$ADD LevelsThis Pine Script is designed to track and visualize the NYSE Advance-Decline Line (ADD). The Advance-Decline Line is a popular market breadth indicator, showing the difference between advancing and declining stocks on the NYSE. It’s often used to gauge overall market sentiment and strength.

1. //@version=5

This line tells TradingView to use Pine Script v5, the latest and most powerful version of Pine.

2. indicator(" USI:ADD Levels", overlay=false)

• This creates a new indicator called ” USI:ADD Levels”.

• overlay=false means it will appear in a separate pane, not on the main price chart.

3. add = request.security(...)

This fetches real-time data from the symbol USI:ADD (Advance-Decline Line) using a 1-minute timeframe. You can change the timeframe if needed.

add_symbol = input.symbol(" USI:ADD ", "Market Breadth Symbol")

add = request.security(add_symbol, "1", close)

4. Key Thresholds

These define the market sentiment zones:

Zone. Value. Meaning

Overbought +1500 Extremely bullish

Bullish +1000 Generally bullish trend

Neutral ±500 Choppy, unclear market

Bearish -1000 Generally bearish trend

Oversold -1500 Extremely bearish

5. Plot the ADD Line hline(...)

Draws static lines at +1500, +1000, +500, -500, -1000, -1500 for reference so you can visually assess where ADD stands.

6. Horizontal Threshold Lines bgcolor(...)

• Green background if ADD > +1500 → extremely bullish.

• Red background if ADD < -1500 → extremely bearish.

7. Background Highlights alertcondition(...)

• Green background if ADD > +1500 → extremely bullish.

• Red background if ADD < -1500 → extremely bearish.

8. Alert Conditions. alertcondition(...)

Lets you create automatic alerts for:

• USI:ADD being very high or low.

• Crosses above +1000 (bullish trigger).

• Crosses below -1000 (bearish trigger).

You can use these to trigger trades or monitor sentiment shifts.

Summary: When to Use It

• Use this script in a market breadth dashboard.

• Combine it with price action and volume analysis.

• Monitor for ADD crosses to signal potential market reversals or momentum.

Tìm kiếm tập lệnh với "美股标普500"

Institutional Volume Profile# Institutional Volume Profile (IVP) - Advanced Volume Analysis Indicator

## Overview

The Institutional Volume Profile (IVP) is a sophisticated technical analysis tool that combines traditional volume profile analysis with institutional volume detection algorithms. This indicator helps traders identify key price levels where significant institutional activity has occurred, providing insights into market structure and potential support/resistance zones.

## Key Features

### 🎯 Volume Profile Analysis

- **Point of Control (POC)**: Identifies the price level with the highest volume activity

- **Value Area**: Highlights the price range containing a specified percentage (default 70%) of total volume

- **Multi-Row Distribution**: Displays volume distribution across 10-50 price levels for detailed analysis

- **Customizable Period**: Analyze volume profiles over 10-500 bars

### 🏛️ Institutional Volume Detection

- **Pocket Pivot Volume (PPV)**: Detects bullish institutional buying when up-volume exceeds recent down-volume peaks

- **Pivot Negative Volume (PNV)**: Identifies bearish institutional selling when down-volume exceeds recent up-volume peaks

- **Accumulation Detection**: Spots potential accumulation phases with high volume and narrow price ranges

- **Distribution Analysis**: Identifies distribution patterns with high volume but minimal price movement

### 🎨 Visual Customization Options

- **Multiple Color Schemes**: Heat Map, Institutional, Monochrome, and Rainbow themes

- **Bar Styles**: Solid, Gradient, Outlined, and 3D Effect rendering

- **Volume Intensity Display**: Visual intensity based on volume magnitude

- **Flexible Positioning**: Left or right side profile placement

- **Current Price Highlighting**: Real-time price level indication

### 📊 Advanced Visual Features

- **Volume Labels**: Display volume amounts at key price levels

- **Gradient Effects**: Multi-step gradient rendering for enhanced visibility

- **3D Styling**: Shadow effects for professional appearance

- **Opacity Control**: Adjustable transparency (10-100%)

- **Border Customization**: Configurable border width and styling

## How It Works

### Volume Distribution Algorithm

The indicator analyzes each bar within the specified period and distributes its volume proportionally across the price levels it touches. This creates an accurate representation of where trading activity has been concentrated.

### Institutional Detection Logic

- **PPV Trigger**: Current up-bar volume > highest down-volume in lookback period + above volume MA

- **PNV Trigger**: Current down-bar volume > highest up-volume in lookback period + above volume MA

- **Accumulation**: High volume + narrow range + bullish close

- **Distribution**: Very high volume + minimal price movement

### Value Area Calculation

Starting from the POC, the algorithm expands both upward and downward, adding volume until reaching the specified percentage of total volume (default 70%).

## Configuration Parameters

### Profile Settings

- **Profile Period**: 10-500 bars (default: 50)

- **Number of Rows**: 10-50 levels (default: 24)

- **Profile Width**: 10-100% of screen (default: 30%)

- **Value Area %**: 50-90% (default: 70%)

### Institutional Analysis

- **PPV Lookback Days**: 5-20 periods (default: 10)

- **Volume MA Length**: 10-200 periods (default: 50)

- **Institutional Threshold**: 1.0-2.0x multiplier (default: 1.2)

### Visual Controls

- **Bar Style**: Solid, Gradient, Outlined, 3D Effect

- **Color Scheme**: Heat Map, Institutional, Monochrome, Rainbow

- **Profile Position**: Left or Right side

- **Opacity**: 10-100%

- **Show Labels**: Volume amount display toggle

## Interpretation Guide

### Volume Profile Elements

- **Thick Horizontal Bars**: High volume nodes (strong support/resistance)

- **Thin Horizontal Bars**: Low volume nodes (weak levels)

- **White Line (POC)**: Strongest support/resistance level

- **Blue Highlighted Area**: Value Area (fair value zone)

### Institutional Signals

- **Blue Triangles (PPV)**: Bullish institutional buying detected

- **Orange Triangles (PNV)**: Bearish institutional selling detected

- **Color-Coded Bars**: Different colors indicate institutional activity types

### Color Scheme Meanings

- **Heat Map**: Red (high volume) → Orange → Yellow → Gray (low volume)

- **Institutional**: Blue (PPV), Orange (PNV), Aqua (Accumulation), Yellow (Distribution)

- **Monochrome**: Grayscale intensity based on volume

- **Rainbow**: Color-coded by price level position

## Trading Applications

### Support and Resistance

- POC acts as dynamic support/resistance

- High volume nodes indicate strong price levels

- Low volume areas suggest potential breakout zones

### Institutional Activity

- PPV above Value Area: Strong bullish signal

- PNV below Value Area: Strong bearish signal

- Accumulation patterns: Potential upward breakouts

- Distribution patterns: Potential downward pressure

### Market Structure Analysis

- Value Area defines fair value range

- Profile shape indicates market sentiment

- Volume gaps suggest potential price targets

## Alert Conditions

- PPV Detection at current price level

- PNV Detection at current price level

- PPV above Value Area (strong bullish)

- PNV below Value Area (strong bearish)

## Best Practices

1. Use multiple timeframes for confirmation

2. Combine with price action analysis

3. Pay attention to volume context (above/below average)

4. Monitor institutional signals near key levels

5. Consider overall market conditions

## Technical Notes

- Maximum 500 boxes and 100 labels for optimal performance

- Real-time calculations update on each bar close

- Historical analysis uses complete bar data

- Compatible with all TradingView chart types and timeframes

---

*This indicator is designed for educational and informational purposes. Always combine with other analysis methods and risk management strategies.*

Sector 50MA vs 200MA ComparisonThis TradingView indicator compares the 50-period Moving Average (50MA) and 200-period Moving Average (200MA) of a selected market sector or index, providing a visual and analytical tool to assess relative strength and trend direction. Here's a detailed breakdown of its functionality:

Purpose: The indicator plots the 50MA and 200MA of a chosen sector or index on a separate panel, highlighting their relationship to identify bullish (50MA > 200MA) or bearish (50MA < 200MA) trends. It also includes a histogram and threshold lines to gauge momentum and key levels.

Inputs:

Resolution: Allows users to select the timeframe for calculations (Daily, Weekly, or Monthly; default is Daily).

Sector Selection: Users can choose from a list of sectors or indices, including Tech, Financials, Consumer Discretionary, Utilities, Energy, Communication Services, Materials, Industrials, Health Care, Consumer Staples, Real Estate, S&P 500 Value, S&P 500 Growth, S&P 500, NASDAQ, Russell 2000, and S&P SmallCap 600. Each sector maps to specific ticker pairs for 50MA and 200MA data.

Data Retrieval:

The indicator fetches closing prices for the 50MA and 200MA of the selected sector using the request.security function, based on the chosen timeframe and ticker pairs.

Visual Elements:

Main Chart:

Plots the 50MA (blue line) and 200MA (red line) for the selected sector.

Fills the area between the 50MA and 200MA with green (when 50MA > 200MA, indicating bullishness) or red (when 50MA < 200MA, indicating bearishness).

Threshold Lines:

Horizontal lines at 0 (zero line), 20 (lower threshold), 50 (center), 80 (upper threshold), and 100 (upper limit) provide reference points for the 50MA's position.

Fills between 0-20 (green) and 80-100 (red) highlight key zones for potential overbought or oversold conditions.

Sector Information Table:

A table in the top-right corner displays the selected sector and its corresponding 50MA and 200MA ticker symbols for clarity.

Alerts:

Generates alert conditions for:

Bullish Crossover: When the 50MA crosses above the 200MA (indicating potential upward momentum).

Bearish Crossover: When the 50MA crosses below the 200MA (indicating potential downward momentum).

Use Case:

Traders can use this indicator to monitor the relative strength of a sector's short-term trend (50MA) against its long-term trend (200MA).

The visual fill between the moving averages and the threshold lines helps identify trend direction, momentum, and potential reversal points.

The sector selection feature allows for comparative analysis across different market segments, aiding in sector rotation strategies or market trend analysis.

This indicator is ideal for traders seeking to analyze sector performance, identify trend shifts, and make informed decisions based on moving average crossovers and momentum thresholds.

SPDR Sectors TableThis script generates an interactive and customizable SPDR Sectors Table designed to monitor and analyze the performance of the 11 main sectors of the S&P 500 via sector-specific ETFs. It offers a dynamic overview of daily or periodic sector movements, making it a valuable tool for traders, analysts, and investors implementing sector rotation strategies.

█ DEFINITIONS

SPDR Sectors ETFs are exchange-traded funds managed by State Street Global Advisors, which divide the S&P 500 into the following 11 sectors:

- Communication Services (XLC)

- Consumer Discretionary (XLY)

- Consumer Staples (XLP)

- Energy (XLE)

- Financials (XLF)

- Health Care (XLV)

- Industrials (XLI)

- Materials (XLB)

- Real Estate (XLRE)

- Technology (XLK)

- Utilities (XLU)

These ETFs aim to replicate the performance of their respective sectors as defined by the Global Industry Classification Standard (GICS). The funds are periodically rebalanced to match changes in the S&P 500 composition, offering an accurate snapshot of sectoral trends.

█ INDICATOR

The table displays each sector's ticker and full name, following official GICS terminology and SPDR color coding. It also shows percentage performance, calculated daily on intraday charts or based on the selected time frame.

Users can sort the table by either percentage performance or the relative weight of each ETF in the S&P 500. The default weight values reflect data updated as of 17 April 2025, and can be manually adjusted based on the most recent sector weightings available on the official SPDR website.

Z-Score Normalized Volatility IndicesVolatility is one of the most important measures in financial markets, reflecting the extent of variation in asset prices over time. It is commonly viewed as a risk indicator, with higher volatility signifying greater uncertainty and potential for price swings, which can affect investment decisions. Understanding volatility and its dynamics is crucial for risk management and forecasting in both traditional and alternative asset classes.

Z-Score Normalization in Volatility Analysis

The Z-score is a statistical tool that quantifies how many standard deviations a given data point is from the mean of the dataset. It is calculated as:

Z = \frac{X - \mu}{\sigma}

Where X is the value of the data point, \mu is the mean of the dataset, and \sigma is the standard deviation of the dataset. In the context of volatility indices, the Z-score allows for the normalization of these values, enabling their comparison regardless of the original scale. This is particularly useful when analyzing volatility across multiple assets or asset classes.

This script utilizes the Z-score to normalize various volatility indices:

1. VIX (CBOE Volatility Index): A widely used indicator that measures the implied volatility of S&P 500 options. It is considered a barometer of market fear and uncertainty (Whaley, 2000).

2. VIX3M: Represents the 3-month implied volatility of the S&P 500 options, providing insight into medium-term volatility expectations.

3. VIX9D: The implied volatility for a 9-day S&P 500 options contract, which reflects short-term volatility expectations.

4. VVIX: The volatility of the VIX itself, which measures the uncertainty in the expectations of future volatility.

5. VXN: The Nasdaq-100 volatility index, representing implied volatility in the Nasdaq-100 options.

6. RVX: The Russell 2000 volatility index, tracking the implied volatility of options on the Russell 2000 Index.

7. VXD: Volatility for the Dow Jones Industrial Average.

8. MOVE: The implied volatility index for U.S. Treasury bonds, offering insight into expectations for interest rate volatility.

9. BVIX: Volatility of Bitcoin options, a useful indicator for understanding the risk in the cryptocurrency market.

10. GVZ: Volatility index for gold futures, reflecting the risk perception of gold prices.

11. OVX: Measures implied volatility for crude oil futures.

Volatility Clustering and Z-Score

The concept of volatility clustering—where high volatility tends to be followed by more high volatility—is well documented in financial literature. This phenomenon is fundamental in volatility modeling and highlights the persistence of periods of heightened market uncertainty (Bollerslev, 1986).

Moreover, studies by Andersen et al. (2012) explore how implied volatility indices, like the VIX, serve as predictors for future realized volatility, underlining the relationship between expected volatility and actual market behavior. The Z-score normalization process helps in making volatility data comparable across different asset classes, enabling more effective decision-making in volatility-based strategies.

Applications in Trading and Risk Management

By using Z-score normalization, traders can more easily assess deviations from the mean in volatility, helping to identify periods when volatility is unusually high or low. This can be used to adjust risk exposure or to implement volatility-based trading strategies, such as mean reversion strategies. Research suggests that volatility mean-reversion is a reliable pattern that can be exploited for profit (Christensen & Prabhala, 1998).

References:

• Andersen, T. G., Bollerslev, T., Diebold, F. X., & Vega, C. (2012). Realized volatility and correlation dynamics: A long-run approach. Journal of Financial Economics, 104(3), 385-406.

• Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307-327.

• Christensen, B. J., & Prabhala, N. R. (1998). The relation between implied and realized volatility. Journal of Financial Economics, 50(2), 125-150.

• Whaley, R. E. (2000). Derivatives on market volatility and the VIX index. Journal of Derivatives, 8(1), 71-84.

ZigZag█ Overview

This Pine Script™ library provides a comprehensive implementation of the ZigZag indicator using advanced object-oriented programming techniques. It serves as a developer resource rather than a standalone indicator, enabling Pine Script™ programmers to incorporate sophisticated ZigZag calculations into their own scripts.

Pine Script™ libraries contain reusable code that can be imported into indicators, strategies, and other libraries. For more information, consult the Libraries section of the Pine Script™ User Manual.

█ About the Original

This library is based on TradingView's official ZigZag implementation .

The original code provides a solid foundation with user-defined types and methods for calculating ZigZag pivot points.

█ What is ZigZag?

The ZigZag indicator filters out minor price movements to highlight significant market trends.

It works by:

1. Identifying significant pivot points (local highs and lows)

2. Connecting these points with straight lines

3. Ignoring smaller price movements that fall below a specified threshold

Traders typically use ZigZag for:

- Trend confirmation

- Identifying support and resistance levels

- Pattern recognition (such as Elliott Waves)

- Filtering out market noise

The algorithm identifies pivot points by analyzing price action over a specified number of bars, then only changes direction when price movement exceeds a user-defined percentage threshold.

█ My Enhancements

This modified version extends the original library with several key improvements:

1. Support and Resistance Visualization

- Adds horizontal lines at pivot points

- Customizable line length (offset from pivot)

- Adjustable line width and color

- Option to extend lines to the right edge of the chart

2. Support and Resistance Zones

- Creates semi-transparent zone areas around pivot points

- Customizable width for better visibility of important price levels

- Separate colors for support (lows) and resistance (highs)

- Visual representation of price areas rather than just single lines

3. Zig Zag Lines

- Separate colors for upward and downward ZigZag movements

- Visually distinguishes between bullish and bearish price swings

- Customizable colors for text

- Width customization

4. Enhanced Settings Structure

- Added new fields to the Settings type to support the additional features

- Extended Pivot type with supportResistance and supportResistanceZone fields

- Comprehensive configuration options for visual elements

These enhancements make the ZigZag more useful for technical analysis by clearly highlighting support/resistance levels and zones, and providing clearer visual cues about market direction.

█ Technical Implementation

This library leverages Pine Script™'s user-defined types (UDTs) to create a robust object-oriented architecture:

- Settings : Stores configuration parameters for calculation and display

- Pivot : Represents pivot points with their visual elements and properties

- ZigZag : Manages the overall state and behavior of the indicator

The implementation follows best practices from the Pine Script™ User Manual's Style Guide and uses advanced language features like methods and object references. These UDTs represent Pine Script™'s most advanced feature set, enabling sophisticated data structures and improved code organization.

For newcomers to Pine Script™, it's recommended to understand the language fundamentals before working with the UDT implementation in this library.

█ Usage Example

//@version=6

indicator("ZigZag Example", overlay = true, shorttitle = 'ZZA', max_bars_back = 5000, max_lines_count = 500, max_labels_count = 500, max_boxes_count = 500)

import andre_007/ZigZag/1 as ZIG

var group_1 = "ZigZag Settings"

//@variable Draw Zig Zag on the chart.

bool showZigZag = input.bool(true, "Show Zig-Zag Lines", group = group_1, tooltip = "If checked, the Zig Zag will be drawn on the chart.", inline = "1")

// @variable The deviation percentage from the last local high or low required to form a new Zig Zag point.

float deviationInput = input.float(5.0, "Deviation (%)", minval = 0.00001, maxval = 100.0,

tooltip = "The minimum percentage deviation from a previous pivot point required to change the Zig Zag's direction.", group = group_1, inline = "2")

// @variable The number of bars required for pivot detection.

int depthInput = input.int(10, "Depth", minval = 1, tooltip = "The number of bars required for pivot point detection.", group = group_1, inline = "3")

// @variable registerPivot (series bool) Optional. If `true`, the function compares a detected pivot

// point's coordinates to the latest `Pivot` object's `end` chart point, then

// updates the latest `Pivot` instance or adds a new instance to the `ZigZag`

// object's `pivots` array. If `false`, it does not modify the `ZigZag` object's

// data. The default is `true`.

bool allowZigZagOnOneBarInput = input.bool(true, "Allow Zig Zag on One Bar", tooltip = "If checked, the Zig Zag calculation can register a pivot high and pivot low on the same bar.",

group = group_1, inline = "allowZigZagOnOneBar")

var group_2 = "Display Settings"

// @variable The color of the Zig Zag's lines (up).

color lineColorUpInput = input.color(color.green, "Line Colors for Up/Down", group = group_2, inline = "4")

// @variable The color of the Zig Zag's lines (down).

color lineColorDownInput = input.color(color.red, "", group = group_2, inline = "4",

tooltip = "The color of the Zig Zag's lines")

// @variable The width of the Zig Zag's lines.

int lineWidthInput = input.int(1, "Line Width", minval = 1, tooltip = "The width of the Zig Zag's lines.", group = group_2, inline = "w")

// @variable If `true`, the Zig Zag will also display a line connecting the last known pivot to the current `close`.

bool extendInput = input.bool(true, "Extend to Last Bar", tooltip = "If checked, the last pivot will be connected to the current close.",

group = group_1, inline = "5")

// @variable If `true`, the pivot labels will display their price values.

bool showPriceInput = input.bool(true, "Display Reversal Price",

tooltip = "If checked, the pivot labels will display their price values.", group = group_2, inline = "6")

// @variable If `true`, each pivot label will display the volume accumulated since the previous pivot.

bool showVolInput = input.bool(true, "Display Cumulative Volume",

tooltip = "If checked, the pivot labels will display the volume accumulated since the previous pivot.", group = group_2, inline = "7")

// @variable If `true`, each pivot label will display the change in price from the previous pivot.

bool showChgInput = input.bool(true, "Display Reversal Price Change",

tooltip = "If checked, the pivot labels will display the change in price from the previous pivot.", group = group_2, inline = "8")

// @variable Controls whether the labels show price changes as raw values or percentages when `showChgInput` is `true`.

string priceDiffInput = input.string("Absolute", "", options = ,

tooltip = "Controls whether the labels show price changes as raw values or percentages when 'Display Reversal Price Change' is checked.",

group = group_2, inline = "8")

// @variable If `true`, the Zig Zag will display support and resistance lines.

bool showSupportResistanceInput = input.bool(true, "Show Support/Resistance Lines",

tooltip = "If checked, the Zig Zag will display support and resistance lines.", group = group_2, inline = "9")

// @variable The number of bars to extend the support and resistance lines from the last pivot point.

int supportResistanceOffsetInput = input.int(50, "Support/Resistance Offset", minval = 0,

tooltip = "The number of bars to extend the support and resistance lines from the last pivot point.", group = group_2, inline = "10")

// @variable The width of the support and resistance lines.

int supportResistanceWidthInput = input.int(1, "Support/Resistance Width", minval = 1,

tooltip = "The width of the support and resistance lines.", group = group_2, inline = "11")

// @variable The color of the support lines.

color supportColorInput = input.color(color.red, "Support/Resistance Color", group = group_2, inline = "12")

// @variable The color of the resistance lines.

color resistanceColorInput = input.color(color.green, "", group = group_2, inline = "12",

tooltip = "The color of the support/resistance lines.")

// @variable If `true`, the support and resistance lines will be drawn as zones.

bool showSupportResistanceZoneInput = input.bool(true, "Show Support/Resistance Zones",

tooltip = "If checked, the support and resistance lines will be drawn as zones.", group = group_2, inline = "12-1")

// @variable The color of the support zones.

color supportZoneColorInput = input.color(color.new(color.red, 70), "Support Zone Color", group = group_2, inline = "12-2")

// @variable The color of the resistance zones.

color resistanceZoneColorInput = input.color(color.new(color.green, 70), "", group = group_2, inline = "12-2",

tooltip = "The color of the support/resistance zones.")

// @variable The width of the support and resistance zones.

int supportResistanceZoneWidthInput = input.int(10, "Support/Resistance Zone Width", minval = 1,

tooltip = "The width of the support and resistance zones.", group = group_2, inline = "12-3")

// @variable If `true`, the support and resistance lines will extend to the right of the chart.

bool supportResistanceExtendInput = input.bool(false, "Extend to Right",

tooltip = "If checked, the lines will extend to the right of the chart.", group = group_2, inline = "13")

// @variable References a `Settings` instance that defines the `ZigZag` object's calculation and display properties.

var ZIG.Settings settings =

ZIG.Settings.new(

devThreshold = deviationInput,

depth = depthInput,

lineColorUp = lineColorUpInput,

lineColorDown = lineColorDownInput,

textUpColor = lineColorUpInput,

textDownColor = lineColorDownInput,

lineWidth = lineWidthInput,

extendLast = extendInput,

displayReversalPrice = showPriceInput,

displayCumulativeVolume = showVolInput,

displayReversalPriceChange = showChgInput,

differencePriceMode = priceDiffInput,

draw = showZigZag,

allowZigZagOnOneBar = allowZigZagOnOneBarInput,

drawSupportResistance = showSupportResistanceInput,

supportResistanceOffset = supportResistanceOffsetInput,

supportResistanceWidth = supportResistanceWidthInput,

supportColor = supportColorInput,

resistanceColor = resistanceColorInput,

supportResistanceExtend = supportResistanceExtendInput,

supportResistanceZoneWidth = supportResistanceZoneWidthInput,

drawSupportResistanceZone = showSupportResistanceZoneInput,

supportZoneColor = supportZoneColorInput,

resistanceZoneColor = resistanceZoneColorInput

)

// @variable References a `ZigZag` object created using the `settings`.

var ZIG.ZigZag zigZag = ZIG.newInstance(settings)

// Update the `zigZag` on every bar.

zigZag.update()

//#endregion

The example code demonstrates how to create a ZigZag indicator with customizable settings. It:

1. Creates a Settings object with user-defined parameters

2. Instantiates a ZigZag object using these settings

3. Updates the ZigZag on each bar to detect new pivot points

4. Automatically draws lines and labels when pivots are detected

This approach provides maximum flexibility while maintaining readability and ease of use.

Money Flow Divergence IndicatorOverview

The Money Flow Divergence Indicator is designed to help traders and investors identify key macroeconomic turning points by analyzing the relationship between U.S. M2 money supply growth and the S&P 500 Index (SPX). By comparing these two crucial economic indicators, the script highlights periods where market liquidity is outpacing or lagging behind stock market growth, offering potential buy and sell signals based on macroeconomic trends.

How It Works

1. Data Sources

S&P 500 Index (SPX500USD): Tracks the stock market performance.

U.S. M2 Money Supply (M2SL - Federal Reserve Economic Data): Represents available liquidity in the economy.

2. Growth Rate Calculation

SPX Growth: Percentage change in the S&P 500 index over time.

M2 Growth: Percentage change in M2 money supply over time.

Growth Gap (Delta): The difference between M2 growth and SPX growth, showing whether liquidity is fueling or lagging behind market performance.

3. Visualization

A histogram displays the growth gap over time:

Green Bars: M2 growth exceeds SPX growth (potential bullish signal).

Red Bars: SPX growth exceeds M2 growth (potential bearish signal).

A zero line helps distinguish between positive and negative growth gaps.

How to Use It

✅ Bullish Signal: When green bars appear consistently, indicating that liquidity is outpacing stock market growth. This suggests a favorable environment for buying or holding positions.

❌ Bearish Signal: When red bars appear consistently, meaning stock market growth outpaces liquidity expansion, signaling potential overvaluation or a market correction.

Best Timeframes for Analysis

This indicator works best on monthly timeframes (M) since it is designed for long-term investors and macro traders who focus on broad economic cycles.

Who Should Use This Indicator?

📈 Long-term investors looking for macroeconomic trends.

📊 Swing traders who incorporate liquidity analysis in their strategies.

💰 Portfolio managers assessing market liquidity conditions.

🚀 Use this indicator to stay ahead of market trends and make informed investment decisions based on macroeconomic liquidity shifts! 🚀

real_time_candlesIntroduction

The Real-Time Candles Library provides comprehensive tools for creating, manipulating, and visualizing custom timeframe candles in Pine Script. Unlike standard indicators that only update at bar close, this library enables real-time visualization of price action and indicators within the current bar, offering traders unprecedented insight into market dynamics as they unfold.

This library addresses a fundamental limitation in traditional technical analysis: the inability to see how indicators evolve between bar closes. By implementing sophisticated real-time data processing techniques, traders can now observe indicator movements, divergences, and trend changes as they develop, potentially identifying trading opportunities much earlier than with conventional approaches.

Key Features

The library supports two primary candle generation approaches:

Chart-Time Candles: Generate real-time OHLC data for any variable (like RSI, MACD, etc.) while maintaining synchronization with chart bars.

Custom Timeframe (CTF) Candles: Create candles with custom time intervals or tick counts completely independent of the chart's native timeframe.

Both approaches support traditional candlestick and Heikin-Ashi visualization styles, with options for moving average overlays to smooth the data.

Configuration Requirements

For optimal performance with this library:

Set max_bars_back = 5000 in your script settings

When using CTF drawing functions, set max_lines_count = 500, max_boxes_count = 500, and max_labels_count = 500

These settings ensure that you will be able to draw correctly and will avoid any runtime errors.

Usage Examples

Basic Chart-Time Candle Visualization

// Create real-time candles for RSI

float rsi = ta.rsi(close, 14)

Candle rsi_candle = candle_series(rsi, CandleType.candlestick)

// Plot the candles using Pine's built-in function

plotcandle(rsi_candle.Open, rsi_candle.High, rsi_candle.Low, rsi_candle.Close,

"RSI Candles", rsi_candle.candle_color, rsi_candle.candle_color)

Multiple Access Patterns

The library provides three ways to access candle data, accommodating different programming styles:

// 1. Array-based access for collection operations

Candle candles = candle_array(source)

// 2. Object-oriented access for single entity manipulation

Candle candle = candle_series(source)

float value = candle.source(Source.HLC3)

// 3. Tuple-based access for functional programming styles

= candle_tuple(source)

Custom Timeframe Examples

// Create 20-second candles with EMA overlay

plot_ctf_candles(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 20,

timezone = -5,

tied_open = true,

ema_period = 9,

enable_ema = true

)

// Create tick-based candles (new candle every 15 ticks)

plot_ctf_tick_candles(

source = close,

candle_type = CandleType.heikin_ashi,

number_of_ticks = 15,

timezone = -5,

tied_open = true

)

Advanced Usage with Custom Visualization

// Get custom timeframe candles without automatic plotting

CandleCTF my_candles = ctf_candles_array(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 30

)

// Apply custom logic to the candles

float ema_values = my_candles.ctf_ema(14)

// Draw candles and EMA using time-based coordinates

my_candles.draw_ctf_candles_time()

ema_values.draw_ctf_line_time(line_color = #FF6D00)

Library Components

Data Types

Candle: Structure representing chart-time candles with OHLC, polarity, and visualization properties

CandleCTF: Extended candle structure with additional time metadata for custom timeframes

TickData: Structure for individual price updates with time deltas

Enumerations

CandleType: Specifies visualization style (candlestick or Heikin-Ashi)

Source: Defines price components for calculations (Open, High, Low, Close, HL2, etc.)

SampleType: Sets sampling method (Time-based or Tick-based)

Core Functions

get_tick(): Captures current price as a tick data point

candle_array(): Creates an array of candles from price updates

candle_series(): Provides a single candle based on latest data

candle_tuple(): Returns OHLC values as a tuple

ctf_candles_array(): Creates custom timeframe candles without rendering

Visualization Functions

source(): Extracts specific price components from candles

candle_ctf_to_float(): Converts candle data to float arrays

ctf_ema(): Calculates exponential moving averages for candle arrays

draw_ctf_candles_time(): Renders candles using time coordinates

draw_ctf_candles_index(): Renders candles using bar index coordinates

draw_ctf_line_time(): Renders lines using time coordinates

draw_ctf_line_index(): Renders lines using bar index coordinates

Technical Implementation Notes

This library leverages Pine Script's varip variables for state management, creating a sophisticated real-time data processing system. The implementation includes:

Efficient tick capturing: Samples price at every execution, maintaining temporal tracking with time deltas

Smart state management: Uses a hybrid approach with mutable updates at index 0 and historical preservation at index 1+

Temporal synchronization: Manages two time domains (chart time and custom timeframe)

The tooltip implementation provides crucial temporal context for custom timeframe visualizations, allowing users to understand exactly when each candle formed regardless of chart timeframe.

Limitations

Custom timeframe candles cannot be backtested due to Pine Script's limitations with historical tick data

Real-time visualization is only available during live chart updates

Maximum history is constrained by Pine Script's array size limits

Applications

Indicator visualization: See how RSI, MACD, or other indicators evolve in real-time

Volume analysis: Create custom volume profiles independent of chart timeframe

Scalping strategies: Identify short-term patterns with precisely defined time windows

Volatility measurement: Track price movement characteristics within bars

Custom signal generation: Create entry/exit signals based on custom timeframe patterns

Conclusion

The Real-Time Candles Library bridges the gap between traditional technical analysis (based on discrete OHLC bars) and the continuous nature of market movement. By making indicators more responsive to real-time price action, it gives traders a significant edge in timing and decision-making, particularly in fast-moving markets where waiting for bar close could mean missing important opportunities.

Whether you're building custom indicators, researching price patterns, or developing trading strategies, this library provides the foundation for sophisticated real-time analysis in Pine Script.

Implementation Details & Advanced Guide

Core Implementation Concepts

The Real-Time Candles Library implements a sophisticated event-driven architecture within Pine Script's constraints. At its heart, the library creates what's essentially a reactive programming framework handling continuous data streams.

Tick Processing System

The foundation of the library is the get_tick() function, which captures price updates as they occur:

export get_tick(series float source = close, series float na_replace = na)=>

varip float price = na

varip int series_index = -1

varip int old_time = 0

varip int new_time = na

varip float time_delta = 0

// ...

This function:

Samples the current price

Calculates time elapsed since last update

Maintains a sequential index to track updates

The resulting TickData structure serves as the fundamental building block for all candle generation.

State Management Architecture

The library employs a sophisticated state management system using varip variables, which persist across executions within the same bar. This creates a hybrid programming paradigm that's different from standard Pine Script's bar-by-bar model.

For chart-time candles, the core state transition logic is:

// Real-time update of current candle

candle_data := Candle.new(Open, High, Low, Close, polarity, series_index, candle_color)

candles.set(0, candle_data)

// When a new bar starts, preserve the previous candle

if clear_state

candles.insert(1, candle_data)

price.clear()

// Reset state for new candle

Open := Close

price.push(Open)

series_index += 1

This pattern of updating index 0 in real-time while inserting completed candles at index 1 creates an elegant solution for maintaining both current state and historical data.

Custom Timeframe Implementation

The custom timeframe system manages its own time boundaries independent of chart bars:

bool clear_state = switch settings.sample_type

SampleType.Ticks => cumulative_series_idx >= settings.number_of_ticks

SampleType.Time => cumulative_time_delta >= settings.number_of_seconds

This dual-clock system synchronizes two time domains:

Pine's execution clock (bar-by-bar processing)

The custom timeframe clock (tick or time-based)

The library carefully handles temporal discontinuities, ensuring candle formation remains accurate despite irregular tick arrival or market gaps.

Advanced Usage Techniques

1. Creating Custom Indicators with Real-Time Candles

To develop indicators that process real-time data within the current bar:

// Get real-time candles for your data

Candle rsi_candles = candle_array(ta.rsi(close, 14))

// Calculate indicator values based on candle properties

float signal = ta.ema(rsi_candles.first().source(Source.Close), 9)

// Detect patterns that occur within the bar

bool divergence = close > close and rsi_candles.first().Close < rsi_candles.get(1).Close

2. Working with Custom Timeframes and Plotting

For maximum flexibility when visualizing custom timeframe data:

// Create custom timeframe candles

CandleCTF volume_candles = ctf_candles_array(

source = volume,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 60

)

// Convert specific candle properties to float arrays

float volume_closes = volume_candles.candle_ctf_to_float(Source.Close)

// Calculate derived values

float volume_ema = volume_candles.ctf_ema(14)

// Create custom visualization

volume_candles.draw_ctf_candles_time()

volume_ema.draw_ctf_line_time(line_color = color.orange)

3. Creating Hybrid Timeframe Analysis

One powerful application is comparing indicators across multiple timeframes:

// Standard chart timeframe RSI

float chart_rsi = ta.rsi(close, 14)

// Custom 5-second timeframe RSI

CandleCTF ctf_candles = ctf_candles_array(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 5

)

float fast_rsi_array = ctf_candles.candle_ctf_to_float(Source.Close)

float fast_rsi = fast_rsi_array.first()

// Generate signals based on divergence between timeframes

bool entry_signal = chart_rsi < 30 and fast_rsi > fast_rsi_array.get(1)

Final Notes

This library represents an advanced implementation of real-time data processing within Pine Script's constraints. By creating a reactive programming framework for handling continuous data streams, it enables sophisticated analysis typically only available in dedicated trading platforms.

The design principles employed—including state management, temporal processing, and object-oriented architecture—can serve as patterns for other advanced Pine Script development beyond this specific application.

------------------------

Library "real_time_candles"

A comprehensive library for creating real-time candles with customizable timeframes and sampling methods.

Supports both chart-time and custom-time candles with options for candlestick and Heikin-Ashi visualization.

Allows for tick-based or time-based sampling with moving average overlay capabilities.

get_tick(source, na_replace)

Captures the current price as a tick data point

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

na_replace (float) : Optional - Value to use when source is na

Returns: TickData structure containing price, time since last update, and sequential index

candle_array(source, candle_type, sync_start, bullish_color, bearish_color)

Creates an array of candles based on price updates

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

candle_type (simple CandleType) : Optional - Type of candle chart to create (candlestick or Heikin-Ashi)

sync_start (simple bool) : Optional - Whether to synchronize with the start of a new bar

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: Array of Candle objects ordered with most recent at index 0

candle_series(source, candle_type, wait_for_sync, bullish_color, bearish_color)

Provides a single candle based on the latest price data

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

candle_type (simple CandleType) : Optional - Type of candle chart to create (candlestick or Heikin-Ashi)

wait_for_sync (simple bool) : Optional - Whether to wait for a new bar before starting

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: A single Candle object representing the current state

candle_tuple(source, candle_type, wait_for_sync, bullish_color, bearish_color)

Provides candle data as a tuple of OHLC values

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

candle_type (simple CandleType) : Optional - Type of candle chart to create (candlestick or Heikin-Ashi)

wait_for_sync (simple bool) : Optional - Whether to wait for a new bar before starting

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: Tuple representing current candle values

method source(self, source, na_replace)

Extracts a specific price component from a Candle

Namespace types: Candle

Parameters:

self (Candle)

source (series Source) : Type of price data to extract (Open, High, Low, Close, or composite values)

na_replace (float) : Optional - Value to use when source value is na

Returns: The requested price value from the candle

method source(self, source)

Extracts a specific price component from a CandleCTF

Namespace types: CandleCTF

Parameters:

self (CandleCTF)

source (simple Source) : Type of price data to extract (Open, High, Low, Close, or composite values)

Returns: The requested price value from the candle as a varip

method candle_ctf_to_float(self, source)

Converts a specific price component from each CandleCTF to a float array

Namespace types: array

Parameters:

self (array)

source (simple Source) : Optional - Type of price data to extract (defaults to Close)

Returns: Array of float values extracted from the candles, ordered with most recent at index 0

method ctf_ema(self, ema_period)

Calculates an Exponential Moving Average for a CandleCTF array

Namespace types: array

Parameters:

self (array)

ema_period (simple float) : Period for the EMA calculation

Returns: Array of float values representing the EMA of the candle data, ordered with most recent at index 0

method draw_ctf_candles_time(self, sample_type, number_of_ticks, number_of_seconds, timezone)

Renders custom timeframe candles using bar time coordinates

Namespace types: array

Parameters:

self (array)

sample_type (simple SampleType) : Optional - Method for sampling data (Time or Ticks), used for tooltips

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks), used for tooltips

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time), used for tooltips

timezone (simple int) : Optional - Timezone offset from UTC (-12 to +12), used for tooltips

Returns: void - Renders candles on the chart using time-based x-coordinates

method draw_ctf_candles_index(self, sample_type, number_of_ticks, number_of_seconds, timezone)

Renders custom timeframe candles using bar index coordinates

Namespace types: array

Parameters:

self (array)

sample_type (simple SampleType) : Optional - Method for sampling data (Time or Ticks), used for tooltips

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks), used for tooltips

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time), used for tooltips

timezone (simple int) : Optional - Timezone offset from UTC (-12 to +12), used for tooltips

Returns: void - Renders candles on the chart using index-based x-coordinates

method draw_ctf_line_time(self, source, line_size, line_color)

Renders a line representing a price component from the candles using time coordinates

Namespace types: array

Parameters:

self (array)

source (simple Source) : Optional - Type of price data to extract (defaults to Close)

line_size (simple int) : Optional - Width of the line

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using time-based x-coordinates

method draw_ctf_line_time(self, line_size, line_color)

Renders a line from a varip float array using time coordinates

Namespace types: array

Parameters:

self (array)

line_size (simple int) : Optional - Width of the line, defaults to 2

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using time-based x-coordinates

method draw_ctf_line_index(self, source, line_size, line_color)

Renders a line representing a price component from the candles using index coordinates

Namespace types: array

Parameters:

self (array)

source (simple Source) : Optional - Type of price data to extract (defaults to Close)

line_size (simple int) : Optional - Width of the line

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using index-based x-coordinates

method draw_ctf_line_index(self, line_size, line_color)

Renders a line from a varip float array using index coordinates

Namespace types: array

Parameters:

self (array)

line_size (simple int) : Optional - Width of the line, defaults to 2

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using index-based x-coordinates

plot_ctf_tick_candles(source, candle_type, number_of_ticks, timezone, tied_open, ema_period, bullish_color, bearish_color, line_width, ema_color, use_time_indexing)

Plots tick-based candles with moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_ticks (simple int) : Number of ticks per candle

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

ema_period (simple float) : Period for the exponential moving average

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

line_width (simple int) : Optional - Width of the moving average line, defaults to 2

ema_color (color) : Optional - Color of the moving average line

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart with EMA overlay

plot_ctf_tick_candles(source, candle_type, number_of_ticks, timezone, tied_open, bullish_color, bearish_color, use_time_indexing)

Plots tick-based candles without moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_ticks (simple int) : Number of ticks per candle

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart without moving average

plot_ctf_time_candles(source, candle_type, number_of_seconds, timezone, tied_open, ema_period, bullish_color, bearish_color, line_width, ema_color, use_time_indexing)

Plots time-based candles with moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_seconds (simple float) : Time duration per candle in seconds

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

ema_period (simple float) : Period for the exponential moving average

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

line_width (simple int) : Optional - Width of the moving average line, defaults to 2

ema_color (color) : Optional - Color of the moving average line

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart with EMA overlay

plot_ctf_time_candles(source, candle_type, number_of_seconds, timezone, tied_open, bullish_color, bearish_color, use_time_indexing)

Plots time-based candles without moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_seconds (simple float) : Time duration per candle in seconds

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart without moving average

plot_ctf_candles(source, candle_type, sample_type, number_of_ticks, number_of_seconds, timezone, tied_open, ema_period, bullish_color, bearish_color, enable_ema, line_width, ema_color, use_time_indexing)

Unified function for plotting candles with comprehensive options

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Optional - Type of candle chart to display

sample_type (simple SampleType) : Optional - Method for sampling data (Time or Ticks)

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks)

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time)

timezone (simple int) : Optional - Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Optional - Whether to tie open price to close of previous candle

ema_period (simple float) : Optional - Period for the exponential moving average

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

enable_ema (bool) : Optional - Whether to display the EMA overlay

line_width (simple int) : Optional - Width of the moving average line, defaults to 2

ema_color (color) : Optional - Color of the moving average line

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart with optional EMA overlay

ctf_candles_array(source, candle_type, sample_type, number_of_ticks, number_of_seconds, tied_open, bullish_color, bearish_color)

Creates an array of custom timeframe candles without rendering them

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to create (candlestick or Heikin-Ashi)

sample_type (simple SampleType) : Method for sampling data (Time or Ticks)

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks)

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time)

tied_open (simple bool) : Optional - Whether to tie open price to close of previous candle

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: Array of CandleCTF objects ordered with most recent at index 0

Candle

Structure representing a complete candle with price data and display properties

Fields:

Open (series float) : Opening price of the candle

High (series float) : Highest price of the candle

Low (series float) : Lowest price of the candle

Close (series float) : Closing price of the candle

polarity (series bool) : Boolean indicating if candle is bullish (true) or bearish (false)

series_index (series int) : Sequential index identifying the candle in the series

candle_color (series color) : Color to use when rendering the candle

ready (series bool) : Boolean indicating if candle data is valid and ready for use

TickData

Structure for storing individual price updates

Fields:

price (series float) : The price value at this tick

time_delta (series float) : Time elapsed since the previous tick in milliseconds

series_index (series int) : Sequential index identifying this tick

CandleCTF

Structure representing a custom timeframe candle with additional time metadata

Fields:

Open (series float) : Opening price of the candle

High (series float) : Highest price of the candle

Low (series float) : Lowest price of the candle

Close (series float) : Closing price of the candle

polarity (series bool) : Boolean indicating if candle is bullish (true) or bearish (false)

series_index (series int) : Sequential index identifying the candle in the series

open_time (series int) : Timestamp marking when the candle was opened (in Unix time)

time_delta (series float) : Duration of the candle in milliseconds

candle_color (series color) : Color to use when rendering the candle

Mogwai Method with RSI and EMA - BTCUSD 15mThis is a custom TradingView indicator designed for trading Bitcoin (BTCUSD) on a 15-minute timeframe. It’s based on the Mogwai Method—a mean-reversion strategy—enhanced with the Relative Strength Index (RSI) for momentum confirmation. The indicator generates buy and sell signals, visualized as green and red triangle arrows on the chart, to help identify potential entry and exit points in the volatile cryptocurrency market.

Components

Bollinger Bands (BB):

Purpose: Identifies overextended price movements, signaling potential reversions to the mean.

Parameters:

Length: 20 periods (standard for mean-reversion).

Multiplier: 2.2 (slightly wider than the default 2.0 to suit BTCUSD’s volatility).

Role:

Buy signal when price drops below the lower band (oversold).

Sell signal when price rises above the upper band (overbought).

Relative Strength Index (RSI):

Purpose: Confirms momentum to filter out false signals from Bollinger Bands.

Parameters:

Length: 14 periods (classic setting, effective for crypto).

Overbought Level: 70 (price may be overextended upward).

Oversold Level: 30 (price may be overextended downward).

Role:

Buy signal requires RSI < 30 (oversold).

Sell signal requires RSI > 70 (overbought).

Exponential Moving Averages (EMAs) (Plotted but not currently in signal logic):

Purpose: Provides trend context (included in the script for visualization, optional for signal filtering).

Parameters:

Fast EMA: 9 periods (short-term trend).

Slow EMA: 50 periods (longer-term trend).

Role: Can be re-added to filter signals (e.g., buy only when Fast EMA > Slow EMA).

Signals (Triangles):

Buy Signal: Green upward triangle below the bar when price is below the lower Bollinger Band and RSI is below 30.

Sell Signal: Red downward triangle above the bar when price is above the upper Bollinger Band and RSI is above 70.

How It Works

The indicator combines Bollinger Bands and RSI to spot mean-reversion opportunities:

Buy Condition: Price breaks below the lower Bollinger Band (indicating oversold conditions), and RSI confirms this with a reading below 30.

Sell Condition: Price breaks above the upper Bollinger Band (indicating overbought conditions), and RSI confirms this with a reading above 70.

The strategy assumes that extreme price movements in BTCUSD will often revert to the mean, especially in choppy or ranging markets.

Visual Elements

Green Upward Triangles: Appear below the candlestick to indicate a buy signal.

Red Downward Triangles: Appear above the candlestick to indicate a sell signal.

Bollinger Bands: Gray lines (upper, middle, lower) plotted for reference.

EMAs: Blue (Fast) and Orange (Slow) lines for trend visualization.

How to Use the Indicator

Setup

Open TradingView:

Log into TradingView and select a BTCUSD chart from a supported exchange (e.g., Binance, Coinbase, Bitfinex).

Set Timeframe:

Switch the chart to a 15-minute timeframe (15m).

Add the Indicator:

Open the Pine Editor (bottom panel in TradingView).

Copy and paste the script provided.

Click “Add to Chart” to apply it.

Verify Display:

You should see Bollinger Bands (gray), Fast EMA (blue), Slow EMA (orange), and buy/sell triangles when conditions are met.

Trading Guidelines

Buy Signal (Green Triangle Below Bar):

What It Means: Price is oversold, potentially ready to bounce back toward the Bollinger Band middle line.

Action:

Enter a long position (buy BTCUSD).

Set a take-profit near the middle Bollinger Band (bb_middle) or a resistance level.

Place a stop-loss 1-2% below the entry (or based on ATR, e.g., ta.atr(14) * 2).

Best Context: Works well in ranging markets; avoid during strong downtrends.

Sell Signal (Red Triangle Above Bar):

What It Means: Price is overbought, potentially ready to drop back toward the middle line.

Action:

Enter a short position (sell BTCUSD) or exit a long position.

Set a take-profit near the middle Bollinger Band or a support level.

Place a stop-loss 1-2% above the entry.

Best Context: Effective in ranging markets; avoid during strong uptrends.

Trend Filter (Optional):

To reduce false signals in trending markets, you can modify the script:

Add and ema_fast > ema_slow to the buy condition (only buy in uptrends).

Add and ema_fast < ema_slow to the sell condition (only sell in downtrends).

Check the Fast EMA (blue) vs. Slow EMA (orange) alignment visually.

Tips for BTCUSD on 15-Minute Charts

Volatility: BTCUSD can be erratic. If signals are too frequent, increase bb_mult (e.g., to 2.5) or adjust RSI levels (e.g., 75/25).

Confirmation: Use volume spikes or candlestick patterns (e.g., doji, engulfing) to confirm signals.

Time of Day: Mean-reversion works best during low-volume periods (e.g., Asian session in crypto).

Backtesting: Use TradingView’s Strategy Tester (convert to a strategy by adding entry/exit logic) to evaluate performance with historical BTCUSD data up to March 13, 2025.

Risk Management

Position Size: Risk no more than 1-2% of your account per trade.

Stop Losses: Always use stops to protect against BTCUSD’s sudden moves.

Avoid Overtrading: Wait for clear signals; don’t force trades in choppy or unclear conditions.

Example Scenario

Chart: BTCUSD, 15-minute timeframe.

Buy Signal: Price drops to $58,000, below the lower Bollinger Band, RSI at 28. A green triangle appears.

Action: Buy at $58,000, target $59,000 (middle BB), stop at $57,500.

Sell Signal: Price rises to $60,500, above the upper Bollinger Band, RSI at 72. A red triangle appears.

Action: Sell at $60,500, target $59,500 (middle BB), stop at $61,000.

This indicator is tailored for mean-reversion trading on BTCUSD. Let me know if you’d like to tweak it further (e.g., add filters, alerts, or alternative indicators)!

2xSPYTIPS Strategy by Fra public versionThis is a test strategy with S&P500, open source so everyone can suggest everything, I'm open to any advice.

Rules of the "2xSPYTIPS" Strategy :

This trading strategy is designed to operate on the S&P 500 index and the TIPS ETF. Here’s how it works:

1. Buy Conditions ("BUY"):

- The S&P 500 must be above its **200-day simple moving average (SMA 200)**.

- This condition is checked at the **end of each month**.

2. Position Management:

- If leverage is enabled (**2x leverage**), the purchase quantity is increased based on a configurable percentage.

3. Take Profit:

- A **Take Profit** is set at a fixed percentage above the entry price.

4. Visualization & Alerts:

- The **SMA 200** for both S&P 500 and TIPS is plotted on the chart.

- A **BUY signal** appears visually and an alert is triggered.

What This Strategy Does NOT Do

- It does not use a **Stop Loss** or **Trailing Stop**.

- It does not directly manage position exits except through Take Profit.

PT Least Squares Moving AveragePT LSMA Multi-Period Indicator

The PT Least Squares Moving Average (LSMA) Multi-Period Indicator is a powerful tool designed for investors who want to track market trends across multiple time horizons in a single, convenient indicator. This indicator calculates the LSMA for four different periods— 25 bars, 50 bars, 450 bars, and 500 bars providing a comprehensive view of short-term and long-term market movements.

Key Features:

- Multi-Timeframe Trend Analysis: Tracks both short-term (25 & 50 bars) and long-term (450 & 500 bars) market trends, helping investors make informed decisions.

- Smoothing Capability: The LSMA reduces noise by fitting a linear regression line to past price data, offering a clearer trend direction compared to traditional moving averages.

- One-Indicator Solution: Combines multiple LSMA periods into a single chart, reducing clutter and enhancing visual clarity.

- Versatile Applications: Suitable for trend identification, market timing, and spotting potential reversals across different timeframes.

- Customizable Styling: Allows users to customize colors and line styles for each period to suit their preferences.

How to Use:

1. Short-Term Trends (25 & 50 bars):Ideal for identifying recent price movements and short-term trade opportunities.

2. Long-Term Trends (450 & 500 bars): Helps investors gauge broader market sentiment and position themselves accordingly for longer holding periods.

3. Trend Confirmation: When shorter LSMA periods cross above longer ones, it may signal bullish momentum, whereas the opposite may indicate bearish sentiment.

4. Support and Resistance: The LSMA lines can act as dynamic support and resistance levels during trending markets.

Best For:

- Long-term investors looking to align their positions with dominant market trends.

- Swing traders seeking confirmation from multiple time horizons.

- Portfolio managers tracking price momentum across various investment durations.

This LSMA Multi-Period Indicator equips investors with a well-rounded perspective on price movements, offering a strategic edge in navigating market cycles with confidence.

Created by Prince Thomas

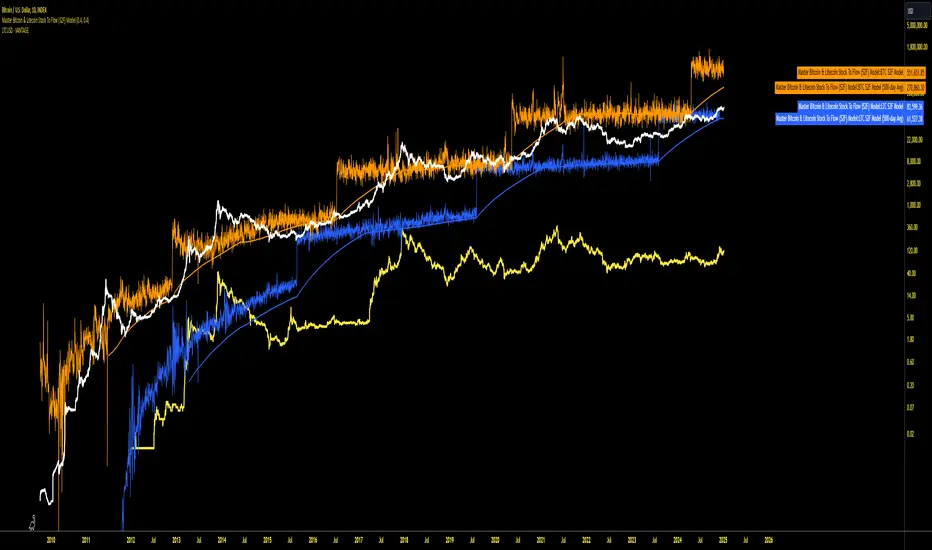

Master Bitcoin & Litecoin Stock To Flow (S2F) ModelMaster Bitcoin & Litecoin Stock-to-Flow (S2F) Model

This indicator visualizes the Stock-to-Flow (S2F) models for Bitcoin (BTC) and Litecoin (LTC) based on Plan B's methodology. It calculates S2F and projects price models for both assets, incorporating daily changes in circulating supply. The script is designed exclusively for daily timeframes.

Features:

LTC & BTC S2F Models:

Calculates Stock-to-Flow values for both assets using daily new supply and circulating supply data.

Models S2F values with a customizable multiplier for precise adjustments.

500-Day Moving Average Models:

Smoothens the S2F model by applying a 500-day (18-month) moving average, providing a long-term trend perspective.

Customizable Inputs:

Adjust LTC and BTC multipliers to fine-tune the models.

Alert for Timeframe:

Alerts users to switch to the daily timeframe if another period is selected.

Plots:

LTC S2F Model: Blue line representing Litecoin’s calculated S2F-based price model.

BTC S2F Model: Orange line representing Bitcoin’s calculated S2F-based price model.

500-Day Avg Models: Smoothened S2F models for both LTC and BTC.

Notes:

Requires daily timeframe (1D) for accurate calculations.

Supply data is sourced from GLASSNODE:LTC_SUPPLY and GLASSNODE:BTC_SUPPLY.

Disclaimer:

This model is derived from Plan B's S2F methodology and is intended for educational and entertainment purposes only. It does not reflect official predictions or financial advice. Always conduct your own research before making investment decisions.

TICK Charting & DivergencesOverview

The TICK index measures the number of NYSE stocks making an uptick versus a downtick. This indicator identifies divergences between price action and TICK readings, potentially signaling trend reversals.

Key Features

Real-time TICK monitoring during market hours (9:30 AM - 4:00 PM ET)

Customizable smoothing factor for TICK values

Regular and hidden divergences detection

Reference lines at ±500 and ±1000 levels

Current TICK value display

TICK Internals Interpretation

Above +1000: Strong buying pressure, potential exhaustion

Above +500: Moderate buying pressure

Below -500: Moderate selling pressure

Below -1000: Strong selling pressure, potential exhaustion

Best Practices

Use in conjunction with support/resistance levels, market trend direction, and time of day.

Higher probability setups with multiple timeframe confirmation, divergence at key price levels, and extreme TICK readings (±1000).

Settings Optimization

Smoothing Factor: 1-3 (lower for faster signals)

Pivot Lookback: 5-10 bars (adjust based on timeframe)

Range: 5-60 bars (wider for longer-term signals)

Warning Signs

Multiple failed divergences

Choppy price action

Low volume periods

Major news events pending

Remember: TICK divergences are not guaranteed signals. Always use proper risk management and combine with other technical analysis tools.

Psychological Levels- Rounding Numbers Psychological Levels Indicator

Overview:

The Psychological Levels Indicator automatically identifies and plots significant price levels based on psychological thresholds, which are key areas where market participants often focus their attention. These levels act as potential support or resistance zones due to human behavioral tendencies to round off numbers. This indicator dynamically adjusts the levels based on the stock's price range and ensures seamless visibility across the chart.

Key Features:

Dynamic Step Sizes:

The indicator adjusts the levels dynamically based on the stock price:

For prices below 500: Levels are spaced at 10.

For prices between 500 and 3000: Levels are spaced at 50, 100, and 1000.

For prices between 3000 and 10,000: Levels are spaced at 100 and 1000.

For prices above 10,000: Levels are spaced at 500 and 1000.

Extended Visibility:

The plotted levels are extended across the entire chart for improved visualization, ensuring traders can easily monitor these critical zones over time.

Customization Options:

Line Color: Choose the color for the levels to suit your charting style.

Line Style: Select from solid, dashed, or dotted lines.

Line Width: Adjust the thickness of the lines for better clarity.

Clean and Efficient Design:

The indicator only plots levels relevant to the visible chart range, avoiding unnecessary clutter and ensuring a clean workspace.

How It Works:

It calculates the relevant step sizes based on the price:

Smaller step sizes for lower-priced stocks.

Larger step sizes for higher-priced stocks.

Primary, secondary, and (if applicable) tertiary levels are plotted dynamically:

Primary Levels: The most granular levels based on the stock price.

Secondary Levels: Higher-order levels for broader significance.

Tertiary Levels: Additional levels for lower-priced stocks to enhance detail.

These levels are plotted across the chart, allowing traders to visualize key psychological areas effortlessly.

Use Cases:

Day Trading: Identify potential intraday support and resistance levels.

Swing Trading: Recognize key price zones where trends may pause or reverse.

Long-Term Investing: Gain insights into significant price zones for entry or exit strategies.

Scatter PlotThe Price Volume Scatter Plot publication aims to provide intrabar detail as a Scatter Plot .

🔶 USAGE

A dot is drawn at every intrabar close price and its corresponding volume , as can seen in the following example:

Price is placed against the white y-axis, where volume is represented on the orange x-axis.

🔹 More detail

A Scatter Plot can be beneficial because it shows more detail compared with a Volume Profile (seen at the right of the Scatter Plot).

The Scatter Plot is accompanied by a "Line of Best Fit" (linear regression line) to help identify the underlying direction, which can be helpful in interpretation/evaluation.

It can be set as a screener by putting multiple layouts together.

🔹 Easier Interpretation

Instead of analysing the 1-minute chart together with volume, this can be visualised in the Scatter Plot, giving a straightforward and easy-to-interpret image of intrabar volume per price level.

One of the scatter plot's advantages is that volumes at the same price level are added to each other.

A dot on the scatter plot represents the cumulated amount of volume at that particular price level, regardless of whether the price closed one or more times at that price level.

Depending on the setting "Direction" , which sets the direction of the Volume-axis, users can hoover to see the corresponding price/volume.

🔹 Highest Intrabar Volume Values

Users can display up to 5 last maximum intrabar volume values, together with the intrabar timeframe (Res)

🔹 Practical Examples

When we divide the recent bar into three parts, the following can be noticed:

Price spends most of its time in the upper part, with relative medium-low volume, since the intrabar close prices are mostly situated in the upper left quadrant.

Price spends a shorter time in the middle part, with relative medium-low volume.

Price moved rarely below 61800 (the lowest part), but it was associated with high volume. None of the intrabar close prices reached the lowest area, and the price bounced back.

In the following example, the latest weekly candle shows a rejection of the 45.8 - 48.5K area, with the highest volume at the 45.8K level.

The next three successive candles show a declining maximum intrabar volume, after which the price broke through the 45.8K area.

🔹 Visual Options

There are many visual options available.

🔹 Change Direction

The Scatter Plot can be set in 4 different directions.

🔶 NOTES

🔹 Notes

The script uses the maximum available resources to draw the price/volume dots, which are 500 boxes and 500 labels. When the population size exceeds 1000, a warning is provided ( Not all data is shown ); otherwise, only the population size is displayed.

The Scatter Plot ideally needs a chart which contains at least 100 bars. When it contains less, a warning will be shown: bars < 100, not all data is shown

🔹 LTF Settings

When 'Auto' is enabled ( Settings , LTF ), the LTF will be the nearest possible x times smaller TF than the current TF. When 'Premium' is disabled, the minimum TF will always be 1 minute to ensure TradingView plans lower than Premium don't get an error.

Examples with current Daily TF (when Premium is enabled):

500 : 3 minute LTF

1500 (default): 1 minute LTF

5000: 30 seconds LTF (1 minute if Premium is disabled)

🔶 SETTINGS

Direction: Direction of Volume-axis; Left, Right, Up or Down

🔹 LTF

LTF: LTF setting

Auto + multiple: Adjusts the initial set LTF

Premium: Enable when your TradingView plan is Premium or higher

🔹 Character

Character: Style of Price/Volume dot

Fade: Increasing this number fades dots at lower price/volume

Color

🔹 Linear Regression

Toggle (enable/disable), color, linestyle

Center Cross: Toggle, color