Expected Move by Option's Implied Volatility Symbols: A - AZZ

This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols within the range of A - AZZ in alphabetical order.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options. There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

Tìm kiếm tập lệnh với "Volatility"

Ultimate Volatility Indicator [CC]The Ultimate Volatility Indicator was created by Richard Poster (Stocks and Commodities July 2021 pg 21) and this is a very simple but effective indicator. The idea behind volatility indicators is that when the indicator rises above a certain threshold then volatility is high enough and you can make a good amount of money riding the trend in the current direction and then exit when volatility drops below the threshold or until the underlying trend changes.

I have included a threshold that you can change from the default but I would recommend trying out different values to see what works best for you. This indicator will let you know as soon as volatility increases and reacts very quickly. I have included strong buy and sell signals in addition to normal ones so darker colors are strong buy and sell signals and lighter colors are normal signals. Buy when the line turns green and sell when it turns red.

Please let me know if you would like to see me publish any other indicators!

Adaptive Volatility Stop by Pedro Paulo de MeloStop ATR is a clean and reliable volatility-based trailing stop system, built to adapt dynamically to market conditions using the Average True Range (ATR).

It identifies trend direction, adjusts the stop level using stair-step logic, and automatically flips the stop when price reversals occur.

How it works

Uses ATR × Multiplier to calculate an adaptive volatility buffer

Tracks trend direction internally

Recomputes and repositions the stop when a trend flip is detected

Plots separate lines for bullish and bearish stop states

Works on any market and timeframe (crypto, forex, commodities, indices, stocks)

Why it’s useful

This Stop ATR implementation is extremely stable and visually clean.

It is particularly effective for:

Trend following

Position management

Swing and position trading

Systematic stop placement

Unlike many ATR-based stop versions, this script uses a corrected flip-handling method that prevents stop misalignment and ensures consistent trend state tracking.

Inputs

Period — ATR length

Multiplier — ATR factor that defines stop distance

Author

Developed by Pedro Paulo de Melo, open-source version.

OTT Volatility [RunRox]📊 OTT Volatility is an indicator developed by the RunRox team to pinpoint the most optimal time to trade across different markets.

OTT stands for Optimal Trade Time Volatility and is designed primarily for markets without a fixed trading session, such as cryptocurrencies that trade 24/7. At the same time, it works equally well on any other market.

🔶 The concept is straightforward. The indicator takes a specified number of historical periods (Samples) and statistically evaluates which hours of the day or which days show the highest volatility for the selected asset.

As a result, it highlights time windows with elevated volatility where traders can focus on searching for trade setups and building positions.

🔶 As the core volatility metric, the indicator uses ATR (Average True Range) to measure intraday volatility. Then it calculates the average ATR value over the last N Samples, creating a statistically stable estimate of typical volatility for the selected asset.

🔶 Statistically, during these highlighted periods the market shows higher-than-average volatility.

This means that in these time windows price is more likely to be subject to stronger moves and potential manipulation, making them attractive for active trade execution and position management.

⚠️ However, historical behavior does not guarantee future results.

These periods should be treated only as zones where volatility has a higher probability of being above normal, not as a promise of movement.

As shown in the screenshot above, the indicator also projects potential future volatility based on historical data. This helps you better plan your trading hours and align your activity with periods where volatility is statistically expected to be higher or lower.

🔶 Current Volatility – as shown in the screenshot above, you can also monitor the real-time volatility of the market without any statistical averaging.

On top of that, you can overlay the current volatility on top of the statistical volatility levels, which makes it easy to see whether the market is now trading in a high- or low-volatility regime relative to its usual behavior.

4 display modes – you can choose any visualization style that fits your trading workflow:

Absolute – displays the raw volatility values.

Relative – shows volatility relative to its typical levels.

Average Centered – centers volatility around its average value.

Trim Low Value – filters out low-volatility noise and highlights only more significant moves.

This indicator helps you define the most effective trading hours on any market by relying on historical volatility statistics.

Use it to quickly see when your market tends to be more active and to structure your trading sessions around those periods.

✅ We hope this tool becomes a useful part of your trading toolkit and helps you improve the quality of your decisions and timing.

Swing-Based Volatility IndexSwing-Based Volatility Index

This indicator helps traders quickly determine whether the market has moved enough over the past few hours to justify scalping.

It measures the percentage price swing (high to low) over a configurable time window (e.g., last 4–8 hours) and compares it to a minimum threshold (e.g., 1%).

✅ If the percent move exceeds the threshold → Market is volatile enough to scalp (green background).

🚫 If it's below the threshold → Market is too quiet (red background).

Features:

Adjustable lookback period in hours

Custom threshold for volatility sensitivity

Automatically adapts to the current chart timeframe

This tool is ideal for scalpers and short-term traders who want to avoid entering trades in low-volatility environments.

Adaptive Volatility-Controlled LSMA [QuantAlgo]Adaptive Volatility-Controlled LSMA by QuantAlgo 📈💫

Introducing the Adaptive Volatility-Controlled LSMA (Least Squares Moving Average) , a powerful trend-following indicator that combines trend detection with dynamic volatility adjustments. This indicator is designed to help traders and investors identify market trends while accounting for price volatility, making it suitable for a wide range of assets and timeframes. By integrating LSMA for trend analysis and Average True Range (ATR) for volatility control, this tool provides clearer signals during both trending and volatile market conditions.

💡 Core Concept and Innovation

The Adaptive Volatility-Controlled LSMA leverages the precision of the LSMA to track market trends and combines it with the sensitivity of the ATR to account for market volatility. LSMA fits a linear regression line to price data, providing a smoothed trend line that is less reactive to short-term noise. The ATR, on the other hand, dynamically adjusts the volatility bands around the LSMA, allowing the indicator to filter out false signals and respond to significant price moves. This combination provides traders with a reliable tool to identify trend shifts while managing risk in volatile markets.

📊 Technical Breakdown and Calculations

The indicator consists of the following components:

1. Least Squares Moving Average (LSMA): The LSMA calculates a linear regression line over a defined period to smooth out price fluctuations and reveal the underlying trend. It is more reactive to recent data than traditional moving averages, allowing for quicker trend detection.

2. ATR-Based Volatility Bands: The Average True Range (ATR) measures market volatility and creates upper and lower bands around the LSMA. These bands expand and contract based on market conditions, helping traders identify when price movements are significant enough to indicate a new trend.

3. Volatility Extensions: To further account for rapid market changes, the bands are extended using additional volatility measures. This ensures that trend signals are generated when price movements exceed both the standard volatility range and the extended volatility range.

⚙️ Step-by-Step Calculation:

1. LSMA Calculation: The LSMA is computed using a least squares regression method over a user-defined length. This provides a trend line that adapts to recent price movements while smoothing out noise.

2. ATR and Volatility Bands: ATR is calculated over a user-defined length and is multiplied by a factor to create upper and lower bands around the LSMA. These bands help detect when price movements are substantial enough to signal a new trend.

3. Trend Detection: The price’s relationship to the LSMA and the volatility bands is used to determine trend direction. If the price crosses above the upper volatility band, a bullish trend is detected. Conversely, a cross below the lower band indicates a bearish trend.

✅ Customizable Inputs and Features:

The Adaptive Volatility-Controlled LSMA offers a variety of customizable options to suit different trading or investing styles:

📈 Trend Settings:

1. LSMA Length: Adjust the length of the LSMA to control its sensitivity to price changes. A shorter length reacts quickly to new data, while a longer length smooths the trend line.

2. Price Source: Choose the type of price (e.g., close, high, low) that the LSMA uses to calculate trends, allowing for different interpretations of price data.

🌊 Volatility Controls:

ATR Length and Multiplier: Adjust the length and sensitivity of the ATR to control how volatility is measured. A higher ATR multiplier widens the bands, making the trend detection less sensitive, while a lower multiplier tightens the bands, increasing sensitivity.

🎨 Visualization and Alerts:

1. Bar Coloring: Customize bar colors to visually distinguish between uptrends and downtrends.

2. Volatility Bands: Enable or disable the display of volatility bands on the chart. The bands provide visual cues about trend strength and volatility thresholds.

3. Alerts: Set alerts for when the price crosses the upper or lower volatility bands, signaling potential trend changes.

📈 Practical Applications

The Adaptive Volatility-Controlled LSMA is ideal for traders and investors looking to follow trends while accounting for market volatility. Its key use cases include:

Identifying Trend Reversals: The indicator detects when price movements break through volatility bands, signaling potential trend reversals.

Filtering Market Noise: By applying ATR-based volatility filtering, the indicator helps reduce false signals caused by short-term price fluctuations.

Managing Risk: The volatility bands adjust dynamically to account for market conditions, helping traders manage risk and improve the accuracy of their trend-following strategies.

⭐️ Summary

The Adaptive Volatility-Controlled LSMA by QuantAlgo offers a robust and flexible approach to trend detection and volatility management. Its combination of LSMA and ATR creates clearer, more reliable signals, making it a valuable tool for navigating trending and volatile markets. Whether you're detecting trend shifts or filtering market noise, this indicator provides the tools you need to enhance your trading and investing strategy.

Note: The Adaptive Volatility-Controlled LSMA is a tool to enhance market analysis. It should be used in conjunction with other analytical tools and should not be relied upon as the sole basis for trading or investment decisions. No signals or indicators constitute financial advice, and past performance is not indicative of future results.

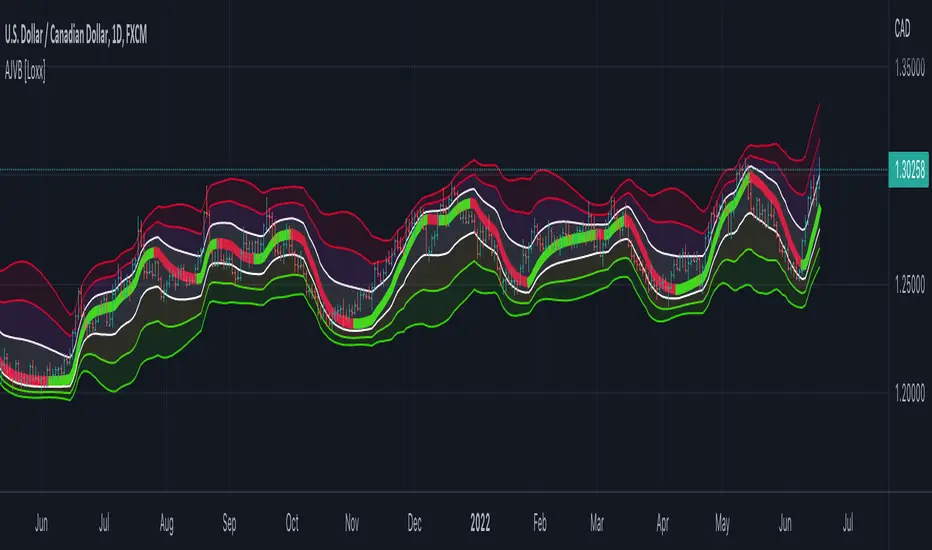

Adaptive Jurik Filter Volatility Bands [Loxx]Adaptive Jurik Filter Volatility Bands uses Jurik Volty and Adaptive, Double Jurik Filter Moving Average (AJFMA) to derive Jurik Filter smoothed volatility channels around an Adaptive Jurik Filter Moving Average. Bands are placed at 1, 2, and 3 deviations from the core basline.

What is Jurik Volty?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

That's why investors, banks and institutions worldwide ask for the Jurik Research Moving Average ( JMA ). You may apply it just as you would any other popular moving average. However, JMA's improved timing and smoothness will astound you.

What is adaptive Jurik volatility?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman’s adaptive moving average ( KAMA ) and Tushar Chande’s variable index dynamic average ( VIDYA ) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index ( RSI ), commodity channel index ( CCI ), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

Included

- UI options to shut off colors and bands

Boom Hunter + Hull Suite + Volatility Oscillator StrategyTRADE CONDITIONS

Long entry:

Boom Hunter (leading indicator): Trigger line crosses over Quotient 2 line (white cross over red)

Hull Suite (trend confirmation): Price closed above hull suite line and hull suite is green (represented by horizontal line at -10 in strategy pane)

Volatility Oscillator (volatility confirmation): Volatility spike trigger line is above upper band (represented by horizontal line at -30 in strategy pane)

Short entry:

Boom Hunter (leading indicator): Trigger line crosses under Quotient 2 line (white cross under red)

Hull Suite (trend confirmation): Price closed below hull suite line and hull suite is red (represented by horizontal line at -10 in strategy pane)

Volatility Oscillator (volatility confirmation): Volatility spike trigger line is below lower band (represented by horizontal line at -30 in strategy pane)

Risk management:

Each trade risks 3% of account (configurable in settings)

SL size determined by swing low/high of previous X candles (configurable in settings) or 1 ATR if swing is less than 1 ATR

TP is calculated by Risk:Reward ratio (configurable in settings)

TIPS

Timeframe: I have found good results running on BTC/USDT 5M chart

Note: To help visual identification of trade entries and exits you may wish to add the Hull Suite and Volatility Oscillator to the chart separately. It was not possible to display them in a clear way within a single panel for the strategy. Make sure you set the settings of the auxiliary indicators to match what is in the settings of this indicator if you do decide to add them.

CREDITS

Boom Hunter Pro by veryfid

Hull Suite by InSilico

Volatility Oscillator by veryfid

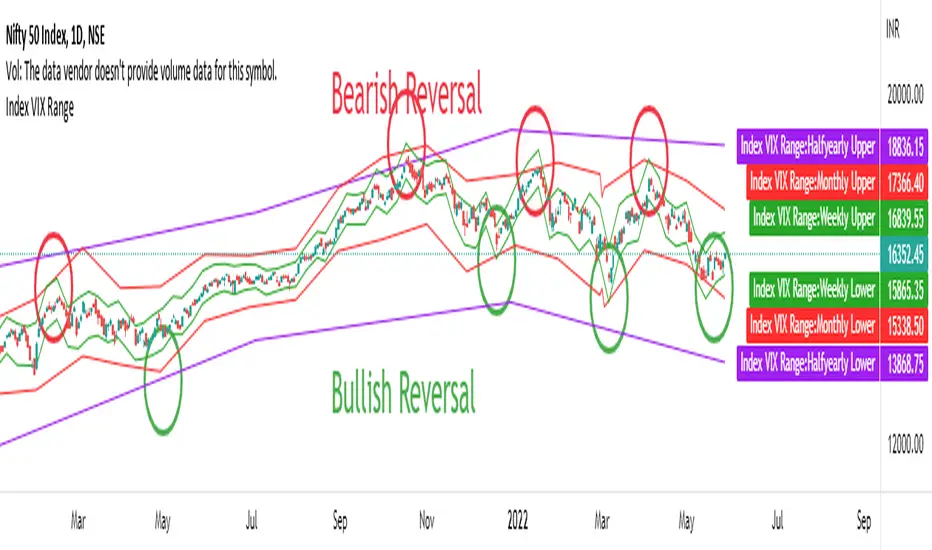

Index Reversal Range with Volatility Index or VIXWhat is the Indicator?

• The indicator is a visualization of maximum price in which the respective index can go up to in comparison with it's Volatility Index or VIX.

Who to use?

• Intraday

• Swing

• Position

• Long term Investors

• Futures

• Options

• Portfolio Managers

• Mutual Fund Managers

• Index Traders

• Volatility based Traders

• Long term Investors and Options Traders gets the maximum benefit

What timeframe to use?

• 1 Year: Position & Investors

• 6 Months: Position & Investors

• 3 Months: Swing & Position

• 1 Month: Swing & Position

• 1 Week: Swing

• 1 Day: Swing

• 1 Hour: Intraday & Swing

What are Upper and Lower lines?

• Upper Line: If the index price reach closer to the Upper line there is a high chance of reversal to Bearish trend.

• Lower Line: If the index price reach closer to the Lower line there is a high chance of reversal to Bullish trend.

• This need to be confirmed with multiple levels like Daily, Weekly, Monthly etc.

How to use?

• If the price reach closer to that level there is a high chance of reversal from the current trend.

• To identify the reversal zone of the index.

• To identify the trend.

• Option Traders can Sell a Call or Put Option from that level.

• Long term Investors, Position or Swing traders can plan for a Long entry.

• Intraday traders can use lower timeframes to do the same.

Indicator Menu

• Input VIX: Identify the VIX Symbol of your Index and type it in the box.

• For example for NIFTY Index chart type INDIAVIX in the box.

• Choose multiple timeframes according to your convenience.

How to turn on indicator Name and Value labels?

• Right side of the screen >

• Right click on the Price scale >

• Labels > Indicators and financial name labels, Indicators and financial value labels

Further Reading:

• Various videos and reading materials are available about this method.

TASC 2022.03 Relative Strength Volatility-Adjusted EMA█ OVERVIEW

TASC's March 2022 edition of Traders' Tips includes the "Relative Strength Moving Averages - Part 3: The Relative Strength Volatility-Adjusted Exponential Moving Average" article authored by Vitali Apirine. This is the code that implements the "RS VolatAdj EMA" from the article.

█ CONCEPTS

In a three-part article series, Vitaly Apirine examines ways to filter price movements and define turning points by applying the Relative Strength concept to exponential moving averages . The resulting indicator is more responsive and is intended to account for the relative strength of volatility .

█ CALCULATIONS

The calculation process uses the following steps:

Select an appropriate volatility index (in our case it is VIX ).

Calculate up day volatility (UV) smoothed by a 10-day EMA.

Calculate down day volatility (DV) smoothed by a 10-day EMA.

Take the absolute value of the difference between UV and DV and divide by the sum of UV and DV. This is the Volatility Strength we need.

Calculate a MLTP constant - the weighting multiplier for an exponential moving average.

Combine Volatility Strength and MLTP to create an exponential moving average on current price data.

Join TradingView!

GCM Volatility-Adaptive Trend ChannelScript Description

Name: GCM Volatility-Adaptive Trend Channel (GCM VATC)

Overview

The GCM Volatility-Adaptive Trend Channel (VATC) is a comprehensive trading tool that merges the low-lag, smooth-trending capabilities of the Jurik Moving Average (JMA) with the classic volatility analysis of Bollinger Bands (BB).

By displaying both trend and volatility in a single, intuitive interface, this indicator aims to help traders see when a trend is stable versus when it's becoming volatile and might be poised for a change.

Core Components:

JMA Trend System: At its core are three dynamically colored JMA lines (Baseline, Fast, and Slow) that provide a clear view of trend direction. The lines change color based on their slope, offering immediate visual feedback on momentum. A colored ribbon between the Baseline and Fast JMA visualizes shorter-term momentum shifts.

Standard Bollinger Bands: Layered on top are standard Bollinger Bands. Calculated from the price, these bands serve as a classic measure of market volatility. They help identify periods where the market is expanding (high volatility) or contracting (low volatility).

How to Use It

By combining these two powerful concepts, this indicator provides a unified view of both trend and volatility. It can help traders to:

Identify the primary trend direction using the smooth JMA lines.

Gauge the strength and stability of that trend.

See when the market is becoming volatile (bands widening) or consolidating (bands contracting), which can often precede a significant price move or a change in trend.

A Note on Originality & House Rules Compliance

This indicator does not introduce a new mathematical formula. Instead, its strength lies in the thoughtful combination of two well-respected, publicly available concepts: the Jurik Moving Average and Bollinger Bands. The JMA implementation is a standard public version. The goal was to create a practical, all-in-one tool for trend and volatility analysis.

This script is published as fully open-source in compliance with TradingView's House Rules. It utilizes standard, publicly available algorithms and does not contain any protected or hidden code.

Settings

All lengths, sources, and colors for the JMA lines and Bollinger Bands are fully customizable in the settings menu, allowing you to tailor the indicator to your specific trading style and asset.

I hope with this indicator Traders even Beginner can can control their emotions which increase the probabilities of the winning rates and cutting the losing strength

Purposely I Didn't plant the High low or Buy Sell signals in the chart. Because everything is in the chart where volatility Signal with the Bollinger Band and Buy Sell Signal in the JMA Dynamic colors. and that's enough to decide when to take trade and when not to.

Thank You and Happy Trading

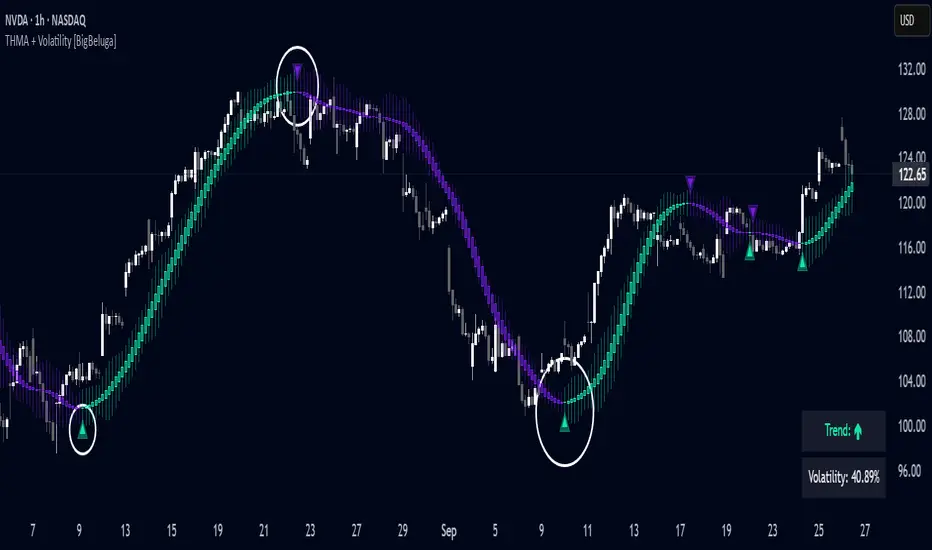

Triangular Hull Moving Average + Volatility [BigBeluga]This indicator combines the Triangular Hull Moving Average (THMA) with a volatility overlay to provide a smoother trend-following tool while dynamically visualizing market volatility.

🔵 Key Features:

THMA-Based Trend Detection: The indicator applies a Triangular Hull Moving Average (THMA) to smooth price data, reducing lag while maintaining responsiveness to trend changes.

// THMA

thma(_src, _length) =>

ta.wma(ta.wma(_src,_length / 3) * 3 - ta.wma(_src, _length / 2) - ta.wma(_src, _length), _length)

Dynamic Volatility Bands: When enabled, the indicator displays wicks extending from the THMA-based candles. These bands expand and contract based on price volatility.

Trend Reversal Signals The indicator marks trend shifts using triangle-shaped signals:

- Upward triangles appear when the THMA trend shifts to bullish.

- Downward triangles appear when the THMA trend shifts to bearish.

Customizable Settings: Users can adjust the THMA length, volatility calculation period, and colors for up/down trends to fit their trading style.

Informative Dashboard: The bottom-right corner displays the current trend direction and volatility percentage, helping traders quickly assess market conditions.

🔵 Usage:

Trend Trading: The colored candles indicate whether the market is trending up or down. Traders can follow the trend direction and use trend reversals for entry or exit points.

Volatility Monitoring: When the volatility feature is enabled, the expanding or contracting wicks help visualize market momentum and potential breakout strength.

Signal Confirmation: The triangle signals can be used to confirm potential entry points when the trend shifts.

This tool is ideal for traders who want a responsive moving average with volatility insights to enhance their trend-following strategies.

Asymmetric volatilityThe "Asymmetric Volatility" indicator is designed to visualize the differences in volatility between upward and downward price movements of a selected instrument. It operates on the principle of analyzing price movements over a specified time period, with particular focus on the symmetrical evaluation of both price rises and falls.

User Parameters:

- Length: This parameter specifies the number of bars (candles) used to calculate the average volatility. The larger the value, the longer the time period, and the smoother the volatility data will be.

- Source: This represents the input data for the indicator calculations. By default, the close value of each bar is used, but the user can choose another data source (such as open, high, low, or any custom value).

Operational Algorithm:

1. Movement Calculation:

- UpMoves: Computed as the positive difference between the current bar value and the previous bar value, if it is greater than zero.

- DownMoves: Computed as the positive difference between the previous bar value and the current bar value, if it is greater than zero.

2. Volatility Calculation:

- UpVolatility: This is the arithmetic mean of the UpMoves values over the specified period.

- DownVolatility: This is the arithmetic mean of the DownMoves values over the specified period.

3. Graphical Representation:

- The indicator displays two plots: upward and downward volatility, represented by green and red lines, respectively.

- The background color changes based on which volatility is dominant: a green background indicates that upward volatility prevails, while a red background indicates downward volatility.

The indicator allows traders to quickly assess in which direction the market is more volatile at the moment, which can be useful for making trading decisions and evaluating the current market situation.

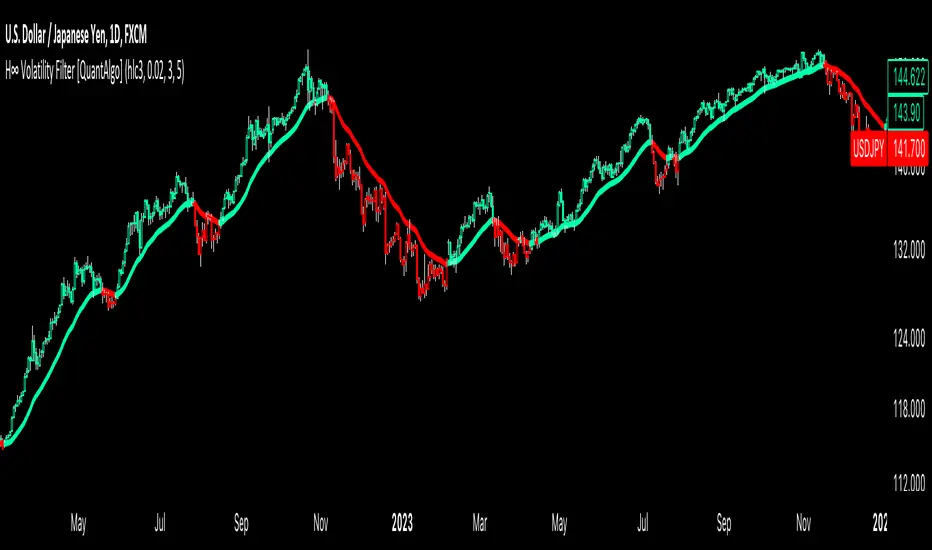

H-Infinity Volatility Filter [QuantAlgo]Introducing the H-Infinity Volatility Filter by QuantAlgo 📈💫

Enhance your trading/investing strategy with the H-Infinity Volatility Filter , a powerful tool designed to filter out market noise and identify clear trend signals in volatile conditions. By applying an advanced H∞ filtering process, this indicator assists traders and investors in navigating uncertain market conditions with improved clarity and precision.

🌟 Key Features:

🛠 Customizable Noise Parameters: Adjust worst-case noise and disturbance settings to tailor the filter to various market conditions. This flexibility helps you adapt the indicator to handle different levels of market volatility and disruptions.

⚡️ Dynamic Trend Detection: The filter identifies uptrends and downtrends based on the filtered price data, allowing you to quickly spot potential shifts in the market direction.

🎨 Color-Coded Visuals: Easily differentiate between bullish and bearish trends with customizable color settings. The indicator colors the chart’s candles according to the detected trend for immediate clarity.

🔔 Custom Alerts: Set alerts for trend changes, so you’re instantly informed when the market transitions from bullish to bearish or vice versa. Stay updated without constantly monitoring the charts.

📈 How to Use:

✅ Add the Indicator: Add the H-Infinity Volatility Filter to your favourites and apply it to your chart. Customize the noise and disturbance parameters to match the volatility of the asset you are trading/investing. This allows you to optimize the filter for your specific strategy.

👀 Monitor Trend Shifts: Watch for clear visual signals as the filter detects uptrends or downtrends. The color-coded candles and line plots help you quickly assess market conditions and potential reversals.

🔔 Set Alerts: Configure alerts to notify you when the trend changes, allowing you to react quickly to potential market shifts without needing to manually track price movements.

🌟 How It Works and Academic Background:

The H-Infinity Volatility Filter is built on the foundations of H∞ (H-infinity) control theory , a mathematical framework originating from the field of engineering and control systems. Developed in the 1980s by notable engineers such as George Zames and John C. Doyle , this theory was designed to help systems perform optimally under uncertain and noisy conditions. H∞ control focuses on minimizing the worst-case effects of disturbances and noise, making it a powerful tool for managing uncertainty in complex environments.

In financial markets, where unpredictable price fluctuations and noise often obscure meaningful trends, this same concept can be applied to price data to filter out short-term volatility. The H-Infinity Volatility Filter adopts this approach, allowing traders and investors to better identify potential trends by reducing the impact of random price movements. Instead of focusing on precise market predictions, the filter increases the probability of highlighting significant trends by smoothing out market noise.

This indicator works by processing historical price data through an H∞ filter that continuously adjusts based on worst-case noise levels and disturbances. By considering several past states, it estimates the current price trend while accounting for potential external disruptions that might influence price behavior. Parameters like "worst-case noise" and "disturbance" are user-configurable, allowing traders to adapt the filter to different market conditions. For example, in highly volatile markets, these parameters can be adjusted to manage larger price swings, while in more stable markets, they can be fine-tuned for smoother trend detection.

The H-Infinity Volatility Filter also incorporates a dynamic trend detection system that classifies price movements as bullish or bearish. It uses color-coded candles and plots—green for bullish trends and red for bearish trends—to provide clear visual cues for market direction. This helps traders and investors quickly interpret the trend and act on potential signals. While the indicator doesn’t guarantee accuracy in trend prediction, it significantly reduces the likelihood of false signals by focusing on meaningful price changes rather than random fluctuations.

How It Can Be Applied to Trading/Investing:

By applying the principles of H∞ control theory to financial markets, the H-Infinity Volatility Filter provides traders and investors with a sophisticated tool that manages uncertainty more effectively. Its design makes it suitable for use in a wide range of markets—whether in fast-moving, volatile environments or calmer conditions.

The indicator is versatile and can be used in both short-term trading and medium to long-term investing strategies. Traders can tune the filter to align with their specific risk tolerance, asset class, and market conditions, making it an ideal tool for reducing the effects of market noise while increasing the probability of detecting reliable trend signals.

For investors, the filter can help in identifying medium to long-term trends by filtering out short-term price swings and focusing on the broader market direction. Whether applied to stocks, forex, commodities, or cryptocurrencies, the H-Infinity Volatility Filter helps traders and investors interpret market behavior with more confidence by offering a more refined view of price movements through its noise reduction techniques.

Disclaimer:

The H-Infinity Volatility Filter is designed to assist in market analysis by filtering out noise and volatility. It should not be used as the sole tool for making trading or investment decisions. Always incorporate other forms of analysis and risk management strategies. No statements or signals from this indicator or us should be considered financial advice. Past performance is not indicative of future results.

Advanced Volatility-Adjusted Momentum IndexAdvanced Volatility-Adjusted Momentum Index (AVAMI)

The AVAMI is a powerful and versatile trading index which enhances the traditional momentum readings by introducing a volatility adjustment. This results in a more nuanced interpretation of market momentum, considering not only the rate of price changes but also the inherent volatility of the asset.

Settings and Parameters:

Momentum Length: This parameter sets the number of periods used to calculate the momentum, which is essentially the rate of change of the asset's price. A shorter length value means the momentum calculation will be more sensitive to recent price changes. Conversely, a longer length will yield a smoother and more stabilized momentum value, thereby reducing the impact of short-term price fluctuations.

Volatility Length: This parameter is responsible for determining the number of periods to be considered in the calculation of standard deviation of returns, which acts as the volatility measure. A shorter length will result in a more reactive volatility measure, while a longer length will produce a more stable, but less sensitive measure of volatility.

Smoothing Length: This parameter sets the number of periods used to apply a moving average smoothing to the AVAMI and its signal line. The purpose of this is to minimize the impact of volatile periods and to make the indicator's lines smoother and easier to interpret.

Lookback Period for Scaling: This is the number of periods used when rescaling the AVAMI values. The rescaling process is necessary to ensure that the AVAMI values remain within a consistent and interpretable range over time.

Overbought and Oversold Levels: These levels are thresholds at which the asset is considered overbought (potentially overvalued) or oversold (potentially undervalued), respectively. For instance, if the AVAMI exceeds the overbought level, traders may consider it as a possible selling opportunity, anticipating a price correction. Conversely, if the AVAMI falls below the oversold level, it could be seen as a buying opportunity, with the expectation of a price bounce.

Mid Level: This level represents the middle ground between the overbought and oversold levels. Crossing the mid-level line from below can be perceived as an increasing bullish momentum, and vice versa.

Show Divergences and Hidden Divergences: These checkboxes give traders the option to display regular and hidden divergences between the AVAMI and the asset's price. Divergences are crucial market structures that often signal potential price reversals.

Index Logic:

The AVAMI index begins with the calculation of a simple rate of change momentum indicator. This raw momentum is then adjusted by the standard deviation of log returns, which acts as a measure of market volatility. This adjustment process ensures that the resulting momentum index encapsulates not only the speed of price changes but also the market's volatility context.

The raw AVAMI is then smoothed using a moving average, and a signal line is generated as an exponential moving average (EMA) of this smoothed AVAMI. This signal line serves as a trigger for potential trading signals when crossed by the AVAMI.

The script also includes an algorithm to identify 'fractals', which are distinct price patterns that often act as potential market reversal points. These fractals are utilized to spot both regular and hidden divergences between the asset's price and the AVAMI.

Application and Strategy Concepts:

The AVAMI is a versatile tool that can be integrated into various trading strategies. Traders can utilize the overbought and oversold levels to identify potential reversal points. The AVAMI crossing the mid-level line can signify a change in market momentum. Additionally, the identification of regular and hidden divergences can serve as potential trading signals:

Regular Divergence: This happens when the asset's price records a new high/low, but the AVAMI fails to follow suit, suggesting a possible trend reversal. For instance, if the asset's price forms a higher high but the AVAMI forms a lower high, it's a regular bearish divergence, indicating potential price downturn.

Hidden Divergence: This is observed when the price forms a lower high/higher low, but the AVAMI forms a higher high/lower low, suggesting the continuation of the prevailing trend. For example, if the price forms a lower low during a downtrend, but the AVAMI forms a higher low, it's a hidden bullish divergence, signaling the potential continuation of the downtrend.

As with any trading tool, the AVAMI should not be used in isolation but in conjunction with other technical analysis tools and within the context of a well-defined trading plan.

Fibonacci Volatility BandsFibonacci Volatility Bands are just an alternative that allows for more margin than regular Bollinger Bands. They are created based on an average of moving averages that use the Fibonacci sequence as lookback periods.

The use of the Fibonacci Volatility Bands is exactly the same as the Bollinger Bands.

Wavetrend in Dynamic Zones with Kumo Implied VolatilityI was asked to do one of those, so here we go...

As always free and open source as it should be. Do not pay for such indicators!

A WaveTrend Indicator or also widely known as "Market Cipher" is an Indicator that is based on Moving Averages, therefore its an "lagging indicator". Lagging indicators are best used in combination with leading indicators. In this script the "leading indicator" component are Daily, Weekly or Monthly Pivots . These Pivots can be used as dynamic Support and Resistance , Stoploss, Take Profit etc.

This indicator combination is best used in larger timeframes. For lower timeframes you might need to change settings to your liking.

The general Wavetrend settings are the same that are used in Market Cipher, Market Liberator and such popular indicators.

What are these circles?

-These are the WaveTrend Divergences. Red for Regular-Bearish. Orange for Hidden-Bearish. Green for Regular-Bullish. Aqua for Hidden-Bullish.

What are these white, orange and aqua triangles?

-These are the WaveTrend Pivots. A Pivot counter was added. Every time a pivot is lower than the previous one, an orange triangle is printed, every time a pivot is higher than the previous one an aqua triangle is printed. That mimics a very common way Wavetrend is being used for trading when using those other paid Wavetrend indicators.

What are these Orange and Aqua Zones?

-These are Dynamic Zones based on the indicator itself, they offer more information than static zones. Of course static lines are also included and can be adjusted.

What are the lines between the waves?

-This is a Kumo Cloud Implied Volatility indicator. It is color coded and can be used to indicate if a major market move/bottom/top happened.

What are those numbers on the right?

-The first number is a Bollinger Band indicator that shows if said Bollinger Band is in a state of Oversold/Overbought, the second number is the actual Bollinger Band Width that indicates if the Bollinger Band squeezes, normally that happens right before the market makes an explosive move.

Please keep in mind that this indicator is a tool and not a strategy, do not blindly trade signals, do your own research first! Use this indicator in conjunction with other indicators to get multiple confirmations.

Higher Time Frame EMAs and 1% volatility indicatorSet the "higher time frame" (HTF) from which the EMAs will be calculated in all timeframes.

Example: I chose timeframe 1D and I will see the EMAs from TF 1D also in smaller TF as 1, 5, 30, 60 minutes.

There are 4 EMAs. The default values are 5, 10, 60 and 223 periods from "Scalping the Bull" indicator.

You can change the periods of each EMA.

The indicator have also a volatility indication, showing -1% and +1% price levels.

Multi-Symbol Volatility Tracker with Range DetectionMulti-Symbol Volatility Tracker with Range Detection

🎯 Main Purpose:

This indicator is specifically designed for scalpers to quickly identify symbols with high volatility that are currently in ranging conditions . It helps you spot the perfect opportunities for buying at lows and selling at highs repeatedly within the same trading session.

📊 Table Data Explanation:

The indicator displays a comprehensive table with 5 columns for 4 major symbols (GOLD, SILVER, NASDAQ, SP500):

SYMBOL: The trading instrument being analyzed

VOLATILITY: Color-coded volatility levels (NORMAL/HIGH/EXTREME) based on ATR values

Last Candle %: The percentage range of the most recent 5-minute candle

Last 5 Candle Avg %: Average percentage range over the last 5 candles

RANGE: Shows "YES" (blue) or "NO" (gray) indicating if the symbol is currently ranging

🔍 How to Identify Trading Opportunities:

Look for symbols that combine these characteristics:

RANGE column shows "YES" (highlighted in blue) - This means the symbol is moving sideways, perfect for range trading

VOLATILITY shows "HIGH" or "EXTREME" - Ensures there's enough movement for profitable scalping

Higher candlestick percentages - Indicates larger candle ranges, meaning more profit potential per trade

⚡ Optimal Usage:

Best Timeframe: Works optimally on 5-minute charts where the ranging patterns are most reliable for scalping

Trading Strategy: When you find a symbol with "YES" in the RANGE column, switch to that symbol and look for opportunities to buy near the lows and sell near the highs of the ranging pattern

Risk Management: Higher volatility symbols offer more profit potential but require tighter risk management

⚙️ Settings:

ATR Length: Adjusts the Average True Range calculation period (default: 14)

Range Sensitivity: Fine-tune range detection sensitivity (0.1-2.0, lower = more sensitive)

💡 Pro Tips:

The indicator updates in real-time, so monitor for symbols switching from "NO" to "YES" in the RANGE column

Combine HIGH/EXTREME volatility with RANGE: YES for the most profitable scalping setups

Use the candlestick percentages to gauge potential profit per trade - higher percentages mean more movement

The algorithm uses advanced statistical analysis including standard deviation, linear regression slopes, and range efficiency to accurately detect ranging conditions

Perfect for day traders and scalpers who want to quickly identify which symbols offer the best ranging opportunities for consistent buy-low, sell-high strategies.

Clustering Volatility (ATR-ADR-ChaikinVol) [Sam SDF-Solutions]The Clustering Volatility indicator is designed to evaluate market volatility by combining three widely used measures: Average True Range (ATR), Average Daily Range (ADR), and the Chaikin Oscillator.

Each indicator is normalized using one of the available methods (MinMax, Rank, or Z-score) to create a unified metric called the Score. This Score is further smoothed with an Exponential Moving Average (EMA) to reduce noise and provide a clearer view of market conditions.

Key Features:

Multi-Indicator Integration: Combines ATR, ADR, and the Chaikin Oscillator into a single Score that reflects overall market volatility.

Flexible Normalization: (Supports three normalization methods)

MinMax: Scales values between the observed minimum and maximum.

Rank: Normalizes based on the relative rank within a moving window.

Z-score: Standardizes values using mean and standard deviation.

Dynamic Window Selection: Offers an automatic window selection option based on a specified lookback period, or a fixed window size can be used.

Customizable Weights: Allows the user to assign individual weights to ATR, ADR, and the Chaikin Oscillator. Optionally, weights can be normalized to sum to 1.

Score Smoothing: Applies an EMA to the computed Score to smooth out short-term fluctuations and reduce market noise.

Cluster Visualization: Divides the smoothed Score into a number of clusters, each represented by a distinct color. These colors can be applied to the price bars (if enabled) for an immediate visual indication of the current volatility regime.

How It Works:

Input & Window Setup: Users set parameters for indicator periods, normalization methods, weights, and window size. The indicator can automatically determine the analysis window based on the number of lookback days.

Calculation of Metrics: The indicator computes the ATR, ADR (as the average of bar ranges), and the Chaikin Oscillator (based on the difference between short and long EMAs of the Accumulation/Distribution line).

Normalization & Scoring: Each indicator’s value is normalized and then weighted to form a raw Score. This raw Score is scaled to a range using statistics from the chosen window.

Smoothing & Clustering: The raw Score is smoothed using an EMA. The resulting smoothed Score is then multiplied by the number of clusters to assign a cluster index, which is used to choose a color for visual signals.

Visualization: The smoothed Score is plotted on the chart with a color that changes based on its value (e.g., lime for low, red for high, yellow for intermediate values). Optionally, the price bars are colored according to the assigned cluster.

_____________

This indicator is ideal for traders seeking a quick and clear assessment of market volatility. By integrating multiple volatility measures into one comprehensive Score, it simplifies analysis and aids in making more informed trading decisions.

For more detailed instructions, please refer to the guide here:

Historical Volatility StudyThe goal of this script it to provide you an idea to forecast the future momentum by looking at historical volatility.

This chart has basically three parts.

1. Three lines are there. The multi color line represents the historical annualized volatility in terms of minimum look back period . The white line represents the historical annualized volatility in terms of medium term look back period . The green line represents the historical annualized volatility in terms of longer term look back period .

2. The back ground color has three components. Green zone is the zone where overall volatility is on the lower side. Red zone is the zone where overall volatility is on the higher side. Purple zone means fluctuating volatility.

3. The multi color line has three colors. Red color means volatility moving towards extreme low. Yellow means it is moving towards extreme high. Purple means it is in normal course of action.

This tool can be used as a confirmation tool with other studies to aid you to make better decisions. For example- look at the diagram below.

Make your thorough study before making any trading decision. Thanks.

Dual Volatility StopThis merges Volatility Stop & its MTF version both published by u/TradingView . Background is colored green or red when both the current timeframe Vstop and higher timeframe Vstop point in same direction. Aim is to take the standard Vstop script which differentiates market from only uptrend/downtrend to uptrend/downtrend/sideways. There is a tradeoff with this, that there is no need for the Vstop to be always in a position which reduces trade time & frees up capital. However this leads to situations where it takes slightly more time to catch on to a trend after a reversal.

Green Background = Buy

Red Background = Sell

No Background = Flat

Volume and Volatility Ratio Indicator-WODI策略名称

交易量与波动率比例策略-WODI

一、用户自定义参数

vol_length:交易量均线长度,计算基础交易量活跃度。

index_short_length / index_long_length:指数短期与长期均线长度,用于捕捉中短期与中长期趋势。

index_magnification:敏感度放大倍数,调整指数均线的灵敏度。

index_threshold_magnification:阈值放大因子,用于动态过滤噪音。

lookback_bars:形态检测回溯K线根数,用于捕捉反转模式。

fib_tp_ratio / fib_sl_ratio:斐波那契止盈与止损比率,分别对应黄金分割(0.618/0.382 等)级别。

enable_reversal:反转信号开关,开启后将原有做空信号反向为做多信号,用于单边趋势加仓。

二、核心计算逻辑

交易量百分比

使用 ta.sma 计算 vol_ma,并得到 vol_percent = volume / vol_ma * 100。

价格波动率

volatility = (high – low) / close * 100。

构建复合指数

volatility_index = vol_percent * volatility,并分别计算其短期与长期均线(乘以 index_magnification)。

动态阈值

index_threshold = index_long_ma * index_threshold_magnification,过滤常规波动。

三、信号生成与策略执行

做多/做空信号

当短期指数均线自下而上突破长期均线,且 volatility_index 突破 index_threshold 时,发出做多信号。

当短期指数均线自上而下跌破长期均线,且 volatility_index 跌破 index_threshold 时,发出做空信号。

反转信号模式(可选)

若 enable_reversal = true,则所有做空信号反向为做多,用于在强趋势行情中加仓。

止盈止损管理

进场后自动设置斐波那契止盈位(基于入场价 × fib_tp_ratio)和止损位(入场价 × fib_sl_ratio)。

支持多级止盈:可依次以 0.382、0.618 等黄金分割比率分批平仓。

四、图表展示

策略信号标记:图上用箭头标明每次做多/做空(或反转加仓)信号。

斐波那契区间:在K线图中显示止盈/止损水平线。

复合指数与阈值线:与原版相同,在独立窗口绘制短、长期指数均线、指数曲线及阈值。

量能柱状:高于均线时染色,反转模式时额外高亮。

Strategy Name

Volume and Volatility Ratio Strategy – WODI

1. User-Defined Parameters

vol_length: Length for volume SMA.

index_short_length / index_long_length: Short and long MA lengths for the composite index.

index_magnification: Sensitivity multiplier for index MAs.

index_threshold_magnification: Threshold multiplier to filter noise.

lookback_bars: Number of bars to look back for pattern detection.

fib_tp_ratio / fib_sl_ratio: Fibonacci take-profit and stop-loss ratios (e.g. 0.618, 0.382).

enable_reversal: Toggle for reversal mode; flips short signals to long for trend-following add-on entries.

2. Core Calculation

Volume Percentage:

vol_ma = ta.sma(volume, vol_length)

vol_percent = volume / vol_ma * 100

Volatility:

volatility = (high – low) / close * 100

Composite Index:

volatility_index = vol_percent * volatility

Short/long MAs applied and scaled by index_magnification.

Dynamic Threshold:

index_threshold = index_long_ma * index_threshold_magnification.

3. Signal Generation & Execution

Long/Short Entries:

Long when short MA crosses above long MA and volatility_index > index_threshold.

Short when short MA crosses below long MA and volatility_index < index_threshold.

Reversal Mode (optional):

If enable_reversal is on, invert all short entries to long to scale into trending moves.

Fibonacci Take-Profit & Stop-Loss:

Automatically set TP/SL levels at entry price × respective Fibonacci ratios.

Supports multi-stage exits at 0.382, 0.618, etc.

4. Visualization

Signal Arrows: Marks every long/short or reversal-add signal on the chart.

Fibonacci Zones: Plots TP/SL lines on the price panel.

Index & Threshold: Same as v1.0, with MAs, index curve, and threshold in a separate sub-window.

Volume Bars: Colored when above vol_ma; extra highlight if a reversal-add signal triggers