Investing!!

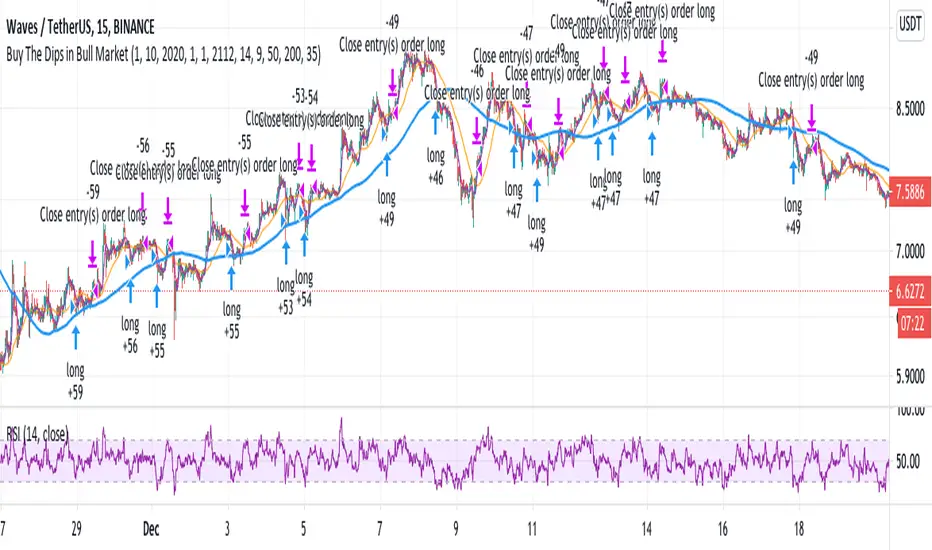

Buy The Dips in Bull Market (by Coinrule)During a Bull market, beating the market, it's challenging. Trading strategies that buy the dips represent one of the best approaches to surf the trend and optimize the returns.

The main obstacle is to gauge the dip's magnitude properly and set up the take profit level accordingly. The RSI is an excellent tool to catch price drops as it adjusts the entry to the asset's current volatility. Nevertheless, using the RSI as an indicator for exit is not an optimal solution in trending markets as it may end up with two scenarios:

The price reverts before reaching overbought conditions. That is the case when the trend is not that strong at that moment. Leaving the position open could result in missed profit opportunities.

The price rebounds strongly, leading the RSI quickly in overbought conditions too soon so that the strategy sells too early.

One interesting option is to combine a trigger based on the RSI to catch the dip and then use two moving averages to spot the right time to seel when the price is entirely back on-trend.

The Setup

The entry-signal comes when the RSI is lower than 35 and the MA9 is above the MA200, indicating that the asset is currently in an uptrend.

The sell-signal comes when at the same time, the price is above the MA9, and the MA9 is above the MA50.

This setup was optimized on the 15-min time frame after over 150 backtests.

A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

888 BOT #backtest█ 888 BOT #backtest (open source)

This is an Expert Advisor 'EA' or Automated trading script for ‘longs’ and ‘shorts’, which uses only a Take Profit or, in the worst case, a Stop Loss to close the trade.

It's a much improved version of the previous ‘Repanocha’. It doesn`t use 'Trailing Stop' or 'security()' functions (although using a security function doesn`t mean that the script repaints) and all signals are confirmed, therefore the script doesn`t repaint in alert mode and is accurate in backtest mode.

Apart from the previous indicators, some more and other functions have been added for Stop-Loss, re-entry and leverage.

It uses 8 indicators, (many of you already know what they are, but in case there is someone new), these are the following:

1. Jurik Moving Average

It's a moving average created by Mark Jurik for professionals which eliminates the 'lag' or delay of the signal. It's better than other moving averages like EMA , DEMA , AMA or T3.

There are two ways to decrease noise using JMA . Increasing the 'LENGTH' parameter will cause JMA to move more slowly and therefore reduce noise at the expense of adding 'lag'

The 'JMA LENGTH', 'PHASE' and 'POWER' parameters offer a way to select the optimal balance between 'lag' and over boost.

Green: Bullish , Red: Bearish .

2. Range filter

Created by Donovan Wall, its function is to filter or eliminate noise and to better determine the price trend in the short term.

First, a uniform average price range 'SAMPLING PERIOD' is calculated for the filter base and multiplied by a specific quantity 'RANGE MULTIPLIER'.

The filter is then calculated by adjusting price movements that do not exceed the specified range.

Finally, the target ranges are plotted to show the prices that will trigger the filter movement.

Green: Bullish , Red: Bearish .

3. Average Directional Index ( ADX Classic) and ( ADX Masanakamura)

It's an indicator designed by Welles Wilder to measure the strength and direction of the market trend. The price movement is strong when the ADX has a positive slope and is above a certain minimum level 'ADX THRESHOLD' and for a given period 'ADX LENGTH'.

The green color of the bars indicates that the trend is bullish and that the ADX is above the level established by the threshold.

The red color of the bars indicates that the trend is down and that the ADX is above the threshold level.

The orange color of the bars indicates that the price is not strong and will surely lateralize.

You can choose between the classic option and the one created by a certain 'Masanakamura'. The main difference between the two is that in the first it uses RMA () and in the second SMA () in its calculation.

4. Parabolic SAR

This indicator, also created by Welles Wilder, places points that help define a trend. The Parabolic SAR can follow the price above or below, the peculiarity that it offers is that when the price touches the indicator, it jumps to the other side of the price (if the Parabolic SAR was below the price it jumps up and vice versa) to a distance predetermined by the indicator. At this time the indicator continues to follow the price, reducing the distance with each candle until it is finally touched again by the price and the process starts again. This procedure explains the name of the indicator: the Parabolic SAR follows the price generating a characteristic parabolic shape, when the price touches it, stops and turns ( SAR is the acronym for 'stop and reverse'), giving rise to a new cycle. When the points are below the price, the trend is up, while the points above the price indicate a downward trend.

5. RSI with Volume

This indicator was created by LazyBear from the popular RSI .

The RSI is an oscillator-type indicator used in technical analysis and also created by Welles Wilder that shows the strength of the price by comparing individual movements up or down in successive closing prices.

LazyBear added a volume parameter that makes it more accurate to the market movement.

A good way to use RSI is by considering the 50 'RSI CENTER LINE' centerline. When the oscillator is above, the trend is bullish and when it is below, the trend is bearish .

6. Moving Average Convergence Divergence ( MACD ) and ( MAC-Z )

It was created by Gerald Appel. Subsequently, the histogram was added to anticipate the crossing of MA. Broadly speaking, we can say that the MACD is an oscillator consisting of two moving averages that rotate around the zero line. The MACD line is the difference between a short moving average 'MACD FAST MA LENGTH' and a long moving average 'MACD SLOW MA LENGTH'. It's an indicator that allows us to have a reference on the trend of the asset on which it is operating, thus generating market entry and exit signals.

We can talk about a bull market when the MACD histogram is above the zero line, along with the signal line, while we are talking about a bear market when the MACD histogram is below the zero line.

There is the option of using the MAC-Z indicator created by LazyBear, which according to its author is more effective, by using the parameter VWAP ( volume weighted average price ) 'Z-VWAP LENGTH' together with a standard deviation 'STDEV LENGTH' in its calculation.

7. Volume Condition

Volume indicates the number of participants in this war between bulls and bears, the more volume the more likely the price will move in favor of the trend. A low trading volume indicates a lower number of participants and interest in the instrument in question. Low volumes may reveal weakness behind a price movement.

With this condition, those signals whose volume is less than the volume SMA for a period 'SMA VOLUME LENGTH' multiplied by a factor 'VOLUME FACTOR' are filtered. In addition, it determines the leverage used, the more volume , the more participants, the more probability that the price will move in our favor, that is, we can use more leverage. The leverage in this script is determined by how many times the volume is above the SMA line.

The maximum leverage is 8.

8. Bollinger Bands

This indicator was created by John Bollinger and consists of three bands that are drawn superimposed on the price evolution graph.

The central band is a moving average, normally a simple moving average calculated with 20 periods is used. ('BB LENGTH' Number of periods of the moving average)

The upper band is calculated by adding the value of the simple moving average X times the standard deviation of the moving average. ('BB MULTIPLIER' Number of times the standard deviation of the moving average)

The lower band is calculated by subtracting the simple moving average X times the standard deviation of the moving average.

the band between the upper and lower bands contains, statistically, almost 90% of the possible price variations, which means that any movement of the price outside the bands has special relevance.

In practical terms, Bollinger bands behave as if they were an elastic band so that, if the price touches them, it has a high probability of bouncing.

Sometimes, after the entry order is filled, the price is returned to the opposite side. If price touch the Bollinger band in the same previous conditions, another order is filled in the same direction of the position to improve the average entry price, (% MINIMUM BETTER PRICE ': Minimum price for the re-entry to be executed and that is better than the price of the previous position in a given %) in this way we give the trade a chance that the Take Profit is executed before. The downside is that the position is doubled in size. 'ACTIVATE DIVIDE TP': Divide the size of the TP in half. More probability of the trade closing but less profit.

█ STOP LOSS and RISK MANAGEMENT.

A good risk management is what can make your equity go up or be liquidated.

The % risk is the percentage of our capital that we are willing to lose by operation. This is recommended to be between 1-5%.

% Risk: (% Stop Loss x % Equity per trade x Leverage) / 100

First the strategy is calculated with Stop Loss, then the risk per operation is determined and from there, the amount per operation is calculated and not vice versa.

In this script you can use a normal Stop Loss or one according to the ATR. Also activate the option to trigger it earlier if the risk percentage is reached. '% RISK ALLOWED'

'STOP LOSS CONFIRMED': The Stop Loss is only activated if the closing of the previous bar is in the loss limit condition. It's useful to prevent the SL from triggering when they do a ‘pump’ to sweep Stops and then return the price to the previous state.

█ BACKTEST

The objective of the Backtest is to evaluate the effectiveness of our strategy. A good Backtest is determined by some parameters such as:

- RECOVERY FACTOR: It consists of dividing the 'net profit' by the 'drawdown’. An excellent trading system has a recovery factor of 10 or more; that is, it generates 10 times more net profit than drawdown.

- PROFIT FACTOR: The ‘Profit Factor’ is another popular measure of system performance. It's as simple as dividing what win trades earn by what loser trades lose. If the strategy is profitable then by definition the 'Profit Factor' is going to be greater than 1. Strategies that are not profitable produce profit factors less than one. A good system has a profit factor of 2 or more. The good thing about the ‘Profit Factor’ is that it tells us what we are going to earn for each dollar we lose. A profit factor of 2.5 tells us that for every dollar we lose operating we will earn 2.5.

- SHARPE: (Return system - Return without risk) / Deviation of returns.

When the variations of gains and losses are very high, the deviation is very high and that leads to a very poor ‘Sharpe’ ratio. If the operations are very close to the average (little deviation) the result is a fairly high 'Sharpe' ratio. If a strategy has a 'Sharpe' ratio greater than 1 it is a good strategy. If it has a 'Sharpe' ratio greater than 2, it is excellent. If it has a ‘Sharpe’ ratio less than 1 then we don't know if it is good or bad, we have to look at other parameters.

- MATHEMATICAL EXPECTATION: (% winning trades X average profit) + (% losing trades X average loss).

To earn money with a Trading system, it is not necessary to win all the operations, what is really important is the final result of the operation. A Trading system has to have positive mathematical expectation as is the case with this script: ME = (0.87 x 30.74$) - (0.13 x 56.16$) = (26.74 - 7.30) = 19.44$ > 0

The game of roulette, for example, has negative mathematical expectation for the player, it can have positive winning streaks, but in the long term, if you continue playing you will end up losing, and casinos know this very well.

PARAMETERS

'BACKTEST DAYS': Number of days back of historical data for the calculation of the Backtest.

'ENTRY TYPE': For '% EQUITY' if you have $ 10,000 of capital and select 7.5%, for example, your entry would be $ 750 without leverage. If you select CONTRACTS for the 'BTCUSDT' pair, for example, it would be the amount in 'Bitcoins' and if you select 'CASH' it would be the amount in $ dollars.

'QUANTITY (LEVERAGE 1X)': The amount for an entry with X1 leverage according to the previous section.

'MAXIMUM LEVERAGE': It's the maximum allowed multiplier of the quantity entered in the previous section according to the volume condition.

The settings are for Bitcoin at Binance Futures (BTC: USDTPERP) in 15 minutes.

For other pairs and other timeframes, the settings have to be adjusted again. And within a month, the settings will be different because we all know the market and the trend are changing.

HFT Fibonacci Bands BacktesterDefault Settings are meant to be used in XBT/USD chart on 15 min time frame. If you want to use for another asset on another time frame YOU MUST CHANGE THE SETTINGS

This is a Fibonacci bands based trading strategy developed by HFT Research. It is a highly customizable strategy and provides endless opportunities to find profitable trades in the market.

Use Fib BB

This is the main decision maker of the strategy. Tuning the settings of this portion of the strategy will change the outcome the most. We have provided default settings. However, they are only good for 15min chart on Bitcoin . Please adjust accordingly.

Fib BB Length: This setting adjusts the middle line of your Fibonacci Bands. It is the moving average that you take it as base for your Fibonacci bands. Default value is currently 20.

Fib Level to Use for Entry: Here, you adjust which one of the Fibonacci Ratio levels you would like to use for your entry. You can only choose one of the following options.

Fibonacci Ratio 1

This is your Fib ratio level 1 and you can put any number here you would like

Fibonacci Ratio 2

This is your Fib ratio level 2 and you can put any number here you would like

Fibonacci Ratio 3

This is your Fib ratio level 3 and you can put any number here you would like

Please keep in mind that Ratio 1 should be higher than Ratio 2 and Ratio 2 should be higher than Ratio 3.

Use RSI

You can also turn on and off the RSI as well. Alternatively, there is an option to use RSI on a different time frame than you are currently on. For example, if you are looking at the 5min chart to use Bollinger bands but you would like to look at the RSI value on the 15min chart. You can do so by selecting the custom RSI timeframe as well as adjusting the Oversold and Overbought value.

Use CCI

Commodity Channel Index is an indicator developed by Donald Lambert. It is a momentum-based oscillator used to help determine when an investment vehicle is reaching conditions of being overbought or oversold. It also used to asses price trend direction and strength. Default settings are usually the safest and the best fit.

Use VWAP

VWAP stands for volume weighted average price . It is an extremely useful indicator when trading intra-day. It does reset every trading session which is at 00:00 UTC . Instead of looking at x number of candles and providing an average price, it will take into consideration volume that’s traded at a certain price and weigh it accordingly.

Use ADX

ADX stands for average directional index . It is an indicator that measures volatility in the market. Unfortunately, the worst market condition for this strategy is sideways market. ADX becomes a useful tool since it can detect trend. If the volatility is low and there is no real price movement, ADX will pick that up and will not let you get in trades during a sideways market. It will allow you to enter trades only when the market is trending.

Use MA Filters

Lookback: It is an option to look back x number of candles to validate the price crossing. If the market is choppy and the price keeps crossing up and down the moving average you have chosen, it will generate a lot of “noisy” signals. This option allows you to confirm the cross by selecting how many candles the price needs to stay above or below the moving average. Setting it 0 will turn it off.

MA Filter Type: There is a selection of moving averages that is available on TradingView currently. You can choose from 14 different moving average types to detect the trend as accurate as possible.

Filter Length: You can select the length of your moving average. Most commonly used length being 50,100 and 200.

Filter Type: This is our propriety smoothing method in order to make the moving averages lag less and influence the way they are calculated slightly. Type 1 being the normal calculation and type 2 being the secret sauce

Reverse MA Filter: This option allows you to use the moving average in reverse. For example, the strategy will go long when the price is above the moving average. However, if you use the reserve MA Filter, you will go short when the price is above the moving average. This method works best in sideways market where price usually retraces back to the moving average. So, in an anticipation of price reverting back to the moving average, it is a useful piece of option to use during sideway markets.

The backtester assumes the following;

- 1000$ capital

- 0.06% commission based on binance

- 1% risk meaning 100% equity on cross leverage

- Backtest results are starting from 2020

If you want to get access to this indicator please DM me or visit our website.

Quickie (Free) BacktesterQuickie is a free tradingview Indicator developed by HFT Research. It works in sideways and trending markets depending the way you set it as well as both on short time frame and long time frame. It comes with backtesting abilities on tradingview.

BITMEX:XBTUSD

Use Bollinger Bands

This piece of the settings will turn and off Bollinger band’s input in the decision making. BB Length will determine the Moving average you are using to take the standard deviation off of which is named as BB Multiplier. Default settings will use 20 moving average and take standard deviation of 2 to create lower and upper bands. Increasing the Multiplier will give you fewer but safer entries

Use RSI

You can also turn on and off the RSI as well. Alternatively, there is an option to use RSI on a different time frame than you are currently on. For example, if you are looking at the 5min chart to use Bollinger bands but you would like to look at the RSI value on the 15min chart. You can do so by selecting the custom RSI timeframe as well as adjusting the Oversold and Overbought value.

Use MA Filter

Lookback: The indicator has an option to look back x number of candles to validate the price crossing. If the market is choppy and the price keeps crossing up and down the moving average you have chosen, it will generate a lot of “noisy” signals. This option allows you to confirm the cross by selecting how many candles the price needs to stay above or below the moving average. Setting it 0 will turn it off.

MA Filter Type: There is a selection of moving averages that is available on TradingView currently. You can choose from 14 different moving average types to detect the trend as accurate as possible.

Filter Length: You can select the length of your moving average. Most commonly used length being 50,100 and 200.

Filter Type: This is our propriety smoothing method in order to make the moving averages lag less and influence the way they are calculated slightly. Type 1 being the normal calculation and type 2 being the secret sauce.

Reverse MA Filter: This option allows you to use the moving average in reverse. For example, the strategy will go long when the price is above the moving average. However, if you use the reserve MA Filter, you will go short when the price is above the moving average. This method works best in sideways market where price usually retraces back to the moving average. So, in an anticipation of price reverting back to the moving average, it is a useful piece of option to use during sideway markets.

For more information please check out our website

inwCoin Bullish/Bearish Divergence - Risk% StrategyEnglish

=========

inwCoin RSI Bullish/ Bearish Divergence Startegy.

RSI Bullish and Bearish divergence is a popular strategy that most people use to find the "reversal pattern" and bet on it.

...But is it really profitable in long run?

To find the answer, I write this strategy to test this hypothesis and the result is interesting.

------

How it work?

------

As you know, the main logic of bullish / bearish divergence are..

Buy Signal : RSI higher low in Oversold zone and price lower low

Sell Signal : RSI lower high in Overbought zone and price lower high

I also add some parameters to my strategy

1) Use stop loss + specific stop loss level

2) lookback period = RSI / Price lookback period to find divergence

----------

The result

----------

Not working at all.

It working ok in some period of time like in sideway market

But when uptrend established, it can't make any profit ( well, it's mean reversion strategy after all haha )

Also, when market keep crashing like in Nov 2018.

This strategy got stop out so many times before you can make 1 profitable trade....

But that trade won't last long because you have to take profit when you got bearish divergence signal.

----------

Conclusion

----------

Combine with trend following strategy.

This strategy might be able to fill the gap of sideway market.

But don't depend solely on this strategy because in long run, it can't beat the market.

GoombX backtest publicGoombX is an MA and stoch RSI based indicator which looks for particular crosses to identify strong trends.

It produces clear signals for:

- LONG ENTRY when it detects a significant MA cross and the right stoch RSI conditions

- LONG EXIT when certain stoch RSI conditions are met

- LONG STOP when price moves x% below entry (default 10%)

- SHORT ENTRY when it detects a significant MA cross and the right stoch RSI conditions

- SHORT EXIT when certain stoch RSI conditions are met

- SHORT STOP when price moves x% above entry (default 10%)

It is best fitted for 1D charts

NOTES

This is the Strategy version of GoombX for backtesting purpose only (stops in October 2019)

I strongly recommend backtesting with fees if you plan on using GoombX for automated trading

A signal is only definitive once the trigger candle has closed

To learn how to backtest, please look here:

backtest-rookies.com

and here:

backtest-rookies.com

EMA Mega Cross StrategyBased on Anvamsi's script which uses 12/26 EMA crosses for entry/exit signals. I also add the following features:

* Optimized default parameters for ETH 4hr chart

* Use EMA 55/200 relationship to filter out signals

* Use RSI vs EMA of RSI to filter out signals

* Use 26/55 EMA relationship to filter out signals

* Use volume climax technique as an additional exit strategy

* Uses bull/bear RSI divs as an additional exit strategy

* Adds bull RSI div quick flip plays when nothing else is going on for extra $$

This very experimental and my first major script. I've kept it invite only because the only people using this should have a direct line of communication open with me at this point.

NOTE #1:

You can get 2018 ETH trade profitability to reach 100% if you change line 97 from:

if (shortEMA and (rsi1 <= ema(rsi1,RSIEMALength)) and shorttrend and (ema(close,26) < ema(close,55)))

to:

if (shortEMA and (rsi1 <= ema(rsi1,RSIEMALength)) and shorttrend)

Basically, you remove an extra filter from the short strategy. It's novel to see profitability hit 100% but if you look at performance from 2017, it increases the max draw down by a lot!

NOTE #2:

I couldn't get RSI bear div quick flips to work so they are disabled. The remaining short strategy is in effect.

NOTE #3:

The profitability is good for long-only, if you check Strategy Tester->Performance Summary.

NOTE #4:

I am not an expert trader (mainly due to psychological factors i think) but i can program and have a good understanding of signal processing from working with analog synthesizers. Use this at your own risk. I am not liable if you lose all of your money!

NOTE #5:

Code is really messy. Old code commented out everywhere. :/

SB_CM_RSI_2_Strategy_Version 1.0The strategy is based on the indicator posted by @ChrisMoody "CM RSI-2 Strategy Lower Indicator" which is based on "Larry Connors RSI-2 Strategy - Lower RSI"

In this strategy the longs are placed when a green color is encountered in the rsi and short when red color is encountered in the rsi.

Although the profits can be booked at different interval.

Just message in the script if you have any different idea regarding this indicator.

For the original indicator you can refer to :

For Tips to continue :) :

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

Cowabunga System from babypips.comPlease do read the information below as well, especially if you are new to Forex.

The Cowabunga System is a type of Mechanical Trading System that filters trades based on the trend of the 4 hour chart with EMAs and some other familiar indicators (RSI, Stochastics and MACD) while entering trades base on 15 minute chart.

I have coded (quite amateurishly) the basic system onto a 15 minute chart (the 4 hour settings are coded as well). The author says the system is to be traded off the 15 minute chart with the 4 hour chart only as a reference for trend direction.

4 Hour Chart Settings

5 EMA

10 EMA

Stochastics (10,3,3)

RSI (9)

Then we move onto the 15 minute chart, where he gives us the trade entry rules.

15 Minute Chart Settings

5 EMA

10 EMA

Stochastics (10,3,3)

RSI (9)

MACD (12,26,9)

Entry Rules - long entry rules used, obviously reverse these for shorting.

1. EMA must cross above the 10 EMA.

2. RSI must be greater than 50 and not overbought.

3. Stochastic must be headed up and not be in overbought territory.

4. MACD histogram must go from negative to positive OR be negative and start to increase in value.

What I did.

1. Set the RSI and Stochastic levels to avoid entries when they indicate overbought conditions for long and oversold conditions for short (80 and 20 levels).

2. Users can input specific times they want to backtest.

3. User's can configure profit targets, trailing stops and stops. Default is set it to was 100 pips profit target with a 40 pip trailing stop. (Note, when you are changing these values, please note that each pip is worth 10, so 100 pips is entered as 1000.)

The Cowabunga System from babypips.com is another popular and active system. The author, Pip Surfer, continues to post wins and losses with this system. It shows there is a lot of honesty and integrity with this system if the author keeps up to date even 10 years later and is not afraid of sharing the times the system causes losses.

As an example of this, here is post he shared just last week . It's almost like a journal, he gives specific times and reasons why he entered, lets the readers know when he was stopped out, etc. I think that what he does is equally important as his system.

To read more about this system, visit the thread on babypips.com, click here.

Intraday for Future By TradeEarnIntraday Strategy (StochRSI + VWAP + EMA)

Overview The Intraday Pullback Scalper is a specialized trend-following strategy designed for futures and equity traders who prefer to enter existing trends on pullbacks rather than chasing breakouts. By combining volume-weighted data (VWAP) with exponential moving averages (EMA) and momentum oscillators (Stochastic RSI), this script identifies high-probability entry points during intraday sessions. It includes built-in automation hooks (Alerts) compatible with bridge services for seamless execution.

How It Works

The strategy relies on a three-step confirmation process to filter noise and precision-time entries:

Trend Definition (The Filter):

VWAP (Volume Weighted Average Price): Acts as the primary regime filter. Longs are only permitted if price > VWAP; Shorts only if price < VWAP.

EMA (Exponential Moving Average): A secondary trend filter (default 100 periods) ensures alignment with the broader trend.

Time Range Breakout (Optional): Users can enable an "Initial Balance" filter where trades are only taken if the price breaks out of a specific time range (e.g., first hour High/Low).

Entry Trigger (The Signal):

Long Entry: The market must be in an Uptrend (Price > VWAP & EMA). The script waits for a "dip" where the Stochastic RSI drops below the Oversold level (default 20) and then crosses back up.

Short Entry: The market must be in a Downtrend (Price < VWAP & EMA). The script waits for a "rally" where the Stochastic RSI rises above the Overbought level (default 80) and then crosses back down.

Risk Management:

The strategy uses fixed Target Profit and Stop Loss values defined in currency (₹) relative to the trade quantity.

It features visual SL and TP lines on the chart for the duration of the trade to assist with manual monitoring.

Key Features

Universal Compatibility: Works on the "Current Chart" (Nifty, Bank Nifty, Stocks, Commodities) without needing complex dropdown selection.

Visual Dashboard: An on-screen table displays the Current Trade Status (Long/Short), Trend Direction, and Running P&L in real-time.

Algobaba Bridge Ready: Pre-formatted alert messages are included for users utilizing the Algobaba bridge for automation (supports MIS/NRML product types).

Customizable Trend Filters: Users can toggle the Time Range filter or adjust the VWAP Anchor (Session, Week, Month).

Settings & Configuration

Trade Quantity: Set your default lot size (e.g., 50 for Nifty).

Risk Settings: Define Target and Stop Loss in Rupees (₹) per trade setup.

Indicators: Adjustable lengths for EMA, RSI, and Stochastic.

Trading Window: Restrict entries to specific session hours (e.g., 09:15 - 15:10).

⚠️ IMPORTANT DISCLAIMER & RISK WARNING ⚠️

1. Educational Purpose Only This strategy script is provided solely for educational, informational, and research purposes. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any securities, futures, or derivatives. The author is not a SEBI registered Research Analyst or Investment Advisor.

2. No Guarantee of Profit The "P&L" and performance metrics displayed on the chart are hypothetical and based on historical data. Past performance is not indicative of future results. Market conditions change, and a strategy that worked in the past may fail in the future.

3. Limitations of Backtesting

Slippage & Commission: The script results may not fully account for real-world execution costs such as broker commissions, taxes (STT/GST), slippage, or liquidity issues.

Repainting/Data Lag: While every effort is made to ensure code stability, real-time data feeds may vary from historical data due to internet latency or data provider differences.

4. High Risk in Derivatives Trading Futures and Options (F&O) involves a substantial risk of loss and is not suitable for every investor. You can lose more than your initial capital. Please assess your risk tolerance and financial situation before trading.

5. Automation & Third-Party Tools This script includes alert messages formatted for third-party bridge services (e.g., Algobaba). The author assumes no responsibility for:

Technical failures, API errors, or connectivity issues with your broker or bridge provider.

Incorrect order execution resulting from automation.

Users are solely responsible for monitoring their trades and verifying order execution.

Usage Agreement By using this script, you acknowledge that you are trading at your own risk and hold the author harmless from any losses incurred. Always test on a paper trading account before deploying real capital.

Candlestick Pattern Strategy with Risk Management + AlertsThis strategy is built to detect volatility-driven squeeze expansion moves and automatically backtest both Breakout Longs and Breakdown Shorts with adjustable take-profit, stop-loss and volume confirmation filters.

It includes a built-in Auto-Optimizer, allowing the script to test multiple TP/SL/RSI/Volume profiles and automatically select the best configuration for the current market environment. Works across Stocks, Crypto and Forex — with each market automatically adjusting core system parameters.

🚀 Strategy Features

Feature Description

🔥 Long + Short Squeeze Detection Entries triggered by volatility expansion + BB break + strong momentum

⚙️ Auto-Optimizer Searches multiple TP/SL/RSI/Volume settings & selects best performer

📈 Full Backtest-Ready Strategy Includes stops, take profits + built-in performance table

🔔 Real-Time Alerts Get alerted instantly when a long or short squeeze event forms

🔄 Multi-Market Mode Tailored volatility & smoothing settings for Stocks / Crypto / Forex

🧠 Vol Spike Validation Filters signals using relative volume impulse

🏁 Trade Exit Logic Dynamic SL/TP calculated automatically based on optimized parameters

📊 How It Works

Detects breakouts above upper Bollinger band or breakdowns below lower band

Confirms strength using ATR expansion + Volume Surge

Confirms momentum using RSI selection (9/14/20 based on profile)

Enters Long/Short squeeze trade depending on breakout direction

Risk management automatically deploys TP + SL, optimized or manual

Displays performance statistics after backtest execution

🧬 Auto-Optimizer Logic

If Optimizer Mode = ON, the script tests:

Variable Range Tested

TP % 8 → 15%

SL % 4 → 8%

Volume Spike Filter 1.5 → 3.0x

RSI Window 9 / 14 / 20

The configuration that produces the highest score becomes active automatically for signals + backtest.

🛎 Alerts Included

🔥 Long Squeeze Alert

💀 Short Squeeze Alert

You can create TradingView alerts using → Add Alert → ANY alert() function call

Recommended Use

✔ Backtest system performance across assets

✔ Use Optimizer mode to find ideal TP/SL profiles

✔ Enable alerts for real-time squeeze entries

✔ Works best on 1h / 4h / 1D timeframes

🚫 Not financial advice — for research + strategy development only

UK Public Oneside V2This strategy combines RSI, Stochastic Oscillator, and a 50 EMA trend filter to identify moderate-risk trading opportunities in trending markets.

How it works:

Long entries occur when RSI and Stochastic are in oversold conditions while price is above the 50 EMA.

Short entries occur when RSI and Stochastic are in overbought conditions while price is below the 50 EMA.

Trades are confirmed on the previous candle, avoiding premature entries and exits.

Risk management is handled using fixed percentage stop-loss with configurable risk-to-reward targets.

Optional RSI-based exits close positions early during overbought or oversold conditions.

Key Features:

Trend-filtered entries using EMA 50

Non-repainting logic (confirmed candle signals)

Configurable stop-loss and reward ratio

Works well for scalping and intraday trading

Suitable for crypto, forex, and indices

Recommended Timeframes:

5m, 15m, 30m

Note:

This strategy is designed for educational and research purposes. Always forward-test and apply proper risk management before using in live trading.

Buy-Dip / Sell-Pullback Buy the Dip / Sell the Pullback – Trend-Following Strategy (EOD → Next Day Execution)

Overview

This is a trend-following futures strategy designed to participate in pullbacks within established trends, not to predict reversals.

It works on End-of-Day (EOD) confirmation and executes trades on the next trading session, making it suitable for positional and swing traders.

The strategy combines momentum, trend direction, volatility, and price location to filter for high-quality setups while avoiding overtrading.

🔍 Core Philosophy

Trade only in the direction of the prevailing trend

Buy dips in uptrends

Sell pullbacks in downtrends

Avoid chasing price after extended gaps

Use volatility-adjusted risk management (ATR-based SL & targets)

📊 Indicators Used

RSI (20)

Measures underlying momentum strength

Stochastic Oscillator (55, 34, 21)

Confirms pullback exhaustion within a trend

Supertrend (10, 2)

Defines primary trend direction

Bollinger Bands (20, 2)

Provides structural trend bias

ATR (5)

Used for:

Entry gap filter

Stop-loss

Profit target

Supertrend buffer

✅ Long (Buy) Setup – Evaluated at EOD

A long setup is generated when all of the following conditions are satisfied at the close of the trading day:

RSI(20) is above the bullish threshold (default: 48)

Stochastic %K is above %D (confirming pullback momentum)

Supertrend direction is bullish

Price is near or above Supertrend, allowing a volatility-adjusted buffer (ATR-based)

Price is above the Bollinger Band middle line

This combination ensures:

The market is trending up

Momentum supports continuation

The pullback is controlled, not a breakdown

❌ Short (Sell) Setup – Evaluated at EOD

A short setup is generated when:

RSI(20) is below the bearish threshold (default: 52)

Stochastic %K is below %D

Supertrend direction is bearish

Price is near or below Supertrend, with an ATR buffer

Price is below the Bollinger Band middle line

This filters for pullbacks within sustained downtrends.

⏰ Trade Execution Logic (Next Day Rule)

Once a setup is confirmed at EOD, a trade is attempted on the next trading session

To avoid chasing gaps:

Long trades are allowed only if price does not move more than a defined multiple of the previous day’s True Range

Short trades follow the same logic in reverse

This is implemented via limit orders, ensuring realistic backtesting and execution behavior

🛑 Risk Management

All exits are volatility-adjusted using ATR:

Stop-Loss:

1.1 × ATR(5) from entry price

Target:

2.2 × ATR(5) from entry price

This results in a risk–reward ratio of approximately 1:2

ATR is frozen at entry to avoid forward-looking bias.

🧠 Why This Strategy Works

Avoids low-quality trades during consolidation

Participates only when trend + momentum align

Prevents emotional gap-chasing

Adapts automatically to changing volatility

Suitable for index futures and liquid stocks

📌 Recommended Usage

Timeframe: Daily

Instruments:

Index Futures (e.g. NIFTY, BANKNIFTY)

Highly liquid stocks

Market Type: Trending markets

Not ideal for: Sideways or low-volatility environments

⚙️ Customization Tips

You can control trade frequency and aggressiveness by adjusting:

RSI thresholds

Supertrend buffer (ATR multiple)

Gap filter multiplier

Stochastic edge parameter

Looser settings → more trades

Stricter settings → higher selectivity

⚠️ Disclaimer

This strategy is for educational and research purposes only.

Backtest results do not guarantee future performance.

Always validate with paper trading before deploying real capital.

Trend Signal MomentumOVERVIEW

Signal Trend Momentum is a hybrid strategy that combines multiple confirmations and filters to obtain better potential trading signals. Each confirmation and filter in Signal Trend Momentum aims to avoid possible false and trap signals.

HYBRID CONCEPTS

Smart Money Concept – This indicator forms market structure and Bullish & Bearish Order Block areas to make it easier to identify market trends and strong areas where price reversals often occur. Its purpose is to simplify recognizing market direction and serve as the first confirmation.

MSS + BOS (Market Structure Shift + Break of Structure) – This indicator serves as additional confirmation for the Smart Money Concept. With the presence of two types of market structure, the market trend direction becomes clearer and more convincing.

RSI Momentum Signal – This indicator becomes the third confirmation. When the Market Trend is clear and convincing, supported by the formation of Bearish and Bullish Order Blocks, the role of the Momentum Signal here becomes crucial as it provides trend momentum based on overbought and oversold areas.

Momentum Position – This indicator becomes the next confirmation based on buyer and seller VOLUME in the market. If buyer volume is higher, the momentum position will be depicted on the chart with an upward arrow, and conversely, if seller volume is higher, it will be depicted with a downward arrow.

SnR (Support and Resistance) – This final indicator is Support and Resistance, which will serve as the last and more convincing confirmation. Support and Resistance will strengthen the Order Block areas formed by the Smart Money Concept indicator. A Bullish Order Block + Support creates a higher possibility for an upward trend in the market, conversely, a Bearish Order Block + Resistance creates a higher possibility for a downward trend in the market.

The combination of these several indicators will provide a strong market direction + persistent buyer and seller areas, as well as depict momentum based on volume + RSI which serve as additional confirmations.

These additional confirmations will produce stronger signals and help avoid false and trap signals in the market.

HOW TO USE

A SHORT SIGNAL will be strong if there is a Downtrend Market Structure + Bearish Order Block + Resistance + Oversold RSI Momentum + Strong Seller Volume Momentum.

A LONG SIGNAL will be strong if there is an Uptrend Market Structure + Bullish Order Block + Support + Overbought RSI Momentum + Strong Buyer Volume Momentum.

CONCLUSION

Signal Trend Momentum is a combination of several powerful indicators designed to produce stronger, clearer, and easier-to-read signals.

This strategy is highly suitable for traders seeking more convincing trade signals based on multiple confirmations from the combined indicators, thereby creating a strong signal with a higher probability.

TrendSight📌 TrendSight — The All-in-One Multi-Timeframe Trend Engine

Key Features & Logic

Multi-Timeframe Trend Confirmation:

Entries are filtered by confirming bullish/bearish alignment across three distinct Supertrend timeframes (e.g., 5-min, 15-min, 45-min, etc.), combined with an EMA and volatility filter, to ensure high-conviction trades that's a powerful combination! Designing the entire strategy around the 15-minute timeframe (M15) and focusing on high-volatility coins maximizes the strategy's effectiveness .

Guaranteed Single-Entry per Signal:

The strategy uses a powerful manual flag and counter system to ensure trades fire only once when a new signal begins. It absolutely prevents immediate re-entry if the signal remains true, waiting instead for the entire trend condition to reset to false.

Dynamic Trailing Stop Loss:

The Stop Loss is set to a moving Supertrend line (current_supertrend), ensuring tight risk management that trails the price as the trade moves into profit.Guaranteed Take Profit (4% Run-up): Uses a precise Limit Order via strategy.exit() to capture profits instantly at a 4% run-up. This ensures accurate profit capture, even on sudden spikes (wicks).

Automated Risk Management:

Position size is dynamically calculated based on a fixed risk percentage (default 2% of equity) relative to the distance to the trailing stop.

🔥 Core Components

1. Adaptive Multi-Timeframe SuperTrend Dashboard

The backbone of mTrendSight is a fully customizable SuperTrend system, enhanced with a multi-timeframe confirmation table displaying ST direction & value.

This compact “Trend Dashboard” provides instant clarity on higher-timeframe direction, trend strength, and market bias.

2. Dynamic Support & Resistance Channels

Automatically detects the strongest support/resistance zones using pivot clustering.

Key Features:

Clustered S/R Channels instead of thin lines

Adaptive width based on recent swings

Breakout markers (optional) for continuation signals

Helps identify structural zones, retest areas, and liquidity pockets

3. Multi-Timeframe Color-Coded EMAs

Plot up to three EMAs, each optionally pulled from a higher timeframe.

Benefits:

Instant visual trend alignment

Bullish/Bearish dynamic color shifts

Precision EMA value table for trade planning

Works perfectly with ST & RSI for multi-layer confirmation

4. Linear Regression Trend Channel

A statistically driven trend channel that measures the most probable path of price action.

Highlights:

Uses Pearson’s R to determine trend reliability

Provides a Confidence Level to judge whether trend slope is credible

Ideal for determining over-extension and mean-reversion zones

5. ATR Volatility Analyzer

A lightweight but powerful volatility classifier using ATR.

Features:

Detects High, Low, or Normal volatility

Clean table display

Helps filter entries during low-energy markets

Strengthens trend-following filters when volatility expands

6. RSI Momentum & Trend Classifier

A significantly improved RSI with multi-layer smoothing and structure-based classification.

Provides:

Bullish / Bearish / Neutral momentum states

Short-term momentum vs long-term RSI trend

Perfect for early trend shifts, pullback entries, and momentum confirmation

⚙️ How the Strategy Works (Execution Logic)

📌 Multi-Timeframe Supertrend + EMA + Volatility Confirmation

Entries are only triggered when:

Multiple Supertrend timeframes align (e.g., 5m + 15m + 45m)

EMA direction aligns with the trend

Volatility conditions (ATR filter) is not Low allow high-probability moves

This ensures strong directional confluence before every trade.

📌 Guaranteed Single-Entry Logic

The strategy uses a flag + counter system to ensure:

Only one entry is allowed per trend signal

Re-entries do not happen until the entire trend condition resets

The Strategy Tester remains clean, without duplicate overlapping trades

This eliminates revenge trades, repeated fills, and choppy overtrading.

📌 Dynamic Supertrend Trailing Stop

Stop Loss is anchored to current Supertrend value, creating:

Automatic trailing

Tight downside control

Protection against deep pullbacks

High responsiveness during volatility expansions

📌 Precision Take-Profit (4% Run-Up Capture)

A dedicated global exit block ensures:

Take Profit triggers exactly at 4% price run-up

Uses strategy.exit() with limit orders to catch spikes (wicks)

Works consistently on all timeframes & assets

📌 Automated Position Sizing (2% Risk Default)

Position size is dynamically calculated based on:

Account Equity

Distance to trailing stop

Configured risk %

This enforces proper risk management without manual adjustments.

📈 How to Interpret Results

Reliable Exits: All exits are globally managed, so stops and take profits trigger accurately on every bar.

Clean Trade History: Because of single-entry logic, backtests show one trade per valid signal.

Consistency: Multi-timeframe logic ensures only high-quality, structured trades.