Acceleration-Based MA Slope PredictionHello traders,

I developed this indicator while working on a trading strategy using moving average slope and acceleration, and I found the concept interesting enough to share it.

Let me briefly explain this indicator.

----About White Plot----

1. Calculate the first derivative approximation at the current point of the Moving Average, and then calculate the second derivative approximation to obtain the 'Acceleration'.

2. Where the acceleration is 0, it signifies a change in the force of the moving average.

3. Therefore, by drawing a parabola based on the acceleration at that time, can depict the parabolic shape of the moving average.

This is represented as a white circle on the indicator.

4. These circles are reset at the next point where the acceleration is 0, indicating a change in the parabolic force.

If the moving average rises more sharply than the predicted value of the rising parabola, a more drastic increase is expected.

5. In this case, you can start risk management around the time the drawn parabola breaks.

(The actual MA is represented by green/red lines)

6. Before the trend changes, i.e., before the direction of the moving average changes, there is a section where the acceleration is 0, and this is represented on the chart as follows.

(The lower indicator shows the acceleration of the corresponding parabola)

----About Red Plot----

1. Calculate the first derivative approximation of the moving average value, the 'slope'.

2. Where the slope is 0, it represents the extreme point of the parabola.

3. Therefore, by using the acceleration at that point as the coefficient of the quadratic function and setting the extreme point as a vertex, we can draw a quadratic function. This is represented as a red circle on the indicator.

(Keep in mind that the actual moving average is not a quadratic function; this is a "forced" quadratic function assuming the parabola is maintained)

4. These circles are reset at the next extreme point where the slope is 0, and a new quadratic function is created.

Based on the formula obtained in the above process, you can predict the future moving average through 'offset'.

5. That is, if the x value at the current point is 'k', you can predict the moving average one candle ahead by substituting (k+1) into the quadratic function.

The predicted value at the past position is shown as a red circle.

6. The smoother the chosen moving average, the fewer extreme points will appear, and the higher the likelihood of the parabola fitting.

For the T3 set as the default value, it shows very high accuracy even when predicting about 20 candles ahead.

On the other hand, rough moving averages like SMA have limited prediction value.

(SMA 60, offset = 10)

--------

The moving average with a very high level of accuracy is JMA (Jurik Moving Average). However, since the code for this moving average is not public, I recommend those interested to check it through my code.

Additionally, I believe the code of this indicator I've uploaded has significant utility.

As an example, you can use the breaking point of the parabola predicted by the acceleration to determine when the force changes again for entries/losses. There are many other possible applications as well.

I look forward to seeing more excellent results from this indicator.

--------

안녕하세요 트레이더여러분.

이 지표는, 제가 이동평균선의 기울기와 가속도를 이용하여 매매를 하기 위한 지표를 개발하다가, 흥미로운 내용이라고 판단하여 만들게 되었습니다.

이 지표에 대해 간단히 설명드리겠습니다.

----하얀색 플롯에 대해----

1. 이동평균선이 진행되는 현재 시점에서 미분의 근사값을 구하고, 다시 한 번 미분의 근사값을 구해서 '가속도'를 얻습니다.

2. 가속도가 0이 되는 곳은, 곧 해당 이동평균선의 힘이 바뀌는 곳을 의미합니다.

3. 따라서, 그 당시 시점 기준으로 포물선을 그려낸다면, 가속도를 이용하여 해당 이동평균선의 포물선을 그려낼 수 있습니다. 이것은 지표의 하얀색점로서 표기됩니다.

4. 이 때, 이러한 점들은 다음의 가속도가 0이 되는 지점, 즉 포물선의 힘이 바뀌는 곳에서 다시 초기화됩니다.

5. 올라가고 있던 포물선에서의 예측치보다 이동평균선이 더 급하게 올라간다면, 더욱 급격한 상승이 예상됩니다. 이 경우, 그려지고있는 포물선이 깨질 때쯤부터 리스크 관리를 시작할 수 있습니다.

(녹색/빨간색의 선으로 실제 MA를 표현했습니다. 거슬리시면 '모습'가셔서 끄셔도 좋습니다. )

6. 추세가 변경되기 전, 즉 이동평균선의 방향이 바뀌기 전에는 가속도가 0이 되는 구간이 존재하고, 그것이 차트 위에 다음과같이 표현됩니다.

(하단의 지표는, 해당 포물선의 가속도을 나타냅니다)

----붉은색 플롯에 대해----

1. 이동평균선 값을 미분 근사값 즉, '기울기'를 구합니다.

2. 기울기가 0이 되는 곳은, 포물선이 극점이 되는 곳을 뜻합니다.

3. 따라서, 해당 시점의 가속도를 2차함수의 계수로 하여, 또한 해당 극점을 하나의 꼭지점으로 설정하여,이차함수를 그려낼 수 있습니다. 이것은 지표의 빨간색점으로서 표현됩니다.

(실제 이동평균선은 2차함수가 아니기에, 포물선이 유지된다는 가정 하에 "억지로"만들어낸 이차함수입니다)

4. 이 때, 이러한 점은 다음 극점이 0이 되는 곳에서 초기화되고 이차함수가 만들어집니다.

5. 위의 과정에서 얻은 식을 바탕으로 'offset'을 통해 미래의 이동평균선을 예측할 수 있습니다.

즉, 현재시점의 x값을 'k'라고 한다면, (k+1)을 이차함수에 대입하여 1캔들 앞의 이동평균선을 예측할 수 있습니다.

해당 예측치가 지나간 자리는, 빨간색점을 통해 보여집니다.

6. 선택한 이동평균선이 스무스할수록 극점은 덜 등장하게되고, 포물선의 위치가 맞아들어갈 가능성이 높습니다.

현재 디폴트값으로 설정된 T3의 경우, 약 20캔들 앞을 예측해도 매우 높은 정확도를 보여줍니다.

반면에, SMA와 같이 울퉁불퉁한 이동평균선은 가능한 예측치가 크지 않습니다.

(SMA 60, offset=10)

--------

매우 높은 수준의 정확도를 보여준 이동평균선은 JMA(Jurik Moving Average)입니다. 다만 이 이동평균선은 코드가 공개되지 않았기때문에, 관심있으신 분은 저의 코드를 통해 한번 확인해보시길 권장드립니다.

추가로, 제가 올린 이 지표의 코드는 이용가치가 높다고 생각합니다.

하나의 예시로서, 가속도로 예측한 포물선이 깨지는 곳을 기준으로, 힘이 다시 한 번 바뀌는 것을 이용해 진입/로스를 할 수 있습니다. 그 외에도 매우 다양한 활용이 가능합니다.

이 지표를 통해 더욱 좋은 새로운 결과물이 나오길 기대해봅니다.

Tìm kiếm tập lệnh với "股价站上60月线"

The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)

Are you tired of manually analyzing charts and trying to find profitable trading opportunities? Look no further! Our algorithmic trading strategy, "Flash," is here to simplify your trading process and maximize your profits.

Flash is an advanced trading algorithm that combines three powerful indicators to generate highly selective and accurate trading signals. The Momentum-RSI, Super-Trend Analysis and EMA-Strategy indicators are used to identify the strength and direction of the underlying trend.

The Momentum-RSI signals the strength of the trend and only generates trading signals in confirmed upward or downward trends. The Super-Trend Analysis confirms the trend direction and generates signals when the price breaks through the super-trend line. The EMA-Strategy is used as a qualifier for the generation of trading signals, where buy signals are generated when the EMA crosses relevant trend lines.

Flash is highly selective, as it only generates trading signals when all three indicators align. This ensures that only the highest probability trades are taken, resulting in maximum profits.

Our trading strategy also comes with two profit management options. Option 1 uses the so-called supertrend-indicator which uses the dynamic ATR as a key input, while option 2 applies pre-defined, fixed SL and TP levels.

The settings for each indicator can be customized, allowing you to adjust the length, limit value, factor, and source value to suit your preferences. You can also set the time period in which you want to run the backtest and how many dollar trades you want to open in each position for fully automated trading.

Choose your preferred trade direction and stop-loss/take-profit settings, and let Flash do the rest. Say goodbye to manual chart analysis and hello to consistent profits with Flash. Try it now!

General Comments

This Flash Strategy has been developed in cooperation between Baby_whale_to_moon and JS-TechTrading. Cudos to Baby_whale_to_moon for doing a great job in transforming sophisticated trading ideas into pine scripts.

Detailed Description

The “Flash” script considers the following indicators for the generation of trading signals:

1. Momentum-RSI

2. ‘Super-Trend’-Analysis

3. EMA-Strategy

1. Momentum-RSI

• This indicator signals the strength of the underlying upward- or downward-trend.

• The signal range of this indicator is from 0 to 100. Values > 60 indicate a confirmed upward- or downward-trend.

• The strategy will only generate trading signals in case the stock (or any other financial security) is in a confirmed upward- (long entry signals) or downward-trend (short entry signals).

• This indicator provides information with regards to the strength of the underlying trend and it does not give any insight with regard to the direction of the trend. Therefore, this strategy also considers other indicators which provide technical confirmation with regards to the direction of the underlying trend.

Graph 1 shows this concept:

• The Momentum-RSI indicator gives lower readings during consolidation phases and no trading signals are generated during these periods.

Example (graph 2):

2. Super-Trend Analysis

• The red line in the graph below represents the so-called super-trend-line. Trading signals are only generated in case the price action breaks through this super-trend-line indicating a new confirmed upward-trend (or downward-trend, respectively).

• If that happens, the super trend-line changes its color from red to green, giving confirmation that the trend changed from bearish to bullish and long-entries can be considered.

• The vice-versa approach can be considered for short entries.

Graph 3 explains this concept:

3. Exponential Moving Average / EMA-Strategy

The functionality of this EMA-element of the strategy has been programmed as follows:

• The exponential moving average and two other trend lines are being used as qualifiers for the generation of trading-signals.

• Buy-signals for long-entries are only considered in case the EMA (yellow line in the graph below) crosses the red line.

• Sell-signals for short-entries are only considered in case the EMA (yellow line in the graph below) crosses the green line.

An example is shown in graph 4 below:

We use this indicator to determine the new trend direction that may occur by using the data of the price's past movement.

4. Bringing it all together

This section describes in detail, how this strategy combines the Momentum-RSI, the super-trend analysis and the EMA-strategy.

The strategy only generates trading-signals in case all of the following conditions and qualifiers are being met:

1. Momentum-RSI is higher than the set value of this strategy. The standard and recommended value is 60 (graph 5):

2. The super-trend analysis needs to indicate a confirmed upward-trend (for long-entry signals) or a confirmed downward-trend (for short-entry signals), respectively.

3. The EMA-strategy needs to indicate that the stock or financial security is in a confirmed upward-trend (long-entries) or downward-trend (short-entries), respectively.

The strategy will only generate trading signals if all three qualifiers are being met. This makes this strategy highly selective and is the key secret for its success.

Example for Long-Entry (graph 6):

When these conditions are met, our Long position is opened.

Example for Short-Entry (graph 7):

Trade Management Options (graph 8)

Option 1

In this dynamic version, the so-called supertrend-indicator is being used for the trade exit management. This supertrend-indicator is a sophisticated and optimized methodology which uses the dynamic ATR as one of its key input parameters.

The following settings of the supertrend-indicator can be changed and optimized (graph 9):

The dynamic SL/TP-lines of the supertrend-indicator are shown in the charts. The ATR-length and the supertrend-factor result in a multiplier value which can be used to fine-tune and optimize this strategy based on the financial security, timeframe and overall market environment.

Option 2 (graph 10):

Option 2 applies pre-defined, fixed SL and TP levels which will appear as straight horizontal lines in the chart.

Settings options (graph 11):

The following settings can be changed for the three elements of this strategy:

1. (Length Mom-Rsi): Length of our Mom-RSI indicator.

2. Mom-RSI Limit Val: the higher this number, the more momentum of the underlying trend is required before the strategy will start creating trading signals.

3. The length and factor values of the super trend indicator can be adjusted:ATR Length SuperTrend and Factor Super Trend

4. You can set the source value used by the ema trend indicator to determine the ema line: Source Ema Ind

5. You can set the EMA length and the percentage value to follow the price: Length Ema Ind and Percent Ema Ind

6. The backtesting period can be adjusted: Start and End time of BackTest

7. Dollar cost per position: this is relevant for 100% fully automated trading.

8. Trade direction can be adjusted: LONG, SHORT or BOTH

9. As we explained above, we can determine our stop-loss and take-profit levels dynamically or statically. (Version 1 or Version 2 )

Display options on the charts graph 12):

1. Show horizontal lines for the Stop-Loss and Take-profit levels on the charts.

2. Display relevant Trend Lines, including color setting options for the supertrend functionality. In the example below, green lines indicate a confirmed uptrend, red lines indicate a confirmed downtrend.

Other comments

• This indicator has been optimized to be applied for 1 hour-charts. However, the underlying principles of this strategy are supply and demand in the financial markets and the strategy can be applied to all timeframes. Daytraders can use the 1min- or 5min charts, swing-traders can use the daily charts.

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The combination of the qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

TOMMAR#TOMMAR #MultiMovingAverages #MMAR

Dear fellow traders, this is Tommy, and today I'd like to introduce you to the Multi-Moving Averages Ribbon (MMAR) indicator, which I believe to be one of the best MMAR indicators available on TradingView. Moving Averages is a popular technical analysis tool used to smooth out price data by creating an average of past price data points over a specified time period. They can be used to identify trends and provide a clearer view of price action, as well as generate buy and sell signals by observing crossovers between different moving average lines.

In the MMAR indicator, we have incorporated 12 different types of Moving Averages, including Simple Moving Averages (SMA), Exponential Moving Averages (EMA), Weighted Moving Averages (WMA), Hull Moving Averages (HMA), and Smoothed Moving Averages (SMMA), among others. This allows traders to choose the optimal type for their preferred trading commodities.

One common technique in technical analysis is using multiple Moving Averages with varying lengths, which provides a more comprehensive view of price action. By analyzing multiple Moving Averages with different timeframes, traders can better understand both short- and long-term trends and make more informed trading decisions. Some of the well-known combinations of multiple moving averages used by traders are (5, 9, 14, 21, 45), (6, 11, 16, 22, 51), [8, 13, 21, 55), (50, 100, 200), and (60, 120, 240).

Another way to gauge the strength of the market trend is to look for the arrangement of the Moving Averages. If they are in a sequential order, with the shortest on top and the longest on the bottom, it is most likely a bullish trend. On the other hand, if they are arranged in reverse order, with the shortest on the bottom and the longest on top, it is most likely a bearish trend. The 'Trend Light' in the indicator settings will automatically signal when the Moving Averages are in either an orderly or reverse arrangement.

Lastly, I have added a useful feature to the indicator: the 'MA Projection'. This feature projects and forecasts the Moving Averages in the future, allowing traders to easily identify confluence zones in future candlesticks. Please note that the projection levels may change in the case of extreme price action that significantly affects the Moving Averages.

This is free so any Tradingview users can use this indicator. Just search TOMMAR in the indicator section located on top of the chart.

#TOMMAR #MultiMovingAverages #MMAR

안녕하세요 트레이더 여러분, 토미입니다. 오늘 여러분들에게 소개드릴 지표는 다양한 길이의 이동평균선 조합을 사용할 수 있는 MMAR (Multiple Moving Averages Ribbon)입니다. 아마 제가 만든 MMAR 지표가 트레이딩뷰에서 가장 쓸만할 겁니다. 이동평균선, 줄여서 이평선은 말 그대로 특정 기간 범위 내의 주가들을 평균한 값들로 이루어진 선입니다. 제가 이평선 관련된 강의 자료는 예전에 올려드린 바 있으니 더 자세한 내용이 궁금하신 분들은 아래 링크/이미지 클릭하시길 바랍니다.

본 지표는 Simple Moving Averages (SMA), Exponential Moving Averages (EMA), Weighted Moving Averages (WMA), Hull Moving Averages (HMA), 그리고 Smoothed Moving Averages (SMMA) 등을 포함해 총 12개 종류의 이평선 지표를 사용할 수 있습니다. 또한 각 이평선의 길이들도 하나하나 일일이 설정하실 수 있습니다. 예를 들어 요즘에 자주 보이는 이평선들의 조합이 , , , , 그리고 등등이 존재하는데 여러분의 취향에 맞게 설정하여 사용하시면 됩니다.

몇 가지 주요 기능에 대해서 설명 드리겠습니다. 설정에서 ‘Trend Light’를 키면 이평선들의 정배열 혹은 역배열 여부를 쉽게 볼 수 있습니다. 이평선이 정배열일때는 맨 아래의 이평선에 초록불이, 역배열일때는 맨 위의 이평선에 빨간불이 켜지며 둘 다 아닐 땐 아무 불도 켜지지 않습니다. 또한 ‘MA Projection’을 키면 이평선들의 미래 예측 값들을 확장해줍니다. 당연히 가격 변동이 갑자기 크게 나오면 이평선 예측 확장 레벨들이 확 바뀌겠죠.

지표창에 TOMMAR 검색하시거나 아래 즐겨찾기 인디케이터에 넣기 클릭하시면 누구나 사용하실 수 있습니다~ 여러분의 구독, 좋아요, 댓글은 저에게 큰 힘이 됩니다.

RSI Multi Symbol/Time Frame DetectorThis code is an implementation of the Relative Strength Index (RSI) indicator, which is a popular momentum indicator used in technical analysis. The RSI measures the strength of an asset's price action and provides information on whether the asset is overbought or oversold. The code also calculates a moving average of the RSI and allows the user to choose the type of moving average to be calculated (SMA, EMA, SMMA, WMA, or VWMA).

The user can select from different time frames (5, 15, 60, or 240), symbols (SP:SPX, OANDA:EURUSD, or OANDA:NZDUSD), RSI lengths, and moving average types and lengths.

The code starts by defining a function called "ma" for calculating different types of moving averages. This function takes as input the source data for the moving average calculation (the RSI), the length of the moving average, and the type of moving average. The function uses a switch statement to return the appropriate calculation based on the inputted moving average type.

Next, the code calculates the RSI and its moving average. The RSI is calculated using the well-known formula for the RSI, which involves calculating the average gains and losses over a specified period of time and then dividing the average gains by the average losses. The moving average is calculated using the "ma" function defined earlier.

Finally, the code allows the user to choose the symbol and time frame to be used in the RSI calculation, as well as the length of the RSI and the moving average, and the type of moving average. The user can choose from three symbols (SP:SPX, OANDA:EURUSD, OANDA:NZDUSD) and four time frames (5, 15, 60, and 240 minutes). The code then uses the "request.security" function to retrieve the RSI calculation for the selected symbol and time frame.

Note: This code is example for you to use multi timeframe/symbol in your indicator or Strategy , also prevent Repainting Calculation

Setup Max e Min Larry WilliansLarry Williams used this system to win the trading championship

Hello friends, I bring a script with a trading strategy to be used in futures such as Index, Forex and Commodities. Developed by famous trader Larry Williams.

In them we use two 3-period Simple Moving Averages (Arithmetic) (one with the high price, the other with the low price), and a 21-period Moving Average (Arithmetic) to determine the trend. This will form an average channel with the prices of the maximums and minimums of the last three candles.

Best time charts use the strategy: from 5 minutes to 60 minutes.

This strategy is quite simple. The 21 Moving Average will color according to the trend (Green for bullish, Red for bearish and Gray for transitions). The Script will signal the entry according to the trend by the colors of the candles and also by the signal:

When green, the buy will be on the crossing of the lower Moving Average crossing the candlestick, and the exit will be on the crossing of the candlestick on the next Upper Moving Average.

When red, the sell will be at the crossing of the Upper Moving Average crossing the candlestick, and the exit will be at the crossing of the candlestick on the next Lower Moving Average.

When the Script signals the candle with a purple X, it means that the trend is changing and the entire open operation must be closed.

This system has no Stop, so be careful when using it.

Na linguagem do autor:

Larry Williams usou esse sistema ganhar campeonato de trade

Olá amigos, trago um script com uma estratégia de trade pra ser usada em futuros como Índice, Forex e Commodities. Desenvolvido pelo famoso trader Larry Willians.

Neles usamos duas Médias Móveis Simples (Aritmética) de 3 períodos (uma com o preço da máxima, outra com o preço da mínima), e uma Média Móvel (Aritmética) de 21 períodos para determinar a tendência. Nisso vai formar uma canal de médias com os preços das máximas e mínimas dos últimos três candles.

Melhores tempos gráficos usar a estratégia: de 5 minutos até 60 minutos.

Essa estratégia é bem simples. A Média Móvel de 21 irá colorir de acordo com a tendência (Green pra alta, Red para baixa e Gray para transições). O Script irá sinalizar a entrada de acordo com a tendência pela cores dos candles e também pela sinalização:

Quando green, a compra será no cruzamento da Média Móvel inferior cruzando o candle, e a saida será no cruzamento do candle na Média Móvel Superior seguinte.

Quando red, a venda será no cruzamento da Média Móvel Superior cruzando o candle, e a saida será no cruzamento do candle na Média Móvel Inferior seguinte.

Quando o Script sinaliza o candle com X purple, significa que a tendência está em mudança e deve ser fechada toda a operação em aberto.

Este sistema não possui Stop, portando cuidado quanto a seu uso.

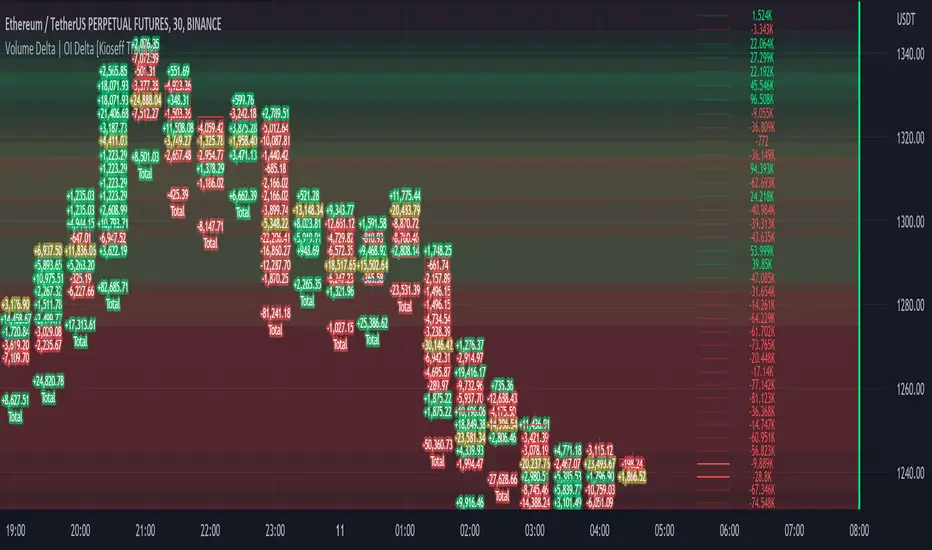

Delta Ladder [Kioseff Trading]Hello!

This script presents volume delta data in various forms!

Features

Classic mode: Volume delta boxes oriented to the right of the bar (sell closer / buy further)

On Bar mode: Volume delta boxes oriented on the bar (sell left / buy right)

Pure Ladder mode: Pure volume delta ladder

PoC highlighting

Color-coordinated delta boxes. Marginal volume differences are substantially shaded while large volume differences are lightly shaded.

Volume delta boxes can be merged and delta values removed to generate a color-only canvas reflecting vol. delta differences in price blocks.

Price bars can be split up to 497 times - allowing for greater precision.

Total volume delta for the bar and timestamp included

The image above shows Classic mode - delta blocks are oriented left/right contingent on positive/negative values!

The image above shows the same price sequence; however, delta blocks are superimposed on the price bar. Left-side blocks reflect negative delta while right-side blocks reflect positive delta! To apply this display method - select "On Bar" for the "Data Display Method" setting!

The image above shows "Pure Ladder" mode. Delta blocks remain color-coordinated; however, all delta blocks retain the same x-axis as the price bar they were calculated for!

Additionally, you can select to remove the delta values and merge the delta boxes to generate a color-based canvas indicative of volume delta at traded price levels!

The image above shows the same price sequence; however, the "Volume Assumption" setting is activated.

When active, the indicator assumes a 60/ 40 split when a level is traded at and only one metric - "buy volume" or "sell volume" is recorded. This means there shouldn't be any levels recorded where "buy volume" is greater than 0 and "sell volume" equals 0 and vice versa. While this assumption was performed arbitrarily, it may help better replicate volume delta and OI delta calculations seen on other charting platforms.

This option is configurable; you can select to have the script not assume a 60/ 40 split and instead record volume "as is" at the corresponding price level!

I plan to roll out additional features for the indicator - particularly tick-based price blocks! Stay tuned (:

Thank you!

Expected Move Plotter IntradayHello everyone!

I am releasing my Intra-day expected move plotter indicator.

About the indicator:

This indicator looks at 3 differing time frames, the 15, 30 and 60 minute time frames.

It calculates the average move from high to low over the past 5 candle period and then plots out the expected move based on that average.

It also attempts to determine the sentiment. How it does this is by taking the average of the High, Low and Close of the previous 5 minute candle and comparing it in relation to the close of the current 5 minute candle. It essentially is the premise of pivot points.

Each time frame can be shut off or selected based on your preference, as well as the sentiment fills.

How to use:

Please play around with it and determine how you feel you could best use it, but I can share with you some tips that I have picked up from using this.

Wait for a clear rejection of respect of a level:

Once you have confirmed rejection or support, you can scalp to the next support level:

As well, you can switch between the 30 and 60 minute time frames as reference

30 Minute:

And that's it!

Its a very simplistic indicator, but it is quite helpful to help identify potential areas of reversal.

There really isn't much to it!

Also, it can be used on any stock!

As always, I have provided a quick tutorial video for your reference, linked below:

Let me know if you have any questions or recommendations for modification to make the indicator more useful and helpful.

Thanks so much for checking it out and trying it out everyone!

As always, safe trades and green days!

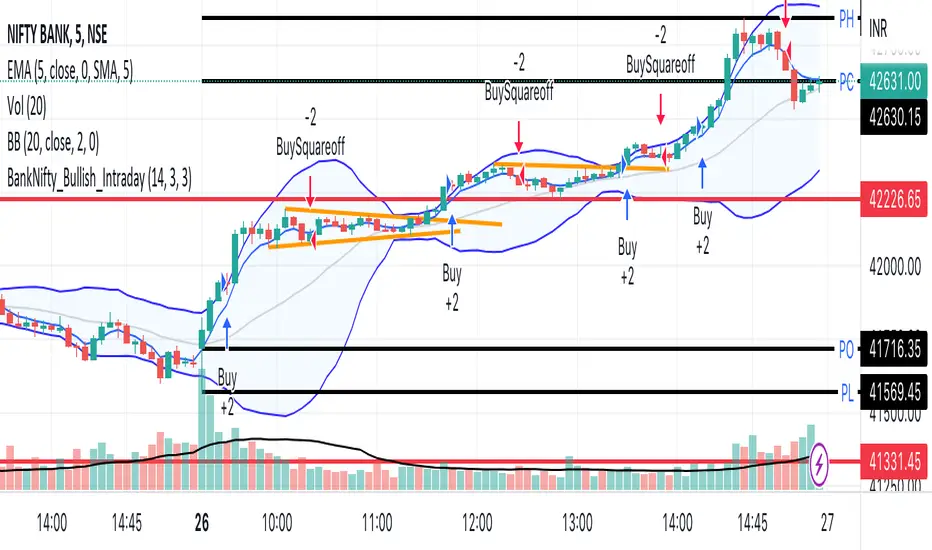

BankNifty_Bullish_Intraday

The script uses following mechanism to give a signal of BUY if multiple parameters evaluated are all passed.

ENTRY-

1. 5 min MACD should be more than its previous tick

2. 15 min MACD should be more than its previous tick

3. 60 min MACD should be more than its previous tick

4. ADX should be more than 12

5. RSI should be more than 60

6. Stochastic %k should have cross over with %d

7. Bollinger band upper band value should be more than previous tick

EXIT

If the 5 min bar price closes below 5 min EMA , it gives an exit signal.

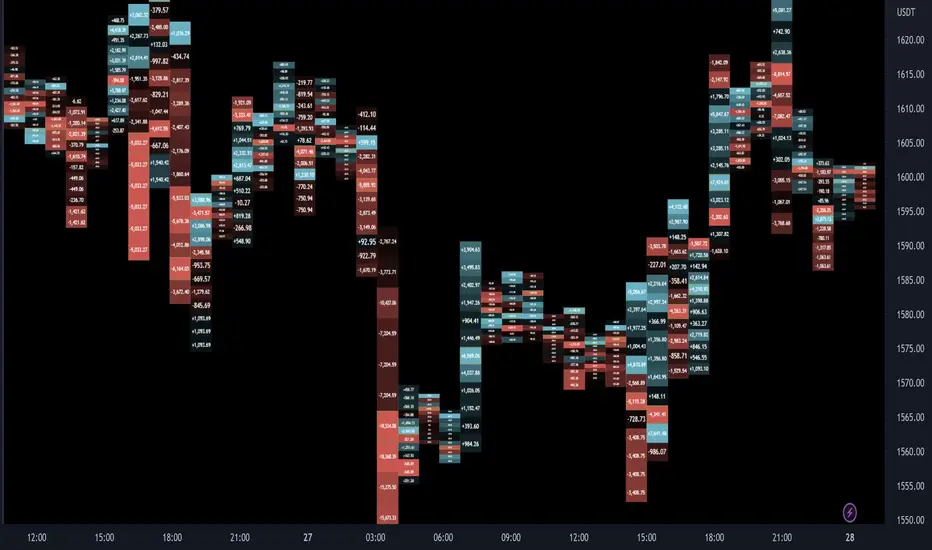

Volume Profile Volume Delta OI Delta [Kioseff Trading]Hello!

This script serves to distinguish volume delta for any asset and open interest delta for Binance perpetual futures.

The image above provides further explanation of functionality and color correspondence.

The image above shows the indicator calculating volume at each tick level and displaying the metric.

The label color outline (neon effect) is configurable; the image above is absent the feature.

The image above shows Open Interest (OI) Delta calculated - similar to how the script calculates volume delta - for a Binance Perpetual Future pair.

This feature only works for Binance Futures pairs; the script will not load when trying to calculate OI Delta on other assets.

Additionally, a heatmap is displayable should you configure the indicator to calculate it.

The image above shows a heatmap using volume delta calculations.

The image above shows a heatmap using OI delta calculations.

Of course, these calculations - when absent requisite data - require some assumptions to better replicate calculations with access to requisite data.

The indicator assumes a 60/40 split when a tick level is traded at and only one metric - "buy volume" or "sell volume" is recorded. This means there shouldn't be any levels recorded where "buy volume" is greater than 0 and "sell volume" equals 0 and vice versa. While this assumption was performed arbitrarily, it may help better replicate volume delta and OI delta calculations seen on other charting platforms.

This option is configurable; you can select to have the script not assume a 60/40 split and instead record volume "as is" at the corresponding tick level.

The script also divides volume and open interest if a one-minute bar violates multiple tick levels. The volume or open interest generated on the one-minute bar will be divided by the number of tick levels it exceeds. The results are, subsequently, appended to the violated tick levels.

Further, the script can be set to recalculate after a user-defined time threshold is exceeded. You can also define the percentage or tick distance between levels.

Also, it'd be great if this indicator can nicely replicate volume delta indicators on other charting platforms. If you've any ideas on how price action can be used to better assume volume at the corresponding price area please let me know!

Thank you (:

ICT IPDA Look BackThis script automatically calculates and updates ICT's daily IPDA look back time intervals and their respective discount / equilibrium / premium, so you don't have to :)

IPDA stands for Interbank Price Delivery Algorithm. Said algorithm appears to be referencing the past 20, 40, and 60 days intervals as points of reference to define ranges and related PD arrays.

Intraday traders can find most value in the 20 Day Look Back box, by observing imbalances and points of interest.

Longer term traders can reference the 40 and 60 Day Look Back boxes for a clear indication of current market conditions.

Ichimoku Breakout Kumo SWING TRADER (By Insert Cheese)A simple strategy for long spot or long futures (swing traders) based on a basic method of Ichimoku Kinko Hyo strategies.

The strategy is simple:

- Buy when the price breaks the cloud

- Close the trade when the price closes again inside the cloud.

The parameters that work best on this strategy are 10,30,60,30 and 1 for Senkou-Span A

but you can try classic Ichimoku parameters (9,26,52,26,26) or whatever you want like (7,22,44,22,22), (10,30,60,30,30) and others.

-1D chart

I have removed everything from the interface except the cloud to make it visually more aesthetic :D (but if you want to see all the ichimoku indicator you can put in again into the chart)

I have also added several functions for you to do your own backtesting:

- Date range

- TP AND SL method

- Includes long or short trades

The strategy starts with 500 $ and use 100% for trade to make the power of the compounding :P

Remember that this is for only educational porpouse and you must to do your own research and backtested on your usually market..

I hope you like it enjoy and support this indicator :)

Donate (BEP20) 0xC118f1ffB3ac40875C13B3823C182eA2Af344c6d

Scalping The Bull - BTC Chart for Trend AnalysisName: BTC Chart for Trend Analysis

Category: Scalping, Trend Analysis .

Timeframe: 1M, 5M, 30M, 1D depending on the specific technique.

Technical Analysis: The indicator supports the operations of the trader named "Scalping The Bull" who uses BTC as an Index for Crypto trading.

Suggested usage: When trading on altcoins, to check whether or not they are trending with Bitcoin and whether those anticipate its movements.

It is therefore possible to see Bitcoin specifically if it makes red or green candles and how it is positioned with respect to the EMA 5, 10, 60, 223, however configurable from the panel.

Used in conjunction with Scalping The Bull Indicator or PRO Indicator, on the main panel.

Configuration:

EMA Length:

- EMA 1: by default 5, configurable

- EMA 2: by default 10, configurable

- EMA 3: by default 60, configurable

- EMA 4: by default 223, configurable

Colors can be modified from "Settings" > "Style"

Designed to be used with the following the indicator:

lower_tf█ OVERVIEW

This library is a Pine programmer’s tool containing functions to help those who use the request.security_lower_tf() function. Its `ltf()` function helps translate user inputs into a lower timeframe string usable with request.security_lower_tf() . Another function, `ltfStats()`, accumulates statistics on processed chart bars and intrabars.

█ CONCEPTS

Chart bars

Chart bars , as referred to in our publications, are bars that occur at the current chart timeframe, as opposed to those that occur at a timeframe that is higher or lower than that of the chart view.

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 intrabars at the LTF of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This framework exemplifies how authors can determine which LTF to use by examining the chart's timeframe. The LTF determines how many intrabars are examined for each chart bar; the lower the timeframe, the more intrabars are analyzed.

Intrabar precision

The precision of calculations increases with the number of intrabars analyzed for each chart bar. As there is a 100K limit to the number of intrabars that can be analyzed by a script, a trade-off occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

█ `ltf()`

This function returns a timeframe string usable with request.security_lower_tf() . It calculates the returned timeframe by taking into account a user selection between eight different calculation modes and the chart's timeframe. You send it the user's selection, along with the text corresponding to the eight choices from which the user has chosen, and the function returns a corresponding LTF string.

Because the function processes strings and doesn't require recalculation on each bar, using var to declare the variable to which its result is assigned will execute the function only once on bar zero and speed up your script:

var string ltfString = ltf(ltfModeInput, LTF1, LTF2, LTF3, LTF4, LTF5, LTF6, LTF7, LTF8)

The eight choices users can select from are of two types: the first four allow a selection from the desired amount of chart bars to be covered, the last four are choices of a fixed number of intrabars to be analyzed per chart bar. Our example code shows how to structure your input call and then make the call to `ltf()`. By changing the text associated with the `LTF1` to `LTF8` constants, you can tailor it to your preferences while preserving the functionality of `ltf()` because you will be sending those string constants as the function's arguments so it can determine the user's selection. The association between each `LTFx` constant and its calculation mode is fixed, so the order of the arguments is important when you call `ltf()`.

These are the first four modes and the `LTFx` constants corresponding to each:

Covering most chart bars (least precise) — LTF1

Covers all chart bars. This is accomplished by dividing the current timeframe in seconds by 4 and converting that number back to a string in timeframe.period format using secondsToTfString() . Due to the fact that, on premium subscriptions, the typical historical bar count is between 20-25k bars, dividing the timeframe by 4 ensures the highest level of intrabar precision possible while achieving complete coverage for the entire dataset with the maximum allowed 100K intrabars.

Covering some chart bars (less precise) — LTF2

Covering less chart bars (more precise) — LTF3

These levels offer a stepped LTF in relation to the chart timeframe with slightly more, or slightly less precision. The stepped lower timeframe tiers are calculated from the chart timeframe as follows:

Chart Timeframe Lower Timeframe

Less Precise More Precise

< 1hr 1min 1min

< 1D 15min 1min

< 1W 2hr 30min

> 1W 1D 60min

Covering the least chart bars (most precise) — LTF4

Analyzes the maximum quantity of intrabars possible by using the 1min LTF, which also allows the least amount of chart bars to be covered.

The last four modes allow the user to specify a fixed number of intrabars to analyze per chart bar. Users can choose from 12, 24, 50 or 100 intrabars, respectively corresponding to the `LTF5`, `LTF6`, `LTF7` and `LTF8` constants. The value is a target; the function will do its best to come up with a LTF producing the required number of intrabars. Because of considerations such as the length of a ticker's session, rounding of the LTF to the closest allowable timeframe, or the lowest allowable timeframe of 1min intrabars, it is often impossible for the function to find a LTF producing the exact number of intrabars. Requesting 100 intrabars on a 60min chart, for example, can only produce 60 1min intrabars. Higher chart timeframes, tickers with high liquidity or 24x7 markets will produce optimal results.

█ `ltfStats()`

`ltfStats()` returns statistics that will be useful to programmers using intrabar inspection. By analyzing the arrays returned by request.security_lower_tf() in can determine:

• intrabarsInChartBar : The number of intrabars analyzed for each chart bar.

• chartBarsCovered : The number of chart bars where intrabar information is available.

• avgIntrabars : The average number of intrabars analyzed per chart bar. Events like holidays, market activity, or reduced hours sessions can cause the number of intrabars to vary, bar to bar.

The function must be called on each bar to produce reliable results.

█ DEMONSTRATION CODE

Our example code shows how to provide users with an input from which they can select a LTF calculation mode. If you use this library's functions, feel free to reuse our input setup code, including the tooltip providing users with explanations on how it works for them.

We make a simple call to request.security_lower_tf() to fetch the close values of intrabars, but we do not use those values. We simply send the returned array to `ltfStats()` and then plot in the indicator's pane the number of intrabars examined on each bar and its average. We also display an information box showing the user's selection of the LTF calculation mode, the resulting LTF calculated by `ltf()` and some statistics.

█ NOTES

• As in several of our recent publications, this script uses secondsToTfString() to produce a timeframe string in timeframe.period format from a timeframe expressed in seconds.

• The script utilizes display.data_window and display.status_line to restrict the display of certain plots.

These new built-ins allow coders to fine-tune where a script’s plot values are displayed.

• We implement a new recommended best practice for tables which works faster and reduces memory consumption.

Using this new method, tables are declared only once with var , as usual. Then, on bar zero only, we use table.cell() calls to populate the table.

Finally, table.set_*() functions are used to update attributes of table cells on the last bar of the dataset.

This greatly reduces the resources required to render tables. We encourage all Pine Script™ programmers to do the same.

Look first. Then leap.

█ FUNCTIONS

The library contains the following functions:

ltf(userSelection, choice1, choice2, choice3, choice4, choice5, choice6, choice7, choice8)

Selects a LTF from the chart's TF, depending on the `userSelection` input string.

Parameters:

userSelection : (simple string) User-selected input string which must be one of the `choicex` arguments.

choice1 : (simple string) Input selection corresponding to "Least precise, covering most chart bars".

choice2 : (simple string) Input selection corresponding to "Less precise, covering some chart bars".

choice3 : (simple string) Input selection corresponding to "More precise, covering less chart bars".

choice4 : (simple string) Input selection corresponding to "Most precise, 1min intrabars".

choice5 : (simple string) Input selection corresponding to "~12 intrabars per chart bar".

choice6 : (simple string) Input selection corresponding to "~24 intrabars per chart bar".

choice7 : (simple string) Input selection corresponding to "~50 intrabars per chart bar".

choice8 : (simple string) Input selection corresponding to "~100 intrabars per chart bar".

Returns: (simple string) A timeframe string to be used with `request.security_lower_tf()`.

ltfStats()

Returns statistics about analyzed intrabars and chart bars covered by calls to `request.security_lower_tf()`.

Parameters:

intrabarValues : (float [ ]) The ID of a float array containing values fetched by a call to `request.security_lower_tf()`.

Returns: A 3-element tuple: [ (series int) intrabarsInChartBar, (series int) chartBarsCovered, (series float) avgIntrabars ].

Higher Time Frame EMAs and 1% volatility indicatorSet the "higher time frame" (HTF) from which the EMAs will be calculated in all timeframes.

Example: I chose timeframe 1D and I will see the EMAs from TF 1D also in smaller TF as 1, 5, 30, 60 minutes.

There are 4 EMAs. The default values are 5, 10, 60 and 223 periods from "Scalping the Bull" indicator.

You can change the periods of each EMA.

The indicator have also a volatility indication, showing -1% and +1% price levels.

RSI ModifiedThe RSI is an excellent indicator for determining when equities are overbought/oversold. Though I believe there is a shortcoming in using the 70/30 levels since they are static and do not adjust for when an equity is trending. It stands to reason that in a downtrend, the overbought might be less than 70 and the oversold less than 30—Vice versa for a bull trend. Using the built-in function of pivots, I have attempted to create overbought/oversold lines that adjust with the trend. Leaving the 70/30 lines on the indicator also helps visualize the equity trend. All pivot settings are adjustable in the input menu. The pivot limits serve as a filter for recording pivot points. For example, with an upper pivot limit of 60, only pivots greater than 60 will be recorded into the array used to determine overbought. The crosses represent which values are used to determine overbought/oversold and do not provide timely indications.

Fast v Slow Moving Averages Strategy (Variable) [divonn1994]This is a simple moving average based strategy that takes 2 moving averages, a Fast and a Slow one, plots them both, and then decides to enter a 'long' position or exit it based on whether the two lines have crossed each other. It goes 'long when the Fast Moving Average crosses above the Slow Moving Average. This could indicate upwards momentum in prices in the future. It then exits the position when the the Fast Moving Average crosses back below. This could indicate downwards momentum in prices in the future. This is only speculative, though, but sometimes it can be a very good indicator/strategy to predict future action.

I've tried some strategy settings and I found different promising strategies. Here are a few:

BTCUSD ( BitStamp ) 1 Day Timeframe : EMA, Fast length 25 bars, Slow length 62 bars => 28,792x net profit (default)

BTCUSD ( BitStamp ) 1 Day Timeframe : VWMA, Fast length 21 bars, Slow length 60 bars => 15,603x net profit

BTCUSD ( BitStamp ) 1 Day Timeframe : SMA, Fast length 18 bars, Slow length 51 bars => 19,507x net profit

BTCUSD ( BitStamp ) 1 Day Timeframe : RMA, Fast length 20 bars, Slow length 52 bars => 5,729x net profit

BTCUSD ( BitStamp ) 1 Day Timeframe : WMA, Fast length 29 bars, Slow length 60 bars => 19,869x net profit

Features:

-You can choose your preferred moving average: SMA , EMA , WMA , RMA & VWMA .

-You can change the length average for each moving average

-I made the background color Green when you're currently in a long position and Red when not. I made it so you can see when you'd be actively in a trade or not. The Red and Green background colors can be toggled on/off in order to see other indicators more clearly overlayed in the chart, or if you prefer a cleaner look on your charts.

-I also have a plot of the Fast moving average and Slow moving average together. The Opening moving average is Purple, the Closing moving average is White. White on top is a sign of a potential upswing and purple on top is a sign of a potential downswing. I've made this also able to be toggled on/off.

Let me know if you think I should change anything with my script, I'm always open to constructive criticism so feel free to comment below :)

Inside Bar SetupScript Details

- This script plots Inside Bar for given day in selected time-frame (applicable only for Timeframes < Day)

- Basis plotted inside bar, relevant targets are marked on the chart

- Targets can be customised from script settings. Example, if range of mother candle is 10 points, then T1 is 10 * x above/below mother candle and T2 is 10 * y above/below mother candle. This x & y are configured via script settings

How to use this script ?

- This script works well on 10-15 mins timeframe for stocks, 15/30 mins timeframe for nifty index and 30/60 mins time frame for bank nifty index

- If mother candle high is broken, take long trade with SL of mother candle low and if low is broken, take short trade with SL of mother candle high

Remember:

1. Above logic is to be combined with support/resistances i.e. price action. This script is an add-on to price action analysis giving you more conviction.

2. If range of mother candle is very high, it is recommended to avoid the trade.

3. Basis inside bar formed on higher time frame, take trade on basis of lower time frame i.e if inside bar is formed on 60 mins, take trade on the basis of 10-15 mins time frame

Example:

1. As seen in the chart, Nifty is near it's resistance and we are seeing Inside Bar being formed, In such scenario, even if High of Mother Candle is broken, we should be more interested to short as we are near resistance and probability of getting our targets in long side is less.

2. So, if I see breakdown of mother candle i.e. price going below low of mother candle, we will short with SL of high of mother candle.

3. As seen in the chart, both the targets are achieved.

Additional Info:

1. Targets on Long/Short Side can be configured via settings. For indices 1 times/1.5 times the range works well.

2. This script plots targets basis the first inside bar formed in the day for selected time frame.

3. Inside bars formed through out the day are coloured separately but lines are plotted only on the basis of 1st formed inside bar as this strategy works well for the first formed inside bar)

4. Don't forget to check volume in case of breakout/breakdown.

Note:

1. Mother Candle - First Candle of Inside Bar

2. Child Candle - Candle formed inside Mother Candle (Second Candle of Inside Bar)

Happy Trading :)

VIDYA Trend StrategyOne of the most common messages I get is people reaching out asking for quantitative strategies that trade cryptocurrency. This has compelled me to write this script and article, to help provide a quantitative/technical perspective on why I believe most strategies people write for crypto fail catastrophically, and how one might build measures within their strategies that help reduce the risk of that happening. For those that don't trade crypto, know that these approaches are applicable to any market.

I will start off by qualifying up that I mainly trade stocks and ETFs, and I believe that if you trade crypto, you should only be playing with money you are okay with losing. Most published crypto strategies I have seen "work" when the market is going up, and fail catastrophically when it is not. There are far more people trying to sell you a strategy than there are people providing 5-10+ year backtest results on their strategies, with slippage and commissions included, showing how they generated alpha and beat buy/hold. I understand that this community has some really talented people that can create some really awesome things, but I am saying that the vast majority of what you find on the internet will not be strategies that create alpha over the long term.

So, why do so many of these strategies fail?

There is an assumption many people make that cryptocurrency will act just like stocks and ETFs, and it does not. ETF returns have more of a Gaussian probability distribution. Because of this, ETFs have a short term mean reverting behavior that can be capitalized on consistently. Many technical indicators are built to take advantage of this on the equities market. Many people apply them to crypto. Many of those people are drawn down 60-70% right now while there are mean reversion strategies up YTD on equities, even though the equities market is down. Crypto has many more "tail events" that occur 3-4+ standard deviations from the mean.

There is a correlation in many equities and ETF markets for how long an asset continues to do well when it is currently doing well. This is known as momentum, and that correlation and time-horizon is different for different assets. Many technical indicators are built based on this behavior, and then people apply them to cryptocurrency with little risk management assuming they behave the same and and on the same time horizon, without pulling in the statistics to verify if that is actually the case. They do not.

People do not take into account the brokerage commissions and slippage. Brokerage commissions are particularly high with cryptocurrency. The irony here isn't lost to me. When you factor in trading costs, it blows up most short-term trading strategies that might otherwise look profitable.

There is an assumption that it will "always come back" and that you "HODL" through the crash and "buy more." This is why Three Arrows Capital, a $10 billion dollar crypto hedge fund is now in bankruptcy, and no one can find the owners. This is also why many that trade crypto are drawn down 60-70% right now. There are bad risk practices in place, like thinking the martingale gambling strategy is the same as dollar cost averaging while also using those terms interchangeably. They are not the same. The 1st will blow up your trade account, and the 2nd will reduce timing risk. Many people are systematically blowing up their trade accounts/strategies by using martingale and calling it dollar cost averaging. The more risk you are exposing yourself too, the more important your risk management strategy is.

There is an odd assumption some have that you can buy anything and win with technical/quantitative analysis. Technical analysis does not tell you what you should buy, it just tells you when. If you are running a strategy that is going long on an asset that lost 80% of its value in the last year, then your strategy is probably down. That same strategy might be up on a different asset. One might consider a different methodology on choosing assets to trade.

Lastly, most strategies are over-fit, or curve-fit. The more complicated and more parameters/settings you have in your model, the more likely it is just fit to historical data and will not perform similar in live trading. This is one of the reasons why I like simple models with few parameters. They are less likely to be over-fit to historical data. If the strategy only works with 1 set of parameters, and there isn't a range of parameters around it that create alpha, then your strategy is over-fit and is probably not suitable for live trading.

So, what can I do about all of this!?

I created the VIDYA Trend Strategy to provide an example of how one might create a basic model with a basic risk management strategy that might generate long term alpha on a volatile asset, like cryptocurrency. This is one (of many) risk management strategies that can reduce the volatility of your returns when trading any asset. I chose the Variable Index Dynamic Average (VIDYA) for this example because it's calculation filters out some market noise by taking into account the volatility of the underlying asset. I chose a trend following strategy because regressions are capturing behaviors that are not just specific to the equities market.

The more volatile an asset, the more you have to back-off the short term price movement to effectively trend-follow it. Otherwise, you are constantly buying into short term trends that don't represent the trend of the asset, then they reverse and loose money. This is why I am applying a trend following strategy to a 4 hour chart and not a 4 minute chart. It is also important to note that following these long term trends on a volatile asset exposes you to additional risk. So, how might one mitigate some of that risk?

One of the ways of reducing timing risk is scaling into a trade. This is different from "doubling down" or "trippling down." It is really a basic application of dollar cost averaging to reduce timing risk, although DCA would typically happen over a longer time period. If it is really a trend you are following, it will probably still be a trend tomorrow. Trend following strategies have lower win rates because the beginning of a trend often reverses. The more volatile the asset, the more likely that is to happen. However, we can reduce risk of buying into a reversal by slowly scaling into the trend with a small % of equity per trade.

Our example "VIDYA Trend Strategy" executes this by looking at a medium-term, volatility adjusted trend on a 4 hour chart. The script scales into it with 4% of the account equity every 4-hours that the trend is still up. This means you become fully invested after 25 trades/bars. It also means that early in the trade, when you might be more likely to experience a reversal, most of your account equity is not invested and those losses are much smaller. The script sells 100% of the position when it detects a trend reversal. The slower you scale into a trade, the less volatile your equity curve will be. This model also includes slippage and commissions that you can adjust under the "settings" menu.

This fundamental concept of reducing timing risk by scaling into a trade can be applied to any market.

Disclaimer: This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Cipher Twister - Long and ShortINTRO / NOTES:

This script is based on Market Cipher B Oscillator by Falcon

The difference in this script is that only the useful points are printed on the indicator, namely Long and Short Trade Execution signals to be used by a bot, namely the PT Bot.

The script also differs from the original that it has been upgraded to Pinescript v4

This oscillator can be used with ALL time frames, but generally works the best on 15 minute and 1 hour charts on ANY market, no matter, stock, forex, crypto, spot, futures, derivatives, Nasdaq etc...

DEFINITIONS:

This oscillator forms the foundation of Buy and Exit of Long and Short Trades.

There are 2 'Red' Lines at the top of the channel and 2 Green Lines at the bottom of the channel.

These two channels are set at default to be +53 / -53 and +60 / -60 respectively. These two lines will serve as the threshold point if one is to make cautious trades only.

There is a center line which divides the Oscillator into two parts. Above the center line, the market is in over bought territory and Below the center line is in over sold territory.

'Red' dots are drawn by the indicator to represent a potential Short (or a signal to exit from a Long position)

'Green' dots are drawn by the indicator to represent a potential Long (or a signal to exit from a Short position)

The 'Red' and 'Green' dots are draw when a Cross between both wt1 & wt2 cross, thus providing a fantastic indication of potential trend reversal and entry/exit of a position.

STRATEGY NOTES:

The strategy to use this indicator with for realistic and proper results would be to use it with an automated Trading Bot such as Profit Trailer (PT-BOT)

You could use this strategy manually, however it would mean you would need to sit in front of the screen all day and night long and activate the trades immediately after the 'red'/'green' dots are drawn. Usually this will result in non-optimal entries and exits as well as loss on various instances when a 'red' and 'green' dot are printed close together (which is usually when the market goes into correction/consolidation) and slow entries/exits will result in a loss rather than a small profit or exit at BE (Break Even)

ACTUAL STRATEGY (For use with automated bot)

To be used in conjunction with Heikin Ashi Candles for added cautionary measures

For LONGs ONLY

--------------------

1/ When 'Green' dot is drawn, ACTIVATE Long Position

(Use 1.5% Risk Management for each trade)

(Use Lot size based on 1.5% risk management and xLeverage (if any))

2/ Make sure bot Opens an SL (Stop Loss) value based on 1.5% Risk Management

3/ When 'Red' dot is drawn, CLOSE Long Position.

*If you want to add extra caution to your trade, only activate the trade if the 'Green' dot is BELOW the 'Green' Markers

*For added caution, use color coded Heikin Ashi candles to 'confirm' Activation and Closing of a trade in the bot configuration

---------------------------------------------------------------------------------------------------

For SHORTs ONLY

--------------------

1/ When 'Red' dot is drawn, ACTIVATE Short Position

(Use 1.5% Risk Management for each trade)

(Use Lot size based on 1.5% risk management and xLeverage (if any))

2/ Make sure bot Opens an SL (Stop Loss) value based on 1.5% Risk Management

3/ When 'Green' dot is drawn, CLOSE Short Position

*If you want to add extra caution to your trade, only activate the trade if the 'Red' dot is Above the Red Markers

*For added caution, use color coded Heikin Ashi candles to 'confirm' Activation and Closing of a trade in the bot configuration

---------------------------------------------------------------------------------------------------

Supplementary Notes:

Make sure that your bot configuration will only activate ONE TRADE when the 'Green'/'Red' dot appears.

Occasionally during high volatility , 'red'/'green' dots will appear intermittently before remaining drawn, thus the oscillator 'redraws' the dots during market movement.

There will be times where occasionally a 'green' dot or a 'red' dot will appear, the trade will be opened, but the trade will fail due to the market manipulation (algorithm/market maker bots/fake volume etc), to wipe out those trading on derivatives and futures markets using leverage. Do not worry about this, no bot can make 100% wins, no strategy will achieve 100% win ratio and one necessarily doesn't need a high win ratio when using strict money management practices with your trading for SL and lot size.

If you use this method, you will see great results, but again I must stress, using this method with a fully automated bot is the only way to achieve proper results.

Weighted Relative Strength IndexWRSI uses 3 different user defined time frames with user defined weight on each time frame to give a final RSI value

Default values:

RSI 1 = 5 minute timeframe with a weightage of 9:14

RSI 2 = 15 minute timeframe with a weightage of 4:14

RSI 1 = 60 minute timeframe with a weightage of 1:14

Works best on a 15 min chart.

Please note this indicator will show exactly same values on all time frame charts so if you are looking at a daily chart you may want to change to 60 min, Daily & Weekly RSI time frame in settings.

The weights used here are basically sqaures of 1,2,& 3, you may choose any numbers that work for you.

The RSI length taken here is 27 (count of nakshatras)

The RSI MA length taken here is 28 (count of nakshatras + Abhijit Nakshatra)

You can obviously change it to what works best for you.

MME MTF CCIHi All,

This is a Dual/Multi TF CCI script to be used for Intraday as well as positional system.

Intraday:

Chart TF : 5 mins

Underlying Trend CCI : CCI 34 of 30 mins TF

Immediate Trend CCI : CCI 34 of 5 mins TF

Execution CCI : CCI 8 of 5 mins TF

The CCIs are used for entry, exit during momentum breakouts or pullbacks.

General Long Setup:

Buy at CCI-8 5m below -135, when CCI-34 30 mins is > +100. Long exit when CCI 34 5 min < -60

General Short Setup:

Sell at CCI-8 5m above -135, when CCI-34 30 mins is < -100. Short exit when CCI 34 5 min > +60

The same CCI settings can be used for positional or investment per appropriate timeframes one is interested to trade, along with HTF above in ratio 1:5.

Hope its helpful!

Time█ OVERVIEW

This library is a Pine Script™ programmer’s tool containing a variety of time related functions to calculate or measure time, or format time into string variables.

█ CONCEPTS

`formattedTime()`, `formattedDate()` and `formattedDay()`

Pine Script™, like many other programming languages, uses timestamps in UNIX format, expressed as the number of milliseconds elapsed since 00:00:00 UTC, 1 January 1970. These three functions convert a UNIX timestamp to a formatted string for human consumption.

These are examples of ways you can call the functions, and the ensuing results:

CODE RESULT

formattedTime(timenow) >>> "00:40:35"

formattedTime(timenow, "short") >>> "12:40 AM"

formattedTime(timenow, "full") >>> "12:40:35 AM UTC"

formattedTime(1000 * 60 * 60 * 3.5, "HH:mm") >>> "03:30"

formattedDate(timenow, "short") >>> "4/30/22"

formattedDate(timenow, "medium") >>> "Apr 30, 2022"

formattedDate(timenow, "full") >>> "Saturday, April 30, 2022"

formattedDay(timenow, "E") >>> "Sat"

formattedDay(timenow, "dd.MM.yy") >>> "30.04.22"

formattedDay(timenow, "yyyy.MM.dd G 'at' hh:mm:ss z") >>> "2022.04.30 AD at 12:40:35 UTC"

These functions use str.format() and some of the special formatting codes it allows for. Pine Script™ documentation does not yet contain complete specifications on these codes, but in the meantime you can find some information in the The Java™ Tutorials and in Java documentation of its MessageFormat class . Note that str.format() implements only a subset of the MessageFormat features in Java.

`secondsSince()`

The introduction of varip variables in Pine Script™ has made it possible to track the time for which a condition is true when a script is executing on a realtime bar. One obvious use case that comes to mind is to enable trades to exit only when the exit condition has been true for a period of time, whether that period is shorter that the chart's timeframe, or spans across multiple realtime bars.

For more information on this function and varip please see our Using `varip` variables publication.

`timeFrom( )`

When plotting lines , boxes , and labels one often needs to calculate an offset for past or future end points relative to the time a condition or point occurs in history. Using xloc.bar_index is often the easiest solution, but some situations require the use of xloc.bar_time . We introduce `timeFrom()` to assist in calculating time-based offsets. The function calculates a timestamp using a negative (into the past) or positive (into the future) offset from the current bar's starting or closing time, or from the current time of day. The offset can be expressed in units of chart timeframe, or in seconds, minutes, hours, days, months or years. This function was ported from our Time Offset Calculation Framework .

`formattedNoOfPeriods()` and `secondsToTfString()`

Our final two offerings aim to confront two remaining issues:

How much time is represented in a given timestamp?

How can I produce a "simple string" timeframe usable with request.security() from a timeframe expressed in seconds?

`formattedNoOfPeriods()` converts a time value in ms to a quantity of time units. This is useful for calculating a difference in time between 2 points and converting to a desired number of units of time. If no unit is supplied, the function automatically chooses a unit based on a predetermined time step.

`secondsToTfString()` converts an input time in seconds to a target timeframe string in timeframe.period string format. This is useful for implementing stepped timeframes relative to the chart time, or calculating multiples of a given chart timeframe. Results from this function are in simple form, which means they are useable as `timeframe` arguments in functions like request.security() .

█ NOTES

Although the example code is commented in detail, the size of the library justifies some further explanation as many concepts are demonstrated. Key points are as follows:

• Pivot points are used to draw lines from. `timeFrom( )` calculates the length of the lines in the specified unit of time.

By default the script uses 20 units of the charts timeframe. Example: a 1hr chart has arrows 20 hours in length.

• At the point of the arrows `formattedNoOfPeriods()` calculates the line length in the specified unit of time from the input menu.

If “Use Input Time” is disabled, a unit of time is automatically assigned.

• At each pivot point a label with a formatted date or time is placed with one of the three formatting helper functions to display the time or date the pivot occurred.

• A label on the last bar showcases `secondsSince()` . The label goes through three stages of detection for a timed alert.

If the difference between the high and the open in ticks exceeds the input value, a timer starts and will turn the label red once the input time is exceeded to simulate a time-delayed alert.

• In the bottom right of the screen `secondsToTfString()` posts the chart timeframe in a table. This can be multiplied from the input menu.

Look first. Then leap.

█ FUNCTIONS

formattedTime(timeInMs, format)

Converts a UNIX timestamp (in milliseconds) to a formatted time string.

Parameters:

timeInMs : (series float) Timestamp to be formatted.

format : (series string) Format for the time. Optional. The default value is "HH:mm:ss".

Returns: (string) A string containing the formatted time.

formattedDate(timeInMs, format)

Converts a UNIX timestamp (in milliseconds) to a formatted date string.

Parameters:

timeInMs : (series float) Timestamp to be formatted.

format : (series string) Format for the date. Optional. The default value is "yyyy-MM-dd".

Returns: (string) A string containing the formatted date.

formattedDay(timeInMs, format)

Converts a UNIX timestamp (in milliseconds) to the name of the day of the week.

Parameters:

timeInMs : (series float) Timestamp to be formatted.

format : (series string) Format for the day of the week. Optional. The default value is "EEEE" (complete day name).

Returns: (string) A string containing the day of the week.

secondsSince(cond, resetCond)

The duration in milliseconds that a condition has been true.

Parameters:

cond : (series bool) Condition to time.

resetCond : (series bool) When `true`, the duration resets.

Returns: The duration in seconds for which `cond` is continuously true.

timeFrom(from, qty, units)

Calculates a +/- time offset in variable units from the current bar's time or from the current time.

Parameters:

from : (series string) Starting time from where the offset is calculated: "bar" to start from the bar's starting time, "close" to start from the bar's closing time, "now" to start from the current time.

qty : (series int) The +/- qty of units of offset required. A "series float" can be used but it will be cast to a "series int".

units : (series string) String containing one of the seven allowed time units: "chart" (chart's timeframe), "seconds", "minutes", "hours", "days", "months", "years".

Returns: (int) The resultant time offset `from` the `qty` of time in the specified `units`.

formattedNoOfPeriods(ms, unit)

Converts a time value in ms to a quantity of time units.

Parameters:

ms : (series int) Value of time to be formatted.

unit : (series string) The target unit of time measurement. Options are "seconds", "minutes", "hours", "days", "weeks", "months". If not used one will be automatically assigned.

Returns: (string) A formatted string from the number of `ms` in the specified `unit` of time measurement

secondsToTfString(tfInSeconds, mult)

Convert an input time in seconds to target string TF in `timeframe.period` string format.

Parameters:

tfInSeconds : (simple int) a timeframe in seconds to convert to a string.

mult : (simple float) Multiple of `tfInSeconds` to be calculated. Optional. 1 (no multiplier) is default.

Returns: (string) The `tfInSeconds` in `timeframe.period` format usable with `request.security()`.

JaeRSI+What is JaeRSI++

🥇 It is an indicator that detects and displays the RSI of the upper frame one step at a time

- It is no different from normal RSI but, u can see the RSI of the upper frame together

- Works based on 5m 15m 1h 4h 1d 1w

🥇Also, if the RSI is (over 70↗️) or (less than 30↘️), changes the background color

- If the background color is continuous, it is recommended to check the frame one step higher

🥇 Meaning of table (table)

- "🌈", RSI, Main, Danger in order

- RSI: It is divided into 5, 15, 60, 240 and indicates the current RSI of each frame (the background color is different from RSI : 33.0 below / 67.0 above)

- Main: Estimate the mainframe

If the previous 14 candles have entered the Danger zone (RSI : below 33.0 / above 67.0) or oversold/number, the corresponding frame is marked as the main frame.

- Danger: If abnormal RSI motion is detected (beam shape) due to sudden surge/fall in a frame, it warns that the frame may be the main frame.

==================================================================================

JaeRSI++란?

🥇 상위 프레임의 RSI를 추가로 표시해 주는 RSI 지표입니다

- 일반 RSI와 알고리즘의 차이가 없으나 상위 프레임의 RSI를 함께 볼 수 있습니다 (빨간 선으로 표시)

- 5m 15m 1h 4h 1d 1w 기준으로 작동합니다

🥇또한 RSI가 (70 이상↗️) 또는 (30↘️)인 경우 배경색을 변경합니다

- 배경색이 연속적인 경우 프레임을 한 단계 높게 확인하는 것이 좋습니다

🥇표(테이블)의 의미

- 순서대로 시간프레임 , RSI , 메인 , 위험

- RSI : 5, 15, 60, 240으로 나뉘어져 각각 프레임의 현재 RSI를 나타낸다 (33.0 아래 / 67.0 위 부터 배경색이 달라짐)

- 메인 : 메인프레임을 추정한다

이전 14개 캔들안에 꺵판존(33.0 아래 / 67.0 위) or 과매도/수에 들어간 적이 있다면 해당 프레임을 메인프레임으로 표시한다

- 위험 : 어떤 프레임에서 급등/급락하여 비 정상적인 RSI의 움직임이 감지된다면(빔 형태) 해당 프레임이 메인 프레임일 수 있다고 경고한다