Investments/swing trading strategy for different assetsStop worrying about catching the lowest price, it's almost impossible!: with this trend-following strategy and protection from bearish phases, you will know how to enter the market properly to obtain benefits in the long term.

Backtesting context: 1899-11-01 to 2023-02-16 of SPX by Tvc. Commissions: 0.05% for each entry, 0.05% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 5 indicators are used:

One Ema of 200 periods

Atr Stop loss indicator from Gatherio

Squeeze momentum indicator from LazyBear

Moving average convergence/divergence or Macd

Relative strength index or Rsi

Trade conditions:

There are three type of entries, one of them depends if we want to trade against a bearish trend or not.

---If we keep Against trend option deactivated, the rules for two type of entries are:---

First type of entry:

With the next rules, we will be able to entry in a pull back situation:

Squeeze momentum is under 0 line (red)

Close is above 200 Ema and close is higher than the past close

Histogram from macd is under 0 line and is higher than the past one

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

For closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Second type of entry:

With the next rules, we will not lose a possible bullish movement:

Close is above 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entry, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

---If we keep Against trend option activated, the rules are the same as the ones above, but with one more type of entry. This is more useful in weekly timeframes, but could also be used in daily time frame:---

Third type of entry:

Close is under 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entries, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Risk management

For calculating the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

If you activate break even using rsi, when rsi crosses under overbought zone break even will be activated. This can work in some assets.

---Important: In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Some assets and timeframes where the strategy has also worked:

BTCUSD : 4H, 1D, W

SPX (US500) : 4H, 1D, W

GOLD : 1D, W

SILVER : 1D, W

ETHUSD : 4H, 1D

DXY : 1D

AAPL : 4H, 1D, W

AMZN : 4H, 1D, W

META : 4H, 1D, W

(and others stocks)

BANKNIFTY : 4H, 1D, W

DAX : 1D, W

RUT : 1D, W

HSI : 1D, W

NI225 : 1D, W

USDCOP : 1D, W

Tìm kiếm tập lệnh với "momentum"

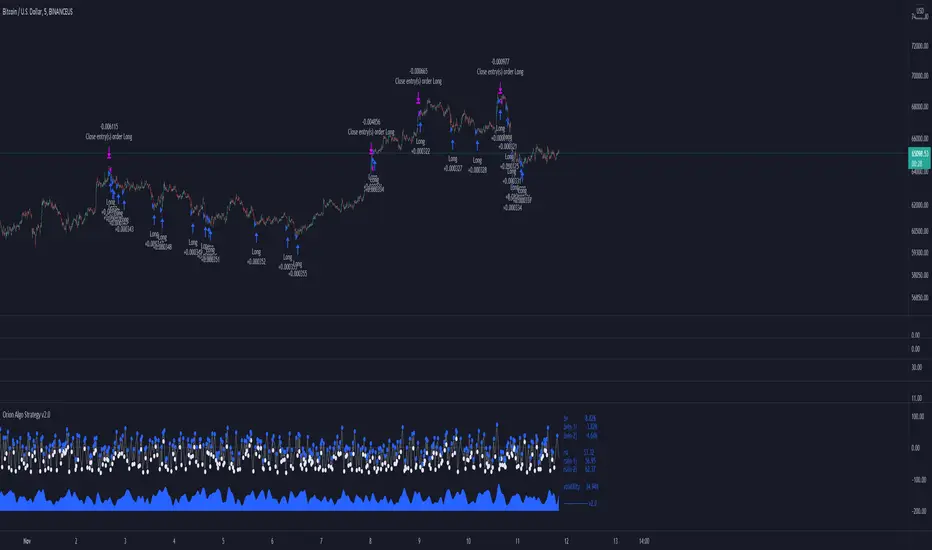

Orion Algo Strategy v2.0Hi everyone.

I decided to make the latest Orion Algo open to people. I don't have enough time to work on it lately, so I figured it would be best that everyone can have it to work on it. I took out some stuff from the original but it should give an idea on how things work. I made two strategies with this so far so you can use that to come up with your own. I recommend the DCA strategy because it gives you the most bang for Orion Algo's buck. It's pretty good at finding long entries.

Overall I hope you guys like this one. Also, Banano is the best crypto currency :)

-INFO-

Orion Algo is a trading algorithm designed to help traders find the highs and lows of the market before, during, and after they happen. We wanted to give an indicator to people that was simple to use. In fact we created the algorithm in such a way that it currently only needs a single input from the user. Since no indicator can predict the market perfectly, Orion should be used as just another tool (although quite a sharp one) for you to trade with. Fundamental knowledge of price action and TA should be used with Orion Algo.

Being an oscillator, Orion currently has a bias towards market volatility . So you will want to be trading markets over 30% volatility . We have plans to develop future versions that take this into account and adjust automatically for dead conditions. Also, while there are some similarities across all oscillators, what sets ours apart is the prediction curve. The prediction curve looks at the current signal values and gives it a relative score to approximate tops and bottoms 1-2 bars ahead of the signal curve. We also designed a velocity curve that attempts to predict the signal curve 2+ bars ahead. You can find the relative change in velocity in the Info panel. The bottom momentum wave is based on the signal curve and helps find overall market direction of higher time-frames while in a lower one.

Settings and How to Use them:

User Agreement – Orion Algo is a tool for you to use while trading. We aren’t responsible for losses OR the gains you make with it. By clicking the checkbox on the left you are agreeing to the terms.

Super Smooth – Smooths the main signal line based on the value inside the box. Lower values shift the pivot points to the left but also make things more noisy. Higher values move things to the right making it lag a bit more while creating a smoother signal. 8 is a good value to start with.

Theme – Changes the color scheme of Orion.

Dashboard – Turns on a dashboard with useful stats, such as Delta v, Volatility , Rsi , etc. Changing the value box will move the dashboard left and right.

Prediction – A secondary prediction model that attempts to predict a reversal before it happens (0-2bars). This can be noisy some times so make your best judgement. Curve will toggle a curve view of the prediction. Pivots will toggle bull/bear dots.

∆v – Delta v (change in velocity). This shows momentum of the signal. Crossing 0 signals a reversal. If you see the delta v changing direction, it may signify a reversal in the several bars depending on the overall momentum of the market.

Momentum Wave – Uses the signal as a macro trend indicator. Changes in direction of the wave can signify macro changes in the market. Average will toggle an averaging algorithm of the momentum waves and makes it easy to understand.

-STRATEGIES-

Simple - Just buy and sell on the dots

DCA - Uses the settings in the script for entries. If a buy dot appears then it will buy, if the price goes below the percentage it will wait for another dot before entering. This drastically improves DCA potential.

MACandles-LinearRegression-StrategyThis is combination of multiple indicators and strategies. Mainly useful for indexes and to time the entry and exits of indexes. No stoploss used - makes it less desirable for leveraged trades or trading individual stocks.

Let us rewind and look back at some of the indicators/strategies published earlier.

1. Moving Average Candles - this is one of my favourite tool for general trend filtering. Applying supertrend on moving average candles is one of the easiest ways to find reversal in trending market without exiting positions too early. Few scripts published on this basis are:

MA Candles Supertrend

MA Candles Supertrend Strategy

2. VixFix and Linear Regression - this itself is combination of two indicators.

Williams-Vix-Fix-Finds-Market-Bottoms - by @ChrisMoody

Squeeze-Momentum-Indicator - by @LazyBear

I have combined these two indicators to derive VIX-Fix linear regression to find absolute market bottoms. More description here:

VixFixLinReg-Strategy

VixFixLinReg-Indicator

Now, in this strategy, we combine all these together.

Derive moving average candles

Derive momentum of moving average candles

Derive Linear regression on momentum

Optionally, also calculate VIX Fix and Linear regression on VixFix momentum

To find market bottom:

There are two options

1. Use when momentum of MA candles hit bottom (red) and slowly turn up (orange). In aggressiveLong mode, signals are also generated when momentum starts going positive from negative.

2. Use Vix Fix linear regression of MA candles as described in the original script of VixFixLinReg-Strategy

To find market top

Here only Ma candles momentum decreasing is used as signal. If looking for longTrades , exit signal is generated only when momentum is turning negative extreme(orange). Or else, exit signal is generated when momentum has turned neutral.

At this stage, it is very much experimental - use it with caution :)

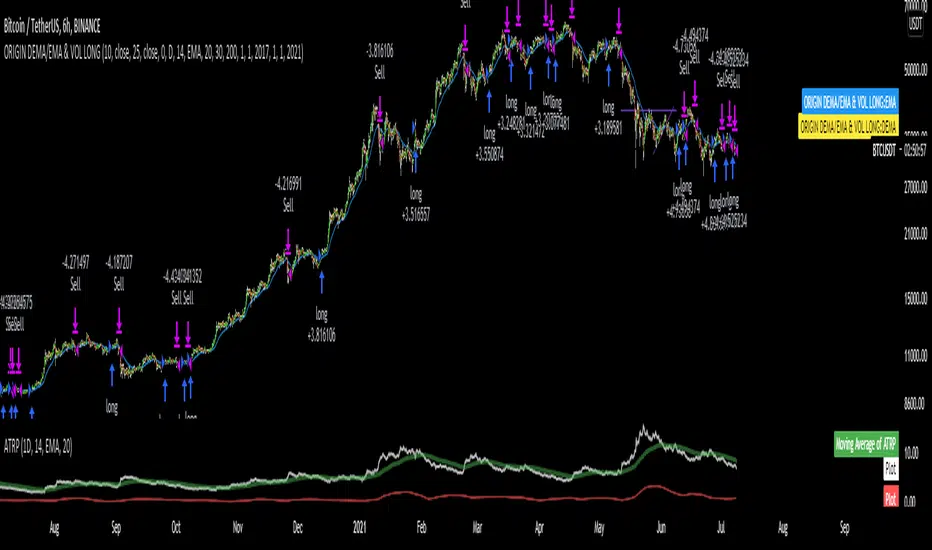

DEMA/EMA & VOLATILITY (VAMS)The biggest issue with momentum following strategies is over signaling during whipsaw periods. I created this strategy that measure momentum with DEMA (Fast Moving) and EMA (Slow moving). In order to mitigate over signaling during whipsaw periods I implemented the average true range percentage (ATRP) to measure realized volatility. If momentum is picking up while volatility is under a certain threshold it purchases the security. If momentum slows while volatility picks up it sells the security. Additionally, if momentum picks up, but volatility is high, it stays out of the security. This follows the theory that during sustained uptrends volatility will decrease, and during market corrections the volatility picks up. Following the old adage that markets climb up the stairs, and fall out the window. Note that this strategy does repaint due to it entering and closing positions at the close of the bars. I forgot to mention how volatility is measured high vs low. If the ATRP is above the EMA of the ATRP the strategy interprets the volatility is increasing and does not enter the security & Vice Versa for selling (with momentum signal of MAs)

This is just my first strategy, any feedback would be much appreciated.

S&P Bear Warning IndicatorTHIS SCRIPT HAS BEEN BUILT TO BE USED AS A S&P500 SPY CRASH INDICATOR ON A DAILY TIME FRAME (should not be used as a strategy).

THIS SCRIPT HAS BEEN BUILT AS A STRATEGY FOR VISUALIZATION PURPOSES ONLY AND HAS NOT BEEN OPTIMIZED FOR PROFIT.

The script has been built to show as a lower indicator and also gives visual SELL signal on top when conditions are met. BARE IN MIND NO STOP LOSS, NOR ADVANCED EXIT STRATEGY HAS BEEN BUILT.

As well as the chart SELL signal an alert option has also been built into this script.

The script utilizes a VIX indicator (maroon line) and 50 period Momentum (blue line) and Danger/No trade zone(pink shading).

When the Momentum line crosses down across the VIX this is a sell off but in order to only signal major sell offs the SELL signal only triggers if the momentum continues down through the danger zone.

A SELL signal could be given earlier by removing the need to wait for momentum to continue down through the Danger Zone however this is designed only to catch major market weakness not small sell offs.

As you can see from the picture between the big October 2018 and March 2020 market declines only 2 additional SELLS were triggered.

To use this indicator to identify ideal buying then you should only buy when Momentum line is crossed above the VIX and the Momentum line is above the Danger Zone (ideally 3 - 5 days above danger zone)

Combo Backtest 123 Reversal & Ergodic TSI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

r - Length of first EMA smoothing of 1 day momentum 4

s - Length of second EMA smoothing of 1 day smoothing 8

u- Length of third EMA smoothing of 1 day momentum 6

Length of EMA signal line 3

Source of Ergotic TSI Close

This is one of the techniques described by William Blau in his book "Momentum,

Direction and Divergence" (1995). If you like to learn more, we advise you to

read this book. His book focuses on three key aspects of trading: momentum,

direction and divergence. Blau, who was an electrical engineer before becoming

a trader, thoroughly examines the relationship between price and momentum in

step-by-step examples. From this grounding, he then looks at the deficiencies

in other oscillators and introduces some innovative techniques, including a

fresh twist on Stochastics. On directional issues, he analyzes the intricacies

of ADX and offers a unique approach to help define trending and non-trending periods.

WARNING:

- For purpose educate only

- This script to change bars colors.

Trading Public School ST1This is a derivative of Trading Public School "TTM Squeeze" volatility indicator, as discussed in his book "Mastering the Trade" (chapter 11).

Black crosses on the midline show that the market just entered a squeeze ( Bollinger Bands are with in Keltner Channel). This signifies low volatility , market preparing itself for an explosive move (up or down). Gray crosses signify "Squeeze release".

Mr.Carter suggests waiting till the first gray after a black cross, and taking a position in the direction of the momentum (for ex., if momentum value is above zero, go long). Exit the position when the momentum changes (increase or decrease --- signified by a color change). My (limited) experience with this shows, an additional indicator like ADX / WaveTrend, is needed to not miss good entry points. Also, Mr.Carter uses simple momentum indicator , while I have used a different method (linreg based) to plot the histogram. 100% Profit & loss 10% Only

Combo Backtest 123 Reversal & CMOfilt This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots a CMO which ignores price changes which are less

than a threshold value. CMO was developed by Tushar Chande. A scientist,

an inventor, and a respected trading system developer, Mr. Chande developed

the CMO to capture what he calls "pure momentum". For more definitive

information on the CMO and other indicators we recommend the book The New

Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to the

CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMOav This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots average of three different length CMO's. This indicator

was developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what he

calls "pure momentum". For more definitive information on the CMO and other

indicators we recommend the book The New Technical Trader by Tushar Chande

and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder?s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMOabsThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the absolute value of CMO. CMO was developed by Tushar

Chande. A scientist, an inventor, and a respected trading system developer,

Mr. Chande developed the CMO to capture what he calls "pure momentum". For

more definitive information on the CMO and other indicators we recommend the

book The New Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented indicators

such as Relative Strength Index, Stochastic, Rate-of-Change, etc. It is most closely

related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMO & WMA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chande Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

CMO & WMA Backtest ver 2.0 This indicator plots Chandre Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

CMOfilt BacktestThis indicator plots a CMO which ignores price changes which are less

than a threshold value. CMO was developed by Tushar Chande. A scientist,

an inventor, and a respected trading system developer, Mr. Chande developed

the CMO to capture what he calls "pure momentum". For more definitive

information on the CMO and other indicators we recommend the book The New

Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to the

CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

CMOabs Backtest This indicator plots the absolute value of CMO. CMO was developed by Tushar

Chande. A scientist, an inventor, and a respected trading system developer,

Mr. Chande developed the CMO to capture what he calls "pure momentum". For

more definitive information on the CMO and other indicators we recommend the

book The New Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented indicators

such as Relative Strength Index, Stochastic, Rate-of-Change, etc. It is most closely

related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

CMO & WMA Backtest This indicator plots Chande Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

Ergotic TSI Strategy Backtest r - Length of first EMA smoothing of 1 day momentum 4

s - Length of second EMA smoothing of 1 day smoothing 8

u- Length of third EMA smoothing of 1 day momentum 6

Length of EMA signal line 3

Source of Ergotic TSI Close

This is one of the techniques described by William Blau in his book "Momentum,

Direction and Divergence" (1995). If you like to learn more, we advise you to

read this book. His book focuses on three key aspects of trading: momentum,

direction and divergence. Blau, who was an electrical engineer before becoming

a trader, thoroughly examines the relationship between price and momentum in

step-by-step examples. From this grounding, he then looks at the deficiencies

in other oscillators and introduces some innovative techniques, including a

fresh twist on Stochastics. On directional issues, he analyzes the intricacies

of ADX and offers a unique approach to help define trending and non-trending periods.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Trend Pulse Channel StrategyOverview

Trend Pulse Channel Strategy is a long-only trend-following breakout strategy built around an adaptive multi-pole smoothing filter and a volatility-adjusted price channel.

The strategy is designed to participate in sustained directional moves by entering only when price confirms momentum strength beyond a dynamic upper boundary, while avoiding mean-reversion and low-quality consolidation phases.

This script is published as a strategy and includes realistic backtesting assumptions for position sizing, commissions, and slippage.

Core Concept

At the heart of the strategy is a multi-pole adaptive EMA-based filter, inspired by advanced digital signal smoothing techniques.

Using multiple poles allows the filter to reduce noise while preserving responsiveness to genuine trend changes.

To adapt the channel width to changing market conditions, the strategy applies the same filtering logic to True Range, producing a volatility-aware envelope rather than a static or fixed-percentage band.

This combination allows the strategy to:

Track directional bias using a smoothed central filter

Adjust channel width dynamically based on market volatility

Trigger entries only when price expansion confirms trend strength

Entry Logic

A long position is opened when:

Price crosses above the upper channel band

The signal occurs within the user-defined date range

This condition represents a volatility-confirmed breakout aligned with the prevailing directional filter.

Exit Logic

The long position is closed when:

Price crosses back below the upper band

This exit logic aims to stay in trending moves while exiting when upside momentum weakens.

The strategy does not open short positions by design.

Inputs and Defaults

The default inputs are selected to balance smoothness, responsiveness, and stability:

Source (HLC3): Reduces single-price noise by averaging high, low, and close

Period (144): Defines the primary smoothing horizon of the adaptive filter

Poles (4): Controls the smoothness vs. responsiveness trade-off

Range Multiplier (1.414): Scales the volatility envelope using filtered True Range

Reduced Lag (optional): Applies lag compensation to improve responsiveness

Fast Response (optional): Blends multi-pole and single-pole filters for quicker reaction at the cost of smoothness

All inputs are fully configurable and can be adjusted to suit different instruments and timeframes.

Risk Management & Position Sizing

The strategy uses:

Position size: 10% of equity per trade

No pyramiding

Long positions only

This sizing approach is intended to reflect sustainable risk exposure rather than aggressive capital deployment. Users may further adjust position size based on their own risk tolerance.

Backtesting Assumptions

The strategy is tested using :

Initial capital: 10,000

Commission: 0.1%

Slippage: 1 tick

Order fill model: Standard OHLC

These settings are chosen to provide more realistic performance estimates compared to idealized backtests.

This strategy is best suited for :

Trend-oriented markets

Higher timeframes where breakouts are more reliable

Users seeking systematic trend participation rather than frequent scalping

In sideways or range-bound market conditions, price may cross the channel boundaries frequently.

This can result in a higher number of entry and exit signals that do not develop into sustained trends.

For this reason, the strategy should be used with an understanding of basic technical analysis concepts, including market structure, trend identification, and consolidation behavior.

It is intended as a decision-support tool, not a standalone trading system.

Users—whether beginners or experienced traders—should avoid relying solely on this strategy and are encouraged to combine it with broader market context and additional analysis methods.

Disclaimer

This script is provided for educational and analytical purposes only. It does not constitute financial advice. Past performance does not guarantee future results.

9 EMA Trend-Flow StrategyThis strategy avoids trading inside the noise and waits for Bitcoin to "coil up" before exploding.

1. Chart Setup

Timeframe: 5 Minutes

Bollinger Bands: Length 20, Standard Deviation 2 (Default).

RSI (Relative Strength Index): Length 14.

EMA (Exponential Moving Average): Length 200 (Trend Filter).

2. The Rules

Long Setup (Buy)

The Trend Filter: Price must be above the 200 EMA.

The Squeeze: The Bollinger Bands must visually contract (narrow), indicating volatility is dying down.

The Trigger: A 5m candle closes strongly above the Upper Bollinger Band.

Confirmation: RSI must be rising and above 50 (but ideally not yet "pegged" at 90+).

Short Setup (Sell)

The Trend Filter: Price must be below the 200 EMA.

The Squeeze: The Bollinger Bands contract.

The Trigger: A 5m candle closes strongly below the Lower Bollinger Band.

Confirmation: RSI must be falling and below 50.

Execution Guide

Entry Technique

Don't enter immediately when the candle touches the band. Wait for the candle close.

Why? Bitcoin frequently "wicks" through bands to trap traders (fakeouts) before reversing. A solid close outside the band confirms momentum.

Exit Strategy (Take Profit)

Target 1 (Conservative): Close 50% of the position when price expands to a fixed risk-reward ratio (e.g., 1.5R).

Target 2 (Runner): Keep the remaining position open as long as price "walks the band" (stays outside or touching the outer band). Close the rest when a candle finally closes back inside the Bollinger Bands.

Stop Loss

Placement: Place your Stop Loss (SL) slightly below the Middle Band (the 20 SMA) at the time of entry.

Trailing: As the price moves in your favor, move your SL to trail the Middle Band.

Monthly DI+ & RSI StrategyOverview This strategy is designed to capture significant trend reversals and continuations on the Monthly timeframe. It combines the trend-following capability of the Directional Movement Index (DMI) with the fast momentum detection of RSI (Period 6).

Core Logic The strategy triggers a long position based on a dual-confirmation system. It looks for a specific "handshake" between Trend (DI) and Momentum (RSI).

Entry Conditions (OR Logic) A Buy signal is generated if EITHER of the following occurs:

Trend Trigger: DI+ crosses over DI- (while RSI is already bullish, trading above its SMA).

Momentum Trigger: RSI(6) crosses over RSI SMA(14) (while the trend is already bullish, with DI+ > DI-).

Exit Condition (Stop Loss)

Trend Reversal: The position is closed immediately if DI- crosses over DI+, indicating the bullish trend has been invalidated.

Default Settings

Timeframe: Optimized for 1M (Monthly) charts.

RSI: Length 6

RSI SMA: Length 14

DMI: Length 14 / Smoothing 14

Risk Warning This script is for educational purposes only. Past performance does not guarantee future results. Always backtest on your specific asset classes before trading.

Daily Open Shift The "Daily Open Shift" System (V2.0)

1. The Setup (Indicators & Timeframe)

• Timeframe: 15-Minute Chart (Execution).

• Key Levels: Daily Open (DO) or New York Open (NYO).

• Trend Indicators:

o 24 & 42 EMA Ribbon (Exponential Moving Averages).

o 30-Minute Supertrend.

________________________________________

2. Phase 1: Establish The Bias (The Filter)

This is the V2 upgrade. We do not trade against the day's opening momentum.

1. Mark the Open: Draw a horizontal line at the Daily Open (00:00) or Session Open.

2. The "First 2H" Rule: Observe the price action for the first 2 hours after the open.

o First 2H are Green/Bullish? → You are LONG BIAS only for the rest of the session. (Ignore all sell signals).

o First 2H are Red/Bearish? → You are SHORT BIAS only for the rest of the session. (Ignore all buy signals).

________________________________________

3. Phase 2: The Signal (The Switch)

Wait for the chart to confirm your bias technically.

1. The Switch: Price must cross and close a 15M candle on the correct side of the Daily Open.

o Longs: Price switches from below to above DO.

o Shorts: Price switches from above to below DO.

2. Indicator Confluence:

o EMAs: Must be crossed in your direction (Green for Long, Red for Short).

o 30M Supertrend: Must match your direction.

________________________________________

4. Phase 3: The Entry (The Trigger)

We never chase the breakdown. We wait for the price to come to us.

1. The Pullback: Wait for the price to retrace and touch/wick into the 24/42 EMA Ribbon.

2. The Confirmation: Watch the candle that touches the EMA.

o It must reject the EMA (wick off it) and close respecting the trend.

o Do not enter if the candle closes forcefully through the EMA, breaking structure.

3. Execution: Enter Market Order immediately on that candle close.

________________________________________

5. Phase 4: Risk Management (The Math)

This is the V2 upgrade. We aim for higher profitability.

1. Stop Loss (SL):

o Longs: Placed strictly below the lowest EMA band.

o Shorts: Placed strictly above the highest EMA band.

o Logic: If price crosses the EMA band completely, the trend is dead. Get out.

2. Take Profit (TP):

o FIXED 3R (Reward = 3x Risk).

o Example: If Risk is $100, TP is set to make $300.

o Rule: Do not move the TP. Do not close early. Let the math play out.

________________________________________

Summary Checklist (Print This)

Time: Is the First 2H bias clear? (Green=Buy / Red=Sell)

Switch: Did price close above/below the Daily Open?

Trend: Are EMAs crossed and Supertrend agreeing?

Patience: Did I wait for the price to pull back to the EMA band?

Trigger: Did the candle close respecting the EMA?

Execution: Market Entry + Stop Loss behind EMA + Fixed 3R Target.

Mindset: Am I at "2/10" emotion? Set the trade and walk away.

Optimized BTC Mean Reversion (RSI 20/65)📈 Optimized BTC Mean Reversion (RSI 20/65)

Optimized BTC Mean Reversion (RSI 20/65) is a rule-based trading strategy designed to capture mean-reversion moves in strong market structures, primarily optimized for Bitcoin, but adaptable to other liquid cryptocurrencies.

The strategy combines RSI extremes, Stochastic momentum, and EMA trend filtering to identify high-probability reversal zones while maintaining strict risk management.

🔍 Strategy Logic

This system focuses on entering trades when price temporarily deviates from equilibrium, while still respecting the broader trend.

✅ Long Conditions

RSI below 20 (oversold)

Stochastic below 25

Price trading above the 200 EMA (or within a controlled deviation)

Designed to buy sharp pullbacks in bullish conditions

❌ Short Conditions

RSI above 65 (overbought)

Stochastic above 75

Price trading below the 200 EMA

Designed to sell relief rallies in bearish conditions

🛡 Risk Management

Fixed Stop Loss: 4%

Fixed Take Profit: 6%

Risk/Reward: 1 : 1.5

No pyramiding (single position at a time)

Full equity position sizing (adjustable)

All exits are predefined at entry, ensuring consistency and emotional discipline.

📊 Indicators Used

200 EMA – Trend direction filter

RSI (14) – Mean-reversion trigger (20 / 65 levels)

Stochastic Oscillator – Momentum confirmation

👁 Visual Features

EMA plotted directly on chart

Real-time Stop Loss, Take Profit, and Entry Price lines

Clear long/short entry markers

Works on all timeframes (optimized for intraday and swing trading)

🔔 Alerts

Long entry alerts

Short entry alerts

(Perfect for automation or discretionary execution)

⚠️ Disclaimer

This strategy is intended for educational and research purposes only. Past performance does not guarantee future results. Always test on a demo account and adjust risk parameters to your own trading plan.

Sinals 15m - RSI 7 e 9This strategy is designed to capture continuation moves on the 15-minute chart by combining trend filters, momentum indicators, and strong-candle confirmation. The core idea is to enter trades shortly after EMA crossovers that signal direction, as long as momentum and candle strength support the move.

[SM-021] Gaussian Trend System [Optimized]This script is a comprehensive trend-following strategy centered around a Gaussian Channel. It is designed to capture significant market movements while filtering out noise during consolidation phases. This version (v2) introduces code optimizations using Pine Script v6 Arrays and a new Intraday Time Control feature.

1. Core Methodology & Math

The foundation of this strategy is the Gaussian Filter, originally conceptualized by @DonovanWall.

Gaussian Poles: Unlike standard moving averages (SMA/EMA), this filter uses "poles" (referencing signal processing logic) to reduce lag while maintaining smoothness.

Array Optimization: In this specific iteration, the f_pole function has been refactored to utilize Pine Script Arrays. This improves calculation efficiency and rendering speed compared to recursive variable calls, especially when calculating deep historical data.

Channel Logic: The strategy calculates a "Filtered True Range" to create High and Low bands around the main Gaussian line.

Long Entry: Price closes above the High Band.

Short Entry: Price closes below the Low Band.

2. Signal Filtering (Confluence)

To reduce false signals common in trend-following systems, the strategy employs a "confluence" approach using three additional layers:

Baseline Filter: A 200-period (customizable) EMA or SMA acts as a regime filter. Longs are only taken above the baseline; Shorts only below.

ADX Filter (Volatility): The Average Directional Index (ADX) is used to measure trend strength. If the ADX is below a user-defined threshold (default: 20), the market is considered "choppy," and new entries are blocked.

Momentum Check: A Stochastic RSI check ensures that momentum aligns with the breakout direction.

3. NEW: Intraday Session Filter

Per user requests, a time-based filter has been added to restrict trading activity to specific market sessions (e.g., the New York Open).

How it works: Users can toggle a checkbox to enable/disable the filter.

Configuration: You can define a specific time range (Default: 09:30 - 16:00) and a specific Timezone (Default: New York).

Logic: The strategy longCondition and shortCondition now check if the current bar's timestamp falls within this window. If outside the window, no new entries are generated, though existing trades are managed normally.

4. Risk Management

The strategy relies on volatility-based exits rather than fixed percentage stops:

ATR Stop Loss: A multiple of the Average True Range (ATR) is calculated at the moment of entry to set a dynamic Stop Loss.

ATR Take Profit: An optional Reward-to-Risk (RR) ratio can be set to place a Take Profit target relative to the Stop Loss distance.

Band Exit: If the trend reverses and price crosses the opposite band, the trade is closed immediately to prevent large drawdowns.

Credits & Attribution

Original Gaussian Logic: Developed by @DonovanWalll. This script utilizes his mathematical formula for the pole filters.

Strategy Wrapper & Array Refactor: Developed by @sebamarghella.

Community Request: The Intraday Session Filter was added to assist traders focusing on specific liquidity windows.

Disclaimer: This strategy is for educational purposes. Past performance is not indicative of future results. Please use the settings menu to adjust the Session Time and Risk parameters to fit your specific asset class.