Scott’s ATR volatility histogram with smoothingATR shows volatility. The sma of the ATR gives a base line for whether volatility is increasing or decreasing. When ATR passes below the sma, the histogram goes red and shows that volatility is lower than the average volatilty over the last 200 (default) periods. The sma represents the zero line. I have added a 'smoothing' sma to the histogram values because it will help as a trade entry filter.... "Is the current volatility expansion (or contraction) momentum increasing or decreasing at this time" When the histogram value is above the smoothing line, volatility expansion momentum is increasing: a confirmation that the buy signal (derived from another indicator) is valid. Volatility expansion momentum also serves as a valid short entry confirmation. Volatility contraction momentum conversely tells one that a trend is not developing.

Tìm kiếm tập lệnh với "Volatility"

RaymondTrending [Qanexra] - Advanced Volatility GaugePrice direction tells you where the market is going, but it doesn't tell you if it has the gas to get there.

RaymondTrending is a proprietary volatility instrument designed to measure the raw "energy" of the market. Unlike standard indicators that lag significantly, this tool uses a rapid-response composite algorithm to detect immediate shifts in market volatility.

What lies inside? The core engine is built on a multi-layered calculation of market range. It filters out static noise to provide a single, clean data stream representing the true "pulse" of the asset.

How to use it:

Rising Line: Volatility is expanding. The current trend (up or down) is backed by real volume and energy.

Falling Line: Volatility is collapsing. The market is entering a consolidation or "squeeze" phase.

Spikes: Sudden spikes often indicate breakout events or climatic tops/bottoms.

Access: This is a closed-source tool. Please contact Qanexra for access.

7D Historical Volatility (Regimes + Stats) - ChrrizzyHere’s what that indicator does—at a glance:

### Core idea

It computes **7-day Historical Volatility (HV)** from **daily** log returns (annualized), then shows:

* the **HV line** and its **30-day average**,

* colored **volatility regimes** (Low / Normal / High / Extreme) with thresholds you set,

* a compact **status panel** (top-right, nudged left) with current stats and time-in-zone.

### Calculations

* **HV (7D)**: `stdev(log(close/close ), 7) * sqrt(365) * 100`, always from **daily data** via `request.security`, so it’s consistent on any chart timeframe.

* **Regimes** (defaults):

Low < 25% • Normal 25–50% • High 50–70% • Extreme > 70% (all editable).

* **30-day avg**: SMA of HV.

* **Time in zone (% over window)**: SMA of boolean flags (e.g., in Low=1 else 0) over `statsWin` days (default 300).

* **Rolling median HV**: 50th percentile over `statsWin`.

### What you see on the chart

* **HV line** (bold) + **30-day HV** (lighter).

* **Horizontal dashed lines** at your regime thresholds.

* **Background shading** that changes with the current regime (green/blue/orange/red).

### Panel (top-right)

Shows:

* BTC Price (daily close)

* Current HV

* 30-day Avg HV

* Median HV (over window)

* Current **Regime**

* A two-line summary: **% of time spent** in Low / Normal / High / Extreme over the chosen window.

The panel is shifted slightly left using a hidden spacer column; tweak the **“Panel right padding (chars)”** input to move it.

### Alerts (ready to use)

* **HV crossed up Low**

* **HV crossed down Low**

* **HV crossed up High**

* **HV crossed up Extreme**

### Inputs you can tune

* `HV Lookback (days)` (default 7)

* `Average HV (days)` (default 30)

* Thresholds: Low/High/Extreme

* `Stats Window (days)` (default 300)

* Panel padding, toggle table/zones on/off.

### How to use it

* **Context**: quickly see if BTC is in **compressed** (Low) or **stressed** (High/Extreme) volatility.

* **Regime cross alerts**: get notified when volatility **expands** from Low (potential breakout conditions) or pushes into High/Extreme (risk increases).

* **Stats/median**: compare today’s HV to its typical level over your lookback window.

If you want, I can add an **HV percentile rank** (e.g., “Current HV is at the 38th percentile over 300d”) or mirror the **low-vol breakout signal** from Script A into this panel.

Ultimate Volatility Scanner by NHBprod - Requested by Client!Hey Everyone!

I created another script to add to my growing library of strategies and indicators that I use for automated crypto and stock trading! This strategy is for BITCOIN but can be used on any stock or crypto. This was requested by a client so I thought I should create it and hopefully build off of it and build variants!

This script gets and compares the 14-day volatility using the ATR percentage for a list of cryptocurrencies and stocks. Cryptocurrencies are preloaded into the script, and the script will show you the TOP 5 coins in terms of volatility, and then compares it to the Bitcoin volatility as a reference. It updates these values once per day using daily timeframe data from TradingView. The coins are then sorted in descending order by their volatility.

If you don't want to use the preloaded set of coins, you have the option of inputting your own coins AND/OR stocks!

Let me know your thoughts.

Roger & Satchell Estimator Historical Volatility Bands [Loxx]Roger & Satchell Estimator Historical Volatility Bands are constructed using:

Average as the middle line.

Upper and lower bands using theRoger & Satchell Estimator Historical Volatility Bands for bands calculation.

What is Roger & Satchell Estimator Historical Volatility?

The Rogers–Satchell estimator does not handle opening jumps; therefore, it underestimates the volatility. It accurately explains the volatility portion that can be attributed entirely to a trend in the price evolution. Rogers and Satchell try to embody the frequency of price observations in the model in order to overcome the drawback. They claim that the corrected estimator outperforms the uncorrected one in a study based on simulated data.

RSEHV = sqrt((Z/n) * sum((log(high/close)*log(high/open)) + (log(low/close)*log(low/open))))

The color of the middle line, unlike the bands colors, has 3 colors. When colors of the bands are the same, then the middle line has the same color, otherwise it's white.

Included

Alerts

Signals

Loxx's Expanded Source Types

Bar coloring

ATR Volatility Spectrum

This indicator estimates price volatility and it is based on ATR only.

The advantage of this indicator is that it can be used with any pair, any time frame.

The fluctuations of a short period ATR with respect to a gently ATR with high period

are calculated.

The only parameters are the periods of the reference ATR and fast ATR, which could be

safely let untouched and modified by experts.

RED areas depict low volatility

GREEN areas depict high volatility.

When the clouds are outside the region delimited by the aqua lines we have

extreme conditions:

Extremely low volatility = red cloud outside the aqua bands

Extremely high volatility = green cloud outside the aqua bands

Vitelot/yanez/Vts December 2018.

Hitting the like button is free act of gratitude

Black-Scholes Probability Model with Time-Based VolatilityI developed this tool to automate probability calculations and to verify if Polymarkets accurately reflects Bitcoin's value. The indicator uses a modified Black-Scholes model to estimate the likelihood of Bitcoin exceeding or falling below a $97,000 strike price by a specified end date, providing a "fair value" probability.

Key Features:

- Timeframe Control: Displays data only between a defined start and end date, ensuring relevance during the prediction period.

- Dynamic Volatility Calculation: Offers a choice between manual input and auto-calculated annualized volatility. The auto-calculation derives historical volatility from recent price data over a selected lookback period and adjusts it based on the time remaining until expiration. More time implies greater expected price movement; less time indicates a narrower expected range.

- Probability Estimation: Calculates an adjusted parameter (d1) and applies a normal cumulative distribution function (CDF) to determine:

- "Yes" (Green Line): Probability that Bitcoin will exceed $97,000.

- "No" (Red Line): Probability that Bitcoin will remain below $97,000.

When Bitcoin's price is exactly $97,000, the tool sets the probabilities to a balanced 50/50 split, indicating fair value.

- Fair Value Indicator: Includes a static white reference line at 50% probability. A 50/50 probability suggests Bitcoin is fairly valued at $97,000; deviations indicate potential overvaluation or undervaluation.

- Polymarkets Tracking & Trading Strategy: I use Polymarkets to access cost-effective, high-leverage long call options on Bitcoin. However, these options don't always mirror Bitcoin's price movements precisely. For instance, if I anticipate Bitcoin rising from $95,000 to $97,000 by day's end, the tool might show a fair value probability of 50%. If Polymarkets quotes a 50% chance, the alignment indicates a fair trade. In such cases, I can avoid an unfavorable trade or exploit the difference as an arbitrage opportunity.

- Personal Motivation: This indicator eliminates the need for manual calculations and ensures I can quickly assess when Polymarkets' pricing aligns with Bitcoin's actual value, leading to more informed trading decisions.

This tool automates probability and fair value assessments, serving as a practical resource for verifying and potentially capitalizing on discrepancies in Polymarkets' Bitcoin pricing. It helps identify when there's a mismatch between the market's implied probability and the calculated fair value, allowing me to avoid unnecessary premiums on high-leverage options.

VARS 2.0: Volatility Adapted Relative StrengthVARS 2.0 (Volatility Adapted Relative Strength)

Basically, my VARS 2.0 indicator uses a stock's alpha in comparison to the SPX to determine whether there is relative strength on an volatility adjusted basis.

The idea for this indicator owes quite obviously to Matt Caruso . In this indicator I combine his Alpha Bars indicator with my interpretation of his CARS indicator, whose calculations are unknown to me.

The goal of this indicator is to give a representation of an asset's relative strength adjusted to its volatility. To find out if this is not only theoretically superior to a more simple representation such as by means of the classic RS Line , but also practically , this indicator is build.

I made this indicator freely available, so that everyone can make up his own mind about it. The representation with the alpha bars also offers the possibility to keep an eye on the daily relative strength, which is a complement to my former version of it. This time I limited myself to only one alpha timeframe because I believe the strength of the RS can be more clearly captured based on the EMAs. I also believe that the absolute strength of VARS is not the key point for traders, but rather its duration, as this is a sign of institutional accumulation.

Have fun and success trying it out!

Btw. The variables such as alpha and beta and the EMAs, which are used to calculate VARS, are largely freely definable. The default values are to be considered as suggestions.

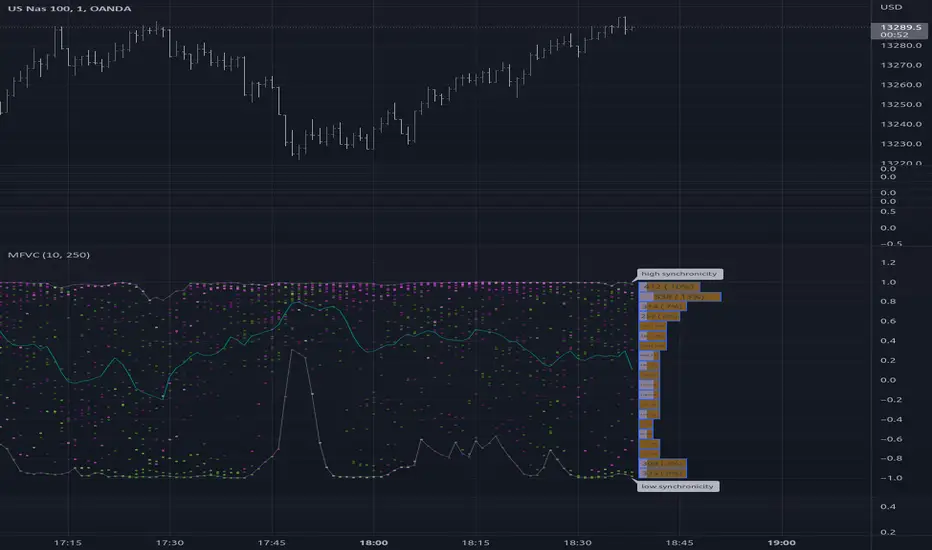

Multiple Frequency Volatility CorrelationThis is a complex indicator that looks to provide some insight into the correlation between volume and price volatility.

Rising volatility is depicted with the color green while falling volatility is depicted with purple.

Lightness of the color is used to depict the length of the window used, darker == shorter in the 2 -> 512 window range.

Stochastic with Volatility-WONTONLooking for a modern stochastic oscillator and volatility together?

Stochastic using an improved calculation.

Volatility overlay.

Price Action tends to follow a bottom in volatility.

(JS) S&P 500 Volatility Oscillator For OptionsThe idea for this started here: www.tradingview.com with the user @dime

This should only be used on SPX or SPY (though you could use it on other things for correlation I suppose) given that the instrument used to create this calculation is derived from the S&P 500 (thank you VIX). There's a lot of moving parts here though, so allow me to explain...

First: The main signal is when Implied Volatility (from VIX) drops beneath Historical Volatility - which is what you want to see so you aren't purchasing a ton of premium on long options. Green and above 0 means that IV% has dropped lower than Historical Volatility. (this signal, for example, would suggest using a Long Call or Put depending on your sentiment)

Second: The green line running underneath zero is the bottom portion of the "Average True Range" derived from the values used to create the oscillator. the closer the bottom histogram is to the green line, the more "normal" IV% is. Obviously, if this gets far away from the line then it could be setting up nicely to short options and sell the IV premium to someone else. (this signal, for example, would suggest using something like a Bull Put Spread)

Third: The red background along with the white line that drops down below zero signals when (and how far) the IV% from 3 months out (from VIX3M) is less than the current IV%. This would signal the current environment has IV way too high, a signal to short options once again (and don't take any long option positions!).

Tried to make this simple, yet effective. If you trade options on SPX, SPY, even ES1! futures - this is a tool tailored specifically for you! As I said before, if you want you can use it for correlation on other securities. Any other ideas or suggestions surrounding this, please let me know! Enjoy!

Ro Hidden Volatility OverlayWorks only on Forex pairs. See the inside bar volatility. Use precision to get data from lower time frames. Be aware that script initialization will be slower with the precision going higher. Added an option to show average volatility for long term as forex market transactions grow rapidly, suppressing all other markets. Bar color changes to green when volatility exceeds average.

Statistical Volatility - Extreme Value Method This indicator used to calculate the statistical volatility, sometime

called historical volatility, based on the Extreme Value Method.

Please use this link to get more information about Volatility.

Scott's historical ATR(volatility) percentileHistorical Volatility Percentile using Average True Range as measure of volatility.

Historical True Range Percentile

TC Volatility ScriptThis indicator uses 4 methods that are an improvement to the standard GARCH model of volatility forecasting. Operates largely on the premise of price consolidation preceding volatility. Diamonds signify moving average compression.

Works on equities, cryptocurrency markets, forex, futures etc.

Enjoy and feel free to message me any questions!

Ro Hidden Volatility V2.0Works only on Forex pairs. See the inside bar volatility. Use precision to get data from lower time frames. Be aware that script initialization will be slower with the precision going higher. Added an option to show average volatility for long term as forex market transactions grow rapidly, suppressing all other markets.

Relative Volatility Index The RVI is a modified form of the relative strength index (RSI).

The original RSI calculation separates one-day net changes into

positive closes and negative closes, then smoothes the data and

normalizes the ratio on a scale of zero to 100 as the basis for the

formula. The RVI uses the same basic formula but substitutes the

10-day standard deviation of the closing prices for either the up

close or the down close. The goal is to create an indicator that

measures the general direction of volatility. The volatility is

being measured by the 10-days standard deviation of the closing prices.

Fibonacci Ratios with VolatilityThis script will plot Fibonacci ratios with volatility. The Fibonacci retracement and extensions are plotted in lower time frames up to 15 minutes and therefore, it can be used for intraday only.

Odin's Volume and Volatility CompositeA simple indicator showing the ratio between Historical Volume and Historical Volatility.

It's meant to be applied to the BitMEX XBTUSD chart.

You can use this to develop profitable breakout strategies.

ATR SpikesVolatility Spike Indicator (ATR based)

I read some of Adam Grimes' work and found he uses a tool called sigma spikes, his concept is to mark significance to daily bars that have returns over x standard deviations of a 20 period average of returns.

I have adapted this idea for intra day trading. I've used an ATR and marked significance to any bar with a range greater than 4 standard deviations of the ATR, this results in attention being drawn to bars with strong momentum behind them and often results in strong follow through.

Additionally, I have included a MA crossover (fast/slow) filter to the indicator, this removes any signals that are counter- short term trend/momentum.

This is a powerful tool for momentum traders as it clearly shows points when the market has significant volatility.

Historical Volatility based Standard Deviation_V2This Plots the Standard Deviation Price Band based on the Historical Volatility. SD 1, 2, 3.

Version update:

Fixed the Standard Deviation mistake on Version 1.

Added Smoothing Options for those who prefer a less choppy version.

Standard Deviation 3 plot is not set to Default

FVE Volatility color-coded Volume bar The FVE is a pure volume indicator. Unlike most of the other indicators

(except OBV), price change doesn?t come into the equation for the FVE

(price is not multiplied by volume), but is only used to determine whether

money is flowing in or out of the stock. This is contrary to the current trend

in the design of modern money flow indicators. The author decided against a

price-volume indicator for the following reasons:

- A pure volume indicator has more power to contradict.

- The number of buyers or sellers (which is assessed by volume) will be the same,

regardless of the price fluctuation.

- Price-volume indicators tend to spike excessively at breakouts or breakdowns.

This study is an addition to FVE indicator. Indicator plots different-coloured volume

bars depending on volatility.

Volatility Aurora [The_lurker]█░░░░░░░░░░░░░░░░░░░ VOLATILITY AURORA ░░░░░░░░░░░░░░░░░░░░█

█░░░░░░░░░░░░░░░ Where Market Energy Meets Visual Poetry ░░░░░░░░░░░░░░░░█

📖 INTRODUCTION

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The Aurora Borealis occurs when charged particles from the sun collide with gases in Earth's atmosphere, creating mesmerizing waves of colorful light.

𝗩𝗼𝗹𝗮𝘁𝗶𝗹𝗶𝘁𝘆 𝗔𝘂𝗿𝗼𝗿𝗮 applies this elegant concept to financial markets:

⚡ Price Momentum = Charged Particles

🌌 ATR Layers = Atmospheric Layers

🎨 Color Intensity = Energy Magnitude

📐 Layer Expansion = Volatility State

When momentum "collides" with volatility layers, the Aurora illuminates potential market regime changes — often before they fully manifest in price action.

🔬 THE SCIENCE BEHIND IT

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Unlike traditional volatility indicators that provide a single value, Volatility Aurora creates a 𝗺𝘂𝗹𝘁𝗶-𝗱𝗶𝗺𝗲𝗻𝘀𝗶𝗼𝗻𝗮𝗹 𝘃𝗼𝗹𝗮𝘁𝗶𝗹𝗶𝘁𝘆 𝗳𝗶𝗲𝗹𝗱 using five distinct ATR layers based on Fibonacci periods:

│ Layer │ Period │ Atmospheric │ Function │

├──────────────────────┼─────────────────┼─────────────────┤

│ Layer 1 │ 5 │ Ionosphere │ Captures immediate vol shifts

│ Layer 2 │ 13 │ Mesosphere │ Medium-term vol response

│ Layer 3 │ 34 │ Stratosphere │ Intermediate vol structure

│ Layer 4 │ 55 │ Troposphere │ Foundational vol baseline

│ Layer 5 │ 89 │ Surface │ Structural, long-term vol

⚡ CORE CONCEPTS

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

𝟭. 𝗟𝗮𝘆𝗲𝗿 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻 & 𝗖𝗼𝗻𝘁𝗿𝗮𝗰𝘁𝗶𝗼𝗻

Each layer dynamically expands or contracts based on its normalized ATR value:

• 𝗘𝘅𝗽𝗮𝗻𝗱𝗶𝗻𝗴 𝗟𝗮𝘆𝗲𝗿𝘀 → Increasing volatility regime

• 𝗖𝗼𝗻𝘁𝗿𝗮𝗰𝘁𝗶𝗻𝗴 𝗟𝗮𝘆𝗲𝗿𝘀 → Decreasing volatility / Consolidation

• 𝗕𝗿𝗲𝗮𝘁𝗵𝗶𝗻𝗴 𝗘𝗳𝗳𝗲𝗰𝘁 → Natural market rhythm visualization

𝟮. 𝗛𝗮𝗿𝗺𝗼𝗻𝘆 𝗦𝗰𝗼𝗿𝗲

Measures alignment between all five layers:

• 𝗛𝗶𝗴𝗵 𝗛𝗮𝗿𝗺𝗼𝗻𝘆 (>70%) → All timeframes agree → Strong, reliable trends

• 𝗟𝗼𝘄 𝗛𝗮𝗿𝗺𝗼𝗻𝘆 (<30%) → Timeframe divergence → Choppy conditions

𝟯. 𝗘𝗻𝗲𝗿𝗴𝘆 𝗜𝗻𝘁𝗲𝗻𝘀𝗶𝘁𝘆

Quantifies how strongly momentum is "hitting" the volatility layers:

• 𝗛𝗶𝗴𝗵 𝗜𝗻𝘁𝗲𝗻𝘀𝗶𝘁𝘆 → Strong directional conviction

• 𝗟𝗼𝘄 𝗜𝗻𝘁𝗲𝗻𝘀𝗶𝘁𝘆 → Weak momentum, potential reversal

𝟰. 𝗥𝗲𝗴𝗶𝗺𝗲 𝗖𝗹𝗮𝘀𝘀𝗶𝗳𝗶𝗰𝗮𝘁𝗶𝗼𝗻

Based on aggregate layer states:

🟢 𝗖𝗔𝗟𝗠 → Low volatility across all layers

🟡 𝗡𝗢𝗥𝗠𝗔𝗟 → Balanced market conditions

🟠 𝗩𝗢𝗟𝗔𝗧𝗜𝗟𝗘 → Elevated activity

🔴 𝗘𝗫𝗧𝗥𝗘𝗠𝗘 → Maximum volatility state

🎨 VISUAL COMPONENTS

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🌈 𝗔𝘂𝗿𝗼𝗿𝗮 𝗟𝗮𝘆𝗲𝗿𝘀 (𝗚𝗿𝗮𝗱𝗶𝗲𝗻𝘁 𝗕𝗮𝗻𝗱𝘀)

• Five pairs of symmetrical bands around the price core

• Color gradient from core (bright) to outer (dim)

• Expansion reflects current volatility state

💠 𝗖𝗼𝗿𝗲 𝗟𝗶𝗻𝗲

• Central EMA-based trend line

• Color changes with momentum direction:

🟢 Cyan/Teal = Bullish

🔴 Pink/Magenta = Bearish

🟣 Purple = Neutral

💫 𝗘𝗻𝗲𝗿𝗴𝘆 𝗣𝘂𝗹𝘀𝗲 𝗟𝗶𝗻𝗲𝘀

• Diagonal flow lines showing momentum trajectory

• Thicker lines = Higher energy

• Direction indicates momentum flow

🎵 𝗛𝗮𝗿𝗺𝗼𝗻𝘆 𝗪𝗮𝘃𝗲𝘀

• Vertical dotted lines appear when harmony exceeds 70%

• Signals timeframe alignment — high-probability zones

📊 HOW TO USE

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 𝗧𝗿𝗲𝗻𝗱 𝗙𝗼𝗹𝗹𝗼𝘄𝗶𝗻𝗴

• Enter when Aurora expands in your direction

• Core line color confirms bias

• High harmony = Higher confidence

💥 𝗩𝗼𝗹𝗮𝘁𝗶𝗹𝗶𝘁𝘆 𝗕𝗿𝗲𝗮𝗸𝗼𝘂𝘁𝘀

• Watch for regime shift from CALM to VOLATILE

• Expanding layers signal incoming movement

• Intensity spike confirms breakout strength

↩️ 𝗠𝗲𝗮𝗻 𝗥𝗲𝘃𝗲𝗿𝘀𝗶𝗼𝗻

• EXTREME regime often precedes reversals

• Contracting layers after expansion = Potential pullback

• Low harmony during trends = Weakening momentum

🛡️ 𝗥𝗶𝘀𝗸 𝗠𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁

• Use outer layers as dynamic support/resistance

• Wider Aurora = Wider stops required

• Contracting Aurora = Tighter risk parameters

⚙️ SETTINGS GUIDE

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🌌 𝗔𝘂𝗿𝗼𝗿𝗮 𝗖𝗼𝗿𝗲

│ Setting │Default │ Description

│ Layer 1-5 │ Fib │ ATR periods (5,13,34,55,89)

│ Expansion Factor │ 2.5 │ Controls layer width multiplier

│ Smoothing │ 5 │ EMA smoothing for visual clarity

⚡ 𝗘𝗻𝗲𝗿𝗴𝘆 𝗙𝗶𝗲𝗹𝗱

│ Setting │ Default │ Description

│ Momentum Length │ 14 │ Period for momentum calculation

│ Energy Lookback │ 21 │ Normalization window

│ Energy Multiplier │ 1.5 │ Amplifies energy display

🎨 𝗩𝗶𝘀𝘂𝗮𝗹

│ Setting │ Default │ Description

│ Language │ EN │ Interface language (EN/AR)

│ Show Aurora │ ✓ │ Toggle layer visibility

│ Show Core Line │ ✓ │ Toggle center line

│ Show Energy Pulse │ ✓ │ Toggle flow lines

│ Show Harmony Waves │ ✓ │ Toggle alignment indicators

🔔 ALERTS

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚡ 𝗥𝗲𝗴𝗶𝗺𝗲 𝗦𝗵𝗶𝗳𝘁 — Volatility regime changed

🎵 𝗛𝗶𝗴𝗵 𝗛𝗮𝗿𝗺𝗼𝗻𝘆 — All layers aligned (>85%)

↕️ 𝗗𝗶𝗿𝗲𝗰𝘁𝗶𝗼𝗻 𝗖𝗵𝗮𝗻𝗴𝗲 — Momentum direction reversed

🔥 𝗜𝗻𝘁𝗲𝗻𝘀𝗶𝘁𝘆 𝗦𝗽𝗶𝗸𝗲 — Energy exceeded 80% threshold

💡 TIPS FOR BEST RESULTS

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

1️⃣ 𝗛𝗶𝗴𝗵𝗲𝗿 𝗧𝗶𝗺𝗲𝗳𝗿𝗮𝗺𝗲𝘀 — Aurora works best on 1H+ charts

2️⃣ 𝗖𝗼𝗺𝗯𝗶𝗻𝗲 𝘄𝗶𝘁𝗵 𝗣𝗔 — Use Aurora as context, not signals

3️⃣ 𝗪𝗮𝘁𝗰𝗵 𝗛𝗮𝗿𝗺𝗼𝗻𝘆 — High harmony setups win more

4️⃣ 𝗥𝗲𝘀𝗽𝗲𝗰𝘁 𝗥𝗲𝗴𝗶𝗺𝗲 — Don't fight EXTREME volatility

5️⃣ 𝗟𝗮𝘆𝗲𝗿 𝗖𝗼𝗻𝗳𝗹𝘂𝗲𝗻𝗰𝗲 — Multi-layer bounces = Strong S/R

⚠️ DISCLAIMER

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This indicator is for educational purposes only. Past performance does not

guarantee future results. Always use proper risk management and conduct your

own analysis before making trading decisions.

█████████████████████████████████████████████████████████████

█░░░░░░░░░░░░░░░░░░░░░ شفق التقلب ░░░░░░░░░░░░░░░░░░░░░░█

█░░░░░░░░░░░░░░░ حيث تلتقي طاقة السوق بالشعور البصري ░░░░░░░░░░░░░░░░█

📖 المقدمة

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

يحدث الشفق القطبي عندما تصطدم الجسيمات المشحونة القادمة من الشمس بالغازات في الغلاف الجوي للأرض، مما يخلق موجات ساحرة من الضوء الملون.

يطبق نفس المفهوم الأنيق على الأسواق المالية

⚡ زخم السعر = الجسيمات المشحونة

🌌 طبقات ATR = طبقات الغلاف الجوي

🎨 شدة اللون = حجم الطاقة

📐 توسع الطبقات = حالة التقلب

عندما "يصطدم" الزخم بطبقات التقلب، يُضيء الشفق التغيرات المحتملة في نظام السوق — غالباً قبل أن تتجلى بالكامل في حركة السعر.

🔬 العلم وراء المؤشر

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

على عكس مؤشرات التقلب التقليدية التي تقدم قيمة واحدة، يُنشئ شفق التقلب 𝗽𝗮𝗾𝗹 𝘁𝗮𝗾𝗮𝗹𝗹𝘂𝗯 𝗺𝘂𝘁𝗮'𝗮𝗱𝗱𝗶𝗱 𝗮𝗹-𝗮𝗯'𝗮𝗱 باستخدام خمس طبقات ATR مميزة مبنية على أرقام فيبوناتشي:

│ الطبقة │ الفترة │ المعادل الجوي │ الوظيفة

│ الطبقة١ │ 5 │ الأيونوسفير │ تلتقط تحولات التقلب الفورية

│ الطبقة٢ │ 13 │ الميزوسفير │ استجابة التقلب متوسطة المدى

│ الطبقة٣ │ 34 │ الستراتوسفير │ هيكل التقلب المتوسط

│ الطبقة٤ │ 55 │ التروبوسفير │ خط الأساس للتقلب

│ الطبقة٥ │ 89 │ السطح │ التقلب الهيكلي طويل المدى

⚡ المفاهيم الأساسية

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

𝟭. توسع وانكماش الطبقات

تتوسع أو تنكمش كل طبقة ديناميكياً بناءً على قيمة ATR المعيارية:

• طبقات متوسعة ← نظام تقلب متزايد

• طبقات منكمشة ← تقلب متناقص / تجميع

• تأثير التنفس ← تصور إيقاع السوق الطبيعي

𝟮. درجة التناغم

تقيس التوافق بين جميع الطبقات الخمس:

• تناغم عالي (>٧٠٪) ← جميع الأطر متفقة ← اتجاهات قوية

• تناغم منخفض (<٣٠٪) ← تباين الأطر ← ظروف متقطعة

𝟯. شدة الطاقة

تحدد مدى قوة "اصطدام" الزخم بطبقات التقلب:

• شدة عالية ← قناعة اتجاهية قوية

• شدة منخفضة ← زخم ضعيف، احتمال انعكاس

𝟰. تصنيف النظام

بناءً على حالات الطبقات المجمعة:

🟢 هادئ ← تقلب منخفض عبر جميع الطبقات

🟡 طبيعي ← ظروف سوق متوازنة

🟠 متقلب ← نشاط مرتفع

🔴 متطرف ← حالة التقلب القصوى

🎨 المكونات البصرية

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🌈 طبقات الشفق (النطاقات المتدرجة)

• خمسة أزواج من النطاقات المتماثلة حول نواة السعر

• تدرج لوني من النواة (ساطع) إلى الخارج (خافت)

• التوسع يعكس حالة التقلب الحالية

💠 خط النواة

• خط اتجاه مركزي قائم على EMA

• يتغير اللون مع اتجاه الزخم:

🟢 سماوي = صاعد

🔴 وردي = هابط

🟣 بنفسجي = محايد

💫 خطوط نبض الطاقة

• خطوط تدفق مائلة تُظهر مسار الزخم

• خطوط أسمك = طاقة أعلى

• الاتجاه يشير إلى تدفق الزخم

🎵 موجات التناغم

• خطوط عمودية منقطة تظهر عندما يتجاوز التناغم ٧٠٪

• تشير إلى توافق الأطر الزمنية — مناطق احتمالية عالية

📊 كيفية الاستخدام

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 تتبع الاتجاه

• ادخل عندما يتوسع الشفق في اتجاهك

• لون خط النواة يؤكد التحيز

• تناغم عالي = ثقة أعلى

💥 اختراقات التقلب

• راقب تحول النظام من هادئ إلى متقلب

• الطبقات المتوسعة تشير إلى حركة قادمة

• ارتفاع الشدة يؤكد قوة الاختراق

↩️ الارتداد للمتوسط

• النظام المتطرف غالباً يسبق الانعكاسات

• طبقات منكمشة بعد التوسع = احتمال تراجع

• تناغم منخفض أثناء الاتجاهات = زخم ضعيف

🛡️ إدارة المخاطر

• استخدم الطبقات الخارجية كدعم/مقاومة ديناميكية

• شفق أوسع = وقف خسارة أوسع مطلوب

• شفق منكمش = معايير مخاطر أضيق

⚙️ دليل الإعدادات

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🌌 نواة الشفق

│ الإعداد │الافتراضي│ الوصف

│ الطبقات ١-٥ │ Fib │ فترات ATR (5,13,34,55,89)

│ معامل التوسع │ 2.5 │ يتحكم في مضاعف عرض الطبقات

│ التنعيم │ 5 │ تنعيم EMA للوضوح البصري

⚡ مجال الطاقة

│ الإعداد │الافتراضي│ الوصف

│ فترة الزخم │ 14 │ فترة حساب الزخم

│ فترة الطاقة │ 21 │ نافذة التطبيع

│ مضاعف الطاقة │ 1.5 │ يضخم عرض الطاقة

🎨 العرض البصري

│ الإعداد │الافتراضي│ الوصف

│ اللغة │ EN │ لغة الواجهة (EN/AR)

│ إظهار الشفق │ ✓ │ تبديل ظهور الطبقات

│ خط النواة │ ✓ │ تبديل الخط المركزي

│ نبض الطاقة │ ✓ │ تبديل خطوط التدفق

│ موجات التناغم │ ✓ │ تبديل مؤشرات التوافق

🔔 التنبيهات

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚡ تحول النظام — تغير نظام التقلب

🎵 تناغم عالي — جميع الطبقات متوافقة (>٨٥٪)

↕️ تغير الاتجاه — انعكس اتجاه الزخم

🔥 ارتفاع الشدة — تجاوزت الطاقة عتبة ٨٠٪

💡 نصائح للحصول على أفضل النتائج

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

1️⃣ الأطر الزمنية الأعلى — الشفق يعمل بشكل أفضل على ساعة فأكثر

2️⃣ ادمج مع حركة السعر — استخدم الشفق كسياق وليس إشارات

3️⃣ راقب التناغم — إعدادات التناغم العالي تربح أكثر

4️⃣ احترم النظام — لا تحارب التقلب المتطرف

5️⃣ تقاطع الطبقات — ارتداد من طبقات متعددة = دعم/مقاومة قوية

⚠️ إخلاء المسؤولية

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

هذا المؤشر للأغراض التعليمية فقط. الأداء السابق لا يضمن النتائج المستقبلية.

استخدم دائماً إدارة مخاطر مناسبة وقم بتحليلك الخاص قبل اتخاذ قرارات التداول.

█████████████████████████████████████████████████████████████