Equilibrium Candles + Pattern [Honestcowboy]The Equilibrium Candles is a very simple trend continuation or reversal strategy depending on your settings.

How an Equilibrium Candle is created:

We calculate the equilibrium by measuring the mid point between highest and lowest point over X amount of bars back.

This now is the opening price for each bar and will be considered a green bar if price closes above equilibrium.

Bars get shaded by checking if regular candle close is higher than open etc. So you still see what the normal candles are doing.

Why are they useful?

The equilibrium is calculated the same as Baseline in Ichimoku Cloud. Which provides a point where price is very likely to retrace to. This script visualises the distance between close and equilibrium using candles. To provide a clear visual of how price relates to this equilibrium point.

This also makes it more straightforward to develop strategies based on this simple concept and makes the trader purely focus on this relationship and not think of any Ichimoku Cloud theories.

Script uses a very simple pattern to enter trades:

It will count how many candles have been one directional (above or below equilibrium)

Based on user input after X candles (7 by default) script shows we are in a trend (bg colors)

On the first pullback (candle closes on other side of equilibrium) it will look to enter a trade.

Places a stop order at the high of the candle if bullish trend or reverse if bearish trend.

If based on user input after X opposite candles (2 by default) order is not filled will cancel it and look for a new trend.

Use Reverse Logic:

There is a use reverse logic in the settings which on default is turned on. It will turn long orders into short orders making the stop orders become limit orders. It will use the normal long SL as target for the short. And TP as stop for the short. This to provide a means to reverse equity curve in case your pair is mean reverting by nature instead of trending.

ATR Calculation:

Averaged ATR, which is using ta.percentile_nearest_rank of 60% of a normal ATR (14 period) over the last 200 bars. This in simple words finds a value slightly above the mean ATR value over that period.

Big Candle Exit Logic:

Using Averaged ATR the script will check if a candle closes X times that ATR from the equilibrium point. This is then considered an overextension and all trades are closed.

This is also based on user input.

Simple trade management logic:

Checks if the user has selected to use TP and SL, or/and big candle exit.

Places a TP and SL based on averaged ATR at a multiplier based on user Input.

Closes trade if there is a Big Candle Exit or an opposite direction signal from indicator.

Script can be fully automated to MT5

There are risk settings in % and symbol settings provided at the bottom of the indicator. The script will send alert to MT5 broker trying to mimic the execution that happens on tradingview. There are always delays when using a bridge to MT5 broker and there could be errors so be mindful of that. This script sends alerts in format so they can be read by tradingview.to which is a bridge between the platforms.

Use the all alert function calls feature when setting up alerts and make sure you provide the right webhook if you want to use this approach.

There is also a simple buy and sell alert feature if you don't want to fully automate but still get alerts. These are available in the dropdown when creating an alert.

Almost every setting in this indicator has a tooltip added to it. So if any setting is not clear hover over the (?) icon on the right of the setting.

The backtest uses a 4% exposure per trade and a 10 point slippage. I did not include a commission cause I'm not personaly aware what the commissions are on most forex brokers. I'm only aware of minimal slippage to use in a backtest. Trading conditions vary per broker you use so always pay close attention to trading costs on your own broker. Use a full automation at your own risk and discretion and do proper backtesting.

Tìm kiếm tập lệnh với "backtesting"

DSL Strategy [DailyPanda]

Overview

The DSL Strategy by DailyPanda is a trading strategy that synergistically combines the idea from indicators to create a more robust and reliable trading tool. By integrating these indicators, the strategy enhances signal accuracy and provides traders with a comprehensive view of market trends and momentum shifts. This combination allows for better entry and exit points, improved risk management, and adaptability to various market conditions.

Combining ideas from indicators adds value by:

Enhancing Signal Confirmation : The strategy requires alignment between trend and momentum before generating trade signals, reducing false entries.

Improving Accuracy : By integrating price action with momentum analysis, the strategy captures more reliable trading opportunities.

Providing Comprehensive Market Insight : The combination offers a better perspective on the market, considering both the direction (trend) and the strength (momentum) of price movements.

How the Components Work Together

1. Trend Identification with DSL Indicator

Dynamic Signal Lines : Calculates upper and lower DSL lines based on a moving average (SMA) and dynamic thresholds derived from recent highs and lows with a specified offset. These lines adapt to market conditions, providing real-time trend insights.

ATR-Based Bands : Adds bands around the DSL lines using the Average True Range (ATR) multiplied by a width factor. These bands account for market volatility and help identify potential stop-loss levels.

Trend Confirmation : The relationship between the price, DSL lines, and bands determines the current trend. For example, if the price consistently stays above the upper DSL line, it indicates a bullish trend.

2. Momentum Analysis

RSI Calculation : Computes the RSI over a specified period to measure the speed and change of price movements.

Zero-Lag EMA (ZLEMA) : Applies a ZLEMA to the RSI to minimize lag and produce a more responsive oscillator.

DSL Application on Oscillator : Implements the DSL concept on the oscillator by calculating dynamic upper and lower levels. This helps identify overbought or oversold conditions more accurately.

Signal Generation : Detects crossovers between the oscillator and its DSL lines. A crossover above the lower DSL line signals potential bullish momentum, while a crossover below the upper DSL line signals potential bearish momentum.

3. Integrated Signal Filtering

Confluence Requirement : A trade signal is generated only when both the DSL indicator and oscillator agree. For instance, a long entry requires both an uptrend confirmation from the DSL indicator and a bullish momentum signal from the oscillator.

Risk Management Integration : The strategy uses the DSL indicator's bands for setting stop-loss levels and calculates take-profit levels based on a user-defined risk-reward ratio. This ensures that every trade has a predefined risk management plan.

--------------------------------------------------------------------------------------------

Originality and Value Added to the Community

Unique Synergy : While both indicators are available individually, this strategy is original in how it combines them to enhance their strengths and mitigate their weaknesses, offering a novel approach not present in existing scripts.

Enhanced Reliability : By requiring confirmation from both trend and momentum indicators, the strategy reduces false signals and increases the likelihood of successful trades.

Versatility : The customizable parameters allow traders to adapt the strategy to different instruments, timeframes, and trading styles, making it a valuable tool for a wide range of trading scenarios.

Educational Contribution : The script demonstrates an effective method of combining indicators for improved trading performance, providing insights that other traders can learn from and apply to their own strategies.

--------------------------------------------------------------------------------------------

How to Use the Strategy

Adding the Strategy to Your Chart

Apply the DSL Strategy to your desired trading instrument and timeframe on TradingView.

--------------------------------------------------------------------------------------------

Configuring Parameters

DSL Indicator Settings :

Length (len) : Adjusts the sensitivity of the DSL lines (default is 34).

Offset : Determines the look-back period for threshold calculations (default is 30).

Bands Width (width) : Changes the distance of the ATR-based bands from the DSL lines (default is 1).

DSL-BELUGA Oscillator Settings :

Beluga Length (len_beluga) : Sets the period for the RSI calculation in the oscillator (default is 10).

DSL Lines Mode (dsl_mode) : Chooses between "Fast" (more responsive) and "Slow" (smoother) modes for the oscillator's DSL lines.

Risk Management :

Risk Reward (risk_reward) : Defines your desired risk-reward ratio for calculating take-profit levels (default is 1.5).

--------------------------------------------------------------------------------------------

Interpreting Signals

Long Entry Conditions :

Trend Confirmation : Price is above the upper DSL line and the upper DSL band (dsl_up1 > dsl_dn).

Price Behavior : The last three candles have both their opens and closes above the upper DSL line.

Momentum Signal : The DSL-BELUGA oscillator crosses above its lower DSL line (up_signal), indicating bullish momentum.

Short Entry Conditions :

Trend Confirmation : Price is below the lower DSL line and the lower DSL band (dsl_dn < dsl_up1).

Price Behavior : The last three candles have both their opens and closes below the lower DSL band.

Momentum Signal : The DSL-BELUGA oscillator crosses below its upper DSL line (dn_signal), indicating bearish momentum.

Exit Conditions :

Stop-Loss : Automatically set at the DSL indicator's band level (upper band for longs, lower band for shorts).

Take-Profit : Calculated based on the risk-reward ratio and the initial risk determined by the stop-loss distance.

Visual Aids

Signal Arrows : Upward green arrows for long entries and downward blue arrows for short entries appear on the chart when conditions are met.

Stop-Loss and Take-Profit Lines : Red and green lines display the calculated stop-loss and take-profit levels for active trades.

Background Highlighting : The chart background subtly changes color to indicate when a signal has been generated.

Backtesting and Optimization

Use TradingView's strategy tester to backtest the strategy over historical data.

Adjust parameters to optimize performance for different instruments or market conditions.

Regularly review backtesting results to ensure the strategy remains effective.

ICT Master Suite [Trading IQ]Hello Traders!

We’re excited to introduce the ICT Master Suite by TradingIQ, a new tool designed to bring together several ICT concepts and strategies in one place.

The Purpose Behind the ICT Master Suite

There are a few challenges traders often face when using ICT-related indicators:

Many available indicators focus on one or two ICT methods, which can limit traders who apply a broader range of ICT related techniques on their charts.

There aren't many indicators for ICT strategy models, and we couldn't find ICT indicators that allow for testing the strategy models and setting alerts.

Many ICT related concepts exist in the public domain as indicators, not strategies! This makes it difficult to verify that the ICT concept has some utility in the market you're trading and if it's worth trading - it's difficult to know if it's working!

Some users might not have enough chart space to apply numerous ICT related indicators, which can be restrictive for those wanting to use multiple ICT techniques simultaneously.

The ICT Master Suite is designed to offer a comprehensive option for traders who want to apply a variety of ICT methods. By combining several ICT techniques and strategy models into one indicator, it helps users maximize their chart space while accessing multiple tools in a single slot.

Additionally, the ICT Master Suite was developed as a strategy . This means users can backtest various ICT strategy models - including deep backtesting. A primary goal of this indicator is to let traders decide for themselves what markets to trade ICT concepts in and give them the capability to figure out if the strategy models are worth trading!

What Makes the ICT Master Suite Different

There are many ICT-related indicators available on TradingView, each offering valuable insights. What the ICT Master Suite aims to do is bring together a wider selection of these techniques into one tool. This includes both key ICT methods and strategy models, allowing traders to test and activate strategies all within one indicator.

Features

The ICT Master Suite offers:

Multiple ICT strategy models, including the 2022 Strategy Model and Unicorn Model, which can be built, tested, and used for live trading.

Calculation and display of key price areas like Breaker Blocks, Rejection Blocks, Order Blocks, Fair Value Gaps, Equal Levels, and more.

The ability to set alerts based on these ICT strategies and key price areas.

A comprehensive, yet practical, all-inclusive ICT indicator for traders.

Customizable Timeframe - Calculate ICT concepts on off-chart timeframes

Unicorn Strategy Model

2022 Strategy Model

Liquidity Raid Strategy Model

OTE (Optimal Trade Entry) Strategy Model

Silver Bullet Strategy Model

Order blocks

Breaker blocks

Rejection blocks

FVG

Strong highs and lows

Displacements

Liquidity sweeps

Power of 3

ICT Macros

HTF previous bar high and low

Break of Structure indications

Market Structure Shift indications

Equal highs and lows

Swings highs and swing lows

Fibonacci TPs and SLs

Swing level TPs and SLs

Previous day high and low TPs and SLs

And much more! An ongoing project!

How To Use

Many traders will already be familiar with the ICT related concepts listed above, and will find using the ICT Master Suite quite intuitive!

Despite this, let's go over the features of the tool in-depth and how to use the tool!

The image above shows the ICT Master Suite with almost all techniques activated.

ICT 2022 Strategy Model

The ICT Master suite provides the ability to test, set alerts for, and live trade the ICT 2022 Strategy Model.

The image above shows an example of a long position being entered following a complete setup for the 2022 ICT model.

A liquidity sweep occurs prior to an upside breakout. During the upside breakout the model looks for the FVG that is nearest 50% of the setup range. A limit order is placed at this FVG for entry.

The target entry percentage for the range is customizable in the settings. For instance, you can select to enter at an FVG nearest 33% of the range, 20%, 66%, etc.

The profit target for the model generally uses the highest high of the range (100%) for longs and the lowest low of the range (100%) for shorts. Stop losses are generally set at 0% of the range.

The image above shows the short model in action!

Whether you decide to follow the 2022 model diligently or not, you can still set alerts when the entry condition is met.

ICT Unicorn Model

The image above shows an example of a long position being entered following a complete setup for the ICT Unicorn model.

A lower swing low followed by a higher swing high precedes the overlap of an FVG and breaker block formed during the sequence.

During the upside breakout the model looks for an FVG and breaker block that formed during the sequence and overlap each other. A limit order is placed at the nearest overlap point to current price.

The profit target for this example trade is set at the swing high and the stop loss at the swing low. However, both the profit target and stop loss for this model are configurable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

For Longs, the selectable stop losses are:

Swing Low

Bottom of FVG or breaker block

The image above shows the short version of the Unicorn Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

For Shorts, the selectable stop losses are:

Swing High

Top of FVG or breaker block

The image above shows the profit target and stop loss options in the settings for the Unicorn Model.

Optimal Trade Entry (OTE) Model

The image above shows an example of a long position being entered following a complete setup for the OTE model.

Price retraces either 0.62, 0.705, or 0.79 of an upside move and a trade is entered.

The profit target for this example trade is set at the -0.5 fib level. This is also adjustable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

The image above shows the short version of the OTE Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

Liquidity Raid Model

The image above shows an example of a long position being entered following a complete setup for the Liquidity Raid Modell.

The user must define the session in the settings (for this example it is 13:30-16:00 NY time).

During the session, the indicator will calculate the session high and session low. Following a “raid” of either the session high or session low (after the session has completed) the script will look for an entry at a recently formed breaker block.

If the session high is raided the script will look for short entries at a bearish breaker block. If the session low is raided the script will look for long entries at a bullish breaker block.

For Longs, the profit target options are:

Swing high

User inputted Lib level

For Longs, the stop loss options are:

Swing low

User inputted Lib level

Breaker block bottom

The image above shows the short version of the Liquidity Raid Model in action!

For Shorts, the profit target options are:

Swing Low

User inputted Lib level

For Shorts, the stop loss options are:

Swing High

User inputted Lib level

Breaker block top

Silver Bullet Model

The image above shows an example of a long position being entered following a complete setup for the Silver Bullet Modell.

During the session, the indicator will determine the higher timeframe bias. If the higher timeframe bias is bullish the strategy will look to enter long at an FVG that forms during the session. If the higher timeframe bias is bearish the indicator will look to enter short at an FVG that forms during the session.

For Longs, the profit target options are:

Nearest Swing High Above Entry

Previous Day High

For Longs, the stop loss options are:

Nearest Swing Low

Previous Day Low

The image above shows the short version of the Silver Bullet Model in action!

For Shorts, the profit target options are:

Nearest Swing Low Below Entry

Previous Day Low

For Shorts, the stop loss options are:

Nearest Swing High

Previous Day High

Order blocks

The image above shows indicator identifying and labeling order blocks.

The color of the order blocks, and how many should be shown, are configurable in the settings!

Breaker Blocks

The image above shows indicator identifying and labeling order blocks.

The color of the breaker blocks, and how many should be shown, are configurable in the settings!

Rejection Blocks

The image above shows indicator identifying and labeling rejection blocks.

The color of the rejection blocks, and how many should be shown, are configurable in the settings!

Fair Value Gaps

The image above shows indicator identifying and labeling fair value gaps.

The color of the fair value gaps, and how many should be shown, are configurable in the settings!

Additionally, you can select to only show fair values gaps that form after a liquidity sweep. Doing so reduces "noisy" FVGs and focuses on identifying FVGs that form after a significant trading event.

The image above shows the feature enabled. A fair value gap that occurred after a liquidity sweep is shown.

Market Structure

The image above shows the ICT Master Suite calculating market structure shots and break of structures!

The color of MSS and BoS, and whether they should be displayed, are configurable in the settings.

Displacements

The images above show indicator identifying and labeling displacements.

The color of the displacements, and how many should be shown, are configurable in the settings!

Equal Price Points

The image above shows the indicator identifying and labeling equal highs and equal lows.

The color of the equal levels, and how many should be shown, are configurable in the settings!

Previous Custom TF High/Low

The image above shows the ICT Master Suite calculating the high and low price for a user-defined timeframe. In this case the previous day’s high and low are calculated.

To illustrate the customizable timeframe function, the image above shows the indicator calculating the previous 4 hour high and low.

Liquidity Sweeps

The image above shows the indicator identifying a liquidity sweep prior to an upside breakout.

The image above shows the indicator identifying a liquidity sweep prior to a downside breakout.

The color and aggressiveness of liquidity sweep identification are adjustable in the settings!

Power Of Three

The image above shows the indicator calculating Po3 for two user-defined higher timeframes!

Macros

The image above shows the ICT Master Suite identifying the ICT macros!

ICT Macros are only displayable on the 5 minute timeframe or less.

Strategy Performance Table

In addition to a full-fledged TradingView backtest for any of the ICT strategy models the indicator offers, a quick-and-easy strategy table exists for the indicator!

The image above shows the strategy performance table in action.

Keep in mind that, because the ICT Master Suite is a strategy script, you can perform fully automatic backtests, deep backtests, easily add commission and portfolio balance and look at pertinent metrics for the ICT strategies you are testing!

Lite Mode

Traders who want the cleanest chart possible can toggle on “Lite Mode”!

In Lite Mode, any neon or “glow” like effects are removed and key levels are marked as strict border boxes. You can also select to remove box borders if that’s what you prefer!

Settings Used For Backtest

For the displayed backtest, a starting balance of $1000 USD was used. A commission of 0.02%, slippage of 2 ticks, a verify price for limit orders of 2 ticks, and 5% of capital investment per order.

A commission of 0.02% was used due to the backtested asset being a perpetual future contract for a crypto currency. The highest commission (lowest-tier VIP) for maker orders on many exchanges is 0.02%. All entered positions take place as maker orders and so do profit target exits. Stop orders exist as stop-market orders.

A slippage of 2 ticks was used to simulate more realistic stop-market orders. A verify limit order settings of 2 ticks was also used. Even though BTCUSDT.P on Binance is liquid, we just want the backtest to be on the safe side. Additionally, the backtest traded 100+ trades over the period. The higher the sample size the better; however, this example test can serve as a starting point for traders interested in ICT concepts.

Community Assistance And Feedback

Given the complexity and idiosyncratic applications of ICT concepts amongst its proponents, the ICT Master Suite’s built-in strategies and level identification methods might not align with everyone's interpretation.

That said, the best we can do is precisely define ICT strategy rules and concepts to a repeatable process, test, and apply them! Whether or not an ICT strategy is trading precisely how you would trade it, seeing the model in action, taking trades, and with performance statistics is immensely helpful in assessing predictive utility.

If you think we missed something, you notice a bug, have an idea for strategy model improvement, please let us know! The ICT Master Suite is an ongoing project that will, ideally, be shaped by the community.

A big thank you to the @PineCoders for their Time Library!

Thank you!

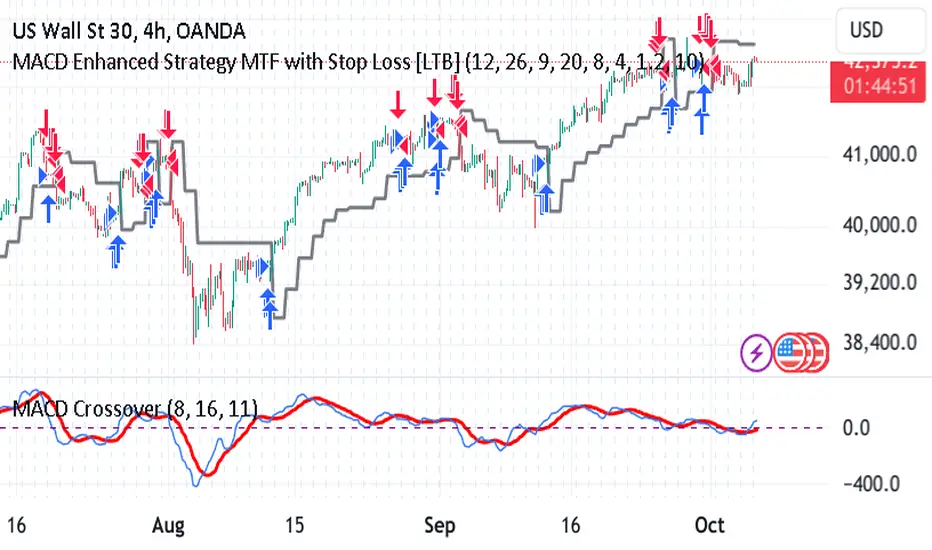

MACD Enhanced Strategy MTF with Stop Loss [LTB]Test strategy for MACD

This strategy, named "MACD Enhanced Strategy MTF with Stop Loss ," is a modified Moving Average Convergence Divergence (MACD) strategy with enhancements such as multi-timeframe (MTF) analysis, custom scoring, and a dynamic stop loss mechanism. Let’s break down how to effectively use it:

Key Elements of the Strategy

MACD Indicator with Modifications:

The strategy uses MACD, a well-known momentum indicator, with customizable parameters:

fastLength, slowLength, and signalLength represent the standard MACD settings.

Instead of relying solely on MACD crossovers, it introduces scoring parameters for histogram direction (histside), indicator direction (indiside), and signal cross (crossscore). This allows for a more nuanced decision-making process when determining buy and sell signals.

Multi-Timeframe Analysis (MTF):

The strategy compares the current timeframe's MACD score with that of a higher timeframe (HTF). It dynamically selects the higher timeframe based on the current timeframe. For example, if the current chart period is 1, it will select 5 as the higher timeframe.

This MTF approach aims to align trades with broader trends, filtering out false signals that could be present when analyzing only a single timeframe.

Scoring System:

A custom scoring system (count() function) is used to evaluate buy and sell signals. This includes calculations based on the direction and momentum of MACD (indi) and the histogram. The score is used to determine the strength of signals.

Positive scores indicate bullish sentiment, while negative scores indicate bearish sentiment.

This scoring mechanism aims to reduce the influence of noise and provide more reliable entries.

Entry Conditions:

Long Condition: When the Result value (a combination of MTF and current MACD analysis) changes and becomes positive, a long entry is triggered.

Short Condition: When the Result changes and becomes negative, a short entry is initiated.

Stop Loss Mechanism:

The countstop() function calculates dynamic stop loss values for both long and short trades. It is based on the Average True Range (ATR) multiplied by a factor (Mult), providing adaptive stop loss levels depending on market volatility.

The stop loss is plotted on the chart to show potential risk levels for open trades, with the line appearing only if shotsl is enabled.

How to Use the Strategy

To properly use the strategy, follow these steps:

Parameter Optimization:

Adjust the input parameters such as fastLength, slowLength, and signalLength to tune the MACD indicator to the specific asset you’re trading. The values provided are typical defaults, but optimizing these values based on backtesting can help improve performance.

Customize the scoring parameters (crossscore, indiside, histside) to balance how much weight you want to put on the direction, histogram, and cross events of the MACD indicator.

Select Appropriate Timeframes:

This strategy employs a multi-timeframe (MTF) approach, so it's important to understand how the higher timeframe (HTF) is selected based on the current timeframe. For instance, if you are trading on a 5-minute chart, the higher timeframe will be 15 minutes, which helps filter out lower timeframe noise.

Ensure you understand the relationship between the timeframe you’re using and the HTF it automatically selects. The strategy’s effectiveness can vary depending on how these timeframes align with the asset’s overall volatility.

Run Backtests:

Always backtest the strategy over historical data to determine its reliability for the asset and timeframes you’re interested in. Note that the MTF approach may require substantial data to capture how different timeframes interact.

Use the backtest results to adjust the scoring parameters or the Stop Loss Factor (Mult) for better risk management.

Stop Loss Usage:

The stop loss is calculated dynamically using ATR, which means that it adjusts with changing volatility. This can be useful to avoid being stopped out too often during periods of increased volatility.

The shotsl parameter can be set to true to visualize the stop loss line on the chart. This helps to monitor the protection level and make better decisions regarding holding or closing a trade manually.

Entry Signals and Trade Execution:

Look for changes in the Result value to determine entry points. For a long position, the Result needs to become positive, and for a short position, it must be negative.

Note that the strategy's entries are more conservative because it waits for the Result to confirm the direction using multiple factors, which helps filter out false breakouts.

Risk Management:

The adaptive stop loss mechanism reduces the risk by basing the stop level on market volatility. However, you must still consider additional risk management practices such as position sizing and profit targets.

Given the scoring mechanism, it might not enter trades frequently, which means using this strategy may result in fewer but potentially more accurate trades. It’s important to be patient and not force trades that don’t align with the calculated results.

Real-Time Monitoring:

Make sure to monitor trades actively. Since the strategy recalculates the score on each bar, real-time changes in the Result value could provide exit opportunities even if the stop loss isn't triggered.

Summary

The "MACD Enhanced Strategy MTF with Stop Loss " is a sophisticated version of the MACD strategy, enhanced with multi-timeframe analysis and adaptive stop loss. Properly using it involves optimizing MACD and scoring parameters, selecting suitable timeframes, and actively managing entries and exits based on a combination of scoring and volatility-based stop losses. Always conduct thorough backtesting before applying it in a live environment to ensure the strategy performs well on the asset you're trading.

Ichimoku Crosses_RSI_AITIchimoku Crosser_RSI_AIT

Overview

The "Ichimoku Cloud Crosses_AIT" strategy is a technical trading strategy that combines the Ichimoku Cloud components with the Relative Strength Index (RSI) to generate trade signals. This strategy leverages the crossovers of the Tenkan-sen and Kijun-sen lines of the Ichimoku Cloud, along with RSI levels, to identify potential entry and exit points for long and short trades. This guide explains the strategy components, conditions, and how to use it effectively in your trading.

1. Strategy Parameters

User Inputs

Tenkan-sen Period (tenkanLength): Default value is 21. This is the period used to calculate the Tenkan-sen line (conversion line) of the Ichimoku Cloud.

Kijun-sen Period (kijunLength): Default value is 120. This is the period used to calculate the Kijun-sen line (base line) of the Ichimoku Cloud.

Senkou Span B Period (senkouBLength): Default value is 52. This is the period used to calculate the Senkou Span B line (leading span B) of the Ichimoku Cloud.

RSI Period (rsiLength): Default value is 14. This period is used to calculate the Relative Strength Index (RSI).

RSI Long Entry Level (rsiLongLevel): Default value is 60. This level indicates the minimum RSI value for a long entry signal.

RSI Short Entry Level (rsiShortLevel): Default value is 40. This level indicates the maximum RSI value for a short entry signal.

2. Strategy Components

Ichimoku Cloud

Tenkan-sen: A short-term trend indicator calculated as the simple moving average (SMA) of the highest high and the lowest low over the Tenkan-sen period.

Kijun-sen: A medium-term trend indicator calculated as the SMA of the highest high and the lowest low over the Kijun-sen period.

Senkou Span A: Calculated as the average of the Tenkan-sen and Kijun-sen, plotted 26 periods ahead.

Senkou Span B: Calculated as the SMA of the highest high and lowest low over the Senkou Span B period, plotted 26 periods ahead.

Chikou Span: The closing price plotted 26 periods behind.

Relative Strength Index (RSI)

RSI: A momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and is used to identify overbought or oversold conditions.

3. Entry and Exit Conditions

Entry Conditions

Long Entry:

The Tenkan-sen crosses above the Kijun-sen (bullish crossover).

The RSI value is greater than or equal to the rsiLongLevel.

Short Entry:

The Tenkan-sen crosses below the Kijun-sen (bearish crossover).

The RSI value is less than or equal to the rsiShortLevel.

Exit Conditions

Exit Long Position: The Tenkan-sen crosses below the Kijun-sen.

Exit Short Position: The Tenkan-sen crosses above the Kijun-sen.

4. Visual Representation

Tenkan-sen Line: Plotted on the chart. The color changes based on its relation to the Kijun-sen (green if above, red if below) and is displayed with a line width of 2.

Kijun-sen Line: Plotted as a white line with a line width of 1.

Entry Arrows:

Long Entry: Displayed as a yellow triangle below the bar.

Short Entry: Displayed as a fuchsia triangle above the bar.

5. How to Use

Apply the Strategy: Apply the "Ichimoku Cloud Crosses_AIT" strategy to your chart in TradingView.

Configure Parameters: Adjust the strategy parameters (Tenkan-sen, Kijun-sen, Senkou Span B, and RSI settings) according to your trading preferences.

Interpret the Signals:

Long Entry: A yellow triangle appears below the bar when a long entry signal is generated.

Short Entry: A fuchsia triangle appears above the bar when a short entry signal is generated.

Monitor Open Positions: The strategy automatically exits positions based on the defined conditions.

Backtesting and Live Trading: Use the strategy for backtesting and live trading. Adjust risk management settings in the strategy properties as needed.

Conclusion

The "Ichimoku Cloud Crosses_AIT" strategy uses Ichimoku Cloud crossovers and RSI to generate trading signals. This strategy aims to capture market trends and potential reversals, providing a structured way to enter and exit trades. Make sure to backtest and optimize the strategy parameters to suit your trading style and market conditions before using it in a live trading environment.

Gann + Laplace Smoothed Hybrid Volume Spread AnalysisThe Gann + Laplace Smoothed Hybrid Volume Spread Analysis ( GannLSHVSA ) Strategy/Indicator is an trading tool designed to fuse volume analysis with trend detection, offering traders a view of market dynamics.

This Strategy/Indicator stands apart by integrating the principles of the upgraded Discrete Fourier Transform (DFT), the Laplace Stieltjes Transform and volume spread analysis, enhanced with a layer of Fourier smoothing to distill market noise and highlight trend directions with unprecedented clarity.

The length of EMA and Strategy Entries are modified with the Gann swings .

This smoothing process allows traders to discern the true underlying patterns in volume and price action, stripped of the distractions of short-term fluctuations and noise.

The core functionality of the GannLSHVSA revolves around the innovative combination of volume change analysis, spread determination (calculated from the open and close price difference), and the strategic use of the EMA (default 10) to fine-tune the analysis of spread by incorporating volume changes.

Trend direction is validated through a moving average (MA) of the histogram, which acts analogously to the Volume MA found in traditional volume indicators. This MA serves as a pivotal reference point, enabling traders to confidently engage with the market when the histogram's movement concurs with the trend direction, particularly when it crosses the Trend MA line, signalling optimal entry points.

It returns 0 when MA of the histogram and EMA of the Price Spread are not align.

WHAT IS GannLSHVSA INDICATOR:

The GannLSHVSA plots a positive trend when a positive Volume smoothed Spread and EMA of Volume smoothed price is above 0, and a negative when negative Volume smoothed Spread and EMA of Volume smoothed price is below 0. When this conditions are not met it plots 0.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

ORIGINALITY & USEFULNESS:

The GannLSHVSA Strategy is unique because it applies upgraded DFT, the Laplace Stieltjes Transform for data smoothing, effectively filtering out the minor fluctuations and leaving traders with a clear picture of the market's true movements. The DFT's ability to break down market signals into constituent frequencies offers a granular view of market dynamics, highlighting the amplitude and phase of each frequency component. This, combined with the strategic application of Ehler's Universal Oscillator principles via a histogram, furnishes traders with a nuanced understanding of market volatility and noise levels, thereby facilitating more informed trading decisions. The Gann swing strategy is developed by meomeo105, this Gann high and low algorithm forms the basis of the EMA modification.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is the meaning of price spread?

In finance, a spread refers to the difference between two prices, rates, or yields. One of the most common types is the bid-ask spread, which refers to the gap between the bid (from buyers) and the ask (from sellers) prices of a security or asset.

We are going to use Open-Close spread.

What is Volume spread analysis?

Volume spread analysis (VSA) is a method of technical analysis that compares the volume per candle, range spread, and closing price to determine price direction.

What does this mean?

We need to have a positive Volume Price Spread and a positive Moving average of Volume price spread for a positive trend. OR via versa a negative Volume Price Spread and a negative Moving average of Volume price spread for a negative trend.

What if we have a positive Volume Price Spread and a negative Moving average of Volume Price Spread?

It results in a neutral, not trending price action.

Thus the Indicator/Strategy returns 0 and Closes all long and short positions.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame. I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Strategy SEMA SDI WebhookPurpose of the Code:

The strategy utilizes Exponential Moving Averages (EMA) and Smoothed Directional Indicators (SDI) to generate buy and sell signals. It includes features like leverage, take profit, stop loss, and trailing stops. The strategy is intended for backtesting and automating trades based on the specified indicators and conditions.

Key Components and Functionalities:

1.Strategy Settings:

Overlay: The strategy will overlay on the price chart.

Slippage: Set to 1.

Commission Value: Set to 0.035.

Default Quantity Type: Percent of equity.

Default Quantity Value: 50% of equity.

Initial Capital: Set to 1000 units.

Calculation on Order Fills: Enabled.

Process Orders on Close: Enabled.

2.Date and Time Filters:

Inputs for enabling/disabling start and end dates.

Filters to execute strategy only within specified date range.

3.Leverage and Quantity:

Leverage: Adjustable leverage input (default 3).

USD Percentage: Adjustable percentage of equity to use for trades (default 50%).

Initial Capital: Calculated based on leverage and percentage of equity.

4.Take Profit, Stop Loss, and Trailing Stop:

Inputs for enabling/disabling take profit, stop loss, and trailing stop.

Adjustable parameters for take profit percentage (default 25%), stop loss percentage (default 4.8%), and trailing stop percentage (default 1.9%).

Calculations for take profit, stop loss, trailing price, and maximum profit tracking.

5.EMA Calculations:

Fast and slow EMAs.

Smoothed versions of the fast and slow EMAs.

6.SDI Calculations:

Directional movement calculation for positive and negative directional indicators.

Difference between the positive and negative directional indicators, smoothed.

7.Buy/Sell Conditions:

Long (Buy) Condition: Positive DI is greater than negative DI, and fast EMA is greater than slow EMA.

Short (Sell) Condition: Negative DI is greater than positive DI, and fast EMA is less than slow EMA.

8.Strategy Execution:

If buy conditions are met, close any short positions and enter a long position.

If sell conditions are met, close any long positions and enter a short position.

Exit conditions for long and short positions based on take profit, stop loss, and trailing stop levels.

Close all positions if outside the specified date range.

Usage:

This strategy is used to automate trading based on the specified conditions involving EMAs and SDI. It allows backtesting to evaluate performance based on historical data. The strategy includes risk management through take profit, stop loss, and trailing stops to protect gains and limit losses. Traders can customize the parameters to fit their specific trading preferences and risk tolerance. Differently, it can perform leverage analysis and use it as a template.

By using this strategy, traders can systematically execute trades based on technical indicators, helping to remove emotional bias and improve consistency in trading decisions.

Important Note:

This script is provided for educational and template purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

Fine-Tune Inputs: Fourier Smoothed Hybrid Volume Spread AnalysisUse this Strategy to Fine-tune inputs for the HSHVSA Indicator.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

I suggest using " Close all " input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using " Close all " input as True , except for the lowest TimeFrame.

MEANINGFUL DESCRIPTION:

The Fourier Smoothed Hybrid Volume Spread Analysis (FSHVSA) Strategy/Indicator is an innovative trading tool designed to fuse volume analysis with trend detection capabilities, offering traders a comprehensive view of market dynamics.

This Strategy/Indicator stands apart by integrating the principles of the Discrete Fourier Transform (DFT) and volume spread analysis, enhanced with a layer of Fourier smoothing to distill market noise and highlight trend directions with unprecedented clarity.

This smoothing process allows traders to discern the true underlying patterns in volume and price action, stripped of the distractions of short-term fluctuations and noise.

The core functionality of the FSHVSA revolves around the innovative combination of volume change analysis, spread determination (calculated from the open and close price difference), and the strategic use of the EMA (default 10) to fine-tune the analysis of spread by incorporating volume changes.

Trend direction is validated through a moving average (MA) of the histogram, which acts analogously to the Volume MA found in traditional volume indicators. This MA serves as a pivotal reference point, enabling traders to confidently engage with the market when the histogram's movement concurs with the trend direction, particularly when it crosses the Trend MA line, signalling optimal entry points.

It returns 0 when MA of the histogram and EMA of the Price Spread are not align.

WHAT IS FSHVSA INDICATOR:

The FSHVSA plots a positive trend when a positive Volume smoothed Spread and EMA of Volume smoothed price is above 0, and a negative when negative Volume smoothed Spread and EMA of Volume smoothed price is below 0. When this conditions are not met it plots 0.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

ORIGINALITY & USEFULNESS:

The FSHVSA Strategy is unique because it applies DFT for data smoothing, effectively filtering out the minor fluctuations and leaving traders with a clear picture of the market's true movements. The DFT's ability to break down market signals into constituent frequencies offers a granular view of market dynamics, highlighting the amplitude and phase of each frequency component. This, combined with the strategic application of Ehler's Universal Oscillator principles via a histogram, furnishes traders with a nuanced understanding of market volatility and noise levels, thereby facilitating more informed trading decisions.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is the meaning of price spread?

In finance, a spread refers to the difference between two prices, rates, or yields. One of the most common types is the bid-ask spread, which refers to the gap between the bid (from buyers) and the ask (from sellers) prices of a security or asset.

We are going to use Open-Close spread.

What is Volume spread analysis?

Volume spread analysis (VSA) is a method of technical analysis that compares the volume per candle, range spread, and closing price to determine price direction.

What does this mean?

We need to have a positive Volume Price Spread and a positive Moving average of Volume price spread for a positive trend. OR via versa a negative Volume Price Spread and a negative Moving average of Volume price spread for a negative trend.

What if we have a positive Volume Price Spread and a negative Moving average of Volume Price Spread?

It results in a neutral, not trending price action.

Thus the Indicator/Strategy returns 0 and Closes all long and short positions.

In the next Image you can see that trend is negative on 4h, we just move Negative on 12h and Positive on 1D. That means trend/Strategy flipped negative .

I am sorry, the chart is a bit messy. The idea is to use the indicator/strategy over more than 1 Timeframe.

Use this Strategy to fine-tune inputs for the HSHVSA Indicator.

(Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data)

I suggest using " Close all " input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using " Close all " input as True , except for the lowest TimeFrame. I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

NASDAQ 100 Peak Hours StrategyNASDAQ 100 Peak Hours Trading Strategy

Description

Our NASDAQ 100 Peak Hours Trading Strategy leverages a carefully designed algorithm to trade within specific hours of high market activity, particularly focusing on the first two hours of the trading session from 09:30 AM to 11:30 AM GMT-5. This period is identified for its increased volatility and liquidity, offering numerous trading opportunities.

The strategy incorporates a blend of technical indicators to identify entry and exit points for both long and short positions. These indicators include:

Exponential Moving Averages (EMAs) : A short-term 9-period EMA and a longer-term 21-period EMA to determine the market trend and momentum.

Relative Strength Index (RSI) : A 14-period RSI to gauge the market's momentum.

Average True Range (ATR) : A 14-period ATR to assess market volatility and to set dynamic stop losses and trailing stops.

Volume Weighted Average Price (VWAP) : To identify the market's average price weighted by volume, serving as a benchmark for the trading day.

Our strategy uniquely applies a volatility filter using the ATR, ensuring trades are only executed in conditions that favor our setup. Additionally, we consider the direction of the EMAs to confirm the market's trend before entering trades.

Originality and Usefulness

This strategy stands out by combining these indicators within the NASDAQ 100's peak hours, exploiting the specific market conditions that prevail during these times. The inclusion of a volatility filter and dynamic stop-loss mechanisms based on the ATR provides a robust method for managing risk.

By focusing on the early trading hours, the strategy aims to capture the initial market movements driven by overnight news and the opening rush, often characterized by higher volatility. This approach is particularly useful for traders looking to maximize gains from short-term fluctuations while limiting exposure to longer-term market uncertainty.

Strategy Results

To ensure the strategy's effectiveness and reliability, it has undergone rigorous backtesting over a significant dataset to produce a sample size of more than 100 trades. This testing phase helps in identifying the strategy's potential in various market conditions, its consistency, and its risk-to-reward ratio.

Our backtesting adheres to realistic trading conditions, accounting for slippage and commission to reflect actual trading scenarios accurately. The strategy is designed with a conservative approach to risk management, advising not to risk more than 5-10% of equity on a single trade. The default settings in the script align with these principles, ensuring that users can replicate our tested conditions.

Using the Strategy

The strategy is designed for simplicity and ease of use:

Trade Hours : Focuses on 09:30 AM to 11:30 AM GMT-5, during the NASDAQ 100's peak activity hours.

Entry Conditions : Trades are initiated based on the alignment of EMAs, RSI, VWAP, and the ATR's volatility filter within the designated time frame.

Exit Conditions : Includes dynamic trailing stops based on ATR, a predefined time exit strategy, and a trend reversal exit condition for risk management.

This script is a powerful tool for traders looking to leverage the NASDAQ 100's peak hours, providing a structured approach to navigating the early market hours with a robust set of criteria for making informed trading decisions.

Inside Candle StrategyIntroduction

The Inside Candle Breakout Strategy leverages the concept of inside candles as a primary signal for potential breakouts. Unlike common trend-following or scalping strategies, this method focuses on the volatility squeeze indicated by inside candles and aims to capture the momentum that follows these periods of consolidation. The strategy's originality lies in its specific integration of timeframes for signal detection and its application across diverse market conditions without relying on conventional trend indicators.

Strategy Description and Mechanics

Inside Candle Identification: At the heart of this strategy is the detection of inside candles, defined as candles fully contained within the range of the preceding candle. This pattern signifies a temporary balance between buyers and sellers, often preceding significant price movements. The strategy scans for these candles within a user-specified timeframe in the input section of the settings of the strategy, allowing for tailored signal generation based on individual trading preferences.

Entry Points and Market Entries: Upon identifying an inside candle and only once this candle closes, the strategy prepares to enter a trade in the direction of the breakout. Trades are executed in the timeframe selected on the chart, ensuring that entry points are aligned with real-time market movements. This process highlights the strategy's adaptability, making it suitable for various trading styles, from day trading to swing trading.

Overlay Indicator for Enhanced Market Analysis: Accompanying the breakout signals is an overlay indicator comprising two moving averages and a volatility cloud. This feature serves as a secondary tool for market analysis, offering insights into the prevailing market trend and volatility levels. While it doesn't influence the entry or exit signals directly, it provides traders with additional context for refining their decisions, enhancing the strategy's utility. This assistance tool is composed by one moving average and a second line which is calculated adding or subtracting the historical volatility of the asset on the moving average, depending on his momentum.

Strategy Results and Commitment to Realism

Backtesting Protocol: In our commitment to transparency and realism, backtesting results are derived from a dataset that ensures a sufficient number of trades (over 100) to validate the strategy's effectiveness. This approach underscores our dedication to providing traders with reliable and actionable insights.

Risk Management and Trade Sizing: Recognizing the importance of sustainable trading practices, the strategy incorporates strict risk management guidelines. Trades are sized to ensure that only a small percentage of equity is risked on a single trade, adhering to widely accepted risk tolerance levels. The initial account size for this script is set to 10000$.

Strategy Defaults and Justification: The default properties of the strategy, including the risk-reward ratio, average length for moving averages, and other parameters, are carefully chosen based on extensive testing and analysis. These settings represent a balanced approach, aiming to optimize the strategy's performance across a variety of market conditions.

Strategy Components:

- Inside Candles: An inside candle occurs when a candle's high and low are completely contained within the high and low of the previous candle. This pattern indicates a period of consolidation or indecision in the market, often preceding a significant price movement. The strategy detects inside candles based on the user-selected timeframe, allowing traders to capture potential breakouts.

Indicator Overlays:

- Moving Average: A simple moving average (SMA) is calculated over a user-defined length (`Average Length`), providing a dynamic baseline to gauge the market's direction. The strategy offers an option (`Show Moving Average`) to display or hide this moving average on the chart, giving traders control over the visual complexity.

- Volatility Measurement: Alongside the moving average, the strategy assesses market volatility using the standard deviation of the closing prices over the same period defined by the `Average Length`. The moving average is adjusted upwards or downwards by this volatility measure, creating a dynamic channel that reflects the current market conditions.

- Color Gradients for Volatility: The strategy uses a color gradient to fill the area between the moving average and its volatility-adjusted counterpart. This gradient visually represents the volatility level, transitioning from gray (low volatility) to a lighter shade (higher volatility), aiding in the assessment of market sentiment and volatility.

Trading Entries:

- Long Entry: A long position is triggered when the closing price exceeds the high of an inside candle, indicating potential bullish momentum. The strategy places a stop-loss at the low of the inside candle and sets a take-profit level based on the predefined risk-reward ratio (`RR Ratio`).

- Short Entry: Conversely, a short position is initiated when the closing price falls below the low of an inside candle, suggesting bearish pressure. A stop-loss is set at the high of the inside candle, with the take-profit level adjusted according to the risk-reward ratio.

Customization Settings:

- Timeframe: Traders can select the desired timeframe for inside candle detection, tailoring the strategy to fit various trading styles and time horizons.

- RR Ratio: The risk-reward ratio is adjustable, allowing traders to manage the potential risk and return of each trade according to their risk tolerance.

- Average Length: This setting determines the period over which the moving average and volatility are calculated, affecting the sensitivity of the strategy to price movements.

- Visual Settings: Users can customize the appearance of the strategy on their charts, including the colors of the moving average and volatility lines, as well as the line width, enhancing chart readability and personal preference adherence.

Disclaimer

Trading involves significant risk, and it is crucial for traders to conduct their own due diligence before engaging with any strategy. The Inside Candle Breakout Strategy is presented for informational purposes only and does not constitute financial advice.

Trend Deviation strategy - BTC [IkkeOmar]Intro:

This is an example if anyone needs a push to get started with making strategies in pine script. This is an example on BTC, obviously it isn't a good strategy, and I wouldn't share my own good strategies because of alpha decay.

This strategy integrates several technical indicators to determine market trends and potential trade setups. These indicators include:

Directional Movement Index (DMI)

Bollinger Bands (BB)

Schaff Trend Cycle (STC)

Moving Average Convergence Divergence (MACD)

Momentum Indicator

Aroon Indicator

Supertrend Indicator

Relative Strength Index (RSI)

Exponential Moving Average (EMA)

Volume Weighted Average Price (VWAP)

It's crucial for you guys to understand the strengths and weaknesses of each indicator and identify synergies between them to improve the strategy's effectiveness.

Indicator Settings:

DMI (Directional Movement Index):

Length: This parameter determines the number of bars used in calculating the DMI. A higher length may provide smoother results but might lag behind the actual price action.

Bollinger Bands:

Length: This parameter specifies the number of bars used to calculate the moving average for the Bollinger Bands. A longer length results in a smoother average but might lag behind the price action.

Multiplier: The multiplier determines the width of the Bollinger Bands. It scales the standard deviation of the price data. A higher multiplier leads to wider bands, indicating increased volatility, while a lower multiplier results in narrower bands, suggesting decreased volatility.

Schaff Trend Cycle (STC):

Length: This parameter defines the length of the STC calculation. A longer length may result in smoother but slower-moving signals.

Fast Length: Specifies the length of the fast moving average component in the STC calculation.

Slow Length: Specifies the length of the slow moving average component in the STC calculation.

MACD (Moving Average Convergence Divergence):

Fast Length: Determines the number of bars used to calculate the fast EMA (Exponential Moving Average) in the MACD.

Slow Length: Specifies the number of bars used to calculate the slow EMA in the MACD.

Signal Length: Defines the number of bars used to calculate the signal line, which is typically an EMA of the MACD line.

Momentum Indicator:

Length: This parameter sets the number of bars over which momentum is calculated. A longer length may provide smoother momentum readings but might lag behind significant price changes.

Aroon Indicator:

Length: Specifies the number of bars over which the Aroon indicator calculates its values. A longer length may result in smoother Aroon readings but might lag behind significant market movements.

Supertrend Indicator:

Trendline Length: Determines the length of the period used in the Supertrend calculation. A longer length results in a smoother trendline but might lag behind recent price changes.

Trendline Factor: Specifies the multiplier used in calculating the trendline. It affects the sensitivity of the indicator to price changes.

RSI (Relative Strength Index):

Length: This parameter sets the number of bars over which RSI calculates its values. A longer length may result in smoother RSI readings but might lag behind significant price changes.

EMA (Exponential Moving Average):

Fast EMA: Specifies the number of bars used to calculate the fast EMA. A shorter period results in a more responsive EMA to recent price changes.

Slow EMA: Determines the number of bars used to calculate the slow EMA. A longer period results in a smoother EMA but might lag behind recent price changes.

VWAP (Volume Weighted Average Price):

Default settings are typically used for VWAP calculations, which consider the volume traded at each price level over a specific period. This indicator provides insights into the average price weighted by trading volume.

backtest range and rules:

You can specify the start date for backtesting purposes.

You can can select the desired trade direction: Long, Short, or Both.

Entry and Exit Conditions:

LONG:

DMI Cross Up: The Directional Movement Index (DMI) indicates a bullish trend when the positive directional movement (+DI) crosses above the negative directional movement (-DI).

Bollinger Bands (BB): The price is below the upper Bollinger Band, indicating a potential reversal from the upper band.

Momentum Indicator: Momentum is positive, suggesting increasing buying pressure.

MACD (Moving Average Convergence Divergence): The MACD line is above the signal line, indicating bullish momentum.

Supertrend Indicator: The Supertrend indicator signals an uptrend.

Schaff Trend Cycle (STC): The STC indicates a bullish trend.

Aroon Indicator: The Aroon indicator signals a bullish trend or crossover.

When all these conditions are met simultaneously, the strategy considers it a favorable opportunity to enter a long trade.

SHORT:

DMI Cross Down: The Directional Movement Index (DMI) indicates a bearish trend when the negative directional movement (-DI) crosses above the positive directional movement (+DI).

Bollinger Bands (BB): The price is above the lower Bollinger Band, suggesting a potential reversal from the lower band.

Momentum Indicator: Momentum is negative, indicating increasing selling pressure.

MACD (Moving Average Convergence Divergence): The MACD line is below the signal line, signaling bearish momentum.

Supertrend Indicator: The Supertrend indicator signals a downtrend.

Schaff Trend Cycle (STC): The STC indicates a bearish trend.

Aroon Indicator: The Aroon indicator signals a bearish trend or crossover.

When all these conditions align, the strategy considers it an opportune moment to enter a short trade.

Disclaimer:

THIS ISN'T AN OPTIMAL STRATEGY AT ALL! It was just an old project from when I started learning pine script!

The backtest doesn't promise the same results in the future, always do both in-sample and out-of-sample testing when backtesting a strategy. And make sure you forward test it as well before implementing it!

Furthermore this strategy uses both trend and mean-reversion systems, that is usually a no-go if you want to build robust trend systems .

Don't hesitate to comment if you have any questions or if you have some good notes for a beginner.

Monthly Performance Table by Dr. MauryaWhat is this ?

This Strategy script is not aim to produce strategy results but It aim to produce monthly PnL performance Calendar table which is useful for TradingView community to generate a monthly performance table for Own strategy.

So make sure to read the disclaimer below.

Why it is required to publish?:

I am not satisfied with the monthly performance available on TV community script. Sometimes it is very lengthy in code and sometimes it showing the wrong PNL for current month.

So I have decided to develop new Monthly performance or return in value as well as in percentage with highly flexible to adjust row automatically.

Features :

Accuracy increased for current month PnL.

There are 14 columns and automatically adjusted rows according to available trade years/month.

First Column reflect the YEAR, from second column to 13 column reflect the month and 14 column reflect the yearly PnL.

In tabulated data reflects the monthly PnL (value and (%)) in month column and Yearly PnL (value and (%)) in Yearly column.

Various color input also added to change the table look like background color, text color, heading text color, border color.

In tabulated data, background color turn green for profit and red for loss.

Copy from line 54 to last line as it is in your strategy script.

Credit: This code is modified and top up of the open-source code originally written by QuantNomad. Thanks for their contribution towards to give base and lead to other developers. I have changed the way of determining past PnL to array form and keep separated current month and year PnL from array. Which avoid the false pnl in current month.

Strategy description:

As in first line I said This strategy is aim to provide monthly performance table not focused on the strategy. But it is necessary to explain strategy which I have used here. Strategy is simply based on ADX available on TV community script. Long entry is based on when the difference between DIPlus and ADX is reached on certain value (Set value in Long difference in Input Tab) while Short entry is based on when the difference between DIMinus and ADX is reached on certain value (Set value in Short difference in Input Tab).

Default Strategy Properties used on chart(Important)

This script backtest is done on 1 hour timeframe of NSE:Reliance Inds Future cahrt, using the following backtesting properties:

Balance (default): 500 000 (default base currency)

Order Size: 1 contract

Comission: 20 INR per Order

Slippage: 5 tick

Default setting in Input tab

Len (ADX length) : 14

Th (ADX Threshhold): 20

Long Difference (DIPlus - ADX) = 5

Short Difference (DIMinus - ADX) = 5

We use these properties to ensure a realistic preview of the backtesting system, do note that default properties can be different for various reasons described below:

Order Size: 1 contract by default, this is to allow the strategy to run properly on most instruments such as futures.

Comission: Comission can vary depending on the market and instrument, there is no default value that might return realistic results.

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from the strategies built are realistic.

Disclaimer:

This script not provide indicative of any future results.

This script don’t provide any financial advice.

This strategy is only for the readymade snippet code for monthly PnL performance calender table for any own strategy.

[tradinghook] - Renko Trend Reversal Strategy V2Title: Renko Trend Reversal Strategy

Short Title: - Renko TRS

> Special thanks to for manually calculating `renkoClose` and `renkoOpen` values in order to remove the infamous repaint issue

Description:

The Renko Trend Reversal Strategy ( - Renko TRS) is a powerful and original trading approach designed to identify trend reversals in financial markets using Renko charts. Renko charts differ from traditional time-based charts, as they focus solely on price movements and ignore time, resulting in a clearer representation of market trends. This strategy leverages Renko charts in conjunction with the Average True Range (ATR) to capture trend reversals with high precision and effectiveness.

Key Concepts:

Renko Charts: Renko charts are unique chart types that only plot price movements beyond a predefined brick size, ignoring time and noise. By doing so, they provide a more straightforward depiction of market trends, eliminating insignificant price fluctuations and making it easier to spot trend reversals.

Average True Range (ATR): The strategy utilizes the ATR indicator, which measures market volatility and provides valuable insights into potential price movements. By setting the brick size of the Renko chart based on the ATR, the strategy adapts to changing market conditions, ensuring optimal performance across various instruments and timeframes.

How it Works:

The Renko Trend Reversal Strategy is designed to identify trend reversal points and generate buy or sell signals based on the following principles:

Renko Brick Generation: The strategy calculates the ATR over a user-defined period (ATR Length) and utilizes this value to determine the size of Renko bricks. Larger ATR values result in bigger bricks, capturing higher market volatility, while smaller ATR values create smaller bricks for calmer market conditions.

Buy and Sell Signals: The strategy generates buy signals when the Renko chart's open price crosses below the close price, indicating a potential bullish trend reversal. Conversely, sell signals are generated when the open price crosses above the close price, suggesting a bearish trend reversal. These signals help traders identify potential entry points to capitalize on market movements.

Stop Loss and Take Profit Management: To manage risk and protect profits, the strategy incorporates dynamic stop-loss and take-profit levels. The stop-loss level is calculated as a percentage of the Renko open price, ensuring a fixed risk amount for each trade. Similarly, the take-profit level is set as a percentage of the Renko open price to secure potential gains.

How to Use:

Inputs: Before using the strategy, traders can customize several parameters to suit their trading preferences. These inputs include the ATR Length, Stop Loss Percentage, Take Profit Percentage, Start Date, and End Date. Adjusting these settings allows users to optimize the strategy for different market conditions and risk tolerances.

Chart Setup: Apply the - Renko TRS script to your desired financial instrument and timeframe on TradingView. The Renko chart will dynamically adjust its brick size based on the ATR Length parameter.

Buy and Sell Signals: The strategy will generate green "Buy" labels below bullish reversal points and red "Sell" labels above bearish reversal points on the Renko chart. These labels indicate potential entry points for long and short trades, respectively.

Risk Management: The strategy automatically calculates stop-loss and take-profit levels based on the user-defined percentages. Traders can ensure proper risk management by using these levels to protect their capital and secure profits.

Backtesting and Optimization: Before implementing the strategy live, traders are encouraged to backtest it on historical data to assess its performance across various market conditions. Adjust the input parameters through optimization to find the most suitable settings for specific instruments and timeframes.

Conclusion:

The - Renko Trend Reversal Strategy is a unique and versatile tool for traders looking to identify trend reversals with greater accuracy. By combining Renko charts and the Average True Range (ATR) indicator, this strategy adapts to market dynamics and provides clear entry and exit signals. Traders can harness the power of Renko charts while effectively managing risk through stop-loss and take-profit levels. Before using the strategy in live trading, backtesting and optimization will help traders fine-tune the parameters for optimal performance. Start exploring trend reversals with the - Renko TRS and take your trading to the next level.

(Note: This description is for illustrative purposes only and does not constitute financial advice. Traders are advised to thoroughly test the strategy and exercise sound risk management practices when trading in real markets.)

[tradinghook] - Renko Trend Reversal Strategy - Renko Trend Reversal Strategy

Short Title: - Renko TRS

Description:

The Renko Trend Reversal Strategy ( - Renko TRS) is a powerful and original trading approach designed to identify trend reversals in financial markets using Renko charts. Renko charts differ from traditional time-based charts, as they focus solely on price movements and ignore time, resulting in a clearer representation of market trends. This strategy leverages Renko charts in conjunction with the Average True Range (ATR) to capture trend reversals with high precision and effectiveness.

Key Concepts:

Renko Charts: Renko charts are unique chart types that only plot price movements beyond a predefined brick size, ignoring time and noise. By doing so, they provide a more straightforward depiction of market trends, eliminating insignificant price fluctuations and making it easier to spot trend reversals.

Average True Range (ATR): The strategy utilizes the ATR indicator, which measures market volatility and provides valuable insights into potential price movements. By setting the brick size of the Renko chart based on the ATR, the strategy adapts to changing market conditions, ensuring optimal performance across various instruments and timeframes.

How it Works:

The Renko Trend Reversal Strategy is designed to identify trend reversal points and generate buy or sell signals based on the following principles:

Renko Brick Generation: The strategy calculates the ATR over a user-defined period (ATR Length) and utilizes this value to determine the size of Renko bricks. Larger ATR values result in bigger bricks, capturing higher market volatility, while smaller ATR values create smaller bricks for calmer market conditions.

Buy and Sell Signals: The strategy generates buy signals when the Renko chart's open price crosses below the close price, indicating a potential bullish trend reversal. Conversely, sell signals are generated when the open price crosses above the close price, suggesting a bearish trend reversal. These signals help traders identify potential entry points to capitalize on market movements.

Stop Loss and Take Profit Management: To manage risk and protect profits, the strategy incorporates dynamic stop-loss and take-profit levels. The stop-loss level is calculated as a percentage of the Renko open price, ensuring a fixed risk amount for each trade. Similarly, the take-profit level is set as a percentage of the Renko open price to secure potential gains.

How to Use:

Inputs: Before using the strategy, traders can customize several parameters to suit their trading preferences. These inputs include the ATR Length, Stop Loss Percentage, Take Profit Percentage, Start Date, and End Date. Adjusting these settings allows users to optimize the strategy for different market conditions and risk tolerances.

Chart Setup: Apply the - Renko TRS script to your desired financial instrument and timeframe on TradingView. The Renko chart will dynamically adjust its brick size based on the ATR Length parameter.

Buy and Sell Signals: The strategy will generate green "Buy" labels below bullish reversal points and red "Sell" labels above bearish reversal points on the Renko chart. These labels indicate potential entry points for long and short trades, respectively.

Risk Management: The strategy automatically calculates stop-loss and take-profit levels based on the user-defined percentages. Traders can ensure proper risk management by using these levels to protect their capital and secure profits.

Backtesting and Optimization: Before implementing the strategy live, traders are encouraged to backtest it on historical data to assess its performance across various market conditions. Adjust the input parameters through optimization to find the most suitable settings for specific instruments and timeframes.

Conclusion:

The - Renko Trend Reversal Strategy is a unique and versatile tool for traders looking to identify trend reversals with greater accuracy. By combining Renko charts and the Average True Range (ATR) indicator, this strategy adapts to market dynamics and provides clear entry and exit signals. Traders can harness the power of Renko charts while effectively managing risk through stop-loss and take-profit levels. Before using the strategy in live trading, backtesting and optimization will help traders fine-tune the parameters for optimal performance. Start exploring trend reversals with the - Renko TRS and take your trading to the next level.

(Note: This description is for illustrative purposes only and does not constitute financial advice. Traders are advised to thoroughly test the strategy and exercise sound risk management practices when trading in real markets.)