Market Regime AnalyzerStatistical regime detection with forward-looking transition probabilities. Combines drift testing, variance ratios, and volume delta to classify markets into 5 regimes and quantify transition probabilities.

What Regime Are We In, and What's Likely Next?

That's the question this indicator answers with statistical rigor and forward-looking probabilities.

The Problem:

Most traders classify regimes arbitrarily: "Bull if price > 200 MA" or "Bear if RSI < 30." These rules ignore statistical significance, volume confirmation, and mean reversion patterns. The result? Late entries, false signals, and confusion when markets transition.

The Solution:

Market Regime Analyzer combines drift detection, variance ratio testing, and volume delta analysis to classify markets into 5 distinct regimes. Then it calculates the probability of transitioning to each regime based on historical patterns.

The Benefit:

Know not just where you are, but where you're likely going - with probabilities, not guesses.

The Five Market Regimes

🟢 Strong Bull (Regime 1)

- Statistically significant upward drift (t-stat > 1.96)

- Strong buying pressure (volume delta > 0.3)

- No mean reversion detected

- **Trade:** Trend-following strategies, ride the momentum

🟢 Weak Bull (Regime 2)

- Upward drift present

- BUT weak volume OR mean reversion detected

- **Trade:** Reduce position size, tighten stops, prepare for consolidation

⚪ Consolidation (Regime 3)

- No statistically significant drift

- Mixed volume signals

- Mean reversion likely present

- **Trade:** Range-trading, avoid trend-following systems

🔴 Weak Bear (Regime 4)

- Downward drift present

- BUT weak volume pressure

- **Trade:** Cautious shorts, reduce exposure, prepare for bounce

🔴 Strong Bear (Regime 5)

- Statistically significant downward drift (t-stat < -1.96)

- Strong selling pressure (volume delta < -0.3)

- No mean reversion detected

- **Trade:** Trend-following shorts, protective puts

The Statistical Framework

1. Drift Detection with T-Statistics

Instead of guessing if there's a trend, we test it statistically.

How it works:

- Calculates mean return over lookback period

- Standardizes by volatility

- Compares to significance threshold (default 1.96 = 95% confidence)

What it tells you:

- T-stat > 1.96: Statistically significant uptrend

- T-stat < -1.96: Statistically significant downtrend

- In between: No significant trend (consolidation)

Why it matters:

Only trades trends that are statistically validated, not just visually apparent.

2. Mean Reversion Testing (Variance Ratio)

Based on Lo & MacKinlay (1988) research, this detects when markets are range-bound.

How it works:

- Compares variance at different time scales

- Variance Ratio < 0.8 indicates mean reversion

What it tells you:

- Mean reversion = NO: Trends can continue

- Mean reversion = YES: Expect price to return to mean, not breakout

Why it matters:

Prevents chasing breakouts in range-bound markets.

3. Volume Delta Analysis

Total volume tells you HOW MUCH traded. Volume delta tells you WHO won.

How it works:

- Buying pressure - Selling pressure = Volume Delta

- Normalized to show relative strength

What it tells you:

- Strong positive delta (>0.3): Buyers in control

- Strong negative delta (<-0.3): Sellers in control

- Weak delta: No clear winner

Why it matters:

Price can move up on weak buying or down on weak selling. Volume delta reveals the truth.

4. Transition Probability Matrix

Historical regime changes predict future regime changes.

How it works:

- Tracks every regime transition over last 100 bars (configurable)

- Builds probability distribution for next regime

- Updates continuously

Example:

Current: Strong Bull

Historical transitions from Strong Bull:

- Stayed Strong Bull: 45%

- Became Weak Bull: 30%

- Became Consolidation: 20%

- Became Weak Bear: 4%

- Became Strong Bear: 1%

What it tells you:

Strong Bull has 75% chance of staying bullish (45% + 30%), only 5% chance of bearish turn.

Why it matters:

Adapts to your specific market's behavior patterns.

How to Use This Indicator

Strategy Adaptation

In Strong Bull/Bear Regimes:

- Use trend-following strategies

- Wider stops, let winners run

- Add to positions on pullbacks

- High confidence in directional trades

In Weak Bull/Bear Regimes:

- Reduce position sizes by 50%

- Tighter stops

- Take profits earlier

- Prepare for regime change

In Consolidation:

- Switch to range-trading strategies

- Avoid trend-following systems

- Sell resistance, buy support

- Wait for regime change before trend trades

Risk Management

Position Sizing:

- Strong regime + high continuation probability (>60%) = Normal size

- Weak regime OR high transition probability = Half size

- Consolidation = Quarter size or skip

Stop Loss Placement:

- Strong regime: Use wider stops (2x ATR)

- Weak regime: Tighter stops (1x ATR)

- Consolidation: Very tight stops (0.5x ATR)

Entry Timing

Best entries:

- Regime just changed to Strong Bull/Bear

- High probability (>50%) of staying in current regime

- No divergence signals present

- Drift and volume delta aligned

Avoid entries:

- High probability of regime change

- Divergence signals appearing

- Mean reversion detected in trending regime

- Weak volume despite price movement

Reading the Dashboard

Current Regime

Color-coded for instant recognition:

- Dark Green = Strong Bull

- Light Green = Weak Bull

- Gray = Consolidation

- Light Red = Weak Bear

- Dark Red = Strong Bear

Annualized Drift

Expected annual return based on recent trend.

- Positive = Upward bias

- Negative = Downward bias

- Near zero = No directional edge

T-Statistic

Measures statistical significance of drift.

- > 1.96 = 95% confident in uptrend

- < -1.96 = 95% confident in downtrend

- Between = Not statistically significant

Mean Reversion

- Yes = Expect price to return to mean (range-bound)

- No = Trends can continue (trending market)

Volume Pressure

Normalized volume delta strength.

- > 0.3 = Strong buying

- < -0.3 = Strong selling

- Near 0 = Balanced

Transition Probabilities

Shows most likely next regime.

- Highest probability = Most likely outcome

- Evenly distributed = High uncertainty

- Concentrated = High confidence in direction

Practical Examples

Example 1: Strong Bull with High Continuation

Dashboard shows:

Current Regime: Strong Bull

Drift: +22% annualized

T-Stat: 3.2

Mean Reversion: No

Volume Pressure: +0.45

Probabilities:

→ Strong Bull: 50%

→ Weak Bull: 25%

→ Consolidation: 20%

→ Bears: 5%

Interpretation:

- Strong uptrend (t-stat 3.2 >> 1.96)

- No mean reversion = trends can continue

- Strong buying pressure (0.45 > 0.3)

- 75% chance stays bullish (50% + 25%)

Action:

- Full position size on long setups

- Use trend-following entries

- Wider stops (2x ATR)

- High conviction trades

Example 2: Weak Bull Before Consolidation

Dashboard shows:

Current Regime: Weak Bull

Drift: +8% annualized

T-Stat: 1.2

Mean Reversion: Yes

Volume Pressure: +0.15

Probabilities:

→ Strong Bull: 10%

→ Weak Bull: 30%

→ Consolidation: 50%

→ Weak Bear: 10%

Interpretation:

- Weak drift (t-stat 1.2 < 1.96)

- Mean reversion detected = range-bound likely

- Weak volume (0.15 < 0.3)

- 50% chance of consolidation

Action:

- Reduce long positions

- Tighten stops

- Prepare for range-bound trading

- Avoid new trend trades

Example 3: Regime Transition Alert

Previous: Weak Bull

Current: Consolidation

Volume divergence signal appeared:

Price made new high, volume delta weakened

Interpretation:

- Trend exhausted

- Buyers losing control

- Regime confirmed the transition

Action:

- Exit trend-following longs

- Switch to range-trading approach

- Wait for new regime before new directional trades

Settings Guide

### Regime Detection Period (50)

Number of bars for statistical calculations.

- **30-40:** More responsive, catches changes faster, more regime switches

- **50 (default):** Balanced for daily/4H charts

- **75-100:** More stable, fewer false regime changes, slower to adapt

Transition History Depth (100)

How much history to use for probabilities.

- **50-75:** Adapts quickly to recent behavior

- **100 (default):** Balanced robustness

- **150-200:** More stable probabilities, slower to adapt

Volume Delta Period (14)

Period for volume calculations.

- **7-10:** More sensitive to volume shifts

- **14 (default):** Standard period

- **20-30:** Smoother, less noise

Significance Threshold (1.96)

T-statistic required for trend classification.

- **1.64:** 90% confidence, more trend regimes detected

- **1.96 (default):** 95% confidence, balanced

- **2.58:** 99% confidence, very conservative, mostly consolidation

Best Practices

Do:

- Wait for regime confirmation (at least 3-5 bars in new regime)

- Use probabilities to size positions appropriately

- Combine with support/resistance for entries

- Respect mean reversion signals

- Adapt strategy to current regime

Don't:

- Trade every regime change immediately

- Ignore high transition probabilities

- Use trend strategies in consolidation

- Override statistical signals with gut feel

- Trade against Strong regimes without clear setup

Timeframe Recommendations

Daily Charts:

- Default settings work well

- Most reliable regime detection

- Best for swing trading

4H Charts:

- Use default or slightly higher lookback (60-75)

- Good for active swing trading

- More regime changes than daily

1H Charts:

- Reduce lookback to 30-40

- More noise, use with caution

- Better for intraday position trading

15M and below:

- Not recommended

- Too much noise for statistical validity

- Regimes change too frequently

Combining with Other Indicators

Works Well With:

Moving Averages

- Use regime for directional bias

- MAs for specific entry/exit points

Support/Resistance

- Regime shows context

- S/R shows specific levels

- High probability at confluence

Volume Profile

- Regime shows regime

- Profile shows where volume is

- Target high-volume nodes

RSI/MACD

- Regime provides context

- Momentum shows entry timing

- Combine for higher probability

Example Combined Setup

Regime: Strong Bull

Price: Above 200 MA

Level: Pullback to support

RSI: Oversold (30)

Volume Delta: Still positive

Setup: Long entry

Reason: Trend intact, healthy pullback, buyers still present

Divergence Signals

The indicator shows volume divergence warnings:

Bearish Divergence (Red Triangle Down)

- Price makes new high

- Volume delta makes lower high

- Warning: Buyers weakening, potential reversal

Bullish Divergence (Green Triangle Up)

- Price makes new low

- Volume delta makes higher low

- Warning: Sellers weakening, potential reversal

How to use:

- Divergence in Strong regime = early warning of regime change

- Confirms when regime actually transitions

- Don't trade divergence alone, wait for regime confirmation

Limitations

This Indicator Cannot:

**Predict black swan events** - Unexpected news overrides all technical regimes

**Work in all markets** - Needs liquid markets with reliable volume data

**Guarantee profits** - Probabilities are not certainties

**Replace fundamental analysis** - Technical regimes can diverge from fundamentals

Works Best:

- Liquid markets (major indices, forex, crypto, large-cap stocks)

- Daily and 4H timeframes

- Combined with other analysis

- With proper risk management

- In normal market conditions

Common Questions

"Why did the regime stay consolidation despite strong price move?"

The indicator detected mean reversion (variance ratio < 0.8), indicating the move will likely reverse. Or the move wasn't statistically significant (t-stat < 1.96). Trust the statistics over visual appearance.

"Probabilities show 30% for each regime. What does that mean?"

High uncertainty. The market is at an inflection point. Reduce position sizes and wait for clearer regime formation.

"Can I use this for day trading?"

Not recommended on timeframes below 1H. Statistical tests need sufficient data. Better suited for swing trading.

"Why does this show Strong Bull when my momentum indicators show weakness?"

Momentum can weaken while the trend remains statistically significant. The indicator focuses on drift and volume, not momentum. Consider it a different perspective.

Technical Notes

Volume Delta Approximation

Uses OHLCV data to approximate order flow:

- Buy volume ≈ Volume on up-closes

- Sell volume ≈ Volume on down-closes

- Delta = Buy - Sell

**Note:** Real order flow (from futures or Level 2) is more precise. This approximation works well on liquid markets.

Statistical Tests

Drift T-Test:

- Null hypothesis: No drift (mean return = 0)

- Reject if |t-stat| > threshold

- Based on standard hypothesis testing

Variance Ratio:

- Compares 2-period variance to 1-period variance

- Ratio = 1 for random walk

- Ratio < 1 for mean reversion

- Threshold of 0.8 based on empirical testing

Transition Probability Implementation

Due to Pine Script v5 limitations (no native 2D arrays), the 5×5 transition matrix is stored as a flat 1D array of 25 elements:

- Position maps to index: `row × 5 + col`

- Example: Transition from Regime 2 to Regime 4 is at index `1 × 5 + 3 = 8`

- Laplace smoothing (0.1) prevents zero probabilities

- Row sums normalized to calculate probabilities

This approach is computationally efficient and maintains statistical accuracy.

No Repainting

All calculations confirmed on bar close. Regime changes appear when the bar closes, not during formation. Historical analysis is accurate.

Alert Conditions

Regime Change

- Triggers when regime transitions to any new state

- Message shows new regime number (1-5)

Bearish Divergence

- Triggers when price makes new high but volume delta doesn't confirm

Bullish Divergence

- Triggers when price makes new low but volume delta doesn't confirm

Disclaimer

FOR EDUCATIONAL PURPOSES ONLY

This indicator uses statistical methods to analyze market regimes. It does not predict the future or guarantee trading success.

Markets are probabilistic, not deterministic. A 70% probability of staying bullish means 30% chance of regime change. Always use proper risk management.

Past regime transitions do not guarantee future transitions. Market structure can change. Statistical relationships can break down.

Never risk more than you can afford to lose. Use stop losses on every trade. Test thoroughly before live trading. Consult a qualified financial advisor.

© 2026 | Open Source

Statistical rigor meets practical application

Statistic

RSquared (log prices)Rolling Trend R² measures the strength of trends using a rolling R² calculation on log prices. Values near 1 indicate a strong, persistent trend, while low values signal choppy or mean-reverting conditions. Includes regime highlighting, reference levels, and an info panel for quick market state identification.

Monte Carlo Simulation BandsMonte Carlo Simulation v2.4.2

Plots a one-bar-ahead price distribution band built from many simulated paths. The green band shows empirical percentiles of simulated final prices—these are distribution bounds, not a confidence interval of the mean.

What It Does

Simulates many one-bar price paths using a directional random walk with volatility scaling (uniform shocks, not Gaussian GBM).

Plots Mean Forecast, Median Forecast, and configurable percentile bounds (default 5th/95th).

Optional rolling HTF-days mean line (yellow) for trend context.

Optional labels and forward projection lines.

Alerts when the confirmed close breaks above or below the percentile band.

Non-Repainting & HTF Behavior (Fail-Closed)

All calculations are gated to confirmed bars only via explicit no_repaint_ok gate (barstate.isconfirmed).

If you select an HTF Resolution, the script uses a strict request.security(..., lookahead_off, gaps_off) pipeline.

If HTF data is unavailable, outputs are na—no silent fallback to chart timeframe.

A separate "HTF Alignment (lagged)" plot shows the prior HTF close (htf_price ) as visual proof of no look-ahead.

Volatility Source & Scaling

If "Use Historical Volatility" is enabled, volatility is estimated from log returns on the selected resolution (HTF if set, otherwise chart).

Annualization adapts to session type:

Equities: 6.5 hours/day, 252 trading days/year

Crypto: 24 hours/day, 365 days/year

Substeps increase path smoothness within the same one-bar horizon—they do not extend the forecast to multiple bars.

Key Inputs

• Prob Up / Prob Down — Must satisfy Prob Up + Prob Down ≤ 1.0. If violated, simulation is skipped and table shows "✗ PROB>1".

• # Simulations / # Substeps — Higher = smoother/more stable, but slower. Default 100×100 is a good balance.

• Lower/Upper Percentile — Define the band width (e.g., 5 and 95 for a 90% distribution band).

• Run On Last Bar Only — Performance mode (recommended). Skips historical computation; updates on each new confirmed bar.

• Resolution (HTF) — Leave blank for chart timeframe, or set to Weekly/Monthly for HTF-aligned simulation.

• Crypto 24/7 Session? — Enable for crypto markets to use correct annualization (365d, 24h).

How to Use (Quickstart)

Start with defaults and keep Run On Last Bar Only = true for speed.

Set Prob Up and Prob Down so their sum ≤ 1.0 (e.g., 0.5 + 0.5 = 1.0 for neutral).

Enable "Use Historical Volatility" and set a Volatility Lookback (e.g., 20 bars) for data-driven vol.

Set Resolution (HTF) if you want the model to run on higher timeframe data (e.g., 1W). Expect updates only when a new HTF interval starts.

Choose percentiles (e.g., 5 and 95) to define your distribution band width.

Enable alerts for "Price Above Upper Percentile" or "Price Below Lower Percentile" to get notified of breakouts.

Limitations & Disclosures

Forecast horizon is one bar only. Substeps do not create a multi-bar forecast.

Model uses uniform shocks with direction chosen from Prob Up/Down. This is not Geometric Brownian Motion (GBM) and is not calibrated to any option-implied distribution.

Bounds are percentiles of final simulated prices, not a statistical confidence interval of the mean.

HTF mode updates at the start of a new HTF interval (first chart bar where the HTF timestamp changes), so the band appears "step-like" in realtime.

Historical volatility requires enough bars for the selected lookback; until then, values may be na.

Performance depends on Sims × Substeps; extreme settings (e.g., 500×500) can be slow.

This indicator does not predict direction—it shows a probabilistic range based on your inputs.

Historical Returns [BigBeluga]🔵 OVERVIEW

The Historical Returns indicator visualizes daily and monthly return data to help traders assess seasonal performance and volatility behavior. It provides a clean and informative dashboard showing the current month’s daily return bubbles, monthly return curves, and a snapshot of the current month and year performance. This tool is ideal for spotting recurring return patterns and understanding the broader profitability context of a symbol.

🔵 CONCEPTS

Daily Return Bubbles: Each trading day is analyzed for its return percentage, and plotted as a bubble with size proportional to the return magnitude.

Monthly Performance Curves: Average or cumulative returns are calculated and plotted to show how the current month is performing relative to historical averages.

Current Year Return: Current year performance as a single return value, giving traders context on long-term profitability.

Current Month Average Return: Current month average performance as a single return value, giving traders context on short-term profitability.

Extreme Return Labels: Optionally highlights daily returns above +4% or below -4% with labeled percentages for spike recognition.

🔵 FEATURES

Shows daily return bubbles (1%–7%+), color-coded by direction.

Labels monthly returns with the month name and percentage value.

Displays a performance dashboard with:

Daily return heatmap for the current month.

Average return for the current month.

Year-to-date return.

Toggle between average and cumulative modes for monthly return curves.

Clearly marks days with abnormal return spikes using optional labels.

Clean fallback warning if not on a daily chart ("⚠️USE DAILY TIMEFRAME").

Custom color themes for bullish and bearish values.

🔵 HOW TO USE

Use the monthly return curve to compare how the current month is performing against historical averages.

Look for clusters of positive or negative bubbles as signals of strong directional weeks.

Watch extreme return labels for volatility spikes or catalyst days.

Use year-to-date return to assess how the asset is trending in the broader macro cycle.

Combine with other BigBeluga tools to align trades with historically favorable periods.

🔵 CONCLUSION

Historical Returns is your visual companion for return analytics — helping you identify profitable months, detect volatility surges, and understand historical seasonality at a glance. With a clean dashboard and insightful overlays, this tool supports better timing and improved statistical edge in both short- and long-term trades.

Stock Relative Strength Rotation Graph🔄 Visualizing Market Rotation & Momentum (Stock RSRG)

This tool visualizes the sector rotation of your watchlist on a single graph. Instead of checking 40 different charts, you can see the entire market cycle in one view. It plots Relative Strength (Trend) vs. Momentum (Velocity) to identify which assets are leading the market and which are lagging.

📜 Credits & Disclaimer

Original Code: Adapted from the open-source " Relative Strength Scatter Plot " by LuxAlgo.

Trademark: This tool is inspired by Relative Rotation Graphs®. Relative Rotation Graphs® is a registered trademark of JOOS Holdings B.V. This script is neither endorsed, nor sponsored, nor affiliated with them.

📊 How It Works (The Math)

The script calculates two metrics for every symbol against a benchmark (Default: SPX):

X-Axis (RS-Ratio): Is the trend stronger than the benchmark? (>100 = Yes)

Y-Axis (RS-Momentum): Is the trend accelerating? (>100 = Yes)

🧩 The 4 Market Quadrants

🟩 Leading (Top-Right): Strong Trend + Accelerating. (Best for holding).

🟦 Improving (Top-Left): Weak Trend + Accelerating. (Best for entries).

⬜ Weakening (Bottom-Right): Strong Trend + Decelerating. (Watch for exits).

🟥 Lagging (Bottom-Left): Weak Trend + Decelerating. (Avoid).

✨ Significant Improvements

This open-source version adds unique features not found in standard rotation scripts:

📝 Quick-Input Engine: Paste up to 40 symbols as a single comma-separated list (e.g., NVDA, AMD, TSLA). No more individual input boxes.

🎯 Quadrant Filtering: You can now hide specific quadrants (like "Lagging") to clear the noise and focus only on actionable setups.

🐛 Trajectory Trails: Visualizes the historical path of the rotation so you can see the direction of momentum.

🛠️ How to Use

Paste Watchlist: Go to settings and paste your symbols (e.g., US Sectors: XLK, XLF, XLE...).

Find Entries: Look for tails moving from Improving ➔ Leading.

Find Exits: Be cautious when tails move from Leading ➔ Weakening.

Zoom: Use the "Scatter Plot Resolution" setting to zoom in or out if dots are bunched up.

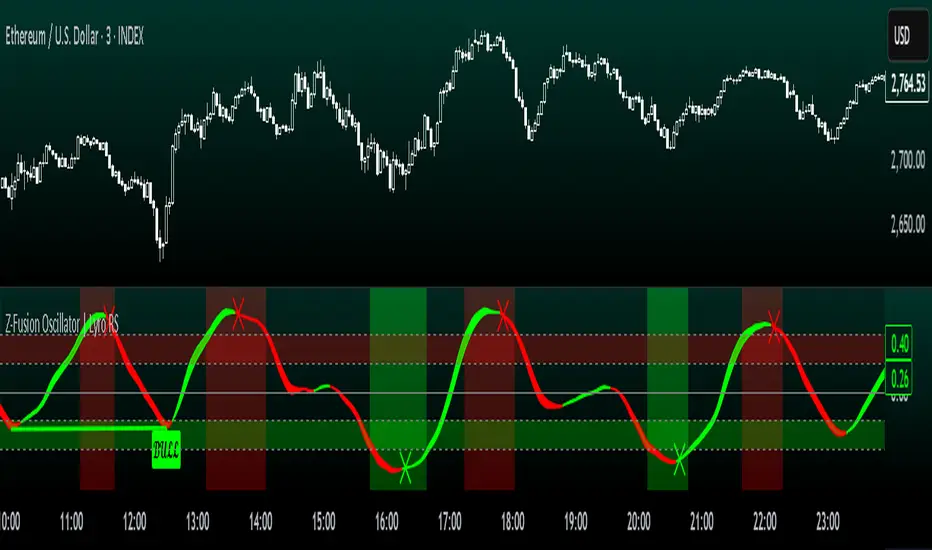

Z-Fusion Oscillator | Lyro RSThe Z-Fusion Oscillator converts five momentum indicators into Z-scores and blends them into one normalized signal that adapts across markets.

By combining normalization, smoothing, and divergence detection, users can easily identify when momentum is accelerating, weakening, reversing, or entering extreme zones

🔶 USAGE

The Z-Fusion Oscillator is designed to give traders a unified reading of market momentum—removing the noise of comparing tools that normally run on different scales.

By transforming RSI, MACD histogram, Stochastic, Momentum, and Rate of Change into Z-scores, this tool standardizes all inputs, making trend strength and shifts easier to interpret.

A dual-line system (fast Z-fusion line + slower baseline) highlights turning points, while overbought/oversold bands and “X-marks” help traders spot exhaustion and potential reversals.

🔹 Unified Momentum Structure

The indicator’s core strength comes from combining five Z-scored signals into one average.

Which makes momentum behavior more consistent across assets, reduces false extremes, and highlights true shifts in trend conviction.

🔹 Divergence Detection

The tool includes fully integrated divergence detection:

Regular Bullish Divergence: Price makes a lower low while Z-Fusion forms a higher low.

Regular Bearish Divergence: Price makes a higher high while Z-Fusion forms a lower high

Bullish and bearish divergences are marked directly on the oscillator with labels and colored pivot connections, making hidden momentum shifts obvious.

🔹 Visual Extremes

Two sets of upper and lower Z-score thresholds help identify:

Extreme overbought surges

Extreme oversold drops

Reversal zones

Potential exhaustion conditions

Background coloring reinforces when the oscillator moves beyond major levels, helping traders quickly assess momentum pressure.

🔹 Detecting Momentum Anomalies

Z-scores allow the oscillator to highlight when market momentum behaves abnormally relative to its own recent history.

For example:

The oscillator reaching +1 or –1 after an extended trend may indicate a climax.

A sharp Z-score reversal within an extreme zone can signal a trend exhaustion or a corrective move.

Divergences often appear earlier due to normalization smoothing out indicator noise.

This makes the Z-Fusion Oscillator particularly useful for spotting subtle shifts in trend direction that traditional indicators may miss.

🔶 DETAILS

🔹 Composite Z-Score Framework

Each momentum tool is smoothed, normalized, and transformed:

RSI → EMA-smoothed, Z-scored

MACD histogram → Z-scored

Stochastic → EMA + SMA smoothing, then Z-scored

Momentum → EMA-smoothed, Z-scored

Rate of Change → EMA-smoothed, Z-scored

These are averaged into one composite Z-score to provide a consistent reading across assets and market conditions.

🔹 Fusion Trend Lines

Two lines serve as the core signal:

Fast Line (savg) – reacts quicker to trend changes

Slow Line (savg2) – acts as a baseline filter

Crossovers between these lines highlight momentum shifts, while their color reflects trend bias.

🔹 Overbought/Oversold Zones

Two upper and two lower Z-score thresholds define “zones”:

Upper zones highlight overheated momentum or potential bearish reversals

Lower zones highlight depressed momentum or potential bullish reversals

Filled regions and background colors help visually confirm extreme conditions.

🔹 Pivot-Based Divergence Engine

The script includes filtered pivot detection with customizable look-backs and range limits to ensure divergences are meaningful, not noise-driven.

🔶 SETTINGS

🔹 Indicator Settings

Source — Price series used for all calculations.

Z-Score Length — Lookback period for Z-score normalization.

Z-Score MA Length — Smoothing length for the fusion signal lines.

Overbought/Oversold Levels — Four customizable threshold lines.

Color Palette — Choose from preset themes or define custom colors.

🔹 RSI

Length — RSI calculation period.

EMA Smoothing Length — Smooths RSI before Z-score conversion.

🔹 MACD

Fast Length — Fast EMA length.

Slow Length — Slow EMA length.

Signal Line Length — MACD signal smoothing.

🔹 Stochastic

%K Length — Main stochastic length.

EMA Smoothing — Smooths %K for stability.

%D Length — Smoothing for the signal line.

🔹 Momentum

Length — Momentum lookback.

EMA Smoothing — Smooths momentum before Z-scoring.

🔹 Rate of Change

Length — ROC lookback.

EMA Smoothing — Smooths ROC values.

🔹 Divergence

Enable/Disable Divergence Detection — Toggle divergence engine.

Pivot Left/Right Lookback — Defines pivot detection sensitivity.

Detection Range Limits — Controls allowable range for divergence.

Bull/Bear Colors & Styling — Customize divergence visualization.

🔶 SUMMARY

The Z-Fusion Oscillator combines multiple momentum signatures into a single normalized signal, enabling traders to:

Identify reversals early

Detect momentum exhaustion

Spot bullish and bearish divergences

Track overbought/oversold conditions

Visualize trend strength with clarity

Whether you're a swing trader, intraday analyst, or trend-reversal hunter, the Z-Fusion Oscillator provides a powerful and adaptive way to read momentum.

Spot-Futures SpreadSpot-Futures Spread Indicator

A comprehensive indicator that automatically calculates and visualizes the percentage spread between spot and perpetual futures prices across multiple exchanges.

Key Features:

Automatic Exchange Detection - Automatically detects your current exchange and finds the corresponding spot/futures pair

Smart Fallback System - If the counterpart isn't available on your exchange, it automatically searches across 7+ major exchanges (Binance, Bybit, OKX, Gate.io, MEXC, KuCoin, HTX) and uses the first valid match

Multi-Exchange Support - Works with 14 exchanges including Binance, Bybit, OKX, MEXC, BitGet, Gate.io, KuCoin, and more

Clear Exchange Attribution - Shows exactly which exchanges are providing spot and futures data in the statistics table

Configurable Moving Average - Track the average spread with customizable period

Standard Deviation Bands - Identify unusual spread conditions with Bollinger-style bands

Built-in Alerts - Get notified when spread crosses bands or zero (parity)

Statistics Table - Real-time stats showing current spread, MA, std dev, and bands

Manual Override Options - Advanced users can manually specify exchanges and symbols

How It Works:

The indicator calculates the spread as: (Futures Price - Spot Price) / Spot Price × 100

Positive spread = Futures trading at a premium (contango)

Negative spread = Futures trading at a discount (backwardation)

Zero = Parity between spot and futures

Use Cases:

Funding Rate Analysis - Correlates with perpetual funding rates

Arbitrage Opportunities - Identify significant spot-futures divergences

Market Sentiment - Premium/discount indicates bullish/bearish positioning

Cross-Exchange Analysis - Compare spreads when spot and futures are on different exchanges

Smart Features:

Works whether you're viewing a spot or futures chart

Automatically handles exchange-specific perpetual contract naming (.P, PERP, SWAP, etc.)

Color-coded visualization (green for premium, red for discount)

Customizable colors and display options

Background shading based on spread direction

Perfect For:

Crypto traders monitoring funding rates, arbitrage traders, market makers, and anyone interested in spot-futures dynamics across multiple exchanges.

Getting Started:

Simply add the indicator to any spot or perpetual futures chart. It will automatically detect the exchange and find the corresponding pair. The statistics table shows which exchanges are being used for maximum transparency.

Note: The indicator automatically ignores invalid symbols, so you'll never see errors even if a specific pair doesn't exist on a particular exchange.

Kudos to @AlekMel that made the "Spot - Fut Spread v2" indicator that I enhance the Automatic detection feature which was not working in some case.

LibWghtLibrary "LibWght"

This is a library of mathematical and statistical functions

designed for quantitative analysis in Pine Script. Its core

principle is the integration of a custom weighting series

(e.g., volume) into a wide array of standard technical

analysis calculations.

Key Capabilities:

1. **Universal Weighting:** All exported functions accept a `weight`

parameter. This allows standard calculations (like moving

averages, RSI, and standard deviation) to be influenced by an

external data series, such as volume or tick count.

2. **Weighted Averages and Indicators:** Includes a comprehensive

collection of weighted functions:

- **Moving Averages:** `wSma`, `wEma`, `wWma`, `wRma` (Wilder's),

`wHma` (Hull), and `wLSma` (Least Squares / Linear Regression).

- **Oscillators & Ranges:** `wRsi`, `wAtr` (Average True Range),

`wTr` (True Range), and `wR` (High-Low Range).

3. **Volatility Decomposition:** Provides functions to decompose

total variance into distinct components for market analysis.

- **Two-Way Decomposition (`wTotVar`):** Separates variance into

**between-bar** (directional) and **within-bar** (noise)

components.

- **Three-Way Decomposition (`wLRTotVar`):** Decomposes variance

relative to a linear regression into **Trend** (explained by

the LR slope), **Residual** (mean-reversion around the

LR line), and **Within-Bar** (noise) components.

- **Local Volatility (`wLRLocTotStdDev`):** Measures the total

"noise" (within-bar + residual) around the trend line.

4. **Weighted Statistics and Regression:** Provides a robust

function for Weighted Linear Regression (`wLinReg`) and a

full suite of related statistical measures:

- **Between-Bar Stats:** `wBtwVar`, `wBtwStdDev`, `wBtwStdErr`.

- **Residual Stats:** `wResVar`, `wResStdDev`, `wResStdErr`.

5. **Fallback Mechanism:** All functions are designed for reliability.

If the total weight over the lookback period is zero (e.g., in

a no-volume period), the algorithms automatically fall back to

their unweighted, uniform-weight equivalents (e.g., `wSma`

becomes a standard `ta.sma`), preventing errors and ensuring

continuous calculation.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

wSma(source, weight, length)

Weighted Simple Moving Average (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

the arithmetic mean if Σweight = 0.

wEma(source, weight, length)

Weighted EMA (exponential kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Exponential-kernel weighted mean; falls

back to classic EMA if Σweight = 0.

wWma(source, weight, length)

Weighted WMA (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

classic WMA if Σweight = 0.

wRma(source, weight, length)

Weighted RMA (Wilder kernel, α = 1/len).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Wilder-kernel weighted mean; falls back to

classic RMA if Σweight = 0.

wHma(source, weight, length)

Weighted HMA (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

classic HMA if Σweight = 0.

wRsi(source, weight, length)

Weighted Relative Strength Index.

Parameters:

source (float) : series float Price series.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Weighted RSI; uniform if Σw = 0.

wAtr(tr, weight, length)

Weighted ATR (Average True Range).

Implemented as WRMA on *true range*.

Parameters:

tr (float) : series float True Range series.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Weighted ATR; uniform weights if Σw = 0.

wTr(tr, weight, length)

Weighted True Range over a window.

Parameters:

tr (float) : series float True Range series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Weighted mean of TR; uniform if Σw = 0.

wR(r, weight, length)

Weighted High-Low Range over a window.

Parameters:

r (float) : series float High-Low per bar.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Weighted mean of range; uniform if Σw = 0.

wBtwVar(source, weight, length, biased)

Weighted Between Variance (biased/unbiased).

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns:

variance series float The calculated between-bar variance (σ²btw), either biased or unbiased.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wBtwStdDev(source, weight, length, biased)

Weighted Between Standard Deviation.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σbtw uniform if Σw = 0.

wBtwStdErr(source, weight, length, biased)

Weighted Between Standard Error.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²btw / N_eff) uniform if Σw = 0.

wTotVar(mu, sigma, weight, length, biased)

Weighted Total Variance (= between-group + within-group).

Useful when each bar represents an aggregate with its own

mean* and pre-estimated σ (e.g., second-level ranges inside a

1-minute bar). Assumes the *weight* series applies to both the

group means and their σ estimates.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns:

varBtw series float The between-bar variance component (σ²btw).

varWtn series float The within-bar variance component (σ²wtn).

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wTotStdDev(mu, sigma, weight, length, biased)

Weighted Total Standard Deviation.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σtot.

wTotStdErr(mu, sigma, weight, length, biased)

Weighted Total Standard Error.

SE = √( total variance / N_eff ) with the same effective sample

size logic as `wster()`.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²tot / N_eff).

wLinReg(source, weight, length)

Weighted Linear Regression.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

Returns:

mid series float The estimated value of the regression line at the most recent bar.

slope series float The slope of the regression line.

intercept series float The intercept of the regression line.

wResVar(source, weight, midLine, slope, length, biased)

Weighted Residual Variance.

linear regression – optionally biased (population) or

unbiased (sample).

Parameters:

source (float) : series float Data series.

weight (float) : series float Weighting series (volume, etc.).

midLine (float) : series float Regression value at the last bar.

slope (float) : series float Slope per bar.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population variance (σ²_P), denominator ≈ N_eff.

false → sample variance (σ²_S), denominator ≈ N_eff - 2.

(Adjusts for 2 degrees of freedom lost to the regression).

Returns:

variance series float The calculated residual variance (σ²res), either biased or unbiased.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wResStdDev(source, weight, midLine, slope, length, biased)

Weighted Residual Standard Deviation.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

midLine (float) : series float Regression value at the last bar.

slope (float) : series float Slope per bar.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σres; uniform if Σw = 0.

wResStdErr(source, weight, midLine, slope, length, biased)

Weighted Residual Standard Error.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

midLine (float) : series float Regression value at the last bar.

slope (float) : series float Slope per bar.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²res / N_eff); uniform if Σw = 0.

wLRTotVar(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Total Variance **around the

window’s weighted mean μ**.

σ²_tot = E_w ⟶ *within-group variance*

+ Var_w ⟶ *residual variance*

+ Var_w ⟶ *trend variance*

where each bar i in the look-back window contributes

m_i = *mean* (e.g. 1-sec HL2)

σ_i = *sigma* (pre-estimated intrabar σ)

w_i = *weight* (volume, ticks, …)

ŷ_i = b₀ + b₁·x (value of the weighted LR line)

r_i = m_i − ŷ_i (orthogonal residual)

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns:

varRes series float The residual variance component (σ²res).

varWtn series float The within-bar variance component (σ²wtn).

varTrd series float The trend variance component (σ²trd), explained by the linear regression.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wLRTotStdDev(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Total Standard Deviation.

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √(σ²tot).

wLRTotStdErr(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Total Standard Error.

SE = √( σ²_tot / N_eff ) with N_eff = Σw² / Σw² (like in wster()).

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √((σ²res, σ²wtn, σ²trd) / N_eff).

wLRLocTotStdDev(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Local Total Standard Deviation.

Measures the total "noise" (within-bar + residual) around the trend.

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √(σ²wtn + σ²res).

wLRLocTotStdErr(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Local Total Standard Error.

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √((σ²wtn + σ²res) / N_eff).

wLSma(source, weight, length)

Weighted Least Square Moving Average.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

Returns: series float Least square weighted mean. Falls back

to unweighted regression if Σw = 0.

Z-Score Momentum | MisinkoMasterThe Z-Score Momentum is a new trend analysis indicator designed to catch reversals, and shifts in trends by comparing the "positive" and "negative" momentum by using the Z-Score.

This approach helps traders and investors get unique insight into the market of not just Crypto, but any market.

A deeper dive into the indicator

First, I want to cover the "Why?", as I believe it will ease of the part of the calculation to make it easier to understand, as by then you will understand how it fits the puzzle.

I had an attempt to create a momentum oscillator that would catch reversals and provide high tier accuracy while maintaining the main part => the speed.

I thought back to many concepts, divergences between averages?

- Did not work

Maybe a MACD rework?

- Did not work with what I tried :(

So I thought about statistics, Standard Deviation, Z-Score, Sharpe/Sortino/Omega ratio...

Wait, was that the Z-Score? I only tried the For Loop version of it :O

So on my way back from school I formulated a concept (originaly not like this but to that later) that would attempt to use the Z-Score as an accurate momentum oscillator.

Many ideas were falling out of the blue, but not many worked.

After almost giving up on this, and going to go back to developing my strategies, I tried one last thing:

What if we use divergences in the average, formulated like a Z-score?

Surprise-surprise, it worked!

Now to explain what I have been so passionately yapping about, and to connect the pieces of the puzzle once and for all:

The indicator compares the "strength" of the bullish/bearish factors (could be said differently, but this is my "speach bubble", and I think this describes it the best)

What could we use for the "bullish/bearish" factors?

How about high & low?

I mean, these are by definitions the highest and lowest points in price, which I decided to interpret as: The highest the bull & bear "factors" achieved that bar.

The problem here is comparison, I mean high will ALWAYS > low, unless the asset decided to unplug itself and stop moving, but otherwise that would be unfair.

Now if I use my Z-score, it will get higher while low is going up, which is the opposite of what I want, the bearish "factor" is weaker while we go up!

So I sat on my ret*rded a*s for 25 minutes, completly ignoring the fact the number "-1" exists.

Surprise surprise, multiplying the Z-Score of the low by -1 did what I wanted!

Now it reversed itself (magically). Now while the low keeps going down, the bear factor increases, and while it goes up the bear factor lowers.

This was btw still too noisy, so instead of the classic formula:

a = current value

b = average value

c = standard deviation of a

Z = (a-b)/c

I used:

a = average value over n/2 period

b = average value over n period

c = standard deviation of a

Z = (a-b)/c

And then compared the Z-Score of High to the Z-Score of Low by basic subtraction, which gives us final result and shows us the strength of trend, the direction of the trend, and possibly more, which I may have not found.

As always, this script is open source, so make sure to play around with it, you may uncover the treasure that I did not :)

Enjoy Gs!

First Passage Time - Distribution AnalysisThe First Passage Time (FPT) Distribution Analysis indicator is a sophisticated probabilistic tool that answers one of the most critical questions in trading: "How long will it take for price to reach my target, and what are the odds of getting there first?"

Unlike traditional technical indicators that focus on what might happen, this indicator tells you when it's likely to happen.

Mathematical Foundation: First Passage Time Theory

What is First Passage Time?

First Passage Time (FPT) is a concept in stochastic processes that measures the time it takes for a random process to reach a specific threshold for the first time. Originally developed in physics and mathematics, FPT has applications in:

Quantitative Finance: Option pricing, risk management, and algorithmic trading

Neuroscience: Modeling neural firing patterns

Biology: Population dynamics and disease spread

Engineering: Reliability analysis and failure prediction

The Mathematics Behind It

This indicator uses Geometric Brownian Motion (GBM), the same stochastic model used in the Black-Scholes option pricing formula:

dS = μS dt + σS dW

Where:

S = Asset price

μ = Drift (trend component)

σ = Volatility (uncertainty component)

dW = Wiener process (random walk)

Through Monte Carlo simulation, the indicator runs 1,000+ price path simulations to statistically determine:

When each threshold (+X% or -X%) is likely to be hit

Which threshold is hit first (directional bias)

How often each scenario occurs (probability distribution)

🎯 How This Indicator Works

Core Algorithm Workflow:

Calculate Historical Statistics

Measures recent price volatility (standard deviation of log returns)

Calculates drift (average directional movement)

Annualizes these metrics for meaningful comparison

Run Monte Carlo Simulations

Generates 1,000+ random price paths based on historical behavior

Tracks when each path hits the upside (+X%) or downside (-X%) threshold

Records which threshold was hit first in each simulation

Aggregate Statistical Results

Calculates percentile distributions (10th, 25th, 50th, 75th, 90th)

Computes "first hit" probabilities (upside vs downside)

Determines average and median time-to-target

Visual Representation

Displays thresholds as horizontal lines

Shows gradient risk zones (purple-to-blue)

Provides comprehensive statistics table

📈 Use Cases

1. Options Trading

Selling Options: Determine if your strike price is likely to be hit before expiration

Buying Options: Estimate probability of reaching profit targets within your time window

Time Decay Management: Compare expected time-to-target vs theta decay

Example: You're considering selling a 30-day call option 5% out of the money. The indicator shows there's a 72% chance price hits +5% within 12 days. This tells you the trade has high assignment risk.

2. Swing Trading

Entry Timing: Wait for higher probability setups when directional bias is strong

Target Setting: Use median time-to-target to set realistic profit expectations

Stop Loss Placement: Understand probability of hitting your stop before target

Example: The indicator shows 85% upside probability with median time of 3.2 days. You can confidently enter long positions with appropriate position sizing.

3. Risk Management

Position Sizing: Larger positions when probability heavily favors one direction

Portfolio Allocation: Reduce exposure when probabilities are near 50/50 (high uncertainty)

Hedge Timing: Know when to add protective positions based on downside probability

Example: Indicator shows 55% upside vs 45% downside—nearly neutral. This signals high uncertainty, suggesting reduced position size or wait for better setup.

4. Market Regime Detection

Trending Markets: High directional bias (70%+ one direction)

Range-bound Markets: Balanced probabilities (45-55% both directions)

Volatility Regimes: Compare actual vs theoretical minimum time

Example: Consistent 90%+ bullish bias across multiple timeframes confirms strong uptrend—stay long and avoid counter-trend trades.

First Hit Rate (Most Important!)

Shows which threshold is likely to be hit FIRST:

Upside %: Probability of hitting upside target before downside

Downside %: Probability of hitting downside target before upside

These always sum to 100%

⚠️ Warning: If you see "Low Hit Rate" warning, increase this parameter!

Advanced Parameters

Drift Mode

Allows you to explore different scenarios:

Historical: Uses actual recent trend (default—most realistic)

Zero (Neutral): Assumes no trend, only volatility (symmetric probabilities)

50% Reduced: Dampens trend effect (conservative scenario)

Use Case: Switch to "Zero (Neutral)" to see what happens in a pure volatility environment, useful for range-bound markets.

Distribution Type

Percentile: Shows 10%, 25%, 50%, 75%, 90% levels (recommended for most users)

Sigma: Shows standard deviation levels (1σ, 2σ)—useful for statistical analysis

⚠️ Important Limitations & Best Practices

Limitations

Assumes GBM: Real markets have fat tails, jumps, and regime changes not captured by GBM

Historical Parameters: Uses recent volatility/drift—may not predict regime shifts

No Fundamental Events: Cannot predict earnings, news, or macro shocks

Computational: Runs only on last bar—doesn't give historical signals

Remember: Probabilities are not certainties. Use this indicator as part of a comprehensive trading plan with proper risk management.

Created by: Henrique Centieiro. feedback is more than welcome!

Anchored Probability Cone by TenozenFirst of all, credit to @nasu_is_gaji for the open source code of Log-Normal Price Forecast! He teaches me alot on how to use polylines and inverse normal distribution from his indicator, so check it out!

What is this indicator all about?

This indicator draws a probability cone that visualizes possible future price ranges with varying levels of statistical confidence using Inverse Normal Distribution , anchored to the start of a selected timeframe (4h, W, M, etc.)

Feutures:

Anchored Cone: Forecasts begin at the first bar of each chosen higher timeframe, offering a consistent point for analysis.

Drift & Volatility-Based Forecast: Uses log returns to estimate market volatility (smoothed using VWMA) and incorporates a trend angle that users can set manually.

Probabilistic Price Bands: Displays price ranges with 5 customizable confidence levels (e.g., 30%, 68%, 87%, 99%, 99,9%).

Dynamic Updating: Recalculates and redraws the cone at the start of each new anchor period.

How to use:

Choose the Anchored Timeframe (PineScript only be able to forecast 500 bars in the future, so if it doesn't plot, try adjusting to a lower anchored period).

You can set the Model Length, 100 sample is the default. The higher the sample size, the higher the bias towards the overall volatility. So better set the sample size in a balanced manner.

If the market is inside the 30% conifidence zone (gray color), most likely the market is sideways. If it's outside the 30% confidence zone, that means it would tend to trend and reach the other probability levels.

Always follow the trend, don't ever try to trade mean reversions if you don't know what you're doing, as mean reversion trades are riskier.

That's all guys! I hope this indicator helps! If there's any suggestions, I'm open for it! Thanks and goodluck on your trading journey!

StatPivot- Dynamic Range Analyzer - indicator [PresentTrading]Hello everyone! In the following few open scripts, I would like to share various statistical tools that benefit trading. For this time, it is a powerful indicator called StatPivot- Dynamic Range Analyzer that brings a whole new dimension to your technical analysis toolkit.

This tool goes beyond traditional pivot point analysis by providing comprehensive statistical insights about price movements, helping you identify high-probability trading opportunities based on historical data patterns rather than subjective interpretations. Whether you're a day trader, swing trader, or position trader, StatPivot's real-time percentile rankings give you a statistical edge in understanding exactly where current price action stands within historical contexts.

Welcome to share your opinions! Looking forward to sharing the next tool soon!

█ Introduction and How it is Different

StatPivot is an advanced technical analysis tool that revolutionizes retracement analysis. Unlike traditional pivot indicators that only show static support/resistance levels, StatPivot delivers dynamic statistical insights based on historical pivot patterns.

Its key innovation is real-time percentile calculation - while conventional tools require new pivot formations before updating (often too late for trading decisions), StatPivot continuously analyzes where current price stands within historical retracement distributions.

Furthermore, StatPivot provides comprehensive statistical metrics including mean, median, standard deviation, and percentile distributions of price movements, giving traders a probabilistic edge by revealing which price levels represent statistically significant zones for potential reversals or continuations. By transforming raw price data into statistical insights, StatPivot helps traders move beyond subjective price analysis to evidence-based decision making.

█ Strategy, How it Works: Detailed Explanation

🔶 Pivot Point Detection and Analysis

The core of StatPivot's functionality begins with identifying significant pivot points in the price structure. Using the parameters left and right, the indicator locates pivot highs and lows by examining a specified number of bars to the left and right of each potential pivot point:

Copyp_low = ta.pivotlow(low, left, right)

p_high = ta.pivothigh(high, left, right)

For a point to qualify as a pivot low, it must have left higher lows to its left and right higher lows to its right. Similarly, a pivot high must have left lower highs to its left and right lower highs to its right. This approach ensures that only significant turning points are recognized.

🔶 Percentage Change Calculation

Once pivot points are identified, StatPivot calculates the percentage changes between consecutive pivot points:

For drops (when a pivot low is lower than the previous pivot low):

CopydropPercent = (previous_pivot_low - current_pivot_low) / previous_pivot_low * 100

For rises (when a pivot high is higher than the previous pivot high):

CopyrisePercent = (current_pivot_high - previous_pivot_high) / previous_pivot_high * 100

These calculations quantify the magnitude of each market swing, allowing for statistical analysis of historical price movements.

🔶 Statistical Distribution Analysis

StatPivot computes comprehensive statistics on the historical distribution of drops and rises:

Average (Mean): The arithmetic mean of all recorded percentage changes

CopyavgDrop = array.avg(dropValues)

Median: The middle value when all percentage changes are arranged in order

CopymedianDrop = array.median(dropValues)

Standard Deviation: Measures the dispersion of percentage changes from the average

CopystdDevDrop = array.stdev(dropValues)

Percentiles (25th, 75th): Values below which 25% and 75% of observations fall

Copyq1 = array.get(sorted, math.floor(cnt * 0.25))

q3 = array.get(sorted, math.floor(cnt * 0.75))

VaR95: The maximum expected percentage drop with 95% confidence

Copyvar95D = array.get(sortedD, math.floor(nD * 0.95))

Coefficient of Variation (CV): Measures relative variability

CopycvD = stdDevDrop / avgDrop

These statistics provide a comprehensive view of market behavior, enabling traders to understand the typical ranges and extreme moves.

🔶 Real-time Percentile Ranking

StatPivot's most innovative feature is its real-time percentile calculation. For each current price, it calculates:

The percentage drop from the latest pivot high:

CopycurrentDropPct = (latestPivotHigh - close) / latestPivotHigh * 100

The percentage rise from the latest pivot low:

CopycurrentRisePct = (close - latestPivotLow) / latestPivotLow * 100

The percentile ranks of these values within the historical distribution:

CopyrealtimeDropRank = (count of historical drops <= currentDropPct) / total drops * 100

This calculation reveals exactly where the current price movement stands in relation to all historical movements, providing crucial context for decision-making.

🔶 Cluster Analysis

To identify the most common retracement zones, StatPivot performs a cluster analysis by dividing the range of historical drops into five equal intervals:

CopyrangeSize = maxVal - minVal

For each interval boundary:

Copyboundaries = minVal + rangeSize * i / 5

By counting the number of observations in each interval, the indicator identifies the most frequently occurring retracement zones, which often serve as significant support or resistance areas.

🔶 Expected Price Targets

Using the statistical data, StatPivot calculates expected price targets:

CopytargetBuyPrice = close * (1 - avgDrop / 100)

targetSellPrice = close * (1 + avgRise / 100)

These targets represent statistically probable price levels for potential entries and exits based on the average historical behavior of the market.

█ Trade Direction

StatPivot functions as an analytical tool rather than a direct trading signal generator, providing statistical insights that can be applied to various trading strategies. However, the data it generates can be interpreted for different trade directions:

For Long Trades:

Entry considerations: Look for price drops that reach the 70-80th percentile range in the historical distribution, suggesting a statistically significant retracement

Target setting: Use the Expected Sell price or consider the average rise percentage as a reasonable target

Risk management: Set stop losses below recent pivot lows or at a distance related to the statistical volatility (standard deviation)

For Short Trades:

Entry considerations: Look for price rises that reach the 70-80th percentile range, indicating an unusual extension

Target setting: Use the Expected Buy price or average drop percentage as a target

Risk management: Set stop losses above recent pivot highs or based on statistical measures of volatility

For Range Trading:

Use the most common drop and rise clusters to identify probable reversal zones

Trade bounces between these statistically significant levels

For Trend Following:

Confirm trend strength by analyzing consecutive higher pivot lows (uptrend) or lower pivot highs (downtrend)

Use lower percentile retracements (20-30th percentile) as entry opportunities in established trends

█ Usage

StatPivot offers multiple ways to integrate its statistical insights into your trading workflow:

Statistical Table Analysis: Review the comprehensive statistics displayed in the data table to understand the market's behavior. Pay particular attention to:

Average drop and rise percentages to set reasonable expectations

Standard deviation to gauge volatility

VaR95 for risk assessment

Real-time Percentile Monitoring: Watch the real-time percentile display to see where the current price movement stands within the historical distribution. This can help identify:

Extreme movements (90th+ percentile) that might indicate reversal opportunities

Typical retracements (40-60th percentile) that might continue further

Shallow pullbacks (10-30th percentile) that might represent continuation opportunities in trends

Support and Resistance Identification: Utilize the plotted pivot points as key support and resistance levels, especially when they align with statistically significant percentile ranges.

Target Price Setting: Use the expected buy and sell prices calculated from historical averages as initial targets for your trades.

Risk Management: Apply the statistical measurements like standard deviation and VaR95 to set appropriate stop loss levels that account for the market's historical volatility.

Pattern Recognition: Over time, learn to recognize when certain percentile levels consistently lead to reversals or continuations in your specific market, and develop personalized strategies based on these observations.

█ Default Settings

The default settings of StatPivot have been carefully calibrated to provide reliable statistical analysis across a variety of markets and timeframes, but understanding their effects allows for optimal customization:

Left Bars (30) and Right Bars (30): These parameters determine how pivot points are identified. With both set to 30 by default:

A pivot low must be the lowest point among 30 bars to its left and 30 bars to its right

A pivot high must be the highest point among 30 bars to its left and 30 bars to its right

Effect on performance: Larger values create fewer but more significant pivot points, reducing noise but potentially missing important market structures. Smaller values generate more pivot points, capturing more nuanced movements but potentially including noise.

Table Position (Top Right): Determines where the statistical data table appears on the chart.

Effect on performance: No impact on analytical performance, purely a visual preference.

Show Distribution Histogram (False): Controls whether the distribution histogram of drop percentages is displayed.

Effect on performance: Enabling this provides visual insight into the distribution of retracements but can clutter the chart.

Show Real-time Percentile (True): Toggles the display of real-time percentile rankings.

Effect on performance: A critical setting that enables the dynamic analysis of current price movements. Disabling this removes one of the key advantages of the indicator.

Real-time Percentile Display Mode (Label): Chooses between label display or indicator line for percentile rankings.

Effect on performance: Labels provide precise information at the current price point, while indicator lines show the evolution of percentile rankings over time.

Advanced Considerations for Settings Optimization:

Timeframe Adjustment: Higher timeframes generally benefit from larger Left/Right values to identify truly significant pivots, while lower timeframes may require smaller values to capture shorter-term swings.

Volatility-Based Tuning: In highly volatile markets, consider increasing the Left/Right values to filter out noise. In less volatile conditions, lower values can help identify more potential entry and exit points.

Market-Specific Optimization: Different markets (forex, stocks, commodities) display different retracement patterns. Monitor the statistics table to see if your market typically shows larger or smaller retracements than the current settings are optimized for.

Trading Style Alignment: Adjust the settings to match your trading timeframe. Day traders might prefer settings that identify shorter-term pivots (smaller Left/Right values), while swing traders benefit from more significant pivots (larger Left/Right values).

By understanding how these settings affect the analysis and customizing them to your specific market and trading style, you can maximize the effectiveness of StatPivot as a powerful statistical tool for identifying high-probability trading opportunities.

DCA Simulation for CryptoCommunity v1.1Overview

This script provides a detailed simulation of a Dollar-Cost Averaging (DCA) strategy tailored for crypto traders. It allows users to visualize how their DCA strategy would perform historically under specific parameters. The script is designed to help traders understand the mechanics of DCA and how it influences average price movement, budget utilization, and trade outcomes.

Key Features:

Combines Interval and Safety Order DCA:

Interval DCA: Regular purchases based on predefined time intervals.

Safety Order DCA: Additional buys triggered by percentage price drops.

Interactive Visualization:

Displays buy levels, average price, and profit-taking points on the chart.

Allows traders to assess how their strategy adapts to price movements.

Comprehensive Dashboard:

Tracks money spent, contracts acquired, and budget utilization.

Shows maximum amounts used if profit-taking is active.

Dynamic Safety Orders:

Resets safety orders when a new higher high is established.

Customizable Parameters:

Adjustable buy frequency, safety order settings, and profit-taking levels.

Suitable for traders with varying budgets and risk tolerances.

Default Strategy Settings:

Account Size: Default account size is set to $10,000 to represent a realistic budget for the average trader.

Commission & Slippage: Includes realistic trading fees and slippage assumptions to ensure accurate backtesting results.

Risk Management: Defaults to risking no more than 5% of the account balance per trade.

Sample Size: Optimized to generate a minimum of 100 trades for meaningful statistical analysis. Users can adjust parameters to fit longer timeframes or different datasets.

Usage Instructions:

Configure Your Strategy: Set the base order, safety order size, and buy frequency based on your preferred DCA approach.

Analyze Historical Performance: Use the chart and dashboard to understand how the strategy performs under different market conditions.

Optimize Parameters: Adjust settings to align with your risk tolerance and trading objectives.

Important Notes:

This script is for educational and simulation purposes. It is not intended to provide financial advice or guarantee profitability.

If the strategy's default settings do not meet your needs, feel free to adjust them while keeping risk management in mind.

TradingView limits the number of open trades to 999, so reduce the buy frequency if necessary to fit longer timeframes.

MathHelpersLibrary "MathHelpers"

Overview

A collection of helper functions for designing indicators and strategies.

calculateATR(length, log)

Calculates the Average True Range (ATR) or Log ATR based on the 'log' parameter. Sans Wilder's Smoothing

Parameters:

length (simple int)

log (simple bool)

Returns: float The calculated ATR value. Returns Log ATR if `log` is true, otherwise returns standard ATR.

CDF(z)

Computes the Cumulative Distribution Function (CDF) for a given value 'z', mimicking the CDF function in "Statistically Sound Indicators" by Timothy Masters.

Parameters:

z (simple float)

Returns: float The CDF value corresponding to the input `z`, ranging between 0 and 1.

logReturns(lookback)

Calculates the logarithmic returns over a specified lookback period.

Parameters:

lookback (simple int)

Returns: float The calculated logarithmic return. Returns `na` if insufficient data is available.

Volume StatsDescription:

Volume Stats displays volume data and statistics for every day of the year, and is designed to work on "1D" timeframe. The data is displayed in a table with columns being months of the year, and rows being days of each month. By default, latest data is displayed, but you have an option to switch to data of the previous year as well.

The statistics displayed for each day is:

- volume

- % of total yearly volume

- % of total monthly volume

The statistics displayed for each column (month) is:

- monthly volume

- % of total yearly volume

- sentiment (was there more bullish or bearish volume?)

- min volume (on which day of the month was the min volume)

- max volume (on which day of the month was the max volume)

The cells change their colors depending on whether the volume is bullish or bearish, and what % of total volume the current cell has (either yearly or monthly). The header cells also change their color (based either on sentiment or what % of yearly volume the current month has).

This is the first (and free) version of the indicator, and I'm planning to create a "PRO" version of this indicator in future.

Parameters:

- Timezone

- Cell data -> which data to display in the cells (no data, volume or percentage)