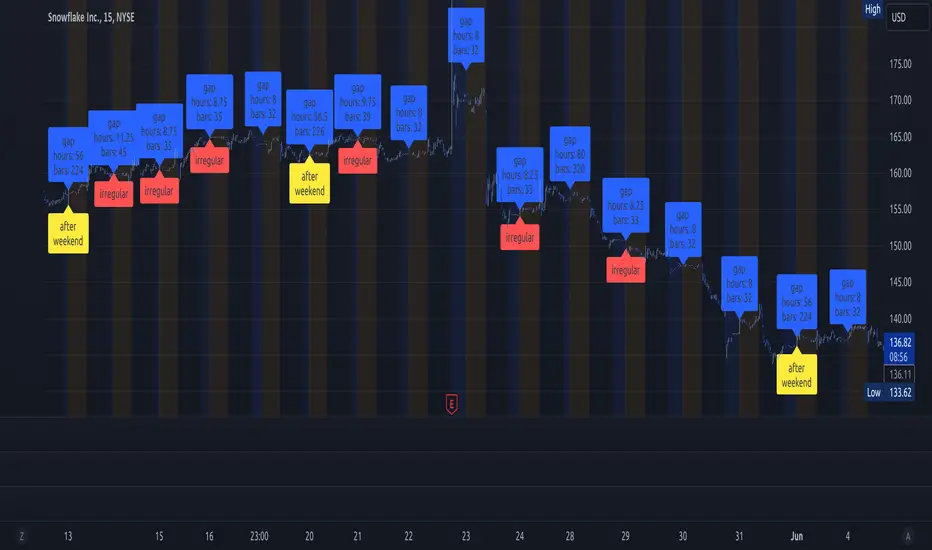

lib_session_gapsLibrary "lib_session_gaps"

simple lib to calculate the gaps between sessions

time_gap()

calculates the time gap between this and previous session (in case of irregular end of previous session, considering extended sessions)

Returns: the time gap between this and previous session in ms (time - time_close )

bar_gap()

calculates the bars missing between this and previous session (in case of irregular end of previous session, considering extended sessions)

Returns: the bars virtually missing between this and previous session (time gap / bar size in ms)

Thư viện Pine Script®